Embed Size (px)

Citation preview

Money and Milestones: Financial Behavior, Debt and Early Life Transitions

1

Rachel E. Dwyer, Randy Hodson, Michael Nau Department of Sociology Ohio State University

Supported by a grant from the Na4onal Endowment for Financial Educa4on

Millenials

Variable pathways to adulthood.

Middle class squeeze

US system of

financed attainment

National Longitudinal Survey of Youth 1997 Cohort

Born around 1981 Oldest Millenials

Come of age in the 2000s.

Interviewed every year since 1997 teenagers- late 20s

Agenda for today

• Overview of debt in the transition to adulthood

• Focus on student loans, the most distinctive

youth debt

• Close with reflections on the institutional context of youth financial decision-making

DEBT ACCRUAL IS LINKED TO ADULT MILESTONES

5

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

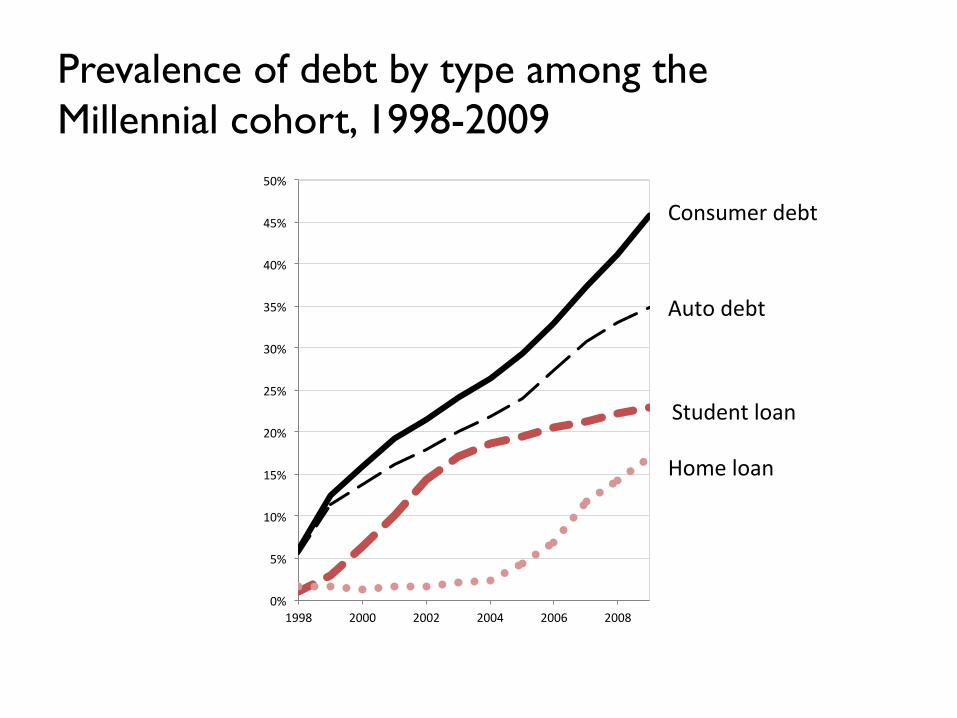

1998 2000 2002 2004 2006 2008

Consumer debt

