Embed Size (px)

Citation preview

Medtech 2015 in ReviewElizabeth Cairns & Madeleine Armstrong – March 2016

2 Copyright © 2016 Evaluate Ltd. All rights reserved.EP Vantage MedTech 2015 in Review

EP Vantage MedTech 2015 in Review

In 2015 the medtech industry saw the same pattern repeat itself across a number of metrics: fewer, bigger deals.

The total expenditure on M&A soared to previously unimagined heights, but the number of deals dropped from a

year earlier. The total amount of venture capital raised by medtech groups remained level, but the number of deals

crashed. And the explosion in IPOs that characterised last year has burned out – but those that did get away were

larger, on average, than in any year since EP Vantage started tracking floats.

Mergers worth more than $127bn were closed last year as companies consolidated in response to the factors

that have become characteristic of this market over that past year or two. Unabating pressure on pricing and a

diminishing number of customers as hospitals and insurers conduct consolidation of their own mean medtech groups

must build scale to meet their growth targets.

This then has knock-on effects. Consolidation of the largest companies means fewer buyers for the smaller groups,

which in turn have difficulty raising early-stage investment as VCs see the chances of an exit shrinking. The amount

of venture investment raised by medtech groups has remained stable over the past few years, yet the number of

deals done has fallen sharply; just 287 medtech companies managed to persuade investors that they were worth a

punt, a 30% decrease from 2014.

Also contributing to the misery of early-stage companies needing capital to keep afloat is the steady decrease in

IPO activity across the sector in 2015. Shareholders, like VCs, are interested only in revenue-stage companies; woe

betide a small medtech company seeking capital to fund R&D.

Medtech groups listed on stock exchanges have not been hammered in the same way as biotechs, but the public

markets have undoubtedly been disappointing across 2015 compared with previous years. Indices of US medtech

stocks posted modest rises, whereas in Europe the performance was flat.

Dismal as the environment appears, it does not seem to be preventing devices reaching patients: the US FDA

approved more products in 2015 than in any year in the previous decade. As if to compensate, however, European

regulation is getting tighter.

Though the effects of the ongoing changes to European regulatory legislation will be hard to quantify, they are

likely to make life harder for start-ups. These companies often rely on a swift, cheap CE mark to allow them to ramp

European sales before turning to the US; raising the bar to CE mark will cut off yet another source of early cash.

This is a harsh climate in which to grow as a medtech group, and the smaller the company is the harder the task becomes.

Unless stated, all data are sourced to EvaluateMedTech and were accessed in January 2016.

3 Copyright © 2016 Evaluate Ltd. All rights reserved.

Source: EvaluateMedTech® January 2016Medtech M&A Activity by Quarter

Dea

l Val

ue

Dea

l Cou

nt

10

20

40

30

50

60

70 90

80

70

60

50

40

30

20

10

0Q1

$4.3bn

Q2

$1.8bn

Q3

$7.9bn

Q4

$8.6bn

Q1

$5.9bn

Q2

$18.8bn

Q3

$9.1bn

Q4

$11.4bn

Q1

$2.5bn

Q2

$28.5bn

Q3

$7.4bn

Q4

$4.7bn

Q1

$3.5bn

Q2

$2.6bn

Q3

$8.4bn

Q4

$5.0bn

Q1

$19.8bn

Q2

$11.1bn

Q3

$5.3bn

Q4

$3.5bn

Q2

$15.3bn

Q3

$23.3bn

Q4

$19.7bn

0

Deal Value ($bn)

Deal Count

2011 2012 2013 2014 20152010

Year *Analysis conducted by deal completion date

Q1

$68.7bn

6360

58

79

59

66

72

55

59 60

52

64

58

47

58

45

58

46

42

30

44

56

45

51

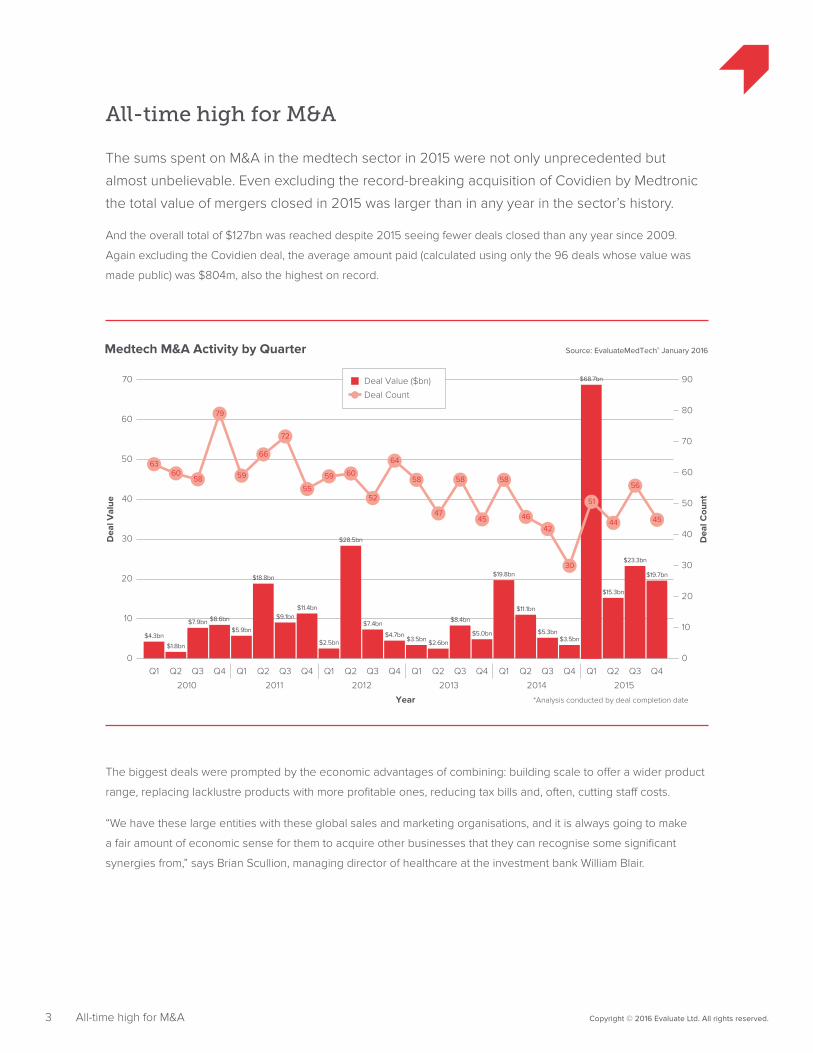

All-time high for M&A

The sums spent on M&A in the medtech sector in 2015 were not only unprecedented but

almost unbelievable. Even excluding the record-breaking acquisition of Covidien by Medtronic

the total value of mergers closed in 2015 was larger than in any year in the sector’s history.

