Embed Size (px)

Citation preview

Medtech 2016 in ReviewElizabeth Cairns – February 2017

2 Copyright © 2017 Evaluate Ltd. All rights reserved.EP Vantage Medtech Year in Review 2016

EP Vantage Medtech Year in Review 2016

2016 was a year of enormous change on the political stage. For the medical device industry, though, it was fairly quiet, with the pyrotechnics of 2015 a fast-fading memory. M&A activity settled back down after an onslaught of megamergers and the number of innovative devices to gain US approval sank slightly from the high of 51 the previous year.

This was to be expected; after the record amount spent on M&A in 2015 it was inevitable that activity would diminish

– not least because the companies that had conducted extensive business development activities would have less

time and money to spend looking at new deals. Even if the large-cap groups had wished to keep up the pace, the

number of targets remaining had dropped significantly.

The public markets were also lacklustre in 2016, with more large-cap companies falling further than in any period

since EP Vantage has been tracking their share price performance. The smaller groups, meanwhile, were buffeted

by the winds, rising or sinking according to their quarterly results rather than forging their own paths with bold

strategic decisions.

Despite the dim performance of listed companies in general, there was one startling upheaval on the public

exchanges: the largest IPO in medtech history, that of Convatec for nearly $2bn. While hardly an IPO in the traditional

sense – Convatec is long established and backed by private equity, rather than a developing company seeking

expansion capital from public investors – the deal was an notable event, all the more so for its location in London.

One area that did not walk back from the extremes of recent years was venture capital fundraising. This has got

progressively worse in terms of the total capital raised by early stage medtechs and in the number of rounds closed.

Each year it seems the situation can get no worse, yet each year it does, and the sector has now surely reached the

point at which the supply of innovative technology is imperilled.

Larger groups understand the importance of maintaining a healthy environment for start-ups and appear to be doing

what they can through their corporate VC arms. But they cannot turn the crisis around on their own.

Unless stated, all data are sourced to EvaluateMedTech and were accessed in January 2017.

3 Copyright © 2017 Evaluate Ltd. All rights reserved.M&A regresses to the mean

M&A regresses to the mean

When it comes to medtech consolidation, 2016 is the new 2014. The two years saw the same

number of M&A deals closed – 217 – and a very similar figure for their total value – $41.8bn last

year, versus $40.8bn two years earlier.

“It’s generally quiet,” says Gareth Down, head of European healthcare at the investment bank William Blair. “There are

areas where people are interested and trying to be active – areas like dental, and ophthalmology’s another one. Do I

see as much medtech activity outside of that? No.”

It is true that several billion-dollar deals were closed last year, but all were relatively modestly priced: the largest was

Canon’s purchase of Toshiba’s medtech division, at just $6bn.

This deal is unusual in that it is not an outright takeover. 2016 is notable for being the only year on record where the

largest deal is the transfer of a subsidiary from one conglomerate to another.

40

60

20

80

100

120

140

2015

127.9

MedtronicCovidien

Deal$49.9bn

Source: EvaluateMedTech® January 2017Medtech M&A Transactions Closed Over The Last Decade

Tota

l Dea

l Val

ue ($

bn)

Dea

l Cou

nt

450

400

350

300

250

200

150

100

50

00

Total Deal Value ($bn)

Deal Count

Year

2007

51.5

267

2008

27.7

226

2009

13.2

176

2010

20.5

267

2011

49.8

263

2012

44.9

245

2013

19.9

230

2014

40.8

217

2016

41.7

217227

Indeed the Canon-Toshiba deal is the largest business unit buy on record. It has transformed Canon’s medical device

business, which a year ago was dwarfed by Toshiba’s in terms of revenue. Canon is now the fourth biggest seller of

diagnostic imaging systems, behind Siemens, GE and Philips.

4 M&A regresses to the mean Copyright © 2017 Evaluate Ltd. All rights reserved.

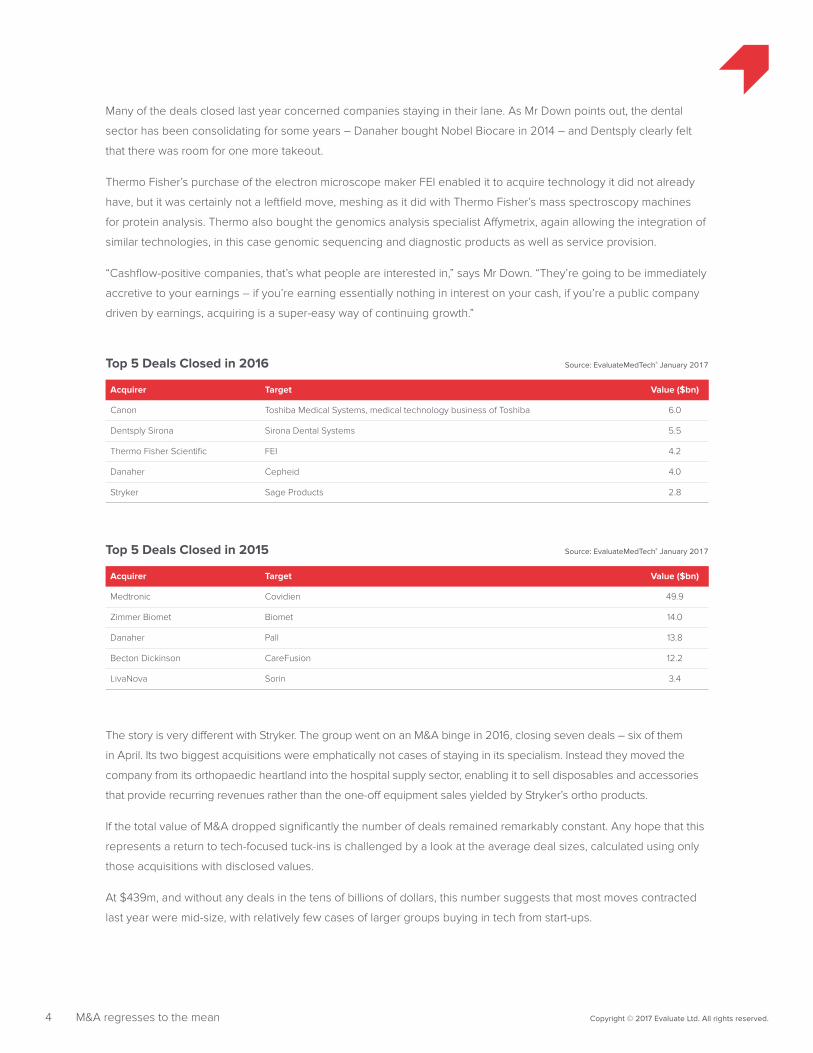

Many of the deals closed last year concerned companies staying in their lane. As Mr Down points out, the dental

sector has been consolidating for some years – Danaher bought Nobel Biocare in 2014 – and Dentsply clearly felt

that there was room for one more takeout.

Thermo Fisher’s purchase of the electron microscope maker FEI enabled it to acquire technology it did not already

have, but it was certainly not a leftfield move, meshing as it did with Thermo Fisher’s mass spectroscopy machines

for protein analysis. Thermo also bought the genomics analysis specialist Affymetrix, again allowing the integration of

similar technologies, in this case genomic sequencing and diagnostic products as well as service provision.

“Cashflow-positive companies, that’s what people are interested in,” says Mr Down. “They’re going to be immediately

accretive to your earnings – if you’re earning essentially nothing in interest on your cash, if you’re a public company

driven by earnings, acquiring is a super-easy way of continuing growth.”

Acquirer Target Value ($bn)

Canon Toshiba Medical Systems, medical technology business of Toshiba 6.0

Dentsply Sirona Sirona Dental Systems 5.5

Thermo Fisher Scientific FEI 4.2

Danaher Cepheid 4.0

Stryker Sage Products 2.8

Acquirer Target Value ($bn)

Medtronic Covidien 49.9

Zimmer Biomet Biomet 14.0

Danaher Pall 13.8

Becton Dickinson CareFusion 12.2

LivaNova Sorin 3.4

Top 5 Deals Closed in 2016 Source: EvaluateMedTech® January 2017

Top 5 Deals Closed in 2015 Source: EvaluateMedTech® January 2017

The story is very different with Stryker. The group went on an M&A binge in 2016, closing seven deals – six of them

in April. Its two biggest acquisitions were emphatically not cases of staying in its specialism. Instead they moved the

company from its orthopaedic heartland into the hospital supply sector, enabling it to sell disposables and accessories

that provide recurring revenues rather than the one-off equipment sales yielded by Stryker’s ortho products.

