Embed Size (px)

Citation preview

MPSC Case No.: U-16892-R Respondent: K. Krishnamurthy Requestor: MEC-1 Question No.: MEC/DE-1.7 Page: 1 of 1 Question: Refer to Exhibit A-3. Explain why total system fuel costs (in $/MMBtu)

were 6.6% higher than planned while total system fossil fuel costs increased 1.2% and nuclear fuel costs decreased 5.2%.

Answer: Please refer to Exhibit A-3 in my Direct Testimony in this Case and the

Table below.

As shown in the Table below for 2012 i) The Actual Total System - Fossil fuel cost was ₵276.7/MMBtu,

which was 1.2% above the PSCR PLAN Total System - Fossil fuel cost of ₵273.5/MMBtu.

ii) The Actual Nuclear fuel cost was ₵59.7/MMBtu, which was 5.2% below the PSCR PLAN Nuclear fuel cost of ₵63.0/MMBtu.

iii) The Actual Total System - Fossil fuel consumption (353,873,543 MBTU) was down 1.5% from the PSCR PLAN Total System - Fossil fuel consumption (359,153,837 MBTU) while the Actual Nuclear fuel consumption (55,728,746 MBTU) was down 36.8% from the PSCR PLAN Nuclear fuel consumption (88,220,000 MBTU).

iv) The Actual consumption of the significantly lower cost Nuclear fuel was 36.8% lower than PSCR PLAN and comprised a significantly lower percentage (13.6%) of the Actual Total System fuel consumption than the Nuclear fuel percentage (19.7%) of the PSCR PLAN Total System fuel consumption.

v) As a result of the significantly lower Nuclear fuel consumption, the actual Total System fuel cost of ₵247.2/MMBtu was 6.6% higher than the PSCR PLAN Total System fuel cost of ₵232.0/MMBtu.

Line (a) (b) (c) (d) (e) (f) (g) (h)

No.

1

2 PERCENTAGE DIFFERENCE

3 FUEL TYPE COST, $ MBTU ₵/MMBtu COST, $ MBTU ₵/MMBtu ACTUAL PLAN (₵/MMBtu)4

5 TOTAL SYSTEM - FOSSIL $979,275,906 353,873,543 276.7 $982,303,741 359,153,837 273.5 1.2%

6

7 NUCLEAR $33,284,081 55,728,746 59.7 $55,591,470 88,220,000 63.0 -5.2%

8

9 TOTAL SYSTEM $1,012,559,986 409,602,289 247.2 $1,037,895,211 447,373,837 232.0 6.6%

2012

ACTUAL PSCR PLAN

Direct Testimony of G. E. Sansoucy on Behalf of MEC MPSC Case No. U-16892-R - October 17, 2013 Exhibit: MEC-36 - MEC/DE-1.7 Page 1 of 1

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 242 of 873

MPSC Case No.: U-16892-R Respondent: R. E. Palmer/Legal Requestor: MEC- 3 Question No.: MEC/DE-3.39e (1) Page: 1 of 1 Question: Refer to Mr. Palmer’s direct testimony at page REP-5 and to discovery

response MEC/DE-1.20. e. For each of the units listed in MEC/DE-1.20, provide the planned and

actual capacity factor for each year from 2008 to 2012. Answer: DTE Electric objects for the reason that the information requested is not

relevant or reasonably calculated to lead to the discovery of admissible evidence in this proceeding. The requested information is for years 2008 to present, which are outside the time frame for this proceeding with the exception of year 2012 which only addressed the reasonableness and prudence of DTE Electric’s power supply costs and expenses for the 2012 PSCR Reconciliation which is the proper subject time frame of this PSCR proceeding under Act 304 pursuant to MCL 460.6j(12). Subject to such objection, and without waiver thereof, DTE Electric would answer as follows:

2012 PSCR Plan 2012 ActualWinter NDC Capacity Factor Capacity Factor

Belle River 1 (DE) 517 72% 71%Belle River 2 (DE) 517 57% 63%Fermi 2 1139 86% 51%Greenwood 785 3% 9%Harbor Beach 103 9% 8%Monroe 1 770 67% 60%Monroe 2 795 47% 51%Monroe 3 783 72% 70%Monroe 4 762 57% 48%River Rouge 2 260 57% 37%River Rouge 3 280 60% 57%St Clair 1 158 50% 45%St Clair 2 162 48% 42%St Clair 3 168 46% 40%St Clair 4 158 49% 48%St Clair 6 320 40% 33%St Clair 7 450 55% 51%Trenton 7 110 47% 63%Trenton 8 100 6% 3%Trenton 9 520 48% 62%

Capacity Factors are based on winter NDC as shown

Direct Testimony of G. E. Sansoucy on Behalf of MEC MPSC Case No. U-16892-R - October 17, 2013 Exhibit: MEC-37 - MEC/DE-3.39e Page 1 of 1

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 243 of 873

MPSC Case No.: U-16892-R Respondent: R. E. Palmer/Legal Requestor: MEC-1 Question No.: MEC/DE-1.20 Page: 1 of 1 Question: Refer to the direct testimony of Robert Palmer at REP-5, lines 11-19.

Provide the Company’s projected and actual loading factor, for each of its base load coal units, from 2008-2012.

Answer: DTE Electric objects for the reason that a subset of the information

requested is for the years 2008-2011, which are outside the timeframe for this proceeding, and is not relevant to the reasonableness and prudence of DTE Electric’s power supply costs and expenses for the 2012 PSCR Reconciliation, which is the proper subject timeframe of this PSCR plan proceeding under Act 304 pursuant to MCL 460.6j(3) and (4), nor is it reasonably calculated to lead to the discovery of admissible evidence. Subject to such objection, and without waiver thereof, DTE Electric would answer as follows:

2008 Loading Factor

2009 Loading Factor

2010 Loading Factor

2011 Loading Factor

2012 Loading Factor

Plan Actual Plan Actual Plan Actual Plan Actual Plan Actual

Belle River 1 95% 91% 95% 94% 96% 90% 90% 89% 84% 83% Belle River 2 93% 95% 94% 92% 88% 92% 89% 92% 84% 89% Monroe 1 90% 87% 83% 88% 88% 87% 72% 80% 79% 67% Monroe 2 82% 80% 81% 84% 88% 85% 75% 72% 57% 65% Monroe 3 88% 85% 84% 84% 89% 87% 70% 86% 81% 77% Monroe 4 90% 85% 89% 87% 89% 88% 76% 75% 82% 65% River Rouge 2 89% 80% 78% 79% 75% 90% 77% 61% 72% 48% River Rouge 3 75% 80% 68% 78% 79% 80% 77% 68% 68% 64% St Clair 1 66% 69% 68% 61% 62% 64% 61% 56% 57% 53% St Clair 2 64% 67% 65% 59% 60% 63% 59% 55% 55% 51% St Clair 3 62% 69% 63% 56% 57% 55% 56% 53% 52% 51% St Clair 4 66% 65% 70% 62% 65% 63% 63% 53% 59% 58% St Clair 6 73% 73% 78% 75% 78% 72% 72% 66% 61% 63% St Clair 7 79% 81% 76% 77% 73% 75% 74% 73% 66% 67% Trenton HS 64% 73% 71% 73% 62% 65% 48% 49% 34% 49% Trenton 9 76% 76% 78% 75% 73% 82% 64% 71% 58% 70%

Direct Testimony of G. E. Sansoucy on Behalf of MEC MPSC Case No. U-16892-R - October 17, 2013 Exhibit: MEC-38 - MEC/DE-1.20 Page 1 of 1

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 244 of 873

MPSC Case No.: U-16892-R Respondent: A.P.Wojtowicz/R.E. Palmer/ Legal Requestor: MEC-1 Question No.: MEC/DE-1.6b Page: 1 of 2 Question: Refer to the direct testimony of Karthik Krishnamurthy at KK-7.

b. Identify and describe, for each month of 2012, how higher-than-forecast coal costs affected the dispatch price, dispatch rate, generation, and overall power supply cost (in $/kWh) of each of the Company’s coal-fired power plants.

Answer: DTE Electric objects for the reasons that the request is unduly

burdensome and overly broad. Subject to such objection, and without waiver thereof, DTE Electric would answer as follows:

The dispatch of the Company’s coal units is performed by MISO and is the

result of a combination of interrelating factors. The dispatch price of our coal units can vary depending on the coal blend that is being burned and the associated emission allowance expense. The price would be based off of the replacement fuel cost (of the blend to be burned) and would only be dispatched by MISO if it was economic to do so or if required for system reliability. Each coal blend changes the capacity limit of each unit differently, so the maximum output from any unit can vary. This means the actual generation from coal-fired power plants will change depending on the MISO dispatch and the blend of coal burned. The MISO dispatch rate of the Company’s coal-fired power plants depends on many factors including the wholesale energy market price, the availability of other market participants’ generation, the amount of load, and the various blends of coal. The overall power supply costs were minimized through the economic dispatch of our coal-fired power plants by MISO.

The contribution of higher coal costs on dispatch rate, generation, and overall power supply costs cannot be determined, but only estimated by performing a detailed hourly analysis of the plan and actual data and evaluating and speculating about numerous operating assumptions. Even a detailed hourly post-analysis would be extremely complicated and only result in an estimate because of multiple interacting variables that are not mutually exclusive and consideration in differing sequences could result in different conclusions. The data that would have to be considered would include, at a minimum; load, wholesale energy market prices, generation and assumptions about what generation would have been

Direct Testimony of G. E. Sansoucy on Behalf of MEC MPSC Case No. U-16892-R - October 17, 2013 Exhibit: MEC-39 - MEC/DE-1.6b Page 1 of 2

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 245 of 873

MPSC Case No.: U-16892-R Respondent: A.P.Wojtowicz/R.E. Palmer/ Legal Requestor: MEC-1 Question No.: MEC/DE-1.6b Page: 2 of 2

under different conditions (i.e., different market prices which can result in different power plant operations and different output capabilities).

Direct Testimony of G. E. Sansoucy on Behalf of MEC MPSC Case No. U-16892-R - October 17, 2013 Exhibit: MEC-39 - MEC/DE-1.6b Page 2 of 2

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 246 of 873

MPSC Case No.: U-16892-R Respondent: R. E. Palmer Requestor: MEC-1 Question No.: MEC/DE-1.21b Page: 1 of 1 Question: Refer to Exhibit A-13. b. Explain why actual plant generation was higher than projected at

Greenwood. Answer: During the summer of 2012 the weather was hotter than the weather

normalized projections and that resulted in higher than forecasted loads in the MISO footprint. The price of natural gas delivered to Greenwood was also lower than forecasted. The combination of those events and others within MISO resulted in the increased Greenwood generation.

