Embed Size (px)

Citation preview

Breakdown of CIP:Breakdown of CIP:Mystery ormyth?Mystery ormyth?by A.Wong & J. Zhangby A.Wong & J. Zhang

Discussant: Dagfinn RimeDiscussant: Dagfinn RimeBI Norwegian Business SchoolBI Norwegian Business School

ECB/Fed-GRFECB/Fed-GRF

OverivewApparently deviations fromCIP!

Du, Tepper, and Verdelhan (2018)

Very important topicArbitrage suggest malfunctioningmarketsNice paper studying long dated relations

I Lots of details on Cross-currency Basis SwapsI Conceptually similar to FX swaps

Decompose deviations into . . .I credit risk premiumI liqudidity premium

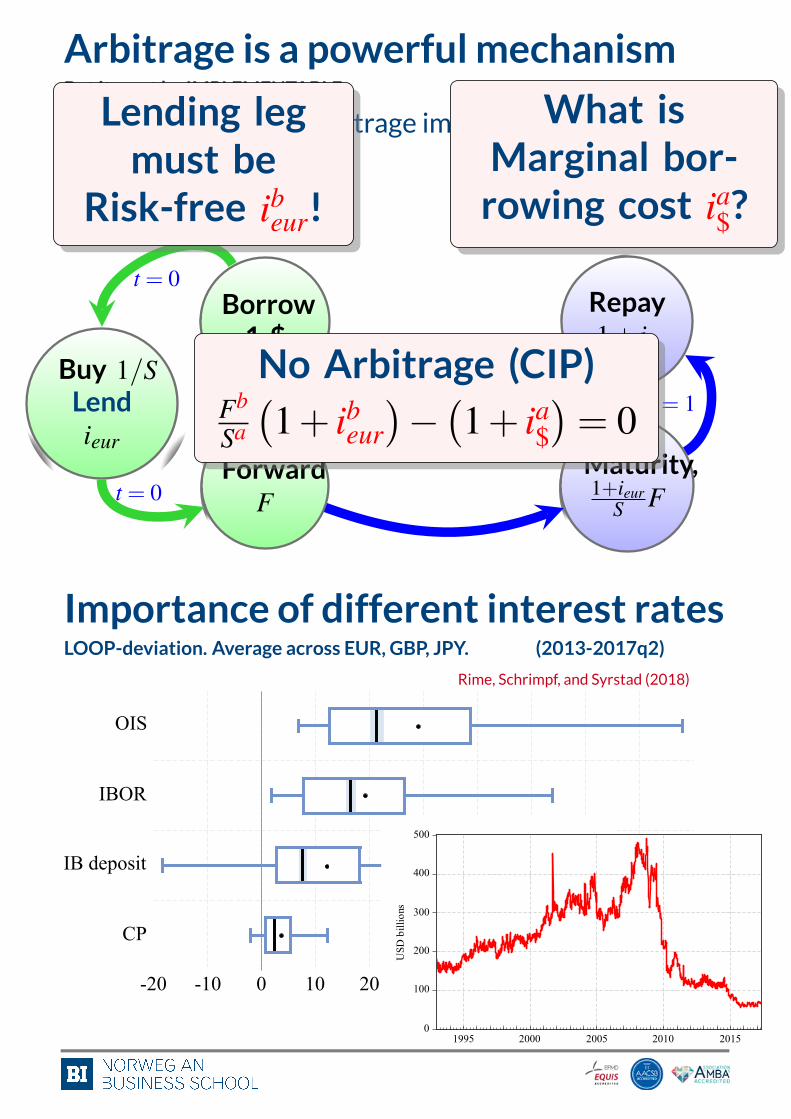

Arbitrage is a powerful mechanismBut it must be IMPLEMENTABLE

HOW is CIP arbitrage implemented?

Borrow1 $

Buy 1/SLendieur

t = 0

ForwardFt = 0

Maturity,1+ieur

S F

Repay1+ i$

t = 1No Arbitrage (CIP)

Fb

Sa

(1+ ibeur

)−(1+ ia$

)= 0

Lending legmust be

Risk-free ibeur!What is

Marginal bor-rowing cost ia$?

