Embed Size (px)

Citation preview

Mueller Industries Inc.

Amanda Miller – [email protected] Park Hunter – [email protected]

Shyla Walton – [email protected] Austin Head – [email protected]

Josh Jacobsen – [email protected]

2

Table of Contents

Executive Overview……………………………………………………………………………………………….6 Company Overview………………….………………………………………………………………………….13 Business & Industry Analysis…………..…………………………………………………………..……….15 Five Forces Model……………………………………………………………………………………………….16 Rivalry Among Existing Firms……………………………………………………………………..16 Industry Growth……………………………….……………………………………………..17 Concentration…………………………….……………………………………………………19 Differentiation…………………………………………………………………….…………..21 Switching Costs……………………………………………………………………………….22 Economies of Scale………………..………………………………………………………..22 Learning Economies………………..……………………………………………………….23 Fixed to Variable Costs……………..……………………………………………………..24 Excess Capacity…………………………………………………..…………………………..25 Exit Barriers………………………………………………….…………………………………26 Conclusion…………………………………………………..………………………………….26 Threat of New Entrants…………………………….……………………………………………….27 Economies of Scale……………………………………….…………………………………27 First Mover Advantages………………………………………….………………………..28 Channels of Distribution & Relationships…………….……………………………..29 Legal Barriers………………………………………………….………………………………29 Conclusion…………………………………………………….………………………………..30 Threat of Substitute Products……………………………………………………………………..31 Relative Price and Performance…………………………………………………………31 Buyers Willingness to Switch…………………………………………………………….32 Conclusion………………………………………………………………………………………32 Bargaining Power of Customers…………………………………………………………………..33 Price Sensitivity……………………………………………………………………………….33 Relative Bargaining Power………………………………………………………………..34 Conclusion………………………………………………………………………………………35 Bargaining Power of Suppliers…………………………………………………………………….36 Conclusion………………………………………………………………………………………37 Five Forces Conclusion…………………………………………………………………………………………37 Key Success Factors of the Industry………………………………………………………………………38 Economies of Scale……………………………………...………………………..………………….38 Economies of Scope…………………………………………………………..……………………...39 Efficient Methods and Cost Control………………..……………………………………………41 Input & Distribution Costs…………………………………………..……………………………..42 Research, Development & Advertising…………………………..…………………………….43 Summary………………………..…………………………………………..……………………………44 Competitive Advantage Analysis……………………………………………………………………..…….45 Large Scale Production……………………….……………………………………………………..45

3

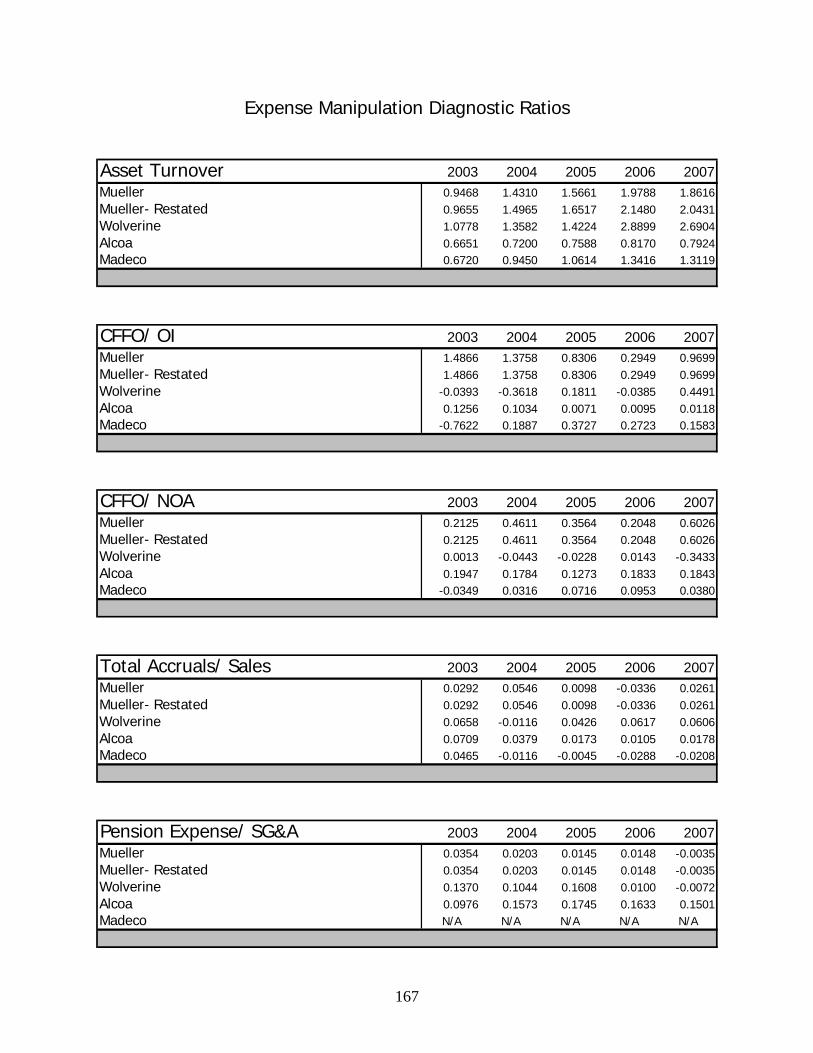

Production Efficiency……………………….…………………………………………………………46 Other Advantages…………………………….……………………………………………………….48 Summary………………………………………………………………………………………………….48 Accounting Analysis…………………………………………………………………………………………….49 Key Accounting Policies………………………………………….…………………………………………...50 Goodwill………………………………………………………..………………………………………….50 Pension Plan & Retirement Compensation………..………………………………………….52 Hedging Activities……………………………………….…………………………………………….53 Management of Fixed Costs…………………………..……………………………………………54 Capital & Operating Leases……………………….………………………………………………..55 Degree of Potential Flexibility……………….………………………………………………………………56 Goodwill………………………………………………..………………………………………………….56 Pension Plan & Retirement Compensation…….……………………………………………..57 Hedging Activities……………………………………………………………………………………..58 Management of Fixed Costs………………….……………………………………………………59 Capital & Operating Leases…………………………………………………………………………59 Actual Accounting Strategy…………………………………………………………………………….……60 Goodwill……………………………………………………………………………………………………60 Pension Plan & Retirement Compensation…………..……………………………………….62 Hedging Activities………………………………………………………………………………………63 Management of Fixed Costs……………………..…………………………………………………64 Capital & Operating Leases…………………………………………………………………………64 Evaluate Quality of Disclosure………………………………………………………………………………66 Qualitative Analysis………………………………………..……………………………………………………66 Goodwill……………………………………………………….…………………………………………..66 Pension Plan & Retirement Compensation……………………………………………………67 Hedging Activities………………………………………………………………………………………69 Management of Fixed Costs…………………………………………..……………………………70 Capital & Operating Leases…………………………………………………………………………71 Quantitative Analysis……………………………………………………………………………………………72 Expense Manipulation Diagnostics…………….…………………………………………………72 Asset Turnover………………..………………………………………………………………72 CFFO/OI………………………………………………….………………………………………74 CFFO/Net Operating Assets………………………………………………………………75 Total Accruals/Sales…………………………………………………………………………76 Pension Expense/ SG&A……………………………………………………………………77 Other Employment Expense/ SG&A……………..…………………………………….78 Conclusion………………………………………………………………………………………79 Revenue Manipulation Diagnostics………………………………………………………………80 Net Sales/ Cash from Sales………………………….……………………………………80 Net Sales/ Net Accounts Receivable……………..……………………………………81 Net Sales/ Inventory………………………………..………………………………………83 Conclusion………………………………………………………………………………………84 Potential Red Flags……………………………………………..………………………………………………85

4

Undo Accounting Distortions………………………………………………………………………………..85 Financial Analysis, Forecasting & Cost of Capital Estimation…….………………………………88

Liquidity Ratio Analysis………………………………………….……..……………………………88 Current Ratio………………………………………..…………………………………………89 Quick Asset Ratio…………………………………………………………………………….90 Accounts Receivable Turnover……………….…………………………………………91 Days in Accounts Receivable…………………………………………………………….92 Inventory Turnover………………………………………………………………………….93 Days Supply of Inventory…………………………………………………………………94 Working Capital Turnover…………………………………………………………………95 Cash to Cash Cycle………………………………………………………………………….96 Conclusion……………………………………………………………………………………..97

Capital Structure Ratios……………………………….…………………………………………….98 Debt to Equity...................................................................................98

Times Interest Earned…………………………………………………………………….100 Debt Service Margin…………..…………………………………………………………..101 Credit Risk…………………….………………………………………………………………102 Conclusion………………………………….…………………………………………………103 Profitability Ratio Analysis…………………………………………………………………………104 Gross Profit Margin…………………………………………………………………………104 Operating Expense Ratio…………………………………………………………………105 Operating Profit Margin…………………………………………………………………..106 Net Profit Margin………………..………………………………………………………….107 Asset Turnover………………………………………………………………………………108 Return on Assets…………..……………………………………………………………….109 Return on Equity……………………………………………………………………………110 Internal Growth Rate………..……………………………………………………………111 Sustainable Growth Rate…………………………………………………………………112 Conclusion…………………….………………………………………………………………113 Financial Statement Forecasting……………….…………………………………………………………114 Income Statement……………….………………………………………………………………….114 Balance Sheet………………………..……………………………………………………………….121 Statement of Cash Flows………….………………………………………………………………127 Cost of Capital Estimation………………………..…………………………………………………………132 Cost of Equity………………………….………………………………………………………………132 Backdoor Cost of Equity……………………………………………………………………………135 Cost of Debt……………………………………………………………………………………………136 Weighted Average Cost of Capital………………….………………………………………….138 Valuation Methods…………….……………………………………………………………………………….140 Method of Comparables……………………………………………….…………………………………….141 Price to Earnings Trailing…………….……………………………..……………………………142 Price to Earnings Forward………….…………………………………………………………….143 Price to Book............………………………………………………………………………………143 Dividends to Price…………………….……………………………………………………………..144

5

Price Earnings Growth…………………………..………………………………………………….144 P/EBITDA……………………………..…………………………………………………………………145 P/FCF………………………………..……………………………………………………………………145 EV/EBITDA………………………………………………………………………………………………146 Conclusion………………..…………………………………………………………………………….146 Intrinsic Valuation Models………………………………..…………………………………………………148 Discounted Dividends Model……………………………………………………………………..149 Discounted Free Cash Flows……………………………………………………………………..152 Residual Income………………………………………………………………………………………156 Long Run Residual Income……………………………………………………………………….159 Abnormal Earnings Growth……………………….………………………………………………163 Conclusion………………………….…………………………………………………………………..165 Appendix………………………………………………………………………………………………………….166 Sales Manipulation Diagnostics…………………………………………………..……………..166 Expense Manipulation Diagnostics………………………………..……………………………167 Effects on Restatement of Goodwill…………………………….…………………………….169 Liquidity Ratios…………………………………………….………………………………………….173 Profitability Ratios…………………………………….……………………………………………..175 Capital Structure Ratios………………….………………………………………………………..177

