Embed Size (px)

Citation preview

MOODYS.COM

26 JANUARY 2015

NEWS & ANALYSIS Corporates 2 » Clean Harbors' Planned Carve-Out of Oil and Gas Services Is

Credit Negative » Kinder Morgan Will Buy Hiland Partners, a Credit Positive

for Hiland » Petrofac Team Wins $4 Billion Oil Project Contract in Kuwait, a

Credit Positive » Telefonica Enters Negotiations to Sell Its UK Subsidiary for £10

Billion, a Credit Positive » Italian Gaming Machine Tax Is Credit Negative for Concessionaires » BHP Billiton's 40% Cut in Oil and Gas Spending Is Credit Negative

for ABB, Weir and Smiths » GPT Group's Redemption of Exchangeable Securities Is

Credit Positive » CITIC Limited and CITIC Group Will Benefit from Itochu's and

Charoen Pokphand's Equity Investment » Itochu's ¥600 Billion Investment in CITIC Limited Is

Credit Negative

Infrastructure 12 » Argentina's Provinces Agree to Freeze Electricity Tariffs Until

December, a Credit Negative » Melbourne and Brisbane Airports Benefit from International

Passenger Increase

Banks 15 » Surprise Canadian Rate Cut Is Credit Negative for Banks » RBC's Acquisition of City National Is Credit Negative » Banca Popolare di Milano Will Benefit from Italy's Reform of

Cooperative Banks » China's Tighter Regulations of Banks' Entrusted Loans Is

Credit Positive » Chinese Securities Firms' Margin-Trading Violations Expose

Weak Operational Controls » Hong Kong's Proposed Resolution Regime for Financial

Institutions Is Credit Negative for Unsecured Creditors » Taiwan Banks' Liquidity Coverage Ratio Implementation Is

Credit Positive » Metropolitan Bank & Trust's Proposed Rights Issue Is

Credit Positive » India Reduces Banks' Loan-Pricing Flexibility, a Credit Negative

