Embed Size (px)

DESCRIPTION

nalco

Citation preview

Corporate Presentation

National Aluminium Company Limited (A Govt. of India Enterprise)

February 2013

Corporate Presentation February 2013

Disclaimer

This presentation does not constitute or form part of any offer or invitation or inducement to sell or issue, or any solicitation of any offer to purchase or subscribe for, any securities of National Aluminium Company Limited (the “Company”), nor shall it or any part of it or the fact of its distribution form the basis of, or be relied on in connection with, any contract or commitment therefor.

This presentation may include statements which may constitute forward-looking statements. All statements that address expectations or projections about the future, including, but not limited to, statements about the strategy for growth, business development, market position, expenditures, and financial results, are forward looking statements. Forward looking statements are based on certain assumptions and expectations of future events. The Company cannot guarantee that these assumptions and expectations are accurate or will be realised. The actual results, performance or achievements, could thus differ materially from those projected in any such forward-looking statements. The Company assumes no responsibility to publicly amend, modify or revise any forward-looking statements, on the basis of any subsequent developments, information or events, or otherwise.

The information contained in these materials has not been independently verified. None of the Company, its Directors, Promoter or affiliates, nor any of its or their respective employees, advisers or representatives or any other person accepts any responsibility or liability whatsoever, whether arising in tort, contract or otherwise, for any errors, omissions or inaccuracies in such information or opinions or for any loss, cost or damage suffered or incurred howsoever arising, directly or indirectly, from any use of this document or its contents or otherwise in connection with this document, and makes no representation or warranty, express or implied, for the contents of this document including its accuracy, fairness, completeness or verification or for any other statement made or purported to be made by any of them, or on behalf of them, and nothing in this document or at this presentation shall be relied upon as a promise or representation in this respect, whether as to the past or the future. The information and opinions contained in this presentation are current, and if not stated otherwise, made as of the date of this presentation. The Company undertake no obligation to update or revise any information or the opinions expressed in this presentation as a result of new information, future events or otherwise. Any opinions expressed in this presentation are subject to change without notice. No part of the information provided herein is to be construed as a solicitation to make any financial investment and is provided for information only. Any person / party intending to provide finance / invest in the shares / businesses of the Company shall do so after seeking their own professional advice and after carrying out their own due diligence procedure to ensure that they are making an informed decision.

This presentation is strictly confidential and may not be copied or disseminated, in whole or in part, and in any manner or for any purpose. No person is authorised to give any information or to make any representation not contained in or inconsistent with this presentation and if given or made, such information or representation must not be relied upon as having been authorized by any person. Failure to comply with this restriction may constitute a violation of the applicable securities laws. This presentation is not intended for distribution or publication in the United States. Neither this document nor any part or copy of it may be distributed, directly or indirectly, in the United States. The distribution of this document in certain jurisdictions may be restricted by law and persons into whose possession this presentation comes should inform themselves about and observe any such restrictions. By participating in this presentation or by accepting any copy of the slides presented, you agree to be bound by the foregoing limitations. You further represent and agree that (i) you are located outside the United States and you are permitted under the laws of your jurisdiction to receive this presentation or (ii) you are located in the United States and are a "qualified institutional buyer" (as defined in Rule 144A under the Securities Act of 1933 (the "Securities Act")).

This presentation is not an offer to sell or a solicitation of any offer to buy the securities of the Company in the United States or in any other jurisdiction where such offer or sale would be unlawful. Securities may not be offered, sold, resold, pledged, delivered, distributed or transferred, directly or indirectly, into or within the United States absent registration under the Securities Act, except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the Securities Act and in compliance with any applicable securities laws of any state or other jurisdiction of the United States.

2

Corporate Presentation February 2013

Table of Contents

3

In this document upto Q3FY13 refers to the nine month period ended 31st December, 2012, and Q3 FY 13 refers to the three month period ended 31st December, 2012.

Overview of NALCO

Production & Sales

Aluminium – Domestic & Global Demand

Financials

Our Expansion Projects

Projects Completed & Under Construction

Projects Under Planning

1

2

3

4

5

6

7

Page #

4

9

13

16

19

22

27

Awards and Governance 8 32

Corporate Presentation February 2013

Overview of NALCO

1

Corporate Presentation February 2013

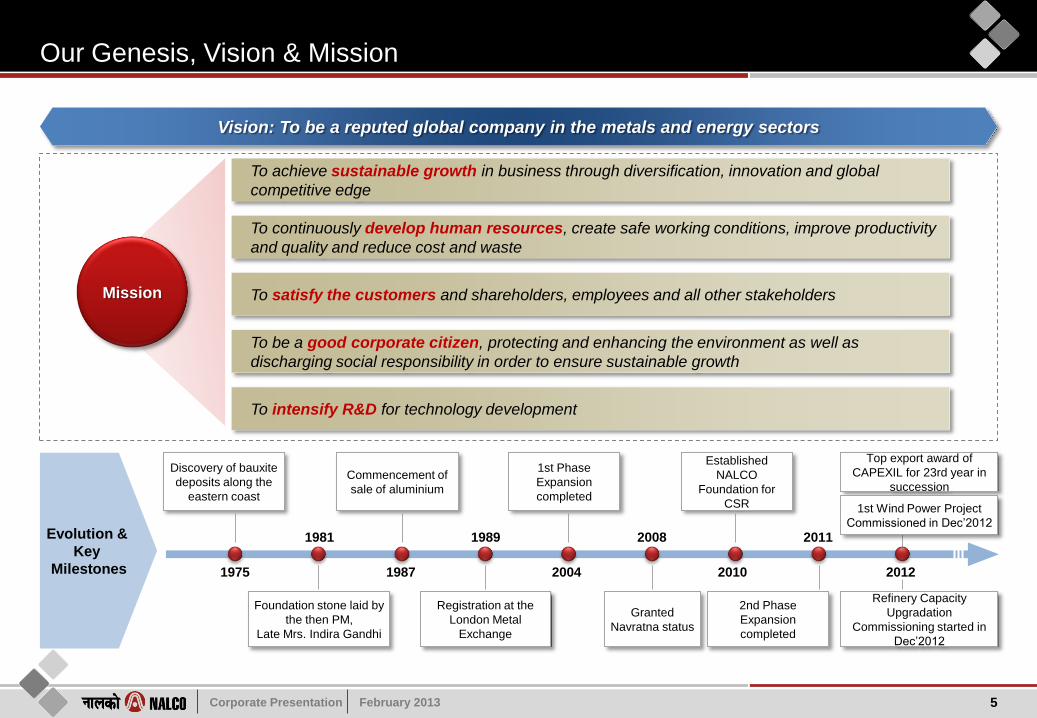

Our Genesis, Vision & Mission

5

Evolution &

Key

Milestones

Discovery of bauxite

deposits along the

eastern coast

Foundation stone laid by

the then PM,

Late Mrs. Indira Gandhi

Registration at the

London Metal

Exchange

1st Phase

Expansion

completed

Granted

Navratna status

Established

NALCO

Foundation for

CSR

2nd Phase

Expansion

completed

Commencement of

sale of aluminium

Top export award of

CAPEXIL for 23rd year in

succession

1975

1981

1987

1989

2004

2008 2011

2010 2012

Refinery Capacity

Upgradation

Commissioning started in

Dec’2012

1st Wind Power Project

Commissioned in Dec’2012

Vision: To be a reputed global company in the metals and energy sectors

To achieve sustainable growth in business through diversification, innovation and global

competitive edge

To continuously develop human resources, create safe working conditions, improve productivity

and quality and reduce cost and waste

To satisfy the customers and shareholders, employees and all other stakeholders

To be a good corporate citizen, protecting and enhancing the environment as well as