Altman’s Z-score……………………………………………………………………………………..178 Cost of Capital Regression Outputs………………….………………………………………..189 Cost of Equity, Debt & WACC………………………………..………………………………….194 Method of Comparables Tables…………………..…………..………………………………..195 Intrinsic Valuations…………………………….…………………………………………………….197 References………………………………………………………………………………………………………205

6

Executive Summary

Investment Recommendation: Overvalued Sell as of November 1st, 2008

52 Week Range: 2003 2004 2005 2006 2007Revenue: $2.74 B As Stated 4.57 2.48 3.21 4.23 4.09Market Capitalization: $865.27 M Restated 4.51 2.53 3.20 4.29 4.18Shares Outstanding: $37.14 M Percent Institutional Ownership: 96.10%

As Stated RestatedBook Value Per Share: $19.13 $15.77 As Stated RestatedROE: 19.61% 23.58% Trailing P/E: $12.23 $10.39ROA: 9.10% 9.94% Forward P/E: $41.86 N/A

P/B: $10.62 $8.75D/P: $6.65 N/A

R^2 Beta Ke P.E.G: - N/A3 Month 36.03% 1.49 18.31% P/EBITDA: $19.54 $17.252 Year 36.05% 1.49 18.28% P/FCF: $20.02 N/A5 Year 35.89% 1.49 18.22% EV/EBITDA: $12.38 $9.927 Year 35.81% 1.48 18.19%10 Year 35.72% 1.48 18.16%

As Stated RestatedUpper and Lower Ke: Discounted Dividends: $10.12 N/APublished Beta: 0.88 Discounted FCF: $35.28 $39.57Back Door Ke: 14.52% Residual Income: $10.35 $10.09Cost of Debt: 5.99% Long Run Redisual Income: $14.33 $11.82WACC (BT) 12.02% A.E.G.: $7.16 N/AUpper and Lower WACC (BT)

Altman's Z-ScoresMLI - NYSE (Nov 1, 2008) $23.31

Cost of Capital Estimate (Including 2.3% Size Premium)

Current Market Share Price (Nov 1, 2008) $23.31

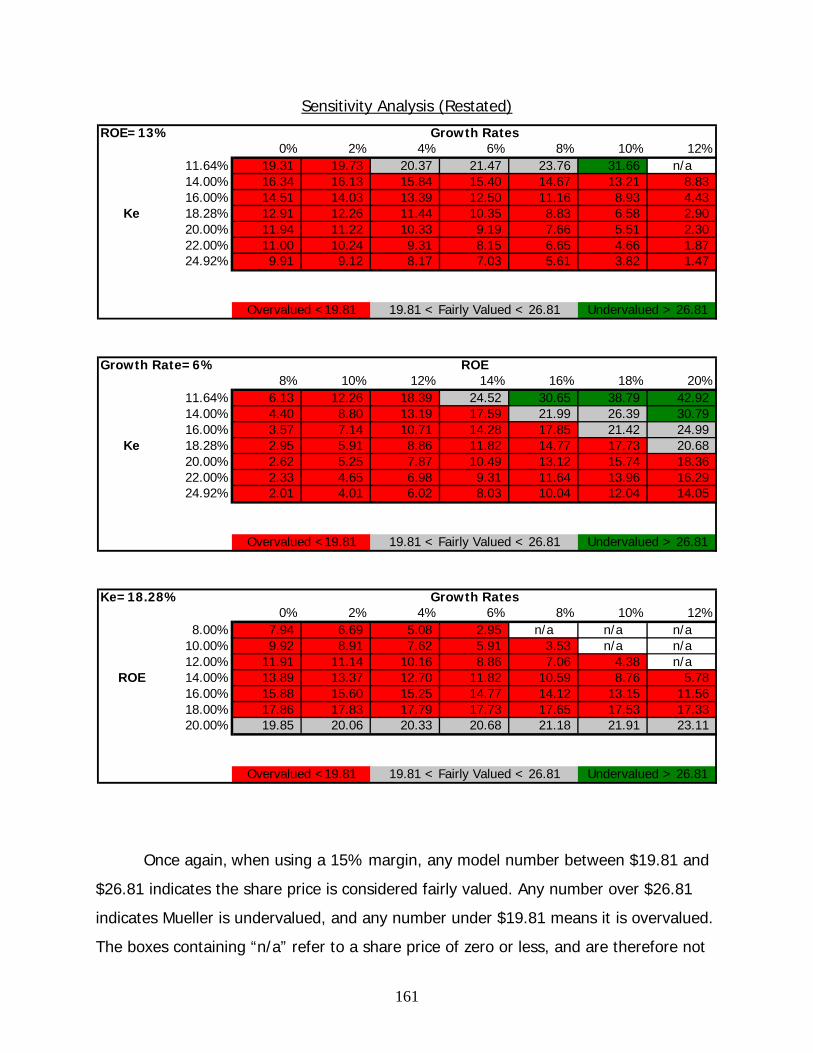

Financial Based Valuations

8.76% - 15.27%

11.64% - 24.92%

Intrinsic Valuations

$17.57 - $35.66

7

Industry Analysis Overview

Mueller competes in the metal fabrication industry and makes all types of pipes,

tubes, and fittings that are sold to a variety of customers across various industries. Our

analysis of the industry consists of Mueller and its three closest publicly traded

competitors: Alcoa, Madeco and Wolverine Tube Inc. Together these companies supply

firms from automotive and housing all of the way to aerospace and electrical industries.

As companies in the metal fabrication industry tend to make relatively simple and

generic products, cost becomes the main source of competition. Cost control and

operation management are imperative to being successful in this industry.

The five forces model allows us to identify threats that are present throughout

the industry as a whole and discuss the methods that are necessary for success. The

following is a brief summary of the model and its conclusions.

Results of the Five Forces Model

It is important to become familiar with the environment of a company’s

competition if one wishes to fairly evaluate it. Our discussion of the metal fabrication

industry illustrates the external matters a company will face. The model describes the

high concern of substitute products as each company makes more or less the same

products. It also suggests the unlikely occurrence of new entrants as the industry

requires a large amount of assets in order to be competitive. These and other concerns

are addressed in the industry analysis section.

Rivalry Among Existing Firms High

Threat of New Entrants Low

Threat of Substitute Products High

Bargaining Power of Customers High

Bargaining Power of Supplies Medium

8

Accounting Analysis Overview

The numbers that are published in the quarterly and annual reports are

supposed to accurately reflect the businesses activities of each company. There are

many regulations imposed by the SEC and GAAP as to how a company can account for

their processes. In an accounting analysis, the first step is to identify the key

accounting policies that can be examined to evaluate a company’s transparency. These

policies should be looked at closely as they provide potential for distortion and

manipulation that can shine a company in a false light.

We used revenue manipulation diagnostics ratios to demonstrate how current

assets and current liabilities relate to net sales. These ratios also help us determine if

there is anything out of the industry norm that could potentially be a “red flag” in the

financial statements. Most of the revenue manipulation diagnostics looked within the

industry norm. The only ratios that had stood out were the net sales divided by net

accounts receivables and net sales divided by inventory. However, we concluded that

both of these slight differences were due to fluctuating copper prices in the market and

did not qualify as a “red flag”.

We did identify one major red flag when examining Mueller’s accounting

practices, this being how the company accounts for goodwill. Over the past five years

Mueller has been involved in a number of mergers and acquisitions, thus adding to their

goodwill. However, they only impaired a small fraction of it. Goodwill does not last a

lifetime; in fact, it should really have a useful life of about five years. Since Mueller

keeps goodwill on their books for much longer than five years, we believe this

significantly distorts the true value of the firm. We undid this distortion by taking the

goodwill balance in 2003 and writing it off for the next five years, adjusting for new

mergers and acquisitions along the way. We restated Muller’s income statement and

balance sheet to reflect these changes. This helps give investors a better picture of the

true value of the firm.

9

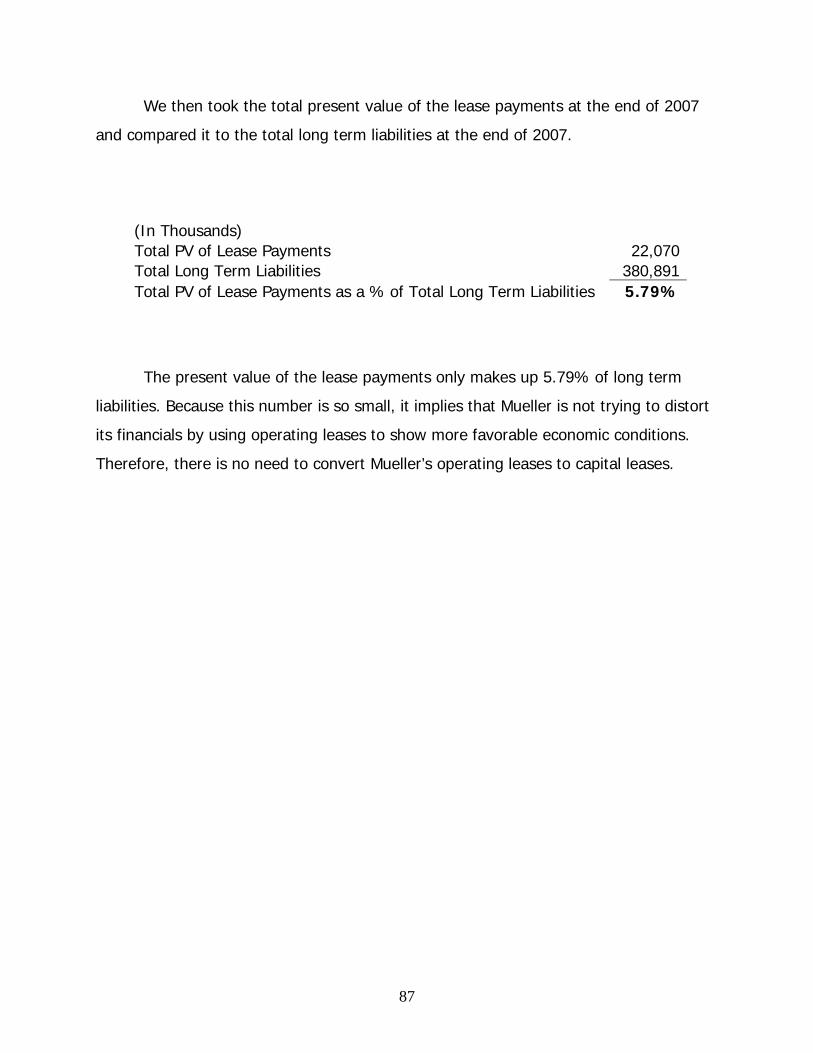

On the other hand, analysis of other policies allows us to verify Mueller’s ‘as

stated’ version. For instance, operating leases only account for 5.79% of total long term

liabilities and thus suggests that the company gives a fair view of its lease liabilities.

