Embed Size (px)

Citation preview

Oscar Salgado Ing. Agr. PUCV-M.B.A

Mercados y países productores de H. Sur

Statistics compiled by A. Hoffmann

Key world table grape countries

producers and exporters

from the

South

Hemisphere

Afrifresh Holdings South AfricaGrowers/packer and exporters

www.afrifresh.co.za

www.origindirectasia.com www.originfruitdirect.nl

Fruit importers in to the Asia and European Continent markets

"El sabio consigue mas ventajas por sus enemigos que el necio por sus

amigos."

Benjamín Franklin

Objetivos

• Tendencias de mercado y lo que se nos viene

• Países productores del Hemisferio Sur, competencias, complementariedad, amenazas y tendencias.

• Entregar información de los otros países Productores de uva de mesa

Todos tenemos esos días en que nos quedamos un poco atascados……..y esperamos que alguien nos ayude………

Con respecto a los que vienen a ayudar o a asesorar ……………!!

…..solo recordar, que no todos los que aparecen, están para ayudarnos!!!!!!.

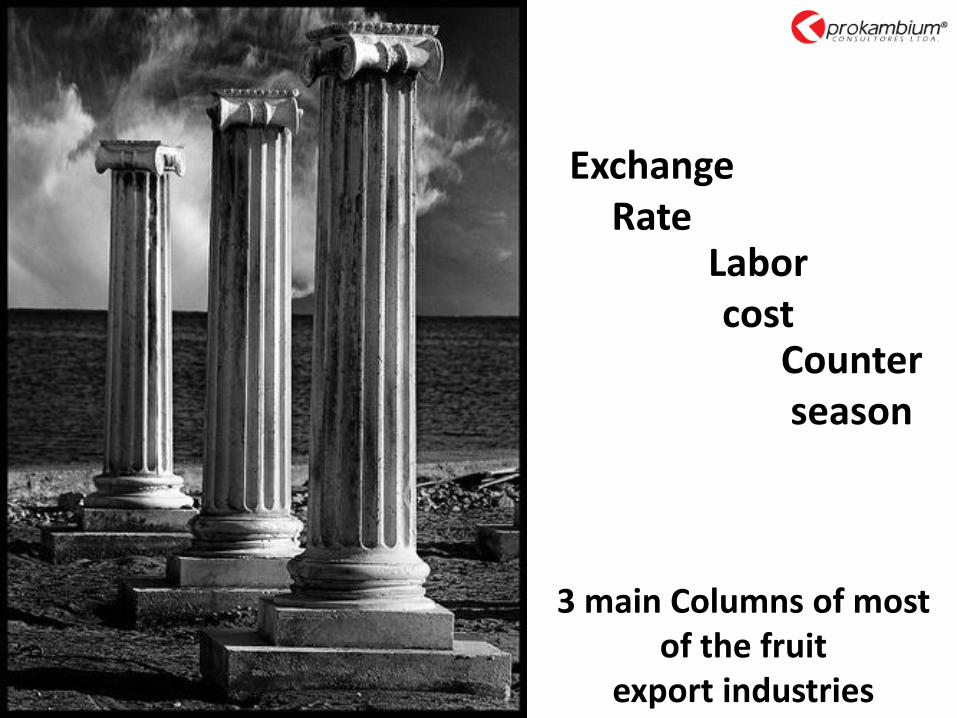

Exchange Rate

Labor cost

Counter season

3 main Columns of most of the fruit

export industries

Trataremos de ver la realidad ………………….

Como entramos en la cuarta gama………….??

Source: Portugal O salgado 2008

130 Grams pack ready to eat grape

SnackValue 1 Pound

Food Court M&S Stansted Airport

August 2011

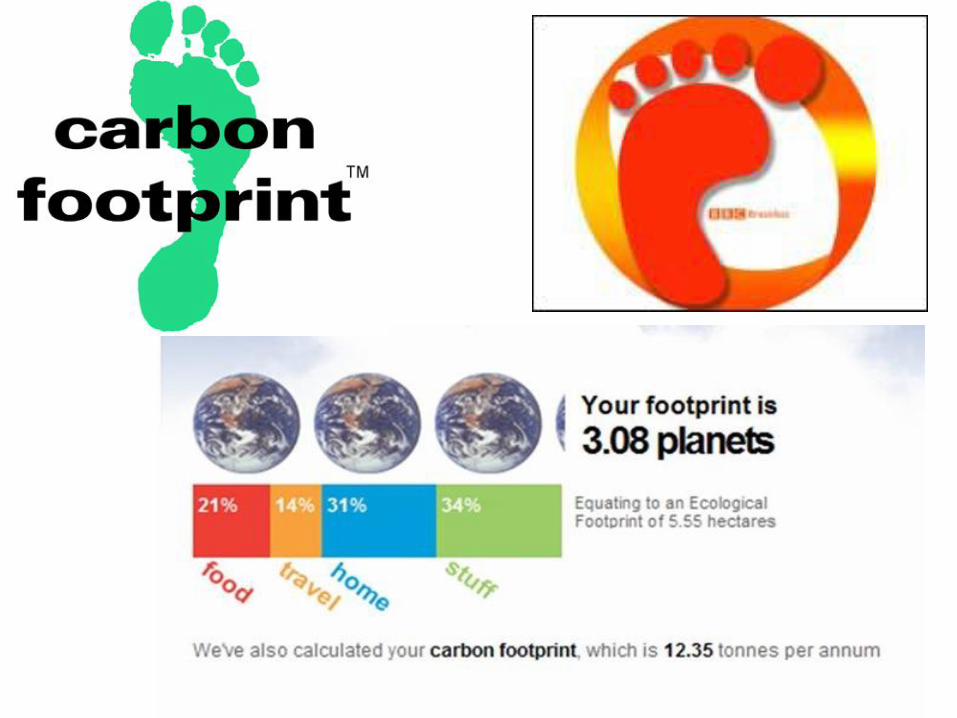

Calentamiento global y las consecuencias en la

deforestación

Brasil

MAFA: Large Egyptian Grower and Exporters s

http://www.magrabi-agriculture.com/

Remember daddy……

“Objects in the Mirror are closer

then they appear”

Recuerda papito…….”los objetos en el espejo están más cerca de lo que aparecen”

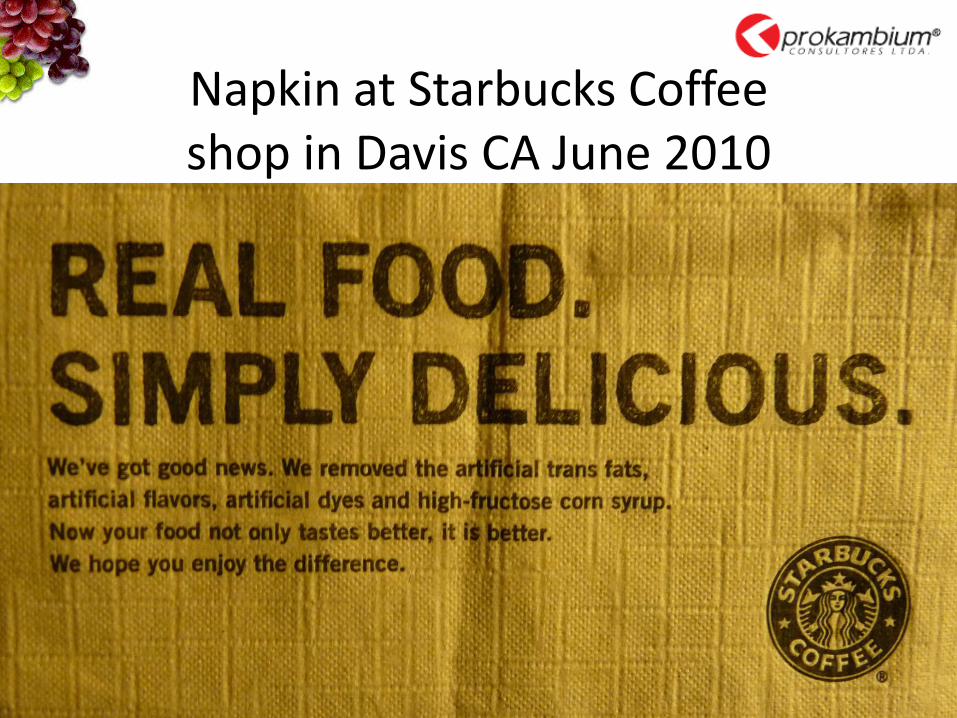

Napkin at Starbucks Coffee shop in Davis CA June 2010

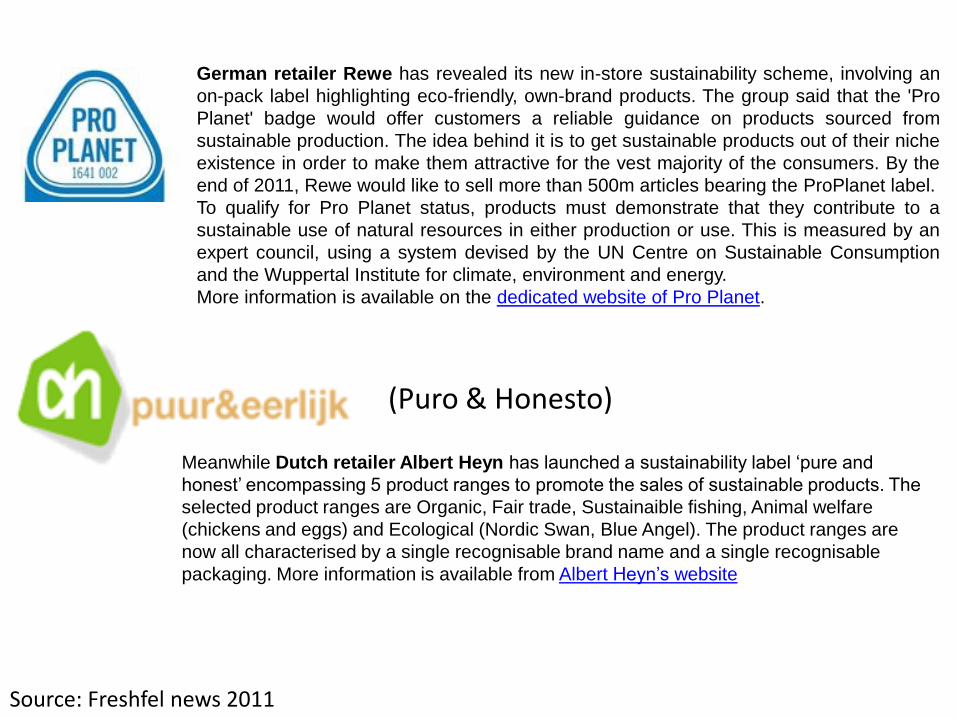

German retailer Rewe has revealed its new in-store sustainability scheme, involving an

on-pack label highlighting eco-friendly, own-brand products. The group said that the 'Pro

Planet' badge would offer customers a reliable guidance on products sourced from

sustainable production. The idea behind it is to get sustainable products out of their niche

existence in order to make them attractive for the vest majority of the consumers. By the

end of 2011, Rewe would like to sell more than 500m articles bearing the ProPlanet label.

To qualify for Pro Planet status, products must demonstrate that they contribute to a

sustainable use of natural resources in either production or use. This is measured by an

expert council, using a system devised by the UN Centre on Sustainable Consumption

and the Wuppertal Institute for climate, environment and energy.

More information is available on the dedicated website of Pro Planet.

Meanwhile Dutch retailer Albert Heyn has launched a sustainability label ‘pure and

honest’ encompassing 5 product ranges to promote the sales of sustainable products. The

selected product ranges are Organic, Fair trade, Sustainaible fishing, Animal welfare

(chickens and eggs) and Ecological (Nordic Swan, Blue Angel). The product ranges are

now all characterised by a single recognisable brand name and a single recognisable

packaging. More information is available from Albert Heyn’s website

Source: Freshfel news 2011

(Puro & Honesto)

September the 11’s

Gulf of Mexico oil spill

Millstones

Outbreak of social turmoil in the Arab worlds

Calidad y Condición no

son mas herramientas o argumentos de Marketing

“Todos pueden hacer buena uva” Entonces:

Estamos con problemas ?

Chile:Our business cluster

have Over shattering…………?