for Consumer Lenders

Insurers 29 » Alliant Buys QBE US Agencies, Joining Credit-Negative Trend of

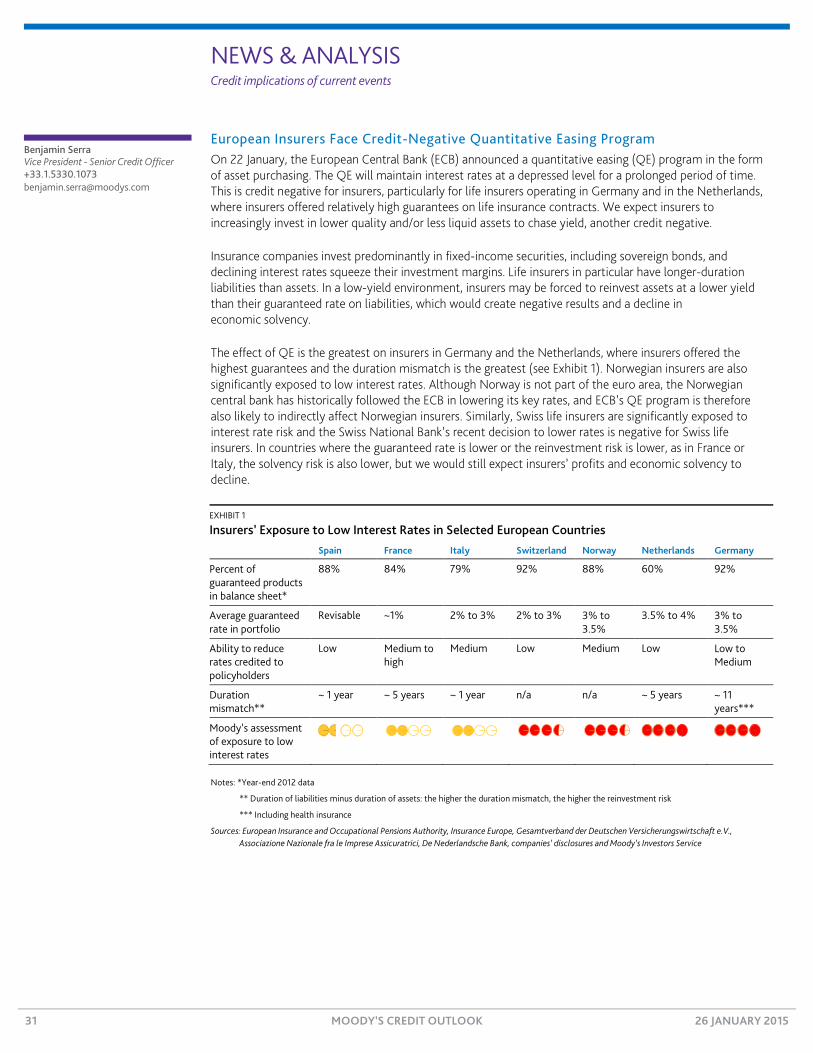

Highly Levered Broker Acquisitions » European Insurers Face Credit-Negative Quantitative

