Embed Size (px)

Citation preview

1

Metaphors and Auditor Professional Judgment: Can Non-Conscious Primes Activate Professionally Skeptical Mindsets?

Mary C. Parlee

Bentley University

Jacob M. Rose Bentley University

Jay C. Thibodeau Bentley University

April 2014

Corresponding Author

Mary C. Parlee PhD Student

Accountancy Department Bentley University 175 Forest Street

Waltham, MA 02452 Phone: 781-891-2134 Fax: 781-891-2896

E-Mail: [email protected]

Acknowledgements: We thank the experienced auditors who took the time to complete the experimental materials. We also wish to thank Kimberly Moreno, Anna Rose, participants of workshops at Northeastern University, Bentley University, and participants of the 2014 Auditing Midyear Meeting for their comments and helpful insights.

2

Metaphors and Auditor Professional Judgment: Can Non-Conscious Primes Activate Professionally Skeptical Mindsets?

Abstract

Results of an experiment with 99 senior auditors from two Big 4 audit firms indicate that

reading simple metaphors promotes professional skepticism and influences auditors’ skeptical

judgments. Relative to auditor participants who did not read a metaphor, participants who read a

metaphor related to concerns about the honesty of sources of information (client-skeptical

metaphor) or concerns about one’s own ability to detect problems (self-skeptical metaphor)

assessed higher levels of fraud risk, assessed greater needs for a risk management partner, and

perceived that fraud-based explanations were more likely to cause fluctuations in client ratios.

Further, the client-skeptical metaphor caused auditors to increase audit hours and increase audit

testing for accounts likely to be influence by fraud. Metaphors are a form of non-conscious

prime, and our results suggest that non-conscious priming represents a powerful and efficient

tool for promoting professional skepticism.

Key words: Audit planning, fraud risk, metaphor, professional skepticism

3

I. INTRODUCTION

Promoting professional skepticism is a high priority for audit firms because professional

skepticism is viewed as essential for the prevention of audit failures, and the Public Company

Accounting Oversight Board (PCAOB) has linked the lack of professional skepticism to audit

deficiencies discovered in their inspections (PCAOB 2008; PCAOB 2012). Professional

skepticism is defined by the PCAOB (2012) as “an attitude that includes a questioning mind and

a critical assessment of audit evidence,” and PCAOB standards require professional skepticism

during the audit process. In a recent Staff Audit Practice Alert, the PCAOB indicated that

features of the audit environment, such as strenuous workloads, can inhibit the appropriate

application of professional skepticism (PCAOB 2012). Thus, determining methods to efficiently

promote skepticism while auditors make professional judgments is critical to audit practitioners

and regulators. The purpose of this study is to examine the potential for simple metaphors to

prime professional skepticism during an auditor’s professional judgment process.

Metaphors represent a potentially valuable tool for promoting professional skepticism

because prior research indicates that metaphors activate complex knowledge structures and

initiate mindsets that guide the search for and analysis of evidence (e.g., Gibbs 1992; Galinsky

and Glucksberg 2000; Boroditsky 2000; Boroditsky and Ramscar 2002; Slobin 2003; Thibodeau

and Boroditsky 2011). In fact, metaphors have been shown to overwhelm the effects of strongly-

held opinions and beliefs and shift individuals’ judgment processes without extensive training

and without increasing the cognitive demands placed upon decision makers. Metaphors exert

influence over decision makers’ reasoning by activating frame-consistent knowledge structures,

and inviting structurally-consistent inferences (Boroditsky 2000; Boroditsky and Ramscar 2002).

As a result, when decision makers seek out evidence to inform their decisions, they tend to

4

choose information that will confirm and elaborate the frame suggested by the metaphor. Even

fleeting and seemingly unnoticed metaphors can activate complex knowledge structures and

influence an individual’s reasoning in a powerful way (Thibodeau and Boroditsky 2011). We

posit that metaphors can promote professional skepticism.

To test our hypotheses, we conduct an experiment with a 3x1 between-participants design

where participants are 99 senior auditors from two Big 4 audit firms. The manipulated

independent variable is the presence of a metaphor (self-skeptical metaphor, client-skeptical

metaphor, or no metaphor). We examine two different types of metaphors because prior research

suggests that different forms of skepticism may result in differential effects on auditor judgment

(Bell et al. 2005; Grenier 2011). One metaphor promotes skepticism of one’s own ability to

detect important evidence (self-skeptical metaphor) and the second metaphor induces skepticism

of the source of evidence (client-skeptical metaphor). Recent research by Quadackers et al.

(2013) indicates that a presumptive doubt perspective (where auditors assume some level of

dishonesty by clients) is more related to auditors’ skeptical judgments than a neutral perspective,

and our client-skeptical metaphor is designed to prime a form of presumptive doubt. Conversely,

research by Grenier (2011) indicates that self-skepticism influences expert auditor’s judgments

related to fraud, but that client-skepticism does not change expert’s judgment processes. Thus,

our second metaphor is designed to prime self-skepticism, and the use of both metaphors allows

us to test the competing findings of existing research.

The experiment asks auditor participants to evaluate audit evidence, including a set of

ratio fluctuations and a client explanation for the fluctuations. Findings from the experiment

indicate that metaphors inducing either skepticism of one’s own capabilities or skepticism related

to clients both increased the participants’ assessments of fraud risk as compared to participants in

5

the control group. In addition, both types of metaphors increased auditors’ perceptions that

fraud-related explanations are likely to explain the ratio fluctuations in the experimental case,

and both increased the perceived need for a risk management partner to participate in the audit.

For audit planning, however, only the client-skepticism metaphor influenced audit judgments.

Specifically, reading a metaphor that primed skepticism related to the source of evidence (i.e.,

the audit client) caused auditors to increase planned audit hours and increase the number of

planned audit tests related to the revenue cycle. Taken together, across a number of proxies for

the level of professional skepticism, our findings support the proposition that metaphors can

effectively promote professional skepticism because they prime skeptical mindsets.

Our results are important to practice because audit firms and the PCAOB are actively

seeking methods to promote professional skepticism, and we find that it is possible to activate

mindsets that do so, independent of the audit task. As a result, we expect that priming techniques

such as metaphors can favorably influence auditors’ professional skepticism across a wide range

of audit tasks and judgments. Perhaps most importantly, employing priming techniques such as

reading metaphors to promote professional skepticism can be done efficiently as priming does

not require costly training or long-term time commitments. Moreover, reading metaphors does

not increase the cognitive burdens or time demands of the audit process. From a theory

perspective, the results of our experiment call into question previous conclusions that skepticism

of one’s judgment abilities has more influence on experienced auditors’ fraud-related judgments

than client-related skepticism. Quite interestingly, we find that skepticism related to clients and

skepticism of one’s capabilities both have the capacity to influence risk assessments, but only the

metaphors that triggered skepticism associated with clients causes auditors to adjust audit hours

and planned procedures.

6

II. BACKGROUND AND HYPOTHESES DEVELOPMENT

Metaphorical Framing

Metaphors are extremely common in everyday communication. Rather than merely

expressive figures of speech, they are fundamental to thought, understanding, and decision

making (Lakoff and Johnson 1980; Young 2001). Studies from psychology and linguistics

demonstrate that reading a metaphor activates schemas from one decision domain which will

prime the reader to encode subsequent information using that schema (e.g., Gibbs 1992;

Galinsky and Glucksberg 2000; Slobin 2003). For example, Thibodeau and Boroditsky (2011)

described crime as a “virus” versus a “beast” and asked participants to propose methods for

reducing crime. Participants’ decisions, information search, and perceptions were all

significantly changed by these single-word metaphors because the metaphors instantiated a

knowledge structure that guided their decision processes. The effects of these simple metaphors

even overwhelmed the effects of existing beliefs and political affiliations on participants’

decisions.

Subtle metaphors such as the single words described above significantly change people’s

judgment processes and decisions (Boroditsky 2000; Boroditsky and Ramscar 2002; Thibodeau

and Boroditsky 2011). Thus, we expect that well-constructed metaphors can be employed to

activate a schema related to professional skepticism, and the activation of this schema will

influence the evaluation of audit evidence and decisions based upon this evidence. Such an

approach represents a very efficient method of promoting professional skepticism because a

single metaphor may have the capacity to induce professional skepticism that is applied across a

wide variety of audit contexts without increasing the cognitive demands of the audit tasks.