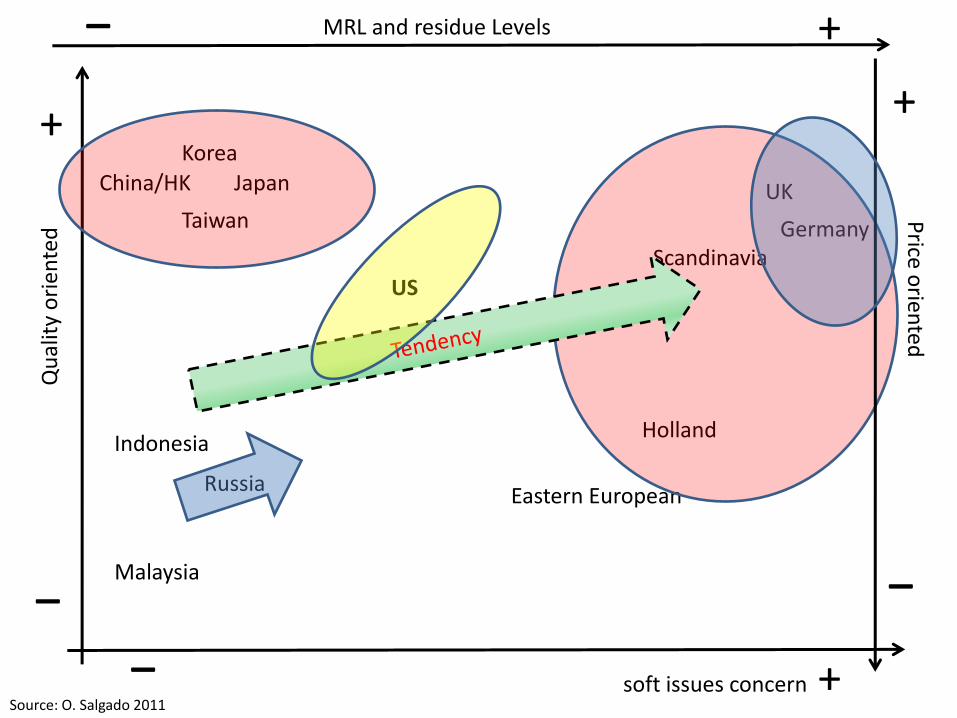

+_

Source: O. Salgado 2011soft issues concern

Qu

alit

y o

rien

ted

Japan UK

Germany

Russia

China/HK

Malaysia

Indonesia

US

Korea

Taiwan

Holland

Eastern European

Scandinavia

Price o

riented

+ +__

_ +MRL and residue Levels

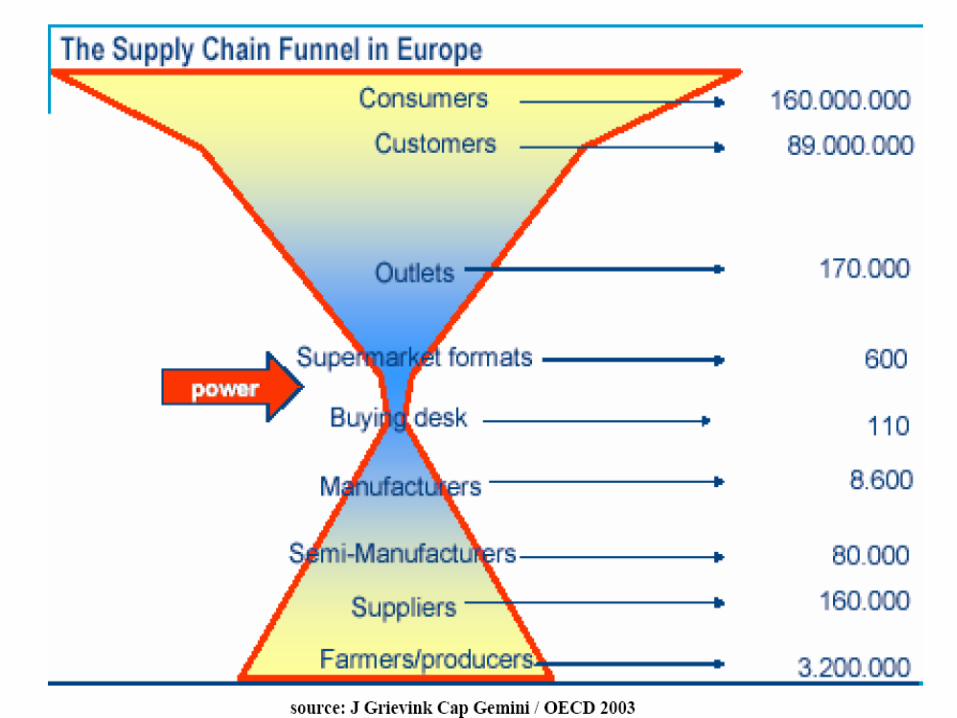

70% del valor de la Fruta se va en logística

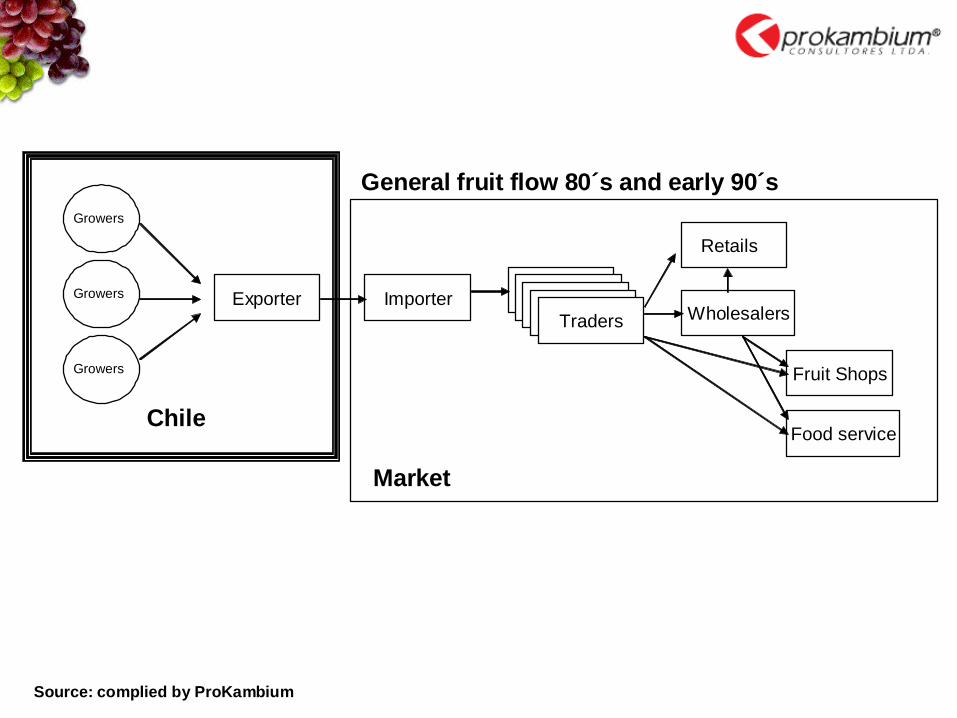

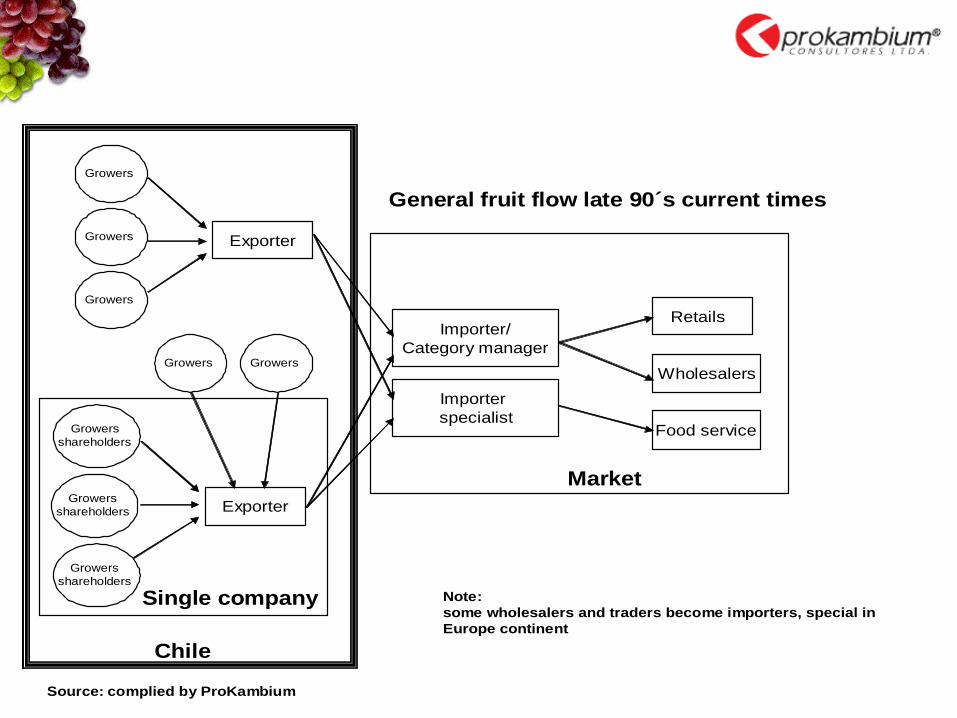

Growers

Growers

Growers

Exporter Importer

Traders

Retails

Wholesalers

Fruit Shops

Food service

General fruit flow 80´s and early 90´s

Chile

Market

Source: complied by ProKambium

Growers

Growers

Growers

Exporter

Importer/

Category manager

Retails

Wholesalers

Food service

General fruit flow late 90´s current times

Market

Source: complied by ProKambium

Exporter

Single company

Growers Growers

Growers

shareholders

Growers

shareholders

Growers

shareholders

Importer

specialist

Chile

Note:

some wholesalers and traders become importers, special in

Europe continent

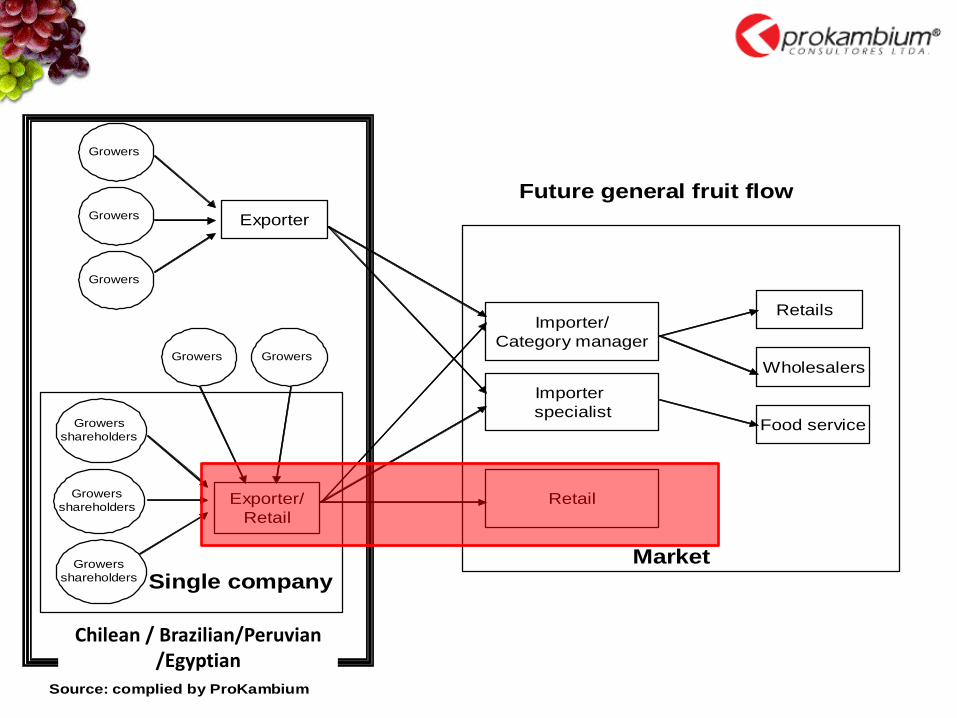

Growers

Growers

Growers

Exporter

Importer/

Category manager

Retails

Wholesalers

Food service

Future general fruit flow

Market

Source: complied by ProKambium

Exporter/

Retail

Single company

Growers Growers

Growers

shareholders

Growers

shareholders

Growers

shareholders

Importer

specialist

Chile

Retail

Chilean / Brazilian/Peruvian /Egyptian

De lo único que estamos seguros es del cambio………….

De las amenazas

Cuando todo va mal …………..

…….recuerden puede ser aun peor!!!!!

New Issues

• From Flavours move to ……………. Smell / odours /aromas

• From Recycle packing materials…………………….Compostable

Who hold the power so far?

sell

2006

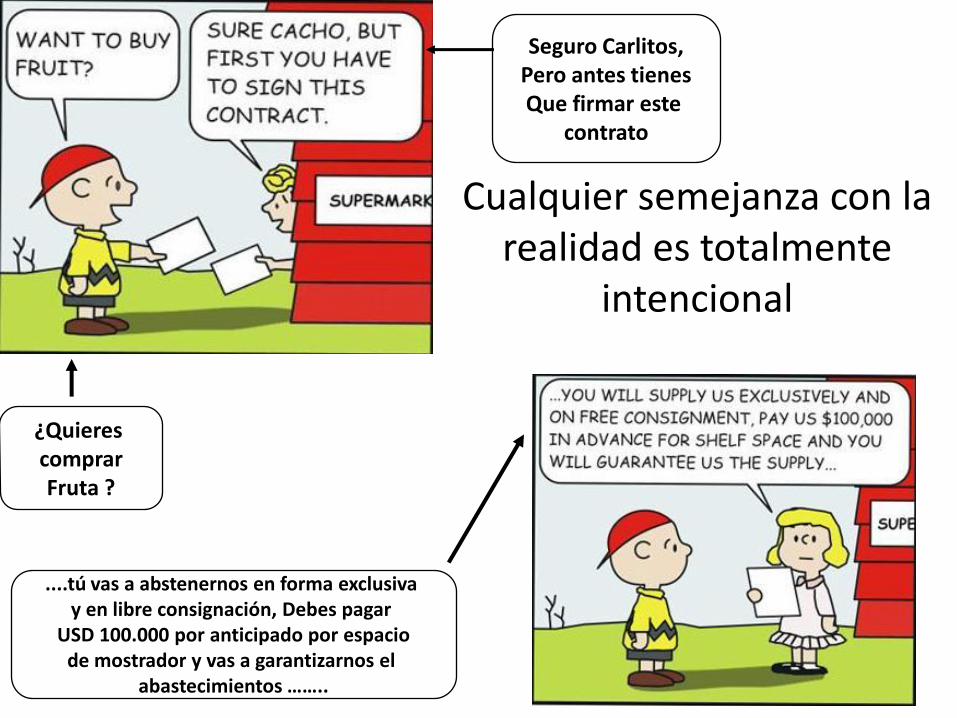

Cualquier semejanza con la realidad es totalmente

intencional

¿Quieres comprarFruta ?

Seguro Carlitos,Pero antes tienesQue firmar este

contrato

....tú vas a abstenernos en forma exclusiva y en libre consignación, Debes pagar

USD 100.000 por anticipado por espaciode mostrador y vas a garantizarnos el

abastecimientos ……..

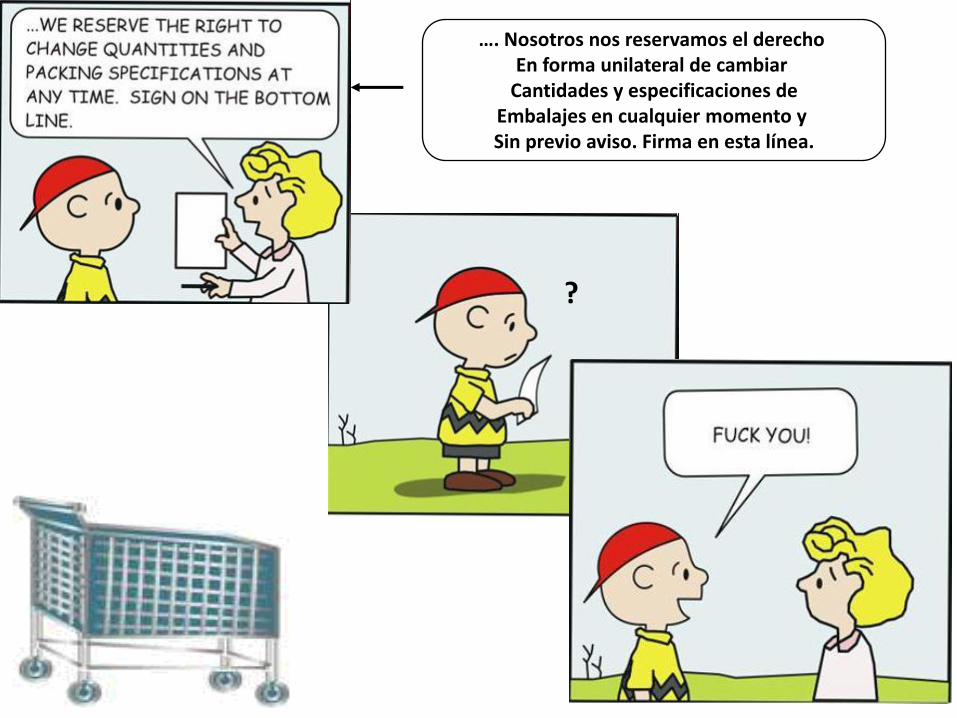

….tú vas a costear nuestros avisos y promociones cuando nosotros lo

determinemos …….

…. tú cumplirás con Global-Gap® yCualquiera otra condición y

Regulación y tu adherirás en formaexacta a cada una de

nuestras especificaciones …

…. tú asumes total responsabilidad, civil y penal por todos los productos frescos …..

…. Nosotros nos reservamos el derecho En forma unilateral de cambiar

Cantidades y especificaciones deEmbalajes en cualquier momento y Sin previo aviso. Firma en esta línea.

?

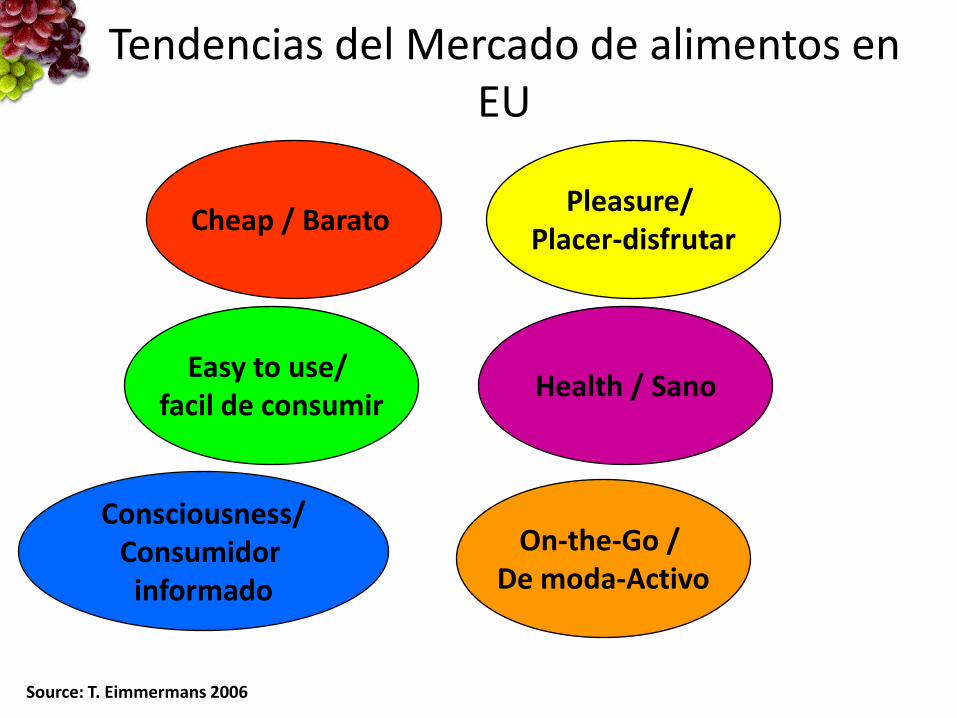

Cheap / Barato

Easy to use/ facil de consumir

Consciousness/Consumidor informado

Pleasure/ Placer-disfrutar

Health / Sano

On-the-Go / De moda-Activo

Tendencias del Mercado de alimentos en EU

Source: T. Eimmermans 2006

Palabras claves

¿Cual es nuestro negocio ?

