Embed Size (px)

Citation preview

MOODYS.COM

4 FEBRUARY 2016

NEWS & ANALYSIS Corporates 2 » Abbott Takes on Significant Debt with Alere Purchase » Axiata Group Berhad and Bharti Airtel Will Merge Bangladesh

Subsidiaries, a Credit Positive » XL Axiata's Proposed Rights Issue Will Reduce Leverage and

Foreign Exchange Risk » Toyota to Acquire Full Stake in Subsidiary Daihatsu, a

Credit Positive

Infrastructure 9 » Court Decision on OAS Reorganization Plan Is Credit Positive

for Invepar

Banks 10 » TCF National Bank’s High Auto Loan Growth Is Credit Negative » Brazil Announces New Measures to Stimulate Loan Growth, a

Credit Negative for Public Banks » Kazakhstan Banks' Mounting Losses Further Weaken Capital » Azerbaijani Banks Benefit from Full Deposit Insurance and Tax

Moratorium for Retail Depositors » Bank of Japan's Negative Interest Rate Policy Is Credit Negative

for Banks

Sovereigns 18 » Uruguay Reports a Wider-than-Expected Deficit » South Africa Continues to Predict Lower Growth » Pakistan's New Monetary Policy Framework Will Improve

Policy Transparency and Transmission, a Credit Positive

Sub-sovereigns 24 » Chinese Regional and Local Government Bond Program

Continues, a Credit Positive

US Public Finance 26 » State Housing Finance Agencies Will Benefit from FHA

Mortgage Insurance Rate Cut

RECENTLY IN CREDIT OUTLOOK

» Articles in Last Monday’s Credit Outlook 28 » Go to Last Monday’s Credit Outlook

Click here for Weekly Market Outlook, our sister publication containing Moody’s Analytics’ review of market activity, financial predictions, and the dates of upcoming economic releases.

NEWS & ANALYSIS Credit implications of current events

2 MOODY’S CREDIT OUTLOOK 4 FEBRUARY 2016

Corporates

Abbott Takes on Significant Debt with Alere Purchase On Monday, Abbott Laboratories (A2 review for downgrade) announced plans to buy diagnostic testing company Alere Inc. (B2 review for upgrade) for $8.4 billion, including $2.6 billion of Alere’s existing debt. The acquisition is credit negative for Abbott because it is taking on significant debt for a non-transformative transaction. Following the deal’s announcement, we placed Abbott’s ratings on review for downgrade and Alere’s rating on review for upgrade.

We expect Abbott to fully fund the acquisition with debt, which will double its gross debt to about $16.8 billion from $8.4 billion as of 30 September 2015. Abbott’s pro forma financial leverage at closing will increase to around 3.9x debt/EBITDA from about 2.2x, excluding EBITDA from the branded generic drug business that Abbott has divested to Mylan N.V. (Baa3 stable).

Abbott’s leverage will remain elevated over the next few years. The company generates high levels of profits and cash outside the US and is unlikely to willingly suffer the tax consequences of repatriating that cash to fund all of its US needs. Therefore, we expect that Abbott will choose to borrow to help fund dividends, share buybacks and mergers and acquisitions.

Abbott’s financial policies have become increasingly shareholder-friendly since spinning off AbbVie Inc. (Baa1 negative) in 2013. One year after the spinoff, Abbott increased its dividend by about 60% and began to increase share buybacks. We also expect that Abbott will continue to pursue acquisitions, most likely seeking targets in the medical device sector.

Alere will only increase Abbott’s sales and EBITDA by about 12% and the acquisition will not result in diversification outside of its current business segments. Alere has faced challenges in growing its business because of product recalls, reimbursement pressures and the negative effects of foreign exchange. However, the deal will improve Abbott’s position in diagnostics, particularly in point-of-care testing, which is performed near the patient and can show results within a short period of time. Abbott expects to realize pre-tax synergies of about $500 million by 2019. Additionally, more than 50% of Alere’s sales are in the US, which will help balance Abbott’s current exposure to emerging markets.

Abbott Park, Illinois-based Abbott is a leading manufacturer of a diverse range of medical products, including diagnostics, devices, nutritionals and generic drugs.

Diana Lee Vice President - Senior Credit Officer +1.212.553.4747 [email protected]

This publication does not announce a credit rating action. For any credit ratings referenced in this publication, please see the ratings tab on the issuer/entity page on www.moodys.com for the most updated credit rating action information and rating history.

NEWS & ANALYSIS Credit implications of current events

3 MOODY’S CREDIT OUTLOOK 4 FEBRUARY 2016

Axiata Group Berhad and Bharti Airtel Will Merge Bangladesh Subsidiaries, a Credit Positive On 28 January, Bharti Airtel Limited (Baa3 stable) and Axiata Group Berhad (Baa2 stable) announced that they had agreed to merge their telecommunication subsidiaries in Bangladesh: Airtel Bangladesh Limited (Airtel, unrated), which is wholly owned by Bharti Airtel, and Robi Axiata Limited (unrated), which is 91.59%-owned by Malaysia-based Axiata and 8.41%-owned by Japan’s NTT Docomo, Inc. (Aa3 stable). The merger, which requires regulatory approval, is credit positive for both Bharti Airtel and Axiata.

The new entity, Robi-Airtel, will have a stronger market position than either Robi or Airtel has on a standalone basis in Bangladesh’s highly competitive mobile telecommunications market. Also, the merger will ultimately enhance network quality and coverage and allow operational synergies without adversely affecting the credit quality of either Bharti Airtel or Axiata.

The merger, which the companies expect to conclude in the first half of the year, will be structured via issuance of ordinary shares, whereby Robi will issue new ordinary shares to Bharti Singapore, a wholly owned subsidiary of Bharti Airtel. Upon completion of the agreed merger, the companies expect that Axiata will own 58.7% of Robi-Airtel, Bharti Airtel 25% and NTT 6.3%.

As of year-end 2015, as shown in Exhibit 1, Robi-Airtel’s market share would have been around 29% with 39 million subscribers, jumping ahead of Banglalink Digital Communications Limited’s (Ba3 stable) 25% market share, making it the second-largest operator behind Grameenphone Ltd. (unrated), which has a 42% market share and 57 million subscribers. The mobile market in Bangladesh is extremely competitive with six operators currently. Banglalink’s market share fell to 25% at December 2015 from its peak of 28% in December 2010, owing to increased competition from Robi and Airtel. Although the gain in market share is credit positive for Robi-Airtel, it is credit negative for Banglalink.

EXHIBIT 1

Bangladesh Mobile Telecommunication Operators’ Share of Subscribers as of Year-End 2015

Note: Total Subscriber base was 134 million as of December 2015. Source: Bangladesh Telecommunications Regulatory Commission

The merged entity will also benefit from better service quality and enhanced network coverage with a combination of Airtel’s and Robi’s telecommunications networks. Notably, the transaction will make Robi-Airtel the largest spectrum holder in both 900-megahertz and 1800-megahertz bands with 12 megahertz and 17 megahertz of spectrum, respectively (see Exhibit 2).

57

39

3328

11

41

0

10

20

30

40

50

60

Grameen Phone42%

Robi-Airtel 29% Banglalink 25% Robi 21% Airtel 8% Teletalk 3% Citycell 1%

Mill

ions

of S

ubsc

riber

s

Market Share

Carole Herve Associate Analyst +852.3758.1505 [email protected]

Annalisa Di Chiara Vice President - Senior Credit Officer +852.3758.1537 [email protected]

NEWS & ANALYSIS Credit implications of current events

4 MOODY’S CREDIT OUTLOOK 4 FEBRUARY 2016

EXHIBIT 2

Bangladesh Mobile Operators’ Spectrum Holdings as of December 2015 Robi-Airtel will be the largest spectrum holder in both the 900-megahertz and 1800-megahertz bands in Bangladesh.

Source: Bangladesh Telecommunications Regulatory Commission

The improved service offering and network coverage through the increased spectrum holdings will increase Robi-Airtel’s opportunities for revenue growth in mobile data services.

We believe there are considerable growth opportunities in Bangladesh since mobile data services penetration and average revenue per user are lower than in other emerging Asian countries at around 7% and $1.90 per month, respectively.

We do not expect Bharti Airtel’s and Axiata’s metrics to be significantly affected by the merger because the contribution from their respective Bangladeshi subsidiaries is relatively small. For the nine months ended September 2015, Robi contributed 13% of Axiata’s total revenues and Airtel contributed less than 2% of Bharti Airtel’s total revenues for the nine months that ended 31 December 2015. In addition, there will be no debt funding associated with the merger.

Although the companies expect cost synergies and lower operating expenses relating to network maintenance costs and selling, as well as lower general and administrative expenses, the benefits are likely to improve profitability over the next two to three years, rather than immediately.

97

12

5

7

5 5

15

17

10

7

10 1010 10

5 5 5

10

0

2

4

6

8

10

12

14

16

18

20

Grameenphone Robi - Airtel Banglalink Robi Airtel Teletalk Citycell

MH

z

850MHz 900MHz 1800MHz 2100MHz

NEWS & ANALYSIS Credit implications of current events

5 MOODY’S CREDIT OUTLOOK 4 FEBRUARY 2016

XL Axiata’s Proposed Rights Issue Will Reduce Leverage and Foreign Exchange Risk On Monday, XL Axiata Tbk (Ba1 stable) announced its intention to offer a rights issue, pending shareholder approval. The net proceeds will be used to repay a $500 million shareholder loan from its parent company, Axiata Group Berhad (Baa2 stable). The rights issue, when completed in the first half of this year, will be credit positive for XL Axiata because it will allow the Indonesia-based mobile phone operator to reduce its leverage by $500 million. XL Axiata will prepay its three-year shareholder loan that matures in March 2017, and which was used to partially fund its acquisition of Axis Telecom (unrated) in April 2014.

