Embed Size (px)

DESCRIPTION

October 13 research note for US Natural Gas Drivers.

Citation preview

Important Notice: In relation to European MIF directive, this publication could not be characterised as independent investment research. Please refer to disclaimer on last page.

Global

Weekly

13 October 200913 October 200913 October 200913 October 2009

IIIImportant Notice: The circumstances in which this publication has been produced are such that it is not appropriate to characterise it as independent investment research as referred to in

European MIF directive and that it should be treated as a marketing material even if it contains a research recommendation (« recommandation d�investissement à caractère promotionnel »).

US Natural Gas US Natural Gas US Natural Gas US Natural Gas Drivers

Laurent Key +1 212 278 57 36 [email protected]

Stephanie Aymes +44 207 762 58 98 [email protected]

www.commodiwww.commodiwww.commodiwww.commodittttiiiies.sgcib.comes.sgcib.comes.sgcib.comes.sgcib.com

US NATURAL GAS SCOREBOARDUS NATURAL GAS SCOREBOARDUS NATURAL GAS SCOREBOARDUS NATURAL GAS SCOREBOARD

ScoreScoreScoreScore WeightWeightWeightWeight CommentCommentCommentComment

Market Fundamentals 2.9 60% Neutral: unexpected rise in production will offset stronger residential demand.

U.S. Demand 3.1 40% Expected colder than normal temperatures in the Northeast and the Midwest are the only bullish factor.

Res/comm 4 55% Up 2 Bcf/d last week with cool temperatures. The rising trend in res. demand should continue with

expected colder than normal temps in high consuming area.

Industrial - US Economy 2 35% Stable w/w but still more than 1 Bcf/d below pre-crisis levels.

Power generation (EG) 2 10% The seasonal decline in EG demand is compounded by less price-related coal-to-gas switching.

U.S. Supply 2.0 30% Production is already back to H1 '09 levels, due to the combined effect of a strong cash market and pipelines returning from maintenance.

Domestic Production 1 60%

A two-week increase of 1.4 Bcf/d, to 56.4 Bcf/d, as Gulf pipeline maintenances finish ahead of

schedule. Current spot prices above $3.5 may result in increasing shale gas production for Oct.

Rising Southeast output may already be offsetting depressed Rockies production.

Canadian Imports 5 20% Down 0.3 Bcf/d last week, on increased domestic demand and declining production.

LNG 2 20% Slightly up last week by 0.3 bcf/d. The completion of global liquefaction facilities, and rising US

spot margins, will boost imports to more than1 Bcf/d for the coming winter.

Inventories (Storage) 3.4 30% Bullish short-term on injection reports; bearish for the medium-term.

Short-term expectations 4 40% Cold weather decreases daily injections: Thursday's EIA report expected at 54 Bcf . Next week in the

30-40 Bcf range, respectively 5 Bcf and 25 Bcf below the 5-yr average.

Long-term expectations 3 60% Since domestic production may have plateaued at high levels, we expect a tighter supply-and-

demand balance by end-of-March 2010. Neutral since inv. Levels will still be high.

Market signals 2.6 40% Bearish short-term, bullish medium term.

Hedge Funds 3 20% As of last week, funds are longer by 5,000 contracts. Total Open Interest is unchanged. With prices

range bound at $4.8-4.9 , ATM vol. may end its decline and stay around 60%.

Implied Probability 1 20% A strong bearish skew on the Nov '09 contract.

Technical Analysis 3 40% Bearish short-term, bullish medium term on a possible reverse head and shoulder pattern.

Global markets 3 20% Rising energy markets may provide a support to NG, but no clear correlation for the moment.

THIS WEEK TREND 2.8 100% A looser supply and demand balance may weigh on prices for the short term. However, flattening production adds a bullish skew for the medium term.

Scoring: 1Scoring: 1Scoring: 1Scoring: 1 = = = = strongly bearis strongly bearis strongly bearis strongly bearishhhh 2222 ==== bearishbearishbearishbearish 3333 ==== neutral neutral neutral neutral 4444 ==== bullishbullishbullishbullish 5555 = = = = strongly bullishstrongly bullishstrongly bullishstrongly bullish

Editorial 2

Natural Gas Price Information 4

Natural Gas Price Information &

Supply/Demand Balance 5

Supply Components 6

Demand Forecasts 7

Demand Breakdown & Inventory 8

Inventory & Withdrawal 9

Weather 10

Technical Analysis NatGas 11

US Natural Gas Forecasts - Last

updated 25/09/09 12

Economic Indicators 13

Trading Contacts 16

���� EDITORIAL

13 October 2009 US Natural Gas US Natural Gas US Natural Gas US Natural Gas DriversDriversDriversDrivers

2222

Editorial

A fundamentally bear market, but only for the short term.

Two Southeast supply area pipelines, recently back from

maintenance, have boosted output to Q1 �09 highs. Total US dry

NG production jumped to 56.4 Bcf/d from 55 Bcf/d by the end-of-

Sept.

The two pipelines, Fayetteville and Greenville laterals, bring natural

gas from the Woodford and Fayetteville shale plays to the Texas

Gas system for exports to the Midwest and Mid-Atlantic consuming

areas. The the Arkoma (Arkansas � Oklahoma) basin flow � which

include the Woodford shale and part of the Fayetteville shale - has

jumped 0.7 Bcf/d from Sep 27. It now sits at 2.6 Bcf/d as of

yesterday. About 60% of the total Arkoma basin gross production

can be monitored with this sample, so the increase in output in this

region may in fact be more than 1 Bcf/d.

This increase in production is bearish for the short-term, until more

winter demand rebalances the market. The total count of drilling

application permits for September suggests that the US output

should remain steady for the next month and then start rising again,

though at a slower pace than by H2 �08. This contradicts SG

research�s previous forecast of a mid-December 2009 rebound.

Arkansas horizontal drilling permit application count peaked in

August 2009 at 152 and was down to 114 for September. After 12

days in October, the count sits at 52, suggesting that total October

applications may reach August levels. This increase will be

reflected in total Fayetteville shale output as early as mid-

November.

The situation is similar to Louisiana�s Haynesville shale: Drilling

application count peaked at 70 in July and fell by 43% in August. It

remained steady m/m for September at about 40. It now sits at 22

after 12 days in October, possibly the first application count

increase since last summer.

The Rockies and Pennsylvania are the only areas to have increases

in horizontal drilling permit applications for September. The one

exception is Colorado, where September permit application count

is down to 72 from 534 in July �09. Colorado production should

continue to head south for the near term � mainly due to concerns

over the environmental cost of shale extraction. The Rockies

remain the region most hurt by the 2009 price decline, due to

higher marginal production costs than in the rest of the US.

Southeast horizontal drilling application countSoutheast horizontal drilling application countSoutheast horizontal drilling application countSoutheast horizontal drilling application count

0

50

100

150

200

250

300

350

Mar-08 Jun-08 Sep-08 Dec-08 Mar-09 Jun-09 Sep-09

Ar - Vertical Ar - Horizontal

La - Vertical La - Horizontal

Source: ZDM, Inc, SG Commodities Research

Overall, US production is now expected to remain at high levels,

since increases in Southeast and Pennsylvania output will offset

decreases in the Rockies. Nov �09 prices should then correct to the

downside, despite the expected below-normal temperatures for the

next 11 days. The resulting increase in residential demand should

impact the cash market, not futures, but at least will keep storage

facilities from high congestion-related pressure issues.

���� EDITORIAL

US Natural Gas US Natural Gas US Natural Gas US Natural Gas DriversDriversDriversDrivers 13 October 2009

3333

A tighter supply-and-demand balance should arise later in the

winter, after the market: 1/ experiences the first withdrawals of the

heating season, and 2/ gets a better view of Canadian imports. The

November temperature forecast is seasonal, which will spur a

consequent y/y increase in residential demand due to the � slowly -

improving economy. In Canada, cold weather and rising rig count

suggest the start of the winter drilling season. In a few weeks, the

market will have a better idea of how much depletion in

conventional production fields is hurting total Canadian output. For

the short-term, Asia and Europe will remain the main spot LNG

buyers, until a 2010 rebound in US imports.