Likewise, the disclosure of hedging activities appears fair and reliable. The accounting

analysis section compares these and other accounting policies that will have an impact

on our valuation.

10

Financial Analysis, Forecasting and Cost of Capital Estimation

We begin the financial analysis by looking at a number of liquidity, profitability

and capital structure ratios. These ratios give us an idea of Mueller’s financial position

and allow us to put them up against their competitors. In doing so, we are able to see

what aspects the company excels at and in what aspects they are lacking. The day’s

supply of inventory is one that Mueller has to its advantage as it is able to turn

inventory into sales relatively quicker than its competitors.

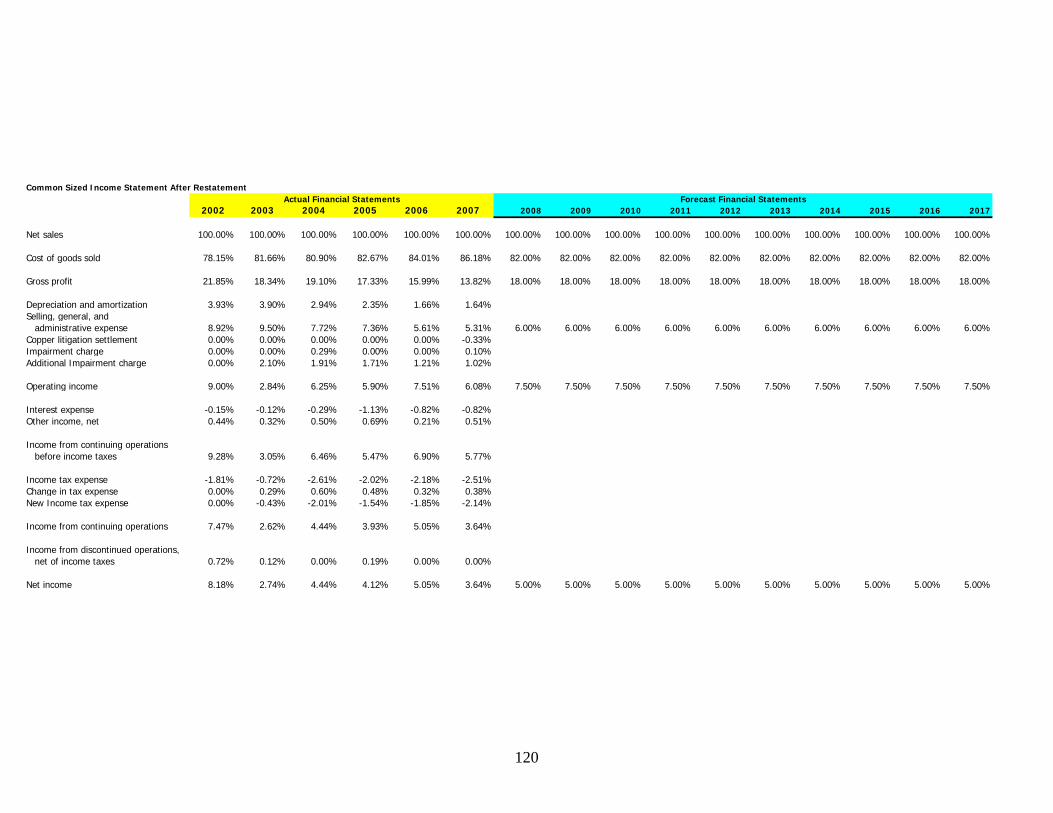

Profitability ratios measure how well a firm’s revenues cover its expenses. The

ratios show a percentage of sales, where sales equal 100%. Overall, Mueller was

efficient in covering its expenses compared to the metal fabrications industry. Mueller

was average using operating profit margin and net profit margin. Mueller outperformed

the industry average in gross profit margin, operating expense ratio, asset turnover,

return on assets, and return on equity. After analyzing these profitability ratios, we

concluded that Mueller has kept a strong competitive strategy over the past 5 years by

continually being either average or above average in the industry.

Liquidity ratios determine the ability at which a firm is able to handle its short

term assets, these assets include: cash, accounts receivables, and inventory. Knowing

how well a firm is able handle its short term assets also explains to analysts how well a

firm is able to pay of its short-term debt. In the case of Mueller, its liquidity ratios

seemed to be average in comparison to competitors within the metal fabrication

industry. The table below states how each of Mueller’s liquidity ratios did in comparison

to the industry average (above, equal, and below).

Results of Liquidity Ratios

Current Quick

Asset

A/R

Turnover

Days in

A/R

Inventory

Turnover

Days in

Inventory

Working

Capital

Turnover

Cash to

Cash Cycle

Above Above Below Below Above Above Below Equal

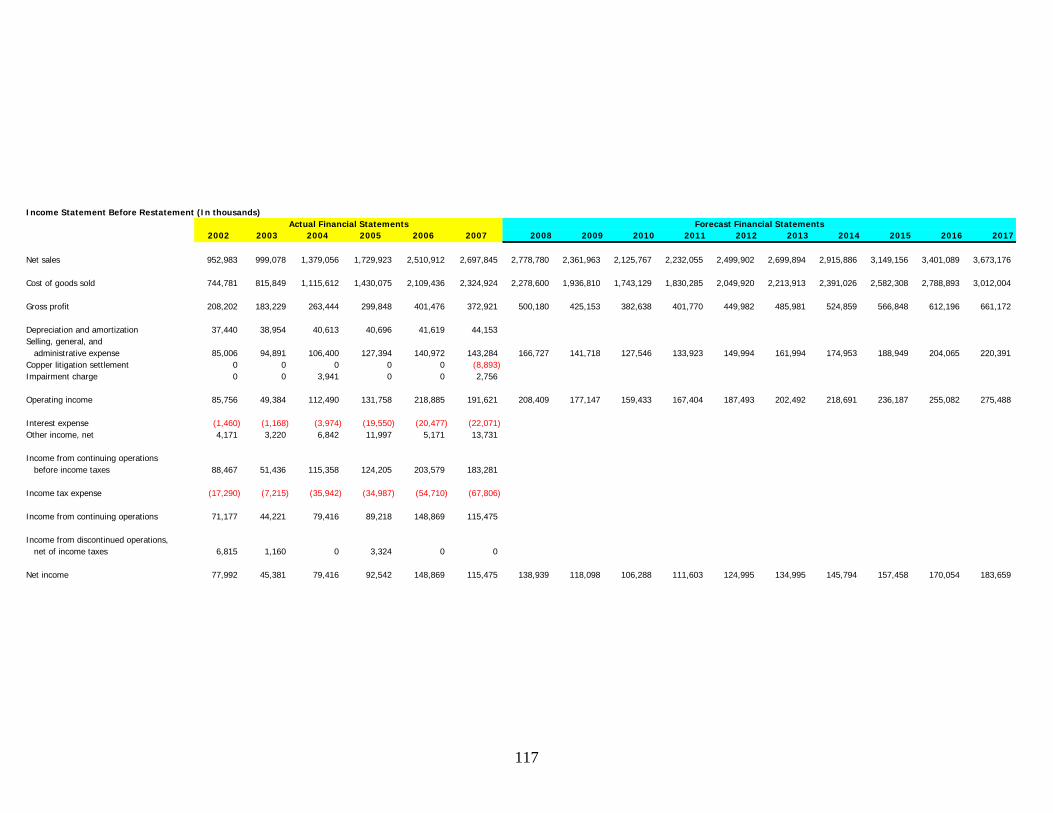

Forecasting financial statements are important as it allows us to get a view of the

company into the near future. Forecasting will never end up exactly as planned, but the

11

analysis of financial ratios helps us improve our accuracy. There are a number of

estimates that go into forecasting, such as growth rates, discount rates and prediction

of the economy in general. Forecasting financial statements involves looking at a

company’s current and past financial data to predict how the company will perform in

the future. The most crucial forecast was had to make was sales growth. We could not

simply look at Mueller’s sales growth over the past few years to predict the future,

mainly because the country is headed into a recession which is sure to affect Mueller’s

revenues. Therefore, we looked back at Mueller’s sales growth during the last major

recession to see how the company was affected. We mirrored our sales growth based

off of these numbers, but assumed Mueller would be hit slightly harder by this

recession. Also, a lot of our forecasts were based upon our previously calculated

financial ratios. For example, we used the asset turnover ratio to link the income

statement and balance sheet. Lastly, we forecasted the statement of cash flows, where

we forecasted out cash flow from operations, cash flow from investing activities, and

dividends. It is also important to note we forecasted out Mueller’s restated financial

statements as well since the changes we made to goodwill significantly altered Mueller’s

financial statements.

