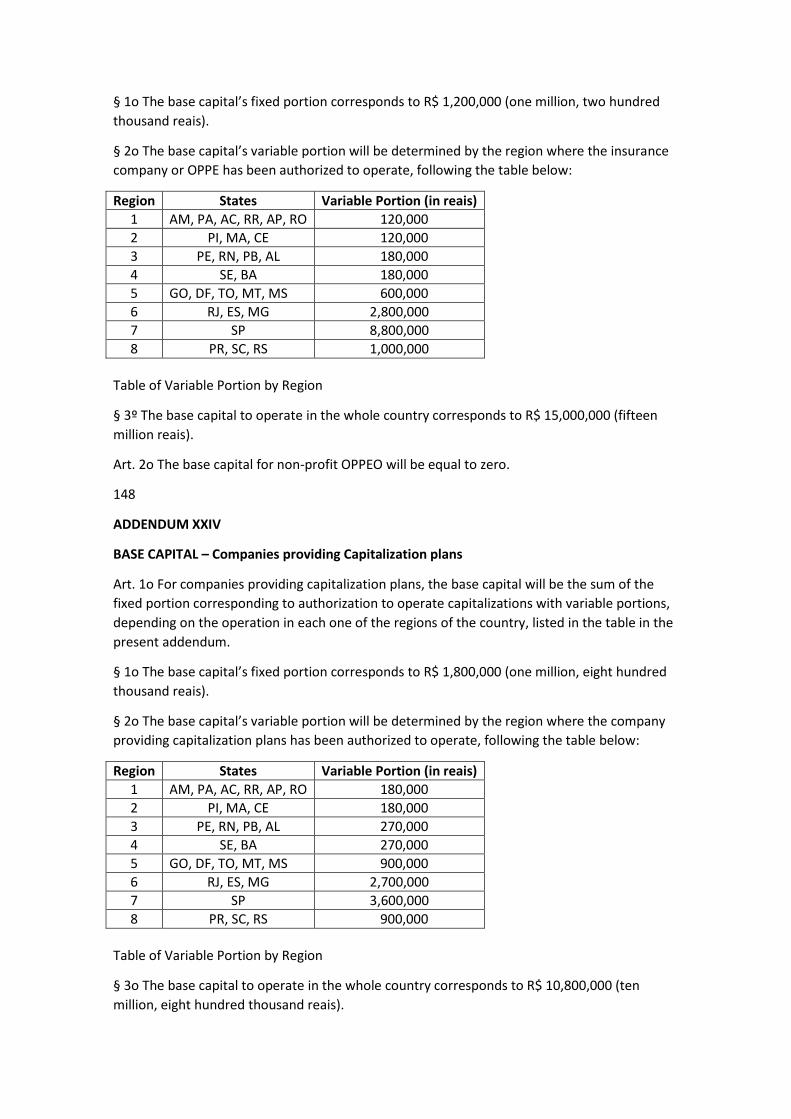

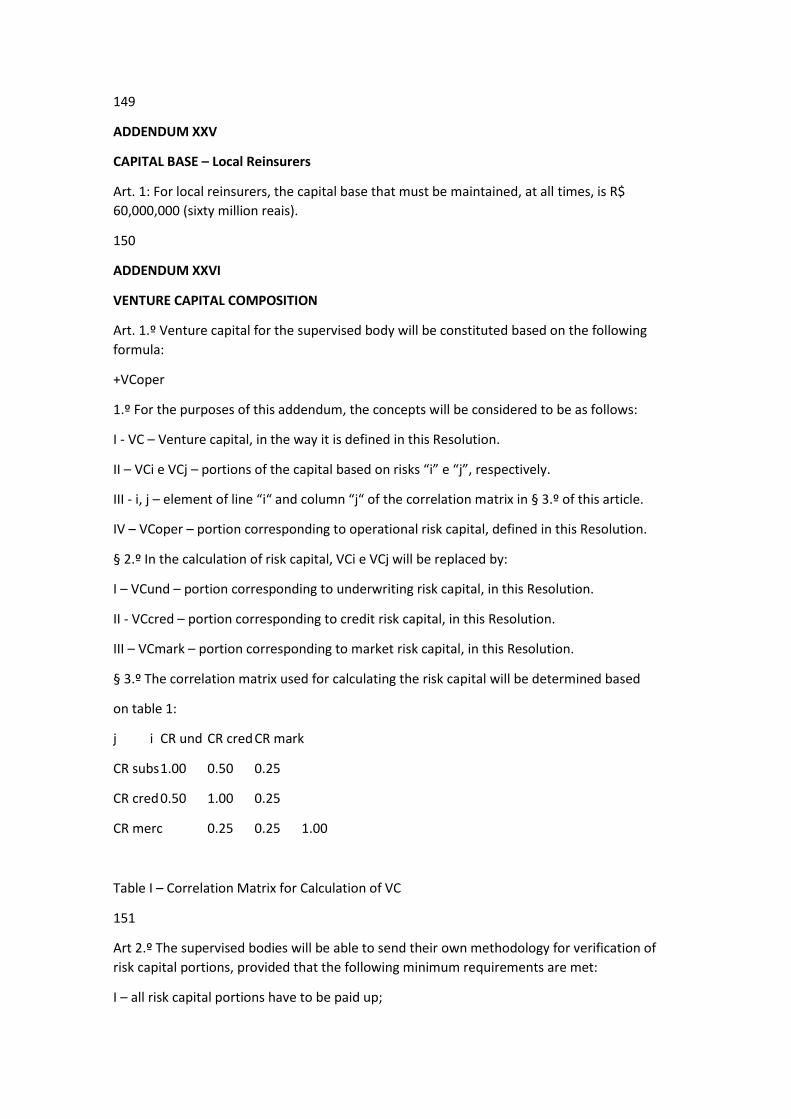

Embed Size (px)

Citation preview

1

MINISTRY OF FINANCE

NATIONAL PRIVATE INSURANCE COUNCIL (CNSP)

CNSP RESOLUTION No. 321 OF 2015.

Addresses technical provisions; assets reducing the technical provision coverage requirement;

underwriting, credit, operational and market risk capital; adjusted net equity; minimum capital

requirement; solvency regularization plan; retention limits; and criteria covering investments,

accounting standards, independent financial and actuarial auditing and the Audit Committee

with regard to insurance companies, open private pension entities, investment firms and

reinsurers.

THE SUPERINTENDENT OF THE PRIVATE INSURANCE AGENCY (SUSEP), in performance of the

duties assigned under Art. 34, sub-item XI of the addendum to Decree nº 60,459 of March 13,

1967, and taking into consideration the provisions of CNSP Proceeding No. 1/2015 and SUSEP

Proceeding No. 15414.000633/2015-18, announces that the NATIONAL PRIVATE INSURANCE

COUNCIL (CNSP), at an OGM held on May 18, 2015 and based on the provisions of Art. 32, sub-

items I, II, III and XI, Art. 84 of Decree No. 73 of November 21, 1966, Articles 3, sub-items III

and V, 37 and 74 of Supplementary Law No. 109 of May 29, 2001, Articles 3, § 1 and 4 of

Decree No. 261 of February 28, 1967, and Supplementary Law No. 126 of January 15, 2007,

DETERMINES:

Art. 1: To address technical provisions; assets reducing the technical provision coverage

requirement; underwriting, credit, operational and market risk capital; adjusted net equity;

minimum capital requirement; solvency regularization plan; retention limits; and criteria

covering investments, accounting standards, independent financial and actuarial auditing and

the Audit Committee with regard to insurance companies, open private pension entities,

investment firms and reinsurers.

Art. 2: For the purposes of this Resolution, consider:

I - supervised bodies: insurance companies, open private pension entities (OPPE), investment

firms and local reinsurers;

Continuation of CNSP Resolution nº 321, of 2015.

II - associated business: an entity, including one not set up in the form of a company, such as a

partnership, over which the investor has significant influence but which is not a subsidiary nor

a stake in a joint venture.

III - significant influence: the ability to participate in the financial and operational decisions of

the investee, without having formal individual or joint control over those policies.

IV - related companies:

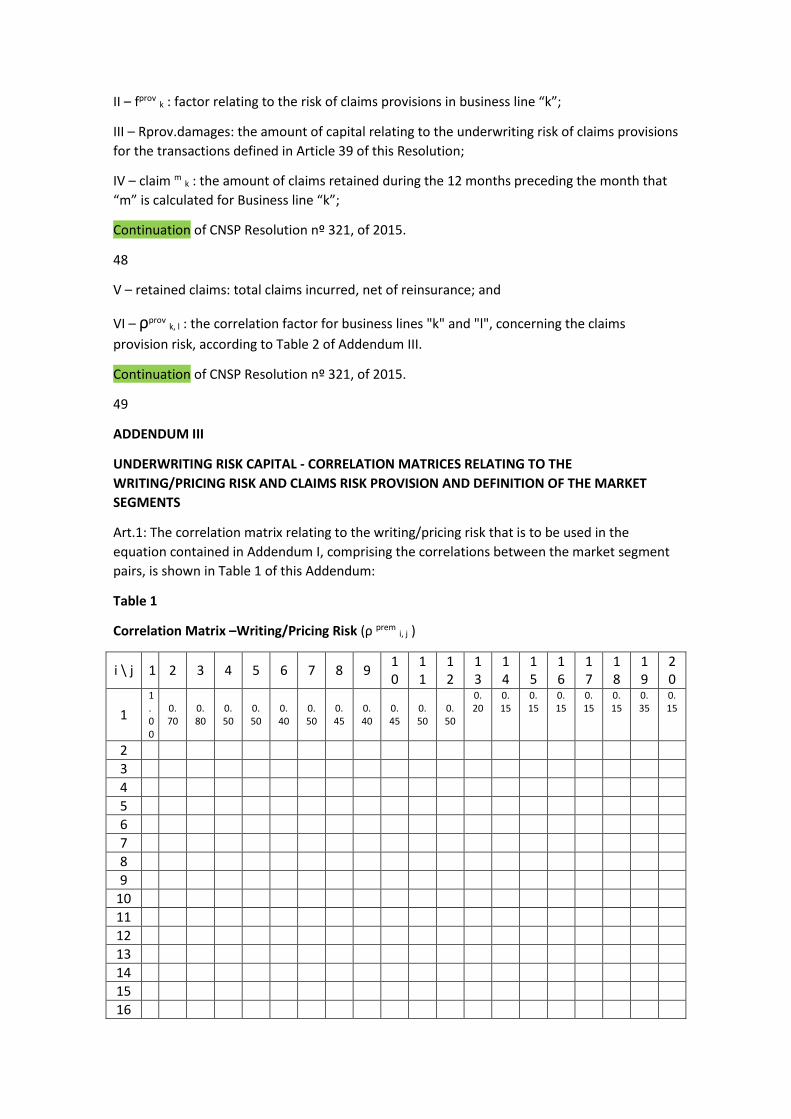

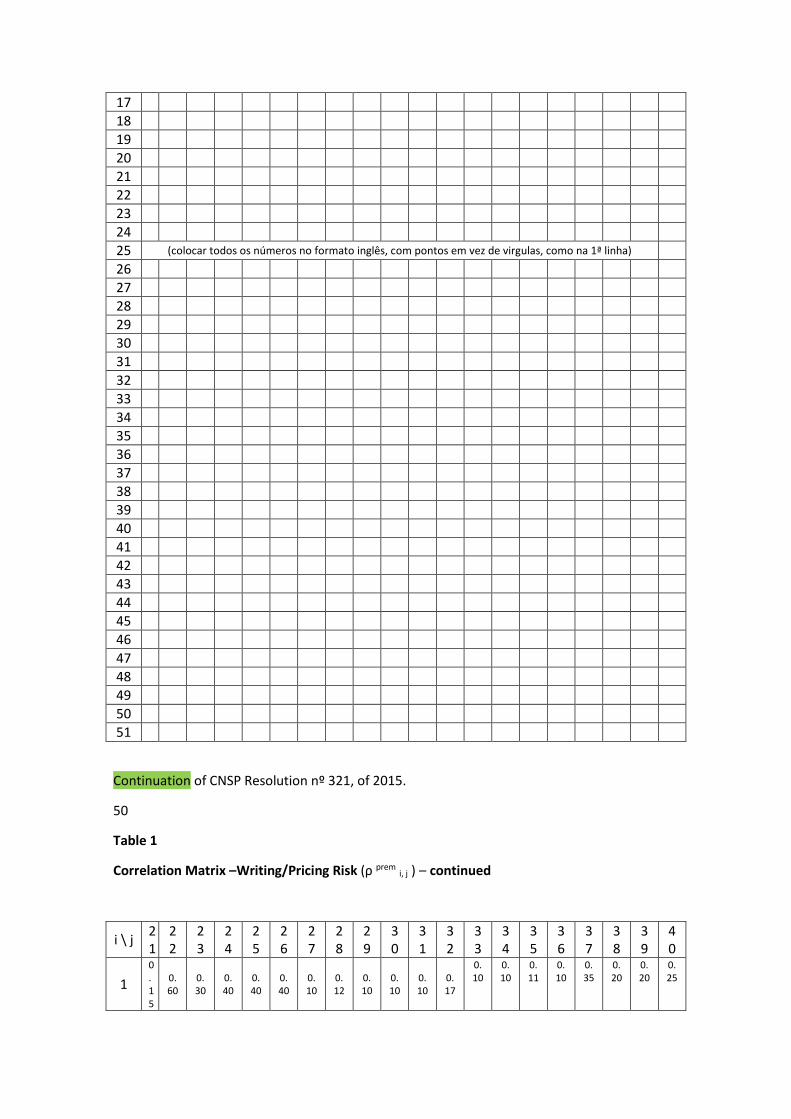

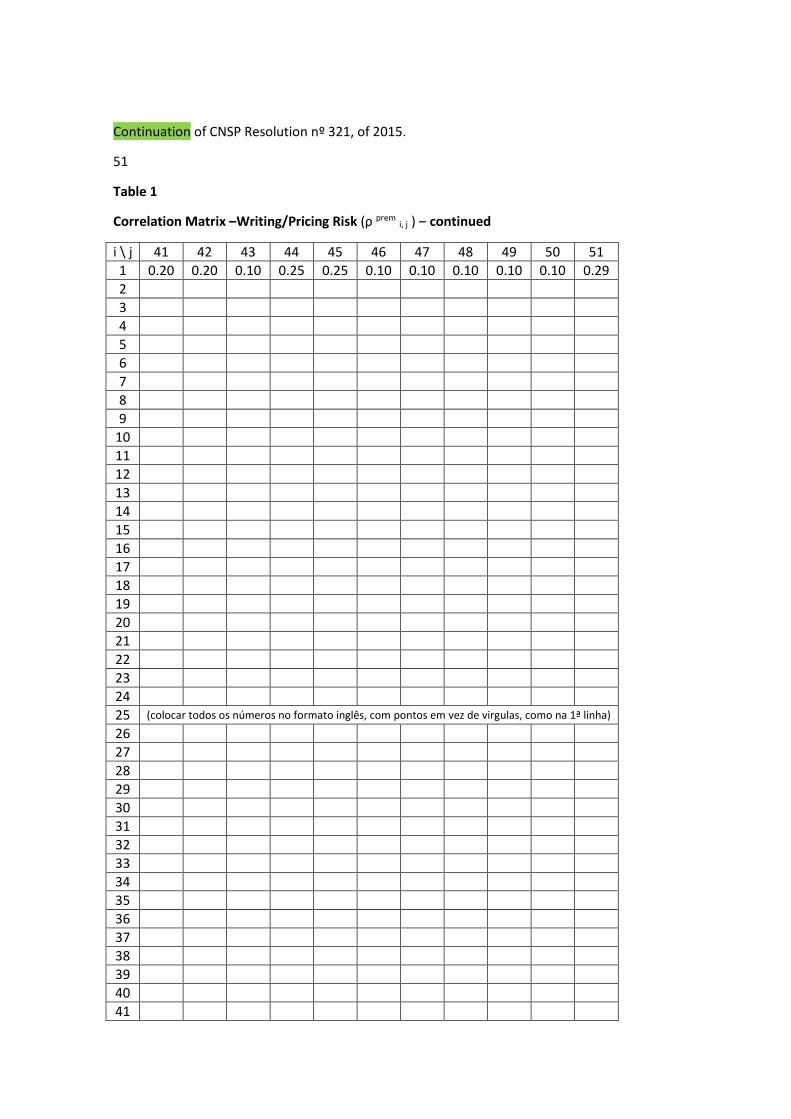

a) associated companies, subsidiaries or equivalent;

b) related legal entities having a direct or indirect stake of 10% (ten percent) or more, through

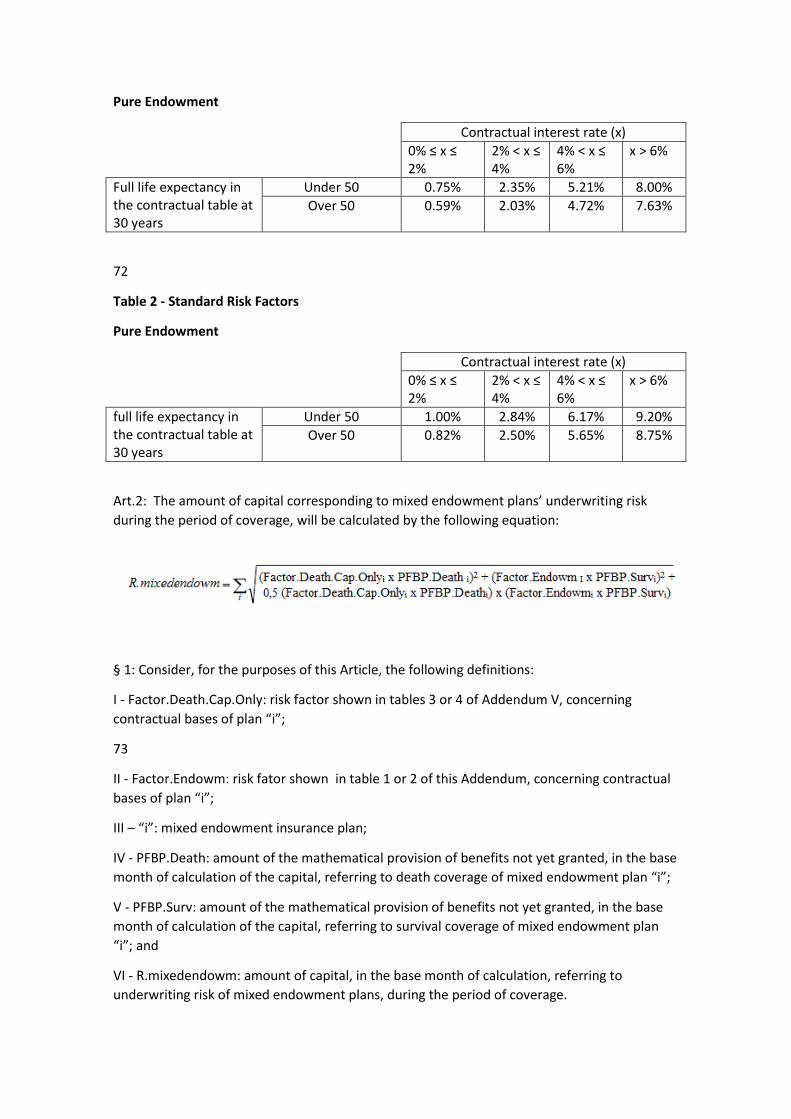

the management and their relatives, up to the 2nd degree, together or individually, in the

capital of the other;

c) related legal entities having a direct or indirect stake of 10% (ten percent) or more, through

the management and their relatives, up to the 2nd degree, together or individually, in the

capital of the other; related legal entities with a direct or indirect stake of 10% (ten percent) or

more, through the controlling members (in the case of non-profit open private pension

entities) or shareholders of one of them, collectively or individually, in the capital or net

equity, as the case may be, in the other;

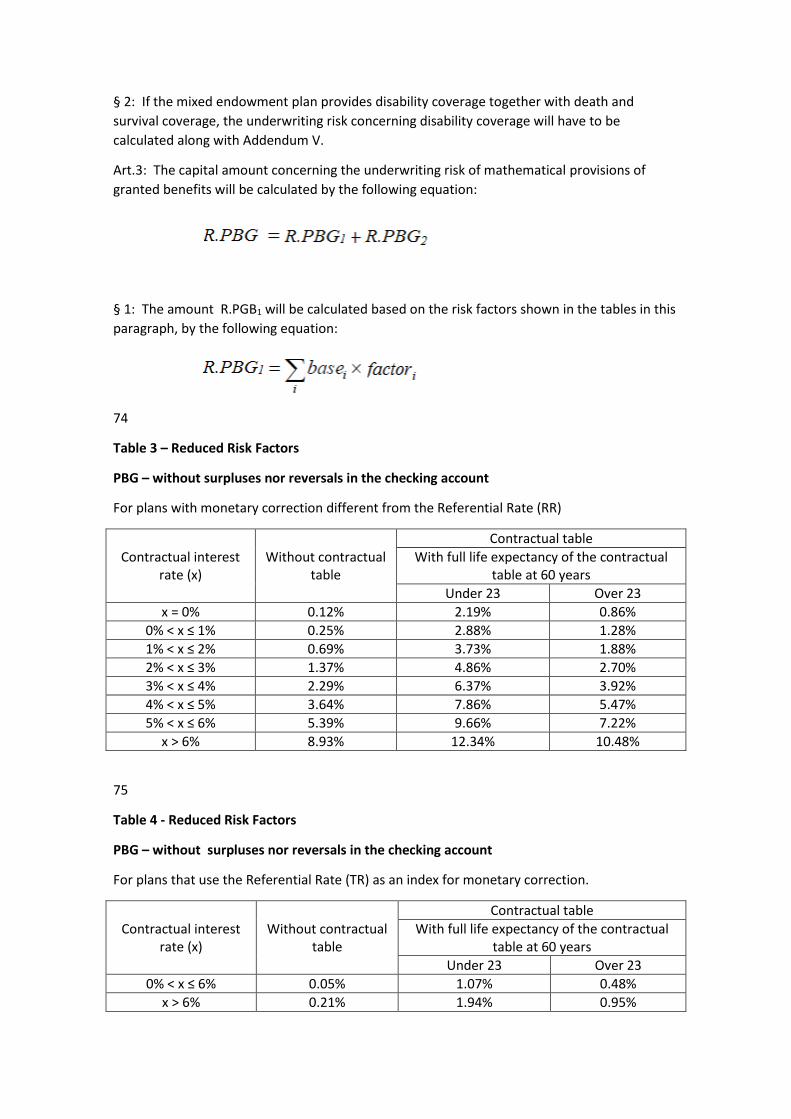

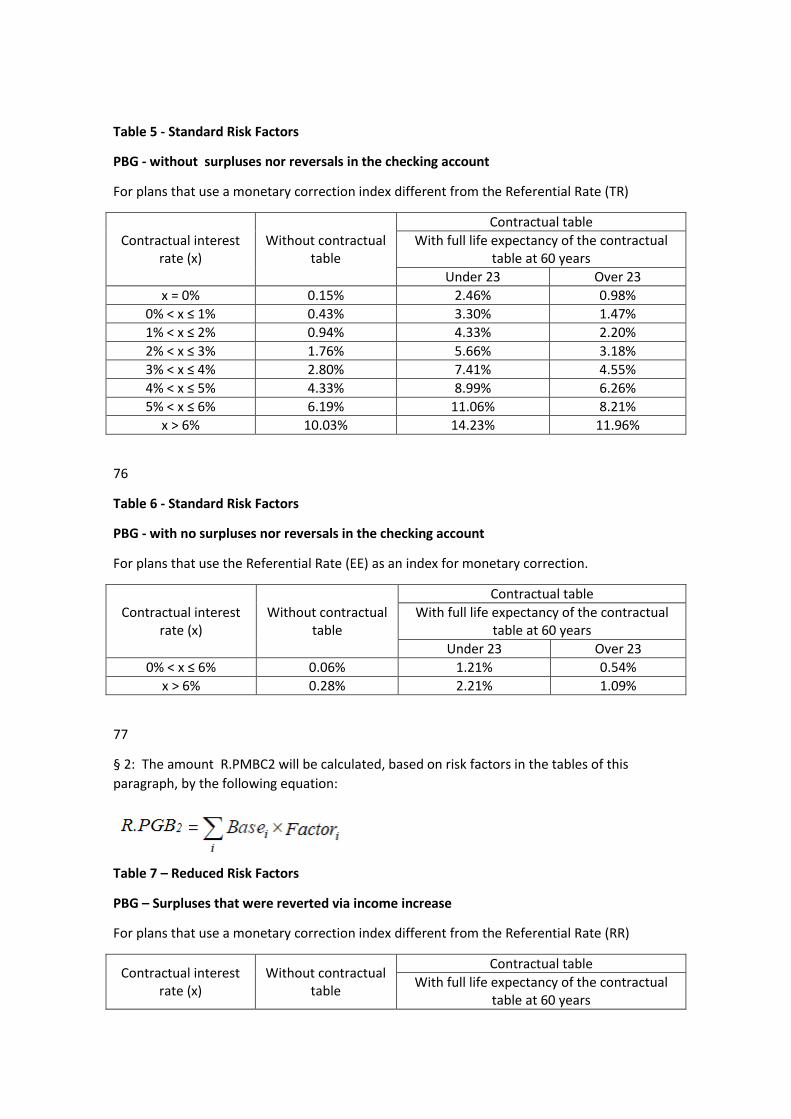

d) legal entities whose management is, wholly or in part, the same as that of the supervised

body, with the exception of posts in collegial bodies, provided for in the bylaws or internal

regulations, as long as the occupants do not exercise managerial powers;

e) related legal entities operating in the market under the same brand or trade name; and

V – adjusted net equity (ANE): the book value of the net equity or net worth, as appropriate,

adjusted for additions and deductions to determine, more qualitatively and precisely, the

available resources that enable the supervised body to perform its activities in the face of

fluctuations and adverse situations, which must be net of intangibles, assets whose valuation is

highly subjective or are already guaranteeing similar financial activities, as well as other assets

whose nature is considered by the regulatory body to be unsuitable to safeguard its solvency.

VI – the structure in the format contained in this sub-item:

TITLE I: QUANTITATIVE ELEMENTS ............................................................................................. 4

CHAPTER I: Technical Provisions ................................................................................................. 4

Section I: Insurance companies and OPPEs ................................................................................ 4

Section II: Investment firms ................................................................. 5

Section III: Local Resinsurers ……………......................................................................................... 6

Section IV: General Provisions of this Chapter ………………………………………………………………………. 7

CHAPTER II: Assets that reduce the need to cover Technical Provisions ……………..….…............. 7

CHAPTER III: Risk Capital to cover Underwriting, Credit, Operational and Market Risks …….….. 7

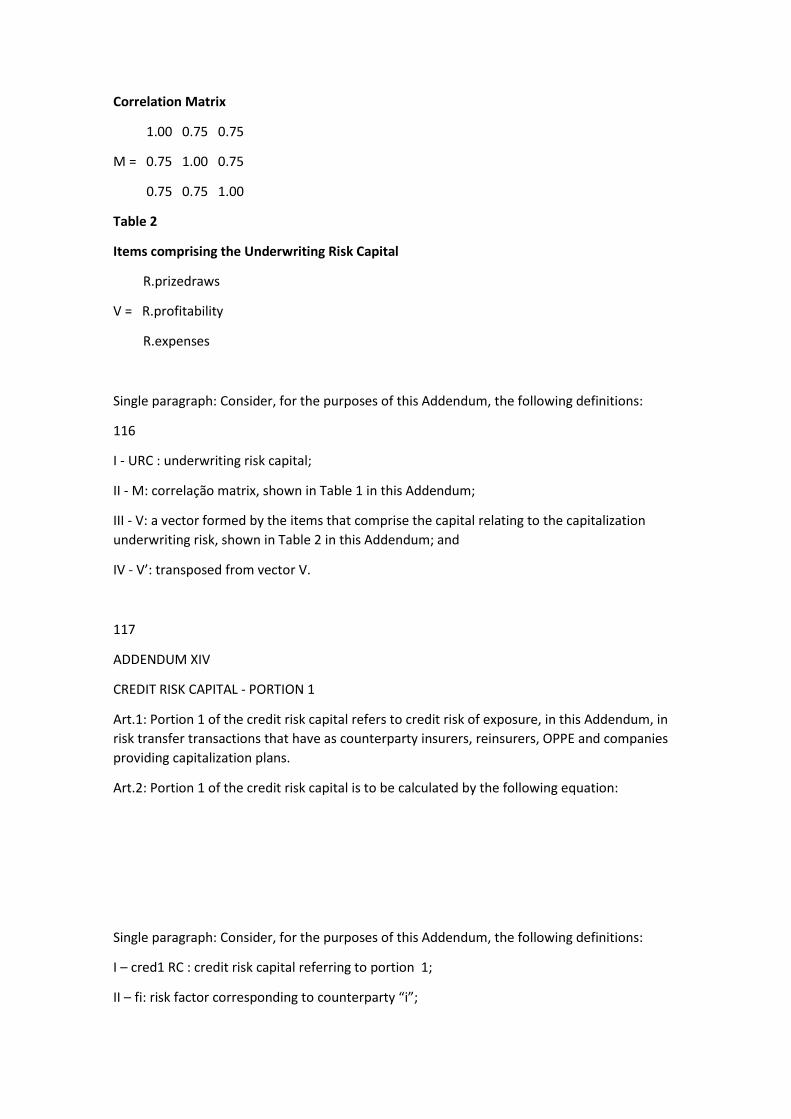

Section I: Risk Capital to cover Underwriting Risk …………………………………………………………………. 8

Section II: Risk Capital to cover Credit Risk ………………………….………………………………………………. 11

Section III: Risk Capital to cover Operational Risk ………………………..………………………………………. 11

Section IV: Risk Capital to cover Market Risk ………………………….……………………………………………. 11

CHAPTER IV: Adjusted Net Equity …………………………………………………………..……………………………. 15

Continuation of CNSP Resolution nº 321, of 2015.

