Embed Size (px)

Citation preview

Luxembourg 04/11/2011

European Microfinance Week

MIS for MFIs

Jean POUIT

2

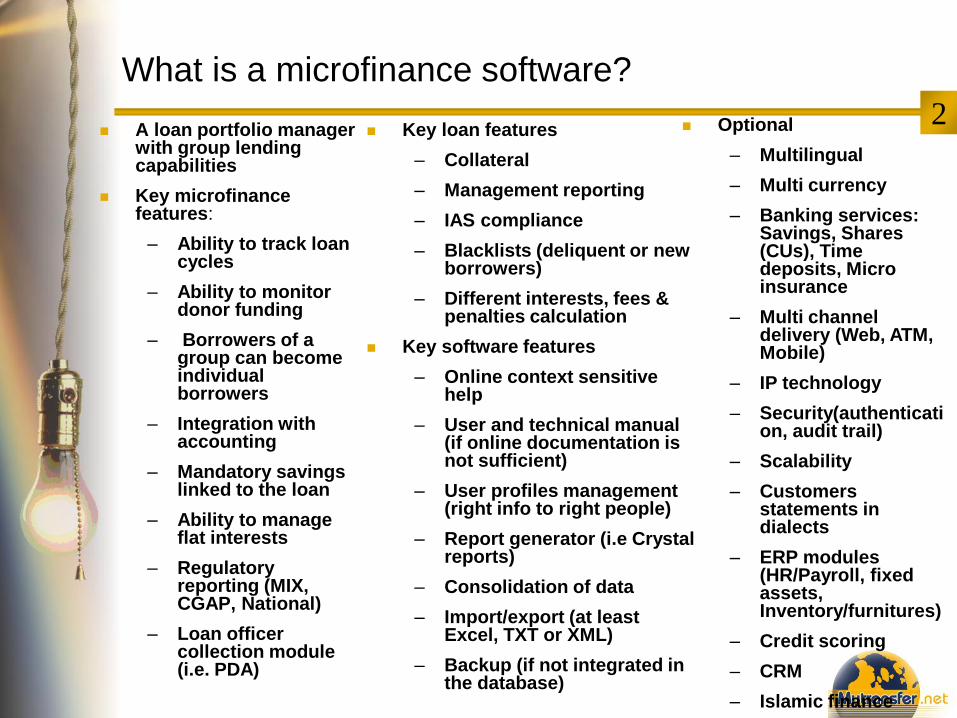

What is a microfinance software?

A loan portfolio manager with group lending capabilities

Key microfinance features:

– Ability to track loan cycles

– Ability to monitor donor funding

– Borrowers of a group can become individual borrowers

– Integration with accounting

– Mandatory savings linked to the loan

– Ability to manage flat interests

– Regulatory reporting (MIX, CGAP, National)

– Loan officer collection module (i.e. PDA)

Key loan features

– Collateral

– Management reporting

– IAS compliance

– Blacklists (deliquent or new borrowers)

– Different interests, fees & penalties calculation

Key software features

– Online context sensitive help

– User and technical manual (if online documentation is not sufficient)

– User profiles management (right info to right people)

– Report generator (i.e Crystal reports)

– Consolidation of data

– Import/export (at least Excel, TXT or XML)

– Backup (if not integrated in the database)

Optional

– Multilingual

– Multi currency

– Banking services: Savings, Shares (CUs), Time deposits, Micro insurance

– Multi channel delivery (Web, ATM, Mobile)

– IP technology

– Security(authentication, audit trail)

– Scalability

– Customers statements in dialects

– ERP modules (HR/Payroll, fixed assets, Inventory/furnitures)