Los postres, somos los últimos a en ser

invitados a la mesa y nadie se muere de

hambre si no llegamos

¿En que negocio estamos?• En el demográfico………………………

Food related risk perception in the EU

Euro-barometer on food related risk perception

LAST UPDATE: NOVEMBER 2010

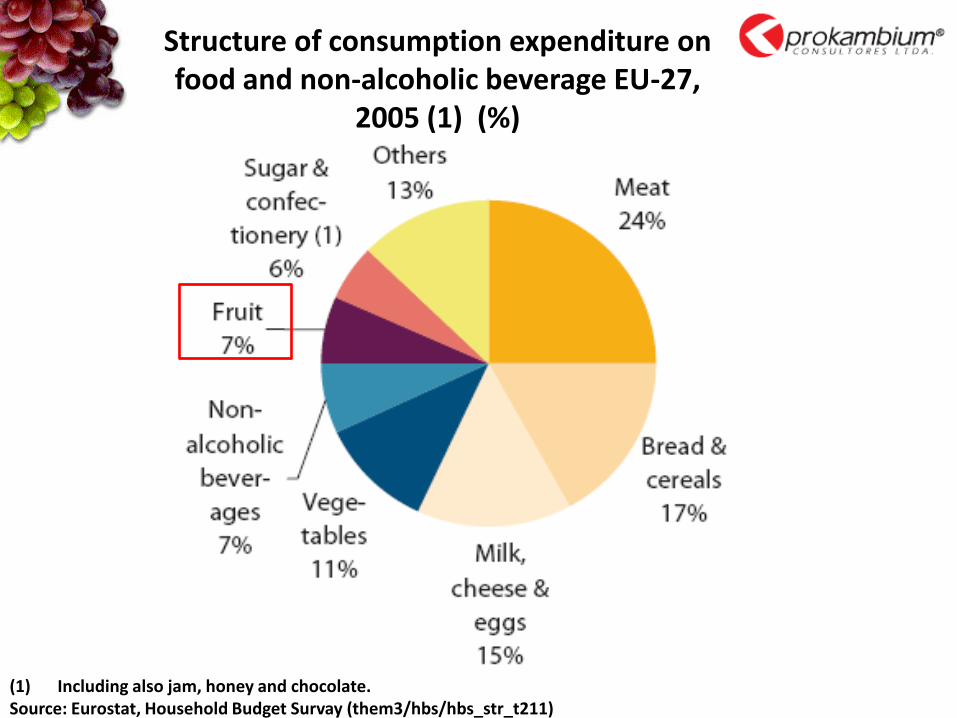

Structure of consumption expenditure on food and non-alcoholic beverage EU-27,

2005 (1) (%)

(1) Including also jam, honey and chocolate.Source: Eurostat, Household Budget Survay (them3/hbs/hbs_str_t211)

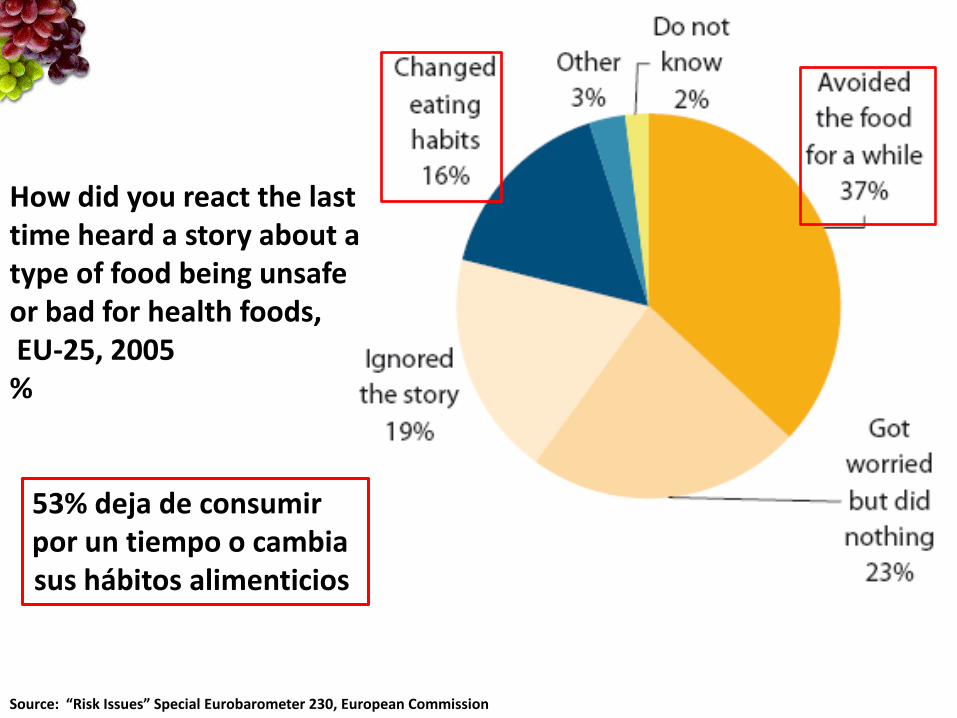

How did you react the last time heard a story about a type of food being unsafe or bad for health foods,EU-25, 2005%

53% deja de consumir por un tiempo o cambia sus hábitos alimenticios

Source: “Risk Issues” Special Eurobarometer 230, European Commission

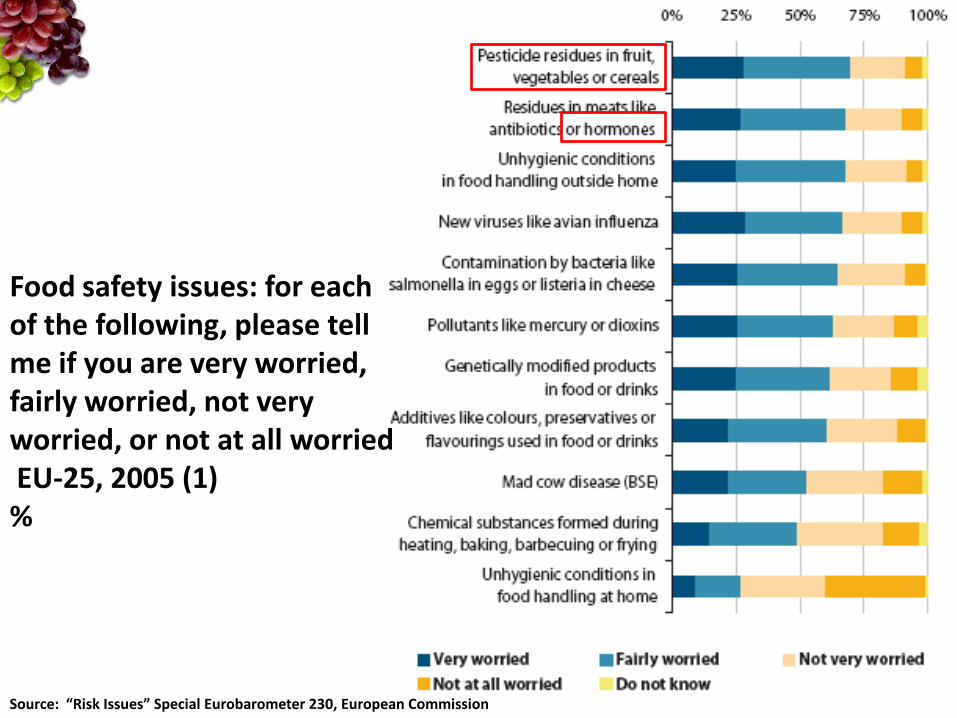

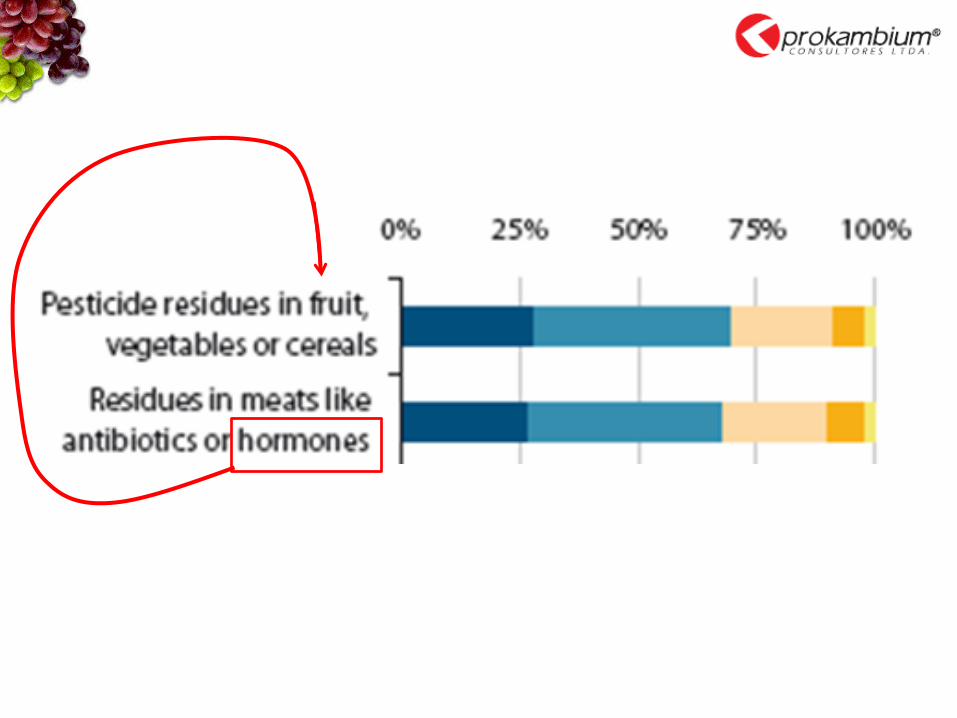

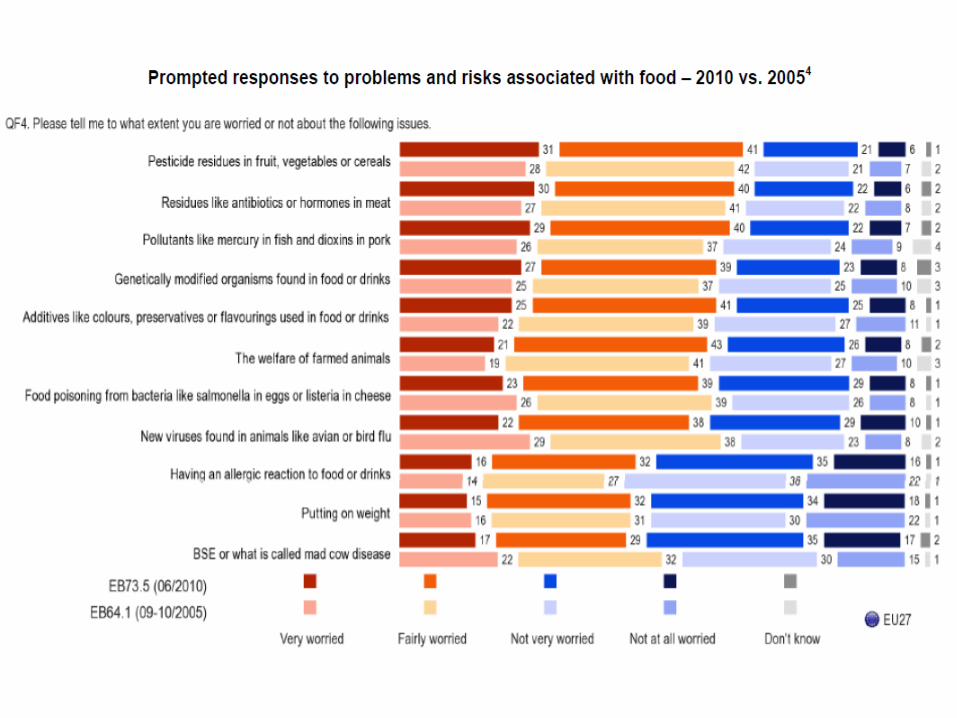

Food safety issues: for each of the following, please tell me if you are very worried, fairly worried, not very worried, or not at all worriedEU-25, 2005 (1)%

Source: “Risk Issues” Special Eurobarometer 230, European Commission

Hormonas/ Fitohormonas/Hormonas vegetales: NO!!!

Son Reguladores de crecimiento vegetal……………

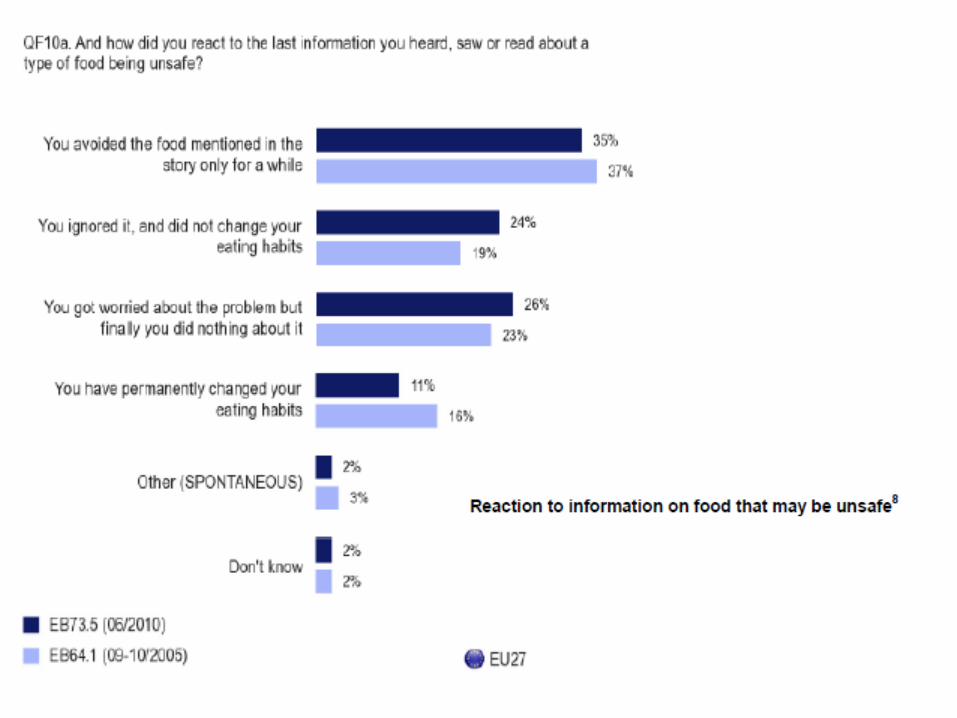

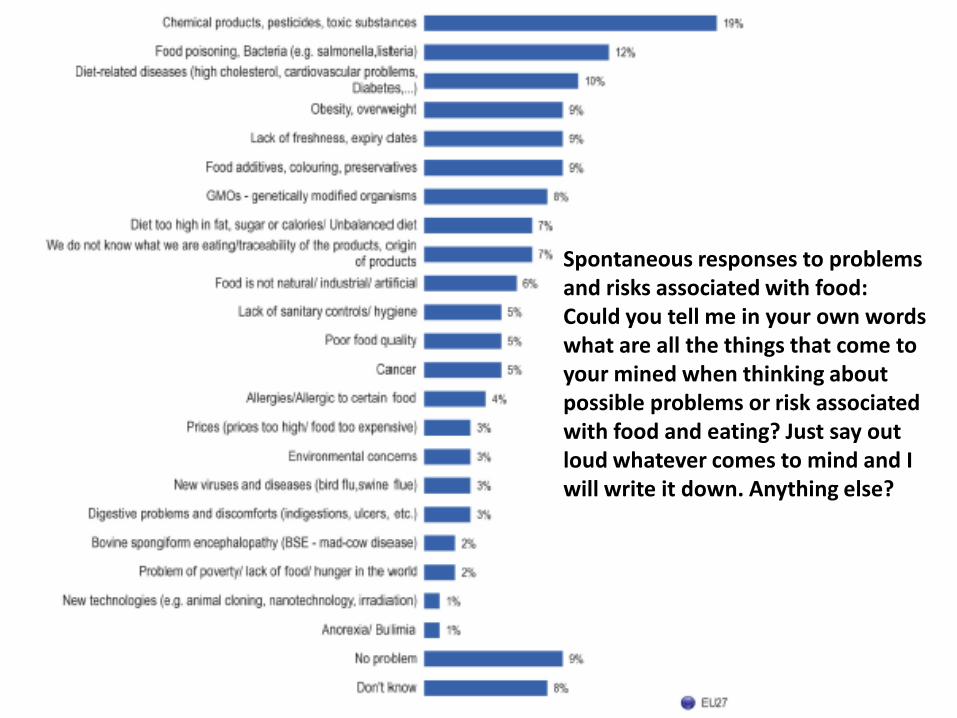

Spontaneous responses to problems and risks associated with food:Could you tell me in your own words what are all the things that come to your mined when thinking about possible problems or risk associated with food and eating? Just say out loud whatever comes to mind and I will write it down. Anything else?