CHAPTER V: Minimum Capital Requirement and Solvency Regularization Plan ….................... 16

Section I: Capital Requirements …............................................................................................. 17

Section II: Net Asset linkage …………………………………………………………………………………………………. 17

Section III: Solvency Regularization Plan …................................................................................ 17

TITLE II: QUALITATIVE ELEMENTS ............................................................................................. 19

CHAPTER I: Retention Limits for Insurance companies, OPPEs and Local Reinsurers …………… 19

CHAPTER II: Investment Criteria ............................................................................................... 21

Section I: Insurance companies, OPPEs, Investment firms and Local Reinsurers .………………… 22

Section II: Investment of Resources Required in Brazil to Guarantee an Admitted Reinsurer’s

Obligations ................................................................................................................................ 27

TITLE III: RULES ON TRANSPARENCY AND DISCLOSURE ............................................................ 25

CHAPTER I: Accounting Standards ............................................................................................ 25

CHAPTER II: Independent actuarial auditors ............................................................................ 25

Section I: Minimum Requirements …........................................................................................ 28

Section II: Independence Requirements ……………….…………………………………………………………….. 26

Section III: Responsibility of the Supervised bodies …………………..…………………………………………. 27

Section IV: Periodic changing of the Independent Actuary …………….…………………………………….. 27

Section V: Documents of the Independent Actuarial Audit …………………………………………………… 27

Section VI: Report of the technically responsible Actuary ……………………….……………………………. 32

Section VII: General Provisions of this Chapter …………………………………………………………………….. 33

CHAPTER III: Independent Accounting Auditors ........................................................................ 34

Section I: Independence Requirements of the Accounting Auditors ........................................ 34

Section II: Obligations ………………………………………………………………………………………………………….. 35

Section III: Responsibility of the Supervised bodies …………………..…………………………………………. 35

Section IV: Periodic changing of the Independent Accounting Auditors ………………………………. 36

Section V: Audit Committee …………………………………………………………..……………………………………. 36

Section VI: Applicability of the General Standards for Independent Accounting Auditors ...... 36

Section VII: Documents of the Independent Accounting Audit …….……………………………………… 40

Section VIII: Certification ……………………………………………………………………………………………………… 41

Section IX: General Provisions of this Chapter ……………………………………………………………………... 41

TITLE IV: FINAL CONSIDERATIONS ............................................................................................ 42

Continuation of CNSP Resolution nº 321, of 2015.

TITLE I

QUANTITATIVE ELEMENTS

CHAPTER I

Technical Provisions

Art. 3: The establishing of Other Technical Provisions (OTP) may be allowed in relation to a

product, plan or portfolio, in addition to those specified in this Chapter, subject to prior

authorization by SUSEP and as long as they are provided for in an actuarial technical note.

Section I

Insurance companies and OPPE

Art. 4: To guarantee their operations, insurers and OPPE must, whenever necessary, make the

following monthly technical provisions:

I – Provision for Unearned Premiums (PUEP);

II – Provision for Claims reported but not yet settled (RBNS);

III – Provision for Claims incurred but not yet reported (IBNR);

IV – Mathematical Provision for Future Benefit Payments (PFBP);

V – Mathematical Provision for Benefits Granted (PBG);

VI – Provision for Supplementary Coverage (PSC);

VII – Provision for Related Expenses (PRE);

VIII – Provision for Technical Surpluses (PTS);

IX – Provision for Financial Surpluses (PFS); and

X – Provision for Redemptions and other unsettled amounts (PRO).

Subsection I

Provisions for Premiums

Art. 5: A PUEP must be set up to cover amounts payable in relation to claims and expenses still

to arise.

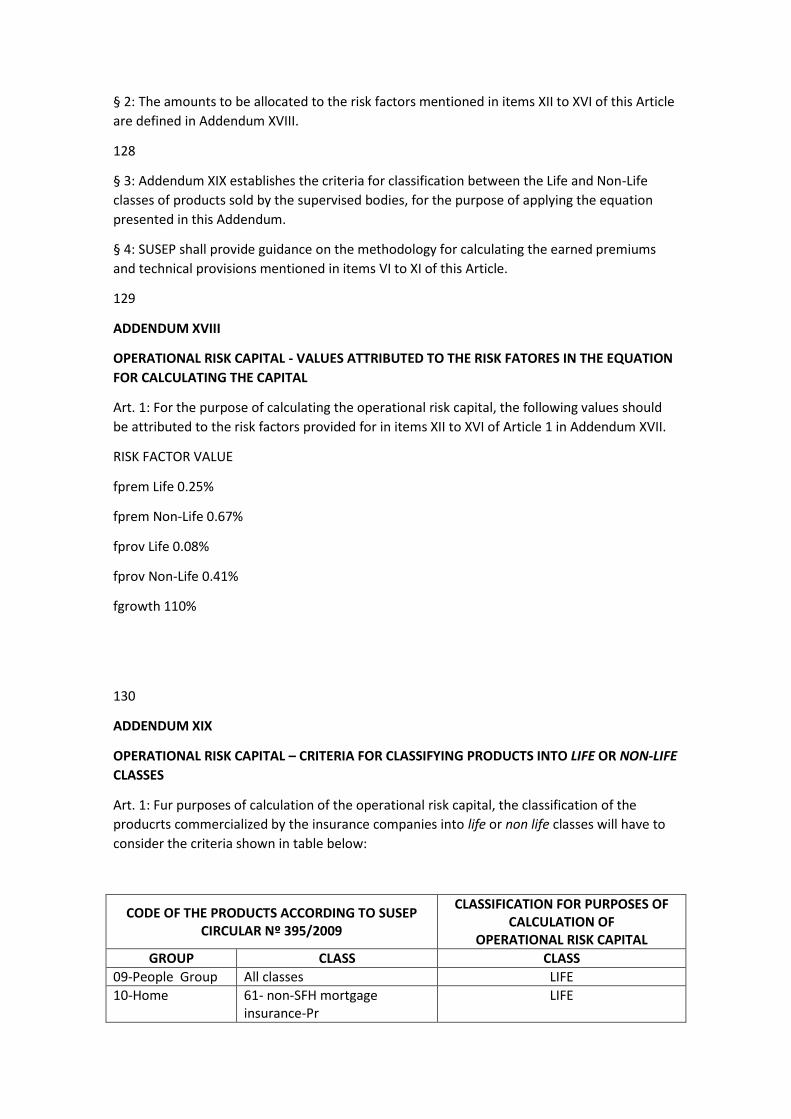

Subsection II

Provisions for Claims

Art. 6: An RBNS must be set up to cover amounts that are expected to be paid in settlement of

payments relating to reported claims.

Art. 7: A provision for IBNR must be set up to cover amounts that are expected to be paid in

relation to claims incurred but not reported.

Subsection III

Mathematical Provisions

Art. 8: A PFBP must be set up before the event that generates the benefit has occurred, to

cover the commitments to participants or policyholders.

Art. 9: A PBG must be set up, once the event that generates the benefit has occurred, to cover

the commitments to participants or policyholders.

Continuation of CNSP Resolution nº 321, of 2015.

5

Subsection IV

Other Provisions

Art. 10: A PSC must be set up whenever a shortage in technical provisions is ascertained.

Art. 11: A PRE must be set up to cover the claims expenses.

Art. 12: A PTS must be set up to guarantee the sums for the distribution of technical surpluses

arising from contractual operations, if such is provided for in the contract.

Art. 13: A PFS must be set up to guarantee the sums for distribution of financial surpluses, in

accordance with the prevailing regulations, if such is provided for in the contract.

Art. 14: The PRO covers other amounts outstanding that are not included in the other technical

provisions.

Section II

Investment firms

Art. 15: To guarantee their operations, the investment firms must, whenever necessary, set up,

on a monthly basis, the following technical provisions:

I – Mathematical Provision for Capitalization (MPC)

II – Provision for Distribution of a Bonus (PDB)

III – Provision for Redemption (PR)

IV – Provision for Prize Draws (PPD)

V – Supplementary Provision for Prize Draws (SPPD)

VI – Provision for Prize Draws Payable (PDP) and

VII – Provision for Administrative Expenses (PAE)

Subsection I

Provisions for Redemptions

Art. 16: An MPC must be set up before the event giving rise to redemption has occurred and

must cover the amounts received for capitalization.

Art. 17: A PDB must be set up before the event giving rise to a bonus distribution has occurred

and must cover the amounts determined for the bonus payment.

Art. 18: A PR must be set up that is in effect from the date of the event that gives rise to

redemption of the security and/or the event that gives rise to distribution of the bonus until

the date of settlement, or in accordance with other cases provided for in the legislation.

Continuation of CNSP Resolution nº 321, of 2015.

6

Subsection II

Provisions for Prize Draws

Art. 19: The PPD covers the amounts received for the prize draw and must be set up before the

prize draw has been carried out.

Art. 20: An SPPD must be set up to supplement the coverage of the draws to be carried out.

Art. 21: A PDP must be set up that is in effect from the date the prize draw is held until the

date of settlement, or in accordance with other cases provided for in the legislation.

Subsection III

Other Provisions

Art. 22: A PAE must be set up to cover the anticipated expenses for administration of the

capitalization plans.

Section III

Local Reinsurers

Art. 23: To guarantee their operations, the local reinsurers must, whenever necessary, set up

the following technical provisions:

I – Provision for Unearned Premiums (PUEP)

II – Provision for Claims reported but not yet settled (RBNS)

III – Provision for Claims incurred but not yet reported (IBNR)

IV – Mathematical Provision for Future Benefit Payments (PFBP)

V – Mathematical Provision for Benefits Granted (PBG)

VI – Provision for Supplementary Coverage (PSC)

VII – Provision for Related Expenses (PRE)

VIII – Provision for Technical Surpluses (PTS) and

IX – Provision for Financial Surpluses (PFS)

Subsection I

Provisions for Premiums

Art. 24: A PUEP must be set up to cover the amounts payable in relation to claims and

expenses to be incurred.

Subsection II

Provisions for Claims

Art. 25: An RBNS must be set up to cover the amounts to be settled in relation to reported

claims.

Art. 26: An IBNR claims provision must be set up to cover the amounts to be settled in relation

to claims that have been incurred but not yet reported.

Continuation of CNSP Resolution nº 321, of 2015.

7

Subsection III

Mathematical Provisions

Art. 27: The PFBP should cover the amount of the commitments assumed by local reinsurers in

their pertinent contracts, in order to guarantee the reinsured benefits that have not yet

started to be drawn.

Art. 28: The PBG should cover the amount of the commitments assumed by local reinsurers in

their pertinent contracts, in order to guarantee the reinsured benefits that have already

started to be drawn.

Subsection IV

Other Provisions

Art. 29: A PSC must be set up whenever a shortfall in the technical provisions is ascertained.

Art. 30: A PRE must be set up to cover the expenses in relation to claims.

Art. 31: A PTS must be set up to guarantee the amounts for the distribution of technical

surpluses arising from contractual operations, if such is provided for in the contract.

Art. 32: A PFS must be set up to guarantee the amounts for the distribution of financial

surpluses, in accordance with the prevailing regulations, if such is provided for in the contract.

Section IV

General Provisions of this Chapter

Art. 33: SUSEP shall address any fields or products that, due to their characteristics, should be

excluded from the setting up of any technical provisions dealt with in this Resolution.

CHAPTER II

Assets that reduce the need to cover Technical Provisions

Art. 34: The following may be offered as collateral assets to offset the need for technical

provision coverage, in accordance with the specific regulations published by SUSEP:

I – creditor rights;

II – reducing reinsurance and retrocession assets;

III – reducing judicial deposits; and

IV – reducing deferred acquisition costs.

Single paragraph: The assets provided to reduce the need for coverage of technical provisions

cannot be offered as collateral for other transactions.

Continuation of CNSP Resolution nº 321, of 2015.

