Embed Size (px)

Citation preview

To protect the confidential and proprietary information included in this material, it may not be disclosed or provided to any third parties without the approval of Hewitt Associates LLC.

Mid-Year view onPerformance & Reward Trends in India

July 2009

2

[Title MM/DD/YYYY]

The current economic crisis is deeper and broader than many of us initially imagined it would be. Stock market fluctuations, shrinking business and consumer credit, job losses, and government interventions are all uneasy reflections of managing businessin today's environment.

Organisations in order to bridge the gap between shrinking margins and declining business opportunities are compelled to reevaluate their cost structures. Even though the war is global, for Indian businesses, the stakes are high since our success islargely contributed by harnessing global talent together, which by far is the most vulnerable commodity in both good and not so good times. organisations have focused on getting a better return on their people cost and hence are focused on productivity, utilization and innovation.

Hewitt has been working actively with organisations in reworking the business and performance agenda. In our commitment to come back to the market we conducted a mid year dip stick research across 137 organisations to study and analyze their decisionson actual salary increase, variable pay and other survival tactics in combating the current downturn and more focused on revival.

As India Inc. recovers from the initial shock of the downturn, it is interesting to see that organisations are adopting a mix ofdeliberate, optimistic, yet slightly cautious strategies for managing rewards and performance.

The subsequent slides display detailed results on the following: Salary Revision, Salary Freeze, Salary Reduction, Salary Increase – by employee group, by industry & by performance ratings, Variable Pay Plan, Layoffs and Attrition

Introduction

3

[Title MM/DD/YYYY]

Content

1

2

3

4

Survey Highlights

Definition Of Terms

5

6

Variable Pay Plans

Layoffs

Salary Increase

Salary Revision and Salary Freeze

7 Attrition

8 Participant List

4

[Title MM/DD/YYYY]

Survey Highlights

5

[Title MM/DD/YYYY]

Mid-Year survey on Performance & Reward Trends in India

Survey Highlights

Hewitt Associates has recently concluded a Mid-Year survey on Performance & Reward Trends in India. The intent was to capture the potential changes and considerations with regards to 2009 salary increase budgets. This survey was a follow up to Hewitt's India Salary Increase Survey which focused on changes to salary increase budgets post the downturn phase.

The survey measures actual salary increases and compensation practices for five specific employee levels - top executive, senior management, middle management, junior manager/professional/ supervisor and manual workforce.

Information used in this report was collected during the period of May to June 2009.

A total of 137 organisations participated in this survey across 9 primary industries.

The following is a brief summary of the results:

Salary Revision Cycle: Approximately 30% of the organisations have deferred their salary revision cycle. Typically, the salary revisions have been deferred from the month of April to July or October.

Salary Freeze & Salary Reduction: 16% of the organisations have a salary freeze currently. These are mainly organisations in the Financial Services, IT & ITES sectors. Salary reduction is not very prevalent, only 6% of the organisations have reduced salaries.

6

[Title MM/DD/YYYY]

Performance & Reward Trends in India

Survey Highlights

7.2

8.8

8.4

8.0

7.4

2009Projected

10.8

14.3

13.8

13.2

12.4

2008

7.7

9.5

8.7

8.1

7.3

Mid Year 2009

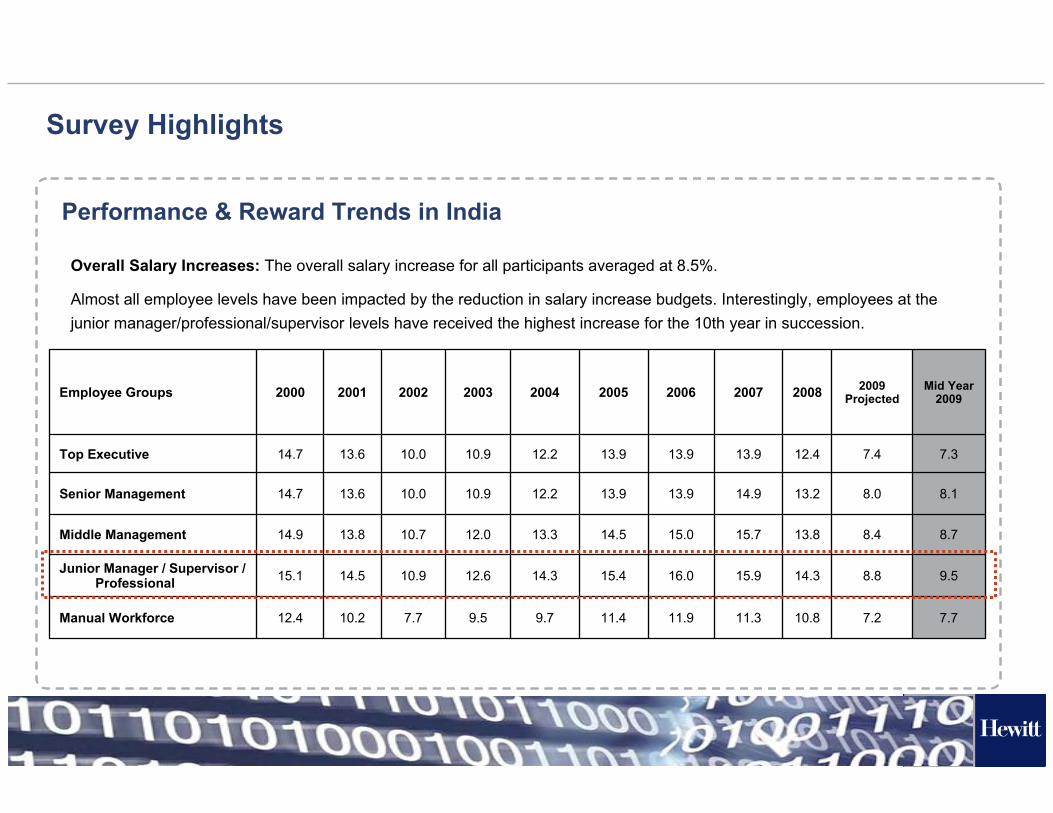

11.311.911.49.79.57.710.212.4Manual Workforce

15.916.015.414.312.610.914.515.1Junior Manager / Supervisor / Professional

15.715.014.513.312.010.713.814.9Middle Management

14.913.913.912.210.910.013.614.7Senior Management

13.913.913.912.210.910.013.614.7Top Executive

20072006200520042003200220012000Employee Groups

Overall Salary Increases: The overall salary increase for all participants averaged at 8.5%.

Almost all employee levels have been impacted by the reduction in salary increase budgets. Interestingly, employees at the junior manager/professional/supervisor levels have received the highest increase for the 10th year in succession.

7

[Title MM/DD/YYYY]

Performance & Reward Trends in India

Survey Highlights

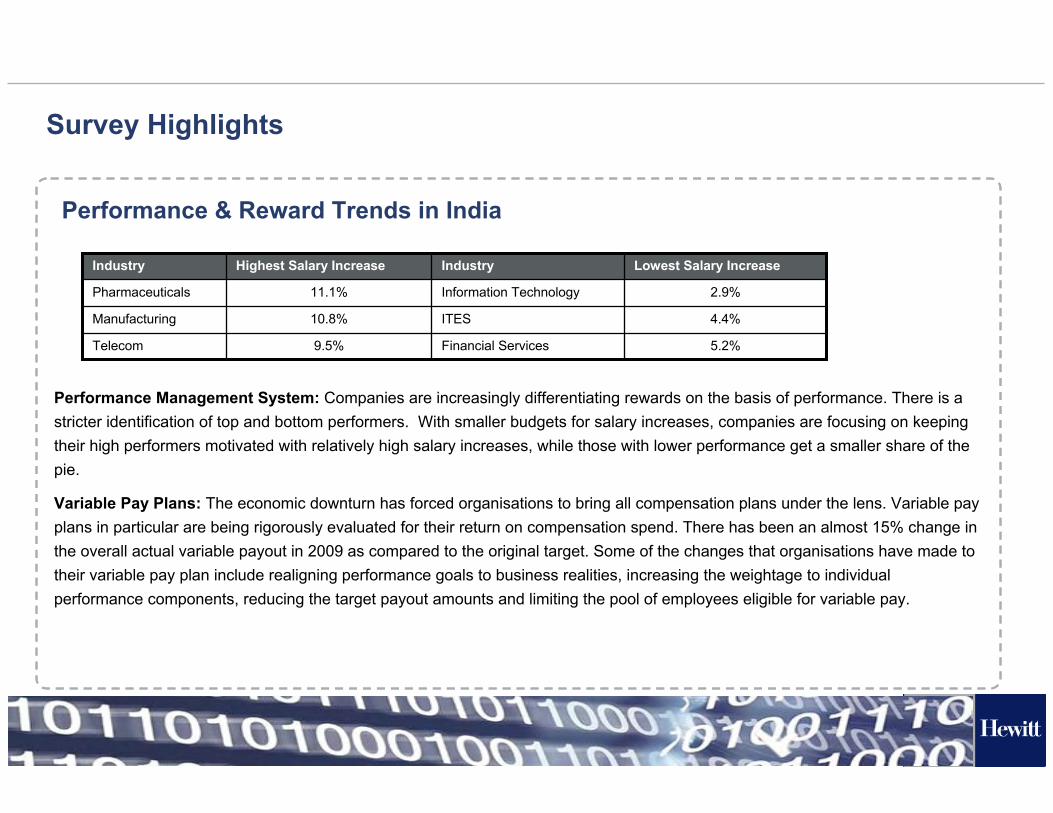

Performance Management System: Companies are increasingly differentiating rewards on the basis of performance. There is a stricter identification of top and bottom performers. With smaller budgets for salary increases, companies are focusing on keeping their high performers motivated with relatively high salary increases, while those with lower performance get a smaller share of the pie.

Variable Pay Plans: The economic downturn has forced organisations to bring all compensation plans under the lens. Variable pay plans in particular are being rigorously evaluated for their return on compensation spend. There has been an almost 15% change in the overall actual variable payout in 2009 as compared to the original target. Some of the changes that organisations have made to their variable pay plan include realigning performance goals to business realities, increasing the weightage to individual performance components, reducing the target payout amounts and limiting the pool of employees eligible for variable pay.

2.9%Information Technology11.1%Pharmaceuticals

9.5%

10.8%

Highest Salary Increase

Telecom

Manufacturing

Industry

Financial Services

ITES

Industry

5.2%

4.4%

Lowest Salary Increase

8

[Title MM/DD/YYYY]

Definition of Terms

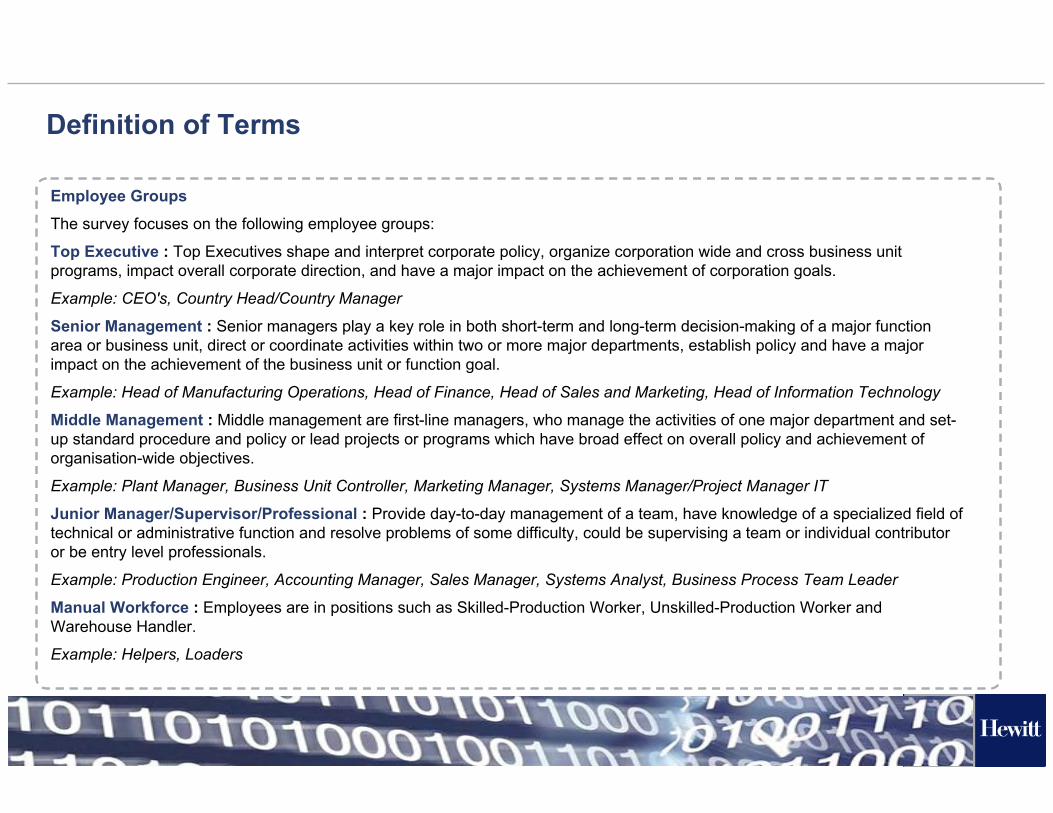

Employee Groups

The survey focuses on the following employee groups:

Top Executive : Top Executives shape and interpret corporate policy, organize corporation wide and cross business unit programs, impact overall corporate direction, and have a major impact on the achievement of corporation goals.

