Embed Size (px)

Citation preview

2005-TIOL-103-ITAT-DEL-SB

IN THE INCOME TAX APPELLATE TRIBUNAL

DELHI BENCH 'A' (SPECIAL BENCH)

I.T.A. NO. 2455/DEL/01 AND I.T.A. NO. 2516/DEL/01

(Assessment Year: 1997-98)

MOTOROLA INC

C/o M/s BHARAT S. RAUT & CO

511, WORLD TRADE CENTRE, BABAR RD., NEW DELHI

Vs

DEPUTY CIT, NON-RESIDENT CIRCLE

NEW DELHI

(and vice-versa)

2. I.T.A. NO 815/DEL/01 AND I.T.A. NO. 1798/DEL/01

(Assessment Year: 1997-98)

ERICSSON RADIO SYSTEMS A.B.

C/o R.S.M. & CO.

516-517, WORLD TRADE CENTRE,

BARAKHAMAB LANE, NEW DELHI-110001

Vs

DEPUTY C.I.T, NON-RESIDENT CIRCLE

NEW DELHI

(and Vice-versa)

Page 1 of 201

C.O. NO. 60/DEL/2001

(Assessment Year: 1997-98)

ERICSSON RADIO SYSTEMS A.B.

C/o R.S.M. & CO.,

516-517, WORLD TRADE CENTRE,

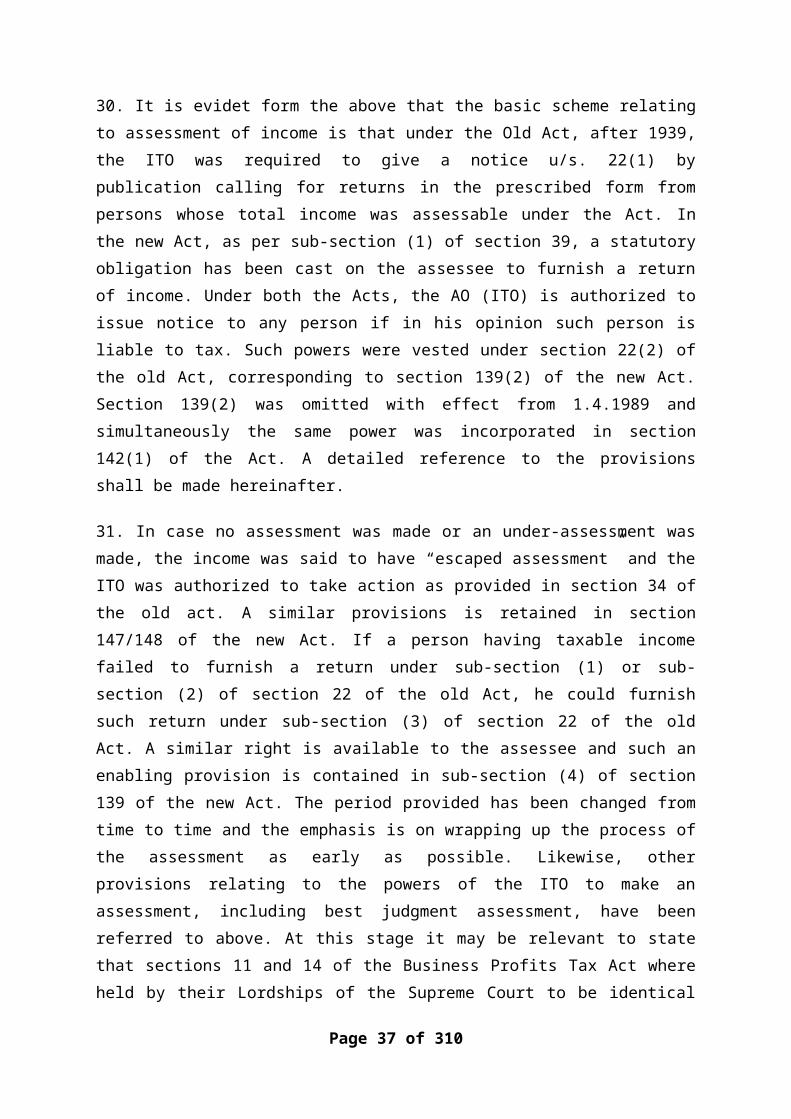

BARAKHAMBA LANE, NEW DELHI-110001

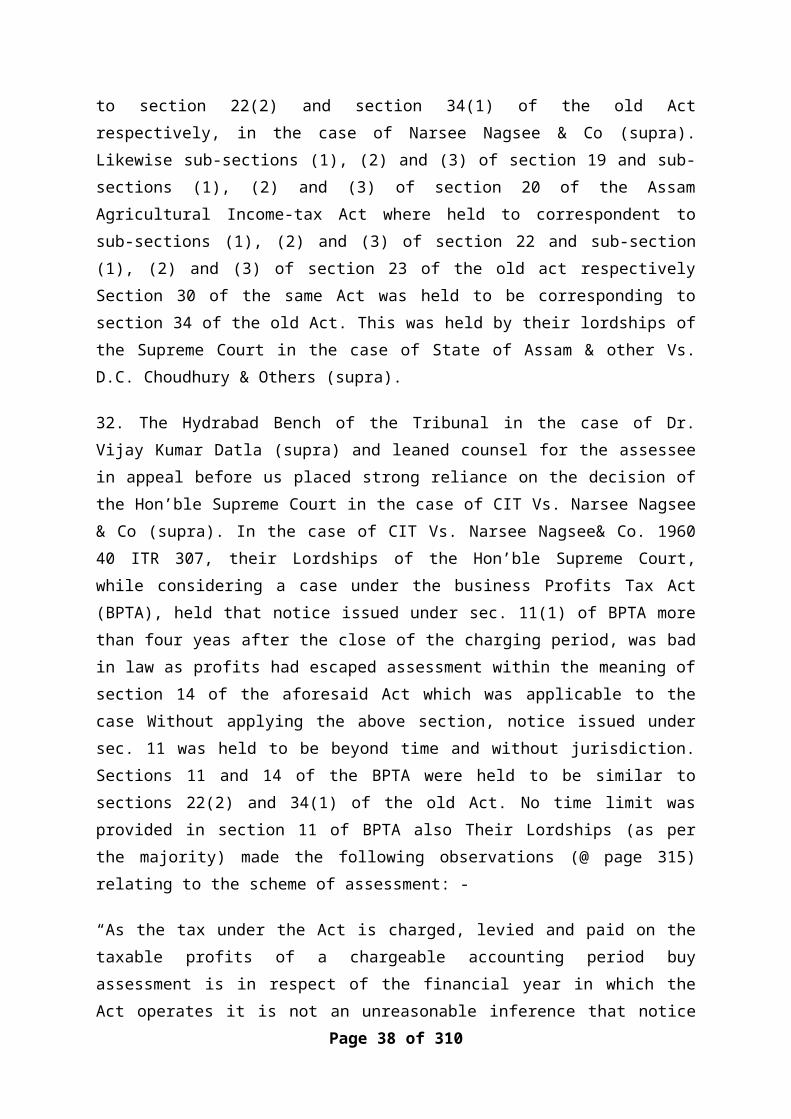

Vs

DEPUTY CIT NON-RESIDENT CIRCLE

NEW DELHI

(Cross Objector)

3. I.T.A. NOS. 1963 & 1964/DEL/01

(Assessment Year: 1997-98 & 1998-99)

NOKIA NETWORKS, OY.KEILALAHDENTIE-4

BOX 300, FIN - 00045

NOKIA GROUP, FINLAND

Vs

DEPUTY C.I.T, NON-RESIDENT CIRCLE

4. I.T.A. NO. 2510 & 2511/DEL/01

(Assessment Year: 1997-98 and 1998-99)

DEPUTY C.I.T.

NON-RESIDENT CIRCLE,

NEW DELHI

Page 2 of 201

Vs

NOKIA NETWORKS OY, (FORMERLY NOKIA TELE

COMMUNICATIONS OY), KEILALAHDENTIE 4,

FIN-02125, ESPOO, BOX 300

FINLAND - 0045

Before Shri Vimal Gandhi, Hon'ble President, Shri R V Easwar, Vice President

and Shri Pradeep Parikh, Accountant Member

Dated: June 22, 2005

Assessees by:

1. Motorola Inc., and Nokia Networks OY: Shri M.S. syali, Sr. Adv, Shri Faroukh Irani, Adv.

(Shri Satyen Sethi, Shri Manu K. Giri, Shri Satish Khosla, Adv and Shri Sanjay Chaudhary, C.A., with them)

2. Ericsson Radio Systems A.B. Shri Sohrab E. Dastur, Sr. Adv and Shri P.J. Pardiwala, Adv. with him.

Department by:

Shri G.C. Sharma, Sr. Adv, (Special Counsel for the Department)

(Shri Anoop Sharma, Shri R.K. Raghvan and Shri T.R. Talwar, Add and Shri Salil Gupta, Sr. D.R., with him)

ORDER

PER BENCH:

All these cross-appeals and cross-objections in respect of the three assessees are directed against the orders of the learned CIT(A) in the respective case. Since common issues are involved in all these appeals, they were heard together and are being disposed of by this consolidated order, for the sake of convenience.

Page 3 of 201

1.1 These matters were fixed before the Division Benches but at the instance of the assessees and in the light of the importance of the issues involved, a request was made to the Hon’ble President to refer the matter to a Special Bench u/s. 255(4) of the Income Tax Act, 1961 (the Act). The President, ITAT after considering the facts and circumstances of the case decided to constitute a Special Bench. The following question was referred to the Special Bench:

“Whether, on the facts and in the circumstances, the revenues earned by the appellant from supply of equipment and software to Indian Telecom Operators were taxable in India?”

2. It may be relevant to mention that the revenue had earlier opposed the constitution of a Special Bench. The Revenue further opposed joining of Ericsson and Nokia as parties before the Special Bench. However, subsequently the learned counsel appearing for the revenue Shri G.C. Sharma, Sr. Advocate agreed that a Special Bench may be constituted and the above mentioned two assessees may also join as parties.

3. Before the hearing started on 19th July, 2004, Mr. M.S. Syali, the learned counsel for Motorola, referred to the assessee’s application dated “Nil” (received in the office of the Tribunal on 26.5.2004) and requested the Bench that he be permitted to argue on the validity of the notice issued u/s. 142(1) of the Act as entire appeals were to be heard by the Bench as per directions dated 19.1.2004. Shri G.C. Sharma, Learned counsel, appearing for the revenue, opposed the above request. It was argued by Shri Sharma that only a specified question has been referred to and is to be considered by the Special Bench. After hearing all the concerned parties at length, the Bench, vide its order dated 20th July, 2004 directed that the entire appeals in all the three cases will be head by the Special Bench.

4. Two Major issues which arise in the appeals are:

(a) The validity of the notice issued under section 142(1) of the Act, and

(b) The validity of the levy of interest under sections 234A and 234B of the Act.

The first issue arises only in the cases of Motorola and Ericsson, whereas the second issue arises in all the three cases namely Motorola, Ericsson and Nokia. We propose to decide these two issues first and thereafter decide the various grounds assessee-wise.

Page 4 of 201

Validity of notice under section 142(1) (Motorola & Ericsson).

5. The first ground in the case of Motorola is against the validity of the notice issued u/s. 142(1) of the Act. The said notice was issued on 3rd of November, 1999 and was served thereafter. The learned counsel for the assessee submitted that the said notice should have been issued and served within one year from the end of the previous year. The notice issued and served after the above date was barred by limitation and hence the assessment was vitiated.

5.1 Shri Syali referred to the provisions of sub-sections (2) and (4) of sec. 139. He contended that before 1.4.1989 sub-section (2) of sec. 139 prescribed that the notice thereunder should be served before the end of the assessment year. After 1.4.1989. section 142(1) was amended to provide for issue of notice calling for the return of income. According to Mr. Syali this was a case of substitution of the earlier section 139(2) and though section 142(1) did not specify any time limit within which the notice should be issued, his contention was that such a limitation was built in and should be inferred having regard to the scheme of the statute. Mr. Syali pointed out that section 142(1) provided for two situations namely:

(a) Where a return was filed u/s. 139(1) in which case the notice u/s. 142(1) could call for further information and particulars, and

(b) Where time allowed u/s. 139(1) had expired and no return was filed by the asessee, the notice u/s. 142(1) could call for a return to be filed by the assessee.

6. Shri M.S. Syali then referred to the decision of the Hydrabad Bench of the Tribunal in the case of Dr. Vijaykumar Datla Vs. Astt. CIT 58 ITD 339 and of the Delhi Bench in the case of Sheraton International Inc. Vs. Dy. CIT 85 ITD 110. Shri Syali pointed out that the Hyderabad Bench while deciding the matter had taken all the relevant provisions of the law into consideration. The decision of the Delhi Bench of the Tribunal, on the other hand, was per incuriam as the decision of the Hon’ble Supreme Court and the relevant statutory provisions were not discussed. Shri Syali at the same time added that both the Benches agree that some period of limitation has to be read in the statutory provisions and it is not possible to hold that the notice u/s. 142(1) could be issued at any time. Shri Syali referred to the decision in the case of Iswara Bhat Vs. Commissioner of Agricultural Income tax 200 ITR 238 (Ker.) to contended that even in the absence of a time limit prescribed by law, any proceedings have to be initiated and computed within a reasonable time. Where no time limit is prescribed for the completion of the proceedings, the logic that the

Page 5 of 201

repository of the power shall initiate the proceeding within a reasonable time should apply an the final order should be passed within a reasonable time, even in the absence of a time limit in the statute concerned. The Kerala High Court held that both initiation and completion of the proceedings stand on the same footing.