discharging social responsibility in order to ensure sustainable growth

To intensify R&D for technology development

Mission

Corporate Presentation February 2013

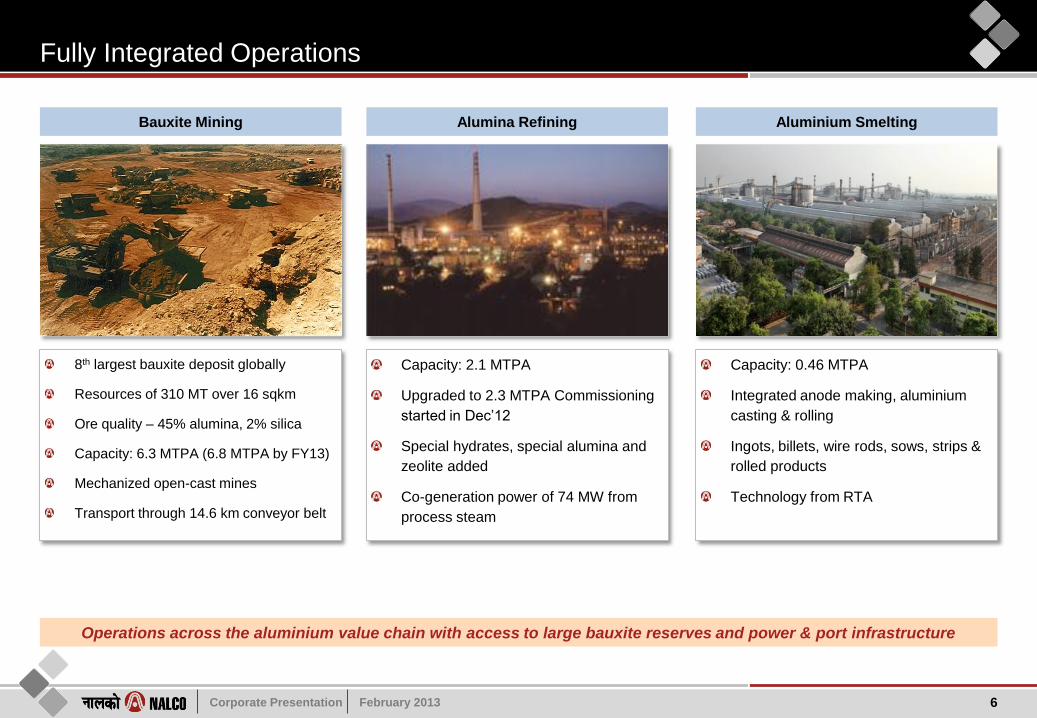

Fully Integrated Operations

6

8th largest bauxite deposit globally

Resources of 310 MT over 16 sqkm

Ore quality – 45% alumina, 2% silica

Capacity: 6.3 MTPA (6.8 MTPA by FY13)

Mechanized open-cast mines

Transport through 14.6 km conveyor belt

Capacity: 2.1 MTPA

Upgraded to 2.3 MTPA Commissioning

started in Dec’12

Special hydrates, special alumina and

zeolite added

Co-generation power of 74 MW from

process steam

Capacity: 0.46 MTPA

Integrated anode making, aluminium

casting & rolling

Ingots, billets, wire rods, sows, strips &

rolled products

Technology from RTA

Operations across the aluminium value chain with access to large bauxite reserves and power & port infrastructure

Bauxite Mining Alumina Refining Aluminium Smelting

Corporate Presentation February 2013

Fully Integrated Operations

7

Operations across the aluminium value chain with access to large bauxite reserves and power & port infrastructure

Capacity: 1,200 MW

High PLF

Zero effluent discharge

Advanced electro-static precipitator for

pollution control

Captive Thermal Power Plant

Capacity: 50.4 MW Wind Power Project

in Gandikota, A.P.

Power Purchase Agreement (PPA) was

signed by NALCO with APSPDCL

(DISCOM) on 22.12.2012.

Commissioned in Dec’2012

Wind Power Project-I

Capacity to handle ships up to 40,000

DWT

Export of alumina & import of caustic

soda

Mechanized mobile ship loader

Mechanized storage and handling

facility

Port Facilities

Corporate Presentation February 2013

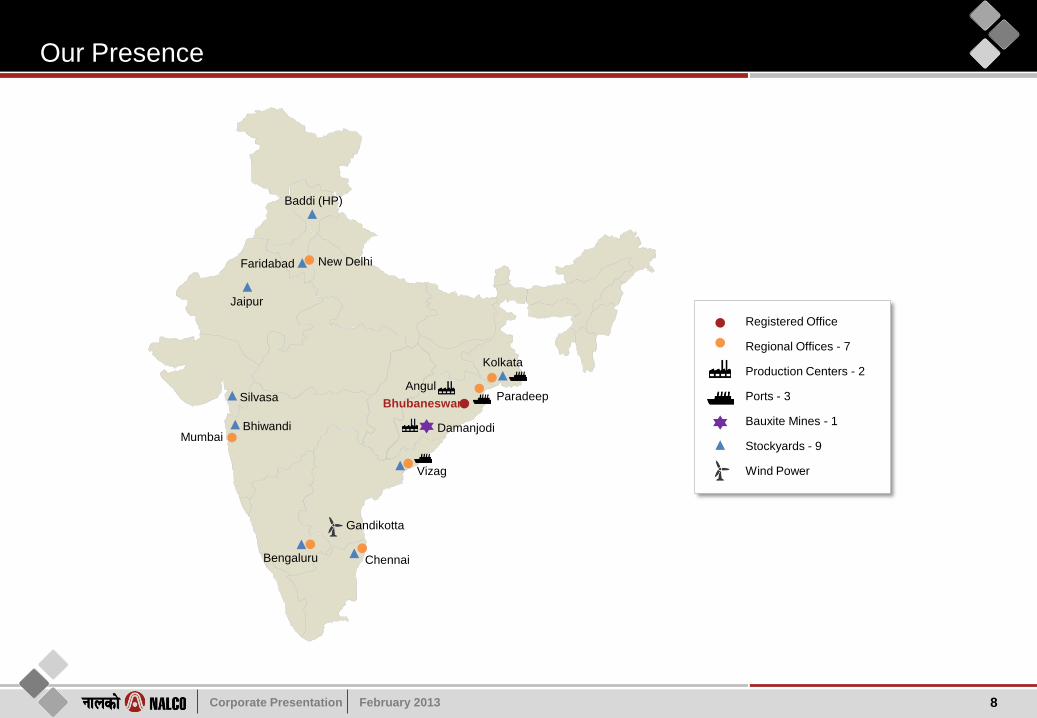

Our Presence

8

Bhubaneswar

Chennai Bengaluru

Bhiwandi

Silvasa

Jaipur

Faridabad

Baddi (HP)

Kolkata

Vizag

Paradeep

New Delhi

Angul

Damanjodi

Gandikotta

Registered Office

Regional Offices - 7

Production Centers - 2

Ports - 3

Bauxite Mines - 1

Stockyards - 9

Wind Power

Mumbai

Corporate Presentation February 2013

Production & Sales

2

Corporate Presentation February 2013

Production Growth

10

Bauxite (MT)

Alumina (MT)

Aluminium (MT)

Power (MU)