Pro forma for the rights issue, we expect XL Axiata’s adjusted leverage to decline to 2.7x-2.8x from 3.3x as of December 2015 (see Exhibit 1).

EXHIBIT 1

XL Axiata’s Repayment of Shareholder Loan Will Substantially Improve Leverage

Sources: XL Axiata, Moody’s Financial Metrics and Moody’s Investors Service estimates

In January, XL Axiata also announced its intention to sell the second tranche of tower assets through a tender process, and to use the sales proceeds to pare down debt. The company expects the transaction to close by the end of the first quarter. Assuming similar valuation and pricing as its tower sale transaction in 2014, we expect the company to raise $250-$300 million. Even after adjusting for capitalized leases, we expect the transaction to reduce leverage to 2.5x-2.6x from 3.3x as of December 2015.

Axiata has expressed its intention to fully subscribe for its pro-rata rights entitlement under the rights issue, which equals 66.4% of the total issuance. The effective conversion of a shareholder loan to equity further demonstrates Axiata’s commitment to support XL Axiata, which is Axiata’s largest non-domestic subsidiary and contributes about 34% of its consolidated reported revenues and EBITDA. XL Axiata’s rating incorporates expected extraordinary support from Axiata, which gives XL Axiata’s rating a one-notch uplift to Ba1. We expect the company’s financial advisors for the rights issue, Credit Suisse and Mandiri Sekuritas, to fully underwrite the remainder of the rights issue.

The early repayment of the shareholder loan also eliminates residual foreign exchange exposure at XL Axiata. The shareholder loan is currently the only unhedged debt instrument in XL Axiata’s overall debt mix, and equals about 24% of total debt (see Exhibit 2). Because of the rupiah depreciation against the US dollar, the principal on its $500 million shareholder loan increased 13% to IDR6.9 trillion as of December 2015 from IDR6.1 trillion as of June 2014.

0.0x

0.5x

1.0x

1.5x

2.0x

2.5x

3.0x

3.5x

4.0x

0

5

10

15

20

25

30

35

40

45

50

2010 2011 2012 2013 2014 2015 2015 Pro Formafor Shareholder

Loan Repayment

IDR

Trill

ions

Gross Adjusted Debt - left axis Adjusted Debt to EBITDA - right axis

Nidhi Dhruv Assistant Vice President - Analyst +65.6398.8315 [email protected]

Maisam Hasnain Associate Analyst +852.3758.1420 [email protected]

NEWS & ANALYSIS Credit implications of current events

6 MOODY’S CREDIT OUTLOOK 4 FEBRUARY 2016

EXHIBIT 2

Repayment of Shareholder Loan Will Diminish XL Axiata’s Forex Exposure

Sources: XL Axiata and Moody’s Investors Service estimates

The principal on XL Axiata’s external US dollar debt of $438 million has been hedged to maturity. However, $300 million of this debt is hedged using call spread options, which only cover rupiah depreciation up to a predetermined level of IDR14,580-IDR14,600. XL Axiata would be exposed to foreign exchange rate risk if the rupiah depreciated beyond this point.

For Axiata, the transaction is credit neutral. Although it will receive proceeds of around $500 million from XL Axiata for the repayment of the shareholder loan, Axiata has said that it intends to fully subscribe to its pro-rata rights entitlement, or 66.4%, under XL Axiata’s proposed rights issue. As a result, we expect the net cash effect of this transaction to have no material effect on Axiata’s credit metrics including its leverage.

56% 73%

24%

21%

27%

0

5

10

15

20

25

30

Dec-2015 Dec-2015 Pro Forma for Shareholder Loan Repayment

IDR

Trill

ions

IDR Debt Including Finance Lease USD Unhedged Debt USD Hedged Debt

NEWS & ANALYSIS Credit implications of current events

7 MOODY’S CREDIT OUTLOOK 4 FEBRUARY 2016

Toyota to Acquire Full Stake in Subsidiary Daihatsu, a Credit Positive Last Friday, Toyota Motor Corporation (Aa3 stable) announced that it would acquire the remaining 48.81% stake that it does not own in Daihatsu Motor Co., Ltd. (unrated), a consolidated subsidiary and the largest mini-vehicle manufacturer in Japan.

The full consolidation of Daihatsu is credit positive because it will allow both Toyota and Daihatsu to focus on their core strengths and will promote greater operational efficiency in product and technological development. Furthermore, it will allow the two companies to more efficiently utilize their business infrastructure globally including sales and distribution. Currently, each brand mainly operates by itself with limited support from the other. The forthcoming organizational integration will allow Daihatsu to take the initiative in small car development for both Toyota and itself.

The transaction will help sustain and enhance Toyota’s global competitiveness in small cars. The Japanese domestic market is already mature and Japan’s light vehicle tax hike in April 2015 has lowered demand for mini-vehicles, whose sales dropped 17% in 2015.

Despite Daihatsu’s position as the top-selling manufacturer of mini-vehicles for nine consecutive fiscal years (ending 31 March), and a 31.6% market share as of the end of fiscal 2015, competition remains strong. To survive in this type of competitive market, the efficient use of Toyota’s annual ¥1 trillion of research and development expenses, which has been trending at 3.5%-4% of revenue, is more important than previously.

Daihatsu will be able to focus on implementing cost savings and developing fuel-efficient technologies, which are at the heart of product competitiveness in the small car segment, further optimizing research and development for the company. Together with the effective utilization of Toyota’s sales expertise and infrastructure, we believe these operational advantages will support Daihatsu in its efforts to remain one of the top players in the domestic market, including in the area of technology.

Furthermore, we expect the announced organizational integration to promote global expansion for both companies, especially in the growing, but highly competitive, emerging markets (see exhibit). These emerging markets are likely to drive auto demand, and affordable and fuel-efficient vehicles play an important role because these countries have low GDP per capita.

EXHIBIT 1

Top 10 Countries by Compound Annual Growth Rate of Unit Car Sales Volume, 2005-14 Growth will come from emerging markets.

Note: The exhibit excludes countries with high growth rates from small bases. Source: International Organization of Motor Vehicle Manufacturers

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

CHINA INDONESIA INDIA BRAZIL IRAN SAUDIARABIA

SOUTHKOREA

RUSSIA THAILAND CANADA

Taishi Yamazaki Associate Analyst +81.3.5408.4032 [email protected]

Motoki Yanase Vice President - Senior Analyst +81.3.5408.4154 [email protected]

NEWS & ANALYSIS Credit implications of current events

8 MOODY’S CREDIT OUTLOOK 4 FEBRUARY 2016

Sales of small cars still dominate in emerging markets. For example, 60%-70% of sales in India are micro, mini and compact cars. Despite Toyota’s strong presence in the emerging markets, it lags its peers in countries such as India, where it has a 5% market share, and Brazil where its market share is around 6%. Moreover, Daihatsu has a significant presence only in Indonesia and Malaysia, and therefore has the opportunity to expand beyond these countries.

An efficient use of Toyota’s operational base and Daihatsu’s lead in transforming product development processes that have been cultivated in the domestic market can help boost its presence in the emerging markets. Daihatsu can quickly push business development.

NEWS & ANALYSIS Credit implications of current events

9 MOODY’S CREDIT OUTLOOK 4 FEBRUARY 2016

Infrastructure

Court Decision on OAS Reorganization Plan Is Credit Positive for Invepar Last Friday, Investimentos e Participações em Infraestrutura S.A. - INVEPAR (Ba3/A2.br stable) announced that the judge of the First Bankruptcy Court of the Judicial District of São Paulo ratified the court-supervised reorganization plan filed by OAS Infraestrutura S.A. (unrated) and Construtora OAS S.A. (unrated), which are wholly owned subsidiaries of the engineering and construction group OAS, a credit positive for INVEPAR. The OAS Group currently owns 24.44% of INVEPAR.

The court-supervised reorganization plan, which OAS’ creditors approved on 17 December, clears the way for the sale of OAS’ stake in INVEPAR for a minimum price of BRL1.35 billion, via a judicial sale. Given the size and importance of INVEPAR’s portfolio of transportation infrastructure investments, we expect that the court’s decision will help attract investors with the financial strength, wherewithal and technical and operational expertise required to manage INVEPAR’s investments, as well as to help INVEPAR bid for new concessions.

Brazil’s economic slowdown, combined with the judicial and administrative proceedings involving corruption allegations at Petroleo Brasileiro S.A. - Petrobras (Ba3 review for downgrade), led to a sharp deterioration of funding available for the Brazilian construction industry since 2014. As a result, OAS has been challenged with its limited liquidity to address large debt amortization payments and concurrently finance its working capital requirements. As of 30 September 2014 (the last available information), OAS reported consolidated debt of BRL8.8 billion. OAS’ filing for judicial recovery under the Brazilian Bankruptcy and Reorganization Law was approved by the court on 1 April 2015.

OAS is the shareholder that has provided the technical expertise for a large number of INVEPAR’s projects, having led the engineering and construction work in some of INVEPAR’s most high-profile infrastructure projects in Brazil and abroad. These include the Sao Paulo International Airport of Guarulhos (unrated), the busiest airport in Latin America; Concessionaria Auto Raposo Tavares S.A. (Ba3 stable), a toll road in the State of Sao Paulo; and Linea Amarilla S.A.C. – LAMSAC (unrated), an urban toll road in Lima, Peru. Despite OAS’ financial challenges, INVEPAR’s projects such as the Guarulhos Airport, have been completed, or are nearing construction completion, such as the Sao Paulo and Lima toll roads, according to the requirements of their respective concession contracts.