6.1. Mr. M.S. Syali referred to Explanation 2(a) to section 147 of the Act which deems certain cases to be cases of escaped assessment. Under this provisions, a case where no return of income has been furnished by the assessee although the total income or the total income of any other person in respect of which he is assessable under the Act exceeded the maximum about not chargeable to income-tax would also be deemed to be a case of escaped assessment. From this provisions, the learned counsel sought to contend that there is a point at which the income escaping assessment is fixed, and any notice u/s. 142(1) could be given only before that point is reached. In the case of escaped assessment, the only remedy with the revenue is to issue notice u/s. 148 treating it as a case of escaped assessment. The present case, according to him can at best be considered as escaped assessment for which no notice u/s. 142(1) could be issued. In such a case, a notice u/s. 148 should have been issued which not having been issued, the assessment is without jurisdiction.

6.2 Shri Syali then pointed out with reference to the impugned order of the CIT (Appeals) and argued that four reasons were given not to accept the decision in the case of Dr. Vijaykumar Datla (supra):

(1) The decision in the case of Dr. Vijaykumar Datla (supra) ignores the provisions of Section 139(2),

(2) The judgment of the Hon’ble Supreme Court in the case of CIT Vs. Narsee Nagsee & Co. (40 ITR 307) was not rendered under the provisions of the Income-tax Act but was rendered under the Business Profits Tax Act, 1947 under which the provisions were materially different.

(3) The order of the Hyderabad Bench in the case of Dr. Vijaykumar Datla (supra) is not a decision of the jurisdictional Bench of the tribunal and hence not binding; and

Page 6 of 201

(4) The Assessing Officer has concurrent jurisdiction over the assessee in the sense that he can issued notice u/s. 142(1) or a notice u/s 148 and if the exercises one of these two options, there is not illegality about the same.

7. Criticising the approach of the CIT(A) as above, Mr. Syali submitted that in the case of Dr. Vijaykumar Datla (supra), the Hyderabad Bench did consider section 139(2) and that too in extenso and he drew out attention to the relevant parts of the order. Secondly, he submitted that the judgement of the Hon’ble Supreme Court in the case of Narsee Nagsee & Co. (supra) clearly notes that the provisions of the Business Profits Tax Act which were before them are in pari material with the provisions of the Indian Income-tax Act, 1922. Thirdly, it was submitted that it was irrelevant that Dr. Vijaykumar Datla (supra) was an order by the Hyderabad Bench which was not the jurisdictional Bench in so far as the present case is concerned, because there is no judgment of any High Court taking a view contrary to the view taken by the Hyderabad Bench in Dr. Vijaykumar Datla’s case. Lastly, Mr. Syali contended that the theory of concurrent jurisdiction was rejected by the Hon’ble Supreme Court in the case of Narsee Nagsee & Co. (supra) and further he added that the rule is that jurisdiction has to be expressly conferred and no inference of concurrent jurisdiction can be drawn.

8. Mr. Syali then referred to the order of the Delhi Bench in the case of Sheraton International Inc. (supra) and submitted for our consideration the following points. According to him Sheraton International Inc. (supra) proceeded entirely on the basis of first principles without referred to the law laid down by the courts including the judgement of the Hon’ble Supreme Court in the case of Narsee Nagsee & Co. (supra). Therefore, the order is per incuriam. He also invited our attention to paragraph 16 of Sheraton’s order and pointed out what according to him were certain incorrect observations made by the Delhi Bench vis-à-vis Dr. Vijaykumar Datla’s case. On merits, Mr. Syali submitted that the interpretation of the expression “for the purpose of making an assessment” appearing in section 142(1), on which strong reliance had been placed by the Delhi Bench in Sheraton International Inc. (supra) case, would equally apply to a case of re-assessment since by definition in section 2(8), an assessment includes a re-assessment. He further pointed out that section 142(1) refers to section 139 at two places. In the first place where the section is referred, no sub-section is specified. In clause (i) of sub-section (1) where there is again a reference to section 139, the reference is specifically to sub-section (1) of section 139. This distinction, according to the learned counsel, is very important for this reason namely; that simply because the assessee has not filed a return, the department is not powerless because notice u/s. 142(1) vis-à-vis production of accounts can be issued after issue of notice u/s. 148 also. It was in this context that he dissected the provisions of section 142(1) into two limbs as mentioned earlier.

Page 7 of 201

9. Shri M.S. Syali also drew out attention to the decision of the Hon’ble Calcutta High Court in the case of CIT Vs. Sultan Ali Gharami 20 IT 432 to contend that merely because the assessee can file a return u/s. 139(4) of the Act, it does not mean that the notice u/s. 142(1) can be issued after the end of the assessment year. Under such circumstances, a notice u/s. 148 was necessary. The learned counsel sought to drew parity between the provisions of sections 142(1) and 143(2) to contend that just as the Assessing Officer. (AO) cannot make an assessment u/s. 143(3) after the expiry of 12 months, similarly no notice could be issued u/s 142(1) after the end of the assessment year. After the end of the assessment year, only notice u/s. 148 could be issued as by that time it becomes a case of escaped assessment. The decision in the case of Sharaton International (supra) overlooked the two limbs of section 142(1) namely: (a) calling for the return and (b) calling for the details. It was submitted that these were two different powers with different attributes governing different situations. It was submitted that in principle, a notice under the section has to be issued during the assessment year which position has been confirmed by the court. Later on limb (a) was incorporated in section 139(2) which now stands substituted by the provisions of section 142(1) and hence the question arises as to why the earlier position cannot be implied into the new provisions.

9.1 On the basis of certain observations of the Calcutta High Court in Sultan Ali Gharami’s case (supra), Mr. Syali contended that on the expiry of the assessment year, which in the case of Motorola was on 31.3.1998, the assessee acquired a vested right not to be disturbed except by a procedure known to law and that procedure has been prescribed only by section 147 of the Act and, therefore, once the assessment year had come to an end on 31.3.1998 and no assessment had been made upon the assessee, the A.O. has no option but to treat it as case of “escaped assessment” and proceed to issue a notice u/s. 148 of the Act. At page 448, of Sultan Ali’s case (supra), the Calcutta High Court observed that on the expiry of the assessment year, “…… the assessee acquires a kind of immunity of which he can be deprived any if certain preliminary conditions laid down in Section 34 are fulfilled.” Accordingly, the contention was that in the case of Motorola the AO could not have validly issued any notice u/s. 142(1) after 31.3.1998 and ought to have issued a notice only u/s 148 and since no such notice was issued, the assessment made was without jurisdiction. To the same effect is the judgment of the Hon’ble Supreme Court in the case of State of Assam and Another Vs. D.C. Choudhuri And another (76 ITR 706) which was also cited by Mr. Syali.

9.2. In support of the contention that a period of limitation has to be contextually inferred reference was made by Mr. Syali to page 132 of the treatise on interpretation of Statutes by francis Benion where there is a reference to the doctrine of Ellipsis which means that a period of limitation has to be read into the statutory

Page 8 of 201

provisions where it is not expressly prescribed, considering the consequences of not reading such limitation into the provisions.

9.3. The learned counsel also made reference to the legislative intention while substituting section 139(2) by section 142(1)(i) w.e.f. 1.4.1989 which was only to shorten the period of limitation prescribed for completion of assessment and certain other matters. In this connection he drew out attention to the amendment to section 139(4) and section 153 where the period of limitation was shortened and submitted that in this background the legislature could not have intended that the period u/s. 142(1) could be enlarged as compared to the period of allowed u/s. 139(4).

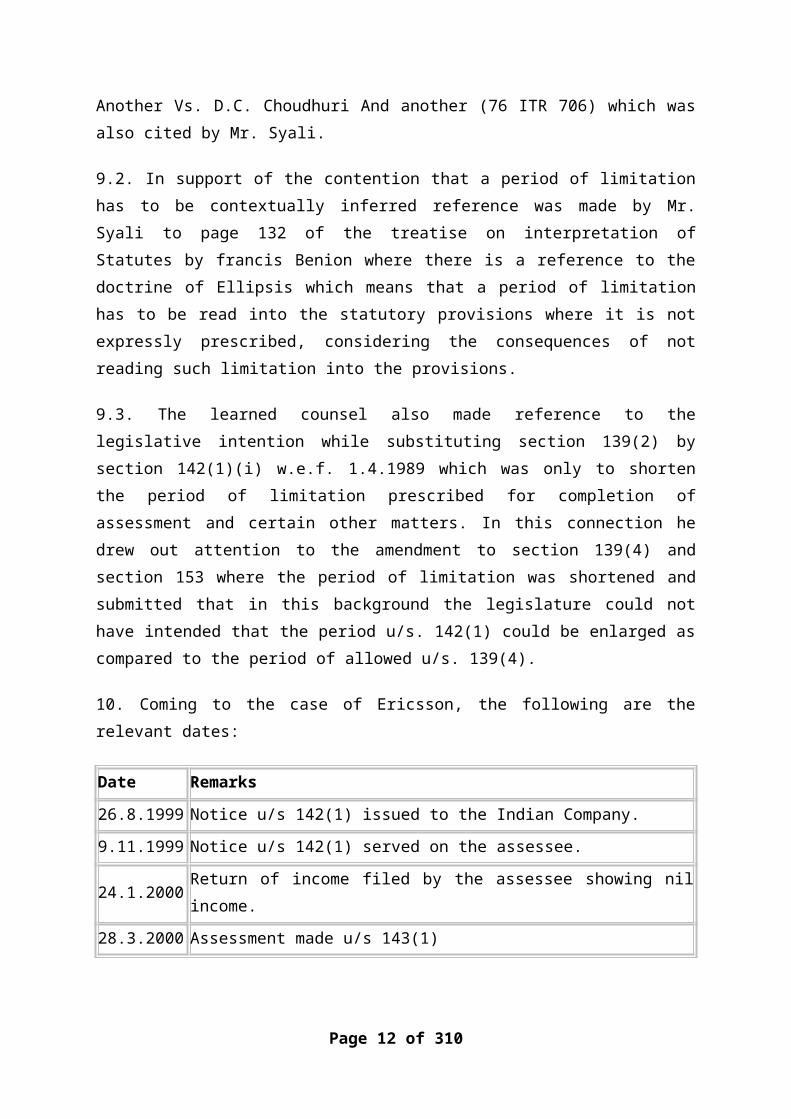

10. Coming to the case of Ericsson, the following are the relevant dates:

Date Remarks

26.8.1999 Notice u/s 142(1) issued to the Indian Company.

9.11.1999 Notice u/s 142(1) served on the assessee.

24.1.2000 Return of income filed by the assessee showing nil income.

28.3.2000 Assessment made u/s 143(1)

It may be noted that all these dates fell in the financial year 1.4.1999 to 31.3.2000.

11. Mr. Dastur, the learned counsel for the assessee (Ericsson) prefaced his arguments regarding the validity of the notice u/s 142(1) with what he called the basis postulate, which according to him was that we should avoid any interpretation which would result in the overlapping of the provisions of section 142(1) and section 148 over the same period of time. The reason according to him was that if this overlap is allowed, then the A.O. will be in a position to discriminate between different assesses and may even choose to issue notice u/s 148 instead of 142(1), since that would give him more time to complete the assessment. In this connection he referred to section 153(2) which provides for the limitation of two years from the end of the financial year in which the notice u/s. 148 was served, to complete the re-assessment. If such a discrimination is allowed the result in the present case would be tat if the assessment is to be completed u/s., 143(3), it would have to be done so on or before 31.3.2000, whereas if the assessment would have to be done us 148, it would have to be done on or before 31.3.200. This may also empower the A.O. to confer an advantage on certain assesses and allow himself mere time to complete the assessment.

12. Mr. Dastur raised on more preliminary point. He submitted that it is agreed on all sides including the orders of the Hyderabad and Delhi Benches of the Tribunal

Page 9 of 201

(supra) that though section 142(1) did not expressly provide for a period of limitation for issuing the notice but such a notice has to be issued within a reasonable time. What is the reasonable time is the question for consideration on a proper interpretation of the relevant provisions.

