Embed Size (px)

Citation preview

Completion Report

Project Number: 29229 Loan Number: 1805 December 2008

Pakistan: Microfinance Sector Development Program

CURRENCY EQUIVALENTS Currency Unit – Pakistan Rupee(s)

(PRe/PRs)

At Appraisal At Program Completion

At Latest Year-End

At Completion of Program Completion Report

25 August 2000 30 June 2003 31 Dec 2007 30 November 2008 PRs1.00 = $0.0179 $0.0173 $0.0164 $0.0127

$1.00 = PRs56.00 PRs57.65 PRs60.94 PRs78.77

ABBREVIATIONS

ADB – Asian Development Bank ADBP – Agricultural Development Bank of Pakistan AKRSP – Aga Khan Rural Support Programme CIF – Community Investment Fund CGAP – Consultative Group to Assist the Poor CLEAR – Country-Level Effectiveness and Accountability Review CO – community organization DAMEN – Development Action for Mobilization and Emancipation DPF – Deposit Protection Fund ELRF – Emergency Livelihood Restoration Fund FBC – Federal Bank for Cooperatives FSS – financial self-sufficiency GDP – gross domestic product KB – Khushhali Bank MF – microfinance MFB – microfinance bank MFI – microfinance institution MOF – Ministry of Finance MSDF – Microfinance Social Development Fund MSDP – Microfinance Sector Development Program NGO – nongovernmental organization NRSP – National Rural Support Programme OSS – operational self-sufficiency PMN – Pakistan Microfinance Network RMF – Risk Mitigation Fund RRP – Report and Recommendation of the President SBP – State Bank of Pakistan SDC – Swiss Agency for Development and Cooperation TA – technical assistance ZTBL – Zarai Taraqiati Bank Limited 2000 Ordinance – Khushhali Bank Ordinance, 2000 2001 Ordinance – Microfinance Ordinance, 2001

NOTE

In this report, "$" refers to US dollars.

Vice-President X. Zhao, Operations Group 1 Director General J. Miranda, Central and West Asia Department (CWRD) Director R. Subramaniam, Governance, Finance, and Trade Division, CWRD Team leader N. P. Knoll, Financial Sector Specialist, CWRD Team member M. Marcelino, Assistant Project Analyst, CWRD

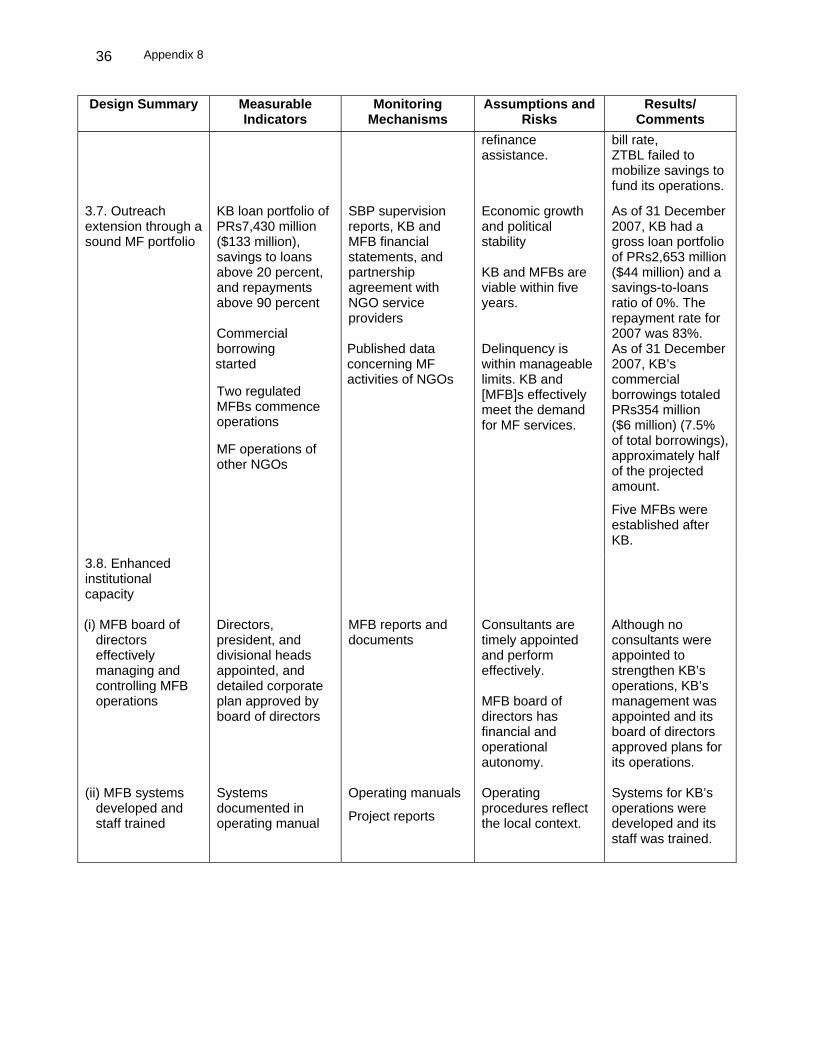

CONTENTS

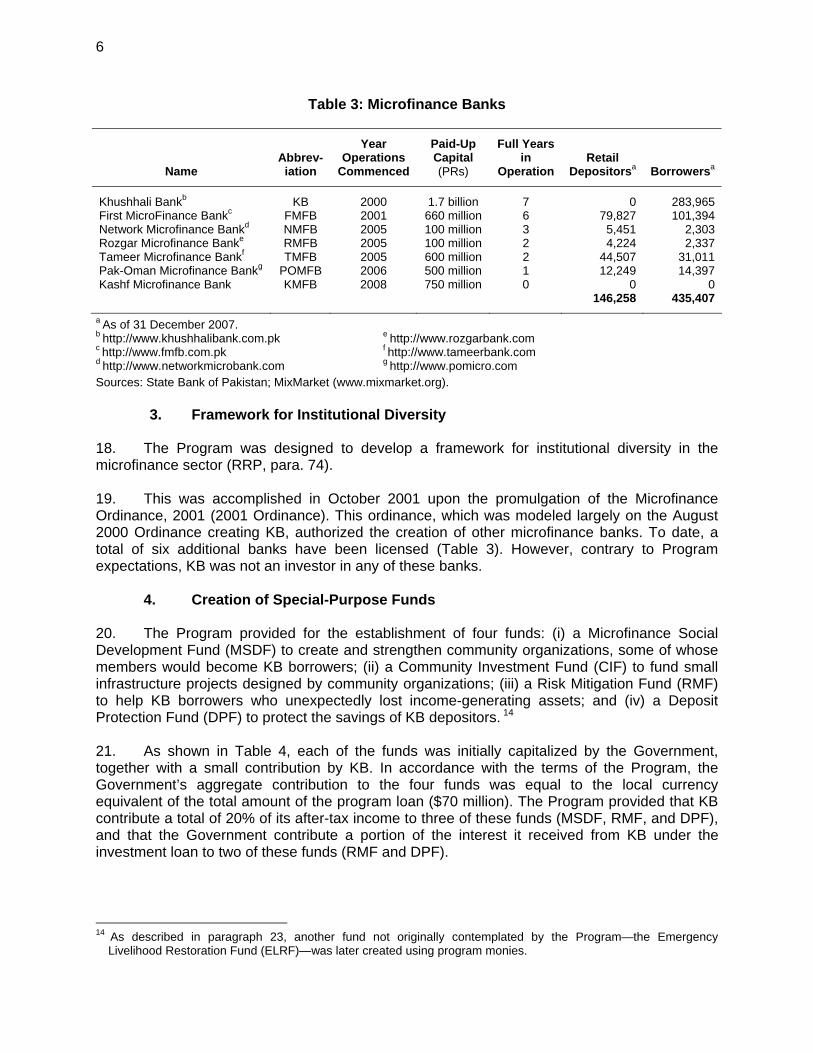

Page BASIC DATA i I. PROGRAM DESCRIPTION 1 II. EVALUATION OF DESIGN AND IMPLEMENTATION 2

A. Program Components 2 B. Program Outputs 3 C. Disbursements 10 D. Program Schedule 11 E. Implementation Arrangements 11 F. Conditions and Covenants 11 G. Related Technical Assistance 12 H. Performance of the Borrower and the Executing Agency 12 I. Performance of the Asian Development Bank 12

