Embed Size (px)

Citation preview

Microfinance and RuralDevelopment

There have been government policies on the role of microfi-nance in the rural development process for more than fourdecades. In the 1960s and 1970s, the policies focused on

the provision of agricultural credit as a necessary support to theintroduction of new, more productive agricultural technologies

A Long-Term Perspective

Henk A. J. Moll

Abstract: The long-term perspective on microfinance starts with a discussion of

three central issues: first, views and policies, with two opposing views: “credit for

target group” and “pushing the financial frontier”; second, the performance of

microfinance institutions measured via two objectives: outreach and financial

sustainability; third, microfinance and rural development. This latter issue is

approached through analyses of the effects of financial services on rural house-

holds and analyses of long term national financial development. Both micro and

macro studies show positive effects of an expansion of savings and lending services,

financial deepening. The negative side of financial deepening, the apparently

unavoidable occurrence of bank insolvancies, is also reviewed. The concluding

section argues that the microfinance sector should be guided by “stability and

expansion”: stability to withstand shocks and to maintain the relationships estab-

lished between rural households and microfinance institutions, and expansion to

include more people within the financial frontier.

Journal of Microf inance

Volume 7 Number 214

that would simultaneously improve farmers’ incomes and feed thenation. Later, the focus broadened to include credit provision tothe rural population engaged in other enterprises, such as trade,handicrafts, and small-scale industry. Presently the internationaldevelopment agenda is dominated by the Millennium Goals, withpoverty eradication heading the list of goals, and with microfi-nance firmly linked to this goal.

The implementation of rural credit policies through financialinstitutions has been debated internationally. What triggered thisdebate was the publication of the “Spring Review,” an evaluationof small-farmer credit programs by USAID in the 1970s (Donald,1976), which made available world wide experience on the achieve-ments and failings of credit programs supported by governmentsand donors. In the 1970s, the discussion shifted from “lack of cap-ital” and consequently “the need for cheap credit,” to “cost-coveringinterest rates” that would enable financial institutions to continueto operate (Adams & Von Pischke, 1992). Later, the discussionwidened to include imperfect information as one of the distinctivecharacteristics of rural credit markets (Hoff & Stiglitz, 1993) thatleads to insight into the screening, monitoring, and enforcementproblems that rural microfinance institutions face. Presently we seea sort of consensus about the operations of microfinance institutions:they should strive towards both outreach and financial sustainability.

The debate on microfinance largely assumes a micro perspec-tive, with a short- to medium-term horizon. From this perspective,assumptions about the behavior of farmers, the rural population,or the poor, and about the constraints these groups face lead topolicies to be implemented by financial institutions. These institu-tions measure the effects of access to finance on their target groupafter a couple of years. Finally, the objective to become financiallysustainable is to be reached in a few years’ time. Long-term analysesof the role of microfinance institutions in rural development arescarce. Mellor (1966) and Timmer (1988) deal in macro terms with

Henk A. J. Moll is associate professor in the Development Economics Group of WageningenUniversity, the Netherlands. Email: [email protected]

Microf inance and Rura l Development

Volume 7 Number 2 15

the role of the agricultural sector in national development and dis-cuss the transfer of people and capital from the agricultural (orrural) sector to the services and industrial sectors in the urbanareas. They do not, however, discuss the mechanisms for such atransfer of capital. McKinnon (1973) and Shaw (1973) deal explic-itly with the development of the financial sector within economicdevelopment and plead for financial liberalization to enable sav-ings to be mobilized, followed by an efficient banking system thatlends to investors with expected high return investments. Morerecently, financial development and the links with economicgrowth and with poverty reduction have been discussed by Kingand Levine (1993) and Li, Squire, and Zou (1998). Though theseauthors make no distinction between the rural and urban sectors,their analyses are relevant for the rural sector too.

The three issues introduced above, views and policies regard-ing microfinance; the operations of microfinance institutions; andthe position of microfinance in rural development, are linked. Inthis article I will discuss these issues and then draw overall conclu-sions regarding the long-term role of microfinance institutions inrural areas.