13. Two alternative were put forth before us in connection with the reasonable period of limitation to be read into section 142(1) for issuing the notice. The first alternative was that the notice should be issued on or before 31.3.1998 i.e. within the assessment year itself (with reference to the facts of this case where the assessment year is 1997-98). The reason is that according to him there is an inherent indication of such a time limit in section 148 itself. Section 149 contemplates the issue of notice u/s. 148 at any time on or after 1.4.1998 i.e. after the end of the assessment year but before a period of four years has elapsed. In certain cases a period of six years has been prescribed but this makes no difference to the argument. Therefore, a notice u/s. 148 in the present case can be issued at any time between 1.4.1998 and 31.3.2002. It, therefore, follows that the notice u/s. 142(1) cannot be issued after 31.3.1998 because from 1.4.1998, it would be a case of income escaping assessment into which field a notice u/s. 142(1) cannot intrude. In other words, if 1.4.1998 is the starting point for the issue of notice u/s. 148 on the footing that it is a case of escaped assessment, then 31.3.1998 is the concluding point for the issue of notice u/s. 142(1).

14. In support of this alternative. Mr. Dastur drew out attention to the observations of the Hon’ble Supreme Court at page 318 of Narsee Nagsee & Co., case (supra) and the judgment of the Bombay High Court in the case of Harakchand Makanji & Co. Vs. CIT (16 ITR 119).

15. The second alternative put forth by Mr. Dastur, which he characterized as the narrower view, is like this. Notice u/s. 142(1) can be issued up to one year from the end of the relevant assessment year i.e. in this case notice can be issued only upto 31.3.1999 and not thereafter. The reason is based on the provisions of section 139(4). This section gives an assessee the right to file a voluntary return up to a period of one year from the end of the assessment year. In the present case, such a right is available to the assessee upto 31.3.1999. As long as it is open to the assessee to file a voluntary return u/s 139(4), it cannot be said that the assessee has not filed any return of income and, therefore, Explanation 2(a) to section 147 which enables a re-assessment to be made in a case where no return of income has been furnished by the assessee, cannot be invoked. In other words, a notice u/s. 148 cannot be issued on the footing that the assessee has failed to file the return, so long as the assessee still has time to file a voluntary return u/s 139(4).

Page 10 of 201

In this situation, it cannot be said that as on 31.03.1998, the assessee had failed to file the return of income. Therefore, the narrower view is that a notice u/s. 142(1) can be issued only up to31.3.1999.

15.1. The above situation, according to Mr. Dastur would also fit in with the provisions of section 139(5) and section 153(1)(b). Section 139(5) gives the assessee a right to revise the return if he has already filed a return u/s. 139(1) or in response to notice u/s. 142(1), if he discovers any omission or wrong statement in the earlier return and such a revised return may be field at any time before the expiry of one year form the end of the relevant assessment year or before completion of the assessment, whichever is earlier. Section 153(1)(b) also provides for a time limit of one year from the end of the financial year in which a return or a revised return is field under sub-section (4) of section 39 or under sub-section (5) of section 139 respectively, for completing an assessment either u/s. 143 section 144.

16. Mr. G.C. Sharma the leaned counsel for the Department put forth the following submissions with regard to the validity of the notice u/s. 142(1). The Question of limitation in statutes, according to him, is of two kinds. The first is that it places an obligation on the subject. The second kind is the limitation which places fetters on the power of the authorities. The notice u/s. 142(1) is of the second kind whereas the obligation on he assessee to file the return is of the first kind. Nothing is to be implied in a taxing statute where it is not expressly stated, more particularly the question of limitation. Section 142(1) does not expressly provides for a period of limitation within which the notice thereunder ought to be issued. The section, it should be remembered, authorizes an enquiry before the assessment or re-assessment and there should be no limit on the power of the A.O. to make such an enquiry. Section 142(1) and section 148 operate in different fields in the sense that the former gives power to the A.O. to conduct an enquiry before making the assessment and call for a return of income in the course of such an enquiry, whereas section 148 is concerned with bringing to charge the escaped income. These fields should not be permitted to overlap and the interpretation to be placed on section 148 or section 147 should not be permitted to control the interpretation to be placed on section 142(1). Under section 142(1), the only limitation is that the notice calling for the return cannot be issued after the assessment. Section 147 has no impact on this aspect of section 142(1) and it should not be permitted to control or limit the filed of operation of section 142(1) or the power of the A.O. to issue a notice thereunder.

17. It was in the above background that Mr. Sharma proceeded to put forth his analysis of section 142(1). He emphasized that section 142(1) commences with the words “for the purpose of making an assessment”, which, according to him can only be read as the determination of the total income. In the determination of the total

Page 11 of 201

income, it is open to the A.O. as a first step, to compel the assessee to file a return of income where it is not filed u/s. 139(1). He pointed out that the words “before the end of the relevant assessment year”, which were there in section 139(2) were omitted w.e.f. 1.4.1989, on which day section 142(1) was introduced, and to reads into section 142(1) the condition that the notice calling for return thereunder should be issued before the end of the relevant assessment year, would be to ignore the fact that words to the effect which were present in the omitted section 139(2), do not find a place in the newly introduced section 142(1). He filed detailed written submissions which were filed by him before Delhi Bench of the Tribunal when he argued the case of Sheraton International (supra) and submitted that the same may be taken as his arguments vis-à-vis section 142(1) in the present case also.

18. Summing up the arguments Mr. Sharma pointed out that the time available to issue the notice u/s 142(1), in the absence of any express time limit prescribed in the section itself, is up to the making of an assessment. When it was enquired of him by the Bench to what would happen if the notice calling for the return is issued on 31.3.2000, which is that last day for completion of assessment for the assessment year 1997-98 u/s. 153(1)(a) and what would be the assessee’s remedy in such a case, Mr. Sharma answered that in such a case the assessment may be quashed for violation of rules of natural justice and the assessee could be given sufficient time to file the return of income. When it was pointed out by the Bench that under Explanation 2(a) of Section 147, even the failure of the assessee to file a return u/s. 142(1) is taken in, Mr. Sharma replied that the A.O. is entitled to wait till the period allowed to the assessee to file a voluntary return u/s. 139(4) expires, before issuing a notice u/s. 148.

18.1. In the course of his arguments Mr. Sharma also relied on the second proviso to section 144 of the Act which says that if a notice u/s. 142(1) calling for a return is issued to the assessee, in response to which no return was filed then it is not necessary for the AO. to issue a sow cause notice under the first proviso to section 144 calling upon the assessee to show cause why a best judgment assessment should not be made in respect of his income. In furtherance of this argument, Mr. Sharma contended that if the notice issued in this case u/s. 142(1) is held to be invalid for any reason, including the reason that it is beyond the period of limitation, then the assessment order passed u/s. 143(1) of the Act should be reads as an assessment made in substance u/s. 144.

19. In reply to the above, the following arguments were put forth by Mr. Dastur, the learned counsel for Ericsson:

Page 12 of 201

(a) Section 11 of the business Profits Tax Act corresponded to section 22(2) of the Indian Income tax Act, 1922 which later corresponded to section 139(2) of the I.T., Act, 1961. Section 139(2) was replaced by section 142(1)(i) w.e.f. 1.4.1989. It is in this background that we have to approach the question.

(b) The ratio of the Hon’ble Supreme Court judgment in Narsee Nagsee & Co (supra) is that the A.O. cannot have a concurrent power to proceed u/s. 11 of the Business Profits Tax Act and section 14 of the same Act. Therefore, the AO cannot have a concurrent power to act u/s 142(1) and section 148 of the 1961 Act.

(c) The marginal note to section 142 is “Inquiry before assessment”. This marginal note was appropriate before 1.4.1989 because section 142 before that date provided only for issue of notices by the AO calling upon the assessee to produce the account books and other relevant information in support of the return or on points on which the AO required clarification. This was the kind of inquiry contemplated by section 142 prior to 1.4.1989. The marginal note, therefore, was appropriate. However, when the section underwent a change w.e.f. 1.4.1989 whereby clause (i) was introduced giving the AO the power to call for a return of income and section 139(2) was omitted w.e.f the same date, the marginal note was not suitably changed and it continued to be “Inquiry before assessment”. In this connection, he referred to the decision of Hon’ble Supreme Court in the case of CIT Vs. Ahmedbhai Umarbhai & Co, 18 ITR 472 at 487 and the later judgment of the Hon’ble Supreme Court in the case of K.P. Varghese vs. ITO (13) ITR 597 at 609. In these judgments, it has been held that the marginal note to the section cannot override or govern the express provisions of the section.

(d) Thee is no dispute that certain powers vest with the AO for issue of notice u/s. 142(1), but these powers are different from the assessee’s right to file a voluntary return u/s. 139(4) within one year from the end of the assessment year.

(e) The contention of Mr. Sharma that if the notice u/s. 142(1) calling for a return is issued on the last day of the period of limitation for completing the assessment thereby preventing the assessee in complying with the same, the assessment may be set aside by the appellate authorities, is a wholly unsatisfactory way of deciding

Page 13 of 201

the issue. This solution is subjective and is not based on rational interpretation of the provisions of the Act. Therefore, there has to be a definite period for issuing such a notice which in this case (Ericsson) was 31.3.1999.

20. In the course of his reply Mr. Dastur also offered parawise comments on the written submissions filed by Mr. Sharma on the question of section 142(1).

21. At this juncture, as Mr. Dastur was winding up his reply, we asked him as to what would be the effect of the invalidity of the notice issued u/s. 142(1) after the period of limitation, assuming the period of limitation ends on 31.3.1998 or 31.3.1999. To this query he replied that the assessment will have to be struck down as invalid and without jurisdiction. He cited the judgment of the Hon’ble Supreme Court in the case of Kumar Jagdish Chandra Sinha (by Legal Representatives) Vs. CIT 220 ITR 67. He submitted that the AO is entitled to make an assessment u/s. 143(3) only (a) if a valid return of income is filed pursuant to a valid notice issued u/s. 142(1) or (b) if the assessee files a voluntary return u/s. 139(4).

22.1. Mr. Dastur further submitted that since the A.O. in the present case has followed the section 143(2) channel, it is not open to him now to change track and say that the assessment may be treated as made u/s. 144 of the Act (best judgement). He pointed out that this is not a case of the A.O. quoting a wrong section of the Act. In essence and substance, the order is one passed only u/s. 143(3) since otherwise the notice issued u/s. 143(2) and the production of material and evidence makes no sense. The AO did not purport to act u/s. 144 at all and the argument that he only quoted the wrong section is, therefore, not available to the revenue. On he question as to why the assessment cannot be deemed to have been made u/s. 144, it was contended hat firstly, thee was no notice to make the best judgment assessment under the first proviso to section 144 and secondly, in order to apply the second proviso, there should have been a valid notice u/s. 142(1), which in this case was not there. Therefore since the procedure laid down in section 144 had not been followed, there was no question of treating the assessment as a best judgment assessment. Mr. Dastur also relied on the judgment of the Calcutta High Court in the case of Sultan Ali Gharami (supra) to contend that there can be no waiver of a statutory condition and in the present case even on facts, the assessee did not waive the condition that a valid notice u/s. 142(1) ought to have been issued.

22. In his reply Mr. Syali learned counsel for Motorola submitted that the remedy of the assessment being set aside by the appellate authority in a case where the notice u/s. 142(1) is issued on the last day of the period of limitation is not an effective remedy. In his submission, the A.O. should not in the first place be permitted as all to wait till the last day of limitation to issue the notice, thereby compelling the assessee

Page 14 of 201

to approach the appellate authorities to have the assessment set aside. Further complications may crop up if the assessment is not set aside by the appellate authority. He supported the argument of Mr. Dastur on this aspect of the matter. He also relied heavily on the judgment of the Calcutta High Court in the case of CIT Vs. Sultan Ali Gharami (supra), Satyanarayan Bhalotia Vs. CIT 207 ITR 1030 and Burdwan Wholesale Consumers’ Co-operative Society Ltd. Vs. CIT 191 ITR 570. As regards the effect of the invalidity of the notice issued by the AO, purported to be a notice u/s. 142(1), Mr. Syali submitted that the requirement of a valid notice is a mandatory requirement and not merely directly, that it is not a mere error of exercising the jurisdiction by the A.O. but of lack of jurisdiction and, therefore, it resulted in an illegality, the consequence of which was that the assessment is null and void. He drew out attention to the observations of the majority judgment of the Hon’ble Supreme Court in the case of Narsee Nagsee & Co. (supra) where, after having held that no valid notice had been issued u/s. 11 of the Business Profits Tax Act, the Hon’ble Supreme Court in terms held that the assessment is without jurisdiction.