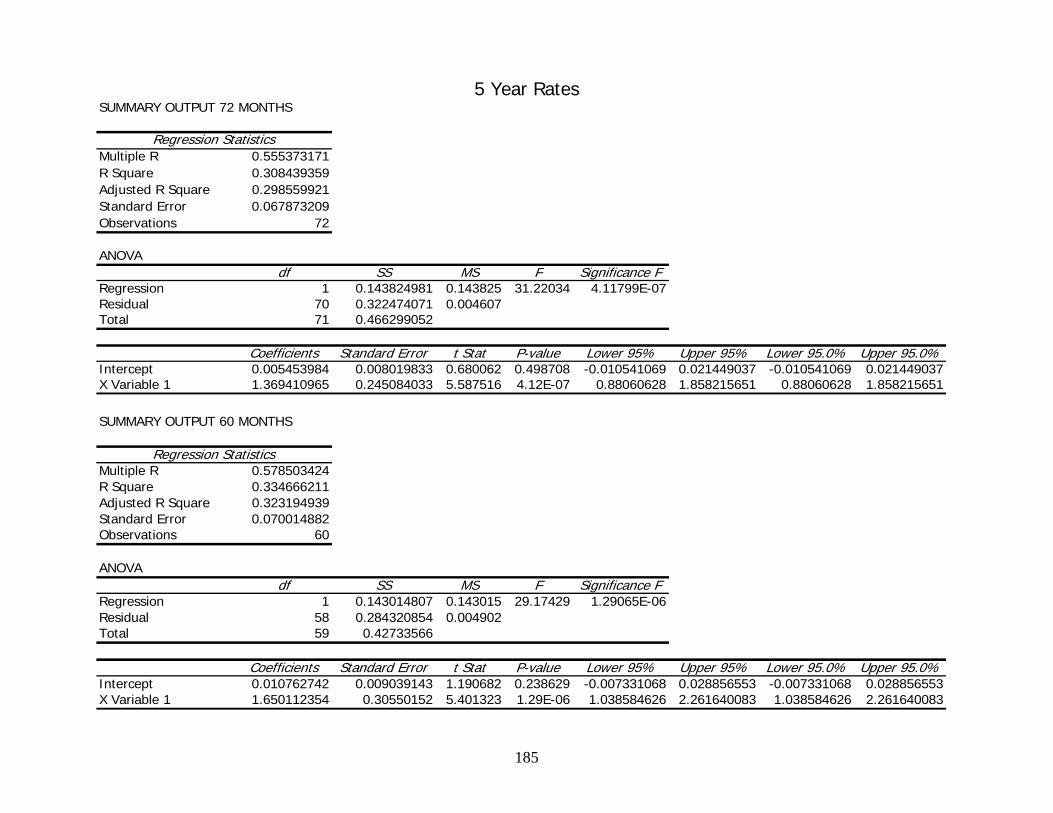

The final subject discussed in this section is the cost of capital for Mueller. This is

the return that investors expect to receive for investing in Mueller’s stock. We calculated

this return by running a regression of U.S. Treasury rates and S&P 500 returns over the

last seven years. Using multiple periods and their treasury rates, we are able to

estimate the beta, or risk for investing with Mueller specifically. With these pieces in

place, we were given an estimated cost of capital for Mueller Industries of 18.28%. This

rate serves as our discount rate in the following section of valuation analysis. Full

discussion of financial ratios, forecasting and cost of capital is disclosed in the

corresponding section.

12

Valuation Analysis

Our method of valuation for Mueller Industries can be divided into two parts.

First, the method of comparables allows us to derive a share price for Mueller based on

the performance of its competitors. Ratios such as the price to earnings ratio and price

to book ratio are calculated for each competitor, and by setting Mueller equal to the

industry average, we can solve for the share price of each equation and thus estimate

Mueller’s value. This method does have significant flaws in that it prices the company

solely on the performance of its competitors. This means that any competitive

advantage that Mueller may have can be overlooked if it is not involved in the ratio.

With this is mind, we found the method of comparables to be less useful than the

intrinsic valuation models.

The intrinsic valuation models hold more weight in our determination of the

value of Mueller as they are based on the actual operations of the company instead of

comparisons to competitors. Our forecasts played a huge part in these valuations as the

share price was based on the present value of future financial estimations. Because

these forecasts are based on multiple estimates, we used five different models before

concluding on Mueller as being an overvalued company. Out of the five models, the

discounted free cash flow model was the only one that did not give Mueller and

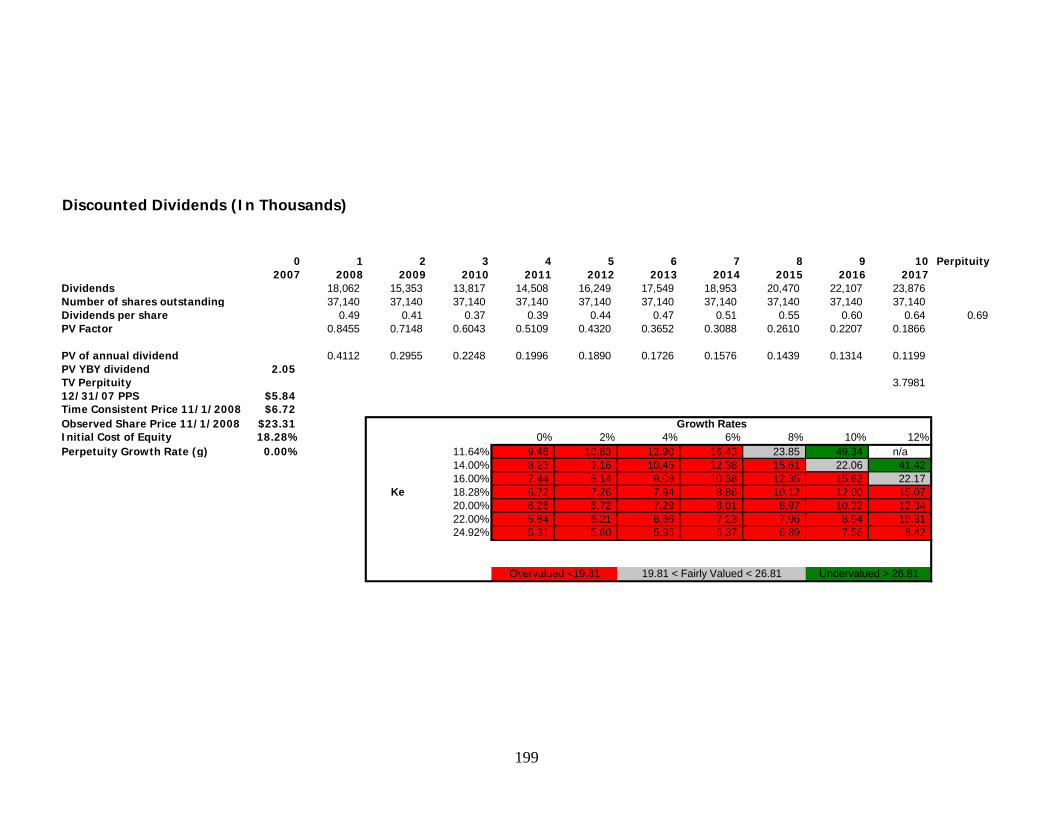

overvalued rating. Models such as the discounted dividend model and residual income

model use the cost of equity as the discount rate to turn future estimates into present

value. In models that use net income as a starting point (an after tax figure), our

weighted average cost of capital before tax is used as the discount rate. In turning to

our valuation section, one can see that Mueller appears to be overvalued and

individuals holding shares would be advised to sell them.

13

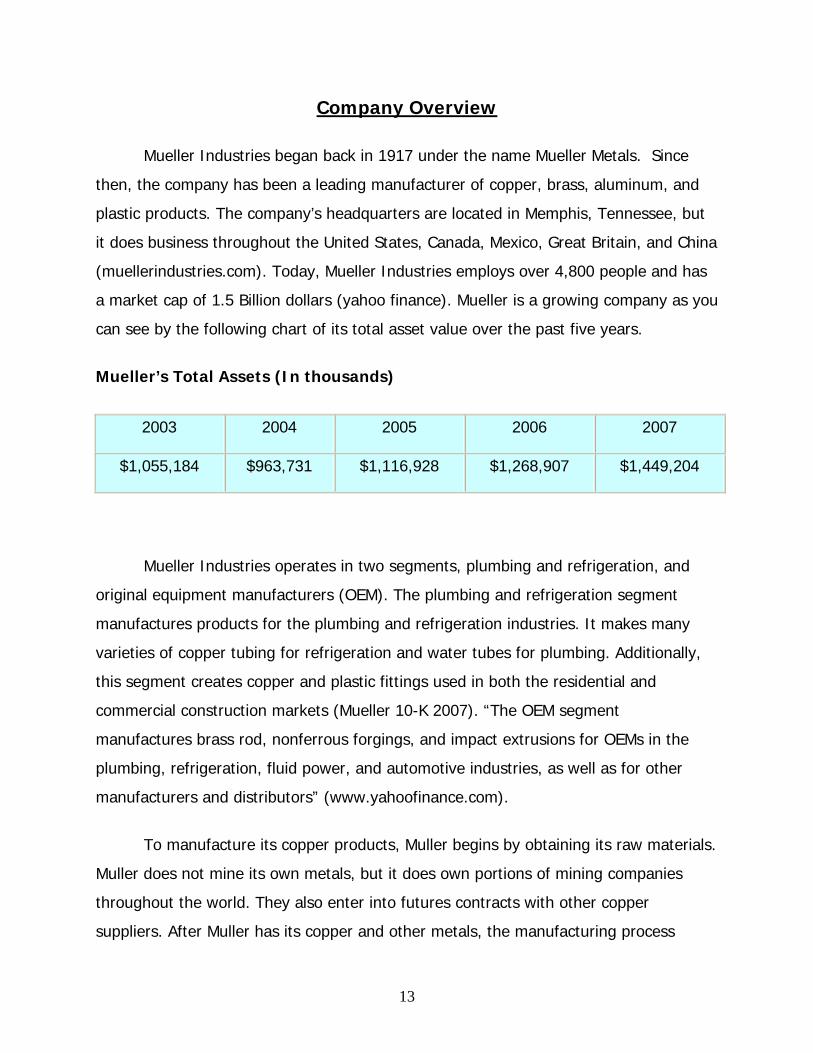

Company Overview

Mueller Industries began back in 1917 under the name Mueller Metals. Since

then, the company has been a leading manufacturer of copper, brass, aluminum, and

plastic products. The company’s headquarters are located in Memphis, Tennessee, but

it does business throughout the United States, Canada, Mexico, Great Britain, and China

(muellerindustries.com). Today, Mueller Industries employs over 4,800 people and has

a market cap of 1.5 Billion dollars (yahoo finance). Mueller is a growing company as you

can see by the following chart of its total asset value over the past five years.

Mueller’s Total Assets (In thousands)

2003 2004 2005 2006 2007

$1,055,184 $963,731 $1,116,928 $1,268,907 $1,449,204

Mueller Industries operates in two segments, plumbing and refrigeration, and

original equipment manufacturers (OEM). The plumbing and refrigeration segment

manufactures products for the plumbing and refrigeration industries. It makes many

varieties of copper tubing for refrigeration and water tubes for plumbing. Additionally,

this segment creates copper and plastic fittings used in both the residential and

commercial construction markets (Mueller 10-K 2007). “The OEM segment

manufactures brass rod, nonferrous forgings, and impact extrusions for OEMs in the

plumbing, refrigeration, fluid power, and automotive industries, as well as for other

manufacturers and distributors” (www.yahoofinance.com).

To manufacture its copper products, Muller begins by obtaining its raw materials.

Muller does not mine its own metals, but it does own portions of mining companies

throughout the world. They also enter into futures contracts with other copper

suppliers. After Muller has its copper and other metals, the manufacturing process

14

begins. This consists of casting, extruding, drawing, forming, joining and finishing.