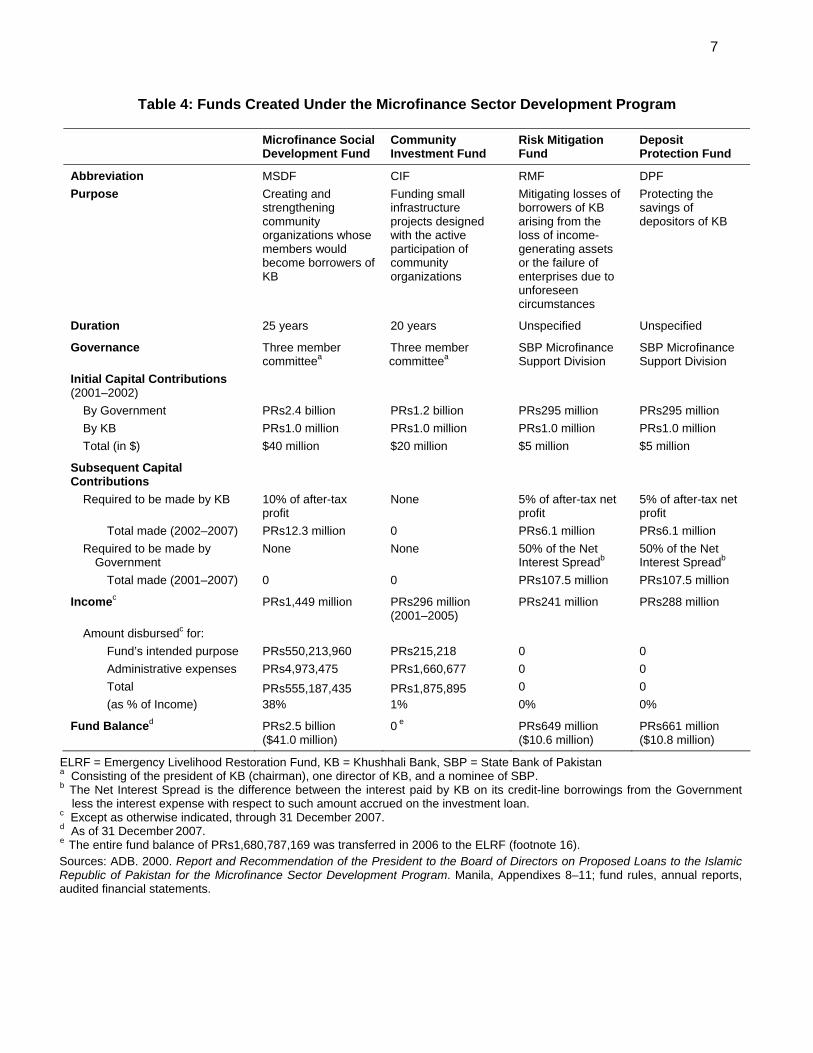

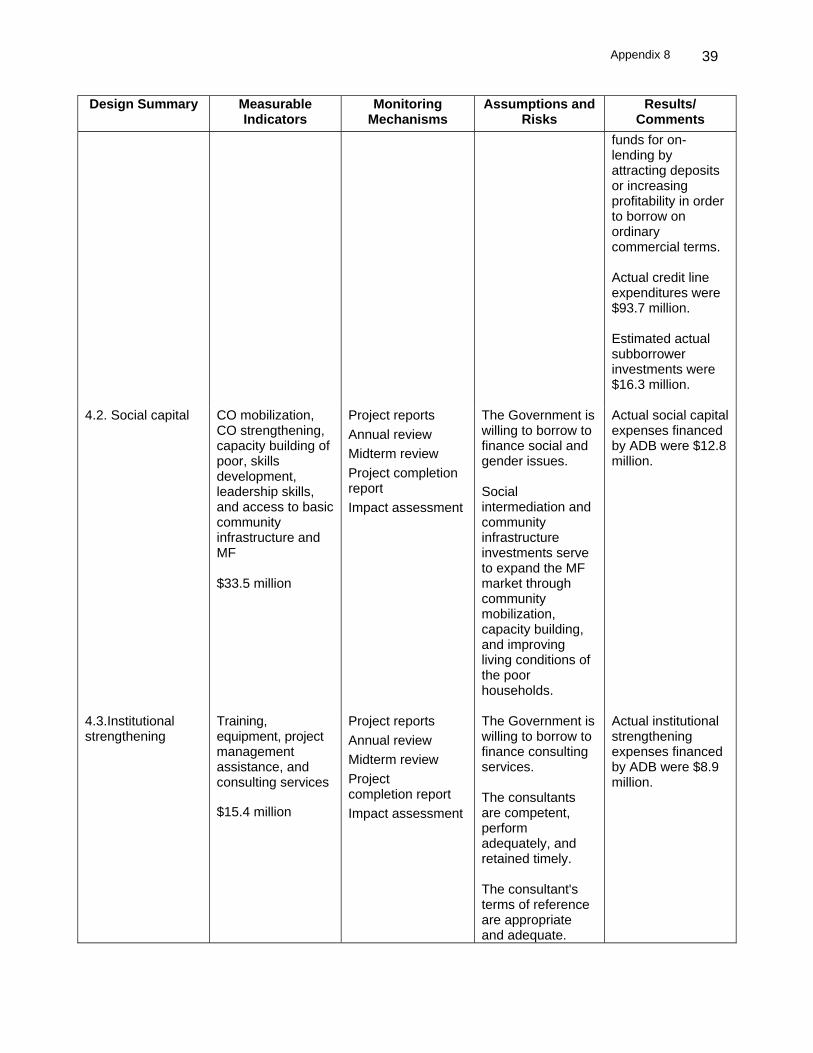

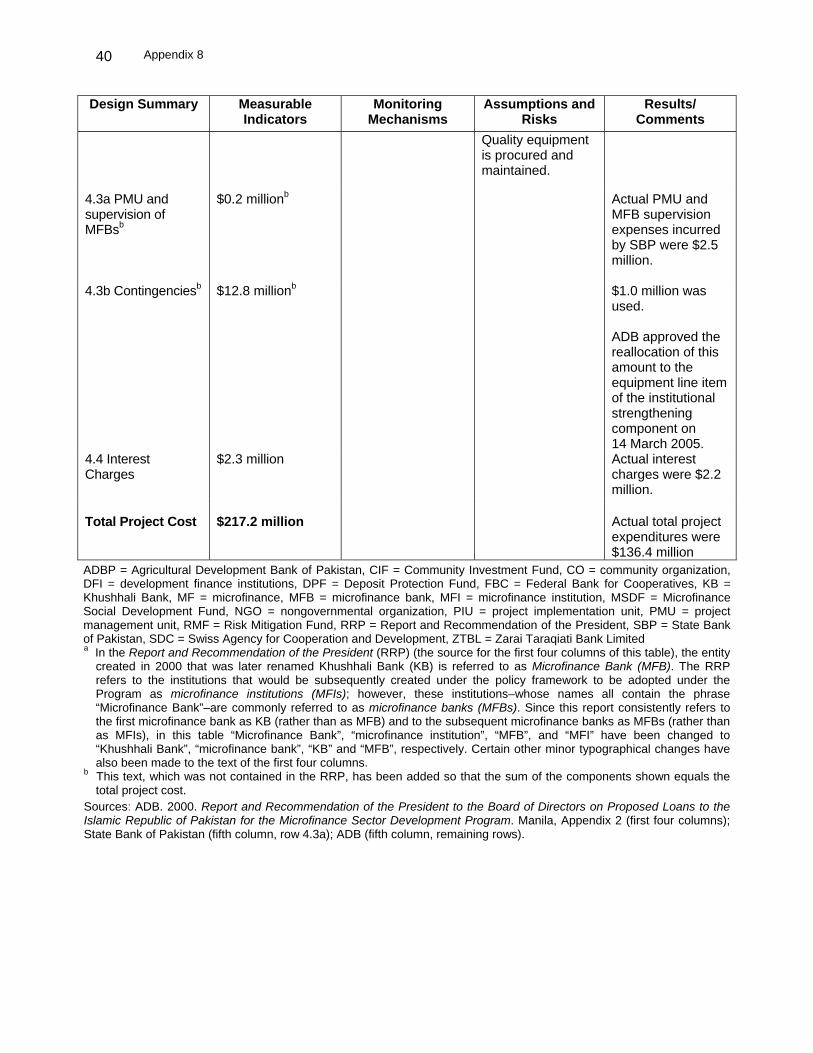

III. EVALUATION OF PERFORMANCE 12 A. Relevance 12 B. Effectiveness in Achieving Outcome 12 C. Preliminary Assessment of Sustainability 13 D. Impact 13

IV. OVERALL ASSESSMENT AND RECOMMENDATIONS 14 A. Overall Assessment 14 B. Lessons Learned 14 C. Recommendations 15

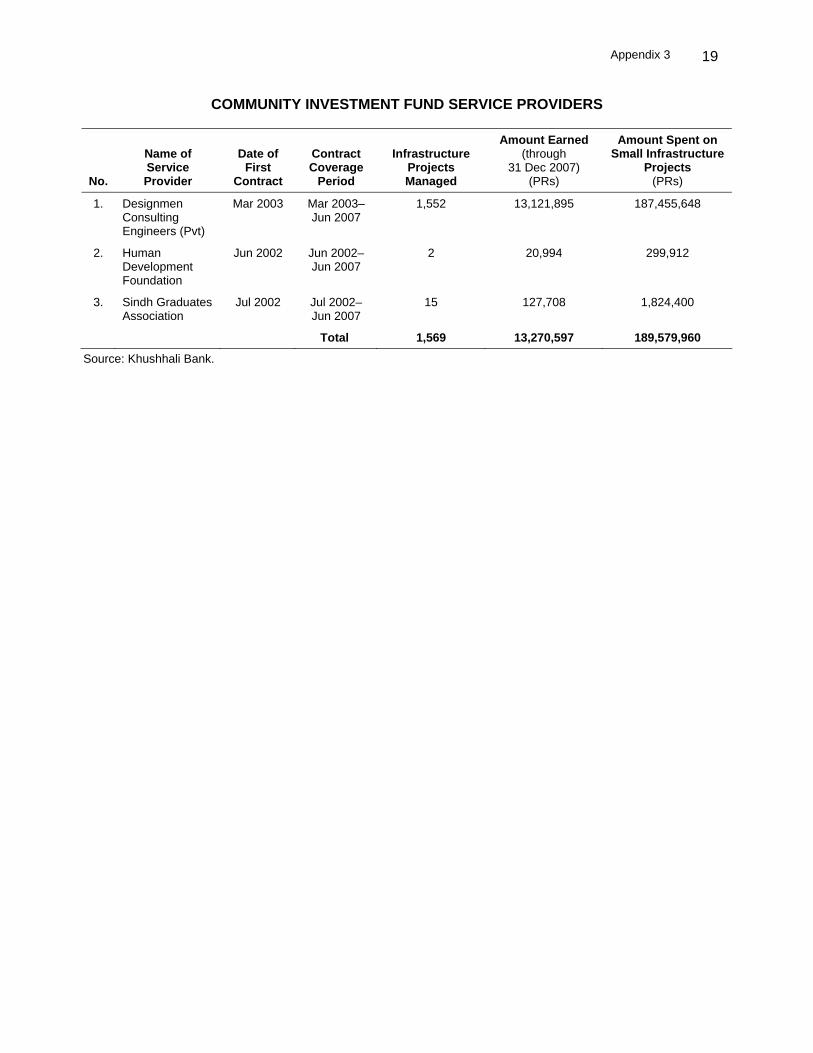

TABLES

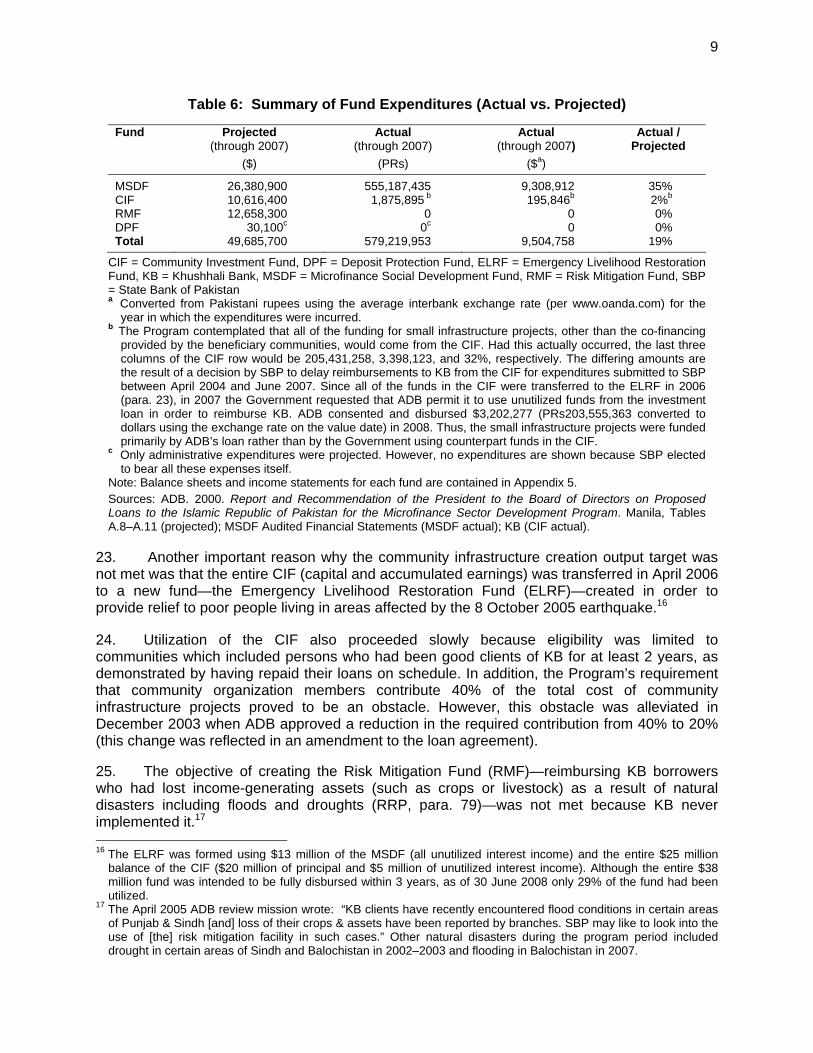

1. Summary of Program Outputs 3 2. Active Clients of Khushhali Bank at Year-End (2001–2007) 5 3. Microfinance Banks 6 4. Funds Created Under the Microfinance Sector Development Program 7 5. Summary of Fund Outputs (Actual vs. Target) 8 6. Summary of Fund Expenditures (Actual vs. Projected) 9 7. Summary of Second Tranche Release Conditions 11

APPENDIXES

1. Circulars Issued by State Bank of Pakistan Regarding Microfinance and/or Microfinance Banks 16 2. Microfinance Social Development Fund Service Providers 18 3. Community Investment Fund Service Providers 19 4. Information on Community Investment Fund Projects 20 5. Balance Sheets and Income Statements of the Funds 21 6. Loan Agreement Covenants 23 7. Sustainability Ratios of Microfinance Banks 29 8. Program Framework 30

BASIC DATA

A. Loan Identification

1. Country 2. Loan Number 3. Program Title 4. Borrower 5. Executing Agency 6. Amount of Loan 7. Program Completion Report Number

Pakistan 1805-PAK(SF) Microfinance Sector Development Program Islamic Republic of Pakistan State Bank of Pakistan SDR54,114,000 PCR: PAK 1090

B. Loan Data

1. Appraisal – Date Started – Date Completed 2. Loan Negotiations – Date Started – Date Completed 3. Date of Board Approval 4. Date of Loan Agreement 5. Date of Loan Effectiveness – In Loan Agreement – Actual – Number of Extensions 6. Closing Date – In Loan Agreement – Actual – Number of Extensions 7. Terms of Loan – Interest Rate – Maturity (number of years) – Grace Period (number of years) 8. Terms of Relending (if any) – Interest Rate – Maturity (number of years) – Grace Period (number of years) – Second-Step Borrower

7 August 2000 25 August 2000 18 October 2000 20 October 2000 13 December 2000 6 February 2001 9 February 2001 9 February 2001 none 30 June 2003 30 June 2003 none 1% during grace period, 1.5% during amortization 24 8 Not applicable Not applicable Not applicable Not applicable

9. Disbursements

a. Dates Initial Disbursement

13 February 2001 (first tranche)

Final Disbursement

23 December 2002 (second tranche)

Time Interval

22 months

Effective Date

9 February 2001

Original Closing Date

30 June 2003

Time Interval

28 months

ii

b. Amount (SDR)

Category Original Allocation

Last Revised Allocation

Amount Canceled

Net Amount Available

Amount Disbursed

Undisbursed Balance

01 54,114,000 0 0 54,114,000 54,114,000 0

C. Program Data

1. Program Cost ($) Actual Cost Appraisal

Estimate First Tranche Second Tranche Total Foreign Exchange 70,000,000 50,000,000 20,909,914 70,909,914 Local Currency 0 0 Total 70,000,000 70,909,914 Note: The difference between the dollar equivalent at appraisal and at disbursement is due to the intervening depreciation of the dollar against the SDR.