7

Metaphors are known to activate conceptual schemas that assist in the comprehension of abstract

concepts (Lakoff and Johnson 1999). Judgments in auditing incorporate numerous abstract

concepts, such as risk, value, and skepticism. Lakoff and Johnson (1980) explain that abstract

concepts are fundamentally metaphorical in nature because they are typically not experienced

physically. The schemas activated by metaphors focus attention and information search on one

aspect of a concept, while diminishing other aspects that are not consistent with the activated

schema (Lakoff and Johnson 1980; Young 2001). By activating a conceptual schema associated

with a skeptical mindset, we suggest that metaphors can prime auditors to employ professional

skepticism in their judgment processes.

Promoting Professional Skepticism

Audit firms have long recognized the importance of exercising professional skepticism

when making professional judgments. Indeed, the recent monograph entitled Elevating

Professional Judgment in Accounting and Auditing: The KPMG Professional Judgment

Framework (KPMG 2011, 6) argues that “Professional skepticism is an objective attitude that

includes a questioning mind and a critical assessment of audit evidence that is an important part

of the professional judgment process.” Thus, while professional skepticism “is not synonymous

with professional judgment” it is clearly an “important component or subset of professional

judgment.”

In its 2010 report, Deterring and Detecting Financial Reporting Fraud, the Center for

Audit Quality (CAQ) defines skepticism as “a questioning mindset and an attitude that withholds

judgment until evidence is adequate - promotes risk awareness and is inherently an enemy of

fraud.” Nelson (2009) defines skepticism as “auditor judgments and decisions that reflect a

heightened assessment of the risk that an assertion is incorrect, conditional on the information

8

available to the auditor.” The conclusion of recent definitions of professional skepticism is that

professional skepticism is necessary for the detection of fraud and is essential for the prevention

of audit failures. Prior academic research provides support for this perspective because a lack of

professional skepticism has been shown to be a primary cause of SEC enforcement actions and

claims of malpractice made against audit firms (Beasley et al. 2001; Anderson and Wolfe 2002;

Benston and Hartgraves 2002). As a result of the correlation between audit failures and

insufficient professional skepticism, the PCAOB now emphasizes professional skepticism

throughout its inspection process (PCAOB 2012).

Auditing standards also stress the importance of professional skepticism. Statement on

Auditing Standards (SAS) No. 99, Consideration of Fraud in a Financial Statement Audit,

requires auditors to place an increased emphasis on professional skepticism. The standard states

that “the auditor should not be satisfied with less-than-persuasive evidence because of a belief

that management is honest” (AICPA 2002). As part of the requirement to exercise due

professional care, PCAOB standards require the auditor to be professionally skeptical while

planning the audit, performing the audit, and preparing the audit report (PCAOB 2012). Even

though professional skepticism is now required, observations from the PCAOB's oversight

activities continue to raise concerns about auditors’ application of professional skepticism.

According to the PCAOB, when auditors are not appropriately skeptical, they may not obtain

sufficient evidence to support their opinions, and they can fail to recognize when material

misstatements exist in the financial statements (PCAOB 2012). Thus, the ultimate effects of

professional skepticism are manifested in auditor judgment.

Evidence from psychology indicates that increased skepticism leads to more critical

evaluation of evidence (Schul et al. 2006). Skepticism of evidence or its source results in the

9

generation of more alternative explanations for evidence, consistent with a questioning mindset

(Hilton et al. 1993; Schul et al. 2006). Academic researchers have proposed that there are two

primary forms of professional skepticism that influence auditor judgment: skepticism related to

the client and skepticism related to one’s self and one’s own judgment capabilities (Bell et al.

2005; Nelson 2009; Grenier 2011; Quadackers et al. 2013). Skepticism associated with the client

involves concerns about the reliability of evidence and honesty of the client, while skepticism of

the self brings about concerns about one’s fallibilities and inability to detect all problems and

errors.

Prior audit research supports the idea that increased skepticism of the client and evidence

influences judgment and decision making. Peecher (1996) promoted professional skepticism by

informing experiment participants that audits were being conducted without adequate skepticism.

When auditors were told to be more skeptical, the auditors relied less on a client’s explanation.

Phillips (1999) and Rose (2007) found that auditors who are made skeptical by audit evidence

suggestive of fraud pay more attention to other evidence indicative of aggressive financial

reporting. Finally, Grenier (2011) conducted an experiment where he informed half of the

auditor participants that they should be skeptical of their own judgment abilities and half to be

skeptical of the client. Auditors who were considered experts in the topic of the experimental

case increased the number of fraud explanations they generated for audit evidence when

instructed to be skeptical of their judgment abilities, but instructing them to be skeptical of the

client did not influence the generation of fraud explanations. Grenier (2011) suggests that expert

auditors exhibit fairly automatic judgments, and telling them to be skeptical of the client has little

effect on their consideration of fraud. However, he suggests that making them more aware of

10

their own judgment fallibilities causes them to be concerned about what they know, and this

heightens concerns about fraud.

We propose that metaphorical primes that either induce self-skepticism or client-

skepticism will both influence auditors’ professional skepticism and judgments. While Grenier

(2011) finds that inducing skepticism of the client does not affect judgment, he primes

participants by instructing them to be more skeptical of the evidence during the task. Peecher

(1996) employed a similar approach to induce skepticism. Such manipulations are not

necessarily representative of true priming but rather are akin to providing instructions to behave

in a specific manner that relies on explicit memory. If auditors with significant expertise employ

relatively automated judgments, these automated judgments largely involve non-conscious

processes (Bargh and Chartrand 1999; Bargh et al. 2001). Automated, non-conscious processing

is influenced more by implicit memory effects than by instructions based on explicit memory

(Goldfarb et al. 2011). Reading metaphors represents true priming that is based on implicit

memory effects, and the effects of metaphorical priming have been demonstrated to significantly

influence information search and judgment through the activation of metaphor consistent

schema. Thus, we expect that metaphorical primes, as well as other forms of true priming, will

have different effects than providing instructions to be skeptical.

Based upon the research related to metaphors, and the differences between metaphorical

priming and providing instructions to be skeptical, we propose that metaphorical primes will

promote professional skepticism (either client skepticism or self-skepticism) and will influence

fraud risk assessments and the generation of explanations for evidence. The first three

hypotheses address the expected effects of metaphors on fraud risk assessment and explanation

generation:

11

H1: Auditors who read a metaphor that primes skepticism (self-skeptical or client-skeptical) will assess higher levels of risk of fraud relative to auditors who do not read a metaphor. H2a: Auditors who read a metaphor that primes skepticism (self-skeptical or client-skeptical) will generate more fraud-based explanations for ratio fluctuations relative to auditors who do not read a metaphor. H2b: Auditors who read a metaphor that primes skepticism (self-skeptical or client-skeptical) will be more likely to perceive that fraud-based actions are the causes of ratio fluctuations than will auditors who do not read a metaphor.

The potential effects of metaphors on audit planning are less clear. The PCAOB states

that auditors who have reason to be skeptical of evidence should “(1) modify the planned audit

procedures to obtain more reliable evidence regarding relevant assertions and (2) obtain

sufficient appropriate evidence to corroborate management's explanations or representations

concerning important matters, such as through third-party confirmation, use of a specialist

engaged or employed by the auditor, or examination of documentation from independent

sources” (PCAOB 2012). However, while increased skepticism has been shown to decrease

auditors’ trust in evidence and/or clients and increase attention to evidence of fraud, auditors

often appear hesitant to adjust planned audit procedures in the face of increased risk. Glover et

al. (2003) and Zimbelman (1997) find that auditors are willing to increase audit hours in

response to increased fraud risk, but they are generally averse to planning to complete new audit

procedures. Similarly, Asare and Wright (2004) find that the outcomes of fraud risk assessments

do not result in the development of more effective audit plans. Thus, we anticipate that increased

professional skepticism will result in more planned audit hours, but may or may not result in

changes to audit procedures.