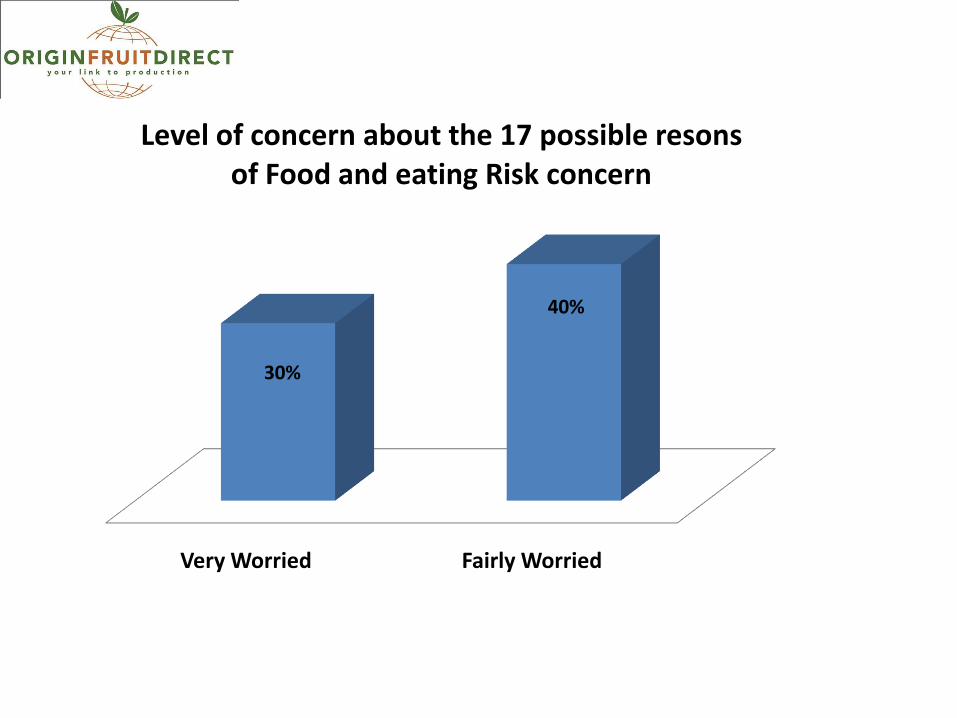

Very Worried Fairly Worried

30%

40%

Level of concern about the 17 possible resons of Food and eating Risk concern

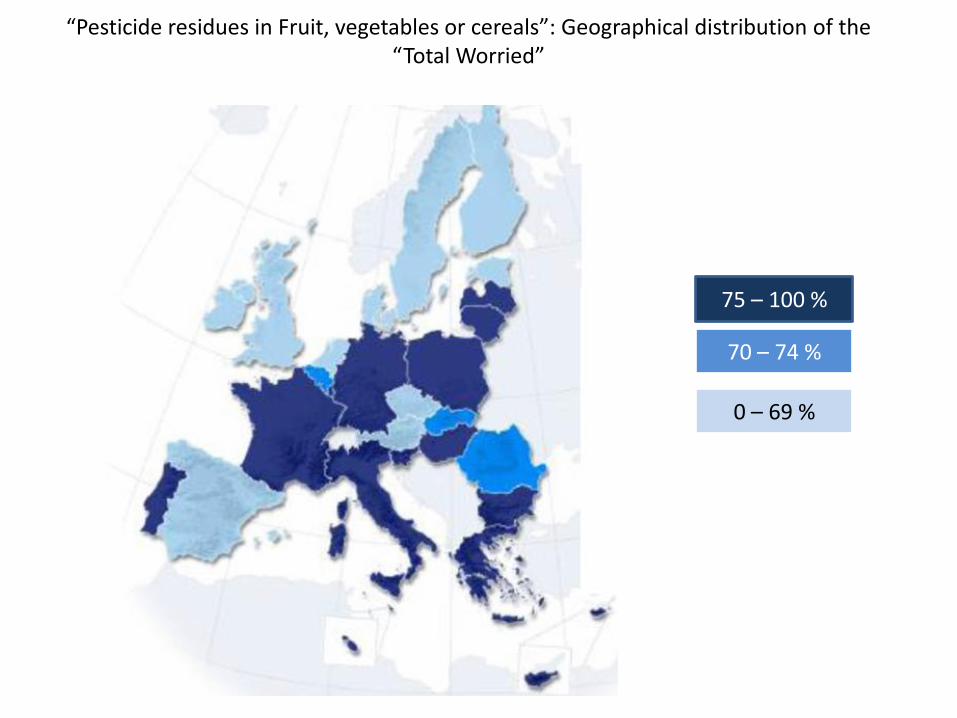

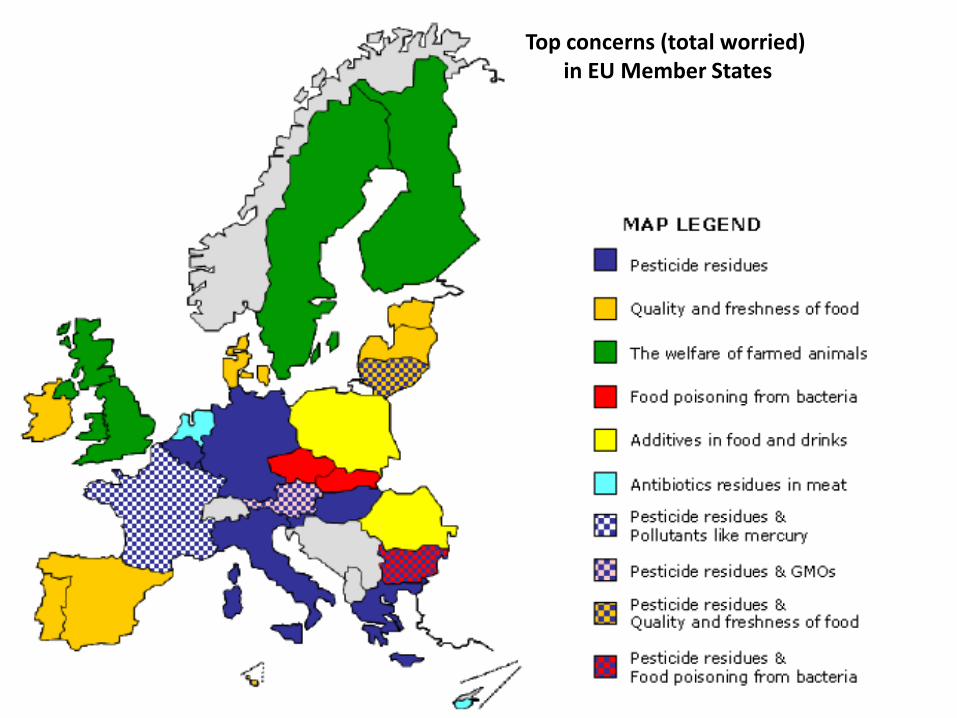

“Pesticide residues in Fruit, vegetables or cereals”: Geographical distribution of the“Total Worried”

75 – 100 %

70 – 74 %

0 – 69 %

Top concerns (total worried) in EU Member States

Above the MRL

Within the MRL

No residue levels

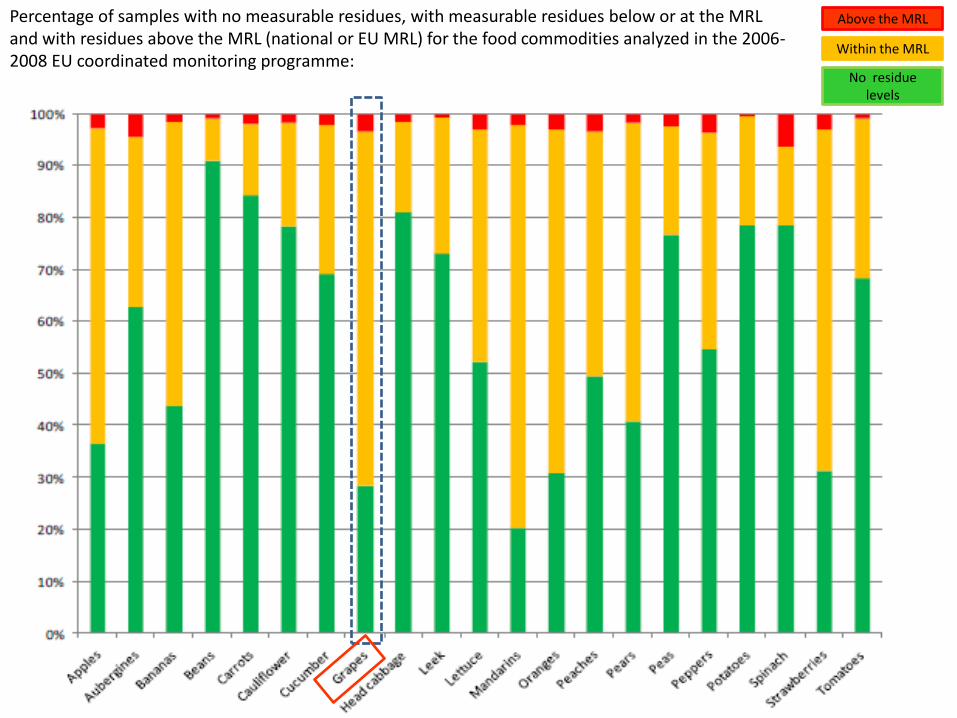

Percentage of samples with no measurable residues, with measurable residues below or at the MRL and with residues above the MRL (national or EU MRL) for the food commodities analyzed in the 2006-2008 EU coordinated monitoring programme:

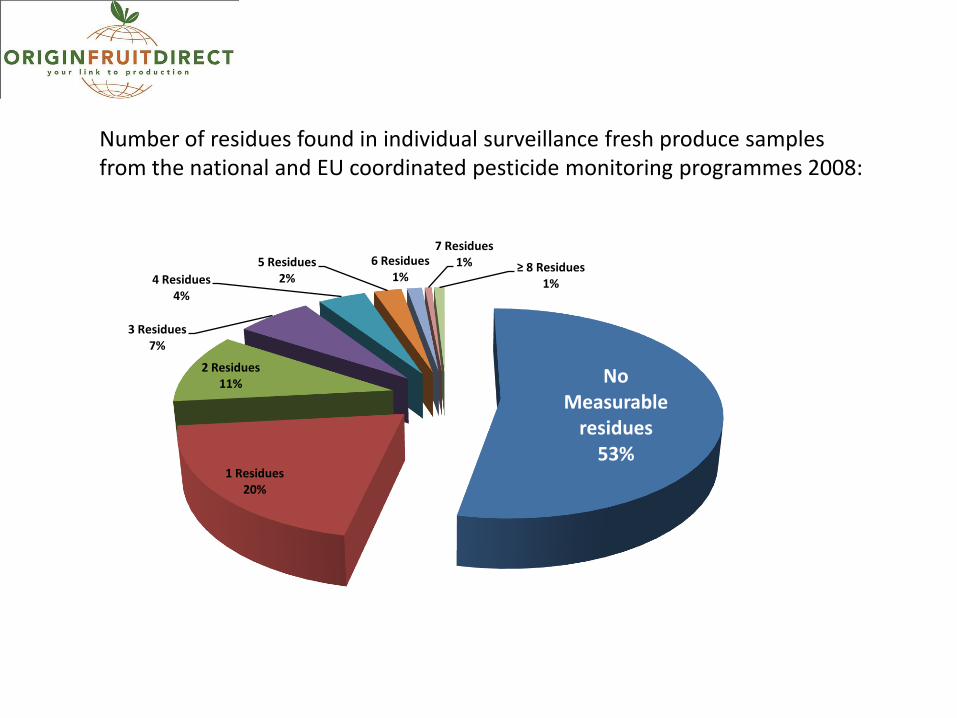

No Measurable

residues 53%

1 Residues 20%

2 Residues 11%

3 Residues7%

4 Residues 4%

5 Residues 2%

6 Residues1%

7 Residues 1% ≥ 8 Residues

1%

Number of residues found in individual surveillance fresh produce samples from the national and EU coordinated pesticide monitoring programmes 2008:

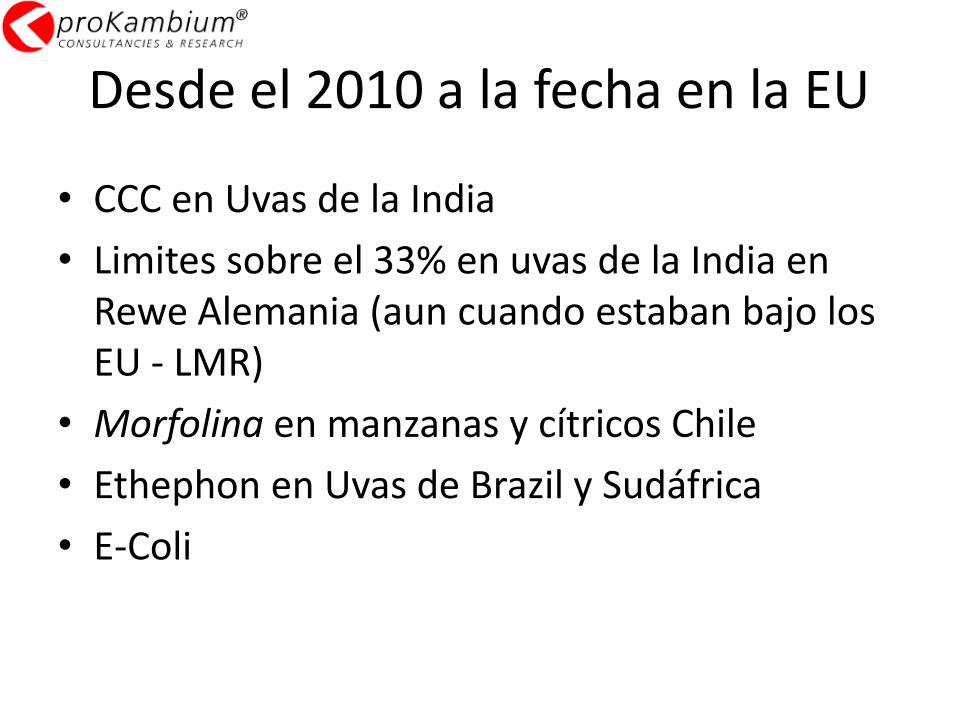

Desde el 2010 a la fecha en la EU

• CCC en Uvas de la India

• Limites sobre el 33% en uvas de la India en Rewe Alemania (aun cuando estaban bajo los EU - LMR)