Example: CEO's, Country Head/Country Manager

Senior Management : Senior managers play a key role in both short-term and long-term decision-making of a major function area or business unit, direct or coordinate activities within two or more major departments, establish policy and have a major impact on the achievement of the business unit or function goal.

Example: Head of Manufacturing Operations, Head of Finance, Head of Sales and Marketing, Head of Information Technology

Middle Management : Middle management are first-line managers, who manage the activities of one major department and set-up standard procedure and policy or lead projects or programs which have broad effect on overall policy and achievement of organisation-wide objectives.

Example: Plant Manager, Business Unit Controller, Marketing Manager, Systems Manager/Project Manager IT

Junior Manager/Supervisor/Professional : Provide day-to-day management of a team, have knowledge of a specialized field of technical or administrative function and resolve problems of some difficulty, could be supervising a team or individual contributor or be entry level professionals.

Example: Production Engineer, Accounting Manager, Sales Manager, Systems Analyst, Business Process Team Leader

Manual Workforce : Employees are in positions such as Skilled-Production Worker, Unskilled-Production Worker and Warehouse Handler.

Example: Helpers, Loaders

9

[Title MM/DD/YYYY]

Salary Revision Cycle and Salary Freeze

10

[Title MM/DD/YYYY]

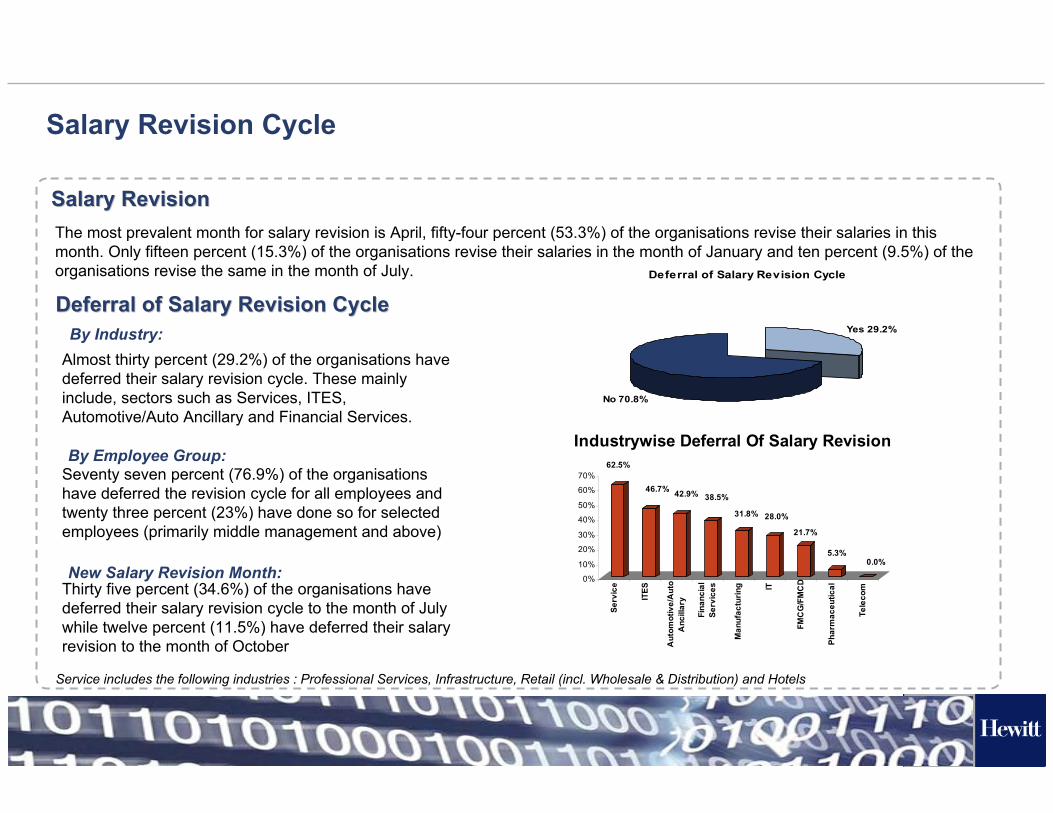

The most prevalent month for salary revision is April, fifty-four percent (53.3%) of the organisations revise their salaries in this month. Only fifteen percent (15.3%) of the organisations revise their salaries in the month of January and ten percent (9.5%) of the organisations revise the same in the month of July.

Salary RevisionSalary Revision

Deferral of Salary Revision CycleDeferral of Salary Revision Cycle

Almost thirty percent (29.2%) of the organisations have deferred their salary revision cycle. These mainly include, sectors such as Services, ITES, Automotive/Auto Ancillary and Financial Services.

Seventy seven percent (76.9%) of the organisations have deferred the revision cycle for all employees and twenty three percent (23%) have done so for selected employees (primarily middle management and above)

Thirty five percent (34.6%) of the organisations have deferred their salary revision cycle to the month of July while twelve percent (11.5%) have deferred their salary revision to the month of October

Salary Revision Cycle

Deferral of Salary Revision Cycle

Yes 29.2%

No 70.8%

Industry wise deferral of Salary Revision

By Industry:

By Employee Group:

New Salary Revision Month:

Service includes the following industries : Professional Services, Infrastructure, Retail (incl. Wholesale & Distribution) and Hotels

62.5%

46.7% 42.9% 38.5%

31.8% 28.0%

21.7%

5.3%0.0%

0%

10%

20%

30%

40%

50%

60%

70%

Serv

ice

ITES

Aut

omot

ive/

Aut

oA

ncill

ary

Fina

ncia

lSe

rvic

es

Man

ufac

turin

g IT

FMC

G/F

MC

D

Phar

mac

eutic

al

Tele

com

Industrywise Deferral Of Salary Revision

11

[Title MM/DD/YYYY]

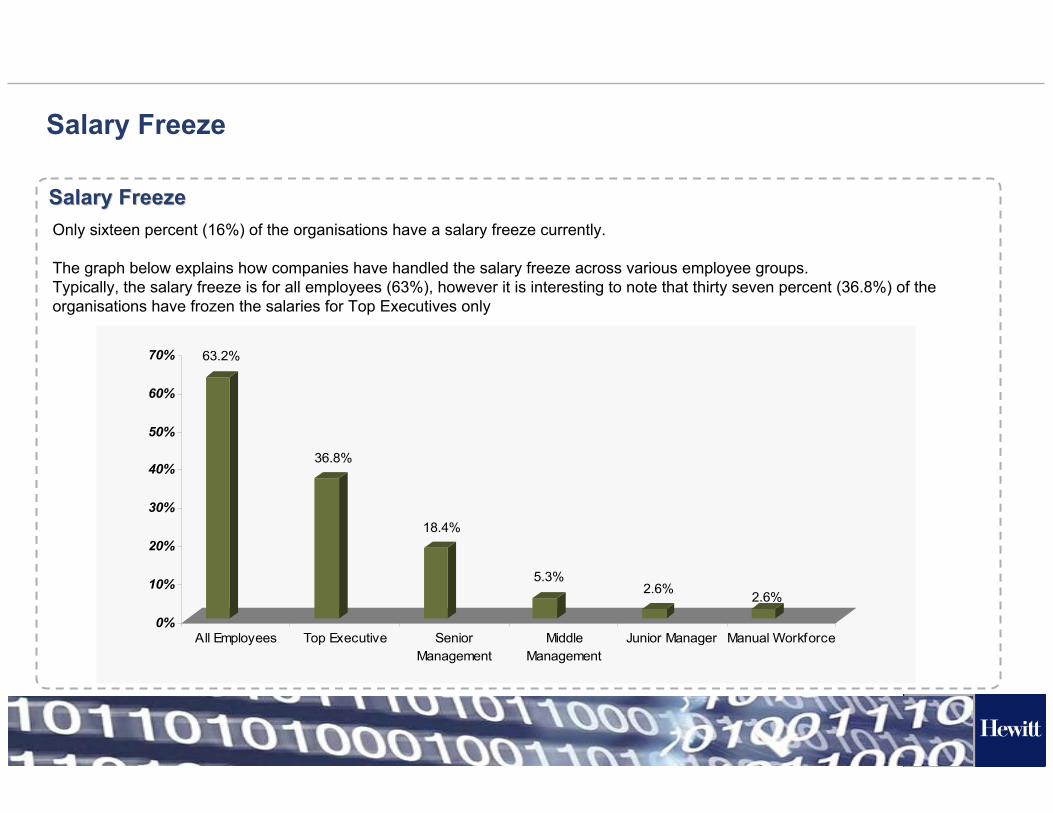

Salary FreezeSalary FreezeOnly sixteen percent (16%) of the organisations have a salary freeze currently.

The graph below explains how companies have handled the salary freeze across various employee groups.Typically, the salary freeze is for all employees (63%), however it is interesting to note that thirty seven percent (36.8%) of the organisations have frozen the salaries for Top Executives only

Salary Freeze

63.2%

36.8%

18.4%

5.3%2.6% 2.6%

0%

10%

20%

30%

40%

50%

60%

70%

All Employees Top Executive SeniorManagement

MiddleManagement

Junior Manager Manual Workforce

12

[Title MM/DD/YYYY]

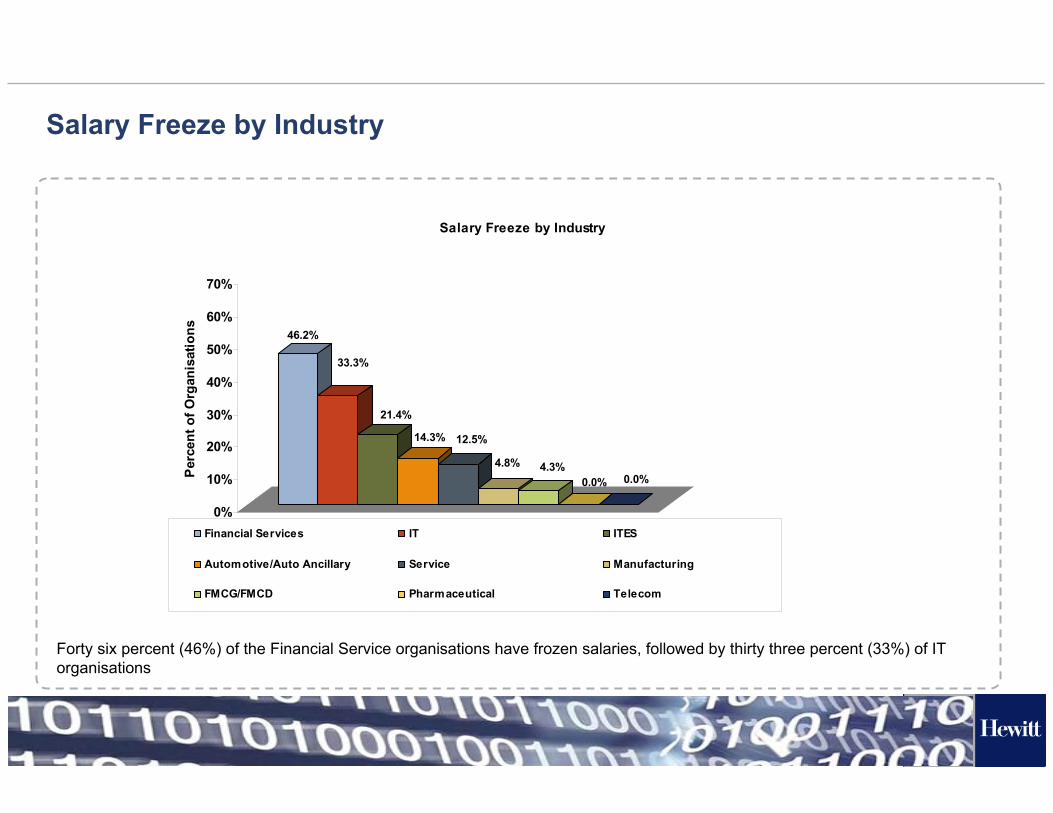

Salary Freeze by Industry

Forty six percent (46%) of the Financial Service organisations have frozen salaries, followed by thirty three percent (33%) of IT organisations

46.2%

33.3%

21.4%

14.3% 12.5%

4.8% 4.3%0.0% 0.0%

0%

10%

20%

30%

40%

50%

60%

70%

Per

cent

of O

rgan

isat

ions

Salary Freeze by Industry

Financial Services IT ITES

Automotive/Auto Ancillary Service Manufacturing

FMCG/FMCD Pharmaceutical Telecom

13

[Title MM/DD/YYYY]