Given the current large contango along the curve, the expectation

for this tighter winter supply-and-demand balance may already be

priced in levels along the curve. To benefit from the expected

medium term tighter S/D balance, SG Research recommends

buying the March/April spread (Buy March, sell April) � at the right

time of course: The spread fell to 0 cents too early in the season,

and then bounced back to 5 cents with the September rise on the

front of the curve. With the October looser supply and demand

balance, it is expected to fall back to below 0 cents. We see this

move as a buying opportunity since the spread will have to return

to high positive levels to encourage withdrawals, as winter gets

underway.

Mar/April 2010 Spread (USD/MMBtu)Mar/April 2010 Spread (USD/MMBtu)Mar/April 2010 Spread (USD/MMBtu)Mar/April 2010 Spread (USD/MMBtu)

-0.04

-0.02

0

0.02

0.04

0.06

0.08

0.1

Jul-09 Aug-09 Sep-09

Daily Close

Source: NYMEX, SG Commodities Research

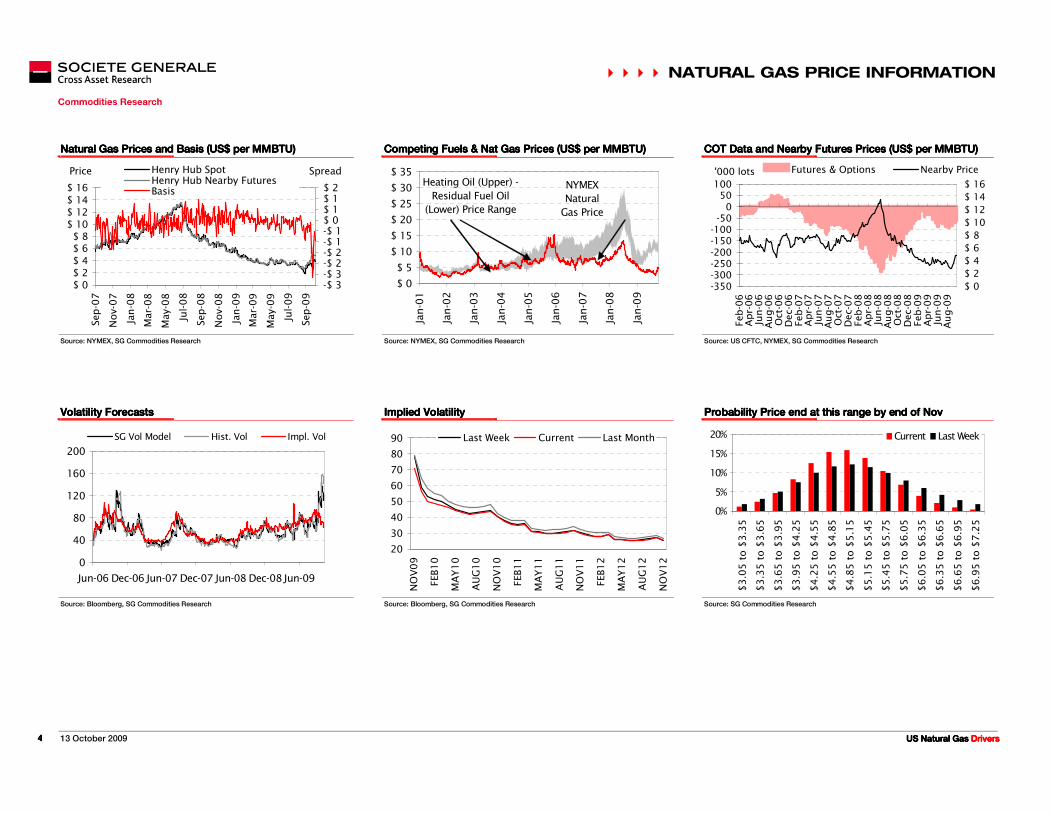

���� NATURAL GAS PRICE INFORMATION

13 October 2009 US Natural Gas US Natural Gas US Natural Gas US Natural Gas DriversDriversDriversDrivers 4444

Natural G as Price I nformation

Natural Gas Prices and Basis (US$ per MMBTU)Natural Gas Prices and Basis (US$ per MMBTU)Natural Gas Prices and Basis (US$ per MMBTU)Natural Gas Prices and Basis (US$ per MMBTU) Competing Fuels & Nat Gas Prices (US$ per MMBTU)Competing Fuels & Nat Gas Prices (US$ per MMBTU)Competing Fuels & Nat Gas Prices (US$ per MMBTU)Competing Fuels & Nat Gas Prices (US$ per MMBTU) COT Data and Nearby Futures PricesCOT Data and Nearby Futures PricesCOT Data and Nearby Futures PricesCOT Data and Nearby Futures Prices (US$ per MMBTU) (US$ per MMBTU) (US$ per MMBTU) (US$ per MMBTU)

$ 0$ 2$ 4

$ 6$ 8$ 10$ 12$ 14

$ 16

Sep-07

Nov-07

Jan-08

Mar-08

May-08

Jul-08

Sep-08

Nov-08

Jan-09

Mar-09

May-09

Jul-09

Sep-09

Price

-$ 3-$ 3-$ 2-$ 2-$ 1-$ 1$ 0$ 1$ 1$ 2

SpreadHenry Hub Spot Henry Hub Nearby FuturesBasis

NYMEX

Natural

Gas Price

$ 0

$ 5

$ 10

$ 15

$ 20

$ 25

$ 30

$ 35

Jan

-01

Jan

-02

Jan

-03

Jan

-04

Jan

-05

Jan

-06

Jan

-07

Jan

-08

Jan

-09

Heating Oil (Upper) -

Residual Fuel Oil

(Lower) Price Range

-350-300-250-200-150-100

-500

50100

Feb

-06

Ap

r-0

6Ju

n-0

6A

ug

-06

Oct-

06

Dec-0

6Feb

-07

Ap

r-0

7Ju

n-0

7A

ug

-07

Oct-

07

Dec-0

7Feb

-08

Ap

r-0

8Ju

n-0

8A

ug

-08

Oct-

08

Dec-0

8Feb

-09

Ap

r-0

9Ju

n-0

9A

ug

-09

'000 lots

$ 0

$ 2

$ 4

$ 6

$ 8

$ 10

$ 12

$ 14

$ 16

Futures & Options Nearby Price

Source: NYMEX, SG Commodities Research Source: NYMEX, SG Commodities Research Source: US CFTC, NYMEX, SG Commodities Research

Volatility ForecastsVolatility ForecastsVolatility ForecastsVolatility Forecasts Implied VolatilityImplied VolatilityImplied VolatilityImplied Volatility Probability Price end at this range bProbability Price end at this range bProbability Price end at this range bProbability Price end at this range by end of Novy end of Novy end of Novy end of Nov

0

40

80

120

160

200

Jun-06 Dec-06 Jun-07 Dec-07 Jun-08 Dec-08 Jun-09

SG Vol Model Hist. Vol Impl. Vol

20

30

40

50

60

70

80

90

NO

V0

9

FEB

10

MA

Y1

0

AU

G1

0

NO

V1

0

FEB

11

MA

Y1

1

AU

G1

1

NO

V1

1

FEB

12

MA

Y1

2

AU

G1

2

NO

V1

2

Last Week Current Last Month

0%

5%

10%

15%

20%

$3

.05

to

$3

.35

$3

.35

to

$3

.65

$3

.65

to

$3

.95

$3

.95

to

$4

.25

$4

.25

to

$4

.55

$4

.55

to

$4

.85

$4

.85

to

$5

.15

$5

.15

to

$5

.45

$5

.45

to

$5

.75

$5

.75

to

$6

.05

$6

.05

to

$6

.35

$6

.35

to

$6

.65

$6

.65

to

$6

.95

$6

.95

to

$7

.25

Current Last Week

Source: Bloomberg, SG Commodities Research Source: Bloomberg, SG Commodities Research Source: SG Commodities Research

���� NATURAL GAS PRICE INFORMATION & SUPPLY/DEMAND BALANCE

US Natural Gas US Natural Gas US Natural Gas US Natural Gas DriversDriversDriversDrivers 13 October 2009