12

H3: Auditors who read a metaphor that primes skepticism (self-skeptical or client-skeptical) will propose more increases in audit hours relative to auditors who do not read a metaphor.

We do not make a directional prediction for the effects of skepticism on audit plans.

H4: Auditors who read a metaphor that primes skepticism (self-skeptical or client-skeptical) will not change planned audit procedures relative to auditors who do not read a metaphor. Generally, prior audit research related to professional skepticism has focused on auditors’

skepticism of audit evidence (i.e. client-skepticism). However, auditors are often overconfident

in their own knowledge and competence (Kennedy and Peecher 1997). Thus, Bell et al. (2005)

call for auditors to be skeptical not only of management and audit evidence but also of their own

judgment processes. Prior research of judgment under uncertainty has shown that decision

makers, including very experienced professionals, are consistently overconfident in their ability

to estimate outcomes or likelihoods. Overconfidence leads to inaccurate predictions, overly-

narrow confidence intervals, and non-calibrated judgments (i.e., confidence exceeds accuracy)

(Kahneman & Tversky 1973; Alpert & Raiffa 1982; Brenner and Kohler 1996). According to

Grenier (2011), reducing this overconfidence by promoting skepticism of one’s own judgment

capabilities allows auditors to recognize the potential imperfections of their judgments and

limitations of their abilities to evaluate evidence. We expect that recognition of one’s own

limitations will increase the likelihood that participants will seek the advice of a specialist risk

management partner.

H5: Auditors receiving a self-skeptical metaphor will be more likely to consult with a risk management partner than will auditors receiving a client-skeptical metaphor or no metaphor.

13

III. RESEARCH METHOD

Participants

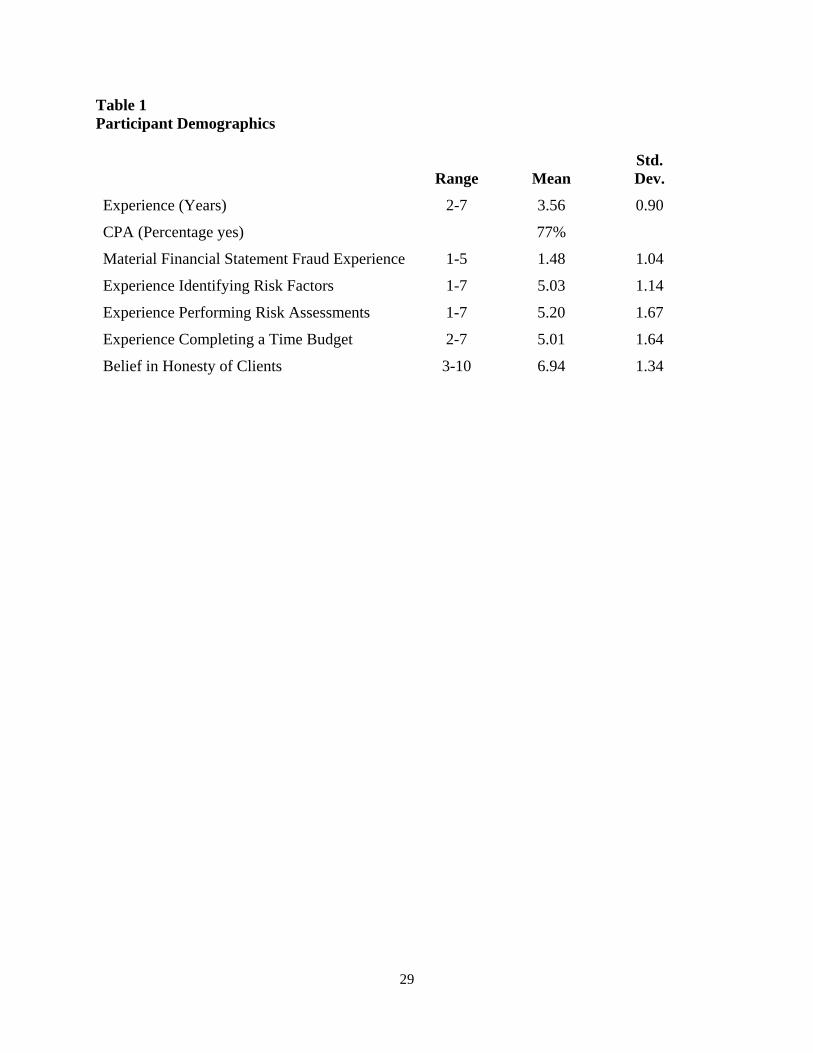

A total of 99 senior auditors, employed at two Big 4 public accounting firms, are

included in the sample.1 All of the participants were audit seniors with two to seven years of

experience (mean experience of 3.5 years). Subjects were randomly assigned to a treatment

condition, and the auditors participated in the experiment while attending firm training. The

majority of the auditors (76%) were CPAs. See Table 1 for demographic data.

Insert Table 1 about Here

Experimental Design and Procedure

The experiment is a 3 x 1 between-participants design. The manipulated factor is the

presence of a metaphor (self-skeptical metaphor, client-skeptical metaphor, or none). All

experimental materials were pilot tested with graduate accounting students prior to the

administration of the experiment.

The participants first read a story (or no story for the no-metaphor treatment) that

included a metaphor. The story was a separate task that was unrelated to the audit judgment

task, which followed in the second phase of the experiment. Participants were informed that they

would be asked questions related to the story at the end of the case in order to test their memory

for the story details. A memory question was asked as part of the manipulation checks. The

inclusion of the memory task was designed to promote careful reading of the metaphor by

participants. After reading the story, participants received brief background information for a

1 A total of 106 auditors participated in the study. The sample was reduced by three participants who did not complete the entire task and three participants who failed the manipulation checks. The statistical inferences are unaffected by the removal of the participants who failed manipulation checks.

14

hypothetical company and information related to the current audit engagement. The audit

evidence included a set of ratio comparisons and a client-provided explanation for the ratio

fluctuations. The evidence in the case materials was adapted from the experiment used in Libby

(1985) and Libby and Frederick (1990). After reviewing the available evidence, participants

complete a series of judgments including: evaluation of the risk of financial fraud, an assessment

of a client-provided explanation for ratio fluctuations, generation of alternative explanations for

ratio fluctuations, and determination of the nature and extent of recommended audit procedures.

The final phase of the experiment included manipulation checks, debriefing questions, and

demographic questions.

The data were collected on three separate occasions over a period of three months. The

materials were administered in a classroom setting, and the average time required to complete

the study was 25 minutes. Two authors administered the experiment to insure that participants

followed instructions and to verify random assignment.

Independent Variable

The independent variable is the presence and type of metaphor. We designed two types

of metaphors based upon existing theory. A “self-skeptical” metaphor focuses an auditor’s

attention on his or her own ability to evaluate evidence and make quality judgments. The short

story with the self-skeptical metaphor describes how experienced physicians often fail to notice

evidence of viral infections, which results in serious judgment errors. A “client-skeptical”

metaphor focuses attention on potential deceit by providers of information. The short story with

this form of metaphor describes how car salesmen often engage in self-serving behavior,

including lying to customers about the condition of a car to earn a commission.

15

Dependent Variables

We are interested in the effects of metaphors on the professional skepticism of auditors.

As Quadackers et al. (2013) point out, there is no single accepted judgment that best reflects

evidence of auditor professional skepticism. As a result, we employ multiple proxies for auditor

skeptical judgments. We employ six proxies derived from prior research related to professional

skepticism (McMillan and White 1993; Peecher 1996; Shaub 1996; Shaub and Lawrence 1996;

Zimbelman 1997; Choo and Tan 2000; Knapp and Knapp 2001; Rose 2007; Hurtt et al. 2012;

Quadackers et al. 2013). The proxies are:

(1) An assessment of fraud risk. Participants responded to the following scale:

Based on all the information you reviewed in this case, what is the overall risk that financial statement fraud is a primary cause of the ratio fluctuations?

(2) The number of fraud-based explanations for audit evidence. Participants listed up to ten

specific explanations that may have led to the change in the financial ratios, and for each

explanation indicated whether the explanation involved a normal operating issue that does not

involve an error (non-error), an unintentional error, or an intentional error (i.e., financial fraud).