– Credit scoring

– CRM

– Islamic finance

3 Table of contents

Computerization: depth and steps

The MIS selection process

Main issues to consider

The CGAP sofware reviews

4

Computerization: depth and steps

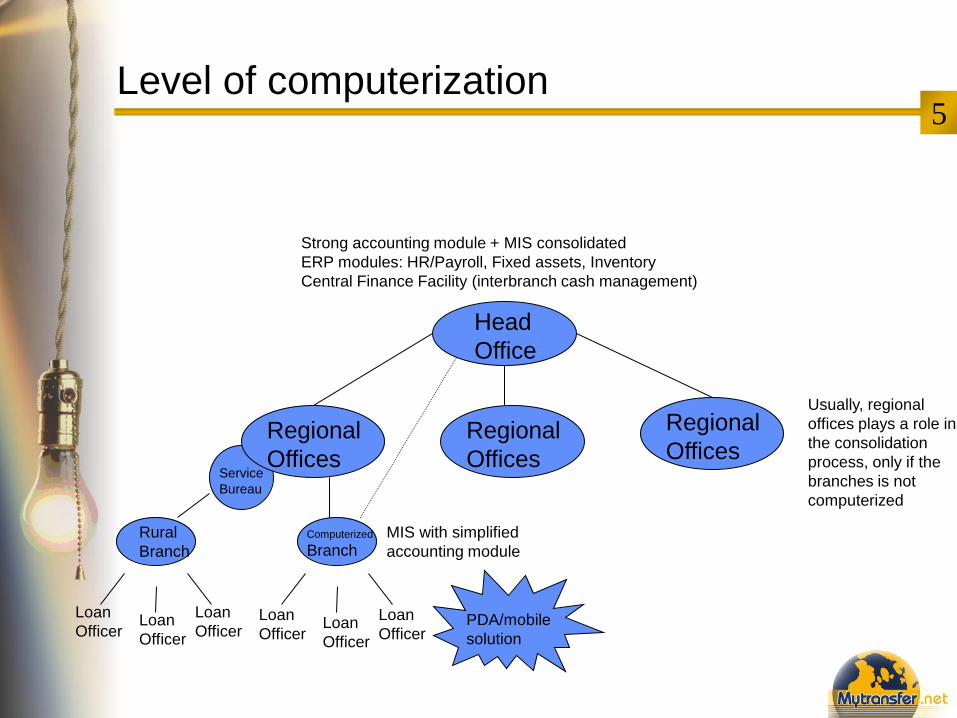

5 Level of computerization

Head

Office

Regional

Offices

Regional

Offices

Regional

Offices

Rural

Branch

Computerized

Branch

Loan

Officer Loan

Officer

Loan

Officer Loan

Officer Loan

Officer

Loan

Officer

Usually, regional

offices plays a role in

the consolidation

process, only if the

branches is not

computerized

Strong accounting module + MIS consolidated

ERP modules: HR/Payroll, Fixed assets, Inventory

Central Finance Facility (interbranch cash management)

PDA/mobile

solution

MIS with simplified

accounting module

Service

Bureau

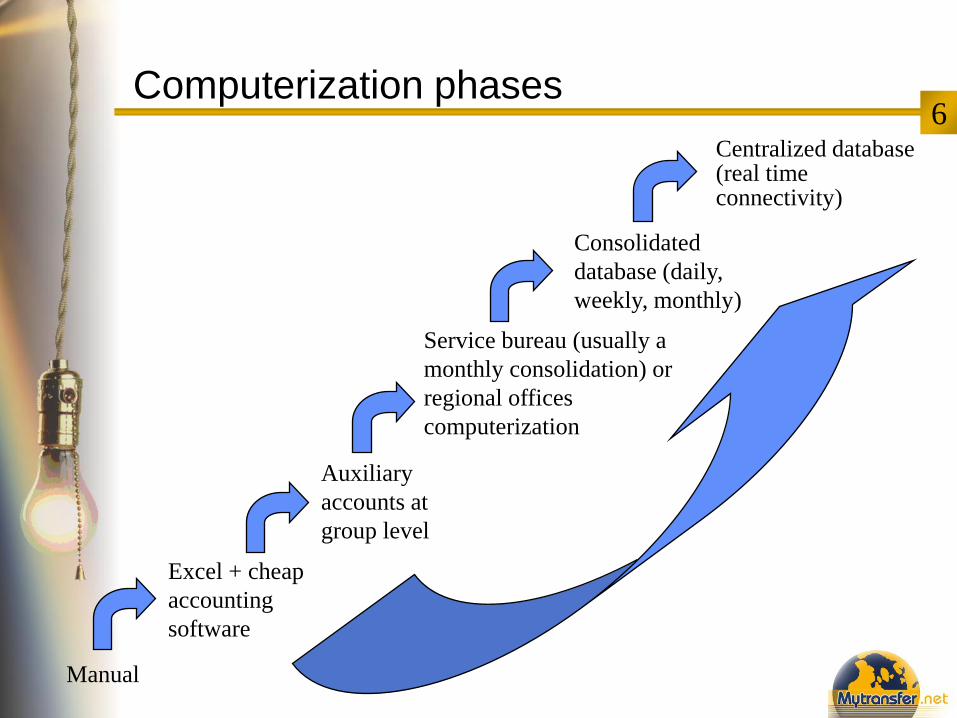

6 Computerization phases

Manual

Excel + cheap

accounting

software

Auxiliary

accounts at

group level

Service bureau (usually a

monthly consolidation) or

regional offices

computerization

Consolidated

database (daily,

weekly, monthly)

Centralized database (real time connectivity)