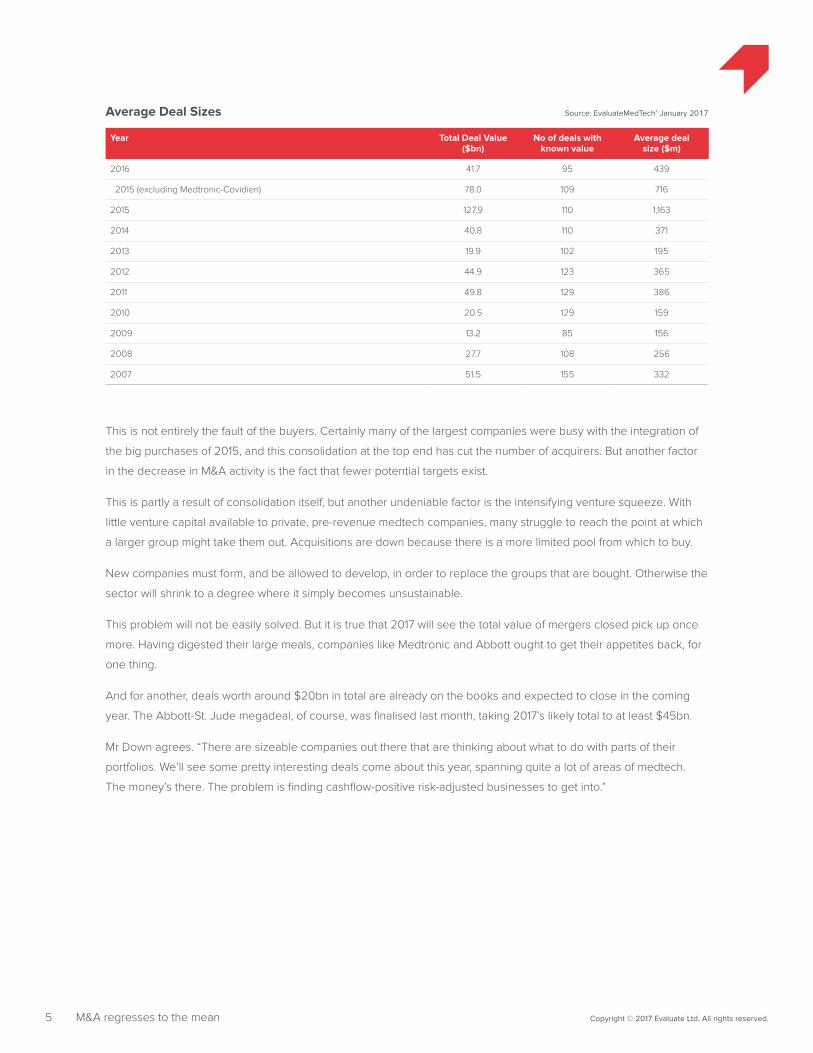

If the total value of M&A dropped significantly the number of deals remained remarkably constant. Any hope that this

represents a return to tech-focused tuck-ins is challenged by a look at the average deal sizes, calculated using only

those acquisitions with disclosed values.

At $439m, and without any deals in the tens of billions of dollars, this number suggests that most moves contracted

last year were mid-size, with relatively few cases of larger groups buying in tech from start-ups.

5

Year Total Deal Value ($bn)

No of deals with known value

Average deal size ($m)

2016 41.7 95 439

2015 (excluding Medtronic-Covidien) 78.0 109 716

2015 127.9 110 1,163

2014 40.8 110 371

2013 19.9 102 195

2012 44.9 123 365

2011 49.8 129 386

2010 20.5 129 159

2009 13.2 85 156

2008 27.7 108 256

2007 51.5 155 332

Average Deal Sizes Source: EvaluateMedTech® January 2017

M&A regresses to the mean Copyright © 2017 Evaluate Ltd. All rights reserved.

This is not entirely the fault of the buyers. Certainly many of the largest companies were busy with the integration of

the big purchases of 2015, and this consolidation at the top end has cut the number of acquirers. But another factor

in the decrease in M&A activity is the fact that fewer potential targets exist.

This is partly a result of consolidation itself, but another undeniable factor is the intensifying venture squeeze. With

little venture capital available to private, pre-revenue medtech companies, many struggle to reach the point at which

a larger group might take them out. Acquisitions are down because there is a more limited pool from which to buy.

New companies must form, and be allowed to develop, in order to replace the groups that are bought. Otherwise the

sector will shrink to a degree where it simply becomes unsustainable.

This problem will not be easily solved. But it is true that 2017 will see the total value of mergers closed pick up once

more. Having digested their large meals, companies like Medtronic and Abbott ought to get their appetites back, for

one thing.

And for another, deals worth around $20bn in total are already on the books and expected to close in the coming

year. The Abbott-St. Jude megadeal, of course, was finalised last month, taking 2017’s likely total to at least $45bn.

Mr Down agrees. “There are sizeable companies out there that are thinking about what to do with parts of their

portfolios. We’ll see some pretty interesting deals come about this year, spanning quite a lot of areas of medtech.

The money’s there. The problem is finding cashflow-positive risk-adjusted businesses to get into.”

6 A bad year for big-caps Copyright © 2017 Evaluate Ltd. All rights reserved.

A bad year for big-caps

The year just passed saw the share prices of more large-cap medical device companies fall

further than during any period since EP Vantage has been tracking their performance.

The worst performer, Coloplast, dropped an unprecedented 18%, and the risers did not perform as well as previously

either. 2016 was a disappointment for many in the medtech world, despite the pausing of the US medical device tax

and the promise of its total repeal in the coming year.

The general performance of medtech companies, as indicated by indices of device makers, has been less than

stellar. The US has declined markedly from the half-year point, but the situation in Europe was worse.

Stock Index % Change in 2016

Thomson Reuters Europe Healthcare (EU) (12%)

Dow Jones U.S. Medical Equipment Index 5%

S&P Composite 1500 HealthCare Equipment & Supplies 7%

Share Price Indices Source: EvaluateMedTech® January 2017

St. Jude Medical led the pack of big-cap movers, up 30% across 2016 thanks to the premium agreed by Abbott

Laboratories for its $25bn acquisition of the cardiovascular specialist. The deal was scheduled to close during 2016,

but this was delayed until the first week of January.

Stryker, in second position, has also been buoyed by deals, though as the buyer rather than the target. The

company’s share price has climbed steadily for years now, as it has positioned itself as a slow-and-steady safe haven

for investors’ cash.

This theory might be borne out by Philips’s rise. The Dutch group sold off its last lighting businesses in 2016 and

when the deal closes Philips will be almost pure medtech. Analysts expect the proceeds to be used to buy in new

technologies to beef up its medtech offering.

Market Capitalisation ($bn)

Top 5 Risers Share Price Change YE 2015 YE 2016 12M Change

St. Jude Medical ($) 30% 17.5 22.9 5.5

Stryker ($) 29% 35.0 44.9 9.9

Philips (€) 23% 24.6 29.7 5.0

Edwards Lifesciences ($) 19% 17.0 20.0 3.0

C. R. Bard ($) 19% 14.0 16.5 2.5

Large Cap ($10bn+) Medtech Companies: Top Risers and Fallers in 2016 Source: EvaluateMedTech® January 2017

continues over...