4.70 4.88 4.82 5.00 3.55

FY09 FY10 FY11 FY12 Upto Q3 FY13

1.12 1.21 1.37 1.29

1.14 1.22 1.19

Q1FY12 Q2FY12 Q3FY12 Q4FY12 Q1FY13 Q2FY13 Q3FY13

1.58 1.59 1.56 1.59 1.27

FY09 FY10 FY11 FY12 Upto Q3 FY13

0.40 0.39 0.39

0.51 0.48

0.40 0.40

Q1FY12 Q2FY12 Q3FY12 Q4FY12 Q1FY13 Q2FY13 Q3FY13

0.36 0.43 0.44 0.41

0.31

FY09 FY10 FY11 FY12 Upto Q3 FY13

0.11 0.11 0.09 0.10 0.10 0.10 0.10

Q1FY12 Q2FY12 Q3FY12 Q4FY12 Q1FY13 Q2FY13 Q3FY13

5,541 6,293 6,608 6,200

4,582

FY09 FY10 FY11 FY12 Upto Q3 FY13

1,679

1,466 1,452

1,603 1,614

1,443 1,525

Q1FY12 Q2FY12 Q3FY12 Q4FY12 Q1FY13 Q2FY13 Q3FY13

Corporate Presentation February 2013

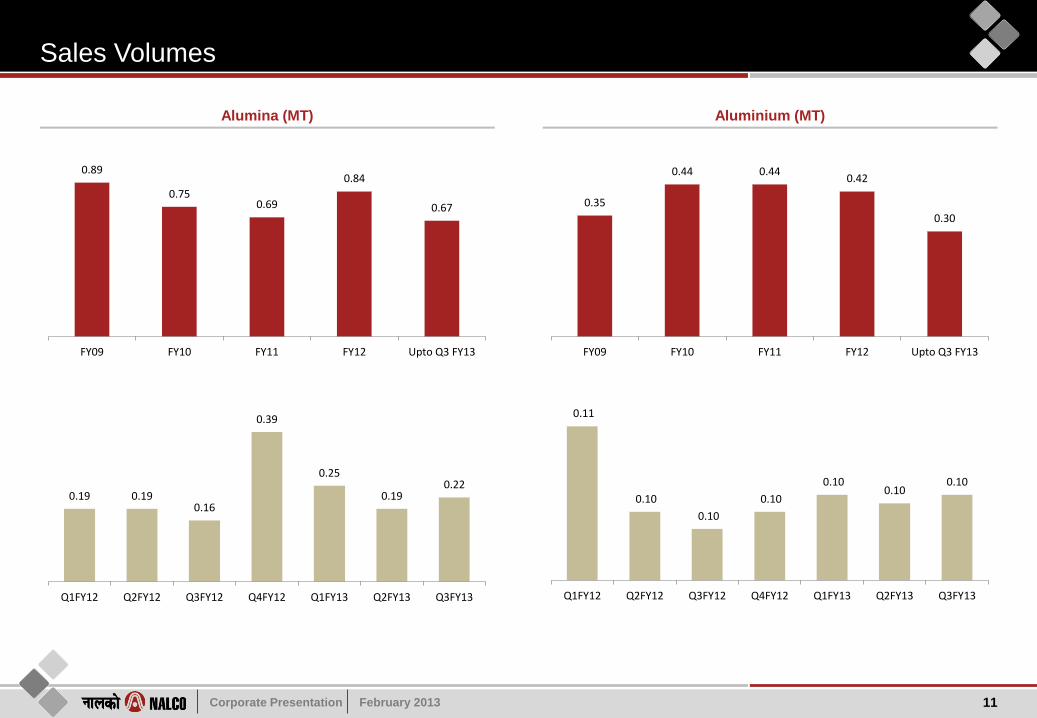

Sales Volumes

11

Alumina (MT)

Aluminium (MT)

0.89

0.75 0.69

0.84

0.67

FY09 FY10 FY11 FY12 Upto Q3 FY13

0.35

0.44 0.44 0.42

0.30

FY09 FY10 FY11 FY12 Upto Q3 FY13

0.19 0.19 0.16

0.39

0.25

0.19 0.22

Q1FY12 Q2FY12 Q3FY12 Q4FY12 Q1FY13 Q2FY13 Q3FY13

0.11

0.10

0.10

0.10

0.10 0.10

0.10

Q1FY12 Q2FY12 Q3FY12 Q4FY12 Q1FY13 Q2FY13 Q3FY13

Corporate Presentation February 2013

Average Realization

12

Alumina Export ($/T)

Aluminium Export ($/T)

Aluminium Domestic

(Rs/T)

316

264

350 374 326

FY09 FY10 FY11 FY12 Upto Q3 FY13

418 400 354 339 341

310 322

Q1FY12 Q2FY12 Q3FY12 Q4FY12 Q1FY13 Q2FY13 Q3FY13

2,234 1,946

2,335 2,434 2,159

FY09 FY10 FY11 FY12 Upto Q3 FY13

2,726 2,599 2,265 2,228 2,191 2,102 2,210

Q1FY12 Q2FY12 Q3FY12 Q4FY12 Q1FY13 Q2FY13 Q3FY13

108,659 95,368

110,038 120,301 126,907

FY09 FY10 FY11 FY12 Upto Q3 FY13

124,365

119,489 115,949

120,986 123,135

128,500 129,244

Q1FY12 Q2FY12 Q3FY12 Q4FY12 Q1FY13 Q2FY13 Q3FY13

Corporate Presentation February 2013

Aluminium – Domestic & Global Demand

3

Corporate Presentation February 2013

India Demand Outlook

14

Consumption Pattern(1)

Consumer appliance market expected to see significant upsides

on account of rapid urbanization and growth in the economy

India is one of the world’s largest auto markets

While power and construction are seeing short term headwinds,

given the “deficits” – they are likely to see continuing investments

Drivers for End Use

Per Capita Consumptions (Kg)(2)

Share of Major Primary Producers (FY 12)

Transport 28%

Construction 20%

Packaging 18%

Electrical 11%

Consumer Durables

6%

Machinery & Equipment

9%

Other 8%

World

Transport 15%

Construction 13%

Packaging 4%

Electrical 48%

Consumer Durables

7%

Machinery & Equipment

7%

Other 6%

India

1.8

6.8

16.7 16.7

22.3 26.2 27.6

38.2

8

IN BRZ CHN CNDA USA ITLY JAP GER Wrld Avg.

(1) Source: EAA, US GS, INDIASTATS, CRU (2) Source: IMF, Industry Estimates

NALCO 25%

HINDALCO 35%

VEDANTA 40%

Corporate Presentation February 2013

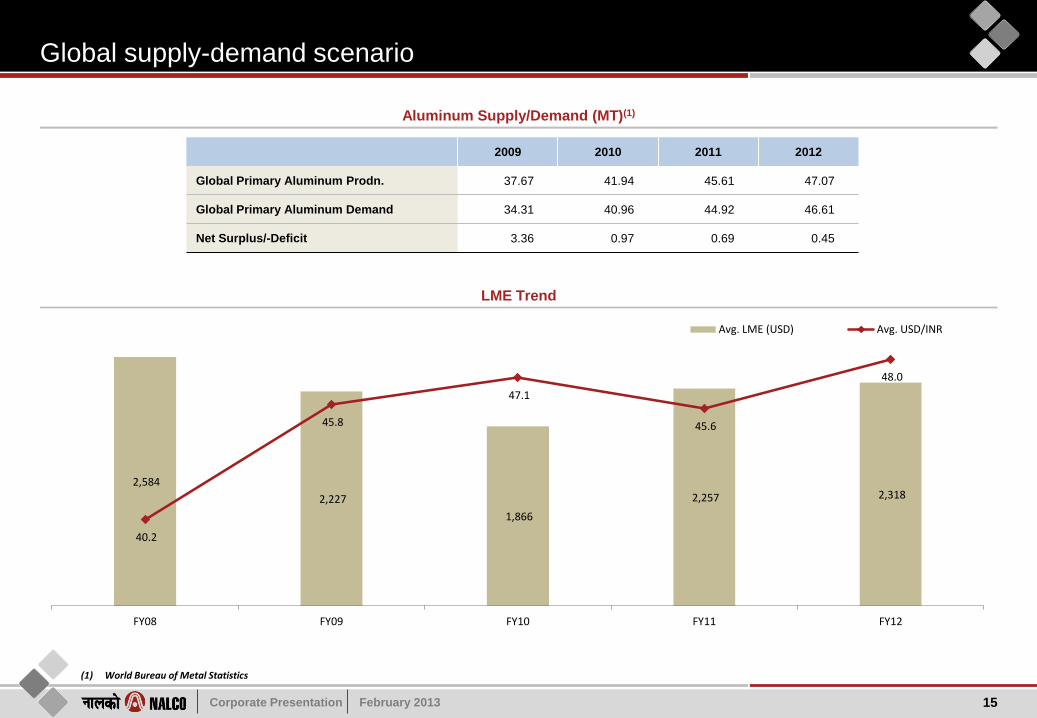

Global supply-demand scenario

2009 2010 2011 2012

Global Primary Aluminum Prodn. 37.67 41.94 45.61 47.07

Global Primary Aluminum Demand 34.31 40.96 44.92 46.61

Net Surplus/-Deficit 3.36 0.97 0.69 0.45

15

Aluminum Supply/Demand (MT)(1)