Alexandre De Almeida Leite Vice President - Senior Credit Officer +55.11.3043.7353 [email protected]

NEWS & ANALYSIS Credit implications of current events

10 MOODY’S CREDIT OUTLOOK 4 FEBRUARY 2016

Banks

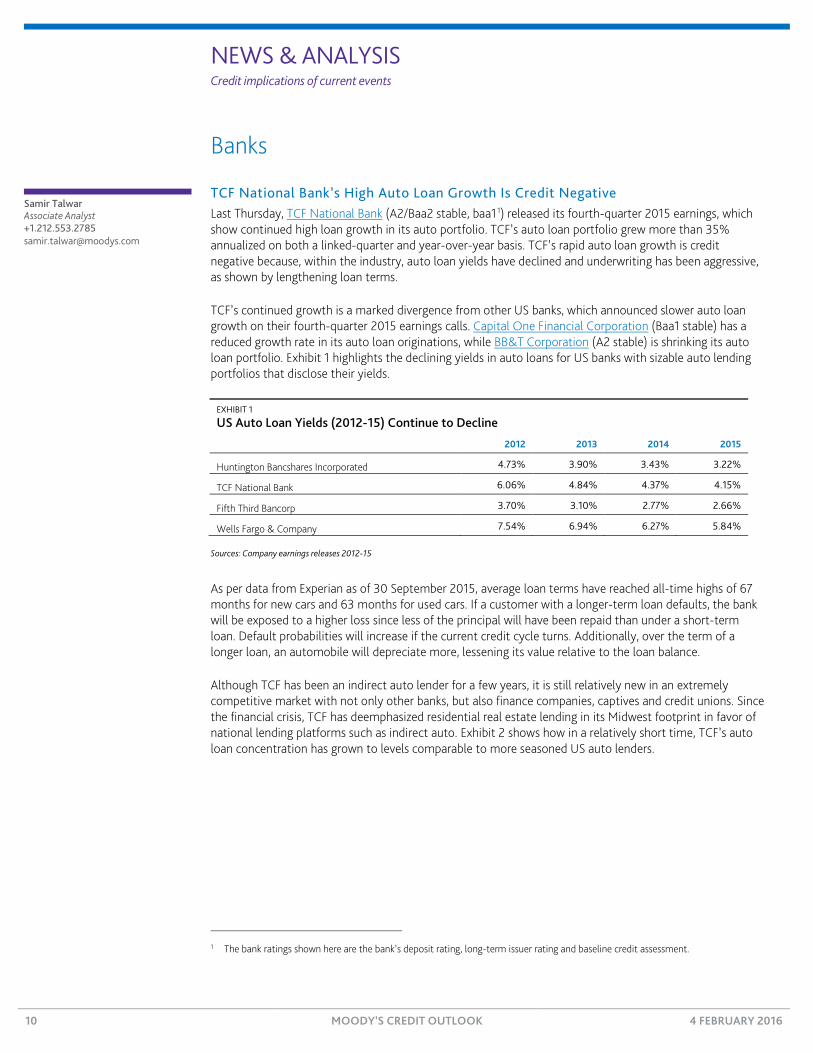

TCF National Bank’s High Auto Loan Growth Is Credit Negative Last Thursday, TCF National Bank (A2/Baa2 stable, baa11) released its fourth-quarter 2015 earnings, which show continued high loan growth in its auto portfolio. TCF’s auto loan portfolio grew more than 35% annualized on both a linked-quarter and year-over-year basis. TCF’s rapid auto loan growth is credit negative because, within the industry, auto loan yields have declined and underwriting has been aggressive, as shown by lengthening loan terms.

TCF’s continued growth is a marked divergence from other US banks, which announced slower auto loan growth on their fourth-quarter 2015 earnings calls. Capital One Financial Corporation (Baa1 stable) has a reduced growth rate in its auto loan originations, while BB&T Corporation (A2 stable) is shrinking its auto loan portfolio. Exhibit 1 highlights the declining yields in auto loans for US banks with sizable auto lending portfolios that disclose their yields.

EXHIBIT 1

US Auto Loan Yields (2012-15) Continue to Decline

2012 2013 2014 2015

Huntington Bancshares Incorporated 4.73% 3.90% 3.43% 3.22%

TCF National Bank 6.06% 4.84% 4.37% 4.15%

Fifth Third Bancorp 3.70% 3.10% 2.77% 2.66%

Wells Fargo & Company 7.54% 6.94% 6.27% 5.84%

Sources: Company earnings releases 2012-15

As per data from Experian as of 30 September 2015, average loan terms have reached all-time highs of 67 months for new cars and 63 months for used cars. If a customer with a longer-term loan defaults, the bank will be exposed to a higher loss since less of the principal will have been repaid than under a short-term loan. Default probabilities will increase if the current credit cycle turns. Additionally, over the term of a longer loan, an automobile will depreciate more, lessening its value relative to the loan balance.

Although TCF has been an indirect auto lender for a few years, it is still relatively new in an extremely competitive market with not only other banks, but also finance companies, captives and credit unions. Since the financial crisis, TCF has deemphasized residential real estate lending in its Midwest footprint in favor of national lending platforms such as indirect auto. Exhibit 2 shows how in a relatively short time, TCF’s auto loan concentration has grown to levels comparable to more seasoned US auto lenders.

1 The bank ratings shown here are the bank’s deposit rating, long-term issuer rating and baseline credit assessment.

Samir Talwar Associate Analyst +1.212.553.2785 [email protected]

NEWS & ANALYSIS Credit implications of current events

11 MOODY’S CREDIT OUTLOOK 4 FEBRUARY 2016

EXHIBIT 2

Auto Loans Were a Sizable Portion of TCF National’s Loan Portfolio as of 30 September 2015

Source: Federal Reserve FR-Y9C

The fourth-quarter announcements are not the first indication of an overheated auto lending market. Whereas many banks with auto portfolios slowed the growth of their loan books as a result of the overheated market, TCF seems to have made the opposite decision. In March 2015, Wells Fargo & Company (A2 stable), a seasoned indirect auto lender, announced a ceiling on its subprime auto lending. Other banks followed throughout 2015. Fifth Third Bankcorp (Baa1 stable), a high quality, prime auto lender, has tempered its pace of auto loan growth for several quarters now. Bank of Montreal (Aa3/Aa3 negative, a22) acquired General Electric Capital Corporation’s (A1) transportation finance business in the US and Canada, focused on commercial trucks. This transaction facilitates a reduction of its US indirect auto book, which is challenged by low yields and, we believe, is not particularly profitable for its US franchise, BMO Financial Corporation (A3 stable). Exhibit 3 shows the pace of growth of TCF’s auto loan book compared to some of its regional peers.

EXHIBIT 3

TCF’s Auto Portfolio Growth Rate versus Regional Peers

Source: Federal Reserve FR-Y9C

2 The ratings shown in this report are Bank of Montreal’s deposit rating, senior unsecured debt rating, and baseline credit assessment.

19.2%18.4%

14.7%

12.0% 11.5%

8.5%

6.4%

0%

3%

6%

9%

12%

15%

18%

21%

Capital OneFinancial

Corporation

HuntingtonBancshares

Incorporated

TCF National Bank Fifth Third Bancorp BMO FinancialCorp

BB&T Corporation Wells Fargo &Company

-20%

0%

20%

40%

60%

80%

100%

120%

140%

TCF National Bank Capital OneFinancial

Corporation

Wells Fargo &Company

HuntingtonBancshares

Incorporated

BB&T Corporation Fifth Third Bancorp BMO FinancialCorportaion

2013 2014 3Q2015

NEWS & ANALYSIS Credit implications of current events

12 MOODY’S CREDIT OUTLOOK 4 FEBRUARY 2016

Brazil Announces New Measures to Stimulate Loan Growth, a Credit Negative for Public Banks Last Thursday, the Government of Brazil (Baa3 review for downgrade) announced new measures to stimulate economic activity by using public banks to increase the supply of credit. The initiatives are credit negative because they will encourage public lenders to take on more asset risks while Brazil’s economic recession, high inflation and rising unemployment are already eroding borrowers’ repayment capacity. It will also put further strains on the banks’ capital positions, which have declined as a result of rapid loan growth.

These latest initiatives will have the greatest effect on Banco Nacional Desenvolvimiento Economico e Social (BNDES, Baa3/Baa3 review for downgrade3), which will be involved in the expansion of three credit programs. First, BNDES will resume offering working capital facilities to small and midsize enterprises at below-market rates. In addition, the bank will extend the maximum maturity of certain export financing facilities to 30 months from the current 24 months, and it will give companies the option to refinance any outstanding loans used to finance machinery and equipment that are maturing this year and in 2017.

The government also aims to use BRL10 billion ($2.5 billion) in resources from the Fundo de Garantia por Tempo de Servico (FGTS), a workers’ unemployment and compensation fund, to increase the supply of mortgage loans. Under the plan, FGTS will buy certificates of mortgage receivables from banks to give them cash that they can use to originate more home loans. This will likely have the greatest effect on Caixa Economica Federal (Caixa, Baa3/Baa3 review for downgrade, ba3), which had to limit its mortgage loan growth over the past year because of funding constraints. These constraints were the result of Caixa having fully used its savings deposits, the main source of mortgage funding.

The government also unveiled a proposal to allow private-sector workers to use their resources at FGTS as collateral for payroll loans as a means to boost the supply of household credit. Although this initiative still requires congressional approval, it has the potential to boost payroll lending in the private sector, which currently constitutes a relatively small 7% of overall payroll lending in Brazil. Banks have been reluctant to offer more payroll loans to private-sector workers because they are more vulnerable to changes in labor market conditions than public-sector employees, which is especially relevant given the current economic downturn.

Separately, the National Monetary Council also announced a BRL2 billion increase in public banks’ mandatory lending quotas for agriculture loans. Under the new rules, every bank that is owned by the federal government or by one of Brazil’s states will have to lend 34% of all demand deposits obtained from its controlling shareholder and from state-owned entities to the agriculture sector.