Direct Testimony of G. E. Sansoucy on Behalf of MEC MPSC Case No. U-16892-R - October 17, 2013 Exhibit: MEC-40 - MEC/DE-1.21b Page 1 of 1

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 247 of 873

MPSC Case No.: U-16892-R Respondent: K. Krishnamurthy Requestor: ST-1 Question No.: ST/DE-1.20 Page: 1 of 1 Question: Does DTE Electric have firm capacity and firm supply for Greenwood? If

so, please indicate the volumes for each. Answer: DTE Electric does not have firm capacity and firm supply for natural gas

for the Greenwood generating station.

Direct Testimony of G. E. Sansoucy on Behalf of MEC MPSC Case No. U-16892-R - October 17, 2013 Exhibit: MEC-41 - ST/DE-1.20 Page 1 of 1

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 248 of 873

DTE Electric Capacity and Generation Analysis

PSCR Plan Year 2012

A B C D E F G H I J K L M N O P Q R S

NDC2012 Net Heat Rate

Planned Outages

Unplanned Outages

2012 Actual On-Line Hours

Total Potential Hours Plan POF

Actual POF

Plan ROF

Actual ROF

Total Planned Outage Factor

Total Actual Outage Factor Availability

2012 Net Generation

Unadjusted Capacity Factor

Adjusted Capacity Factor*

Net Generation based on 80% capacity factor

Net Generation @ 80% CF less Actual

Net Generation**(MW) (Btu/kWh) (Hours) (Hours) (Hours) (Hours) (%) (%) (%) (%) (%) (%) (%) (MWh) (%) (%) (MWh) (MWh)

MCAAA/DE-3.92 Exh. A-14

MEC/DE-3.44

MEC/DE-2.36a Exh. A-14 (Col. D+E+F)

MEC/DE-2.36b

MEC/DE-2.36b

MEC/DE-2.36b

MEC/DE-2.36b

Col. H + Col. J (Col. I + K)

(100% - Col. M) Exh. A-14

(Col. O ÷ (Col. B X Col. G)

(Col. O ÷ (Col. B X Col. F)

(80% X (Col. B X Col. F)) Col. R - Col. O

BRVPP - 1 517 10,235 726 498 7557 8,781 7% 8.3% 8% 6.1% 15.0% 14.4% 85.6% 3,234,146 71.24% 82.78% 3,125,575 BRVPP - 2 517 10,112 2,048 486 6248 8,782 23% 23.4% 9% 5.9% 32.0% 29.3% 70.7% 2,843,761 62.63% 88.04% 2,584,173 MONPP - 1 770 10,454 629 389 7767 8,785 5% 7.2% 9% 4.8% 14.0% 12.0% 88.0% 4,017,056 59.38% 67.17% 4,784,472 767,416 MONPP - 2 795 10,170 913 926 6944 8,783 8% 10.4% 10% 11.4% 18.0% 21.8% 78.2% 3,563,477 51.03% 64.55% 4,416,384 852,907 MONPP - 3 783 9,819 708 8076 8,784 2% 0.1% 10% 9.3% 12.0% 9.4% 90.6% 4,779,578 69.49% 75.58% 5,058,806 279,228 MONPP - 4 762 10,461 2,113 209 6462 8,784 24% 24.2% 7% 2.6% 31.0% 26.8% 73.2% 3,175,316 47.44% 64.49% 3,939,235 763,919 RRGPP - 2 260 10,827 1,722 251 6314 8,287 14% 19.9% 7% 3.2% 21.0% 23.1% 76.9% 852,689 39.57% 51.94% 1,313,312 460,623 RRGPP - 3 280 10,521 177 724 7479 8,380 4% 2.0% 7% 9.7% 11.0% 11.7% 88.3% 1,400,059 59.67% 66.86% 1,675,296 275,237 STCPP - 1 158 11,675 439 157 8187 8,783 3% 5.1% 9% 10.0% 12.0% 15.1% 84.9% 622,647 44.87% 48.13% 1,034,837 412,190 STCPP - 2 162 11,620 864 361 7559 8,784 3% 10.0% 9% 6.3% 12.0% 16.3% 83.7% 600,721 42.21% 49.06% 979,646 378,925 STCPP - 3 168 11,774 1,546 362 6754 8,662 3% 17.5% 8% 5.4% 11.0% 22.9% 77.1% 582,424 40.02% 51.33% 907,738 325,314 STCPP - 4 158 11,559 830 673 7217 8,720 9% 9.6% 12% 8.3% 21.0% 17.9% 82.1% 664,427 48.23% 58.27% 912,229 247,802 STCPP - 6 320 10,973 2,485 999 5303 8,787 22% 28.5% 13% 18.6% 35.0% 47.1% 52.9% 934,541 33.24% 55.07% 1,357,568 423,027 STCPP - 7 450 10,663 757 877 7099 8,733 4% 9.0% 10% 14.9% 14.0% 23.9% 76.1% 2,023,831 51.50% 63.35% 2,555,640 531,809 TCHPP - 9 520 9,674 477 346 7961 8,784 2% 6.7% 16% 4.9% 18.0% 11.6% 88.4% 2,818,892 61.71% 68.09% 3,311,776 492,884 TOTALS 32,113,565 37,956,687 6,211,281

* Adjusted for Actual Outages** Belle River ran at a capacity factor over 80%, as such, no additional generation is estimated.

Direct Testimony of G. E. Sansoucy on Behalf of MEC MPSC Case No. U-16892-R - October 17, 2013 Exhibit: MEC-42 - DTE Electric Capacity and Generation Analysis Page 1 of 1

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 249 of 873

DTE Electric Fly Ash Analysis

PSCR Plan Year 2012

A B C D E F GNon-REF REF

Fly Ash Produced per Coal Ton - Non

REF Coal

Fly Ash Produced per Coal Ton -

REF Coal

Additional Fly Ash Produced per Coal Ton from REF Coal

REF Coal Consumed in 2012

Additional Fly Ash Produced

Additional Cost of Fly Ash Disposal @ $8.90/ton

(Ton) (Ton) (Ton) (Ton) (Ton) ($)MEC/DE-3-52c MEC/DE-3-52d Col. C - Col. B KK-10, ln 18-20 Col. D X Col E Col. F X $8.90

St. Clair 0.035 0.038 0.003 1,769,118 5,307 47,235 Belle River 0.035 0.038 0.003 1,735,213 5,206 46,330 Monroe 0.048 0.051 0.003 7,438,570 22,316 198,610 TOTALS 10,942,901 32,829 292,175

Direct Testimony of G. E. Sansoucy on Behalf of MEC MPSC Case No. U-16892-R - October 17, 2013 Exhibit: MEC-43 - DTE Electric Fly Ash Analysis Page 1 of 1

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 250 of 873

MPSC Case No.: U-17097 Respondent: K. Krishnamurthy/Legal Requestor: MEC-1 Question No.: MEC/DE-1.23a Page: 1 of 1 Question: Please state whether the Company or any of its witnesses has any more

information, on any of the following topics related to REF, than was provided in discovery responses and cross-examination in Case U-16892, and discovery and testimony (direct and rebuttal) in Case U-16434-R. For any affirmative answer, describe in detail the new information and produce any documents referenced, reviewed, or relied upon for the answer.

a. Identities of the third party tax credit investors.

Answer: Detroit Edison objects for the reason that the information requested is not

relevant to the reasonableness and prudence of power supply costs and expenses that are the proper subject of PSCR proceedings under Act 304, nor is it reasonably calculated to lead to the discovery of admissible evidence. Subject to such objection, and without waiver thereof, Detroit Edison would answer as follows:

No.

MPSC Case No. U-17097 - March 7, 2013 Exhibit MEC-33; Source: MEC-DE-1.23a-g (Krishnamurthy, Dau), U-17097 Page 1 of 7

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 251 of 873

MPSC Case No.: U-17097 Respondent: K. Krishnamurthy/Legal Requestor: MEC-1 Question No.: MEC/DE-1.23b Page: 1 of 1 Question: Please state whether the Company or any of its witnesses has any more

information, on any of the following topics related to REF, than was provided in discovery responses and cross-examination in Case U-16892, and discovery and testimony (direct and rebuttal) in Case U-16434-R. For any affirmative answer, describe in detail the new information and produce any documents referenced, reviewed, or relied upon for the answer.

b. Purchase price of the interests in the Fuel Companies sold to the third

party tax credit investors. Answer: Detroit Edison objects for the reason that the information requested is not

relevant to the reasonableness and prudence of power supply costs and expenses that are the proper subject of PSCR proceedings under Act 304, nor is it reasonably calculated to lead to the discovery of admissible evidence. Subject to such objection, and without waiver thereof, Detroit Edison would answer as follows:

No.

MPSC Case No. U-17097 - March 7, 2013 Exhibit MEC-33; Source: MEC-DE-1.23a-g (Krishnamurthy, Dau), U-17097 Page 2 of 7

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 252 of 873

MPSC Case No.: U-17097 Respondent: K. Krishnamurthy/Legal Requestor: MEC-1 Question No.: MEC/DE-1.23c Page: 1 of 1 Question: Please state whether the Company or any of its witnesses has any more

information, on any of the following topics related to REF, than was provided in discovery responses and cross-examination in Case U-16892, and discovery and testimony (direct and rebuttal) in Case U-16434-R. For any affirmative answer, describe in detail the new information and produce any documents referenced, reviewed, or relied upon for the answer.

c. Projected or actual revenues accruing to DTE Energy Company and/or

any subsidiaries from the REF program, including but not limited to tax credit revenues and membership interest sale proceeds.

Answer: Detroit Edison objects for the reason that the information requested is not

relevant to the reasonableness and prudence of power supply costs and expenses that are the proper subject of PSCR proceedings under Act 304, nor is it reasonably calculated to lead to the discovery of admissible evidence. Subject to such objection, and without waiver thereof, Detroit Edison would answer as follows:

No.