7

The MIS selection process

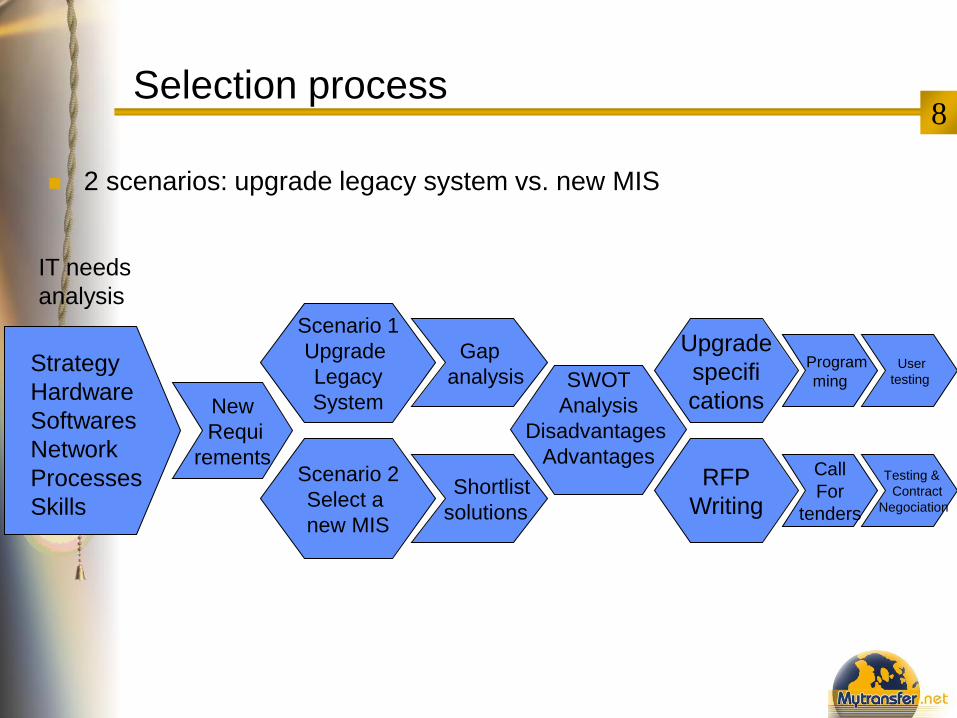

8 Selection process

2 scenarios: upgrade legacy system vs. new MIS

IT needs

analysis

Strategy

Hardware

Softwares

Network

Processes

Skills

Scenario 1

Upgrade

Legacy

System

Scenario 2

Select a

new MIS

Gap

analysis

New

Requi

rements

SWOT

Analysis

Disadvantages

Advantages

Shortlist

solutions

RFP

Writing

Upgrade

specifi

cations

Call

For

tenders

Testing &

Contract

Negociation

Program

ming User

testing

9 Recommendations on selection

Selection of criteria matrix with weighting

Licences are only 15% of the total cost of ownership: don’t forget training, installation, migration of data, user testing, change management (procedures)

Keep a B plan until the signature (don’t give a free hand to the selected provider to keep competitive pressure to negotiate customization)

Don’t transfer the last payment before at least 2 weeks after the go live (define milestones like x% at the order, y% installation, z% user acceptance)

Make sure your customized modules don’t diverge from the main version: in the short term, it seems cheaper, then in the long term, you need to pay customization again to benefit from major upgrades

10 SWOT analysis

Examples of pros and cons

Strengths Weaknesses

Opportunities Threats

Inte

rnal

Exte

rnal

-Funding available to

support the use of this MIS

-Sharing costs with another

MFI

-New regulatory

requirements not available

-Sustainability of the

provider not ensured

-Strong accounting features

-Integration accounting/loan

portfolio manager

-Not multilingual

- Not multi currency

-Scalability not demonstrated

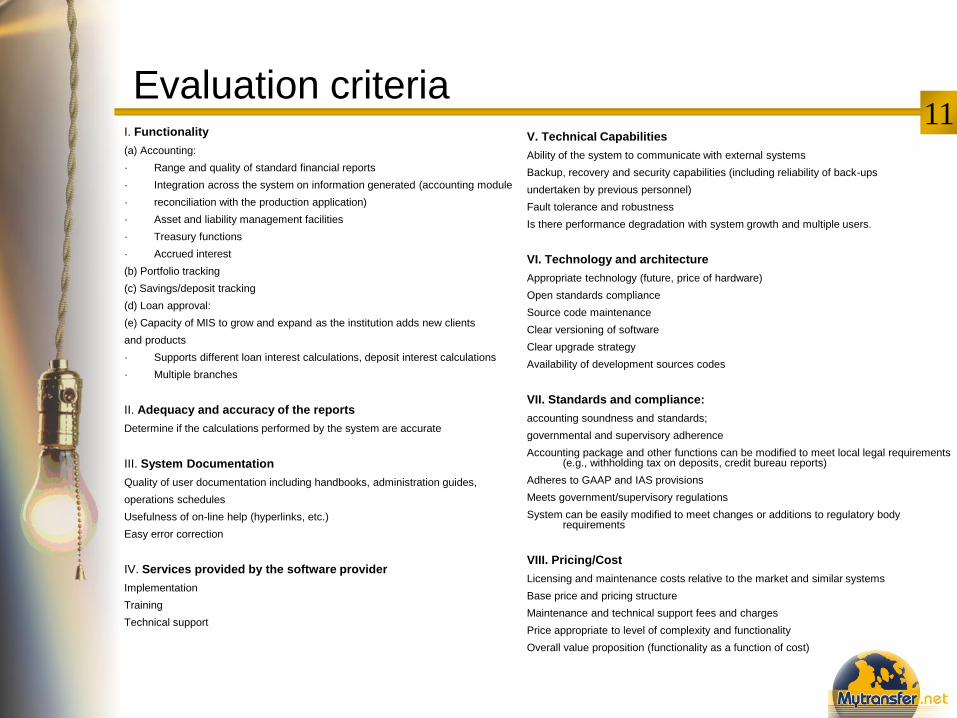

11 Evaluation criteria

I. Functionality

(a) Accounting:

· Range and quality of standard financial reports

· Integration across the system on information generated (accounting module

· reconciliation with the production application)

· Asset and liability management facilities

· Treasury functions

· Accrued interest

(b) Portfolio tracking

(c) Savings/deposit tracking

(d) Loan approval:

(e) Capacity of MIS to grow and expand as the institution adds new clients

and products

· Supports different loan interest calculations, deposit interest calculations

· Multiple branches

II. Adequacy and accuracy of the reports

Determine if the calculations performed by the system are accurate

III. System Documentation

Quality of user documentation including handbooks, administration guides,

operations schedules

Usefulness of on-line help (hyperlinks, etc.)

Easy error correction

IV. Services provided by the software provider

Implementation

Training

Technical support

V. Technical Capabilities

Ability of the system to communicate with external systems

Backup, recovery and security capabilities (including reliability of back-ups

undertaken by previous personnel)

Fault tolerance and robustness

Is there performance degradation with system growth and multiple users.

VI. Technology and architecture

Appropriate technology (future, price of hardware)

Open standards compliance

Source code maintenance

Clear versioning of software

Clear upgrade strategy

Availability of development sources codes

VII. Standards and compliance:

accounting soundness and standards;

governmental and supervisory adherence

Accounting package and other functions can be modified to meet local legal requirements (e.g., withholding tax on deposits, credit bureau reports)

Adheres to GAAP and IAS provisions

Meets government/supervisory regulations

System can be easily modified to meet changes or additions to regulatory body requirements

VIII. Pricing/Cost

Licensing and maintenance costs relative to the market and similar systems

Base price and pricing structure

Maintenance and technical support fees and charges

Price appropriate to level of complexity and functionality

Overall value proposition (functionality as a function of cost)

12 Comparison

0

1

2

3

4Functionalities

Ease of use

ReportingServices

Technology

Sigma

Banker Realms

TMS Microfit

Abacus

13

Main issues to consider

14 Main issues

Consolidation of data

Integration between loan portfolio manager and accounting

Customization of reports

Security

Interests calculation

15 Consolidation

Copy of pre-filled formats

Sending floppies/backup cartridges/CD/USB keys & mails (flat file interface)

Automated interface, Synchronization, replication of data (full or partial)

Centralized database requires efficient connectivity for real time update

16 Integration

Accounting module: 15 accounts at branch level versus ERP needs (payroll, assets, inventory, central finance facility) at HO level

Totals by product (capital, interests, fees, penalties) to generate automatic entries

17 Customization of reports

Set of predefined reports

Reports generator like Crystal reports/BO

2 skills required:

– Knowledge of data model

– Ability to write SQL extracts

18 Security

Availability: backup policy, hot restart

Integrity of data: no direct access to data, good database technology, no inconsistencies (fault tolerance, UPS)

Confidentiality: authentication, right information delivered to the right people through user management

Accountability: audit trail, personal password changed regularly

19 Interests calculation

Installments, capital (or principal) and interests are fixed or increasing, decreasing

Penalties can have a grace period but also a grace amount and be a flat amount or a %

Many MFIs prefer to avoid day-to-day calculation of interests, less profitable than flat interests

20

The CGAP software reviews

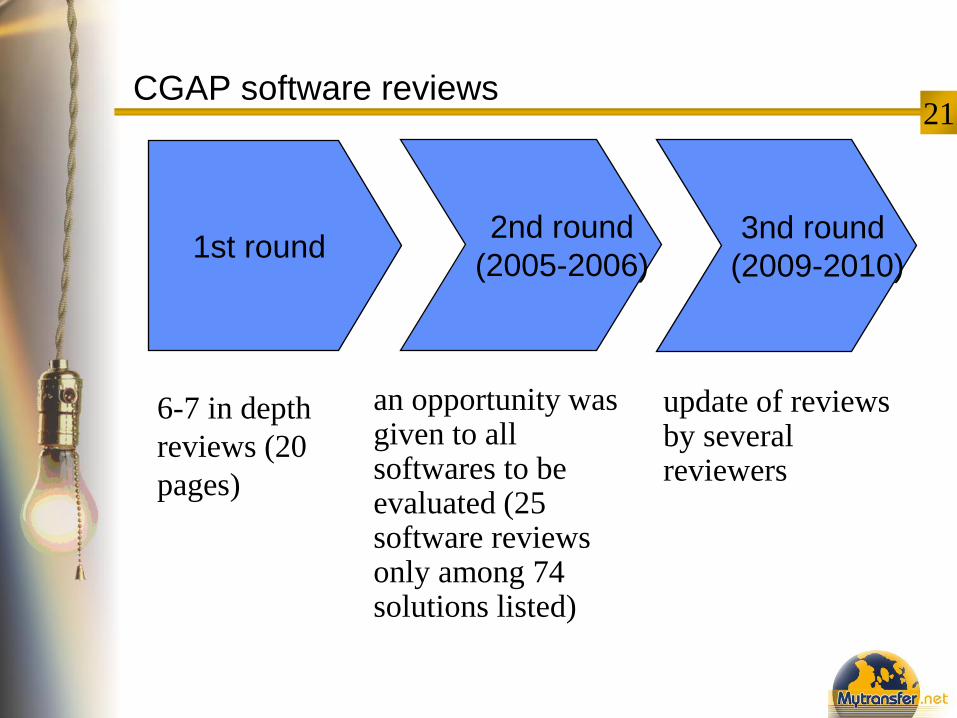

21 CGAP software reviews

1st round 2nd round

(2005-2006)