The reason for focusing on rural microfinance is because thisdiffers from microfinance in urban areas in several ways. The mostobvious difference is that the dominant economic enterprise inrural areas is agriculture, with known seasonality and unpre-dictable climatic conditions. This results in similar cash flowrequirements for many households and in co-variant risk.Additionally, in many rural areas the population is widely dis-persed, which means high transaction costs for clients and possiblylow volumes of services per microfinance location. These aspectsrequire specific attention from microfinance institutions operatingin rural areas, in addition to the general microfinance problem ofhandling financial transactions for the small sums low-incomeclients require.

Views and Policies

Nowadays microfinance enjoys widespread support from govern-ments, development agencies and nongovernmental organizations.The reasons for this support are, however, diverse, and the termmicrofinance is linked with very different views and assumptionsabout the relationship between finance and development. Variousauthors have attempted to classify these views. Krahnen andSchmidt (1994), for example, distinguish four views by tracingdevelopment thinking from the 1950s: capital as the engine foreconomic growth, financing specific target groups, the focus onfinancial systems, and, from the 1990s onwards, the insights fromthe new institutional economics emphasizing the dominant role ofinstitutions in development and with specific views on the pecu-liarities of financial institutions. Robinson (2001) distinguishestwo approaches to microfinance: the poverty lending approach andthe financial system approach. Different views or approaches haveconsequences for the policies shaping the environment of micro-finance institutions, the financial services provided, and microfi-nance institutions themselves. Below I will discuss two opposingviews and their resulting policies. The consequences for microfi-nance institutions and for the role of microfinance in rural areaswill be discussed in the sections that follow.

The two opposing views are: (a) credit for target group and (b)pushing the financial frontier. Based on Robinson’s poverty lendingapproach, the first view is defined in a wider sense, with the poorbeing replaced by any target group. The phrasing of the secondview echoes Von Pischke (1991), who refers to the financial fron-tier as the dividing line between the established formal financialinstitutions with their large-scale business and private clients, andthe majority of the rural population without access to formalfinance.

Credit for target group is the oldest view and can be summa-rized as follows: A specified group of people lacks the capital toundertake certain enterprises that would lead to development. Thegroup of people and their enterprises can be specified to a greateror lesser degree: small farmers, fishermen, market women, or

Journal of Microf inance

Volume 7 Number 216

Microf inance and Rura l Development

Volume 7 Number 2

small-scale entrepreneurs with their respective enterprises in agri-culture, fishing, trade, and industry. The specification of develop-ment too may differ: improved health, food security, povertyreduction, or improvement in general welfare. The perspective onthe financial environment of the specified group is limited: theonly way the target group can access credit is through privatemoneylenders whose interest rates are unacceptably high andwould nullify any positive effect of the credit.

It was this view that led many governments in the 1960s and1970s to provide targeted credit with or without support fromdonors; for example, to enable small farmers to use modern pro-duction technologies, such as hybrid seeds or imported dairy cows.This credit would increase their incomes and provide enough andsufficiently diversified food for the domestic market. The credit fortarget group view is still widespread and nowadays is generally tar-geted at “the poor,” in line with the international attention forpoverty eradication. The micro-credit summit (not microfinancesummit) held in Washington in 1997, for example, advocated pro-viding credit to the world’s poor to enable them to shed theirpoverty. Barrett (2003) mentions targeted microfinance (togetherwith land reform, targeted school meals programs, and subsidiesfor agricultural inputs) as one of the “cargo net policies” that canlift people out of poverty. In short, the credit for target group viewis based on the following two central assumptions:

1. The factor constraining development is capital.2. The target group is unable to mobilize this capital under

acceptable conditions.

The policy implication of these assumptions is straight-forward: lend capital to the target group.

The pushing the financial frontier view developed in the 1970sto the 1990s from an increasing understanding of the financialcapabilities of low-income rural households and the existing formaland informal financial institutions in rural financial markets.According to this view, rural households are economic units thatmake daily decisions about production, consumption, and the

17

resource base under conditions that are characterised by (a) sea-sonality that rules rural economic life, (b) uncertainty about futureproduction and consumption requirements, and (c) income levelsthat are generally not far above subsistence. The decisions arereflected internally in the size and composition of the household’sassets and in the enterprise choice, and externally in the house-hold’s participation as buyer and seller of financial assets in ruralfinancial markets (Moll, 1989).