CHAPTER III

Risk Capital to cover Underwriting, Credit, Operational and Market Risks

Art. 35: For the purposes of this Chapter, it shall be considered that:

I – underwriting risk: the possibility of incurring losses that confound the expectations of the

supervised body, directly or indirectly related to the technical bases utilized for calculating

premiums, contributions, shares and technical provisions;

II – underwriting risk capital (URC): variable amount of capital that a supervised body must

maintain, at all times, to guarantee the underwriting risk;

III – credit risk: the possibility of incurring losses associated with the policyholder or

counterparty’s, non-compliance with their respective financial obligations under the agreed

terms, and/or devaluation of the receivables due to a reduction in the risk rating of the

policyholder or counterparty;

IV – credit risk capital (CRC): variable amount of capital that a supervised body must maintain,

at all times, to guarantee the credit risk to which it is exposed;

V – operational risk: the possibility of incurring losses as a result of the failure, deficiency or

inadequacy of internal processes, employees or systems, or from fraud or external events,

including legal risk but excluding the risks relating to strategic decisions or the reputation of

the institution;

VI – external events: events occurring outside the supervised body, such as stoppages caused

by riots, strikes, revolts, acts of terrorism, uprisings, natural disasters, fires, blackouts or any

other event not directly related to the activities of the supervised body but that could cause

the failure or collapse of services essential to the performing of its operational activities;

VII – legal risk: the possibility of losses arising from fines, penalties or reparations as a result of

the action of supervisory and control bodies, as well as losses arising from unfavorable

decisions in judicial or administrative proceedings;

VIII – operational risk capital (RCoper): variable amount of capital that a supervised body must

maintain, at all times, to guarantee the operational risk to which it is exposed;

IX – market risk: the possibility of incurring losses due to fluctuations in the financial markets

that bring about changes in the economic appraisal of the assets and liabilities of the

supervised bodies;

X – market risk capital (RCmarket): variable amount of capital that a supervised body must

maintain, at all times, to guarantee the market risk to which it is exposed;

XI – direct reinsurance: reinsurance operations net of loading fee, cancellations, refunds and

discounts;

X – goodwill: an asset that represents future economic benefits to arise from other assets

acquired in a business combination, which are not individually identified and separately

recognized in the books.

Continuation of CNSP Resolution nº 321, of 2015.

Section I

Risk Capital to cover Underwriting Risk

Art. 36: This Section does not apply to transactions within the DPVAT (Personal Injury caused

by Land Vehicles) and DPEM (Personal Injury caused by Watercraft) insurance classes.

Art. 37: The underwriting risk capital of insurers and OPPE is to be calculated using the

standard risk factors listed in Addendums I to VII, following the correlation matrix and

equation shown in Addendum VIII.

§ 1: SUSEP shall regulate specific criteria that, if met by the insurers and OPPE, will enable the

calculation of the underwriting risk capital to be made using the reduced risk factors listed in

Addendums I to VII, following the correlation matrix and equation shown in Addendum VIII.

§ 2: Insurers that, on the date this Resolution comes into force, were already using the

reduced risk factors listed in Addendums I and II to calculate the underwriting risk capital shall

be allowed an adaptation period, to be defined by SUSEP, to bring their procedure into line

with the new criteria referred to in the preceding paragraph.

Art. 38: The portions of underwriting risk capital of the insurers and OPPE defined in

Addendums I, II and VII, the calculation of which depends on the historical data of the

transactions, are only to be calculated using the actual amounts involved.

Single paragraph: In the case of supervised bodies created from a split-off or supervised bodies

receiving portfolios transferred by other supervised bodies, the historical record of the

transactions received shall be treated according to the SUSEP regulations.

Art. 39: Calculation of the underwriting risk capital for insurance transactions shall be

performed on the basis set out in Addendums I, II and III, except in the case of the following:

I - free benefit generator life insurance (VGBL);

II - life insurance with guaranteed update plus performance (VAGP);

III - life insurance with guaranteed remuneration plus performance (VRGP);

IV - life insurance with guaranteed remuneration and no performance update (VRSA);

V - life insurance with immediate income (VRI);

VI - pure endowment;

VII - mixed endowment;

VIII - private individual - funeral insurance (class 1329);

IX - private individual - life (class 1391);

X - private individual - life (run-off) (class 0991); and

XI - other personal insurance structured according to the capitalization financial method or the

terminal funding method.

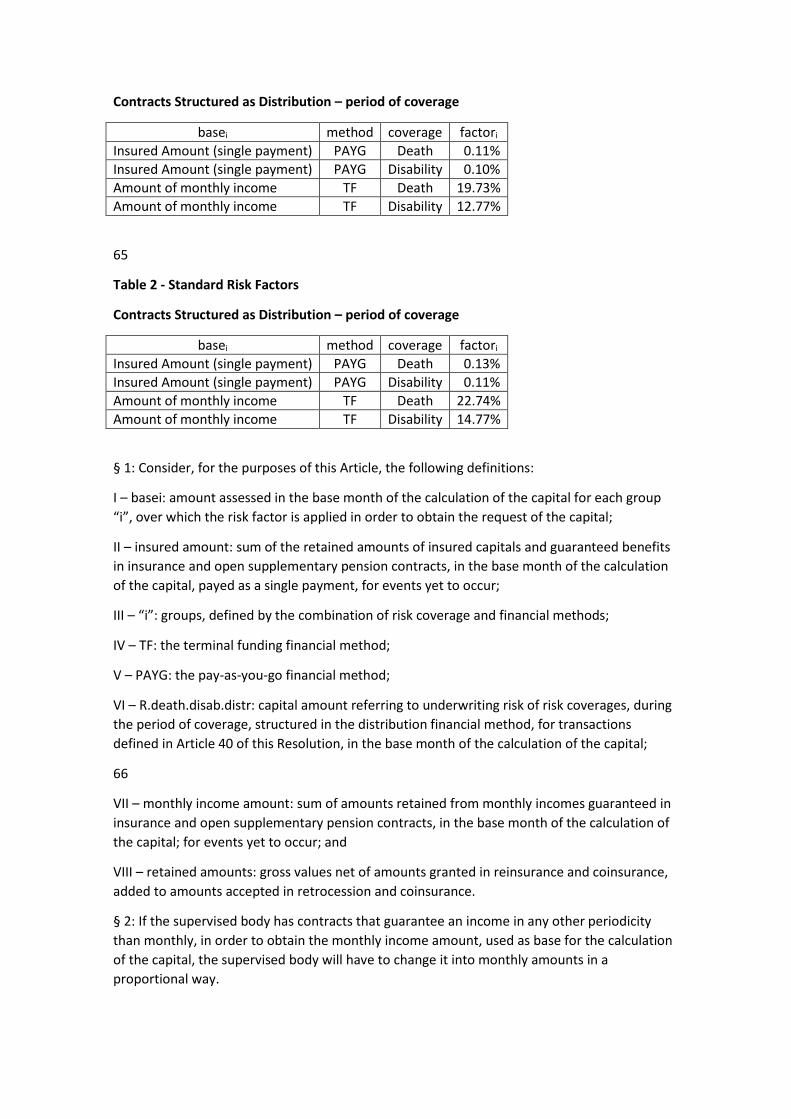

Art. 40: Addendums IV, V, VI and VII shall be used for calculating the underwriting risk capital

of open private supplementary pension and insurance transactions, except for those

mentioned in the preceding Article.

Art. 41: The underwriting risk capital of investment firms shall be calculated using the standard

risk factors and equations set out in Addendums IX to XII, following the correlation matrix in

Addendum XIII.

Single paragraph: SUSEP shall regulate the specific criteria for the investment firms to be able

to use the reduced risk factors listed in Addendums IX to XII.

Continuation of CNSP Resolution nº 321, of 2015.

Art. 42: The underwriting risk capital of the local insurers shall be comprised of the sum of two

parts:

I – the amount obtained by applying the insurers’ underwriting risk model to the proportional

reinsurance, taking into consideration the corresponding transactions and business lines to

which it relates; and

II – the amount obtained by applying the specific procedure, defined in Article 44, to the non-

proportional reinsurance and all other transactions not listed in item I.

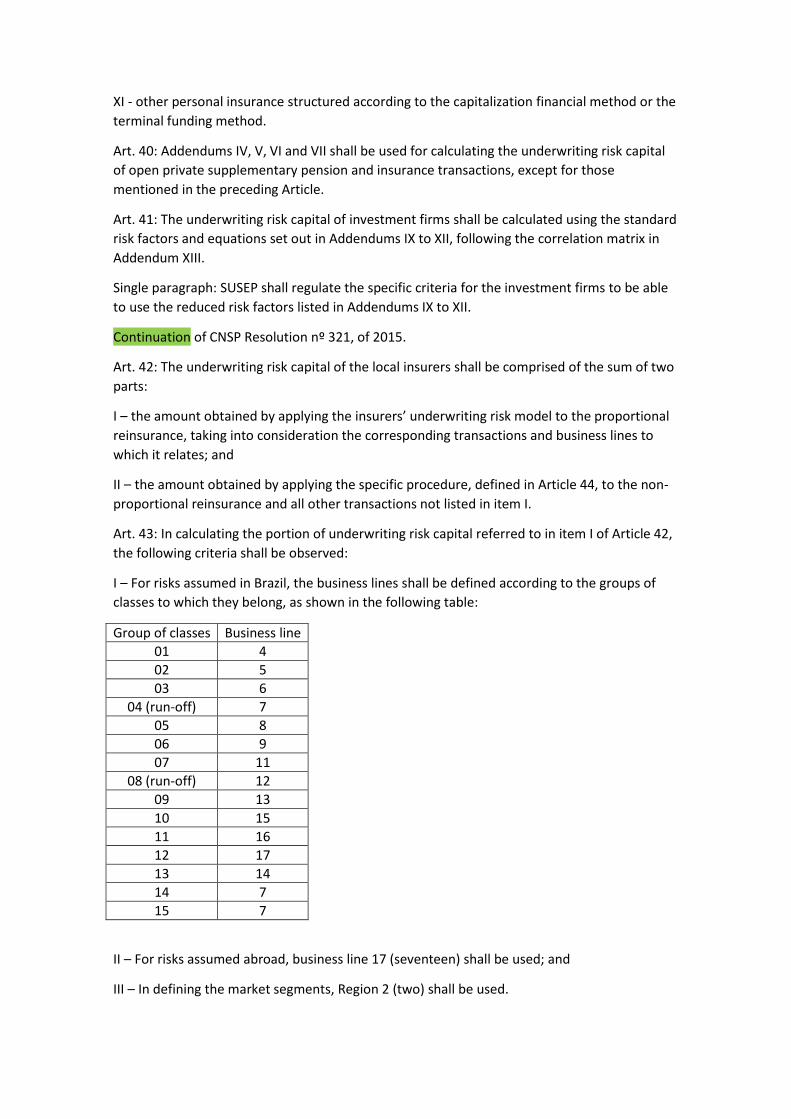

Art. 43: In calculating the portion of underwriting risk capital referred to in item I of Article 42,

the following criteria shall be observed:

I – For risks assumed in Brazil, the business lines shall be defined according to the groups of

classes to which they belong, as shown in the following table:

Group of classes Business line

01 4

02 5

03 6

04 (run-off) 7

05 8

06 9

07 11

08 (run-off) 12

09 13

10 15

11 16

12 17

13 14

14 7

15 7

II – For risks assumed abroad, business line 17 (seventeen) shall be used; and

III – In defining the market segments, Region 2 (two) shall be used.

Art. 44: The specific procedure for obtaining the amount provided for in item II of Art. 42 must

meet the following criteria:

I – For reinsurance coverage structured according to the capitalization financial method and

for the granting of income, the required amount shall be equal to 4% (four percent) of the sum

of the mathematical provisions for benefits to be granted and benefits granted in relation to

direct reinsurance and accepted retrocessions, without deducting ceded retrocessions,

multiplied by the maximum percentage between 85% (eighty five percent) and the ratio

obtained from the sum of the mathematical provisions for benefits to be granted and benefits

granted, net of ceded retrocessions, and the sum mathematical provisions for benefits to be

granted and gross benefits granted, calculated on the last December base date;

Continuation of CNSP Resolution nº 321, of 2015.

II – For reinsurance coverage structured according to the pay-as-you-go or terminal funding

financial methods and risk transactions arising from insurance contracts covering damages, the

greatest of the following amounts:

a) 20% (twenty percent) of the total premiums retained over the last 12 (twelve) months; or

b) 33% (thirty three percent) of the annual average of total claims retained over the last 36

(thirty six) months.