LME Trend

(1) World Bureau of Metal Statistics

2,584

2,227

1,866

2,257 2,318

40.2

45.8

47.1

45.6

48.0

FY08 FY09 FY10 FY11 FY12

Avg. LME (USD) Avg. USD/INR

Corporate Presentation February 2013

Financials

4

Corporate Presentation February 2013

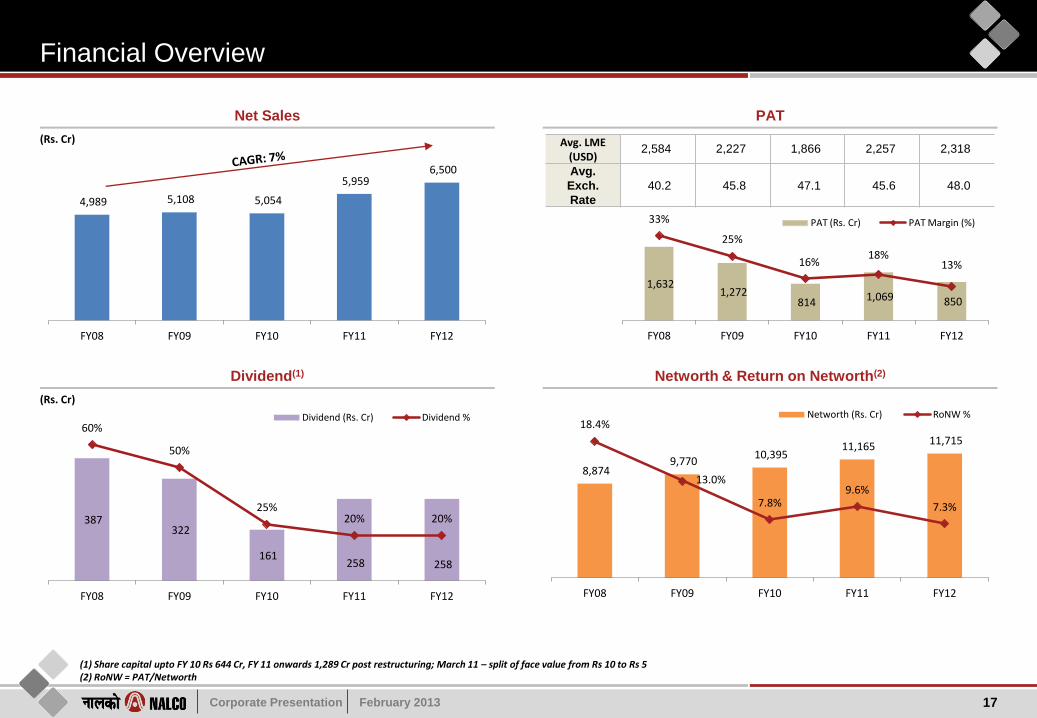

Financial Overview

17

Net Sales

Dividend(1)

PAT

Networth & Return on Networth(2)

(1) Share capital upto FY 10 Rs 644 Cr, FY 11 onwards 1,289 Cr post restructuring; March 11 – split of face value from Rs 10 to Rs 5 (2) RoNW = PAT/Networth

4,989 5,108 5,054

5,959 6,500

FY08 FY09 FY10 FY11 FY12

1,632 1,272

814 1,069 850

33%

25%

16% 18%

13%

FY08 FY09 FY10 FY11 FY12

PAT (Rs. Cr) PAT Margin (%)

387 322

161 258 258

60%

50%

25% 20% 20%

FY08 FY09 FY10 FY11 FY12

Dividend (Rs. Cr) Dividend %

(Rs. Cr)

(Rs. Cr)

8,874 9,770

10,395 11,165 11,715

18.4%

13.0%

7.8% 9.6%

7.3%

FY08 FY09 FY10 FY11 FY12

Networth (Rs. Cr) RoNW %

Avg. LME (USD)

2,584 2,227 1,866 2,257 2,318

Avg.

Exch.

Rate

40.2 45.8 47.1 45.6 48.0

Corporate Presentation February 2013

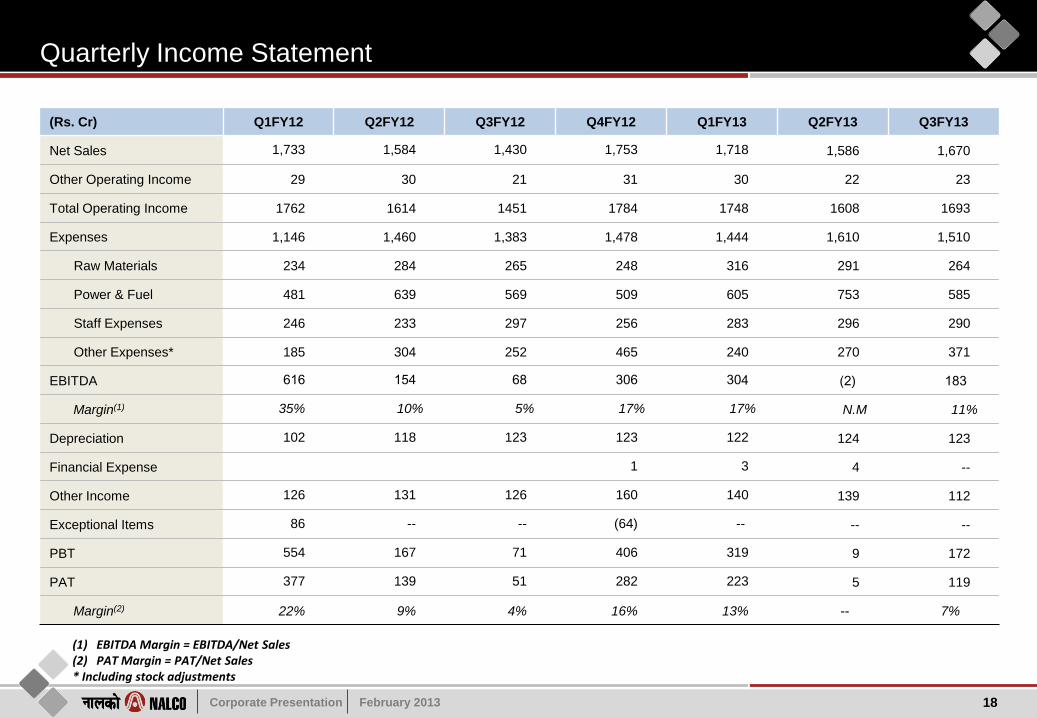

Quarterly Income Statement

18

(1) EBITDA Margin = EBITDA/Net Sales (2) PAT Margin = PAT/Net Sales * Including stock adjustments