• Morfolina en manzanas y cítricos Chile

• Ethephon en Uvas de Brazil y Sudáfrica

• E-Coli

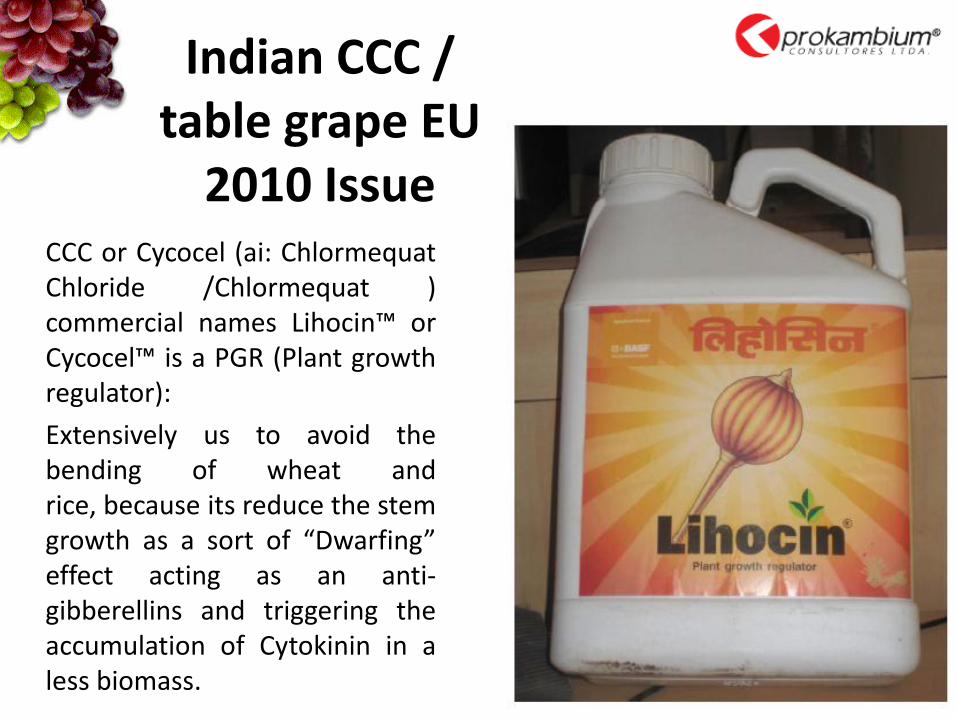

Indian CCC / table grape EU

2010 IssueCCC or Cycocel (ai: ChlormequatChloride /Chlormequat )commercial names Lihocin™ orCycocel™ is a PGR (Plant growthregulator):

Extensively us to avoid thebending of wheat andrice, because its reduce the stemgrowth as a sort of “Dwarfing”effect acting as an anti-gibberellins and triggering theaccumulation of Cytokinin in aless biomass.

Source: D. Crook 2010

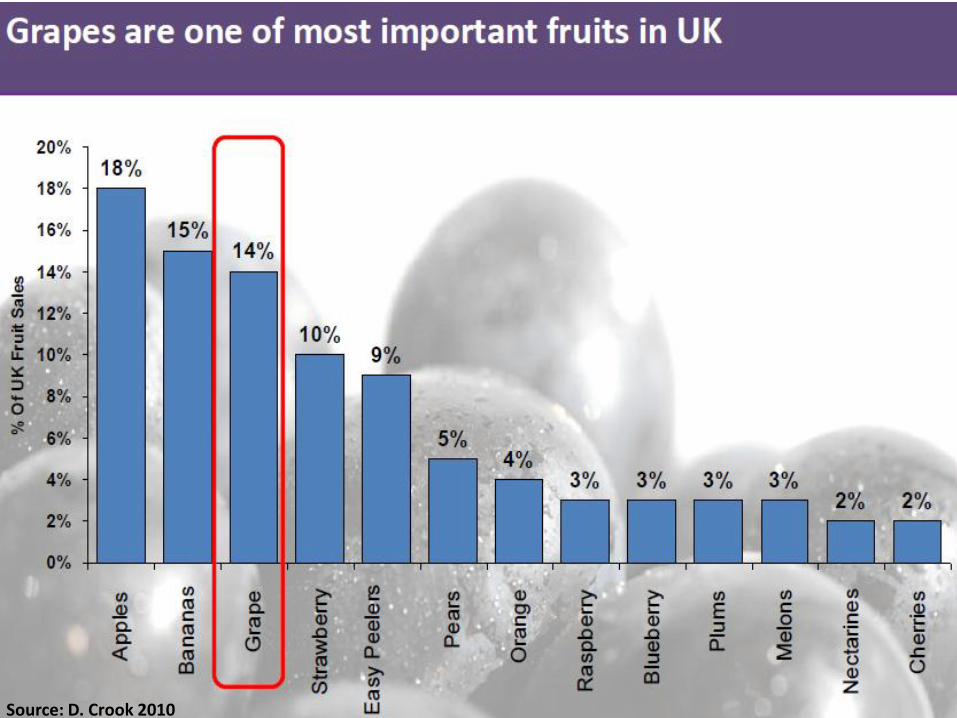

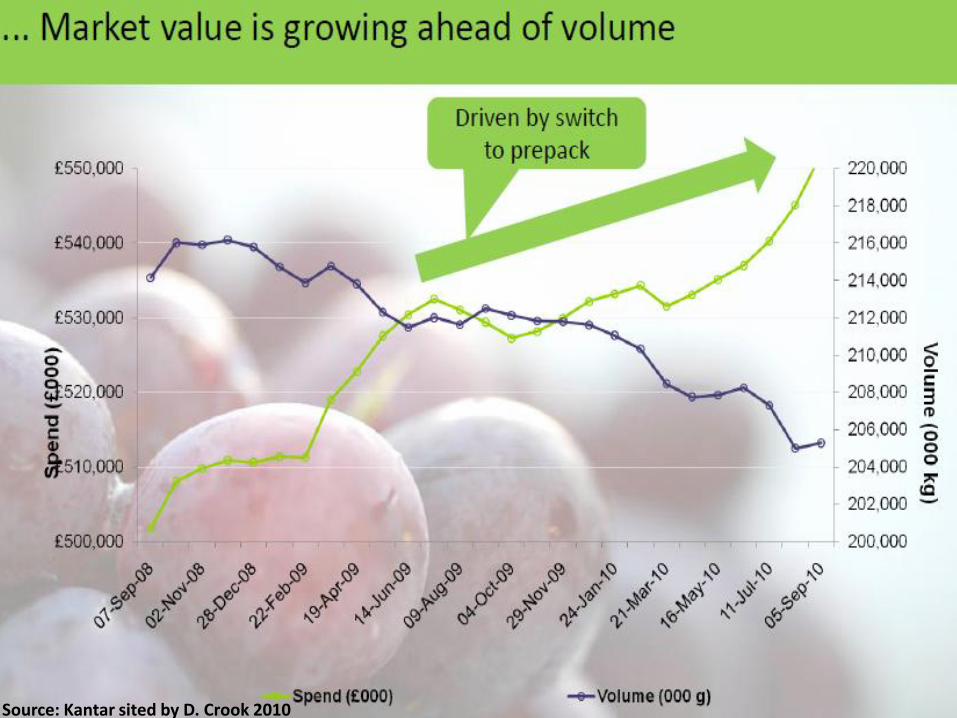

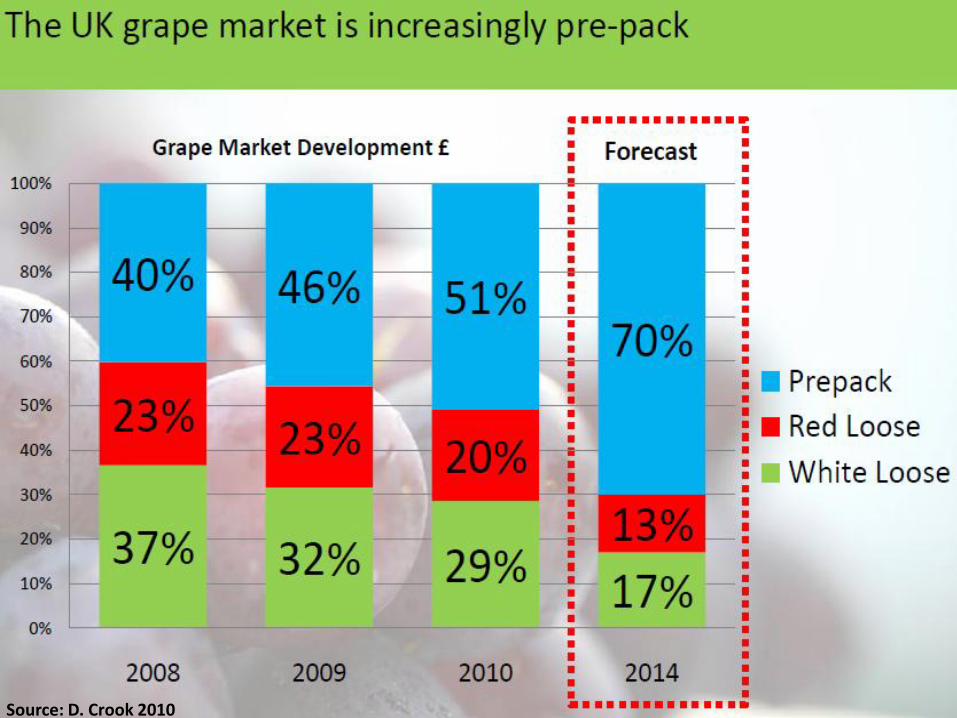

Source: Kantar sited by D. Crook 2010

Source: Kantar sited by D. Crook 2010

Source: D. Crook 2010

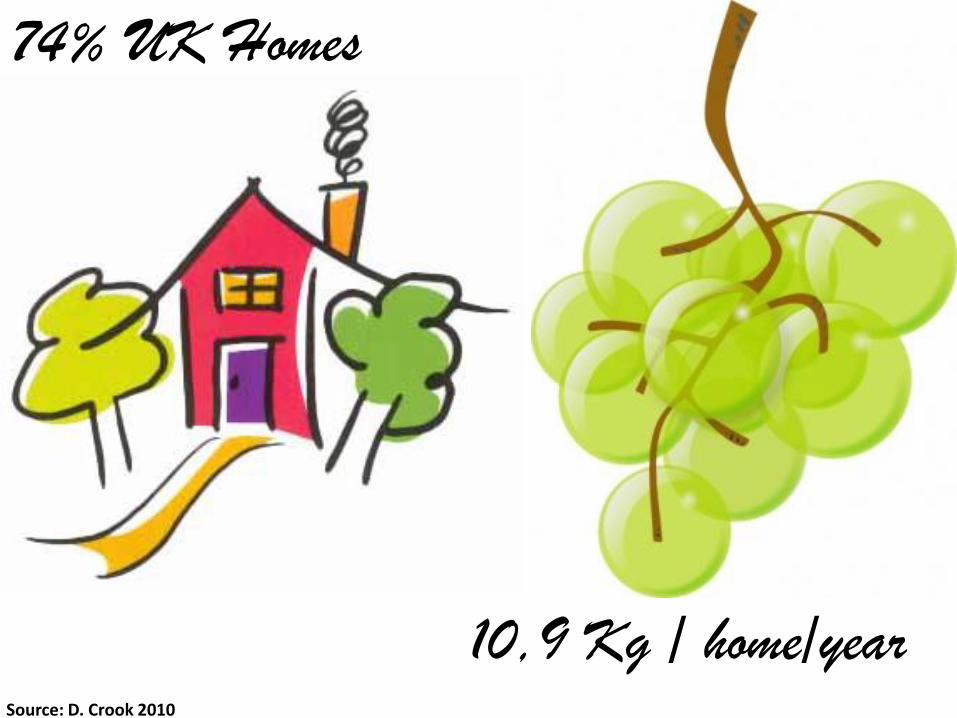

74% UK Homes

10,9 Kg / home/yearSource: D. Crook 2010

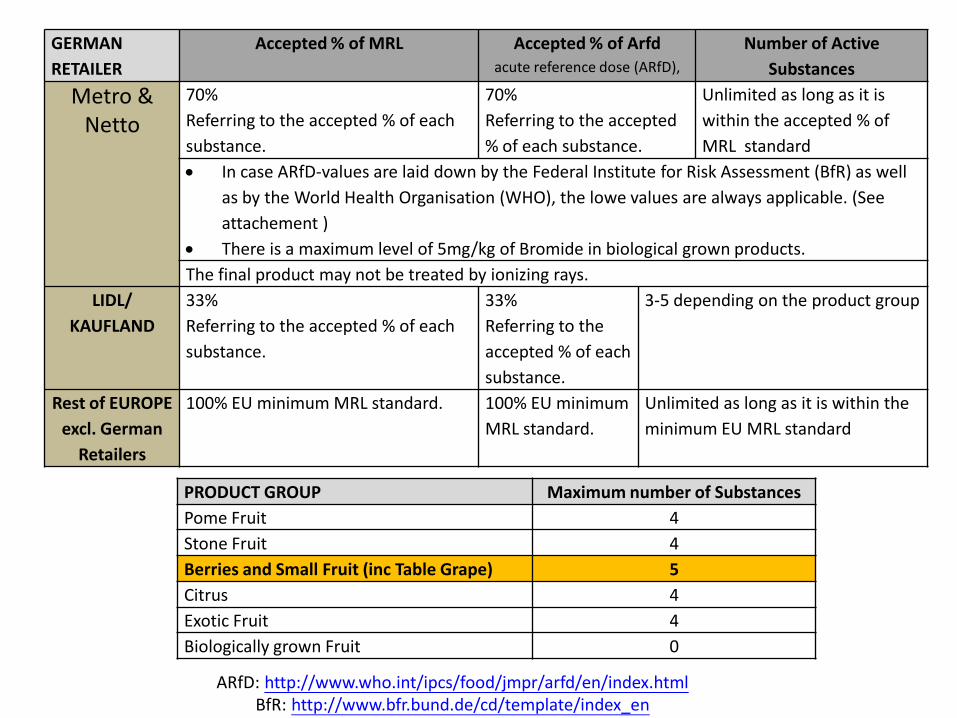

GERMAN

RETAILER

Accepted % of MRL Accepted % of Arfdacute reference dose (ARfD),

Number of Active

Substances

Metro &Netto

70%

Referring to the accepted % of each

substance.

70%

Referring to the accepted

% of each substance.

Unlimited as long as it is

within the accepted % of

MRL standard

In case ARfD-values are laid down by the Federal Institute for Risk Assessment (BfR) as well

as by the World Health Organisation (WHO), the lowe values are always applicable. (See

attachement )

There is a maximum level of 5mg/kg of Bromide in biological grown products.

The final product may not be treated by ionizing rays.

LIDL/

KAUFLAND

33%

Referring to the accepted % of each

substance.

33%

Referring to the

accepted % of each

substance.

3-5 depending on the product group

Rest of EUROPE

excl. German

Retailers

100% EU minimum MRL standard. 100% EU minimum

MRL standard.