5555

Natural G as Price I nformation & Supply/Dem and Balance

Spread NBP (UK) Spread NBP (UK) Spread NBP (UK) Spread NBP (UK) ---- Henry Hub (US) (US$ per Henry Hub (US) (US$ per Henry Hub (US) (US$ per Henry Hub (US) (US$ per MMBTU) MMBTU) MMBTU) MMBTU) Forward CurvesForward CurvesForward CurvesForward Curves US, UK + Shipping Natural Gas Prices (US$ per MMBTU)US, UK + Shipping Natural Gas Prices (US$ per MMBTU)US, UK + Shipping Natural Gas Prices (US$ per MMBTU)US, UK + Shipping Natural Gas Prices (US$ per MMBTU)

-1.0

0.0

1.0

2.0

3.0

4.0

No

v-0

9

Feb

-10

May-1

0

Au

g-1

0

No

v-1

0

Feb

-11

May-1

1

Au

g-1

1

No

v-1

1

Feb

-12

May-1

2

Au

g-1

2

No

v-1

2

Feb

-13

Latest Last Week Last Month

3

4

5

6

7

8

9

NOV09 SEP10 JUL11 MAY12 MAR13 JAN14 NOV14

Latest Last Month Last Week

0

2

4

6

8

10

12

14

16

Oct-

08

No

v-0

8

Dec-0

8

Jan

-09

Feb

-09

Mar-

09

Ap

r-0

9

May-0

9

Jun

-09

Jul-

09

Au

g-0

9

Sep

-09

Oct-

09

UK US UK + cost of shipping

Source: NYMEX, SG Commodities Research Source: Bloomberg, SG Commodities Research Source: NYMEX, SG Commodities Research

Supply and Demand (Bcf/Supply and Demand (Bcf/Supply and Demand (Bcf/Supply and Demand (Bcf/d)d)d)d) Net Supply and DemandNet Supply and DemandNet Supply and DemandNet Supply and Demand Demand in Bcf/d (w/o Bal. Items w/o Mexican Exports)Demand in Bcf/d (w/o Bal. Items w/o Mexican Exports)Demand in Bcf/d (w/o Bal. Items w/o Mexican Exports)Demand in Bcf/d (w/o Bal. Items w/o Mexican Exports)

25

35

45

55

65

20-Jun 20-Jul 20-Aug 20-Sep 20-Oct

SG Supply Estimate SG Demand Estimate

-10

0

10

20

30

20-Jun 20-Jul 20-Aug 20-Sep 20-Oct

2006-2007 2007-2008 2008-2009

25

35

45

55

65

75

20-Jun 20-Jul 20-Aug 20-Sep 20-Oct

2006-2007 2007-2008 2008-2009

Source: Bentek Energy LLC, DOE EIA, SG Commodities Research Source: Bentek Energy LLC, DOE EIA, SG Commodities Research Source: Bentek Energy LLC, DOE EIA, SG Commodities Research

���� SUPPLY COMPONENTS

13 October 2009 US Natural Gas US Natural Gas US Natural Gas US Natural Gas DriversDriversDriversDrivers 6666

Supply Compo nents

Supply (Bcf/d, incl. netting of Mexican Exports)Supply (Bcf/d, incl. netting of Mexican Exports)Supply (Bcf/d, incl. netting of Mexican Exports)Supply (Bcf/d, incl. netting of Mexican Exports) Domestic Production (Bcf/d)Domestic Production (Bcf/d)Domestic Production (Bcf/d)Domestic Production (Bcf/d) Net Imports (Bcf/d)Net Imports (Bcf/d)Net Imports (Bcf/d)Net Imports (Bcf/d)

47

49

51

53

55

57

59

61

63

65

20-Jun 20-Jul 20-Aug 20-Sep 20-Oct

2006-2007 2007-2008 2008-2009

37

39

41

43

45

47

49

51

53

20-Jun 20-Jul 20-Aug 20-Sep 20-Oct

2006-2007 2007-2008 2008-2009

6

8

10

12

14

16

20-Jun 20-Jul 20-Aug 20-Sep 20-Oct

2006-2007 2007-2008 2008-2009

Source: Bentek Energy LLC, DOE EIA, SG Commodities Research Source: Bentek Energy LLC, DOE EIA, SG Commodities Research Source: Bentek Energy LLC, DOE EIA, SG Commodities Research

Net Imports from Canada (Bcf/d)Net Imports from Canada (Bcf/d)Net Imports from Canada (Bcf/d)Net Imports from Canada (Bcf/d) LNG Sendout (Bcf/d)LNG Sendout (Bcf/d)LNG Sendout (Bcf/d)LNG Sendout (Bcf/d) Rig CountsRig CountsRig CountsRig Counts

4

5

6

7

8

9

10

11

12

20-Jun 20-Jul 20-Aug 20-Sep 20-Oct

2006-2007 2007-2008 2008-2009

0

1

2

3

4

20-Jun 20-Jul 20-Aug 20-Sep 20-Oct

2006-2007 2007-2008 2008-2009

0

400

800

1200

1600

2000

2000200120022003200420052006200720082009

North America US Canada

Source: Bentek Energy LLC, DOE EIA, SG Commodities Research Source: Bentek Energy LLC, DOE EIA, SG Commodities Research Source: Baker Hughes, SG Commodities Research

���� DEMAND FORECASTS

US NaturaUS NaturaUS NaturaUS Natural Gas l Gas l Gas l Gas DriversDriversDriversDrivers 13 October 2009

7777

Demand Forecasts

LNG Sendout by Location (MMcf/d)LNG Sendout by Location (MMcf/d)LNG Sendout by Location (MMcf/d)LNG Sendout by Location (MMcf/d) Lower 48 States (Observed) Demand Forecast (Bcf/d)Lower 48 States (Observed) Demand Forecast (Bcf/d)Lower 48 States (Observed) Demand Forecast (Bcf/d)Lower 48 States (Observed) Demand Forecast (Bcf/d) NorthEast (Observed) Demand Forecast (BNorthEast (Observed) Demand Forecast (BNorthEast (Observed) Demand Forecast (BNorthEast (Observed) Demand Forecast (Bcf/d)cf/d)cf/d)cf/d)

0

500

1000

1500

2000

2500

3000

Mar-07 Sep-07 Mar-08 Sep-08 Mar-09 Sep-09

Lake Charles Excelerate

Elba Island Cove Pt

Everett Sabine Pass

34

38

42

29-Sep 4-Oct 9-Oct 14-Oct 19-Oct 24-Oct

2008 Demand 2009 Demand Forecast

5

7

9

11

29-

Sep

6-

Oct

13-

Oct

20-

Oct

2008 Demand 2009 Demand Forecast

Source: Bentek Energy LLC, SG Commodities Research Source: Bentek Energy LLC, SG Commodities Research Source: Bentek Energy LLC, SG Commodities Research

SouthEast (Observed) Demand (Bcf/d)SouthEast (Observed) Demand (Bcf/d)SouthEast (Observed) Demand (Bcf/d)SouthEast (Observed) Demand (Bcf/d) Gulf (Observed) Demand (BcGulf (Observed) Demand (BcGulf (Observed) Demand (BcGulf (Observed) Demand (Bcf/d)f/d)f/d)f/d) Midwest (Observed) Demand (Bcf/d)Midwest (Observed) Demand (Bcf/d)Midwest (Observed) Demand (Bcf/d)Midwest (Observed) Demand (Bcf/d)

5

6

7

8

29-Sep 4-Oct 9-Oct 14-Oct 19-Oct 24-Oct

2008 Demand 2009 Demand Forecast

0

1

2

3

4

5

6

29-Sep 4-Oct 9-Oct 14-Oct 19-Oct 24-Oct

2008 Demand 2009 Demand Forecast

9

10

11

12

13

29-Sep 4-Oct 9-Oct 14-Oct 19-Oct 24-Oct

2008 Demand 2009 Demand Forecast

Source: Bentek Energy LLC, SG Commodities Research Source: Bentek Energy LLC, SG Commodities Research Source: Bentek Energy LLC, SG Commodities Research

���� DEMAND BREAKDOWN & INVENTORY

13 October 2009 US Natural Gas US Natural Gas US Natural Gas US Natural Gas DriversDriversDriversDrivers 8888

Demand Breakdown & I nv entory

WestWestWestWest (Observed) Demand (Bcf/d) (Observed) Demand (Bcf/d) (Observed) Demand (Bcf/d) (Observed) Demand (Bcf/d) Power Demand (Bcf/d)Power Demand (Bcf/d)Power Demand (Bcf/d)Power Demand (Bcf/d) Industrial Demand (Bcf/d)Industrial Demand (Bcf/d)Industrial Demand (Bcf/d)Industrial Demand (Bcf/d)