MPSC Case No. U-17097 - March 7, 2013 Exhibit MEC-33; Source: MEC-DE-1.23a-g (Krishnamurthy, Dau), U-17097 Page 3 of 7

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 253 of 873

MPSC Case No.: U-17097 Respondent: J. C. Dau Requestor: MEC-1 Question No.: MEC/DE-1.23d Page: 1 of 1 Question: Please state whether the Company or any of its witnesses has any more

information, on any of the following topics related to REF, than was provided in discovery responses and cross-examination in Case U-16892, and discovery and testimony (direct and rebuttal) in Case U-16434-R. For any affirmative answer, describe in detail the new information and produce any documents referenced, reviewed, or relied upon for the answer.

d. Status of the testing at Belle River.

Answer: The current plan is to continue testing Unit 1 in 2013. The testing is

planned around the Unit 1 outage that is currently scheduled for March 8, 2013 through May 23, 2013. The first test period is to begin January 1 to the start of the outage and the second test period is to begin after the outage for a minimum of 90 days. Any outcome as to a decision and or further testing on Unit 1 and/or 2 will be based on the test results.

No documents were relied upon to support the discovery response.

MPSC Case No. U-17097 - March 7, 2013 Exhibit MEC-33; Source: MEC-DE-1.23a-g (Krishnamurthy, Dau), U-17097 Page 4 of 7

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 254 of 873

MPSC Case No.: U-17097

Respondent: K. Krishnamurthy

Requestor: MEC-1

Question No.: MEC/DE-1.23e

Page: 1 of 1 Question: Please state whether the Company or any of its witnesses has any more

information, on any of the following topics related to REF, than was provided in discovery responses and cross-examination in Case U-16892, and discovery and testimony (direct and rebuttal) in Case U-16434-R. For any affirmative answer, describe in detail the new information and produce any documents referenced, reviewed, or relied upon for the answer.

e. Revision of any agreements with any of the Fuel Companies related to

the REF program. Answer: To the extent that REF testing is continuing at BRPP, the Acceptance

Period Inventory Purchase Agreement is extended under the same Terms & Conditions to accommodate the sale of additional Coal Inventory.

MPSC Case No. U-17097 - March 7, 2013 Exhibit MEC-33; Source: MEC-DE-1.23a-g (Krishnamurthy, Dau), U-17097 Page 5 of 7

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 255 of 873

MPSC Case No.: U-17097 Respondent: K. Krishnamurthy/Legal Requestor: MEC-1 Question No.: MEC/DE-1.23f Page: 1 of 1 Question: Please state whether the Company or any of its witnesses has any more

information, on any of the following topics related to REF, than was provided in discovery responses and cross-examination in Case U-16892, and discovery and testimony (direct and rebuttal) in Case U-16434-R. For any affirmative answer, describe in detail the new information and produce any documents referenced, reviewed, or relied upon for the answer.

f. Sale of any interests in any of the Fuel Companies.

Answer: Detroit Edison objects for the reason that the information requested is not

relevant to the reasonableness and prudence of power supply costs and expenses that are the proper subject of PSCR proceedings under Act 304, nor is it reasonably calculated to lead to the discovery of admissible evidence. Subject to such objection, and without waiver thereof, Detroit Edison would answer as follows:

No.

MPSC Case No. U-17097 - March 7, 2013 Exhibit MEC-33; Source: MEC-DE-1.23a-g (Krishnamurthy, Dau), U-17097 Page 6 of 7

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 256 of 873

MPSC Case No.: U-17097

Respondent: K. L. O’Neill

Requestor: MEC-1

Question No.: MEC/DE-1.23g

Page: 1 of 1

Question: Please state whether the Company or any of its witnesses has any more

information, on any of the following topics related to REF, than was provided in discovery responses and cross-examination in Case U-16892, and discovery and testimony (direct and rebuttal) in Case U-16434-R. For any affirmative answer, describe in detail the new information and produce any documents referenced, reviewed, or relied upon for the answer.

g. Disclosures to the Commission of any coal inventory sales to the Fuel

Companies. Answer: The Company submitted The Detroit Edison Company’s Affiliate

Transactions Compliance Report for the year 2011 as required by the order issued by the Michigan Public Service Commission dated January 21, 2003 in Case No. U-13502 which can be found at the following url:

http://efile.mpsc.state.mi.us/efile/docs/13502/0041.pdf

MPSC Case No. U-17097 - March 7, 2013 Exhibit MEC-33; Source: MEC-DE-1.23a-g (Krishnamurthy, Dau), U-17097 Page 7 of 7

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 257 of 873

9

1 STATE OF MICHIGAN

2 BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION

3 In the matter of the application of

The Detroit Edison Company for Case No. U-16434-R

4 reconciliation of its power supply

cost recovery plan for the 12-month Volume No. 2

5 period ending December 31, 2011.

_____________________________________/

6

CROSS-EXAMINATION

7

Proceedings held in the above-entitled matter

8

before Mark D. Eyster, J.D., Administrative Law Judge

9

with Michigan Administrative Hearing System, at the

10

Michigan Public Service Commission, Constitution Hall,

11

525 West Allegan, Nisbet Room, Lansing, Michigan, on

12

Tuesday, January 8, 2013, at 9:03 a.m.

13

APPEARANCES:

14

DAVID MAQUERA, J.D.

15 JON P. CHRISTINIDIS, J.D.

DTE Energy

16 One Energy Plaza, #688WCB

Detroit, Michigan 48226

17

On behalf of The Detroit Edison Company

18

DON L. KESKEY, J.D.

19 Public Law Resource Center, PLLC

139 West Lake Lansing Road, Suite 210

20 East Lansing, Michigan 48823

21 On behalf of Michigan Community Action

Agency Association

22

23

24

25 (Continued)

Metro Court Reporters, Inc. 248.426.9530

MPSC Case No. U-17097 - March 7, 2013 Exhibit MEC-34; Source: Examination of G. Lapplander (Jan. 8, 2013 direct and cross), U-16434-R Page 1 of 190

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 258 of 873

10

1 APPEARANCES Continued:

2 CHRISTOPHER BZDOK, J.D.

EMERSON HILTON, J.D.

3 Olson, Bzdok & Howard PC

420 East Front Street

4 Traverse City, Michigan 49686

5 On behalf of Michigan Environmental Council

6 DONALD E. ERICKSON,

Assistant Attorney General

7 Special Litigation Division

525 West Ottawa, 6th Floor

8 Lansing, Michigan 48909

9 On behalf of Attorney General Bill Schuette

10 ANNE M. UITVLUGT,

Assistant Attorney General

11 6545 Mercantile Way, Suite 15

Lansing, Michigan 48911

12

On behalf of Michigan Public Service

13 Commission Staff

14 - - -

15

16

17

18

19

20

21

22

23 REPORTED BY: Lori Anne Penn (CSR-1315)

24

25

Metro Court Reporters, Inc. 248.426.9530

MPSC Case No. U-17097 - March 7, 2013 Exhibit MEC-34; Source: Examination of G. Lapplander (Jan. 8, 2013 direct and cross), U-16434-R Page 2 of 190

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 259 of 873

11

1 I N D E X

2 WITNESS: PAGE

3 John C. Dau

4 Testimony Bound In 19

5 Jeffrey A. Jewell

6 Testimony Bound In 29

7 Kelly A. Holmes

8 Testimony Bound In 39

9 Michael W. Shields

10 Testimony Bound In 58

11 James D. Good

12 Direct Examination by Mr. Maquera 83

Cross-Examination by Mr. Keskey 95

13 Cross-Examination by Mr. Bzdok 101

Cross-Examination by Mr. Erickson 103

14

Kevin L. O'Neill

15

Direct Examination by Mr. Maquera 107

16 Cross-Examination by Mr. Keskey 129

17 Gary E. Lapplander

18 Direct Examination by Mr. Maquera 136

Cross-Examination by Mr. Keskey 182

19

20

21

22

23

24

25

Metro Court Reporters, Inc. 248.426.9530

MPSC Case No. U-17097 - March 7, 2013 Exhibit MEC-34; Source: Examination of G. Lapplander (Jan. 8, 2013 direct and cross), U-16434-R Page 3 of 190

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 260 of 873

MPSC Case No. U-16434-R

January 8, 2013 - Transcript 2

Testimony of Gary E. Lapplander

Other testimony atpp. 12 through 135

removed as unrelated

MPSC Case No. U-17097 - March 7, 2013 Exhibit MEC-34; Source: Examination of G. Lapplander (Jan. 8, 2013 direct and cross), U-16434-R Page 4 of 190

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 261 of 873

136

1 JUDGE EYSTER: Briefly. We're off the

2 record.

3 (At10:01 a.m., there was a two-minute recess.)

4 JUDGE EYSTER: Back on the record.

5 MR. MAQUERA: Yes, your Honor. The

6 Company has no redirect for this witness.

7 JUDGE EYSTER: All right. Thank you.

8 You're excused.

9 (The witness was excused.)

10 - - -

11 MR. KESKEY: Your Honor, can we go off

12 the record a minute?

13 JUDGE EYSTER: Sure. We're off the

14 record.

15 (At 10:04 a.m., there was a 38-minute recess.)

16 (Documents marked for identification by the Court

17 Reporter as Exhibit Nos. MCA-12 through MCA-26.)

18 JUDGE EYSTER: We're back on the record.

19 G A R Y E. L A P P L A N D E R

20 was called as a witness on behalf of The Detroit Edison

21 Company and, having been duly sworn to testify the truth,

22 was examined and testified as follows:

23 DIRECT EXAMINATION

24 BY MR. MAQUERA:

25 Q Mr. Lapplander, would you please state your full name and

Metro Court Reporters, Inc. 248.426.9530

MPSC Case No. U-17097 - March 7, 2013 Exhibit MEC-34; Source: Examination of G. Lapplander (Jan. 8, 2013 direct and cross), U-16434-R Page 5 of 190

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 262 of 873

137

1 business address for the record?

2 A Gary E. Lapplander, One Energy Plaza, Detroit, Michigan

3 48226.

4 Q Mr. Lapplander, did you file or cause to be filed with

5 the Commission a document entitled the Qualifications and

6 Direct Testimony of Gary E. Lapplander, consisting of a

7 cover sheet and 21 pages of questions and answers?

8 A Yes.

9 Q Do you have any changes you wish to make to your direct

10 testimony?

11 A No.

12 Q Is that then the direct testimony that you are adopting

13 today?

