Embed Size (px)

Citation preview

Journal of Accounting and Economics 7 (1985) 43-66. North-Holland

EXECUTIVE COMPENSATION, MANAGEMENT TURNOVER, AND FIRM PERFORMANCE

An Empirical Investigation*

Anne T. COUGHLAN and Ronald M. SCHMIDT

University of Rochester, Rochester, NY 14627, USA

Received April 1984, final version received November 1984

This paper investigates the internal managerial control mechanisms at the disposal of a corpora- tion's compensation-setting board or committee. The hypotheses tested are that both compensation changes and management changes are methods used to control top management, and that the use of these control methods is motivated by changes in the firm's stock price performance. Public data from the period 1977-1980 support our hypotheses. We conclude that the firm's board creates managerial incentives consistent with those of the firm's owners, both by setting compensation and following management change policies which benefit shareholders.

1. Introduction

The set of formal and informal cooperative agreements labelled a corpora- tion has long been the subject of critical evaluation. Researchers have at- tempted to determine whether this institution, in fact, is characterized by managerial behavior beneficial to shareholders. Some have alleged that because ownership is separated from control, managers of the corporation can use corporate resources to enhance their specific interests and that such use will not be in the interests of shareholders [e.g., Berle and Means (1932)].

Conceptual work by Manne (1965) and more recent empirical research has examined one management-disciplining mechanism: corporate takeovers. This research is summarized in Jensen and Ruback (1983). They show that the evidence from financial markets supports the hypothesis that mergers, acquisi- tions and takeovers generally benefit the shareholders of participating corpora- tions. Since these events must be associated with some executive changes, managers who value their jobs have incentives to increase shareholder wealth

*Support from the Managerial Economics Research Center, Graduate School of Management, University of Rochester, is gratefully acknowledged. The authors have benefited from discussions with Andrew Christie, Harry DeAngelo, Linda DeAngelo, Michael Jensen, Clifford Smith, and Jerold Zimmerman, as well as with the members of the Organizations and Markets Workshop at the University of Rochester. We are indebted to Kevin Murphy for insights on the relationship between pay changes and sales growth, as well as for access to his data and for his time.

0165-4101/85/$3.30© 1985, Elsevier Science Publishers B.V. (North-Holland)

44 A.T. Coughlan and R.M. Schmidt, Compensation, turnover and performance

and thereby to avoid mergers, acquisitions, and takeovers. In essence, this research is consistent with the view that when the internal control mechanisms of the corporation function imperfectly, forces from outside the institution can bring about necessary changes in management.

This paper provides an empirical evaluation of corporate internal control procedures, in particular, compensation and managerial replacement or turnover. The next section summarizes alternative views of the role of com- pensation in corporate control. It also develops three testable hypotheses about executive compensation and changes in management personnel under the assumption that managers operate in the interests of shareholders. The first hypothesis is that rates of change in executive compensation are positively associated with stock price performance, and the second is that the probability of changes in top management is conditional on stock price performance. The hypotheses are tested using data on compensation and management changes for a set of firms which were not the object of successful merger or takeover efforts. The paper tests whether the standard measure of changes in share- holder wealth (changes in stock price) is associated with the compensation and replacement of top management. All of the hypotheses are supported in the tests. Conclusions are advanced in the final section.

2. Alternative hypotheses

This section develops three testable hypotheses about compensation and control of top management by a board of directors. The hypotheses concern the relation between stock price performance and management compensation; sales growth rates and management compensation; and stock price perfor- mance and management turnover. The section also includes a discussion of other empirical work. Tests of the hypotheses developed in this section are reported in the following two sections.

2.1. Stock price performance and compensation

Monitoring and review of managers by the board of directors is a major internal managerial control mechanism. The board approves the structure of incentives to which managers respond, including decisions about the com- pensation of top management. Smith and Watts (1984) present evidence indicating that the compensation plans approved by boards of directors generally link pay to performance measures which are themselves directly related to shareholder wealth. For instance, the value of stock options held by a manager at the beginning of a year gives him an incentive to act in ways which maximize stockholder wealth throughout that year. Phantom stock or

A.T. Coughlan and R.M. Schmidt, Compensation, turnover and performance 45

stock appreciation rights, if awarded prior to or at the beginning of the year, have the same incentive effect. 1

Nonetheless, some investigators have argued that compensation plans do not induce top management to maximize shareholder wealth and advance evidence which they claim supports this argument. Baumol (1967) and Marris (1963) assert that a CEO is more concerned with the size or growth rate of the firm than with profitability. They claim a preoccupation with size or growth occurs because compensation plans link pay to these characteristics and because greater prestige is associated with the management of a large firm. An extreme version of the argument that managers are not paid to enhance shareholder wealth is advanced by Loomis (1982), who claims that there is no link between compensation and any measure of profitability or stock price performance.

Implicit in these arguments is the assertion that formidable agency problems are created when a firm's owners grant decision making rights to a small group of managers, some of whom may also be owners of the firm. Granting management authority presumably improves administration, but agency prob- lems are created when rights are so vested. Agency problems result because managers have monopoly access to the information required to construct and administer compensation plans. These compensation plans ideally tie the self-interest of the managers to the interests of outside shareholders, but managers may withhold some relevant information from compensation com- mittees when that information would attribute poor firm performance to bad management. Some argue that agency problems are not solved because boards are captives of top management and make compensation decisions based only on the information supplied to them by that management.

Asymmetric information resulting from the delegation of authority, not the frequently referenced separation of ownership and control, creates the agency problem corporate directors must address. Indeed, the term 'separation of ownership and control' is misleading for two reasons. First, top management of a corporation generally owns some fraction, albeit small, of the firm. Second, even if control and ownership were completely separate, no serious agency:problems would be present if the information known to the managers was costlessly available to the owners. If those responsible for compensation always knew ex pos t the extent of managerial opportunism, then the com- pensation of top management would not be a difficult problem for boards of directors.

The mere existence of a serious agency problem does not necessarily imply that corporations are unable to develop institutional arrangements which

1 Stock options or other similar components awarded at the end of the year, on the other hand, do not provide an incentive for the manager to maximize shareholder wealth in that year, unless the n u m b e r to be awarded were tied to shareholder wealth in that year.

46 A.T. Coughlan and R.M. Schmidt, Compensation, turnover and performance

minimize its effects. While Baumol, Marris, and Loomis may claim that the incentives of the manager and the firm's owners remain divergent, the existence of competition in capital markets makes the survival of corporations depend on the construction of incentive arrangements which encourage top manage- ment to act in the shareholders' interest. Firms which fail to compensate managers in this way will face higher costs and thus will not compete successfully with firms whose managers act in the shareholders' interest. Presumably an executive compensation committee of the board of directors can respond to such competitive pressures by giving the firm's chief executive a set of monetary incentives which induces management to act in the interests of shareholders. This can be accomplished by positively correlating a portion of the executive's pay with the firm's abnormal stock price performance. 2 Such is the assumption in a paper by Smith and Watts (1983). 3

The argument that compensation plans encourage management to act in the interests of shareholders by linking pay to abnormal stock price performance rests on the assumption that the effects of good management will ultimately be reflected in the stock price. In other words, information that management has acted prudently or imprudently must be reflected in the movement of a firm's stock price after adjusting that movement for the effects of general market changes and other identifiable factors outside the control of the executive. Existing evidence about the operation of financial markets indicates that investors react quickly to information relevant to the financial performance of a firm. In many cases, abnormal stock price behavior reflects information prior to its official announcement. Existing evidence on the quick exploitation of profit opportunities merits the classification of financial markets as efficient. 4 This evidence provides the impetus for our efforts to construct and test a theory based on the assumption that good management will be reflected in stock price performance.

2Abnormal stock price performance is measured using estimates of a i and fli from the market model as discussed in Fama (1976, chs. 3 and 4), estimated on a set of data from a period just prior to the period of interest. These estimates of ai and fli can then be used to calculate daily excess returns or abnormal stock price performance according to the formula:

~it ~ R i t - a i - [ ~ i R m t ,

where eit is the daily abnormal stock price performance, R i t is the daily return on the firm's stock, and Rmt is the daily return on the value-weighted market portfolio.

3Miller and Scholes (1980), in a paper dealing with the rationale for different compensation components, argue instead that many incentive compensation components are used more because of their tax benefits than because of their motivational aspects. However, they are not able to reject analytically the hypothesis that incentive components like stock price performance in fact have some motivational effects.

4See Brealey and Myers (1981, ch. 13) for evidence of capital market efficiency.

A.T. Coughlan and R.M. Schmidt, Compensation, turnover and performance 47

2.2. Sales growth and compensation

Existing empirical evidence 5 indicates that the compensation of top manage- ment is positively correlated with firm size. This relation is consistent with the proposition that incentives exist for management to act in the interest of shareholders. Higher compensation for the management of larger firms may be necessary because managing those firms involves more complex and demand- ing tasks. Mnrphy (1985) presents evidence of positive correlation between changes in the compensation of top management and the real rate of growth of firm sales and shows that the relation is observed when stock price perfor- mance is held constant. This evidence constitutes an important empirical puzzle and we are able to corroborate his finding for a portion of our sample. An explanation of the puzzle, however, is not easily constructed.