9

10

11

12

29-Sep 4-Oct 9-Oct 14-Oct 19-Oct 24-Oct

2008 Demand 2009 Demand Forecast

5

15

25

35

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Power 2006 Power 2007

Power 2008 Power 2009

15

16

17

18

19

20

Jan FebMar Apr May Jun Jul Aug Sep Oct Nov Dec

Industrial 2006 Industrial 2007

Industrial 2008 Industrial 2009

Source: Bentek Energy LLC, SG Commodities Research Source: Bentek Energy LLC, SG Commodities Research Source: Bentek Energy LLC, SG Commodities Research

Residential/Commercial Demand (Bcf/d)Residential/Commercial Demand (Bcf/d)Residential/Commercial Demand (Bcf/d)Residential/Commercial Demand (Bcf/d) US Working Gas Inventory (Bcf)US Working Gas Inventory (Bcf)US Working Gas Inventory (Bcf)US Working Gas Inventory (Bcf) Eastern Region Gas Inventory (Bcf)Eastern Region Gas Inventory (Bcf)Eastern Region Gas Inventory (Bcf)Eastern Region Gas Inventory (Bcf)

0

10

20

30

40

50

60

70

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Res/Comm/Bal 2006 Res/Comm/Bal 2007

Res/Comm/Bal 2008 Res/Comm/Bal 2009

0

1 000

2 000

3 000

4 000

Jan FebMar Apr May Jun Jul Aug Sep Oct Nov Dec

2004-2008 Range 2004-2008 Average

2008 2009

0

500

1 000

1 500

2 000

2 500

Jan FebMar AprMay Jun Jul AugSep Oct NovDec

2004-2008 Range 2004-2008 Average

2008 2009

Source: Bentek Energy LLC, DOE EIA, SG Commodities Research Source: DOE EIA, SG Commodities Research Source: DOE EIA, SG Commodities Research

���� INVENTORY & WITHDRAWAL

US Natural Gas US Natural Gas US Natural Gas US Natural Gas DriversDriversDriversDrivers 13 October 2009

9999

Inventory & Withdrawal

Western Region Gas Inventory (Bcf)Western Region Gas Inventory (Bcf)Western Region Gas Inventory (Bcf)Western Region Gas Inventory (Bcf) Producing Region Gas Inventory (Bcf)Producing Region Gas Inventory (Bcf)Producing Region Gas Inventory (Bcf)Producing Region Gas Inventory (Bcf) Total Lower 48 States Injection/Withdrawal (Bcf)Total Lower 48 States Injection/Withdrawal (Bcf)Total Lower 48 States Injection/Withdrawal (Bcf)Total Lower 48 States Injection/Withdrawal (Bcf)

100

200

300

400

500

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2004-2008 Range 2004-2008 Average

2008 2009

0

200

400

600

800

1 000

1 200

1 400

Jan FebMar Apr May Jun Jul Aug Sep Oct Nov Dec

2004-2008 Range 2004-2008 Average

2008 2009

-300-250-200-150-100

-500

50100150

Jan FebMar Apr May Jun Jul Aug Sep Oct Nov Dec

2004-2008 Range 2004-2008 Average

2008 2009

Source: DOE EIA, SG Commodities Research Source: DOE EIA, SG Commodities Research Source: DOE EIA, SG Commodities Research

Producing U.S. Region Injection/Withdrawal (Bcf)Producing U.S. Region Injection/Withdrawal (Bcf)Producing U.S. Region Injection/Withdrawal (Bcf)Producing U.S. Region Injection/Withdrawal (Bcf) Eastern Region Injection/Withdrawal (Bcf)Eastern Region Injection/Withdrawal (Bcf)Eastern Region Injection/Withdrawal (Bcf)Eastern Region Injection/Withdrawal (Bcf) Western U.S. Region Injection/Withdrawal (Bcf)Western U.S. Region Injection/Withdrawal (Bcf)Western U.S. Region Injection/Withdrawal (Bcf)Western U.S. Region Injection/Withdrawal (Bcf)

-100

-50

0

50

100

Jan FebMar Apr May Jun Jul Aug Sep Oct Nov Dec

2004-2008 Range 2004-2008 Average

2008 2009

-200

-150

-100

-50

0

50

100

Jan FebMar Apr May Jun Jul Aug Sep Oct Nov Dec

2004-2008 Range 2004-2008 Average

2008 2009

-40

-30

-20

-10

0

10

20

30

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2004-2008 Range 2004-2008 Average

2008 2009

Source: DOE EIA, SG Commodities Research Source: DOE EIA, SG Commodities Research Source: DOE EIA, SG Commodities Research

���� WEATHER

13 October 2009 US Natural Gas US Natural Gas US Natural Gas US Natural Gas DriversDriversDriversDrivers 10101010

Weather

Actual v Normal HDD in U.S.Actual v Normal HDD in U.S.Actual v Normal HDD in U.S.Actual v Normal HDD in U.S. Actual v Normal CDD in U.S.Actual v Normal CDD in U.S.Actual v Normal CDD in U.S.Actual v Normal CDD in U.S. Heating/Cooling Demand Forecast (U.S)Heating/Cooling Demand Forecast (U.S)Heating/Cooling Demand Forecast (U.S)Heating/Cooling Demand Forecast (U.S)

0

50

100

150

200

250

Dec-0

5

Mar-

06

Jun

-06

Sep

-06

Dec-0

6

Mar-

07

Jun

-07

Sep

-07

Dec-0

7

Mar-

08

Jun

-08

Au

g-0

8

No

v-0

8

Feb

-09

May-0

9

Au

g-0

9

Normal HDD Actual HDD

0

20

40

60

80

100

120

140

Dec-0

5

Mar-

06

Jun

-06

Sep

-06

Dec-0

6

Mar-

07

Jun

-07

Sep

-07

Dec-0

7

Mar-

08

Jun

-08

Au

g-0

8

No

v-0

8

Feb

-09

May-0

9

Au

g-0

9

Normal CDD Actual CDD

% Difference from Normal

0

10

20

30

40

50

60

70

14-Oct 15-Oct 16-Oct 17-Oct 18-Oct

Source: Bloomberg, SG Commodities Research Source: Bloomberg, SG Commodities Research Source: Dominion Energy Index, Dominion

Heating/Cooling Demand Forecast Heating/Cooling Demand Forecast Heating/Cooling Demand Forecast Heating/Cooling Demand Forecast ---- Central Central Central Central Heating/Cooling Demand Forecast Heating/Cooling Demand Forecast Heating/Cooling Demand Forecast Heating/Cooling Demand Forecast ---- Eastern Eastern Eastern Eastern Heating/Cooling Demand Forecast Heating/Cooling Demand Forecast Heating/Cooling Demand Forecast Heating/Cooling Demand Forecast ---- Western Western Western Western

% Difference from Normal

-50

0

50

100

150

200

14-Oct 15-Oct 16-Oct 17-Oct 18-Oct

Great Lakes Great Plains Lower Mississippi

% Difference from Normal

-50

0

50

100

150

200

250

300

350

400

450

14-Oct 15-Oct 16-Oct 17-Oct 18-Oct

Mid-Atlantic New England South Atlantic

% Difference from Normal

-60

-40

-20

0

20

40

60

80

14-Oct 15-Oct 16-Oct 17-Oct 18-Oct

Pacific Rocky Mountains Southwest

Source: Dominion Energy Index, Dominion Source: Dominion Energy Index, Dominion Source: Dominion Energy Index, Dominion