(3) Likelihood that fraud-based explanations for audit evidence account for the ratio

fluctuations. Participants indicated the likelihood that each of the explanations they provided

accounts for most of the fluctuations in the ratios on a scale between 0 - 100 (0 = impossible; 100

= absolutely certain).

0 1 2 3 4 5 6 7 8 9 10 Very Moderate Very Low High

16

(4) Determination of audit hours. Participants were asked to revise the budget, if desired, for the

final revenue program. They indicated that percentage change that they desired (e.g., +5%) for

each category in the revenue program.

(5) Planning of audit procedures. Participants listed up to ten audit procedures that they

perceived were the most important for determining the cause of the ratio fluctuations.

(6) Assessment of the need for a risk management partner. Participants responded to the

following scale:

What is your opinion regarding the necessity of conferring with a risk management partner to finalize the audit plan for MedEquip. Risk management partners are very experienced with fraud risk situations. Given the need for efficient audits, risk management partners are not consulted on every engagement. They are only involved with an audit when the engagement team believes its audit program may not reduce the risk of detecting fraud to a tolerable level. Would you recommend consulting with a risk management partner in order to plan the current year’s audit for MedEquip?

IV. RESULTS

Manipulation Checks and Preliminary Tests

We tested the metaphor manipulations with the following questions (there was no

question for the participants in the no metaphor treatment condition):

For the story you read, what did the speaker essentially say? (please select one of the two choices below related to the story that you read)

Those who read the physician story made the following choice:

The senior physician essentially sent the following message to the junior surgeons:

5 4 3 2 1 0 1 2 3 4 5 Definitely Uncertain Definitely Would Not Would Consult Risk Consult Risk Management Partner Management

Partner

17

_______You are a trained professional with excellent judgment skills. When making complex judgments, particularly on issues for which you have little experience, do not be too confident in your ability to properly diagnose a rare, complex problem.

______You are a trained professional with excellent judgment skills. When making complex judgments, particularly on issues for which you have little experience, you should be very confident in your ability to properly diagnose a rare, complex problem.

Those who read the salesperson story made the following choice:

The senior salesperson essentially sent the following message to the junior salespersons:

_______Salespersons have a negative public reputation for being unscrupulous and self-serving; in truth, this reputation is totally inaccurate and undeserved.

_______Salespersons have a negative public reputation for being unscrupulous and self-serving; in truth, this reputation is totally accurate and deserved.

Three participants failed the metaphor treatment manipulation check, and these participants are

not included in the hypotheses tests.

We also conducted a preliminary MANOVA with the metaphor treatment as the

independent variable, and the dependent variables were the demographic factors listed in Table

1. This model is used to evaluate the effectiveness of participant randomization to treatment

conditions. None of the demographic variables were significant in the model, indicating that the

randomization procedure was effective with regard to participant demographics.

Test of Hypotheses

The first hypothesis posits that metaphors that prime client-skepticism or self-skepticism

will cause auditors to assess higher levels of risk of fraud. Hypothesis one is tested using an

ANOVA model with the assessment of fraud risk as the dependent variable and metaphor

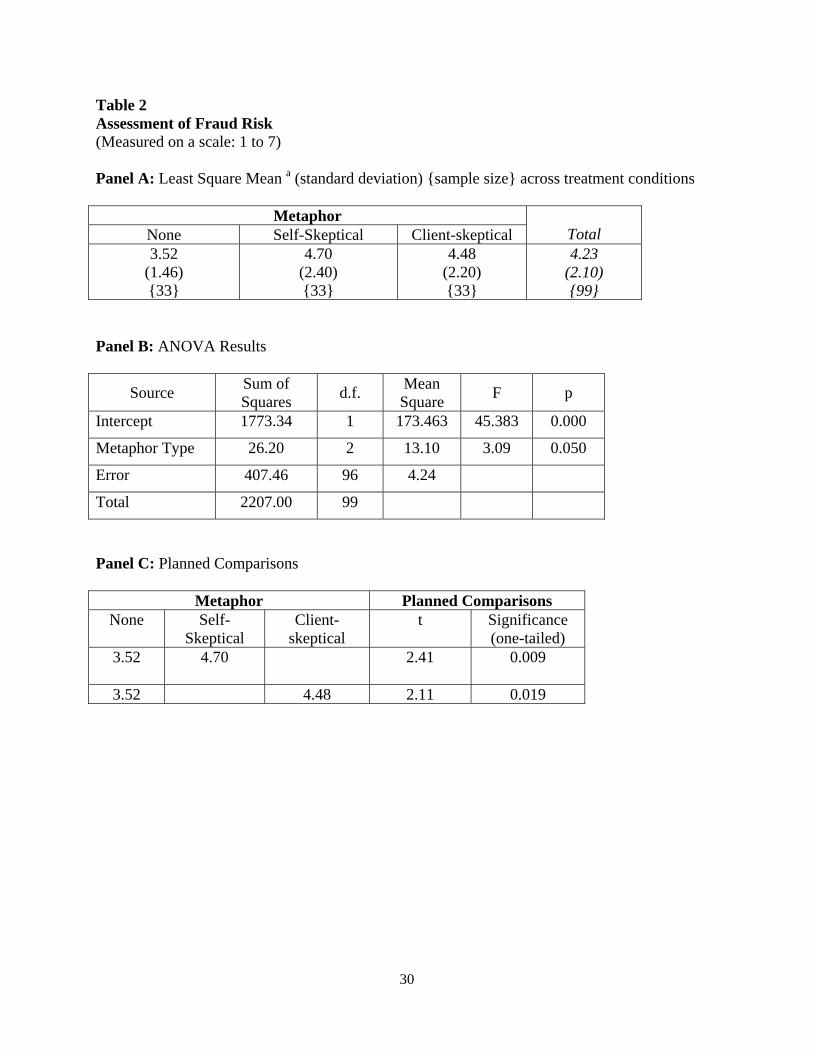

treatment as the independent variable.2 Results are presented in Table 2. Planned comparisons

that compare the no-metaphor treatment mean fraud risk assessment of 3.52 to the self-skeptical

2 None of the demographic factors were significant covariates in this or the following models used to test the hypotheses. Thus, no demographic covariates are included in the models.

18

risk assessment of 4.70 and to the client-skepticism risk assessment of 4.48 are statistically

significant (p = 0.009 and p = 0.019 respectively). Thus, H1 is supported.3

Insert Table 2 about Here

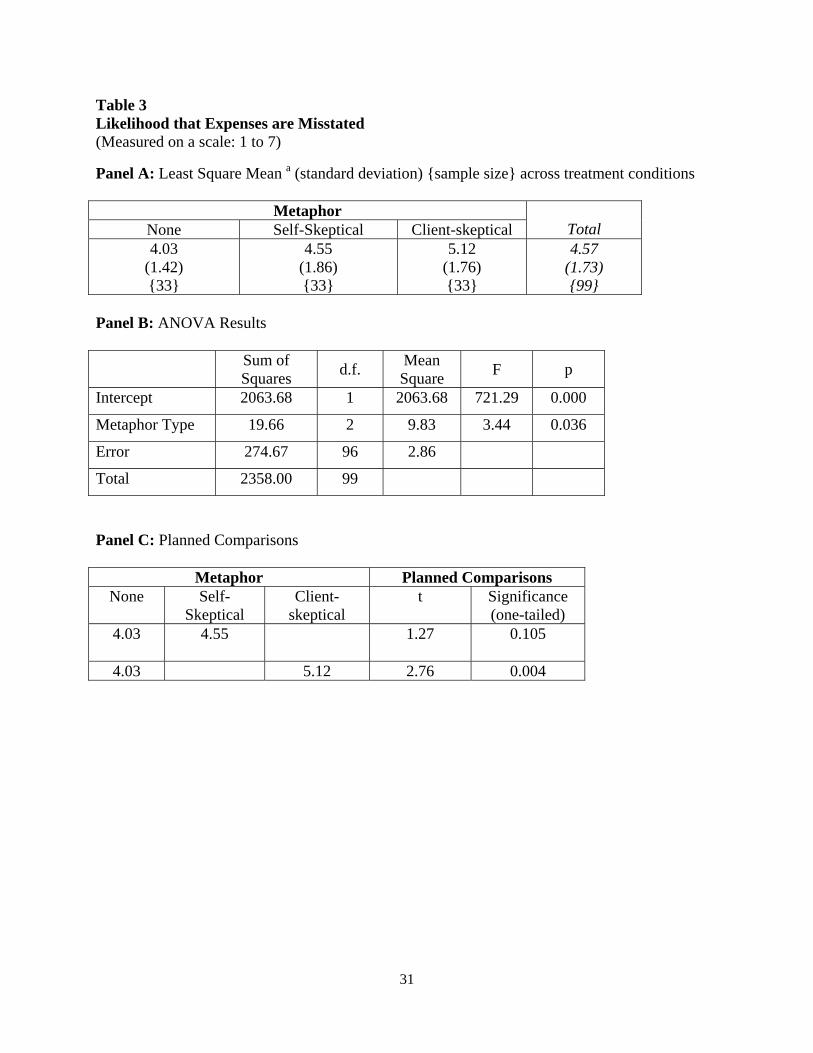

In addition to the hypothesized effects of metaphors on the assessment of fraud risk, we