An explanation for the correlation between sales growth and pay change must begin with the realization that optimal pay packages will not be based exclusively on stock options or other direct links between pay and stock performance. Pay packages based exclusively on stock price performance are inefficient methods for compensating risk-averse executives, since stock price variation is influenced by factors such as monetary policy, tax laws, or other political events outside the executive's control. Risk-averse executives would demand pay premiums to compensate for the windfall gains and losses in pay that would be caused by these events. A more efficient scheme would combine stock related components with salary or other components not linked ex ante to shareholder wealth. Bonuses can be used as ex post rewards for various facets of performance, and some portion of the bonus can be linked to stock performance at the discretion of the directors in order to signal that stock price is regularly monitored.

If pay is not based exclusively on stock performance, then the possibility of a link between sales growth and pay changes exists even if the effects on profitability of increased sales are reflected in a firm's stock price. By linking pay and sales growth, a board can tie pay to measurable results in a manner that protects the CEO from the effects of outside events on stock price. Basing bonuses on sales growth, however, will not always constitute an optimal compensation policy. If an executive near retirement expects pay to be based on sales, then he may approve advertising expenditures or increases in the sales force which increase sales revenue, but exceed profit-maximizing levels. Thus, we would expect pay plans based on sales to apply only when such undesirable incentives are absent; but in any event, we do not expect the effect of stock price performance on pay to be weakened by the inclusion of a significant sales growth effect.

5See, for instance, The Conference Board (1982, pp. 1-2).

48 A.T. Coughlan and R.M. Schmidt, Compensation, turnover and performance

2.3. Turnover and stock price performance

In addition to adjusting compensation, a board also has the power to effect a change in management. If boards discipline managers for actions or results that harm shareholders, stock price performance will be a predictor of changes in management. The empirical confirmation of such a relation, however, is complicated because there exist many other possible reasons for a change in top management: attraction of a successful executive to a better-paying posi- tion at another firm; normal retirement; or death. Excluding these cases, however, the monitoring hypothesis implies an observable relation between turnover and stock price performance.

2.4. Other empirical work

Many empirical studies have focused on the relation between executive pay and performance without producing conclusive tests of the above hypotheses. Examples of such articles include Cosh (1975), Hirschey and Pappas (1981), Lewellen and Huntsman (1970), Masson (1971), McGuire, Chiu and Elbing (1962), and Meeks and Whittington (1975). Since these investigations use accounting information to measure profitability, measurement errors are created and the empirical results are biased. A more objective measure of profitability, not at the discretion of the firm's management, such as abnormal stock price performance, is preferable. Further, studies using compensation components which are clearly correlated with stock price performance (e.g., the change in the value of stock options) reflect direct relations between pay and perfor- mance resulting from past decisions of the board to award the options. If these elements were excluded from the pay measure and one observed a positive relation between pay and stock price performance, one could conclude that the board's adjustments of supposed 'non-incentive' components encouraged the manager to act in the owners' interest. Finally, since these studies do not deal with executive turnover, they cannot reveal the extent of long-term monitoring reflected in the relation between turnover and performance.

One recent paper [Murphy (1985)] is not characterized by the empirical problems of other studies. He uses a measure of abnormal stock price perfor- mance and sales growth to predict changes in executive pay, and finds that both variables are significant, with positive coefficients. We discuss Murphy's findings below, when discussing our examination of the relation between pay, stock price performance, and sales growth.

In the remainder of the paper, we present tests of hypotheses derived from the assumption that competition forces compensation committees to link top management's income with the wealth of the firm's owners. Our data solves some of the measurement problems in previous studies. In addition, we avoid a serious methodological problem common to the existing literature. Specifically,

A.T. Coughlan and R.M. Schmidt, Compensation, turnover and performance 49

existing empirical efforts attempt to explain cross-sectional variation in the level of compensation of corporate managers with profitability being one of the independent variables. However, inter-firm and inter-industry differences may be the key variables explaining cross-sectional differences in salary levels, rather than differences in the degree to which specific managers increase or decrease shareholder wealth. Since identification and quantification of these inter-firm and inter-industry differences affecting the level of wages is difficult, cross-sectional analysis using the level of compensation as a dependent vari- able is not likely to test our hypotheses adequately. We avoid this problem by using rates of change in compensation as a dependent variable and by assuming that the existing wage structure represents an equilibrium dispersion of wage levels.

In summary, competition among corporations for capital and managerial talent implies the following testable hypotheses:

(H1) The executive compensation decisions of boards produce a positive correlation between changes in executive compensation and abnormal stock price performance.

(H2) Inclusion of sales growth as a predictor of changes in executive com- pensation along with stock price performance will not make the relation between pay. and stock price performance insignificant.

(H3) The frequency of CEO tumover is related to past stock price perfor- mance.

3. The data

We test our hypotheses using surveys appearing in Forbes magazine which identify chief executive officers and their compensation. The subsequent statis- tical analysis tests whether our measure of compensation, the real rate of change in salary plus bonus, is related to stock price performance. Specifically, we test for statistical dependence between stock price performance in period t and the real rate of change in salary plus bonus experienced by a given executive from periods (t - 1) to t, with all periods being fiscal years. We refer to fiscal year t as the performance year because it is the year for which stock performance is measured and, in the subsequent analysis, t is 1978, 1979 or 1980. We obtain compensation data for any fiscal year from the first Forbes compensation survey published after the close of the fiscal year. The issue containing that survey appears in late May or early June. We test for a relation between changes in management and stock price performance by determining whether poor stock performance in a given fiscal year is associated with an increase in the probability of a subsequent CEO turnover.

Our test sample is derived from the records of 249 corporations and contains 597 observations. Each observation consists of cumulative abnormal stock

50 A.T. Coughlan and R.M. Schmidt, Compensation, turnover and performance

returns realized by a given firm during a performance year, fiscal 1978, 1979 or 1980; the name of the firm's CEO during the performance year; that individ- ual's salary plus bonus for the performance year and the previous year; the CEO's age; and the identity of the CEO in the fiscal year following the performance year. The sample includes 195 observations for which 1978 is the performance year, 206 for which 1979 is the performance year, and 196 for which the performance year is 1980. The history of a given corporation can yield a maximum of three observations.

We include the data for a particular firm and fiscal year in our test sample only if several conditions are met. First, stock price data for the relevant performance year, fiscal year t, must be available from the CRSP tape. 6 Since our dependent variable is the rate of change in salary plus bonus, 7 we also require that the firm be managed by the same CEO for two consecutive fiscal years with the second year being fiscal 1978, 1979 or 1980. In addition, we include any two consecutive fiscal years as an observation only if compensation data for both years reflects payment of salary plus bonus for a full fiscal year.

We also require the CEO for the performance year to hold that position until after the publication of the Forbes issue containing compensation data for that year, thereby insuring that compensation data for the performance year reflects salary plus bonus for a full year. In addition, the constraint reduces the probability that any decision to replace a CEO was made before all stock price information for the performance year was in the possession of a corporation's board of directors. We also exclude a small number of firms that have a fiscal year which doses in June or July in order to guarantee a contemporaneous match of our measure of stock performance with the com- pensation data reported in Forbes.8

Finally, we require that the firm be listed in all five of the Forbes compensa- tion surveys published from 1978 to 1982, even though for some firms, changes in the CEO preclude our constructing observations using data from all of the issues. We use data from all five issues when the records of a firm yield three

6 CRSP stands for 'Center for Research on Securities Prices' (at the University of Chicago) and the CRSP tape contains (among other things) data on stock prices for firms hsted on the New York and American Stock Exchanges.

7The definition of salary plus bonus given in Forbes 'includes - in addition to salary and cash bonuses - directors' fees, commissions and payments made on long-term incentive plans' in 1978 through 1980. In 1977, directors' fees are excluded from the salary plus bonus figure. Excluded are bonuses earned in prior years and directors' fees received from unaffiliated companies.

8For some firms having fiscal years closing in June or July, we discovered that a Forbes compensation survey did not report the compensation data for the most recently completed fiscal year, but reported instead compensation for the fiscal year prior to it. This occurred apparently because the most recent fiscal year's compensation data was not available to Forbes at the time of publication. We did not possess the proxy statements required to identify all such irregularities, and thus excluded all firms with June or July fiscal closings from the sample. There are no particular regularities among the firms so deleted. This is not a problem for firms with fiscal year-ends in other months, since Forbes then reports compensation information for the same fiscal year as that for which the CRSP tape reports stock performance information.

A.T. Coughlan and R.M. Schmidt, Compensation, turnover and performance 51

observations for the sample, but the constraint is imposed on all firms to exclude cases where a change in management occurs because one corporation was acquired by another. 9 When such an acquisition takes place, the acquired firm is not listed in the compensation surveys published after the acquisition date, and changes in management or compensation are, therefore, difficult to identify. Furthermore, empirical evidence indicates that stock price variation in our performance year will reflect the acquisition process [Jensen and Ruback (1983)]. The inclusion of such firms in our sample, therefore, would complicate our efforts to examine the internal control process.