2. Cost Breakdown by Program Component ($)

Component Appraisal Estimate Actual Social Mobilization (financed by the MSDF) 40,000,000 40,455,000 Community Infrastructure (financed by the CIF) 20,000,000 20,455,000 Risk Mitigation (financed by the RMF) 5,000,000 5,000,000 Deposit Protection (financed by the DPF) 5,000,000 5,000,000 Total 70,000,000 70,910,000a a $70,909,914 rounded to nearest thousand.

3. Program Performance Report Ratings

Ratings Implementation Period

Development Objectives

Implementation Progress

From 9 February 2001 to 31 December 2001 Highly satisfactory Satisfactory From 01 January 2002 to 31 December 2002 Highly satisfactory Satisfactory From 01 January 2003 to 31 June 2003 Highly satisfactory Satisfactory

D. Data on Asian Development Bank Missions

Name of Mission

Date

No. of Persons

No. of Person-Days

Specialization of Membersa

Appraisal 7–25 August 2000 4 76 a,c,d,e Inception 13–18 February 2001 2 12 a, b Review 13–17 August 2001 1 5 a Review 20–28 December 2001 1 9 a Review 15–26 April 2002 1 12 a Review 12–13 February 2003 1 4 a Review 26 September–

2 October 2004 1 4 a

Review 16–18 April 2005 1 4 a Project Completion Review 15–28 July 2008 2 14 a,b a a = project officer, b = project analyst, c=senior counsel, d=financial analyst, e=social development specialist

I. PROGRAM DESCRIPTION

1. In the 1990s, the number of poor people in Pakistan increased by more than 100%.1 The purpose of the Microfinance Sector Development Program (MSDP) was to reduce poverty by providing affordable, sustainable financial services to the poor2 in Pakistan from institutional sources. 2. The financial services which were included in the Program were borrowing and savings. The premise of the Program was that the poor could improve their lives by increasing their income and financial security. 3. By using borrowed funds to create, expand, or improve income-generating activities, the poor were expected to increase their incomes. These income-generating activities would include trade, manufacturing, services, animal husbandry, and farming. If the additional income that was generated exceeded the cost of borrowing (interest and service charges), the poor could use the excess funds for consumption (especially for items considered socially beneficial, such as food, children’s school fees, and medical expenses) or reinvest them in their income-generating activities. 4. The poor could increase their financial security by having a safe place for their savings. Although some among the poor never have any savings because they immediately consume whatever they earn, most of the poor have some savings at some time during each year. For example, farmers who raise cash crops (such as cotton or sugar cane) typically do not have a steady income and expenditure flow. Rather, they receive all of their income at a single point in time—when the crop is harvested—while incurring expenses throughout the year in the form of consumption and agricultural inputs. 5. The Program was designed to provide affordable financial services. Although this term does not have a precise definition, a loan can be considered affordable if the borrower can obtain the loan when the funds are needed and at a reasonable cost (in terms of time and out-of-pocket expenses), and can make the required payments at the prescribed times. Savings products are particularly attractive if they earn a positive real return. 6. The Program contemplated that these financial services would be provided from institutional sources. Thus, loans and savings products would be provided by institutions rather than by informal sources such as family members and moneylenders. 7. The Program was also designed to provide sustainable financial services. In other words, the income received by the institutional providers of these services would be sufficient to cover the operational and financial costs of providing the services (including loan losses), so that they could operate without periodic or continuing subsidies from the Government of Pakistan or donors. 8. This program completion report provides an overview and evaluation of Program implementation.

1 ADB. 2000. Report and Recommendation of the President to the Board of Directors on Proposed Loans to the

Islamic Republic of Pakistan for the Microfinance Sector Development Program (RRP). Manila, p. ii. 2 The RRP does not define “poor.” But see footnote 8.

2

II. EVALUATION OF DESIGN AND IMPLEMENTATION

A. Program Components

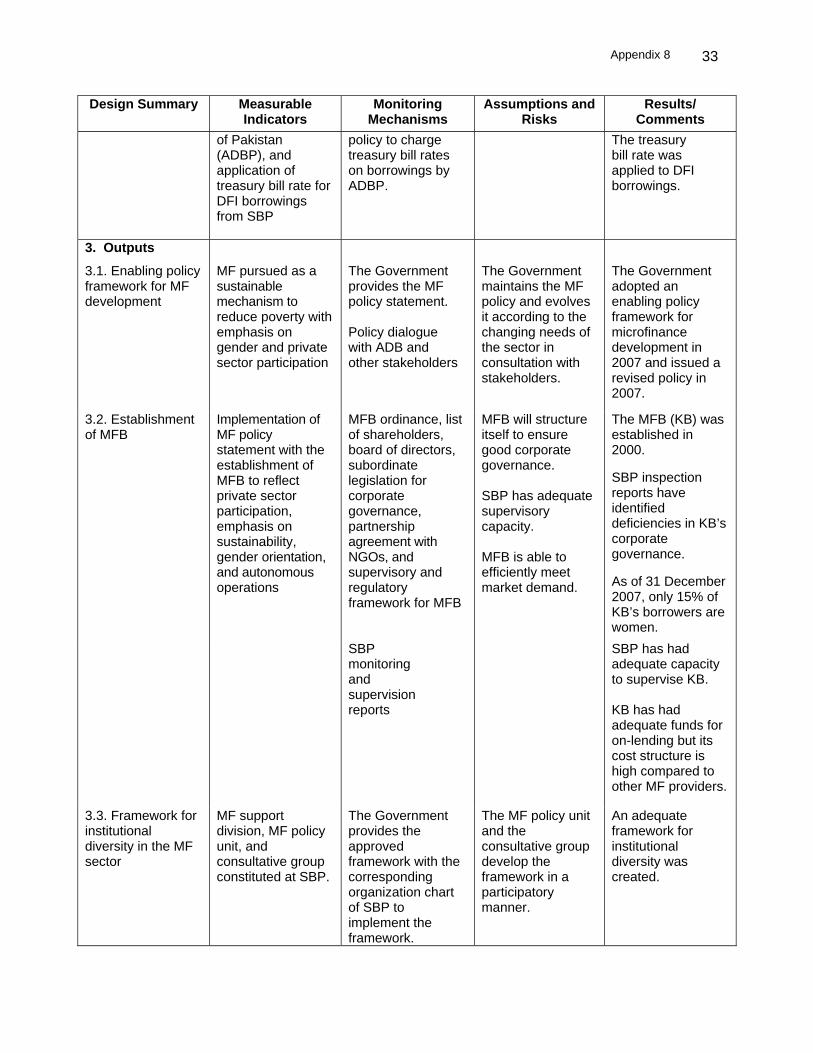

9. The Program was designed to provide sustainable microfinance services to the poor through an integrated policy and investment package. Its design was consistent with the strategies of the Government and ADB regarding poverty reduction and microfinance.3 The Program had ten components:

(i) developing government policies, laws, and regulations that would facilitate the growth of microfinance services in Pakistan;

(ii) establishing and providing long-term funding for a lead microfinance bank—Khushhali Bank (KB)—whose success would catalyze the establishment of additional microfinance banks;

(iii) developing a framework for the establishment and supervision of these additional microfinance banks;

(iv) establishing and maintaining a fund for the benefit of depositors of the lead microfinance bank in the event of its insolvency;

(v) providing financial assistance to clients of the lead microfinance bank whose income-generating assets are lost due to unforeseen circumstances beyond their control;

(vi) creating basic community infrastructure for poor people; (vii) enhancing the ability of the poor, especially women, to effectively utilize

microfinance services by organizing them into groups commonly known as community organizations, a process known as social mobilization;

(viii) initiating the restructuring of two development finance institutions—the Federal Bank for Cooperatives (FBC) and the Agricultural Development Bank of Pakistan (ADBP)—whose politically influenced operations were believed to be retarding the entry into rural areas of other providers of microfinance services;

(ix) strengthening the ability of the lead microfinance bank to achieve its mandate of providing a full range of financial services to the poor by providing it with grants; and

(x) strengthening the ability of the State Bank of Pakistan (SBP) to achieve its mandate of effectively supervising and regulating microfinance banks by providing it with capacity-building grants (RRP, paras. 69-84).

10. The Program, which was designed in 2000, consisted of a $70 million equivalent program loan [1805-PAK(SF)] and an $80 million equivalent investment loan [1806-PAK(SF)]. The $50 million first tranche of the program loan was disbursed upon loan effectiveness in 2001. The $20 million second tranche was disbursed two months ahead of schedule in 2002 after the five conditions for disbursal were fulfilled (paragraph 33 and Table 7). Disbursements under the investment loan began in 2001 and ended in 2008. Most of the proceeds of the investment loan

3 ADB. 2000. Finance for the Poor: Microfinance Development Strategy. Manila. ADB. 1999. Country Operational

Framework for Pakistan, 1999-2000). Manila, http://www.adb.org/Documents/CAPs/2000/ pak.pdf.; Government of Pakistan. 2001. Pakistan Interim Poverty Reduction Strategy Paper (I-PRSP), Islamabad, paras. 117, 119, http://www.imf.org/External/NP/prsp/2001/pak/01/113001.pdf.; Government of Pakistan. 2003. Accelerating Economic Growth and Reducing Poverty: The Road Ahead (Poverty Reduction Strategy Paper), Islamabad, paras. 5.176–5.181,http://www.imf.org/external/pubs/ft/scr/2004/cr0424.pdf?bcsi_scan_D4A612CF62FE9576=0&bcsi_sca n_filename=cr0424.pdf.

3

were on-lent by the Government to KB at a low rate—the average rate paid on deposits by all Pakistani banks (footnote 23). A separate project completion report has been prepared for the investment loan.4 B. Program Outputs

11. Of the 10 program objectives, four were accomplished, five were partially accomplished, and one was not accomplished (Table 1).

Table 1: Summary of Program Outputs

Output Status Comment

Enabling policy environment established and maintained

Accomplished

Lead microfinance bank provided with subsidized funding in its early years in order to enable it to become operationally self-sufficient

Partially accomplished

Funding was provided, but KB never became operationally self-sufficient.

Additional microfinance banks established Accomplished Six additional microfinance banks were established.

Fund established for protection of depositors of lead microfinance bank

Partially accomplished

The fund was established but was unnecessary since KB did not take deposits.

Assistance provided to borrowers losing income-generating assets

Not accomplished

Basic infrastructure projects created Partially accomplished

Only one third of the expected number of projects were completed.

Social mobilization conducted to stimulate demand for microfinance

Partially accomplished

Although community organizations were formed, none of the proposed training of community leaders was conducted.

Restructuring of two development banks initiated

Accomplished

Institutional capacity of lead microfinance bank enhanced

Partially accomplished

A complete management information system (including a deposit-taking module) was not installed.

Technical assistance provided to SBP for microfinance regulation

Accomplished Although SBP obtained the technical assistance, it elected to utilize an SDC grant rather than borrow funds from ADB.

KB = Khushhali Bank, SBP = State Bank of Pakistan, SDC = Swiss Agency for Development and Cooperation

1. Microfinance Policy 12. Pakistan developed a sound regulatory framework for microfinance during the program period. The Government issued microfinance policies in 2000 and 2007, and ordinances were promulgated in 2000 and 2001 pursuant to which the lead microfinance bank and five other

4 ADB. 2008. Project Completion Report on the Microfinance Sector Development Project in Pakistan. Manila.

4

microfinance banks were established and regulated.5 Amendments to the ordinances were adopted in 2000, 2006, and 2007.6 SBP played a critical role in these activities and issued regulations in a timely manner to govern the operations of the microfinance banks (Appendix 1).7 However, the Government’s microfinance policies have not been adequately supported by financial commitments or a sound implementation strategy. 2. Establishment of Microfinance Banks 13. Prior to 2000, microfinance services in Pakistan had been delivered by nongovernmental organizations (NGOs), cooperatives, multi-sector social service organizations known as rural support programs, the government-controlled ADBP, and three other government-owned microfinance institutions founded between 1971 and 1985.8 The Program contemplated the creation of another kind of legal entity to provide microfinance services—specialized deposit-taking institutions called microfinance banks. Like other banks, microfinance banks would be licensed and supervised by the banking regulator, SBP. Unlike other banks, however, they could legally provide services only to the poor.9 14. The Program contemplated a two-step process in the development of microfinance banks. First, a lead microfinance bank would be created. Second, after the legal framework for this bank was developed and SBP developed the capacity to regulate and supervise it, additional microfinance banks would be licensed to provide microfinance services. The lead microfinance bank was expected to be a strategic investor in these additional microfinance banks (RRP, para. 74). 15. KB,10 the lead microfinance bank, was created by a special law in August 2000.11 The Program contemplated that KB would provide a full range of financial services to the poor

5 ADB. 2002. Progress Report on the Microfinance Sector Development Program in the Islamic Republic of Pakistan.

Manila, para. 8; State Bank of Pakistan. 2007. Expanding Microfinance Outreach in Pakistan. Karachi, http://www.sbp.org.pk/about/speech/governors/dr.shamshad/2007/MF-PM-17-Apr-07.pdf; Micro-Finance Bank Ordinance, 2000 (Ordinance No. XXXII of 2000, Gazette of Pakistan, Extraordinary, Part I (4 August 2000) (“2000 Ordinance”); Microfinance Institutions Ordinance, 2001 (Ordinance No. LV of 2001) (“2001 Ordinance”).