Unlimited as long as it is within the

minimum EU MRL standard

PRODUCT GROUP Maximum number of Substances

Pome Fruit 4

Stone Fruit 4

Berries and Small Fruit (inc Table Grape) 5

Citrus 4

Exotic Fruit 4

Biologically grown Fruit 0

ARfD: http://www.who.int/ipcs/food/jmpr/arfd/en/index.htmlBfR: http://www.bfr.bund.de/cd/template/index_en

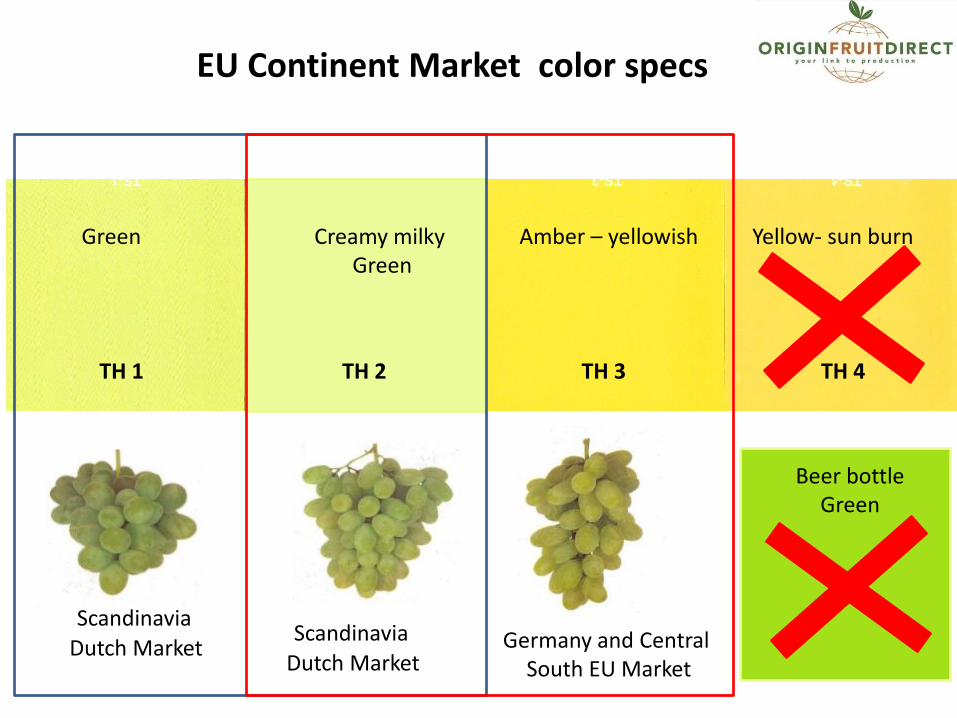

TH 1 TH 3 TH 4TH 2

Dutch Market Germany and Central South EU Market

Green Creamy milky Green

Amber – yellowish Yellow- sun burn

EU Continent Market color specs

Beer bottle Green

Scandinavia

Dutch MarketScandinavia

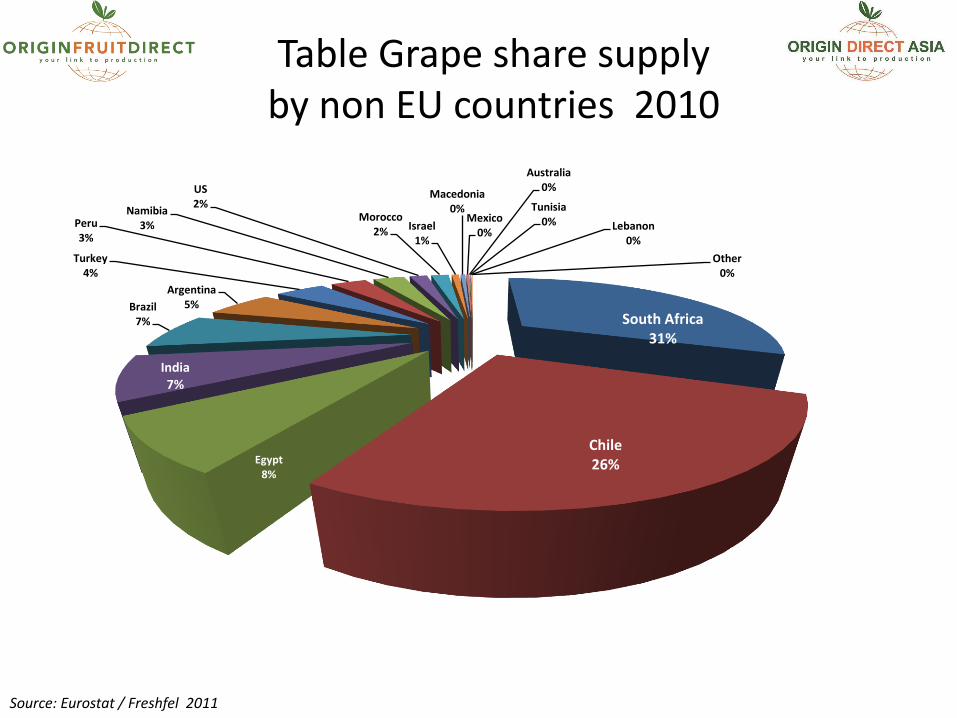

Monthly Table Grape supply by non EU countries 2005 - 2010 (tones)

Source: Eurostat / Freshfel 2011

South Africa31%

Chile26%Egypt

8%

India7%

Brazil7%

Argentina5%

Turkey4%

Peru3%

Namibia3%

US2%

Morocco2% Israel

1%

Macedonia0%

Mexico0%

Australia0%

Tunisia0% Lebanon

0%

Other 0%

Table Grape share supply by non EU countries 2010

Source: Eurostat / Freshfel 2011

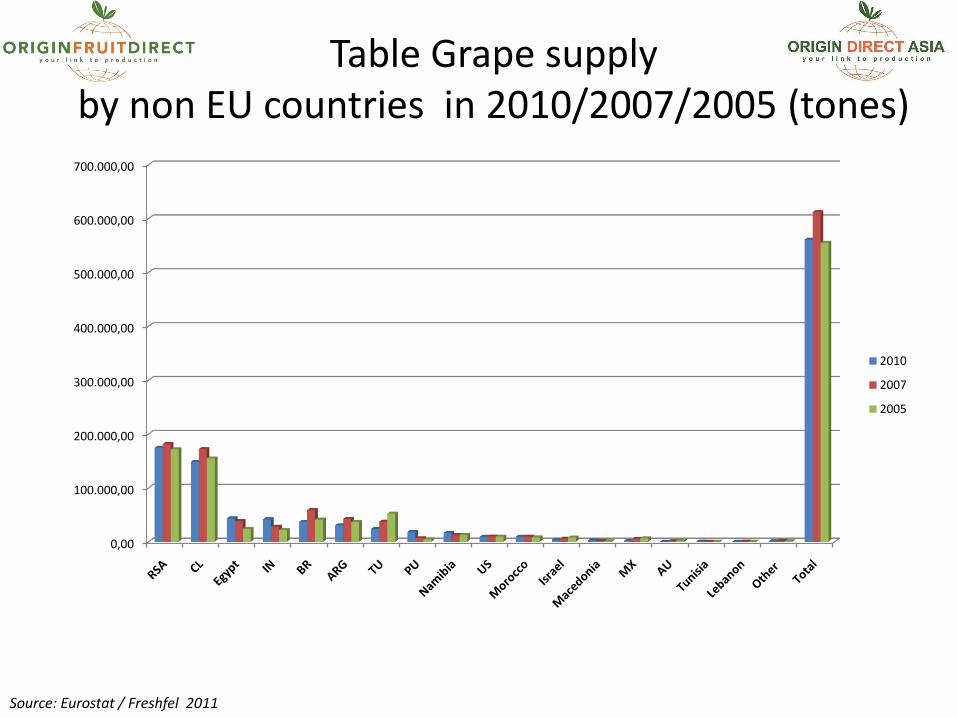

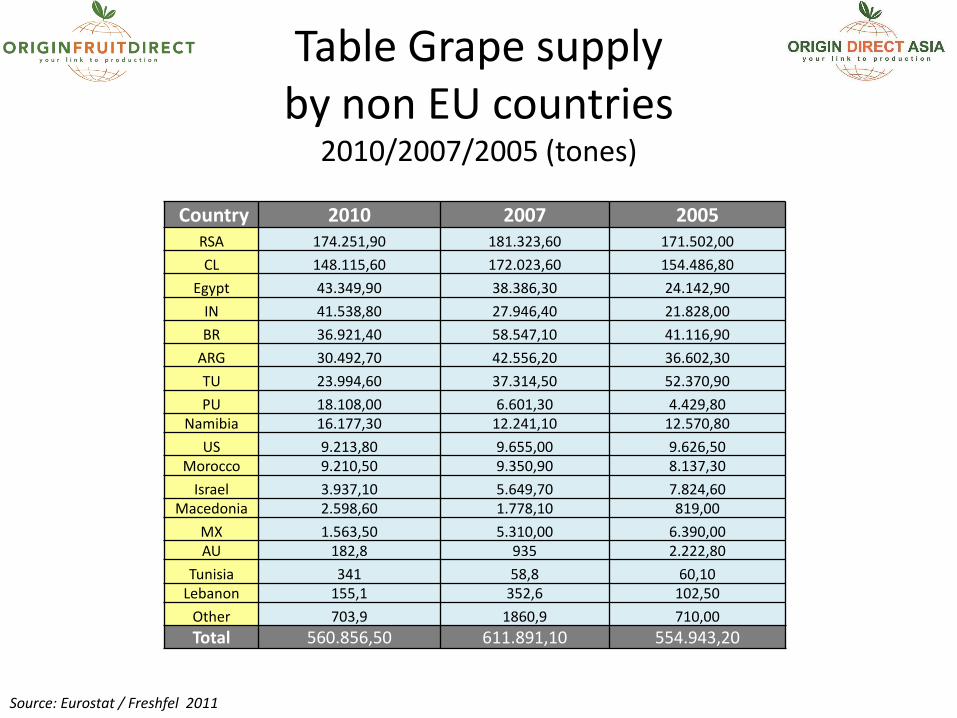

Table Grape supply by non EU countries in 2010/2007/2005 (tones)

Source: Eurostat / Freshfel 2011

0,00

100.000,00

200.000,00

300.000,00

400.000,00

500.000,00

600.000,00

700.000,00

2010

2007

2005

Country 2010 2007 2005RSA 174.251,90 181.323,60 171.502,00

CL 148.115,60 172.023,60 154.486,80

Egypt 43.349,90 38.386,30 24.142,90

IN 41.538,80 27.946,40 21.828,00

BR 36.921,40 58.547,10 41.116,90

ARG 30.492,70 42.556,20 36.602,30

TU 23.994,60 37.314,50 52.370,90

PU 18.108,00 6.601,30 4.429,80Namibia 16.177,30 12.241,10 12.570,80

US 9.213,80 9.655,00 9.626,50Morocco 9.210,50 9.350,90 8.137,30

Israel 3.937,10 5.649,70 7.824,60Macedonia 2.598,60 1.778,10 819,00

MX 1.563,50 5.310,00 6.390,00AU 182,8 935 2.222,80

Tunisia 341 58,8 60,10Lebanon 155,1 352,6 102,50

Other 703,9 1860,9 710,00

Total 560.856,50 611.891,10 554.943,20

Table Grape supply by non EU countries

2010/2007/2005 (tones)