One hundred forty-nine of the 249 corporations represented in the sample have management histories permitting construction of observations for all three performance years, and for 129 of these 149 firms, the same individual is identified as CEO in all of the Forbes surveys from 1978 to 1982. For the remaining 100 firms, the data for at least one performance year could not be used because a change in CEO occurred in a manner that prevented the satisfaction of at least one of our selection criteria. In most of these instances, the change in top management caused the chief executive for the excluded performance year to differ from the CEO for the previous year. 1°

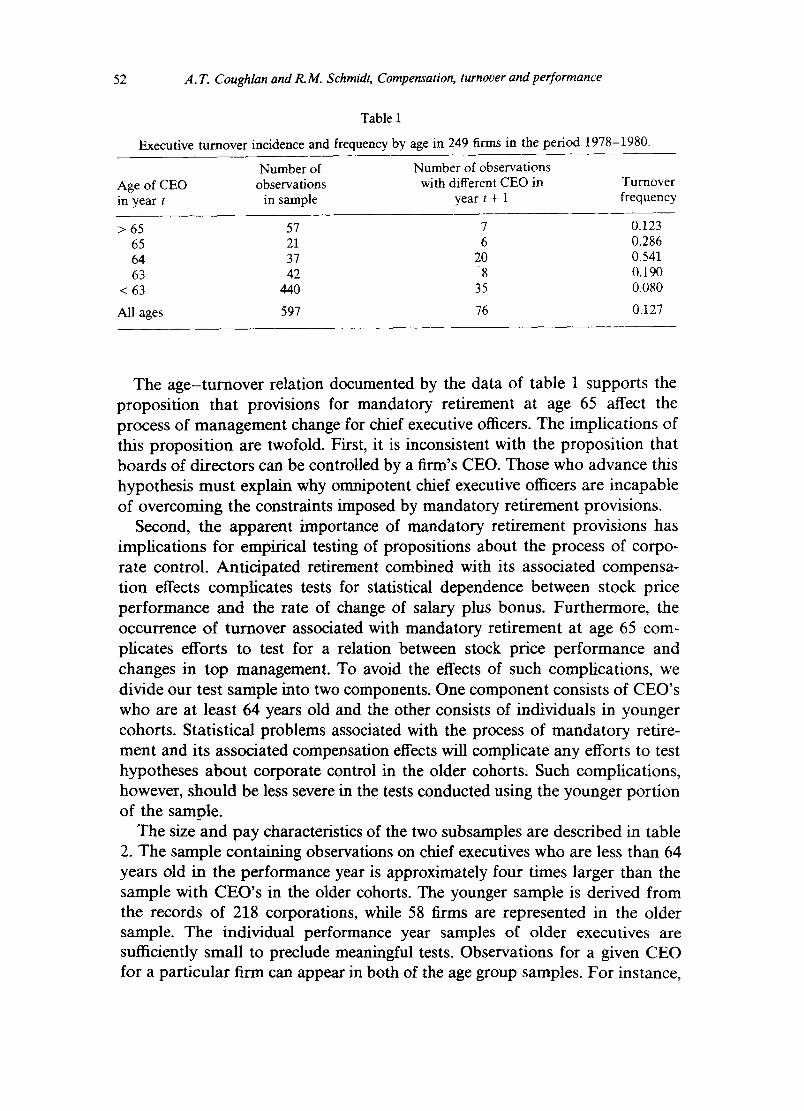

The structure of our empirical tests has been shaped by the relation between age and the probability of a change in CEO which we observe for the firms in our sample. In the context of our test sample, a change in CEO is recorded when the CEO identified in the survey containing compensation data for the performance year differs from the CEO identified in the subsequent Forbes. As table 1 indicates, the probability of observing such a change is substantially increased if the performance year CEO is 64 years old. For chief executive officers in this age cohort, one can expect to observe one management turnover in every two cases. For older individuals, the probability of management change is one chance in six, and for younger individuals it is less than one chance in eleven.

9Since compensation data for fiscal year t is obtained from the Forbes appearing in calendar (t + 1), we require the first four issues to obtain the compensation data necessary for computation of the relevant rates of pay change. For example, we compute the rate of pay change between fiscal 1977 and fiscal 1978 using the Forbes from June 1978 and June 1979, and the rate of pay change between fiscal 1979 and fiscal 1980 using data from the 1980 and 1981 Forbes. The 1982 issue yields information necessary to construct the turnover variable.

1°For 50 of these 100 firms, data for two performance years were used. In these cases, either (a) a management change occurred before the start of the 1978 fiscal year, and hence 1978 was excluded, or (b) a management change occurred after the close of the 1979 fiscal year, and hence 1980 was excluded. Given our requirements, it is not possible for a firm to be represented in the 1978 and 1980 fiscal years, but not the 1979 fiscal year. For an additional 25 of these 100 firms, a management change following the close of the 1978 performance year allowed use of data for only that year. For an additional 6 of the 100 firms, the pattern of management change allowed only the use of the 1979 performance year; and for an additional 19 firms, management changes allowed only the use of the 1980 performance year.

52 A.T. Coughlan and R.M. Sehmidt, Compensation, turnover and performance

Table 1

Executive turnover incidence and frequency by age in 249 firms in the period 1978-1980.

Number of Number of observations Age of CEO observations with different CEO in Turnover in year t in sample year t + 1 frequency

> 65 57 7 0.123 65 21 6 0.286 64 37 20 0.541 63 42 8 0.190

< 63 440 35 0.080

All ages 597 76 0.127

The age-turnover relation documented by the data of table 1 supports the proposition that provisions for mandatory retirement at age 65 affect the process of management change for chief executive officers. The implications of this proposition are twofold. First, it is inconsistent with the proposition that boards of directors can be controlled by a firm's CEO. Those who advance this hypothesis must explain why omnipotent chief executive officers are incapable of overcoming the constraints imposed by mandatory retirement provisions.

Second, the apparent importance of mandatory retirement provisions has implications for empirical testing of propositions about the process of corpo- rate control. Anticipated retirement combined with its associated compensa- tion effects complicates tests for statistical dependence between stock price performance and the rate of change of salary plus bonus. Furthermore, the occurrence of turnover associated with mandatory retirement at age 65 com- plicates efforts to test for a relation between stock price performance and changes in top management. To avoid the effects of such complications, we divide our test sample into two components. One component consists of CEO's who are at least 64 years old and the other consists of individuals in younger cohorts. Statistical problems associated with the process of mandatory retire- ment and its associated compensation effects will complicate any efforts to test hypotheses about corporate control in the older cohorts. Such complications, however, should be less severe in the tests conducted using the younger portion of the samt)le.

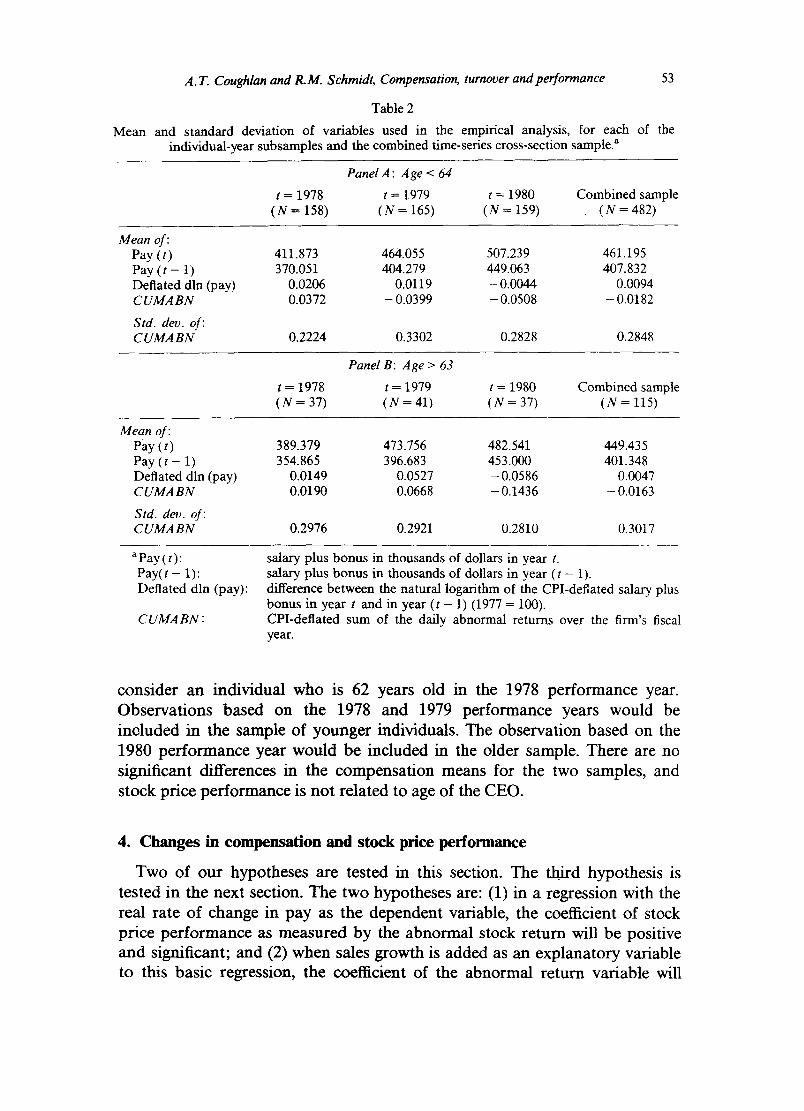

The size and pay characteristics of the two subsamples are described in table 2. The sample containing observations on chief executives who are less than 64 years old in the performance year is approximately four times larger than the sample with CEO's in the older cohorts. The younger sample is derived from the records of 218 corporations, while 58 firms are represented in the older sample. The individual performance year samples of older executives are sufficiently small to preclude meaningful tests. Observations for a given CEO for a particular firm can appear in both of the age group samples. For instance,

A.T. Coughlan and R.M. Schmidt, Compensation, turnover and performance 53

Table 2

M e a n and s tandard deviation o f variables used in the empirical analysis, for each of the individual-year subsamples and the combined time-series cross-section sample, a

Panel A : Age < 64

t = 1978 t = 1979 t = 1980 Combined sample ( N = 158) ( N = 165) (N = 159) ( N = 482)