Easing Program

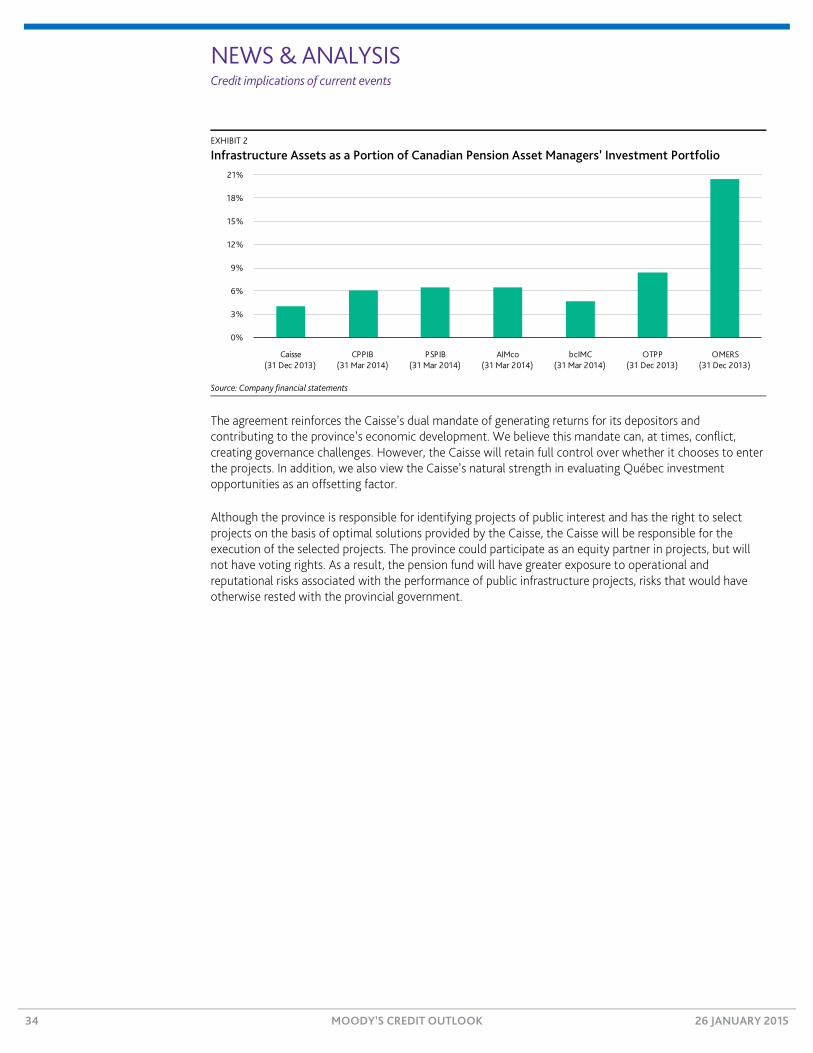

Asset Managers 33 » Caisse de dépôt et placement du Québec's Infrastructure

Agreement with Québec Is Credit Negative