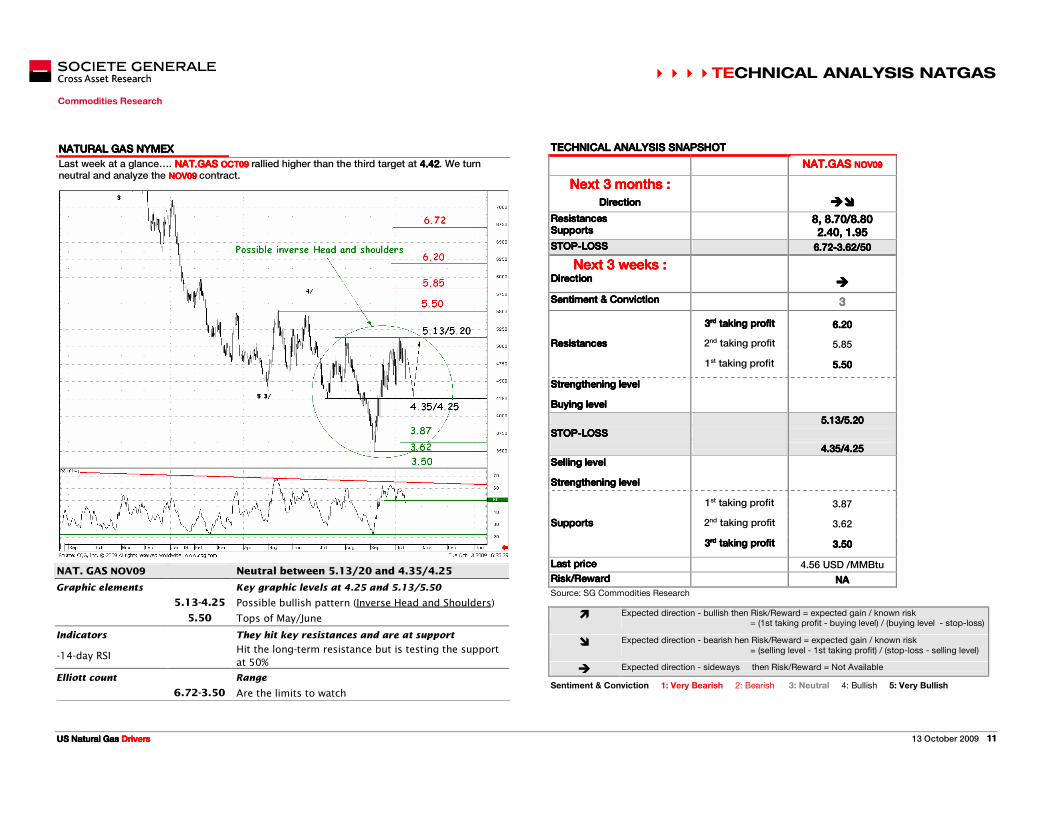

����TECHNICAL ANALYSIS NATGAS

US Natural Gas US Natural Gas US Natural Gas US Natural Gas DriversDriversDriversDrivers 13 October 2009

11111111

chnical Analysis NatGas

NATURAL GAS NYMEXNATURAL GAS NYMEXNATURAL GAS NYMEXNATURAL GAS NYMEX Technical Analysis SnapshotTechnical Analysis SnapshotTechnical Analysis SnapshotTechnical Analysis Snapshot

Last week at a glance…. NAT.GAS NAT.GAS NAT.GAS NAT.GAS OCTOCTOCTOCT09090909 rallied higher than the third target at 4.424.424.424.42. We turn neutral and analyze the NOVNOVNOVNOV09090909 contract.

TECHNICAL ANALYSIS SNAPSHOTTECHNICAL ANALYSIS SNAPSHOTTECHNICAL ANALYSIS SNAPSHOTTECHNICAL ANALYSIS SNAPSHOT

NAT.GAS NAT.GAS NAT.GAS NAT.GAS NOV09NOV09NOV09NOV09

Next 3 months :Next 3 months :Next 3 months :Next 3 months :

DirectionDirectionDirectionDirection ��������

ResistancesResistancesResistancesResistances SupportsSupportsSupportsSupports

8, 8.70/8.808, 8.70/8.808, 8.70/8.808, 8.70/8.80 2.40, 1.952.40, 1.952.40, 1.952.40, 1.95

STOPSTOPSTOPSTOP----LOSSLOSSLOSSLOSS 6.726.726.726.72----3.62/503.62/503.62/503.62/50

Next 3 weeks :Next 3 weeks :Next 3 weeks :Next 3 weeks :

DirectionDirectionDirectionDirection ����

Sentiment & ConvictionSentiment & ConvictionSentiment & ConvictionSentiment & Conviction 3333

3333rdrdrdrd taking profit taking profit taking profit taking profit 6.206.206.206.20

ResistancesResistancesResistancesResistances 2nd taking profit 5.85

1st taking profit 5.505.505.505.50

Strengthening levelStrengthening levelStrengthening levelStrengthening level

Buying levelBuying levelBuying levelBuying level

5.13/5.205.13/5.205.13/5.205.13/5.20

STOPSTOPSTOPSTOP----LOSSLOSSLOSSLOSS

4.35/4.254.35/4.254.35/4.254.35/4.25

Selling levelSelling levelSelling levelSelling level

Strengthening levelStrengthening levelStrengthening levelStrengthening level

1st taking profit 3.87

SupportsSupportsSupportsSupports 2nd taking profit 3.62

3333rdrdrdrd taking profit taking profit taking profit taking profit 3.503.503.503.50

Last priceLast priceLast priceLast price 4.56 USD /MMBtu

Risk/RewardRisk/RewardRisk/RewardRisk/Reward NANANANA

Source: SG Commodities Research

� Expected direction - bullish then Risk/Reward = expected gain / known risk = (1st taking profit - buying level) / (buying level - stop-loss)

� Expected direction - bearish hen Risk/Reward = expected gain / known risk = (selling level - 1st taking profit) / (stop-loss - selling level)

� Expected direction - sideways then Risk/Reward = Not Available

Sentiment & Conviction 1: Very Bearish 2: Bearish 3: Neutral 4: Bullish 5: Very Bullish

NAT. GAS NOV09 Neutral between 5.13/20 and 4.35/4.25

Graphic elements Key graphic levels at 4.25 and 5.13/5.50

5.13-4.25 Possible bullish pattern (Inverse Head and Shoulders)

5.50 Tops of May/June

Indicators They hit key resistances and are at support

-14-day RSI Hit the long-term resistance but is testing the support

at 50%

Elliott count Range

6.72-3.50 Are the limits to watch

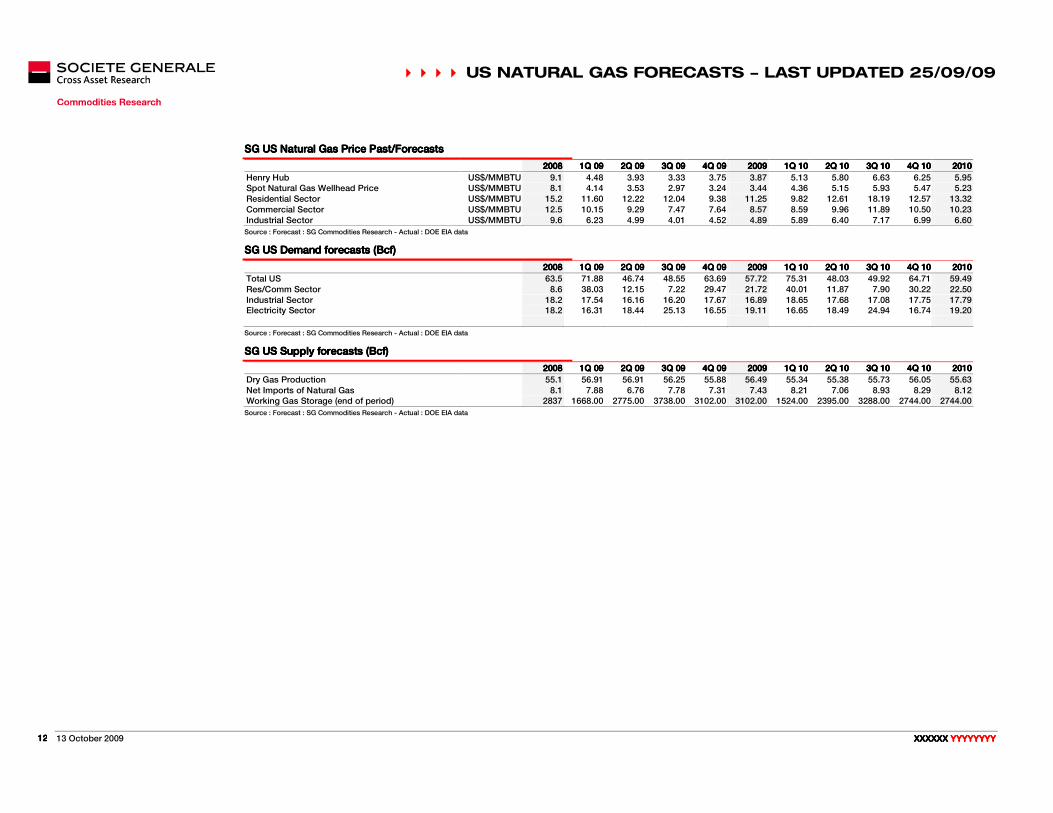

���� US NATURAL GAS FORECASTS - LAST UPDATED 25/09/09

13 October 2009 XXXXXX XXXXXX XXXXXX XXXXXX YYYYYYYYYYYYYYYYYYYYYYYYYYYYYYYY

12121212

US Natur al Gas Forecasts - Last updated 25/09/09

SG US Natural Gas Price Past/ForecastsSG US Natural Gas Price Past/ForecastsSG US Natural Gas Price Past/ForecastsSG US Natural Gas Price Past/Forecasts

