Embed Size (px)

Citation preview

Microfinance Regulation in India

MicrofinanceRegulation

in India

Sa-Dhan

New Delhi 2001

�������������� �������� �

�������� �����������

����� ����������

© Sa-Dhan 2001

AuthorsKurumi Fukaya

Narayanan ShadagopanSa-Dhan Research Team (Chapter 4)

Published bySa-Dhan

B4/3133 Vasant Kunj, New Delhi [email protected]

Typeset for print and e-book byAstricks

New Delhi 110070www.astricks.com

Jacket design by Neelima Rao

Rs 225 $ 25

Sa-Dhan — The Associationof Community DevelopmentFinance Institutions

The Mission‘To build the field of community development finance, helpingmember and associate institutions in rendering better servicesto low income households, particularly women, in both ruraland urban India, in their quest for establishing stable livelihoodsand improving their quality of life.’

Aims and Objectives I. To provide a forum for organizations and individuals en-

gaged in the field of community development finance toshare and exchange experiences, expertise and resources;

II. To serve as a catalyst for building these institutions;III. To strengthen the capacities of community development

finance institutions (CDFIs) through research, consult-ancy and training in different aspects;

IV. To disseminate and publish sound financial practicesfrom both national and international;

V. To act as a self regulating organization for communitydevelopment finance institution and seek recognitionfrom relevant regulatory;

VI. To establish linkages between numbers and resources in-stitutions such as funding agencies, financial institutions,

rating agencies, training and consultancy and researchinstitutions;

VII. To establish minimum standard of performance, bothdevelopmental and financial aspects which membershave to adhere;

VIII. To work with other networking and coalition of com-munity development finance institutions; and

IX. To represent its members in governmental agencies suchas RBI, and other regulatory and policy making bodiesso as to promote community development finance andhelp create a favourable policy environment at nationaland international level etc.

(Memorandum of Association, Sa-Dhan, 1999)

Members of Sa-DhanSa-Dhan’s members cover the entire spectrum of microfinanceplayers — NGOs, Non-Banking Finance Companies, Profes-sional support organizations and Specialised Networks. As ofJanuary 2001, Sa-Dhan’s primary and associate members are:SEWA Bank, Ahmedabad; BASIX, Hyderabad; Friends ofWomen’s World Banking (FWWB), Ahmedabad; SHARE, Hy-derabad; Indian Grameen Services (IGS), Hyderabad; ADITHI,Patna; DHAN Foundation, Madurai; AWAKE, Bangalore; De-velopment Support Team (DST), Pune; EDA Rural SystemsPrivate Limited, Gurgaon; PRADAN, Ranchi; CHAITANYA,Pune; Association for Social Advancement (ASA), Trichy; SarvaJana Seva Kosh Limited (SJSK), Chennai; Rashtriya GraminVikas Nidhi (RGVN), Guwahati; Watershed OrganisationTrust (WOTR), Ahmednagar; OUTREACH, Bangalore;HDFC, Mumbai; All India Association of Micro EnterpriseDevelopment (AIAMED), New Delhi; Sanghamitra Rural Fi-nancial Services, Mysore; CARE-India, New Delhi; Microfi-nance Consulting Group (MCG), Chennai; ARAVALI, Jaipur;Bharat Sewak Samaj (BSS), Thiruvananthapuram; ShramikBharti, Kanpur; Grameen Development Services (GDS),

vi Microfinance Regulation in India

Lucknow; Amhi Amchya Arogyasathi (AAA), Gadchiroli;SHEPHERD, Trichy; Centre for Youth and Social Develop-ment (CYSD), Bhubaneshwar; and Kalrayan Hills Area Devel-opment Project (KHADP), Salem.

Sa-Dhan B-4/3133 Vasant Kunj, New Delhi 110070 Tel: (91) (11) 26138932 Fax: (91) (11) 26132629 e-mail: [email protected]

Sa-Dhan vii

Acknowledgement

Discussions for the research outline for this report beganimmediately after the presentation of the report of NationalTask Force on Supportive Policy and Regulatory Frameworkfor Microfinance to the Governor of the Reserve Bank of India.The report besides suggesting the need to encourage the devel-opment of a self-regulatory mechanism went on to define someof the broad parameters under which such a regulatory mecha-nism could be given shape. Specific features that required de-tailed examination, of the Indian context, remained an urgentneed.

This study is an exercise in unravelling the features of theself-regulatory regime for India. Fortunately, the study hasreceived the attention and time of a wide variety of supporters:foremost the Policy Sub-Group in Sa-Dhan, well-wishers andsupporters, prominent among them, Bharathi Ramola-Guptaof Price Waterhouse Coopers, Malcolm Harper and ThomasFisher from the New Economics Foundation. In addition, allthe different stakeholders — members and non-members ofSa-Dhan, central bankers and policy makers, retail bankers anddonors — welcomed the study team warmly and with greatgenerosity with their time. We are thankful for all your insightsand suggestions, which we have hopefully summarized honestlyand clearly in the study.

Further, the work of my colleagues in Sa-Dhan, particularlyRaja who has put together one of the most extensive appoint-ments lists, covering a hundred meetings, stretching fromLucknow in the East to Ahmedabad in the West, and fromDelhi in the North to Madurai in the South, was a delicate

balancing exercise. Assisting in these hundred meetings acrossthe country were a dedicated team of practitioners turnedresearch assistants, who undertook, the at times, arduous jour-ney across the country: Srikant, Santosh Sharma and LangsunT. Mate. They together with the researchers explained, lis-tened, debated and informed the respondents the purpose ofthe study. They met with leaders of organizations, key manag-ers, frontline retail staff and technical service providers. Forcapturing the diversity of views and putting them systematicallyinto a report of high order, one must thank Kurumi Fukayaand Narayanan Shadagopan of the London Business School.

Finally, for turning this document into one immensely read-able and well produced book, we need to thank our editor,Dr Janaki Turaga.

We hope this study stimulates and informs each one of you.

Mathew TitusExecutive DirectorSa-DhanJanuary 2001

x Microfinance Regulation in India

Foreword

During the past few years the role of microfinance as acomponent of poverty reduction strategies has come to be wellrecognized. As a result, increasing numbers of NGOs, as wellas government, bilateral and multilateral funded developmentactivities are including microfinance components in their pro-grammes. This has resulted in a substantial expansion in theavailability of micro-loan and savings facilities for the poor.With a more liberal policy environment emerging, microfinanceinstitutions (MFIs) are also starting to consider micro- insuranceservices for their poor clients.

Despite the recent activity in the microfinance sector, how-ever, its outreach is to no more than 2 per cent of the 60 millionpoor families in the country. And yet, on account of theirunfortunate experience with the Integrated Rural DevelopmentProgramme (IRDP) and other government sponsored lendingprogrammes, the banks are very reluctant to lend to the poor.Improving the access of the poor to capital, therefore, repre-sents a challenge for the microfinance sector.

At the same time, there are opportunities for the microfinancesector. First, NABARD has set a target of one million SHGs tobe covered by the bank linkage programme by the year 2008.The government has provided NABARD with a fund of Rs l00crores (US$ 21 million) for this purpose and for strengtheningthe sector. Second, SIDBI’s Foundation for Micro-Credit(SFMC) has raised substantial funds for providing loan capitalto MFIs and for undertaking a capacity building support pro-gramme for them. The Foundation proposes to have an out-standing portfolio of Rs 443 crores and to cover 1.3 million

clients over seven years. Third, HUDCO, HDFC and otherapex funding organizations such as Friends of Women’s WorldBanking, India (FWWB) have also committed significantamounts to the sector. This means that a substantial increase inthe resources available to the sector is currently taking place.

For the microfinance sector, this situation represents athreat as well as an opportunity. While it is apparent that theadditional resources available will foster a significant increasein the growth of the sector, transforming this into qualityoutreach is a challenge that needs to be managed carefully. Theprovision of financial services means not only the handling offunds that belong to public organizations but also the manage-ment of savings that belong to poor people. The availability ofresources combined with a liberal policy environment couldresult in NGOs or others undertaking microfinance withouthaving a full understanding of the complexities and disciplineof financial management.

It is possible that the entry of under prepared or ill-moti-vated organizations has already happened to some extent. If thegrowth of this important sector is to be managed withoutsignificant disaster stories, it is important that not only arestandards introduced in the immediate future but also that someform of regulation be considered — as in the case of banks andnon-banking financial institutions (NBFCs).

As a network of responsible institutions engaged in thesector, Sa-Dhan has already launched an important initiativeto introduce performance and management standards for MFIs.Over the next few months the draft standards will be discussedwith the MFIs themselves and with other stakeholders beforethey are announced as benchmarks.

The study undertaken here is an attempt by Sa-Dhan toinvestigate the feasibility of introducing some form of regu-lation for microfinancial service provision in India. KuramiFukaya and Narayanan Shadagopan, students of the LondonBusiness School undertook the study. Over a period of twomonths, in mid-2000, they carried out an exhaustive studyinteracting with major stakeholders and groups of stakeholders

xii Microfinance Regulation in India

in the microfinance sector to discuss the issues related tothe introduction of regulation — particularly self-regulation— in Indian micro-finance. They also reviewed the literatureon the international experience with microfinance regulation.Their very well focussed report has helped to clarify theseissues including why self-regulation is required at all, whoshould be covered by it, how feasible it is and what Sa-Dhan’srole should be.

I trust this report will serve as a basis for carrying forwardthe discussion on regulation for microfinance in India and thataction emerging from it will help to foster the orderly growthof this very important sector. Readers are encouraged to com-municate their views both formally and informally to theSa-Dhan secretariat and to members of the Board so thatappropriate action can be initiated in the near future. Ela R. BhatChairpersonSa-Dhan— The Association of Community Development Finance Institutions

Foreword xiii

Preface

The National Bank for Agriculture and Rural Development(NABARD) Task Force Report (The Task Force Report) suggeststhat a body comprising practitioners should organize a self-regulatory body that establishes norms and standards for thepractice of microfinance. The Task Force Report gives variousreasons for establishing a self-regulatory body. The study ex-plores whether and how the self-regulatory organization (SRO)will be able to fulfil the objectives as outlined in the Task ForceReport, whether a SRO is necessary to fulfil the objectives, whatform the SRO should take, and related issues.

Microfinance, has traditionally been practised extensively inIndia — first through the agricultural co-operatives establishedat the turn of the last century, and later through commercialbanks and Regional Rural Banks (RRBs). As a result, India hasone of the largest microfinance banking networks in the world.Why then, does a large gap exist between the supply and demandof financial services in rural India? Is it possible that the largenumber of non-government organizations, both voluntary andfor profit, can fill that gap? What kind of policy and regulatoryenvironment will address the bridging of the gap?