6 The Micro-finance Bank (Amendment) Ordinance, 2000, renamed the 2000 Ordinance as the Khushhali Bank Ordinance and renamed the Micro-finance Bank as Khushhali Bank. Gazette of Pakistan, F.No.2 (1)/2000-Pub. (2 December 2000). Section 18 of the Finance Act, 2006 (Act No. III of 2006, Gazette of Pakistan, Extra (1 July 2006)), amended eleven sections of the 2001 Ordinance and added four new sections. See generally, Syed Mohsin Ahmed and Mehr Shah, Amendments to the Microfinance Institutions Ordinance: Implications for the Sector (Microfinance Regulation and Supervision Resource Center, Essays on Regulation and Supervision, No. 25, October 2007) (“Syed and Shah”), http://www.microfinancegateway.org/files/44639_file_Ahmed_Shah_ Pakistan_FINAL_.pdf. Section 18 of the Finance Act, 2007 (Act No. IV of 2007), Gazette of Pakistan, Extra (2 July 2007), amended sub-section (2) of Section 20 of the 2000 Ordinance to eliminate a provision limiting the president of KB to two three-year terms.

7 The main players involved in developing the 2001 Ordinance were SBP, the Ministry of Finance, and the Ministry of Law, Justice and Human Rights. Syed and Shah, p. 4.

8 These institutions (Small Business Finance Corporation, Regional Development Finance Corporation, and Youth Investment Promotion Society) were amalgamated into the Small and Medium Enterprises (SME) Bank in 2003.

9 Originally, “poor persons” was defined as “persons who have meager means of subsistence and whose total income or receipt during a year is less than the minimum taxable limit for income-tax.” 2000 Ordinance, §§ 2(i), 5(2)(a); 2001 Ordinance, §§ 2(k), 6(2)(a). In other words, persons whose annual income was not high enough for them to pay income tax (i.e., approximately PRs100,000, or $1,785 at appraisal) were considered “poor.” In 2006, the 2001 Ordinance was amended to authorize SBP to define “poor person”. Finance Bill, 2006, § 18(1)(b). SBP subsequently defined “poor person” as persons whose annual total income after deducting business expenses was less than PRs150,000 (currently around $1,900).” Prudential Regulations for Microfinance Banks, art. 30, http://www.sbp.org.pk/publications/prudential/micro_prs.pdf.

10 KB is referred to in the RRP as MFB.

5

(including savings, credit, leasing, money transfer, and risk mitigation services) and serve 560,000 borrowers and 640,000 savers by end of its sixth full year of operations (2006) (RRP, para. 91). However, by the end of 2006 KB was offering only one of these five services—credit—and to only 42% of the projected number of borrowers (Table 2 and paragraph 25).

Table 2: Active Clients of Khushhali Bank at Year-End (2001–2007)

2001 2002 2003 2004 2005 2006 2007 Borrowers Projected 62,250 107,613 185,593 297,448 426,933 563,225 684,450 Actual 12,755 56,324 91,532 168,105 227,172 236,917 283,965 20% 52% 49% 57% 53% 42% 41% Depositors Projected 71,588 123,755 213,432 342,065 490,973 647,709 787,118 Actual 0 0 0 0 0 0 0 0% 0% 0% 0% 0% 0% 0%

Sources: ADB. 2000. Report and Recommendation of the President to the Board of Directors on Proposed Loans to the Islamic Republic of Pakistan for the Microfinance Sector Development Program. Manila, Supplementary Appendix F (projected); Khushhali Bank (actual).

16. One important reason why KB did not fulfill its outreach goals was that, contrary to expectations, it did not take over the existing microfinance operations of the rural support programs, including their loan portfolio, staff, and facilities. 12 In part, this did not happen because KB and the National Rural Support Programme (NRSP) did not agree on the value of NRSP’s loan portfolio, while another microfinance bank—First MicroFinance Bank Ltd. (FMFB)—eventually took over much of the lending activities of the Aga Khan Rural Support Programme (AKRSP). 17. KB initiated deposit-taking activities in 2008 with a small pilot program in its Rawalpindi branch.13 Despite the Program’s target of having KB fund at least 20% of its loan portfolio with deposits, KB did not start deposit-taking before 2008 because (i) it was concentrating on expanding its branch network and maximizing the number of loan clients it served, (ii) it experienced delays in installing the technology required to effectively handle deposit-taking, (iii) it had easy access to low-cost funding provided under the investment loan, and (iv) the Program did not require it to take deposits. Although other microfinance banks successfully raised deposits, only one of them (FMFB) concentrated on serving rural markets like KB; the others operated almost exclusively in the urban market of Karachi (Table 3).

11 Its paid-in capital of PRs1.7 billion was subscribed by 16 commercial banks, most of which were state-owned. The

Government provided low-cost, long-term funding to KB through the ADB investment loan. KB’s operations are described at length in the project completion report of the investment loan. ADB. 2008. Project Completion Report on the Microfinance Sector Development Project in Pakistan. Manila.

12 2000. Phase I: Rationale and Feasibility of Proposed Microfinance Bank (TA No. 2937-PAK), Manila, para. 36. As of 30 June 1999, NRSP and AKRSP had a total of 58,097 borrowers, loan portfolio of PRs708,313, 104 credit officers, and 323,314 savers. Id., Table A1.4.

13 Aggregate savings to date total approximately PRs500,000 (less than $11,000).

6

Table 3: Microfinance Banks

Name Abbrev-iation

Year Operations

Commenced

Paid-Up Capital (PRs)

Full Years in

Operation Retail

Depositorsa Borrowersa

Khushhali Bankb KB 2000 1.7 billion 7 0 283,965 First MicroFinance Bankc FMFB 2001 660 million 6 79,827 101,394 Network Microfinance Bankd NMFB 2005 100 million 3 5,451 2,303 Rozgar Microfinance Banke RMFB 2005 100 million 2 4,224 2,337 Tameer Microfinance Bankf TMFB 2005 600 million 2 44,507 31,011 Pak-Oman Microfinance Bankg POMFB 2006 500 million 1 12,249 14,397 Kashf Microfinance Bank KMFB 2008 750 million 0 0 0 146,258 435,407

a As of 31 December 2007. b http://www.khushhalibank.com.pk e http://www.rozgarbank.com c http://www.fmfb.com.pk f http://www.tameerbank.com d http://www.networkmicrobank.com g http://www.pomicro.com Sources: State Bank of Pakistan; MixMarket (www.mixmarket.org).

3. Framework for Institutional Diversity 18. The Program was designed to develop a framework for institutional diversity in the microfinance sector (RRP, para. 74). 19. This was accomplished in October 2001 upon the promulgation of the Microfinance Ordinance, 2001 (2001 Ordinance). This ordinance, which was modeled largely on the August 2000 Ordinance creating KB, authorized the creation of other microfinance banks. To date, a total of six additional banks have been licensed (Table 3). However, contrary to Program expectations, KB was not an investor in any of these banks.

4. Creation of Special-Purpose Funds 20. The Program provided for the establishment of four funds: (i) a Microfinance Social Development Fund (MSDF) to create and strengthen community organizations, some of whose members would become KB borrowers; (ii) a Community Investment Fund (CIF) to fund small infrastructure projects designed by community organizations; (iii) a Risk Mitigation Fund (RMF) to help KB borrowers who unexpectedly lost income-generating assets; and (iv) a Deposit Protection Fund (DPF) to protect the savings of KB depositors. 14 21. As shown in Table 4, each of the funds was initially capitalized by the Government, together with a small contribution by KB. In accordance with the terms of the Program, the Government’s aggregate contribution to the four funds was equal to the local currency equivalent of the total amount of the program loan ($70 million). The Program provided that KB contribute a total of 20% of its after-tax income to three of these funds (MSDF, RMF, and DPF), and that the Government contribute a portion of the interest it received from KB under the investment loan to two of these funds (RMF and DPF).

14 As described in paragraph 23, another fund not originally contemplated by the Program—the Emergency

Livelihood Restoration Fund (ELRF)—was later created using program monies.

7

Table 4: Funds Created Under the Microfinance Sector Development Program

Microfinance Social Development Fund

Community Investment Fund

Risk Mitigation Fund

Deposit Protection Fund

Abbreviation MSDF CIF RMF DPF Purpose Creating and

strengthening community organizations whose members would become borrowers of KB

Funding small infrastructure projects designed with the active participation of community organizations

Mitigating losses of borrowers of KB arising from the loss of income-generating assets or the failure of enterprises due to unforeseen circumstances

Protecting the savings of depositors of KB

Duration 25 years 20 years Unspecified Unspecified

Governance Three member committeea

Three member committeea

SBP Microfinance Support Division

SBP Microfinance Support Division

Initial Capital Contributions (2001–2002)

By Government PRs2.4 billion PRs1.2 billion PRs295 million PRs295 million By KB PRs1.0 million PRs1.0 million PRs1.0 million PRs1.0 million Total (in $) $40 million $20 million $5 million $5 million

Subsequent Capital Contributions

Required to be made by KB 10% of after-tax profit

None 5% of after-tax net profit

5% of after-tax net profit

Total made (2002–2007) PRs12.3 million 0 PRs6.1 million PRs6.1 million Required to be made by

Government None None 50% of the Net

Interest Spreadb 50% of the Net Interest Spreadb

Total made (2001–2007) 0 0 PRs107.5 million PRs107.5 million

Incomec PRs1,449 million PRs296 million (2001–2005)

PRs241 million PRs288 million

Amount disbursedc for: Fund’s intended purpose PRs550,213,960 PRs215,218 0 0 Administrative expenses PRs4,973,475 PRs1,660,677 0 0 Total PRs555,187,435 PRs1,875,895 0 0 (as % of Income) 38% 1% 0% 0%

Fund Balanced PRs2.5 billion ($41.0 million)

0 e PRs649 million ($10.6 million)

PRs661 million ($10.8 million)

ELRF = Emergency Livelihood Restoration Fund, KB = Khushhali Bank, SBP = State Bank of Pakistan a Consisting of the president of KB (chairman), one director of KB, and a nominee of SBP. b The Net Interest Spread is the difference between the interest paid by KB on its credit-line borrowings from the Government

less the interest expense with respect to such amount accrued on the investment loan. c Except as otherwise indicated, through 31 December 2007. d As of 31 December 2007. e The entire fund balance of PRs1,680,787,169 was transferred in 2006 to the ELRF (footnote 16). Sources: ADB. 2000. Report and Recommendation of the President to the Board of Directors on Proposed Loans to the Islamic Republic of Pakistan for the Microfinance Sector Development Program. Manila, Appendixes 8–11; fund rules, annual reports, audited financial statements.

8

22. As shown in Tables 5 and 6, fund outputs were significantly below targets, and fund expenditures were correspondingly below projections. The principal reason why the MSDF and the CIF did not achieve their social mobilization and infrastructure creation goals is because the goals were predicated on the incorrect assumption that the activities would be implemented principally by NRSP and the other rural support programs. Since these organizations were the only ones in Pakistan with substantial experience in these activities, their lack of participation after the first year had a significant adverse effect on the Program’s progress. Although eight NGOs were eventually contracted to implement social mobilization activities (Appendix 2), they were never able to scale up dramatically. Consequently, KB ultimately formed 80% of all community organizations, thereby performing a role which was not anticipated for it in the Program’s design. 15 In addition, 99% of the completed small infrastructure projects were managed by a single for-profit company (Appendix 3), rather than by NGOs (as the Program had contemplated).