Auto debt

Student loan

Home loan

Prevalence of debt by type among the Millennial cohort, 1998-2009

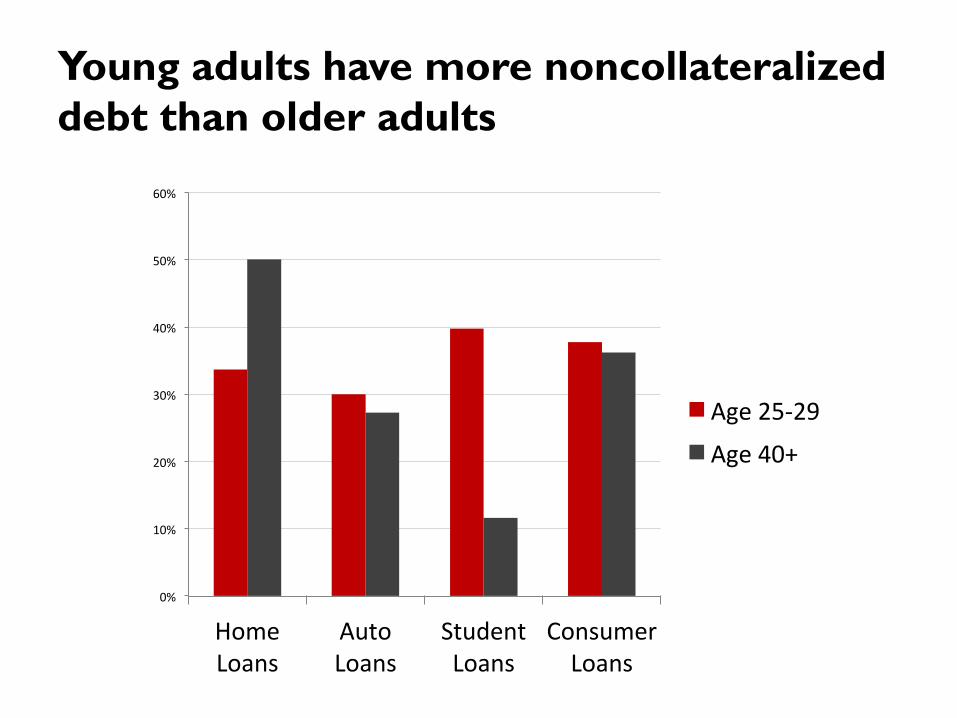

Young adults have more noncollateralized debt than older adults

0%

10%

20%

30%

40%

50%

60%

Home Loans

Auto Loans

Student Loans

Consumer Loans

Age 25-‐29

Age 40+

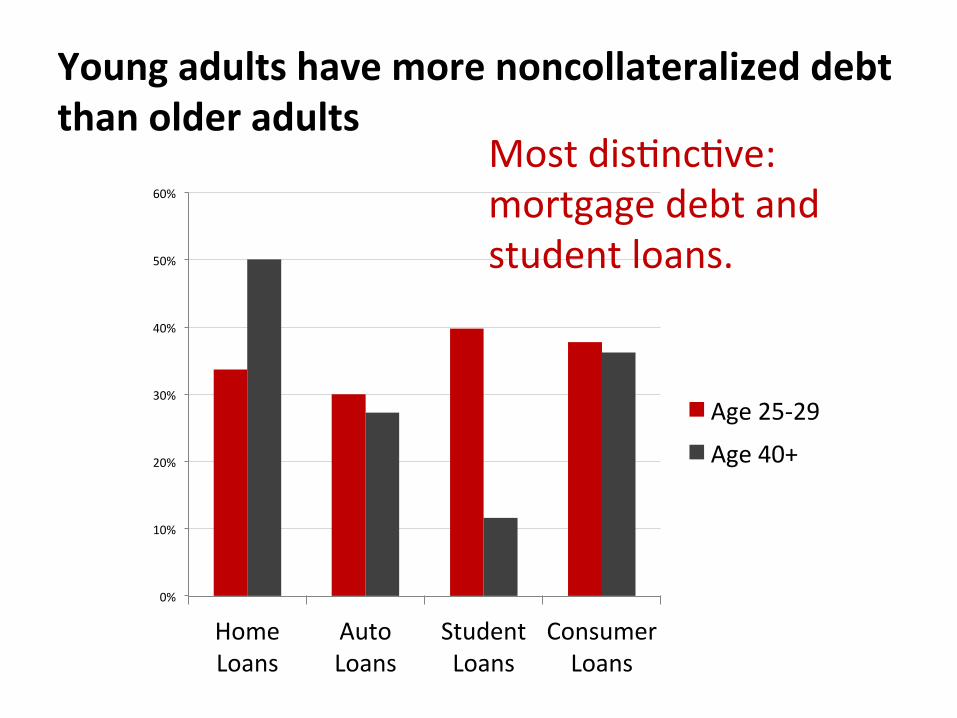

Young adults have more noncollateralized debt than older adults

0%

10%

20%

30%

40%

50%

60%

Home Loans

Auto Loans

Student Loans

Consumer Loans

Age 25-‐29

Age 40+

Most dis4nc4ve: mortgage debt and student loans.

WHAT IS THE RELATIONSHIP BETWEEN DEBT ACCRUAL AND ADULT MILESTONES?

9

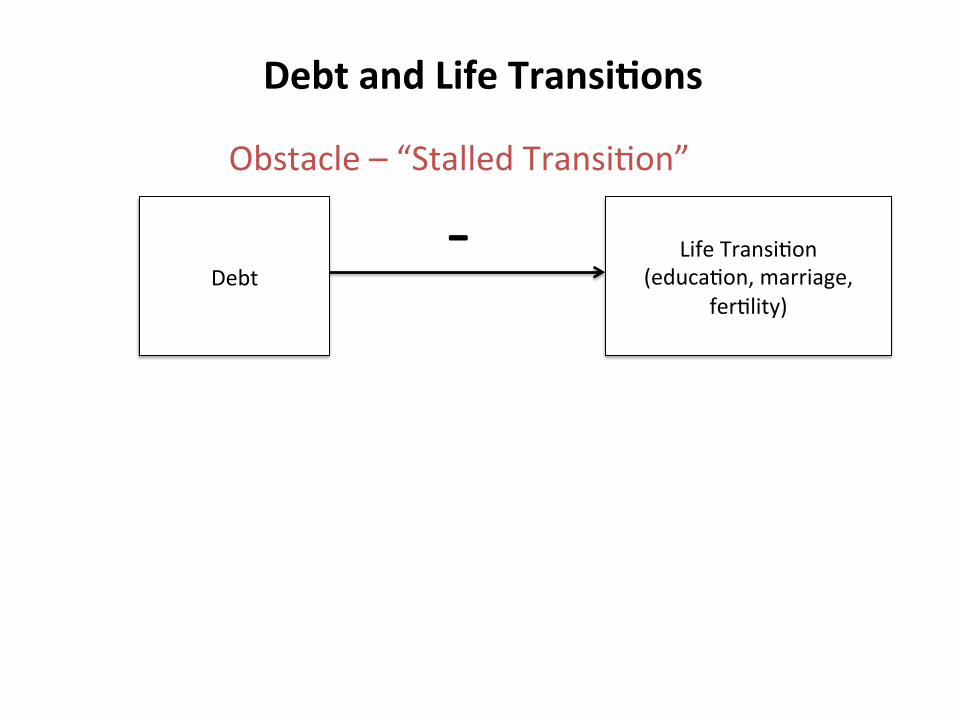

Debt and Life Transi9ons

Life Transi4on (educa4on, marriage,

fer4lity)

Debt An4cipated/Desired Transi4on

+-‐

Facilitator – “Financing Family Forma4on”

Debt

Life Transi4on (educa4on, marriage,

fer4lity)

Obstacle – “Stalled Transi4on”