Overall Salary ReductionOverall Salary Reduction

Overall Salary Reduction in 2009

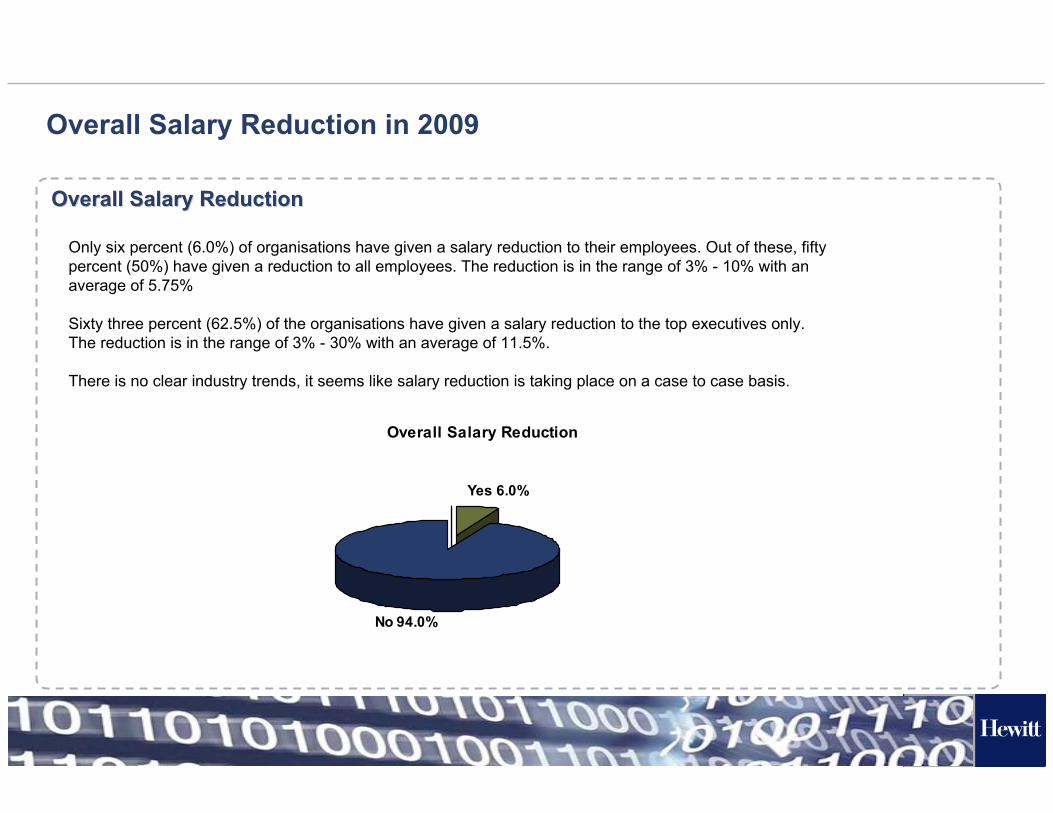

Only six percent (6.0%) of organisations have given a salary reduction to their employees. Out of these, fifty percent (50%) have given a reduction to all employees. The reduction is in the range of 3% - 10% with an average of 5.75%

Sixty three percent (62.5%) of the organisations have given a salary reduction to the top executives only. The reduction is in the range of 3% - 30% with an average of 11.5%.

There is no clear industry trends, it seems like salary reduction is taking place on a case to case basis.

Overall Salary Reduction

No 94.0%

Yes 6.0%

14

[Title MM/DD/YYYY]

Salary Increase

15

[Title MM/DD/YYYY]

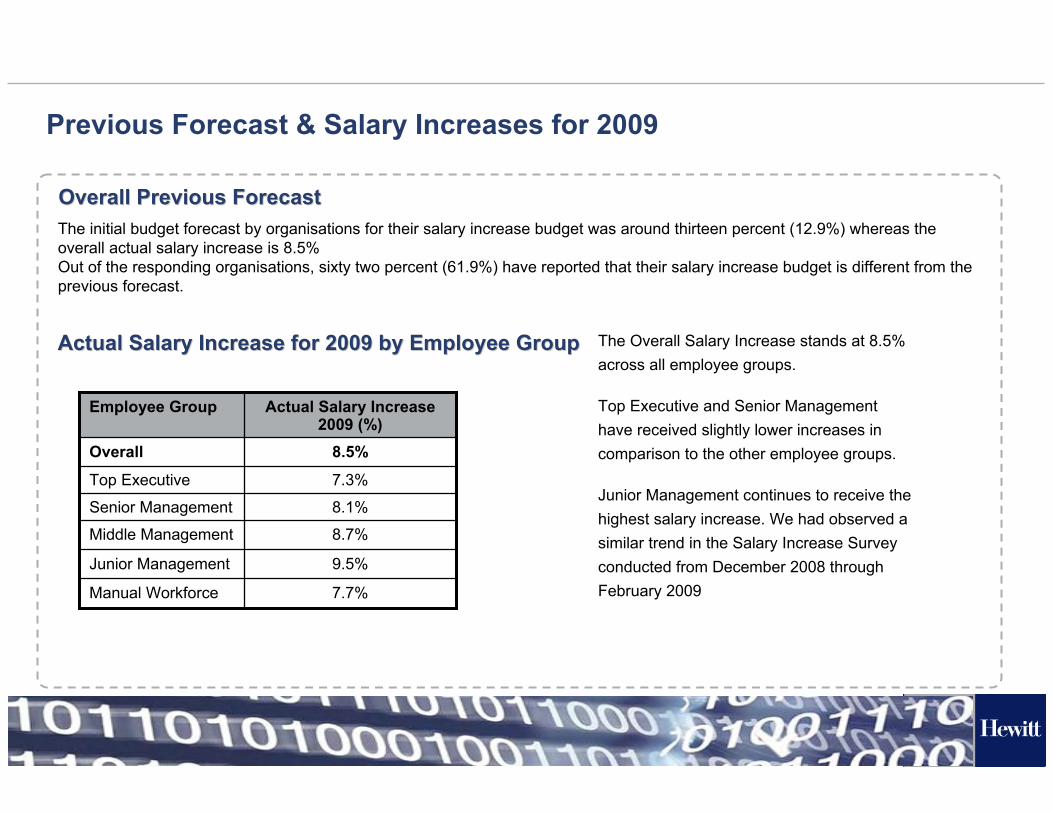

Overall Previous ForecastOverall Previous ForecastThe initial budget forecast by organisations for their salary increase budget was around thirteen percent (12.9%) whereas the overall actual salary increase is 8.5% Out of the responding organisations, sixty two percent (61.9%) have reported that their salary increase budget is different from the previous forecast.

Previous Forecast & Salary Increases for 2009

Actual Salary Increase for 2009 by Employee GroupActual Salary Increase for 2009 by Employee Group

Manual Workforce

Junior Management

Middle Management

Senior Management

Top Executive

Overall

Employee Group

7.7%

9.5%

8.7%

8.1%

7.3%

8.5%

Actual Salary Increase 2009 (%)

The Overall Salary Increase stands at 8.5% across all employee groups.

Top Executive and Senior Management have received slightly lower increases in comparison to the other employee groups.

Junior Management continues to receive the highest salary increase. We had observed a similar trend in the Salary Increase Survey conducted from December 2008 through February 2009

16

[Title MM/DD/YYYY]

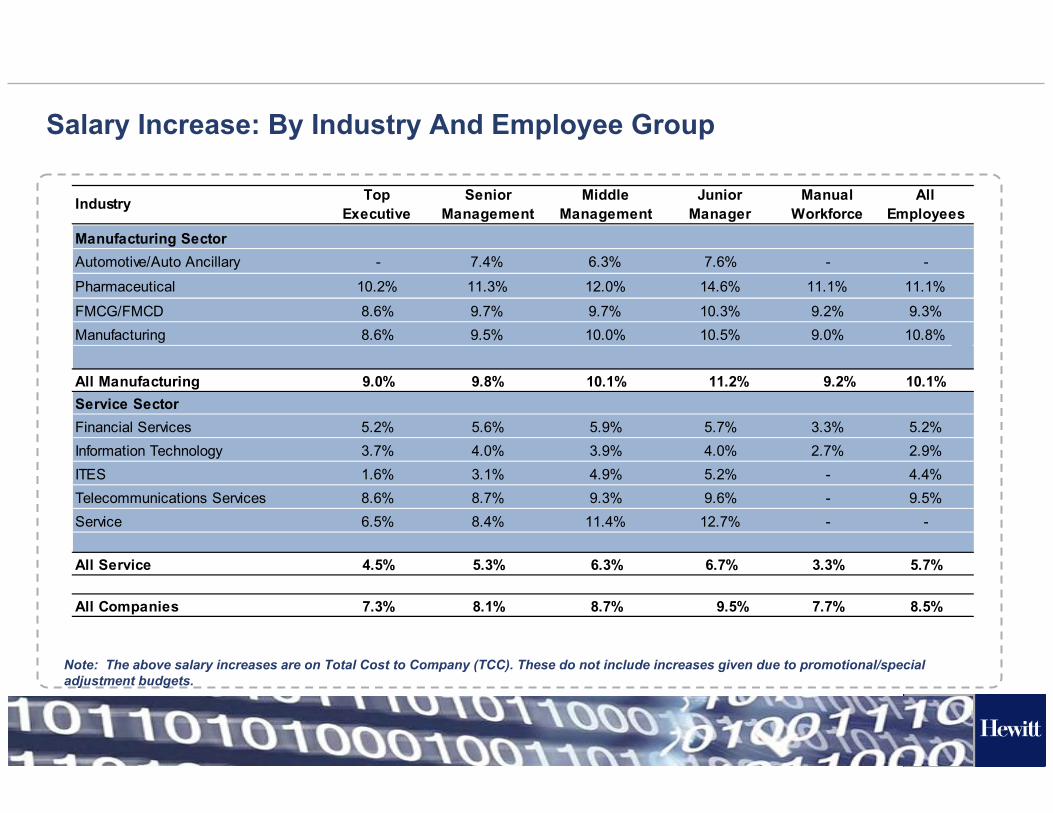

Salary Increase: By Industry And Employee Group

Note: The above salary increases are on Total Cost to Company (TCC). These do not include increases given due to promotional/special adjustment budgets.

- 7.6% -

10.2% 14.6% 11.1%

8.6% 10.3% 9.2%8.6% 10.5% 9.0%

9.0% 11.2% 9.2%Service Sector

5.2% 5.7% 3.3%3.7% 4.0% 2.7%1.6% 5.2% -8.6% 9.6% -6.5% 12.7% -

4.5% 6.7% 3.3%

7.3% 9.5% 7.7%All Companies

Industry

Pharmaceutical

Automotive/Auto AncillaryManufacturing Sector

Service

All Manufacturing

Telecommunications Services

Financial Services

ITESInformation Technology

FMCG/FMCDManufacturing

All Service

Top Executive

Junior Manager

Middle Management

Manual Workforce

Senior Management

All Employees

-

11.1%

9.3%10.8%

10.1%

5.2%2.9%4.4%9.5%

-

5.7%

8.5%

7.4%

11.3%

9.7%9.5%

9.8% 10.1%

10.0%9.7%

12.0%

6.3%

5.9%3.9%4.9%9.3%

11.4%

6.3%

8.7%

3.1%4.0%5.6%

8.1%

5.3%

8.4%8.7%

17

[Title MM/DD/YYYY]

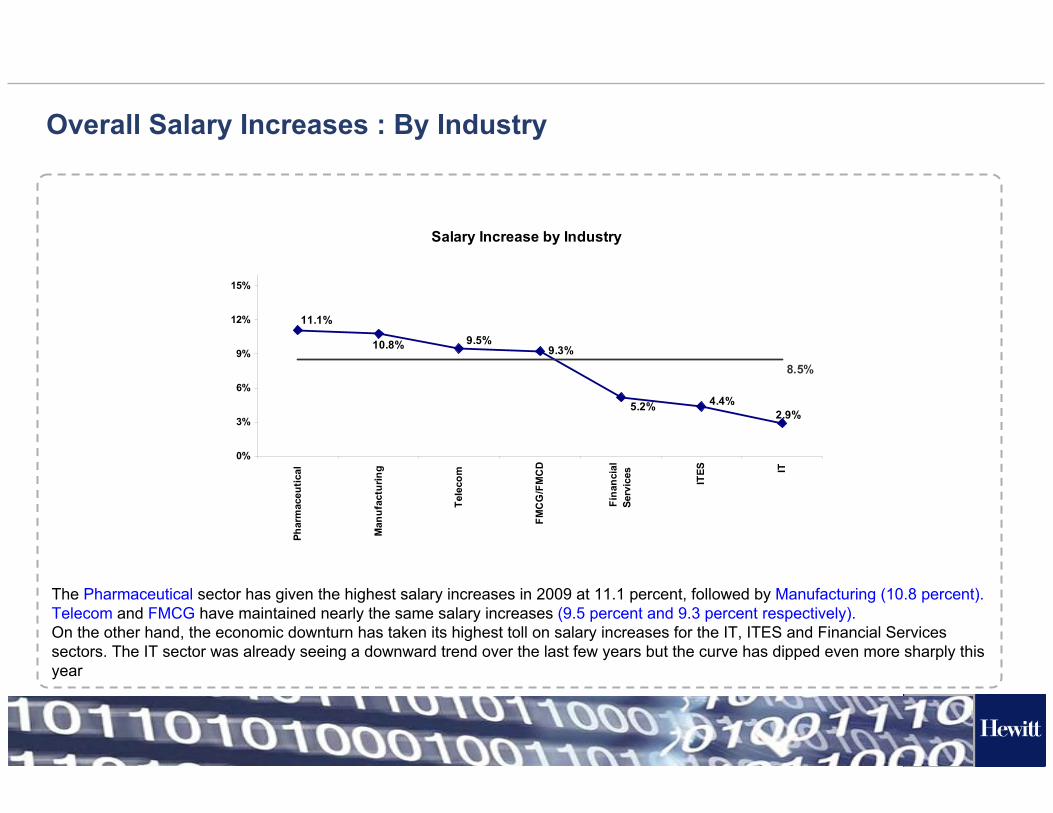

Overall Salary Increases : By Industry

The Pharmaceutical sector has given the highest salary increases in 2009 at 11.1 percent, followed by Manufacturing (10.8 percent).Telecom and FMCG have maintained nearly the same salary increases (9.5 percent and 9.3 percent respectively).On the other hand, the economic downturn has taken its highest toll on salary increases for the IT, ITES and Financial Services sectors. The IT sector was already seeing a downward trend over the last few years but the curve has dipped even more sharply this year