23. Mr. G.C. Sharma, the learned counsel for the revenue, wished to make a few clarifications on this issue and, therefore, we permitted him to do so. He started by saying that each case cited by the assessee has been decided on the peculiar facts and no general inference can be drawn. He also filed his submissions in three parts wherein part-I were submissions in general part-II pertained to the principle of estoppel wherein it was contended that the assessee cannot at the same time approbate and reprobate and Part – III contained the distinguishing features between the provisions of three Act, namely 1922 Act, the Business Profits Tax Act and the 1961 Act. Apart form the written submissions he also contended that the assessment cannot be quashed, even assuming that the notice issued u/s. 142(1) was beyond the period of limitation. He pointed out that at any rate this point was not raised by the assessee before the A.O. but was raised only before the CIT(Appeals). The assessee, according to Mr. Sharma, led the Department to believe that the notice as well as the return were valid, participated in the proceedings, permitted the AO to make an assessment u/s 143 and thereby prevented the AO from making a best judgment assessment u/s 144 and by doing all this, an advantage was gained by the assessee. Once the assessment was completed, the assessee field an appeal an it was only in this appeal that it look the point that the notice issued by the AO is beyond the period of limitation and, therefore, the assessment was null and void. This should nor be permitted. He relied strongly on the authorities referred to by him in part-II of his written submissions dealing with the principle of estoppel / approbare – reprobate. He further pointed out that the provisions of the Business Profit Tax act considered by the Hon’ble Supreme Court in Narsee Nagsee & Co’s (supra) were

Page 15 of 201

materially different from the provisions which are now under consideration. In this connection he drew our attention to the fact that no time limit for issue of notice u/s. 11 of the Business Profits Tax Act was provided. According to him, section 142(1) of the 1961 Act is not the same as section 139(2) of the 1961 Act or section 22(2) of the 1922 Act. He reiterated the even assuming that the notice and the return are invalid, the assessment must be treated as one having been made u/s. 144.

24. Since Ms. Sharma for the revenue had filed written submissions in three parts in relation to the issue of notice u/s. 142(1), we though it appropriate to permit the assesses to offer their comments on the written submissions and the authorities cited therein, especially because the question of estoppel and the principle of approbate and reprobate wee not raised earlier. Accordingly we called upon Mr. Dastur to address arguments with reference to the written submission.

25. Mr. Dastur submitted as follows:

(a) Section 22(2) of the 1922 Act did prescribe a time limit but it is not relevant and nothing turns on it.

(b) Section 142(1) does not prescribe a time limit and similar was the position u/s. 11 of the Business Profits Tax Act.

(c) Though section 11 of the Business Profits Tax Act did not prescribe a time limit, section 14 of the said Act was reads long with it by the Supreme Court in Narsee Nagsee & Co. (supra) case and a time limit was read into the provisions of section 11. Similarly, a time limit should be read into the provisions of section 142(1)(i), reading the same along with section 147.

(d) It is agreed by every one concerned that a time limit, though not expressly prescribed in section 142(1), must be read into the provisions of section 142(1)(i). In fact, even in the case of Sheraton International (supra), the Delhi Bench of the Tribunal agreed a reasonable time limit should be read into the provisions. There are two options in this regard. The first is that the notice should be issued before the end of the assessment year because after that date the period of limitation for issue of notice u/s. 148 will start. The second option is to avoid an interpretation of the

Page 16 of 201

provisions which would given concurrent jurisdiction to the A.O. in the sense that he can issue a notice either u/s. 142(1) or u/s. 148 in respect of the same period.

(e) Without prejudice to the above Mr. Dastur contended that the period of one year from the end of the assessment year i.e. 31.3.1999 in this case should be considered as the period of limitation for issue of notice because section 139(4) gives the assessee a rights to file a voluntary return before that date. Till that period expires, income cannot be said to have escaped assessment.

26. It was contended that the provisions of clause (i) of section 142(1) were different from the provisions of clauses (ii) and (iii) of Section 142(1) in so far as the later two clauses were procedural in nature, the breach of which was curable, if no notice had been issued. However, so far as clause (i) was concerned, it was a substantial provision bestowing jurisdiction on the AO to call for the return form the assessee and the breach of this provisions would render the assessment null and void. In substance, the contention was that there could be different limitation periods in the same section for issue of different notices. This is not strange or unknown and as an illustration Mr. Dastur pointed out the provisions of section 148 in this regard, where periods like 4 years and 6 years have been prescribed for issue of notice depending upon the circumstances.

27. As regards the application of the principle of estoppel, it was submitted by Mr. Dastur that there was no question of estoppel as the assessee had field the return of income simply in compliance with the notice issued u/s. 142(1)(i) of the Act. At the earlier stages, the assessee did not contest this notice only because its Chartered Accountant was not aware of the legal position. Even in the original grounds of appeal, objection to the notice was not raised as a ground. It was raised only as an additional ground, which was admitted by the leaned CIT(Appeals) u/s. 250(5) on being satisfied that the assessee was entitled to raise such a ground and its conduct was bonafide. Complying with a statutory notice by filing the return, participating in the proceedings etc. cannot be termed as misleading as was argued by he learned counsel for the revenue and when any question goes to the root of the matter, the assessee cannot be prevented from raising the same at any stage of the proceedings. The principle of “approbate and reprobate” applied to a factual situation where an assessee has taken some advantage at one stage of the proceedings and then turns round to contest that very situation when it appears to be disadvantageous to the assessee. There cannot be any approbate reprobate on legal principles but the validity of a notice is to be examined by the revenue authorities. It is their duty to act in accordance with law and in such a situation, there

Page 17 of 201

could but no “approbate and reprobate”. There may be approbate and reprobate only on questions of act. In support of his contention, Mr. Dastur relied on the decision of the Allahabad High Court in Mir Iqbal Husain Vs. State of UP 52 ITR 625 where it was held that mere filing of a return as directed by the notice does not in itself establish that the assessee had waived his right to object to the notice. He also cited the judgment of the Gujarat High Court in P.V. Doshi Vs. CIT, Gujarat 113 ITR 22 where it was held that the jurisdictional provision which was mandatory and enacted in public interest could never be waived and there can be no question of waiver of such a condition by the assessee. Mr. Dastur also made parawise comments vis-à-vis the written submissions filed by Mr. G.C. Sharma on this question.

28. We have given careful thought to the submissions advanced before us by the parties. We have also examined the relevant statutory provisions of the Indian Income Tax Act, 1922 (Old Act) as also of the Income-tax Act, 1961 (New Act) to which our attention was drawn. We have also considered the case law cited before us. It is an admitted position that no time is prescribed under sec. 142(1)(i) to issue notice. However, both the Benches of the Tribunal i.e. Hydrabad Bench in the case of Dr. Vijaykumar Datla (supra) and Delhi Bench in the case of Sheraton International Inc. (supra) agreed that some reasonable time limit has to be read into the provisions. Notice under the above provision calling for a return cannot be issued any time at the whims and fancies of the Assessing Officer. Even Delhi Bench held that some time limit has to be read and held that notice under the above provisions could be issued till the date of the completion of the assessment. Therefore, the proposition that notice is to be issued within a reasonable time having regard to the scheme of the Act is not in dispute. However, there is a controversy as to what is the inbuilt scheme of the Act, which indicates that such notice can be issued within a particular time limit. As per the assessee, the notice is to be issued within the assessment year or within one year of the assessment year. The revenue on the other hand, contends that the said notice can be issued till the time, the AO can make an assessment.

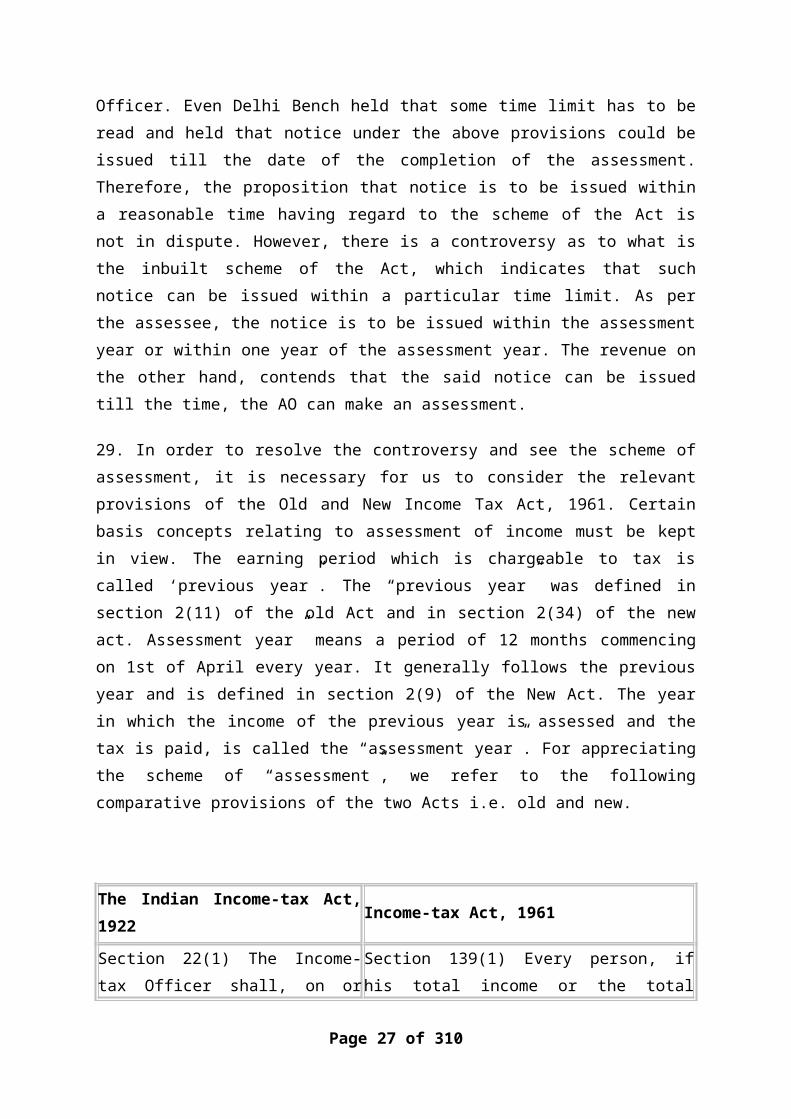

29. In order to resolve the controversy and see the scheme of assessment, it is necessary for us to consider the relevant provisions of the Old and New Income Tax Act, 1961. Certain basis concepts relating to assessment of income must be kept in view. The earning period which is chargeable to tax is called ‘previous year”. The “previous year” was defined in section 2(11) of the old Act and in section 2(34) of the new act. Assessment year” means a period of 12 months commencing on 1st of April every year. It generally follows the previous year and is defined in section 2(9) of the New Act. The year in which the income of the previous year is assessed and the tax is paid, is called the “assessment year”. For appreciating the scheme of

Page 18 of 201

“assessment”, we refer to the following comparative provisions of the two Acts i.e. old and new.

The Indian Income-tax Act, 1922 Income-tax Act, 1961

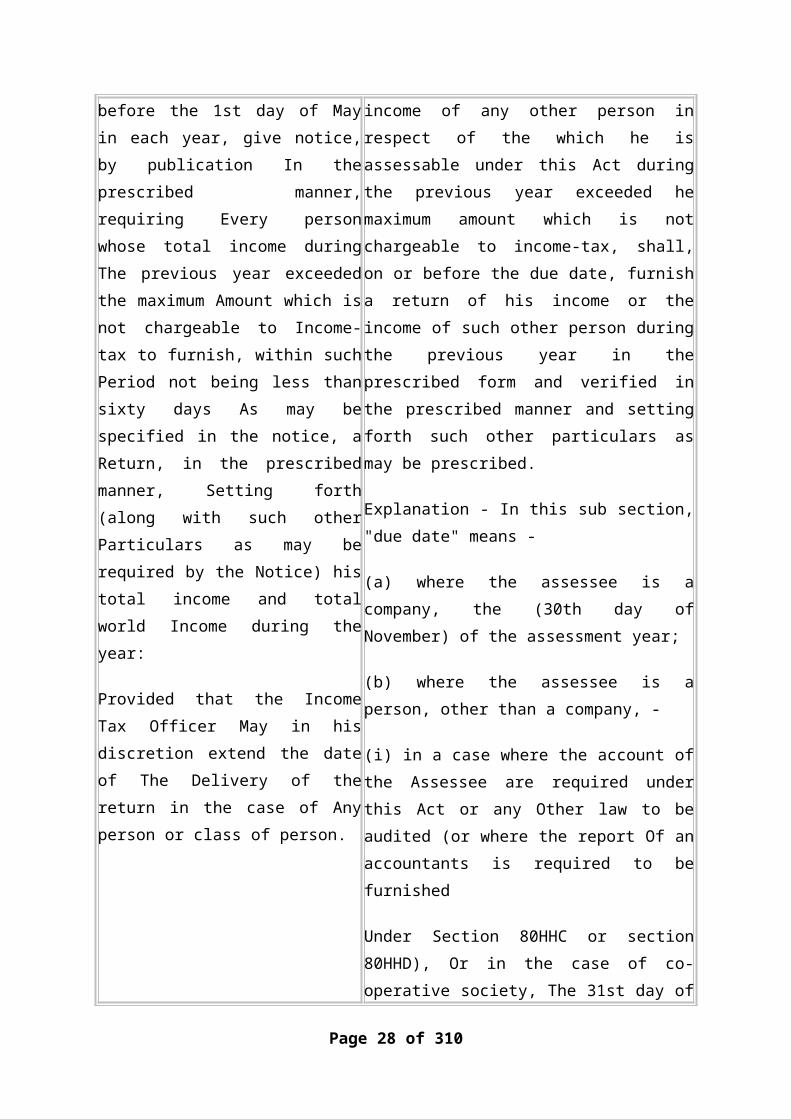

Section 22(1) The Income-tax Officer shall, on or before the 1st day of May in each year, give notice, by publication In the prescribed manner, requiring Every person whose total income during The previous year exceeded the maximum Amount which is not chargeable to Income-tax to furnish, within such Period not being less than sixty days As may be specified in the notice, a Return, in the prescribed manner, Setting forth (along with such other Particulars as may be required by the Notice) his total income and total world Income during the year:

Provided that the Income Tax Officer May in his discretion extend the date of The Delivery of the return in the case of Any person or class of person.