Mean of: Pay ( t ) 411.873 464.055 507.239 461.195 Pay (t - 1) 370.051 404.279 449.063 407.832 Deflated din (pay) 0.0206 0.0119 - 0.0044 0.0094 CUMA BN 0.0372 - 0.0399 - 0.0508 - 0.0182

Std. dev. of: CUMA B N 0.2224 0.3302 0.2828 0.2848

Panel B: Age > 63

t = 1978 t = 1979 t = 1980 Combined sample ( N = 37) ( N = 41) ( N = 37) ( N = 115)

Mean of: Pay ( t ) 389.379 473.756 482.541 449.435 Pay (t - 1) 354.865 396.683 453.000 401.348 Deflated din (pay) 0.0149 0.0527 - 0 . 0 5 8 6 0.0047 CUMA B N 0.0190 0.0668 - 0.1436 - 0.0163

Std. dev. of: CUMA BN 0.2976 0.2921 0.2810 0.3017

a p a y ( t ) : P a y ( t - 1): Deflated dln (pay):

C UMA BN :

salary plus bonus in thousands of dollars in year t. salary plus bonus in thousands of dollars in year ( t - 1). difference between the natural logarithm of the CPI-deflated salary plus bonus in year t and in year (t - 1) (1977 = 100). CPI-deflated sum of the daily abnormal returns over the firm's fiscal year.

consider an individual who is 62 years old in the 1978 performance year. Observations based on the 1978 and 1979 performance years would be included in the sample of younger individuals. The observation based on the 1980 performance year would be included in the older sample. There are no significant differences in the compensation means for the two samples, and stock price performance is not related to age of the CEO.

4. Changes in compensation and stock price performance

Two of our hypotheses are tested in this section. The thi.'rd hypothesis is tested in the next section. The two hypotheses are: (1) in a regression with the real rate of change in pay as the dependent variable, the coefficient of stock price performance as measured by the abnormal stock return will be positive and significant; and (2) when sales growth is added as an explanatory variable to this basic regression, the coefficient of the abnormal return variable will

54 A.T. Coughlan and R.M. Schmidt, Compensation, turnover and performance

remain significant. The tests are performed using the difference in the natural logarithms of CPI-deflated salary plus bonus paid to a CEO in performance year t and the previous year as a dependent variable. Salary plus bonus is not usually linked by an explicit formula to stock price performance as are other pay components such as stock options. Because these other components explicitly relate compensation to stock performance, a significant relation between salary plus bonus and stock price performance is not necessary for a conclusion that boards construct executive compensation plans that increase shareholder wealth. A significant positive relation between salary plus bonus and stock price performance, however, strengthens our argument that boards purposefully set discretionary pay components to induce the executive to increase shareholder wealth.

The regression model is then:

ln( (deflated salary + bonus)i,t (deflated salary + bonus) i, t - 1 )

= a +/3- (cumulative residual) i,t + El, t, (1)

where the subscript (i, t) denotes firm i at time t. The abnormal return is measured as the CPI-deflated sum of the daily abnormal returns over the firm's fiscal year (the variable C U M A B N ) . n To test the second hypothesis, that the inclusion of sales growth does not diminish the relation between pay and abnormal stock price performance, we add CPI-deflated percentage sales growth between fiscal years ( t - 1 ) and t as an independent variable in regression equation (1). Our results are robust both to using raw stock returns rather than abnormal stock returns as an independent variable, and to using the natural logarithm of salary plus bonus in year t as the dependent variable and the same variable for year (t - 1) as an independent variable.

We estimate regressions for three different groups of observations. The test sample is first divided into two groups based on age of the CEO in the performance year, and five regressions are estimated for each age group. One group contains observations based on individuals who are at least 64 years old in the performance year, and the other consists of observations based on younger executives. For each age group, we estimate the regression described in eq. (1) for three performance years: 1978, 1979, and 1980. In these regressions, the stock performance variable is the cumulative residual for fiscal 1978, 1979, or 1980. We then form a sample by pooling the observations used

l iThe daily abnormal returns were deflated by the monthly CPI divided by the number of trading days in the month. Also, similar empirical results were obtained using the CPI-deflated product of the daily abnormal returns over the firm's fiscal year, minus one, as the measure of abnormal returns.

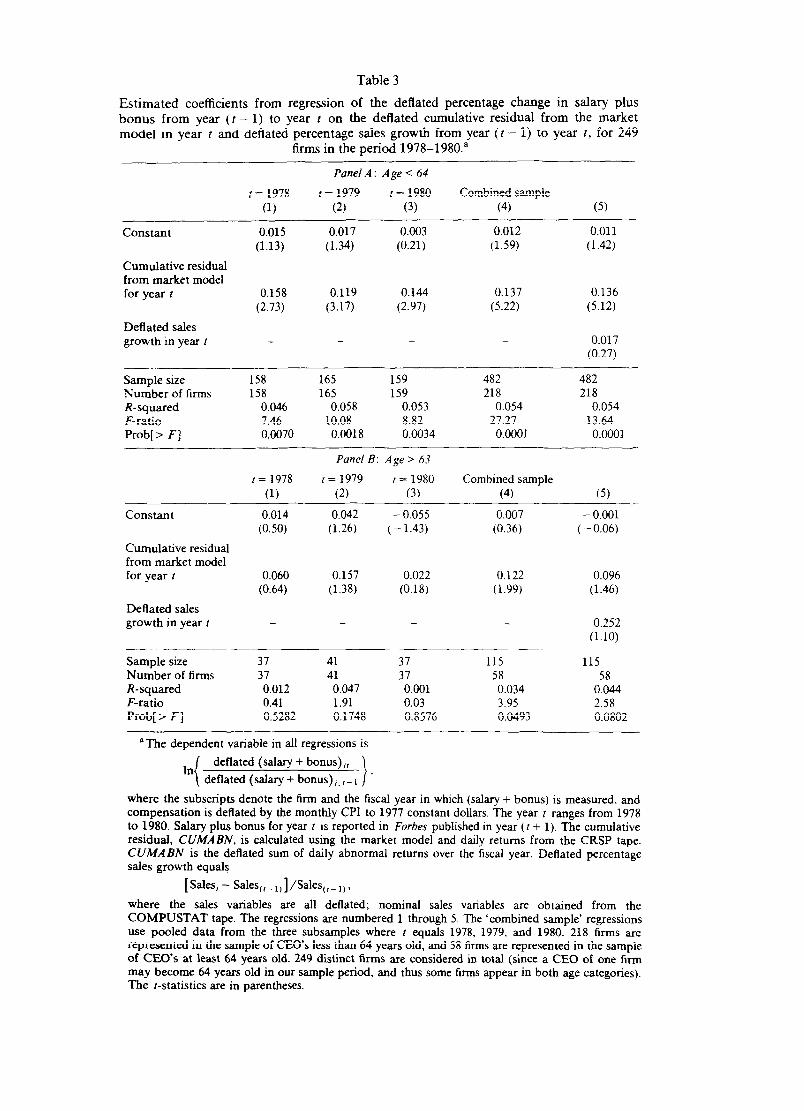

A.T. Coughlan and R.M. Schmidt, Compensation, turnover and performance 55

to estimate these regressions and estimate eq. (1) and a second regression in which sales growth and stock price performance appear as independent vari- ables. Finally, we define a third group of observations based on firms which experienced no change in CEO during the period we examine, to determine whether such changes affect the compensation regressions. Eq. (1) and a regression including both stock performance and sales growth are estimated for this sample.

Regressions testing our first two hypotheses are presented in table 3. Panel A reports results for the sample of younger executives, and panel B reports for the older sample. In panel A, the coefficient on the cumulative residual from the market model is positive and significant in all regressions. All t-statistics on the cumulative residual coefficients indicate significance at greater than the one-percent level. The low R-squared in this regression (0.054) indicates that stock price performance explains a small portion of the variation in salary plus bonus. This is not surprising, since the purpose of salary plus bonus is to give income security to the executive and to compensate him for performing various other tasks inside the firm. Nonetheless, the F-tests reveal considerable significance.

The results for the sample of observations with CEO's at least 64 years old yield mixed evidence. Only in the combined sample, regression 4 in panel B, does the abnormal returns variable have a coefficient significant at the five-per- cent level, and then the size of the coefficient is smaller than in the analogous regressions for younger executives. The R-squared and F-values for the regres- sion are also correspondingly lower. Nonetheless, the coefficient of the stock price variable for all individual years is positive, if not significant. We suspect that the results for this age group reflect the effect of retirement-related events on changes in compensation.

Neither panel of table 3 displays a positive and significant coefficient for the sales growth variable. For younger executives, the coefficient is both very small (0.017) and insignificantly different from zero. For older executives, the coeffi- cient is considerably larger (0.252), but not significant at the ten-percent level. Murphy (1984) finds a positive and significant relation between sales growth and compensation, and the discrepancy between his result and ours is puzzling. Murphy derives his observations from the compensation histories of 72 corpo- rations over the period 1964 to 1981. One observation consists of annual compensation of a given executive in a particular year and his total sample includes 4500 observations, 943 of which reflect CEO compensation. He finds a positive and significant relation between sales growth and compensation when he restricts his analysis to CEO's.