Table 5: Summary of Fund Outputs (Actual vs. Target)

Fund Output Target (by end-2006)

Actual (by end-2007)

Actual / Target

MSDF Community organizations (COs) formed

24,750 (23 households per CO)

90,468 (8 households per CO)

366% 35%

Workshops for community leaders: 4-day management skills training

workshops 24,750 participants no workshops held 0%

3-day capacity enhancement

training 12,412 participants no workshops held 0%

10-day leadership management

skills training 1,240 participants no workshops held 0%

Annual 2-day workshops for all

community leaders 1,409 workshops no workshops held 0%

CIF Small-scale community infrastructure

projects created 4,500 1,569 a

35%

RMF Borrowers reimbursed for loss of income-generating assets

27,000 0 0%

DPF Accumulation of substantial fund to protect KB depositors

$15.7 million Fund > 51% of KB’s deposits

PRs661 million ($10.8 million) KB’s deposits = 0

69% —

CIF = Community Investment Fund, CO = community organization, DPF = Deposit Protection Fund, KB = Khushhali Bank, MSDF = Microfinance Social Development Fund, RMF = Risk Mitigation Fund a Additional information regarding the infrastructure projects is contained in Appendix 4. Sources: ADB. 2000. Report and Recommendation of the President to the Board of Directors on Proposed Loans to the Islamic Republic of Pakistan for the Microfinance Sector Development Program. Manila, paras. 92–94; fund annual reports; Khushhali Bank.

15 KB and the NGOs received a fixed sum for each community organization member who became a KB loan client.

During the Program, the amount increased gradually from PRs750 to PRs1,000 per member.

9

Table 6: Summary of Fund Expenditures (Actual vs. Projected)

Fund Projected (through 2007)

($)

Actual (through 2007)

(PRs)

Actual (through 2007)

($a)

Actual / Projected

MSDF 26,380,900 555,187,435 9,308,912 35% CIF 10,616,400 1,875,895 b 195,846b 2%b RMF 12,658,300 0 0 0% DPF 30,100c 0c 0 0% Total 49,685,700 579,219,953 9,504,758 19%

CIF = Community Investment Fund, DPF = Deposit Protection Fund, ELRF = Emergency Livelihood Restoration Fund, KB = Khushhali Bank, MSDF = Microfinance Social Development Fund, RMF = Risk Mitigation Fund, SBP = State Bank of Pakistan a Converted from Pakistani rupees using the average interbank exchange rate (per www.oanda.com) for the

year in which the expenditures were incurred. b The Program contemplated that all of the funding for small infrastructure projects, other than the co-financing

provided by the beneficiary communities, would come from the CIF. Had this actually occurred, the last three columns of the CIF row would be 205,431,258, 3,398,123, and 32%, respectively. The differing amounts are the result of a decision by SBP to delay reimbursements to KB from the CIF for expenditures submitted to SBP between April 2004 and June 2007. Since all of the funds in the CIF were transferred to the ELRF in 2006 (para. 23), in 2007 the Government requested that ADB permit it to use unutilized funds from the investment loan in order to reimburse KB. ADB consented and disbursed $3,202,277 (PRs203,555,363 converted to dollars using the exchange rate on the value date) in 2008. Thus, the small infrastructure projects were funded primarily by ADB’s loan rather than by the Government using counterpart funds in the CIF.

c Only administrative expenditures were projected. However, no expenditures are shown because SBP elected to bear all these expenses itself.

Note: Balance sheets and income statements for each fund are contained in Appendix 5. Sources: ADB. 2000. Report and Recommendation of the President to the Board of Directors on Proposed Loans to the Islamic Republic of Pakistan for the Microfinance Sector Development Program. Manila, Tables A.8–A.11 (projected); MSDF Audited Financial Statements (MSDF actual); KB (CIF actual).

23. Another important reason why the community infrastructure creation output target was not met was that the entire CIF (capital and accumulated earnings) was transferred in April 2006 to a new fund—the Emergency Livelihood Restoration Fund (ELRF)—created in order to provide relief to poor people living in areas affected by the 8 October 2005 earthquake.16 24. Utilization of the CIF also proceeded slowly because eligibility was limited to communities which included persons who had been good clients of KB for at least 2 years, as demonstrated by having repaid their loans on schedule. In addition, the Program’s requirement that community organization members contribute 40% of the total cost of community infrastructure projects proved to be an obstacle. However, this obstacle was alleviated in December 2003 when ADB approved a reduction in the required contribution from 40% to 20% (this change was reflected in an amendment to the loan agreement). 25. The objective of creating the Risk Mitigation Fund (RMF)—reimbursing KB borrowers who had lost income-generating assets (such as crops or livestock) as a result of natural disasters including floods and droughts (RRP, para. 79)—was not met because KB never implemented it.17 16 The ELRF was formed using $13 million of the MSDF (all unutilized interest income) and the entire $25 million

balance of the CIF ($20 million of principal and $5 million of unutilized interest income). Although the entire $38 million fund was intended to be fully disbursed within 3 years, as of 30 June 2008 only 29% of the fund had been utilized.

17 The April 2005 ADB review mission wrote: “KB clients have recently encountered flood conditions in certain areas of Punjab & Sindh [and] loss of their crops & assets have been reported by branches. SBP may like to look into the use of [the] risk mitigation facility in such cases.” Other natural disasters during the program period included drought in certain areas of Sindh and Balochistan in 2002–2003 and flooding in Balochistan in 2007.

10

26. The objective of the Deposit Protection Fund (DPF)—protecting the savings of KB depositors (RRP, para. 80)—was not achieved because KB did not begin accepting deposits until 2008, and then only on a small pilot basis in one branch (para. 17). Although the assets of the DPF are not presently available to protect the depositors of other deposit-taking microfinance banks, such a change is currently being discussed.

5. Restructuring of Development Banks 27. The Program required that the Government initiate steps to restructure FBC and ADBP (RRP, Policy Matrix, Appendix 1).18 In compliance with this requirement, the Government closed FBC and transferred all of ADBP’s assets and liabilities to a new entity, Zarai Taraqiati Bank Limited (ZTBL). 6. Capacity Building 28. The Program was designed to strengthen the managerial capacity of KB and other microfinance banks to operate successfully and the capacity of SBP to regulate microfinance banks. To address these needs, the Program provided funding for (i) technical assistance to SBP to design and implement a policy framework, including a supervisory system appropriate to microfinance banks; (ii) consulting services to help KB establish operating systems and procedures, conduct training, price and promote products, improve social mobilization, enhance the impact of its services on poverty reduction, and build a sound customer base; (iii) training of community organization members and leaders; (iv) assistance to new microfinance banks wishing to enter the market; and (v) vehicles and equipment for KB to ensure the mobility of its female staff to reach out to poor women in remote areas (RRP, para. 84). Because the funds for these grants were provided from the investment loan instead of the program loan, their impact is evaluated in the investment loan’s project completion report. C. Disbursements

29. The MSDP was approved on 13 December 2000. The first tranche ($50 million) was disbursed on 13 February 2001. The second tranche ($20 million equivalent) was scheduled for disbursal within 24 months thereafter (13 February 2003) and was actually disbursed (in the amount of $20.9 million) on 23 December 2002.

18 A recent report explains:

The establishment of the Agricultural Development Bank of Pakistan (now ZTBL) in the early 1970s represent[ed] an early effort to extend credit to poor people. The bank was established with a vision to provide rural finance to farmers, especially small farmers. However, as has been the case of many agricultural banks worldwide, the Agricultural Development Bank ran huge losses because of low lending rates and political lending that resulted in major defaults by large landlords. It thus required continuous injections of government subsidies.

CGAP. 2007. Country Level Effectiveness and Accountability Review with a Policy Diagnostic: Pakistan Washington. (“CGAP CLEAR”), p. 6. Although ZTBL remains the largest microfinance provider in the country, it has never become sustainable. (As of year-end 2007, 71% of its liabilities were funded by subsidized loans from SBP. ZTBL Audited Financial Statements (2007), notes 14, 15.) In addition, it suffers from a high rate of arrears. CGAP CLEAR, p. 39 (estimating arrears of more than 50%); ZTBL Audited Financial Statements (2007), footnote 10 (showing 13% arrears rate).

11

D. Program Schedule

30. The scaling up of KB was significantly delayed when NRSP did not transfer its loan portfolio and related staff to KB (Table 2). In addition, NRSP’s decision not to participate in the activities funded by the MSDF and the CIF delayed for two years the beginning of any significant implementation of the social mobilization and infrastructure creation components of the Program. E. Implementation Arrangements

31. SBP was the executing agency for the program loan and had overall responsibility for implementation. SBP consulted with the Ministry of Finance (MOF) to ensure that reforms were implemented promptly. The operations of the MSDF and the CIF were governed by three-person committees, while the RMF and the DPF were managed by SBP’s microfinance division (Table 4). These implementation arrangements were generally satisfactory. F. Conditions and Covenants

32. As noted in paragraph 10, the Program was supported by two loans, both funded from ADB’s special funds resources. The investment loan is described in its project completion report. The program loan principal of SDR54,114,000 (equivalent to $70 million) is repayable in 32 equal, semi-annual installments beginning 1 May 2009 and ending on 1 November 2024. The loan carries an interest rate of 1% until 1 May 2009 (the end of the grace period) and 1.5% thereafter. There were no delays in meeting the conditions of effectiveness. The Loan Agreement became effective 3 days after signing. 33. The loan was designed to be released in two tranches. The first tranche of SDR38,527,000 (equivalent to $50 million) was to be released upon loan effectiveness, and the release of the second tranche of SDR15,587,000 was to occur upon the fulfillment of five conditions. These five conditions, which are summarized in Table 7, were complied with and the second tranche was released on 23 December 2002.

Table 7: Summary of Second Tranche Release Conditions

Condition Comment

Enact a law providing a legal and regulatory framework for microfinance acceptable to ADB

2001 Ordinance enacted in October

Review the 2000 Ordinance and amend it to ensure a level playing field between KB and other microfinance banks

Review conducted; no amendments deemed necessary in light of SBP’s October 2002 action applying to KB the prudential regulations applicable to other microfinance banks

Close and liquidate FBC Liquidation order issued in October 2002

Complete a portfolio audit assessing the magnitude of the nonperforming loan portfolio of ADBP

Completed circa October 2002

Finalize a restructuring plan for ADBP acceptable to ADB Plan adopted in October 2002 pursuant to which all of its assets and liabilities would be transferred to a new entity (ZTBL)

ADBP = Agricultural Development Bank of Pakistan, FBC = Federal Bank for Cooperatives, KB = Khushhali Bank, SBP = State Bank of Pakistan, ZTBL = Zarai Taraqiati Bank Limited Source: ADB. 2002. Progress Report on the Microfinance Sector Development Program in the Islamic Republic of Pakistan. Manila, Table 1.

12

34. Compliance with reporting requirements was generally satisfactory. However, the 2007 audit reports for the funds were not completed on time and no 2006 audit report for the CIF was prepared. The covenants in the Loan Agreement were highly relevant and well designed to achieve the Program’s objectives (additional covenants that would have been desirable are suggested in paragraph 46). One covenant was modified. This covenant required community members to contribute 40% of the total cost of each community investment project (item 11 of Schedule 5 of the Loan Agreement). In December 2003, ADB agreed to reduce the community cost-sharing amount to 20% (paragraph 24 and Appendix 6). 35. Although covenant compliance was generally satisfactory, several covenants relating to the use of counterpart funds were breached (Appendix 6, items 9–12). For example, as discussed in paragraph 25, the covenant on the use of the RMF was violated because the risk mitigation component of the Program was never implemented. The covenant limiting the total cost of each community investment project to PRs150,000 ($2,700 at appraisal) was breached because KB had instead followed the inconsistent provision set forth in item 4 of Appendix 9 of the RRP, which limited the grant portion of each project to PRs150,000. G. Related Technical Assistance

36. The Program was formulated with a project preparatory technical assistance19 as men-tioned in paragraph 5 of the investment loan’s project completion report. H. Performance of the Borrower and the Executing Agency

37. Overall, the performance of the Borrower and the executing agency, SBP, was satisfactory. SBP’s role in developing and implementing laws and regulations governing microfinance banks deserves special positive mention. I. Performance of the Asian Development Bank

38. ADB’s performance in administering the program loan was generally satisfactory. Although no review missions were undertaken after April 2005, it does not seem likely that additional missions would have resulted in material improvements in program outputs.

III. EVALUATION OF PERFORMANCE

A. Relevance

39. The Program is assessed as highly relevant. It was designed to implement the Government’s strategy of reducing poverty by providing affordable, sustainable financial services to the poor in Pakistan from institutional sources. B. Effectiveness in Achieving Outcome

40. The Program is rated as less effective. It resulted directly in the creation and funding of one institution, KB, and indirectly in the creation of six other institutions (since these institutions

19 ADB. 1997. Technical Assistance to the Islamic Republic of Pakistan for the Rural Microfinance Project. Manila,

approved on 12 December 1997 for $600,000.