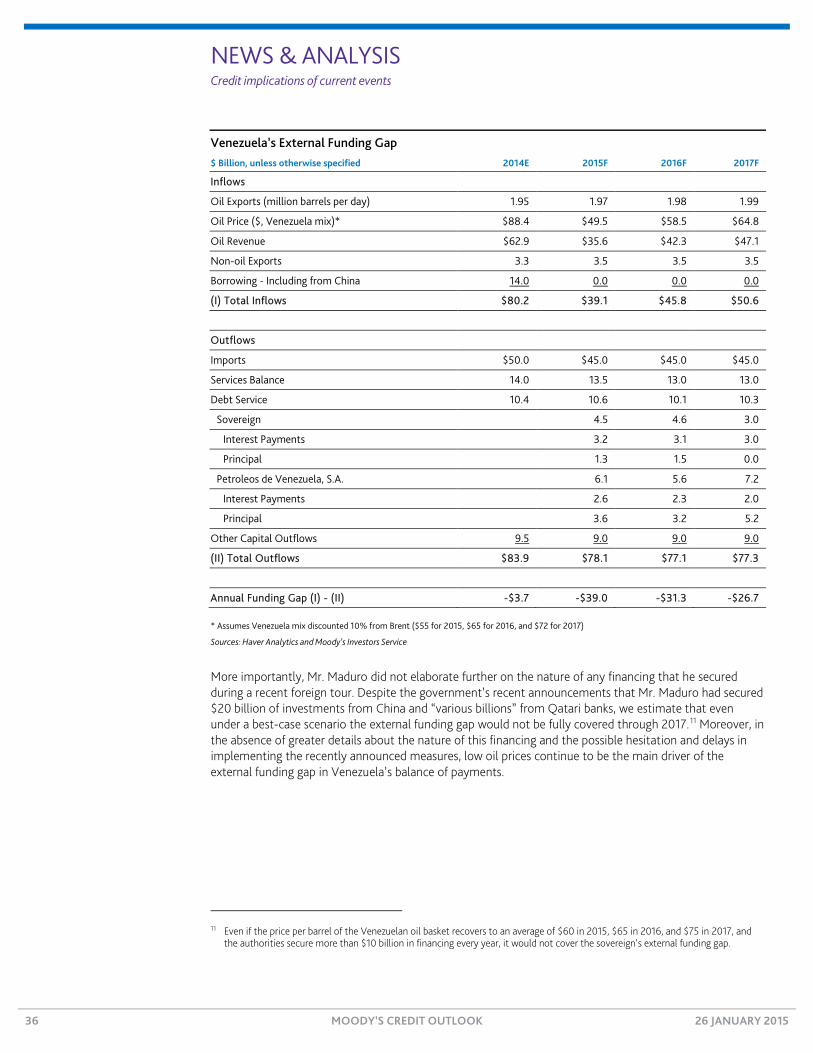

Sovereigns 35 » Venezuela's Economic Measures Do Little to Stave Off a Threat

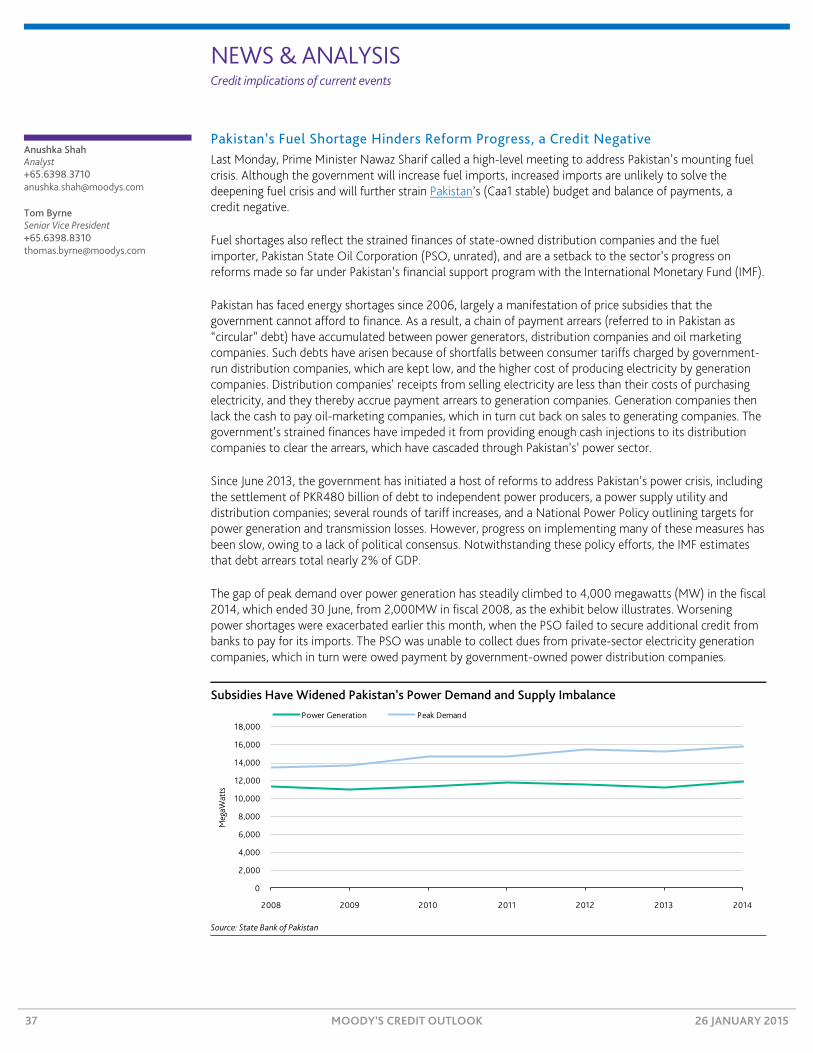

of Default » Pakistan's Fuel Shortage Hinders Reform Progress, a