7 A bad year for big-caps Copyright © 2017 Evaluate Ltd. All rights reserved.

Market Capitalisation ($m)

Risers Share Price Change YE 2015 YE 2016 12M Change

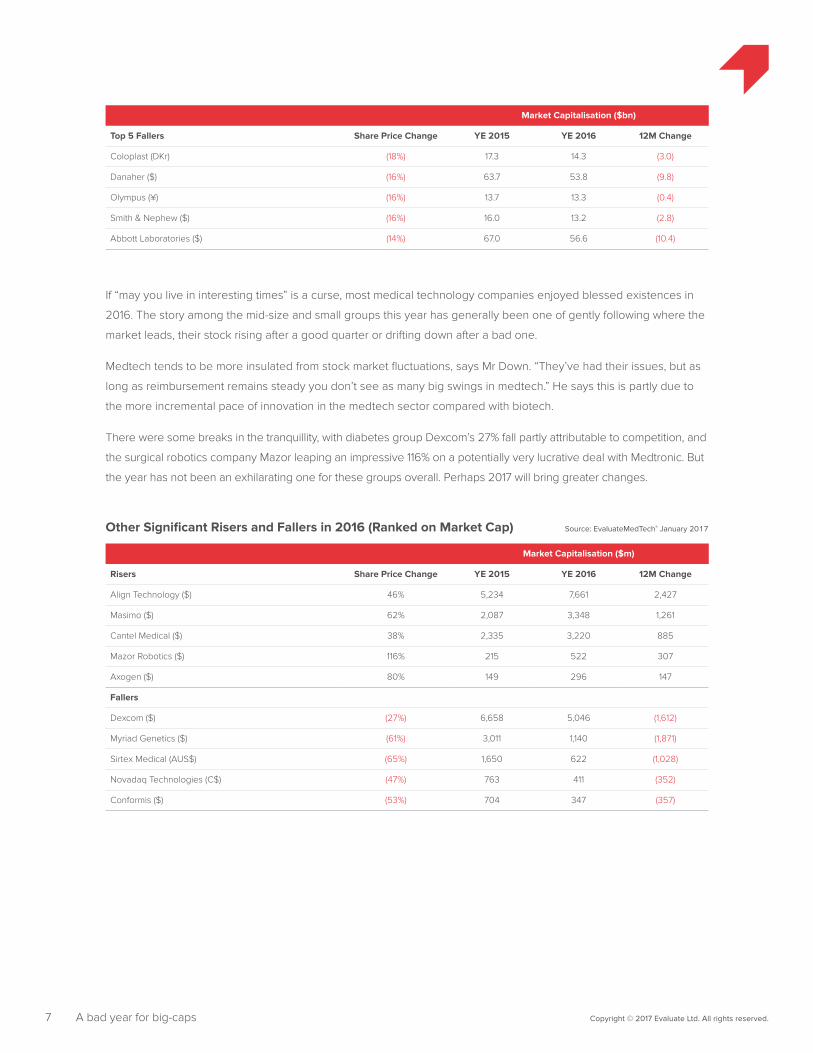

Align Technology ($) 46% 5,234 7,661 2,427

Masimo ($) 62% 2,087 3,348 1,261

Cantel Medical ($) 38% 2,335 3,220 885

Mazor Robotics ($) 116% 215 522 307

Axogen ($) 80% 149 296 147

Fallers

Dexcom ($) (27%) 6,658 5,046 (1,612)

Myriad Genetics ($) (61%) 3,011 1,140 (1,871)

Sirtex Medical (AUS$) (65%) 1,650 622 (1,028)

Novadaq Technologies (C$) (47%) 763 411 (352)

Conformis ($) (53%) 704 347 (357)

Other Significant Risers and Fallers in 2016 (Ranked on Market Cap) Source: EvaluateMedTech® January 2017

Market Capitalisation ($bn)

Top 5 Fallers Share Price Change YE 2015 YE 2016 12M Change

Coloplast (DKr) (18%) 17.3 14.3 (3.0)

Danaher ($) (16%) 63.7 53.8 (9.8)

Olympus (¥) (16%) 13.7 13.3 (0.4)

Smith & Nephew ($) (16%) 16.0 13.2 (2.8)

Abbott Laboratories ($) (14%) 67.0 56.6 (10.4)

If “may you live in interesting times” is a curse, most medical technology companies enjoyed blessed existences in

2016. The story among the mid-size and small groups this year has generally been one of gently following where the

market leads, their stock rising after a good quarter or drifting down after a bad one.

Medtech tends to be more insulated from stock market fluctuations, says Mr Down. “They’ve had their issues, but as

long as reimbursement remains steady you don’t see as many big swings in medtech.” He says this is partly due to

the more incremental pace of innovation in the medtech sector compared with biotech.

There were some breaks in the tranquillity, with diabetes group Dexcom’s 27% fall partly attributable to competition, and

the surgical robotics company Mazor leaping an impressive 116% on a potentially very lucrative deal with Medtronic. But

the year has not been an exhilarating one for these groups overall. Perhaps 2017 will bring greater changes.

8 A bad year for big-caps Copyright © 2017 Evaluate Ltd. All rights reserved.

It is striking how few of the mid and small-cap medtech companies rose or fell on data readouts or corporate activity.

Mostly the largest share movements came as a result of their financial reporting, as well as being a reflection of the

generally muted markets.

If the merger market does pick up in the coming year shares could surge once more; there are plenty of large

medtechs sitting on significant cash piles which, if they are able to find revenue-generating de-risked targets, could

push their earnings and hence their shares skywards.

Equally, uncertainty over the political changes coming in 2017 on both sides of the Atlantic could also mean that a

more turbulent year is on the way.

9 London sees biggest IPO ever Copyright © 2017 Evaluate Ltd. All rights reserved.

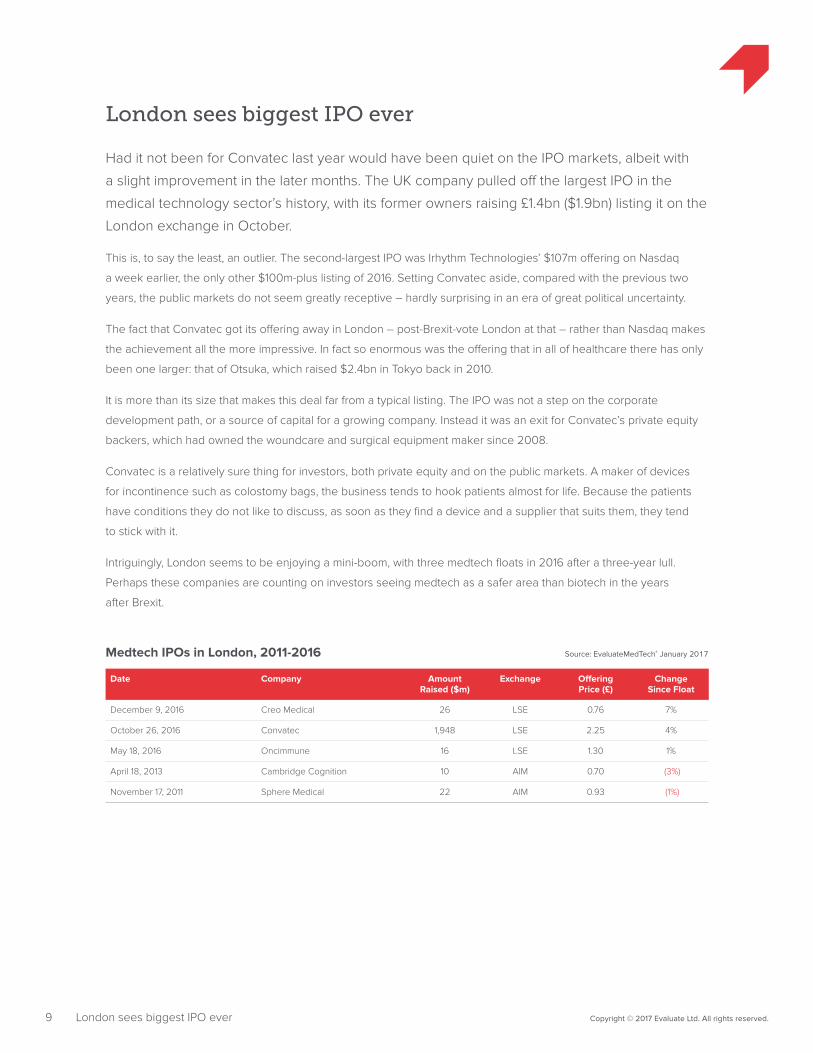

London sees biggest IPO ever

Had it not been for Convatec last year would have been quiet on the IPO markets, albeit with

a slight improvement in the later months. The UK company pulled off the largest IPO in the

medical technology sector’s history, with its former owners raising £1.4bn ($1.9bn) listing it on the

London exchange in October.

This is, to say the least, an outlier. The second-largest IPO was Irhythm Technologies’ $107m offering on Nasdaq

a week earlier, the only other $100m-plus listing of 2016. Setting Convatec aside, compared with the previous two

years, the public markets do not seem greatly receptive – hardly surprising in an era of great political uncertainty.