3nd round

(2009-2010)

6-7 in depth

reviews (20

pages)

an opportunity was given to all softwares to be evaluated (25 software reviews only among 74 solutions listed)

update of reviews by several reviewers

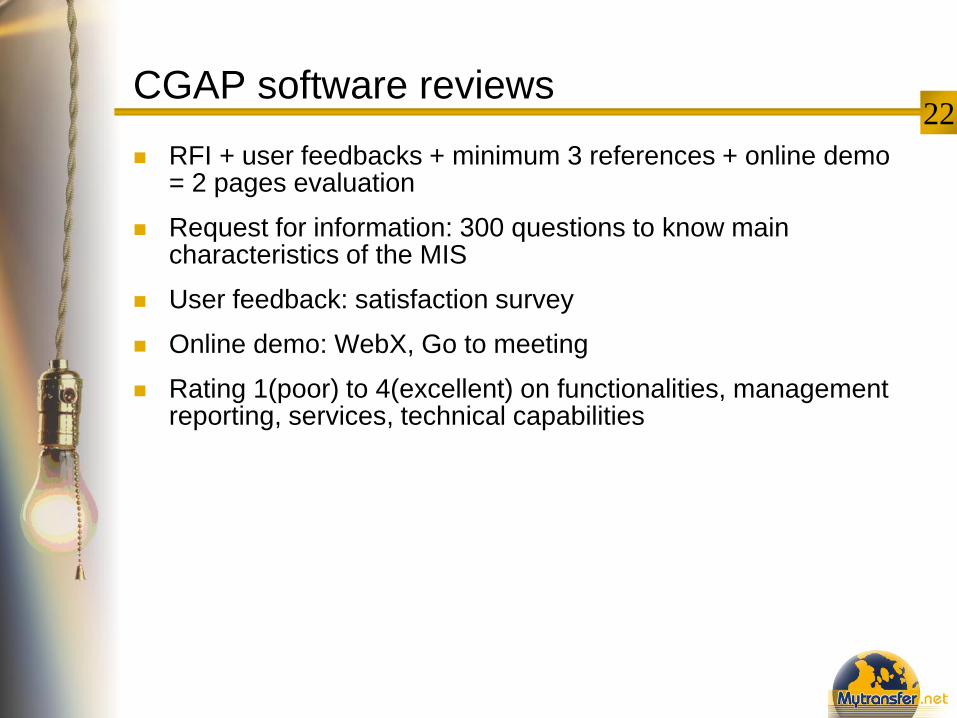

22 CGAP software reviews

RFI + user feedbacks + minimum 3 references + online demo = 2 pages evaluation

Request for information: 300 questions to know main characteristics of the MIS

User feedback: satisfaction survey

Online demo: WebX, Go to meeting

Rating 1(poor) to 4(excellent) on functionalities, management reporting, services, technical capabilities

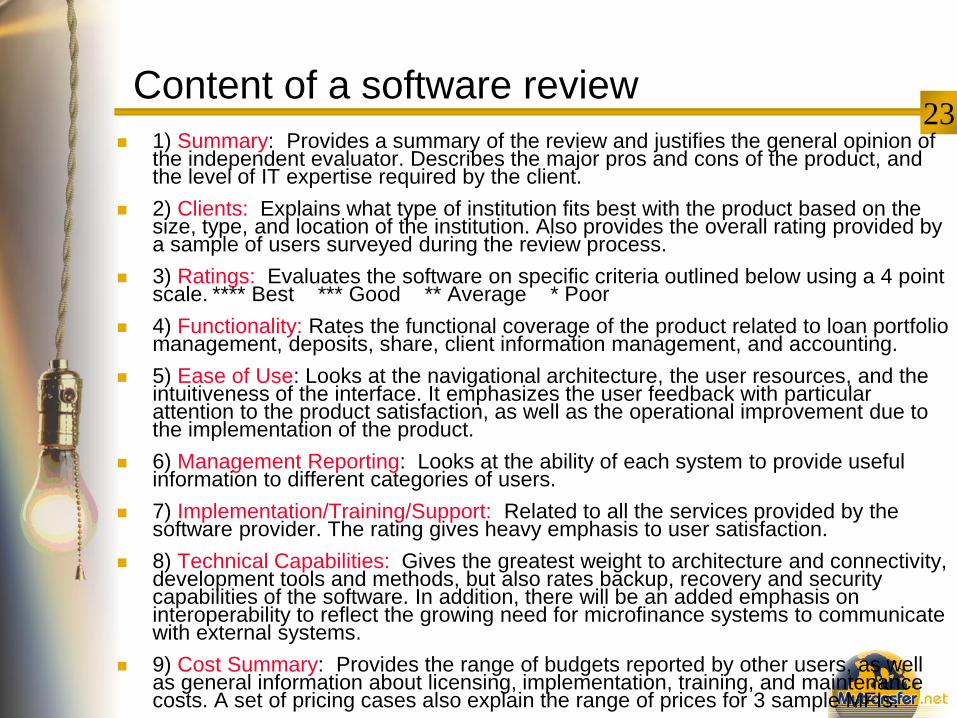

23 Content of a software review

1) Summary: Provides a summary of the review and justifies the general opinion of the independent evaluator. Describes the major pros and cons of the product, and the level of IT expertise required by the client.