+

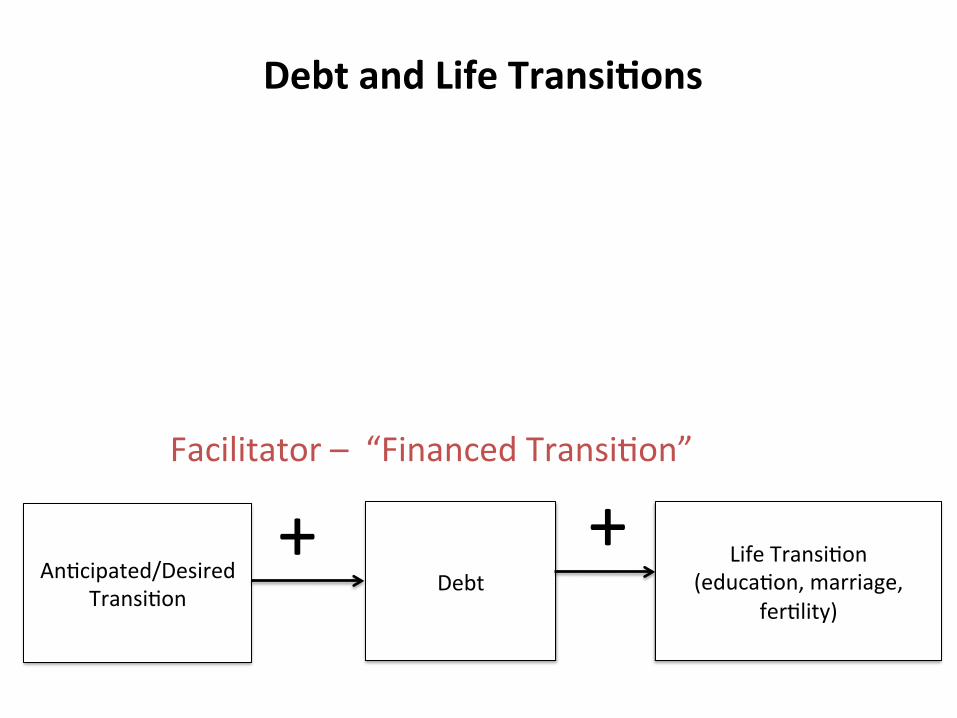

Debt and Life Transi9ons

Life Transi4on (educa4on, marriage,

fer4lity)

Debt An4cipated/Desired Transi4on

+-‐

Facilitator – “Financed Transi4on”

Debt

Life Transi4on (educa4on, marriage,

fer4lity)

Obstacle – “Stalled Transi4on”