An individual is present in Murphy's sample only if he was listed in a firm's proxy statement during the period 1964 to 1970 and remained with the firm for at least five years. He follows the careers of such individuals throughout his sample period, and his data could include the compensation history of a CEO

Table 3

Estimated coefficients from regression of the deflated percentage change in salary plus bonus from year (t - 1) to year t on the deflated cumulative residual from the market model in year t and deflated percentage sales growth from year (t - 1) to year t, for 249

firms in the period 1978-1980.”

t = 1978

(1)

Panel A: Age < 64

1 = 1979 t = 1980

(2) (3) Combined sample

(4) (5)

Constant

Cumulative residual from market model for I year

Deflated sales growth in year t

0.015 0.017 0.003 0.012 0.011 (1.13) (1.34) (0.21) (1.59) (1.42)

0.158 0.119 0.144 0.137 0.136 (2.73) (3.17) (2.97) (5.22) (5.12)

- _ _ 0.017 (0.27)

Sample size 158 165 159 482 482 Number of firms 158 165 159 218 218 R-squared 0.046 0.058 0.053 0.054 0.054 F-ratio 7.46 10.08 8.82 27.27 13.64 Prob[ > F] 0.0070 0.0018 0.0034 0.0001 0.0001

t = 1978 (1)

Punel B: Age > 63

I = 1979 r = 1980 (2) (3)

Combined sample (4) (5)

Constant

Cumulative residual from market model for year I

Deflated safes growth in year r

0.014 0.042 - 0.055 0.007 - 0.001 (0.50) (1.26) (- 1.43) (0.36) ( - 0.06)

0.060 0.157 0.022 0.122 0.096 (0.64) (1.38) (0.18) (1.99) (1.46)

- - 0.252 (1.10)

Sample size 37 41 37 115 115 Number of firms 37 41 37 58 58 R-squared 0.012 0.047 0.001 0.034 0.044 F-ratio 0.41 1.91 0.03 3.95 2.58 Prob[ > F] 0.5282 0.1748 0.8576 0.0493 0.0802

aThe dependent variable in all regressions is

In (

deflated (salary + bonus) ,,

i deflated (salary+ bonus),,,-t .

where the subscripts denote the firm and the fiscal year in which (salary + bonus) is measured, and compensation is deflated by the monthly CPI to 1977 constant dollars. The year t ranges from 1978 to 1980. Salary plus bonus for year z is reported in Forbes published in year ( t + 1). The cumulative residual, CUMABN, is calculated using the market model and daily returns from the CRSP tape. CUMABN is the deflated sum of daily abnormal returns over the fiscal year. Deflated percentage sales growth equals

[Sales, - Sales(,_,,]/Sales(,_,,,

where the safes variables are all deflated; nominal sales variables are obtained from the COMPUSTAT tape. The regressions are numbered 1 through 5. The ‘combined sample’ regressions use pooled data from the three subsamples where f equals 1978, 1979, and 1980. 218 firms are represented in the sample of CEO’s less than 64 years old, and 58 firms are represented in the sample of CEO’s at least 64 years old. 249 distinct firms are considered in total (since a CEO of one firm may become 64 years old in our sample period, and thus some firms appear in both age categories). The r-statistics are in parentheses.

A.T. Coughlan and R.M. Schmidt, Compensation, turnover and performance 57

for his entire tenure in that position. Our sample contains a maximum of three performance years per executive. If the frequency of CEO changes is the same for both samples, Murphy's, given the difference in construction procedures, will contain a smaller proportion of observations based on a CEO's last year of service. In our sample, an executive who leaves his firm is represented by a maximum of three observations, while in Murphy's there must be more, since average tenure for a CEO is considerably in excess of three years. The same argument that a last year of service will be less frequent in Murphy's sample also implies that initial years of service will appear less frequently. While a performance year cannot be the initial year of service for a CEO in our sample, some of our observations are based on the second year. In fact, the test sample of 597 observations includes 140 observations on executives in 76 firms for which turnover occurred during the period 1979 to 1981. Obviously, 76 of those observations are on executives in their last year of service with the company. In addition, there are 70 observations on executives in 43 firms for which the CEO during the 1980 performance year became CEO after 1977.

One can argue that the optimal compensation policy for a CEO's initial or final years of service will differ from that of other years. For example, pay for a CEO in his last year may not be linked to sales because such a link would encourage excessive advertising-or marketing expenditures. Pay for a new CEO may not be linked to sales because such a link would reward him for the efforts of his predecessor, x2 Accordingly, a sample containing a greater proportion of early or final year observations may be less likely to reflect a positive and significant relation between sales growth and compensation. Thus, there exists the possibility that the difference between our results and Murphy's occurs because our sample includes a greater proportion of executives who are beginning or ending their careers as CEO's.

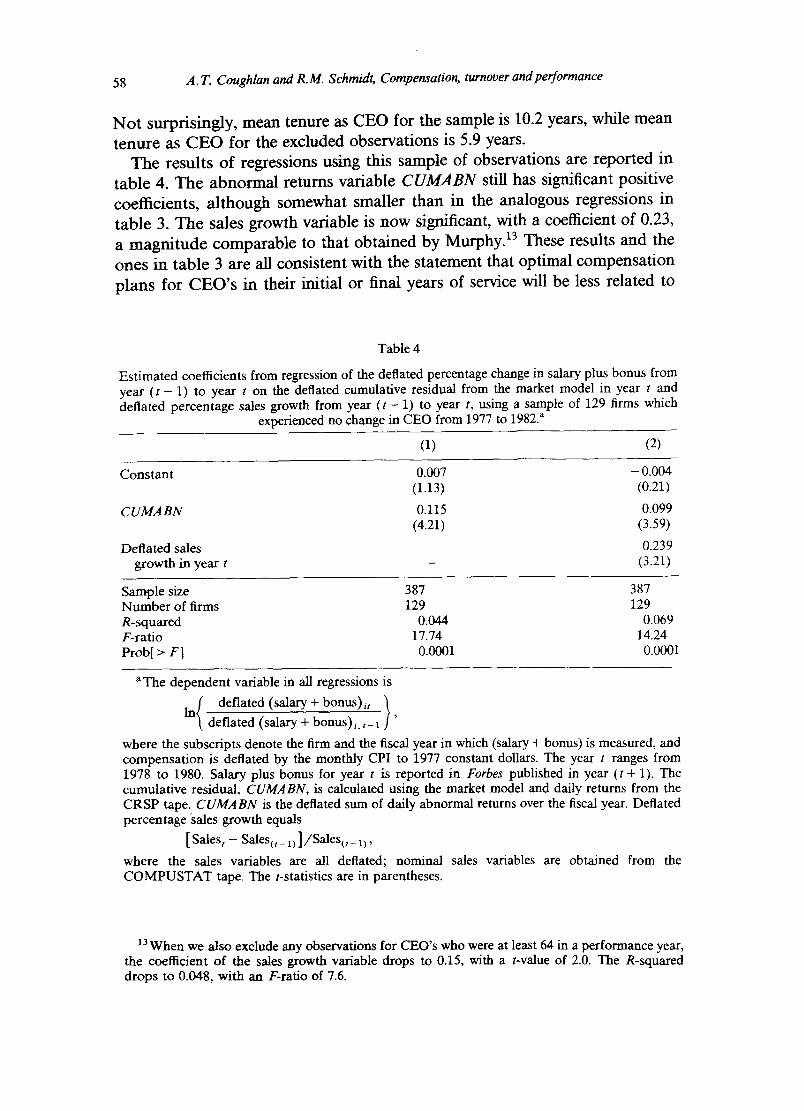

To determine if sample differences are the cause of the difference in results, we constructed a sample using only observations from firms which experienced no change in CEO between 1977 and 1982. Since the last performance year we investigate is 1980 and since all executives in this sample served through 1981, no observation in this sample is based on the last year of service for a CEO. The selection procedure also eliminates observations on individuals who be- come CEO after 1977. This construction procedure yields a sample of 387 observations, based on the records of 127 firms. The average age of a CEO in this sample is 57.8 years, identical to the average age for our complete sample.

12For instance, positive net present value investments like new-product development projects undertaken by the predecessor are impounded in the stock price during the predecessor's term, but affect sales with a lag. In this case, stock price performance would improve during the predecessor's tenure, but sales growth would not be experienced until the tenure of the new CEO. It would be inappropriate to reward the new CEO for sales growth resulting from these efforts of a predeces- sor.

58 A. T. Coughlan and R.M. Schmidt, Compensation, turnover and performance

Not surprisingly, mean tenure as CEO for the sample is 10.2 years, while mean tenure as CEO for the excluded observations is 5.9 years.

The results of regressions using this sample of observations are reported in table 4. The abnormal returns variable CUMABN still has significant positive coefficients, although somewhat smaller than in the analogous regressions in table 3. The sales growth variable is now significant, with a coefficient of 0.23, a magnitude comparable to that obtained by Murphy. 13 These results and the ones in table 3 are all consistent with the statement that optimal compensation plans for CEO's in their initial or final years of service will be less related to

Table 4

Estimated coefficients from regression of the deflated percentage change in salary plus bonus from year ( t - 1) to year t on the deflated cumulative residual from the market model in year t and deflated percentage sales growth from year ( t - 1) to year t, using a sample of 129 firms which

experienced no change in CEO from 1977 to 1982. a

(1) (2)

Constant 0.007 - 0.004 (1.13) (0.21)

CUMA BN 0.115 0.099 (4.21) (3.59)

Deflated sales 0.239 growth in year t - (3.21)

Sample size 387 387 Number of firms 129 129 R-squared 0.044 0.069 F-ratio 17.74 14.24 Prob[ > F] 0.0001 0.0001

The dependent variable in all regressions is

{ d e f l a t e d ( s a l a r y + b o n u s ) i t )

In deflated (salary+ bonus)i,t-1 '

where the subscripts denote the firm and the fiscal year in which (salary + bonus) is measured, and compensation is deflated by the monthly CPI to 1977 constant dollars. The year t ranges from 1978 to 1980. Salary plus bonus for year t is reported in Forbes published in year (t + 1). The cumulative residual, CUMABN, is calculated using the market model and daily returns from the CRSP tape. CUMABN is the deflated sum of daily abnormal returns over the fiscal year. Deflated percentage "sales growth equals

[ Sales t - Sales(t_ 1) ]/Sales(t - 1),

where the sales variables are all deflated; nominal sales variables are obtained from the COMPUSTAT tape. The t-statistics are in parentheses.