This sharper focus on rural households was accompanied byinsight into the rural financial markets (Von Pischke et al., 1983),defined as the totality of relationships between buyers and sellersof financial assets who are active in rural economies. Rural finan-cial markets are characterized by having a range of institutions thatare usually divided into formal institutions, such as state or privatebanks, semiformal institutions such as cooperatives and NGOsinvolved in financial services, and informal institutions, ranging fromprivate moneylenders and traders to relatives and friends and groups.Despite the wide range of institutions present, individual rural house-holds generally have access to only some of the institutions and theproducts these institutions provide, as rural financial markets arehighly segmented (Moll, Ruben, Mol & Sanders, 2000).

New, comprehensive explanations for the observed segmenta-tion in rural financial markets have been offered by Bell (1988),Hoff and Stiglitz (1993), and others. These focus on the informa-tion asymmetry between lender and borrower as a central issue incredit provision, with as consequences the absence of credit rela-tionships where information on borrowers was perceived as insuf-ficient, and the failure of government-supported financialinstitutions if these information asymmetries were neglected.

The insights gained firstly contradict the two assumptions ofthe credit for target group view: (a) low-income rural householdscan and do save both in kind and in financial assets through a vari-ety of informal arrangements, and (b) the existing savings capacityin rural financial markets refutes the assumption that capital assuch is the major factor constraining rural development. Secondly,the insights into rural households and the rural financial market

Journal of Microf inance

Volume 7 Number 218

Microf inance and Rura l Development

Volume 7 Number 2

institutions revealed the limitations of the informal financial insti-tutions in mobilizing and storing savings, dealing with co-variantrisk, and transforming small, short-term savings into larger loansof medium-term duration. In this way, these insights revealed anunfulfilled demand for financial services that formal institutionscan address more readily than informal ones:

1. Mobilizing savings together with providing unrestrictedwithdrawal.

2. Short-term lending for working capital, as and whenrequired.

3. Medium- and long-term lending for investments.

The overall conclusion was that rural households would benefitfrom the presence of formal financial institutions with servicesadjusted to their capabilities. The policy implications are twofold:(a) government policy attention for rural finance was vindicated,though not policies with the aim to provide capital, but policies toenable formal financial institutions to intermediate between saversand borrowers; and (b) policies should encourage financial institu-tions to participate in pushing the financial frontier to includenew, low-income rural households as their clients, by tackling theinformation problem through innovative screening, monitoring,and enforcement procedures.

The Performance of Microfinance Institutions

The views and policies described above translate into the operationsof microfinance institutions and thereafter into the assessment oftheir performance. The credit for target group view results in micro-finance institutions that focus on providing loans, generally in spec-ified quantities and possibly provided in kind and earmarked for aspecific enterprise. These loans are provided to the defined targetgroup, to be used to attain the specified development goals. Theloans are generally at subsidized interest rates, as the target group ispoor—in whatever terms poverty is defined. The assessment of theperformance initially focuses on the number of loans provided, orthe number of people who have received one or more loans,

19

because this number of people is assumed to reach the anticipateddevelopment goal. The latter assumption can be tested throughimpact assessment,1 for which elaborate methodologies have beendeveloped. This operational approach can be summed up as “supplyleading finance.” Adams and Von Pischke (1992) are among thosewho have analyzed this approach in detail and shown that govern-ment interference adversely influences lending and causes the basiceconomics of banking to be bypassed. The consequences of thesefailings have been that microfinance institutions incurred lossesand sooner or later ceased operating—but not before destroyingrepayment morale in the population and giving bank staff wrongideas about banking. Most importantly, the target group was onlypartly and temporarily reached, and after the demise of the finan-cial institution was again left without financial services.