Section 139(1) Every person, if his total income or the total income of any other person in respect of the which he is assessable under this Act during the previous year exceeded he maximum amount which is not chargeable to income-tax, shall, on or before the due date, furnish a return of his income or the income of such other person during the previous year in the prescribed form and verified in the prescribed manner and setting forth such other particulars as may be prescribed.

Explanation - In this sub section, "due date" means -

(a) where the assessee is a company, the (30th day of November) of the assessment year;

(b) where the assessee is a person, other than a company, -

(i) in a case where the account of the Assessee are required under this Act or any Other law to be audited (or where the report Of an accountants is required to be furnished

Under Section 80HHC or section 80HHD), Or in the case of co-operative society, The 31st day of October of the assessment year;

(ii) in a case where the total income referred to in this sub-section includes any income from business or profession, not being a case falling under sub-clause (i), the 31st day of

Page 19 of 201

August of the assessment year;

(iii) in any other case, the 30th day of June of the assessment year.)

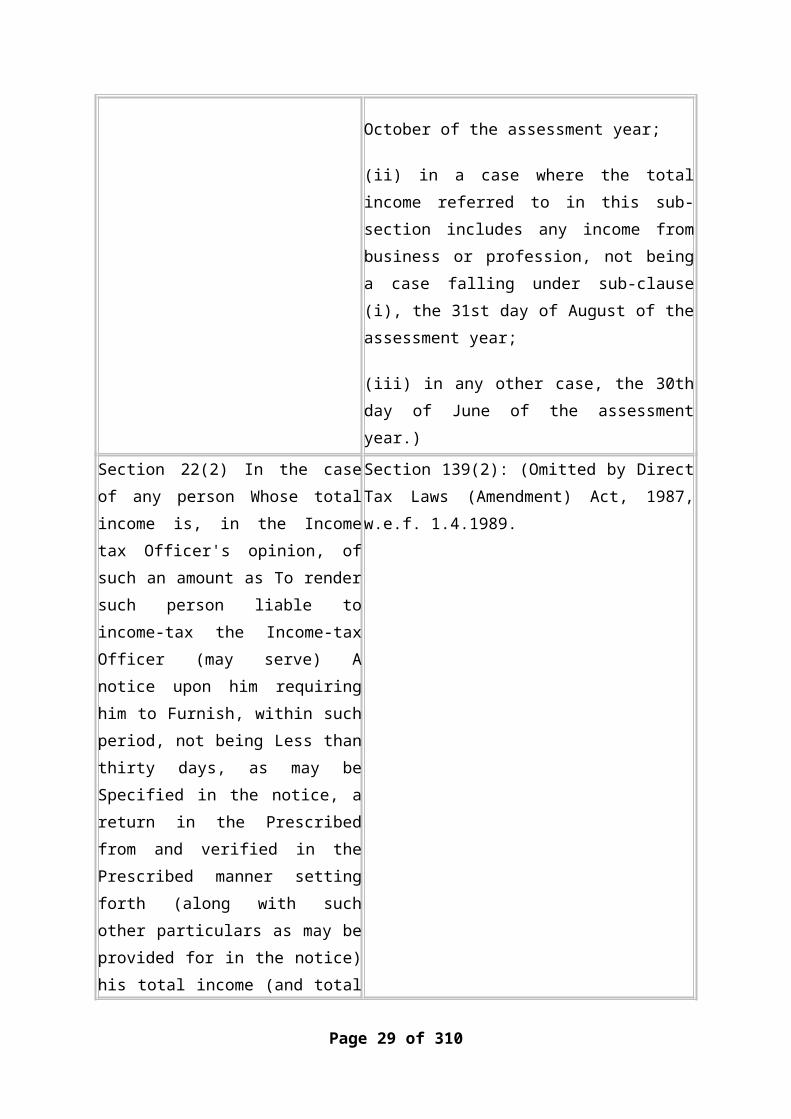

Section 22(2) In the case of any person Whose total income is, in the Income tax Officer's opinion, of such an amount as To render such person liable to income-tax the Income-tax Officer (may serve) A notice upon him requiring him to Furnish, within such period, not being Less than thirty days, as may be Specified in the notice, a return in the Prescribed from and verified in the Prescribed manner setting forth (along with such other particulars as may be provided for in the notice) his total income (and total words income) during the previous year:

Provided that the Income-tax officer may In his discretion extend the date of for the delivery of the return.)

Section 139(2): (Omitted by Direct Tax Laws (Amendment) Act, 1987, w.e.f. 1.4.1989.

Section 22(2A) xxxxxxxxxxxxxx xxxxxxxxxxxxxxxxxxxxxxx

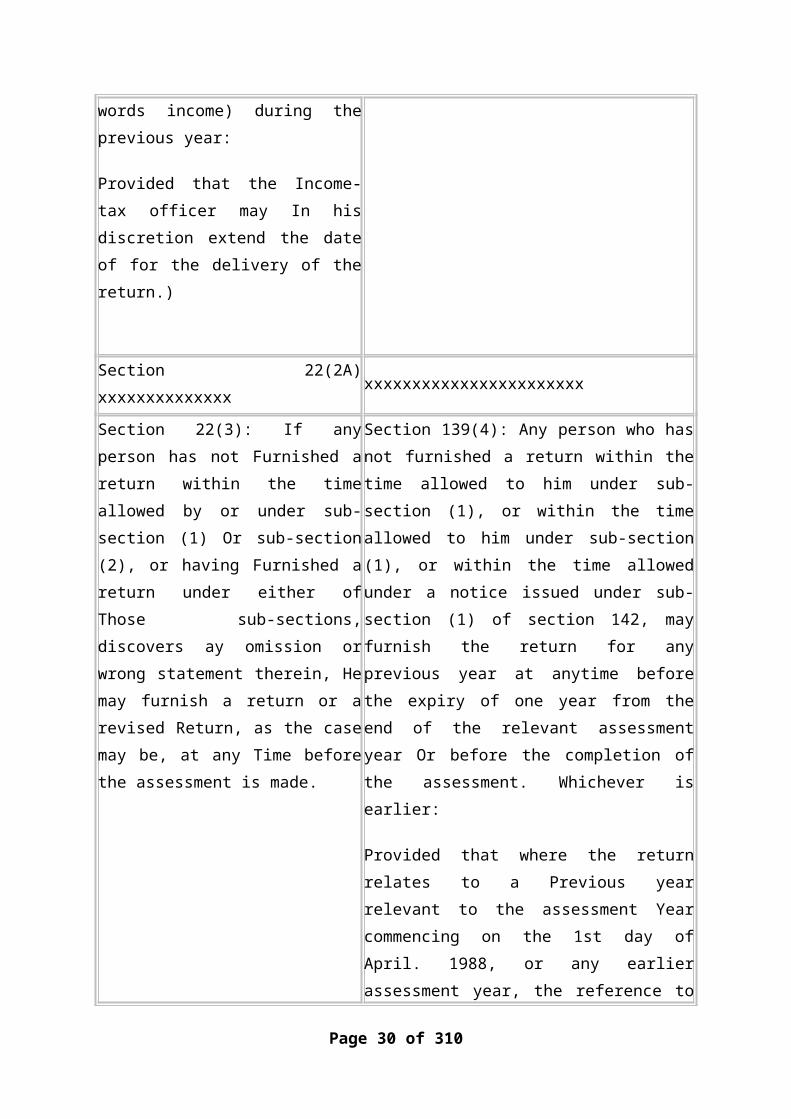

Section 22(3): If any person has not Furnished a return within the time allowed by or under sub-section (1) Or sub-section (2), or having Furnished a return under either of Those sub-sections, discovers ay omission or wrong statement therein, He may furnish a return or a revised Return, as the case may be, at any Time before the assessment is made.

Section 139(4): Any person who has not furnished a return within the time allowed to him under sub-section (1), or within the time allowed to him under sub-section (1), or within the time allowed under a notice issued under sub-section (1) of section 142, may furnish the return for any previous year at anytime before the expiry of one year from the end of the relevant assessment year Or before the completion of the assessment. Whichever is earlier:

Page 20 of 201

Provided that where the return relates to a Previous year relevant to the assessment Year commencing on the 1st day of April. 1988, or any earlier assessment year, the reference to one year aforesaid shall be construed as a reference to two years form the end of the relevant assessment year.)

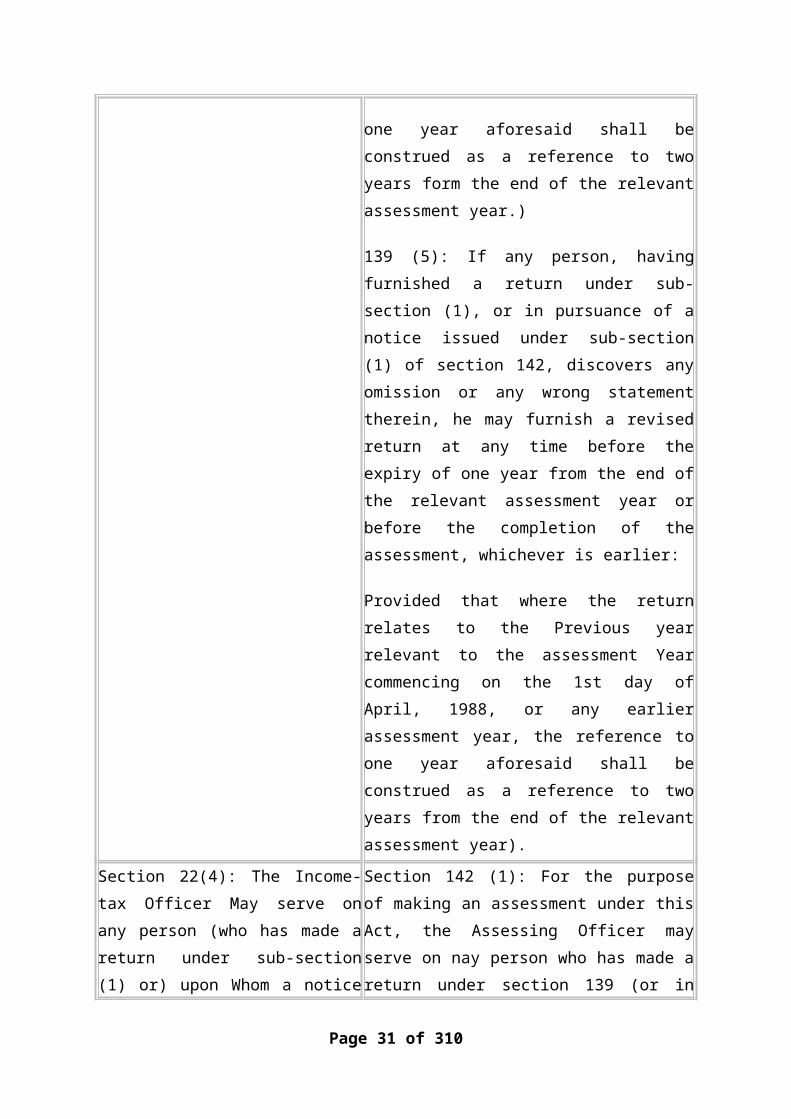

139 (5): If any person, having furnished a return under sub-section (1), or in pursuance of a notice issued under sub-section (1) of section 142, discovers any omission or any wrong statement therein, he may furnish a revised return at any time before the expiry of one year from the end of the relevant assessment year or before the completion of the assessment, whichever is earlier:

Provided that where the return relates to the Previous year relevant to the assessment Year commencing on the 1st day of April, 1988, or any earlier assessment year, the reference to one year aforesaid shall be construed as a reference to two years from the end of the relevant assessment year).