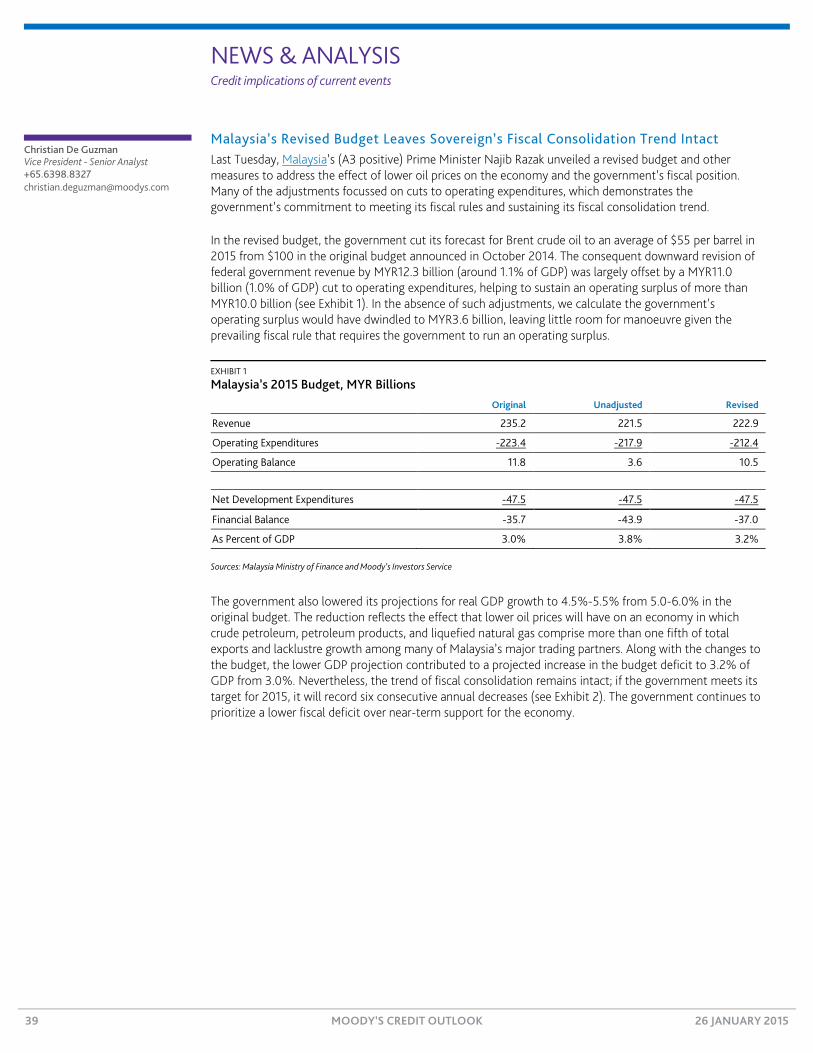

Credit Negative » Malaysia's Revised Budget Leaves Sovereign's Fiscal

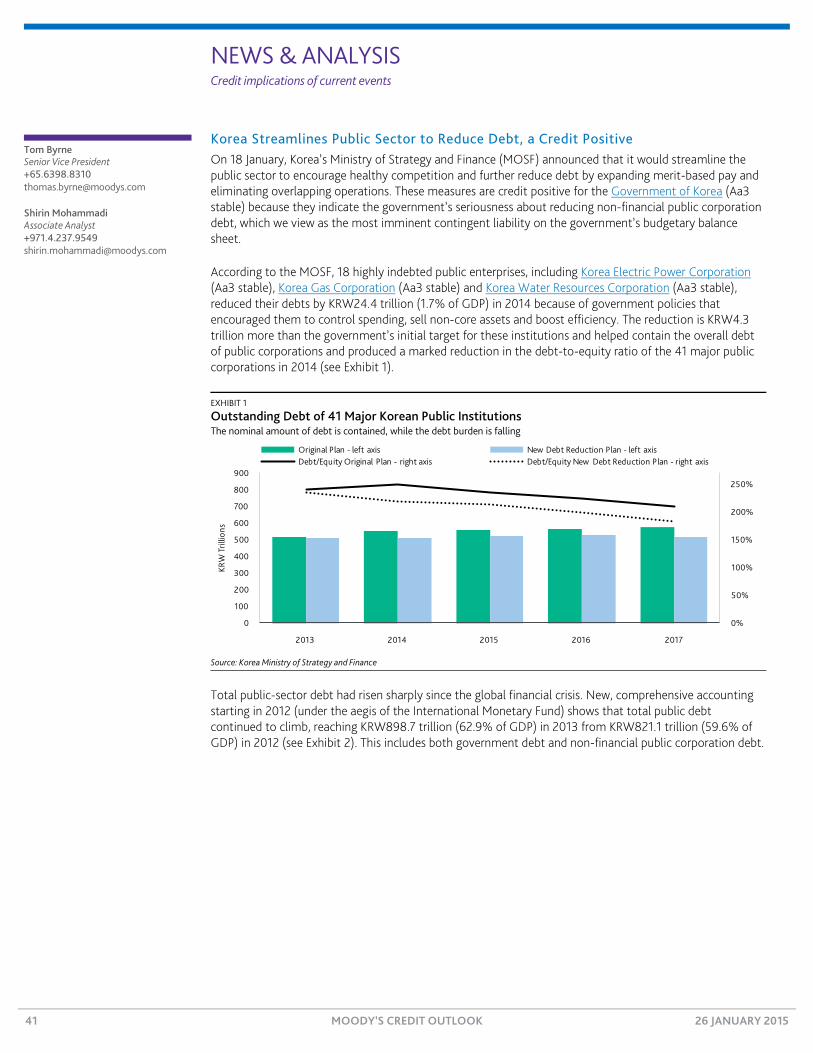