Two developments in the 1980s and 1990s changed the situa-tion. The emerging pushing the financial frontier view showed theimportance of permanent financial relationships for rural house-holds, and thereby the permanence of financial institutions. The“cost-covering interest rates” for microfinance institutions (insteadof the subsidized interest rates) advocated by Adams and VonPischke were a major step towards achieving such permanence.Financial sustainability became part of the microfinance discussionand Yaron (1992) made this operational by devising the subsidydependence index with two levels of achievement: operational sus-tainability and financial sustainability, whereby the latter indicatesthe total independence from subsidies. New microfinance institu-tions took on board the increased insight and the attention forfinancial sustainability and used new approaches to reach peoplewho had previously lacked access to institutional financial services.

The emergence and expansion of microfinance institutions wasgreatly facilitated by a second development: financial liberaliza-tion. This meant a reduced role for government in the allocation ofcapital, less interference with banking, and thus new opportunitiesfor banks and microfinance institutions to engage in the centralfunction of financial institutions: intermediating between saversand borrowers. Less interference with banking generally meant the

Journal of Microf inance

Volume 7 Number 220

Microf inance and Rura l Development

Volume 7 Number 2

abandonment of interest rate control on savings and credit, andthat enabled the microfinance institutions to pay attention tofinancial objectives.

By the end of the 1980s, case studies had become available onmicrofinance institutions that had succeeded in reaching low-income households with savings and credit services (Moll, 1989;Patten & Rosengard, 1991; Yaron, 1992) and that showed a widevariety of organizational structures and operations. These casestudies provided the material for comparative analyses and theemergence of “best practices” in microfinance literature. These bestpractices offer a wealth of experience, but as the description of thebackground that shaped the specific institutions is generally lim-ited, these best practices need to be tested, assessed, and adapted tothe individual circumstances.

Presently there seems to be consensus on at least the objec-tives of microfinance institutions: outreach towards low-incomepeople and financial sustainability. Given these two objectives,microfinance institutions must deal with two central issues intheir day-to-day operations:

(a) the information issue: how to establish borrowers’ abilityand willingness to repay; and

(b) the cost issue: how to handle cost-effectively the smallfinancial transactions with a short duration generallyrequired by low-income people.

The first issue requires screening, monitoring, and enforcementprocedures that comply with the specific circumstances of low-income people and that deviate widely from the usual bankingpractices. The second issue requires operating with transactioncosts (including information costs and risk) that necessarily lead tointerest rates that are well above commercial bank rates, but thatare nevertheless still competitive and thus attractive for themicrofinance institution’s clients.

Microfinance institutions generally experience a trade-off intheir operations between the two objectives: a focus on the some-what better known clients who require somewhat larger loans eases

21

the cost issue and brings financial sustainability closer. This,however, leaves the smaller clients outside the financial frontier.Conversely, a focus on new clients with small financial capacitieswho require small loans does bring new clients inside the frontier,but also brings more costs and risk due to an initial shortage ofinformation on the new clients. The consequence is that it is moredifficult to achieve financial sustainability. It is in this trade-offbetween the two objectives that the two views sketched in the pre-vious section have maintained their roles up until today. The creditfor target group view complies directly with the outreach objective,as outreach can be made operational in terms of reaching a specifictarget group. Successfully reaching the target group with loans,possibly measured through impact studies, may easily provide ajustification for slackening the financial sustainability objective byaccepting “structural subsidies” or by postponing the date forachieving sustainability. The pushing the financial frontier viewoffers more opportunity for a better balance between the twoobjectives, as financial sustainability is required to keep low-income people inside the financial frontier. The resulting greateremphasis on financial sustainability may, however, slow the flow ofnew people across the frontier.

The balance between the two objectives often remains hiddenin management decisions on organization, operations, and thefinancial products offered. The consequences of these decisionsare, however, reflected in the annual accounts; whether or notthese are considered acceptable depends on the views of the gov-erning body of the microfinance institution.