13When we also exclude any observations for CEO's who were at least 64 in a performance year, the coefficient of the sales growth variable drops to 0.15, with a t-value of 2.0. The R-squared drops to 0.048, with an F-ratio of 7.6.

A.T. Coughlan and R.M. Schmidt, Compensation, turnover and performance 59

sales growth than those for CEO's in other stages of their careers. In the two samples (younger and older executives) in table 3, CEO's at all stages of their tenure with the firm are included in each age regression. 14 We are less likely to observe a significant relation between rates of change in pay and sales growth in a sample with mixed lengths of tenure because optimal compensation plans which employ sales growth are more difficult to construct for part of that sample (the CEO's in their initial or final year of service). In the sample based on firms without CEO turnover in table 4, the relation between sales growth and compensation is stronger; observations for final years and initial years are less frequent. The sales growth variable is not only significant in this sample, but of a size commensurate with that in Murphy's work. This evidence, in combination with Murphy's, indicates both a weU-established relation between sales growth and rates of change in compensation, and is consistent with our notion that this relation is stronger for CEO's in intermediate stages of tenure with their firms. Further research is required to state this explanation defini- tively.

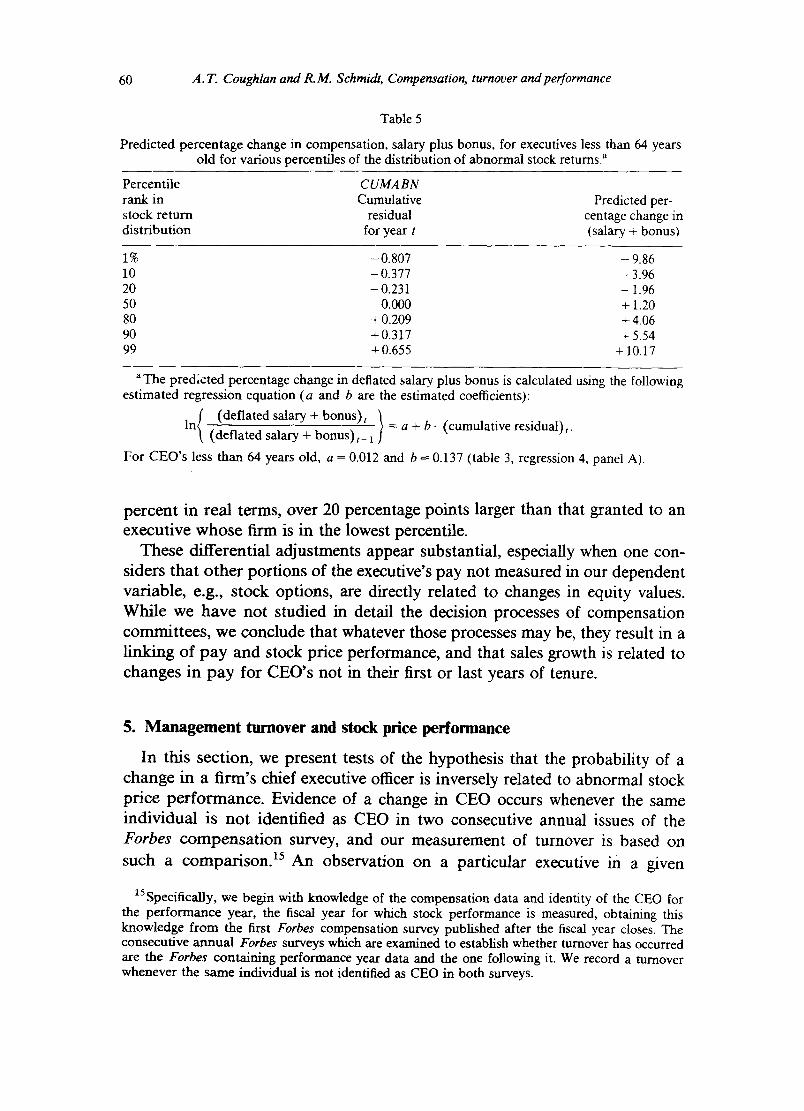

While the results in table 3 indicate that compensation is significantly related to abnormal stock price performance, the magnitude of the predicted effect for various percentiles of stock price performance is also of interest. We report this information in table 5 for regression 4 of table 3, panel A (CEO's less than 64 years old). To calculate the entries in table 5, we substitute the estimated coefficients from regression 4 in panel A of table 3 for a and fl in eq. (1), and substitute various percentiles of the cumulative residual distribution of our sample for the cumulative residual variable in eq. (1). For example, to find the predicted percentage change in salary plus bonus for an executive whose firm is in the 99th percentile of the abnormal stock return distribution (i.e., the top one percent, where the cumulative residual equals 0.655), we set o~ equal to 0.012 and fl equal to 0.137 (from regression 4 in panel A of table 3) in eq. (1) and solve for the percentage change in deflated salary plus bonus. The solution is a rate of pay increase of 10.17 percent.

In table 5, our regression model predicts that a firm in the first (i.e., lowest) percentile of the stock return distribution would decrease its CEO's deflated salary plus bonus by 9.86 percent in the current year over the previous year. Since the mean percentage change in deflated salary plus bonus for the combined sample is 0.9 percent (an increase of 0.9 percent in real terms), there is a substantial penalty for a CEO of a firm in the bottom of the return distribution. In contrast, an executive who places shareholders in the top 1 percent of the return distribution will receive an upward adjustment of 10.17

14In fact, a CEO with as little as two years of tenure can be included in any one of the samples under discussion, if he is in his second year as CEO in 1977. There is no upward limit to the length of tenure a CEO can have in any of the samples under discussion.

60 A.T. Coughlan and R.M. Schmidt, Compensation, turnover and performance

Table 5

Predicted percentage change in compensation, salary plus bonus, for executives less than 64 years old for various percentiles of the distribution of abnormal stock returns, a

Percentile CUMA BN rank in Cumulative Predicted per- stock return residual centage change in distribution for year t (salary + bonus)

1% - 0.807 - 9.86 10 - 0.377 - 3.96 20 - 0.231 - 1.96 50 0.000 + 1.20 80 + 0.209 + 4.06 90 + 0.317 + 5.54 99 +0.655 + 10.17

a The predicted percentage change in deflated salary plus bonus is calculated using the following estimated regression equation (a and b are the estimated coefficients):

( (de f l a t edsa l a ry+bonus ) t } In (deflated salary + bonus) t_ a = a + b. (cumulative residual)t.

For CEO's less than 64 years old, a = 0.012 and b = 0.137 (table 3, regression 4, panel A).

percent in real terms, over 20 percentage points larger than that granted to an executive whose firm is in the lowest percentile.

These differential adjustments appear substantial, especially when one con- siders that other portions of the executive's pay not measured in our dependent variable, e.g., stock options, are directly related to changes in equity values. While we have not studied in detail the decision processes of compensation committees, we conclude that whatever those processes may be, they result in a linking of pay and stock price performance, and that sales growth is related to changes in pay for CEO's not in their first or last years of tenure.

5. Management turnover and stock price performance

In this section, we present tests of the hypothesis that the probability of a change in a firm's chief executive officer is inversely related to abnormal stock price performance. Evidence of a change in CEO occurs whenever the same individual is not identified as CEO in two consecutive annual issues of the Forbes compensation survey, and our measurement of turnover is based on such a comparison. 15 An observation on a particular executive in a given

aSSpecifically, we begin with knowledge of the compensation data and identity of the CEO for the performance year, the fiscal year for which stock performance is measured, obtaining this knowledge f rom the first Forbes compensation survey published after the fiscal year closes. The consecutive annual Forbes surveys which are examined to establish whether turnover has occurred are the Forbes containing performance year data and the one following it. We record a turnover whenever the same individual is not identified as CEO in both surveys.

A.T. Coughlan and R.M. Schmidt, Compensation, turnover and performance 61

performance year is not included in the sample if the individual retires or is replaced as CEO before the Forbes containing performance year information is published, and information in that issue allows us to determine whether this condition is satisfied.16 This procedure increases the probability that a board’s approval of a management change did not occur before it possessed all the information contained in our measure of performance year stock price varia- tion.

Nonetheless, exceptionally poor abnormal stock price performance should not always result in a board’s effecting a management change as we record it. Poor stock performance can have a variety of causes, many of which do not reflect incompetence or poor performance on the part of top management and which, therefore, do not merit the dismissal of that manager. Furthermore, a board convinced that the CEO is responsible for poor stock results in the performance year may not effect a change in management within the time period we observe (the twelve-month interval between the publications of the performance-year Forbes survey and the subsequent survey), because replacing a CEO requires considerable deliberation.