Salary Increase by Industry

9.3%

2.9%5.2%

10.8% 9.5%

11.1%

4.4%

8.5%

0%

3%

6%

9%

12%

15%Ph

arm

aceu

tical

Man

ufac

turin

g

Tele

com

FMC

G/F

MC

D

Fina

ncia

lSe

rvic

es ITES IT

18

[Title MM/DD/YYYY]

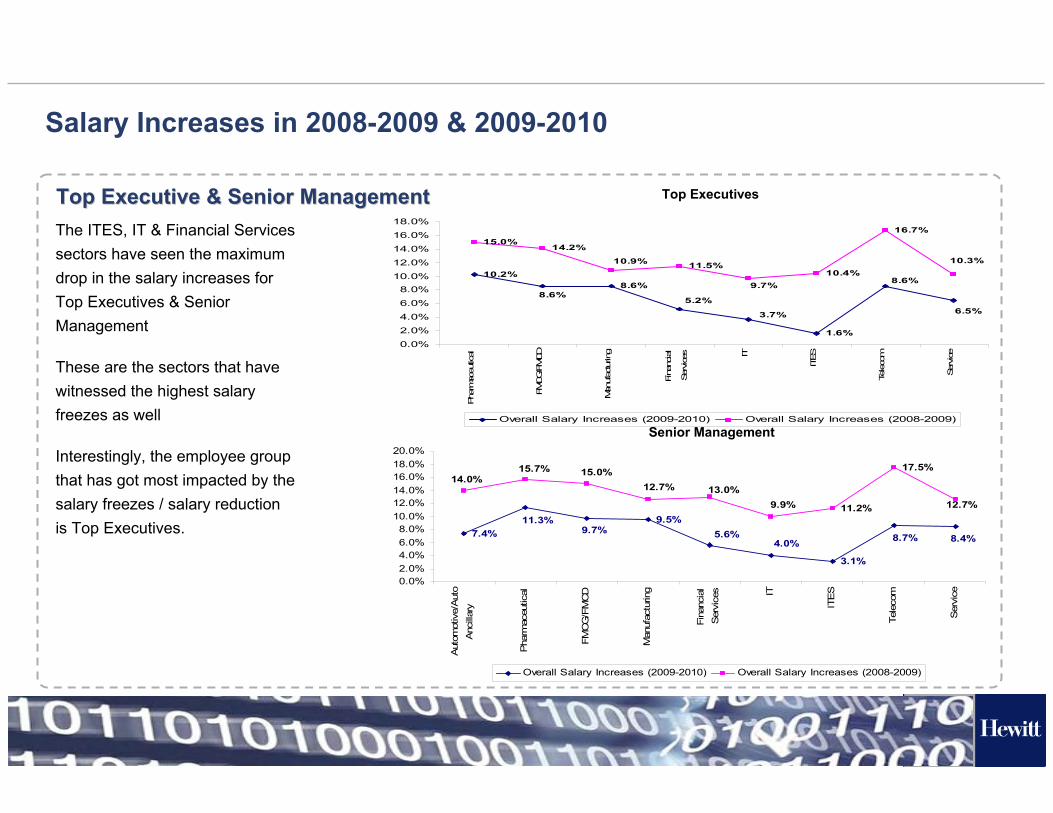

Top Executive & Senior ManagementTop Executive & Senior Management

Salary Increases in 2008-2009 & 2009-2010

The ITES, IT & Financial Services sectors have seen the maximum drop in the salary increases for Top Executives & Senior Management

These are the sectors that have witnessed the highest salary freezes as well

Interestingly, the employee group that has got most impacted by the salary freezes / salary reduction is Top Executives.

10.2%8.6%

1.6%

15.0%14.2%

11.5%10.4%

16.7%

3.7%

5.2%8.6%

6.5%

8.6%

10.9%

9.7%

10.3%

0.0%

2.0%

4.0%

6.0%

8.0%10.0%

12.0%

14.0%

16.0%

18.0%

Pha

rmac

eutic

al

FMCG/FMCD

Man

ufac

turin

g

Fina

ncial

Ser

vice

s IT

ITES

Teleco

m

Service

Overall Salary Increases (2009-2010) Overall Salary Increases (2008-2009)

Top Executives

7.4%9.5%

3.1%

11.2%

17.5%

11.3%9.7% 5.6%

4.0% 8.7% 8.4%

12.7%9.9%13.0%12.7%

15.0%15.7%14.0%

0.0%2.0%4.0%6.0%8.0%

10.0%12.0%14.0%16.0%18.0%20.0%

Aut

omot

ive/

Aut

oA

ncill

ary

Pha

rmac

eutic

al

FMC

G/F

MC

D

Man

ufac

turin

g

Fina

ncia

lS

ervi

ces IT

ITE

S

Tele

com

Ser

vice

Overall Salary Increases (2009-2010) Overall Salary Increases (2008-2009)

Senior Management

19

[Title MM/DD/YYYY]

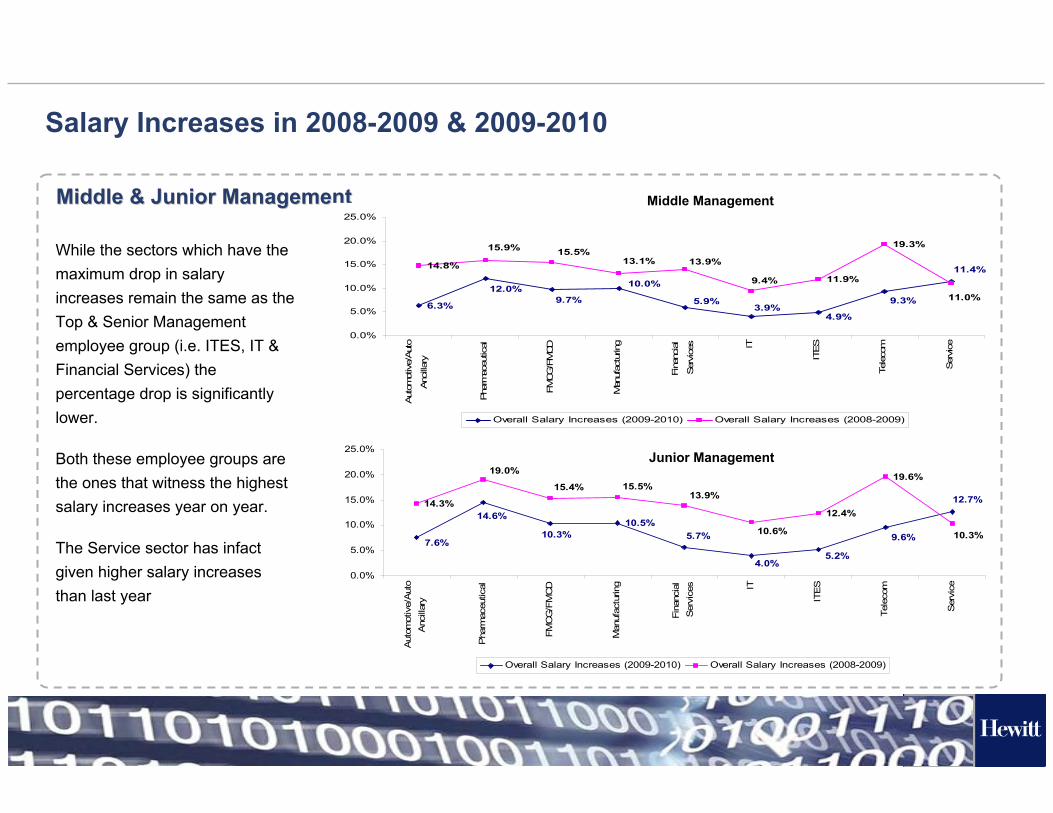

Middle & Junior ManagementMiddle & Junior Management

Salary Increases in 2008-2009 & 2009-2010

6.3%

14.8%11.9%

19.3%

11.4%

9.3%12.0%

9.7%

10.0%

5.9%3.9%

4.9%

11.0%

13.9%13.1%15.5%15.9%

9.4%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Aut

omot

ive/

Aut

o

Anc

illar

y

Pha

rmac

eutic

al

FMCG

/FM

CD

Man

ufac

turin

g

Fina

ncial

Ser

vice

s IT

ITES

Tele

com

Ser

vice

Overall Salary Increases (2009-2010) Overall Salary Increases (2008-2009)

10.5%

14.3%12.4%

19.6%

12.7%

9.6%

5.2%4.0%

5.7%10.3%

14.6%

7.6%

19.0%

15.4% 15.5%13.9%

10.6% 10.3%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Aut

omot

ive/

Aut

oA

ncill

ary

Pha

rmac

eutic

al

FMC

G/F

MC

D

Man

ufac

turin

g

Fina

ncia

lS

ervi

ces IT

ITE

S

Tele

com

Ser

vice

Overall Salary Increases (2009-2010) Overall Salary Increases (2008-2009)

Middle Management

Junior Management

While the sectors which have the maximum drop in salary increases remain the same as the Top & Senior Management employee group (i.e. ITES, IT & Financial Services) the percentage drop is significantly lower.

Both these employee groups are the ones that witness the highest salary increases year on year.

The Service sector has infact given higher salary increases than last year

20

[Title MM/DD/YYYY]

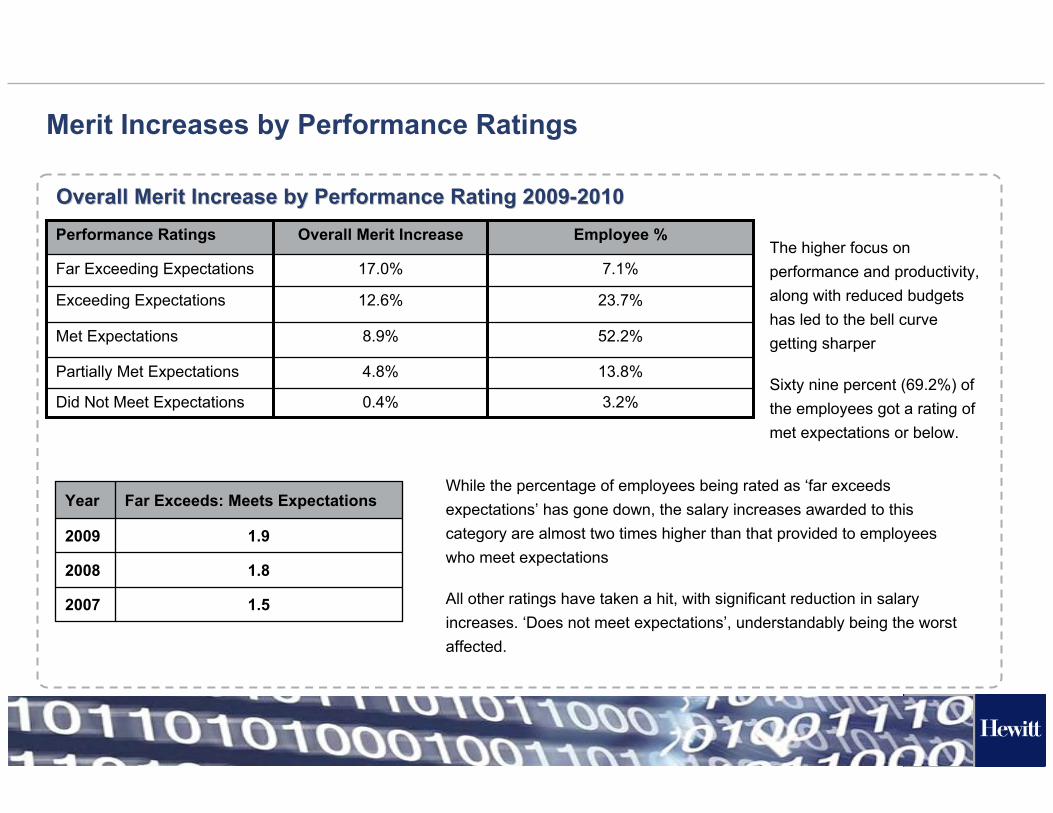

Overall Merit Increase by Performance Rating 2009Overall Merit Increase by Performance Rating 2009--20102010

Merit Increases by Performance Ratings

3.2%

13.8%

52.2%

23.7%

7.1%

Employee %

Did Not Meet Expectations

Partially Met Expectations

Met Expectations

Exceeding Expectations

Far Exceeding Expectations

Performance Ratings

0.4%

4.8%

8.9%

12.6%

17.0%

Overall Merit IncreaseThe higher focus on performance and productivity, along with reduced budgets has led to the bell curve getting sharper

Sixty nine percent (69.2%) of the employees got a rating of met expectations or below.