Microfinance and Rural Development

No studies have been done on the long-term effect of microfi-nance, most likely due to the relative youth of many microfinanceinstitutions and the generally still limited coverage within theirareas of operation. However, an exploration of studies on theeffects of microfinance on rural households and studies on the roleof finance at national level provides indications of what the long-term effect might be. As a start, an overview of the position of a

Journal of Microf inance

Volume 7 Number 222

Microf inance and Rura l Development

Volume 7 Number 2

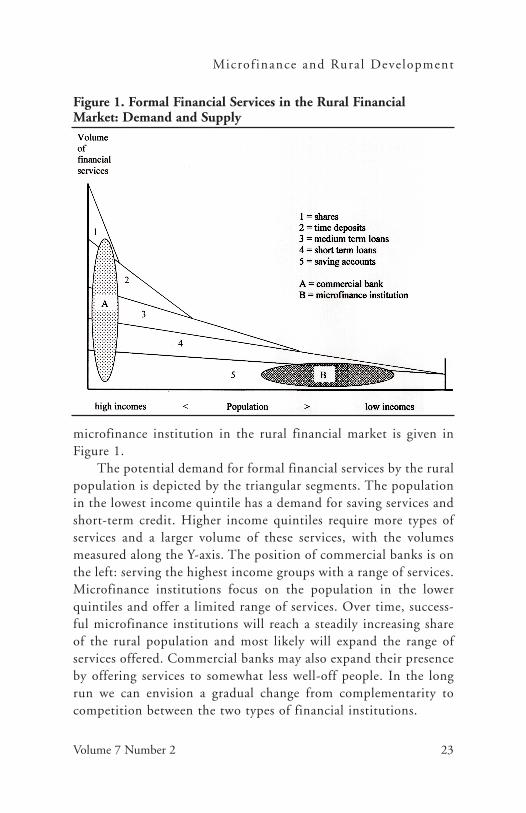

microfinance institution in the rural financial market is given inFigure 1.

The potential demand for formal financial services by the ruralpopulation is depicted by the triangular segments. The populationin the lowest income quintile has a demand for saving services andshort-term credit. Higher income quintiles require more types ofservices and a larger volume of these services, with the volumesmeasured along the Y-axis. The position of commercial banks is onthe left: serving the highest income groups with a range of services.Microfinance institutions focus on the population in the lowerquintiles and offer a limited range of services. Over time, success-ful microfinance institutions will reach a steadily increasing shareof the rural population and most likely will expand the range ofservices offered. Commercial banks may also expand their presenceby offering services to somewhat less well-off people. In the longrun we can envision a gradual change from complementarity tocompetition between the two types of financial institutions.

23

Figure 1. Formal Financial Services in the Rural FinancialMarket: Demand and Supply

The effect of microfinance on individual low-income house-holds has been studied through microeconomic impact studies.Three aspects are generally highlighted. Firstly, there is an increasedcapacity to deal with risk through the withdrawal of savings orobtaining credit in the case of an emergency. This may mean thatproductive assets (machinery, inventory, land, livestock) need notbe sold during an emergency and thus that the flow of income isnot interrupted. Secondly, there is an improved management ofconsumption requirements over the year, to maintain adequatelevels of food intake (Pitt & Khandker, 1998). This is of majorimportance, as labor is often the main resource of low-incomehouseholds. Thirdly, opportunities to invest in productive enter-prises increase. These increased capabilities of rural households toproduce, consume, and invest may be reflected only partly in theactual credit and savings relationships with microfinance institu-tions, because reliable access to microfinance forms a potentialthat can be tapped if and when required. This potential may, forexample, mean that the household’s own resources will be utilizedmore fully for production, with access to microfinance being reliedon if there is an emergency.

Extrapolating the effects of microfinance on individual house-holds to rural areas in total gives some idea of the overall conse-quences. The increased individual capacity to deal with shocksreduces the effects of a co-variant shock for the rural population asa whole, at least when a substantial proportion of the population iswithin the financial frontier. Further, increased saving in financialassets means a shift away from storing wealth in assets with zero orlow productivity. The financial savings become available for invest-ment in agriculture, in agriculture-related trade and processing,and in a host of other enterprises with expected benefits for tech-nological progress and rural employment. In a later stage, whenremunerative investment opportunities in rural areas become lim-ited and the volume of savings overtakes the volume of credit,excess capital can be channelled via microfinance institutions andthe national banking system to urban areas where large-scale indus-tries and services offer extensive investment opportunities. In this

Journal of Microf inance

Volume 7 Number 224

Microf inance and Rura l Development

Volume 7 Number 2

way, rural savers will benefit from those investments and the chil-dren of the savers might find the urban jobs they are looking for.