And the overall total of $127bn was reached despite 2015 seeing fewer deals closed than any year since 2009.

Again excluding the Covidien deal, the average amount paid (calculated using only the 96 deals whose value was

made public) was $804m, also the highest on record.

All-time high for M&A

The biggest deals were prompted by the economic advantages of combining: building scale to offer a wider product

range, replacing lacklustre products with more profitable ones, reducing tax bills and, often, cutting staff costs.

“We have these large entities with these global sales and marketing organisations, and it is always going to make

a fair amount of economic sense for them to acquire other businesses that they can recognise some significant

synergies from,” says Brian Scullion, managing director of healthcare at the investment bank William Blair.

4 Copyright © 2016 Evaluate Ltd. All rights reserved.

Date Closed Target Sector(s) Value ($m)

26 January Covidien Anesthesia & Respiratory; Cardiology; General & Plastic Surgery; General Hospital & Healthcare Supply; Neurology; Patient Monitoring

49,900

2 October Twelve Cardiology 458

11 August RF Surgical Systems General & Plastic Surgery; General Hospital & Healthcare Supply 240

31 August Medina Medical Cardiology; Neurology 150

19 June Aptus Endosystems Cardiology 110

18 November Aircraft Medical Anesthesia & Respiratory; Ear, Nose & Throat; Endoscopy 110

28 September Lazarus Effect Cardiology 100

19 June CardioInsight Technologies Cardiology; Diagnostic Imaging 93

26 March Sophono Ear, Nose & Throat -

Medtronic’s 2015 Spending Spree Source: EvaluateMedTech® January 2016

All-time high for M&A

The interest of technology and software companies in devices is also hard to miss, with groups such as Google and

IBM forming alliances with medtech companies or buying them outright.

While the megamergers dominate the headlines, smaller and arguably more interesting deals are still occurring in

the background.

“Medtronic-Covidien, Zimmer-Biomet, St Jude-Thoratec – these are all noteworthy deals, but the important point

is that there’s still a fairly active acquisition market out there for smaller companies,” Mr Scullion told EP Vantage.

“Maybe they’re not worthy of the front page of the Wall Street Journal, but the source of innovation and the economic

benefit of consolidation continues to be pronounced.”

Indeed, a company making a large purchase does not have to forswear smaller deals. Medtronic has been

extraordinarily active as a buyer, closing eight acquisitions besides its integration of Covidien, and spending over $1bn

among them. These nine deals put it way out in front as the most prolific acquirer as well as the biggest spender.

Medtronic is a good illustration of the two main reasons for M&A. The Covidien deal was about scale, dovetailing

the two groups’ portfolios to provide hospitals and other customers with a single vendor for many of their products,

particularly in cardiology and neurology.

The other take outs, though, were more to do with the promise of each company’s technology. Medtronic swooped

on Twelve to get hold of its catheter-mounted artificial mitral valve, gaining a presence in the technology area that

arguably saw 2015’s most frenzied activity.

These kinds of technology-focused tuck-in deals have historically been the lifeblood of the sector, and they are more

important to its long-term health than the megamergers. It is vital that they continue.

Daniel Bertholet, a senior investment director at the VC company Endeavour Vision, is optimistic on this point. “The

large strategic medtech companies need innovation in order to generate revenue growth. They’re very selective in

their acquisitions, but they keep making acquisitions,” he says. “It’s the business model of the industry.”

5 Copyright © 2016 Evaluate Ltd. All rights reserved.All-time high for M&A

The poor performance of medtech stocks – not as bad as biotech, but disappointing compared with prior years –

might also work to keep merger activity going as targets become more affordable.

Acquirer Target Value ($bn)

Medtronic Covidien 49.9

Zimmer Biomet Biomet 14.0

Danaher Pall 13.8

Becton Dickinson CareFusion 12.2

LivaNova Sorin 3.4

Wright Medical Group Tornier 3.3

St. Jude Medical Thoratec 3.3

EQT Partners Audiology Solutions business of Siemens 2.7

Hill-Rom Welch Allyn 2.1

Cardinal Health Cordis business of Johnson & Johnson 1.9

Top 10 Takeouts Closed in 2015 Source: EvaluateMedTech® January 2016

Another sign that 2015 was no ordinary year is the fact that all of the top 10 deals were worth in excess of $1bn. In fact

there were no fewer than 18 billion-dollar deals last year, compared with seven in 2014 and four in 2013. The last year

that saw anything like this number was 2007, when 14 billion-dollar transactions were concluded.

So 2015 was one for the record books on a number of counts. 2016 will not match it, and might well trail it significantly.

6 Copyright © 2016 Evaluate Ltd. All rights reserved.

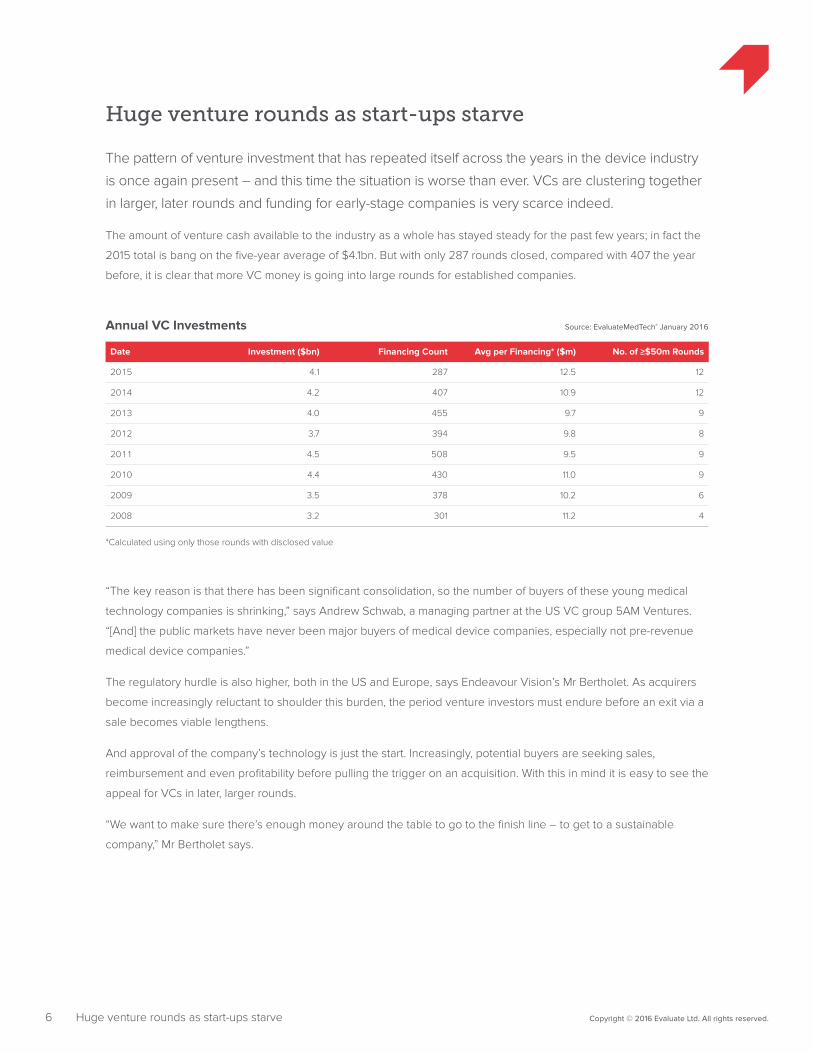

Huge venture rounds as start-ups starve

The pattern of venture investment that has repeated itself across the years in the device industry

is once again present – and this time the situation is worse than ever. VCs are clustering together

in larger, later rounds and funding for early-stage companies is very scarce indeed.