also conduct a test of participants’ assessments of the likelihood that expenses are understated.

The ratios in the experimental case are derived from Libby (1985). Libby found that experts

perceived that underreporting of bad debt expense was the most likely error-related cause of the

fluctuations in ratios in our experimental task. As a result, we conduct a supplemental test to

determine whether inducing skepticism increases auditors’ assessments of the risk that expenses

have been misstated, as this would indicate that the participants who read the metaphors made

judgments about the ratios that are more similar to experts’ judgments than were the judgments

of participants who did not read a metaphor. The results are presented in Table 3, and planned

comparisons indicate that the client-skeptical metaphor resulted in significantly increased (p =

0.004) perceived likelihood that expenses are misstated (5.12), relative to the no-metaphor

condition (4.03). The self-skeptical metaphor (4.55) did not result in a statistically significant

increase in the perceived likelihood that expenses are misstated.

Insert Table 3 about Here

Hypothesis 2a proposes that auditors who read a metaphor that primes self-skepticism or

client skepticism will generate more intentional error explanations for ratio fluctuations relative

to auditors who do not read a metaphor. Results of an ANOVA model with the number of

intentional error explanations for ratio fluctuations as the dependent variable indicate that there

are no significant effects of either metaphor on the number of intentional error explanations (p >

3 We also confirmed the main effect of the metaphor treatments on fraud risk assessment and all other dependent variables with a single MANOVA. Results are all consistent with the individual ANOVA results.

19

0.45). Similarly, an additional test of the effects of the metaphors on the proportion of

intentional error explanations generated relative to the total number of explanations is not

significant (p > 0.80). The results do not support H2a.

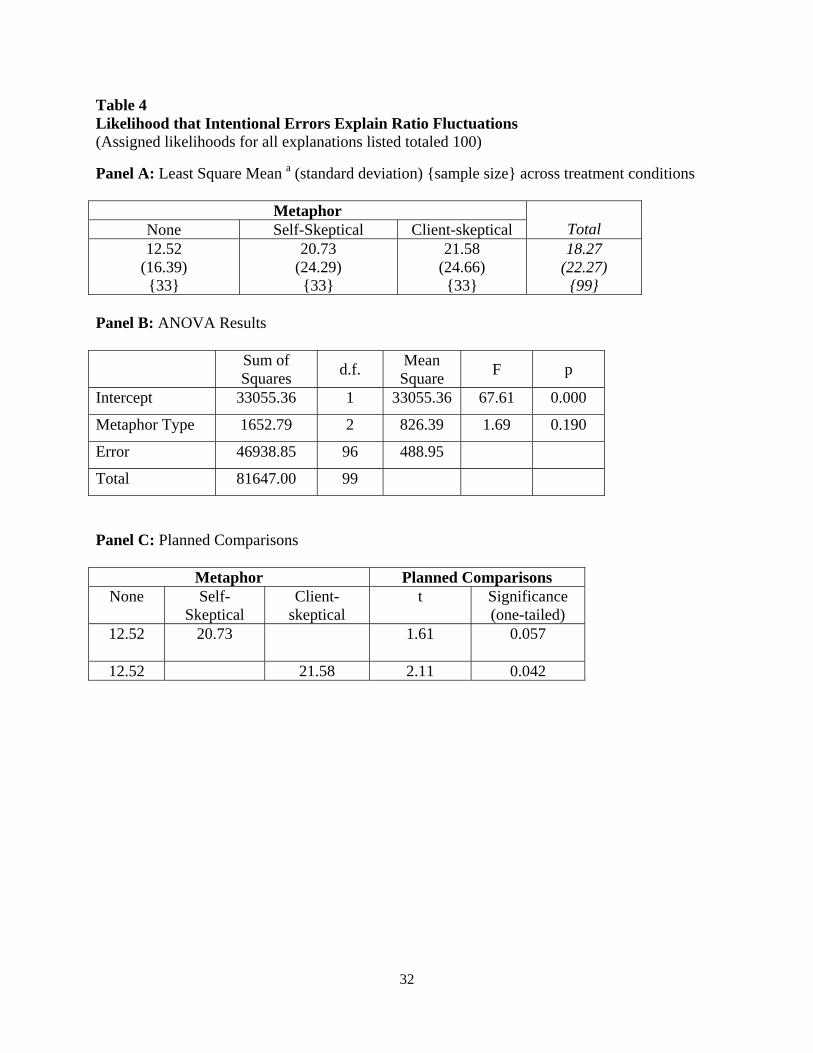

While Hypothesis 2a examined the number of intentional error explanations generated by

auditors, Hypothesis 2b focuses on auditor participants’ assessments of the likelihood that the

intentional error explanations they generated are likely to explain the ratio fluctuations. Results

are presented in Table 4. Auditors who read a metaphor that primes self-skepticism (mean =

20.73) or client skepticism (mean = 21.58) perceived that the intentional errors they generated

were more likely to cause the ratio fluctuations (p = 0.057 and p = 0.042) than were auditors who

did not read a metaphor (mean = 12.52). Results support Hypothesis 2b.

Insert Table 4 about Here

The third hypothesis examines whether metaphors that prime client or self-skepticism

cause auditors to increase planned audit hours. Participants had the opportunity to adjust audit

hours for six categories in the revenue program (test aged trial balance, confirmations, adequacy

of bad debt provision, cutoff tests, analytical procedures, and other). We evaluated all six

categories, and the metaphors significantly influenced the category for bad debt provision, but

none of the other categories. Participants reading the client-skeptical metaphor increased audit

hours related to the bad debt provision (mean = +5.39%) significantly more (p < 0.066) than did

participants in the no-metaphor treatment (mean = +3.0%) or self-skepticism metaphor treatment

(mean = +3.06%). Thus, we find evidence that metaphors that induce client skepticism cause

auditors to increase audit hours related to tests that are intended to detect the most likely

fraudulent causes of ratio fluctuations.