2) Clients: Explains what type of institution fits best with the product based on the size, type, and location of the institution. Also provides the overall rating provided by a sample of users surveyed during the review process.

3) Ratings: Evaluates the software on specific criteria outlined below using a 4 point scale. **** Best *** Good ** Average * Poor

4) Functionality: Rates the functional coverage of the product related to loan portfolio management, deposits, share, client information management, and accounting.

5) Ease of Use: Looks at the navigational architecture, the user resources, and the intuitiveness of the interface. It emphasizes the user feedback with particular attention to the product satisfaction, as well as the operational improvement due to the implementation of the product.

6) Management Reporting: Looks at the ability of each system to provide useful information to different categories of users.

7) Implementation/Training/Support: Related to all the services provided by the software provider. The rating gives heavy emphasis to user satisfaction.

8) Technical Capabilities: Gives the greatest weight to architecture and connectivity, development tools and methods, but also rates backup, recovery and security capabilities of the software. In addition, there will be an added emphasis on interoperability to reflect the growing need for microfinance systems to communicate with external systems.

9) Cost Summary: Provides the range of budgets reported by other users, as well as general information about licensing, implementation, training, and maintenance costs. A set of pricing cases also explain the range of prices for 3 sample MFIs.

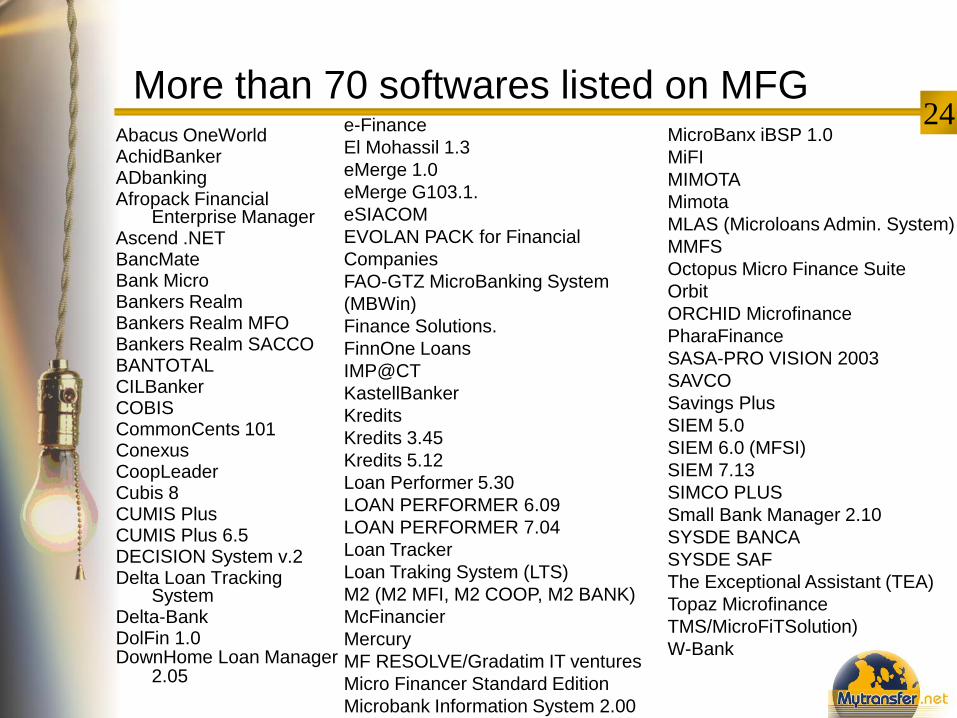

24 More than 70 softwares listed on MFG

Abacus OneWorld AchidBanker ADbanking Afropack Financial

Enterprise Manager Ascend .NET BancMate Bank Micro Bankers Realm Bankers Realm MFO Bankers Realm SACCO BANTOTAL CILBanker COBIS CommonCents 101 Conexus CoopLeader Cubis 8 CUMIS Plus CUMIS Plus 6.5 DECISION System v.2 Delta Loan Tracking

System Delta-Bank DolFin 1.0 DownHome Loan Manager

2.05

e-Finance

El Mohassil 1.3

eMerge 1.0

eMerge G103.1.

eSIACOM

EVOLAN PACK for Financial

Companies

FAO-GTZ MicroBanking System

(MBWin)

Finance Solutions.