14 A Yes.

15 Q And are you sponsoring any exhibits associated with your

16 direct testimony in this case?

17 A Yes.

18 Q For purposes of identification, would that be exhibit, or

19 include Exhibit A-10, consisting of 10 pages; Exhibit

20 A-11, consisting of two pages; and Exhibit A-24,

21 consisting of nine pages?

22 A Yes.

23 Q Were these exhibits prepared by you or for you or at your

24 direction?

25 A Yes.

Metro Court Reporters, Inc. 248.426.9530

MPSC Case No. U-17097 - March 7, 2013 Exhibit MEC-34; Source: Examination of G. Lapplander (Jan. 8, 2013 direct and cross), U-16434-R Page 6 of 190

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 263 of 873

138

1 Q Do you have any changes to make to any of those three

2 direct exhibits?

3 A No.

4 Q Mr. Lapplander, did you also cause to be filed with the

5 Commission a document entitled the Rebuttal Testimony of

6 Gary E. Lapplander, consisting of a cover sheet and 19

7 pages of questions and answers?

8 A Yes.

9 Q Do you have any changes you wish to make to your rebuttal

10 testimony?

11 A No.

12 Q Is that then the rebuttal testimony that you are adopting

13 today?

14 A Yes.

15 Q Did you sponsor any exhibits associated with your

16 rebuttal testimony in this case?

17 A Yes.

18 Q For purposes of identification, would those exhibits

19 include and be designated as Exhibit A-25, which consists

20 of one page; Exhibit A-26, which consists of one page,

21 Exhibit A-27, consisting of 82 pages; Exhibit A-28,

22 consisting of 61 pages; Exhibit A-29, consisting of one

23 page; Exhibit A-30, consisting of 806 pages; Exhibit

24 A-31, consisting of two pages; Exhibit A-32, consisting

25 of two pages; Exhibit A-33, consisting of one page; and

Metro Court Reporters, Inc. 248.426.9530

MPSC Case No. U-17097 - March 7, 2013 Exhibit MEC-34; Source: Examination of G. Lapplander (Jan. 8, 2013 direct and cross), U-16434-R Page 7 of 190

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 264 of 873

139

1 Exhibit A-34, consisting of two pages?

2 A Yes.

3 Q Were these exhibits prepared by you or for you or at your

4 direction?

5 A Yes.

6 Q Do you have any changes you wish to make to any of those

7 ten rebuttal exhibits?

8 A No.

9 MR. MAQUERA: Your Honor, Detroit Edison

10 moves to bind into the record the Direct Testimony and

11 Rebuttal Testimony of Gary E. Lapplander, and moves for

12 admission at the end of cross-examination of Exhibits

13 A-10, A-11 and A-24, and A-25, A-26, A-27, A-28, A-29,

14 A-30, A-31, A-32, A-33 and A-34, and tenders

15 Mr. Lapplander for cross-examination.

16 JUDGE EYSTER: O.K. Are there any

17 objections to the testimony being bound into the record?

18 MR. BZDOK: Judge, we have no objection

19 to the testimony. We anticipate some voir dire questions

20 relative to Exhibit A-30. I understand you're holding a

21 ruling on the admission of the exhibits until the end,

22 but I just wanted to put that there as a heads up.

23 JUDGE EYSTER: All right. Hearing no

24 objection, the testimony is bound into the record.

25 (Testimony bound in.)

Metro Court Reporters, Inc. 248.426.9530

MPSC Case No. U-17097 - March 7, 2013 Exhibit MEC-34; Source: Examination of G. Lapplander (Jan. 8, 2013 direct and cross), U-16434-R Page 8 of 190

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 265 of 873

STATE OF MICHIGAN

BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION

In the matter of the Application of ) THE DETROIT EDISON COMPANY for ) Reconciliation of its Power Supply ) Case No. U-16434-R Cost Recovery Plan for the 12-month Period ) Ending December 31, 2011 )

QUALIFICATIONS

AND

DIRECT TESTIMONY

OF

GARY E. LAPPLANDER

MPSC Case No. U-17097 - March 7, 2013 Exhibit MEC-34; Source: Examination of G. Lapplander (Jan. 8, 2013 direct and cross), U-16434-R Page 9 of 190

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 266 of 873

THE DETROIT EDISON COMPANY QUALIFICATIONS OF GARY E. LAPPLANDER

Line No.

GEL - 1

Q. Would you please state your name and business address? 1

A. My name is Gary E. Lapplander. I am the Director - Fuel Supply for The Detroit 2

Edison Company (Detroit Edison or the Company). My business address is One 3

Energy Plaza, Detroit, Michigan 48226. I am testifying on behalf of Detroit 4

Edison. 5

6

Q. Would you please summarize your educational background? 7

A. I received a Bachelor of Science Degree in Mechanical Engineering in 1975 from 8

Western Michigan University (WMU). In 1978, I also received from WMU a 9

Bachelor of Science Degree in Automotive Engineering Technology. In 1982, I 10

received a Masters Degree in Business Administration from Wayne State 11

University, with a major in Finance. I have completed many Company-sponsored 12

courses and have attended numerous seminars to further my development with 13

Detroit Edison. 14

15

Q. Would you please describe your professional experience? 16

A. I began working for Detroit Edison in 1975, and for the period 1975 through 1981, I 17

held various positions within the Special Projects Group of the Mechanical 18

Engineering Division of the Generation Engineering Department. My primary 19

responsibilities focused on engineering economic analysis, thermodynamic analysis 20

of power plant cycles, cost/benefit analysis of new capital additions and various 21

regulatory matters. While I was a member of the Special Projects Group, I cross-22

trained with Strategic Planning, the Greenwood Project Management Organization 23

and the Greenwood Production Organization. 24

25

MPSC Case No. U-17097 - March 7, 2013 Exhibit MEC-34; Source: Examination of G. Lapplander (Jan. 8, 2013 direct and cross), U-16434-R Page 10 of 190

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 267 of 873

G. E. LAPPLANDER Line U-16434-R No.

GEL- 2

In 1982, I joined the Planning and Development Division of the Fuel Supply 1

Department as a Fuel Resources Engineer. 2

3

In 1985, I undertook a one-year management training assignment as the Assistant 4

Maintenance Engineer at the Company’s River Rouge Power Plant. Upon my 5

return to Fuel Supply in 1986, I was promoted to Senior Fuel Resources Engineer 6

and had responsibility for the preparation of short and long-term fuel plans. A fuel 7

plan considers all aspects of the fuel supply function including fuel consumption, 8

fuel requirements, etc. Fuel plans form the basis for the development of fuel 9

expense and fuel requirement forecasts. In addition, I assisted in, or was 10

responsible for, the initial negotiations for long-term procurement of fuels and 11

related transportation. Also, I was involved with the development of fuel 12

specifications for individual electric power plants operated by the Company. 13

14

In 1991, I was appointed to the position of Director - Planning & Contracts, Fuel 15

Supply. My responsibilities included planning, development and procurement of 16

fossil fuels to meet the Company’s electric generating needs. In addition, I was 17

responsible for the negotiation and administration of the Company’s long-term 18

fossil fuel and related transportation contracts. 19

20

In 1994, I was appointed Director - Power Supply Initiatives/Business Planning. 21

My responsibilities included development and implementation of a management 22

and control system for Power Supply, assessment of utility deregulation and its 23

impact on the electric generating business and the introduction of risk management 24

in Power Supply. 25

MPSC Case No. U-17097 - March 7, 2013 Exhibit MEC-34; Source: Examination of G. Lapplander (Jan. 8, 2013 direct and cross), U-16434-R Page 11 of 190

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 268 of 873

G. E. LAPPLANDER Line U-16434-R No.

GEL- 3

In 1997, I was promoted to Director - Fuel Supply (the title for this position 1

changed from Manager in 2002 in conjunction with the reversal of the naming 2

convention that took place with the merger with Michigan Consolidated Gas 3

Company) the position I currently hold. 4

5

Q. What are your specific responsibilities as Director - Fuel Supply? 6

A. As Director I am responsible for fossil fuel supply and transportation requirements 7

for Detroit Edison’s fossil fueled electric generating assets, as well as the 8

Company’s coal transshipment facility, Midwest Energy Resources Company 9

(MERC). 10

11

Q. Are you a registered professional engineer? 12

A. Yes. I became registered as a professional engineer with the State of Michigan in 13

1980 by examination. 14

15

Q. Are you a member of any professional societies or organizations? 16

A. Yes. I am a member of the American Society of Mechanical Engineers. 17

18

Q. Have you testified or been involved in any hearings before the MPSC while 19

employed with Detroit Edison? 20

A. Yes. I have supplied direct testimony and/or testified in the Steam Heating Fuel 21

Cost Recovery Case No. U-7906, the 1984 and 1986 Power Supply Cost Recovery 22

Reconciliation Case Nos. U-7775-R and U-8291-R, respectively, the 1987, 1988 23

and 2012 Power Supply Cost Recovery Plan Case Nos. U-8578, U-8880 and U-24

16892, respectively, and Main Electric Rate Case Nos. U-8789, U-10102, U-13808, 25

MPSC Case No. U-17097 - March 7, 2013 Exhibit MEC-34; Source: Examination of G. Lapplander (Jan. 8, 2013 direct and cross), U-16434-R Page 12 of 190

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 269 of 873

G. E. LAPPLANDER Line U-16434-R No.

GEL- 4

U-15244 and U-14838. Also, I presented Supplemental and Rebuttal testimony in 1

Case Nos. U-7775-R, U-8020-R and U-16047-R. Furthermore, I assisted in the 2

development of testimony and/or provided support for Company witnesses in other 3

Main Electric Rate and Power Supply Cost Recovery cases. 4

MPSC Case No. U-17097 - March 7, 2013 Exhibit MEC-34; Source: Examination of G. Lapplander (Jan. 8, 2013 direct and cross), U-16434-R Page 13 of 190

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 270 of 873

THE DETROIT EDISON COMPANY DIRECT TESTIMONY OF GARY E. LAPPLANDER

Line No.