The international experience of microfinance regulation isreviewed for possible relevant applicability for India. Countrieslike South Africa and Philippines are beginning to recognizethat microfinance could be central to achieving overall socialobjectives and that a conducive environment needs to be pro-vided for the sector to grow. Their recent interventions haveas yet had little impact, the philosophy and mindset underlyingtheir institutions is reviewed.

Despite the different philosophical orientations, practitio-ners share a major concern regarding voluntary regulatoryarrangements whether the social objectives of microfinance willbe pushed aside in the quest for a more mature market for thefinancial services to the poor. Concerns such as — will it servethe interests of the most powerful? Would the rules be tooonerous to comply with — are shared with organizations un-dertaking voluntary regulation.

Practitioners were unanimous that the Government of India(GoI) should not be excessively involved in the process of altern-ate, self-regulatory framework. Despite differences about therole of the SRO among the practitioners in the microfinancesector, consensus exists for a self-regulatory framework to caterto the Indian microfinance market.

xvi Microfinance Regulation in India

Contents

Front Cover

Half-Title i

Title iii

Copyright information iv

About Sa-Dhan v

Acknowledgement ix

Foreword xi

Preface xv

1. Introduction 11.1 Background 1

1.2 Concept of Microfinance 2

1.3 Methodology 3

1.4 Layout of the Book 4

2. Microfinance and Regulation 52.1 What does regulation accomplish? 5

2.2 Principles of Regulation 5

2.3 Regulation versus Supervision 7

2.4 Costs of Regulation 8

2.5 Constraints to Regulating 8

3. Rural Credit in India: State Interventions 103.1 Government Sponsored Programmes 11

3.1.1 IRDP 113.1.2 Priority Sector Lending 123.1.3 Regional Rural Banks and the

outreach of formal institutions 133.1.4 Causes of poor performance of RRBs

and commercial banks 133.1.5 NABARD and SHG-bank linkage

programmes 15

3.2 Co-operatives 163.2.1 Government control of co-operatives 163.2.2 Mutually Aided Co-operative Societies

(MACS) Act 173.2.3 Is an enlightened Co-operative Act

sufficient for ensuring stability of the financial system? 18

4. Microfinance Services in India 214.1 Introduction 214.2 The Task Force on Microfinance

Regulation 224.3 Emerging Microfinance Institutions

in India 234.3.1 Legal Forms of MFIs 234.3.2 Operating Models of Retail MFIs 24

4.4 State Regulated Microfinance Intermediaries 244.4.1 NBFCs 254.4.2 Co-operative Banks 25

4.5 Unregulated Microfinance Intermediaries 264.5.1 NGO-MFIs 26

4.5.1.1 Retail NGO-MFIs 274.5.1.2 SHG Federations 284.5.1.3 Apex Institutions 31

4.5.2 MACS 324.6 Conclusion 32

xviii Microfinance Regulation in India

5. International Experience in MicrofinanceRegulation 345.1 Different approaches in Microfinance

Regulation 345.1.1 Initial Steps (No Regulation) 345.1.2 Self-Regulation 355.1.3 The hybrid approach 375.1.4 Existing law 375.1.5 Special law 39

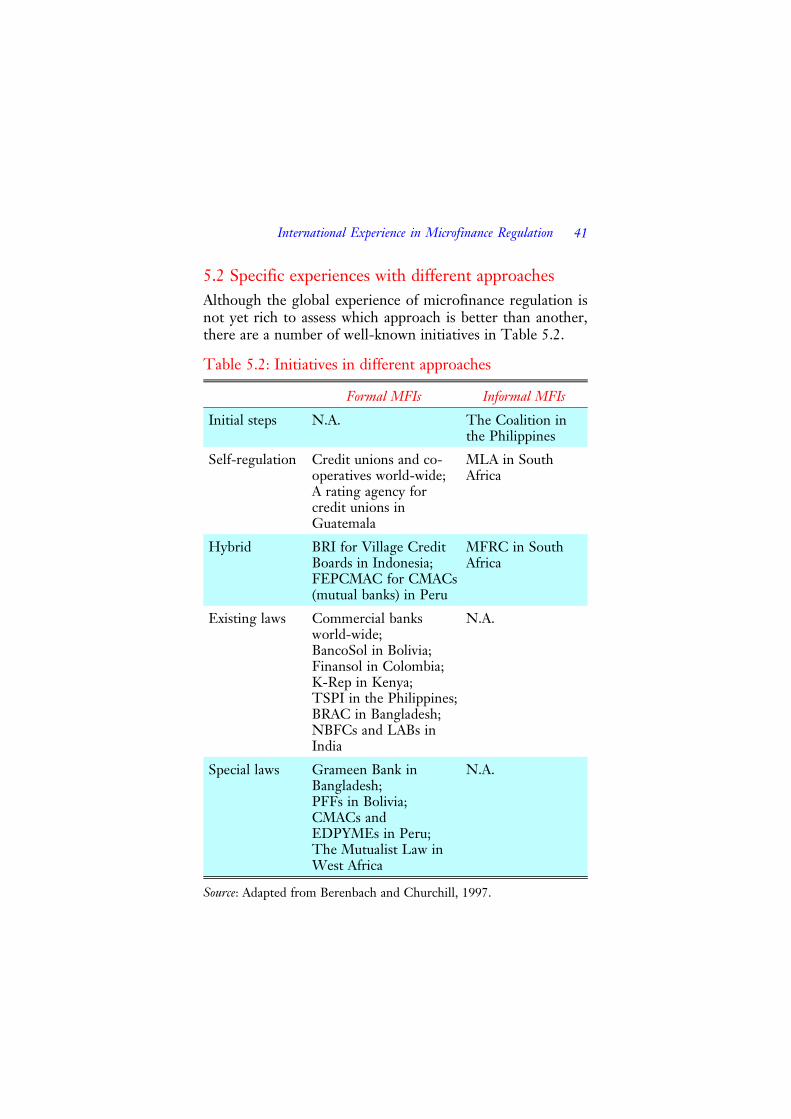

5.2 Specific experiences with different approaches 415.2.1 Initial Steps: Philippine Coalition for

Microfinance Standards 425.2.2 Self-Regulation: Credit Unions and

Co-operatives 435.2.3 Hybrid approach: Microfinance

Regulatory Council in South Africa 445.2.4 Existing law: BancoSol in Bolivia 465.2.5 Special law: PFFs in Bolivia 48

6. Self-Regulation in India: Concerns and Prospects 516.1 Why self-regulation in the Indian

microfinance sector? 516.2 Objectives and benefits of self-regulation 526.3 Who should come under self-regulation? 566.4 What should SROs do? 576.5 Who should be SROs? 586.6 Typology of SROs 596.7 How feasible is self-regulation? 626.8 Dissemination Workshop: Issues

and Concerns 65

7. Self-Regulation: Potential and Pre-conditions 687.1 Potential of Microfinance Regulation

in India 687.2 Pre-conditions to self-regulation 71

Contents xix

References 73

Annexures 75

Back Cover

Tables and Figures

Box 4.1 State Profiles: Maharashtra and Orissa 29

Table 4.1 NABARD’s Bank-SHG Linkage Programme 27

Table 5.1 Approaches in Microfinance Regulation 35

Table 5.2 Initiatives in different approaches 41

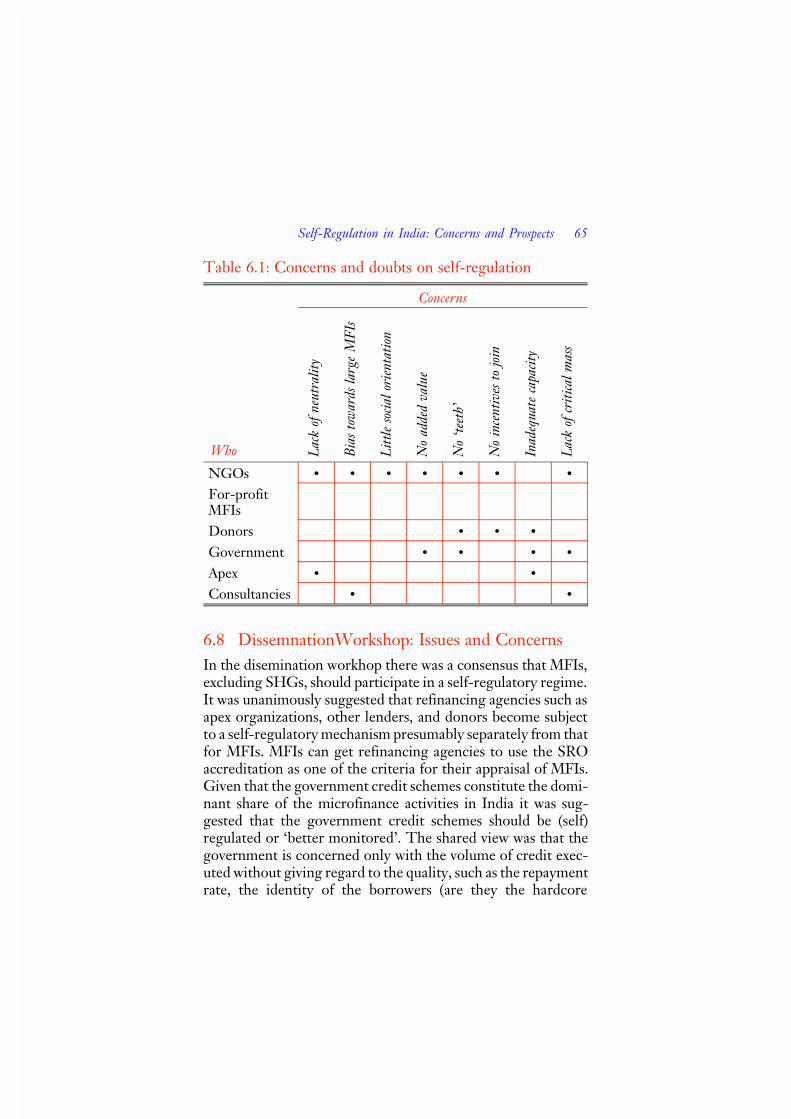

Table 6.1 Concerns and doubts on self-regulation 65

Table 6.2 Activity/Institution approach based Regulation 66

Figure 6.1 SROs by Region 60

Figure 6.2 SROs by Institution Type 61

Figure 6.3 SROs by Maturity 61

xx Microfinance Regulation in India

1

Introduction

1.1 BackgroundThe NABARD Task Force Report (1999) (The Task ForceReport) suggests that a body comprising of practitioners shouldorganize a self-regulatory body that establishes norms andstandards for the practice of microfinance. The Task ForceReport gives various reasons for establishing a self-regulatorybody. The study explores whether and how the self-regulatoryorganization (SRO) will be able to fulfil the objectives, whethersuch a body is necessary at all to fulfil the objectives, whatform the SRO should be, and related issues.