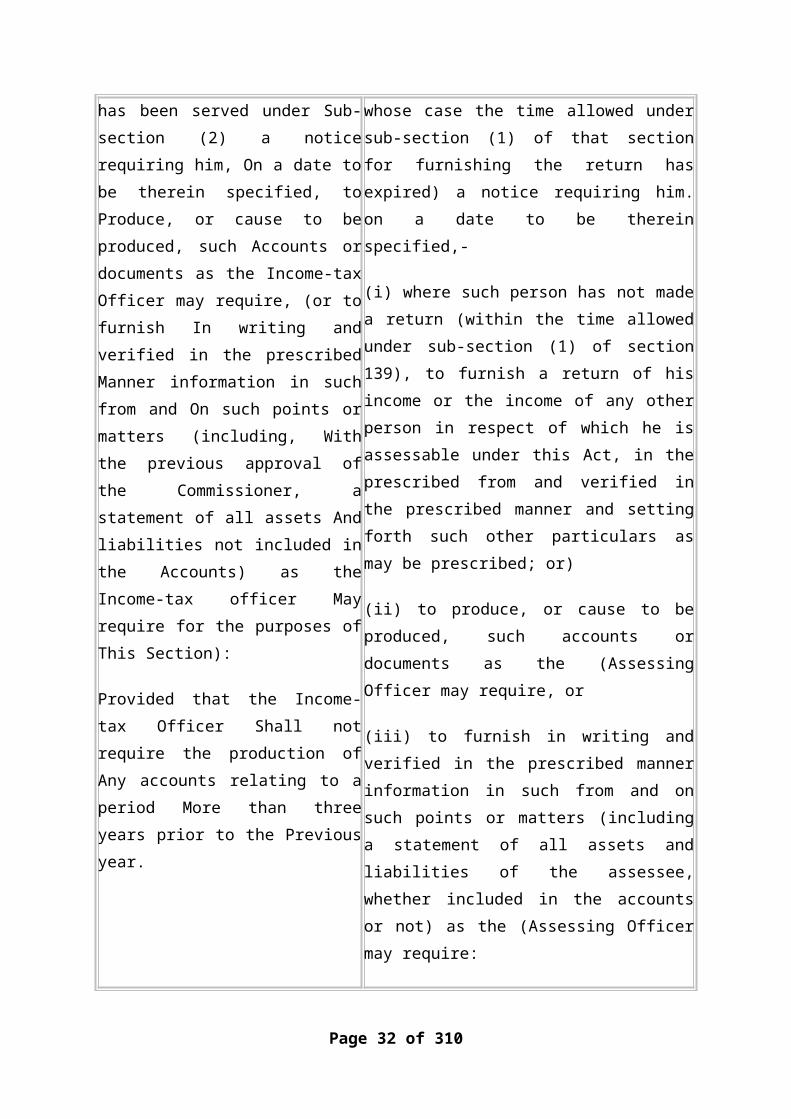

Section 22(4): The Income-tax Officer May serve on any person (who has made a return under sub-section (1) or) upon Whom a notice has been served under Sub-section (2) a notice requiring him, On a date to be therein specified, to Produce, or cause to be produced, such Accounts or documents as the Income-tax Officer may require, (or to furnish In writing and verified in the prescribed Manner information in such from and On such points or matters (including, With the previous

Section 142 (1): For the purpose of making an assessment under this Act, the Assessing Officer may serve on nay person who has made a return under section 139 (or in whose case the time allowed under sub-section (1) of that section for furnishing the return has expired) a notice requiring him. on a date to be therein specified,-

(i) where such person has not made a return (within the time allowed under sub-section (1) of section 139), to furnish a return of his income or the income of any other person in respect of which he is assessable under this

Page 21 of 201

approval of the Commissioner, a statement of all assets And liabilities not included in the Accounts) as the Income-tax officer May require for the purposes of This Section):

Provided that the Income-tax Officer Shall not require the production of Any accounts relating to a period More than three years prior to the Previous year.

Act, in the prescribed from and verified in the prescribed manner and setting forth such other particulars as may be prescribed; or)

(ii) to produce, or cause to be produced, such accounts or documents as the (Assessing Officer may require, or

(iii) to furnish in writing and verified in the prescribed manner information in such from and on such points or matters (including a statement of all assets and liabilities of the assessee, whether included in the accounts or not) as the (Assessing Officer may require:

provided that -

(a) the previous approval of the (Deputy Commissioner shall be obtained before Requiring the assessee to furnish a statement Of all assets and liabilities not included in the accounts;

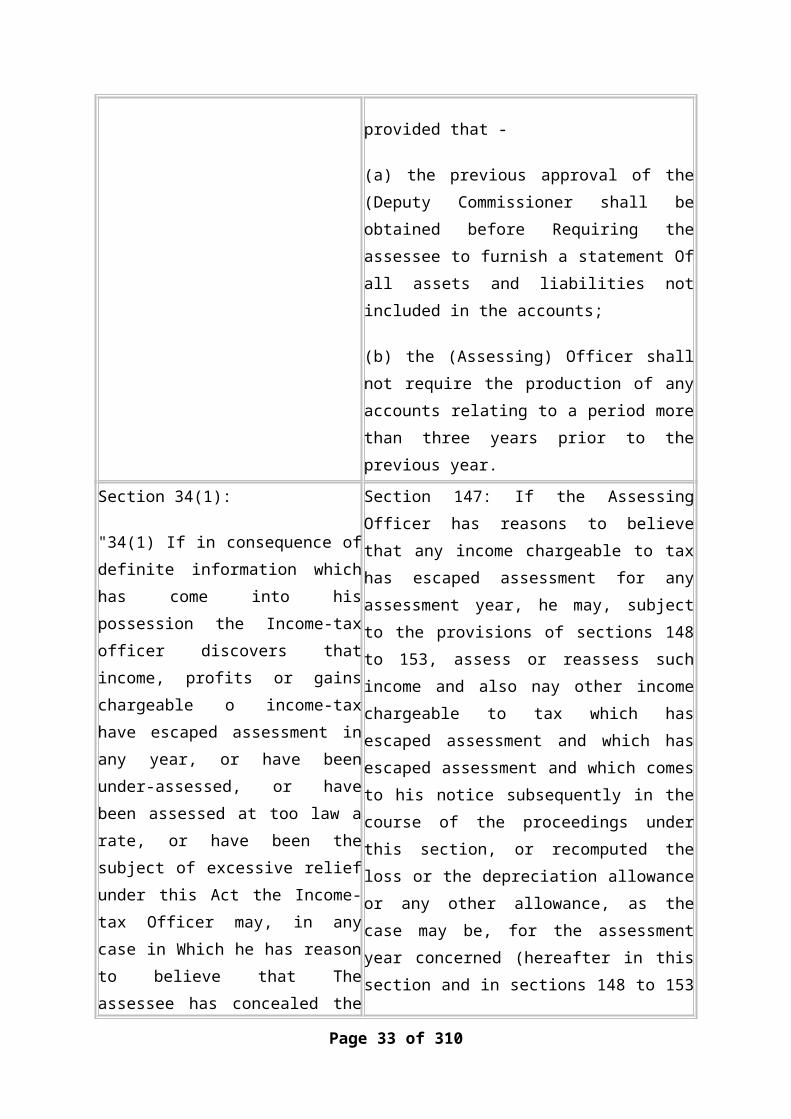

(b) the (Assessing) Officer shall not require the production of any accounts relating to a period more than three years prior to the previous year.

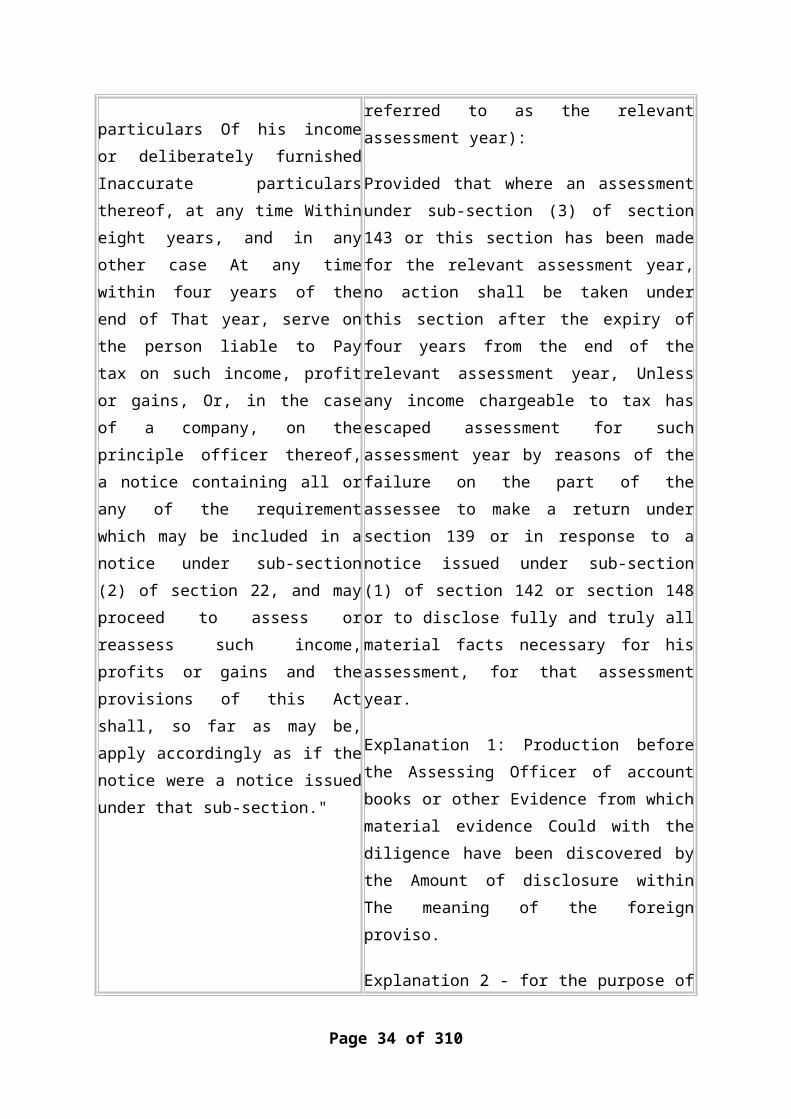

Section 34(1):

"34(1) If in consequence of definite information which has come into his possession the Income-tax officer discovers that income, profits or gains chargeable o income-tax have escaped assessment in any year, or have been under-assessed, or have been assessed at too law a rate, or have been the subject of excessive relief under this Act the Income-tax Officer may, in any case in Which he

Section 147: If the Assessing Officer has reasons to believe that any income chargeable to tax has escaped assessment for any assessment year, he may, subject to the provisions of sections 148 to 153, assess or reassess such income and also nay other income chargeable to tax which has escaped assessment and which has escaped assessment and which comes to his notice subsequently in the course of the proceedings under this section, or recomputed the loss or the depreciation allowance or any other allowance, as the case may be, for the

Page 22 of 201

has reason to believe that The assessee has concealed the particulars Of his income or deliberately furnished Inaccurate particulars thereof, at any time Within eight years, and in any other case At any time within four years of the end of That year, serve on the person liable to Pay tax on such income, profit or gains, Or, in the case of a company, on the principle officer thereof, a notice containing all or any of the requirement which may be included in a notice under sub-section (2) of section 22, and may proceed to assess or reassess such income, profits or gains and the provisions of this Act shall, so far as may be, apply accordingly as if the notice were a notice issued under that sub-section."

assessment year concerned (hereafter in this section and in sections 148 to 153 referred to as the relevant assessment year):

Provided that where an assessment under sub-section (3) of section 143 or this section has been made for the relevant assessment year, no action shall be taken under this section after the expiry of four years from the end of the relevant assessment year, Unless any income chargeable to tax has escaped assessment for such assessment year by reasons of the failure on the part of the assessee to make a return under section 139 or in response to a notice issued under sub-section (1) of section 142 or section 148 or to disclose fully and truly all material facts necessary for his assessment, for that assessment year.

Explanation 1: Production before the Assessing Officer of account books or other Evidence from which material evidence Could with the diligence have been discovered by the Amount of disclosure within The meaning of the foreign proviso.