2008200820082008 1Q 091Q 091Q 091Q 09 2Q 092Q 092Q 092Q 09 3Q 093Q 093Q 093Q 09 4Q 094Q 094Q 094Q 09 2009200920092009 1Q 101Q 101Q 101Q 10 2Q 102Q 102Q 102Q 10 3Q 103Q 103Q 103Q 10 4Q 104Q 104Q 104Q 10 2010201020102010

Henry Hub US$/MMBTU 9.1 4.48 3.93 3.33 3.75 3.87 5.13 5.80 6.63 6.25 5.95 Spot Natural Gas Wellhead Price US$/MMBTU 8.1 4.14 3.53 2.97 3.24 3.44 4.36 5.15 5.93 5.47 5.23 Residential Sector US$/MMBTU 15.2 11.60 12.22 12.04 9.38 11.25 9.82 12.61 18.19 12.57 13.32 Commercial Sector US$/MMBTU 12.5 10.15 9.29 7.47 7.64 8.57 8.59 9.96 11.89 10.50 10.23 Industrial Sector US$/MMBTU 9.6 6.23 4.99 4.01 4.52 4.89 5.89 6.40 7.17 6.99 6.60

Source : Forecast : SG Commodities Research - Actual : DOE EIA data

SSSSG US Demand forecasts (Bcf)G US Demand forecasts (Bcf)G US Demand forecasts (Bcf)G US Demand forecasts (Bcf)

2008200820082008 1Q 091Q 091Q 091Q 09 2Q 092Q 092Q 092Q 09 3Q 093Q 093Q 093Q 09 4Q 094Q 094Q 094Q 09 2009200920092009 1Q 101Q 101Q 101Q 10 2Q 102Q 102Q 102Q 10 3Q 103Q 103Q 103Q 10 4Q 104Q 104Q 104Q 10 2010201020102010

Total US 63.5 71.88 46.74 48.55 63.69 57.72 75.31 48.03 49.92 64.71 59.49 Res/Comm Sector 8.6 38.03 12.15 7.22 29.47 21.72 40.01 11.87 7.90 30.22 22.50 Industrial Sector 18.2 17.54 16.16 16.20 17.67 16.89 18.65 17.68 17.08 17.75 17.79 Electricity Sector 18.2 16.31 18.44 25.13 16.55 19.11 16.65 18.49 24.94 16.74 19.20

Source : Forecast : SG Commodities Research - Actual : DOE EIA data

SG US SuSG US SuSG US SuSG US Supply forecasts (Bcf)pply forecasts (Bcf)pply forecasts (Bcf)pply forecasts (Bcf)

2008200820082008 1Q 091Q 091Q 091Q 09 2Q 092Q 092Q 092Q 09 3Q 093Q 093Q 093Q 09 4Q 094Q 094Q 094Q 09 2009200920092009 1Q 101Q 101Q 101Q 10 2Q 102Q 102Q 102Q 10 3Q 103Q 103Q 103Q 10 4Q 104Q 104Q 104Q 10 2010201020102010

Dry Gas Production 55.1 56.91 56.91 56.25 55.88 56.49 55.34 55.38 55.73 56.05 55.63 Net Imports of Natural Gas 8.1 7.88 6.76 7.78 7.31 7.43 8.21 7.06 8.93 8.29 8.12 Working Gas Storage (end of period) 2837 1668.00 2775.00 3738.00 3102.00 3102.00 1524.00 2395.00 3288.00 2744.00 2744.00

Source : Forecast : SG Commodities Research - Actual : DOE EIA data

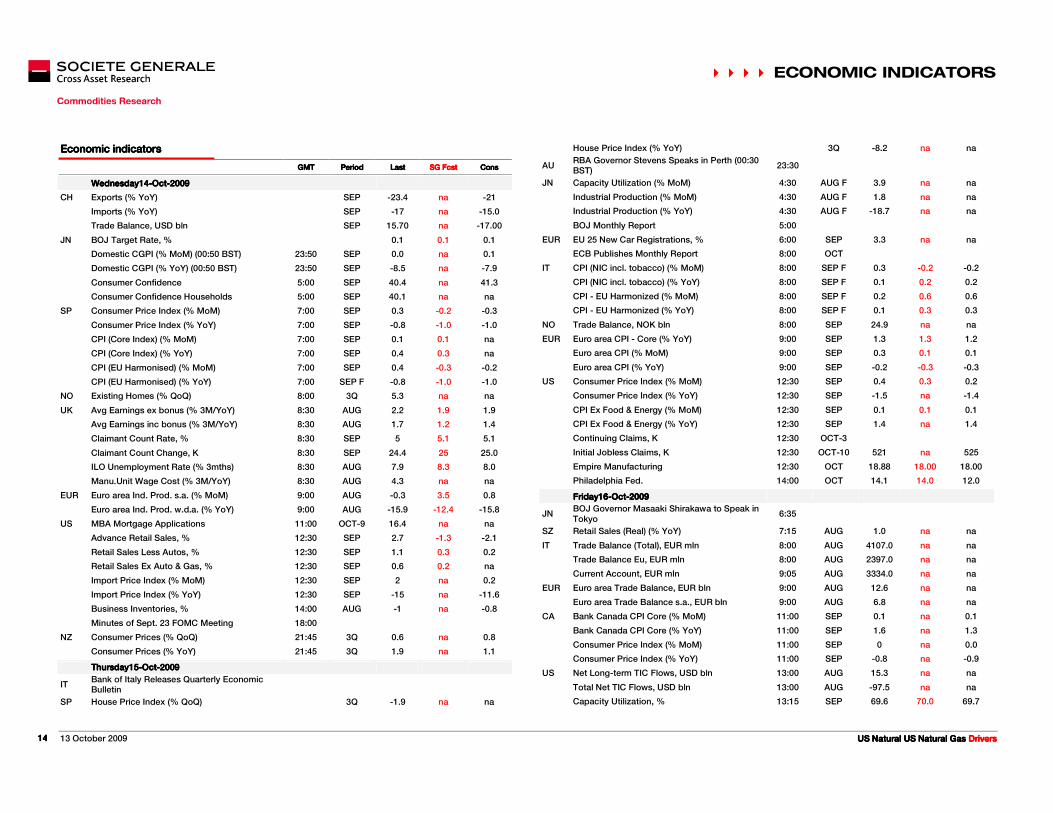

���� ECONOMIC INDICATORS

US Natural Gas US Natural Gas US Natural Gas US Natural Gas DriversDriversDriversDrivers 13 October 2009

13131313

Economic Indi cators

Economic indicatorsEconomic indicatorsEconomic indicatorsEconomic indicators

GMTGMTGMTGMT PeriodPeriodPeriodPeriod LastLastLastLast SG SG SG SG FcstFcstFcstFcst ConsConsConsCons