Through this process, the copper is transformed into finished products to meet the

needs and demands of Muller’s customers.

Mueller Industries competes with various companies in the metal fabrication

industry. Some of its competitors include Wolverine Tube Inc. (WLVT.OB), Madeco S.A.

(MAD), and Alcoa Inc. (AA). Wolverine is Mueller’s most direct competitor because both

companies create copper, aluminum, and brass products for the housing and

construction industries. While not direct competitors, Madeco and Alcoa also compete

with Mueller across certain product lines. Madeco, located in Chile, manufactures and

sells products created from copper, aluminum, and related metals, while Alcoa produces

mainly aluminum products (Madeco and Alcoa 10-Ks 2007).

While the industry is highly competitive, the sales growth among the firms is

very inconsistent as shown in the graph below. All the companies show similar zigzag

patterns of sales growth from 2004 to 2007. This means sales decreased, increased,

and then decreased again across all firms. From this, it clear that there has been an

inconsistency in the market over the past few years. There is nothing an individual

company is doing to cause such fluctuations, but rather the conditions in the industry or

economy are to blame. There is a large decrease in sales growth from 2006- 2007,

mainly because of the United State’s declining economy. Since all the firms in this

industry are very “sensitive to changes in general economic conditions, including, in

particular, conditions in the housing and commercial construction industry” (Mueller’s

2008 10-K 2008, Pg 11), they will all be affected by the recession. Sales will most likely

continue to decline for the next few years.

15

Sales Growth

-20.00%-10.00%

0.00%10.00%20.00%30.00%40.00%50.00%60.00%70.00%

2004 2005 2006 2007

Year

Sale

s gr

owth

as

perc

anta

ge

MuellerWolverineAlcoaMadecoIndustry

Business and Industry Analysis

Mueller produces various pipes, tubes and accessories that are sold to

wholesalers of industries with residential/commercial construction, refrigeration, heating

and plumbing involvement. Like its competitors in the industry, a focus is held on cost

leadership and large scale production as this is the best way to achieve stability in the

market. Maintaining strong relationships with customers and suppliers is important as

there are multiple choices for each to do business with. This is going to be very

important now, since the United States is in a recession. Competition among firms in

the industry is going to be extremely high and most everyone will see a decline is sales

for the next few years. It will be harder for companies to focus on cost leadership and

large scale production, especially when their costs for raw materials and such are going

up as well. The industry as a whole is dependent on prices of raw materials and inputs

that are used by all competitors. Further analysis of how the industry competes on

these and other variables of concern are discussed below.

16

Five Forces Model

When valuing a firm, it is important to understand the nature of the industry it

competes in. The five forces model allows analysts to identify and examine five

competitive forces that shape the industry. The model shows that when analyzing the

degree of actual and potential competition, you need to be aware of the rivalry among

existing firms, the threat of new entrants, and the threat of substitute products. It also

takes into the account the bargaining power of customers and suppliers. With these

five forces identified, an analyst can fully understand the competitive nature of the

industry and the things that create value. The flowing table shows our analysis of the

five forces impacting the metal fabrication industry, and the degree of competition

produced by each one.

Results of the Five Forces Model

Rivalry Among Existing Firms High

Threat of New Entrants Low

Threat of Substitute Products High

Bargaining Power of Customers High

Bargaining Power of Supplies Medium

Rivalry among Existing Firms

When applying the Five Forces Model in the valuation of a corporation, one must

contemplate the rivalry amongst existing firms in order to achieve a complete industry

analysis. The rival among existing firms is measured by nine significant categories,

these being: Industry growth, Concentration, Differentiation, Switching costs, Scale,

Learning Economies, Fixed-Variable Costs, Excess Capacity, and Exit Barriers. In using

these nine distinct categories we hope to express our corporation’s industry as a whole,

17

whether that may be by the pricing of our products compared to those of our

competitors, or by some other non-price related differentiation.

Industry Growth

The growth of an industry has a major role in determining how a corporation

must function when it comes to competing with other firms. For example, existing

firms entrenched in an industry booming with growth are less likely to have to strongly

compete with each other in order grow themselves. The opposite of this situation being

if an industry’s growth is in the decline or remaining constant, then the firms within the

industry will have to battle for their individual market share. The best way of measuring

an industry’s growth is by breaking down the total number of sales over the past five

years from all the existing firms involved in the industry and comparing each firm’s

annual percentage change.

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

Gro

wth

%

2004 2005 2006 2007

Year

Industry Sales Growth

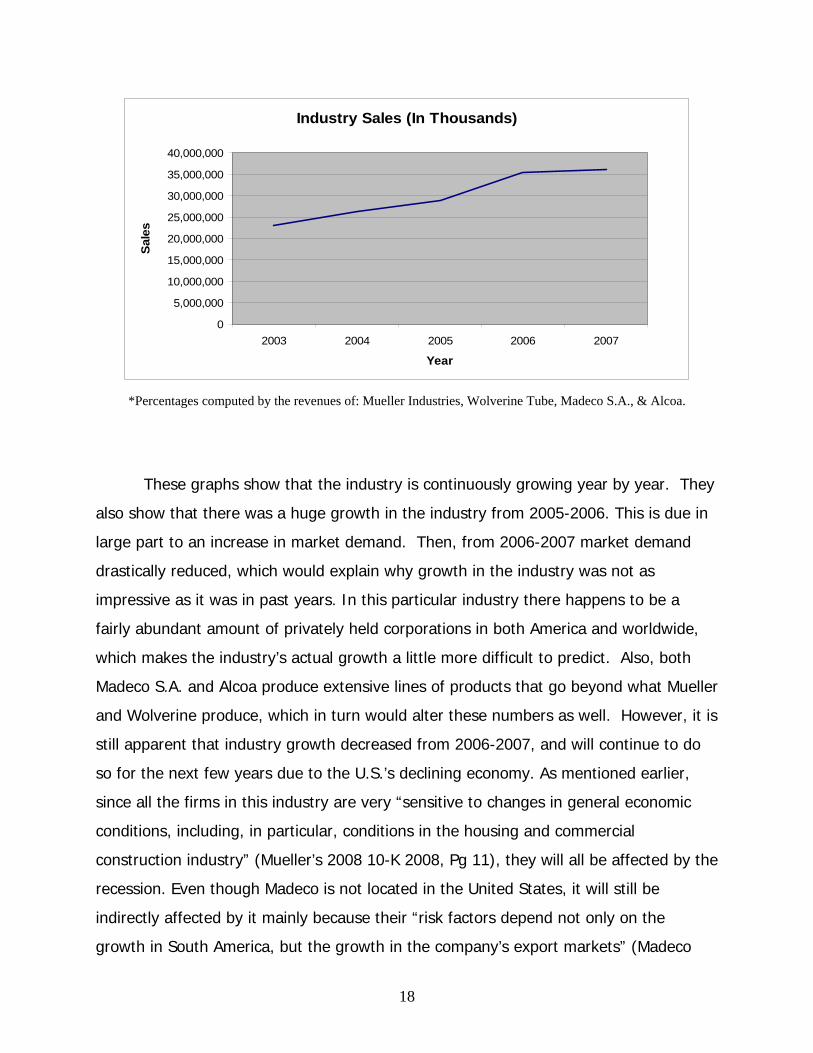

*Percentages computed by the revenues of: Mueller Industries, Wolverine Tube, Madeco S.A., & Alcoa.

18

Industry Sales (In Thousands)

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

40,000,000

2003 2004 2005 2006 2007

Year

Sale

s

*Percentages computed by the revenues of: Mueller Industries, Wolverine Tube, Madeco S.A., & Alcoa.

These graphs show that the industry is continuously growing year by year. They

also show that there was a huge growth in the industry from 2005-2006. This is due in

large part to an increase in market demand. Then, from 2006-2007 market demand

drastically reduced, which would explain why growth in the industry was not as

impressive as it was in past years. In this particular industry there happens to be a

fairly abundant amount of privately held corporations in both America and worldwide,

which makes the industry’s actual growth a little more difficult to predict. Also, both

Madeco S.A. and Alcoa produce extensive lines of products that go beyond what Mueller

and Wolverine produce, which in turn would alter these numbers as well. However, it is

still apparent that industry growth decreased from 2006-2007, and will continue to do

so for the next few years due to the U.S.’s declining economy. As mentioned earlier,

since all the firms in this industry are very “sensitive to changes in general economic

conditions, including, in particular, conditions in the housing and commercial

construction industry” (Mueller’s 2008 10-K 2008, Pg 11), they will all be affected by the

recession. Even though Madeco is not located in the United States, it will still be

indirectly affected by it mainly because their “risk factors depend not only on the

growth in South America, but the growth in the company’s export markets” (Madeco

19

Annual Report 2007). Since the United States is one of their export markets, their sales

will probably decrease as well. Also, “Alcoa’s operations consume substantial amounts

of energy, and profitability may decline if energy costs rise or if energy supplies are

interrupted” (Alcoa 10-k 2007). During 2007 energy costs such as oil were on the rise.

This adversely affected Alcoa’s sales during 2007, along with other firms in the metal

fabrication industry that consume a lot of energy. Because of the very weak and volatile

economic conditions the U.S. is facing, sales in the metal industry are likely to decrease

over the next two or three years.

Concentration

The concentration and balance of firms in an industry is the determining factor

which tells us which competitors have the power in the industry. The fewer

competitors that exist in an industry, the higher the concentration will be and vice

versa. The amount of concentration in an industry usually determines how a

corporation is going to set their prices, and other business shifts, in comparison to their

competitors. Wolverine stated in their most recent 10-k that in some of its product

lines “certain competitors have significantly larger market shares than us, and tend to

be price leaders in the industry” (Wolverine 10-k 2007). Since Wolverine has

significantly lower market share, they are forced to set their prices based upon what the

market leaders are charging for the same products. Of course, a monopoly would be

the best case scenario for any corporation who wanted a high concentration, but with

monopolies being regulated, companies just hope to take the biggest portion of market

share they can get.

20

2003 Market Share

Mueller

Wolverine

Madeco

2004 Market Share

Mueller

Wolverine

Madeco

2005 Market Share

Mueller

Wolverine

Madeco

2006 Market Share

MuellerWolverineMadeco

2007 Market Share

MuellerWolverineMadeco

Some of the fortunate companies are able to maintain a high market share and

concentration by becoming a dominant figure in their industry (i.e. Microsoft).