Consolidation Trend Intact » Korea Streamlines Public Sector to Reduce Debt, a

Credit Positive

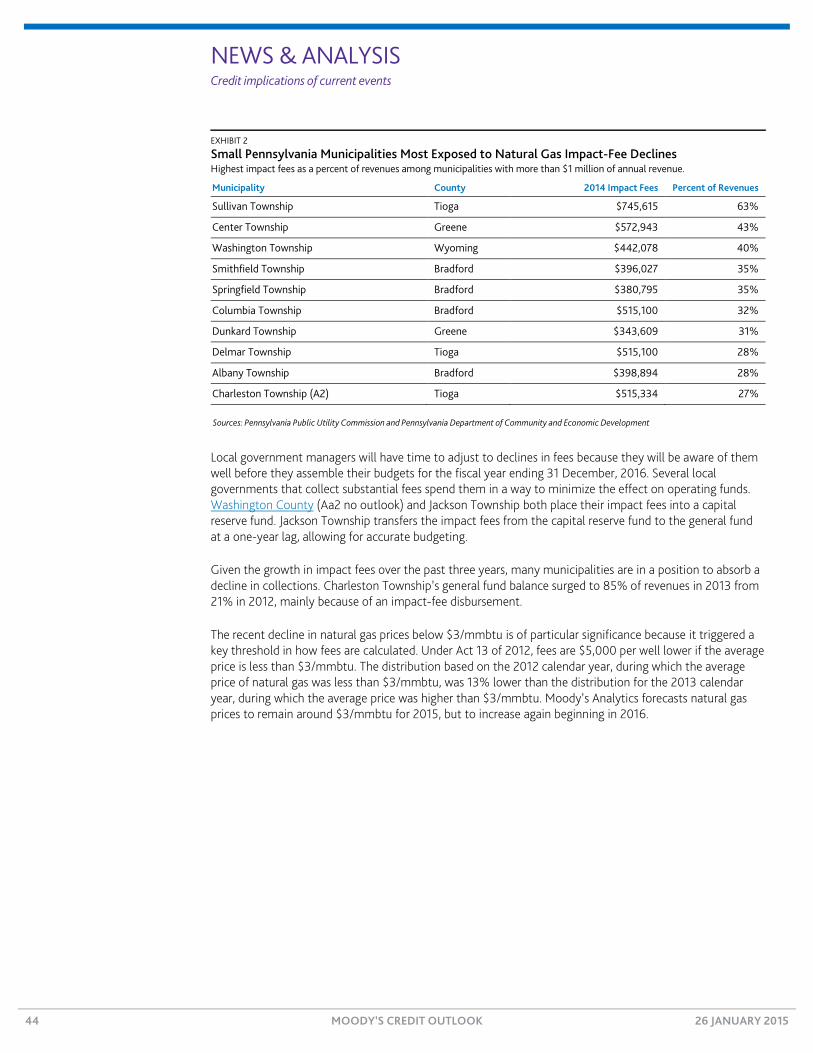

US Public Finance 43 » Lower Natural Gas Prices Will Dent Pennsylvania Impact Fees, a