(Rs. Cr) Q1FY12 Q2FY12 Q3FY12 Q4FY12 Q1FY13 Q2FY13 Q3FY13

Net Sales 1,733 1,584 1,430 1,753 1,718 1,586 1,670

Other Operating Income 29 30 21 31 30 22 23

Total Operating Income 1762 1614 1451 1784 1748 1608 1693

Expenses 1,146 1,460 1,383 1,478 1,444 1,610 1,510

Raw Materials 234 284 265 248 316 291 264

Power & Fuel 481 639 569 509 605 753 585

Staff Expenses 246 233 297 256 283 296 290

Other Expenses* 185 304 252 465 240 270 371

EBITDA 616 154 68 306 304 (2) 183

Margin(1) 35% 10% 5% 17% 17% N.M 11%

Depreciation 102 118 123 123 122 124 123

Financial Expense 1 3 4 --

Other Income 126 131 126 160 140 139 112

Exceptional Items 86 -- -- (64) -- -- --

PBT 554 167 71 406 319 9 172

PAT 377 139 51 282 223 5 119

Margin(2) 22% 9% 4% 16% 13% -- 7%

Corporate Presentation February 2013

Our Expansion Projects

5

Corporate Presentation February 2013

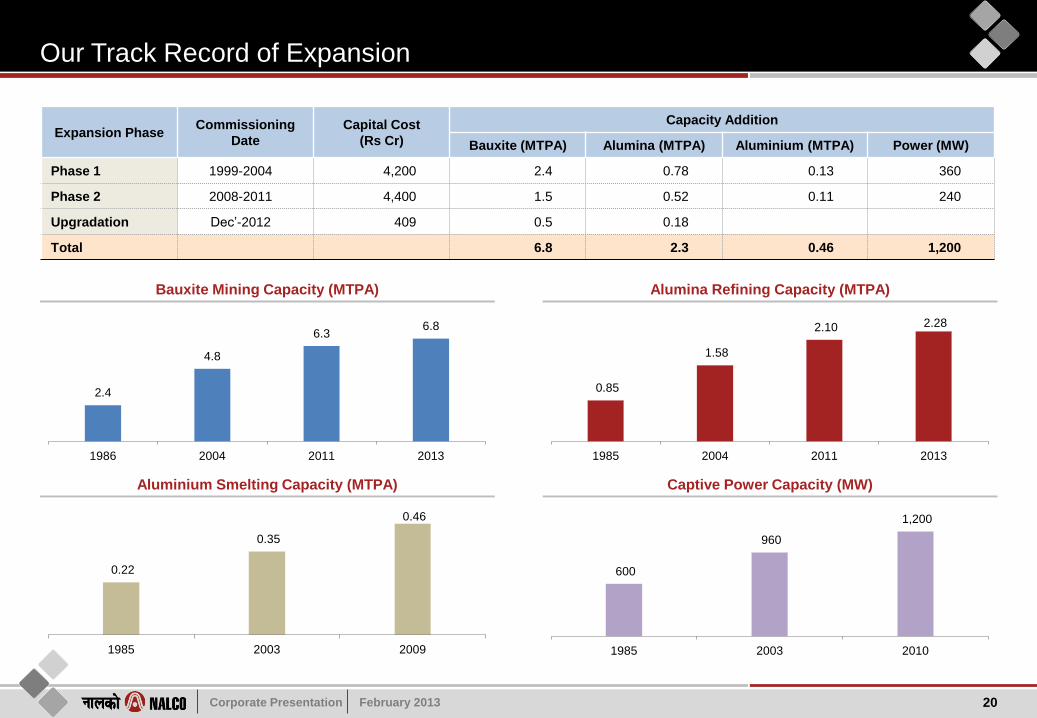

Our Track Record of Expansion

2.4

4.8

6.3 6.8

1986 2004 2011 2013

20

Bauxite Mining Capacity (MTPA)

Aluminium Smelting Capacity (MTPA)

0.85

1.58

2.10 2.28

1985 2004 2011 2013

Alumina Refining Capacity (MTPA)

Captive Power Capacity (MW)

0.22

0.35

0.46

1985 2003 2009

600

960

1,200

1985 2003 2010

Expansion Phase Commissioning

Date

Capital Cost

(Rs Cr)

Capacity Addition

Bauxite (MTPA) Alumina (MTPA) Aluminium (MTPA) Power (MW)

Phase 1 1999-2004 4,200 2.4 0.78 0.13 360

Phase 2 2008-2011 4,400 1.5 0.52 0.11 240

Upgradation Dec’-2012 409 0.5 0.18

Total 6.8 2.3 0.46 1,200

Corporate Presentation February 2013

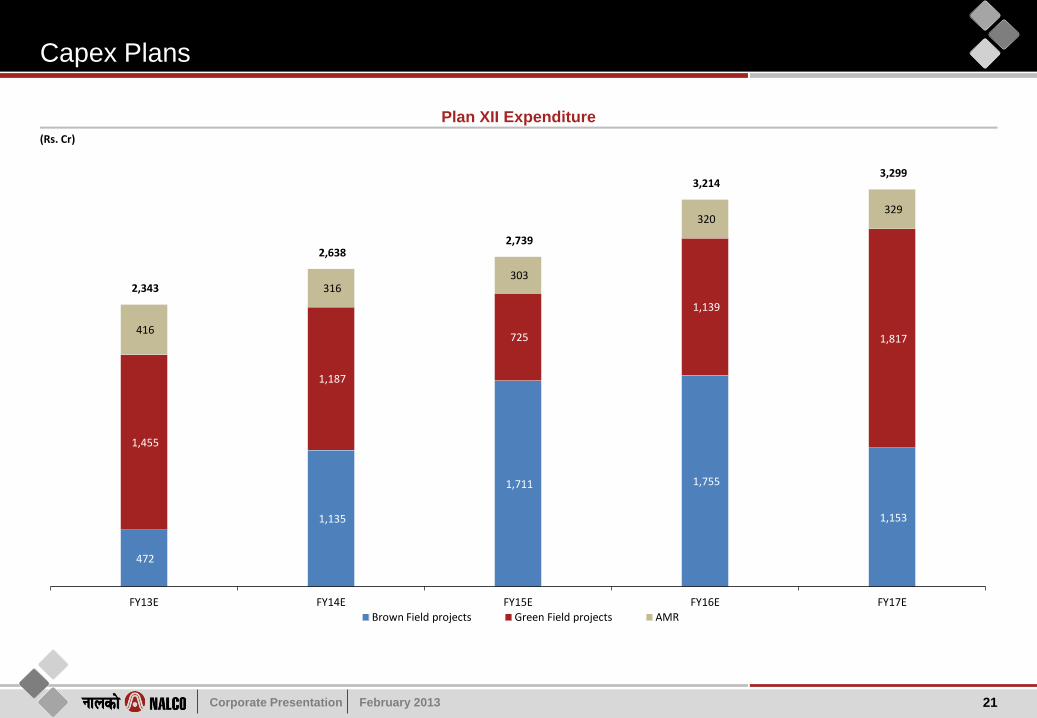

Capex Plans

21

Plan XII Expenditure

472

1,135

1,711 1,755

1,153

1,455

1,187

725

1,139

1,817 416

316 303

320 329

2,343

2,638 2,739

3,214 3,299

FY13E FY14E FY15E FY16E FY17E

Brown Field projects Green Field projects AMR

(Rs. Cr)

Corporate Presentation February 2013

Projects Completed & Under Construction

6

Corporate Presentation February 2013

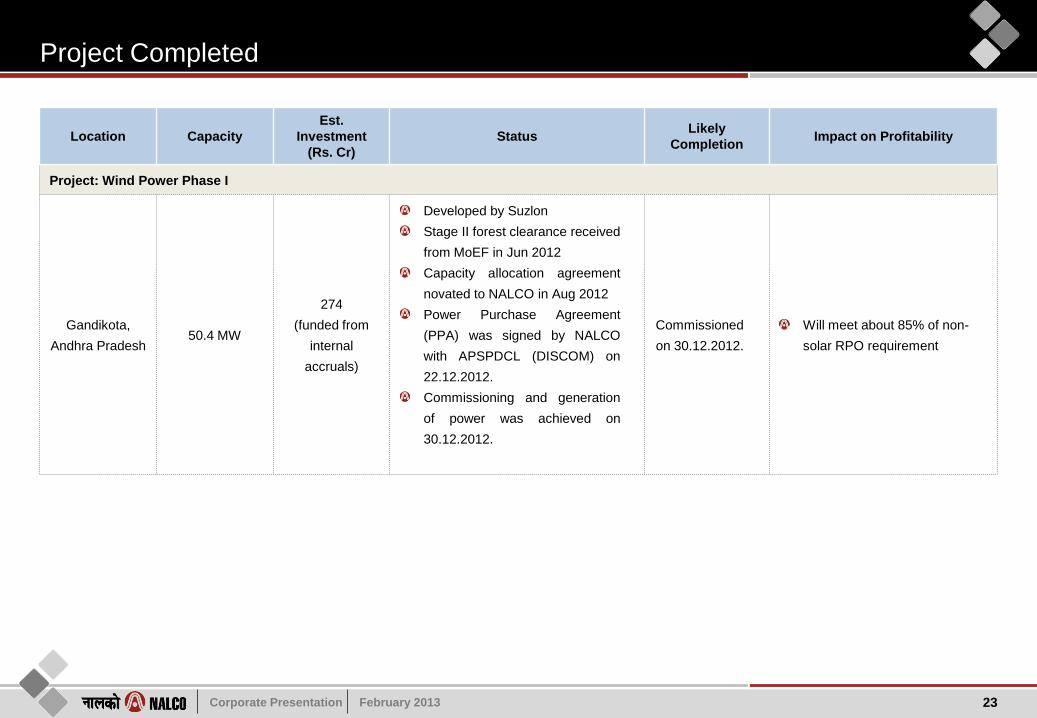

Project Completed

Location Capacity

Est.

Investment

(Rs. Cr)

Status Likely

Completion Impact on Profitability

Project: Wind Power Phase I

Gandikota,

Andhra Pradesh 50.4 MW

274

(funded from

internal

accruals)

Developed by Suzlon

Stage II forest clearance received

from MoEF in Jun 2012

Capacity allocation agreement

novated to NALCO in Aug 2012

Power Purchase Agreement

(PPA) was signed by NALCO

with APSPDCL (DISCOM) on

22.12.2012.

Commissioning and generation

of power was achieved on

30.12.2012.

Commissioned

on 30.12.2012.