The amount of venture cash available to the industry as a whole has stayed steady for the past few years; in fact the

2015 total is bang on the five-year average of $4.1bn. But with only 287 rounds closed, compared with 407 the year

before, it is clear that more VC money is going into large rounds for established companies.

Date Investment ($bn) Financing Count Avg per Financing* ($m) No. of ≥$50m Rounds

2015 4.1 287 12.5 12

2014 4.2 407 10.9 12

2013 4.0 455 9.7 9

2012 3.7 394 9.8 8

2011 4.5 508 9.5 9

2010 4.4 430 11.0 9

2009 3.5 378 10.2 6

2008 3.2 301 11.2 4

Annual VC Investments Source: EvaluateMedTech® January 2016

*Calculated using only those rounds with disclosed value

Huge venture rounds as start-ups starve

“The key reason is that there has been significant consolidation, so the number of buyers of these young medical

technology companies is shrinking,” says Andrew Schwab, a managing partner at the US VC group 5AM Ventures.

“[And] the public markets have never been major buyers of medical device companies, especially not pre-revenue

medical device companies.”

The regulatory hurdle is also higher, both in the US and Europe, says Endeavour Vision’s Mr Bertholet. As acquirers

become increasingly reluctant to shoulder this burden, the period venture investors must endure before an exit via a

sale becomes viable lengthens.

And approval of the company’s technology is just the start. Increasingly, potential buyers are seeking sales,

reimbursement and even profitability before pulling the trigger on an acquisition. With this in mind it is easy to see the

appeal for VCs in later, larger rounds.

“We want to make sure there’s enough money around the table to go to the finish line – to get to a sustainable

company,” Mr Bertholet says.

7 Copyright © 2016 Evaluate Ltd. All rights reserved.Huge venture rounds as start-ups starve

1,000

800

600

400

200

Source: EvaluateMedTech® January 2016Quarterly Medtech VC Investments

Inve

stm

ent

Fina

ncin

g C

ount

1,400

1,200

1,600

1,800

2,000 140

120

100

80

60

40

20

0

Investment ($m)

Financing Count

Year

2008 2009 2010 2011 2012 2013 2014 2015

Q1

81

Q2

70

Q3

72

Q4

78

Q1

81

Q2

100

Q3

95

Q4

102

Q1

102

Q2

113

Q3

104

Q4

111

Q1

131

Q2

123

Q3

135

Q4

119

Q1

110

Q2

102

Q3

85

Q4

97

Q1

118

Q2

128

Q3

118

Q4

91

Q1

104

Q2

101

Q3

104

Q4

98

Q1

88

Q2

97

Q3

51

Q4

$796

m

$607

m

$805

m $951

m

$659

m

$1,15

9m

$885

m

$818

m

$826

m

$1,3

96m

$1,0

73m

$1,14

1m

$1,12

6m

$1,0

78m $1

,232

m

$1,0

81m

$1,10

3m

$1,14

2m

$690

m

$727

m

$995

m

$1,2

48m

$931

m

$876

m

$816

m

$1,2

06m

$1,0

08m

$1,19

3m

$922

m $1,15

2m

$1,10

2m

$832

m

51

0

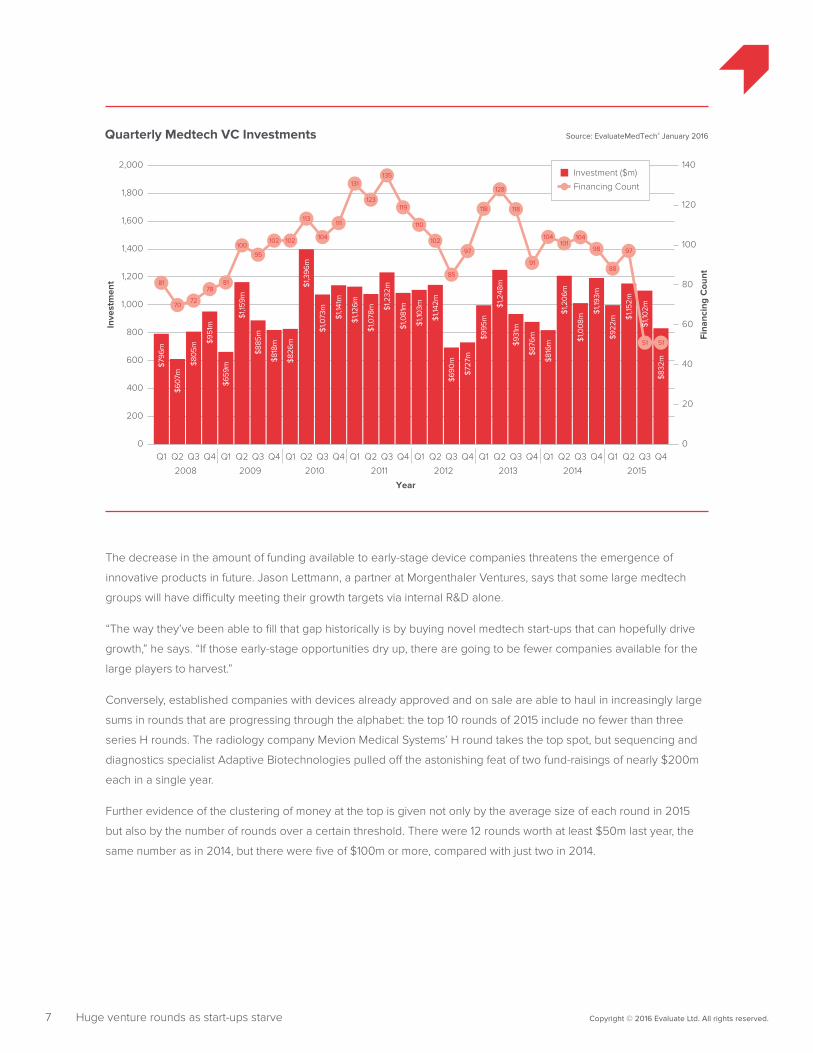

The decrease in the amount of funding available to early-stage device companies threatens the emergence of

innovative products in future. Jason Lettmann, a partner at Morgenthaler Ventures, says that some large medtech

groups will have difficulty meeting their growth targets via internal R&D alone.