Despite these considerations, we advance the hypothesis that the monitoring of corporate boards of directors in behalf of shareholders implies an inverse relation between stock performance and turnover. As described in section 3, the relation between age and turnover that we observe for our sample supports the proposition that procedures requiring mandatory retirement at age 65 are the cause of a large proportion of our observed turnovers. Therefore, we conduct two separate tests for a relation between stock performance and turnover: one using a sample consisting of CEO’s who are less than 64 years old, and a second using the remainder of the sample. We expect the occurrence of mandatory retirements in the older sample to complicate efforts to test for a relation between turnover and stock performance using that sample. The younger sample, however, tests whether stock performance is a predictor of management turnover. Nonetheless, even in that sample some portion of the observed turnovers may result from death or early retirement and thus may be unrelated to the firm’s stock performance.

The statistical methodology underlying our empirical tests is a logit regres-

sion in which the dependent variable is dichotomous, having a value of one

16For example, consider the case where a firm’s fiscal year closes on December, 31, 1979. Compensation data for that year are obtained from the Forbes appearing in June of 1980 and that issue would identify whether the CEO for fiscal 1979 left office sometime after the 1979 fiscal year closed. If such an event occurred, say a different individual assumed the position of CEO on January 15,1980, an observation for that firm and individual based on the 1979 fiscal year would be excluded from our compensation and turnover analyses.

J.A.E.- C

62 A.T. Coughlan and R.M. Schmidt, Compensation, turnover and performance

when a CEO turnover occurs and a value of zero otherwise. 17 The hypothesis is that the stock price variable will be inversely related to the probability-of management turnover. Thus, we expect the sign for the coefficient of this variable in the logit regression to be negative.

In addition to stock performance, each logit regression contains a constant term and two other independent variables, age and the residual from the appropriate compensation regressions. In the younger sample, the probability of turnover is hypothesized to be an increasing function of age and thus, we expect the variable's coefficient to have a positive sign in the regression for that sample. In the older sample, we expect the age variable to reflect the effects of mandatory retirement and thus for its coefficient to be negative. In other words, for the sample consisting of individuals of age 64 and older, mandatory retirement at age 65 will cause the probability of turnover to be higher for the 64- and 65-year-old members of the sample.

We include the residual (RES) from the appropriate compensation regres- sion as an independent variable in each logit regression. In the younger sample where the complications of mandatory retirement are not present, this variable should serve as a proxy for factors other than stock price which a board would consider in setting compensation. We interpret a large positive residual, a rate of pay increase larger than is expected given stock price performance, as implying that in evaluating these other factors, the board reached a favorable assessment of the CEO's performance and adjusted compensation accordingly. For example, a board may have decided that the stock performance was determined by factors beyond the executive's control and that the CEO should receive a considerable pay increase because he managed well despite these events. A large negative residual in the compensation regression can be interpreted as implying that other considerations more than offset stock performance and that an unfavorable assessment of the CEO's efforts governed the pay decision. For this portion of the sample, therefore, we expect to find an inverse relation between the compensation residual and turnover probability.

For the older sample, we expect the residual, RES, to reflect compensation events related to mandatory retirement in addition to the above considerations. If such events take the form of retirement bonuses (a 'golden handshake'), a large increase in salary plus bonus could accompany retirement. Thus, a large positive residual could be associated with higher turnover probabilities in this sample, producing a positive coefficient for RES.

lVWhen the dependent variable in a regression is dichotomous, estimation via ordinary least squares produces unbiased but inefficient estimates. The log, it regression constrains the dependent variable to range between zero and one, and produces unbiased and efficient estimates under the assumption that the error term has the Weibull distribution. The formula for the log, it regression is given in the text below. The SAS LOGIST routine was used to estimate the logit regressions reported here. See Kmenta (1971, pp. 425 ft.) and McFadden (1976) for further discussions of the uses of log, it.

A.T. Coughlan and R.M. Sehmidt, Compensation, turnover and performance 63

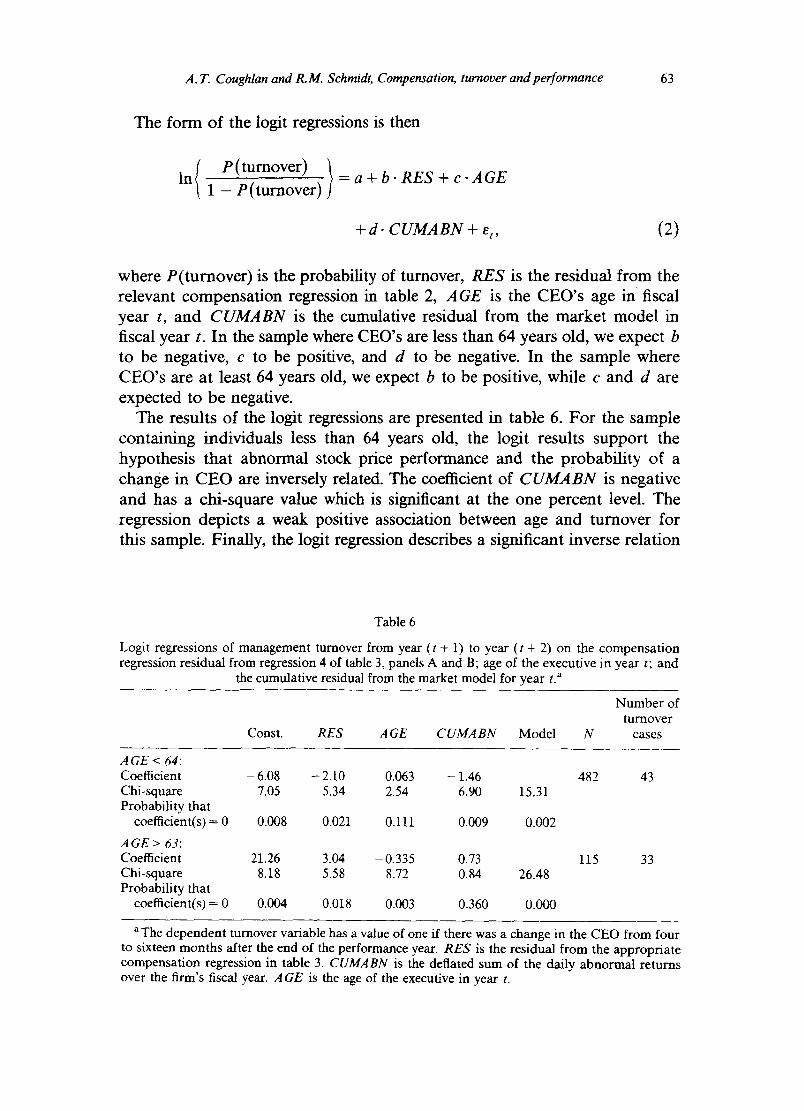

The form of the logit regressions is then

{ P(turnover) } In 1 -P( turnover) = a + b . R E S + c . A G E

+ d . C U M A B N + El, (2)

where P(turnover) is the probability of turnover, R E S is the residual from the relevant compensation regression in table 2, A G E is the CEO's age in fiscal year t, and C U M A B N is the cumulative residual from the market model in fiscal year t. In the sample where CEO's are less than 64 years old, we expect b to be negative, c to be positive, and d to be negative. In the sample where CEO's are at least 64 years old, we expect b to be positive, while c and d are expected to be negative.

The results of the logit regressions are presented in table 6. For the sample containing individuals less than 64 years old, the logit results support the hypothesis that abnormal stock price performance and the probability of a change in CEO are inversely related. The coefficient of C U M A B N is negative and has a chi-square value which is significant at the one percent level. The regression depicts a weak positive association between age and turnover for this sample. Finally, the logit regression describes a significant inverse relation

Table 6

Logit regressions of management turnover from year ( t + 1) to year ( t + 2) on the compensation regression residual from regression 4 of table 3, panels A and B; age of the executive in yea r t; and

the cumulative residual from the market model for year t. a

Const. R ES AGE CUMA BN Model

N u m b e r of turnover

N cases

A G E < 64: Coefficient - 6.08 - 2.10 0.063 - 1.46 482 43 Chi -square 7.05 5.34 2.54 6.90 15.31 Probability that

coefficient(s) = 0 0.008 0.021 0.111 0.009 0.002

A GE > 63: Coefficient 21.26 3.04 - 0.335 0.73 115 33 Chi -square 8.18 5.58 8.72 0.84 26.48 Probability that

coefficient(s) = 0 0.004 0.018 0.003 0.360 0.000

a The dependent turnover variable has a value of one if there was a change in the C E O f rom four to sixteen months after the end of the performance year. R E S is the residual from the appropriate compensation regression in table 3. C UMABN is the deflated sum of the da i ly a b n o r m a l returns over the f i rm's fiscal year. A G E is the age of the executive in year t.

64 A.T. Coughlan and R.M. Schmidt, Compensation, turnover and performance

between the compensation residual and the probability of turnover in the younger sample. Pay increases exceeding those implied by our measure of stock performance imply a lower probability of a change in CEO.

For the portion of the sample containing individuals who are at least 64 years old, the logit regression does not support the hypothesis that stock price performance is inversely related to the probability of turnover. The coefficient of the stock price variable has the wrong sign, but is not significant. The dominant variable for this group is AGE. The coefficient for that variable is negative a,'zd of greater statistical significance than any independent variable in the logit regressions for either age group. Undoubtedly this variable is captur- ing the substantially larger probability of turnover for those age 64. The regressions depict a positive and significant relation between the compensation residual and turnover probability, perhaps reflecting the payment of retirement bonuses.