+

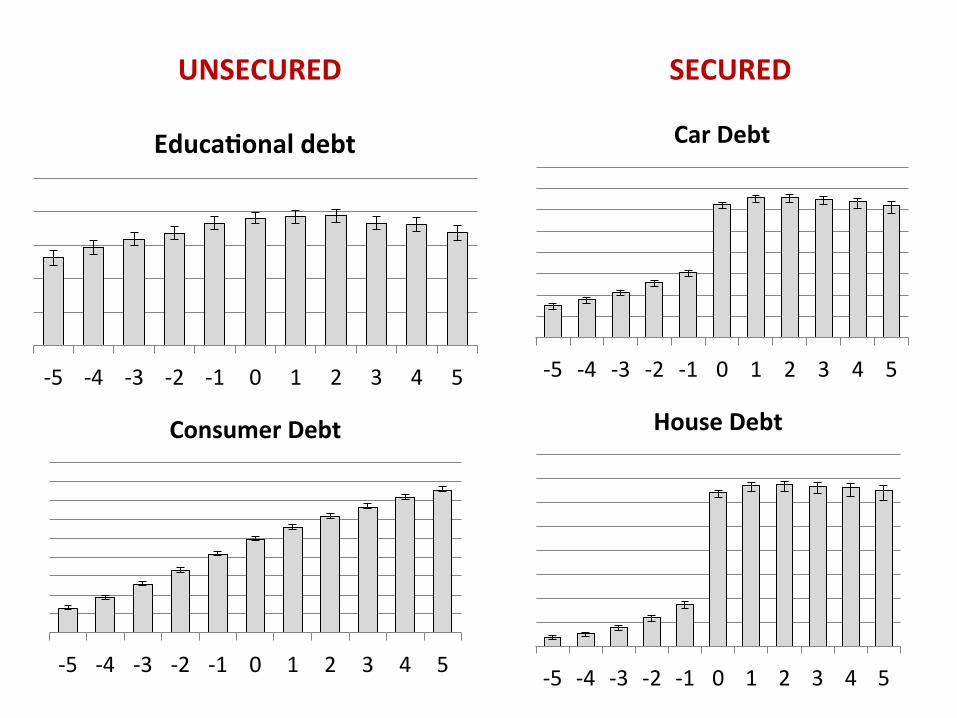

Opportunity + risk à Debt can be a resource, but also a liability

à Debt maZers more for some than others à Different debts

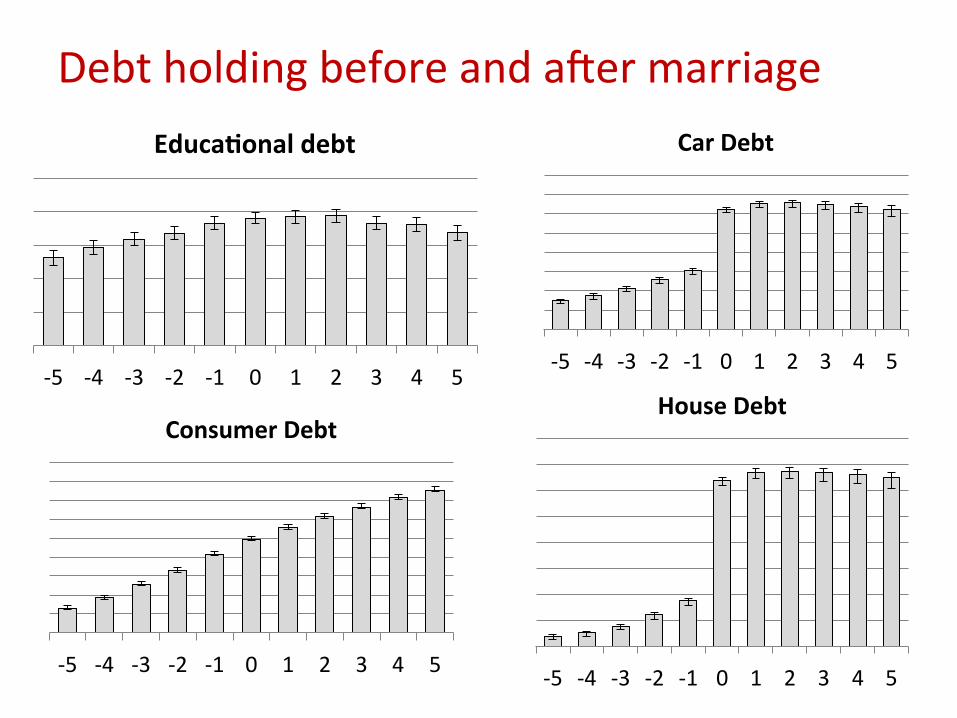

Debt holding before and a\er marriage

-‐5 -‐4 -‐3 -‐2 -‐1 0 1 2 3 4 5

Consumer Debt

-‐5 -‐4 -‐3 -‐2 -‐1 0 1 2 3 4 5

Car Debt

-‐5 -‐4 -‐3 -‐2 -‐1 0 1 2 3 4 5

House Debt -‐5 -‐4 -‐3 -‐2 -‐1 0 1 2 3 4 5

Educa9onal debt

UNSECURED SECURED

-‐5 -‐4 -‐3 -‐2 -‐1 0 1 2 3 4 5

Consumer Debt

-‐5 -‐4 -‐3 -‐2 -‐1 0 1 2 3 4 5

Car Debt

-‐5 -‐4 -‐3 -‐2 -‐1 0 1 2 3 4 5

House Debt

-‐5 -‐4 -‐3 -‐2 -‐1 0 1 2 3 4 5

Educa9onal debt

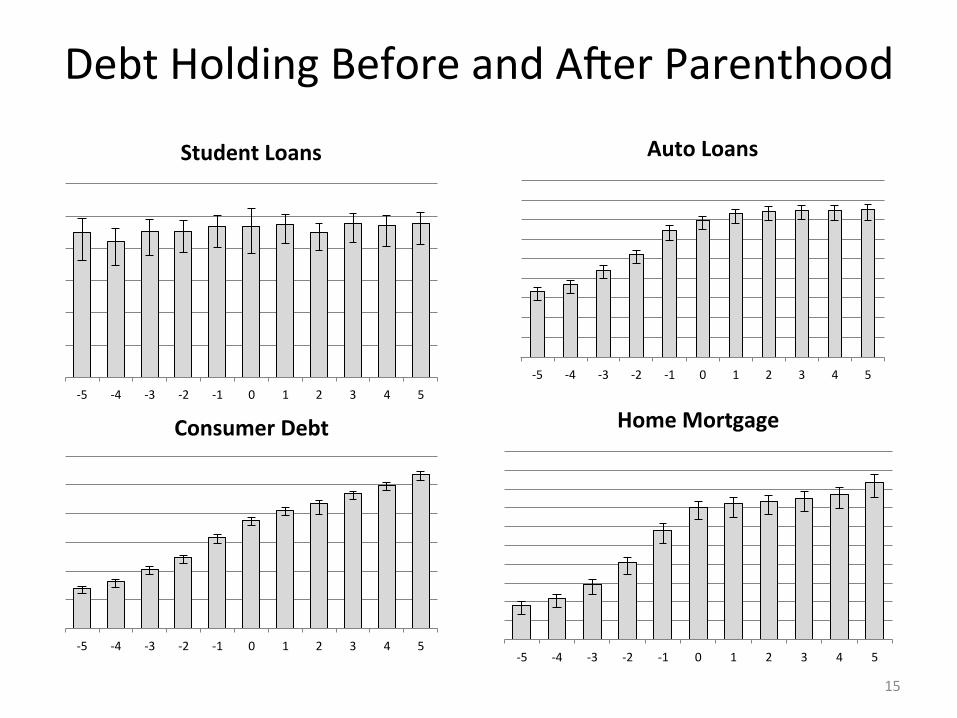

Debt Holding Before and A\er Parenthood

15

-‐5 -‐4 -‐3 -‐2 -‐1 0 1 2 3 4 5

Home Mortgage

-‐5 -‐4 -‐3 -‐2 -‐1 0 1 2 3 4 5

Auto Loans

-‐5 -‐4 -‐3 -‐2 -‐1 0 1 2 3 4 5

Consumer Debt

-‐5 -‐4 -‐3 -‐2 -‐1 0 1 2 3 4 5

Student Loans

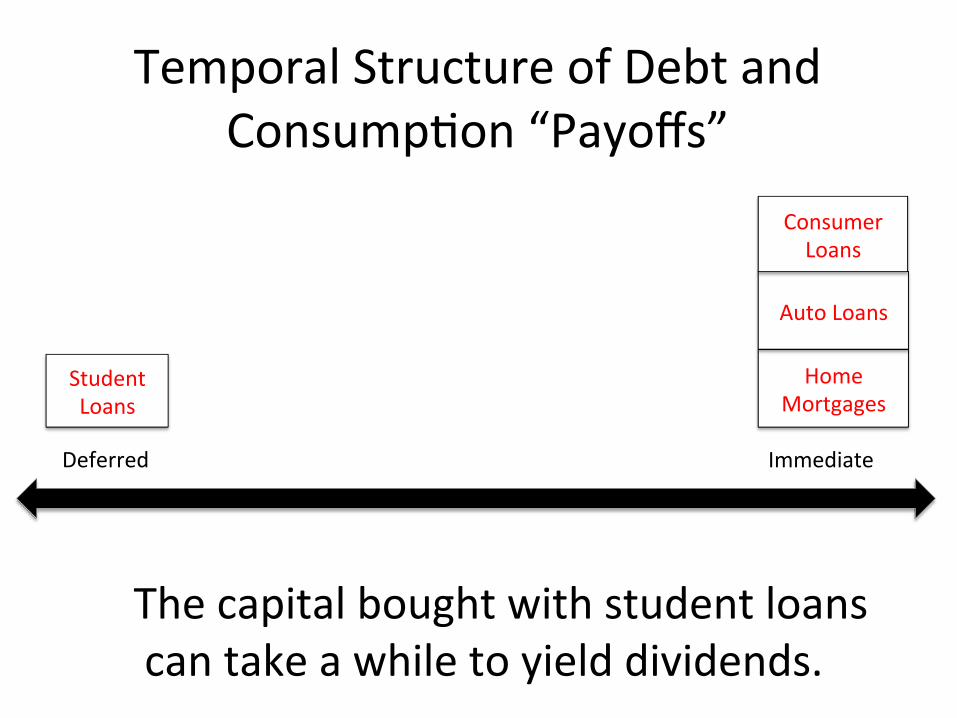

Temporal Structure of Debt and Consump4on “Payoffs”

Deferred Immediate

Home Mortgages

Auto Loans

Consumer Loans

Student Loans

The capital bought with student loans can take a while to yield dividends.