“The way they’ve been able to fill that gap historically is by buying novel medtech start-ups that can hopefully drive

growth,” he says. “If those early-stage opportunities dry up, there are going to be fewer companies available for the

large players to harvest.”

Conversely, established companies with devices already approved and on sale are able to haul in increasingly large

sums in rounds that are progressing through the alphabet: the top 10 rounds of 2015 include no fewer than three

series H rounds. The radiology company Mevion Medical Systems’ H round takes the top spot, but sequencing and

diagnostics specialist Adaptive Biotechnologies pulled off the astonishing feat of two fund-raisings of nearly $200m

each in a single year.

Further evidence of the clustering of money at the top is given not only by the average size of each round in 2015

but also by the number of rounds over a certain threshold. There were 12 rounds worth at least $50m last year, the

same number as in 2014, but there were five of $100m or more, compared with just two in 2014.

8 Copyright © 2016 Evaluate Ltd. All rights reserved.

Company Round Investment ($m)

Mevion Medical Systems Series H 200.0

Adaptive Biotechnologies Series F 195.0

Adaptive Biotechnologies Series E 189.5

Oxford Nanopore Technologies Series H 109.0

CeQur Series C 100.0

Silk Road Medical Series D 57.0

Natera Series F 55.5

Calhoun Vision Series G 52.0

Outset Medical Series Undisclosed 51.0

EndoGastric Solutions Series H 50.0

Top 10 VC Rounds of 2015 Source: EvaluateMedTech® January 2016

Huge venture rounds as start-ups starve

A clustering effect is also seen in terms of therapy areas. Adaptive and Mevion are both cancer focused, and Oxford

Nanopore Technologies and Natera are diagnostics groups. Mr Schwab says that investing in a hot area can be a

catch-22, with overexcitement leading to overly risky companies being funded. “You get a high degree of failures,”

he says, though he adds that it can be very rewarding, and a company being active in a high-growth area is usually

a positive.

While excessively risky companies should be avoided, some risk is necessary. Investors must take more chances

if the medtech sector is to remain healthy. It is vital to plant the seeds now if there is to be a new crop of takeover

targets available in years to come.

9 Copyright © 2016 Evaluate Ltd. All rights reserved.

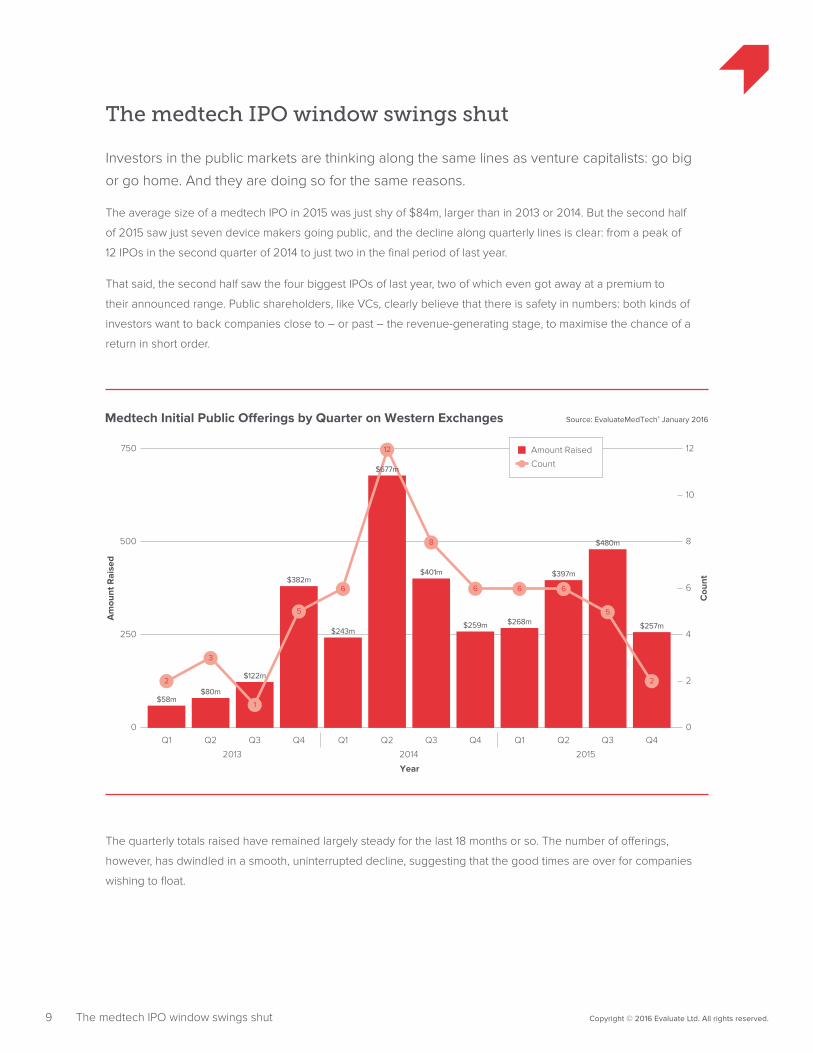

The medtech IPO window swings shut

Investors in the public markets are thinking along the same lines as venture capitalists: go big

or go home. And they are doing so for the same reasons.

The average size of a medtech IPO in 2015 was just shy of $84m, larger than in 2013 or 2014. But the second half

of 2015 saw just seven device makers going public, and the decline along quarterly lines is clear: from a peak of

12 IPOs in the second quarter of 2014 to just two in the final period of last year.

That said, the second half saw the four biggest IPOs of last year, two of which even got away at a premium to

their announced range. Public shareholders, like VCs, clearly believe that there is safety in numbers: both kinds of

investors want to back companies close to – or past – the revenue-generating stage, to maximise the chance of a

return in short order.

Source: EvaluateMedTech® January 2016Medtech Initial Public O�erings by Quarter on Western Exchanges

Am

ount

Rai

sed

Cou

nt

250

500

750 12

10

8

6

4

2

00

Amount Raised

Count

2013 2014 2015

Year

Q1

$58m

Q2

$80m

Q3

$122m

Q4

$382m

Q1

$243m

Q2 Q3

$401m

Q4

$259m

Q1

$268m

Q2

$397m

Q3

$480m

Q4

$257m

2

3

1

5

6

12

8

6 6 6

5

2

$677m

The medtech IPO window swings shut

The quarterly totals raised have remained largely steady for the last 18 months or so. The number of offerings,

however, has dwindled in a smooth, uninterrupted decline, suggesting that the good times are over for companies

wishing to float.