1.52007

1.82008

1.92009

Far Exceeds: Meets ExpectationsYearWhile the percentage of employees being rated as ‘far exceeds expectations’ has gone down, the salary increases awarded to this category are almost two times higher than that provided to employees who meet expectations

All other ratings have taken a hit, with significant reduction in salary increases. ‘Does not meet expectations’, understandably being the worst affected.

21

[Title MM/DD/YYYY]

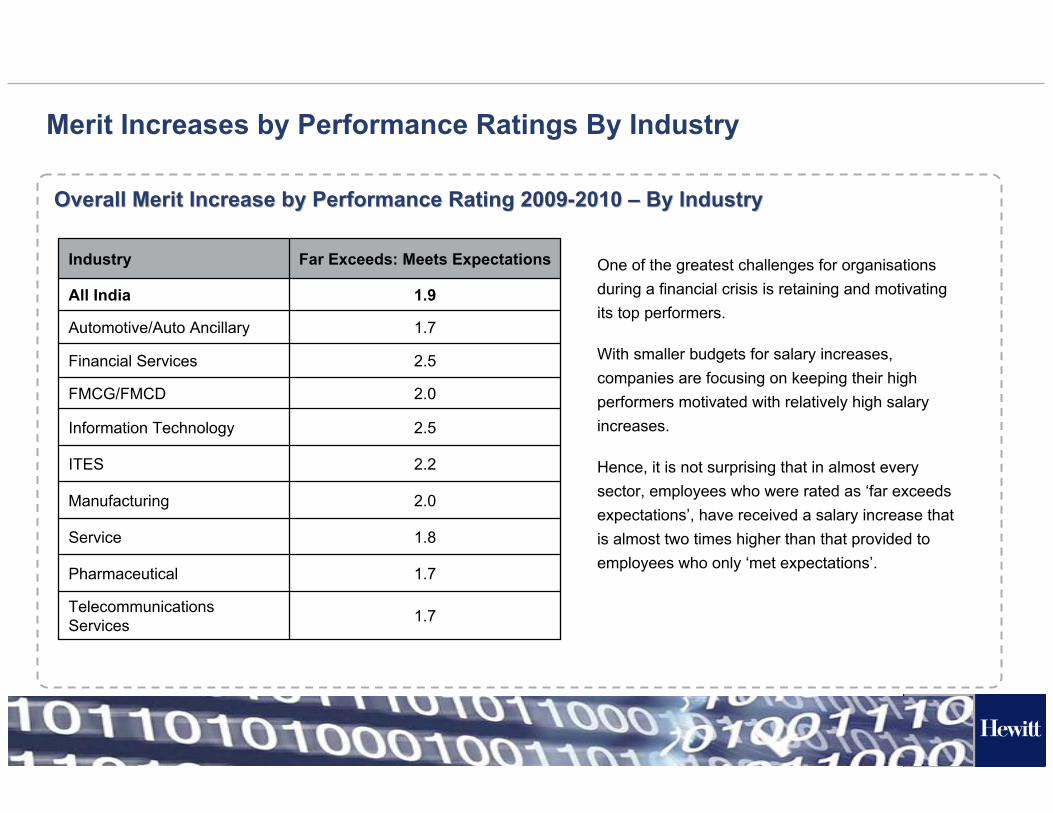

Overall Merit Increase by Performance Rating 2009Overall Merit Increase by Performance Rating 2009--2010 2010 –– By IndustryBy Industry

Merit Increases by Performance Ratings By Industry

1.8Service

1.7Pharmaceutical

2.5Financial Services

2.0FMCG/FMCD

2.5Information Technology

2.2ITES

2.0Manufacturing

1.7Telecommunications Services

1.7Automotive/Auto Ancillary

1.9All India

Far Exceeds: Meets ExpectationsIndustry One of the greatest challenges for organisations during a financial crisis is retaining and motivating its top performers.

With smaller budgets for salary increases, companies are focusing on keeping their high performers motivated with relatively high salary increases.

Hence, it is not surprising that in almost every sector, employees who were rated as ‘far exceeds expectations’, have received a salary increase that is almost two times higher than that provided to employees who only ‘met expectations’.

22

[Title MM/DD/YYYY]

Variable Pay Plans

23

[Title MM/DD/YYYY]

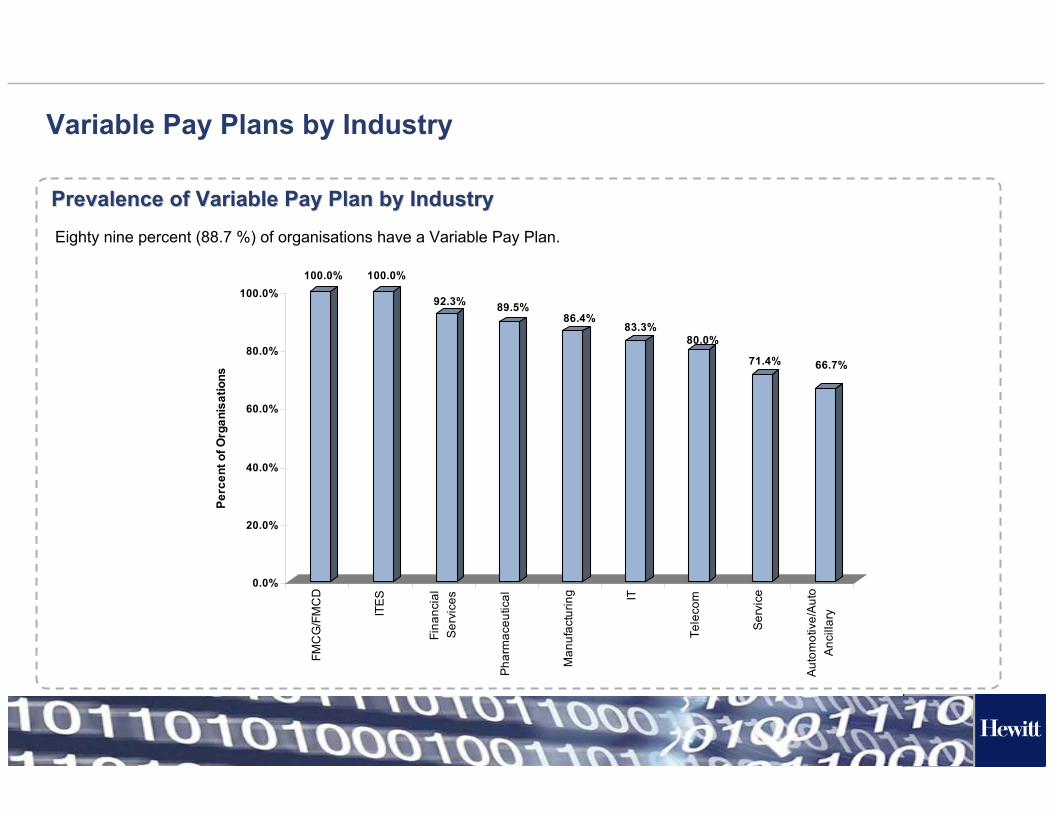

Prevalence of Variable Pay Plan by IndustryPrevalence of Variable Pay Plan by Industry

Variable Pay Plans by Industry

Eighty nine percent (88.7 %) of organisations have a Variable Pay Plan.

100.0% 100.0%

92.3% 89.5%86.4%

83.3%80.0%

71.4% 66.7%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

Perc

ent o

f Org

anis

atio

ns

FMC

G/F

MC

D

ITES

Fina

ncia

lSe

rvic

es

Phar

mac

eutic

al

Man

ufac

turin

g IT

Tele

com

Ser

vice

Aut

omot

ive/

Aut

oA

ncill

ary

24

[Title MM/DD/YYYY]

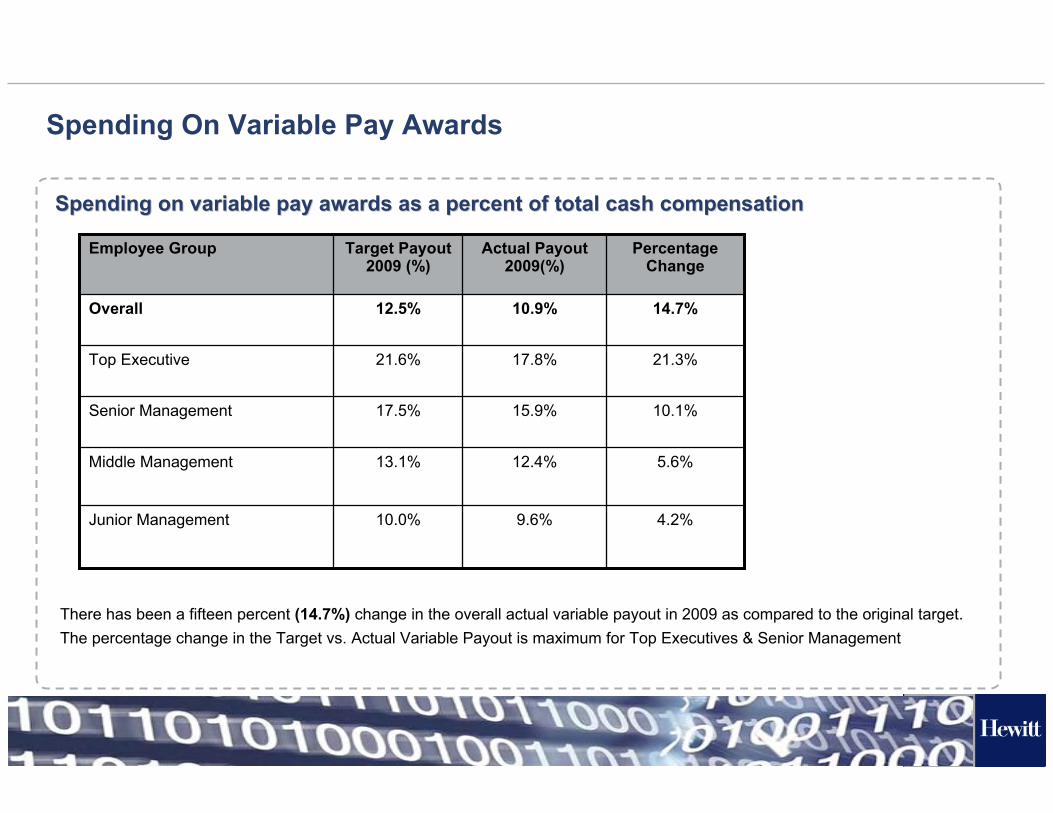

Spending On Variable Pay Awards

Spending on variable pay awards as a percent of total cash compeSpending on variable pay awards as a percent of total cash compensationnsation

9.6%

12.4%

15.9%

17.8%

10.9%

Actual Payout 2009(%)

4.2%

5.6%

10.1%

21.3%

14.7%

Percentage Change

10.0%Junior Management

13.1%Middle Management

17.5%Senior Management

21.6%Top Executive

12.5%Overall

Target Payout 2009 (%)

Employee Group

There has been a fifteen percent (14.7%) change in the overall actual variable payout in 2009 as compared to the original target. The percentage change in the Target vs. Actual Variable Payout is maximum for Top Executives & Senior Management

25

[Title MM/DD/YYYY]