The above process of increased saving in financial assets fol-lowed by intermediation by the banking system and investmentby borrowers has been studied extensively at the national level.In their theory of financial development, Shaw (1973) andMcKinnon (1973) describe this process as financial deepening.This theory was developed in the 1960s when governments usedthe banking system to support investment in their priority sectors(often industry), thereby bypassing efficiency considerations inmany cases and neglecting domestic savings. Since the 1980s, manycountries have shifted policy from financial repression towardsfinancial liberalization, or from shallow finance to deep finance.

The relationship between financial development and economicgrowth at the national level has received renewed attention nowthat databases covering many countries over prolonged periodshave become available. In a cross-country sample of 80 countriesover the period 1960 to 1989, King and Levine (1993) found apositive relationship between financial depth, measured throughfour indicators,2 and economic growth. They also showed thatfinancial development has predictive power for future growth,indicating a causal relationship between financial development andgrowth. Khan and Senhadji (2000) reviewed methodological issuesregarding the relationship between financial development andgrowth and applied these insights to a data set covering 159 coun-tries over the period 1960–1999. Their results are in line with thefindings of King and Levine, and they conclude that financialdepth is an important determinant of economic growth.

The analysis of the relationships between financial develop-ment and economic growth has been expanded to include poverty.Li, Squire, and Zou (1998) studied income inequality in a largedata set from 112 developed and developing countries for the years1947–1994. They found that financial deepening helped reduceinequality and raise the income of the lower 80% of the popula-tion. Honohan (2004) gives a recent overview of financial development, economic growth, and poverty and concludes that

25

finance-intensive growth is empirically associated with lowerpoverty ratios.

The discussion of financial deepening, economic growth, andpoverty cited above considers these issues at the national level.However, the central tenet of financial deepening, a shift to savingin financial assets followed by intermediation by the banking systemand investment by borrowers, has direct relevance for microfinancein rural areas, since providing rural households for the first timewith access to savings and credit through local intermediation isthe core of financial deepening. The effects of financial deepeninggo beyond the individual links between microfinance institutionsand households, because a reduction of the capital locked up inpoorly productive assets and the availability of capital for new,trustworthy clients with productive uses fundamentally affectseconomic relationships in rural areas. Rajan and Zingales (2003),for example, state: “a healthy financial system can be a powerfulanti-monopoly tool, providing the lubrication for the emergence ofcompetitors that can undermine the power of incumbent firms,and the means for poor households and small-scale producers toescape the tyranny of exploitative middlemen.” Microfinance thuspositively affects economic life in rural areas; expanding outreach,enlarging the microfinance oval in Figure 1 to include a substantialproportion of the rural population, will make these effects morevisible.

The review of long-term financial development at the nationallevel also provides a perspective on a potentially negative side offinancial deepening: the occurrence of bank insolvency. Caprioand Klingebiel (1996) give an overview of bank insolvencies in 69countries since the late 1970s. The list includes countries from allfive continents and covers industrialized, transitional, and alsodeveloping countries. A number of countries saw more than onecrisis in the period covered. The crises involved governmentbanks, private banks, savings banks, and rural banks and rangedfrom a few banks to the entire banking sector in a country. Thecosts or losses ranged from less than 1% of GDP to as much as55% of GDP and were borne by taxpayers, savers, or a combina-

Journal of Microf inance

Volume 7 Number 226

Microf inance and Rura l Development

Volume 7 Number 2

tion of both. The factors cited as reasons for the crises range frommacroeconomic factors, through weak incentives for banks to actprudently, to lack of managerial skill and fraud.

The widespread occurrence of national bank crises means thatviewed from a long-term perspective, financial institutions are atrisk irrespective of current apparently stable situations. Formicrofinance institutions this risk has special dimensions. A pos-sible collapse of a microfinance institution in a national bankingcrisis means a loss of savings for their low-income clients, andthis is the more damaging as a financial crisis is usually followedby a period of economic recession. Less visible, but with similargrave consequences, is the loss of the relationship-specific socialcapital built up between the microfinance institution and clients.This social capital cannot be replaced without again overcomingthe information gap and building up new confidence betweenfinancial institution and clients—a costly affair that will takeyears. Finally, in a national banking crisis the government’s pri-orities are usually with the larger commercial banks. These banksare more likely to be rescued in the name of national interest andwith taxpayers’ money than the smaller, less visible, rural micro-finance institutions.