STUDENT DEBT AND TRANSITIONS: EDUCATION, MARRIAGE, AND PARENTHOOD

17

Opportunity + risk à Student loans have posi4ve or neutral consequences for many

à Student loans have nega4ve consequences for some.

Underlying vulnerabili4es, triggered in crisis.

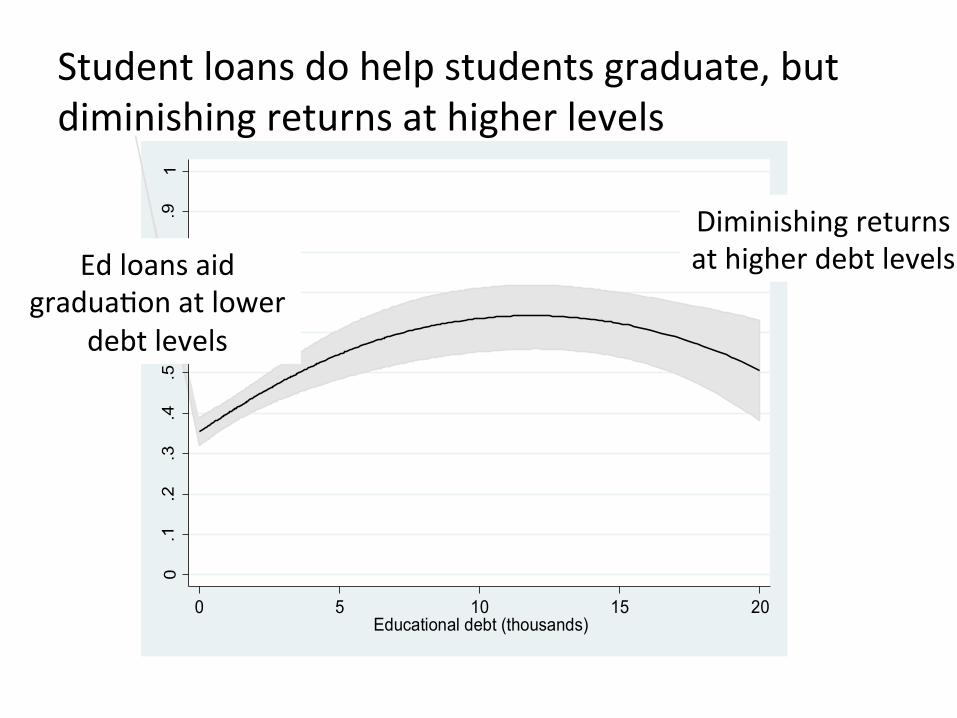

Student loans do help students graduate, but diminishing returns at higher levels

0.1

.2.3

.4.5

.6.7

.8.9

1

0 5 10 15 20Educational debt (thousands)