Over the past three years, public banks’ loan books have grown at a compounded average growth rate of 16.6%, which equaled 2.1x Brazil’s nominal GDP. Although growth has slowed, the banks continued to grow at a pace of 10.9% in 2015, even as real GDP is expected to have contracted and nominal GDP grew by 4.3% (as per the central bank’s latest estimates). Although the banks benefited from a capital injection in 2014, overall capital consumption has outpaced retained earnings growth, which has led to a decline in their capitalization. For example, BNDES’ common equity Tier 1 (CET1) ratio fell 80 basis points to 9.8% in the first nine months of 2015, and at Caixa, the CET1 ratio dropped 190 basis points to 10.1%. These banks’ capital ratios remain above the regulatory minimum, but the plan to spur continued rapid loan growth at these banks will likely lead to further declines in capitalization.

3 The bank ratings shown in this report are the bank’s deposit rating, senior unsecured debt rating and baseline credit assessment

(where available).

Alcir Freitas Vice President - Senior Analyst +55.11.3043.7308 [email protected]

NEWS & ANALYSIS Credit implications of current events

13 MOODY’S CREDIT OUTLOOK 4 FEBRUARY 2016

Kazakhstan Banks’ Mounting Losses Further Weaken Capital Last Friday, the National Bank of Kazakhstan (NBK) stated that 13 of 35 banks (37%) reported operating losses. Losses will further impair many banks’ capital levels, already under significant strain owing to a recent steep increase in banks’ risk-weighted assets following a sharp local currency depreciation, a credit negative.

Banks’ profitability is starting to deteriorate (see Exhibit 1) because of weaker oil prices, a decelerating economy and an almost 50% depreciation of Kazakhstan’s currency, the tenge, since August 2015. An accelerated build-up in nonperforming loans (NPLs) and higher funding costs are driving banks’ profitability lower. The depreciated tenge makes it more difficult for borrowers to stay current on foreign-currency-denominated loans, which account for 34% of banks’ gross loans. It will also fuel higher inflation, which rose to 14.4% in January 2016 from 7.4% in 2014 and 4.8% in 2013, eroding households’ real disposable income and impairing banks’ retail and small and midsize enterprise portfolios denominated in the tenge. Funding costs are also growing given the combination of decreased confidence in the tenge and banks’ almost full reliance on deposits. Some banks have had to compensate depositors for not converting their tenge savings into foreign currencies, in accordance with a presidential decree, and this has also translated into losses.

EXHIBIT 1

Number of Kazakhstan Banks Reporting Monthly Decline in Shareholder Equity

Source: The National Bank of Kazakhstan

House Construction and Savings Bank of Kazakhstan JSC (Baa3 stable, ba24), Kaspi Bank JSC (B1/B2 negative, b2) and Delta Bank (unrated) reported the most significant decline in shareholders’ equity in December 2015.

The increased risk of operating losses will likely exacerbate the recent decline in banks’ capital adequacy. As a result of the currency depreciation since August 2015 and the corresponding increase in lenders’ risk-weighted assets, the system’s aggregate regulatory Tier 1 ratio declined to 13.5% as of 1 December 2015 from 15% as of 30 June 2015 (see Exhibit 2), with many banks reporting a decline in their common equity Tier 1 and Tier 1 ratios of more than 200 basis points.

4 The ratings shown are the bank’s deposit rating, senior unsecured debt rating (where available) and baseline credit assessment.

45

4

7 7

13

2

4

6

8

10

12

14

Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15

Semyon Isakov Assistant Vice President - Analyst +7.495.228.6061 [email protected]

NEWS & ANALYSIS Credit implications of current events

14 MOODY’S CREDIT OUTLOOK 4 FEBRUARY 2016

EXHIBIT 2

Kazakhstan Banks’ Regulatory Common Equity Tier 1 and Tier 1 Ratios

Source: The National Bank of Kazakhstan

0%

2%

4%

6%

8%

10%

12%

14%

16%

1-Jul-15 1-Aug-15 1-Sep-15 1-Oct-15 1-Nov-15 1-Dec-15

CET 1 Ratio (k1) Tier 1 Ratio (k1-2)

NEWS & ANALYSIS Credit implications of current events

15 MOODY’S CREDIT OUTLOOK 4 FEBRUARY 2016

Azerbaijani Banks Benefit from Full Deposit Insurance and Tax Moratorium for Retail Depositors On 1 February, a new law providing full insurance for retail depositors in Azerbaijan took effect. At the same time, Azerbaijani authorities said that as of 1 February, they will not tax individual savings for three years. These two measures are credit positive for Azerbaijani banks because they will bolster depositor confidence and help stabilize banks’ funding base.

Depositors in Azerbaijan have been withdrawing their savings in past months after the local currency, the manat, depreciated 25% over January and February 2015 in response to tumbling oil prices. The new insurance law will cover all retail deposits, including foreign-currency-denominated deposits with an interest rate below a cap, which has not yet been determined.

The 25% depreciation in January and February 2015 has taken a toll on bank deposits. Retail deposits fell to around AZN7 billion as of November 2015 from AZN8 billion in February 2015. Local currency deposits have been particularly hard hit, nearly halving to around AZN1.7 billion from AZN3 billion over the same period (see Exhibit 1).

EXHIBIT 1

Dynamics of Azerbaijani Household Deposits

Source: Central Bank of Azerbaijan

There has also been a noticeable shift to foreign currency deposits. Foreign currency deposits increased to 76% of total customer deposits as of the end of November 2015 from 50% as of the beginning of the year, and the proportion of foreign-currency-denominated retail deposits doubled over the same period to 76% from 38%. We expect that a further 32% currency depreciation in December 2015 from the end of November 2015 and the adoption of a floating currency regime will prompt more dollarization of the banks’ deposit base.

However, the introduction of full insurance coverage by the Azerbaijan Deposit Insurance Fund (ADIF) will help to limit further deposit outflows from the banking system. The endorsed measure is applicable to individual deposits with an annual interest rate that does not exceed the maximum set by ADIF, and it will be valid for three years starting 1 February 2016. Although 91% of deposits paid in by members of ADIF were insured as of September 2015, according to ADIF’s estimates, the manat’s depreciation is likely to have pushed a considerable proportion of foreign currency deposits above the AZN30,000 insurance limit.

0

1

2

3

4

5

6

7

8

AZN

Bill

ions

Foreign Currency Deposits Local Currency Deposits Revaluation Effect

Ilya Pestryakov Associate Analyst +7.495.228.6117 [email protected]

Maria Malyukova Assistant Vice President - Analyst +7.495.228.6106 [email protected]

NEWS & ANALYSIS Credit implications of current events

16 MOODY’S CREDIT OUTLOOK 4 FEBRUARY 2016

Banks that rely most on retail deposits to fund their lending will be the biggest beneficiaries, including OJSC XALQ Bank (B2 negative, b35), OJSC Bank of Baku (B3 negative, b3), and UniBank Commercial Bank (B3 negative, b3), which have the highest shares of individual deposits in their total non-equity liabilities (see Exhibit 2).

EXHIBIT 2

Share of Retail Deposits in Rated Azerbaijani Banks’ Funding

Notes: XALQ = OJSC XALQ BANK; BoB = OJSC Bank of Baku; Unibank = UniBank Commercial Bank; Kapital = Kapital Bank OJSC; Respublika = Joint Stock Commercal Bank Respublika; IBA = International Bank of Azerbaijan; VTBA = VTB Bank (Azerbaijan). Data as of year-end 2015 except data for International Bank of Azerbaijan and VTB Bank (Azerbaijan), which are as of 1 December 2015. Sources: Banks’ local GAAP reports and Moody’s Investors Service

5 The bank ratings shown in this report are the banks’ deposit ratings and baseline credit assessment.

65%60%

50%

34% 32%

16% 15%

77%

90% 88%

57%49%

36%

95%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

XALQ BoB Unibank Kapital Respublika IBA VTBA

Individual Funds to Total Liabilities Individual Funds to Total Customer Funds

NEWS & ANALYSIS Credit implications of current events

17 MOODY’S CREDIT OUTLOOK 4 FEBRUARY 2016

Bank of Japan's Negative Interest Rate Policy Is Credit Negative for Banks On 29 January, the Bank of Japan (BOJ) announced a three-tier framework whereby it will apply a negative interest rate of minus 0.1% to any incremental amounts on banks’ current account balances with the central bank, after certain adjustments. A rate of positive 0.1% will continue to apply to banks’ existing current account balances, or basic balances, and a zero interest rate will apply on balances required under the reserve requirement system, or macro add-on balances.

The decision to adopt a negative interest rate policy is credit negative for Japanese banks because it will encourage them to direct excess funds to assets with higher risk and/or lower liquidity than central bank deposits. Japan’s three major banks, The Bank of Tokyo-Mitsubishi UFJ, Ltd. (A1/A1 stable, a36), Sumitomo Mitsui Banking Corporation (A1/A1 stable, a3), and Mizuho Bank, Ltd. (A1/A1 stable, baa1), are most affected by the new policy because they have seen the strongest growth in excess liquidity under the government’s qualitative and quantitative monetary easing program.

As shown in the exhibit below, the three Japanese megabanks’ cash and balances with the central bank grew by ¥87 trillion between March 2013 and September 2015, while domestic loans increased by just ¥5 trillion during the same period.

Three Japanese Megabanks’ Excess Liquidity and Domestic Loan Growth Since March 2013 Excess liquidity continues to grow faster than domestic loans.

Sources: The Bank of Tokyo Mitsubishi UFJ, Ltd., Sumitomo Mitsui Banking Corporation, Mizuho Bank, Ltd., Mizuho Trust and Banking Co., Ltd. and Moody's Investors Service

With 10-year yields dropping below 0.1%, Japanese government bonds are no longer attractive investments for the banks. Because most other investment options have higher risk and/or lower liquidity than central bank deposits, the risk profile of the banks’ balance sheets will likely increase if this trend of excess liquidity growth continues. Even a pickup in domestic loan growth may be credit negative if credit spreads tighten to the point that they do not cover credit costs.