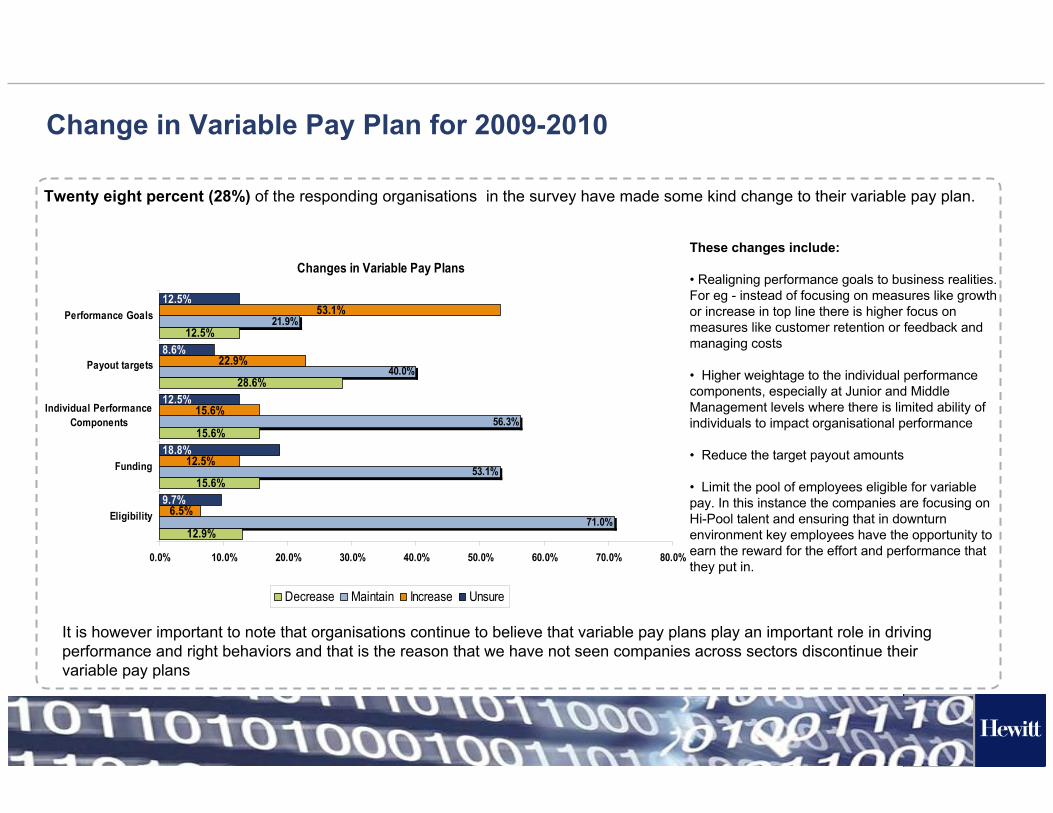

Change in Variable Pay Plan for 2009-2010

Changes in Variable Pay Plans

12.9%

28.6%

12.5%

71.0%

53.1%

21.9%

15.6%

22.9%

18.8%

12.5%

15.6%

15.6%

56.3%

40.0%

53.1%

6.5%

12.5%

9.7%

8.6%

12.5%

0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0% 70.0% 80.0%

Eligibility

Funding

Individual PerformanceComponents

Payout targets

Performance Goals

Decrease Maintain Increase Unsure

These changes include:

• Realigning performance goals to business realities. For eg - instead of focusing on measures like growth or increase in top line there is higher focus on measures like customer retention or feedback and managing costs

• Higher weightage to the individual performance components, especially at Junior and Middle Management levels where there is limited ability of individuals to impact organisational performance

• Reduce the target payout amounts

• Limit the pool of employees eligible for variable pay. In this instance the companies are focusing on Hi-Pool talent and ensuring that in downturn environment key employees have the opportunity to earn the reward for the effort and performance that they put in.

Twenty eight percent (28%) of the responding organisations in the survey have made some kind change to their variable pay plan.

It is however important to note that organisations continue to believe that variable pay plans play an important role in drivingperformance and right behaviors and that is the reason that we have not seen companies across sectors discontinue their variable pay plans

26

[Title MM/DD/YYYY]

Layoffs

27

[Title MM/DD/YYYY]

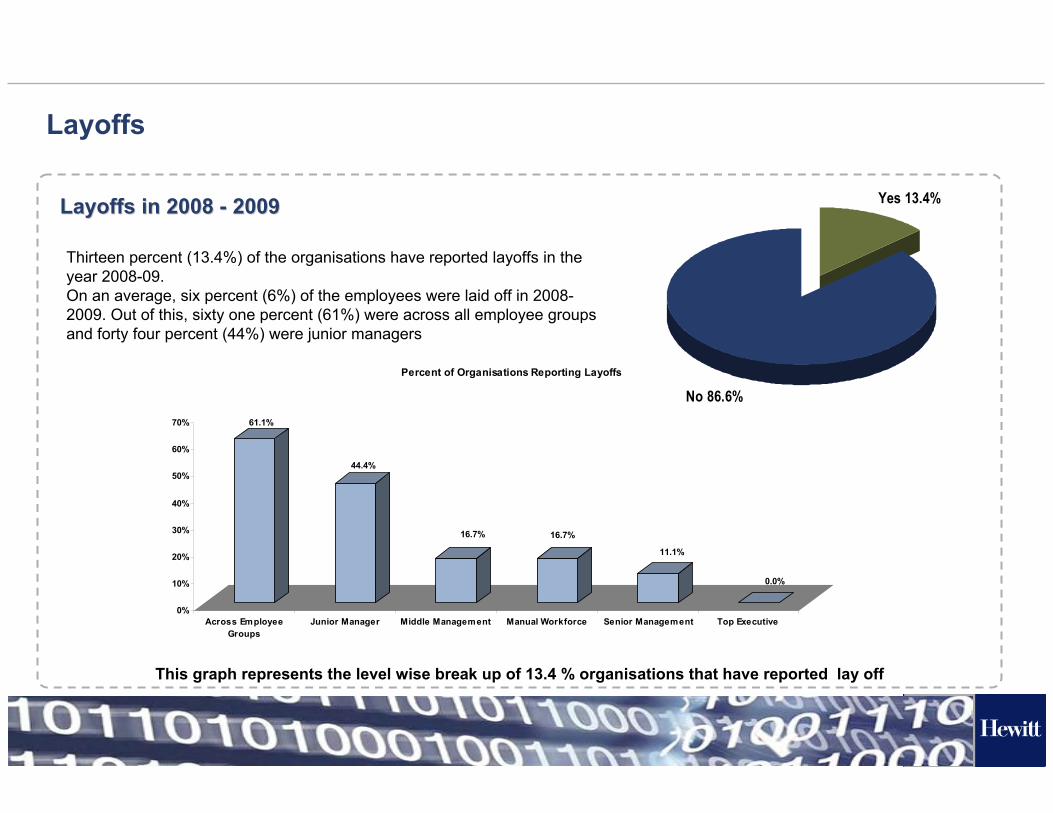

Layoffs in 2008 Layoffs in 2008 -- 20092009

Layoffs

Thirteen percent (13.4%) of the organisations have reported layoffs in the year 2008-09.On an average, six percent (6%) of the employees were laid off in 2008-2009. Out of this, sixty one percent (61%) were across all employee groups and forty four percent (44%) were junior managers

61.1%

44.4%

16.7% 16.7%

11.1%

0.0%

0%

10%

20%

30%

40%

50%

60%

70%

Across EmployeeGroups

Junior Manager Middle Management Manual Workforce Senior Management Top Executive

Percent of Organisations Reporting Layoffs

Yes 13.4%

No 86.6%

This graph represents the level wise break up of 13.4 % organisations that have reported lay off

28

[Title MM/DD/YYYY]

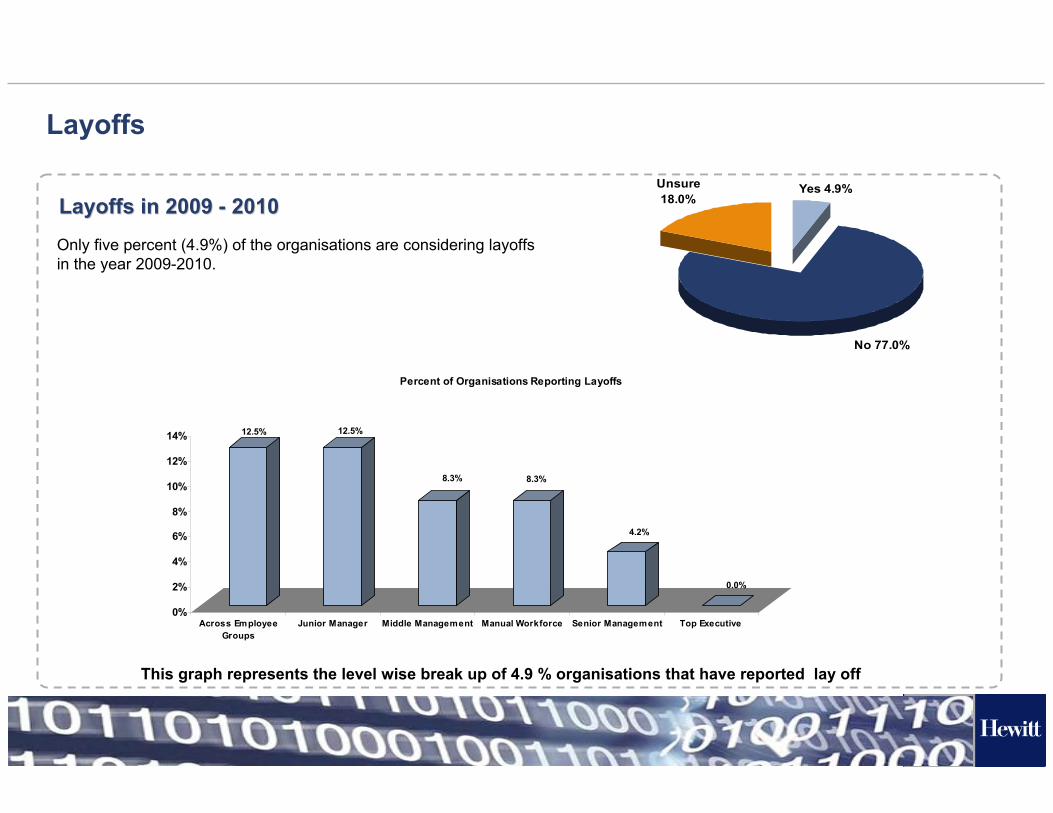

Layoffs in 2009 Layoffs in 2009 -- 20102010

Layoffs

Only five percent (4.9%) of the organisations are considering layoffs in the year 2009-2010.

Yes 4.9%

No 77.0%

Unsure 18.0%

12.5% 12.5%

8.3% 8.3%

4.2%

0.0%

0%

2%

4%

6%

8%

10%

12%

14%

Across EmployeeGroups

Junior Manager Middle Management Manual Workforce Senior Management Top Executive

Percent of Organisations Reporting Layoffs

This graph represents the level wise break up of 4.9 % organisations that have reported lay off

29

[Title MM/DD/YYYY]

Attrition

30

[Title MM/DD/YYYY]

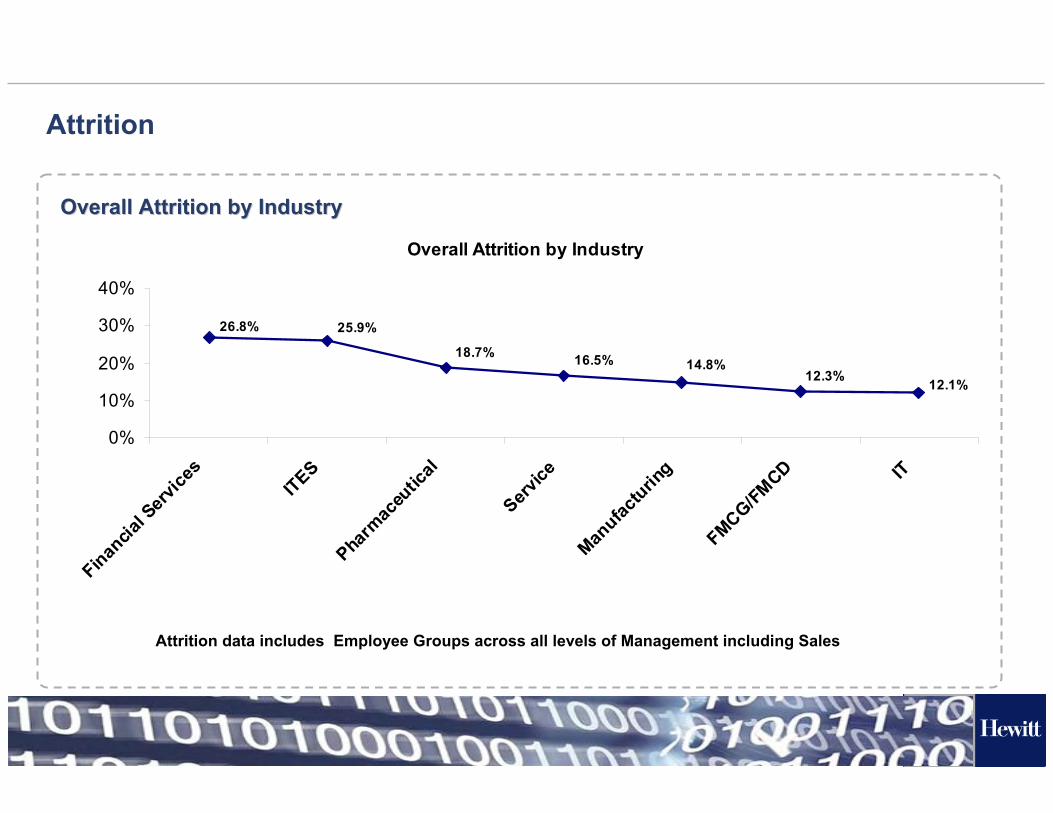

Overall Attrition by IndustryOverall Attrition by Industry

Attrition

Overall Attrition by Industry

26.8% 25.9%

18.7% 16.5% 14.8%12.3% 12.1%

0%

10%

20%

30%

40%

Financia

l Serv

ices

ITES

Pharm

aceu

tical

Service

Manufac

turing

FMCG/FMCD IT

Attrition data includes Employee Groups across all levels of Management including Sales