13

were licensed under the 2001 Ordinance).20 As of 31 December 2007, these seven institutions had a total of 435,000 active loan clients and 146,000 retail depositors (Table 3). However, none of these institutions is currently operationally or financially sustainable (Appendix 7).21 Moreover, as a group, microfinance banks are currently the least sustainable providers of microfinance services, while the best performers are NGOs.22 C. Preliminary Assessment of Sustainability

41. The Program’s sustainability is assessed as less likely. The Program was designed to provide financial services to the poor on a sustainable basis through a special-purpose entity known as a microfinance bank. The Program has not achieved this result, as KB is not sustainable. After 7 years of operation financed with very low-cost funding, its profits are small.23 Under the terms of the investment loan, KB will be required to make principal payments totaling PRs213,237,688 ($2.7 million) per year beginning in 2009. At its current rate of growth (25% increase in loan portfolio from 2006 to 2007), starting in 2010 or 2011 KB will have to constrain its growth and cap its loan portfolio at around PRs5 billion ($63.5 million) unless it obtains substitute financing. Given its low profitability, it will be very difficult for KB to attract unsecured loans from commercial lenders, especially since such loans would likely bear an interest rate of at least twice the interest rate currently paid on the credit line provided under the investment loan.24 One solution to address KB’s long-term funding needs would be for it to be acquired by a regular commercial bank with a large existing deposit base. D. Impact

42. By encouraging the creation and effective supervision of microfinance banks, the Program had a positive impact on the development of microfinance in Pakistan. However, the empirical evidence is inconclusive regarding whether the Program’s lending component had any effect in increasing household income and alleviating poverty. Although the Program’s design critically omitted a carefully designed longitudinal survey,25 a one-time survey of 2,881 house-

20 Effective 1 April 2008, Khushhali Bank became licensed under the same ordinance as the other microfinance

banks. On that date, all of its assets and liabilities were transferred to a new legal entity—Khushhali Bank Limited—licensed under the 2001 Ordinance instead of the 2000 Ordinance.

21 A microfinance institution is considered (i) “operationally sustainable” if its operating revenues cover (Operational Self-Sufficiency (OSS) ratio=100%) or exceed (OSS ratio>100%) its costs and (ii) “financially sustainable” if its operating revenues would cover (Financial Self-Sustainability (FSS) ratio=100%) or exceed (FSS ratio>100%) its costs if its operations were unsubsidized and if it were funding its expansion with commercial-cost liabilities. SEEP. 2005. Measuring Performance of Microfinance Institutions: A Framework for Reporting, Analysis, and Monitoring Washington, p. 66, http://www.seepnetwork.org/content/library/ detail/3259.

22 Among the hundreds of microfinance providers in Pakistan, only five are currently sustainable. CGAP CLEAR, p. 1. Both of the two fully sustainable organizations (profit margin>3%) are NGOs—Kashf and Orangi Pilot Project. Two of the three marginally sustainable organizations (profit margin=0–3%) are NGOs—DAMEN and Sungi Development Foundation—while the third is NRSP, a rural support program. Pakistan Microfinance Network. 2007. Pakistan Microfinance Review 2007. Islamabad, pp. 12-13.

23 Between 2001 and 2007, its funding cost ranged between 1.3% and 4.3%. ADB. 2008. Project Completion Report on the Microfinance Sector Development Project in Pakistan. Manila, para. 6, footnote 11. The estimated value of the subsidy provided under the investment loan in 2007 was PRs246,420,000 ($3.5 million). Pakistan Microfinance Network. 2007. Pakistan Microfinance Review 2007. Islamabad, p. 38.

24 See footnote 23. 25 “[A]ssessing the true relationship between micro-finance services and poverty reduction is not straightforward. . . .

Accurate assessment . . . . requires empirically a control group identical in characteristics to the recipients of credit and engaged in the same productive activities, who have not received credit, and whose income (or other measure) can be traced through time to compare with that of the credit recipients.” Weiss, John, Heather Montgomery and Elvira Kurmanalieva. 2005. Micro-finance and Poverty Reduction in Asia. In Poverty Targeting in Asia, edited by John Weiss. Cheltenham: Edward Elgar, p. 253 (emphasis supplied).

14

holds (half of which were KB borrowers) was conducted in 2005 by an independent survey company using funds provided by the ADB Institute.26 Two sets of researchers analyzed the data using different methodologies. Setboonsarng and Parpiev were unable to confirm that being a KB borrower had any beneficial impact on a household’s food consumption, healthcare and educational expenditures, savings, or accumulation of durables.27 Montgomery reached similar conclusions, but found some evidence that the very poorest KB borrowers increased expenditures on their children’s education.28 In addition, no empirical evidence was systemat-ically collected and evaluated regarding the actual impact and sustainability of the Program’s social mobilization and community infrastructure components.

IV. OVERALL ASSESSMENT AND RECOMMENDATIONS

A. Overall Assessment

43. Overall, the Program is rated as partly successful. 44. One critical component of the Program was implemented as conceived: the creation of an enabling policy environment, including the enactment of laws, adoption of regulations, and strengthening of supervisory capacity. However, the Program contemplated that the lending and savings programs of KB, as well as the activities funded by the MSDF and the CIF, would not be starting from scratch but would utilize NRSP’s pre-existing lending and social mobilization operations. Although KB management worked hard to find alternative providers, this effort was time-consuming and achieved only limited success. As a result, KB ultimately performed the vast majority of social mobilization itself. The results framework contained in the RRP (an annotated version of which is found in Appendix 8), was generally adequate, with the exception of targets pertaining to KB’s progress in becoming self-sustainable (paragraph 46). B. Lessons Learned

45. Diversify and Focus on More Institutions. Since the Program only supported a single microfinance institution, it is difficult to assess the extent to which KB’s difficulties in becoming self-sustainable and achieving its outreach targets were attributable to institution-specific factors as against general sector conditions. In retrospect, it would have been preferable to establish several institutions, let them compete for a few years, and then deprive the laggards of additional funding while providing additional funding to the better performing ones. 46. Measure and Promote Sustainability. The Program’s results framework contained a single numerical target pertaining to KB—the number of households receiving loans—and did not provide sufficiently clear signals and incentives to promote sustainability. To achieve better results, microfinance programs should establish incentives and condition continued funding on reaching targets related to sustainability. These targets should include (i) requiring charging an interest rate that results in margins high enough to generate retained earnings and (ii) requiring entities that are legally allowed to accept deposits to actively solicit them in order to try to

26 In addition, researchers from the University of Agriculture in Faisalabad surveyed 100 KB borrowers in a single

district in southern Punjab. Ahmad, S., M. S. Naveed, and A. Ghafoor. 2004. Role of micro finance in alleviating rural poverty: A Case Study of Khushhali Bank Program in Rahim Yar Khan – Pakistan. Int. J. Agric. Biol. 6: 426–8.

27 Setboonsarng, Sununtar, and Ziyodullo Parpiev. 2008. Microfinance and the Millennium Development Goals in Pakistan: Impact Assessment Using Propensity Score Matching (Discussion Paper No. 104). Tokyo: ADB Institute, p. 6, http://www.adbi.org/files/dp104.2008.microfinance.millennium.dev.goals.pakistan.pdf, p. 6.

28 Montgomery, Heather. 2005. Serving the Poorest of the Poor: The Poverty Impact of the Khushhali Bank’s Microfinance Lending in Pakistan. Tokyo: ADB Institute, http://www.adbi.org/files/2005.09.28.book.khush hali.microfinance.study.pdf.

15

generate a base of low-cost funding.29 For example, in 2007 KB charged an interest rate of 20%. If, instead, it had charged a rate of 30% (a rate still lower than that charged by some other microfinance institutions in Pakistan), its operational self-sustainability ratio in 2007 would have increased from 76% to 100%, and its return on equity from 5.0% to approximately 13.5%. 30 47. The Program was similar to the microfinance programs of other donors in Pakistan in that it did not emphasize sustainability.31 Instead, the Program provided a continuing stream of funds regardless of the sustainability of the institution supported, following an approach that had contributed to the poor performance of donor-funded agricultural and development banks in prior decades.32 C. Recommendations

1. Program Related

48. ADB and the Borrower should amend the covenants in the Loan Agreement relating to the four funds. Since only 38% of the income of the MSDF, and none of the income of the RMF, has been used for their respective intended purposes, the related covenants should be modified to permit the Borrower to use the two funds for other purposes that should be promptly agreed upon with ADB. Since the CIF has been terminated, covenants relating to it should be removed. The covenant relating to the DPF should be modified to allow deposits of other microfinance banks to be protected under revised rules since, unlike KB, other microfinance banks engage in significant deposit-taking. The Borrower has expressed its agreement with this recommendation.

2. General 49. Any future microfinance lending programs financed by ADB should reflect the lessons from this Program, for its design and intended impact and purpose are highly relevant.

29ADB’s microfinance strategy, which was adopted prior to the appraisal of the Program, recognizes that microfinance

clients are more concerned about access to services than the price of the services and that expansion of savings services can have a significant impact on institutional sustainability and poverty reduction. ADB. 2000. Finance for the Poor: Microfinance Development Strategy, Manila (June 2005 ed.), p. 22, items (ii), (vi).

30 See footnote 24. 31 “Though donors never actively obstructed retail financial providers from focusing on sustainability in the past, they

were mostly mute or complacent on the issue. To provide far greater numbers of the poor with access to quality financial services, donors must send clear signals, establish incentives, and condition funding to microfinance providers based on a commitment to reaching sustainability.” CGAP CLEAR, p. 11.

32 “[W]ith seemingly unlimited supplies of finance, the development banks failed to develop savings products and deposit-taking activities and thus failed to provide this important service for the poor and to become self-sustainable.” Oxford Policy Management. 2006. Poverty and Social Impact Assessment: Pakistan Microfinance Policy, p. 16, http://www.dfid.gov.uk/pubs/files/pakistan-micro-final.pdf.

Appendix 1

16

CIRCULARS ISSUED BY STATE BANK OF PAKISTAN REGARDING MICROFINANCE AND/OR MICROFINANCE BANKS

Date No. Title Link 13 October 2000 BSD

Circular No. 29

Microfinance Rules http://www.sbp.org.pk/bsd/2000/bsd29.htm

24 April 2002 BSD Circular No. 13

Microfinance Institutions–Branch Licensing Policy

http://www.sbp.org.pk/bsd/2002/C13.htm Superseded by BPRD Circular No. 15 http://www.sbp.org.pk/bprd/2007/C15.htm

14 October 2002 BSD Circular No. 18

Prudential Regulations for Microfinance Banks/Institutions

http://www.sbp.org.pk/bsd/2002/C18.htm Superseded by BPRD Circular No. 1 http://www.sbp.org.pk/bprd/2007/C1.htm

14 February 2003 BSD Circular No. 2

Guidelines for Mobile Banking Operations of Microfinance Banks/Institutions

http://www.sbp.org.pk/bsd/2003/C2.htm

17 November 2003 BSD Circular No. 10

Credit Rating of Micro-finance Banks: Pruden-tial Regulation 29 for Microfinance Banks

http://www.sbp.org.pk/bsd/2003/C10.htm

30 December 2003 BSD Circular No. 11

Forms of Financial Statements for Microfinance Banks/Institutions

http://www.sbp.org.pk/bsd/2003/C11.htm

8 July 2004 BID Circular No. 1

Questionnaires for Self-Assessment-IRAF

http://www.sbp.org.pk/bid/2004/C1-04.htm

5 October 2004 BPD Circular No. 31

Renewal Fee for Banking/Branch(es) Licenses Issued under Sections 27 & 28 of Banking Companies Ordinance, 1962

http://www.sbp.org.pk/bpd/2004/C31.htm

12 October 2004 BID Circular Letter No. 1

Questionnaires for Self Assessment Under Institutional Risk Assessment Framework (IRAF)

http://www.sbp.org.pk/bid/2004/CL1.htm

28 March 2005 BSD Circular No. 2

Fit & Proper Criteria for Board Members and President/Chief Executive of Microfinance Banks

http://www.sbp.org.pk/bsd/2005/C2.htm Superseded by BPRD Circular No. 1 http://www.sbp.org.pk/bprd/2007/C1.htm

13 April 2006 SMED Circular No. 7

Amendments in Prudential Regulation Nos. 12 and 14 for Microfinance Banks (MFBs)

http://www.sbp.org.pk/mfd/2006/C7.htm Superseded by BPRD Circular No.1 http://www.sbp.org.pk/bprd/2007/C1.htm