The fact that Convatec got its offering away in London – post-Brexit-vote London at that – rather than Nasdaq makes

the achievement all the more impressive. In fact so enormous was the offering that in all of healthcare there has only

been one larger: that of Otsuka, which raised $2.4bn in Tokyo back in 2010.

It is more than its size that makes this deal far from a typical listing. The IPO was not a step on the corporate

development path, or a source of capital for a growing company. Instead it was an exit for Convatec’s private equity

backers, which had owned the woundcare and surgical equipment maker since 2008.

Convatec is a relatively sure thing for investors, both private equity and on the public markets. A maker of devices

for incontinence such as colostomy bags, the business tends to hook patients almost for life. Because the patients

have conditions they do not like to discuss, as soon as they find a device and a supplier that suits them, they tend

to stick with it.

Intriguingly, London seems to be enjoying a mini-boom, with three medtech floats in 2016 after a three-year lull.

Perhaps these companies are counting on investors seeing medtech as a safer area than biotech in the years

after Brexit.

Date Company Amount Raised ($m)

Exchange Offering Price (£)

Change Since Float

December 9, 2016 Creo Medical 26 LSE 0.76 7%

October 26, 2016 Convatec 1,948 LSE 2.25 4%

May 18, 2016 Oncimmune 16 LSE 1.30 1%

April 18, 2013 Cambridge Cognition 10 AIM 0.70 (3%)

November 17, 2011 Sphere Medical 22 AIM 0.93 (1%)

Medtech IPOs in London, 2011-2016 Source: EvaluateMedTech® January 2017

10 London sees biggest IPO ever Copyright © 2017 Evaluate Ltd. All rights reserved.

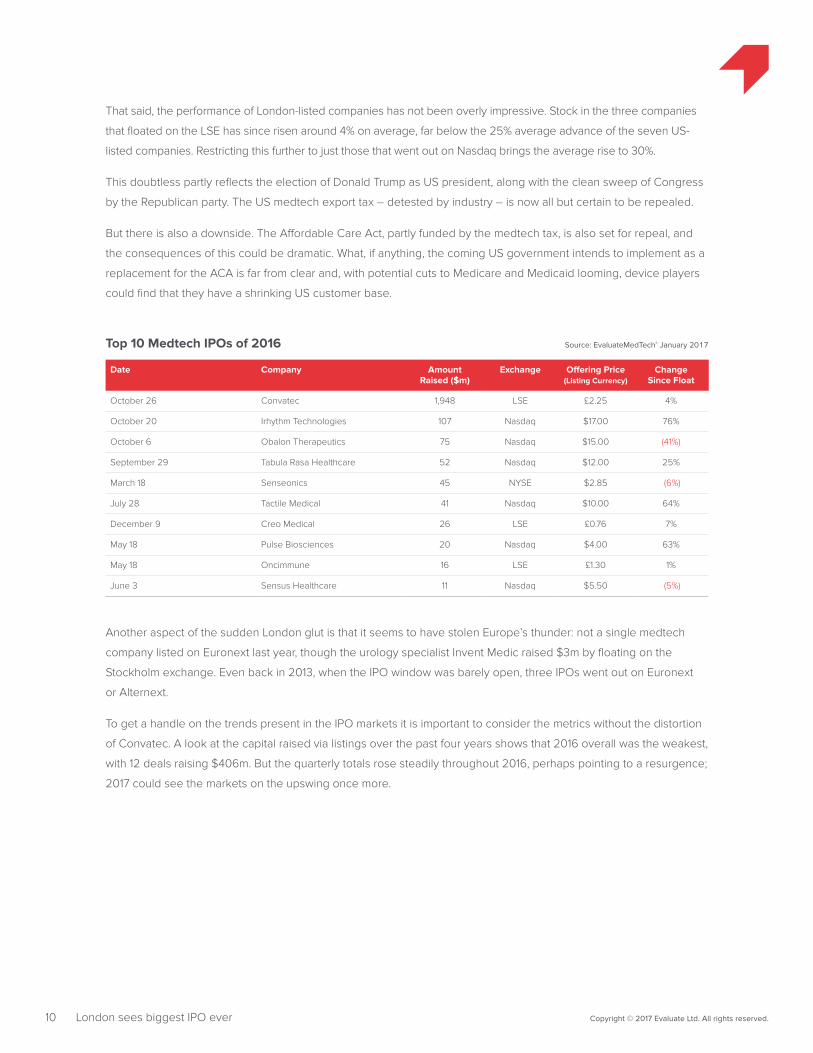

That said, the performance of London-listed companies has not been overly impressive. Stock in the three companies

that floated on the LSE has since risen around 4% on average, far below the 25% average advance of the seven US-

listed companies. Restricting this further to just those that went out on Nasdaq brings the average rise to 30%.

This doubtless partly reflects the election of Donald Trump as US president, along with the clean sweep of Congress

by the Republican party. The US medtech export tax – detested by industry – is now all but certain to be repealed.

But there is also a downside. The Affordable Care Act, partly funded by the medtech tax, is also set for repeal, and

the consequences of this could be dramatic. What, if anything, the coming US government intends to implement as a

replacement for the ACA is far from clear and, with potential cuts to Medicare and Medicaid looming, device players

could find that they have a shrinking US customer base.

Date Company Amount Raised ($m)

Exchange Offering Price (Listing Currency)

Change Since Float

October 26 Convatec 1,948 LSE £2.25 4%

October 20 Irhythm Technologies 107 Nasdaq $17.00 76%

October 6 Obalon Therapeutics 75 Nasdaq $15.00 (41%)

September 29 Tabula Rasa Healthcare 52 Nasdaq $12.00 25%

March 18 Senseonics 45 NYSE $2.85 (6%)

July 28 Tactile Medical 41 Nasdaq $10.00 64%

December 9 Creo Medical 26 LSE £0.76 7%

May 18 Pulse Biosciences 20 Nasdaq $4.00 63%

May 18 Oncimmune 16 LSE £1.30 1%

June 3 Sensus Healthcare 11 Nasdaq $5.50 (5%)

Top 10 Medtech IPOs of 2016 Source: EvaluateMedTech® January 2017

Another aspect of the sudden London glut is that it seems to have stolen Europe’s thunder: not a single medtech

company listed on Euronext last year, though the urology specialist Invent Medic raised $3m by floating on the

Stockholm exchange. Even back in 2013, when the IPO window was barely open, three IPOs went out on Euronext

or Alternext.

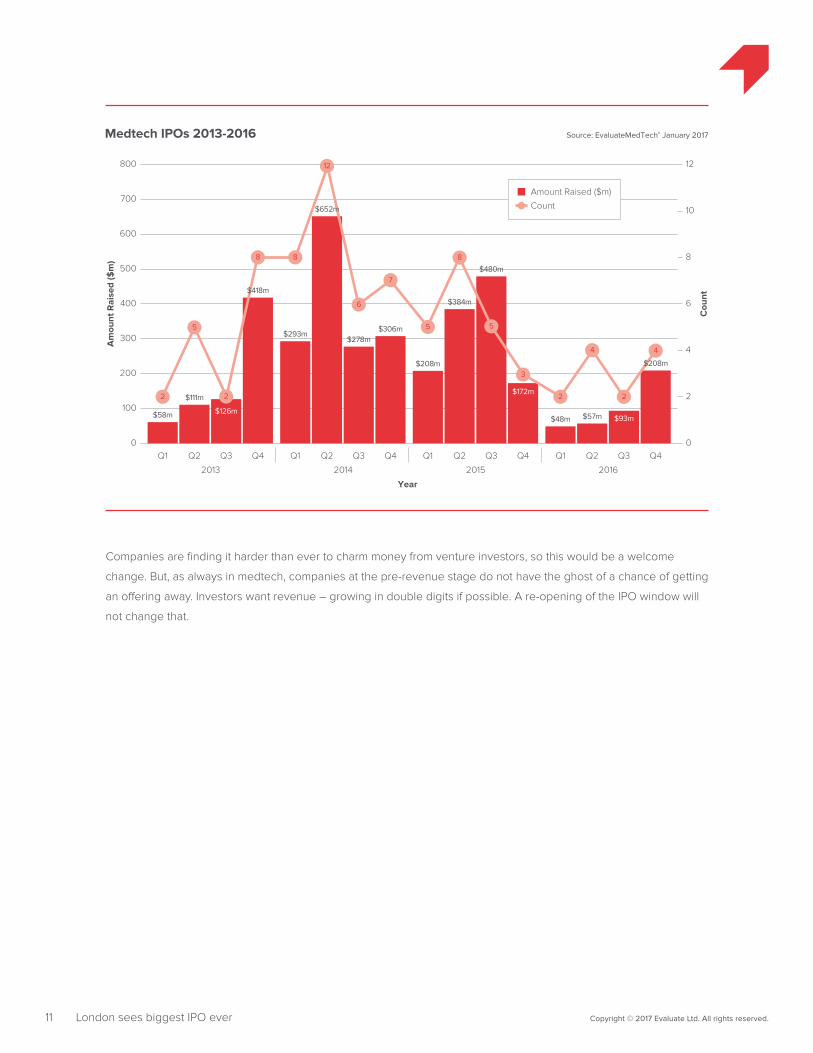

To get a handle on the trends present in the IPO markets it is important to consider the metrics without the distortion