We expect the overall effect on the banks’ profitability to be mixed. Because the BOJ will only apply negative interest rates to additional current account deposits above the existing balances, there is no immediate effect on their existing profits.

6 The bank ratings shown in this report are the bank’s deposit rating, senior unsecured debt rating, rating outlook, and baseline credit

assessment

¥0

¥10

¥20

¥30

¥40

¥50

¥60

¥70

¥80

¥90

Mar-13 Sep-13 Mar-14 Sep-14 Mar-15 Sep-15

¥Tr

illio

ns

Domestic Loans Cash & Balances with Central Bank

Shunsaku Sato Vice President - Senior Credit Officer +81.3.5408.4159 [email protected]

NEWS & ANALYSIS Credit implications of current events

18 MOODY’S CREDIT OUTLOOK 4 FEBRUARY 2016

Sovereigns

Uruguay Reports a Wider-than-Expected Deficit Last Friday, Uruguay’s (Baa2 stable) Ministry of Finance reported that the sovereign’s 2015 deficit had increased by more than 15% from 2014 levels. The wider deficit was mainly driven by large increases in pension expenditures and higher-than-budgeted interest expense. The wider deficit is credit negative and we estimate that it grew to 2.8% of GDP (based on our 2015 GDP estimate) from 2.3% in 2014, much higher than our 2.4% deficit expectation.

Given the rigid nature of Uruguay’s expenditures and a challenging macroeconomic environment, the government appears unlikely to meet fiscal consolidation targets in 2016, which would threaten its fiscal policy credibility.

Total budget revenues grew 7.9% during the year to UYU287 billion, below the government’s expectations. Expenditures were close to UYU329 billion, 10.8% higher than in 2014. Because capital expenditures are only about 6% of total spending, fiscal adjustment at the central government level has been challenging because of expenditure rigidity. Pension expenditures, which are politically unfeasible to cut, increased by 18% on a yearly basis. Moreover, given Uruguay’s high reliance on foreign currency funding, the depreciation of the Uruguayan peso has pushed the interest payments-to-revenue ratio to above 12% versus a median of 8.9% for Baa-rated sovereigns.

We estimate that debt to GDP rose to 44.5% in 2015 from 39.5% in 2014 as a result of the wider fiscal deficit and the peso’s depreciation. Because 55% of Uruguay’s debt is denominated in foreign currencies (mainly dollars), this makes public finances vulnerable to currency weakness. In 2015, the Uruguayan peso weakened 23.3%, making interest payments on debt more costly and increasing the debt burden by an amount greater than just the fiscal deficit.

Weaker fiscal revenue growth in 2015 is due to a significant slowdown in economic activity. Real GDP growth likely slowed to 1.8% in 2015 from an average 4.9% in 2010-14. This highlights how dependent the fiscal accounts are on strong economic growth, given that implementing expenditure cuts would require adopting unpopular policies.

The economy will continue to face headwinds given that Uruguay’s main trading partner, Brazil (Baa3 review for downgrade), is in the midst of a protracted recession. We expect 2016 GDP growth of 2.1% for Uruguay, but the balance of risks to our growth projection is tilted toward the downside. Moreover, because the deficit was larger than we expected, we are revising our fiscal deficit forecast for 2016 to 2.7% of GDP from 2.0%, which will push debt to just under 47% of GDP, as shown in the exhibit below.

Jaime Reusche Vice President - Senior Analyst +1.212.553.0358 [email protected]

Carlos Morales Associate Analyst +1.212.553.0554 [email protected]

NEWS & ANALYSIS Credit implications of current events

19 MOODY’S CREDIT OUTLOOK 4 FEBRUARY 2016

Uruguay’s Fiscal Deficit and Debt as a Percent of GDP

Sources: Central Bank of Uruguay and Moody’s Investors Service

We believe that expenditure cuts, particularly on capital investment and intermediate consumption, will curb the growth in overall expenditures in 2016. The government is likely to adopt measures to boost fiscal revenues and underpin the fiscal consolidation effort. Nevertheless, should consolidation measures fall short of reducing the deficit, debt will continue to rise toward 50% of GDP by 2017, undermining fiscal policy credibility and weakening Uruguay’s credit metrics relative to rating peers.

0%

10%

20%

30%

40%

50%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

2009 2010 2011 2012 2013 2014 2015F 2016F

Fiscal Deficit to GDP - left axis Debt to GDP - right axis

NEWS & ANALYSIS Credit implications of current events

20 MOODY’S CREDIT OUTLOOK 4 FEBRUARY 2016

South Africa Continues to Predict Lower Growth On 28 January, during a meeting of its Monetary Policy Committee, the South African Reserve Bank (SARB) revised its forecast for South Africa’s (Baa2 negative) real GDP growth to 0.9% from the 1.5% it had projected in November, a credit negative. This is SARB’s third downward revision to its 2016 real GDP growth forecast in as many meetings.

SARB’s Monetary Policy Committee uses its forecasts in its quarterly meetings to set interest rates. The subdued 2016 forecast falls within our own 0.5%-1.5% forecast, and is similar to the International Monetary Fund (IMF) forecast of 0.6%, and the World Bank’s 0.8% forecast. The SARB also reduced its forecast for 2017 growth to 1.6% from 2.1% (Exhibit 1).

EXHIBIT 1

South Africa’s Revised GDP Growth Forecasts for 2016 and 2017

Sources: International Monetary Fund World Economic Outlook and South African Reserve Bank

Lower growth is credit negative for the sovereign because it will hamper efforts to raise tax revenues and broaden the tax base. Current levels of tax and other government receipts fall short of the government’s spending needs by 3%-4% of GDP annually. Even though the National Treasury has budgeted conservatively for the current fiscal year and next, including an accurate assumption of very weak corporate income tax revenues, the near-zero growth rate is a significant further downward shift in the already narrow tax base that buoyant tax elasticities cannot overcome.

In past years, the government has met its fiscal targets, which nevertheless led to continued debt accumulation and reduced the effectiveness of countercyclical fiscal policy. Government credibility was also weakened by abrupt and multiple changes in the Minister of Finance position in December.

As the 2015 Medium Term Budget Statement underscored last October, the considerably lower growth than projected under the initial 2015 budget has necessitated downward revisions in the revenue estimates by the government for the period ahead. A further decline in growth is likely to additionally dampen revenues. These factors will make it challenging to maintain a sound fiscal position at the time when the government faces difficulties adhering to its spending ceiling. In turn, a widening fiscal deficit combined with reduced growth will delay stabilizing and reversing the rising public debt/GDP trajectory, bringing the ratio to more than 50% for the first time in more than a decade.

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

2011 2012 2013 2014 2015 (e) 2016 (p) 2017 (p)

IMF Apr 2015 SARB and IMF Oct 2015 IMF Jan 2016 SARB Jan 2016

Kristin Lindow Senior Vice President +1.212.553.3896 [email protected]

Zuzana Brixiova Vice President - Senior Analyst +44.20.7772.1628 [email protected]

David Kamran Associate Analyst +1.212.553.2109 [email protected]

NEWS & ANALYSIS Credit implications of current events

21 MOODY’S CREDIT OUTLOOK 4 FEBRUARY 2016

The latest cuts in 2016 and 2017 growth will hamper investment, including in infrastructure and human capital, further lowering potential long-term growth. This is likely to contribute to prolonged high unemployment and worsening social tensions. More immediately, lower growth will reduce the fiscal space needed to tackle the effects of South Africa’s most severe drought in decades. According to the World Bank, the drought has already pushed an additional 50,000 people below the poverty line of ZAR501 ($31) a month.

Low and declining real GDP growth was a key driver of the negative outlook we assigned to South Africa in December. The reduced growth is driven by “low for long” commodity prices (with metal prices negatively affecting South Africa), declining demand from China, electricity shortages and subdued consumer and business confidence (Exhibit 2). These drivers have been exacerbated by the drought and tightening financial conditions owing to rising interest rates. On Thursday, the SARB raised its policy rate to 6.75%, citing inflationary pressures and the challenges to stay within its targeted inflation range as factors outweighing growth concerns.

EXHIBIT 2

South Africa Business and Consumer Confidence, March 2007-December 2015

Source: Bureau of Economic Research of South Africa

-25

-20

-15

-10

-5

0

5

10

15

20

25

30

10

20

30

40

50

60

70

80

90

Mar

-07

Jul-

07

Nov

-07

Mar

-08

Jul-

08

Nov

-08

Mar

-09

Jul-

09

Nov

-09

Mar

-10

Jul-

10

Nov

-10

Mar

-11

Jul-

11

Nov

-11

Mar

-12

Jul-

12

Nov

-12

Mar

-13

Jul-

13

Nov

-13

Mar

-14

Jul-

14

Nov

-14

Mar

-15

Jul-

15

Nov

-15

Inde

x -1

00 to

100

, 0 =

Neu

tral

Inde

x 0

to 1

00, 5

0 =

Neu

tral

Business Confidence Condex - left axis Consumer Confidence Index - right axis

NEWS & ANALYSIS Credit implications of current events

22 MOODY’S CREDIT OUTLOOK 4 FEBRUARY 2016

Pakistan’s New Monetary Policy Framework Will Improve Policy Transparency and Transmission, a Credit Positive Last Saturday, the State Bank of Pakistan’s Monetary Policy Committee (MPC) issued its first policy statement, marking the central bank’s operation of a new monetary policy framework introduced a week earlier. The new MPC framework is a crucial step toward the eventual introduction of an inflation-targeting mechanism, which we expect will increase policy transparency and effectiveness, a credit positive. Moreover, its successful implementation should gradually bring Pakistan’s (B3 stable) inflation down to stable and predictable levels, thereby supporting external competitiveness, households’ purchasing power and the wider economy.