27 June 2006 SMED Circular No. 10

Guidelines for Commercial Banks to Undertake Microfinance Business

http://www.sbp.org.pk/mfd/2006/C10.htm

Appendix 1

17

Date No. Title Link 27 June 2006 SMED

Circular No. 11

Prudential Regulations for Commercial Banks to Undertake Microfinance Business

http://www.sbp.org.pk/mfd/2006/C11.htm

31 October 2006 BPRD Circular Letter No. 24

Consolidation of Licensing, Corporate Governance & Regulations at BPRD

http://www.sbp.org.pk/bpd/2006/CL24.htm

2 February 2007 SME&MFD Circular Letter No. 1

Submission of Period-ical Returns and Min-utes of Board of Direc-tors’/General Meetings

http://www.sbp.org.pk/mfd/2007/CL1.htm

5 March 2007 BPRD Circular No. 1

Revised Prudential Regulations for Microfinance Banks (MFBs)

http://www.sbp.org.pk/bprd/2007/C1.htm

13 July 2007 BPRD Circular No. 9

Guidelines on Outsourcing Arrangements

http://www.sbp.org.pk/bprd/2007/C9.htm

28 August 2007 BPRD Circular Letter No. 24

Evening Banking http://www.sbp.org.pk/bprd/2007/CL24.htm

10 September 2007 IBD Circular No. 5

Guidelines for Islamic Microfinance Business

http://www.sbp.org.pk/ibd/2007/C5.htm

8 October 2007 DFSD Circular No. 1

Creation of Development Finance Support Department

http://www.sbp.org.pk/sbp_bsc/BSC/DFSD/cir/cir-01-07.pdf

12 October 2007 BPRD Circular No. 15

Revised Branch Licensing Policy

http://www.sbp.org.pk/bprd/2007/C15.htm

28 November 2007 BPRD Circular No. 37

Notification

http://www.sbp.org.pk/bprd/2007/CL37.htm

4 January 2008 DFSD Circular No. 1

Regional Plans for Increasing Outreach of Development Finance

http://www.sbp.org.pk/sbp_bsc/BSC/DFSD/cir/cir-01-08.pdf

20 March 2008 BSD Circular No. 7

Prudential Regulation No. 4: Minimum Capital Requirements

http://www.sbp.org.pk/bsrvd/2008/C7.htm

31 March 2008 BPRD Circular No. 2

Branchless Banking Regulations for Financial Institutions

http://www.sbp.org.pk/bprd/2008/C2.htm

26 May 2008 OSED Circular No. 1

Upward Revision in Penalties for Misreporting/Late Submission of Returns

http://www.sbp.org.pk/osed/2008/C1.htm

BID = Banking Inspection Department, BPRD = Banking Policy & Regulations Department, BSD = Banking Supervision Department, DFSD = Development Finance Support Department, IBD = Islamic Banking Department, IRAF = Institutional Risk Assessment Framework, MFB = Microfinance Bank, OSED = Off-Site Supervision & Enforcement Department, SMED = Small and Medium Enterprises Department, SME&MFD = SME and Microfinance Department Source: State Bank of Pakistan.

Appendix 2

18

MICROFINANCE SOCIAL DEVELOPMENT FUND SERVICE PROVIDERS

No. Name

Contract Coverage

Period

COs Formed

(as of June 2008)

CO Members Organized

(as of June 2008)

Amount Earned (as of

June 2008) (PRs)

Average Amount Earned per CO member

Districts Covered

1. National Rural Support Programme

Aug 2000–Aug 2001

— — — — —

Abbottabad Charsadda Karachi Kohat Lahore Muzaffarabad Nowshera Peshawar Quetta

2. Family Planning Association of Pakistan

May 2002– Jun 2009

8,940 53,630 46,329,308 864

Rawalpindi Badin Hyderabad Thatta Tando Allahyar

3. Health and Nutrition Development Society

Jun 2003– Jun 2009

2,524 19,752 17,798,250 901

Tando Muham-mmad Khan

Khairpur Mardan

4. Human Development Foundation

Jun 2002– Jun 2009

1,372 13,332 11,066,579 830

Rahim Yar Khan

Ghotki Larkana Mirpurkhas Nawabshah

5. Sindh Graduate Association

Jul 2002–Jun 2009

2,690 26,676 22,797,000 855

Shikarpur Dadu Khairpur

6. Indus Resource Center

Dec 2004–Jun 2009

807 6,094 5,757,000 945

Sukkur Faisalabad Jhang

7. Society For Human Development

Dec 2004– Jun 2009

850 4,996 4,101,768 821

Toba Tek Singh

Hafizabad Layyah Mandi

Bahauddin Sialkot Sargodha

8. Buniyad Literacy Community Council

Dec 2004– Jun 2007

1,051 9,059 6,805,305 751

Sheikhupura 9. Taraqee Trust Jun 2002–

Sep 2003 132 1158 822,000 710 Sibi

Subtotal 18,232 134,697 115,477,210 857

10. Khushhali Bank 2003–ongoing

72,234 607,623 508,265,750 836 All districts where KB has branches

Total 90,468 742,320 623,742,960

CO = community organization, KB = Khushhali Bank, — = Not Available Source: Khushhali Bank.

Appendix 3

19

COMMUNITY INVESTMENT FUND SERVICE PROVIDERS

No.

Name of Service Provider

Date of First

Contract

Contract Coverage

Period

Infrastructure Projects Managed

Amount Earned (through

31 Dec 2007) (PRs)

Amount Spent on Small Infrastructure

Projects (PRs)

1. Designmen Consulting Engineers (Pvt)

Mar 2003 Mar 2003–Jun 2007

1,552 13,121,895 187,455,648

2. Human Development Foundation

Jun 2002 Jun 2002–Jun 2007

2 20,994 299,912

3. Sindh Graduates Association

Jul 2002 Jul 2002–Jun 2007

15 127,708 1,824,400

Total 1,569 13,270,597 189,579,960

Source: Khushhali Bank.

Appendix 4

20

INFORMATION ON COMMUNITY INVESTMENT FUND PROJECTS

Year of Completion ADB-Funded Portion (PRs) Types/Description

2004 2005 2006 2007

Total Amount Average

Project Cost Agricultural Irrigation 80 150 374 108 712 85,255,414 119,741 Community Halls 12 70 143 43 268 39,801,501 148,513 Domestic Water Supply 29 32 96 9 166 16,011,697 96,456 Road and Bridges 19 20 74 15 128 14,217,906 111,077 Community Latrines 3 11 31 26 71 8,226,017 115,859 School Buildings 9 15 12 12 48 6,940,088 144,585 Rural Electrification 4 7 21 22 54 6,919,365 128,136 Flood Protection Walls 3 11 5 3 22 3,023,604 137,437 Drainage and Sewerage 8 3 7 5 23 2,575,421 111,975 Community Wheat Mills 2 10 3 1 16 1,742,604 108,913 Livestock Shelters 1 7 4 3 15 2,153,200 143,547 Other 15 22 5 4 46 2,713,143 58,981

Subtotal 185 358 775 251 1,569 189,579,960 118,768Consultancy Fee 13,270,597 Management Cost 704,806

Total 203,555,363 Source: Khushhali Bank.

Appendix 5

21

BALANCE SHEETS AND INCOME STATEMENTS OF THE FUNDS

Table A5.1: Microfinance Social Development Fund ($ million)

2001 2002 2003 2004 2005 2006 2007 Balance Sheet Assets 30.1 41.6 42.5 40.8 40.7 40.5 40.9 Liabilities 0.0 0.0 0.0 0.0 0.0 0.0 0.0 Net Assets 30.1 41.6 42.5 40.8 40.7 40.5 40.9

Represented by Government of Pakistan Contribution 29.1 40.8 41.7 40.0 39.8 39.1 39.1 Khushhali Bank Contribution 0.0 0.1 0.1 0.2 0.2 0.2 0.2 Accumulated Surplus 1.0 0.6 0.6 0.6 0.7 1.2 1.6 Total 30.1 41.6 42.5 40.8 40.7 40.5 40.9 Income Statement Income 2.6 2.4 3.4 3.3 3.6 4.3 4.2 Expenses 0.0 0.1 1.8 1.6 1.9 1.7 2.3 Net Contribution to Accumulated Surplus 2.6 2.3 1.6 1.8 1.8 2.6 1.9

Note: Numbers may not sum precisely due to rounding. Source: Audited financial statements.

Table A5.2: Community Investment Fund ($ million)

2001 2002 2003 2004 2005 Balance Sheet Assets 10.0 20.8 21.3 20.4 20.4 Liabilities 0.0 0.0 0.0 0.0 0.0 Net Assets 10.0 20.8 21.3 20.4 20.4

Represented by Government of Pakistan Contribution 9.7 20.6 21.0 20.2 20.1 Khushhali Bank Contribution 0.0 0.0 0.0 0.0 0.0 Accumulated Surplus 0.3 0.2 0.2 0.2 0.4 Total 10.0 20.8 21.3 20.4 20.4 Income Statement Income 0.9 0.8 1.1 1.1 1.3 Expenses 0.0 0.0 0.0 0.2 0.9 Net Contribution to Accumulated Surplus 0.9 0.8 1.1 0.9 0.4

Note: Numbers may not sum precisely due to rounding. Source: Audited financial statements.

Table A5.3: Risk Mitigation Fund ($ million)

2001 2002 2003 2004 2005 2006 2007 Balance Sheet Assets 5.3 6.0 6.8 7.1 7.8 9.0 10.7 Liabilities 0.0 0.0 0.0 0.0 0.0 0.0 0.0 Net Assets 5.3 6.0 6.8 7.1 7.8 9.0 10.7

Represented by Government of Pakistan Contribution 4.9 5.1 5.3 5.1 5.3 5.7 6.6 Khushhali Bank Contribution 0.0 0.1 0.1 0.1 0.1 0.1 0.1 Accumulated Surplus 0.4 0.9 1.4 1.9 2.5 3.2 3.9 Total 5.3 6.0 6.8 7.1 7.8 9.0 10.7 Income Statement Income 0.4 0.4 0.5 0.5 0.6 0.8 0.6 Expenses 0.0 0.0 0.0 0.0 0.0 0.0 0.0 Net Contribution to Accumulated Surplus 0.4 0.4 0.5 0.5 0.6 0.8 0.6

Note: Numbers may not sum precisely due to rounding. Source: Audited financial statements.

Appendix 5

22

Table A5.4: Deposit Protection Fund ($ million)

2001 2002 2003 2004 2005 2006 2007 Balance Sheet Assets 5.3 6.0 6.8 7.2 7.9 9.1 10.7 Liabilities 0.0 0.0 0.0 0.0 0.0 0.0 0.0 Net Assets 5.3 6.0 6.8 7.2 7.9 9.1 10.8

Represented by Government of Pakistan Contribution 4.9 5.1 5.3 5.1 5.3 5.7 6.6 Khushhali Bank Contribution 0.0 0.1 0.1 0.1 0.1 0.1 0.1 Accumulated Surplus 0.4 0.9 1.5 2.0 2.6 3.3 4.1 Total 5.3 6.0 6.8 7.2 7.9 9.1 10.8 Income Statement Income 0.4 0.4 0.6 0.6 1.2 0.8 0.7 Expenses 0.0 0.0 0.0 0.0 0.0 0.0 0.0 Net Contribution to Accumulated Surplus 0.4 0.4 0.6 0.6 1.2 0.8 0.7

Note: Numbers may not sum precisely due to rounding. Source: Audited financial statements.

Table A5.5: Emergency Livelihood Restoration Fund

($ million) 2005 2006 2007 Balance Sheet Assets 20.4 34.5 36.6 Liabilities 0.0 0.0 0.0 Net Assets 20.4 34.5 36.6

Represented by Government of Pakistan Contribution 20.1 19.7 19.7 Khushhali Bank Contribution 0.0 0.0 0.0 Transfer from MSDF Income Account 0.0 12.9 12.9 Transfer from CIF Income Account 0.0 4.8 4.8 Accumulated Surplus 0.3 2.1 4.3 Transfer to ELRF Account 0.0 (4.9) (4.9) Total 20.4 34.5 36.6 Income Statement Income 1.2 1.8 2.1 Expenses 0.0 0.0 0.0 Net Contribution to Accumulated Surplus 1.2 1.8 2.1

( ) = negative, CIF = Community Investment Fund, ELRF = Emergency Livelihood Restoration Fund, MSDF = Microfinance Social Development Fund Note: Numbers may not sum precisely due to rounding. Source: Audited financial statements.