GEL - 5

Q. Mr. Lapplander, what is the purpose of your testimony in this case? 1

A. The purpose of my testimony is to support both the use of Reduced Emission Fuel 2

(REF or the Project) at various Detroit Edison Power Plants and the computation of 3

the REF Adder and to discuss why the REF business structure complies with the 4

Code of Conduct. 5

6

Q. Are you sponsoring any exhibits? 7

A. Yes. I am sponsoring the following exhibits 8

Exhibit Description 9

A-10 Overview of Reduced Emissions Fuel (REF) Projects 10

A-11 Refined Coal Adder Inputs Calculation Worksheet 11

A-24 REF Transaction: MPSC Code of Conduct 12

13

Q. Please describe Exhibit A-10 Overview of REF Project? 14

A. Exhibit A-10 is a presentation developed in 2012 that provides an overview of the 15

REF Project at the St. Clair (SCPP), Belle River (BRPP) and Monroe (MPP) Power 16

Plants which will assist the parties in understanding the business structure of the 17

REF Project. 18

19

Q. Please explain Exhibit A-24 REF Transactions: Code of Conduct? 20

A. Exhibit A-24 is a presentation explaining the REF projects’ compliance with the 21

MPSC Code of Conduct. 22

23

Q. At which Detroit Edison Plants was REF consumed in 2011? 24

A. In 2011 REF was consumed at St. Clair Units 1-4 & 6, Monroe Units 1-4 and was 25

MPSC Case No. U-17097 - March 7, 2013 Exhibit MEC-34; Source: Examination of G. Lapplander (Jan. 8, 2013 direct and cross), U-16434-R Page 14 of 190

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 271 of 873

G. E. LAPPLANDER Line U-16434-R No.

GEL- 6

being tested at the Belle River Units 1 & 2. 1

2

Q. When did the REF facilities begin operation at Detroit Edison plants? 3

A. The Belle River Fuels Company (BRFC) and St. Clair Fuels Company (SCFC), 4

subsidiaries of DTE Energy Services, placed in service their respective facilities in 5

December 2009. The Monroe Fuels Company (MFC), also a subsidiary of DTE 6

Energy Services, placed their facility in service in November 2011. The facility at 7

Belle River has two production lines, the facility at St. Clair has three production 8

lines and the facility at the Monroe Power Plant (MPP) has two production lines. 9

DTE Energy Resources, Inc, the parent company of the Fuels Companies, has an 10

exclusive license to use Chem-Mod, the unique and proprietary chemical additive 11

technology, at all DTE Energy sites. 12

13

Q. Did BRFC, SCFC or the MFC sell an interest in any of their production lines 14

at the BRPP, SCPP or MPP? 15

A. Yes. In January 2011 a membership interest was sold in the SCFC, the owner of 16

one of the REF production lines at the SCPP. This arrangement allows the SCFC to 17

begin generating tax credits through the production of Refined Coal sold to Detroit 18

Edison. In November 2011, a membership interest was sold in the MFC, the owner 19

of one of the REF production lines at the Monroe Power Plant. This arrangement 20

similarly allows the MFC to begin generating tax credits through the sale of 21

Refined Coal sold to Detroit Edison. 22

23

Q. What is the status of REF consumption at the Belle River, Monroe and St. 24

Clair Power Plants? 25

MPSC Case No. U-17097 - March 7, 2013 Exhibit MEC-34; Source: Examination of G. Lapplander (Jan. 8, 2013 direct and cross), U-16434-R Page 15 of 190

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 272 of 873

G. E. LAPPLANDER Line U-16434-R No.

GEL- 7

A. REF is being consumed at the St. Clair Power Plant Units 1 through 4, and 6, with a 1

targeted annual REF consumption of approximately 1.8 million tons. REF is 2

continuing to be tested at the BRPP, although the BRFC equipment is considered 3

“in-service” for purposes of qualification for Section 45 production tax credits. The 4

Monroe Power Plant began consuming REF on November 28, 2011. 5

6

Q. How much REF did the Belle River, St. Clair and Monroe Power Plants 7

consume during 2011? 8

A. The Belle River Plant consumed 4,401,402 tons of coal in 2011 and approximately 9

628,662 tons or 14.3% was REF. The St. Clair Plant consumed approximately 10

1,568,222 tons of REF or 44.6% of its total consumption of 3,519,979 tons of coal. 11

The Monroe Plant consumed 8,504,819 tons of coal in 2011 and approximately 12

712,102 tons or 8.4% was REF. 13

14

Q. What is the price charged to Detroit Edison to purchase REF from the Fuels 15

Companies? 16

A. In 2011, the price charged to Detroit Edison to purchase treated coal, REF, from the 17

Fuels Companies was as follows: 18

At Belle River plant, the price was the same as the cost for coal sold by Detroit 19

Edison to the BRFC. i.e. without the Refined Coal Adder (RCA). At St Clair plant, 20

the price was the same as the cost for coal sold by Detroit Edison to SCFC plus 21

RCA. The RCA is offset by the value of reduced emissions. At the Monroe plant, 22

the price is the same as the costs for coal sold by Detroit Edison to MFC. 23

Additionally, there is a Coal Fee Rate paid to Detroit Edison by MFC for each ton 24

of REF consumed. 25

MPSC Case No. U-17097 - March 7, 2013 Exhibit MEC-34; Source: Examination of G. Lapplander (Jan. 8, 2013 direct and cross), U-16434-R Page 16 of 190

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 273 of 873

G. E. LAPPLANDER Line U-16434-R No.

GEL- 8

Q. What were the amounts for Refined Coal Adder at Belle River and St. Clair? 1

A. In 2011, the SO2 portion of, the Refined Coal Adder (RCA) was as follows: 2

Belle River Power Plant: $0 3

St. Clair Power Plant: $544 4

5

The annual cost of the RCA has no impact on the PSCR costs for the above plants 6

since the value of the RCA is offset by the value of reduced SO2 emissions. 7

8

Q. What was the amount for the Coal Fee Rate at the Monroe Power Plant? 9

A. The total Coal Fee Rate amount received by Detroit Edison from MFC at the 10

Monroe Power Plant in 2011 was $738,806, of which $275,940 was credited to 11

O&M and $462,866 was credited to coal inventory. As described later in my 12

testimony, Detroit Edison retains the value of reduced SO2 emissions, realizes the 13

savings of reduced mercury compliance and coal inventory carrying costs. 14

15

Q. What was the reason for crediting a portion of the Coal Fee Rate at the 16

Monroe Power Plant to O&M Expense? 17

A. The Monroe Power Plant determined that to realize the benefits of REF, certain 18

incremental O&M expenditures would need to be incurred related to REF 19

consumption at Monroe. The credit to O&M of a portion of the Coal Fee Rate 20

provides for reimbursement of the incremental O&M expense incurred at the 21

Monroe Power Plant related to the REF consumption. 22

23

MPSC Case No. U-17097 - March 7, 2013 Exhibit MEC-34; Source: Examination of G. Lapplander (Jan. 8, 2013 direct and cross), U-16434-R Page 17 of 190

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 274 of 873

G. E. LAPPLANDER Line U-16434-R No.

GEL- 9

Q. How is Detroit Edison’s sale of coal to its affiliates, BRFC, SCFC and the MFC 1

(collectively, the Fuels Companies), consistent with both the letter and the 2

intent of the Code of Conduct? 3

A. Shipments of coal for consumption at the BRPP and SCPP will be sold at Detroit 4

Edison’s MERC transshipment facility. All rail shipments of coal for consumption 5

at MPP will be sold FOB mine and all vessel delivered western coal for 6

consumption at MPP will be sold FOB vessel at Detroit Edison’s MERC facility. 7

Notwithstanding these sales, the coal always remains under the supervision and 8

control of Detroit Edison and MERC (no Fuels Company employees are involved in 9

any process other than operation of the Fuels Companies’ separate equipment and 10

facilities) and Detroit Edison’s and MERC’s books and records are maintained 11

separately from the Fuels Companies. Most importantly, Section III.C of the Code 12

of Conduct, as approved in the Commission’s October 29, 2001 Order on Rehearing 13

in Case No. U-12134, provides for sales to affiliates at the higher of fully allocated 14

cost or market price. With respect to fully allocated cost, the price at which Detroit 15

Edison is selling the coal is equal to Detroit Edison’s fully allocated cost, or book 16

cost. The Fuels Companies will simply use the coal to produce REF and sell the 17

REF back to Detroit Edison for consumption at the BRPP, SCPP and MPP and any 18

adjustments to the sale price to reflect any higher market pricing would only serve 19

to increase the resale price to Detroit Edison. Since the asymmetrical pricing 20

provision of the Code of Conduct is intended to prevent Detroit Edison from 21

subsidizing its unregulated affiliates, it is clear that this transaction is consistent 22

with that intent and effectuates the proper outcome. 23

24

In addition, Exhibit A-24 describes how the REF projects’ comply with all aspects 25

MPSC Case No. U-17097 - March 7, 2013 Exhibit MEC-34; Source: Examination of G. Lapplander (Jan. 8, 2013 direct and cross), U-16434-R Page 18 of 190

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 275 of 873

G. E. LAPPLANDER Line U-16434-R No.

GEL- 10

of the MPSC Code of Conduct including providing structural separation, avoiding 1

preferential treatment and avoiding subsidized pricing. 2

3

Q. Why didn’t Detroit Edison construct the REF processing facilities? 4

A. At the time the arrangements between Detroit Edison and SCFC and BRFC were 5

consummated, there were a number of reasons why Detroit Edison’s affiliates, 6

rather than Detroit Edison itself, or an independent third party, designed, 7

constructed, owned and operated the REF processing facilities. First and foremost 8

was the fact that the arrangements provided Detroit Edison a risk free option to help 9

it meet the mercury emission reduction requirements contained in Michigan Rule 10

1503 beginning in 2015. Detroit Edison was not required to make any capital 11

investment to support the REF processing facilities and therefore did not assume 12

any risk that the REF project would not be successful. Detroit Edison also 13

reasonably determined that the tax risks and commitment to an unproven 14

technology at its generating facilities were not appropriate for a regulated utility. 15

16

Q. Why did Detroit Edison select its affiliate for this proposal? 17

A. DTE Energy Services (DTEES), the parent company of both BRFC and SCFC, has 18

experience designing, constructing, and operating the production equipment and 19

was willing to take on the associated risk. At the time the REF facilities were 20

constructed at the Belle River and St. Clair Power Plants, the existing legislation 21

required the facilities to achieve commercial operation (i.e. be in service) by 22

January 1, 2010 and Detroit Edison had only a limited time to pursue alternative 23

processes or suppliers. Further, Detroit Edison was not aware of any other supplier 24

that was willing to make this type of investment at the time the REF project needed 25