10 Copyright © 2016 Evaluate Ltd. All rights reserved.

Company Amount Raised ($m) Offering Price Discount/Premium 2015 YE Chg Since Float

Natera 180 $18.00 13% (40%)

Novocure 165 $22.00 (6%) (34%)

ConforMIS 135 $15.00 0% 15%

Penumbra 120 $30.00 13% 79%

Biocartis 109 €11.50 7% 15%

Glaukos 108 $18.00 9% 37%

Advanced Accelerator Applications 92 $16.00 0% 95%

Entellus Medical 78 $17.00 6% (1%)

Avinger 65 $13.00 0% 75%

Carbylan Therapeutics 65 $5.00 0% (28%)

Average across top 10 IPOs 112 - 4% 21%

Average across all 19 IPOs 74 - (3%) (4%)

Top 10 Medtech IPOs of 2015 Source: EvaluateMedTech® January 2016

The medtech IPO window swings shut

The poor performance of the Nasdaq and other markets across 2015 – most medtech indices rose but nowhere near

as much as they have in previous years – has effectively shut the window. Only two offerings got away in the last

three months of 2015 and as of mid-February there have been no listings on Western exchanges this year either.

“As valuations fall that tends to make IPOs more problematic,” says William Blair’s Mr Scullion. “Generally for younger,

faster-growing companies that money’s no longer available for them.”

Once again it is start-ups that are caught with no way out: most buyers will not look at companies without approvals,

sales and reimbursement, and potential shareholders appear to have the same criteria.

“Unless you’ve got a revenue-stage company with strong growth prospects it’s almost impossible at this point,” says

5AM Ventures’ Mr Schwab.

This is reflected in the largest IPOs of 2015. Nasdaq-listed Novocure’s technology is FDA-approved for glioblastoma,

and Natera, which closed the largest IPO of the past three years when it scored $180m in July, also has sales in the US.

Morgenthaler Ventures’ Mr Lettmann strikes a more optimistic note. “I still think there’s going to be an appetite for

device companies,” he says. “Particularly companies that are revenue-stage and growing, I believe those companies

will always be able to go out regardless of the market.”

Natera’s success was not just due to being on the market – it also benefited from a takeout of one of its peers. Its

flagship technology is Panorama, which can diagnose foetal abnormalities by testing not the foetus’s blood but the

pregnant woman’s. This arena has been the subject of huge excitement since a group with a similar technology,

Ariosa Diagnostics, was taken out by Roche at the end of 2014.

With IPOs increasingly regarded as financing events rather than exits in themselves, Natera’s venture investors are

doubtless keen on a similar outcome.

11 Copyright © 2016 Evaluate Ltd. All rights reserved.The medtech IPO window swings shut

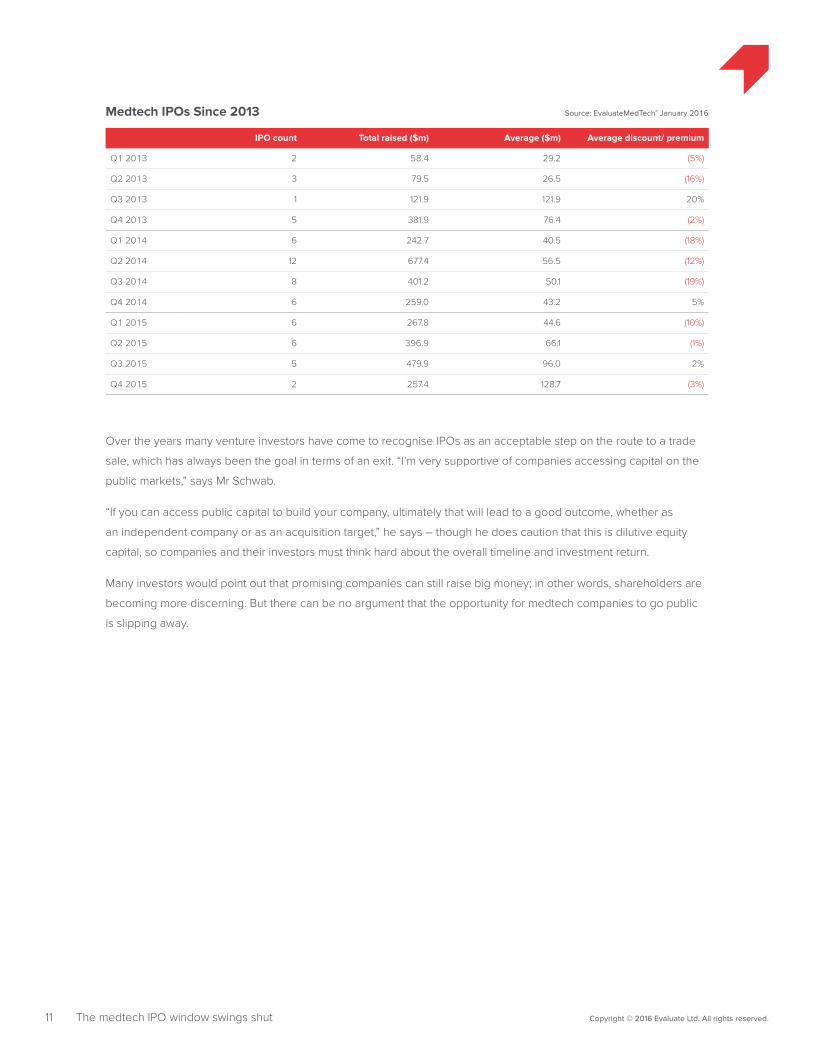

IPO count Total raised ($m) Average ($m) Average discount/ premium

Q1 2013 2 58.4 29.2 (5%)

Q2 2013 3 79.5 26.5 (16%)

Q3 2013 1 121.9 121.9 20%

Q4 2013 5 381.9 76.4 (2%)

Q1 2014 6 242.7 40.5 (18%)

Q2 2014 12 677.4 56.5 (12%)

Q3 2014 8 401.2 50.1 (19%)

Q4 2014 6 259.0 43.2 5%

Q1 2015 6 267.8 44.6 (10%)

Q2 2015 6 396.9 66.1 (1%)

Q3 2015 5 479.9 96.0 2%

Q4 2015 2 257.4 128.7 (3%)

Medtech IPOs Since 2013 Source: EvaluateMedTech® January 2016

Over the years many venture investors have come to recognise IPOs as an acceptable step on the route to a trade

sale, which has always been the goal in terms of an exit. “I’m very supportive of companies accessing capital on the

public markets,” says Mr Schwab.

“If you can access public capital to build your company, ultimately that will lead to a good outcome, whether as

an independent company or as an acquisition target,” he says – though he does caution that this is dilutive equity

capital, so companies and their investors must think hard about the overall timeline and investment return.

Many investors would point out that promising companies can still raise big money; in other words, shareholders are

becoming more discerning. But there can be no argument that the opportunity for medtech companies to go public

is slipping away.