The term ‘regulation’ means ways in which the govern-ment, motivated by various reasons, makes rules for peopleand institutions in a society by legislation or decree. Histori-cally rules have been established by government functionand voluntary action. Market rules enable efficient and pro-ductive transactions by constraining and governing decision-making powers and actions. In the microfinance sectordifficulties arise regarding the source of the regulatory frame-work — where do the rules come from, who makes them,who decides on the penalties, and who does the policing?The prevailing view in India, as in many other places, bestowson ‘the State’ the task of establishing and enforcing therules. Public and political apprehensions about potential crisesand the assumption that the government has a solution withmore benefits than costs result in state regulations forcingout alternative arrangements. Such a position implies thatother arrangements are inherently less effective and proneto varied conflicts of interests and opportunistic behaviour.

The alternative to state regulation is a continuum of voluntaryregulatory arrangements.

Regulation of financial services to the poor is consideredbecause:

1. The vast majority of moral hazard problems potentiallyoccur in financial services;

2. A systematic erosion of faith in the economy poses longerlasting problems in society; and

3. Non-Government Organizations (NGOs) providingfinancial services is the fastest growing segment of theNGO population.

1.2 Concept of MicrofinanceThe study has adopted The Task Force Report’s definition ofmicrofinance which is ‘the provision of thrift, credit and otherfinancial services and products of very small amounts to the poorin rural, semi-urban or urban areas for enabling them to raisetheir income levels and improve living standards’ (1999: 17).Thrift implies savings created by postponing almost necessaryconsumption while savings implies the existence of surpluswealth.

Much of the existing literature on microfinance focuses onexperiences in Latin America and Africa which is differentfrom the Indian experience. Consensus that the practice ofattending to the financial needs of the poor is nowhere thesame, exists among the international practitioners. The diver-sity of the practitioners and clientele makes defining basicdefinitions difficult.

Credit to the poor by banks and microfinance institut-ions (MFIs) is usually extended without any collateral re-quirements. Some part of the high interest-rates charged tothe poor reflects the riskiness of unsecured loans. The loansare based on subjective assessments of the borrowers’ abilityto repay. The features of micro-credit are — small loansfor working capital or consumption; informal appraisal of

2 Microfinance Regulation in India

borrowers and investments; substitutes for collateral such asjoint-liability groups and compulsory savings; training forboth skills and fiscal discipline; larger repeat loans based onpast loan performance; and low costs loan disbursement andrecovery.

1.3 MethodologyThe research methodology adopted was literature survey andinterviews with key stakeholders in the sector in India. A surveyon literature covering regulation both within and outside mi-crofinance was carried out. The literature on microfinanceregulation is not extensive and largely consists of summaries ofworkshops or discussion papers (see References), as the field ofnon-government sponsored microfinance programmes is stillyoung, MFIs are subject to little regulation and hence there islittle experience in regulating them. However, considerableliterature and experience of other financial institutions withregulation (and self-regulation) exists.

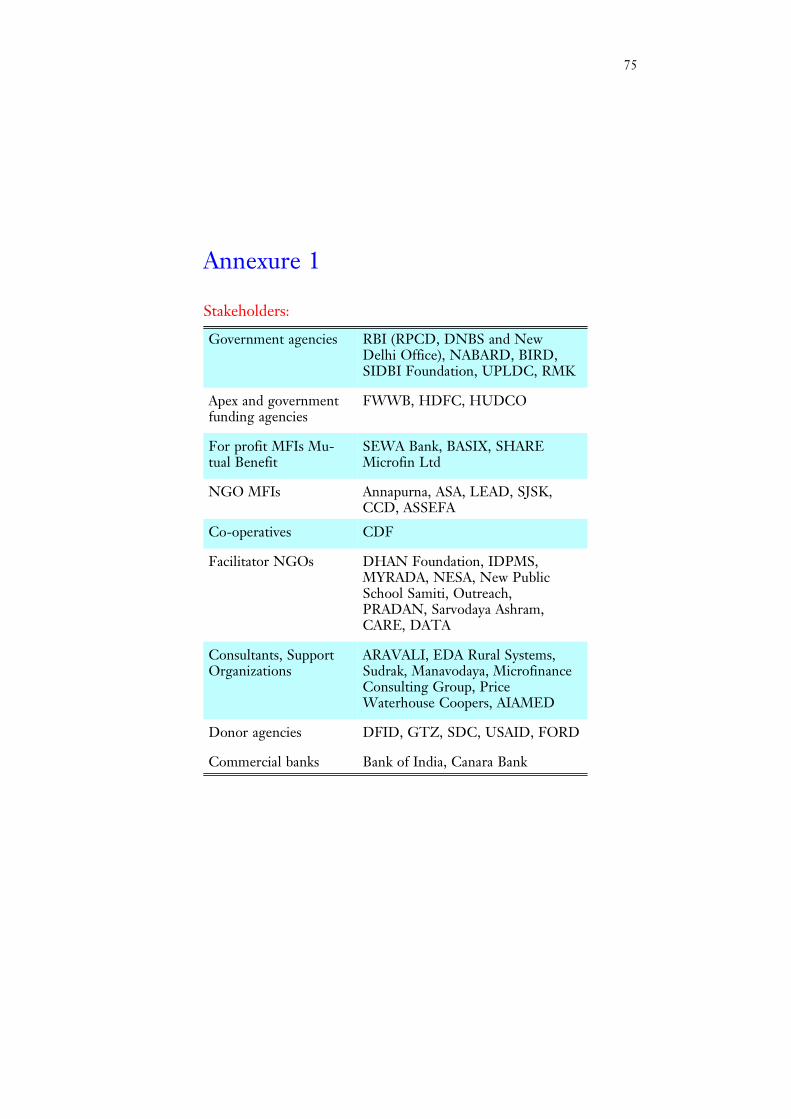

Key stakeholders like the Reserve Bank of India (RBI),NABARD, MFIs, NGOs, multi-lateral agencies, donor agen-cies, institutions and consultancies involved in microfinance inIndia (Annexure 1) responded to the following questions:

• Why did the institutions feel the need for a SRO?• What benefits did they expect to be brought to the

sector by an SRO?• What benefits would accrue to them by belonging to an

SRO?• What form should the SRO take — by region, institu-

tional, size and maturity or all-encompassing?• What were their concerns in belonging to an SRO?

In some instances questions were modified for institutionsfaced with the issue of self-regulation for the first time. A modelof self-regulation was put forth to the institutions to criticize.Approximately 100 meetings were held across the country withdifferent stakeholders.

Introduction 3

1.4 Layout of the BookChapter 1 — The introduction sets the contextual backgroundof the study, the concepts and methodology adopted; Chapter 2— Microfinance and Regulation, addresses the issues in regu-lation; Chapter 3 — Rural Credit in India: State Interventions,examines the state initiatives in the development programmesand co-operative sector; Chapter 4 — Microfinance Services inIndia, delineates the range and issue across the stakeholders;Chapter 5 — International Experience in Microfinance Regu-lation, examines worldwide experience, landmark initiatives, de-velopments and their relevance and applicability to the Indiancontext; Chapter 6 — Self-Regulation in India: Concerns andProspects, addresses the concerns and prospects vis-à-vis self-regulation in India which are discussed by extensively drawingfrom the field data and dissemination workshop and finallyChapter 7 — Self-Regulation: Potential and Pre-conditions,summarizes the current situation and suggests ways of resolvingthem.

4 Microfinance Regulation in India

2

Microfinance and Regulation

2.1 What does regulation accomplish?The regulation and supervision of MFIs has the larger aim ofdeveloping a niche market based financial system for all prod-ucts — credit, savings, insurance, transfer facilities and otherservices for the clients. A market-based financial system, as-sumes the existence of sufficient competition and incentivesto provide the lowest-cost services possible to clients, wherecost includes all costs — interest rates, transaction, and monit-oring. The ultimate aim of MFIs and NGO facilitators in-volved in financial services for the poor ought to be to‘mainstream’ their client base to avoid the marginalization ofthe clients vis-à-vis financial services. The corollary aim israising the standard of practice, making it sustainable andenabling it to contribute to the development of the financialsystem.

In the Indian context, MFIs are highly dependent on donorfunds to carry out their capacity building activities. Donorfunds will not keep pace with the rapidly expanding microfi-nance sector. Furthermore, the risk of the donor funds dryingup is quite high if the better known MFIs go bust, which willaffect all the players in the microfinance field, irrespective ofthe institutional form.

2.2 Principles of RegulationThe motivation for regulatory intervention is based on theassumption that an asymmetry of information exists betweenthe lender and the borrower. The borrower knows more about

what he is going to do with his funds and his ability to repaythan the lender. In deposit-taking, the financial institutionknows more about how the deposits are going to be used or itsown solvency than the depositor. This asymmetry of informa-tion results in problems of ‘adverse selection’ and ‘moral haz-ard’ in the transaction. (Staschen 1999a)

Regulation to match the actions of the institution (agent)and the client (principal) exists and is accomplished in threeways — control the actions of the agent, restrict the decision-making power of the agent, and set appropriate incentives forthe agent such that the interests of the agent and principal areharmonized. The last option, while least costly in terms ofmonitoring, is the hardest to design. The first two optionsinvolve a supervising agency with statutory authority to controlthe agent and lead to inefficiencies in the market. In economictheory (but not in development finance), the manager’s role isto maximize his information advantage not only over his com-petition but also over the clients which is curbed by regulation.In practice, all three methods are employed to regulate financialinstitutions.

The reasons for regulation are:

1. Since it is difficult and costly for a depositor or aninvestor to monitor closely the performance of an insti-tution, the danger of a run on the institution is present.The definition of ‘run’ is expanded in the study from awithdrawal of all deposits motivated by panic leading tothe bankruptcy of the institution to the withdrawal ofinvestor and donor funds. Runs have knock-on effects— a run or collapse of one institution might precipitateruns on other perfectly viable institutions which is linkedto the drying up of donor funds following failures of‘good’ MFIs.