Appendix 6

23

LOAN AGREEMENT COVENANTS

Covenant Compliance Status

Article IV, Particular Covenants

Section 4.01

(a) The Borrower shall cause the Program to be carried out with due diligence and efficiency and in conformity with sound administrative, financial, environmental, social organization and microfinance practices.

Fully complied

(b) In the carrying out of the Program, the Borrower shall perform, or cause to be performed, all obligations set forth in Schedule 5 to this Loan Agreement.

Partially complied – Not all obligations set forth in Schedule 5 were complied with (see below)

Section 4.02

The Borrower shall make available, promptly as needed, the funds, facilities, services and other resources which are required, in addition to the proceeds of the Loan, for the carrying out of the Program.

Fully complied

Section 4.03

The Borrower shall ensure that the activities of its departments and agencies with respect to the carrying out of the Program are conducted and coordinated in accordance with sound administrative policies and procedures.

Fully complied

Section 4.04

(a) The Borrower shall maintain, or cause to be maintained, records and documents adequate to identify the Eligible Items financed out of the proceeds of the Loan and to record the progress of the Program.

Fully complied

(b) The Borrower shall enable the Bank's representatives to inspect any relevant records and documents referred to in paragraph (a) of this Section.

Fully complied

Section 4.05

(a) The Borrower shall furnish, or cause to be furnished, to the Bank all such reports and information as the Bank shall reasonably request concerning (i) the Loan, and the expenditure of the proceeds and maintenance of the service thereof; (ii) the goods financed out of the proceeds of the Loan; (iii) the Counterpart Funds and the use thereof; (iv) the implementation of the Program, including the accomplishment of the targets and carrying out of the actions set out in the Policy Letter; (v) financial and economic conditions in the territory of the Borrower and the international balance-of-payments position of the Borrower; and (vi) any other matters relating to the purposes of the Loan.

Fully complied

(b) Without limiting the generality of the foregoing, the Borrower shall cause SBP, in consultation with MOF, to furnish to the Bank six-monthly reports on the carrying out of the Program and on the accomplishment of the targets and carrying out of the actions set out in the Policy Letter. Such reports shall be submitted in such form and in such detail and within such a period as the Bank shall reasonably request, and shall indicate, among other things, progress made and problems encountered during the six-month period under review, steps taken or proposed to be taken to remedy these problems, and proposed program of, activities and expected progress during the following six-month period.

Fully complied

Appendix 6

24

Covenant Compliance Status

(c) Promptly after the closing date for withdrawals from the Loan Account, but in any event not later than three (3) months thereafter or such later date as may be agreed for this purpose between the Borrower and the Bank, the Borrower shall prepare and furnish to the Bank a report, in such form and in such detail as the Bank shall reasonably request, on the execution of the Program, including its cost, the performance by the Borrower of its obligations under this Loan Agreement and the accomplishment of the purposes of the Loan.

Not complied Since the closing date for the Loan was 30 June 2003, the report should have been furnished to the Bank no later than 30 September 2003. Although the report was not delivered until 8 May 2008, ADB did not remind the Borrower of its obligation to file this report until 26 February 2008.

Section 4.06

(a) It is the mutual intention of the Borrower and the Bank that no other external debt owed a creditor other than the Bank shall have any priority over the Loan by way of a lien on the assets of the Borrower. To that end, the Borrower undertakes (i) that, except as the Bank may otherwise agree, if any lien shall be created on any assets of the Borrower as security for any external debt, such lien will ipso facto equally and ratably secure the payment of the principal of, and interest charge and any other charge on, the Loan; and (ii) that the Borrower, in creating or permitting the creation of any such lien, will make express provision to that effect.

Fully complied

(b) The provisions of paragraph (a) of this Section shall not apply to (i) any lien created on property, at the time of purchase thereof, solely as security for payment of the purchase price of such property; or (ii) any lien arising in the ordinary course of banking transactions and securing a debt maturing not more than one year after its date.

(c) The term "assets of the Borrower as used in paragraph (a) of this Section includes assets of any political subdivision or any agency of the Borrower and assets of any agency of any such political, subdivision, including SBP and any other institution performing the functions of a central bank for the Borrower.

Schedule 5, Program Implementation and Other Matters

Program Implementation

1. The Borrower shall (a) ensure that the policies adopted and actions taken as described in the Policy Letter prior to the date of this Loan Agreement continue in effect for the duration of the Program period and subsequently, and (b) promptly adopt the other policies and take the other actions indicated in the Program as specified in the Policy Letter, including the Policy Matrix, and ensure that such policies and actions continue in effect during and after the Program period.

Fully complied

2. Except as the Bank may otherwise agree, the Program Executing Agency shall bear overall responsibility for the Program and implement the Program through the PMU. The Program Executing Agency shall consult MOF in implementing the Program.

Fully complied

Appendix 6

25

Covenant Compliance Status

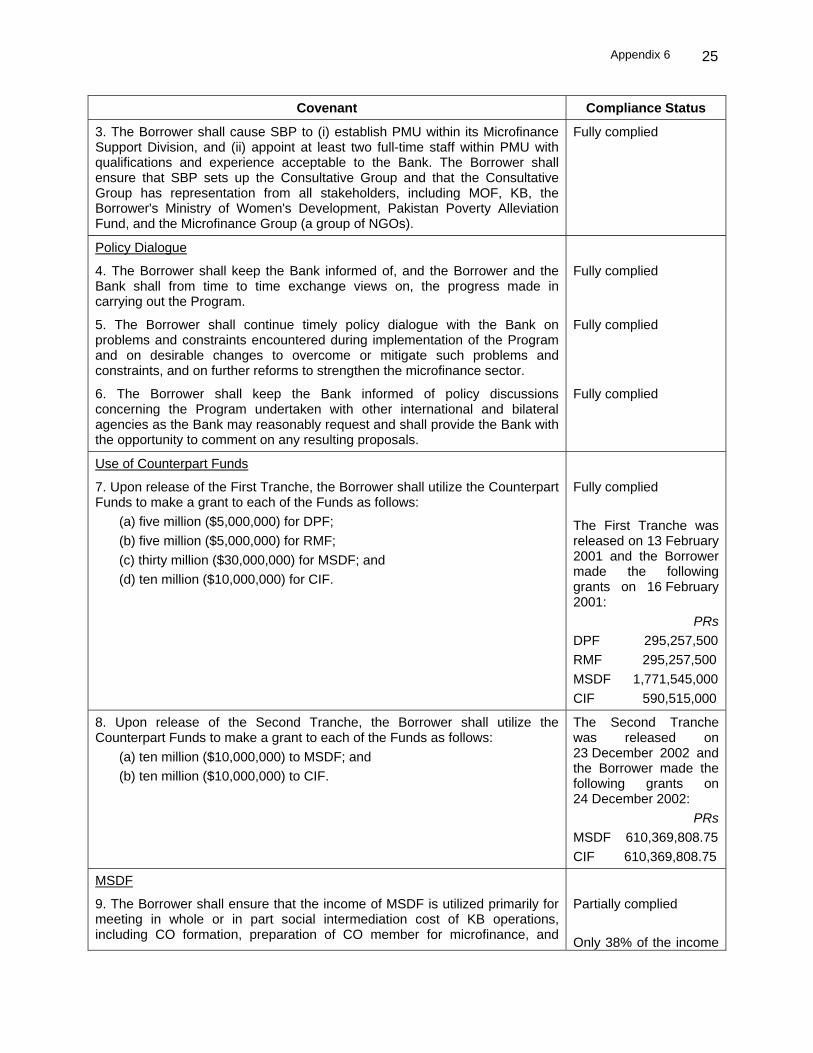

3. The Borrower shall cause SBP to (i) establish PMU within its Microfinance Support Division, and (ii) appoint at least two full-time staff within PMU with qualifications and experience acceptable to the Bank. The Borrower shall ensure that SBP sets up the Consultative Group and that the Consultative Group has representation from all stakeholders, including MOF, KB, the Borrower's Ministry of Women's Development, Pakistan Poverty Alleviation Fund, and the Microfinance Group (a group of NGOs).

Fully complied

Policy Dialogue

4. The Borrower shall keep the Bank informed of, and the Borrower and the Bank shall from time to time exchange views on, the progress made in carrying out the Program.

Fully complied

5. The Borrower shall continue timely policy dialogue with the Bank on problems and constraints encountered during implementation of the Program and on desirable changes to overcome or mitigate such problems and constraints, and on further reforms to strengthen the microfinance sector.

Fully complied

6. The Borrower shall keep the Bank informed of policy discussions concerning the Program undertaken with other international and bilateral agencies as the Bank may reasonably request and shall provide the Bank with the opportunity to comment on any resulting proposals.

Fully complied

Use of Counterpart Funds

7. Upon release of the First Tranche, the Borrower shall utilize the Counterpart Funds to make a grant to each of the Funds as follows:

(a) five million ($5,000,000) for DPF; (b) five million ($5,000,000) for RMF; (c) thirty million ($30,000,000) for MSDF; and (d) ten million ($10,000,000) for CIF.

Fully complied The First Tranche was released on 13 February 2001 and the Borrower made the following grants on 16 February 2001:

PRsDPF 295,257,500 RMF 295,257,500 MSDF 1,771,545,000 CIF 590,515,000

8. Upon release of the Second Tranche, the Borrower shall utilize the Counterpart Funds to make a grant to each of the Funds as follows:

(a) ten million ($10,000,000) to MSDF; and (b) ten million ($10,000,000) to CIF.

The Second Tranche was released on 23 December 2002 and the Borrower made the following grants on 24 December 2002:

PRsMSDF 610,369,808.75 CIF 610,369,808.75

MSDF

9. The Borrower shall ensure that the income of MSDF is utilized primarily for meeting in whole or in part social intermediation cost of KB operations, including CO formation, preparation of CO member for microfinance, and

Partially complied Only 38% of the income

Appendix 6

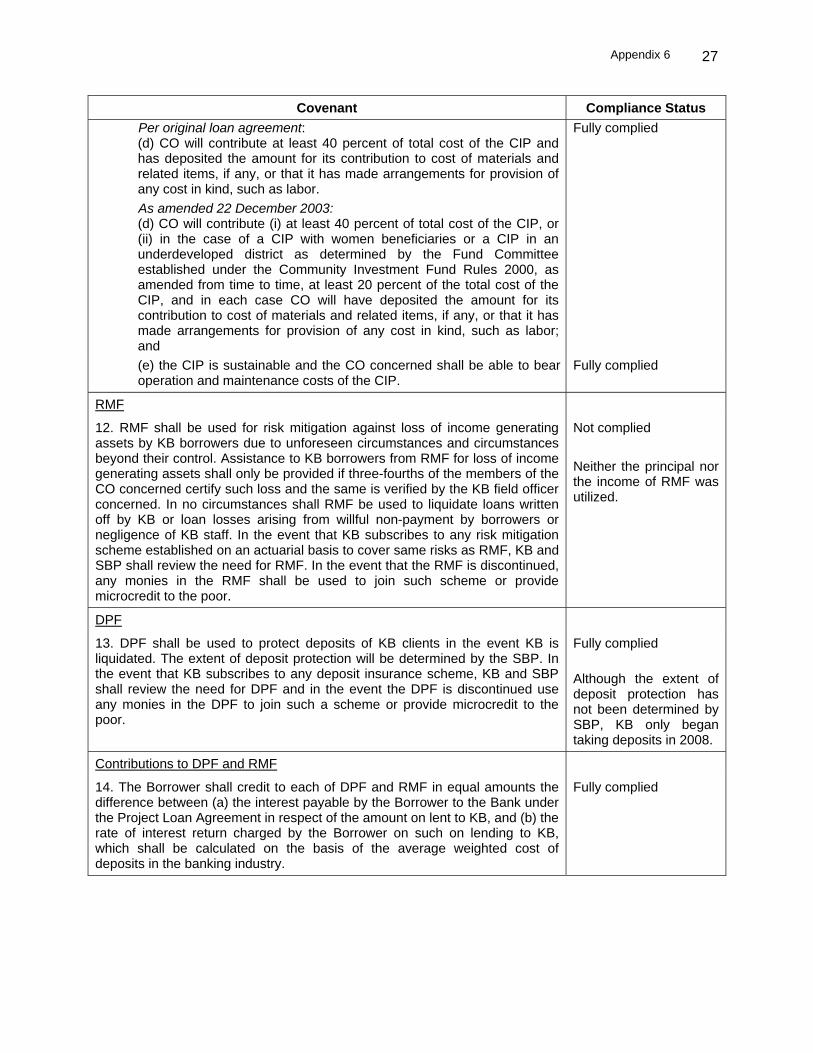

26