of Convatec. A look at the capital raised via listings over the past four years shows that 2016 overall was the weakest,

with 12 deals raising $406m. But the quarterly totals rose steadily throughout 2016, perhaps pointing to a resurgence;

2017 could see the markets on the upswing once more.

11 London sees biggest IPO ever Copyright © 2017 Evaluate Ltd. All rights reserved.

Source: EvaluateMedTech® January 2017Medtech IPOs 2013-2016

Am

ount

Rai

sed

($m

)

Cou

nt

300

200

100

600

700

500

400

800 12

10

8

6

4

2

00

Amount Raised ($m)

Count

2013 201620152014

Year

Q1

$58m

Q2

$111m

Q3

$126m

Q4 Q1

$293m

Q2 Q3

$278m

Q4

$306m

Q1

$208m

Q2

$384m

Q3

$480m

Q4

$172m

Q1

$48m

Q2

$57m

Q3

$93m

Q4

44

22

$208m3

5

8

5

7

6

8

$652m

12

$418m

8

5

22

Companies are finding it harder than ever to charm money from venture investors, so this would be a welcome

change. But, as always in medtech, companies at the pre-revenue stage do not have the ghost of a chance of getting

an offering away. Investors want revenue – growing in double digits if possible. A re-opening of the IPO window will

not change that.

12 Even a $100m series A cannot save the venture climate Copyright © 2017 Evaluate Ltd. All rights reserved.

Even a $100m series A cannot save the venture climate

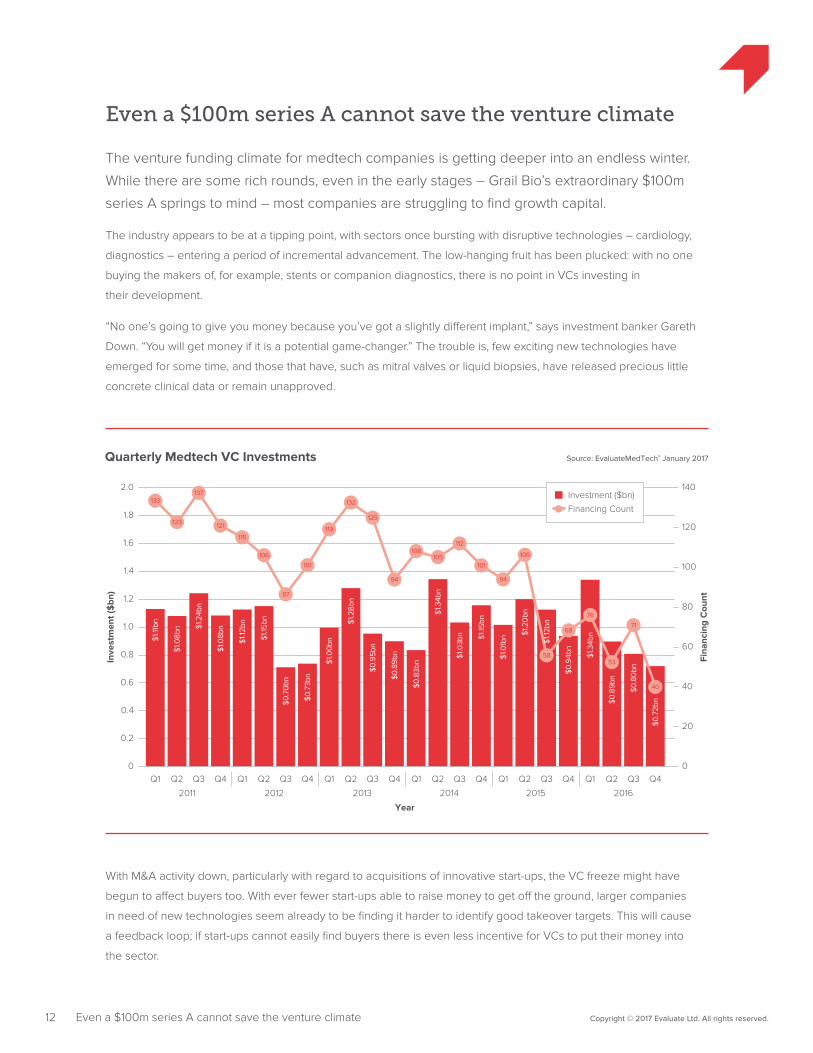

The venture funding climate for medtech companies is getting deeper into an endless winter.

While there are some rich rounds, even in the early stages – Grail Bio’s extraordinary $100m

series A springs to mind – most companies are struggling to find growth capital.

The industry appears to be at a tipping point, with sectors once bursting with disruptive technologies – cardiology,

diagnostics – entering a period of incremental advancement. The low-hanging fruit has been plucked: with no one

buying the makers of, for example, stents or companion diagnostics, there is no point in VCs investing in

their development.

“No one’s going to give you money because you’ve got a slightly different implant,” says investment banker Gareth

Down. “You will get money if it is a potential game-changer.” The trouble is, few exciting new technologies have

emerged for some time, and those that have, such as mitral valves or liquid biopsies, have released precious little

concrete clinical data or remain unapproved.

1.0

0.8

0.6

0.4

0.2

Source: EvaluateMedTech® January 2017Quarterly Medtech VC Investments

Inve

stm

ent (

$bn

)

Fina

ncin

g C

ount

1.4

1.2

1.6

1.8

2.0 140

120

100

80

60

40

20

0

Investment ($bn)

Financing Count

Year

20162011 2012 2013 2014 2015

Q2

$0.8

9bn

Q1

$1.11

bn

Q2

$1.0

8bn

Q3

$1.2

4bn

Q4

$1.0

8bn

Q1

$1.12

bn

Q2

$1.15

bn

Q3

$0.7

0bn

Q4

$0.7

3bn

Q1

$1.0

0bn

Q2

$1.2

8bn

Q3

$0.9

5bn

Q4

$0.8

9bn

Q1

$0.8

3bn

Q2

$1.3

4bn

Q3

$1.0

3bn

Q4

$1.15

bn

Q1

$1.0

1bn

Q2

$1.2

0bn

Q3 Q4

$0.9

4bn

Q1

$1.3

4bn

Q3

$0.8

0bn

Q4

$0.7

2bn

76

133137

123 121

115119

125

106

101

108105

112

101

106

132

87

94 94

0

71

53

40

58

68

$1.12

bn

With M&A activity down, particularly with regard to acquisitions of innovative start-ups, the VC freeze might have

begun to affect buyers too. With ever fewer start-ups able to raise money to get off the ground, larger companies

in need of new technologies seem already to be finding it harder to identify good takeover targets. This will cause

a feedback loop; if start-ups cannot easily find buyers there is even less incentive for VCs to put their money into

the sector.