The State Bank of Pakistan’s (SBP) formation of a nine-member, independent MPC that is empowered to make monetary decisions replaces an internal advisory committee that made recommendations to the central bank’s board of directors. As an independent committee, the MPC includes representatives from outside the central bank. Their breadth of expertise and the views that they provide will benefit policy decisions and improve overall institutional strength through greater policy credibility. Monetary policy statements published following MPC meetings will further ensure public accountability and transparency.

The introduction of the new framework also points to the SBP’s continued commitment to move to a flexible inflation-targeting regime. Over the past year, the central bank has fulfilled several benchmarks specified under Pakistan’s Extended Credit Facility with the International Monetary Fund (IMF) aimed at facilitating this move. Key among these was reviewing the interest rate corridor in early 2015 to introduce a target rate in addition to a ceiling and floor rate to clearly signal SBP’s monetary policy stance. Other pre-conditions put in place by the IMF include the development of the central bank’s technical forecasting capacity, and oversight and approval of the reserves management strategy.

The formation of the MPC is an important step toward central bank independence. Pakistan enacted amendments to the SBP laws to give the central bank autonomy in its pursuit of price stability in November 2015. Together, these measures will reduce the likelihood of fiscal policy driving inflation trends. Historically, large fiscal deficits, funded by central bank lending, drove excessive credit growth through the 2000s and resulted in persistently high inflation (see Exhibit 1).

EXHIBIT 1

Year-over-Year Change in Pakistan’s Inflation and Central Bank Lending to Government

Sources: Pakistan Bureau of Statistics, State Bank of Pakistan, Haver Analytics and Moody's Investors Service

Ceilings on net government borrowing from the SBP that are a quantitative criteria under the IMF program have helped reduce this reliance to some extent, although the government has now shifted primarily to commercial banks as a source of funding. The new MPC will serve to further check fiscal dominance.

-5%

0%

5%

10%

15%

20%

25%

30%

-50%

0%

50%

100%

150%

200%

250%

300%

Jan-

06Ap

r-06

Jul-

06O

ct-0

6Ja

n-07

Apr-

07Ju

l-07

Oct

-07

Jan-

08Ap

r-08

Jul-

08O

ct-0

8Ja

n-09

Apr-

09Ju

l-09

Oct

-09

Jan-

10Ap

r-10

Jul-

10O

ct-1

0Ja

n-11

Apr-

11Ju

l-11

Oct

-11

Jan-

12Ap

r-12

Jul-

12O

ct-1

2Ja

n-13

Apr-

13Ju

l-13

Oct

-13

Jan-

14Ap

r-14

Jul-

14O

ct-1

4Ja

n-15

Apr-

15Ju

l-15

Oct

-15

Central Bank Net Claims on General Government - left axis Headline CPI - right axis

Anushka Shah Assistant Vice President - Analyst +65.6398.3710 [email protected]

Matthew Circosta Associate Analyst +65.6398.8324 [email protected]

NEWS & ANALYSIS Credit implications of current events

23 MOODY’S CREDIT OUTLOOK 4 FEBRUARY 2016

Combined, these factors will limit government borrowing, and in turn reduce the government’s influence on prices.

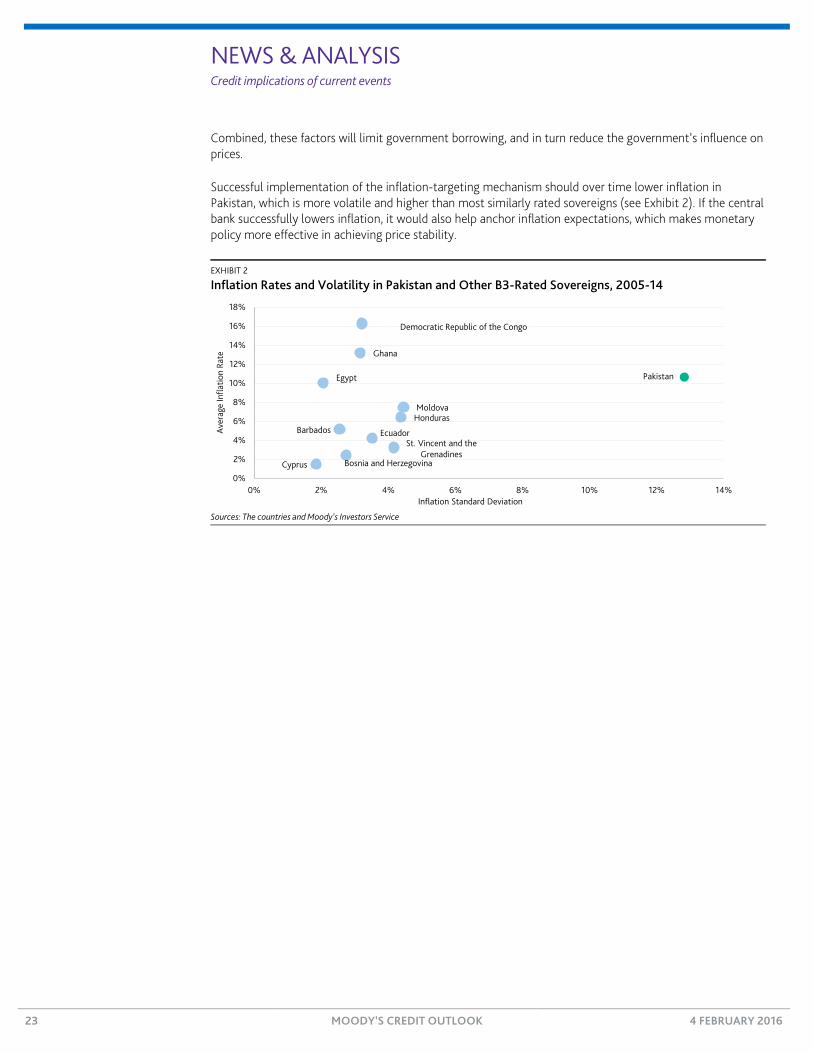

Successful implementation of the inflation-targeting mechanism should over time lower inflation in Pakistan, which is more volatile and higher than most similarly rated sovereigns (see Exhibit 2). If the central bank successfully lowers inflation, it would also help anchor inflation expectations, which makes monetary policy more effective in achieving price stability.

EXHIBIT 2

Inflation Rates and Volatility in Pakistan and Other B3-Rated Sovereigns, 2005-14

Sources: The countries and Moody’s Investors Service

Barbados

Bosnia and HerzegovinaCyprus

Democratic Republic of the Congo

Ecuador

Egypt

Ghana

HondurasMoldova

Pakistan

St. Vincent and the Grenadines

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0% 2% 4% 6% 8% 10% 12% 14%

Aver

age

Infla

tion

Rate

Inflation Standard Deviation

NEWS & ANALYSIS Credit implications of current events

24 MOODY’S CREDIT OUTLOOK 4 FEBRUARY 2016

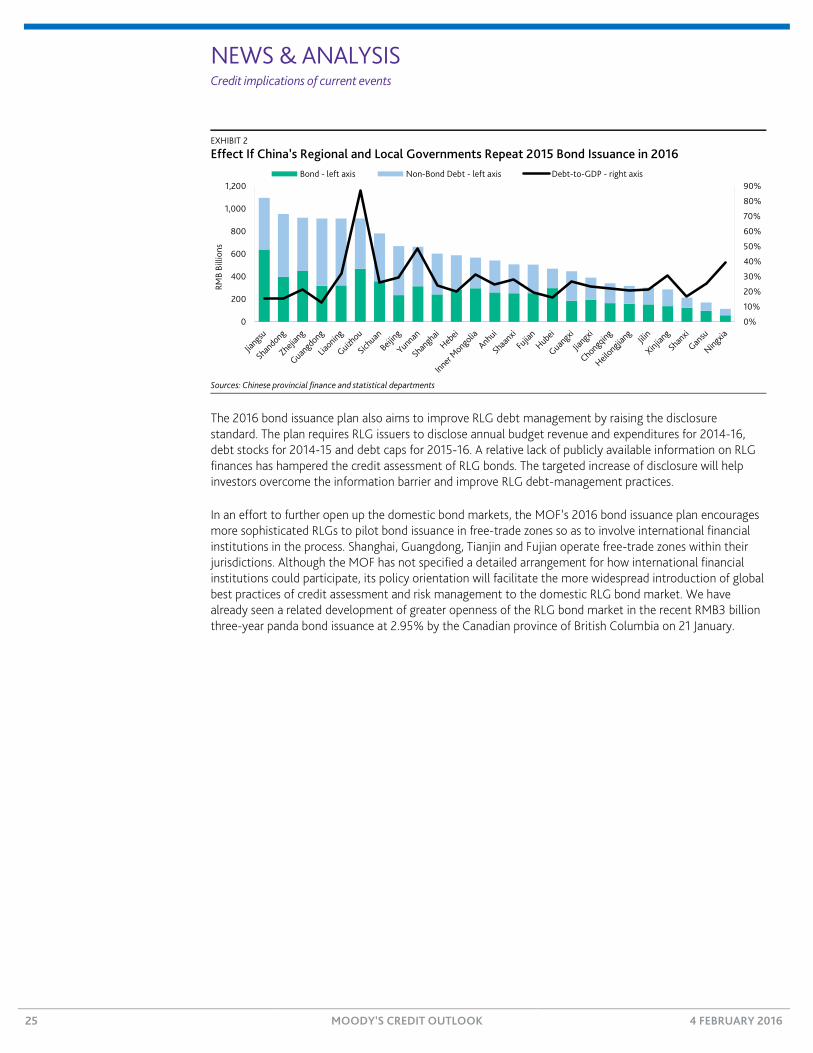

Sub-sovereigns

Chinese Regional and Local Government Bond Program Continues, a Credit Positive On 28 January, China’s (Aa3 stable) Ministry of Finance (MOF) announced the 2016 bond issuance program for regional and local governments (RLGs). The plan is credit positive because it retires outstanding debt and replaces it with lower-interest, longer-maturity bonds, caps new debt issuance and improves disclosures.