20

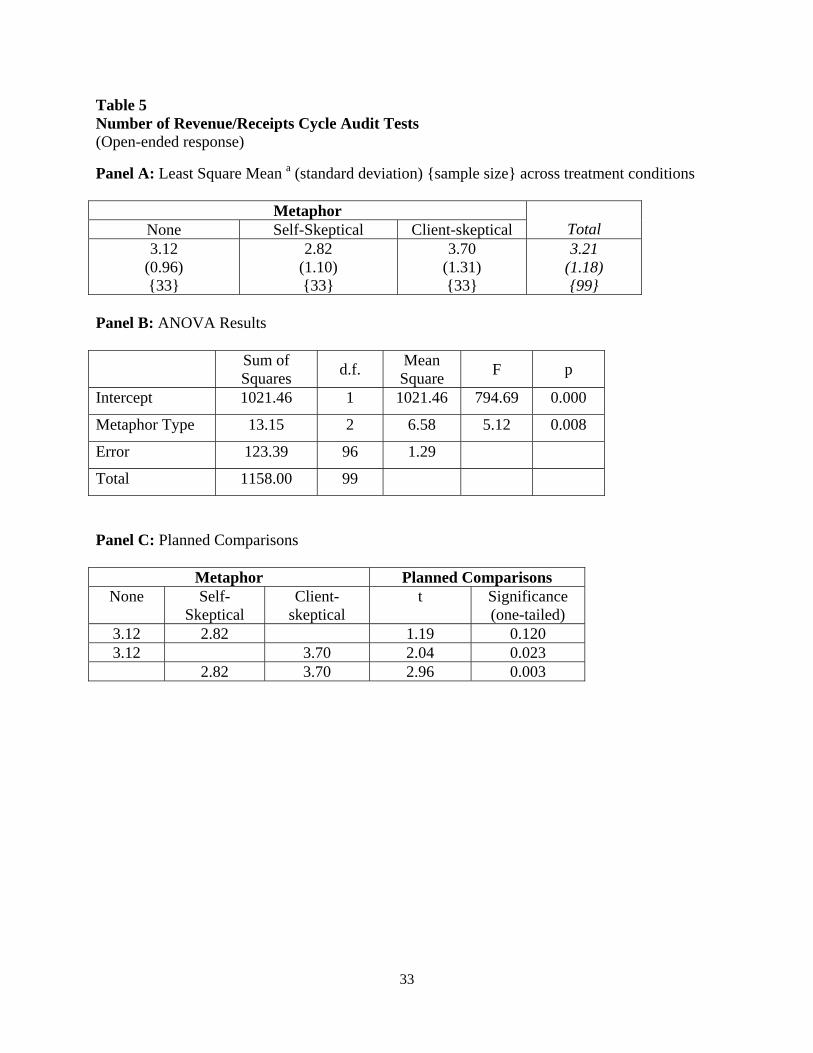

The next hypothesis (H4) is non-directional and examines whether metaphors influence

or do not influence audit plans. Participants listed up to ten audit procedures that they perceived

were the most important given the ratio fluctuations. We classified each audit procedure

according to audit cycle, and summed the number of procedures within each cycle. The only

cycle where the number of audit procedures differed across treatment conditions is the

revenue/receipts cycle. The results for tests of the number of audit procedures generated for the

revenue/receipts cycle are presented in Table 5. Similar to the results for audit hours, only the

client-skeptical metaphor caused changes in audit procedures. Planned comparisons indicate that

participants who read the client-skeptical metaphor generated more revenue/receipts cycle audit

procedures (mean = 3.70) than did participants in either the no-metaphor treatment (mean = 3.12,

difference significant at p = 0.02) or the self-skeptical metaphor (mean = 2.82, difference

significant at p = 0.003).

Insert Table 5 about Here

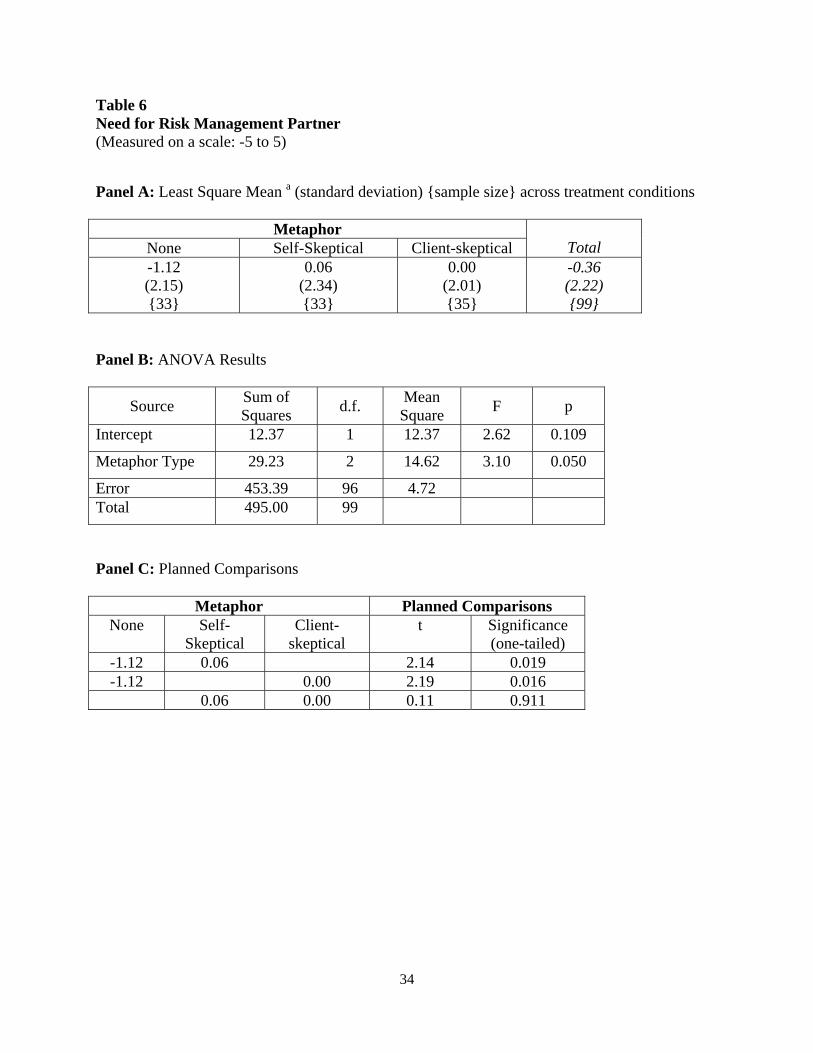

The final hypothesis (H5) posits that auditors who read a self-skeptical metaphor will be

more likely to consult with a risk management partner than will auditors receiving a client-

skeptical metaphor or no metaphor. Results for tests of H5 are presented in Table 6. Participants

reading either the self-skeptical metaphor (0.06) or the client-skeptical metaphor (0.00) both

perceived greater need (p = 0.019 and 0.016 respectively) for a risk management partner relative

participants who did not read a metaphor (-1.12). Results partially support hypothesis five.

Insert Table 6 about Here

Supplemental Tests

While metaphors are known to activate non-conscious changes to judgment processes

and activate mental models, it is also possible that the metaphors employed in this study alter

21

conscious perceptions of one’s own ability or beliefs about the honesty of specific clients. We

test for these possibilities with the following debriefing questions:

How confident are you in your ability to analyze complex, rare problems and arrive at sound and accurate judgments?

What do you believe about the honesty of most clients? (0 = Most clients are totally dishonest with me when I ask them audit‐related questions, regardless of the issue at hand, 5 = Most clients are selectively honest with me when I ask them audit‐related questions, depending on the issue at hand; 10 = Most clients are extremely honest with me when I ask them audit‐related questions, regardless of the issue at hand)

There are no differences across the three treatment conditions (p > 0.70) in beliefs about the

honesty of clients, indicating that the client-skeptical metaphor does not change perceptions of

the honesty of our audit participants’ clients. There is evidence, however, that the self-

skepticism metaphor decreased perceptions of one’s own abilities relative to the other treatments.

Participants in the self-skepticism condition rated their confidence in their judgment ability

(mean = 5.96) significantly lower (p = 0.08 and p = 0.04, two-tailed) than did participants in the

client-skepticism condition (mean = 6.88) or the no-metaphor condition (mean = 6.73).

V. DISCUSSION

We conducted an experiment with 99 senior auditors from two Big 4 audit firms in order

to investigate the potential for simple metaphors to promote professional skepticism and

facilitate skeptical judgment. Recent research of the effects of professional skepticism on auditor

0 1 2 3 4 5 6 7 8 9 10 Not Moderately Totally Confident Confident Confident at All

0 1 2 3 4 5 6 7 8 9 10 Totally Selectively Extremely Dishonest Honest Honest

22

judgment finds conflicting results regarding the effectiveness of client skepticism versus self-

skepticism. In addition, there is limited research that examines effective methods for promoting

professional skepticism throughout the audit process. Our research addresses the current

theoretical conflicts and practice needs.