2. Even if MFIs that do not take deposits (except for ‘earnestmoney’) and refinance themselves through external fi-nance and donor funds, MFIs are liable to behave oppor-tunistically, that is pursue personal gain at the expense of

6 Microfinance Regulation in India

the creditors. Regulatory measures might curb this kindof opportunistic behaviour. The argument is put forththat funders should exercise the responsibility to do theirdue diligence on the institution to which they are lendingwhile regulation should play only a small part and that thecosts of due diligence should not be incurred by someoneelse (for example, the RBI). Regulation can act as a signalto prospective investors that a particular institution isfinancially sound. Access to certain channels of revenuesmight be contingent on regulation. Some regulatoryframework is necessary if the ultimate aim is to expand,scale and mainstream this segment of the financial system.

Thus regulation attempts to accomplish limiting the danger

of opportunistic behaviour on the part of the institution (con-sumer protection) and preventing unwarranted runs on thesystem thereby ensuring stability. If public deposits are notmobilized, then regulation should be kept at a minimum. Butif deposits are mobilized, the RBI should monitor in the samemanner as it monitors banks. For institutions not mobilizingpublic deposits, the issues of consumer protection and govern-ment regulation are not relevant.

2.3 Regulation versus Supervision Regulation is the provision of rules while supervision is themonitoring and enforcing of the rules. Regulation and supervi-sion can be done by different entities as done in India where theRBI makes the rules and the NABARD enforces them on finan-cial intermediaries in the rural sector. Supervision is the keyelement as regulation without supervision is pointless and willviolate fundamental principles such as providing a level playingfield for the market participants. A serious problem currentlyfacing the RBI is the number of institutions applying for Non-Banking Finance Company (NBFC) status. Since it is almostinconceivable that the RBI can properly monitor them, the endresult will be that other departments in Government of India

Microfínance and Regulation 7

(GoI) will try to reduce the ‘slack’ by imposing constraints thatmay essentially kill the market. For example, in the event of thenon-relaxation by the Home Ministry of the constraints ofForeign Contribution Regulatory Act (FCRA) regulations in anera of globalization will certainly hamper the practice of certainmicrofinance models. Unless explicitly stated otherwise, thestudy uses regulation as inclusive of regulation and supervision.

2.4 Costs of Regulation As government regulation has grown in recent years, seriousconcerns have emerged about the total costs of regulationswhich are difficult to estimate. The government budget costsare only a small part of the overall costs. The ‘compliance’ costsare the costs incurred by the institutions that are regulated, andthese costs are typically estimated to be 50 times the budgetcosts of regulation. The more serious ‘invisible’ costs (Blundell1999) that is, the adverse effects on enterprise development andless efficient markets are not yet known. For the government,the cost of regulation is mostly external that is, the governmentdoes not incur the bulk of those costs and when the bulk of thecosts does not fall on the regulators, regulation is likely toexceed its optimal level. Hence the government, as a monopolyprovider of statutory regulation will bring in levels of regulationwhich exceed the justified levels of all costs and benefits. Giventhat government regulation is difficult to change because of thelength and complex political process, regulation always lagsbehind innovation and change occurring in the system andthereby doe not relate to the present.

2.5 Constraints to RegulatingGovernment departments are compartmentalized into variousfunctions addressing direct different aspects of governance. Atypical NGO provides various services to its clients — educa-tion, training, health-care and financial services are bundled and,in areas where these services are poor or nearly non-existent,

8 Microfinance Regulation in India

are integrated. Though the government’s role in monitoringand controlling the NGOs is based on its obligation to maximizesocial welfare, it is not clear which government organizationwhether the Ministry of Education, Health Services, the CentralBank, or some other department is vested with the responsibilityfor controlling the NGO. Theoretically, with proper coordina-tion, all the relevant departments could monitor the NGOwhich in practice, is very costly — both to the government andto the NGO, which are prone to various bureaucratic problems.Ideally, government organizations should provide an integratedapproach to monitoring but considering the evolution of gov-ernment institutions, this is hardly a practical suggestion.

One of the unintended consequences of government regu-lation is accumulation of layers of regulation which results inless transparency and democratic accountability. The intellec-tual basis for government intervention as articulated by the‘public interest’ theory of regulation is that the state shouldstep in when ‘public interest’ objectives are not met due to‘market failure’. It is assumed that the government is an altru-istic and omniscient body which can unfailingly detect andcorrect the problems without any self-interest and politicalconsiderations. Consequently, the invisible costs of regulationresult in higher prices and lower standards for consumers asevident in the Indian experience of microfinance (AIAMEDand Opportunity International 1999). Government regulationcan be very oppressive with respect to setting rules as it focuseson a particular process or situation for example the crisis in-volving a large NBFC in India.

The tenuous foundations of principles on which practicalregulation rests leads to many difficulties, and it should not beassumed that ‘on balance’, government regulation will result inmore benefits than costs.

Microfínance and Regulation 9

3

Rural Credit in India: State Interventions

The history of microfinance in India is much longer andmore complex than other developing nations. For many othercountries, the experience of extending credit on a systematicbasis and on a large scale to the rural population is new whichgives them the advantage of a fresh start without resorting toretrofitting new programmes into existing regime. Though thedisadvantage is their lack of experience vis-à-vis the behaviourof rural poor towards microfinance programmes.

Credit demands in the rural sector were largely met byco-operative societies till the mid-1960s. Until then, the com-mercial banks’ presence in rural India largely supported agri-business and marketing. The amount of credit flow to the ruralsector was never sufficient to meet the demands, and one ofthe objectives of bank nationalizations that occurred in 1969and 1980 was to increase the flow of credit to the rural popu-lation. According to the RBI and NABARD the largest micro-credit programme in the world was institutionalized by the GoIthrough its various poverty alleviation schemes, most notablythe Integrated Rural Development Programme (IRDP). Theeconomic crisis in the beginning of the 1990s forced the GoIto re-examine its economic policy, necessitating in a reorien-tation of the economy from centrally planned to market-based.One of the lessons drawn from the gradual demise or transfor-mation of planned economies all over the world is that a mar-ket-oriented approach leads to more efficient resourceallocation than in planned economies. It is our contention that

a market-based approach is not at odds with developmentalgoals. Hence if the aim of the government and microfinancepractitioners is to ‘mainstream’ the rural poor, it necessarilyrequires the introduction of markets, without which the ruralpopulace instead of relying on the invisible hand of the market,will be dependant on the divine hand of the government.

3.1 Government Sponsored Programmes In this section, an overview of the programmes and channels ofdisbursing credit and mobilizing deposits in rural areas in Indiais discussed. The perspective is two-fold — the lack of anymarket-based incentives for performance for the channels (thatis, commercial banks and RRBs) of credit and deposit mobiliza-tion and the continued use of lending technology which hassystematically eroded credit discipline and has made the practiceof microfinance difficult in India than in many other developingcountries.

The GoI added one more channel to reach the poor throughcredit. In the sixth five-year plan, the government launchedseveral anti-poverty programmes like, Integrated Rural De-velopment Programme (IRDP), Training of Rural Youth forSelf-Employment (TRYSEM), Development of Women andChildren in Rural Areas (DWRCA), National Rural Employ-ment Programme (NREP) and Rural Landless EmploymentGuarantee Programme (RLEGP).

3.1.1 IRDPIRDP was launched in 1979 in 2,300 selected communitydevelopment blocks and from 2 October 1980, it was extendedto all the blocks in the country. IRDP was aimed to promoteself-employment with the provision of productive assets topoor households by providing them soft bank loans with acapital subsidy upto 50 per cent. The total number of bor-rowers brought under the scheme till November 1998 were53.8 million involving a credit flow of Rs 19,500 crores. De-spite massive outreach, the impact of the programme in terms

Rural Credit in India: State Interventions 11

of upliftment of households above the poverty line was dismalat 16–18 per cent.

Over nearly two decades of its existence, the IRDP pro-gramme has extended credit to 55 million families (not 55million different families due to many repeat loans). The repay-ment rate in the IRDP programme has been abysmal — in thevicinity of 25–33 per cent with the result that the amount ofloanable funds is not as large as it could be due to poor recyclingof funds thereby possibly reinforcing the Indian banker’s notionthat the poor are not credit-worthy and lastly for the ruralperson, ‘government loans’ and ‘subsidies’ have become synony-mous. The IRDP programme also included as part of the loanpackage a subsidy which has 25–50 per cent of advance. Asubsidy, like loan forgiveness, is warned against by microcreditexperts, the world over, which was institutionalized in the IRDPscheme. Most practitioners and other experts agree that mixingsubsidies and loans is not a sound practice. However, the shareof government programmes in the small borrowal accounts(SBAs) of commercial banks, has increased by 15 per cent inamount outstanding between 1993 and 1997 (Nair 2000).

IRDP alone created over 40 million defaulters and nearlyone million cynical bankers. It led to the inevitable — loanwaiver by the central government in 1989 under the Agricultureand Rural Debt Relief Scheme. The massive failure of IRDPand its allied programmes forced the government to overhauland restructure them. The central government came up witha new holistic self-employment programme called SwarnjayantiGram Swarojgar Yoja (YGSY) which was launched on 1 April1999, replacing all the earlier self-employment programmes.

3.1.2 Priority Sector LendingAfter bank nationalization the vast banking system apparatuswas used to advance credit to the rural population and func-tioned as the conduit for poverty alleviation schemes under theFive Year Plans and the IRDP. The RBI’s stipulation that atleast 40 per cent of the bank advances must be made towardsthe so-called priority sectors was important in two very different

12 Microfinance Regulation in India

ways. Firstly, the developmental goals of the government andits intention to use the banks to achieve those goals were maderealizable that is the bank had to function beyond its ‘typical’role, in a development oriented capacity. Secondly, by specifyingthe amounts to be lent to the priority sectors (18 per cent foragriculture, 10 per cent for the weaker sections and so on), thedecision making powers of the bank were severely curtailed.Consequently, the bank while doing directed lending, aimed tomeet targets in terms of amounts advanced against guidelinesstipulated by the RBI. The Agricultural Credit Review Com-mittee states in its report that, ‘They [Commercial Bank man-agers] have been reduced to the position of mere instrumentsto carry out the instructions of governmental functionaries atthe local level’ (1993).