The 2016 issuance plan for RLGs is similar to the 2015 outcome of RMB3.8 trillion ($575.8 billion) issuance (see Exhibit 1). In addition, the MOF has capped at RMB16.0 trillion the total amount of RLG direct debt, including newly issued bonds. Most existing RLG debt consists of loans from commercial banks and trust companies that will exchange their debt claims for bonds. Commercial banks have accepted lower-yielding bonds because of their lower 20% risk-weight versus 100% for loans to RLG-related corporate entities. RLG bonds are also eligible collateral for commercial banks when bidding for RLG fiscal deposits. Asset managers such as mutual funds and institutional investors such as insurance companies are buyers of newly issued bonds.

EXHIBIT 1

Chinese Regional and Local Government Bond Issuance in 2014 and 2015

Sources: Bond prospectuses

In a related statement, the MOF has indicated a policy preference to replace RMB11.1 trillion of existing debt out of the RMB16.0 trillion total of direct debt with bonds within three years. It is very likely that 2016 bond issuance will be no less than RMB3-RMB4 trillion. To minimize potential disruption to capital markets, the MOF has capped both new issuance and bonds issued to replace existing debt for individual RLG issuers. Furthermore, the 2016 issuance plan paces bond issuance to no more than 30% of the capped amount by the end of the first quarter; no more than 60% cumulatively by the end of the second quarter; and no more than 90% cumulatively by the end of the third quarter.

As seen in Exhibit 2, if 2016 bond issuance for individual provinces equals 2015 issuance, the overall share of lower-interest and longer-maturity bonds in total RLG direct debt would be 54%, which would improve debt profiles, especially for provinces with high debt burdens such as Guizhou.

0

100

200

300

400

500

600

700

800

2014 May-15 Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15

RMB

Billi

ons

Exchange for Existing Debt New Issuance

Nicholas Zhu, Ph.D. Vice President - Senior Analyst +86.10.6319.6536 [email protected]

NEWS & ANALYSIS Credit implications of current events

25 MOODY’S CREDIT OUTLOOK 4 FEBRUARY 2016

EXHIBIT 2

Effect If China’s Regional and Local Governments Repeat 2015 Bond Issuance in 2016

Sources: Chinese provincial finance and statistical departments

The 2016 bond issuance plan also aims to improve RLG debt management by raising the disclosure standard. The plan requires RLG issuers to disclose annual budget revenue and expenditures for 2014-16, debt stocks for 2014-15 and debt caps for 2015-16. A relative lack of publicly available information on RLG finances has hampered the credit assessment of RLG bonds. The targeted increase of disclosure will help investors overcome the information barrier and improve RLG debt-management practices.

In an effort to further open up the domestic bond markets, the MOF’s 2016 bond issuance plan encourages more sophisticated RLGs to pilot bond issuance in free-trade zones so as to involve international financial institutions in the process. Shanghai, Guangdong, Tianjin and Fujian operate free-trade zones within their jurisdictions. Although the MOF has not specified a detailed arrangement for how international financial institutions could participate, its policy orientation will facilitate the more widespread introduction of global best practices of credit assessment and risk management to the domestic RLG bond market. We have already seen a related development of greater openness of the RLG bond market in the recent RMB3 billion three-year panda bond issuance at 2.95% by the Canadian province of British Columbia on 21 January.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0

200

400

600

800

1,000

1,200

RMB

Billi

ons

Bond - left axis Non-Bond Debt - left axis Debt-to-GDP - right axis

NEWS & ANALYSIS Credit implications of current events

26 MOODY’S CREDIT OUTLOOK 4 FEBRUARY 2016

US Public Finance

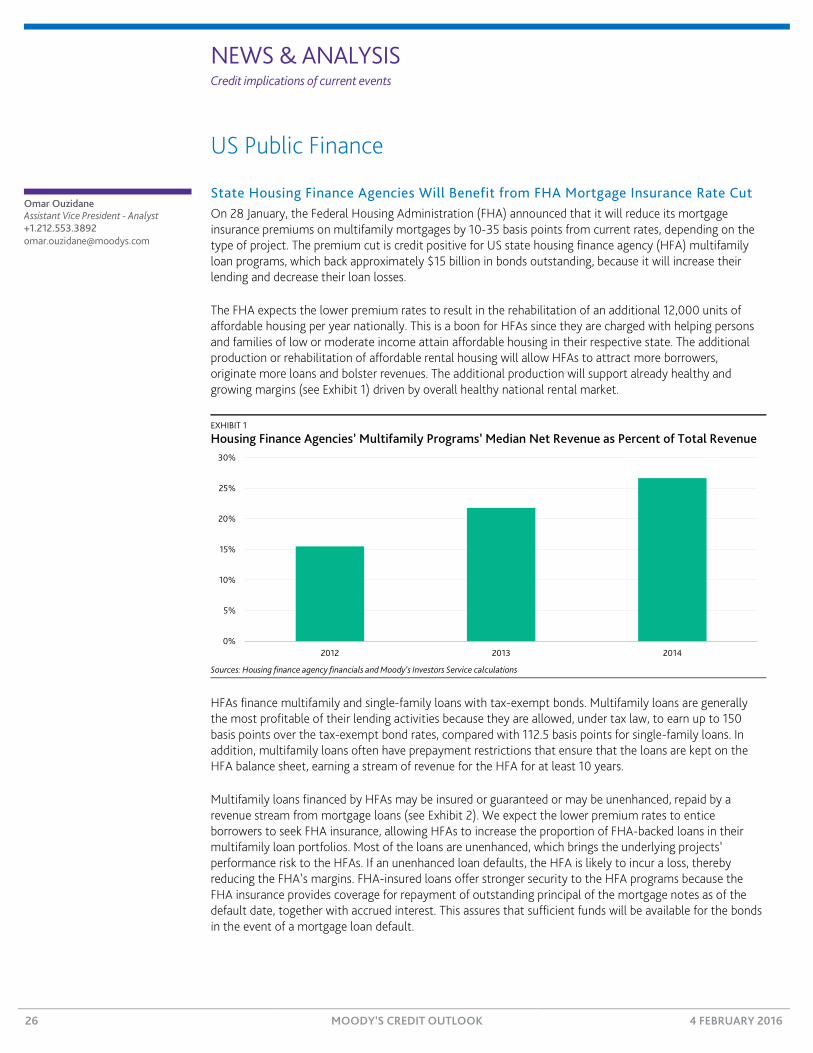

State Housing Finance Agencies Will Benefit from FHA Mortgage Insurance Rate Cut On 28 January, the Federal Housing Administration (FHA) announced that it will reduce its mortgage insurance premiums on multifamily mortgages by 10-35 basis points from current rates, depending on the type of project. The premium cut is credit positive for US state housing finance agency (HFA) multifamily loan programs, which back approximately $15 billion in bonds outstanding, because it will increase their lending and decrease their loan losses.

The FHA expects the lower premium rates to result in the rehabilitation of an additional 12,000 units of affordable housing per year nationally. This is a boon for HFAs since they are charged with helping persons and families of low or moderate income attain affordable housing in their respective state. The additional production or rehabilitation of affordable rental housing will allow HFAs to attract more borrowers, originate more loans and bolster revenues. The additional production will support already healthy and growing margins (see Exhibit 1) driven by overall healthy national rental market.

EXHIBIT 1

Housing Finance Agencies’ Multifamily Programs’ Median Net Revenue as Percent of Total Revenue

Sources: Housing finance agency financials and Moody’s Investors Service calculations

HFAs finance multifamily and single-family loans with tax-exempt bonds. Multifamily loans are generally the most profitable of their lending activities because they are allowed, under tax law, to earn up to 150 basis points over the tax-exempt bond rates, compared with 112.5 basis points for single-family loans. In addition, multifamily loans often have prepayment restrictions that ensure that the loans are kept on the HFA balance sheet, earning a stream of revenue for the HFA for at least 10 years.