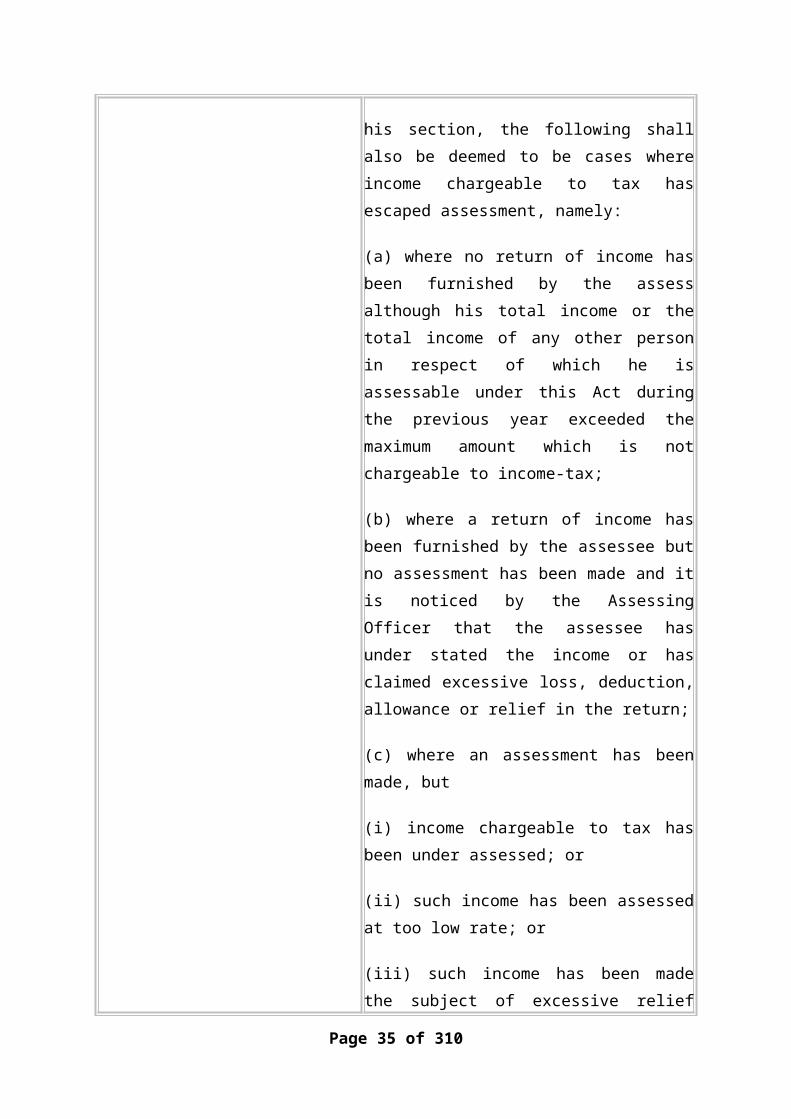

Explanation 2 - for the purpose of his section, the following shall also be deemed to be cases where income chargeable to tax has escaped assessment, namely:

(a) where no return of income has been furnished by the assess although his total income or the total income of any other person in respect of which he is assessable under this Act during the previous year exceeded the maximum amount which is not chargeable to income-tax;

(b) where a return of income has been

Page 23 of 201

furnished by the assessee but no assessment has been made and it is noticed by the Assessing Officer that the assessee has under stated the income or has claimed excessive loss, deduction, allowance or relief in the return;

(c) where an assessment has been made, but

(i) income chargeable to tax has been under assessed; or

(ii) such income has been assessed at too low rate; or

(iii) such income has been made the subject of excessive relief under this Act; or

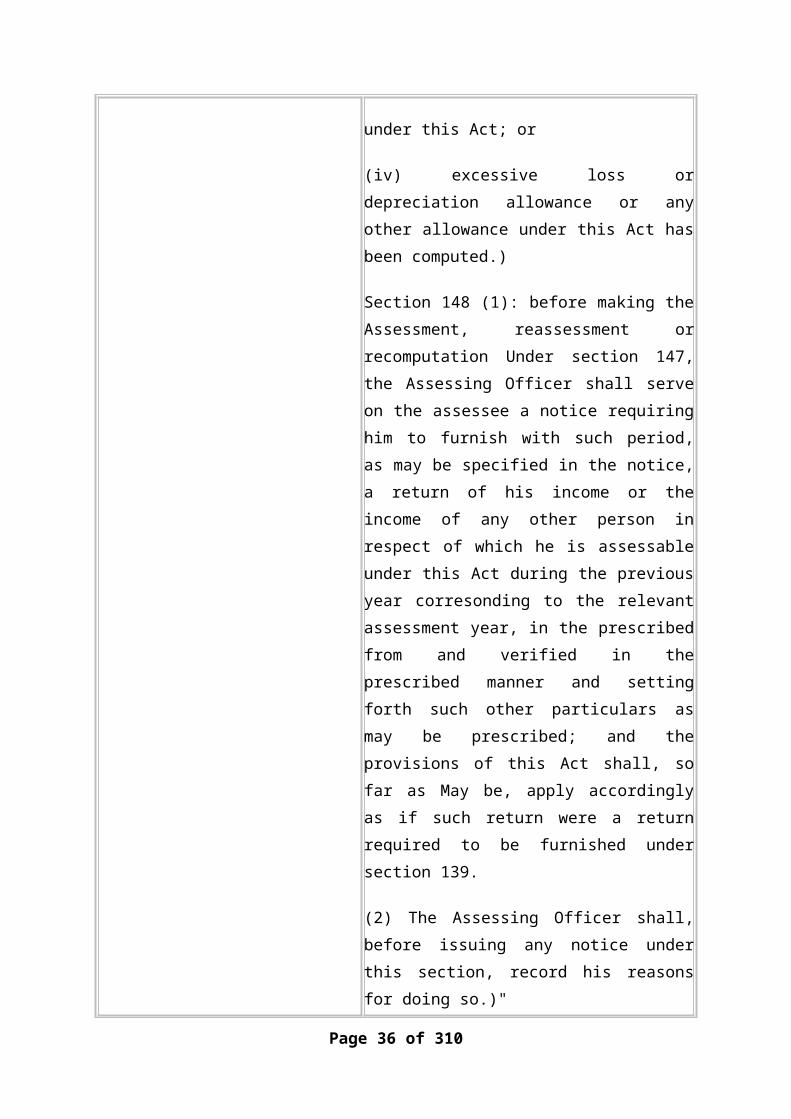

(iv) excessive loss or depreciation allowance or any other allowance under this Act has been computed.)

Section 148 (1): before making the Assessment, reassessment or recomputation Under section 147, the Assessing Officer shall serve on the assessee a notice requiring him to furnish with such period, as may be specified in the notice, a return of his income or the income of any other person in respect of which he is assessable under this Act during the previous year corresonding to the relevant assessment year, in the prescribed from and verified in the prescribed manner and setting forth such other particulars as may be prescribed; and the provisions of this Act shall, so far as May be, apply accordingly as if such return were a return required to be furnished under section 139.

(2) The Assessing Officer shall, before issuing

Page 24 of 201

any notice under this section, record his reasons for doing so.)"

30. It is evidet form the above that the basic scheme relating to assessment of income is that under the Old Act, after 1939, the ITO was required to give a notice u/s. 22(1) by publication calling for returns in the prescribed form from persons whose total income was assessable under the Act. In the new Act, as per sub-section (1) of section 39, a statutory obligation has been cast on the assessee to furnish a return of income. Under both the Acts, the AO (ITO) is authorized to issue notice to any person if in his opinion such person is liable to tax. Such powers were vested under section 22(2) of the old Act, corresponding to section 139(2) of the new Act. Section 139(2) was omitted with effect from 1.4.1989 and simultaneously the same power was incorporated in section 142(1) of the Act. A detailed reference to the provisions shall be made hereinafter.

31. In case no assessment was made or an under-assessment was made, the income was said to have “escaped assessment” and the ITO was authorized to take action as provided in section 34 of the old act. A similar provisions is retained in section 147/148 of the new Act. If a person having taxable income failed to furnish a return under sub-section (1) or sub-section (2) of section 22 of the old Act, he could furnish such return under sub-section (3) of section 22 of the old Act. A similar right is available to the assessee and such an enabling provision is contained in sub-section (4) of section 139 of the new Act. The period provided has been changed from time to time and the emphasis is on wrapping up the process of the assessment as early as possible. Likewise, other provisions relating to the powers of the ITO to make an assessment, including best judgment assessment, have been referred to above. At this stage it may be relevant to state that sections 11 and 14 of the Business Profits Tax Act where held by their Lordships of the Supreme Court to be identical to section 22(2) and section 34(1) of the old Act respectively, in the case of Narsee Nagsee & Co (supra). Likewise sub-sections (1), (2) and (3) of section 19 and sub-sections (1), (2) and (3) of section 20 of the Assam Agricultural Income-tax Act where held to correspondent to sub-sections (1), (2) and (3) of section 22 and sub-section (1), (2) and (3) of section 23 of the old act respectively Section 30 of the same Act was held to be corresponding to section 34 of the old Act. This was held by their lordships of the Supreme Court in the case of State of Assam & other Vs. D.C. Choudhury & Others (supra).

32. The Hydrabad Bench of the Tribunal in the case of Dr. Vijay Kumar Datla (supra) and leaned counsel for the assessee in appeal before us placed strong reliance on the decision of the Hon’ble Supreme Court in the case of CIT Vs. Narsee Nagsee &

Page 25 of 201

Co (supra). In the case of CIT Vs. Narsee Nagsee& Co. 1960 40 ITR 307, their Lordships of the Hon’ble Supreme Court, while considering a case under the business Profits Tax Act (BPTA), held that notice issued under sec. 11(1) of BPTA more than four yeas after the close of the charging period, was bad in law as profits had escaped assessment within the meaning of section 14 of the aforesaid Act which was applicable to the case Without applying the above section, notice issued under sec. 11 was held to be beyond time and without jurisdiction. Sections 11 and 14 of the BPTA were held to be similar to sections 22(2) and 34(1) of the old Act. No time limit was provided in section 11 of BPTA also Their Lordships (as per the majority) made the following observations (@ page 315) relating to the scheme of assessment: -

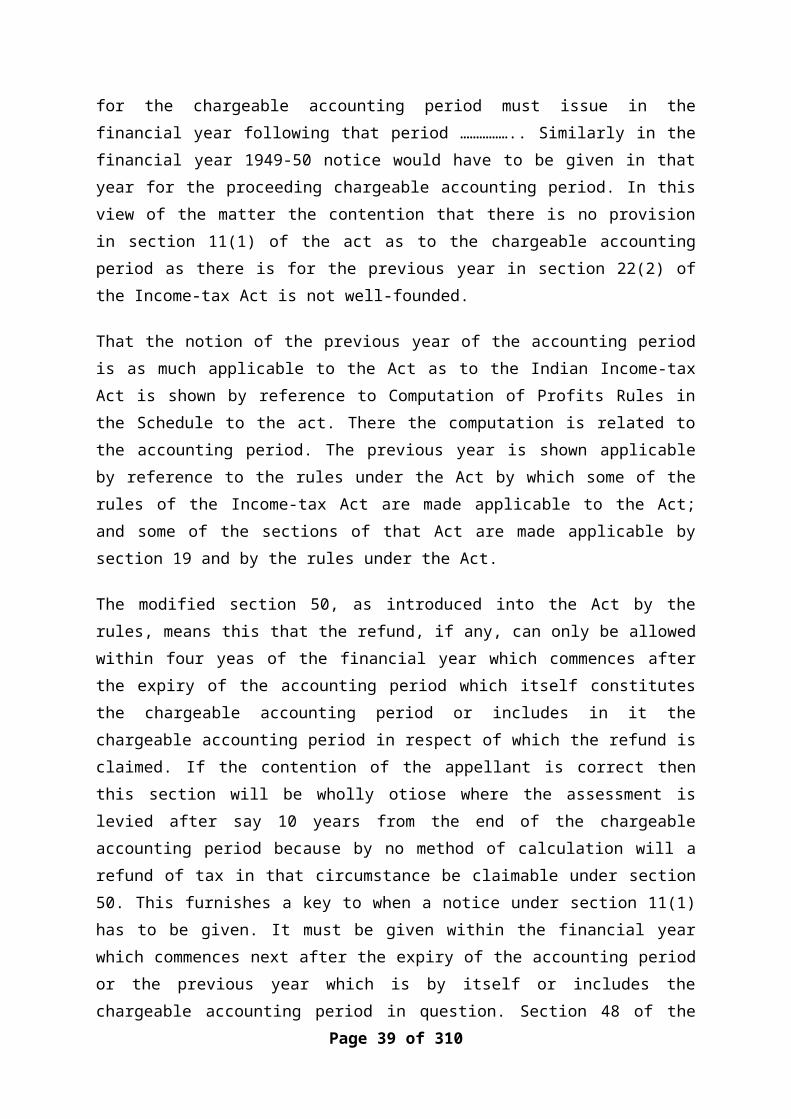

“As the tax under the Act is charged, levied and paid on the taxable profits of a chargeable accounting period buy assessment is in respect of the financial year in which the Act operates it is not an unreasonable inference that notice for the chargeable accounting period must issue in the financial year following that period …………….. Similarly in the financial year 1949-50 notice would have to be given in that year for the proceeding chargeable accounting period. In this view of the matter the contention that there is no provision in section 11(1) of the act as to the chargeable accounting period as there is for the previous year in section 22(2) of the Income-tax Act is not well-founded.

That the notion of the previous year of the accounting period is as much applicable to the Act as to the Indian Income-tax Act is shown by reference to Computation of Profits Rules in the Schedule to the act. There the computation is related to the accounting period. The previous year is shown applicable by reference to the rules under the Act by which some of the rules of the Income-tax Act are made applicable to the Act; and some of the sections of that Act are made applicable by section 19 and by the rules under the Act.

The modified section 50, as introduced into the Act by the rules, means this that the refund, if any, can only be allowed within four yeas of the financial year which commences after the expiry of the accounting period which itself constitutes the chargeable accounting period or includes in it the chargeable accounting period in respect of which the refund is claimed. If the contention of the appellant is correct then this section will be wholly otiose where the assessment is levied after say 10 years from the end of the chargeable accounting period because by no method of calculation will a refund of tax in that circumstance be claimable under section 50. This furnishes a key to when a notice under section 11(1) has to be given. It must be given within the financial year which commences next after the expiry of the accounting period or the previous year which is by itself or includes the chargeable

Page 26 of 201

accounting period in question. Section 48 of the Income-tax Act, as amended and applied to the Act, does not affect the operation of section 50 because the two sections have to be read together and the assessee must apply for the refund within the period specified by section 50: Adam Haji Dawoo & Co. Ltd. Commissions of Income-tax (1936) 4 ITR 100.”