The results from the experiment indicate that metaphors that prime client skepticism or

self-skepticism do cause auditors to increase their assessments of fraud risk, increase the

likelihood that auditors perceive that fraud-based explanations account for audit evidence, and

increase the perceived need for a risk management partner to evaluate the audit evidence. We

had also expected that the metaphors would increase the number of fraud-related explanations

generated for the audit evidence, but we did not find any effects of either metaphor on the

number of fraud-based explanations. While the auditor participants did not generate more fraud-

based explanations, they did perceive that explanations related to fraud were more likely to

explain ratio fluctuations.

Tests of the effects of the metaphors on planned audit hours and audit procedures indicate

that only the client-skepticism metaphor caused auditors to increase audit hours and change

planned audit procedures. These results are particularly important because they indicate that

client skepticism and self-skepticism have different effects on auditors’ skeptical judgments.

The results also indicate that priming skepticism, rather than instructing auditors to be skeptical,

produces different effects and potentially more widespread effects on auditor judgments.

Finally, many prior researchers have discussed the problem that interventions designed to

improve fraud detection change risk assessments but do not result in changes to the actual audit

(e.g., Bloomfield 1995; Zimbelman 1997). We find that true primes have the capacity to change

23

auditors’ assessments of fraud risk and audit plans (i.e., hours, procedures, and need for risk

management partners).

While not hypothesized, we also find evidence that promoting professional skepticism

with metaphors caused auditor participants to increase their focus on the understatement of

expenses and particularly on provisions for bad debt expense. Further, evaluation of audit plan

changes reveals increased testing of the revenue and receipts cycle (which is the cycle related to

bad debt expenses) for readers of the client-skeptical metaphor. Prior research that employed the

same three ratio fluctuations found that expert auditors rated the understatement of bad debt

expense as the most likely error-related cause of the changes in ratios (Libby 1985). These

findings suggest that when skepticism is primed through non-conscious methods such as

metaphors, auditors’ focus more of their attention on the most likely fraud schemes and redirect

more audit effort towards detecting the most likely frauds. Based upon these and our other

results, metaphors and other forms of non-conscious priming appear to represent powerful and

effective tools for improving auditors’ professional skepticism and skeptical judgments.

24

REFERENCES

Alpert, M., and H. Raiffa. 1982. A progress report on the training of probability assessors. In D. Kahneman, P. Slovic, and A. Tversky (Eds.), Judgment under uncertainty: Heuristics and biases. Cambridge: Cambridge University Press.

American Institute of Certified Public Accountants (AICPA). 2002. Consideration of Fraud in a

Financial Statement Audit. Statement on Auditing Standards No. 99. New York, NY: AICPA.

Anderson, S., and J. Wolfe. 2002. A perspective on audit malpractice claims. Journal of

Accountancy 194 (3): 59–66. Asare, K. and A. Wright. 2004. The effectiveness of alternative risk assessment and program

planning tools in a fraud setting. Contemporary Accounting Research 21 (2): 325–352. Bargh, J. A. and T. L. Chartrand. 1999. The unbearable automaticity of being. American

Psychologist 54(7): 462 - 479. Bargh, J. A., P. M. Gollwitzer, A. Lee-Chai, K. Barndollar and R. Troetschel. 2001. The

automated will: Nonconscious activation and pursuit of behavioral goals. Journal of Personality and Social Psychology 81(6): 1014 - 1027.

Beasley, M. S., J. V. Carcello and D. R. Hermanson. 2001. Top 10 audit deficiencies. Journal of

Accountancy 191(4): 63 - 66. Bell, T. B., M. E. Peecher and I. Solomon. 2005. The 21st Century Public Company Audit:

Conceptual Elements of KPMG's Global Audit Methodology. U.S.A., KPMG International.

Benston, G.J., and A.L. Hartgraves. 2002. Enron: What happened and what we can learn from it.

Journal of Accounting and Public Policy: 105-127 Bloomfield, R. 1995. Strategic dependence and inherent risk assessments. The Accounting

Review January: 71-90. Boroditsky, L. 2000. Metaphoric structuring: Understanding time through spatial metaphors.

Cognition 75: 1–28. Boroditsky, L., and M. Ramscar. 2002. The roles of body and mind in abstract thought.

Psychological Science 13: 185–188 Brenner, L. A., and D. J. Koehler. 1996. Overconfidence in Probability and Frequency

Judgments: A Critical Examination. Organizational Behavior and Human Decision Processes 65(3): 212 – 219.

25

Center for Audit Quality (CAQ). 2010. Deterring and Detecting Financial Reporting Fraud: A Platform for Action. Washington, D.C.: CAQ.

Choo, F., and K. Tan. 2000. Instruction, skepticism, and accounting students’ ability to detect

frauds in auditing. Journal of Business Education Fall: 72-87. Galinsky, A. D., and Glucksberg, S. 2000. Inhibition of the literal: metaphors and idioms as

judgmental primes. Social Cognition 18: 35–54. Gibbs, R. 1992. Categorization and metaphor understanding. Psychological Review 99: 572–577. Glover, M., D. F. Prawitt, and J. J. Schultz. 2003. A test of changes in auditors’ fraud-related

planning judgments since the issuance of SAS No. 82. Auditing: A Journal of Practice & Theory 22 (2): 237–251.

Goldfarb, L., D. Aisenberg, and A. Henik. 2011. Think the thought, walk the walk – Social

priming reduces the Stroop effect. Cognition 118 (2): 193-200. Grenier, J. 2011. Encouraging professional skepticism in the industry specialization era: A dual-

process model and an experimental test. Working paper. Miami University. Hilton, J., S. Fein, and D. Miller. 1993. Suspicion and dispositional inference. Personality and

Social Psychology Bulletin 19: 501-512. Hurtt, R.K., M. Eining, and D. Plumlee. 2012. An Experimental Examination of Professional

Skepticism. Working paper. Baylor University and University of Utah. Kahneman, D., and Tversky, A. 1973. On the psychology of prediction. Psychological Review

80: 237–251. Kennedy, S.J., and M. Peecher. 1997. Judging Auditors Technical Knowledge. Journal of

Accounting Research 35 (2): 279–293. Knapp, C.A., and M.C. Knapp. 2001. The effects of experience and explicit fraud risk

assessment in detecting fraud with analytical procedures. Accounting, Organizations and Society 26: 25-37.

KPMG. 2011. Elevating Professional Judgment in Accounting and Auditing: The KPMG

Professional Judgment Framework. Lakoff, G. and M. Johnson. 1980. Conceptual metaphor in everyday language. The Journal of

Philosophy, 77(8), 453-486. Lakoff, G. and M. Johnson. 1999. Philosophy in the Flesh. New York: Basic Books.

26

Libby, R. 1985. Availability and the generation of hypotheses in analytical review. Journal of Accounting Research (Autumn): 648–667.

Libby, R., and D. M. Frederick. 1990. Experience and the ability to explain audit findings.

Journal of Accounting Research 28: 348-67. McMillan, J.J., and R.A. White. 1993. Auditors' belief revisions and evidence search: The effect

of hypothesis frame, confirmation and professional skepticism. The Accounting Review 68: 443-465.

Nelson, M. W. 2009. A model and literature review of professional skepticism in auditing.

Auditing: A Journal of Practice and Theory 28 (2): 1-34. Peecher, M. 1996. The influence of auditors' justification processes on their decisions: A

cognitive model and experimental evidence. Journal of Accounting Research 34(1): 125 - 141.

Phillips, F. 1999. Auditor attention to and judgments of aggressive financial reporting. Journal of

Accounting Research 37: 167-189. Public Company Accounting Oversight Board (PCAOB). 2008. Report on the PCAOB’s 2004,

2005, 2006, and 2007 Inspections of Domestic Annually Inspected Firms. Release No. 2008-008. Washington, D.C.: PCAOB.

Public Company Accounting Oversight Board (PCAOB). 2012. Staff Audit Practice Alert No. 10: Maintaining and Applying Professional Skepticism in Audits. Washington, D.C.: PCAOB.

Quadackers, L., T. Groot, and A. Wright. 2013. Auditors’ professional skepticism: Neutrality

versus presumptive doubt. Contemporary Accounting Research. In press. Rose, J. 2007. Attention to aggressive and potentially fraudulent reporting: Effects of

experience and trust. Behavioral Research in Accounting 19: 215-230. Schul, Y., E. Burnstein, and A. Bardi. 1996. Dealing with deceptions that are difficult to detect:

Encoding and judgment as a function of preparing to receive invalid information. Journal of Experimental Social Psychology 32: 228-253.