13 Copyright © 2017 Evaluate Ltd. All rights reserved.

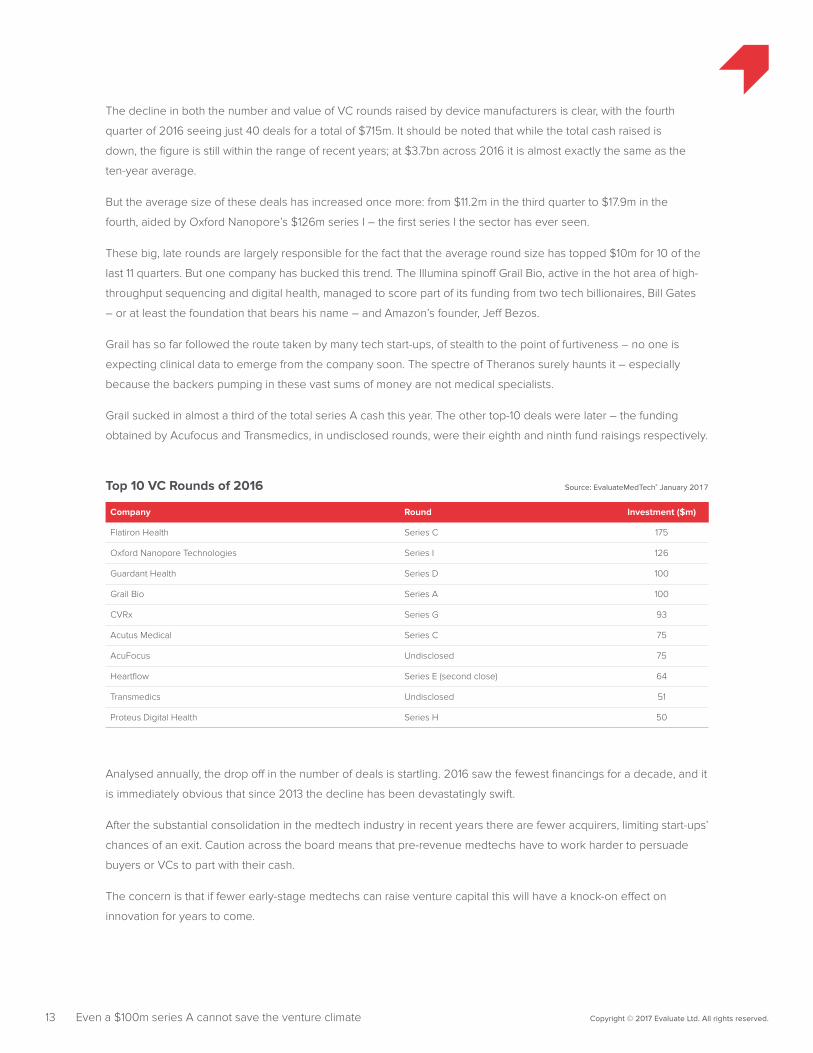

The decline in both the number and value of VC rounds raised by device manufacturers is clear, with the fourth

quarter of 2016 seeing just 40 deals for a total of $715m. It should be noted that while the total cash raised is

down, the figure is still within the range of recent years; at $3.7bn across 2016 it is almost exactly the same as the

ten-year average.

But the average size of these deals has increased once more: from $11.2m in the third quarter to $17.9m in the

fourth, aided by Oxford Nanopore’s $126m series I – the first series I the sector has ever seen.

These big, late rounds are largely responsible for the fact that the average round size has topped $10m for 10 of the

last 11 quarters. But one company has bucked this trend. The Illumina spinoff Grail Bio, active in the hot area of high-

throughput sequencing and digital health, managed to score part of its funding from two tech billionaires, Bill Gates

– or at least the foundation that bears his name – and Amazon’s founder, Jeff Bezos.

Grail has so far followed the route taken by many tech start-ups, of stealth to the point of furtiveness – no one is

expecting clinical data to emerge from the company soon. The spectre of Theranos surely haunts it – especially

because the backers pumping in these vast sums of money are not medical specialists.

Grail sucked in almost a third of the total series A cash this year. The other top-10 deals were later – the funding

obtained by Acufocus and Transmedics, in undisclosed rounds, were their eighth and ninth fund raisings respectively.

Company Round Investment ($m)

Flatiron Health Series C 175

Oxford Nanopore Technologies Series I 126

Guardant Health Series D 100

Grail Bio Series A 100

CVRx Series G 93

Acutus Medical Series C 75

AcuFocus Undisclosed 75

Heartflow Series E (second close) 64

Transmedics Undisclosed 51

Proteus Digital Health Series H 50

Top 10 VC Rounds of 2016 Source: EvaluateMedTech® January 2017

Even a $100m series A cannot save the venture climate

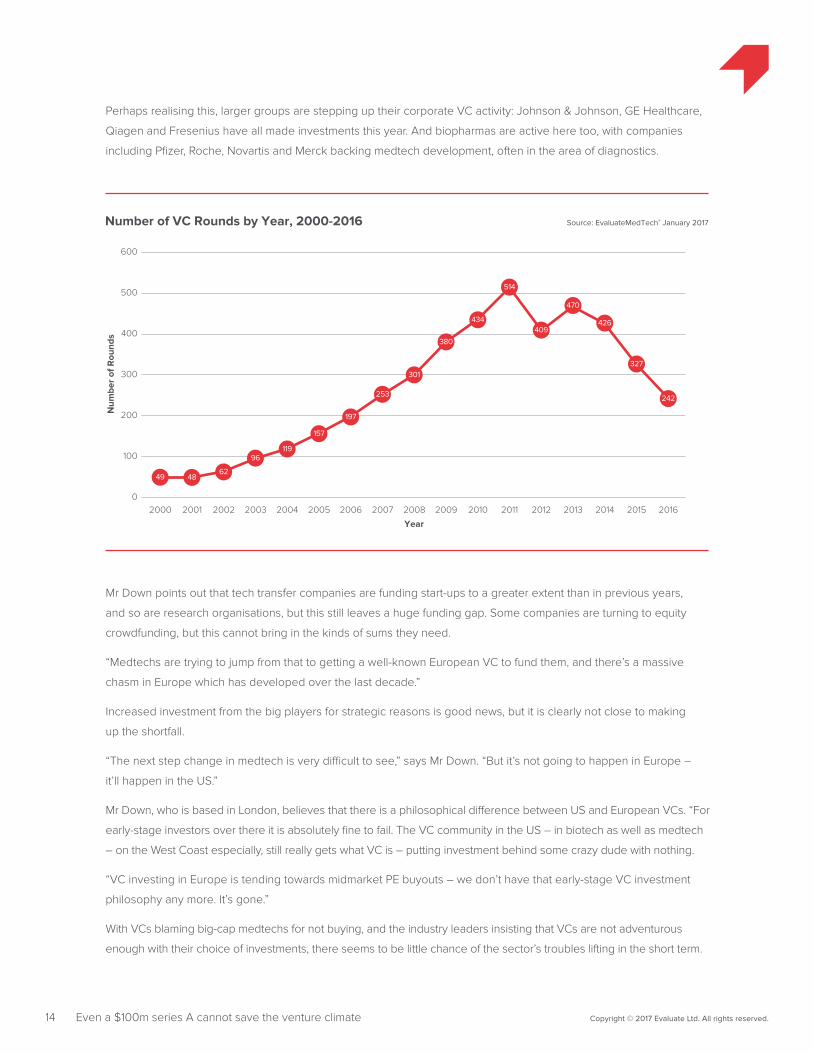

Analysed annually, the drop off in the number of deals is startling. 2016 saw the fewest financings for a decade, and it

is immediately obvious that since 2013 the decline has been devastatingly swift.

After the substantial consolidation in the medtech industry in recent years there are fewer acquirers, limiting start-ups’

chances of an exit. Caution across the board means that pre-revenue medtechs have to work harder to persuade

buyers or VCs to part with their cash.

The concern is that if fewer early-stage medtechs can raise venture capital this will have a knock-on effect on

innovation for years to come.

14 Copyright © 2017 Evaluate Ltd. All rights reserved.

Perhaps realising this, larger groups are stepping up their corporate VC activity: Johnson & Johnson, GE Healthcare,

Qiagen and Fresenius have all made investments this year. And biopharmas are active here too, with companies

including Pfizer, Roche, Novartis and Merck backing medtech development, often in the area of diagnostics.