The exploration of microfinance and rural development showsa potentially positive impact of microfinance institutions on ruraleconomic life, as they are the primary vehicles for the process offinancial deepening in rural areas. This process is not without risk,however, as a failure of a microfinance institution, whetherinduced by a national bank crisis or by the institution’s ownactions, will result in a loss of both financial capital and the rela-tionship-specific social capital built up between institution andclient.

Discussion

The foregoing review of views and policies on microfinance andthe operations of microfinance institutions vis-à-vis the position ofmicrofinance in the long-term process of rural development leadsto the conclusions given below.

27

First, the generally accepted objective of microfinance institu-tions—financial sustainability, or independence from subsidies—seems to be outdated. It was certainly relevant in the 1980s and 1990swhen microfinance institutions were struggling into existence.Nowadays, many microfinance institutions are operational and theestablished relationships with clients deserve to be safeguarded. Thisis the more relevant as history has shown that bank crises are therule rather than the exception. The financial objective must there-fore be raised towards financial stability, defined as the ability towithstand financial shocks, whether the shocks come from insidedue to the adverse conditions of clients or from outside, transmittedthrough the financial links with the national economic and finan-cial sectors. Financial stability must be approached from two sides:diversification of the loan portfolio to minimize the negativeeffects of co-variant risks facing the rural population, and buildingup reserves. The latter means making a profit, not as an objectiveas such, but as a requirement for continuation.

Second, outreach in the sense of reaching a more or less nar-rowly defined group is, in the long run, not justified. First, a focuson one group of clients makes a microfinance institution vulnerable,thereby endangering financial stability. Second, a focus on onetype of clients overlooks the indirect positive effects of wider accessto financial services for the rural population as a whole. Therefore,the objective that is beneficial for all rural households in the longrun is expansion towards new clients and the provision of newfinancial services. Profit comes in again for two additional reasons:profitable microfinance institutions are more likely to be able todraw capital from the national market for expansion, and profit isrequired for experiments to include new groups of clients and todevelop new financial products to serve old clients better.

The two opposing views on microfinance, credit for targetgroup and pushing the financial frontier can be united into one newperspective for policy formulation: stability and expansion. Fromthis perspective the first priority is to achieve financial stability tomaintain what has been achieved; the second is to expand towardsnew clients. It is interesting to note that from a long-term perspective,

Journal of Microf inance

Volume 7 Number 228

Microf inance and Rura l Development

Volume 7 Number 2

there is no trade-off between stability and expansion, as financialstability is a necessary condition for an expansion of services.

Government policies that are based on stability and expansionmust support microfinance institutions in two ways. First, they mustpass legislation that allows microfinance institutions to mobilizesavings, to provide credit, and to undertake other services, such asinsurance and money transfers. This combination of servicesresults in economies of scale and scope, which strengthens thefinancial position of individual microfinance outlets and thusallows geographical expansion and financial deepening in ruralareas. Second, prudent regulations are required that buttress thefinancial stability of microfinance institutions in their specificcircumstances.

Notes

This article is based on a paper presented at the International Seminar on BRI

Microbanking System, Bali, Indonesia, 1–3 December 2004.

1. Impact assessment may include an assessment of the effect of credit on clients

as well as a study of the appropriateness of credit services.

2. (1) The ratio of liquid liabilities (M3) of the financial system to GDP; (2) the

ratio of deposit money bank domestic assets to deposit money bank assets plus cen-

tral bank domestic assets; (3) the ratio of claims on the nonfinancial private sector to

total domestic credit; and (4) the ratio of claims on the nonfinancial private sector to

GDP.

References

Adams, D. W., & Von Pischke, J. D. (1992). Microenterprise credit programs: Déjà

vu. World Development 20 (10): 1463–1470.