During the weekDuring the weekDuring the weekDuring the week

CH Actual FDI YTD (% YoY) SEP -17.5 na na

Foreign Exchange Reserves, USD SEP 2131.61 na na

Money Supply - M2 (% YoY) SEP 28.5 na 28.4

New Yuan Loans, bln SEP 410.4 na 420.0

JN BOJ to Hold Regular Policy Board Meeting

Monday12Monday12Monday12Monday12----OctOctOctOct----2009200920092009

IN Industrial Production (% YoY) AUG 6.8 na 9.7

SW AMV Unemployment Rate, % 8:00 SEP 5.4 na 5.4

US Treasury's Krueger Speaks to Economists in St. Louis

17:00

NZ Retail Sales (% MoM) 21:45 AUG -0.5 na 0.5

Retail Sales Ex-Auto (% MoM) 21:45 AUG -0.5 na 0.5

Tuesday13Tuesday13Tuesday13Tuesday13----OctOctOctOct----2009200920092009

CH Business Climate Index 3Q 115.9 na na

Entrepreneur Confidence Index 3Q 110.2 na na

UK BRC Retail Sales Monitor (00:01 BST) 23:01 SEP

RICS House Price Balance, % (00:01 BST) 23:01 SEP 10.7 na 15.0

JN Bank Lending (% YoY) (00:50 BST) 23:50 SEP 1.8 na 1.7

Bank Lending Banks (% YoY) (00:50 BST) 23:50 SEP 1.9 na

Money Stock M2 (% YoY) (00:50 BST) 23:50 SEP 2.8 na 2.9

BoJ Monetary Policy Meeting 4:00

FR Consumer Price Index (% MoM) 6:45 SEP 0.5 -0.1 -0.1

Consumer Price Index (% YoY) 6:45 SEP -0.2 -0.2 -0.2

CPI - EU Harmonised (% MoM) 6:45 SEP 0.6 0.0 0.0

CPI - EU Harmonised (% YoY) 6:45 SEP -0.2 -0.2 -0.3

CPI Ex Tobacco Index 6:45 SEP 118.41 118.35 na

Current Account, EUR bln 6:45 AUG -1.2 na na

SP House transactions (% YoY) 7:00 AUG -20.3 na na

SW CPI - Headline Rate (% MoM) 7:30 SEP 0.2 na 0.4

CPI - Headline Rate (% YoY) 7:30 SEP -0.8 na -1.4

UK Core CPI (% YoY) 8:30 SEP 1.8 na 1.7

CPI (% MoM) 8:30 SEP 0.4 0.1 0.2

CPI (% YoY) 8:30 SEP 1.6 1.1 1.3

DCLG House Prices (% YoY) 8:30 AUG -8.3 na na

RPI (% YoY) 8:30 SEP -1.3 na -1.5

RPI Ex Mort Int.Payments (% YoY) 8:30 SEP 1.4 na 1.2

GE Zew Survey (Current Situation) 9:00 OCT -74 -68 -68.3

Zew Survey (Econ. Sentiment) 9:00 OCT 57.7 50 59.0

US White House's Romer Speaks to Economists in St. Louis

12:30

Fed's Kohn Speaks to Economists in St. Louis 17:00

New York Fed's Dudley Speaks to International Bankers in NYC

17:15

ABC Consumer Confidence 21:00 OCT-11 -45.0 na na

���� ECONOMIC INDICATORS

13 October 2009 US Natural US Natural Gas US Natural US Natural Gas US Natural US Natural Gas US Natural US Natural Gas DriversDriversDriversDrivers

14141414

Economic indicatorsEconomic indicatorsEconomic indicatorsEconomic indicators

GMTGMTGMTGMT PeriodPeriodPeriodPeriod LastLastLastLast SG FcstSG FcstSG FcstSG Fcst ConsConsConsCons

Wednesday14Wednesday14Wednesday14Wednesday14----OctOctOctOct----2009200920092009

CH Exports (% YoY) SEP -23.4 na -21

Imports (% YoY) SEP -17 na -15.0

Trade Balance, USD bln SEP 15.70 na -17.00

JN BOJ Target Rate, % 0.1 0.1 0.1

Domestic CGPI (% MoM) (00:50 BST) 23:50 SEP 0.0 na 0.1

Domestic CGPI (% YoY) (00:50 BST) 23:50 SEP -8.5 na -7.9

Consumer Confidence 5:00 SEP 40.4 na 41.3

Consumer Confidence Households 5:00 SEP 40.1 na na

SP Consumer Price Index (% MoM) 7:00 SEP 0.3 -0.2 -0.3

Consumer Price Index (% YoY) 7:00 SEP -0.8 -1.0 -1.0

CPI (Core Index) (% MoM) 7:00 SEP 0.1 0.1 na

CPI (Core Index) (% YoY) 7:00 SEP 0.4 0.3 na

CPI (EU Harmonised) (% MoM) 7:00 SEP 0.4 -0.3 -0.2

CPI (EU Harmonised) (% YoY) 7:00 SEP F -0.8 -1.0 -1.0

NO Existing Homes (% QoQ) 8:00 3Q 5.3 na na

UK Avg Earnings ex bonus (% 3M/YoY) 8:30 AUG 2.2 1.9 1.9

Avg Earnings inc bonus (% 3M/YoY) 8:30 AUG 1.7 1.2 1.4

Claimant Count Rate, % 8:30 SEP 5 5.1 5.1

Claimant Count Change, K 8:30 SEP 24.4 25 25.0

ILO Unemployment Rate (% 3mths) 8:30 AUG 7.9 8.3 8.0

Manu.Unit Wage Cost (% 3M/YoY) 8:30 AUG 4.3 na na

EUR Euro area Ind. Prod. s.a. (% MoM) 9:00 AUG -0.3 3.5 0.8

Euro area Ind. Prod. w.d.a. (% YoY) 9:00 AUG -15.9 -12.4 -15.8

US MBA Mortgage Applications 11:00 OCT-9 16.4 na na

Advance Retail Sales, % 12:30 SEP 2.7 -1.3 -2.1

Retail Sales Less Autos, % 12:30 SEP 1.1 0.3 0.2

Retail Sales Ex Auto & Gas, % 12:30 SEP 0.6 0.2 na

Import Price Index (% MoM) 12:30 SEP 2 na 0.2

Import Price Index (% YoY) 12:30 SEP -15 na -11.6

Business Inventories, % 14:00 AUG -1 na -0.8

Minutes of Sept. 23 FOMC Meeting 18:00

NZ Consumer Prices (% QoQ) 21:45 3Q 0.6 na 0.8

Consumer Prices (% YoY) 21:45 3Q 1.9 na 1.1

ThursdayThursdayThursdayThursday15151515----OctOctOctOct----2009200920092009

IT Bank of Italy Releases Quarterly Economic Bulletin

SP House Price Index (% QoQ) 3Q -1.9 na na

House Price Index (% YoY) 3Q -8.2 na na

AU RBA Governor Stevens Speaks in Perth (00:30 BST)