Ed loans aid gradua4on at lower

debt levels

Diminishing returns at higher debt levels

0%

5%

10%

15%

20%

25%

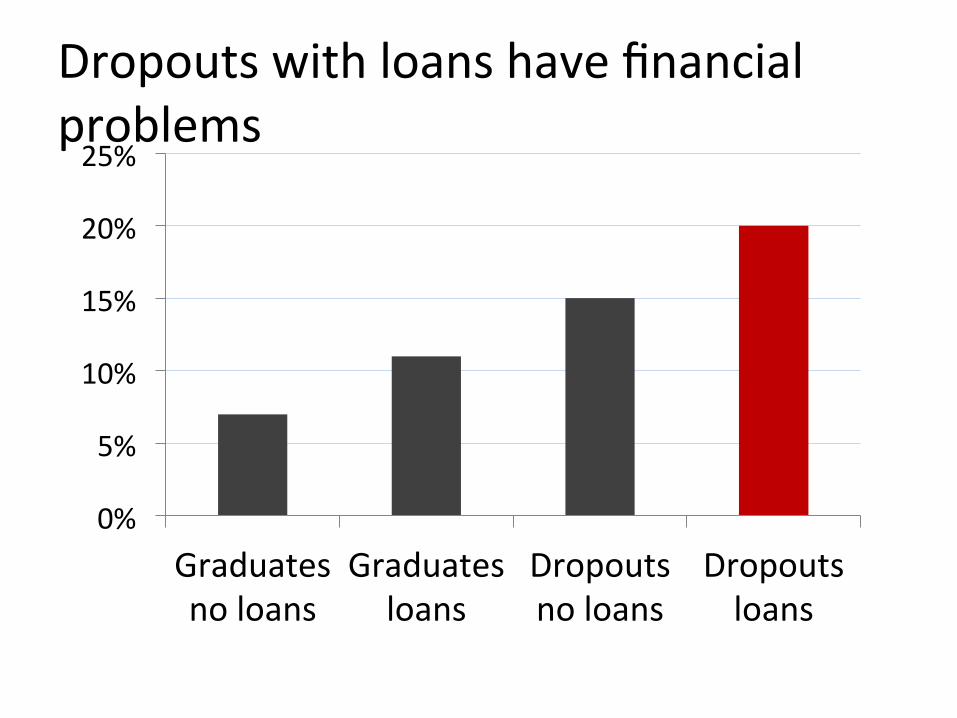

Graduates no loans

Graduates loans

Dropouts no loans

Dropouts loans

Dropouts with loans have financial problems

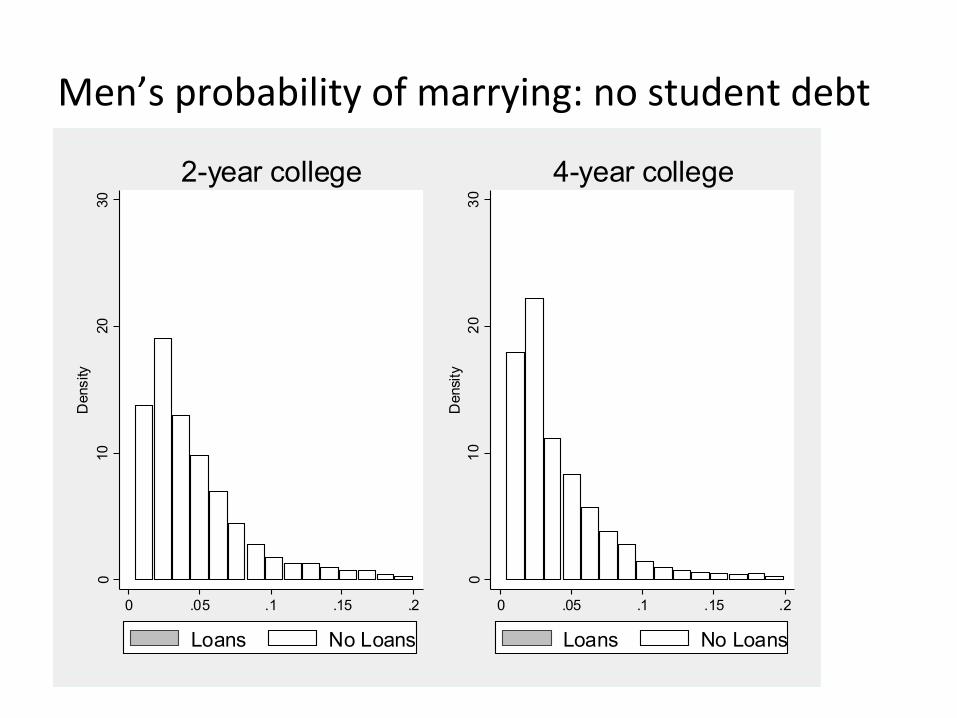

Men’s probability of marrying: no student debt 0

1020

30D

ensi

ty

0 .05 .1 .15 .2

Loans No Loans

2-year college

010

2030

Den

sity

0 .05 .1 .15 .2

Loans No Loans

4-year college

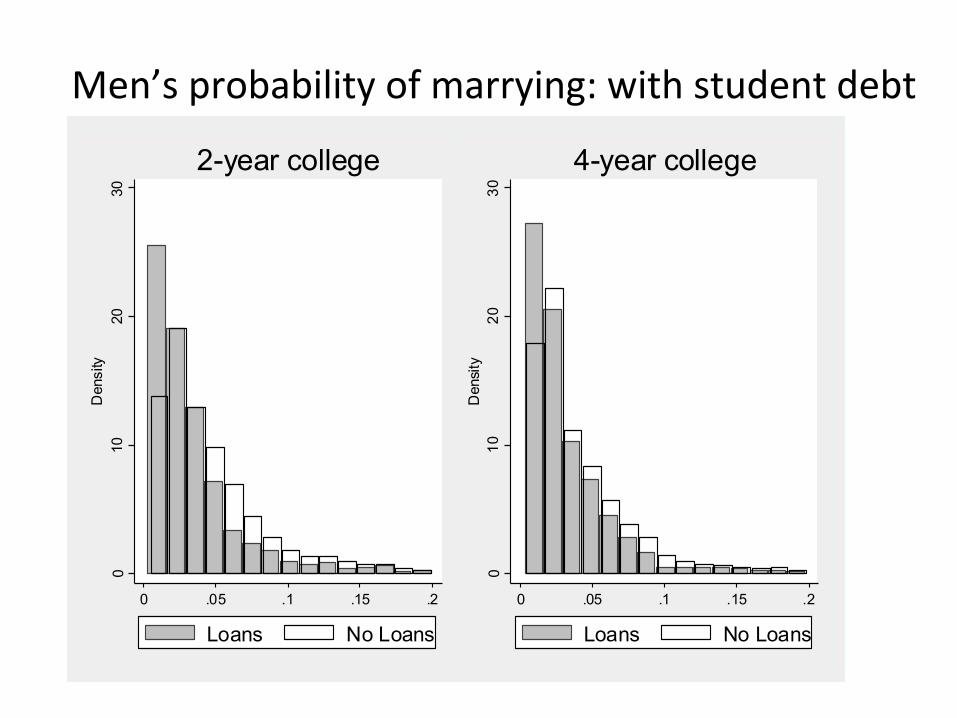

Men’s probability of marrying: with student debt 0

1020

30D

ensi

ty

0 .05 .1 .15 .2

Loans No Loans

2-year college

010

2030

Den

sity

0 .05 .1 .15 .2

Loans No Loans

4-year college

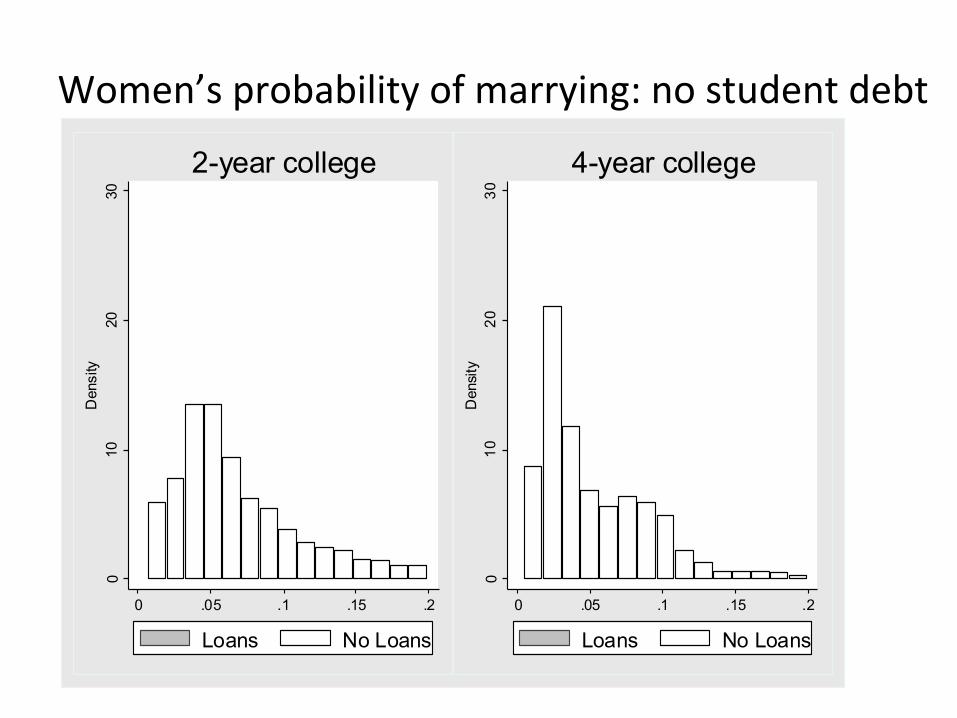

Women’s probability of marrying: no student debt 0

1020

30D

ensi

ty

0 .05 .1 .15 .2

Loans No Loans

2-year college