Shaub, M.K. 1996. Trust and suspicion: The effects of situational and dispositional factors on

auditors’ trust of clients. Behavioral Research in Accounting 8: 154-174. Shaub, M.K., and J.E. Lawrence. 1996. Ethics, experience, and professional skepticism: A

situational analysis. Behavioral Research in Accounting. Supplement: 124-157.

27

Slobin, D. I. 2003. Language and thought online: cognitive consequences of linguistic relativity. In D. Gentner & S. Goldin-Meadow (Eds.), Language in mind: Advances in the study of language and thought (pp. 157–192). Cambridge, MA: MIT Press.

Thibodeau, P., and L. Boroditsky. 2011. Metaphors we think with: The role of metaphor in

reasoning. PLoS ONE 6(2). Young J. 2001. Risk(ing) metaphors. Critical Perspectives on Accounting 12: 607–25. Zimbelman, M. 1997. The effects of SAS No. 82 on auditors’ attention to fraud risk factors and

audit planning decisions. Journal of Accounting Research 35: 75-94.

28

Appendix A Independent Variable Manipulation

Internally Focused Skepticism

A well-known senior physician gave a seminar to a large group of younger practicing physicians from around the country. The senior physician was speaking about his expertise related to viruses. At one point in the seminar, the physician stated “Many deadly viruses quietly spread throughout the body and are nearly impossible to detect, even by the most skilled doctors. No matter how knowledgeable one is about viruses and how much experience one has in the field, many viruses are extremely difficult to detect. Even minor viral infections can spread and cause serious harm. I have found that many of the brightest and most experienced physicians regularly miss evidence of viral infections and then make very serious judgment errors that result in terrible harm. We tend to be far too confident in our own ability to detect viruses and other problems in the body.” The sage physician warned the younger physicians to always be aware of their human limitations with regard to analyzing complex problems, particularly rare viruses where there are very few occurrences, because being over-confident during such a diagnosis can lead to deadly consequences for the patient. “Always be circumspect about your own capabilities”, warned the senior physician, “It is okay, even healthy, to question your own capabilities.” Externally Focused Skepticism A highly successful car salesman gave a seminar to a large group of less experienced used car salespeople from around the country. The salesman was speaking about his views on how to be successful selling used cars. At one point in the seminar, the salesman stated “Car salespeople have become famous for telling colossal lies and for engaging in unscrupulous behavior. Most buyers believe that salespeople will do anything to obscure a car’s faults and mislead them. The public also believes that salespeople regularly sell cars that break down and leave the drivers stranded.” “To be honest”, he went on, “there is a lot of truth to these negative perceptions. Let’s be honest with ourselves…our motives are purely self-serving in nature. What we need to do is buy a car at a low price and sell it at a high price. This is how we and our dealerships make a living. Since used cars are sold ‘as is’, once the customer walks out of the door, do we really care whether the car runs well or not? Personally, I don’t give a flip, and I suggest that you should not either. Our job is not to make friends with the buyers, our job is to sell, move cars off the lot, and make money. If during the sales process this means that we need to stretch the truth to make the sale, well, buyer beware!”

29

Table 1 Participant Demographics

Range Mean Std. Dev.

Experience (Years) 2-7 3.56 0.90

CPA (Percentage yes) 77%

Material Financial Statement Fraud Experience 1-5 1.48 1.04

Experience Identifying Risk Factors 1-7 5.03 1.14

Experience Performing Risk Assessments 1-7 5.20 1.67

Experience Completing a Time Budget 2-7 5.01 1.64

Belief in Honesty of Clients 3-10 6.94 1.34

30

Table 2 Assessment of Fraud Risk (Measured on a scale: 1 to 7) Panel A: Least Square Mean a (standard deviation) {sample size} across treatment conditions

Metaphor Total None Self-Skeptical Client-skeptical

3.52 (1.46) {33}

4.70 (2.40) {33}

4.48 (2.20) {33}

4.23 (2.10) {99}

Panel B: ANOVA Results

Source Sum of Squares

d.f. Mean Square

F p

Intercept 1773.34 1 173.463 45.383 0.000

Metaphor Type 26.20 2 13.10 3.09 0.050

Error 407.46 96 4.24

Total 2207.00 99

Panel C: Planned Comparisons

Metaphor Planned Comparisons None Self-

Skeptical Client-

skeptical t Significance

(one-tailed) 3.52

4.70

2.41 0.009

3.52 4.48 2.11 0.019

31

Table 3 Likelihood that Expenses are Misstated (Measured on a scale: 1 to 7)

Panel A: Least Square Mean a (standard deviation) {sample size} across treatment conditions

Metaphor Total None Self-Skeptical Client-skeptical

4.03 (1.42) {33}

4.55 (1.86) {33}

5.12 (1.76) {33}

4.57 (1.73) {99}

Panel B: ANOVA Results

Sum of Squares

d.f. Mean Square

F p

Intercept 2063.68 1 2063.68 721.29 0.000

Metaphor Type 19.66 2 9.83 3.44 0.036

Error 274.67 96 2.86

Total 2358.00 99

Panel C: Planned Comparisons

Metaphor Planned Comparisons None Self-

Skeptical Client-

skeptical t Significance

(one-tailed) 4.03

4.55

1.27 0.105

4.03 5.12 2.76 0.004

32

Table 4 Likelihood that Intentional Errors Explain Ratio Fluctuations (Assigned likelihoods for all explanations listed totaled 100)

Panel A: Least Square Mean a (standard deviation) {sample size} across treatment conditions

Metaphor Total None Self-Skeptical Client-skeptical

12.52 (16.39) {33}

20.73 (24.29) {33}

21.58 (24.66) {33}

18.27 (22.27)

{99} Panel B: ANOVA Results

Sum of Squares

d.f. Mean Square

F p

Intercept 33055.36 1 33055.36 67.61 0.000

Metaphor Type 1652.79 2 826.39 1.69 0.190

Error 46938.85 96 488.95

Total 81647.00 99

Panel C: Planned Comparisons

Metaphor Planned Comparisons None Self-

Skeptical Client-

skeptical t Significance

(one-tailed) 12.52

20.73

1.61 0.057

12.52 21.58 2.11 0.042

33

Table 5 Number of Revenue/Receipts Cycle Audit Tests (Open-ended response)

Panel A: Least Square Mean a (standard deviation) {sample size} across treatment conditions

Metaphor Total None Self-Skeptical Client-skeptical

3.12 (0.96) {33}

2.82 (1.10) {33}

3.70 (1.31) {33}

3.21 (1.18) {99}

Panel B: ANOVA Results

Sum of Squares

d.f. Mean Square

F p

Intercept 1021.46 1 1021.46 794.69 0.000

Metaphor Type 13.15 2 6.58 5.12 0.008

Error 123.39 96 1.29

Total 1158.00 99

Panel C: Planned Comparisons

Metaphor Planned Comparisons None Self-

Skeptical Client-

skeptical t Significance

(one-tailed) 3.12 2.82 1.19 0.120 3.12 3.70 2.04 0.023

2.82 3.70 2.96 0.003

34

Table 6 Need for Risk Management Partner (Measured on a scale: -5 to 5)

Panel A: Least Square Mean a (standard deviation) {sample size} across treatment conditions

Metaphor Total None Self-Skeptical Client-skeptical

-1.12 (2.15) {33}

0.06 (2.34) {33}

0.00 (2.01) {35}

-0.36 (2.22) {99}

Panel B: ANOVA Results

Source Sum of Squares

d.f. Mean Square

F p

Intercept 12.37 1 12.37 2.62 0.109

Metaphor Type 29.23 2 14.62 3.10 0.050

Error 453.39 96 4.72 Total 495.00 99

Panel C: Planned Comparisons

Metaphor Planned Comparisons None Self-

Skeptical Client-

skeptical t Significance

(one-tailed) -1.12 0.06 2.14 0.019 -1.12 0.00 2.19 0.016

0.06 0.00 0.11 0.911