3.1.3 Regional Rural Banks and the outreach of formal institutions

Financial services in the rural sector are provided mainly byaround 33,000 branches of the commercial banks and the 196RRBs. The Banking Commission felt the need for a specializednetwork of bank branches to cater to the needs of the rural sectorand subsequently the GoI in 1975 instituted the Regional RuralBank. The performance of these banks has been dismal but partlydue to political pressure, the RRBs and commercial banks arelikely to maintain their position in the rural credit scene. TheUnion Budget Speech of 2000 stated that: ‘Due to our efforts atrecapitalizing RRBs, 158 RRBs are posting operating profits.Out of these 48 RRBs have been able to wipe out their accumu-lated losses. In view of the importance of the RRBs in ruralfinancing, we will continue with this programme of strengthen-ing the RRBs.’ Despite the decision to support the RRBs, thefundamental problem of the mechanism of disbursement, loanand subsidy made by the RRBs is not addressed at all.

3.1.4 Causes of poor performance of RRBs and commercial banks

The question arises whether the planned system of rural credit

Rural Credit in India: State Interventions 13

alone has contributed to the existing performance or therewere other factors that contributed to the poor performanceof commercial banks and RRBs in the rural sector? Threefactors requiring consideration are: (a) The bankers from com-mercial banks probably did not perceive the rural agriculturalsector as a bankable segment of society which is substantiatedby the percentage of funds advanced to agriculture over 1985–95. In 1985 over half the credit in rural areas wa given toagriculture. A decade later after the economic crisis when thebanks had to perform and mindful of fiscal prudence, theamount advanced to agriculture was around 11 per cent (Nair2000). Similarly the total amount outstanding in SBA accountsdecreased from 19.8 per cent of total amounts in all accountsto 14.2 per cent. Such significant declines suggest that thecommercial bankers did not consider agriculture as a profitablebusiness for them. Therefore, bankers by training and mind-set, are as yet not capable of managing investments in ruralareas. (b) The process of personnel recruitment in the RRBs,devised to address the needs of rural areas did not give expectedresults. The RRBs hired a lot of their personnel from ruralareas under the assumption that rural people are much moreattuned to the needs of people in their regions. The qualityof the recruits did not match with other bankers and were notcompetent bankers and managers. According to some bankersdespite a pay scale which was on par with the well-trainedurban bankers; absence of or few transfers and lower cost ofliving unlike their urban counterparts, the local people re-cruited at the RRBs were equally apathetic to the issues ofrural credit and poverty alleviation as were the commercialbankers. (c) Politicians periodically ran what were known as‘loan melas’ — waiving debts for political gain and votes duringelection. The local politicians and relatively well-to-do in therural areas appropriated funds set aside for the marginalizedsegments of the rural population. The politicians acquiredleverage as these were government administered programmes.Fortunately, open loan melas do not happen anymore, but thedamage they have done to credit discipline is lasting and is

14 Microfinance Regulation in India

yet another hindrance that MFIs face while conducting theirbusiness in rural areas.

3.1.5 NABARD and SHG-bank linkage programmesIn 1992, NABARD issued policy guidelines for bank linkageswith Self Help Groups (SHGs). Bank managers were initiallyreluctant to use the new lending technology that is, the useof joint liability groups (which is the status of SHGs in themicrocredit context) instead of collateral for the loans. Thisprogramme has so far been very successful mainly due topromotion of these SHGs by many NGOs. The formation ofSHGs is a difficult and costly task requiring intensive effortsin identifying groups of people with common interests andsubsequent training of these groups. The cost of group for-mation has thus far been subsidized by the NGOs throughtheir grants which in the future should be worked into theoverall transaction cost. However, NABARD is likely to linkas many as 50,000 SHGs to banks this year.

The Union Budget Speech of 2000 highlights another dis-turbing trend in the government policy. NABARD and SmallIndustrial Development Bank of India (SIDBI) which set tar-gets for government agencies in SHG coverage have to coveran additional 100,000 SHGs in the year 2000–2001 despite thefact that group formation is not an easy task. Experience ofbanks shows that in one of the Gramin Banks where the man-agers were motivated to form groups, a total of 15 groups wereformed (seven by managers and the rest by other staff). Of the15 that were formed, six were already defunct (Srinivasan andSatish 2000). None of the bank staff had experience in groupformation and formed ideas on group formation from the cir-cular issued by the Head Office and periodical discussions withthe officials at the Head Office.

A recent development is the formation of groups by DistrictCollectors. It is unlikely that civil servants are trained tooperate at grass-root levels in the manner of NGOs hence thefailure rates in those groups is likely to be on par with thegroups formed by bank branch managers. Target setting for

Rural Credit in India: State Interventions 15

government agencies reflects policy orientation at the Centrewhich does not specify amounts to be disbursed to varioussectors, and instead specifies the number of borrowing groupsand does not address the incentive structure for bankers.

Some of the confusion in the government regarding policyis reflected in some ways in the structure of NABARD andSIDBI. NABARD is an apex organization with two duties ofsupervising the banks and co-operatives providing rural financialservices, and functioning as a refinance institution responsiblefor promoting microfinance. The obvious conflict of interestbetween the two responsibilities is heightened when targetshave to be met, thereby exacerbating the ‘identity crisis’ facedby NABARD. As NABARD lacks adequate manpower forbuilding the capacity of SHGs the enormous amount of fundsheld by it, have largely remained unutilized since the last fouryears.

3.2 Co-operatives 3.2.1 Government control of co-operativesIn India, formal rural credit and its regulation, beyond the failedlaws enacted for taccavi 1 loans to farmers, began with the es-tablishment of Co-operative Societies Act in 1904. But even adecade before that, societies were established which put intopractice the principles of cooperation and mutual benefit. Fromthe late 1890s to the late 1950s, co-operatives were the mainformal source of credit to the rural poor. Co-operatives duringthe pre-Independence era, were in many ways an extension ofthe government. Interference from the government diluted thegoverning principles of the co-operatives. In 1928 the RoyalCommission on Agriculture recommended the expansion ofrural credit with state patronage using co-operatives as conduitfor credit. Furthermore, the principles of ‘one-member one-vote’ and mutuality were corroded as co-operatives were usedby stronger members to misuse the co-operative for personal

1. Introduced by the British in 1793 for ensuring stability in revenue collec-tion for farmers and subordinate tenants.

16 Microfinance Regulation in India

gain leading inevitably to malfunctioning co-operatives andfinally in 1945, to the recommendation of the liquidation ofassets of the co-operatives by the Agricultural Finance sub-committee. A decline in the faith in a co-operative damagedcredit discipline. To make matters worse, the co-operativeswere protected from competition. These problems of moralhazard often cited in economic literature prominently figurein issues of regulation.

The Post-Independence scenario was no better with the AllIndia Rural Credit Survey in 1954 recommending majorityparticipation at all levels by the state in co-operatives. Stateintervention caused the same problems as before and added afew more in the post-Independence era. In places like TamilNadu, the co-operative functioned as a source of illicit fundingfor politicians at many levels. Currently approximately 94,000co-operative outlets exist either in the form of branches orvillage level societies under the supervisory authority ofNABARD. In addition, the Rotating Savings and Credit Asso-ciations (ROSCAs), Chit Funds, Nidhis and other ‘informal’means of obtaining financial services, imply that the amount ofcredit extended and savings mobilized should be huge but anenormous gap continues to exist in the demand and supply forthe same financial services.

3.2.2 Mutually Aided Co-operative Societies (MACS) ActOnly in the post-liberalization era, when the Khusro Commit-tee in 1991 recommended a less interventionist and more mar-ket-oriented approach for co-operatives and when the BrahmPrakash Committee in 1991 advocated a model Co-operativeSocieties Act, was there relief in the sad history of the Indianco-operative movement.

This study does not consider the variations among states andother intricacies of the system, which have an impact on themodels implemented in various regions. Andhra Pradesh en-acted the Mutually Aided Co-operative Societies (MACS) Act in1995. Co-operatives formed under this act are largely immunefrom government intervention and a number of co-operatives

Rural Credit in India: State Interventions 17

have been formed under this Act. While in neighbouring TamilNadu, the co-operative act allows for a great deal of governmentintervention. The co-operative cannot even enact its own bye-laws and must adopt bye-laws given by the state of Tamil Naduwhich were formulated in pre-Independent India where theco-operative was an extension and victim of the government. Inaddition Tamil Nadu has its own Societies Act which gives thegovernment the power, under certain circumstances, to takecontrol of an organization registered under the Act. Hence inTamil Nadu, the co-operative movement is naturally not asrobust as it is in Andhra Pradesh. Some prominent MFIs haveadopted variants of the Grameen model for lack of satisfactoryalternatives.

Following Andhra Pradesh, three states — Bihar, MadhyaPradesh and Jammu & Kashmir, have enacted similar MACSActs. However, they are considered by many to be weaker formsof the Andhra Pradesh MACS Act. Far fewer co-operatives havebeen formed in these states as compared to Andhra Pradesh.Registering under a particular Act is only one aspect of regula-tion. Issues requiring attention are whether the act of registra-tion in itself prevents anomalies from occurring in the financialsystem and does the MACS Act in itself guarantee that theco-operatives will function properly? While recognizing thedifferent characteristics of thrift co-operatives and consumerco-operatives (just as the characteristics of banks and manufac-turing businesses are different) they certainly should not comeunder a similar regulatory regime. This argument is based on theprinciple of regulating the activity and not the institutional form.

3.2.3 Is an enlightened Co-operative Act sufficient for ensuring stability of the financial system?

The MACS Act lays down rules of conduct between the mem-bers of a co-operative and the member–board and specifies therules of conduct between the co-operative and the externalworld. A co-operative registered under this Act has to reportall transactions to the Registrar of Co-operatives. For an aver-age co-operative, several thousand transactions may have to be

18 Microfinance Regulation in India

reported. In terms of reporting then, the co-operative in Indiais not given the same privileges as a microfinance institution.The reason for this is clear — a co-operative should be fundingitself through the deposits that it mobilizes. Given the largenumber of thrift co-operatives that are being formed, the ideathat the Registrar of Co-operatives or NABARD are able toproperly supervise them is not credible. The Income Tax De-partment and the Home Ministry (under FCRA) will be effec-tive to a certain extent only as ‘supervisory’ authorities. Whileco-operatives developed with the help of an institution like theCo-operative Development Foundation in Andhra Pradesh willbe functioning well, they will not constitute the majority ofco-operatives in the state. With the emergence of appropriateincentives, it might be a matter of time before politician con-trolled MACS emerge.

Lack of proper regulation has been blamed for many of theills afflicting the banking system in India. It is not the lack ofadequate regulation but the ex-post control nature of the legalsystem posing problems for the banking system. Numerouslaws govern all aspects of organizations and strictly prescribethe relationships between the members of the organization, therelationship between the members and the governing body, thegoverning body and other external bodies. The legal system isex-post control. Once fraudulent behaviour has occurred, thereis recourse to the legal system. Perpetrators might be caughtand punished. The poor often do not have adequate access tothe judicial process and when they do the process can take along time making the fight worthless and expensive to prose-cute perpetrators.