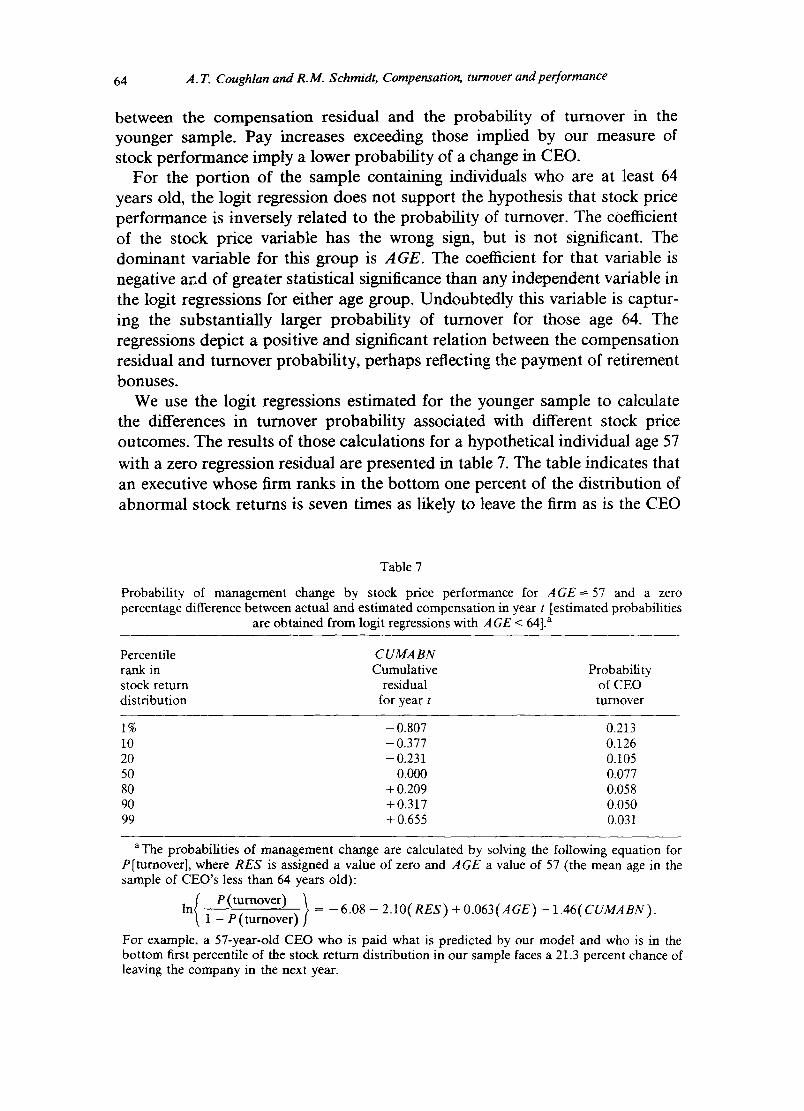

We use the logit regressions estimated for the younger sample to calculate the differences in turnover probability associated with different stock price outcomes. The results of those calculations for a hypothetical individual age 57 with a zero regression residual are presented in table 7. The table indicates that an executive whose firm ranks in the bottom one percent of the distribution of abnormal stock returns is seven times as likely to leave the firm as is the CEO

Table 7

Probability of management change by stock price performance for A G E = 57 and a zero percentage difference between actual and estimated compensation in year t [estimated probabilities

are obtained from logit regressions with A GE < 64]. a

Percentile CUMA BN rank in Cumulative Probability stock return residual of CEO distribution for year t turnover

1% - 0.807 0.213 10 - 0 . 3 7 7 0.126 20 - 0 . 2 3 1 0.105 50 0.000 0.077 80 + 0.209 0.058 90 +0 .317 0.050 99 +0 .655 0.031

a The probabilities of management change are calculated by solving the following equation for P[turnover], where RES is assigned a value of zero and AGE a value of 57 (the mean age in the sample of C E O ' s less than 64 years old):

in 1 - p ( t u ~ o v e r ) = - 6 . 0 8 - 2 . 1 0 ( R e S ) + 0.063 ( A a e ) - 1.46 ( C U M A ~ U / -

For example, a 57-year-old CEO who is paid what is predicted by our model and who is in the bottom first percentile of the stock return distribution in our sample faces a 21.3 percent chance of leaving the company in the next year.

A.T. Coughlan and R.M. Schmidt, Compensation, turnover and performance 65

of a firm in the top percentile. If the firm ranks at the twentieth percentile, the chance of a change in CEO is double that for a firm which ranks at t h e eightieth percentile. 18

In summary, the logit regression results are consistent with the hypothesis that stock price l~erformance and the probability of a change in CEO are inversely related. In the younger sample, where mandatory retirement is not a factor, that inverse relation is highly significant. The impact of stock price performance on turnover probability as depicted in table 7 appears substantial, given that many of the determinants of abnormal stock price variation are outside the control of top management and given that events, such as the death of a CEO, can result in management turnovers which are uncorrelated with stock performance. The results for the sample of older individuals reflect the retirement process for that group and therefore provide little evidence for our stock price/turnover hypothesis.

6. Conclusion

The modem corporation is a successful method for the organization of economic activity. It has survived the test of competition and continues to be a common organizational form. Nonetheless, many question whether the corpo- ration's operating procedures cause decision-makers to act in ways that benefit shareholders, the intended beneficiaries of the institution. In this paper, we attempt to give empirical content to alternative claims about the consequences of the corporation's internal control procedures. By examining the internal control mechanism, we seek to supplement the body of empirical literature which demonstrates that capital markets provide one solution for the problem of bad management [Jensen and Ruback (1983)].

In this paper we advance the hypothesis that corporate boards control top management behavior by making compensation and management termination decisions related to the firm's stock price performance. Our results are con- sistent with these hypotheses. In addition, we find some evidence that rates of change in compensation are related to sales growth for a portion of our sample, but in no case does such a significant relation diminish the significance or size of the relation between rates of change in pay and stock price performance. The relation between rates of change in pay and sales growth is strongest in a sample of CEO's which did not experience turnover during our sample period. These CEO's have the least incentive to engage in sales-enhanc- ing activities which do not increase current or future profits. In summary, we

18Actual frequencies for CEO's less than 64 years old are: 16 turnovers among the 96 observations (16.7 percent) in the lowest 20 percent of the abnormal stock return distribution, and 6 turnovers among the 96 observations (6.3 percent) in the top 20 percent of the distribution.

66 A.T. Coughlan and R.M. Schmidt, Compensation, turnover and performance

find empirical support for the proposition that executive compensation plans and management replacement decisions tend to align the incentives of top management with those of the firm's owners.

References

Baumol, William J., 1967, Business behavior, value and growth, Rev. ed. (Harcourt, Brace & World, New York).

Berle, A.A. and Gardner C. Means, 1932, The modern corporation and private property (Macmil- lan, New York).

Brealey, Richard and Stewart Myers, 1981, Principles of corporate finance (McGraw-Hill, New York).

Brown, Stephen J. and Jerold B. Warner, 1980, Measuring security price performance, Journal of Financial Economics 8, 205-258.

Cosh, Andrew, 1975, The remuneration of chief executives in the United Kingdom, Economic Journal 85, 75-94.

Fama, Eugene F., 1976, Foundations of finance (Basic Books, New York). Forbes Magazine, annual reports on executive compensation, May 29, 1978, 86-111; June 11,

1979, 117-148; June 9, 1980, 116-148; June 8, 1981, 114-146. Fox, Harland, 1982, Top executive compensation, 1982 ed. (The Conference Board, New York). Hirschey, Mark and James L. Pappas, 1981, Regulatory and life cycle influences of managerial

incentives, Southern Economic Journal 48, 327-334. Jensen, Michael C. and William H. Meckling, 1976, Theory of the firm: Managerial behavior,

agency costs, and ownership structure, Journal of Financial Economics 3,305-360. Jensen, Michael C. and Richard S. Ruback, 1983, The market for corporate control: The scientific

evidence, Journal of Financial Economics 11, 5-50. Kmenta, Jan, 1971, Elements of econometrics (Macmillan, New York). Lazear, Edward P. and Sherwin Rosen, 1981, Rank-order tournaments as optimum labor con-

tracts, Journal of Political Economy 89, 841-864. Lewellen, Wilbur G. and Blaine Huntsman, 1970, Managerial pay and corporate performance,

American Economic Review 60, 710-720. Loomis, Carol J., 1982, The madness of executive compensation, Fortune, July 12, 42-52. Manne, Henry G., 1965, Mergers and the market for corporate control, Journal of Political

Economy 73, 110-120. Marris, Robin, 1963, A model of the managerial enterprise, Quarterly Journal of Economics 77,

185-209. Masson, Robert T., 1971, Executive motivations, earnings, and consequent equity performance,

Journal of Political Economy 79, 1278-1292. McFadden, Daniel, 1976, The revealed preferences of a government bureaucracy: Empirical

evidence, Bell Journal of Economics 7, 55-72. McGuire, Joseph W., John S.Y. Chiu and Alvar O. Elbing, 1962, Executive income, sales and

profits, American Economic Review 52, 753-761. Meeks, Geoffrey and Geoffrey Whittington, 1975, Directors' pay, growth and profitability, Journal

of Industrial Economics 24, 1-14. Miller, Merton H. and Myron S. Scholes, 1982, Executive compensation, taxes, and incentives, in:

William F. Sharpe and Cathryn M. Cootner, eds., Financial economics: Essays in honor of Paul Cootner (Prentice-Hall, Englewood Cliffs, N J).

Murphy, Kevin J., 1985, Corporate performance and managerial remuneration, Journal of Accounting and Economics, forthcoming.

Smith, Clifford W., Jr. and Ross L. Watts, 1984, The structure of executive compensation contracts and the control of management, Working paper (Graduate School of Management, University of Rochester, Rochester, NY).