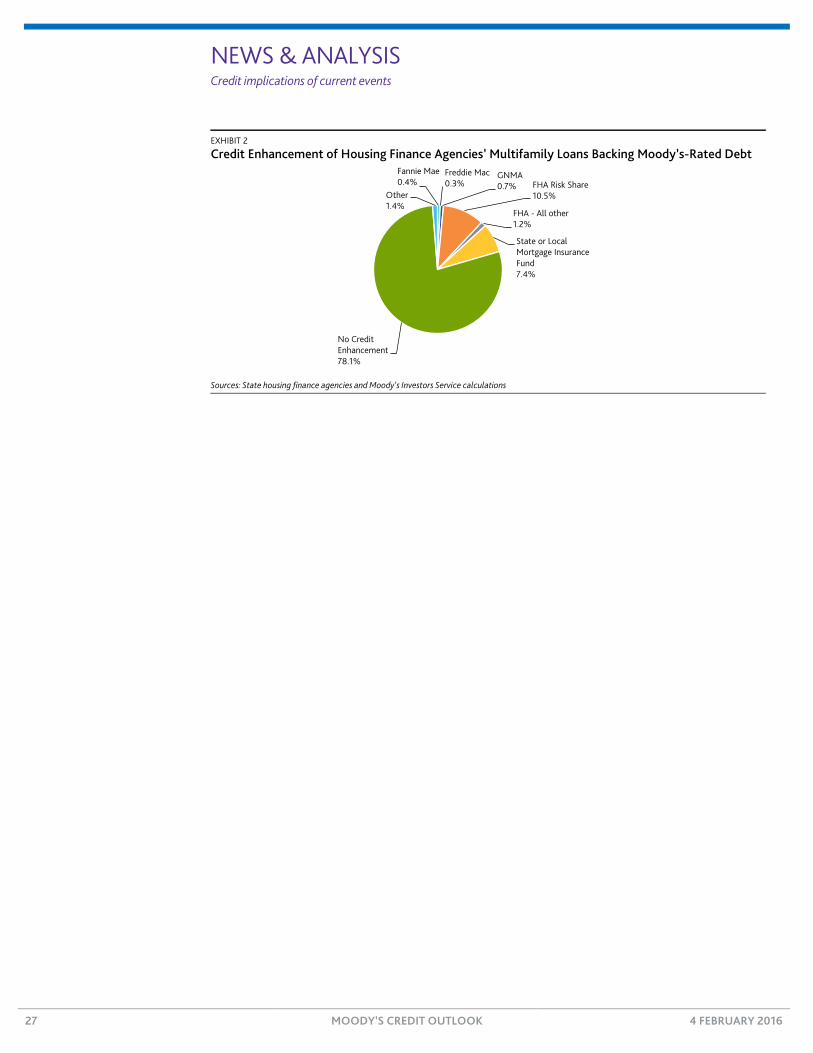

Multifamily loans financed by HFAs may be insured or guaranteed or may be unenhanced, repaid by a revenue stream from mortgage loans (see Exhibit 2). We expect the lower premium rates to entice borrowers to seek FHA insurance, allowing HFAs to increase the proportion of FHA-backed loans in their multifamily loan portfolios. Most of the loans are unenhanced, which brings the underlying projects’ performance risk to the HFAs. If an unenhanced loan defaults, the HFA is likely to incur a loss, thereby reducing the FHA’s margins. FHA-insured loans offer stronger security to the HFA programs because the FHA insurance provides coverage for repayment of outstanding principal of the mortgage notes as of the default date, together with accrued interest. This assures that sufficient funds will be available for the bonds in the event of a mortgage loan default.

0%

5%

10%

15%

20%

25%

30%

2012 2013 2014

Omar Ouzidane Assistant Vice President - Analyst +1.212.553.3892 [email protected]

NEWS & ANALYSIS Credit implications of current events

27 MOODY’S CREDIT OUTLOOK 4 FEBRUARY 2016

EXHIBIT 2

Credit Enhancement of Housing Finance Agencies’ Multifamily Loans Backing Moody’s-Rated Debt

Sources: State housing finance agencies and Moody’s Investors Service calculations

Fannie Mae0.4%

Freddie Mac0.3%

GNMA0.7% FHA Risk Share

10.5%

FHA - All other1.2%

State or Local Mortgage Insurance Fund 7.4%

No Credit Enhancement78.1%

Other1.4%

RECENTLY IN CREDIT OUTLOOK Select any article below to go to last Monday’s Credit Outlook on moodys.com

28 MOODY’S CREDIT OUTLOOK 4 FEBRUARY 2016

NEWS & ANALYSIS Corporates 2 » Xerox’s Planned Split Is Credit Negative » Merger Is Credit Positive for Johnson Controls, Credit

Negative for Tyco International » Lockheed Martin’s IT Services Spinoff Is Credit Negative » FedEx’s New Share Repurchase Authorization Is Credit Negative » Proposed US Accounting Standards Would Improve

Postemployment Benefit Accounting » Total System Services’ Planned $2.35 Billion Acquisition of

TransFirst Is Credit Negative » Brown-Forman’s $1 Billion Stock Buyback Plan Is

Credit Negative » Times Property Holdings’ Land Acquisition Is Credit Negative

Infrastructure 11 » US Supreme Court Upholds Federal Authority over Demand

Response, a Negative for PJM Interconnection Generators » Kansai’s Restart of Nuclear Reactor Will Improve Earnings

and Price Competitiveness

Banks 15 » FirstMerit Sale Shows that Even Highly Rated Small Banks

Face Credit-Negative Strategic Choices » Italy’s Bad-Bank Scheme Will Require the Recognition of

Loan Losses » RBS Announces Various Large Charges, a Credit Negative » Ukrainian Government’s Capital Injections Will Benefit State-

Owned Banks » Egypt’s Central Bank Increase of US Dollar Deposit Caps Will

Not Ease Banks’ Liquidity Pressures » South Africa’s Interest Rate Hike Will Weaken Banks’

Asset Quality

Insurers 27 » AIG’s Ongoing P&C Reserve Woes Are Credit Negative » Aetna’s Reinsurer Deal Provides Limited Risk Protection

Managed Investments 32 » Legg Mason’s Acquisitions to Boost Its Presence in

Alternative Assets Are Credit Negative » China’s New Money Market Fund Rules Are Credit Positive

Sovereigns 38 » Saudi Arabia’s and China’s Financial Support to Egypt Will

Ease Strains on Its External Position » Philippines’ Growth Shows Resistance to Global Slowdown, a

Credit Positive » Malaysia’s Revised Budget Indicates Strong Commitment to

Fiscal Consolidation

Securitization 44 » Threatened Labor Strike Would Be Credit Negative for

Argentine Oil and Gas Royalty Rights Securitization

RATINGS & RESEARCH Rating Changes 45

Last week we downgraded Discovery Communications, SK E&S, AIG’s North American property and casualty subsidiaries, seven German banks, five Italian banks, AIG Europe Limited, Bank of Nova Scotia and US CMBS, and upgraded Alleghany Corporation, RSUI Indemnity Company, Landmark American Insurance Company, Mortgage Guaranty Insurance Corporation, Radian Guaranty, 22 German banks, 16 Italian banks, Bahrain Islamic Bank, KBC Bank, US subprime RMBS and US CMBS, among other rating actions.

Research Highlights 53

Last week we published on US building materials, US corporates rated B3 and lower, European satellite services, US chemicals, global oil and natural gas, global base metals, Asian telecom and media, Chinese property developers, US wireline telecom, Mexican construction, US covenant quality, Asia-Pacific corporates, Nebraska public power utilities, SK E&S, European banks, German and Italian banks, Chinese banks, Malaysia, Zimbabwe, Jordan, Texas local governments, US military housing, US universities, US equipment ABS, US CLOs, European covered bonds, European CLOs and UK RMBS, among other reports.

MOODYS.COM

Report: 187432

© 2016 Moody’s Corporation, Moody’s Investors Service, Inc., Moody’s Analytics, Inc. and/or their licensors and affiliates (collectively, “MOODY’S”). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. AND ITS RATINGS AFFILIATES (“MIS”) ARE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND CREDIT RATINGS AND RESEARCH PUBLICATIONS PUBLISHED BY MOODY’S (“MOODY’S PUBLICATIONS”) MAY INCLUDE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES. MOODY’S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUAL, FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT. CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS AND MOODY’S OPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT. MOODY’S PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLISHED BY MOODY’S ANALYTICS, INC. CREDIT RATINGS AND MOODY’S PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. NEITHER CREDIT RATINGS NOR MOODY’S PUBLICATIONS COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY’S ISSUES ITS CREDIT RATINGS AND PUBLISHES MOODY’S PUBLICATIONS WITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

MOODY’S CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE RECKLESS AND INAPPROPRIATE FOR RETAIL INVESTORS TO USE MOODY’S CREDIT RATINGS OR MOODY’S PUBLICATIONS WHEN MAKING AN INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACT YOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER.

ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW, AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT.

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as well as other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. MOODY'S adopts all necessary measures so that the information it uses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However, MOODY’S is not an auditor and cannot in every instance independently verify or validate information received in the rating process or in preparing the Moody’s Publications.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for any indirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use any such information, even if MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses or damages, including but not limited to: (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of a particular credit rating assigned by MOODY’S.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatory losses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for the avoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the control of, MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers, arising from or in connection with the information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCH RATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.

Moody’s Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody’s Investors Service, Inc. have, prior to assignment of any rating, agreed to pay to Moody’s Investors Service, Inc. for appraisal and rating services rendered by it fees ranging from $1,500 to approximately $2,500,000. MCO and MIS also maintain policies and procedures to address the independence of MIS’s ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO and rated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually at www.moodys.com under the heading “Investor Relations — Corporate Governance — Director and Shareholder Affiliation Policy.”

Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY’S affiliate, Moody’s Investors Service Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody’s Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intended to be provided only to “wholesale clients” within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, you represent to MOODY’S that you are, or are accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly or indirectly disseminate this document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001. MOODY’S credit rating is an opinion as to the creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors. It would be reckless and inappropriate for retail investors to use MOODY’S credit ratings or publications when making an investment decision. If in doubt you should contact your financial or other professional adviser.

Additional terms for Japan only: Moody's Japan K.K. (“MJKK”) is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is wholly-owned by Moody’s Overseas Holdings Inc., a wholly-owned subsidiary of MCO. Moody’s SF Japan K.K. (“MSFJ”) is a wholly-owned credit rating agency subsidiary of MJKK. MSFJ is not a Nationally Recognized Statistical Rating Organization (“NRSRO”). Therefore, credit ratings assigned by MSFJ are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by an entity that is not a NRSRO and, consequently, the rated obligation will not qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registered with the Japan Financial Services Agency and their registration numbers are FSA Commissioner (Ratings) No. 2 and 3 respectively.

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by MJKK or MSFJ (as applicable) have, prior to assignment of any rating, agreed to pay to MJKK or MSFJ (as applicable) for appraisal and rating services rendered by it fees ranging from JPY200,000 to approximately JPY350,000,000.

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.

EDITORS PRODUCTION ASSOCIATE News & Analysis: Elisa Herr and Jay Sherman Alisa Llorens