Will meet about 85% of non-

solar RPO requirement

23

Corporate Presentation February 2013

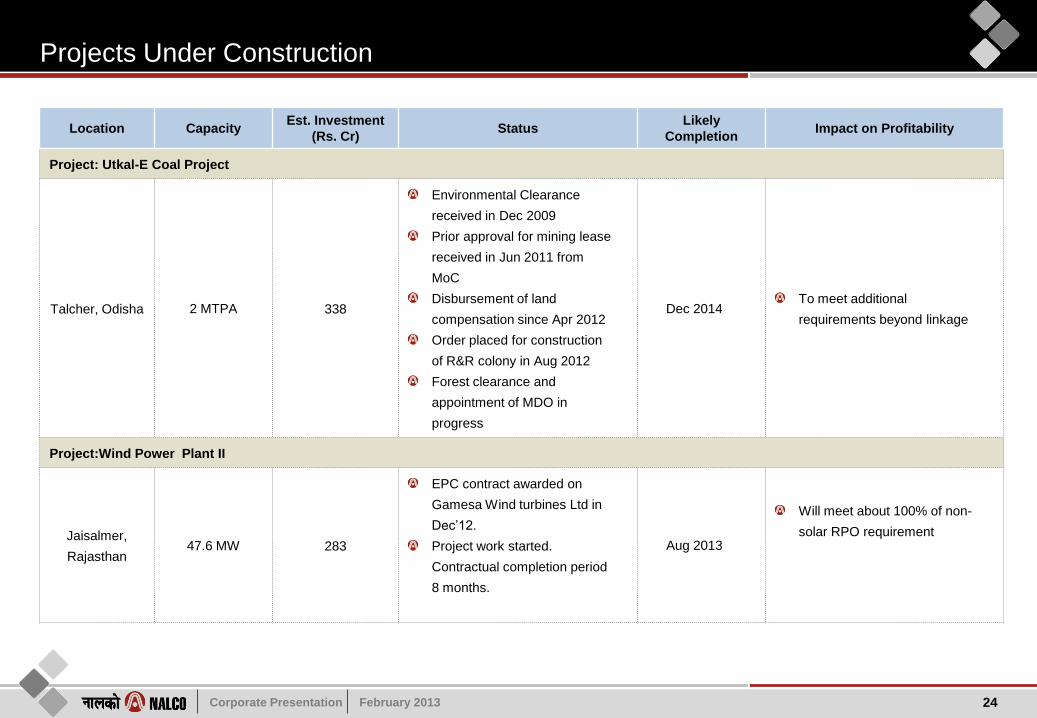

Projects Under Construction

Location Capacity Est. Investment

(Rs. Cr) Status

Likely

Completion Impact on Profitability

Project: Utkal-E Coal Project

Talcher, Odisha 2 MTPA 338

Environmental Clearance

received in Dec 2009

Prior approval for mining lease

received in Jun 2011 from

MoC

Disbursement of land

compensation since Apr 2012

Order placed for construction

of R&R colony in Aug 2012

Forest clearance and

appointment of MDO in

progress

Dec 2014 To meet additional

requirements beyond linkage

Project:Wind Power Plant II

Jaisalmer,

Rajasthan 47.6 MW 283

EPC contract awarded on

Gamesa Wind turbines Ltd in

Dec’12.

Project work started.

Contractual completion period

8 months.

Aug 2013

Will meet about 100% of non-

solar RPO requirement

24

Corporate Presentation February 2013

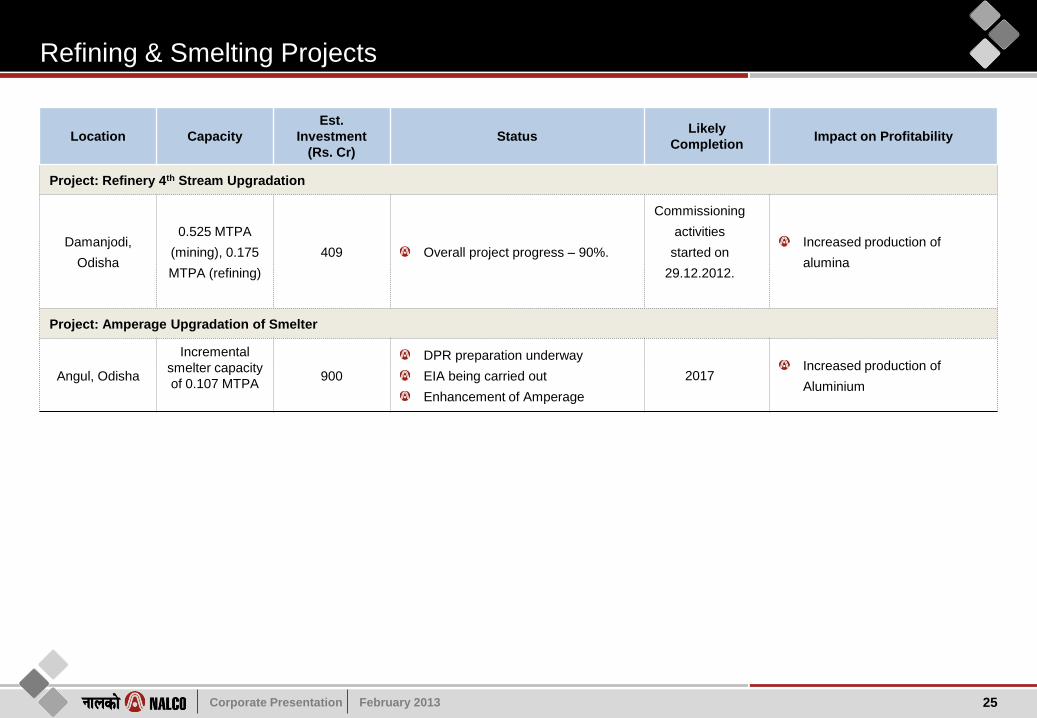

Refining & Smelting Projects

Location Capacity

Est.

Investment

(Rs. Cr)

Status Likely

Completion Impact on Profitability

Project: Refinery 4th Stream Upgradation

Damanjodi,

Odisha

0.525 MTPA

(mining), 0.175

MTPA (refining)

409 Overall project progress – 90%.

Commissioning

activities

started on

29.12.2012.

Increased production of

alumina

Project: Amperage Upgradation of Smelter

Angul, Odisha

Incremental

smelter capacity

of 0.107 MTPA

900

DPR preparation underway

EIA being carried out

Enhancement of Amperage

2017 Increased production of

Aluminium

25

Corporate Presentation February 2013

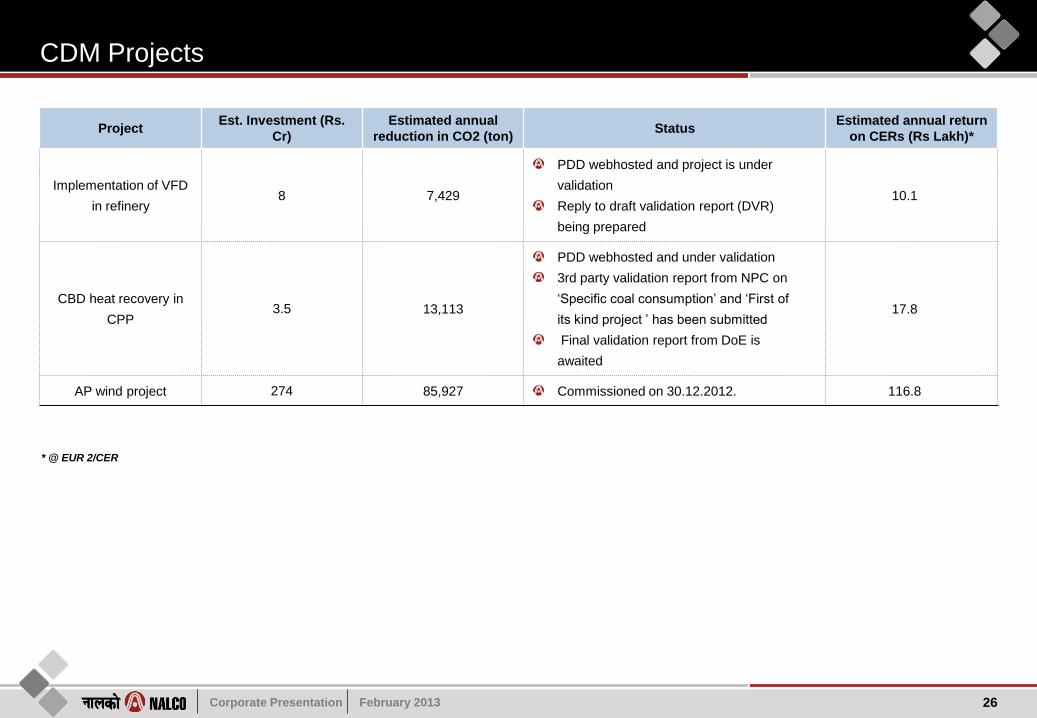

CDM Projects

26

Project Est. Investment (Rs.