Section II

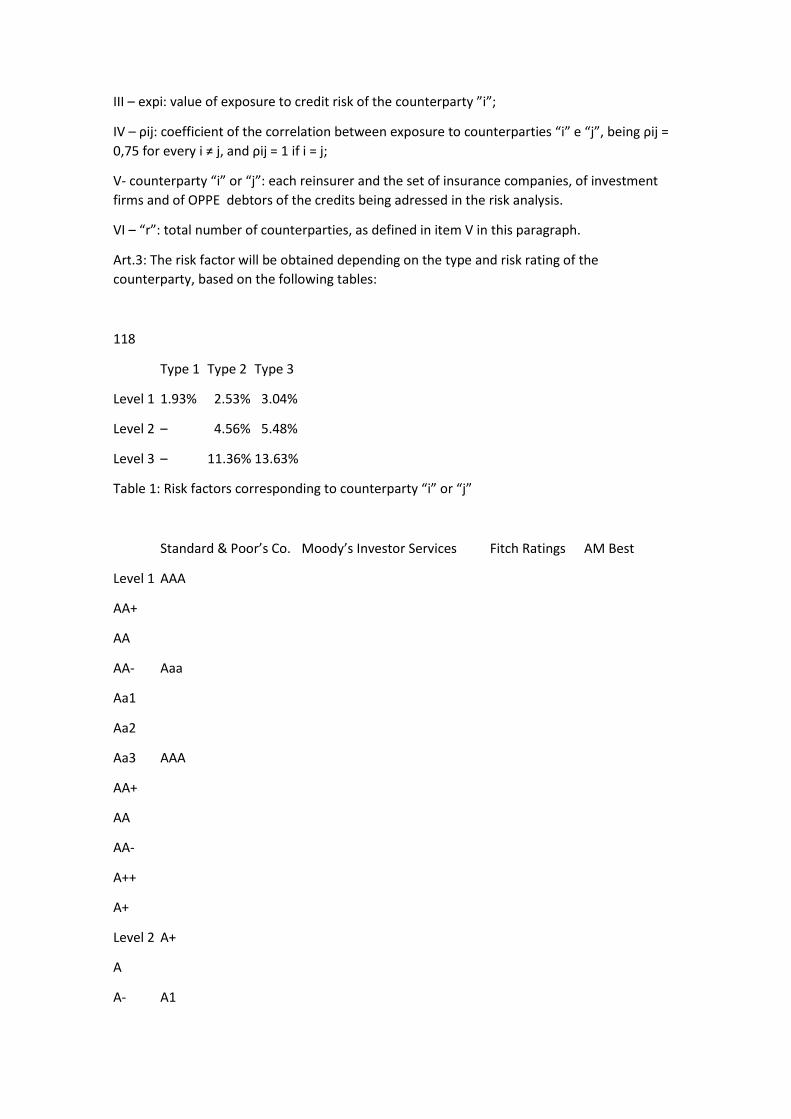

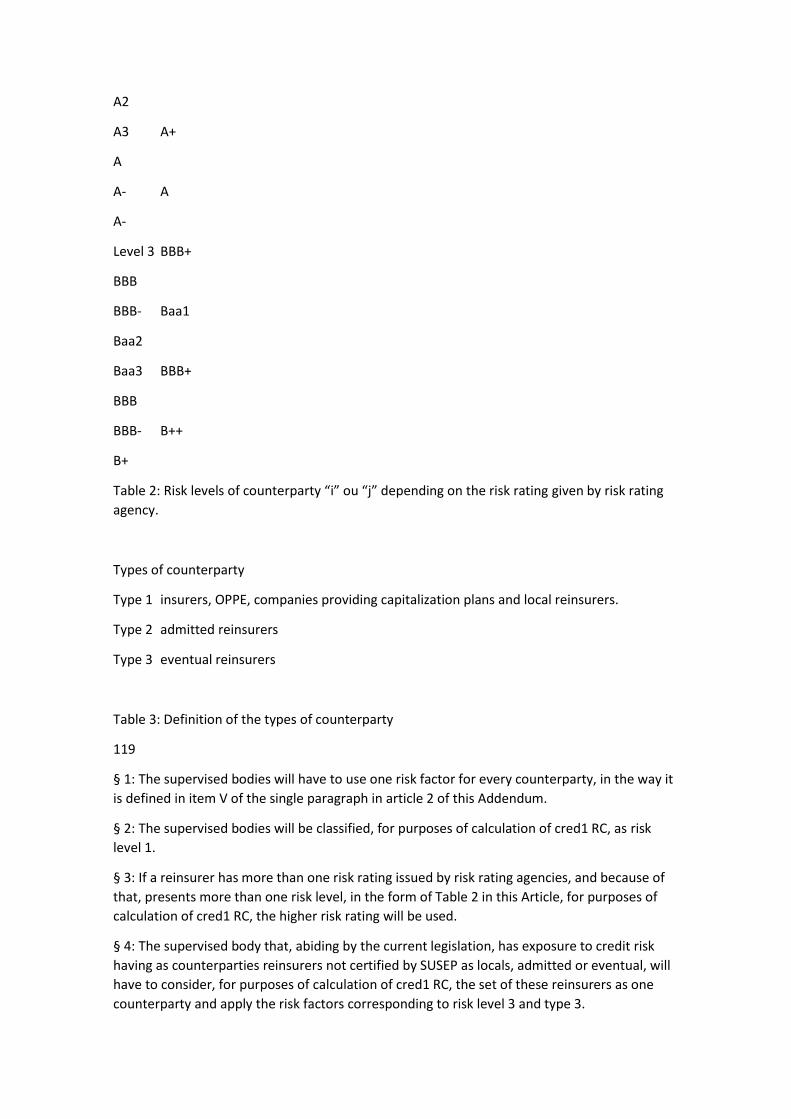

Risk Capital to cover Credit Risk

Art. 45: This Section does not apply to transactions in the DPVAT and DPEM classes.

Art. 46: The credit risk capital of the supervised bodies shall be comprised of two parts and

shall be calculated according to the terms of Addendums XIV to XVI.

Section III

Risk Capital to cover Operational Risk

Art. 47: The operational risk capital of the supervised bodies is calculated according to the

criteria listed in Addendums XVII to XIX.

Section IV

Risk Capital to cover Market Risk

Art. 48: This Section does not apply to transactions in the DPVAT and DPEM classes.

Art. 49: For the purposes of this Section, it shall be considered that:

I – material cash flows: cash flows that, if omitted or poorly assessed, could, considering their

volume, nature and whether they are individual or collective, lead to material misstatement in

the assessment of market risk;

II – economic value: fair price to be paid or received in relation to a particular item, on the

base date of the cash flow calculation, if it were to be traded in the market or between

interested parties that have the same level of knowledge and bargaining power;

III – standard vertices: predetermined and standardized duration periods for grouping cash

flows according to the fixed interest rate, price index coupon or foreign currency coupon that

affects their economic assessment;

IV – net exposure: positive or negative algebraic sum, in reais, of the economic values of all the

material cash flows, rights and obligations whose valuation is subject to the variations of a

particular index, interest rate, foreign currency, share price or commodity price, which must be

calculated for each standard vertex or, where this does not apply, to the total cash flow; and

V – products with a financial surplus guarantee: insurance or pension products that guarantee

the policyholder or participant a portion of any profitability surplus on the investment

portfolio, expressed as a guaranteed minimum rate.

Single paragraph: The concept defined in item I must not be applied to cash flows arising from

financial assets, with must be estimated in their entirety.

Continuation of CNSP Resolution nº 321, of 2015.

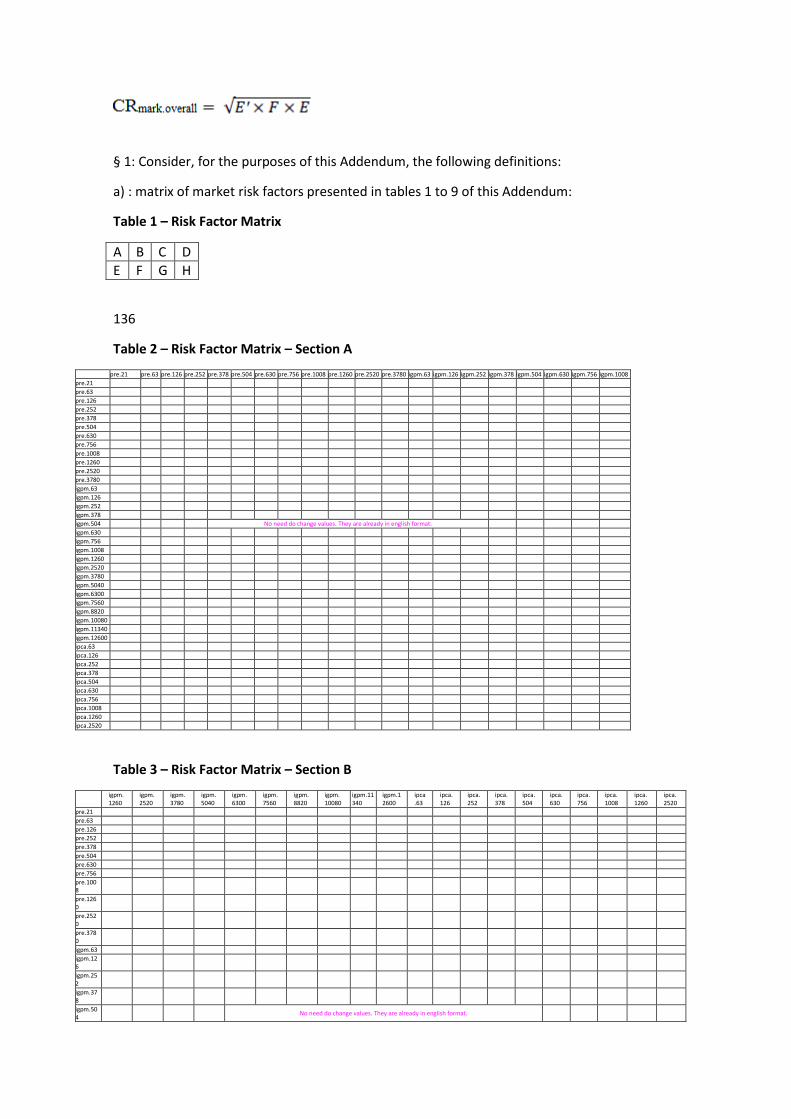

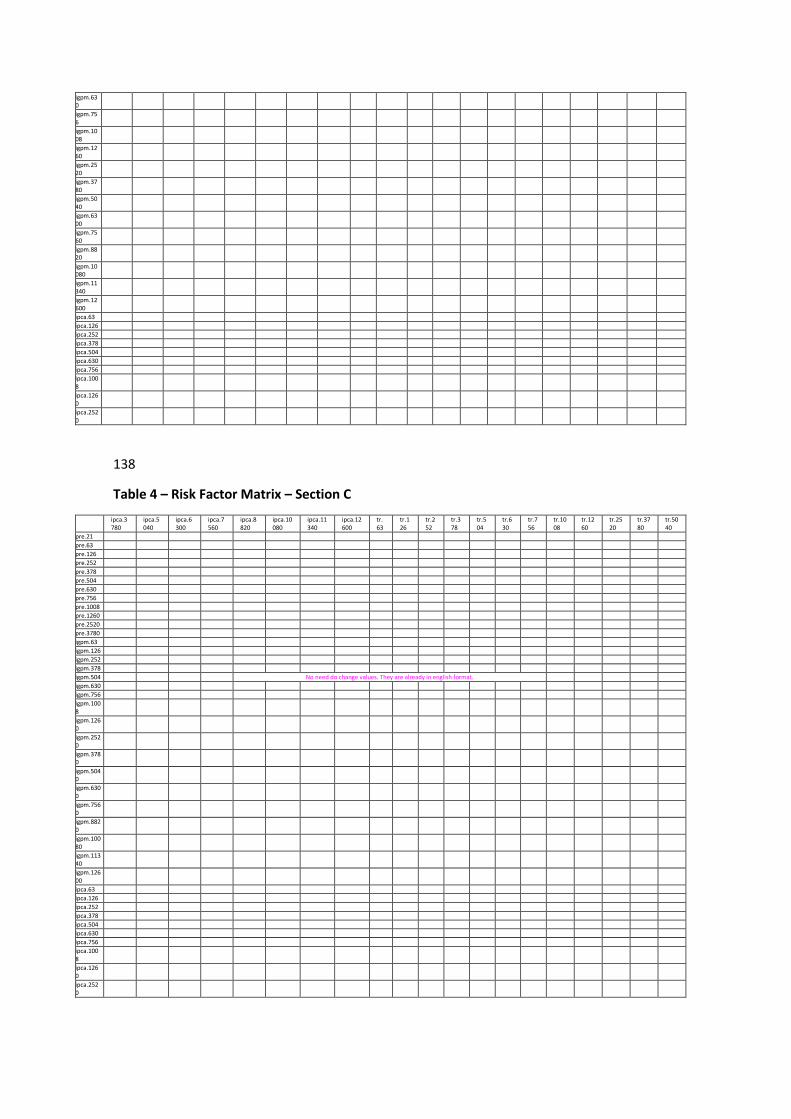

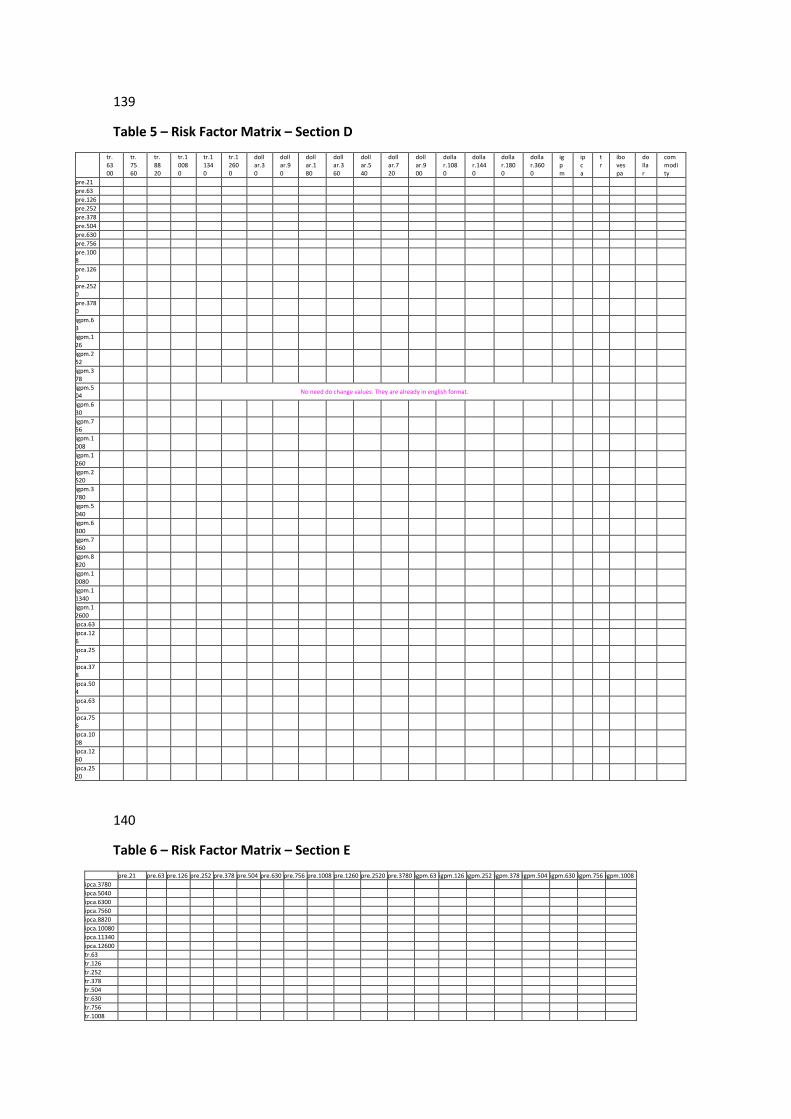

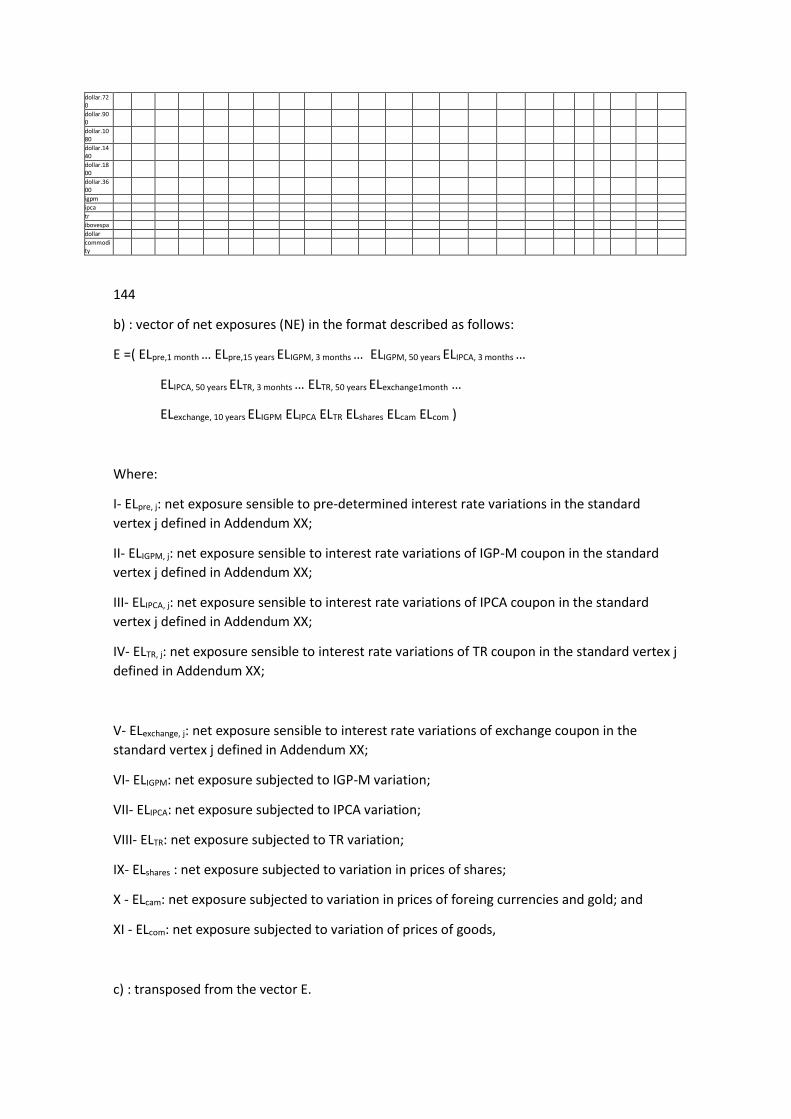

Art. 50: The market risk capital of the supervised bodies is to be calculated as set out in this

Article, in accordance with the methods determined in Addendums XX to XXII.