MPSC Case No. U-17097 - March 7, 2013 Exhibit MEC-34; Source: Examination of G. Lapplander (Jan. 8, 2013 direct and cross), U-16434-R Page 19 of 190

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 276 of 873

G. E. LAPPLANDER Line U-16434-R No.

GEL- 11

to move forward given the existing legislation. 1

2

In addition, at the time that Detroit Edison entered into discussions with DTEES to 3

supply REF for Belle River Power Plant, DTE Energy Resources, parent of 4

DTEES, was one of only three known licensees for the provision of the proprietary 5

technology and held an exclusive license to use the unique and proprietary chemical 6

additive technology, Chem-Mod, at Detroit Edison sites. 7

8

Q. What are some of the other reasons that Detroit Edison moved forward with 9

this REF project with DTEES? 10

A. It seemed reasonable since DTEES had already reached a similar agreement with 11

the Michigan Public Power Agency (MPPA), a partial owner of the Belle River 12

Power Plant. The MPPA is an unaffiliated entity that negotiated at arms-length 13

with DTEES. The MPPA had no particular incentive to reach an agreement with 14

DTEES as opposed to reaching an agreement with any other unrelated third party. 15

As such, the agreement reached with the MPPA was rightfully considered to 16

represent the market for a business deal of this nature. 17

18

In addition, the DTEES proposal provided the following: 19

(a) Reduction in Detroit Edison’s working capital expense by not carrying coal 20

inventory; 21

(b) Reduction in NOX emission allowance expense; and; 22

(c) PSCR customers will never pay more than the value of the environmental 23

benefits received. 24

25

MPSC Case No. U-17097 - March 7, 2013 Exhibit MEC-34; Source: Examination of G. Lapplander (Jan. 8, 2013 direct and cross), U-16434-R Page 20 of 190

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 277 of 873

G. E. LAPPLANDER Line U-16434-R No.

GEL- 12

Q. Why did Detroit Edison move forward with the Monroe REF project with 1

DTEES? 2

A. DTEES, the parent of the MFC, offered an attractive proposal for siting a REF 3

facility at Monroe. The agreement between Detroit Edison and the MFC provides 4

for a Coal Fee Rate payable to Detroit Edison for each ton of REF purchased. In 5

my opinion, this Coal Fee Rate is economically favorable to Detroit Edison and its 6

customers and is at a level which approximates market. The agreement with MFC 7

further provides for the retention of all environmental benefits by Detroit Edison 8

and a reduction in working capital as a result of the MFC owning a portion of the 9

Monroe Power Plant coal inventory. In addition, as previously stated, DTE Energy 10

Resources, Inc., holds an exclusive license to use the unique and proprietary 11

chemical additive technology, Chem-Mod, at Detroit Edison sites. 12

13

Q. Can you provide details as to how REF has been implemented at the Belle 14

River and St. Clair Power Plants? 15

A. Yes. A number of activities have occurred including the sale of a portion of Detroit 16

Edison’s coal inventory to the BRFC and SCFC at the end of 2009, coal handling 17

and consulting activities have been provided by Detroit Edison to the Fuels 18

Companies and the REF has been produced and sold by the Fuels Companies to 19

Detroit Edison for consumption. In addition, arrangements have been made for 20

environmental indemnity protection and payment for other Detroit Edison services 21

by the Fuels Companies. 22

23

Q. When did Detroit Edison sell a portion of its coal inventory to the Fuels 24

Companies? 25

MPSC Case No. U-17097 - March 7, 2013 Exhibit MEC-34; Source: Examination of G. Lapplander (Jan. 8, 2013 direct and cross), U-16434-R Page 21 of 190

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 278 of 873

G. E. LAPPLANDER Line U-16434-R No.

GEL- 13

A. Detroit Edison initially sold 1.7 million ton of its coal inventory at the BRPP and 1

SCPP in December 2009 for $38.6 million, its book cost of inventory. The BRFC 2

purchased one million tons and the SCFC purchased 700,000 tons. Because all of 3

the coal will ultimately be resold to Detroit Edison as either REF or untreated coal 4

(resold coal), I believe it is appropriate to make this transaction at book cost. 5

Detroit Edison customers will benefit from reduced costs associated with not 6

carrying the relevant fuel inventory on its books. At the end of the 10-year REF 7

consumption period, any remaining coal inventory will be sold back to Detroit 8

Edison at the Fuels Companies’ book cost. Notwithstanding these sales, the coal 9

always remains under the supervision and control of Detroit Edison and MERC (no 10

Fuels Company employees are involved in any process other than operation of the 11

Fuels Companies’ separate equipment and facilities) and Detroit Edison’s and 12

MERC’s books and records are maintained separately from the Fuel Companies’ 13

books and records. 14

15

Q. How do Detroit Edison’s customers benefit from the sale of coal inventory to 16

the Fuels Companies? 17

A. In Detroit Edison's rate case, Case No. U-16472, the 12-month ending historical 18

period was the 12-month period ending December 2009. To project the working 19

capital component of rate base for the forecast period, the starting point was the 20

December 31, 2009 balance sheet values, which reflected the reduction in inventory 21

from the sale to the Fuels Companies. Therefore, the resulting rate base also 22

reflects the coal sale to the Fuels Companies that occurred in December of 2009. 23

Customers are experiencing lower base rates of approximately $4 million due to 24

this sale of Detroit Edison’s coal inventory to the Fuel Companies. 25

MPSC Case No. U-17097 - March 7, 2013 Exhibit MEC-34; Source: Examination of G. Lapplander (Jan. 8, 2013 direct and cross), U-16434-R Page 22 of 190

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 279 of 873

G. E. LAPPLANDER Line U-16434-R No.

GEL- 14

Q. Have there been additional sales of Detroit Edison coal inventory subsequent 1

to the initial sale of 1.7 million tons in December 2009? 2

A. Yes. Detroit Edison has periodically sold coal inventory from the coal yard to 3

BRFC at book cost for continued testing at BRPP. In addition, Detroit Edison sold 4

the SCFC 714,000 tons of inventory at a book cost of $19.6 million in January 5

2011, the date the SCFC sold an interest in their facility. The sale of coal inventory 6