(underlining ours)

32.1 Hidayatullah J. (as His Lordship then was) did not agree with the majority view as according to him, the provisions of the BPTA were different from the provisions of the Indian Income-tax Act, 1922 and therefore the latter Act could not be applied to the case Yet, in respect of the provisions of the Indian Income-tax Act, the learned Judge made relevant and pertained observations and noted the decision of the Privy Council in the case of CIT Vs. Ved Nath Singh 1940 8 ITR 222, to the following effect: @ page 331 of 40 ITR)

“We are of opinion that section 34 is applicable to cases in which either no assessment at all has been made upon the person who received the income, profits or gains liable to assessment, or where an assessment has been made in the course of the year, but some portion of the income, profits or gains of such assessee for some reason or other ha not been includes in the other of assessment, such income is income which has escaped assessment in the year, and falls within the ambit of section 34 of the Act.” (underlining ours)

His Lordship further observed as under @ page 331 of 40 ITR

“These cases arose before the amendments of 1939 and in those days there was no provision for a general notice such as is now issued under section 22(1). Even in those days, the return asked for the particulars of the total income during the previous year. Thus, as the end of the assessment year it was not possible to issue a notice for a back period beyond the previous year. By the force of section 22(2) it could b said at the end of any assessment year that in so far as he income of the corresponding previous year was concerned, it had escaped assessment. The logical result of this was that if no notice calling for a return under section 22 was issued within the assessment year, then section 34 was the only means to get at the tax. See Rajenderanath Mukerjee Vs. Commissioner of income-ax 1934 2 ITR 71. The scheme of the Indian Income-tax Act is entirely different, and by fixing a time limit for the issuance of a notice under section 22(2) makes it clear that in section 34 of the Indian Income-tax Act, the words “escaped assessment” ex facie covered all case of escaped assessment whether within or without a period assessment. The assessment there “escapes” when once the assessment year expires.”

Page 27 of 201

32.2 In the case of State of Assam & another Vs. D.C. Choudhury & Another 1970 76 ITDR 706 (SC) (supra), the assessee had sold their tea estate in Assam on July 9, 1953 and had submitted their returns in respect of the income form the business of cultivation, manufacturing and sale of black tea from January 1, 1948 to July 9, 1953. On January 25, 1961 a letter was received by the assesses from the Agricultural Income Tax Officer directing both the assesses to furnish returns of their agricultural income for the assessment years 1949-50 to 1953-54. Thereafter ex parte assessment were made for the assessment years 1951-52 to 1953-54. All these assessment were challenged by means of four write petitions before the High Court on the main ground that no notice under sec. 30 of the relevant Act was served in respect of the assessment years covered by the impugned orders. In the absence of a notice, the Agricultural Income-tax officer had no jurisdiction to make any assessment after the expiry of three years from the end of the financial year. The Division Bench of Assam High Court allowed all the write petitions. About the decision of the Hon’ble High Court, their Lordship of the Supreme Court have observed as under: @ pages 708 – 9 of 76 ITR )

“The learned Chief justice held that where no return had been filed pursuant to a general notice under section 19(1) the Agricultural Income-tax Office was bound to proceed under section 30 and issue a notice under section 19(2) of the Act within the prescribed period, namely, three years of the end of the financial year. He further held that there was no service of notice on the respondent in respect of the assessment years in question either under section 19(2) or section 30 of the Act. S.K. Dutta J. Came to the same conclusion as the learned Chief Justice but he relied on a judgement of the Calcutta High Court in Commissioner of Agricultural Income-tax Vs. Sultan Ali Gharami 20 ITR 432, in which a dissent had been expressed from the Bombay judgment in Harakchand Makanji & Co. Vs. Commissioner of income tax (16 ITR 119), on the question as to when proceedings relating to assessment could be regarded as having commenced. According to the learned judge if no return is made in response to a public notice under section 19(1) of the Act and no individual notice is served under section 19(2) there would be no pending proceedings and it would be a case of escaped assessment. But this would be so only after the expiry of the financial year. In other words after the publication of the notice under section 19(1) there would be no escapement of income till the end of the financial year. Once the financial year is over and no return has been made is response to a notice under section 19(1) and no individual notice had been served under section 19(2) a case would arise of “escaped assessment for the financial year”.

32.3 On appeal after considering the relevant statutory provisions, their Lordship held that the provisions of sections 19 & 20 of the Assam Agricultural Income-tax act were similar to sections 22 & 23 of the Income-tax Act, 1922. Particularly sub-section

Page 28 of 201

(1), (2) & (3) of sec. 19 of the Agricultural Income-tax Act were held to be identical with sub-sec. (1), (2) & (3) of sec. 22 of the old Act. Likewise, sub-sec. (1), (2) & (3) & (4) of sec. 20 of the Assam Agricultural Income-tax Act were held to correspond with sec. (1), (2) & (3) of sec. 23 of the old Act. Section 30 of the Agricultural Income-tax Act was found to be corresponding to section 34 of the old Act. Their Lordships referred to the decision in Harakchand Makanji & Co. Vs. CIT (16 ITR 119) and observed as under @ page 711 of 76 ITR: -

“…… that once a public notice is given under sub-section (1) of section 22 of the Income-tax Act, which is similar in terms to section 19(1) of the Act, the assessment proceedings should be deemed to have commenced and there is no obligation on the Income-tax Officer to serve a notice on an assessee individually as well. But in the same case it was said that “a notice under section 34 is only necessary if at the end of the assessment year no return has been made by the assessee and the income-tax authorities wish to proceed under section 22(2) by serving a notice individually. It may then the stated that as the assessment year had come to an end and as no return had been furnished an as the authorities wished to proceed under section 22(2) they should not do so without a notice under section 34.”

Their Lordship finally upheld the decision of the Hon’ble Assam High Court with the following observations at page 712 of 76 ITR:

“Keeping in view the above principles it must be held that in the absence of a return having been filed by the assesses in the present case pursuant to a general notice under section 19(1) of the act assessment could be made only after due notice under section 19(2) or by initiating proceedings under section 30 of the Act. Section 19(20 requires that an individual notice is to be served in the financial year. If no notice is served under that section proceedings under section 30 can be initiated by a notice in accordance with that section within three years of the end of that financial year.”

33. The basis scheme of “assessment” under the new Act continues to be the same. Instead of quoting large number of decisions on the proposition, we have deemed it convenient to rely on the latest 2004 commentary of the famous commentators Kanga, Palkhiwala and Vyas in law & Practice of Income-tax 9th edition. With reference to the provisions of sec. 147, the learned authors have observed as under at page 1826:

“nature and basis of Assessment under this Section

The proceedings taken under this section must be deemed to relate to the original assessment proceedings which commenced with the return filed under sec. 139(1)

Page 29 of 201

or the issue of a notice under sec. 139(2) (now deleted) Calling for return of income. If a particular income was not included in the total income of the relevant year of account, it can be brought to charge only by taking proceedings under this section and by including it in the total income of any other of account.” (sic)

33.1 It can further be seen from the foregoing discussion that even when not time limit was prescribed under sec. 22(2) of the old Act, yet courts held, having regard to the scheme of assessment, that the notice was to be served before the end of the assessment year, otherwise income would escape assessment at the end of the assessment year. What was implicit in the old Act was made explicit in the new Act. The judicial Interpretation was given statutory recognition and in section 139(2) of the new Act it was specifically provided that the notice was to be issued “before the end of the relevant assessment year”. The provisions of section 139(2) of new Act, prior to its omission w.e.f 1.4.1989. read as under:

“(2) In the case of any person who, in the Assessing Officer’s opinion, is assessable under this Act, whether on his own total income or on the total income of any other person during the previous year, the Assessing Officer may, before the end of the relevant assessment year, issue a notice to him and serve the same upon him requiring him to furnish, within thirty days from the date of service of the notice, a return of his income or the income of such other person during the previous year, in the prescribed form the verified in the prescribed manner and setting forth such other, particulars as may be prescribed”:

32.2 It the notice was served on the assessee and no return was filed, the proceedings could be said to be validly initiated and pending at the close of the assessment year and could be completed within the time and manner provided under the Income-tax Act. Such a case was not a case of “escaped assessment”. One could safely hold that till section 139(2) remained in the new Act, there was no change in the scheme of assessment noted above.

33.3. The new Act was amended with effect from 1st April, 1989 omitting sub-section (2) of section 139 and in its place, the ITO was authorized to call upon the assessee to furnish a return under clause (i) of section 142(1). The said sub-section provides as under:

“142(1) For the purpose of making an assessment under this Act, the Assessing Officer may serve on any person who has made a return under section 139 (or in whose case the time allowed under sub-section (1) of that section for furnishing the return has expired) a notice requiring him, on a date to be therein specified,

Page 30 of 201

(i) Where such person has not made a return within the time allowed under sub-section (10 of section 139, to furnish a return of his income or the income of any other person in respect of which he is assessable under this act, in the prescribed from and verified in the prescribed manner and setting forth such other particulars as may be prescribed, or……..”

[The words “within the time allowed under sub-section (1) of section 139” in the above clause wee substituted for the words “before the end of the relevant assessment year” by the Finance Act, 1990 with effect from 1.4.1990.]

33.4. The section as inserted with effect from 1.4.1989 particularly the words “before the end of the relevant assessment year” were not in line with the basis scheme of the Act as it authorized the Income-tax officer to call for a return as per clause (i) after the “end of the assessment Year”., As per the settled law, the scheme of the Act, as noted above, was that income would be treated as having “escaped assessment”, if neither the return was field under sub-section (1) nor any notice under sub-section (2) of section 139 was issued before the end of the assessment year. In the cases of such escaped assessment, the AO was, required to issue notice under section 148 of the Income-tax Act. However, the clause as inserted also authorized the AO to call for a return after the close of the assessment year.

33.5. The provision as inserted was found to be not workable and problematic. Accordingly the changes in the said provisions was made with effect from 1.4.1990 just one year after its insertion. In the change provisions, there is not time limit for issuing notice except that it has to be after the time provided in sub-section (1) of sec. 139 is over. The AO cannot issued notice and call for the return as he could do under sc. 139(2) or section 22(2) of the old Act even before the expiry of time under sub-section (1) of section 139. In other words, the starting point empowering the AO to issue notice calling for the return is specifically indicated. This is the difference. Otherwise, the amended section 142(i) is similar to the provisions of section 22(20 of the Old Act which have been considered in great details by he Apex Court in the case of Narsee Nagsee & Co. (supra) as also in the case of D.C Choudhury (supra). Once can therefore safely hold that a notice calling for a return under the above clause cannot be issued after “the end of the assessment year”. The reasoning given by the Supreme Court in the above two decisions and their interpretation of the scheme of assessment under the Income-tax Act are fully applicable to the provisions and the situation under consideration. No such change in the new Act has been brought t our notice after 1st of April, 1989 which can lead us to infer that the basis scheme of “assessment” and “escapement” of income considered by their Lordships stand modified. As noted above section 139(2) specifically recognized that notice calling for a return is to be issued ‘before the and of the relevant assessment

Page 31 of 201

year”. With the deletion of section 139(2) and amendment of sec. 142(1)(i), we are relegated to the position similar to once considered by their Lordships in above decision. Even under other Acts, where no period of limitation was prescribed for issuing the notice calling for the period of limitation was prescribed for issuing the notice calling for the return of income, the said notice was held to be required to be issued before the end of the assessment year having regard to similar scheme of assessment. The authoritative pronouncements which held so are equally applicable to the provisions of the Income tax Act under consideration. Therefore, we are inclined to accept the contention of the assesses that a period of limitation to issue a notice calling for the return under sec. 142(1)(i) is inbuilt in the scheme of the act. As per the said scheme, the notice has to be issued after the end of period in section 139(1) and before the end of the relevant assessment year.

34. We now turn to examine Explanation 2 to section 147 which is as under: -

Explanation 2 – For the purpose of this section, the following shall also be deemed to be cases where income chargeable to tax has escaped assessment, namely:

(a) where no return of income has been furnished by the assessee although his total income or the total income of any other person in respect of which he is assessable under this Act during the previous year exceeded the maximum amount which is not chargeable to income-tax;

(b) where a return of income has been furnished by the assessee but no assessment has been made and it is noticed by the Assessing officer that the assessee has understated the income or has claimed excessive loss, deduction, allowance or relief in the return;

(c) where an assessment has been made, but-

(i) income chargeable to tax has been under-assessed; or

(ii) such income has been assessed at too low a rate; or

(iii) such income has been made the subject of excessive relief under this Act; or

(iv) excessive loss or depreciation allowance or any other allowance under this Act has been computed.”

34.1. Explanation 2 to section 147 would not make any differences as the said Explanation starts with the words “the following shall also be deemed to be cases where income chargeable to tax has escaped assessment.” The word “ALSO” in the

Page 32 of 201