However, most companies must deal with stringent competition, as such in the metal

fabrication industry. In these competitive industries, companies must use an unspoken

understanding of prices in order to avoid an extreme driving down of prices within the

given industry. The graphs above show the break down of market share over the past

five years in the metal industry. Alcoa was excluded because it is a much more

expansive firm than the others, in that they do more than just manufacture

metal/plastic fittings, tubes, rods, and bars. If it was included in the pie chart it would

consume over 90% of the pie. Knowing this one can make the assumption that Alcoa is

not a true direct competitor. Nevertheless, the graphs indicate that Mueller has the

highest market share, followed by Madeco, then Wolverine. However, the three firms

have been fighting over market share. Over the past five years, Wolverine went from

having 28% market share to 24%, Madeco went from 21% to 25%, and Mueller has

fluctuated right around 51%. There are not any dramatic changes, but it is still evident

that competition over market share exists among firms in the industry.

21

Another important factor to consider in regards to concentration would be to find

out if firms within the industry mine their own metals. After much research one could

come to the conclusion that some firms in this industry do mine their own metals, and

some of them do in fact own portions of mining companies throughout the world.

Everyday worldwide Alcoa Mines 86,300 tons of bauxite, an aluminum ore (Alcoa 10-k

2007). Also, Mueller owns 49.5% of Jiangsu Mueller-Xingrong Mining Company, and

25% of Ruby Hill Mining Company (Mueller 10-k 2007). By mining their own metals

and having ownership in mining companies, firms within the metal fabrication industry

are able to cover their costs of buying raw materials by technically buying it from

themselves.

Differentiation

Firms that are able to differentiate their products within the industry are better

suited when it comes to combating with the competitors they are up against. For

example, a firm that has a certain product that is superior to that of its competitors is

going to have more leverage in the market, such as Apple’s iPhone in the cell phone

market. Having a product, in the iPhone, that stands out from the rest allows Apple to

charge whatever they please for this product. Consumers are forced to purchase at

Apple’s price if they wish to have this product, because none of its competitors have

anything like it. However, in an industry of little product differentiation, firms are

regulated to compete solely on who has the lower price. This is due to the fact that

consumers are not going to pay more for a product that is identical to every other

product manufactured in the industry.

This industry’s products consist of different types of materials such as copper,

brass, plastic, and aluminum. These materials are used to produce items that include

tubing, non-iron forgings, impact extrusions, and brass rods. These products are used

in the air-conditioning, refrigerating, and plumbing industries. One must also take into

account that firms included in the measurement of this industry such as Alcoa produce

a much more extensive line of products.

22

In the metal fabrication industry, there is going to be very little differentiation

amongst the competitors. “Minimal product differentiation among competitors in the

U.S. wholesale product categories creates a pricing structure that enables customers to

select products almost exclusively on price” (Wolverine 10-k 2007). It also does not

help that two of the more important factors in making products dissimilar are almost

non-existent in this industry, these two factors being: technology and innovation.

Switching Costs

Switching costs refers to a company’s ability to switch to a producing a different

product or service. These are the costs subjected to the company if it were to switch to

a completely different industry. When switching costs are high, companies are more

inclined to continue producing the same type of product due to the high cost of

changing businesses. In the case of the metal fabrication industry, research and

development spending for most firms involved is almost non-existent, leading to lower

levels of switching costs. However, there is a lot of money invested in machinery,

equipment, and plants which are meant to build the distinctive products designed by

the corporation, thus leading to higher levels of switching costs. Conversely, one could

make the argument that this equipment and machinery could be used to manufacture

products in another industry. This assumption, of course, would be in accordance to

what the equipment/machinery are actually capable of doing. The evidence presented

would have to conclude that the metal fabrication industry would typically have

moderate levels of switching costs.

Economies of Scale

The economies of scale in the metal fabrication industry are remotely large

because the entire industry does not have much product differentiation along with the

fact that there is very little spending on research and development. With little product

differentiation and many different competitors, the biggest firm in the industry really

23

has an advantage over the smallest one, in terms of capital. This is because the little

guy is offering the exact same product at the exact same price as the bigger firms in

the industry, leading to the assumption that one must have large numbers of capital

and production in order to maximize profits. These large numbers of capital help the

larger firms produce mass quantities of products compared to that of smaller firms, and

the more products you can produce at an efficient rate, the cheaper the price you are

able to offer. This is tremendously important in an industry in which prices play the

most vital role. The following chart shows the total assets of each firm in the industry.

It is obvious that Alcoa has the most capital, but once again it is because it is a much

larger firm that the rest, and therefore, it is not considered a direct competitor. When

looking at the other companies, Mueller and Wolverine have continued to increase their

capital, while Wolverine’s capital has slightly decreased. This could help explain why

Wolverine’s market share has decreased over the past five years and Madeco’s has

increased. Firm’s with greater capital have a distinct advantage in a cost competitive

industry.

Total Assets (In Thousands) 2003 2004 2005 2006 2007

Mueller 1,055,184 963,731 1,116,928 1,268,907 1,449,204

Madeco 622,805 637,328 683,801 841,533 979,066

Wolverine 553,258 587,458 568,765 455,330 456,673

Alcoa 31,711,000 32,609,000 33,696,000 37,183,000 38,803,000

Learning Economies

Similar to the economies of scale, the lack of use of the research and

development in the metal fabrication industry makes the learning curve in this particular

industry very minuscule. There are not many new innovations or technological

advances being discovered when it comes to making rods, bars, shapes, forgings,

impact extrusions, pipes, valves, tubes, faucets, and fittings from different types of

metals and plastics.

24

Ratio of Fixed to Variable Costs

Determining whether an industry usually has more fixed or variable costs is

important when valuing an individual firm within that industry. In the metal fabrication

industry, firms are more likely to have an equal volume of fixed costs compared to

variable costs. This is mostly due in part to the fact that the firms within the metal

fabrication industry usually outsource their finished products to other companies such

as the auto, refrigeration, and plumbing industries. Along with the outsourcing of

finished products, much of the firms in the metal fabrication industry also categorize

their ownership of giant factories, mills, buildings, machinery and equipment as fixed

costs.

The variable costs that exist in this industry are very prevalent as well. For

example, “escalating production costs and cooling commodity prices are dragging down

once-mighty mining and metal companies” (Wall Street Journal). In order for firms to

manufacture their product, they must first purchase the metals needed from their

suppliers. Firms must first pay the market price for metals such as copper and brass in

order to manufacture their products. This would be considered a variable cost to the

company because these prices are never the same from year to year, and sometimes

even vary from day to day. Although one must take in to account that even though

these metals are variable costs to a firm, every other firm within the same industry

must pay the exact same price as other. This importance of each firm having to pay

the same price for these materials is; if high raw material costs were to occur for one

firm, the same outcome would arise for the other industry firms as well, thus creating

no particular advantage for any firm in terms of these costs.

Another important factor to take into account in regards to an industry’s fixed to

variable costs ratio, would be research and development costs. Research and

development usually plays a vital role in the costs a firm incurs, but as aforementioned

in previous sections, R&D is limited in the metal fabrication industry.

25

Excess Capacity

Excess capacity is defined in our book as: If consumer demand is lower than the

capacity of the industry, then the firms within that particular industry will have to most

likely lower their prices in order to restore capacity. (Palepu & Healy P. 2-3) The

opposite of this situation being if the consumers demand is greater than supply, then

the competitors are not going to have to compete with each other when it comes to

prices. In this industry however, consumer demand is not very high as of late, this is

fact is stated in Mueller’s 10-K, “The majority of the Company’s manufacturing facilities

operated at moderate levels during 2005 and the first half of 2006. In the latter half of

2006, and in 2007, the Company’s manufacturing facilities operated at low levels due to

reduced market demand.” (Mueller Industries 10-K Filed February 26th, 2008, Pg. 4, Pg

6 on Adobe Reader). Wolverine also stated in its 10-k that because of the excess

capacity in the copper tube manufacturing markets, they have had little success in

selling their used equipment.

These numbers in the diagram above state each firm in the industry’s total

revenue divided by their total property, plant, and equipment. This is important

because it shows how well a firm is able to convert assets into revenue. Most of the

firms which deal directly with only the metal fabrication industry seem to have

extremely successful efficiency in their management of excess capacity.

Sales / Total Property, Plant & Equipment

2003 2004 2005 2006 2007

Mueller 2.89 4.10 5.64 7.97 8.76

Madeco 1.46 2.16 2.52 3.78 3.82

Wolverine 2.72 3.74 4.47 9.89 18.62

Alcoa 1.69 1.86 2.03 2.17 1.82

26

Exit Barriers

Similar to switching costs, a company’s barriers to exit depend on the on the

number of specialized fixed assets they have. The greater number of specialized assets

that exist in a given industry will in turn make the barriers of exit greater as well. This

is because with specialized assets companies become limited to that certain industry,

thus forcing them to stay in the industry they’re in and continue to battle it out with

their existing competitors. As mentioned earlier, Wolverine had trouble selling its used

equipment because of excess capacity in the industry, but it was also because the

equipment was very specialized. “Many times the equipment we have tried to sell, while

productive and essential to the operations for which they were originally purchased, has

been modified or built for specialized processes and products” (Wolverine 10-k 2007).

Other companies in the industry are likely to have similar specialized machinery. In the

metal fabrication industry, since machinery is highly specialized, it leads us to the

conclusion that the industry has medium to high exit barriers.

Conclusion

In the Five Forces Model all five sections play a significant role in the defining of

an industry. The Rivalry of Existing Firms may be only one of these sections but has to

be the one of the more noteworthy. In this section we drew conclusions about the

entire industry, some of its competitors, and how they all factor into the 9 distinct

categories: industry growth, concentration, differentiation, switching-costs, economies

of scale, learning economies, ratio of fixed vs. variable costs, excess capacity, and exit

barriers.

In the industry growth section we learned that growth in the industry is based

greatly upon market demand. The concentration section taught us that this industry

deals with low levels of concentration, in that most of the firms are roughly the same

size with the exception of Alcoa. We also learned that firms within the metal fabrication

industry deal with high levels of differentiation, moderate levels of switching-costs and

27

exit barriers, and low levels of economies of scale and learning economies. Through all

this information we can conclude that the metal fabrication industry is highly

competitive when it comes to the Rivalry of Existing Firms.

Threat of New Entrants

Aside from dealing with the competition and rivalry that exists between current

firms in the market, a company must also be weary of potential new competitors

entering into the market. In an industry of low concentration, like metal fabrication, a

firm cannot afford to lose what market share it already has. With the earning of

abnormal profits being low in this industry, the threat of new entrants is low as well. If

the industry were less established and not as stable, the potential for profit would be

much higher resulting in a higher threat of new companies entering the industry. The

various aspects that will better determine the risk of new firms are discussed below.