23:30

JN Capacity Utilization (% MoM) 4:30 AUG F 3.9 na na

Industrial Production (% MoM) 4:30 AUG F 1.8 na na

Industrial Production (% YoY) 4:30 AUG F -18.7 na na

BOJ Monthly Report 5:00

EUR EU 25 New Car Registrations, % 6:00 SEP 3.3 na na

ECB Publishes Monthly Report 8:00 OCT

IT CPI (NIC incl. tobacco) (% MoM) 8:00 SEP F 0.3 -0.2 -0.2

CPI (NIC incl. tobacco) (% YoY) 8:00 SEP F 0.1 0.2 0.2

CPI - EU Harmonized (% MoM) 8:00 SEP F 0.2 0.6 0.6

CPI - EU Harmonized (% YoY) 8:00 SEP F 0.1 0.3 0.3

NO Trade Balance, NOK bln 8:00 SEP 24.9 na na

EUR Euro area CPI - Core (% YoY) 9:00 SEP 1.3 1.3 1.2

Euro area CPI (% MoM) 9:00 SEP 0.3 0.1 0.1

Euro area CPI (% YoY) 9:00 SEP -0.2 -0.3 -0.3

US Consumer Price Index (% MoM) 12:30 SEP 0.4 0.3 0.2

Consumer Price Index (% YoY) 12:30 SEP -1.5 na -1.4

CPI Ex Food & Energy (% MoM) 12:30 SEP 0.1 0.1 0.1

CPI Ex Food & Energy (% YoY) 12:30 SEP 1.4 na 1.4

Continuing Claims, K 12:30 OCT-3

Initial Jobless Claims, K 12:30 OCT-10 521 na 525

Empire Manufacturing 12:30 OCT 18.88 18.00 18.00

Philadelphia Fed. 14:00 OCT 14.1 14.0 12.0

Friday16Friday16Friday16Friday16----OctOctOctOct----2009200920092009

JN BOJ Governor Masaaki Shirakawa to Speak in Tokyo

6:35

SZ Retail Sales (Real) (% YoY) 7:15 AUG 1.0 na na

IT Trade Balance (Total), EUR mln 8:00 AUG 4107.0 na na

Trade Balance Eu, EUR mln 8:00 AUG 2397.0 na na

Current Account, EUR mln 9:05 AUG 3334.0 na na

EUR Euro area Trade Balance, EUR bln 9:00 AUG 12.6 na na

Euro area Trade Balance s.a., EUR bln 9:00 AUG 6.8 na na

CA Bank Canada CPI Core (% MoM) 11:00 SEP 0.1 na 0.1

Bank Canada CPI Core (% YoY) 11:00 SEP 1.6 na 1.3

Consumer Price Index (% MoM) 11:00 SEP 0 na 0.0

Consumer Price Index (% YoY) 11:00 SEP -0.8 na -0.9

US Net Long-term TIC Flows, USD bln 13:00 AUG 15.3 na na

Total Net TIC Flows, USD bln 13:00 AUG -97.5 na na

Capacity Utilization, % 13:15 SEP 69.6 70.0 69.7

���� ECONOMIC INDICATORS

US Natural Gas US Natural Gas US Natural Gas US Natural Gas DriversDriversDriversDrivers 13 October 2009

15151515

Industrial Production, % 13:15 SEP 0.8 0.3 0.1

U. of Michigan Confidence 14:00 OCT P 73.5 75.0 73.5

���� TRADING CONTACTS

13 October 2009 US Natural Gas US Natural Gas US Natural Gas US Natural Gas DriversDriversDriversDrivers

16161616

Trading Contacts

COMMODITIESCOMMODITIESCOMMODITIESCOMMODITIES RESEARCH RESEARCH RESEARCH RESEARCH COMMODITY MARKETINGCOMMODITY MARKETINGCOMMODITY MARKETINGCOMMODITY MARKETING

HeaHeaHeaHeadddd HeadHeadHeadHead

Dr. Frederic LasserreDr. Frederic LasserreDr. Frederic LasserreDr. Frederic Lasserre (33) 1 42 13 44 06 Xavier LannegraceXavier LannegraceXavier LannegraceXavier Lannegrace (33) 1 42 13 88 10 ParisParisParisParis ParisParisParisParis HoustonHoustonHoustonHouston Carbon & Coal Energy Energy

Dr. Emmanuel Fages (33) 1 42 13 30 29 [email protected] (33) 1 42 13 90 35 [email protected] (1) 713 759 63 60 Oil & Products / Cross Commodity Strategy Metals, Steel CalgaryCalgaryCalgaryCalgary

Remy Penin (33) 1 42 13 55 74 [email protected] (33) 1 42 13 88 10 [email protected] Energy

Agricultural Commodities [email protected] (1) 403 698 89 10 Emmanuel Jayet (33) 1 42 13 57 03 Investors [email protected] (33) 1 42 13 69 59 HongHongHongHong----KongKongKongKong Energy Special Advisor

Sadek Boussena (33) 1 42 14 59 11 LondonLondonLondonLondon Energy, Metals, Steel [email protected] (852) 2166 5515 LondonLondonLondonLondon Energy, Plastics

[email protected] (44) 207 867 87 21 Cross Commodity Technical Analysis

Stephanie Aymes (44) 207 762 58 98 Plastics & Steel Specialist Sebastian Castelli (44) 207 762 52 75 Oil & Products

Michael Wittner (44) 207 762 57 25 Metals [email protected] (44) 207 867 87 21 Cross Commodity Strategy

Jesper Dannesboe (44) 207 762 56 03 New YorkNew YorkNew YorkNew York Metals Energy

David Wilson (44) 207 762 53 84 [email protected] (1) 212 278 56 08 New YorkNew YorkNew YorkNew York Base Metals, Steel [email protected] (1) 212 278 56 61 US Natural Gas

Laurent Key (1) 212 278 57 36 Precious Metals [email protected] (1) 212 278 56 61 Société GénéraleSociété GénéraleSociété GénéraleSociété Générale Corporate & Investment BankingCorporate & Investment BankingCorporate & Investment BankingCorporate & Investment Banking Plastics Tours Société Générale

[email protected] (1) 212 278 56 08 17, cours Valmy 92972 Paris - La Défense Cedex Email:Email:Email:Email: Please click on the analyst name Investors France

([email protected]) [email protected] (1) 212 278 62 55 www.commodities.sgcib.comwww.commodities.sgcib.comwww.commodities.sgcib.comwww.commodities.sgcib.com

���� DISCLAIMER

US Natural Gas US Natural Gas US Natural Gas US Natural Gas DriversDriversDriversDrivers 13 October 2009

17171717

The information herein is not intended to be an offer to buy or sell, or a solicitation of an offer to buy or sell, any securities and including any expression of opinion, has been obtained from or is based upon sources believed to be reliable but is not guaranteed as to accuracy or completeness although Société Générale (�SG�) believe it to be fair and not misleading or deceptive. SG, and their affiliated companies in the SG Group, may from time to time deal in, profit from the trading of, hold or act as market-makers or act as advisers, brokers or bankers in relation to the securities, or derivatives thereof, of persons, firms or entities mentioned in this document or be represented on the board of such persons, firms or entities. Employees of SG, and their affiliated companies in the SG Group, or individuals connected to them may from time to time have a position in or be holding any of the investments or related investments mentioned in this document. SG and their affiliated companies in the SG Group are under no obligation to disclose or take account of this document when advising or dealing with or for their customers. The views of SG reflected in this document may change without notice. To the maximum extent possible at law, SG does not accept any liability whatsoever arising from the use of the material or information contained herein. Dealing in warrants and/or

derivative products such as futures, options, and contracts for differences has specific risks and other significant aspects. You should not deal in these products unless you understand their nature and the extent of your exposure to risk. This research document

is not intended for use by or targeted at retail customers. Should a retail customer obtain a copy of this report they should not base their investment decisions solely on the basis of this document but must seek independent financial advice. Important Notice: The circumstances in which this publication has been produced are such (for example because of reporting or remuneration structures or the physical location of the author of the material), that it is not appropriate to characterise it as independent investment

research as referred to in European MIF directive and that it should be treated as a marketing material even if it contains a research recommendation (« recommandation d�investissement à caractère promotionnel »). This publication is also not subject to any prohibition on

dealing ahead of the dissemination of investment research. However, it must be made clear that all publications issued by SG will be clear, fair, and not misleading. Analyst Certification: Each author of this research report hereby certifies that the views expressed in the research report accurately reflect his or her personal views about any and all of the subject securities or issuers.

Notice to French Investors: This publication is issued in France by or through Société Générale ("SG") which is authorised by the CECEI and regulated by the AMF (Autorité des Marchés Financiers). Notice to UK Investors: This publication is issued in the United Kingdom by or through Société Générale ("SG") London Branch which is regulated by the Financial Services Authority ("FSA") for the conduct of its UK business.

Notice to US Investors: This report is issued solely to major US institutional investors pursuant to SEC Rule 15a-6. Any US person wishing to discuss this report or effect transactions in any security discussed herein should do so with or through SG Americas Securities, LLC to

conform with the requirements of US securities law. SG Americas Securities, LLC, 1221 Avenue of the Americas, New York, NY, 10020. (212) 278-6000. Some of the securities mentioned herein may not be qualified for sale under the securities laws of certain states, except for unsolicited orders. Customer purchase orders made on the basis of this report cannot be considered to be unsolicited by SG Americas Securities, LLC and therefore may not be accepted by SG Americas Securities, LLC investment executives unless the security is qualified for sale in the state. Notice to Japanese Investors: This report is distributed in Japan by Société Générale Securities (North Pacific) Ltd., Tokyo Branch, which is regulated by the Financial Services Agency of Japan. The products mentioned in this report may not be eligible for sale in Japan and

they may not be suitable for all types of investors. Notice to Australian Investors: Société Générale Australia Branch (ABN 71 092 516 286) (SG) takes responsibility for publishing this document. SG holds an AFSL no. 236651 issued under the Corporations Act 2001 (Cth) ("Act"). The information contained in this newsletter is

only directed to recipients who are aware they are wholesale clients as defined under the Act. http://www.sgcib.com. Copyright: The Société Générale Group 2009. All rights reserved.