Cr)

Estimated annual

reduction in CO2 (ton) Status

Estimated annual return

on CERs (Rs Lakh)*

Implementation of VFD

in refinery 8 7,429

PDD webhosted and project is under

validation

Reply to draft validation report (DVR)

being prepared

10.1

CBD heat recovery in

CPP 3.5 13,113

PDD webhosted and under validation

3rd party validation report from NPC on

‘Specific coal consumption’ and ‘First of

its kind project ’ has been submitted

Final validation report from DoE is

awaited

17.8

AP wind project 274 85,927 Commissioned on 30.12.2012. 116.8

* @ EUR 2/CER

Corporate Presentation February 2013

Projects Under Planning

7

Corporate Presentation February 2013

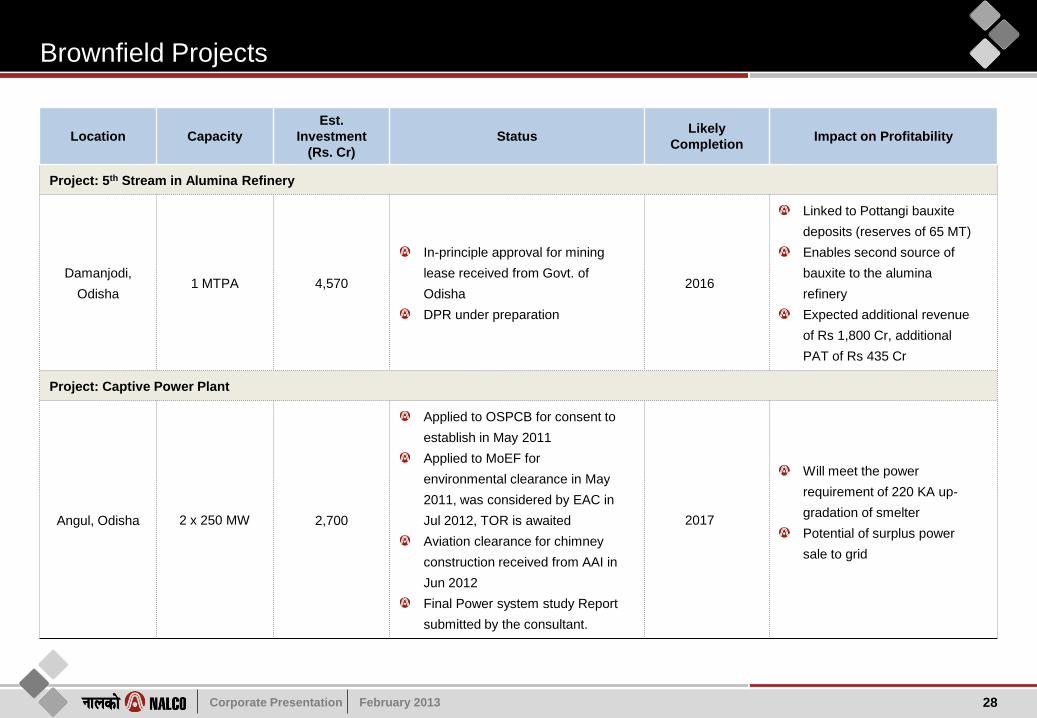

Brownfield Projects

28

Location Capacity

Est.

Investment

(Rs. Cr)

Status Likely

Completion Impact on Profitability

Project: 5th Stream in Alumina Refinery

Damanjodi,

Odisha 1 MTPA 4,570

In-principle approval for mining

lease received from Govt. of

Odisha

DPR under preparation

2016

Linked to Pottangi bauxite

deposits (reserves of 65 MT)

Enables second source of

bauxite to the alumina

refinery

Expected additional revenue

of Rs 1,800 Cr, additional

PAT of Rs 435 Cr

Project: Captive Power Plant

Angul, Odisha 2 x 250 MW 2,700

Applied to OSPCB for consent to

establish in May 2011

Applied to MoEF for

environmental clearance in May

2011, was considered by EAC in

Jul 2012, TOR is awaited

Aviation clearance for chimney

construction received from AAI in

Jun 2012

Final Power system study Report

submitted by the consultant.

2017

Will meet the power

requirement of 220 KA up-

gradation of smelter

Potential of surplus power

sale to grid

Corporate Presentation February 2013

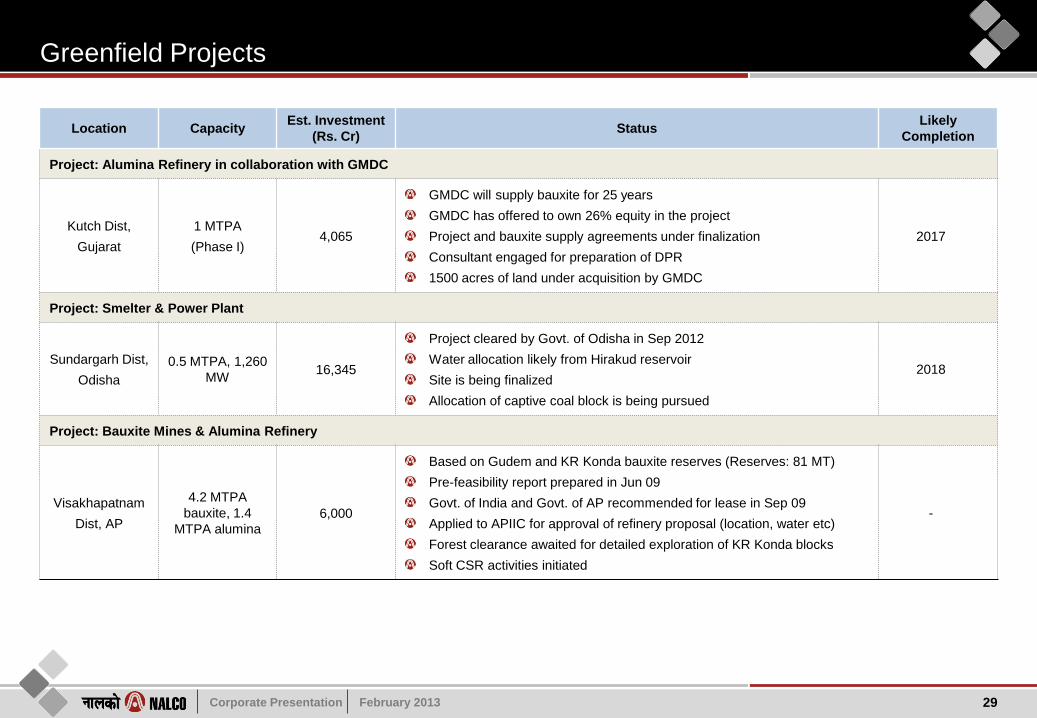

Greenfield Projects

29

Location Capacity Est. Investment

(Rs. Cr) Status

Likely

Completion

Project: Alumina Refinery in collaboration with GMDC

Kutch Dist,

Gujarat

1 MTPA

(Phase I) 4,065

GMDC will supply bauxite for 25 years

GMDC has offered to own 26% equity in the project

Project and bauxite supply agreements under finalization

Consultant engaged for preparation of DPR

1500 acres of land under acquisition by GMDC

2017

Project: Smelter & Power Plant

Sundargarh Dist,

Odisha

0.5 MTPA, 1,260

MW 16,345

Project cleared by Govt. of Odisha in Sep 2012

Water allocation likely from Hirakud reservoir

Site is being finalized

Allocation of captive coal block is being pursued

2018

Project: Bauxite Mines & Alumina Refinery

Visakhapatnam

Dist, AP

4.2 MTPA

bauxite, 1.4

MTPA alumina

6,000

Based on Gudem and KR Konda bauxite reserves (Reserves: 81 MT)