Credit Negative for Some Municipalities

RATINGS & RESEARCH Rating Changes 45

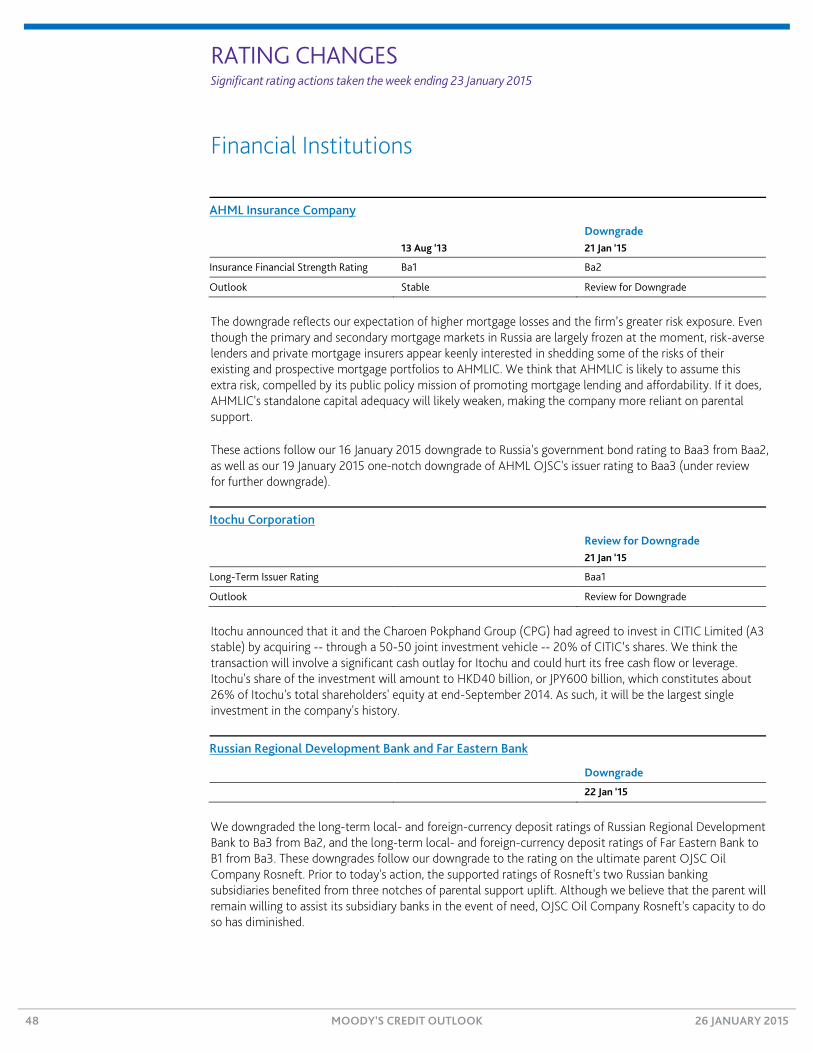