Importance of different interest ratesLOOP-deviation. Average across EUR, GBP, JPY. (2013-2017q2)

Rime, Schrimpf, and Syrstad (2018)

-20 -10 0 10 20 30 40 50 60 70 80

OIS

IBOR

IB deposit

CP

Basis points0

100

200

300

400

500

1995 2000 2005 2010 2015

USD

bill

ions

LOOP using Corporate bondsSyrstad (2018): “CIP in bondmarkets”

-160

-120

-80

-40

0

40

80

2010 2012 2014 2016

Bond spread differentialLibor basis 5y

Basi

s poi

nts

(a) EU-140

-120

-100

-80

-60

-40

-20

2010 2012 2014 2016

JPY-USD bond spread differentialLibor basis 5y (JPY/USD)

Basi

s poi

nts

(b) JP

Basis = Bond spreaddiff for similarcorporate bonds⇒ LOOP holds

Regression analysis∆FP$U = c0 + c1∆OISU+ c2∆OIS$

+ c3∆IBORU+ c4∆IBOR$

40

model predicts.

-1.2

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2EUR GBP CHF JPY GBP CHF JPY

Coefficients of FC OIS

Coefficients of FC IRS

Coefficients of DC OIS

Coefficients of DC IRS

Domestic currency: USD Domestic currency: EUR

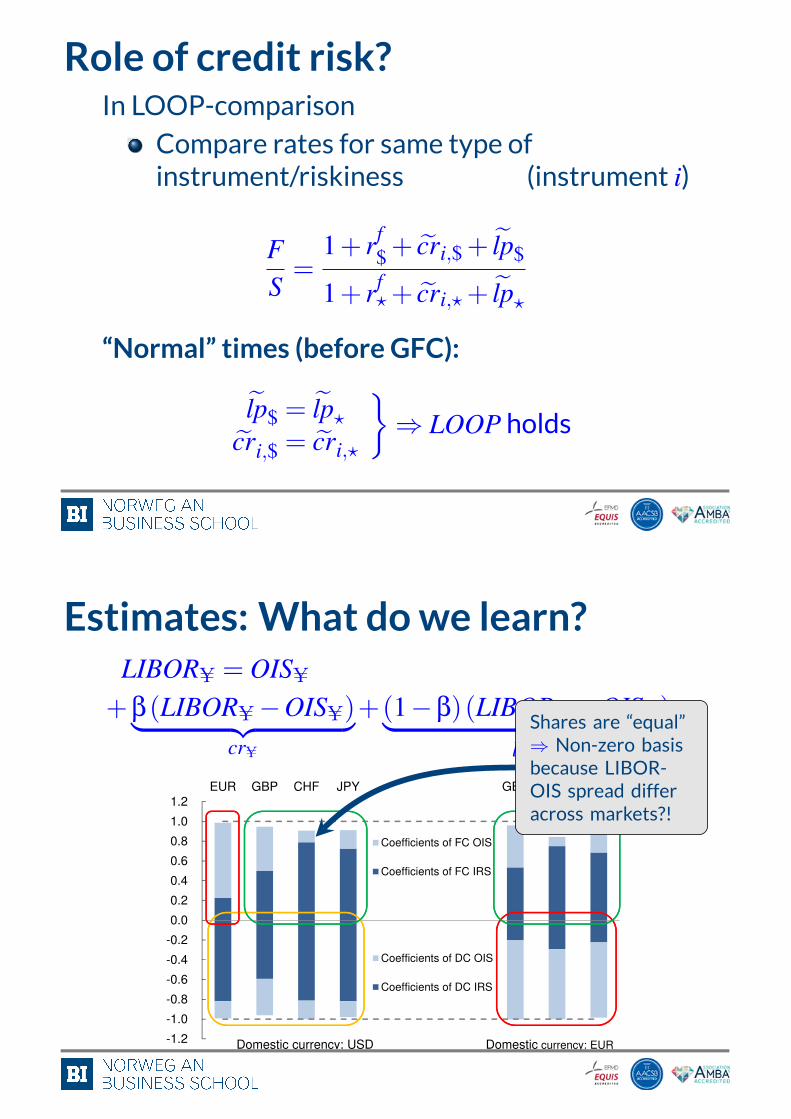

FIGURE 9. SUM OF COEFFICIENTS OF IRS AND OIS

Source: Table 4

Moreover, the results are highly robust across the currency pairs. The relative

size of the OIS and IRS coefficients, i.e., the relative share of counterparty and

liquidity risk premiums, for each of the currencies is extremely consistent across