31

[Title MM/DD/YYYY]

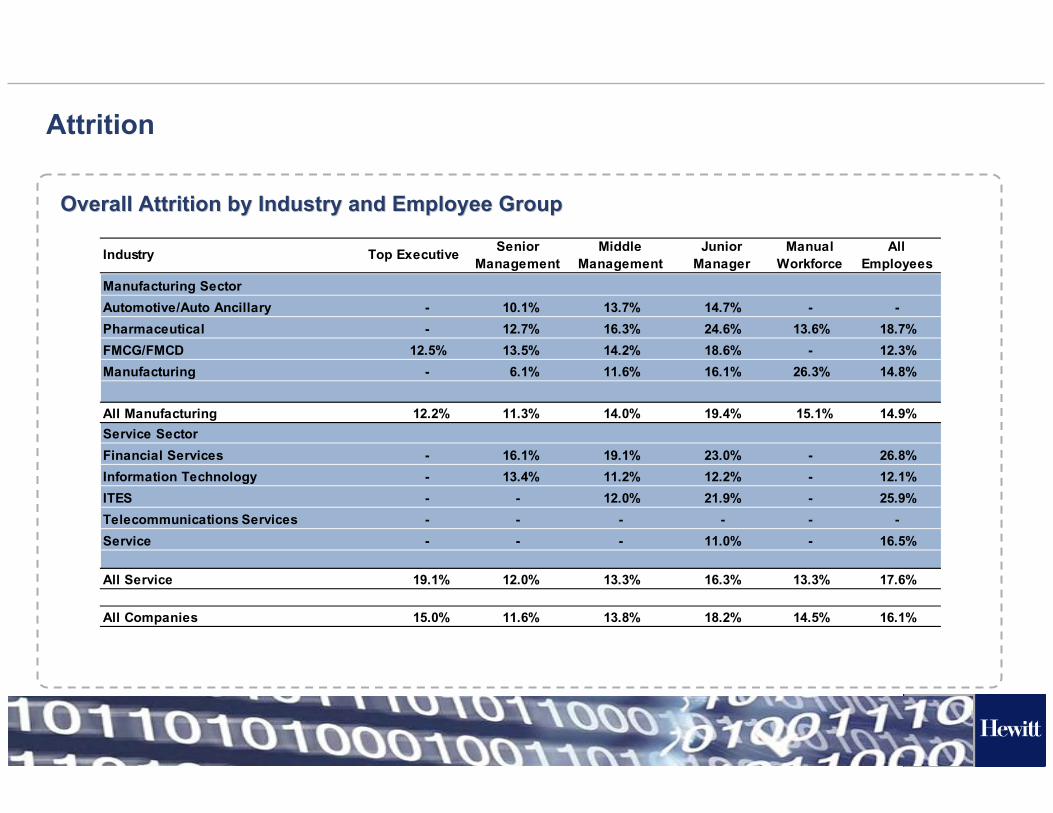

Overall Attrition by Industry and Employee GroupOverall Attrition by Industry and Employee Group

Attrition

- -- 13.6%

12.5% -- 26.3%

12.2% 15.1%Service Sector

- -- -- -- - -- -

19.1% 13.3%

15.0% 14.5%

13.5%12.7%10.1%

-13.4%16.1%

11.3%

12.0%

11.6%

--

12.0%--

13.3%

16.5%

17.6%

16.1%

13.7%16.3%14.2%11.6%

14.0%

19.1%11.2%

26.8%12.1%25.9%

-

-18.7%12.3%

Industry Top Executive Senior Management

Middle Management

Junior Manager

Manual Workforce

All Employees

Manufacturing SectorAutomotive/Auto AncillaryPharmaceuticalFMCG/FMCDManufacturing 14.8%6.1%

All Manufacturing 14.9%19.4%

Financial ServicesInformation TechnologyITESTelecommunications ServicesService

All Service

All Companies 13.8%

14.7%24.6%18.6%16.1%

16.3%

18.2%

23.0%

21.9%

11.0%

12.2%

32

[Title MM/DD/YYYY]

Participant List

33

[Title MM/DD/YYYY]

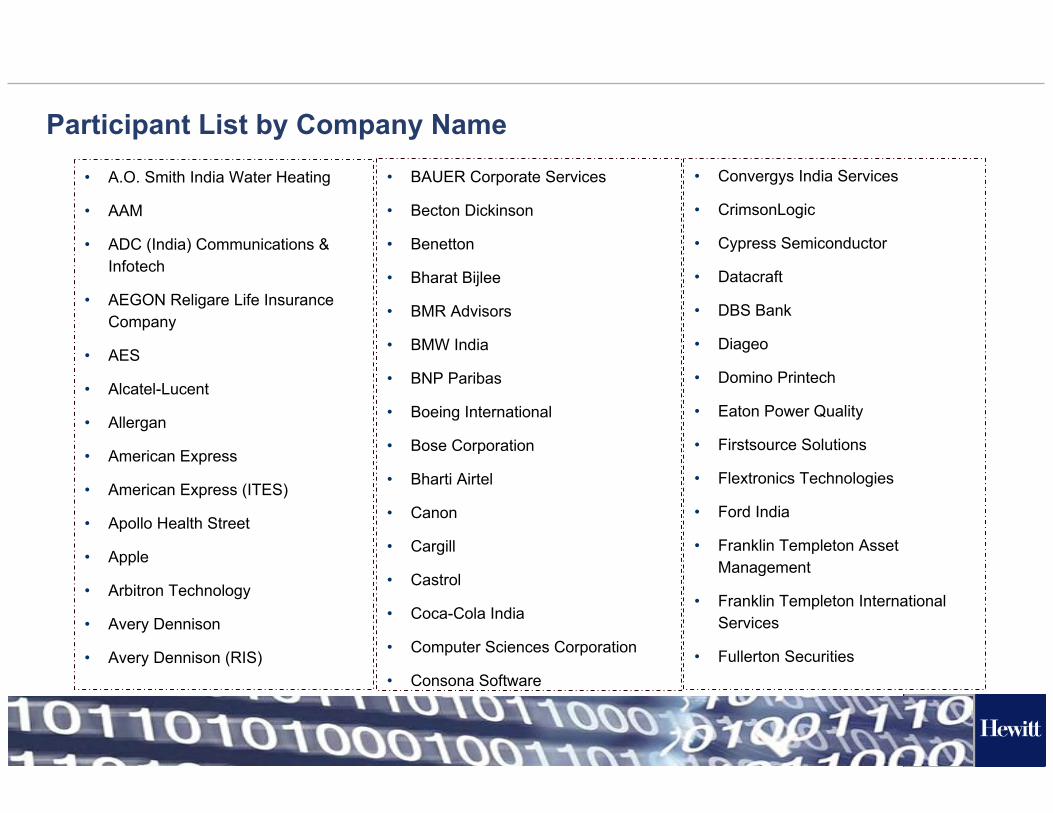

• A.O. Smith India Water Heating

• AAM

• ADC (India) Communications & Infotech

• AEGON Religare Life Insurance Company

• AES

• Alcatel-Lucent

• Allergan

• American Express

• American Express (ITES)

• Apollo Health Street

• Apple

• Arbitron Technology

• Avery Dennison

• Avery Dennison (RIS)

• BAUER Corporate Services

• Becton Dickinson

• Benetton

• Bharat Bijlee

• BMR Advisors

• BMW India

• BNP Paribas

• Boeing International

• Bose Corporation

• Bharti Airtel

• Canon

• Cargill

• Castrol

• Coca-Cola India

• Computer Sciences Corporation

• Consona Software

• Convergys India Services

• CrimsonLogic

• Cypress Semiconductor

• Datacraft

• DBS Bank

• Diageo

• Domino Printech

• Eaton Power Quality

• Firstsource Solutions

• Flextronics Technologies

• Ford India

• Franklin Templeton Asset Management

• Franklin Templeton International Services

• Fullerton Securities

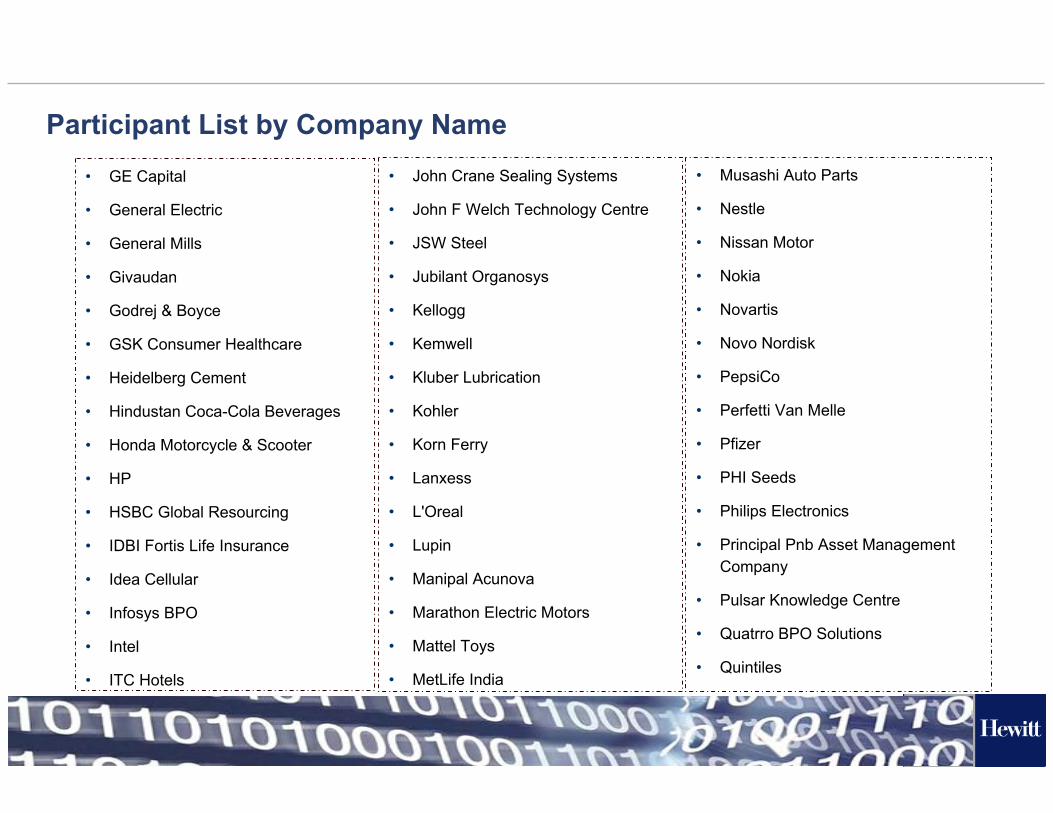

Participant List by Company Name

34

[Title MM/DD/YYYY]

• GE Capital

• General Electric

• General Mills

• Givaudan

• Godrej & Boyce

• GSK Consumer Healthcare

• Heidelberg Cement

• Hindustan Coca-Cola Beverages

• Honda Motorcycle & Scooter

• HP

• HSBC Global Resourcing

• IDBI Fortis Life Insurance

• Idea Cellular

• Infosys BPO

• Intel

• ITC Hotels

• John Crane Sealing Systems

• John F Welch Technology Centre

• JSW Steel

• Jubilant Organosys

• Kellogg

• Kemwell

• Kluber Lubrication

• Kohler

• Korn Ferry

• Lanxess

• L'Oreal

• Lupin

• Manipal Acunova

• Marathon Electric Motors

• Mattel Toys

• MetLife India

• Musashi Auto Parts

• Nestle

• Nissan Motor

• Nokia

• Novartis

• Novo Nordisk

• PepsiCo

• Perfetti Van Melle

• Pfizer

• PHI Seeds

• Philips Electronics

• Principal Pnb Asset Management Company

• Pulsar Knowledge Centre

• Quatrro BPO Solutions

• Quintiles

Participant List by Company Name

35

[Title MM/DD/YYYY]

• Rambus Chip Technologies

• Ranbaxy Laboratories

• Reliance Infrastructure

• RFCL (Chemicals)