The guiding principle of regulation is the provision of anenvironment where there is no distortion of competition. Un-fortunately, the distortions introduced into the microfinancesector in the process of implementing government policy, withall good intentions, have been enormous. There is no dearthof regulation in India — there are laws for every conceivableeventuality and regulation for a vast array of institutional forms.The state of Indian banks is testament to the damage done by

Rural Credit in India: State Interventions 19

the confusion between policy and regulation. Governmentregulation is particularly not appropriate for the Indian micro-finance sector but the aims and principles of regulation asoutlined earlier are necessary for the survival of the financialsector, and available alternatives need to be considered to en-sure the continued and sustainable functioning of microfinancein India.

20 Microfinance Regulation in India

4

Microfinance Services in India

4.1 IntroductionThe share of supply of credit to rural areas through institu-tional sources has increased substantially since 1971. The AllIndia Debt and Investment Survey (AIDIS) (1991) shows thatout of the total credit supplied to rural households, nearly 64per cent were met by institutional sources as against approxi-mately 30 per cent in 1971. Despite the fact that over theyears there has been an increase in overall outreach and ab-solute disbursement of institutional sources, since 1990 therehas been deceleration in the growth of bank credit to ruralareas. The share of rural credit in total credit disbursed byscheduled commercial banks was about 3.5 per cent in 1971,which steadily grew up to 15 per cent over the two decades.After 1990, the share of rural credit declined steadily droppingdown to 11 per cent the end of 1998. Between 1991 and 1993,the share of bank credit to rural households went up by 22per cent when compared to the rise of 40 per cent and 52 percent to the private and public corporate sector respectively(EPW 1997; RBI 1998).

This decline in the share of rural credit has been coupledwith the increase in the absolute number of poor householdsin the country. Estimated at 75 million, the total credit usageof these households (Rs 6,000 for urban households andRs 4,500 for rural households) works out to a staggeringRs 45,000 crores demand which has led to the emergence ofmany new institutional forms.

4.2 The Task Force on Microfinance Regulation The increase in the number of NGO–MFIs, which borrowfunds for on-lending and possess loan portfolios of more thana million Indian Rupees, has posed the challenge of estab-lishing a framework signalling the stability of the market andthe provision of service. Hence a National Task Force onSupportive Policy and Regulatory Framework for Microfi-nance (NABARD 1999) (Task Force), was established whichclosely examined four main issues relating to: (i) the main-streaming of NGOs and other emerging institutions; (ii) theregulation and supervision of these bodies; (iii) organizationalfeatures; and (iv) requirements to increase capacity for growthand service.

On the specific issues of the emerging diversity in mi-crofinance, the Task Force recommended establishing thresh-olds for different functional roles undertaken by NGOs.The following broad categories and recommended thresholdsare:

1. MFIs purveying credit only;2. MFIs purveying credit and mobilizing savings from the

clients/loanees (below cut-off limit of Rs 2 lakhs); 3. MFIs purveying credit and mobilizing savings from the

clients/loanees (above cut-off limit between Rs 2–25lakhs); and (10 per cent reserve requirement in the formof bank deposit and rising to 15 per cent as and whenthe deposits go past the Rs 25 lakh ceiling);

4. MFIs purveying credit and mobilizing savings from theclients/loanees and general public.

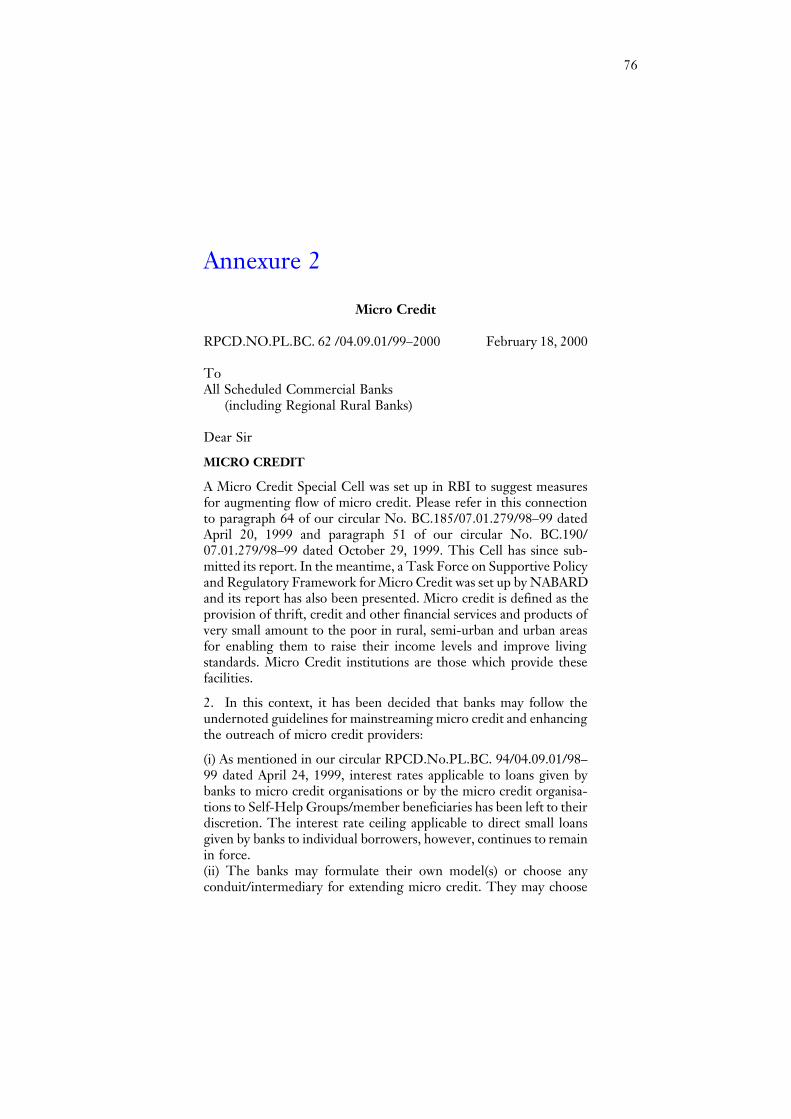

Though the RBI has not made specific announcementson business volumes and thresholds it has made other legaland operational policy pronouncements. Microfinance agen-cies can develop products with banks — credit and savings,at rates and terms acceptable to both parties, irrespective oflegal form of the promoting microfinance agencies (RPCD.No. PL.BC. 62/04.09.01/99–2000 dated 18 February 2000).

22 Microfinance Regulation in India

(Annexure 2). The RBI has also exempted the not-for-profitcompany, (Sec 25) (DNBS. 138/CGM (VSNM) dated 13January 2000) (Annexure 3) providing micro-credit from ful-filling NBFC norms, provided they do not mobilize deposits.By expressing its neutrality to any form of organization andfocussing on the activity, the RBI has indicated the direction,which it will possibly take to build its microfinance framework.

4.3 Emerging Microfinance Institutions in IndiaIn recognition of the demand for financial services among thepoor, over the past few years (MFIs) have evolved systems thatallow for the poor to receive credit supply. Today, this pro-vision of credit and other services is reaching a critical sizeforcing NGO-MFIs to take new forms and establish newlinkages.

4.3.1 Legal Forms of MFIsThese new MFIs can be broadly divided into three categorieson the basis of the legal form adopted by them:

1. Not for Profit MFIs such as societies registered underSocieties Registration Act, 1860 or similar State Acts;Public Trusts registered under the Public Trust Act,1882, and Section 25 companies of the Companies Act,1956;

2. Mutual Benefit MFIs include co-operative societies reg-istered under the Co-operative Societies Act of the re-spective state or the central Multi-State Co-operativeAct, 1984; Mutual Benefit Trusts or Nidhis under Sec620 of the Companies Act, 1956; and

3. For Profit MFIs that includes NBFCs registered underthe Company Act, 1956 (Mahajan et al 2000).

Among these forms of organizations, only NBFCs and Co-operative banks are regulated by RBI as financial intermediarieswhile the rest are de facto financial intermediaries requiringminimal regulatory compliance.

Microfínance Services in India 23

4.3.2 Operating Models of Retail MFIsIrrespective of their legal form, the retail MFIs in India haveadopted a wide spectrum of operating models of which the mostprominent are (adapted from Arunachalam 1999):

1. The Self Help Group (SHG) model: SHGs tend to behomogeneous in nature (either caste, occupational orregional). The SHG lends money to its members bothfrom members’ savings as well as money mobilized fromexternal sources. NGOs mobilize clients into SHGs andprovide savings and credit services. Linkages with thelocal banks are also arranged for credit purposes.

2. The Federated SHG model: SHGs are federated into aninstitution in any of the following ways:

(a) SHGs are registered as co-operatives in states wherean enabling co-operative environment exists.

(b) Some small SHGs operate as solidarity groups byadapting the Grameen model and in turn are feder-ated into large co-operatives.

(c) Within this broad structure there can be many op-erating variations depending on the strategy of thepromoting NGOs and the juncture at which theyopen and manage bank accounts.

3. Urban Co-operative Bank model: Direct lending to cli-ents in urban areas through an Urban Co-operativeBank. Two prominent examples are the SEWA Bank inAhmedabad and the Cuttack Urban Co-operative Bankin Orissa.

4. Trade based group model: The establishment of a struc-ture which manages ‘typically industrial’ activity, and

5. The eclectic NBFC model.

4.4 State Regulated Microfinance IntermediariesThere are very few regulated microfinance intermediaries inthe country. Institutions in this category are (NBFCs) andCo-oper-ative Banks who have to comply with and fulfil the

24 Microfinance Regulation in India

stipulated regulatory requirements. The limitation of the ex-isting regulation is that it does not take into considerationportfolio related characteristics arising from microfinance re-lated services with the result that compliance is high cost andrestrictive.

4.4.1 NBFCsNBFCs are registered under the Companies Act, 1956 andregulated by RBI. Under the RBI (Amendment) Act, 1997, itis mandatory for NBFCs to get a Certificate of Registrationfrom RBI, which is granted only if a NBFC has a minimumNet Owned Fund (NOF) of Rs 25 lakhs and for a new NBFC,Rs 2 crores. To protect the interests of depositors, the RBI hasintroduced strict regulations for NBFCs such as the mainte-nance of a minimum standard of NBFC, rating by approvedrating agencies, capital adequacy and liquid assets as prescribedby RBI. The prominent NBFCs who also work among the poorare BASIX, Hyderabad; Sarva Jana Seva Kosh, Chennai; Sang-hamitra, Bangalore; SHARE Microfin Ltd, Hyderabad; CFTS,Mirzapur (UP); Indian Association of Savings and Credit(ISAC), Marthandam, Tamil Nadu.