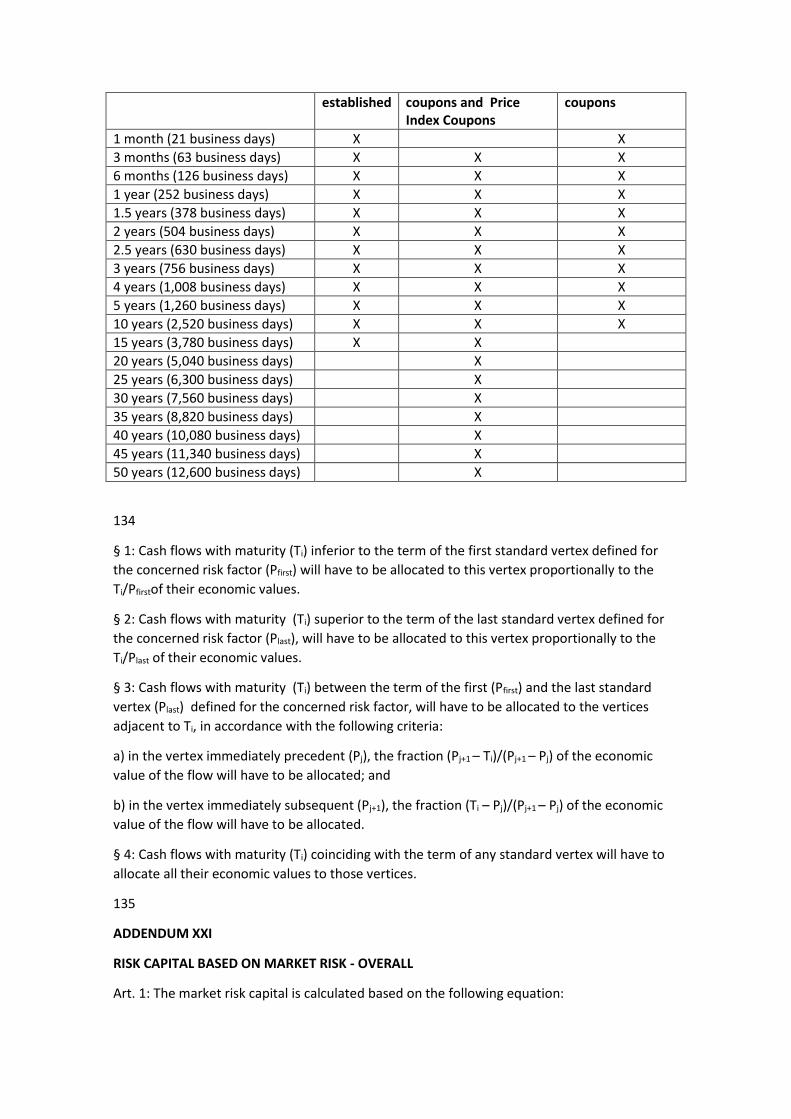

§ 1: For application of the methodology described in Addendum XXI, the economic values of

the cash flows estimated by the supervised bodies shall be allocated in standard vertices

according to their duration and risk factor, in accordance with the procedure set out in

Addendum XX.

§ 2: For supervised bodies that do not have products with a financial surplus guarantee, or that

choose not to use the option provided for in § 3, the RCmarket shall correspond to the

RCmarket.general defined in Addendum XXI.

§ 3: Supervised bodies that have products with a financial surplus guarantee, provided they

have not yet allocated the surplus to a provision for the individual policyholder or participant,

may choose to calculate the amount of market risk capital for these products (RCmarket.surplus)

separately, according to the methodology set out in Addendum XXII, with the RCmarket in this

case defined by the sum of:

a) RCmarket.general: As defined in Addendum XXI, but considering only the net exposure in

relation to products without a financial surplus guarantee and products with such a guarantee,

for which the supervised body chooses not to use the option provided for in the above clause;

and

b) Ʃni=1 RCmarket.surplus: Sum of the RCmarket.surplus calculated, considering the net exposure for

each group i of products with financial surpluses (freely defined), which should include all the

products for which the supervised body chooses to use the option provided for in the above

clause.

§ 4: The amount of market risk capital that is effectively required shall correspond to:

a) 0% of the RCmarket to December 30, 2016;

b) 50% of the RCmarket between December 31, 2016 and December 30, 2017; or

c) 100% of the RCmarket as of December 31, 2017.

Subsection I

Minimum Criteria for estimating the Cash Flows

Art. 51: The supervised bodies should draw up a methodology manual, which is to be made

available to SUSEP, describing the techniques, assumptions, procedures and materiality criteria

adopted for estimating the cash flows.

Single paragraph: The period for preparation of the first version of the methodology manual

should coincide with that determined by SUSEP for the first submission of data by the

supervised bodies.

Art. 52: The calculation of the market risk capital must not consider cash flows in relation to:

a) Share holdings in subsidiaries or affiliates;

b) Tax credits arising from a tax loss or negative social contribution calculation base;

c) Intangible assets;

d) Real estate and closed-end real estate investment funds;

e) Rights and obligations in relation to the transactions of branches abroad;

f) Works of art;

g) Precious stones;

h) Any other assets excluded from the calculation of Adjusted Net Equity (ANE), in accordance

with the current regulations or a decision by the SUSEP;

i) Any other assets or liabilities excluded by a decision of the SUSEP, contained in a document

providing guidance on the calculating of market risk capital.

Continuation of CNSP Resolution nº 321, of 2015.

Art. 53: All the estimated cash flows must be gross of refunds, reimbursements and related

expenses and, if material, be considered as separate streams.

Art. 54: High frequency payments and receipts may be grouped into annual flows, or over a

shorter time period, the length of which should correspond to half the period considered in

the grouping.

Art. 55: To determine the economic value of the cash flows pertaining to general obligations

and rights in relation to insurance, pension, capitalization and reinsurance contracts, the

future amounts of payments and receipts must be discounted using the risk-free Term

Structure of Interest Rates (TSIR ), established by SUSEP, for the corresponding risk factor,

unless the supervised body has received express permission from the autonomous entity to

use its own TSIR.

Art. 56: When estimating the cash flows pertaining to rights and obligations in relation to

insurance, pension, capitalization and reinsurance contracts, a supervised body must apply

statistical and actuarial methods based on realistic assumptions.

Single paragraph: Where applicable, the supervised body must observe the SUSEP standards

and guidelines in relation to the Liability Adequacy Test (LAT) and adopt the same

methodology and assumptions used to carry out the LAT, except where the contents of this

Resolution or a specific guideline for calculating the market risk capital state the contrary.

Art. 57: Supervised bodies must not include in the market risk capital calculation the cash flows

pertaining to rights and obligations relating to the deferral phase of VGBL and PGBL plans.

Single paragraph: In cases referred to in the above clause, the supervised body must consider

only the cash flows arising from the exercising of the conversion into income option by the

policyholder or participant.

Art. 58: When estimating the cash flows of financial assets, the supervised bodies must not

consider reinvestment activities, but include only the assets that they actually hold at the time

of the appraisal.

Art. 59: For investment funds in which the supervised body holds a stake, the cash flows must

be considered only in proportion to the shares it holds, directly or indirectly.

§ 1: Whenever possible, the supervised body should consider the individual cash flows for each

asset that comprises the investment fund portfolios.

§ 2: In the case provided for in § 1, the cash flows for each investment fund asset should be

grouped according to the risk factor to which it is exposed, in accordance with the provisions

of Addendum XXI.

§ 3: Should it be impossible to identify the risk factor, maturity or net risk exposure of any

asset belonging to an investment fund, at any level, the total shares that the supervised body

holds, directly or indirectly, in that fund should be considered in calculating the corresponding

net exposure to the share risk factor, in accordance with the provisions of Addendum XXI.

Continuation of CNSP Resolution nº 321, of 2015.

Art. 60: The cash flows for financial assets whose profitability is pegged to a percentage of the

DI or Selic rate and whose contractual yield differs from that practiced by the market must be

used by the supervised body to determine the net exposure to the fixed interest rate risk

factor, in accordance with the provisions of Addendum XXI.

§ 1: In the case referred to in the above clause, the economic values of the cash flows must

only be considered in proportion to the difference between the contractual yield and the

market yield on that security.

§ 2: If the contractual yield of the asset exceeds the market yield on that security, the cash

flows, proportional to the difference, shall be considered a unit price oversold exposure. For

the opposite scenario, they shall be considered an overpurchased exposure.

Art. 61: Supervised bodies should estimate the cash flows for financial derivatives.

§ 1: In the case of futures contracts, in determining the net exposure to the risk factors listed

in Addendum XXI, consideration should be given to:

a) a cash flow with the same term and notional amount as the underlying asset; and

b) a cash flow similar to that of item "a" and term and value but with the opposite sign, which

will be considered in the calculation of the net exposure corresponding to the risk factor of

fixed interest rates, in accordance with the provisions of Addendum XXI.

§ 2: In the case of swaps, the cash flows should be considered for both long and short

positions.

§ 3: In the case of options, a cash flow should be included that is calculated as the product of

the delta of the option, the size of the contract and the value of the underlying asset.

Art. 62: Cash flows used for calculating the market risk capital should, at the very least, be

estimated upon the closure of the trial balances for the months of March, June, September

and December.

Single paragraph: SUSEP shall set the deadline for the first submission of data provided for in

this Resolution and shall provide guidance to the supervised bodies as to the form of delivery.

Continuation of CNSP Resolution nº 321, of 2015.

Subsection II

Transitory Provisions of this Chapter

Art. 63: A requirement for market risk capital in any proportion other than 0% of the RCmarket,

as provided for in items "b" and "c" of § 4 of Article 50, will only occur if, by December 31,

2016, regulations come into force that increase the sensitivity of the ANE to variations in the

economic values used to calculate the market risk capital.

§ 1: Alternatively, a new parameter may be introduced for the purpose of calculating the

capital adequacy that would meet the objective set out in the above clause.

§ 2: If the regulations referred to in this Article come into force after the abovementioned

date, the requirement for market risk capital in any proportion other than 0% of the RCmarket

would be as follows:

a) 50% of the RCmarket as of the date on which the aforementioned regulations come into force;

and

b) 100% of the RCmarket 1 (one) year later.

CHAPTER IV

Adjusted Net Equity

Art. 64: Calculation of the ANE shall be based on the accounting net equity or accounting

shareholders' equity, as appropriate, after the following deductions:

I – the value of equity stakes in financial and non-financial companiesa classified as permanent

investments, in Brazil or abroad, considering the added value and goodwill, as well as any

reductions to recovery value;

II – pre-paid expenses unrelated to reinsurance;

III – tax credits arising from tax losses in relation to income tax and a negative social

contribution base;

IV – intangible assets;

V - urban properties and real estate investment funds linked to urban property, considering

revaluations, impairment and depreciation, that exceeds 14% of the total adjusted assets;

VI - rural properties and real estate investment funds linked to rural properties, considering

revaluations, impairment and depreciation;

VII - deferred assets;

VIII - rights and obligations relating to the transactions of branches abroad;

IX - works of art;

X - precious stones; and

Continuation of CNSP Resolution nº 321, of 2015.

XI - credits from the sale of assets listed in the preceding items, observing the deduction rule in

item V in the case of the disposal of urban property.

§ 1: Consider as total adjusted assets, for the purposes of the provisions in item V, the balance

of the total assets net of the deductions listed in Items I, II, III, IV, VI, VII, VIII, IX, X and XI.

§ 2: Real estate investment funds linked to urban or rural property, provided they are open to

public trading, in accordance with the Brazilian Securities Commission (CVM) Instruction

dealing with the public offering of marketable securities, are not liable to the deductions

mentioned in item V and VI.

CHAPTER V

Minimum Capital Requirement and Solvency Regularization Plan

Art. 65. Consider, for the purposes of this Chapter:

I – capital base: the fixed amount of capital that the supervised body must maintain, at all

times, as provided for in Addendums XXIII to XXV, while for supervised bodies operating

exclusively in micro-insurance it shall be 20% (twenty percent) of the amount determined in

Addendum XXIII.