FinnOne Loans

IMP@CT

KastellBanker

Kredits

Kredits 3.45

Kredits 5.12

Loan Performer 5.30

LOAN PERFORMER 6.09

LOAN PERFORMER 7.04

Loan Tracker

Loan Traking System (LTS)

M2 (M2 MFI, M2 COOP, M2 BANK)

McFinancier

Mercury

MF RESOLVE/Gradatim IT ventures

Micro Financer Standard Edition

Microbank Information System 2.00

MicroBanx iBSP 1.0

MiFI

MIMOTA

Mimota

MLAS (Microloans Admin. System)

MMFS

Octopus Micro Finance Suite

Orbit

ORCHID Microfinance

PharaFinance

SASA-PRO VISION 2003

SAVCO

Savings Plus

SIEM 5.0

SIEM 6.0 (MFSI)

SIEM 7.13

SIMCO PLUS

Small Bank Manager 2.10

SYSDE BANCA

SYSDE SAF

The Exceptional Assistant (TEA)

Topaz Microfinance

TMS/MicroFiTSolution)

W-Bank

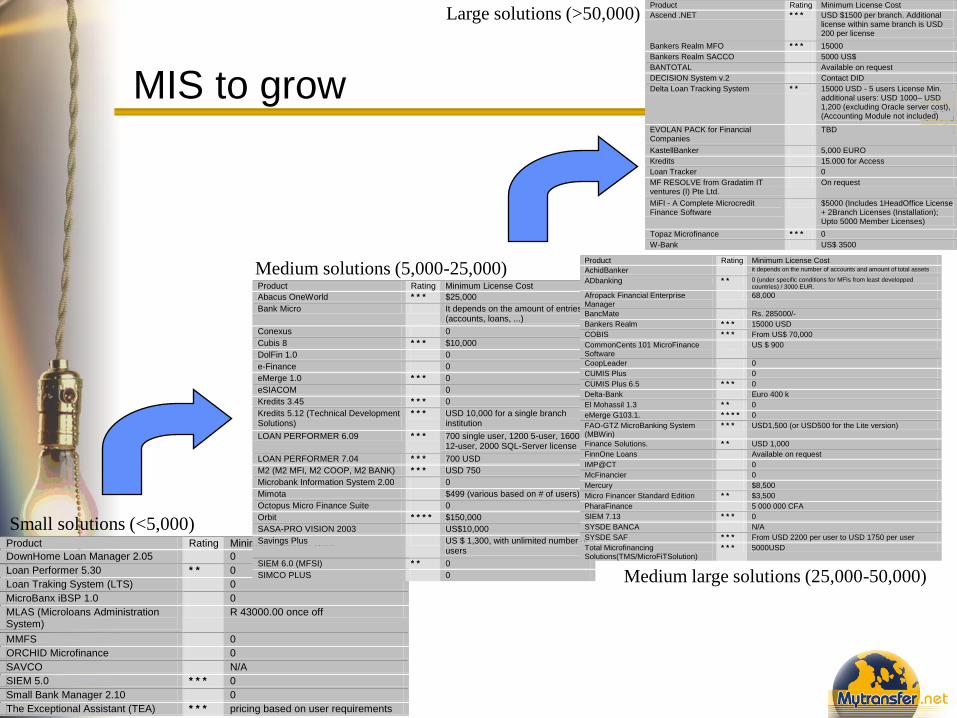

25 MIS to grow

Product Rating Minimum License Cost

Ascend .NET * * * USD $1500 per branch. Additional license within same branch is USD 200 per license

Bankers Realm MFO * * * 15000

Bankers Realm SACCO 5000 US$

BANTOTAL Available on request

DECISION System v.2 Contact DID

Delta Loan Tracking System * * 15000 USD - 5 users License Min. additional users: USD 1000– USD 1,200 (excluding Oracle server cost), (Accounting Module not included)

EVOLAN PACK for Financial Companies

TBD

KastellBanker 5,000 EURO

Kredits 15.000 for Access

Loan Tracker 0

MF RESOLVE from Gradatim IT ventures (I) Pte Ltd.

On request

MiFI - A Complete Microcredit Finance Software

$5000 (Includes 1HeadOffice License + 2Branch Licenses (Installation); Upto 5000 Member Licenses)

Topaz Microfinance * * * 0

W-Bank US$ 3500

Product Rating Minimum License Cost

DownHome Loan Manager 2.05 0

Loan Performer 5.30 * * 0

Loan Traking System (LTS) 0

MicroBanx iBSP 1.0 0

MLAS (Microloans Administration System)

R 43000.00 once off

MMFS 0

ORCHID Microfinance 0

SAVCO N/A

SIEM 5.0 * * * 0

Small Bank Manager 2.10 0

The Exceptional Assistant (TEA) * * * pricing based on user requirements

Large solutions (>50,000)

Product Rating Minimum License Cost

Abacus OneWorld * * * $25,000

Bank Micro It depends on the amount of entries (accounts, loans, ...)