Pre-feasibility report prepared in Jun 09

Govt. of India and Govt. of AP recommended for lease in Sep 09

Applied to APIIC for approval of refinery proposal (location, water etc)

Forest clearance awaited for detailed exploration of KR Konda blocks

Soft CSR activities initiated

-

Corporate Presentation February 2013

Vertical Integration Projects

30

Location Capacity Est. Investment

(Rs. Cr) Status

Likely

Completion

Project: Caustic Soda plant in collaboration with GACL

Dahej, Gujarat 0.2 MTPA 600-800

MoU signed with Gujarat Alkalis and Chemicals Ltd (GACL)

DPR being prepared by GACL

Critical factors are availability of salt (main raw material) and disposal of

chlorine (toxic by-product)

Favourable factors are availability of salt & ethylene and well-developed

market for chlorine in Gujarat

2016

Project: Aluminium Conductor plant in collaboration with PGCIL

To be firmed up 0.55 MTPA 200

MOU signed with PGCIL in Oct 2011

NALCO to supply aluminium and PGCIL to source conductors from the

JV at mutually agreed price

Feasibility report under preparation

-

Corporate Presentation February 2013

Diversification Projects (Power)

31

Location Capacity Est. Investment

(Rs. Cr) Status

Likely

Completion

Project: Nuclear Power in collaboration with NPCIL

Kakkarpar,

Gujarat 2 x 700 MW

11,459

(NALCO’s 49%

share of equity:

1,685)

JV incorporated in Mar 12

Initial equity investment of 26% (Rs 894 Cr) approved by the Board, to

be enhanced to 49% upon approval of GoI through CCS

Approval of CCS is awaited for 1st tranche of equity contribution.

2016

Project: Solar Power

To be firmed up 15 MW 150

Feasibility report prepared

Selection of suitable site is underway

Power generation will meet future solar RPO

2015

Project: Wind Power Plant III

Odisha

Capacity and investment would be

ascertained in the feasibility report.

Wind data validation done by C-WET.

Consultant engaged for preparation of Techno Economic Feasibility

Report (TEFR).

Power evacuation arrangement /infrastructure and statutory compliances

being reviewed.

2014

Project: IPP (UMPP) in consortium

To be firmed up 4,000 MW 20,000

Participating in consortium as a lead partner

Discussions held with interested CPSEs for consortium bidding for

UMPPs

RFQ submitted for UMPP Odisha & will be submitted for UMPP

Chhattisgrah (Due Date 3rd April’13).

-

Corporate Presentation February 2013

Awards & Governance

8

Corporate Presentation February 2013

Recent Awards

33

Non-ferrous Best Performance Award:2011-12” in the category of large integrated plants, instituted by the Indian Institute

of Metals.

2012

PSE Excellence Award for CSR initiatives by Govt. of India 2011

National Energy Conservation Award 2011, 2010

Top Export Award of CAPEXIL 1998-2011

Best Listed CPSE Award by Govt. of India 2010

EEPC (Eastern Region)’s Gold Award as Top Exporter in Large Enterprise category 2010

Think Odisha Leadership Award for the Education Initiative in Tribal Belt of Koraput organized by the Times of India

Group 2012

Dun & Bradstreet’s Best PSU Award in Non-Ferrous Metal Category

2012

IPE- CSR Corporate Governance Award. 2012

Corporate Presentation February 2013

CSR Initiatives

Started allocating 0.5% of net profit every year for periphery

development activities since FY99

Doubled to 1.0% of net profit since FY03

Further increased to 2.0% of net profit since FY11 (equally split

between periphery development & CSR)

Allocation:

40% - Damanjodi area where mines & refinery are located

40% - Angul area where smelter & power plants are located

20% - Other areas

34

CSR Policy

Set up by the Board in Jul 2010 for CSR activities, to be funded

to the extent of 1.0% of net profit

Focused on development of villages located within 15 km of

NALCO’s Mines & Plants in Damanjodi and Angul including

proposed mining areas such as Pottangi (Koraput) and Gudem &

KR Konda (Visakhapatnam & East Godavari districts of AP)

361 tribal & non-tribal children from periphery villages have been

sponsored for education in reputed institutions

Skill development initiatives

NALCO Foundation

Rehabilitation & Periphery Development Advisory Committees

(RPDACs), at Koraput and Angul headed by concerned RDCs,

with local representatives decide all policy and project matters

NALCO has contributed Rs 158 Cr since inception for rural roads,

education, healthcare, water supply, community development,

social welfare and environment

4 schools (DPS and Saraswati Vidya Mandir) are being run at

both complexes since 1983-84, in which nearly half of the

students belong to periphery villages

Periphery Development Expenditure

Shifted away from the earlier donor-based approach

Ensuring participation of the primary stakeholders at the

grassroots in the decision making process

Broad methodology:

Need assessment & baseline survey

Project identification

Selection of implementing agencies

Monitoring and evaluation

Social auditing by independent bodies

Documentation of experience

Project-based Accountability Approach

Corporate Presentation February 2013

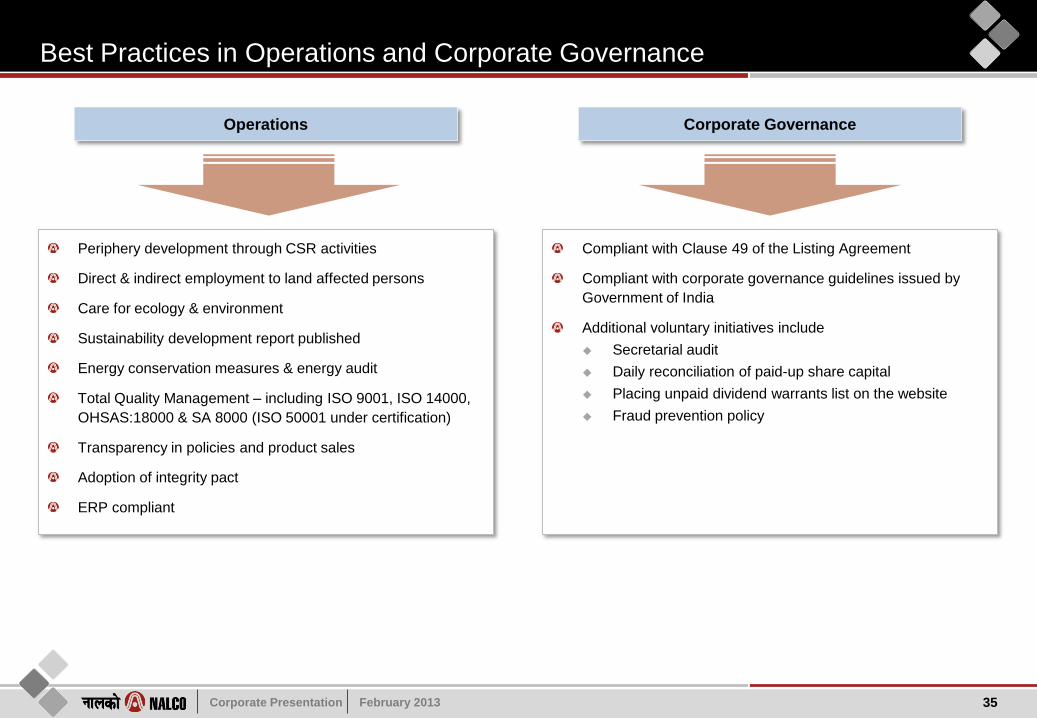

Best Practices in Operations and Corporate Governance

35

Periphery development through CSR activities

Direct & indirect employment to land affected persons

Care for ecology & environment

Sustainability development report published

Energy conservation measures & energy audit

Total Quality Management – including ISO 9001, ISO 14000,

OHSAS:18000 & SA 8000 (ISO 50001 under certification)

Transparency in policies and product sales

Adoption of integrity pact

ERP compliant

Operations Corporate Governance

Compliant with Clause 49 of the Listing Agreement

Compliant with corporate governance guidelines issued by

Government of India

Additional voluntary initiatives include

Secretarial audit

Daily reconciliation of paid-up share capital

Placing unpaid dividend warrants list on the website

Fraud prevention policy

Corporate Presentation February 2013

Thank You

![Presentation on Aluminum Park at Anugul-Odisha by NALCO[1]](https://img.pdfslide.net/doc/110x75/577ce72e1a28abf103948453/presentation-on-aluminum-park-at-anugul-odisha-by-nalco1.jpg)