Source: Eurostat / Freshfel 2011

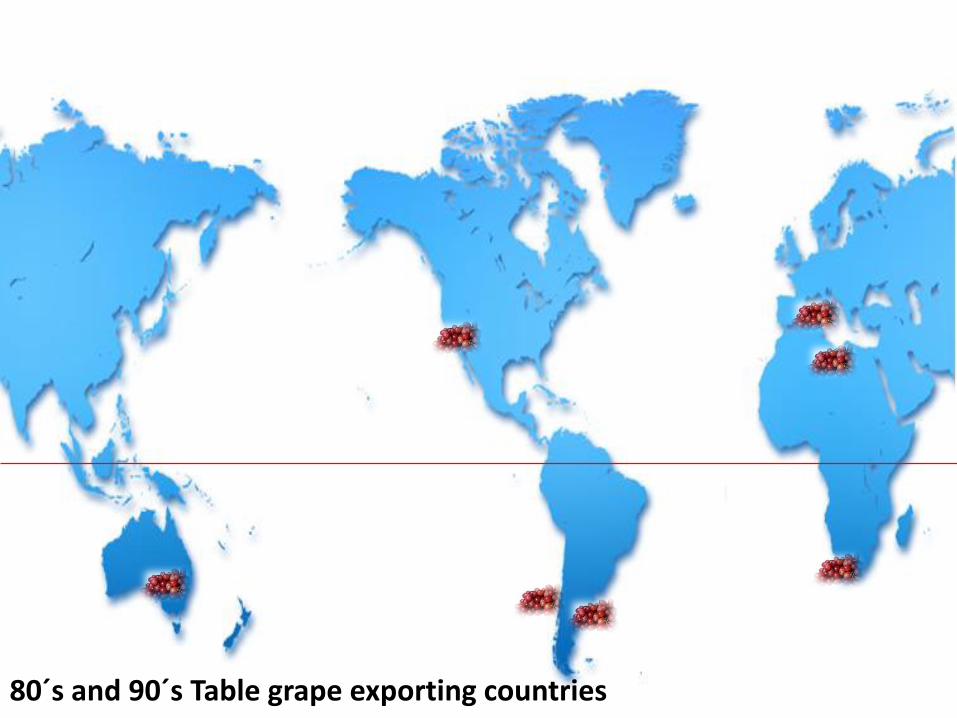

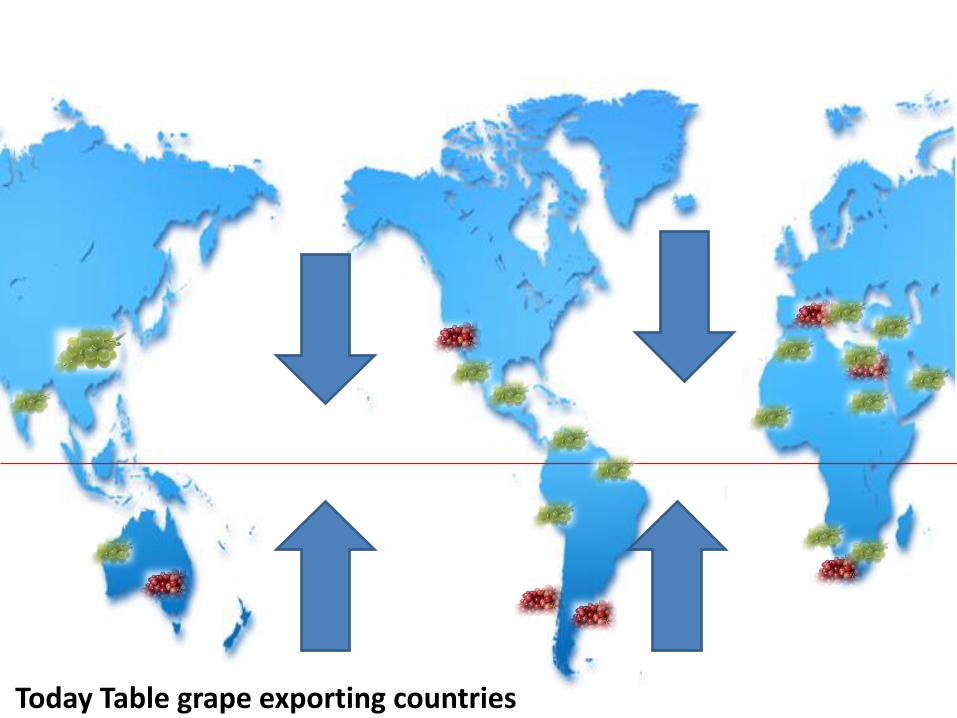

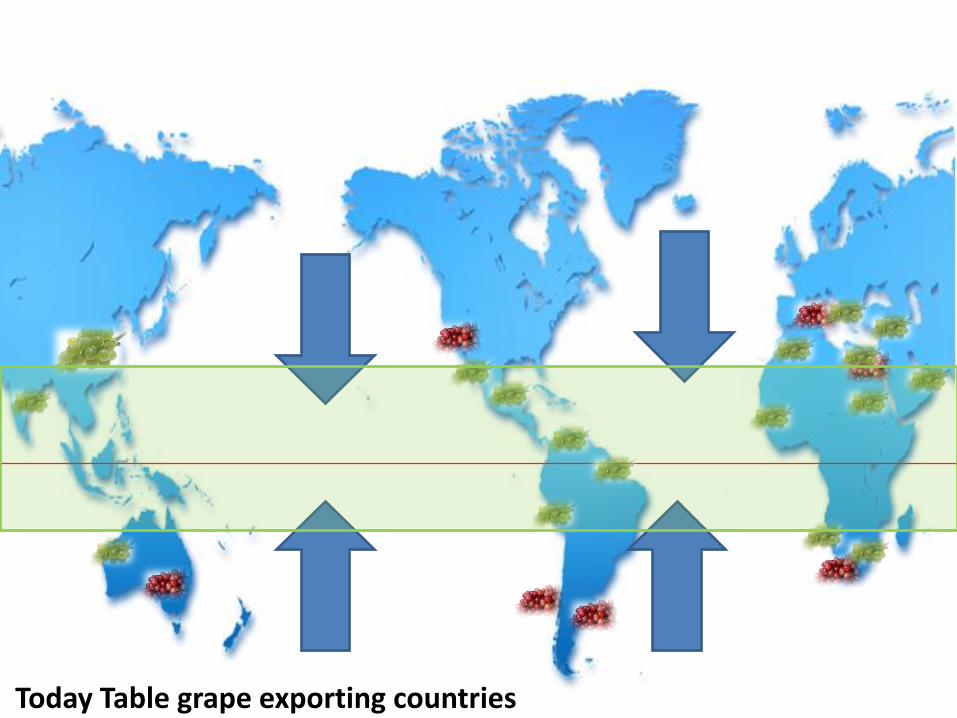

Who are the Tale Grape Players

80´s and 90´s Table grape exporting countries

Today Table grape exporting countries

Today Table grape exporting countries

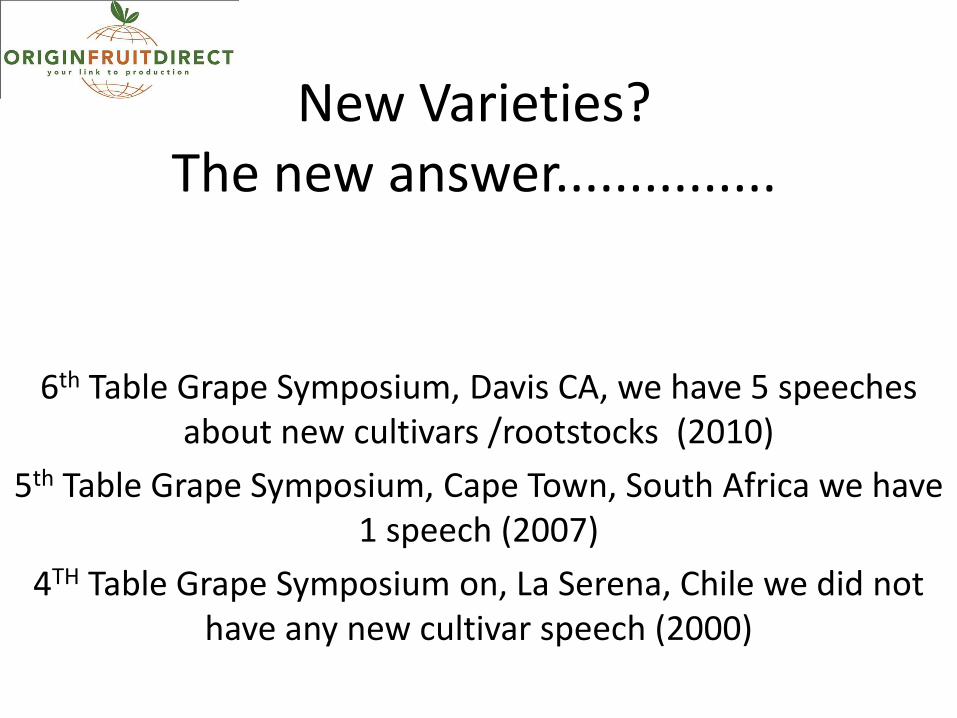

New Varieties?The new answer...............

6th Table Grape Symposium, Davis CA, we have 5 speeches about new cultivars /rootstocks (2010)

5th Table Grape Symposium, Cape Town, South Africa we have 1 speech (2007)

4TH Table Grape Symposium on, La Serena, Chile we did not have any new cultivar speech (2000)

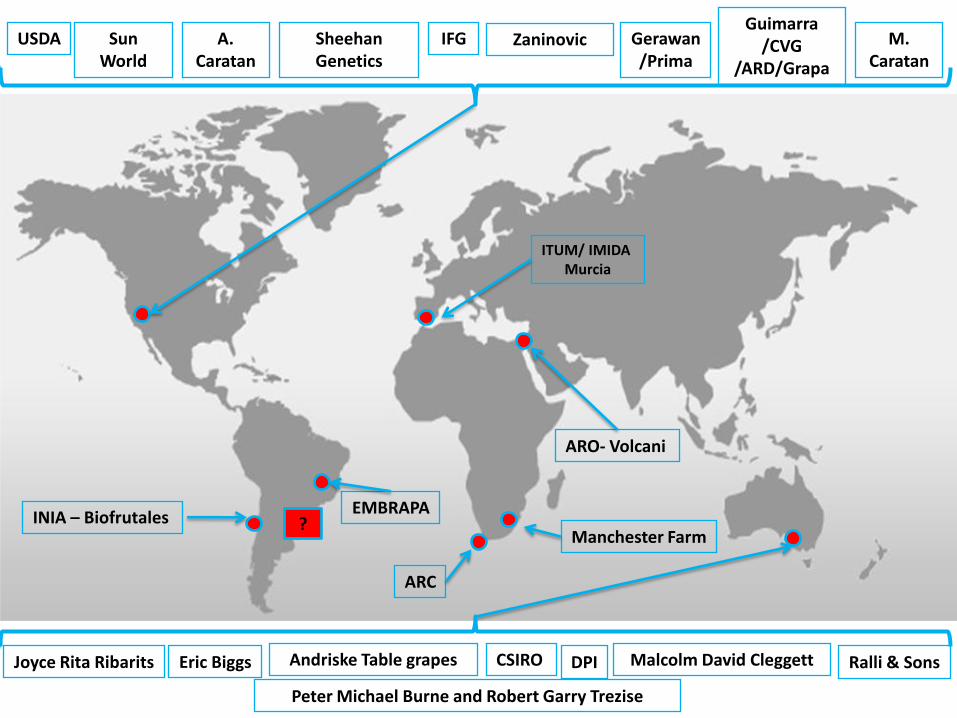

INIA – BiofrutalesEMBRAPA

ARC

Manchester Farm

ARO- Volcani

ITUM/ IMIDA Murcia

USDA Sun World

A. Caratan

Sheehan Genetics

Zaninovic Gerawan/Prima

Guimarra/CVG

/ARD/Grapa

M.Caratan

CSIRO

IFG

Andriske Table grapes DPIEric BiggsJoyce Rita Ribarits Malcolm David Cleggett

Peter Michael Burne and Robert Garry Trezise

Ralli & Sons

?

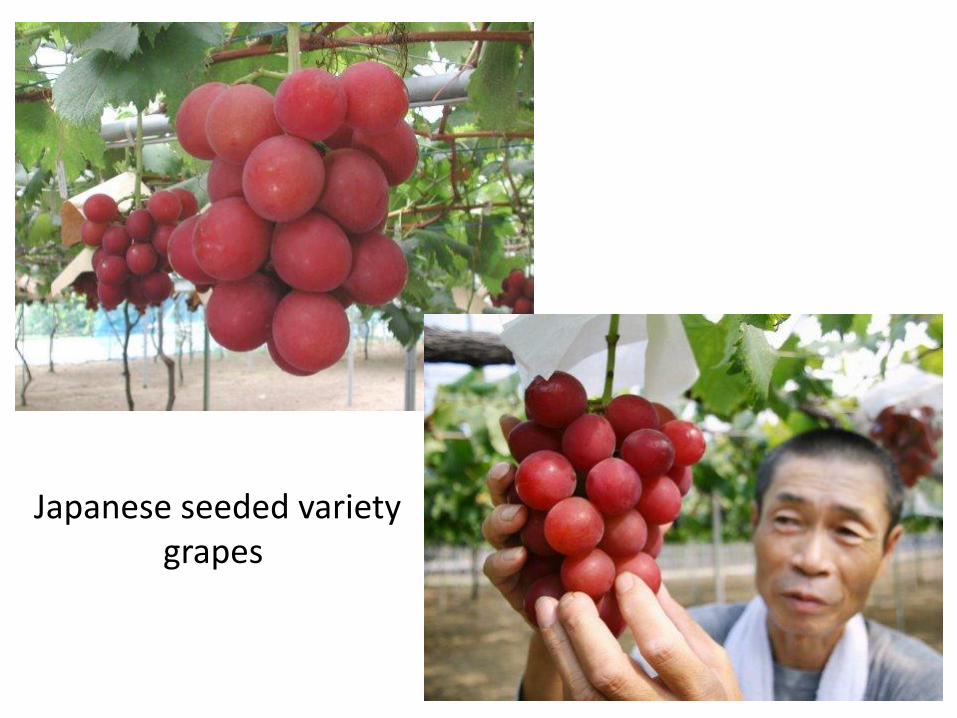

Japanese seeded varietygrapes

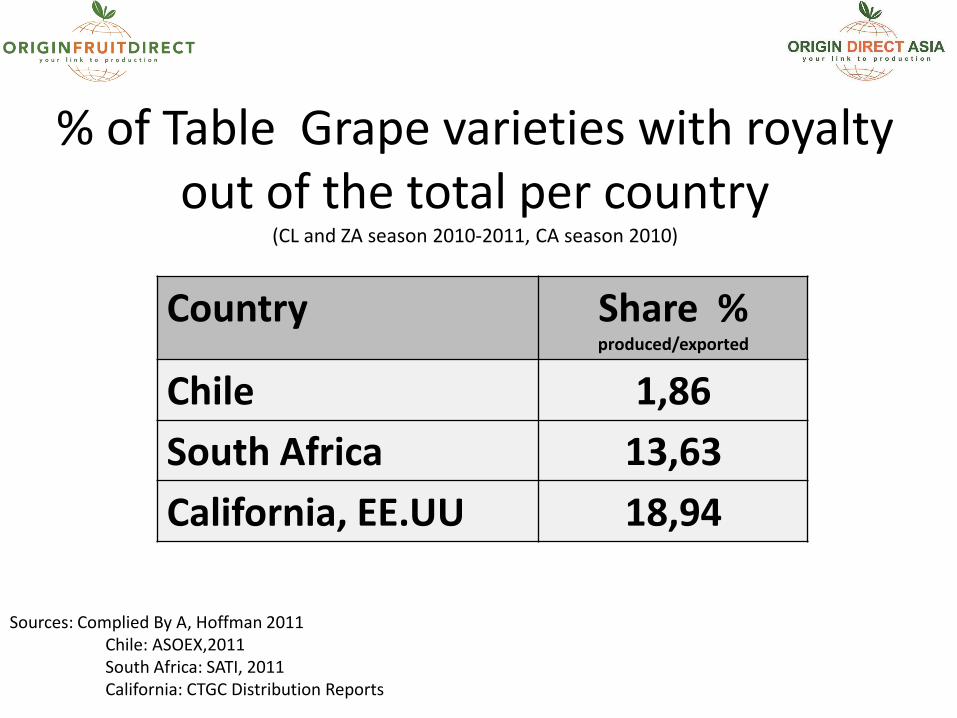

Country Share % produced/exported

Chile 1,86

South Africa 13,63

California, EE.UU 18,94

% of Table Grape varieties with royalty out of the total per country

(CL and ZA season 2010-2011, CA season 2010)

Sources: Complied By A, Hoffman 2011Chile: ASOEX,2011South Africa: SATI, 2011California: CTGC Distribution Reports

Pronósticos………….

El mapa de abastecimiento de uva de exportación tendrá un dramático cambio

• Descubrimiento de nuevas zonas productivas, tendiendo a zonas tropicales o subtropicales con periodos sin lluvias (hacia el Ecuador) para manejar las fechas de cosecha.

• Nuevas variedades (las exitosas) resaltarán el impacto de estas zonas.

• Mientas se limpia el mercado de las variedades perdedoras, habrá confusión, las variedades tradicionales seguirán jugando un papel importante por varios años.

• Focalizar en que requerimos para seleccionar las variedades.

• Cada nueva variedad tiene un modelos de negocio, las variedades “Libres se acabaron”

• Algunas zonas tradicionales de producción de uva de mesa quedaran obsoletas.