Conexus 0

Cubis 8 * * * $10,000

DolFin 1.0 0

e-Finance 0

eMerge 1.0 * * * 0

eSIACOM 0

Kredits 3.45 * * * 0

Kredits 5.12 (Technical Development Solutions)

* * * USD 10,000 for a single branch institution

LOAN PERFORMER 6.09 * * * 700 single user, 1200 5-user, 1600 12-user, 2000 SQL-Server license

LOAN PERFORMER 7.04 * * * 700 USD

M2 (M2 MFI, M2 COOP, M2 BANK) * * * USD 750

Microbank Information System 2.00 0

Mimota $499 (various based on # of users)

Octopus Micro Finance Suite 0

Orbit * * * * $150,000

SASA-PRO VISION 2003 US$10,000

Savings Plus US $ 1,300, with unlimited number of users

SIEM 6.0 (MFSI) * * 0

SIMCO PLUS 0

Small solutions (<5,000)

Medium solutions (5,000-25,000) Product Rating Minimum License Cost

AchidBanker it depends on the number of accounts and amount of total assets

ADbanking * * 0 (under specific conditions for MFIs from least developped countries) / 3000 EUR.

Afropack Financial Enterprise Manager

68,000

BancMate Rs. 285000/-

Bankers Realm * * * 15000 USD

COBIS * * * From US$ 70,000

CommonCents 101 MicroFinance Software

US $ 900

CoopLeader 0

CUMIS Plus 0

CUMIS Plus 6.5 * * * 0

Delta-Bank Euro 400 k

El Mohassil 1.3 * * 0

eMerge G103.1. * * * * 0

FAO-GTZ MicroBanking System (MBWin)

* * * USD1,500 (or USD500 for the Lite version)

Finance Solutions. * * USD 1,000

FinnOne Loans Available on request

IMP@CT 0

McFinancier 0

Mercury $8,500

Micro Financer Standard Edition * * $3,500

PharaFinance 5 000 000 CFA

SIEM 7.13 * * * 0

SYSDE BANCA N/A

SYSDE SAF * * * From USD 2200 per user to USD 1750 per user

Total Microfinancing Solutions(TMS/MicroFiTSolution)

* * * 5000USD

Medium large solutions (25,000-50,000)

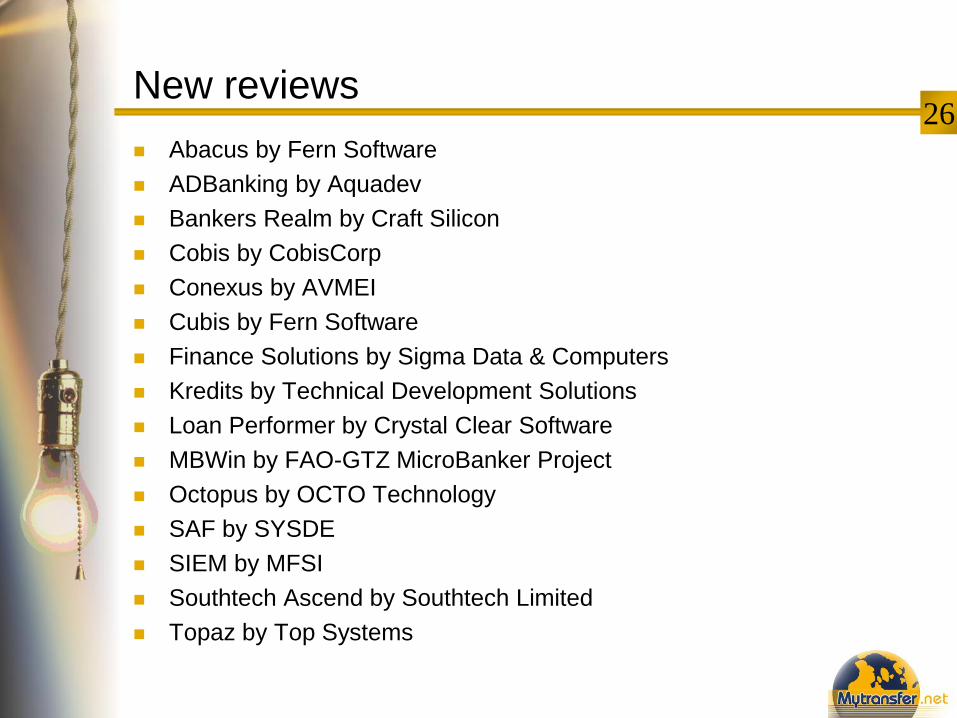

26 New reviews

Abacus by Fern Software

ADBanking by Aquadev

Bankers Realm by Craft Silicon

Cobis by CobisCorp

Conexus by AVMEI

Cubis by Fern Software

Finance Solutions by Sigma Data & Computers

Kredits by Technical Development Solutions

Loan Performer by Crystal Clear Software

MBWin by FAO-GTZ MicroBanker Project

Octopus by OCTO Technology

SAF by SYSDE

SIEM by MFSI

Southtech Ascend by Southtech Limited

Topaz by Top Systems

27

Thank you for your attention !

Jean POUIT, Executive Director & founder MyTransfer (Luxembourg)

email [email protected]

Mobile: +31 623704102 Skype:simbajp

Contact information