at Monroe is discussed later in this testimony. 7

8

Q. How are the coal handling and consulting activities provided? 9

A. These activities are provided under the Coal Handling and Consulting Agreements 10

between Detroit Edison and the Fuels Companies. 11

12

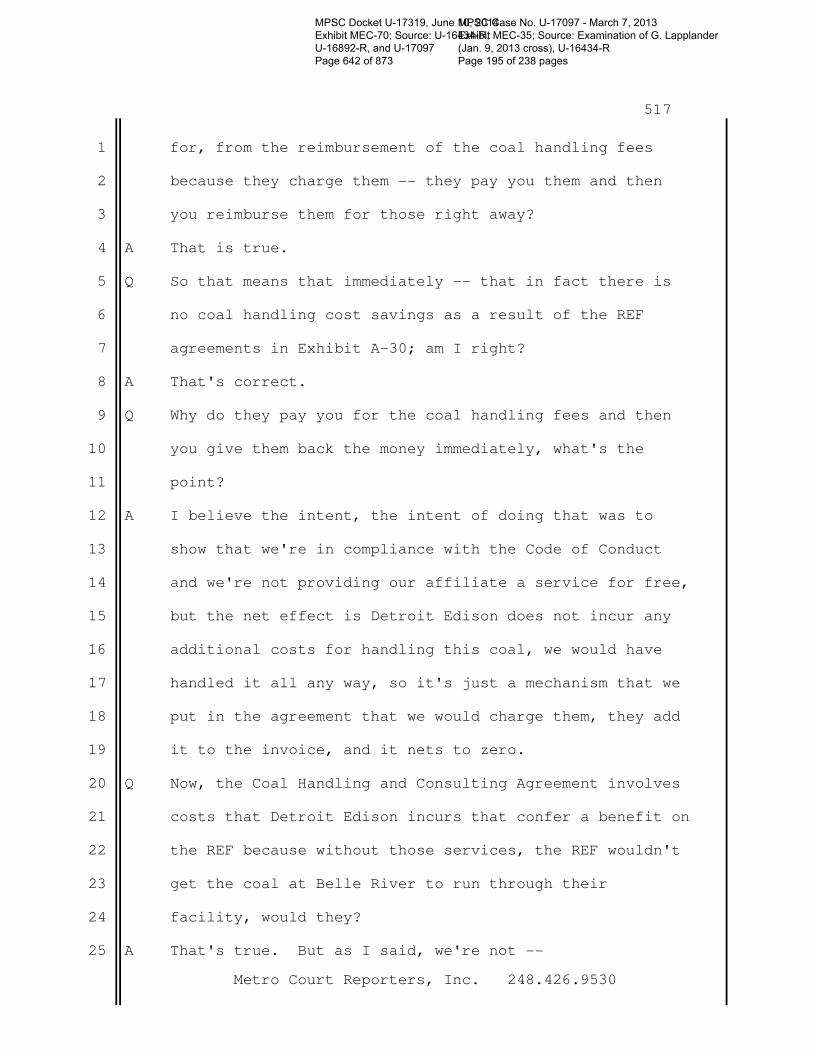

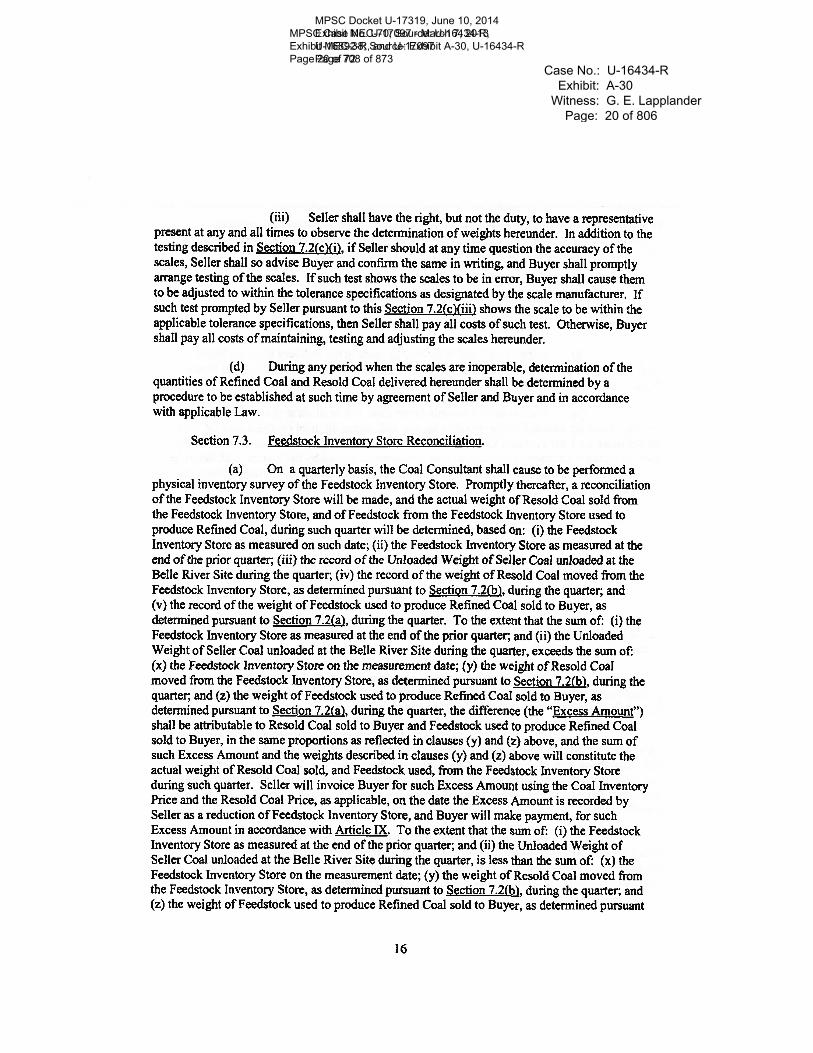

Q. What are some of Detroit Edison’s duties or obligations under the Coal 13

Handling and Consulting Agreements for the BRPP and SCPP? 14

A. The Coal Handling and Consulting Agreements provide that Detroit Edison will, in 15

exchange for a fee, perform all functions related to the delivery of coal to the BRPP 16

and SCPP. These functions, which Detroit Edison has always performed, cover all 17

fuel procurement, fuel processing and fuel handling activities including 18

consumption forecasting, specification of coal quality, coal purchasing, coal 19

transportation, coal shipment scheduling, receiving and unloading of coal, coal 20

sampling and analysis, coal stockpile management and maintenance, etc. The Fuels 21

companies utilize their own employees for management and operation of their own 22

facilities. The operating employees of Detroit Edison are completely separate from 23

the operating employees of the Fuels Companies. 24

25

MPSC Case No. U-17097 - March 7, 2013 Exhibit MEC-34; Source: Examination of G. Lapplander (Jan. 8, 2013 direct and cross), U-16434-R Page 23 of 190

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 280 of 873

G. E. LAPPLANDER Line U-16434-R No.

GEL- 15

Q. Are the costs related to the functions performed by Detroit Edison under the 1

Coal Handling and Consulting Agreement included in the PSCR expenses? 2

A. No. There is no fuel handling expense whatsoever included in PSCR expense, 3

either fuel handling related to Detroit Edison or its affiliates. Coal handling and 4

consulting services are provided by Detroit Edison at cost to the Fuel Companies to 5

support the processing and delivery of REF to the Belle River & St. Clair Power 6

Plants. The rationale for providing these services at cost is that these services are 7

only supporting the provision of REF feedstock coal to the Belle River and St. Clair 8

Power Plants and these same costs eventually flow back to Detroit Edison. In other 9

words, the costs of these services are a zero-sum proposition with costs charged to 10

the Fuels Companies ultimately flowing back to Detroit Edison as REF is 11

purchased. 12

13

Q. Can you describe the details of BRFC’s and SCFC’s sale of REF to Detroit 14

Edison? 15

A. Yes. After the coal is processed and treated by the Fuels Companies, the REF will 16

be sold and delivered to BRPP and the SCPP for “just in time” consumption. The 17

REF sale transaction will be priced out at the fully allocated cost at which Detroit 18

Edison sold the coal to the Fuels Companies plus an REF adder (the REF adder is 19

waived for Belle River during REF testing). The REF adder will consist of several 20

components: (1) an adjustment amount related to fly ash disposal costs designed to 21

keep Detroit Edison whole for any incremental fly ash disposal costs (beginning in 22

January 2011); (2) an adjustment amount related to fly ash revenue, if applicable 23

(beginning in 2015); (3) an adjustment amount based upon and no greater than 24

Detroit Edison’s reduction in actual SO2 emission allowance expense (beginning in 25

MPSC Case No. U-17097 - March 7, 2013 Exhibit MEC-34; Source: Examination of G. Lapplander (Jan. 8, 2013 direct and cross), U-16434-R Page 24 of 190

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 281 of 873

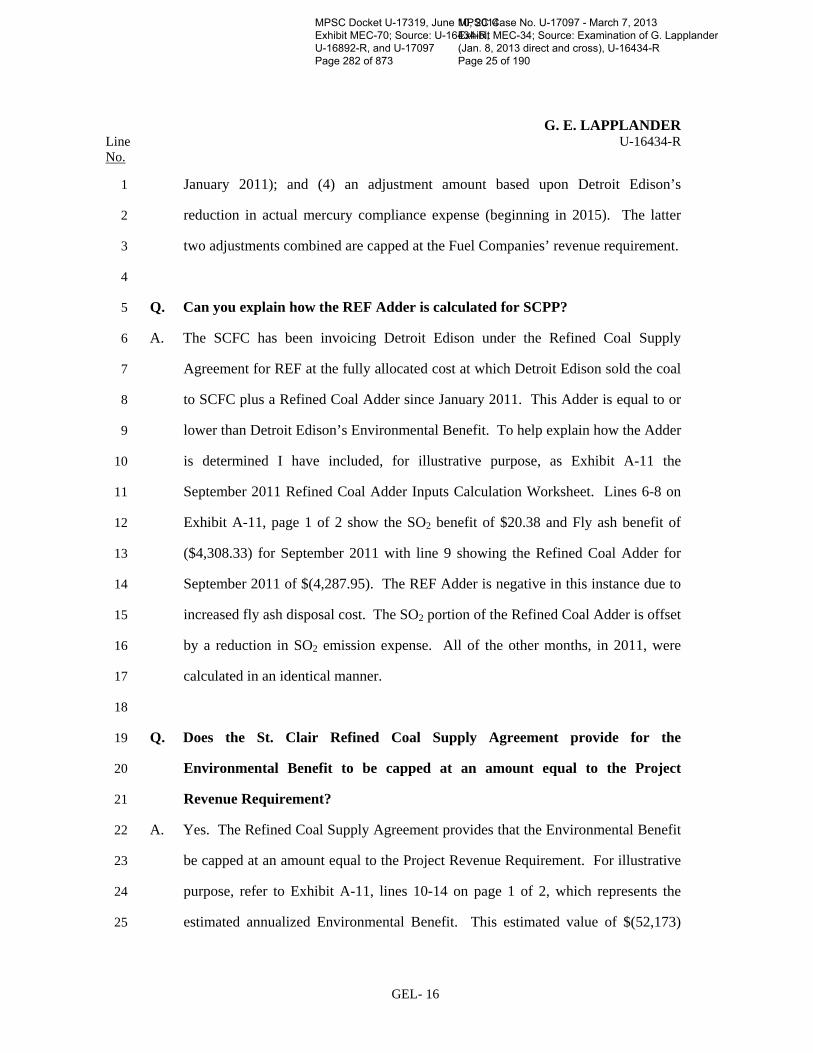

G. E. LAPPLANDER Line U-16434-R No.

GEL- 16

January 2011); and (4) an adjustment amount based upon Detroit Edison’s 1

reduction in actual mercury compliance expense (beginning in 2015). The latter 2

two adjustments combined are capped at the Fuel Companies’ revenue requirement. 3

4

Q. Can you explain how the REF Adder is calculated for SCPP? 5

A. The SCFC has been invoicing Detroit Edison under the Refined Coal Supply 6

Agreement for REF at the fully allocated cost at which Detroit Edison sold the coal 7

to SCFC plus a Refined Coal Adder since January 2011. This Adder is equal to or 8

lower than Detroit Edison’s Environmental Benefit. To help explain how the Adder 9

is determined I have included, for illustrative purpose, as Exhibit A-11 the 10

September 2011 Refined Coal Adder Inputs Calculation Worksheet. Lines 6-8 on 11

Exhibit A-11, page 1 of 2 show the SO2 benefit of $20.38 and Fly ash benefit of 12

($4,308.33) for September 2011 with line 9 showing the Refined Coal Adder for 13

September 2011 of $(4,287.95). The REF Adder is negative in this instance due to 14

increased fly ash disposal cost. The SO2 portion of the Refined Coal Adder is offset 15

by a reduction in SO2 emission expense. All of the other months, in 2011, were 16

calculated in an identical manner. 17

18

Q. Does the St. Clair Refined Coal Supply Agreement provide for the 19

Environmental Benefit to be capped at an amount equal to the Project 20

Revenue Requirement? 21

A. Yes. The Refined Coal Supply Agreement provides that the Environmental Benefit 22

be capped at an amount equal to the Project Revenue Requirement. For illustrative 23

purpose, refer to Exhibit A-11, lines 10-14 on page 1 of 2, which represents the 24

estimated annualized Environmental Benefit. This estimated value of $(52,173) 25

MPSC Case No. U-17097 - March 7, 2013 Exhibit MEC-34; Source: Examination of G. Lapplander (Jan. 8, 2013 direct and cross), U-16434-R Page 25 of 190

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 282 of 873

G. E. LAPPLANDER Line U-16434-R No.

GEL- 17

(again this is negative due to increased fly ash disposal cost) is only used to 1

compare with SCFC’s Revenue Requirement to determine the Refined Coal Adder 2

as shown on lines 2-5. Line 2 is the estimated annual Environmental Benefit while 3

line 3 is the Revenue Requirement for the Project of $11,112,482. Line 5 compares 4

the Environmental Benefit with the Revenue Requirement to determine if the 5

Environmental Benefit should be capped at an amount equal to the Revenue 6

Requirement. Clearly the Environmental Benefit is lower and the Revenue 7

Requirement has no impact on the calculation of the Refined Coal Adder for 2011. 8