• RFCL- Pharmaceutical

• RM Education Solutions

• Robert Bosch Engineering & Business Solutions

• Rockwell Automation

• Royal Sundaram Alliance Insurance Company

• Sandoz

• Schering Plough

• Schneider Electric

• Schreiber Foods

• SI Group

• Siegwerk

• Simon Carves

• Steria

• Steria - ITES

• Swarovski

• Symphony Marketing Solutions

• Target Corporation

• Tata AiG General Insurance

• Tata Communications

• TCS e-Serve

• Tech Mahindra

• Technip KT

• Tetra Pak

• The Nielsen Company

• Thomson Reuters

• Toyota Kirloskar

• UCB

• Unisys Global Services

• Unitech Wireless

• ValueSource Technologies

• Virage Logic

• Virbac Animal Health

• Virgin Mobile

• Visa Worldwide

• Woodward Governor

• Woolworths Wholesale

• Wrigley (Commercial)

• Wrigley (Supply Chain)

• Wyeth Limited

• Yahoo

• Zenta

• Zydus

Participant List by Company Name

36

[Title MM/DD/YYYY]

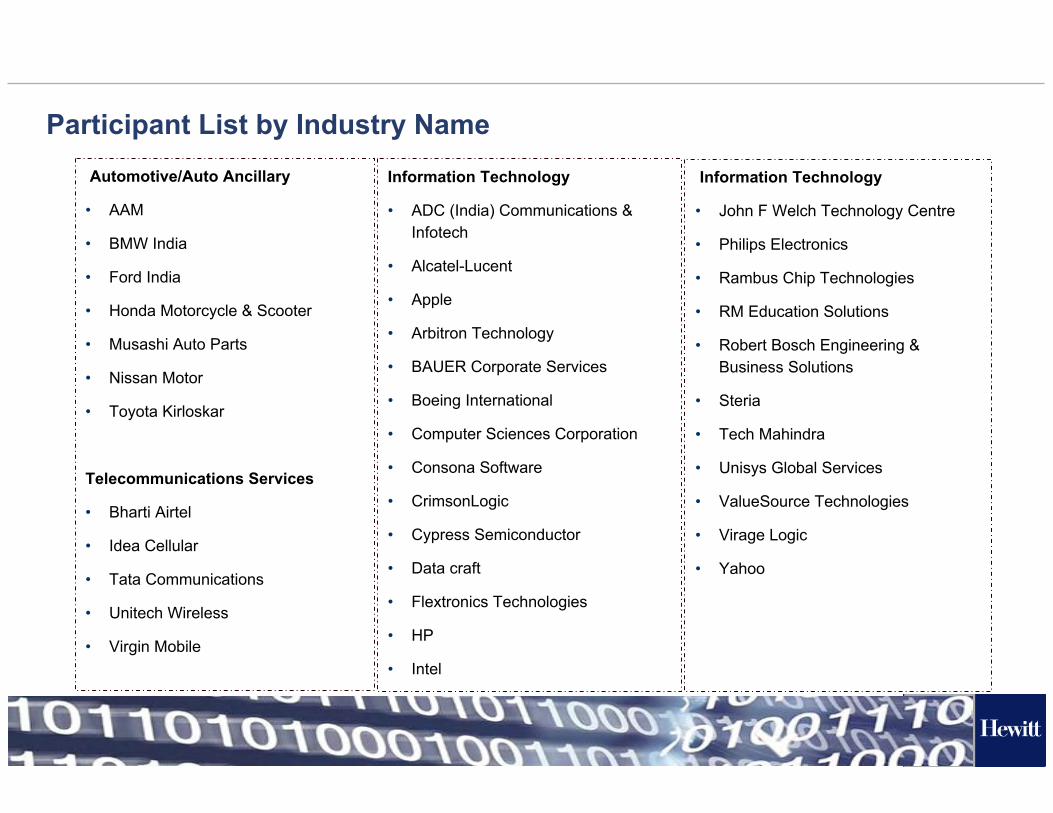

Automotive/Auto Ancillary

• AAM

• BMW India

• Ford India

• Honda Motorcycle & Scooter

• Musashi Auto Parts

• Nissan Motor

• Toyota Kirloskar

Telecommunications Services

• Bharti Airtel

• Idea Cellular

• Tata Communications

• Unitech Wireless

• Virgin Mobile

Information Technology

• ADC (India) Communications & Infotech

• Alcatel-Lucent

• Apple

• Arbitron Technology

• BAUER Corporate Services

• Boeing International

• Computer Sciences Corporation

• Consona Software

• CrimsonLogic

• Cypress Semiconductor

• Data craft

• Flextronics Technologies

• HP

• Intel

Information Technology

• John F Welch Technology Centre

• Philips Electronics

• Rambus Chip Technologies

• RM Education Solutions

• Robert Bosch Engineering & Business Solutions

• Steria

• Tech Mahindra

• Unisys Global Services

• ValueSource Technologies

• Virage Logic

• Yahoo

Participant List by Industry Name

37

[Title MM/DD/YYYY]

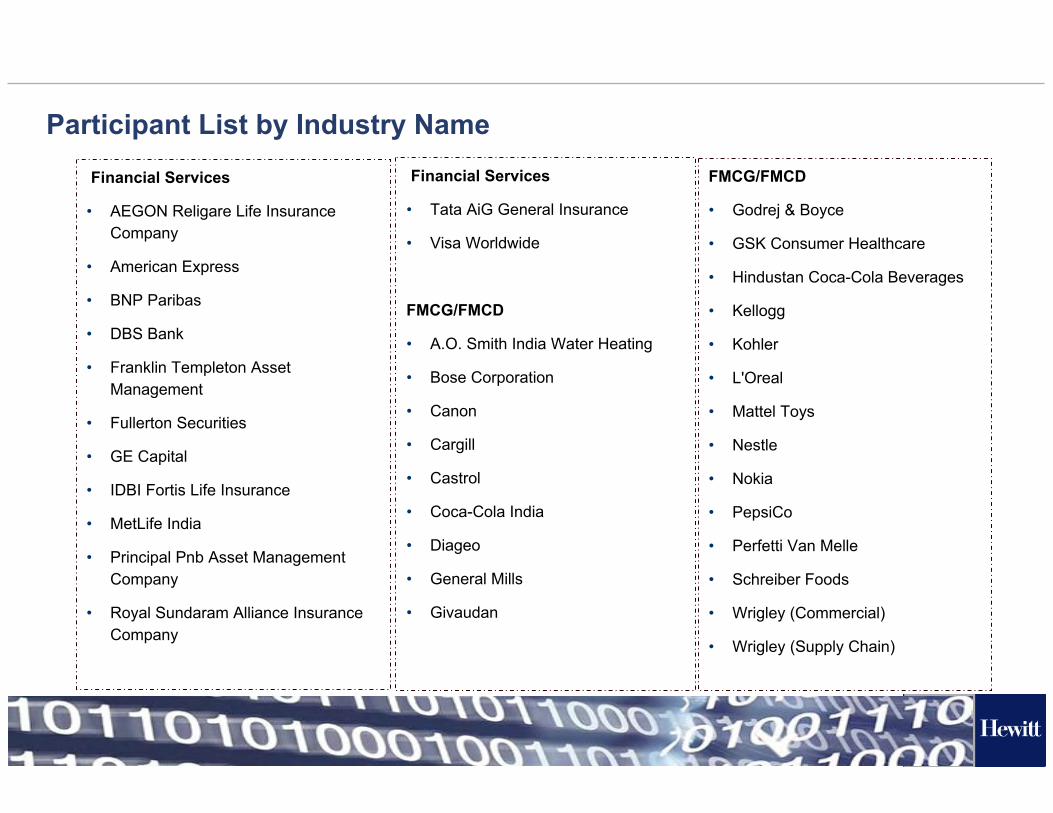

Financial Services

• AEGON Religare Life Insurance Company

• American Express

• BNP Paribas

• DBS Bank

• Franklin Templeton Asset Management

• Fullerton Securities

• GE Capital

• IDBI Fortis Life Insurance

• MetLife India

• Principal Pnb Asset Management Company

• Royal Sundaram Alliance Insurance Company

Financial Services

• Tata AiG General Insurance

• Visa Worldwide

FMCG/FMCD

• A.O. Smith India Water Heating

• Bose Corporation

• Canon

• Cargill

• Castrol

• Coca-Cola India

• Diageo

• General Mills

• Givaudan

FMCG/FMCD

• Godrej & Boyce

• GSK Consumer Healthcare

• Hindustan Coca-Cola Beverages

• Kellogg

• Kohler

• L'Oreal

• Mattel Toys

• Nestle

• Nokia

• PepsiCo

• Perfetti Van Melle

• Schreiber Foods

• Wrigley (Commercial)

• Wrigley (Supply Chain)

Participant List by Industry Name

38

[Title MM/DD/YYYY]

Manufacturing

• AES

• Avery Dennison

• Avery Dennison (RIS)

• Bharat Bijlee

• Domino Printech

• Eaton Power Quality

• General Electric

• Heidelberg Cement

• John Crane Sealing Systems

• JSW Steel

• Kluber Lubrication

• Lanxess

• Marathon Electric Motors

• RFCL (Chemicals)

• Rockwell Automation

Manufacturing

• PHI Seeds

• Schneider Electric

• SI Group

• Siegwerk

• Simon Carves

• Technip KT

• Tetra Pak

• Woodward Governor

Service

• Benetton

• BMR Advisors

• ITC Hotels

• Korn Ferry

• Reliance Infrastructure

• Swarovski

• The Nielsen Company

• Woolworths Wholesale

Participant List by Industry Name

39

[Title MM/DD/YYYY]

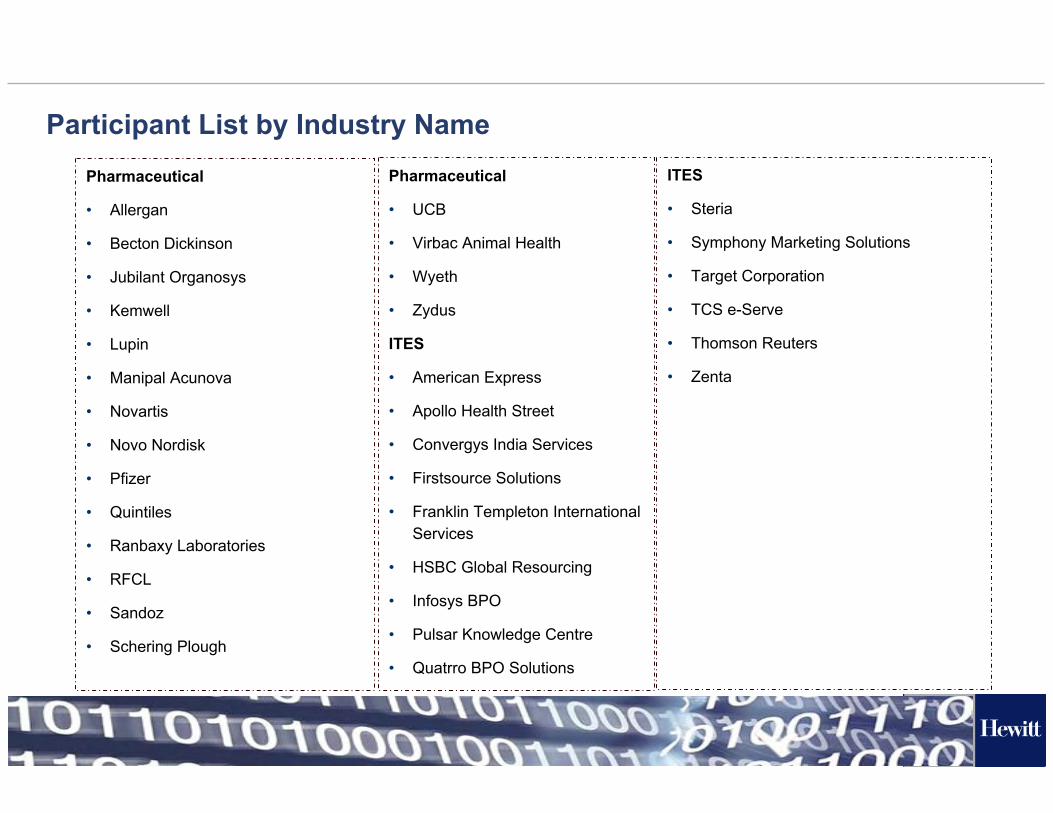

Pharmaceutical

• Allergan

• Becton Dickinson

• Jubilant Organosys

• Kemwell

• Lupin

• Manipal Acunova

• Novartis

• Novo Nordisk

• Pfizer

• Quintiles

• Ranbaxy Laboratories

• RFCL

• Sandoz

• Schering Plough

Pharmaceutical

• UCB

• Virbac Animal Health

• Wyeth

• Zydus

ITES

• American Express

• Apollo Health Street

• Convergys India Services

• Firstsource Solutions

• Franklin Templeton International Services

• HSBC Global Resourcing

• Infosys BPO

• Pulsar Knowledge Centre

• Quatrro BPO Solutions

ITES

• Steria

• Symphony Marketing Solutions

• Target Corporation

• TCS e-Serve

• Thomson Reuters

• Zenta

Participant List by Industry Name

40

[Title MM/DD/YYYY]

Thank you for your Participation.

For any further queries, please feel free to reach out to the Survey Coordinator:

Mehak Awasthy, [email protected],

or send a mail to: [email protected]

Thank You!!