II – risk capital (RC): the variable amount of capital that the supervised body must maintain, at

all times, to guarantee the risks inherent in its operations, as provided for in Addendum XXVI;

III – Minimum Capital Requirement (MCR): the total capital that the supervised body must

maintain in order to operate, equivalent to the higher of the capital base, as defined in

Addendums XXIII to XXV, and the risk capital, as defined in Addendum XXVI;

IV – liquid assets: all the assets accepted by the National Monetary Council (CMN) in 100%

(one hundred percent) coverage of the technical provisions;

V – liquidity in relation to the RC: a situation where the supervised body holds an amount of

liquid assets that is in excess of the need to cover the technical provisions, equivalent to more

than 20% (twenty percent) of the RC;

VI – Solvency Regularization Plan (SRP): a plan that must be sent by a supervised body to the

SUSEP, in the manner determined in this Resolution, aimed at restoring a state of solvency

when there is a shortfall in the ANE in relation to the MCR of up to 50% (fifty percent) or when

the supervised body has insufficient liquidity in relation to the RC.

VII – local reinsurer: a reinsurer domiciled in Brazil and set up as a corporation, which has the

sole purpose the performing of reinsurance and retrocession transactions;

VIII – admitted reinsurer: a reinsurer domiciled abroad, with a representative office in Brazil,

that, meeting the requirements of Supplementary Law No. 126 of January 15, 2007 and the

rules applicable to reinsurance and retrocession activities, has been registered as such by the

Private Insurance Agency (SUSEP) to perform reinsurance and retrocession transactions;

Continuation of CNSP Resolution nº 321, of 2015.

Section I

Capital Requirements

Art. 66: Supervised bodies must show, every month, when closing their monthly trial balances,

an ANE that is equal to or above the MCR and liquidity in relation to the RC.

Art. 67: In the even of an ANE shortfall in relation to the MCR of up to 50% (fifty percent) or a

liquidity shortfall in relation to the RC, the supervised body must submit an SRP, in the manner

provided for in this Chapter, proposing an action plan aimed at restoring a state of solvency.

§ 1: An SRP will only be required if a shortfall is ascertained in 3 (three) consecutive months or,

specifically, in the months of June and December.

§ 2: A worsening of the ANE shortfall to the levels provided for in Articles 68 and 69 shall make

the supervised body subject to special treatment, under the terms of the prevailing legislation.

Art. 68: A supervised body shall be subject to the special treatment of direct management

supervision, pursuant to the prevailing legislation, if its ANE shortfall in relation to the MCR is

greater than 50% (fifty percent) and less than or equal to 70% (seventy percent).

Art. 69: A supervised body shall be subject to being placed in receivership, pursuant to the

prevailing legislation, if its ANE shortfall in relation to the MCR is greater than 70% (seventy

percent).

Section II

Liquid Asset linkage

Art. 70: Liquid assets in excess of the coverage need, as defined in this Chapter, shall be

recorded in an account linked to SUSEP, in accordance with the prevailing legislation.

Section III

Solvency Regularization Plan

Art. 71: The supervised body must submit the SRP to the SUSEP within 45 (forty-five) days from

the date the notification from the SUSEP was received.

Single paragraph: The SRP must be approved by the supervised body’s executive board and, if

there is one, supervisory board or steering committee.

Continuation of CNSP Resolution nº 321, of 2015.

Art. 72: The SRP must contain well-defined deadlines and targets and provide precise details of

the procedures to be adopted in order to resolve any shortfall, including the following

essential features:

I – identification of the factors that contributed to the shortfall;

II – identification of any problems in relation to assets and liabilities, growth of the business,

extraordinary exposure to risk, product diversification, reinsurance and any other factors that

the supervised body considers to be relevant; and

III – proposals for corrective action that the supervised body intends to adopt.

§ 1: The maximum period for the resolution of the ANE shortfall shall be 18 (eighteen) months

from the month following the date of receipt of the notification provided for in the main

clause of Article 71.

§ 2: The maximum period for the resolution of the liquidity shortfall in relation to the RC shall

be 6 (six) months from the month following the date of receipt of the notification provided for

in the main clause of Article 71.

§ 3: In the event of an adverse economic situation in the market of the supervised body or in

the financial situation, SUSEP may extend the periods referred to the preceding paragraphs by

up to 9 (nine) months and 3 (three) months, respectively.

§ 4: The SRP must additionally comply with the supplementary instructions that are issued by

SUSEP in specific regulations or in the notification mentioned in the main clause of Article 71.

Art. 73: The SRP shall be submitted for the decision of the SUSEP Technical Board.

§ 1: The decision mentioned in the above clause shall result in it being approved or rejected,

which shall be announced by the Office for Solvency Monitoring General Coordination (CGSOA)

and, in the case of rejection, confirmed by the SUSEP Steering Committee.

§ 2: In the event of the plan's rejection, SUSEP shall additionally inform the reasons underlying

its decision, and the supervised body shall have one more chance to submit, within a

maximum period of 45 (forty-five) days from the date of receipt of the notification, a new SRP.

§ 3: As long as this does not involve non-compliance with the laws or regulations in force, the

actions proposed in the SRP must be adopted by the supervised body even before the SUSEP

has declared its approval or rejection of the plan.

Continuation of CNSP Resolution nº 321, of 2015.

Art. 74: While carrying out the SRP, in order to facilitate its monitoring, the supervised body

must send to the SUSEP, at specified intervals, any reports that autonomous entity shall deem

to be necessary.

Single paragraph: Whenever it deems necessary, the SUSEP may request a review of the SRP,

which must be approved by the SUSEP Technical Board.

Art. 75: In the event of failure to submit an SRP, rejection of the SRP for the second time or

non-compliance with the SRP, the supervised body shall be subject to the special treatment of

direct management supervision, even if its ANE shortfall in relation to the MCR or liquidity

shortfall in relation to the RC is less than or equal to 50% (fifty percent).

Single paragraph: The SRP must contain an explicit statement that the executive board and, if

there is one, the supervisory board or steering committee are aware that, in the circumstances

provided for in the above clause, the supervised body shall be subject to the special treatment

of direct management supervision.

Art. 76: The SUSEP Steering Committee may, as an alternative to the special treatment in

relation to the situations set out in this Chapter and following analysis of the specific situation

of the supervised body, request the submitting of a new SRP to the SUSEP.

TITLE II

QUALITATIVE ELEMENTS

CHAPTER I

Retention Limits for the Insurance companies, OPPE and Local Reinsurers

Art. 77: For the purposes of this Chapter, it shall be considered that:

I – isolated risk: the object or set of objects of the insurance or pension coverage of risk, the

possibility of being affected by the same loss generating event of which is significant; and

II – risk coverage: coverage for which the generating event is not the participant's survival past

a predetermined date.

Art. 78: The retention limit is the maximum amount of liability that insurers, OPPE and local

reinsurers may retain for each isolated risk, which is determined based on the values of the

respective ANE.

Continuation of CNSP Resolution nº 321, of 2015.

Art. 79: For calculation of the values of the retention limits, the insurers, OPPE and local

reinsurers must make an actuarial technical note, prepared by the technically responsible

actuary, available to SUSEP, observing the following:

I – the calculation must be performed using a scientifically proven method that can generate

consistent results;

II – the actuarial technical note containing the calculation methodology must be submitted to

SUSEP within five (5) business days from the date the request was received;

III – SUSEP may, at any time, as may be necessary in each case, determine for the insurer,

OPPE or local reinsurer the use of a specific method for calculating the retention limits or set

retention limit values that are different to those calculated by the supervised body; and

IV – in the situation provided for in item III of this Article, an insurer, OPPE or local reinsurer

may submit to the SUSEP a request to use its own method, the application of which shall be

dependent upon prior authorization by SUSEP.

Art. 80: The insurers, OPPE and local insurers must calculate their retention limits in the

months of February and August, but they are allowed to calculate new retention limits in the

other months of the year.

§ 1: The calculation base for calculating the values in the months between February and July

must be the ANE for December of the previous year.

§ 2: The calculation base for calculating the values in the months between August and January

must be the ANE for the previous June.

§ 3: The values of the retention limits must be submitted to the SUSEP in accordance with the

specific regulations.

§ 4: The values of the retention limits calculated for a specific base date shall come into effect

from the first day of the month following the calculation month.

§ 5: In the case of a capital increase, in cash or assets, paid in after the December or June base

date, the insurers, OPPE and local reinsurers may, in the month immediately following that

increase, calculate the retention limits based on the ANE for the month of the increase, which

shall come into effect from the first day of the month following the calculation month.

§ 6: For transactions involving the risk coverage of the supplementary pension products of the

insurers and OPPE, the retention limits must be calculated by type of risk coverage.

§ 7: For insurance transactions, the retention limits must be calculated by class.

Continuation of CNSP Resolution nº 321, of 2015.

§ 8: For reinsurance transactions, the retention limits must be calculated by group of classes.

§ 9: The provisions of this Article do not apply to survivor coverage transactions.

Art. 81: Retention limit values calculated by the insurers or OPPE that are less than or equal to

5% of the ANE do not require prior authorization by the SUSEP.

Single paragraph: Subject to prior authorization by the SUSEP, insurers or OPPE may be

allowed to use retention limits with a values greater than 5% of the ANE.

Art. 82: Insurers, OPPE and local insurers may not set retention limits and therefore cannot

accept risks when the amount of the book loss would be greater than the sum of the paid in

capital plus reserves provided for in the net equity.

Art. 83. Insurers, OPPE and local insurers must keep available, in digital format, for inspection

by the SUSEP, during a period of 5 (five) years, all the documentation and statistical data

corroborating their full compliance with the provisions of this Chapter.

CHAPTER II

Investment Criteria

Art. 84: For the purposes of this Chapter, it shall be considered that:

I – colateral assets: assets linked to the securing of the provisions, in accordance with the

guidelines issued by the National Monetary Council (CMN);

II – CPR: Rural Product Note;

III – derivatives: contracts for financial assets or marketable securities whose trading value and

characteristics derive from other assets, that serve as their base of reference;

IV – risk factor: price index, interest rate, share index or asset price whose variations may have

an impact on the market value of the investment portfolio;

V – FIE: specially constituted investment fund or investment fund investing in the shares of

investment funds specially set up to directly or indirectly receive resources from supervised

bodies;

VI – investments: assets and operational formats of insurers, OPPE, investment firms or local

reinsurers, such as options, the forward market, futures and swaps, among others, and the

financial assets and the operational formats held by an admitted reinsurer, relating to the

resources required in Brazil to guarantee its obligations.

VII – portfolio protection: reducing the exposure to certain risk factors, in order to protect the

portfolio against possible variations in the fair value of an asset;

VIII – spot market position synthesis: using derivatives to synthesize financial structures traded

in the spot market;

Continuation of CNSP Resolution nº 321, of 2015.

IX – BM&FBOVESPA (Bolsa de Valores, Mercadorias e Futuros S.A.) - the São Paulo Stock

Exchange;

X – CETIP (Cetip S.A.) - Clearing House for the Custody and Financial Settlement of Securities;

and

XI – SELIC (Sistema Especial de Liquidação e Custódia) - Special System for Settlement &

Custody.

Section I

Insurance companies, OPPE, Investment firms or Local reinsurers

Art. 85: Management of the investments made by insurers, OPPE, investment firms or local

insurers should observe the following:

I – the princíiples of security, profitability, solvency and liquidity; and

II – specific features, such as the characteristics of its liabilities, with a view to maintaining the

necessary economic, financial and actuarial balance between the assets and liabilities.

Subsection I

Recording, Financial Settlement and Custody of Investments

Art. 86: The financial assets, including those comprising an FIE portfolio, should be:

I – held in custody or recorded in a registration system, in the name of the supervised body or

FIE, as appropriate, in specific individual accounts at the BM&FBOVESPA, CETIP or SELIC; or

II – deposited, if acceptable, in a custody account with a financial institution or entity

authorized by the Brazilian Central Bank (BCB) or the Brazilian Securities Commission (CVM) to

provide such service.

§ 1: Derivative transactions must be registered in the name of the insurer, OPPE, investment

firm, local reinsurer or FIE, in a system of registration at an institution duly authorized by the

BCB or CVM.

§ 2: Registration of the CPR used as a collateral asset or as part of an FIE portfolio whose

shares are used as collateral assets must identify any financial institution(s) sharing joint-

liability or state the number of the insurance policy that it secures, the name of the insurer and

the number of the SUSEP process stating the contractual terms and the actuarial technical

note.

§ 3: The insurer, OPPE, investment firm or local insurer needs to authorize the managers of the

systems, the institutions and the entities referred to in items I and II and § 1 to make the

information relating to its investments available to the SUSEP.

Continuation of CNSP Resolution nº 321, of 2015.

§ 4: Exclusively in regard to the investments comprising an FIE portfolio, the insurer, OPPE,

investment firm or local reinsurer, along with the fund management company, must authorize

the systems managers, institutions and entities referred to in items I and II and § 1 to make the

information concerning the composition of that portfolio available to the SUSEP.

§ 5: The provisions of item I apply to the managers of the assets securing the DPVAT insurance

technical provisions.

Art. 87: The property that is among the investments of the insurers, OPPE, investment firms or

local reinsurers is to be registered in their own name at a real estate registry office.

Single paragraph: The property sales contract, as well as any sale against payment in cash or in

installments, should also be registered under the terms of this Article.

Subsection II

Special Conditions for an FIE

Art. 88: In the case of an FIE whose shares are linked to securing technical provisions, repo

transactions can only be carried out in relation to assets securing technical provisions,

according to the CMN regulations.

Art. 89: FIE operations in the derivatives markets:

I - must be carried out exclusively for the protection of the portfolio, which may include

carrying out spot market position synthesis transactions;

II - must not generate, at any time, exposure that exceeds the value of the respective net

equity;

III - must not generate, at any time or cumulatively with the spot positions, exposure in

relation to each risk factor that exceeds the respective net equity;

IV - must not carry out uncovered option sales transactions; and

V - must not be carried out in the "unsecured" category.

Continuation of CNSP Resolution nº 321, of 2015.

§ 1: The use of derivatives by an FIE is conditional upon the fund regulations containing specific

clauses explaining the provisions of items I to V.

§ 2: The exposure resulting from the use of derivatives shall be considered, for classification of

the FIE portfolio within the criteria for diversification defined in its regulations, in its products

sold and in the guidelines issued by the CMN in relation to the collateral assets of technical

provisions.

§ 3: The provisions of item III of this Article shall only apply when the FIE shares are linked to

the securing of technical provisions.