the currency pairs, i.e., regardless of which currency is in the other leg. As shown

in Figure 9, the relative size of the light and dark blue bars for EUR is almost

uniform across the currency pairs (circled in red). The light blue bars are longer,

suggesting that the counterparty risk premium accounts for a larger share of the

Libor-OIS spread in the EUR Libor market, all falling within the range of 70-

80%. The relative size of the bars for USD is also very much the same across the

currency pairs with longer dark blue bars (circled in yellow), reflecting a larger

proportion of the liquidity risk premium, about 60% vis-a-vis GBP and slightly

above 80% vis-a-vis the other three currencies. Similarly, the relative size of

c1 + c3 = 1c1 + c3 = 1c2 + c4 =−1

What does e.g.0.98 mean?2% deviation?

Arb: Each caseimportant.Average notsufficient

Role of credit risk?In LOOP-comparison

Compare rates for same type ofinstrument/riskiness (instrument i)

FS=

1+ rf$ + cri,$ + lp$

1+ rf?+ cri,?+ lp?

“Normal” times (before GFC):lp$ = lp?

cri,$ = cri,?

}⇒ LOOP holds

Estimates: What dowe learn?LIBORU = OISU

+β(LIBORU−OISU)︸ ︷︷ ︸crU

+(1−β)(LIBORU−OISU)︸ ︷︷ ︸lpU

40

model predicts.

-1.2

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2EUR GBP CHF JPY GBP CHF JPY

Coefficients of FC OIS

Coefficients of FC IRS

Coefficients of DC OIS

Coefficients of DC IRS

Domestic currency: USD Domestic currency: EUR

FIGURE 9. SUM OF COEFFICIENTS OF IRS AND OIS

Source: Table 4

Moreover, the results are highly robust across the currency pairs. The relative

size of the OIS and IRS coefficients, i.e., the relative share of counterparty and

liquidity risk premiums, for each of the currencies is extremely consistent across

the currency pairs, i.e., regardless of which currency is in the other leg. As shown

in Figure 9, the relative size of the light and dark blue bars for EUR is almost

uniform across the currency pairs (circled in red). The light blue bars are longer,

suggesting that the counterparty risk premium accounts for a larger share of the

Libor-OIS spread in the EUR Libor market, all falling within the range of 70-

80%. The relative size of the bars for USD is also very much the same across the

currency pairs with longer dark blue bars (circled in yellow), reflecting a larger

proportion of the liquidity risk premium, about 60% vis-a-vis GBP and slightly

above 80% vis-a-vis the other three currencies. Similarly, the relative size of

Shares are “equal”⇒ Non-zero basisbecause LIBOR-OIS spread differacross markets?!