100

200

300

400

500

600

0

Source: EvaluateMedTech® January 2017Number of VC Rounds by Year, 2000-2016

Num

ber

of R

ound

s

Year

2000

49

2001

48

2002

62

2003

96

2004

119

2005

157

2006

197

2007

253

2008

301

2010

434

2009

380

2011

514

2012

409

2013

470

2014

426

2015

327

2016

242

Even a $100m series A cannot save the venture climate

Mr Down points out that tech transfer companies are funding start-ups to a greater extent than in previous years,

and so are research organisations, but this still leaves a huge funding gap. Some companies are turning to equity

crowdfunding, but this cannot bring in the kinds of sums they need.

“Medtechs are trying to jump from that to getting a well-known European VC to fund them, and there’s a massive

chasm in Europe which has developed over the last decade.”

Increased investment from the big players for strategic reasons is good news, but it is clearly not close to making

up the shortfall.

“The next step change in medtech is very difficult to see,” says Mr Down. “But it’s not going to happen in Europe –

it’ll happen in the US.”

Mr Down, who is based in London, believes that there is a philosophical difference between US and European VCs. “For

early-stage investors over there it is absolutely fine to fail. The VC community in the US – in biotech as well as medtech

– on the West Coast especially, still really gets what VC is – putting investment behind some crazy dude with nothing.

“VC investing in Europe is tending towards midmarket PE buyouts – we don’t have that early-stage VC investment

philosophy any more. It’s gone.”

With VCs blaming big-cap medtechs for not buying, and the industry leaders insisting that VCs are not adventurous

enough with their choice of investments, there seems to be little chance of the sector’s troubles lifting in the short term.

US approvals dip

Fewer approvals that are slower to arrive – not what the medical device industry wanted to see

from the US FDA. Just 38 first-time premarket approvals were granted to innovative devices last

year, down 25% from the 51 awarded the year before. And the agency has taken slightly longer,

on average, to grant those approvals – 18.1 months compared with 17.3 months in 2015.

The coming year could be very different. The 21st Century Cures Act came into force at the end of last year,

containing provisions that would relax approval criteria for medical devices. And with the current US administration

dropping hints that the requirements for device approval could be loosened further still, the years to come might see

higher numbers and faster decisions.

15 US approvals dip Copyright © 2017 Evaluate Ltd. All rights reserved.

Source: EvaluateMedTech® January 2017Number of US Approvals Granted, 2005-2016

Num

ber

of A

ppro

vals

10

20

30

40

50

60

0

Year

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 20162015

5 47

3 4 3

10 10

18

28

24

18

34

44

3230

18

22

4341

23

33

38

Number of De Novo Clearances

51

Number of PMAs and HDEs

Only around 1% of the medical devices approved in the US are first-time PMAs. A larger proportion are

supplementary PMAs – tweaks to approved high-risk devices. But the lion’s share are granted 510(k) clearance,

whereby the developer of a low-risk device offers evidence that it is substantially equivalent to a product already on

the market.

One of the factors contributing to the smaller number of approvals in 2016 might have been the ongoing, and

worsening, venture crisis. There are hints that larger medtech groups are finally discovering that the pool of start-ups

through whose acquisition they can obtain innovative technologies has appreciably shrunk.

16 US approvals dip Copyright © 2017 Evaluate Ltd. All rights reserved.

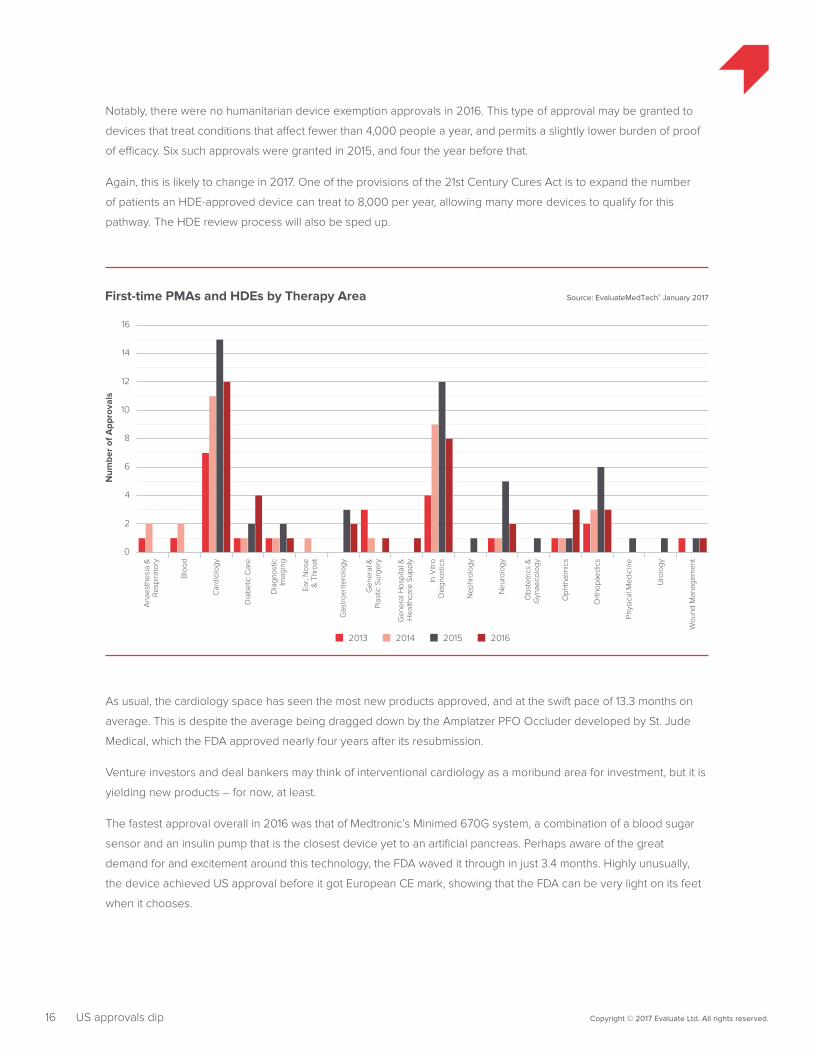

Source: EvaluateMedTech® January 2017First-time PMAs and HDEs by Therapy Area

Num

ber

of A

ppro

vals

2

4

6

12

10

8

16

14

2013 201620152014

Ana

esth

esia

&Re

spira

tory

Blo

od

Car

diol

ogy

Dia

betic

Car

e

Dia

gnos

ticIm

agin

g

Ear,

Nos

e&

Thr

oat

Gas

troen

tero

logy

Gen

eral

&Pl

astic

Sur

gery

Gen

eral

Hos

pita

l &H

ealth

care

Sup

ply

In V

itro

Dia

gnos

tics

Nep

hrol

ogy

Neu

rolo

gy

Obs

tetri

cs &

Gyn

aeco

logy

Oph

thal

mic

s

Orth

opae

dics

Phys

ical

Med

icin

e

Uro

logy

Wou

nd M

anag

emen

t

0

Notably, there were no humanitarian device exemption approvals in 2016. This type of approval may be granted to

devices that treat conditions that affect fewer than 4,000 people a year, and permits a slightly lower burden of proof

of efficacy. Six such approvals were granted in 2015, and four the year before that.

Again, this is likely to change in 2017. One of the provisions of the 21st Century Cures Act is to expand the number

of patients an HDE-approved device can treat to 8,000 per year, allowing many more devices to qualify for this

pathway. The HDE review process will also be sped up.

As usual, the cardiology space has seen the most new products approved, and at the swift pace of 13.3 months on

average. This is despite the average being dragged down by the Amplatzer PFO Occluder developed by St. Jude

Medical, which the FDA approved nearly four years after its resubmission.

Venture investors and deal bankers may think of interventional cardiology as a moribund area for investment, but it is

yielding new products – for now, at least.

The fastest approval overall in 2016 was that of Medtronic’s Minimed 670G system, a combination of a blood sugar

sensor and an insulin pump that is the closest device yet to an artificial pancreas. Perhaps aware of the great

demand for and excitement around this technology, the FDA waved it through in just 3.4 months. Highly unusually,

the device achieved US approval before it got European CE mark, showing that the FDA can be very light on its feet

when it chooses.