Barret, C. B. (2003). Rural poverty dynamics: Development policy implications. Paper

presented at the 25th International Conference of Agricultural Economists,

Durban, South Africa.

Bell, C. (1988). Credit markets and interlinked transactions. In H. Chenery and

T. N. Srinivasan (Eds.), Handbook of development economics (Vol. I, pp.

763–772). Amsterdam: North-Holland.

Billah, P. (1984). Report on indigenous savings and credit arrangements in Lombok.

Unpublished manuscript.

Bouman, F. J. A. (1977). Indigenous savings and credit societies in the third world: A

message. Savings and Development, 1(4), 181–218.

29

Caprio, G. Jr., & Klingebiel, D. (1996). Bank insolvencies: Cross-country experience

(Policy Research Working Paper 1620). Washington DC: World Bank.

Donald, G. (1976). Credit for small farmers in developing countries. Boulder, Colorado:

Westview Press.

Hoff, K., & Stiglitz, J. E. (1993). Imperfect information and rural credit markets:

puzzles and policy perspectives. In: K. Hoff, A. Braverman, & J. E. Stiglitz. The

economics of rural organization, theory, practice, and policy. Oxford: Oxford

University Press.

Honohan, P. (2004). Financial development, growth and poverty: How close are the

links? (Policy Research Working Paper 3203). World Bank.

Khan, M. S., & Senhadji, A. S. (2000). Financial development and economic growth:

An overview (IMF Working Paper).

King, R. G., & Levine, R. (1993). Finance and growth: Schumpeter might be right.

The Quarterly Journal of Economics, 108(3), 717–737.

Krahnen, J. P., & Schmidt, R. H. (1994). Development finance as institution building:

A new approach to poverty-oriented banking. Boulder: Westview Press.

Li, H., Squire, L., & Zou, H. (1998). Explaining international and intertemporal

variations in income inequality. The Economic Journal, 108 (446), 26–43.

Mellor, J. W. (1966). The economics of agricultural development. Ithaca: [publisher]

McKinnon, R. I. (1973). Money and capital in economic development. Washington,

DC: Brookings Institution.

Moll, H. A. J. (1989). Farmers and finance: Experience with institutional savings and

credit in West Java. Wageningen: Wageningen Agricultural University.

Moll, H. A. J., Ruben, R., Mol, E. W. G., & Sanders, A. A. (2000). Exploring seg-

mentation in rural financial markets: An application in El Salvador. Savings

and Development, 1(24), 33–54.

Moll, H. A. J. (1994). The performance of banks in rural financial markets. In F. J.

A. Bouman and O. Hospes (Eds.), Financial landscapes reconstructed: The fine

art of mapping development (pp. 71–84). Boulder: Westview Press.

Patten, R. H. & Rosengard, J. K. (1991). Progress with profits: The development of

rural banking in Indonesia. San Fransisco: ICS Press.

Pitt, M. M., & Khandker, S. R. (1998). The impact of group-based credit programs

on poor households in Bangladesh: Does the gender of participants matter? The

Journal of Political Economy, 106(5), 958–996.

Rajan, R., & Zingales, L. (2003). Financial depencence and growth. University of

Chicago, unpublished. Quoted in Khan and Senhadji (2003).

Robinson, M. S. (2001). The microfinance revolution: Sustainable finance for the poor.

Washington, DC: World Bank.

Shaw, E. S. (1973). Financial deepening in economic development. New York: Oxford

University Press.

Journal of Microf inance

Volume 7 Number 230

Microf inance and Rura l Development

Volume 7 Number 2

Timmer, C. P. (1988). The agricultural transformation. In: H. Chenery and T. N.

Srinivasan (Eds), Handbook of development economics (Vol. 1 pp. 275–331).

Amsterdam: Elsevier Science Publishers B.V.

Von Pischke, J. D. (1991). Finance at the frontier: Debt capacity and the role of credit

in the private economy. Washington, DC: EDI Development Studies.

Von Pischke, J. D., et al. (1983). Rural financial markets in developing countries.

Baltimore: Johns Hopkins University Press.

Yaron, J. (1992). Successful rural finance institiutions (World Bank Discussion Paper

No. 150). Washington, DC: World bank.

31