12 Copyright © 2016 Evaluate Ltd. All rights reserved.

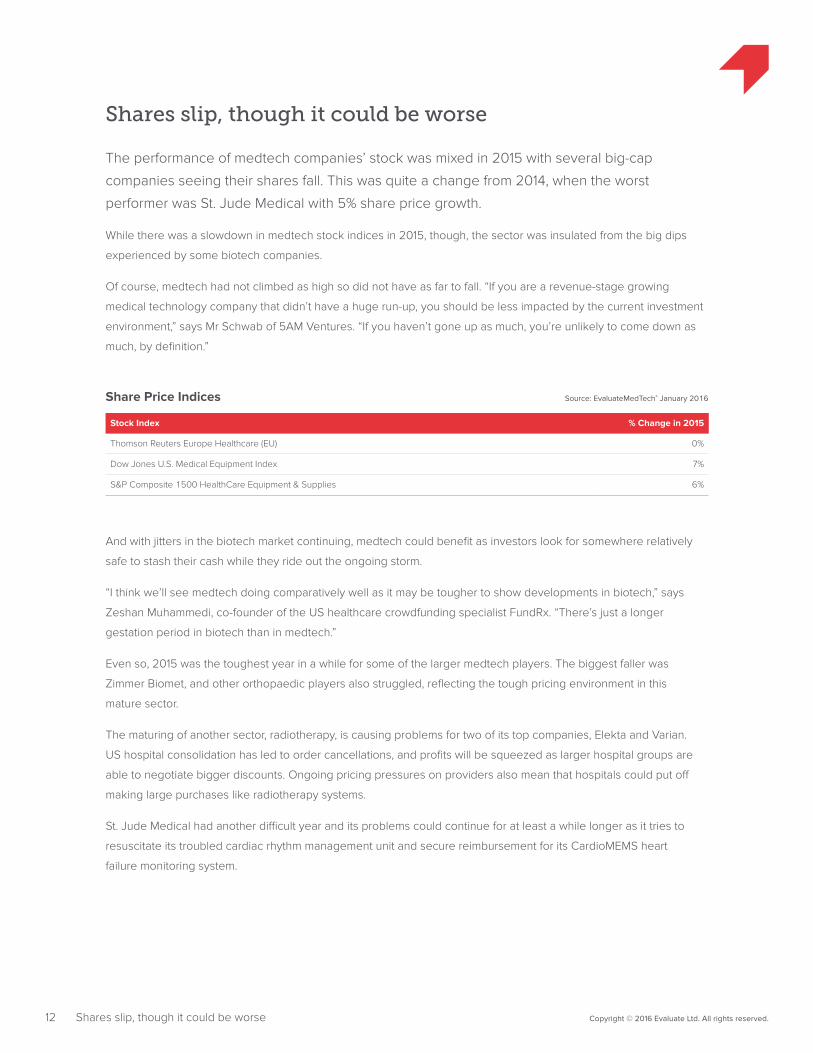

Shares slip, though it could be worse

The performance of medtech companies’ stock was mixed in 2015 with several big-cap

companies seeing their shares fall. This was quite a change from 2014, when the worst

performer was St. Jude Medical with 5% share price growth.

While there was a slowdown in medtech stock indices in 2015, though, the sector was insulated from the big dips

experienced by some biotech companies.

Of course, medtech had not climbed as high so did not have as far to fall. “If you are a revenue-stage growing

medical technology company that didn’t have a huge run-up, you should be less impacted by the current investment

environment,” says Mr Schwab of 5AM Ventures. “If you haven’t gone up as much, you’re unlikely to come down as

much, by definition.”

Stock Index % Change in 2015

Thomson Reuters Europe Healthcare (EU) 0%

Dow Jones U.S. Medical Equipment Index 7%

S&P Composite 1500 HealthCare Equipment & Supplies 6%

Share Price Indices Source: EvaluateMedTech® January 2016

Shares slip, though it could be worse

And with jitters in the biotech market continuing, medtech could benefit as investors look for somewhere relatively

safe to stash their cash while they ride out the ongoing storm.

“I think we’ll see medtech doing comparatively well as it may be tougher to show developments in biotech,” says

Zeshan Muhammedi, co-founder of the US healthcare crowdfunding specialist FundRx. “There’s just a longer

gestation period in biotech than in medtech.”

Even so, 2015 was the toughest year in a while for some of the larger medtech players. The biggest faller was

Zimmer Biomet, and other orthopaedic players also struggled, reflecting the tough pricing environment in this

mature sector.

The maturing of another sector, radiotherapy, is causing problems for two of its top companies, Elekta and Varian.

US hospital consolidation has led to order cancellations, and profits will be squeezed as larger hospital groups are

able to negotiate bigger discounts. Ongoing pricing pressures on providers also mean that hospitals could put off

making large purchases like radiotherapy systems.

St. Jude Medical had another difficult year and its problems could continue for at least a while longer as it tries to

resuscitate its troubled cardiac rhythm management unit and secure reimbursement for its CardioMEMS heart

failure monitoring system.

Share Price (Local Currency) Market Capitalisation ($bn)

Top 5 Risers YE 2014 YE 2015 Change YE 2015 12M Change

Boston Scientific $13.25 $18.44 39% 24.8 7.2

Essilor International €92.68 €115.05 24% 27.9 2.6

Edwards Lifesciences* $63.69 $78.98 24% 17.0 3.4

HOYA ¥4,105.00 ¥4,981.00 21% 17.3 1.1

Becton Dickinson $139.16 $154.09 11% 32.7 5.6

Top 5 Fallers

Zimmer Biomet** $113.42 $102.59 (10%) 20.9 1.7

St. Jude Medical $65.03 $61.77 (5%) 17.5 (1.1)

Baxter International*** $39.82 $38.15 (4%) 20.9 (18.9)

Smith & Nephew $36.74 $35.60 (3%) 16.0 (0.9)

Stryker $94.33 $92.94 (1%) 35.0 (0.7)

Large Cap ($15bn+) Medtech Companies: Top Risers and Fallers in 2015 Source: EvaluateMedTech® January 2016

* Corrected for 2:1 stock split** Name change from Zimmer post Biomet acquisition*** Corrected for spinout of Baxalta

13 Copyright © 2016 Evaluate Ltd. All rights reserved.Shares slip, though it could be worse

While some companies suffered, there were also some impressive risers – and unlike in 2014, when stock

performance was bolstered by acquisitions, 2015’s biggest gainers largely had innovation to thank, with groups like

Boston Scientific, Edwards Lifesciences and Abiomed rising on the back of key product approvals.

Others were helped by being active in hot sectors. The blood glucose monitoring specialist DexCom made it into the

top five mid-cap risers in both 2014 and 2015, partly owing to its presence in an ever-expanding area, diabetes, and

its involvement in the next big thing in that space, the artificial pancreas.