4.4.2 Co-operative Banks In the co-operative banking segment engaged in microfinanceamong the poor, in addition to the SEWA Bank, Ahmedabad,the latest entrant is the Cuttack Urban Co-operative Bank.The SEWA Bank is registered as co-operative society withbanking license from the RBI. SEWA Bank started with 4,000shareholding members in 1974 and by the end of 1998 it hadmore than 26,000 shareholders. The total loans outstandingin 1998 were about Rs 86.6 million and total deposits wereRs 171 million. Although as a bank, a co-operative bank hasmany advantages over NBFCs, the dual control of Registrarof Co-operatives (ROC) and the RBI has in many ways re-stricted these institutions in achieving their full potential. Itis now time to remove the unnecessary control of the ROCor alternatively the ROC regulates only the institutional aspect

Microfínance Services in India 25

of the co-operative bank while the RBI regulates the functionalaspect. The committee under Deputy Governor, RBI, JagdishKapoor to suggest measures to strengthen the co-operativebanking movement in India submitted its report in July 2000,in which several legislative reforms to strengthen co-op bankswere suggested. The recommendations of the committee areyet to be accepted.

4.5 Unregulated Microfinance IntermediariesMany financially unregulated entities provide microfinance ser-vices, whose important features are delineated in this section.

4.5.1 NGO-MFIsRegistered as Societies or Trust Acts or Section 25 Companies,the entire swathe of NGO-MFIs choose to function as one ofthe following:

1. Specialized Service Providers — These institutions are ex-clusively working as MFIs, with a minimal provision ofother services such as health or education. The domi-nating framework in the establishment of policy and theinvestment of resources is determined by the need toprovide efficient services. Within this category, thereexist two sub categories, (a) one which provide retailMicrofinance services like savings, lending money etc.to the poor, especially their members and raise fundsfrom members and other financial institutions, (b) onewhich function as Microfinance Wholesalers or ApexBodies, giving financial support to the smaller institu-tions (retailers) providing Microfinance services.

2. Multi-service Providers — In the Indian scenario, a largenumber of NGOs registered either as societies or trustshave taken up Microfinance services as an extension oftheir community development programmes like provid-ing health services, education, income generation, envi-ronment etc. In this case microfinance is either bundledwith existing social intervention or occupies a position

26 Microfinance Regulation in India

equal to or less than the dominance of other program-mes.

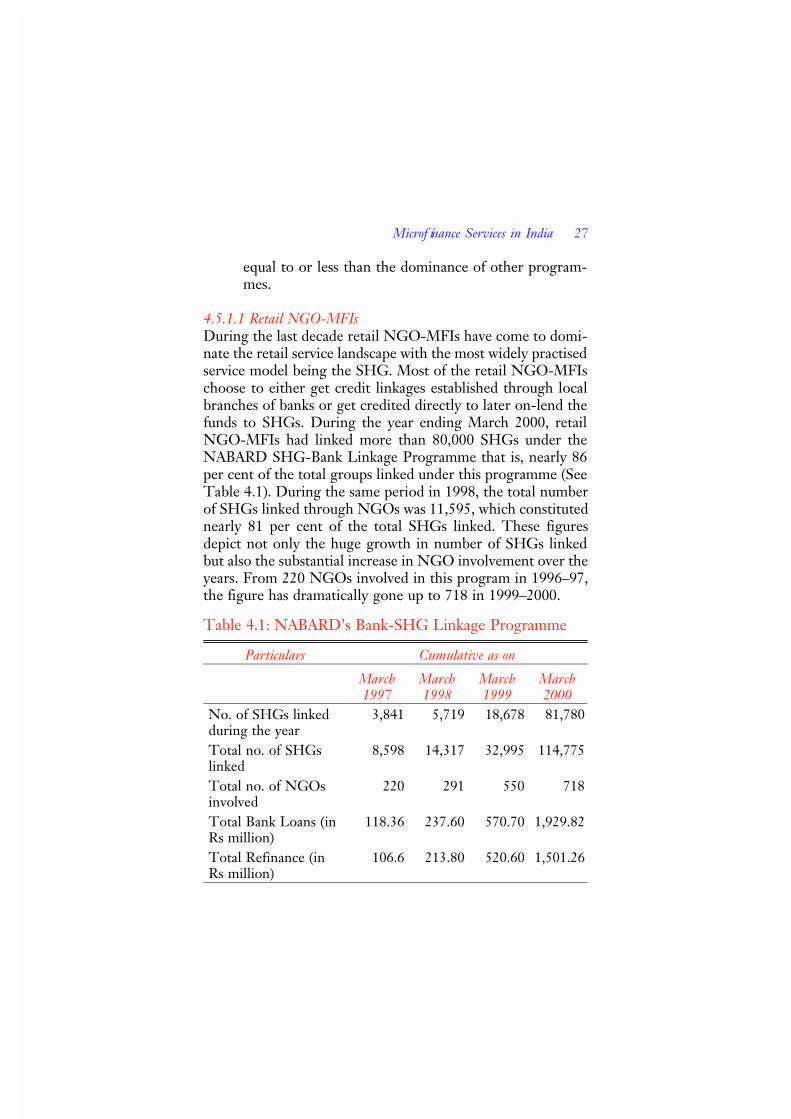

4.5.1.1 Retail NGO-MFIsDuring the last decade retail NGO-MFIs have come to domi-nate the retail service landscape with the most widely practisedservice model being the SHG. Most of the retail NGO-MFIschoose to either get credit linkages established through localbranches of banks or get credited directly to later on-lend thefunds to SHGs. During the year ending March 2000, retailNGO-MFIs had linked more than 80,000 SHGs under theNABARD SHG-Bank Linkage Programme that is, nearly 86per cent of the total groups linked under this programme (SeeTable 4.1). During the same period in 1998, the total numberof SHGs linked through NGOs was 11,595, which constitutednearly 81 per cent of the total SHGs linked. These figuresdepict not only the huge growth in number of SHGs linkedbut also the substantial increase in NGO involvement over theyears. From 220 NGOs involved in this program in 1996–97,the figure has dramatically gone up to 718 in 1999–2000.

Table 4.1: NABARD’s Bank-SHG Linkage Programme

Particulars Cumulative as on

March1997

March1998

March1999

March2000

No. of SHGs linkedduring the year

3,841 5,719 18,678 81,780

Total no. of SHGslinked

8,598 14,317 32,995 114,775

Total no. of NGOsinvolved

220 291 550 718

Total Bank Loans (inRs million)

118.36 237.60 570.70 1,929.82

Total Refinance (inRs million)

106.6 213.80 520.60 1,501.26

Microfínance Services in India 27

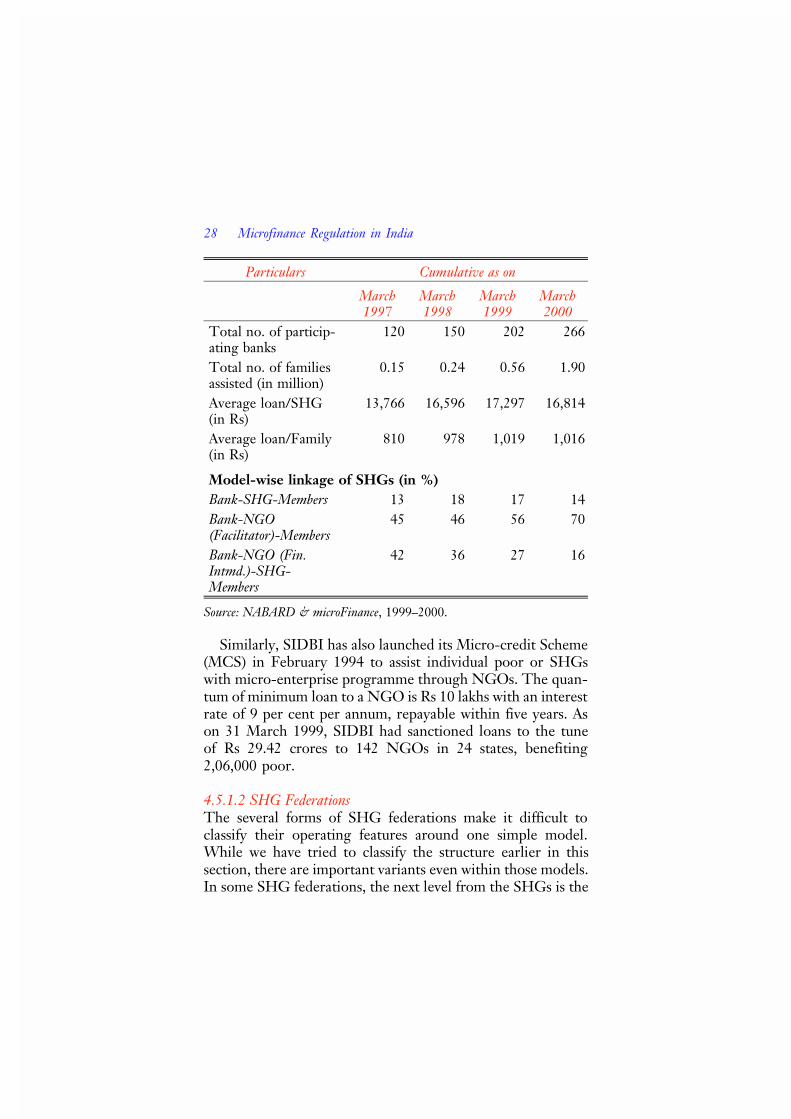

Particulars Cumulative as on

March1997

March1998

March1999

March2000

Total no. of particip-ating banks

120 150 202 266

Total no. of familiesassisted (in million)

0.15 0.24 0.56 1.90

Average loan/SHG(in Rs)

13,766 16,596 17,297 16,814

Average loan/Family(in Rs)

810 978 1,019 1,016

Model-wise linkage of SHGs (in %)Bank-SHG-Members 13 18 17 14Bank-NGO (Facilitator)-Members

45 46 56 70

Bank-NGO (Fin.Intmd.)-SHG-Members

42 36 27 16

Source: NABARD & microFinance, 1999–2000. Similarly, SIDBI has also launched its Micro-credit Scheme

(MCS) in February 1994 to assist individual poor or SHGswith micro-enterprise programme through NGOs. The quan-tum of minimum loan to a NGO is Rs 10 lakhs with an interestrate of 9 per cent per annum, repayable within five years. Ason 31 March 1999, SIDBI had sanctioned loans to the tuneof Rs 29.42 crores to 142 NGOs in 24 states, benefiting2,06,000 poor.