• Tiempos de mirar con calma, de oportunidades y muchos daños colaterales

• Habrá que abandonar algunos mercados

• Concentración de la producción

• Commoditiesación de la uva de mesa

The New frontier

GMO

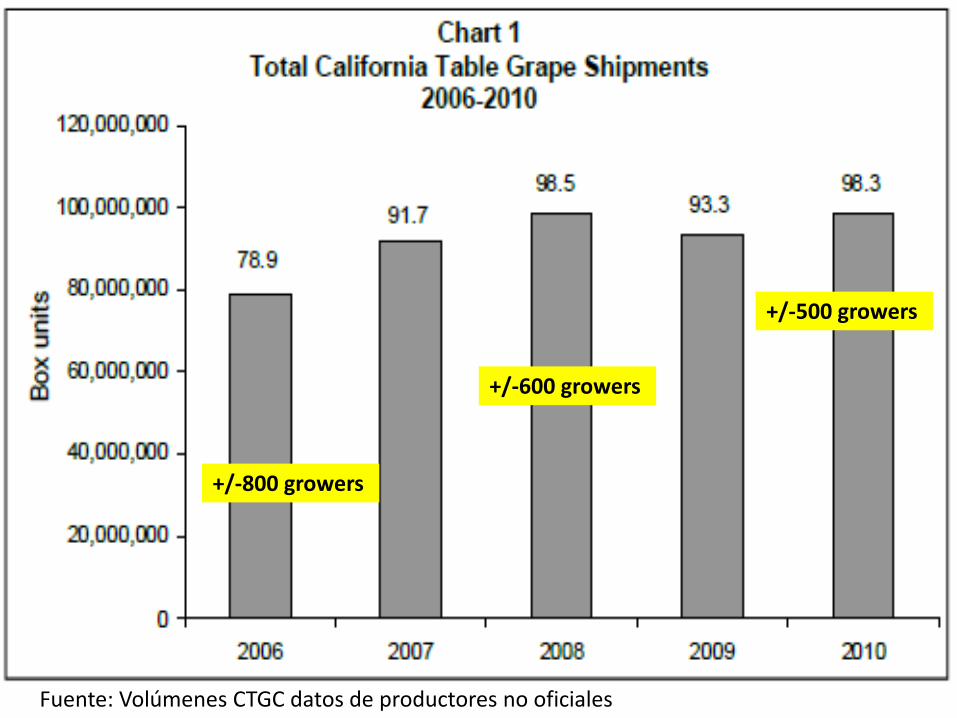

+/-800 growers

+/-600 growers

+/-500 growers

Fuente: Volúmenes CTGC datos de productores no oficiales

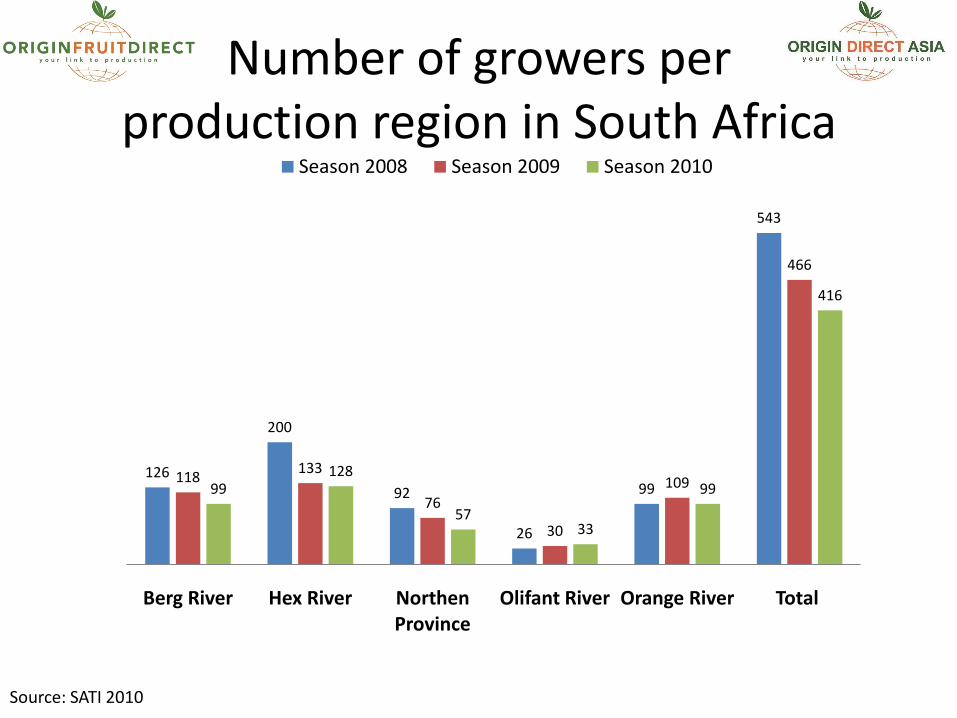

126

200

92

26

99

543

118133

76

30

109

466

99128

5733

99

416

Berg River Hex River Northen Province

Olifant River Orange River Total

Season 2008 Season 2009 Season 2010

Number of growers per production region in South Africa

Source: SATI 2010

21-26 días+1 a 3

12 -15 días(20 días en contenedor)

35–45 días+7 - 12

50-55 días+7 a 10

Tiempos de transito Uva de Chile a diferentes mercados

Fuente: recopilado de varias navieras por O. Salgado a marzo 2011

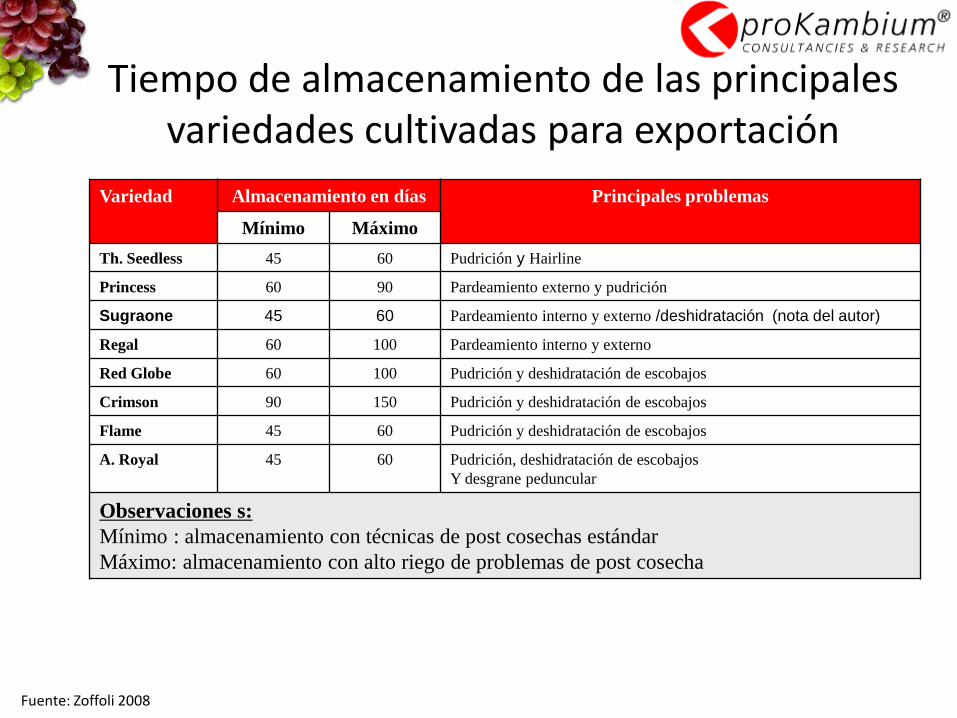

Variedad Almacenamiento en días Principales problemas

Mínimo Máximo

Th. Seedless 45 60 Pudrición y Hairline

Princess 60 90 Pardeamiento externo y pudrición

Sugraone 45 60 Pardeamiento interno y externo /deshidratación (nota del autor)

Regal 60 100 Pardeamiento interno y externo

Red Globe 60 100 Pudrición y deshidratación de escobajos

Crimson 90 150 Pudrición y deshidratación de escobajos

Flame 45 60 Pudrición y deshidratación de escobajos

A. Royal 45 60 Pudrición, deshidratación de escobajos

Y desgrane peduncular

Observaciones s:

Mínimo : almacenamiento con técnicas de post cosechas estándar

Máximo: almacenamiento con alto riego de problemas de post cosecha

Fuente: Zoffoli 2008

Tiempo de almacenamiento de las principales variedades cultivadas para exportación

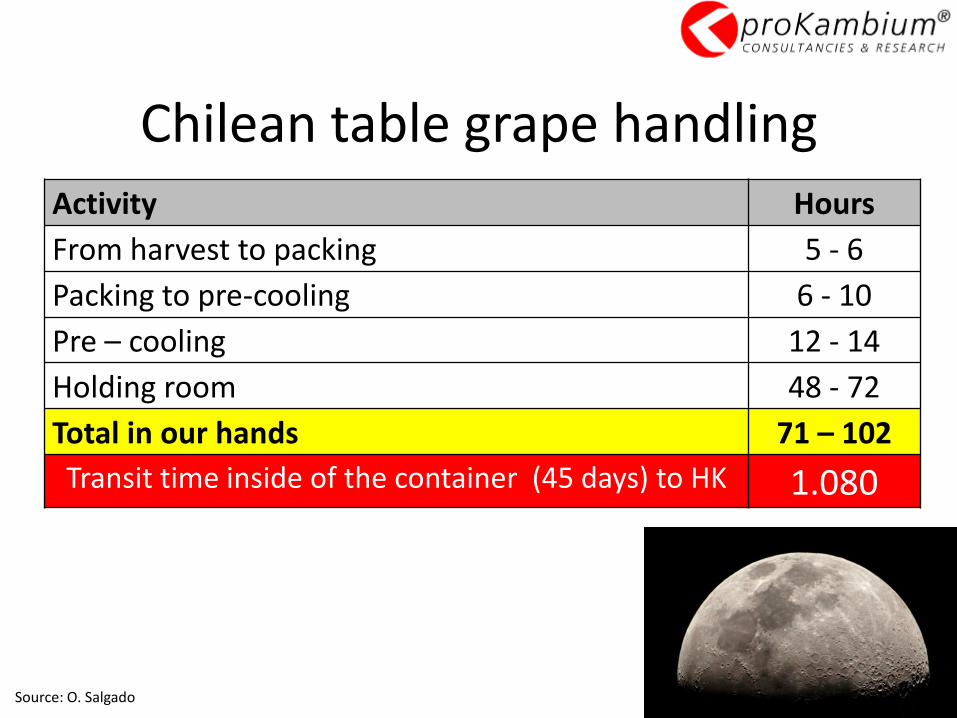

Activity Hours

From harvest to packing 5 - 6

Packing to pre-cooling 6 - 10

Pre – cooling 12 - 14

Holding room 48 - 72

Total in our hands 71 – 102

Transit time inside of the container (45 days) to HK 1.080

Source: O. Salgado

Chilean table grape handling

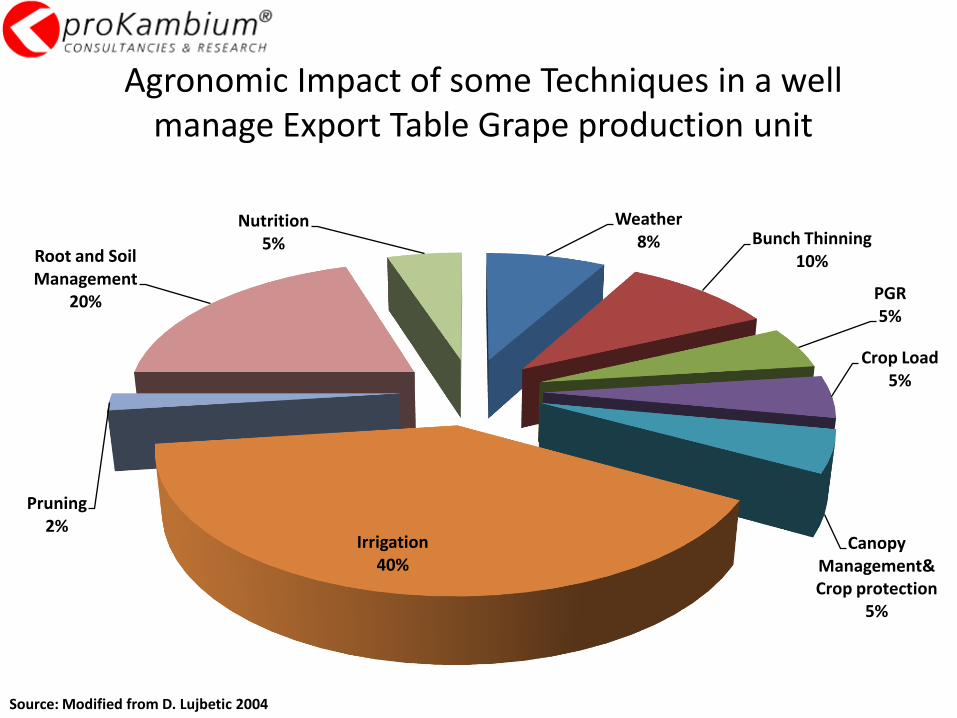

Weather 8% Bunch Thinning

10%

PGR5%

Crop Load 5%

Canopy Management&Crop protection

5%

Irrigation 40%

Pruning 2%

Root and Soil Management

20%

Nutrition 5%

Agronomic Impact of some Techniques in a well manage Export Table Grape production unit

Source: Modified from D. Lujbetic 2004

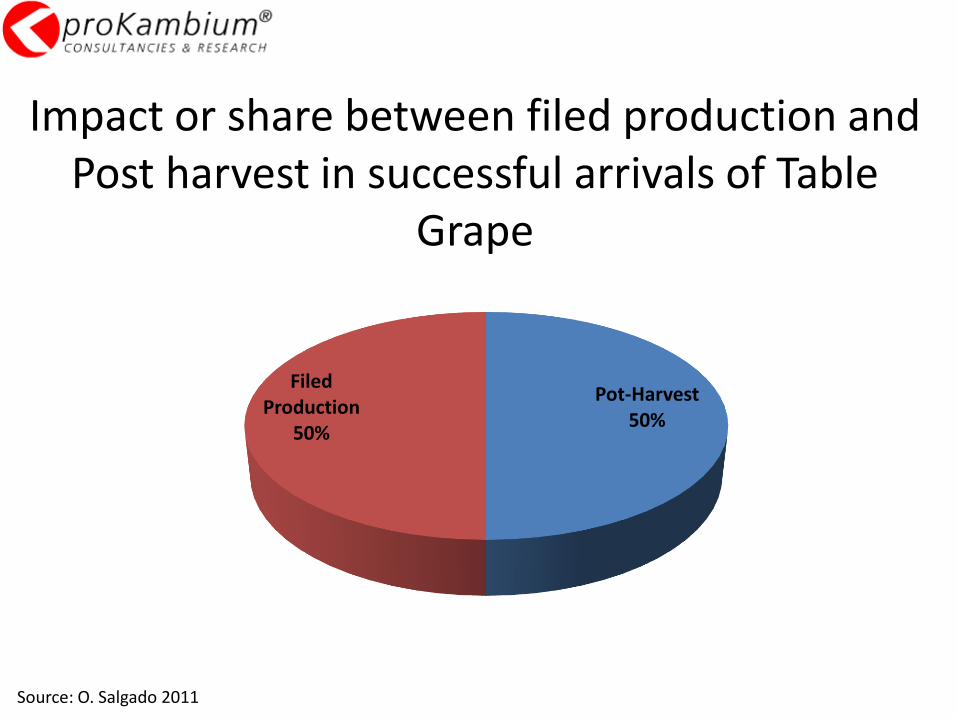

Pot-Harvest 50%

Filed Production

50%

Impact or share between filed production and Post harvest in successful arrivals of Table

Grape

Source: O. Salgado 2011

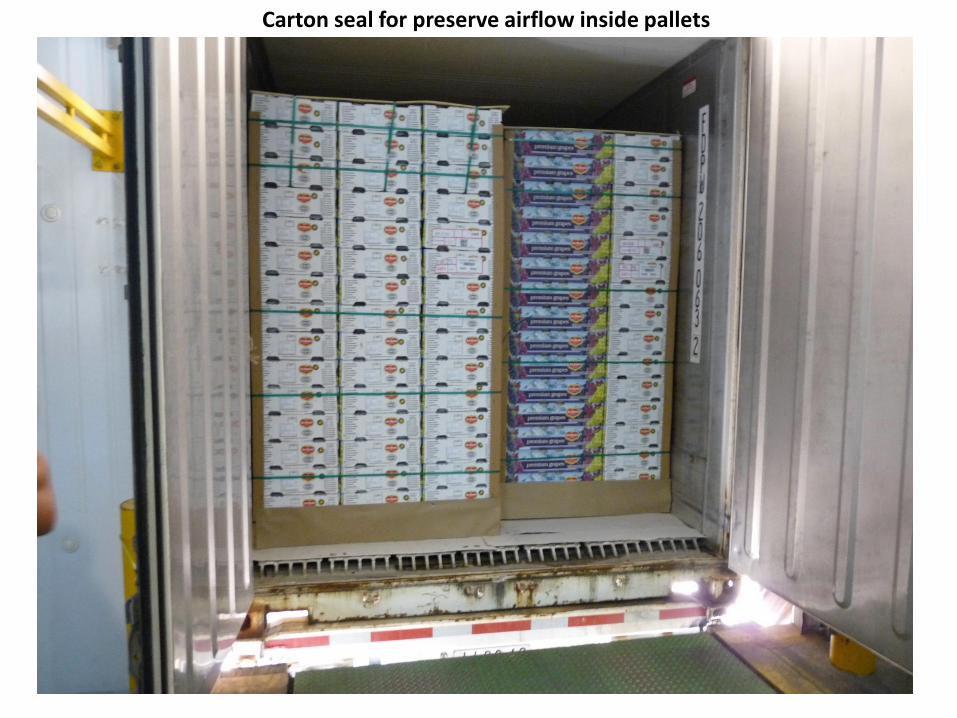

Carton seal for preserve airflow inside pallets

0% Ventilation for Table Grapes

Emergen nuevamente las ventas…………..:

• Noviembre que era de Brazil……………..Candidato “Perú artista invitado………………… Piura”

• Abril - Mayo que era de la India…………….Candidatos………..“Puede ser Perú? O Senegal o Kenia o Sudan….”

• Si Perú las cubre que le pasa a Chile………………..?