010

2030

Den

sity

0 .05 .1 .15 .2

Loans No Loans

4-year college

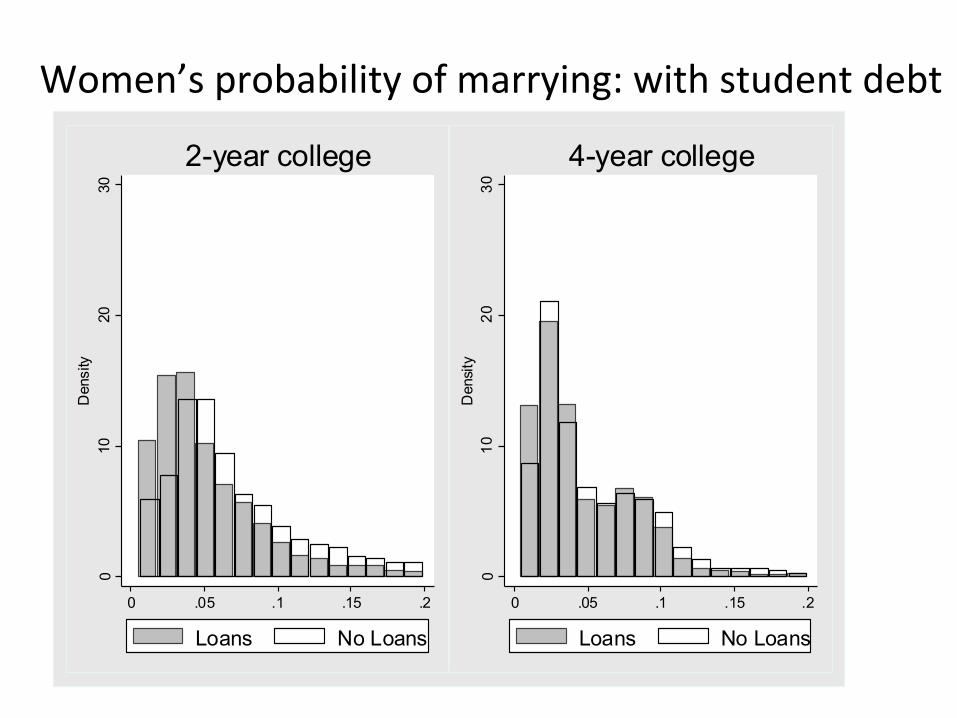

Women’s probability of marrying: with student debt 0

1020

30D

ensi

ty

0 .05 .1 .15 .2

Loans No Loans

2-year college

010

2030

Den

sity

0 .05 .1 .15 .2

Loans No Loans

4-year college

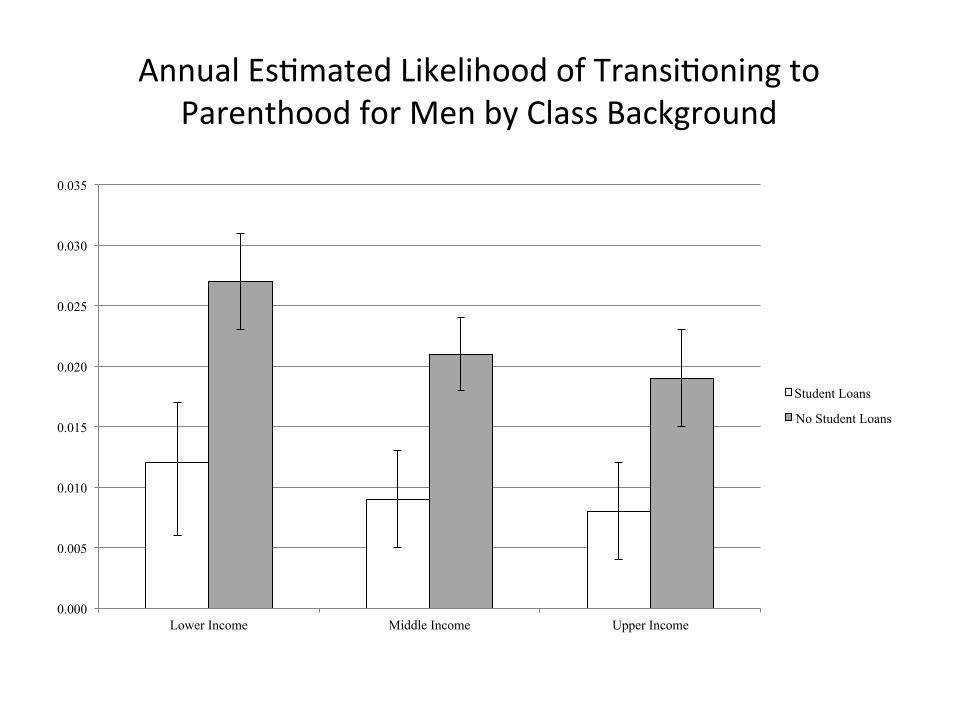

Annual Es4mated Likelihood of Transi4oning to Parenthood for Men by Class Background

0.000

0.005

0.010

0.015

0.020

0.025

0.030

0.035

Lower Income Middle Income Upper Income

Student Loans

No Student Loans

Opportunity + risk à Student loans have posi4ve or neutral consequences for many

à Student loans have nega4ve consequences for some.

Underlying vulnerabili4es, triggered in crisis.

Opportunity + risk for other forms of debt too à Mortgages in economic crisis

à Consumer credit causes anxiety, especially for middle class.