9

Q. What is the value of the Refined Coal Adder SO2 emission benefit for REF 10

consumed at SCPP for 2011? 11

A. The value of the Refined Coal Adder SO2 emission benefit for REF consumed at 12

SCPP for 2011 was $544. This value is the product of the allowance consumption 13

reduction and or allowances not consumed due to REF of 2,174 allowances and the 14

value of $0.25 per allowance. The allowance value of $0.25 per allowance is the 15

actual revenue price realized by the sale of the allowances not consumed as 16

discussed by Company Witness Ms. Wojtowicz. There is no impact on PSCR costs 17

for SCPP since the value of the Refined Coal Adder SO2 benefit is offset by the 18

value of reduced SO2 emissions. As described later in my testimony, Detroit 19

Edison retains the value of reduced emissions for the Monroe REF project. 20

21

Q. Can you summarize the details of the other arrangements? 22

A. Yes. An arrangement has been made for environmental indemnity protection 23

included in the Environmental Indemnity Agreement. Detroit Edison has also 24

entered into a License and Services Agreement where Detroit Edison has agreed to 25

MPSC Case No. U-17097 - March 7, 2013 Exhibit MEC-34; Source: Examination of G. Lapplander (Jan. 8, 2013 direct and cross), U-16434-R Page 26 of 190

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 283 of 873

G. E. LAPPLANDER Line U-16434-R No.

GEL- 18

provide, for a fee, among other things, potable water, sanitary sewer and storm 1

water disposal to the Fuels Companies in order to make certain that Detroit Edison 2

is not subsidizing the Fuels Companies. 3

4

Q. Can you describe the REF arrangement at the Monroe Power Plant? 5

A. Yes. A number of activities have occurred including the sale of a portion of Detroit 6

Edison’s coal inventory to the MFC, coal handling and consulting activities have 7

been provided by Detroit Edison to the MFC, and the REF has been produced and 8

sold by the MFC to Detroit Edison for consumption. Unlike the arrangement 9

Detroit Edison has with the BRFC and SCFC where the price of REF is the fully 10

allocated cost at which Detroit Edison sold the coal to the Fuels Companies plus a 11

Refined Coal Adder, Detroit Edison has negotiated a Coal Fee Rate, payable to 12

Detroit Edison, based on the amount of REF consumed at the Monroe Power Plant. 13

The MFC will sell Detroit Edison refined coal at the fully allocated cost at which 14

Detroit Edison sold the coal to the MFC and MFC will pay a Coal Fee Rate to 15

Detroit Edison for all tons of REF coal purchased by Detroit Edison. Detroit 16

Edison’s PSCR customers will not only receive the benefit of the Coal Fee Rate but 17

also the benefits of reduced working capital from not carrying a portion of the coal 18

inventory, the benefit of reduced SO2 emissions and the benefit of reduced cost of 19

mercury compliance. 20

21

Q. Why is the REF arrangement at the Monroe Power Plant different than the 22

arrangements at the St. Clair and Belle River Power Plants? 23

A. The refined coal production tax credit was enacted by Congress to encourage 24

investment in emissions control technologies prior to the time such technologies 25

MPSC Case No. U-17097 - March 7, 2013 Exhibit MEC-34; Source: Examination of G. Lapplander (Jan. 8, 2013 direct and cross), U-16434-R Page 27 of 190

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 284 of 873

G. E. LAPPLANDER Line U-16434-R No.

GEL- 19

would otherwise be required by law. During 2011, subsequent to the time the 1

arrangements with BRFC and SCFC were negotiated, the IRS issued guidance that 2

certain rules under the Internal Revenue Code should not be applied to transactions 3

that generate targeted tax incentives in a manner inconsistent with the 4

Congressional intent for creating those incentives. My understanding is that this 5

guidance provided that reduced emissions fuel projects no longer had to generate a 6

2-3% internal rate of return to earn the production tax credits. It was this 7

requirement that had prevented the Coal Fee Rate structure from being offered on 8

the arrangements at the St. Clair and Belle River Power Plants. Without this 9

requirement, Detroit Edison was able to negotiate for the Coal Fee Rate structure 10

for REF consumed at the Monroe Power Plant. 11

12

Q. Can you summarize the details of the Refined Coal Supply from the MFC? 13

A. Yes. The MFC will supply REF to Detroit Edison on a “just in time” delivery 14

basis. The MFC’s REF facilities have been constructed on the plant site and are 15

integrated into the Company’s coal delivery process. The cost of the REF will be 16

based upon the fully allocated cost at which Detroit Edison sold the coal to the 17

MFC. 18

19

Q. Can you summarize the Coal Inventory Purchase by the MFC? 20

A. Yes. At closing in November 2011, Detroit Edison sold 250,000 tons of its coal 21

inventories at the plant to the MFC at book cost plus another 48,000 tons of coal-in-22

transit also at book cost for a total of $15.6 million. Subsequently, MFC will take 23

ownership of all coal destined for the Monroe Power Plant, in transit, as it enters the 24

rail car for rail delivered coal and FOB vessel for water born deliveries from 25

MPSC Case No. U-17097 - March 7, 2013 Exhibit MEC-34; Source: Examination of G. Lapplander (Jan. 8, 2013 direct and cross), U-16434-R Page 28 of 190

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 285 of 873

G. E. LAPPLANDER Line U-16434-R No.

GEL- 20

MERC. Notwithstanding these sales, the coal always remains under the supervision 1

and control of Detroit Edison and MERC (no Fuels Company employees are 2

involved in any process other than operation of the Fuels Companies’ separate 3

equipment and facilities) and Detroit Edison’s and MERC’s books and records are 4

maintained separately from MFC’s books and records. MFC will purchase the coal 5

at the same price Detroit Edison pays its coal suppliers and will reimburse Detroit 6

Edison for all transportation costs. Detroit Edison customers will ultimately benefit 7

from reduced costs associated with not carrying the relevant fuel inventory on its 8

books when base rates are reset. At the end of the 10-year REF consumption 9

period, the remaining coal inventory will be resold to Detroit Edison at the MFC’s 10

book cost. 11

12

Q. Can you summarize the details of the other arrangements? 13

A. Yes. The coal handling and consulting services will be provided by Detroit Edison 14

to the MFC to support the processing and delivery of REF to the Monroe Power 15

Plant. These functions, which Detroit Edison has always performed, cover all fuel 16

procurement, fuel processing and fuel handling activities including consumption 17

forecasting, specification of coal quality, coal purchasing, coal transportation, coal 18

shipment scheduling, receiving and unloading of coal, coal sampling and analysis, 19

coal stockpile management and maintenance, etc. As stated previously, the MFC 20

will pay a Coal Fee Rate for these coal handling and consulting services. 21

22

In addition, an arrangement has been made for environmental indemnity protection 23

included in the Environmental Indemnity Agreement. Detroit Edison has also 24

entered into a License and Services Agreement where Detroit Edison has agreed to 25

MPSC Case No. U-17097 - March 7, 2013 Exhibit MEC-34; Source: Examination of G. Lapplander (Jan. 8, 2013 direct and cross), U-16434-R Page 29 of 190

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 286 of 873

G. E. LAPPLANDER Line U-16434-R No.

GEL- 21

provide for a fee, among other things, potable water, sanitary sewer and storm water 1

disposal to the MFC in order to make certain that Detroit Edison is not subsidizing 2

the MFC. 3

4

Q. Are the REF business arrangements at St. Clair and Belle River Power Plants 5

reasonable and prudent? 6

A. Yes. The REF business arrangements allow Detroit Edison customers to receive 7

cost reductions through their base rates. The REF adder will never exceed the 8

environmental benefit realized by the customer. Detroit Edison’s customers benefit 9

without assuming any technology, tax or capital risk. 10

11

Q. Is the REF business arrangement at the Monroe Power Plant reasonable and 12

prudent? 13

A. Yes. The REF business arrangement allows Detroit Edison customers to receive 14

cost reductions through their base rates while PSCR customers realize lower cost 15

through the Coal Fee Rate paid by the MFC to Detroit Edison and the value of 16

reduced SO2 and reduced mercury compliance costs. Detroit Edison’s customers 17

benefit without assuming any technology, tax or capital risk. 18

19

Q. Does this complete your direct testimony? 20

A. Yes, it does. 21

MPSC Case No. U-17097 - March 7, 2013 Exhibit MEC-34; Source: Examination of G. Lapplander (Jan. 8, 2013 direct and cross), U-16434-R Page 30 of 190

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 287 of 873

STATE OF MICHIGAN

BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION

In the matter of the Application of ) THE DETROIT EDISON COMPANY ) For Reconciliation of its Power ) Case No. U-16434-R Supply Cost Recovery Plan for the ) 12 month- Period Ending ) December 31, 2011 )

REBUTTAL TESTIMONY

OF

GARY E. LAPPLANDER

MPSC Case No. U-17097 - March 7, 2013 Exhibit MEC-34; Source: Examination of G. Lapplander (Jan. 8, 2013 direct and cross), U-16434-R Page 31 of 190

MPSC Docket U-17319, June 10, 2014 Exhibit MEC-70; Source: U-16434-R, U-16892-R, and U-17097 Page 288 of 873

THE DETROIT EDISON COMPANY REBUTTAL TESTIMONY OF GARY E. LAPPLANDER

Line No.

GEL Rebuttal - 1

Q. Are you the same Gary E. Lapplander who previously offered testimony in this 1

proceeding? 2

A. Yes, I am. 3

4

Q. Mr. Lapplander, what is the purpose of your testimony in this case? 5

A. The purpose of my testimony is to rebut the testimonies of Witness Mr. Crandall on 6

behalf of the Michigan Community Action Agency Association (MCAAA), 7

Witness Mr. McGarry, Sr. on behalf of the Attorney General Bill Schuette (AG) 8

and Witness Mr. Sansoucy on behalf of the Michigan Environmental Council and 9

the Natural Resources Defense Council (MEC), which pertain to Reduced 10

Emissions Fuel (REF). 11

12

Q. Are you sponsoring any rebuttal exhibits? 13

A. Yes. I am sponsoring the following exhibits: 14

Exhibit Description 15

A-25 U-16892 Discovery Question/Response MCAAA/DE 1.52 16

A-26 U-16892 Discovery Question/Response MCAAA/DE 1.25d 17

A-27 U-16892 Discovery Question/Attachment MCAAA/DE 1.30 18

A-28 U-16434-R Discovery Question/Attachment MCAAA/DE 31j 19