The growing popularity of proton therapy propelled IBA Group to the top of the small-cap chart, while Nevro’s

presence in pain management, with its best-in-class spinal cord stimulator, helped its share price surge.

Morgenthaler Ventures’ Mr Lettmann agrees that neurology is a popular area for public and private investors.

“There’s still a lot of unmet need there, and a lot of places where devices can play a role.”

He also rates structural heart as a compelling sector, as well as any area where devices can impact drug markets.

14 Copyright © 2016 Evaluate Ltd. All rights reserved.Shares slip, though it could be worse

Share Price (Local Currency) Market Capitalisation ($bn)

Five Selected Risers YE 2014 YE 2015 Change YE 2015 12M Change

DexCom $55.05 $81.90 49% 6.7 2.4

Lepu Medical Technology Yuan23.8 Yuan38.6 62% 4.9 1.8

Abiomed $38.06 $90.28 137% 3.8 2.3

Nevro $38.67 $67.51 75% 1.9 0.9

LeMaitre Vascular $7.65 $17.25 125% 0.3 0.2

Five Selected Fallers

Sonova SFr146.9 SFr127.3 (13%) 8.8 (1.6)

Varian Medical Systems $89.00 $80.80 (9%) 7.9 (1.1)

Elekta SKr79.7 SKr72.1 (10%) 3.2 (0.9)

GenMark Diagnostics $13.61 $7.76 (43%) 0.3 (0.2)

OvaScience $44.22 $9.77 (78%) 0.3 (0.8)

Other Significant Risers and Fallers in 2015 (Ranked on Market Cap) Source: EvaluateMedTech® January 2016

This focus on innovation bodes well for the industry. If larger companies are being rewarded for the approval of

novel devices, they will hopefully be willing to invest in new technology, perhaps by acquiring smaller players with

promising approaches. This is vital to the medtech ecosystem.

There was a great deal of variation in stock performance in 2015 – much more than in 2014. The volatility seen so far

in 2016 suggests that even more medtech companies will end the coming year in the red.

15 Copyright © 2016 Evaluate Ltd. All rights reserved.

More FDA approvals than ever

FDA approvals were the one unalloyed positive of the year – the agency gave the go-ahead

to 51 novel devices in 2015, the most in a decade. This just missed EP Vantage’s mid-year

prediction of 52 first-time premarket approvals and humanitarian device exemptions – but

nonetheless marked a 55% increase over 2014.

And the time taken to evaluate approvals was not markedly changed: the average review time was 17 months,

compared with 16.7 months in 2014. This suggests that measures brought in by the FDA to speed up approval times,

such as the expedited access PMA route, are yet to have their full effect, meaning that decisions could become even

quicker in the years to come.

Source: EvaluateMedTech® January 2016Number of PMAs and HDEs Granted, 2005-2015

Num

ber

of A

ppro

vals

10

20

30

40

50

60

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 20150

Year

34

44

3230

18

22

4341

23

33

51

More FDA approvals than ever

That said, removing a couple of outliers shows that things are already getting faster. Integrum’s OPRA osseo-

anchored prostheses for amputees took more than six and a half years to get the go-ahead, while Wright Medical’s

Augment bone graft took five and a half years. Excluding these, the average approval time for PMAs and HDEs was

just 14.6 months.

Other measures, including the de novo clearance route, introduced in 2014 for low-risk novel technologies, point to a

more accommodating FDA and an easier path to the market. If this is indeed the case it is a plus for smaller players,

especially with investors and potential acquirers increasingly looking for companies that have already cleared the

regulatory hurdles.

16 Copyright © 2016 Evaluate Ltd. All rights reserved.More FDA approvals than ever

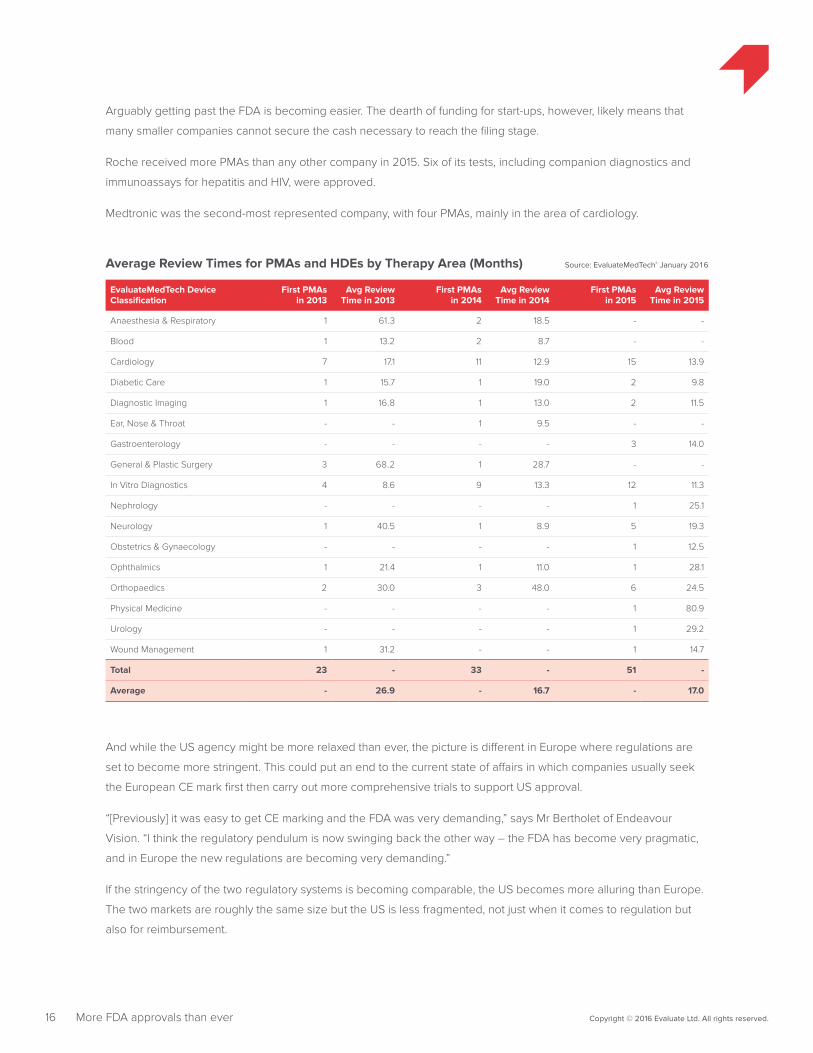

Arguably getting past the FDA is becoming easier. The dearth of funding for start-ups, however, likely means that

many smaller companies cannot secure the cash necessary to reach the filing stage.

Roche received more PMAs than any other company in 2015. Six of its tests, including companion diagnostics and

immunoassays for hepatitis and HIV, were approved.

Medtronic was the second-most represented company, with four PMAs, mainly in the area of cardiology.