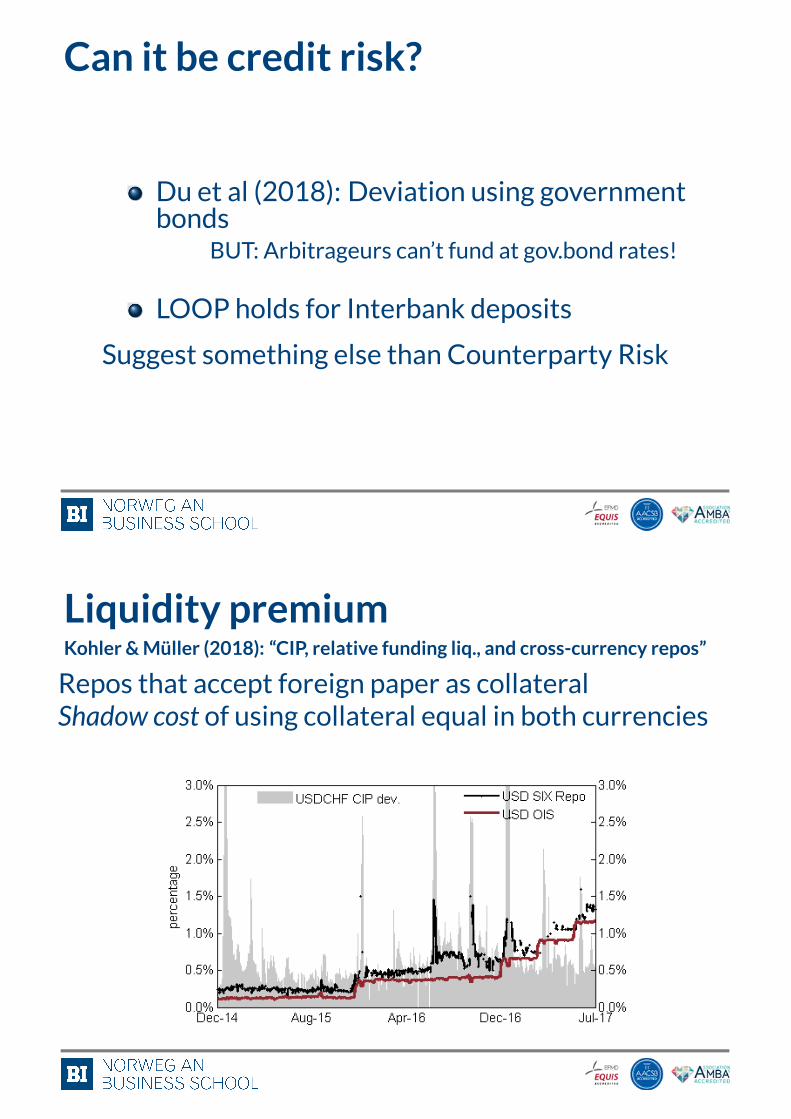

Can it be credit risk?

Du et al (2018): Deviation using governmentbondsBUT: Arbitrageurs can’t fund at gov.bond rates!

LOOP holds for Interbank depositsSuggest something else than Counterparty Risk

Liquidity premiumKohler &Müller (2018): “CIP, relative funding liq., and cross-currency repos”Repos that accept foreign paper as collateralShadow cost of using collateral equal in both currencies

deviations.28

Figure 1 depicts US dollar CCY SIX Repo rates (black line), US dollar OIS rates (red

line) and the USDCHF FX basis derived from OIS interest rate differentials, all shown for a

maturity of one week. Recall that US dollar CCY SIX Repo rates are not available on a daily

basis, which explains the missing observations compared to US dollar OIS rates in Figure 1.

The following observations can be made: first, US dollar CCY SIX Repo rates indeed trade

above US dollar OIS rates. Second, the USDCHF FX basis spikes towards quarter-ends. 1W

US dollar OIS rates fail to capture these dynamics while 1W US dollar CCY SIX Repo rates

interestingly exhibit similar quarter-end spikes.

Fig. 1. US dollar CCY SIX Repo, US dollar OIS interest rates and the USDCHF FX basis

Figure 1 shows US dollar CCY SIX Repo rates (black line), US dollar OIS rates (red line) and the USDCHFOIS-based FX basis (grey shaded). All instruments are depicted for a maturity of one week.

These stylized facts are first evidence that the spread between US dollar CCY repo and

US dollar OIS rates on the one hand and OIS-based CIP deviations on the other move

very much in parallel, in particular, over quarter-ends. To provide further evidence for our

hypothesis, the predictive power of the spread between US dollar CCY SIX Repo and US

28In fact, there is hardly any price difference between Swiss franc CCY repo and Swiss franc OIS rates orbetween euro CCY repo and euro OIS rates. The same is not true for US dollar interest rates where CCYrepos trade at a considerable and persistent premium compared to OIS. It is hence the US dollar CCY repowhich makes the difference when testing CIP in Equation (2).

23

SummaryVery interesting paper on a hot topicClarify economic interpretation ofregression resultsWhat does themagnitudes imply?Do constrained panel regressions:Get consistent USD-premiums acrosscurrenciesTriangular relation: Do Risk-shares add up?

Thank you!Thank you!home.bi.no/dagfinn.rimehome.bi.no/dagfinn.rime

[email protected]@bi.no

References IWenxin Du, Alexander Tepper, and Adrien Verdelhan.Deviations from covered interest rate parity. Journal ofFinance, 73(3):915–957, 2018.

Daniel Kohler and BenjaminMüller. Covered interest rateparity, relative funding liquidity and cross-currencyrepos. typescript, Swiss National Bank, 2018. URLhttps://www.snb.ch/n/mmr/reference/sem_2018_09_21_mueller/source/sem_2018_09_21_mueller.n.pdf.

Dagfinn Rime, Andreas Schrimpf, andOlav Syrstad.Covered interest parity arbitrage. Working Paper 15,Norges Bank, 2018.

Olav Syrstad. Covered interest rate parity in bondmarkets.typescript, Norges Bank, 2018.