Economies of Scale

Success in the metal fabrication industry can be achieved through a few means.

The first being the ability to produce and move large amounts of product in the most

cost-efficient manner. This involves being able to take advantage of the benefits of

producing in large volume. In a highly competitive market, profits come by selling mass

quantities at the competitive price that is set by the market as a whole. Companies

unable to produce at the large scale will be forced to take a cut on profit due to their

lack of quantity produced, thus forcing them to surrender market share to those

companies who can produce at a large level. This implies that in order for a new

company to be successful in this industry, they must be able to attain the capital and

resources that will be large enough to meet this high quantity standard. The difficulty in

doing so is one of the reasons the threat of new entrants is relatively low. A simple

chart showing each firm’s assets will illustrate the scale necessary to be successful in

this industry.

28

Total Assets

(In thousands of dollars)

2003 2004 2005 2006 2007

Mueller 1,055,184 963,731 1,116,928 1,268,907 1,449,204

Madeco 622,805 637,328

683,801

841,533

979,066

Wolverine 553,258 587,458 568,765 455,330 456,673

Alcoa 31,711,000 32,609,000 33,696,000 37,183,000 38,803,000

*All data obtained from 10-K of each company

The magnitude of the numbers above proves quite a hurdle that any incoming

company would have to clear. The magnitude of the business activities necessary to

account for such assets is immense. It would be very difficult for a competitor to step in

and obtain enough resources to be able to compete against these already established

companies. The large scale of assets needed is only one of the difficulties new entrants

will face in the metal fabrication industry.

First Mover Advantages

A second aspect involving threat of new companies has to do with the benefits

gained by the early pioneers of the industry. In a setting where low production costs

can be the difference between life and death, one can understand how being among

the first companies of the industry will benefit from building the best relationships in

each of the businesses activities. This leaves each company in succession less and less

of a chance to find cost efficient alternatives that their other competitors have not

already taken advantage of. Among these problems is the difficulty a newcomer might

face in acquiring the copper, brass and other raw materials necessary to compete.

These inputs are by no means infinite, and thus they can at times become scarce. A

company’s ability to lock down purchase agreements can prove challenging and the

29

room left for new entrants is slim. Take industry giant Alcoa for instance, who has

already secured $9,067 billion dollars in raw material and service agreements for the

next five years alone (Alcoa Annual Report 2007). This further highlights the troubles

faced by prospective companies and why the first mover advantage is so crucial in this

industry.

Access to Channels of Distribution and Relationships

With the industrial sector making goods that are relatively widely used, multiple

channels of distribution is one thing that can be beneficial to new entrants. A lot of the

goods here are generic and companies that use these products may be indifferent

between which company supplies them. This puts further stress on the importance of

relationships between a company in the metal fabrication industry and those they

distribute to. Most of the companies in this industry supply to wholesalers who in turn

sell to the company making the refrigerator, air conditioner, etc. Since these customers

will go with the company selling at the lowest price, every step in the distribution

process is crucial. Mueller notes that, “a growing portion of our products are…acquired

from suppliers in lower cost regions” and this effort early in the process keeps costs low

which allows the company to sell to its customers without passing on the extra costs

incurred in the distribution process (Mueller 10-K 2007). Maintaining positive and open

relationships are vital to firms of this industry as the threat of substitution and losing

market share is one that is very threatening.

Legal Barriers

The list of legal issues facing companies in the metal fabrication industry is not

long, but that does not mean these companies don’t face legal challenges. Perhaps the

greatest legal issue in this industry is the environmental standard enforced by the

government and its agencies. With the growing concern of humanity’s effect on the

planet, these standards are only going to get higher and the costs continue to fall on

30

the companies. Wolverine notes that their operating facilities are, “subject to extreme

environmental laws and regulations [and they are] currently involved in various

proceedings relating to environmental matters.” They continue to disclose that they

“are not involved in any other legal proceedings” which suggests that environmental

standards account for most of the legal barriers faced in this industry (Wolverine 10-K

2007). While this may be one of the only legal concerns facing a company, it is one that

companies must meet in order to make their product . Each company has discussed

various ‘monitoring costs’ that are necessary to comply with the environmental

standards they face. As one can expect, these costs will be incorporated into the price

of their product, and is one more cost that new entrants will have to deal with in their

effort to compete in a low cost industry.

Conclusion

Overall, the threat of new entrants is low in this industry. For the firms already in

existence, this serves as motivation to push their limits and to be cautious of

complacency. Due to the large scale of production and the advantages of already being

established, it is not likely that a new company can intrude on a company’s current

success without suffering serious difficulty. The advantage of moving first is seen in

customer relationships and agreements and has already been captured by the

established firms. Environmental monitoring to meet legal standards is one more cost

that new companies will have to deal with in their effort to keep costs as low as

possible. All of these issues would prove challenging for any newcomer trying to

compete. Should a new company enter and bring its production to the par of the

industry, existing companies would want to ensure that their current practices are at

maximum capacity; however the likelihood of this occurrence is slim.

31

Threat of Substitute Products

The third measure of competition in the industry is the threat of substitute

products. Substitute products have a major impact on the metal industry. While no

two firms have the exact same product lines, many of their products do overlap. These

products, such as copper tubes, steel pipes, copper fittings, and valves are all

standardized products. They are created to standard specifications to serve mainly the

housing and commercial construction industries (www.muellerindustries.com). Thus,

these highly standardized products are easily substituted for one another, causing the

firms to compete primarily on price.

Relative Price and Performance

In the metal fabrication industry, prices for the same products are extremely

similar. This is because standards established by customers and governmental bodies

extremely limit the industries ability to differentiate their products. A particular product

will have to abide by a certain size, measurement, and function (www.wlv.com). Thus,

companies are creating almost identical products. This leads to high price competition

across all product lines.

The prices of the products are based upon the prices and availability of the raw

materials used to manufacture them, like copper for example. All the firms in the

industry who use copper to make a particular product will experience its price

fluctuations. So, no firm will have a definite advantage over another firm when

purchasing raw materials. However, a firm that can create an identical product by using

a material that does not suffer from price fluctuations will have a distinct advantage.

“Certain products such as plumbing tube are competing with products made of

alternative materials, such as polybutylene plastic” (Wolverine 10-k 2007). Alcoa, who

mainly produces aluminum products, also competes with products made out of glass.

Products made of plastic and glass are becoming substitutes for products originally

made of copper and other metals. While Mueller Industries manufactures both metal

32

and plastic products, most other firms in the industry need to be aware of the threat

these substitute products pose.

Buyer’s Willingness to Switch

Customers for metal fabrication products are primarily the housing and

commercial construction type industries. These businesses demand particular products

at competitive prices. They are very sensitive to price and product availability because

these factors have a major influence on their financial performance (Mueller 10-K

2007). Because competitors in the industry provide the same products, customers’

willingness to switch is fairly high. Customer’s have the ability to shop around for the

products they need, so other factors such as customer service and product availability

tend to influence who they do business with.

Another important factor relating to buyer’s willingness to switch is the existence

of substitute products that are composed of different materials, such as polybutylene

plastic. These materials can be used to create some of the same products sold in the

industry. Many of the buyer’s are willing to switch to these products because they can

be created to the same design features as copper and other materials and they perform

the same function at a lower price. As the price of copper and other metals rise,

copper products will become less attractive and people will be willing to buy products

made of plastic instead. The use of substitute products can have major negative effects

on all businesses in the metal fabrication industry. Madeco’s brass mills unit suffered

and 91% drop in earnings due partly to the strong presence of substitute products

(Madeco Annual Report 07).

Conclusion

Since firms in this industry tend to create similar, if not identical, products, it

forces them to compete by creating perceived value through customer service, product

availability, and price (Mueller 10-K 07). These are the only ways for firms in this

33

industry to differentiate themselves from one another. Companies also need to be

aware of substitute products such as plastic tubing that can negatively affect their

earnings and profitability. Buyers are more than willing to purchase various substitute

products that perform the same function as metal products for a lower price. For these

reasons, the threat of substitute products in the metal industry is very high.

The Bargaining Power of Customers

The bargaining power of customers in an industry is primarily determined by

price sensitivity and relative bargaining power. In order to clearly assess the industry

and these determinants, one must understand the industry structure. When evaluating

any industry, analysts must focus on the direct suppliers and direct customers and the

relationship from company to each of these. Customers of the metal fabrications

industry typically include the following markets: residential and commercial air

conditioning manufacturers, plumbing, refrigeration, electronic, lighting, aerospace, and

other metal joining industries (Wolverine 10-k 2007). In the following section, we will

analyze the metal fabrications industry and their customers in order to determine who

holds the bargaining power of the two.

Price Sensitivity

Price is a major decision-making factor in the buying process of the metal

fabrications industry. Price sensitivity is determined by looking at a number of different

aspects of an industry. For example, if the product has lower switching costs and is a

lesser part of the customer’s overall cost, then customers tend to be more price

sensitive. The main portions of the products sold in the metal fabrications industry are

ultimately sold to the domestic residential and commercial construction markets

(Mueller 10K 2007 pg. 5). The switching costs for these two markets would be

relatively low since the companies in this industry have similar product lines. Because

of the many generic products in the industry such as copper tube, steel pipe, copper

34

and plastic fittings, valves, etc., customers have the ability to easily choose between

suppliers (www.muellerindustries.com). Therefore, price, customer service and quality

greatly determine who the customers do business with.

Another aspect of determining price sensitivity is the importance of the product

to the buyers’ own product quality (Palepu & Healy). Customers of the metal

fabrications industry typically do not look at quality as a key determinate in choosing

their product because the products sold to buyers are made out of high quality metals

such as copper, brass, steel, etc. throughout the entire industry. Furthermore, since

there is not much differentiation due to the standards established by customers and

governmental bodies, the customer will usually want to do business with the company

that does the job at the lowest price. Like Wolverine states in its 10-k, “minimal

product differentiation enables customers to select products almost exclusively on price”

(Wolverine 10-k 2007). Overall, the metal fabrications industry seems to have high price

sensitivity.

Relative Bargaining Power

Relative bargaining power establishes the amount to which the customers will

succeed in driving the price down. Depending on the cost to each party of not doing

business with the other party, the relative bargaining power will be high or low. There

are several factors in determining the industry’s bargaining power including volume of

purchases by a single customer and differentiation. As stated earlier, the metal

fabrication industry’s main customer is the residential and commercial construction

markets. Therefore, because the main customers are typically entire markets or

businesses, the volume of purchases for each customer is usually in excess. “In 2007,

2006, and 2005, Wolverine’s ten largest customers accounted for approximately 60.2%,

51.2%, and 49.7%, respectively, of their consolidated net sales” (Wolverine 10-k 2007).