17 US approvals dip Copyright © 2017 Evaluate Ltd. All rights reserved.

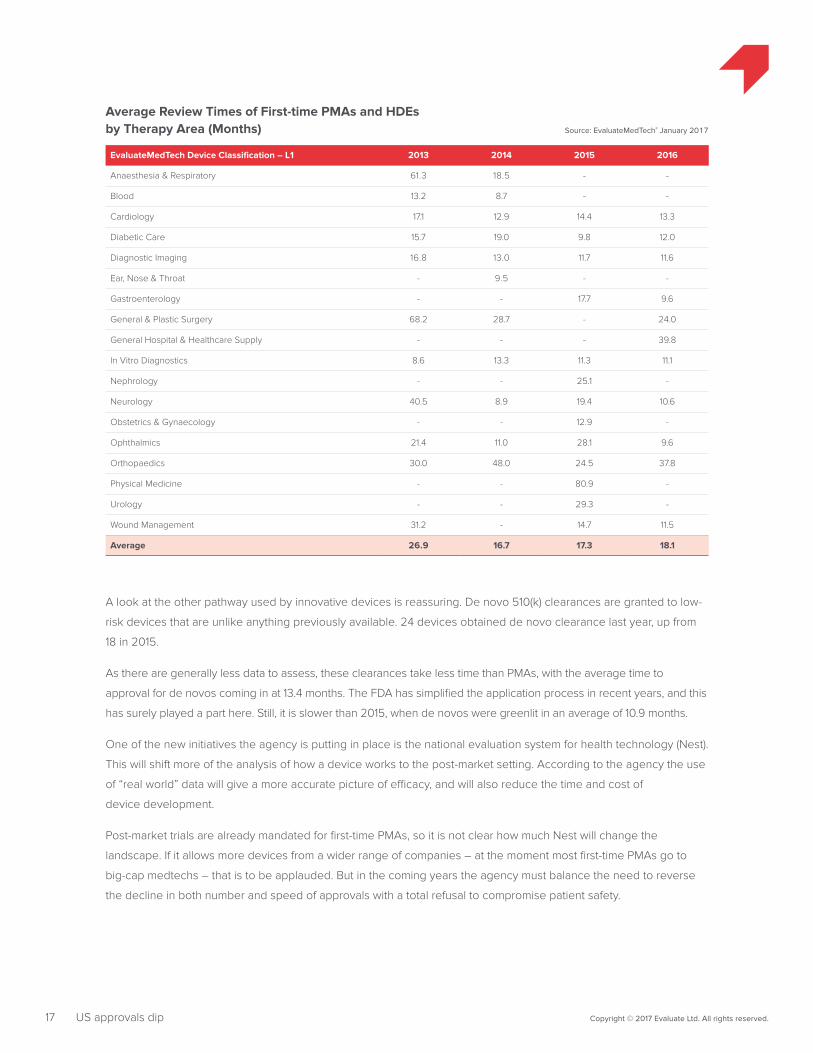

EvaluateMedTech Device Classification – L1 2013 2014 2015 2016

Anaesthesia & Respiratory 61.3 18.5 - -

Blood 13.2 8.7 - -

Cardiology 17.1 12.9 14.4 13.3

Diabetic Care 15.7 19.0 9.8 12.0

Diagnostic Imaging 16.8 13.0 11.7 11.6

Ear, Nose & Throat - 9.5 - -

Gastroenterology - - 17.7 9.6

General & Plastic Surgery 68.2 28.7 - 24.0

General Hospital & Healthcare Supply - - - 39.8

In Vitro Diagnostics 8.6 13.3 11.3 11.1

Nephrology - - 25.1 -

Neurology 40.5 8.9 19.4 10.6

Obstetrics & Gynaecology - - 12.9 -

Ophthalmics 21.4 11.0 28.1 9.6

Orthopaedics 30.0 48.0 24.5 37.8

Physical Medicine - - 80.9 -

Urology - - 29.3 -

Wound Management 31.2 - 14.7 11.5

Average 26.9 16.7 17.3 18.1

Average Review Times of First-time PMAs and HDEsby Therapy Area (Months) Source: EvaluateMedTech® January 2017

A look at the other pathway used by innovative devices is reassuring. De novo 510(k) clearances are granted to low-

risk devices that are unlike anything previously available. 24 devices obtained de novo clearance last year, up from

18 in 2015.

As there are generally less data to assess, these clearances take less time than PMAs, with the average time to

approval for de novos coming in at 13.4 months. The FDA has simplified the application process in recent years, and this

has surely played a part here. Still, it is slower than 2015, when de novos were greenlit in an average of 10.9 months.

One of the new initiatives the agency is putting in place is the national evaluation system for health technology (Nest).

This will shift more of the analysis of how a device works to the post-market setting. According to the agency the use

of “real world” data will give a more accurate picture of efficacy, and will also reduce the time and cost of

device development.

Post-market trials are already mandated for first-time PMAs, so it is not clear how much Nest will change the

landscape. If it allows more devices from a wider range of companies – at the moment most first-time PMAs go to

big-cap medtechs – that is to be applauded. But in the coming years the agency must balance the need to reverse

the decline in both number and speed of approvals with a total refusal to compromise patient safety.

18 2017 Copyright © 2017 Evaluate Ltd. All rights reserved.

2017

Last year might look like a disappointment compared with the tumult of 2015. But the underlying

trends are not necessarily disastrous, with signs in many areas of determination to keep the

sector rolling.

M&A deals are certain to pick back up, with fewer scale-building megamergers than 2015 and more mid-size deals.

It would be a healthy sign if an uptick in the smallest acquisitions also came about in 2017. Some sectors will always

remain quiet, but some industry watchers believe that there are pockets where interest is actually growing, with

investors seeing the medtech industry as an interesting way of putting money to work.

These areas might include orthopaedics or ophthalmology from a merger perspective, or on the venture investment

side, digital health or cancer diagnostics.

If some big medtech M&A deals are announced this year, they ought to lead to additional deals such as divestments,

which could change the industry in unexpected ways.

The intriguing signs of a reawakening of the IPO markets at the tail end of 2016 are not conclusive. But such an event

would certainly be welcome, not least because it might come as a consequence of, or even contribute to, a more

positive outlook on the public markets.

The effects of regulatory change in the US are difficult to predict, but there is certainly political will to speed the

passage of innovative technologies to patients. The impact of the 21st Century Cures Act and the Nest programme

might not be fully felt for a couple of years, but if the number of devices approved in 2017 does not increase from last

year’s total it will not be for want of trying.

It will be for want of cash. Start-ups can often drum up a million or so of seed funding, but to hook venture capital

they must show a concrete achievement with their device. In the absence of the expensive but useful phased trials

as are seen in biopharma the only thing a medtech can show to VCs is approval. How they are expected to get

from concept to commercialisation is a question to which no one has yet found the answer. Maybe 2017 will see a

relaxation of VCs’ attitudes to risk. But the industry will not be holding its breath.

Report author | Elizabeth Cairns

Additional complimentary copies of this report can be downloaded at: www.evaluategroup.com/Medtech2016Review

Evaluate Headquarters Evaluate Ltd. 1 1 -29 Fashion Street London E1 6PX United Kingdom T +44 (0)20 7377 0800 F +44 (0)20 7539 1801

Evaluate North America EvaluatePharma USA Inc. 15 Broad Street, Suite 401 Boston, MA 02109, USA T +1 617 573 9450 F +1 617 573 9542

Evaluate Japan Evaluate Japan KK Akasaka Garden City 4F 4-15-1 Akasaka, Minato-ku Tokyo 107-0052, Japan T +81 (0)80 1164 4754

www.evaluate.com

Evaluate is the trusted provider of commercial intelligence including product sales and consensus forecasts to 2022 for commercial teams and their advisors within the global life science industry. We help our clients make high value decisions through superior quality, timely, must-have data and insights, combined with personalised, expert client support.

EvaluatePharma® delivers exclusive consensus sales forecasts and trusted commercial insight into biotech and pharmaceutical performance.

@EvaluatePharma

EvaluateMedTech® sets a new standard in commercial analysis and consensus forecasts of the global medical device and diagnostic industry.

@EvaluateMedTech

EvaluateClinical Trials® delivers unique clinical trial intelligence expertly curated to efficiently analyse the global clinical trial landscape.

@EPClinicalTrial

EP Vantage an award winning editorial team, provides daily commentary and analysis with fresh perspectives and insight into current and future industry trends.

@EPVantage

Evaluate Custom Services provides customised solutions to help you access, analyse and manage the information you need to support effective decision-making.

The Evaluate services enable the life science community to make sound business decisions about value and opportunity.