4.5.1.2 SHG FederationsThe several forms of SHG federations make it difficult toclassify their operating features around one simple model.While we have tried to classify the structure earlier in thissection, there are important variants even within those models.In some SHG federations, the next level from the SHGs is the

28 Microfinance Regulation in India

cluster, which gathers self-help groups from a geographic unittogether and in turn federates them into a larger unit calledfederations. In some instances the retail services are undertakenby the SHGs, in others by the cluster and in still others by thefederations. The point of service in this structure finally deter-mines the point of interface with the local bank.1 During thepast few years, community-based organizations (CBOs) areemerging which are directly borrowing from either the gov-ernment or non-government on-lenders and are well on theirway to become full-fledged MFIs.2 These variations result fromthe strategic choices the promoting NGOs make in mobilizingthe SHGs (See Box 4.1).

Box 4.1: State Profiles: Maharashtra and Orissa

State Profiles:What is happening in Maharashtra and Orissa?

Given the diversity in the microfinance sector, gen-eralizations are difficult. Across the sector, the oper-ating differences are large, though the commonelement is the multi-service providing profile of mostof the players with only a few specialized service pro-vider organizations. The variations in the sector arehighlighted by the cases of Maharashtra and Orissa.

MaharashtraThe Maharashtra Rural Credit Programme focussedon providing promotional resources for NGOs to linkSHGs to banks. All the organizations were registeredas either Trusts or Societies and have significant de-velopment experience. While 50 per cent of the or-ganizations have a development presence of more than15 years, only 10 per cent of the organizations were

1. Though the co-operative might be the most appropriate organization, thelevel of potential interference by the government makes organizations preferother legal forms. 2. NGOs like PRADAN, MYRADA, ASSEFA, DHAN Foundation, Chai-tanya, Shramik Bharathi, etc. in different parts of the country have promoteda number of SHGs’ Federations.

Microfínance Services in India 29

less than three years old. Further, 50 per cent of theseorganizations possessed a portfolio of at least fiveprogrammes. In addition most of these organizationshad a small geographical coverage of a maximum offive taluks, and 20 per cent worked in more than 20taluks. In terms of outreach 50 per cent of theseorganizations worked with more than 2,500 clientsbut less than 7,000 clients. Invariably all of them have adopted the SHGmethod to make available both savings and credit ser-vices. The average savings per member accounts tobetween Rs 225 and Rs 375 irrespective of clients ororganization experience because savings are returnedto members after every five years and then savingsare restarted. In doing so, only one organization wasdriving the credit programme with savings mobilized,the rest used the revolving fund from the organiza-tion’s own funds, the bank linkage, and finally bor-rowed from an apex institution, such as FWWB,RMK, SIDBI or HFDC. Thirty per cent amongthese NGOs had promoted federations of SHGs toexclusively manage micro-finance activity but noneof them have been registered as a co-operative.

OrissaAll the organizations are registered under the Socie-ties Act of 1860. While 50 per cent organizationshave a development presence of more than 10 years,of which 30 per cent organizations have more than15 years and the rest are 7–10 years old. Further, 60per cent of these organizations possessed a portfolioof at least five programmes. In addition, most of theorganizations have the geographical coverage of lessthan 500 villages and only 20 per cent organizationswork in more than 500 villages. In terms of outreach,32 per cent of these organizations have more than3,000 members and the rest below 3,000 members. Predominantly, SHG model is followed, except ina few cases, where the co-operative approach is adop-ted. The main source for credit operation is savings.About 56 per cent of the states have mobilized savings

30 Microfinance Regulation in India

of more than Rs 5 lakhs from the members. Othermajor sources for credit operation are bank linkagesand apex institutions.

We believe that over the next few years more efforts needto be focussed on understanding and managing these institu-tions more effectively which will lead to functional claritybetween the NGOs, the federations, and the banks or anyother refinancing arm. We hope that the functional clarity ofdifferent models will stabilize resulting in a better under-standing about the nature of entity and define the inputsrequired to be a optimal firm providing financial servicesefficiently, and intermediating for its clients. Only such acondition will make it possible for the development for anyregulatory effort to succeed.

4.5.1.3 Apex InstitutionsFollowing the recommendation of GoI’s Shramshakti report(1988) the GoI established the RMK in March 1993 to accel-erate the flow of credit to the women to support self-employ-ment, particularly to those in the unorganized sector. Thespecific mandate was to ensure the direct supply of credit toNGOs and bypass the arduous bank process. Apart from theregular lending activity, the fund has resources for capacitybuilding. Till 1999, RMK has supported more than 377 NGOswith the disbursement of Rs 45.22 crores to benefit 2,95,000(The Task Force Report 1999).

RGVN, established in April 1990, with corpuses from theIndustrial Finance Corporation of India (IFCI), Industrial De-velopment Bank of India (IDBI) and NABARD aims to improvethe quality of life of the poor or otherwise underprivileged ruraland urban people through social action. It is registered as anon-profit society under Societies Registration Act 1860.RGVN is working as an indigenous donor agency with smallNGOs and CBOs to promote livelihoods for the poorest peoplein economically least developed regions. It has substantial pres-ence in eastern and northeastern part of the country. It is

Microfínance Services in India 31

working with more than 800 NGOs across 13 states. The totalamount disbursed during the decade was more than Rs 10 crorescovering nearly 53,000 families.

FWWB was established in 1982 as an affiliate of Women’sWorld Banking, New York to promote direct participation ofwomen in the economy through access to financial services.Other intermediaries like BASIX, supporting NGOs on-lendingto SHGs and direct assistance to the beneficiaries are also com-ing up to assist poor with the micro-finance services.

4.5.2 MACS A landmark in the history of the Indian co-operative movementwas created when the Government of Andhra Pradesh (AP)enacted the MACS Act in 1995. Subsequently Bihar, MadhyaPradesh and Jammu & Kashmir enacted MACS Act in theirstates while in many states, it is in pipeline.

Co-operatives formed under this act are largely immune fromgovernment interventions in their affairs such as, fund raising,governance etc. Over 2,000 MACS were reportedly registeredin AP recently. According to the CDF, Hyderabad, 234 thriftco-operative societies (with 59,000 rural men and women mem-bers) promoted by CDF were registered in Warangal district ofAP under MACS Act till December 1999. These MACS providesavings, borrowing and loan insurance services to their mem-bers. So far the MACS have mobilized Rs 837 lakhs exclusivelyfrom their members and in 1999, had lent Rs 1,038 lakhs to40,000 members (CDF 1999). In Bihar, out of 667 societiesformed under the Bihar Self Supporting Co-operative SocietiesAct 1996, only 14 of were credit co-operatives (The Link 2000).We believe that this legislative framework will increasingly beutilised by CBOs to develop as financial intermediaries.

4.6 ConclusionThe failure of the state agencies to provide financial servicesto poor has led to the mushrooming of large number of alter-native financial institutions which have addressed bridging of

32 Microfinance Regulation in India

the wide gap between demand and supply of microfinanceservices. They have designed their operation according to theneeds of the poor customers and demonstrated that even bank-ing with the poor is financially viable. In being responsive theneeds of the poor, many are still innovating the design of thedelivery of the programme which has lead to a large numberof variations in the operating model.

We need to take the next step by understanding the natureof these variations and the causes driving them. While assidu-ously avoiding the dangers of evaluating these models, effortmust be made to understand the minimal possible effort thatwill be required to regulate them. This should serve two pur-poses — one to maintain stability and the other to ensure thatsome of the fly-by-night operators, so prevalent in the countrydo not make an appearance in this sector. Regulation shouldnot serve to limit the growth and presence of genuine andserious players in the market. As per the current trend, the widegap between supply and demand, the growth rate of alternativefinancial institutions will continue to be high in the future.Given the tenuous nature of the balances necessary to maintainit is important that serious attention is paid in establishing theappropriate regulatory context for the microfinance sector.

Microfínance Services in India 33

5

International Experience in Microfinance Regulation

5.1 Different approaches in Microfinance RegulationMicrofinance has been practised around the world in manyforms and by various institutions, ranging from informalROSCAs, NGOs, credit co-operatives, non-bank financial in-stitutions, and commercial banks. The challenge facing regul-ators considering appropriate regulatory approaches iscomplicated by the fact that MFIs range significantly in insti-tutional type, scale of operations, and level of professionalism(Berenbach and Churchill 1997). Given the diversity of eco-nomic and legal environments under which microfinance isprovided, as well as the motivations of actors involved in mi-crofinance, controversy over the manner of regulation andsupervision of microfinance is not surprising. The variety oflegislative proposals, regulatory frameworks, and supervisorypractices the world over reflect this reality (Valenzuela andYoung 1999). Responses to MFIs have ranged from no regu-lation to full external regulation, outlined in Table 5.1.

5.1.1 Initial Steps (No Regulation)Microfinance has generally evolved outside a regulatory frame-work though instances of completely unregulated MFIs arerare, as even NGOs are usually registered with the appropriategovernment authority either as a society, trust, or any otherentity and are usually required to submit a memorandum ofassociation and periodic financial statements to the authority,especially if they are to qualify for favourable tax treatment.

The problem is that such existing mechanisms are neitherenforced vigorously nor driven from the perspective of moni-toring financial intermediary activities. The legal requirementon NGOs does not state whether an NGO is doing a good jobas a financial institution.

Table 5.1: Approaches in Microfinance Regulation

Regulator Supervisor FeaturesInitial steps None None Industry

standardsSelf-regulation Federation

or SROFederation or SRO

Peer pressureto abideincentives/sanctions

Hybrid Statutory body

Third party(federation,accountant,etc.)

Jointappointment

Existing laws Statutory body

Statutory body

Governmentmandate

Special laws Statutory body

Statutory body

Governmentmandate

Source: Adapted from Berenbach and Churchill, 1997.

In some countries, with the maturing of microfinance in-dustry, MFIs have established associations or interest groupsto initiate formalization process. They have initiated a dialoguewith regulators and policy makers to define the appropriateregulatory approach for their environment and supporting theinitiative, they built up databases, defined best practices and,specified industry standards though the adoption of industrystandards is voluntary.