Underlying vulnerabili4es, some4mes manifested in crisis.

IF STUDENT DEBT IS A PROBLEM, WHAT KIND OF A PROBLEM IS IT?

28

These mixed effects are a necessary consequence of having a credit system embedded in our financial aid system. What is the nature of this credit system?

Student loans embody 2 different visions of attainment in uneasy tension

Market vision Collectivist vision

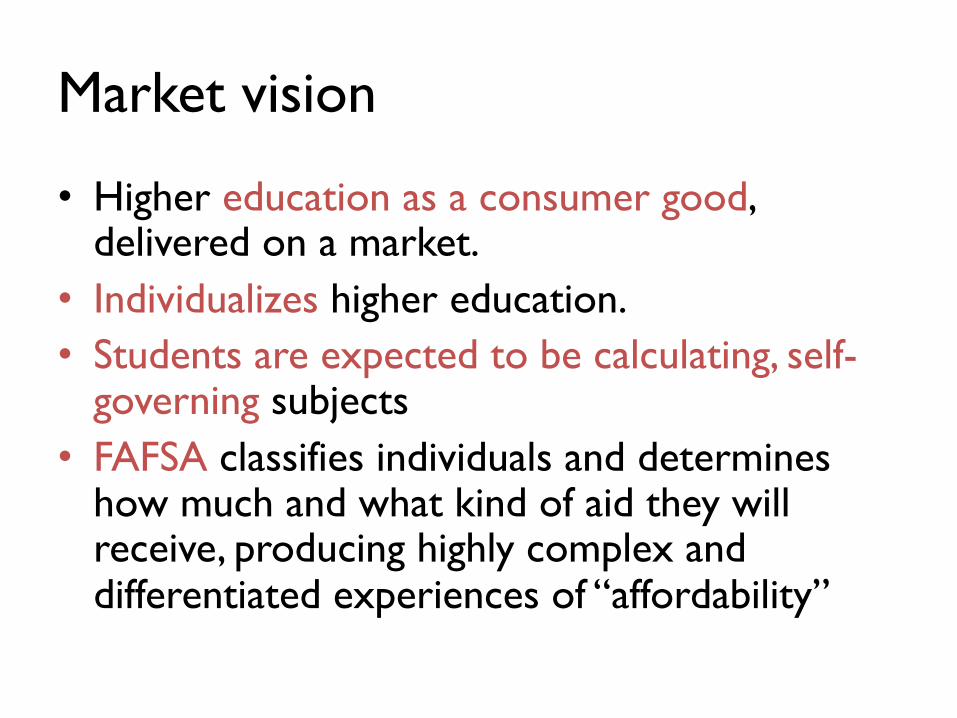

Market vision

• Higher education as a consumer good, delivered on a market.

• Individualizes higher education. • Students are expected to be calculating, self-

governing subjects • FAFSA classifies individuals and determines

how much and what kind of aid they will receive, producing highly complex and differentiated experiences of “affordability”

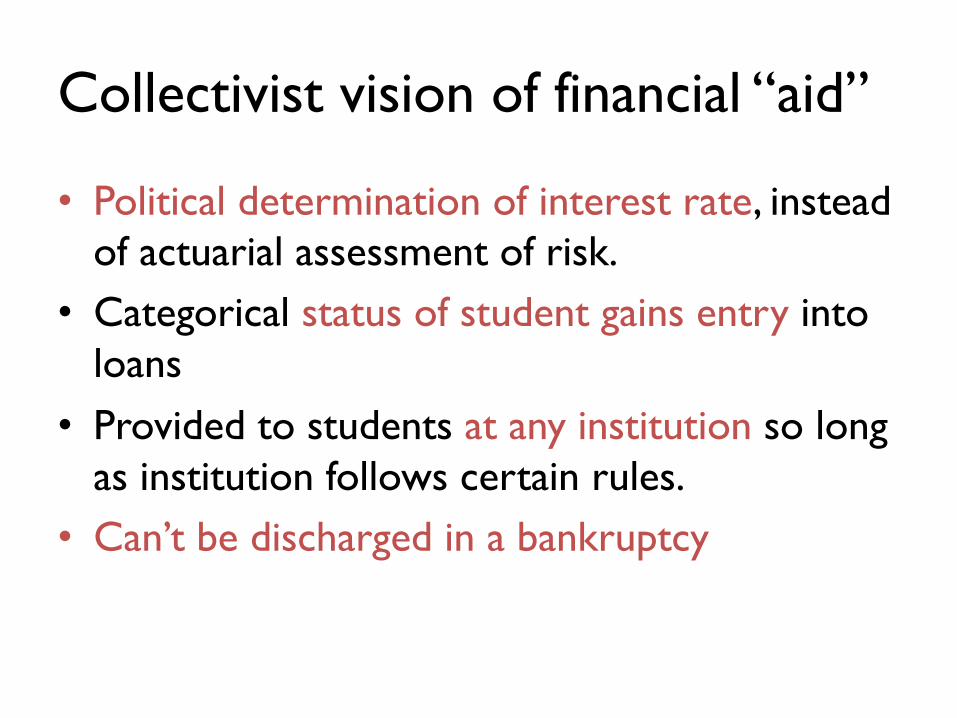

Collectivist vision of financial “aid”

• Political determination of interest rate, instead of actuarial assessment of risk.

• Categorical status of student gains entry into loans

• Provided to students at any institution so long as institution follows certain rules.

• Can’t be discharged in a bankruptcy

Tensions In the most favorable view, students benefit from both worlds. Access to credit insured by the state. In the most jaundiced view, students have the worst of both worlds. Lack the informa4on and “equity” of segmented loan markets, but must accept state limita4ons. Market failures are blamed on collec4vist system.

2 visions shape debate over policy remedies

• Market: Make loan disbursal more segmented and individualized.

• Collec4vist: Make loan repayment more collec4vist and public interest. Even get rid of loans altogether.

Back to individuals No maZer what, increases complexity and requirement of financial capability. But there are limits to what individuals can plan. Our findings suggest that an important policy goal should be to provide insurance against the risks for some.