Art. 90: It is forbidden for an FIE to have in its portfolio, directly or indirectly, investments in

the shares of investment funds whose performance in the derivatives markets generates, at

any time, exposure that exceeds the value of their net equity.

Subsection III

Investment Prohibitions

Art. 91: It is forbidden for an insurance company, OPPE, investment firm or local reinsurer to,

directly or indirectly:

I – perform derivative transactions that, at any time, generate exposure that exceeds the total

amount of the spot positions held;

II – perform derivative transactions in the “unsecured” category;

III – invest in the shares of investment funds whose involvement, directly or indirectly, in

derivative markets generates, at any time, exposure that exceeds the value of the respective

net equity;

IV – carry out uncovered option sales transactions;

V – invest funds in portfolios managed by private individuals, or in investment funds whose

portfolios are managed by private individuals;

VI – invest in assets abroad, except in the following cases:

a) those explicitly provided for in the CMN regulations;

b) those explicitly provided for in the regulations of the Brazilian Securities Commission

governing the assets that comprise investment fund portfolios;

c) investments made through affiliates or branches set up abroad, in compliance with Art. 54

of Decree nº 60,459, of March 13, 1967;

d) share holdings of a permanente nature in insurers, OPPE, investment firms, reinsurers or

similar, subject to prior approval by the SUSEP.

VII – invest in the shares of investment funds that do not have procedures for the assessment

and measurement of the investment portfolio risk;

VIII – provide a guarantee, surety or acceptance or take on a joint liability;

IX - grant loans or advances, or open a line of credit in any category to private individuals or

legal entities, especially those listed in Art. 17 of Law No. 7,492, of June 16, 1986, apart from

the exceptions specifically provided for in the current regulations;

Continuation of CNSP Resolution nº 321, of 2015.

X – carry out any commercial, financial or real estate transactions with:

a) its management or members of statutory committees, or their spouses, partners or relatives

up to the second degree;

b) companies in which any of the people referred to in sub-item “a” of this item participate,

except in the case of participation as a shareholder with a stake of up to 5% (five percent); and

c) a counterparty, even if indirectly, who is one of the private individuals defined in sub-item

“a” of this item or an affiliated company;

XI – invest in marketable securities issued by or the joint liability of affiliated companies;

XII – invest in the shares of investment funds whose portfolio contains marketable securities

issued by and/or the joint liability of the insurance company, OPPE, investment firm or local

reinsurer, its controlling shareholders, companies that it holds a direct or indirect controlling

stake in, or affiliated companies or other companies under joint control; and

XIII – invest in assets that were issued by, the joint liability of or otherwise secured by a private

individual.

§ 1: The transactions referred to in item I must be exclusively for the purpose of portfolio

protection and spot market position synthesis;

§ 2: The prohibition on joint liability, referred to in item VIII, does not apply to:

I – insurance company participation in co-insurance or retrocession transactions, or

II – local reinsurer participation in reinsurance or retrocession transactions.

§ 3: The prohibitions referred to in item X of this Article do not apply to:

I – transactions relating to the merger or demerger of assets for purpose of a share capital

increase or reduction;

II – policyholders or participants in plans that, in such status, conduct transactions with an

insurance company, OPPE, investment firm or local reinsurer, when these are in the exclusive

performance of their corporate purpose, in accordance with the specific regulations issued by

the SUSEP;

III – service provision operations, provided that the contractual remuneration is compatible

with market values and the contracts have been approved by and are overseen by the

supervisory board and executive board of the insurance company, OPPE, investment firm or

local reinsurer;

IV – transactions that, respecting the prevailing regulations, are agreed between insurers,

OPPE, investment firms or local reinsurers as a result of operational agreements whose sole

objective is the promotion of product marketing regulated under the National Private

Insurance System (SNSP); and

V – risk transfer agreements made between insurers and reinsurers.

Continuation of CNSP Resolution nº 321, of 2015.

§ 4: The prohibitions referred to in items XI and XII do not apply to securities issued by the

National Treasury to credits securitized by the National Treasury or to securities issued by the

states or municipalities that are the objects of contracts under the terms of Law nº 9,496, of

September 11, 1997, or Provisional Measure nº 2,185-35, of August 24, 2001.

§ 5: The prohibition referred to in item XII does not apply to shares comprising a market index

that is a benchmark for the fund's investment policy, provided that the proportional

participation of each share in that index is observed.

§ 6: The prohibition referred to in item XIII does not apply to:

I – financial assistance granted in accordance with specific regulations issued by the SUSEP; or

II – investments in the shares of investment funds whose portfolio contains assets issued,

under joint liability or in any other way guaranteed by a private individual, as long as the

administrator or management institution considers such assets as low credit risk, based on the

classification made by a rating agency operating in Brazil.

Art. 92: In addition to the provisions of Art. 91, exclusively with regard to collateral assets,

insurance companies, OPPE, investment firms or local reinsurers are prohibited from:

I – offering collateral assets to secure transactions in the futures markets or in any other

situations;

II – selling, pledging or in any other way encumbering collateral assets or the rights deriving

therefrom, without explicit prior authorization from the SUSEP;

III – leasing, lending or pledging marketable securities;

IV – conducting share transactions through private negotiations;

V – offering as collateral shares issued by companies that are not listed for trading in the stock

market or in over the counter markets run by a CVM accredited entity, except in the cases

already authorized by the CMN and approved by the SUSEP, in accordance with paragraphs 4

and 5 of Art.77 of Supplementary Law nº 109, of May 29, 2001;

VI – offering assets that have not been accepted under the terms of the CMN regulations;

VII – offering permanent shareholdings as collateral, except in the cases already authorized by

the CMN and approved by the SUSEP, in accordance with paragraphs 4 and 5 of Art.77 of

Supplementary Law nº 109, of May 29, 2001; or

VIII – offering CPR secured by the insurance company itself or by an affiliated company.

Subsection IV

General Provisions of this Section

Art. 93: The distribution of shares, debentures and other marketable securities, as well as the

subscription bonuses of listed companies and deposit certificates relating to shares that

comprise the investments of insurance companies, OPPE, investment firms, local reinsurers or

FIE must be previously registered with the CVM.

Continuation of CNSP Resolution nº 321, of 2015.

Single paragraph: The provisions of this Article do not apply to cases where the prior

registration of the distribution has been waived by the CVM.

Art. 94: The marketable securities that comprise the investments of insurance companies,

OPPE, investment firms, local reinsurers or FIE shall be identified using an ISIN (International

Securities Identification Number) code.

Section II

Investment of the Funds Required in Brazil to Secure the Liabilities of an Admitted Reinsurer

Art. 95: The funds required in Brazil to secure the liabilities of an admitted reinsurer are to be

held in accounts linked to the SUSEP and must be:

I – deposited, in foreign currency, in a bank authorized to operate in the foreign exchange

market in Brazil; or

II – invested, following conversion into reais, and deposited, in the name of the admitted

reinsurer, with a custodian or registered with a system of registration and deposited in specific

individual accounts held at the BM&FBOVESPA, CETIP or SELIC, as appropriate.

§ 1: The admitted reinsurer shall authorize the financial institution that maintains the account,

referred to in item I, to make available to the SUSEP the information relating to the daily

turnover and balance of such account.

§ 2: The admitted reinsurer shall authorize the managers of the systems, institutions and

entities, referred to in items I and II, to make available to the SUSEP the information pertaining

to its investments.

Art. 96: In relation to the funds required in Brazil to secure its liabilities, it is forbidden for an

admitted reinsurer, directly or indirectly, to:

I – lease, lend or pledge marketable securities;

II – have as a counterparty in its transactions, even if indirectly, the institution responsible for

the management of its investments or investment fund(s), or any of its affiliates;

III – have an affiliated company as a counterparty in its transactions, even if indirectly;

IV – invest in investment funds whose portfolios are managed by private individuals, or in

portfolios that are managed by private individuals;

V – invest in marketable securities issued by and/or the joint liability of the institution

responsible for managing its investments, or those if its affiliates;

VI – invest in marketable securities issued by and/or the joint liability of affiliated companies or

other companies that are under joint control;

VII – invest in investment funds whose portfolio contains marketable securities that were

issued by and/or are the joint liability of:

a) the institution responsible for the management of its investments or those of its controllers,

direct or indirect subsidiaries, affiliated companies or other companies that are under joint

control; or

b) the admitted reinsurer itself, its controllers, its direct or indirect subsidiaries, affiliated

companies or other companies that are under joint control.

Continuation of CNSP Resolution nº 321, of 2015.

VIII – invest in assets that were issued by, are the joint liability of or in any other way are

guaranteed by a private individual;

IX – offer assets that are not accepted under the terms of the CMN regulations.

Art. 97: The marketable securities that comprise the investments of the admitted reinsurer

shall be identified using an ISIN (International Securities Identification Number) code.

TITLE III

RULES GOVERNING TRANSPARENCY AND DISCLOSURE

CHAPTER I

Accounting Standards

Art. 98: The supervised bodies must observe the Accounting Standards, in accordance with the

specific regulations published by the SUSEP.

CHAPTER II

Independent Actuarial Auditing

Art. 99: For the purposes of this Chapter, it shall be considered that:

I – independent actuary: the private individual or legal entity responsible for performing the

independent actuarial audit;

II – technically responsible actuary: the actuary responsible for calculating the technical

provisions, for the actuarial technical notes and for the actuarial information presented by the

supervised bodies to the SUSEP, as well as any other duties provided for in specific regulations;

III – member responsible for the independent actuarial auditing: a person with technical

responsibility, a director, manager, supervisor or any other person in a management role who

is a member of the team responsible for the work of the independent actuarial auditing;

IV – serious error: an error that results in material inaccuracy in the calculation of the technical

provisions or in the actuarial information submitted to the SUSEP;

V – Consistency test: comparison between the established and effectively observed amounts,

for the purpose of assessing the adequacy of the amounts estimated on previous base dates;

and

VI – actuarial recalculation: recalculation of the amounts estimated or determined on previous

base dates, using updated databases or different methodologies and assumptions to those

used originally.

Continuation of CNSP Resolution nº 321, of 2015.

Section I

Minimum Requirements

Art. 100: The members responsible for the independent actuarial auditing must meet, at the

very least, the following requirements:

I – have valid registration and specific certification with the Brazilian Institute of Actuaries

(IBA);

II – have more than 3 (three) years’ experience in providing actuarial services;

III – meet the independence requirements defined in this Chapter; and

IV – meet any other requirements set out in this Resolution and in the rules to be published by

the SUSEP.

Section II

Independence Requirements

Art. 101: Any of the following situations shall be considered non-compliance with the actuarial

auditing independence requirements:

I – any case of impediment or incompatibility for the provision of independent actuarial

auditing services provided for in the IBA rules and regulations received by the SUSEP;

II – existence of a marital or family relationship, without limit to degree in direct bloodline, to

the 3rd degree in terms of a common ancestor or up to the 2nd degree in terms of affinity,

between a member responsible for the independent actuarial auditing, at a supervised body or

at any of its subsidiaries, affiliates or equivalent, and an administrator, controlling shareholder,

partner or employee who has influence over the management of the business or who is

responsible for the actuarial services at the supervised body;

III – a direct or indirect shareholding, of a member responsible for the independent actuarial

auditing, in the supervised body or at any of its subsidiaries, affiliates or equivalent;

IV – existence, on the part of a member responsible for the independent actuarial auditing, of

a direct, immediate or mediate, financial interest or substantial indirect financial interest in the

supervised body, for business dealings of any kind or the carrying out of joint ventures;

V – participation in the provision of independent actuarial auditing services, by a member

responsible for the independent actuarial auditing, at the same supervised body during the

financial year preceding the periodic replacement determined in Art. 109;

VI – existence of a member responsible for the independent actuarial auditing who has or

continues to participate in the consulting services that have provided actuarial services to the

supervised body within the last 3 (three) years; and

VII – existence of a member responsible for the independent actuarial auditing who has or has

had, within the last 2 (two) years, a direct or indirect working relationship, as an employee,

administrator or collaborator on the payroll, with the supervised body.

Continuation of CNSP Resolution nº 321, of 2015.

§ 1: At the time of hiring, the independent actuary must provide a formal declaration stating

that the services shall not be in conflict with the situations described in items I to VII, either at

the time of hiring or throughout the period the services are provided.

§ 2: Should any of the situations described, regarding subsidiaries, affiliates or equivalent, arise

in relation to the the independent actuary, it would mean the prohibition of hiring and

retaining same.

Art. 102: The provisions of this Section do not waive the need for checking, by the supervised

bodies and independent actuaries, of other situations that could affect the independence of

the actuarial auditing services.

Art. 103: Supervised bodies are forbidden to hire a responsible member of the team involved

in the work of the independent actuarial auditing for the preceding year, for a position related

to services that would be considered as impediment or incompatibility for the provision of

independent actuarial auditing services or that would make it possible to influence the

management of the supervised body.

Art. 104: The supervised body should include in the contract for the provision of independent

actuarial auditing services a clause whereby the independent actuary undertakes to deliver a

document containing his or her policy of independence, which should also be made available

to the SUSEP.

Single paragraph: The document referred to in the above clause must show, in addition to the

situations provided for in this Regulation, any others that, at the discretion of the independent

actuary, could affect his or her independence, as well as his or her adopted internal control

procedures for monitoring, identifying and avoiding such situations.

Section III

Responsibility of the Supervised Bodies

Art. 105: Should non-compliance with the requirements of this Resolution be ascertained, the

supervised body shall be held liable and the actuarial services shall be considered void, in

terms of compliance with the regulations issued by the CNSP and the SUSEP.

Art. 106: The supervised bodies must provide independent actuary with all the data,

information and conditions necessary for the effective performance of the services provided.

Art. 107: The supervised bodies should take the necessary steps to immediately replace the

independent actuary in the event that any serious errors committed in the performing of his or

her duties are detected.

Art. 108: The supervised bodies should appoint a technically responsible director to answer to

the SUSEP for the monitoring, supervision and fulfillment of the actuarial procedures provided

for in the current regulations.

Single paragraph: The technically responsible director shall be held accountable for the

information provided and the occurrence of any situations indicating fraud, negligence,

carelessness or incompetence in the performing of his or her duties, without prejudice to the

application of the penalties provided for in the prevailing legislation.

Continuation of CNSP Resolution nº 321, of 2015.

Section IV