EvaluateMedTech Device Classification

First PMAs in 2013

Avg Review Time in 2013

First PMAs in 2014

Avg Review Time in 2014

First PMAs in 2015

Avg Review Time in 2015

Anaesthesia & Respiratory 1 61.3 2 18.5 - -

Blood 1 13.2 2 8.7 - -

Cardiology 7 17.1 11 12.9 15 13.9

Diabetic Care 1 15.7 1 19.0 2 9.8

Diagnostic Imaging 1 16.8 1 13.0 2 11.5

Ear, Nose & Throat - - 1 9.5 - -

Gastroenterology - - - - 3 14.0

General & Plastic Surgery 3 68.2 1 28.7 - -

In Vitro Diagnostics 4 8.6 9 13.3 12 11.3

Nephrology - - - - 1 25.1

Neurology 1 40.5 1 8.9 5 19.3

Obstetrics & Gynaecology - - - - 1 12.5

Ophthalmics 1 21.4 1 11.0 1 28.1

Orthopaedics 2 30.0 3 48.0 6 24.5

Physical Medicine - - - - 1 80.9

Urology - - - - 1 29.2

Wound Management 1 31.2 - - 1 14.7

Total 23 - 33 - 51 -

Average - 26.9 - 16.7 - 17.0

Average Review Times for PMAs and HDEs by Therapy Area (Months) Source: EvaluateMedTech® January 2016

And while the US agency might be more relaxed than ever, the picture is different in Europe where regulations are

set to become more stringent. This could put an end to the current state of affairs in which companies usually seek

the European CE mark first then carry out more comprehensive trials to support US approval.

“[Previously] it was easy to get CE marking and the FDA was very demanding,” says Mr Bertholet of Endeavour

Vision. “I think the regulatory pendulum is now swinging back the other way – the FDA has become very pragmatic,

and in Europe the new regulations are becoming very demanding.”

If the stringency of the two regulatory systems is becoming comparable, the US becomes more alluring than Europe.

The two markets are roughly the same size but the US is less fragmented, not just when it comes to regulation but

also for reimbursement.

17 Copyright © 2016 Evaluate Ltd. All rights reserved.More FDA approvals than ever

Traditionally companies target CE mark first for their devices, taking the easier path to bring in revenue to keep them

going while negotiating the relatively lengthy and expensive US regulatory system. A change to this well-established

pattern could deprive young companies of a way of staying afloat.

Not all sectors are created equal when it comes to getting the FDA’s blessing. As in previous years, the cardiology

market saw the most approvals – 15 – while in vitro diagnostics was in second place with 12.

Source: EvaluateMedTech® January 2016First-time PMAs and HDEs by Therapy Area

Num

ber

of A

ppro

vals

2

4

6

12

10

8

16

14

2013 2014 2015

Car

diol

ogy

Blo

od

Ana

esth

esia

& R

espi

rato

ry

Ear,

Nos

e&

Thr

oat

Dia

gnos

ticIm

agin

g

Dia

betic

Car

e

In V

itro

Dia

gnos

tics

Gen

eral

&Pl

astic

Sur

gery

Gas

troen

tero

logy

Obs

tetri

cs &

Gyn

aeco

logy

Neu

rolo

gy

Nep

hrol

ogy

Phys

ical

Med

icin

e

Orth

opae

dics

Wou

ndM

anag

emen

t

Uro

logy

Oph

thal

mic

s

0

Cardiology and IVD approvals were also faster than the overall average, suggesting that the agency was keen to get

these products onto the market.

Concerns have been raised this year that the increasing pace at the agency could allow unsafe technologies onto

the market. But medtech companies will not be complaining. While doom pervades the sector the increase in FDA

approvals and the short time it took to get these were rare positives in 2015.

18 Copyright © 2016 Evaluate Ltd. All rights reserved.Where now?

Where now?

The only surprise in the device sector in 2015 is the degree to which the trends already long

evident have become even more entrenched.

The venture crisis is only becoming more pronounced, and eventually its effects will be felt in a big way: as more

start-ups fall by the wayside, unable to find the money to sustain themselves, fewer disruptive technologies will be

available for acquisition, and larger groups will be unable to sustain their growth rates.

As of mid-February 2016 there had already been five billion-dollar acquisitions, aimed either at building a wider

product range to help absorb the kind of discounts demanded by payers and providers, or at shifting a company’s

focus into areas of higher margins or greater demand. The number of tech-focused acquisitions of young companies

continues to drop: perhaps the groups at the top of the sector are already seeing the first consequences of the VC

downturn.

There appears to be little sign of the markets improving; device indices are down between 4% and 10% year to date.

It is hardly a surprise that not a single medtech company has yet braved Western stock exchanges so far this year.

The industry can at least hope that the sharp upward trend in FDA approvals seen over the past two years will

continue at the same rate. If it does, 2016 could see 70 or more novel devices reach the US.

But even then the majority of the approvals would go to established companies – those best able to afford them and,

in a sense, least in need of them.

Report authors: Elizabeth Cairns and Madeleine Armstrong

Additional complimentary copies of this report can be downloaded at: www.evaluategroup.com/Medtech2105Review

Evaluate Headquarters Evaluate Ltd. 1 1 -29 Fashion Street London E1 6PX United Kingdom T +44 (0)20 7377 0800 F +44 (0)20 7539 1801

Evaluate North America EvaluatePharma USA Inc. 15 Broad Street, Suite 401 Boston, MA 02109, USA T +1 617 573 9450 F +1 617 573 9542

Evaluate Japan Evaluate Japan KK Akasaka Garden City 4F 4-15-1 Akasaka, Minato-ku Tokyo 107-0052, Japan T +81 (0)80 1164 4754

www.evaluate.com

Established in 1996, Evaluate Ltd is the trusted leader in high quality life science sector analysis and consensus forecasts to 2020. Evaluate’s team of expert analysts transform life science information into insights so companies can perform well.

EvaluatePharma® delivers exclusive consensus sales forecasts and trusted commercial insight into biotech and pharmaceutical performance.

@EvaluatePharma

EvaluateMedTech® sets a new standard in commercial analysis and consensus forecasts of the global medical device and diagnostic industry.

@EvaluateMedTech

EvaluateClinical Trials® delivers unique clinical trial intelligence expertly curated to efficiently analyse the global clinical trial landscape.

@EPClinicalTrial

EP Vantage an award winning editorial team, provides daily commentary and analysis with fresh perspectives and insight into current and future industry trends.

@EPVantage

Evaluate Custom Services provides customised solutions to help you access, analyse and manage the information you need to support effective decision-making.

The Evaluate services enable the life science community to make sound business decisions about value and opportunity.

![[MR15] ハードコア デバッギング ~ Windows のアプリケーション運用トラブルシューティング実践](https://img.pdfslide.net/doc/110x75/5a6478857f8b9a27568b462f/mr15-windows-.jpg)