Since customers typically buy in mass quantities, they have more bargaining power over

price because they control so much of each company’s inventory.

35

Additionally, differentiation can always have an impact on who has the relative

bargaining power. Since tubes and fittings are not very unique, these same products

can be found in almost any company within the industry. Customers that do not agree

with the price that one company has set can buy the same products at another

company with ease. Whereas if our products were unlike any other, customers would

be forced to pay the prices that the companies set. As stated in Mueller’s 2007 10K,

“The markets we serve are competitive across all product lines. Some consolidation of

customers has occurred and may continue, which could shift buying power to

customers. In some cases, customers have moved production to low-cost countries

such as China…These conditions could have a material adverse impact on our ability to

maintain margins and profitability” (Mueller 10K 2007 pg. 11). Because this industry is

not very differentiated, there is a high amount of competition between the companies.

Customers have such a high amount of bargaining power over the firms in this industry

that they can even move production to low-cost countries in order to keep the price

lower for them.

Conclusion

Due to the high sensitivity of price and high relative bargaining power of

customers, buyers in the industry seem to have a high importance to the overall

profitability of the industry firms. We have determined that customers are relatively

sensitive to price because of the low switching cost to change from one company’s

products to another. We have also concluded that customers have a high bargaining

power over the metal fabrications industry because of the lack of differentiation and the

high volume per buyer. Because of these factors, customer service, quality, product

availability and continued relationships with existing customers are essential in order to

be successful in the metal fabrications industry.

36

Bargaining Power of Suppliers

Bargaining power of suppliers is the power that suppliers have over their

customers. This analysis is a mirror image of the bargaining power of customers,

analyzing switching costs, differentiation, the importance of product costs and quality,

number of suppliers and volume per supplier. The major difference between the

powers of customers compared to suppliers is that supply heavily influences a firm’s

profits and market share within the industry. When there are few substitute products

or materials available to firms, suppliers have more power over them.

In the metal fabrication industry suppliers do have power over their customers.

This power is somewhat limited compared to other industries since raw materials in

scrap form such as copper, metal, and aluminum are set by market price. Most

competitors in the industry acquire raw materials through short-term supply contracts.

“The major portion of Mueller's base metal requirements (primarily

copper) is normally obtained through short-term supply contracts with

competitive pricing provisions (for cathode) and the open market (for

scrap).” (Mueller Inc. 10k)

Suppliers in the metal fabrication industry sell a generic product which allows buyers

the power to choose from many different suppliers. This limits some of the supplier’s

power over its customers. Most of the power suppliers hold is exercised through short

term contracts including price, quality and most importantly quantity. In recent years,

the demand for copper and other raw materials have increased dramatically over seas,

thus raising prices. So far, the new demand has not affected firm’s supply in the US.

At the same time, supplier’s raw materials in the metal fabrication industry are

vital to a company’s entire business. Without necessary supply, companies could

experience exponential losses. Suppliers use this to their advantage allowing them to

dictate delivery options. Many suppliers take advantage of this and have a developed a

good track record within the industry. Alcoa a steel fabrication company operates as

37

both a fabricator and as a supplier because the company is so large. “Slightly more than

half of Alcoa’s alumina production is sold under supply contracts to third parties

worldwide, while the remainder is used internally.” (Alcoa ’07 10k). Most suppliers have

been supplying the metal fabrication industry for many years. Firms buying vital

supplies are not normally willing to risk buying from an unproven supplier due to the

possible consequences that could follow.

Conclusion

In the metal fabrication industry supply is a deciding factor for most firm’s

profits. It is important to have bargaining power for both sides so that there is a

balance of power. Factors such as generic product, large number of suppliers and

overall necessity of product lead us to conclude that the bargaining power of suppliers

is neither high, nor low.

Five Forces Conclusion

After fully analyzing the five forces that impact the metal fabrication industry, we

concluded that this industry is highly competitive. There is a high rivalry among existing

firms in the industry, a high threat of substitute products, high bargaining among

customers, and moderate bargaining power of suppliers. These factors lead firms in the

industry to create a competitive advantage based on cost leadership rather than

differentiation. Companies are creating essentially the same products, and therefore,

cost leadership is one of the only ways to become profitable in the industry.

38

Key Success Factors of the Industry

In general there are two avenues that a business can take to achieve competitive

success. Cost leadership applies to those industries that tend to produce homogeneous

products where the threat of substitute products is high. However consumers will also

pay for differentiated products that compete on innovation and features that distinguish

their product from another. This price premium is relative to the amount of brand

imaging, research and development and sheer creativity that firms in the industry use

to set themselves apart from the pack. Fabrication of plastic and metal piping and

accessories utilizes many more traits of costs leadership as there are many firms in the

industry making essentially the same products. What allows for gaining a step on the

competition is how the company can diminish cost across all aspects of business as well

as maintain the capacity to supply to as many customers as possible. Continued below

are the specifics of cost leadership and how these strategies are used in the industry.

Economies of Scale

It has been established that large amounts of production are necessary to be

successful for various reasons. Economies of scale imply a lower average unit cost due

to producing at high output. A large volume of production further displaces the high

fixed costs of assets that are fundamental to operating in this industry. The more that

can be made and sold with the given capital will result in a higher return on capital,

which in turn allows for further expansion for a firm. Competing on cost implies being a

price taker, meaning that the price that customers will pay for your product is set by

the industry as a whole. The price is not set by means of a committee or any form of

official system, but rather by the informal actions of the industry altogether. This is

because customers of the metal fabrication industry will go with the supplier that can

get them what they want at the lowest cost. With products of the industry unable to

differentiate themselves, cost becomes the sole concern. If one company can sell for a

lower price, it requires all other firms to move to that price, thus resulting in a stable

39

price for the market. The table below highlights the large amount of assets that are

needed to compete in this industry. Such large numbers imply that the larger the

amount of output, the lower the unit cost will be. As low costs are the name of the

game, economies of scale are vital in this industry.

Total Assets

(In thousands of dollars)

2003 2004 2005 2006 2007

Mueller 1,055,184 963,731 1,116,928 1,268,907 1,449,204

Madeco 622,805 637,328

683,801

841,533

979,066

Wolverine 553,258 587,458 568,765 455,330 456,673

Alcoa 31,711,000 32,609,000 33,696,000 37,183,000 38,803,000

*All data obtained from 10-K of each company

Economies of Scope

There is often confusion in the difference between economies of scale and

scope. We have previously defined economies of scale as a firm’s necessity to produce

large volumes of output when they are dependent on large amounts of fixed assets to

run their operations. This lowers the average unit cost, and thus creates more profit on

the sale price. Economies of scope are present when, “the total cost of producing [two

goods] Q1 and Q2 together is less than the total cost of producing [them] separately”

(Managerial Economics and Business Strategy, p.188). This idea is common sense to

most people, and it is present in every company of the industry. In other words, a

company makes multiple types of pipes, fittings, and accessories because it is more cost

efficient to do so. It would not make sense for company A to have such large amounts

of assets to only make copper pipe, while company B spends the same on assets to

40

make plastic pipe, and company C produces only fittings and accessories. Since making

most of these products requires using more or less the same machinery, it is more

efficient for one company to produce all of these under one roof, using the same

assets. The table below illustrates the economies of scope that are present due to each

company’s multitude of products.

Economies of Scope in the Metal Fabrication Industry

Company Products Alcoa A primary producer of aluminum products including casts,

industrial fasteners, and food service packages as well as making contributions to the aerospace and electrical/electronic

industries Mueller Makes copper, brass, plastic and aluminum pipes, tubes and

accessories for heating, refrigerating and other industries Madeco Maker of pipes, bars, and other products used in the

construction sector; they make a variety of copper, brass, and aluminum products

Wolverine Produces a variety of copper alloy tube and metal joining products; their product line is wide enough to supply to commercial air conditioning manufacturers, appliance manufacturers, automotive manufacturers, industrial equipment manufacturers, refrigeration equipment manufacturers, and plumbing fittings and fixture

manufacturers *All data from yahoo.finance.com

41

Efficient Production Methods and Cost Control

A basic requirement of cost leadership is how efficiently a firm in the industry

can make its product. Efficiency can be attributed to a number of things including

machinery processes, material acquisition, personnel decisions and means of

distribution. One thing that is key in all of these categories is organization. Having

various process segmented allows for each to operate at the best of its ability while still

being part of the company as a whole. Subdivisions can be divided based on where

they fall in the process line as well as what geographic area they deal with. Having

these segments reduces the level of complication that may be encountered when

multiple processes are involved to make a product, and allows each branch to operate

as efficiently as possible. It also enables a branch to make changes that are of concern

to that branch in particular.

For example, if the capacity for production were to increase, expansions could

be made to the molding and fabrication sector without interference of other segments.

Organization will also give a more structured illustration of how the company stands,

and will make planning for the future much easier. Assessments of raw materials will be

easier, and will allow arrangements for materials to be made for further in the future

that will be of much benefit to the company as a whole.

It is important for a company to minimize costs where it can as there are some

costs that will be out of their control. Madeco notes that, “the increase in the costs of

sales is basically caused by the increase in…raw materials like copper, aluminum and

other plastics materials” (Madeco Annual Report 2007). As certain costs like raw

materials are unable to be controlled, it is necessary to be efficient in the production

methods that are under the company’s control.

Perhaps the biggest step towards efficiency is through mergers and acquisitions

involving two companies sharing the same interests. For a company that acquires

another, there is no bigger indicator of market dominance and company progression

than by obtaining a company with which one has a strong interest in. The ability to

control another step in the business process implies fewer points of view and other

42

complications that one company may suffer when dealing with another. A business

merger or acquisition is in essence the definition of efficiency. Here we will refer to

Mueller’s acquisition table to highlight this idea of efficiency in the industry.

Mueller’s Acquisitions and Mergers Date Level of

Involvement Company Activities Means of

AcquisitionAug. 2004

Acquisition Vemco

(England)

Important distributor of

plumbing products

in UK and Ireland

Acquired 100% of stock O/S

Aug.

2005

Acquisition Brassware

(England)

Important distributor of plumbing and

residential heating products

Acquired 100% of stock O/S

Dec.

2005

Joint Venture Jiangsu Xingrong & Jiangsu

Buiyand Ind.

(China)

Producer of various tubes and tube

coils

50.5% interest in

joint venture

Feb.

2007

Acquisition Extruded Metals

(Michigan)

Manufacturer of brass rod products

Acquired 100% of stock O/S

*All data from Mueller 10-K 2007