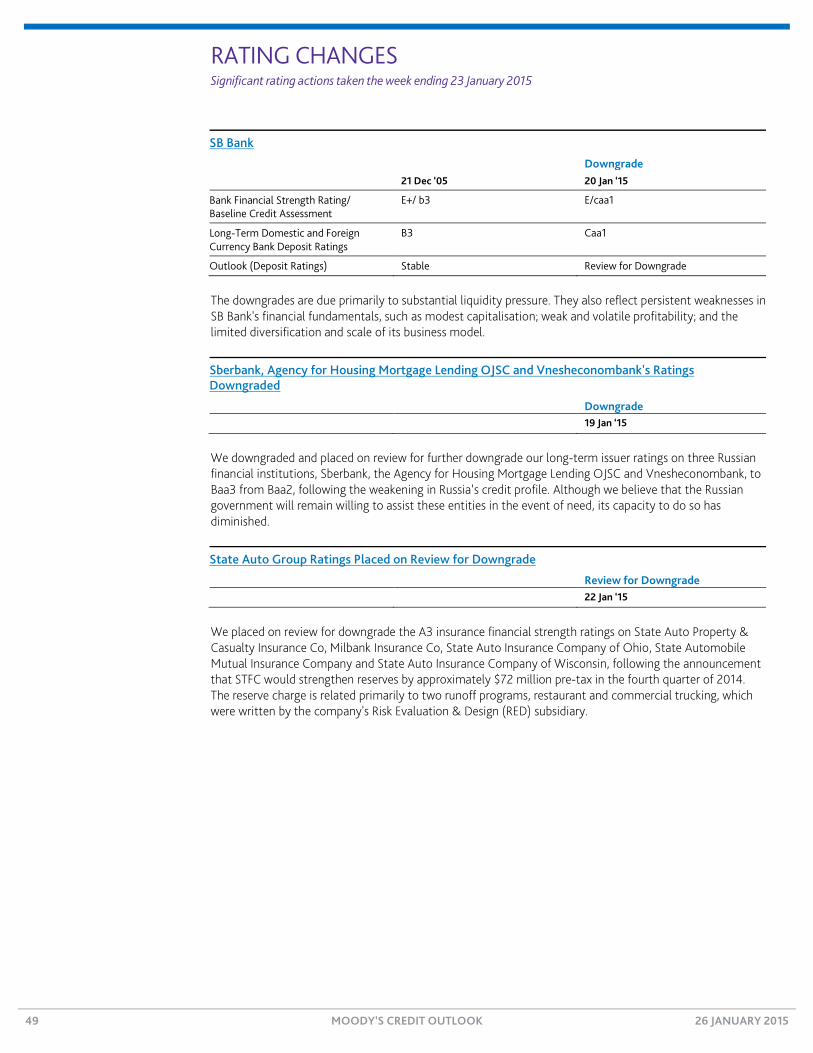

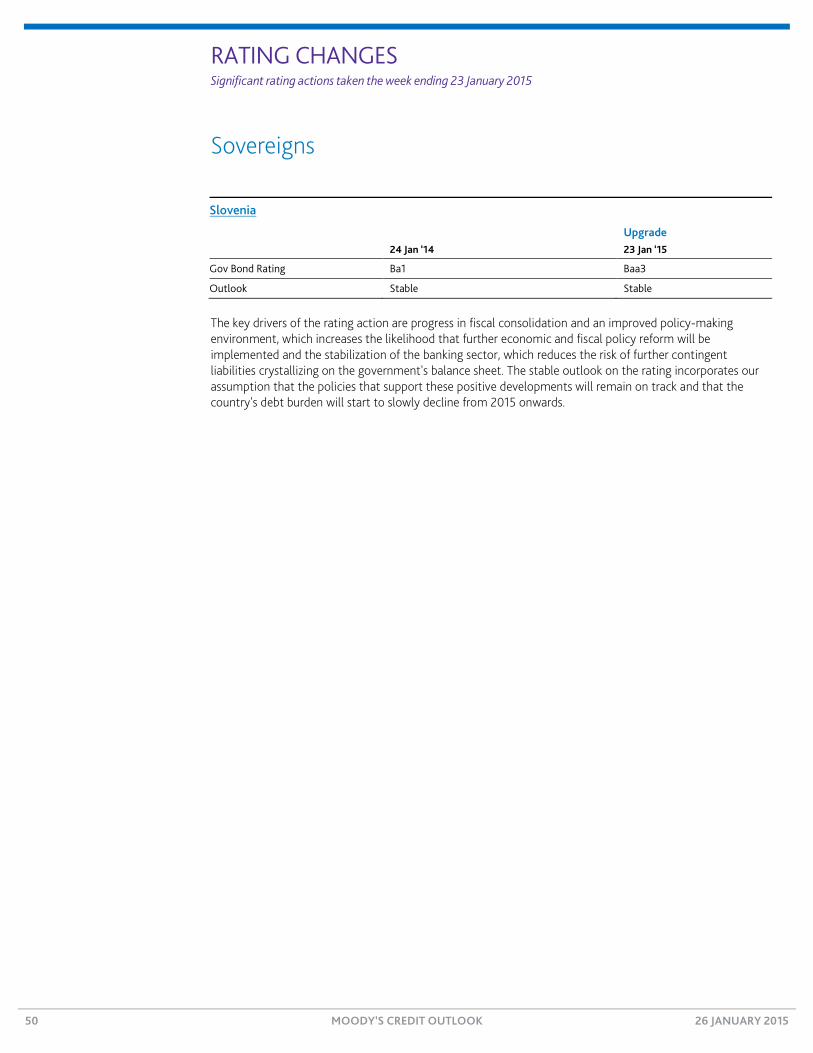

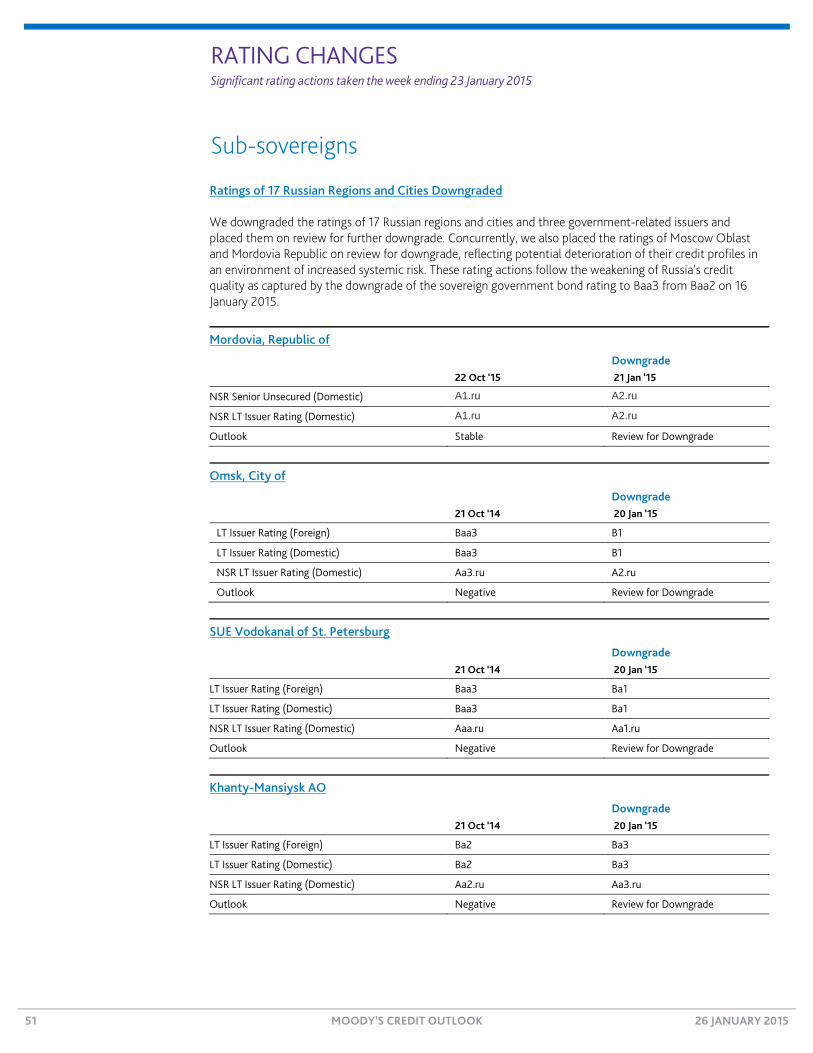

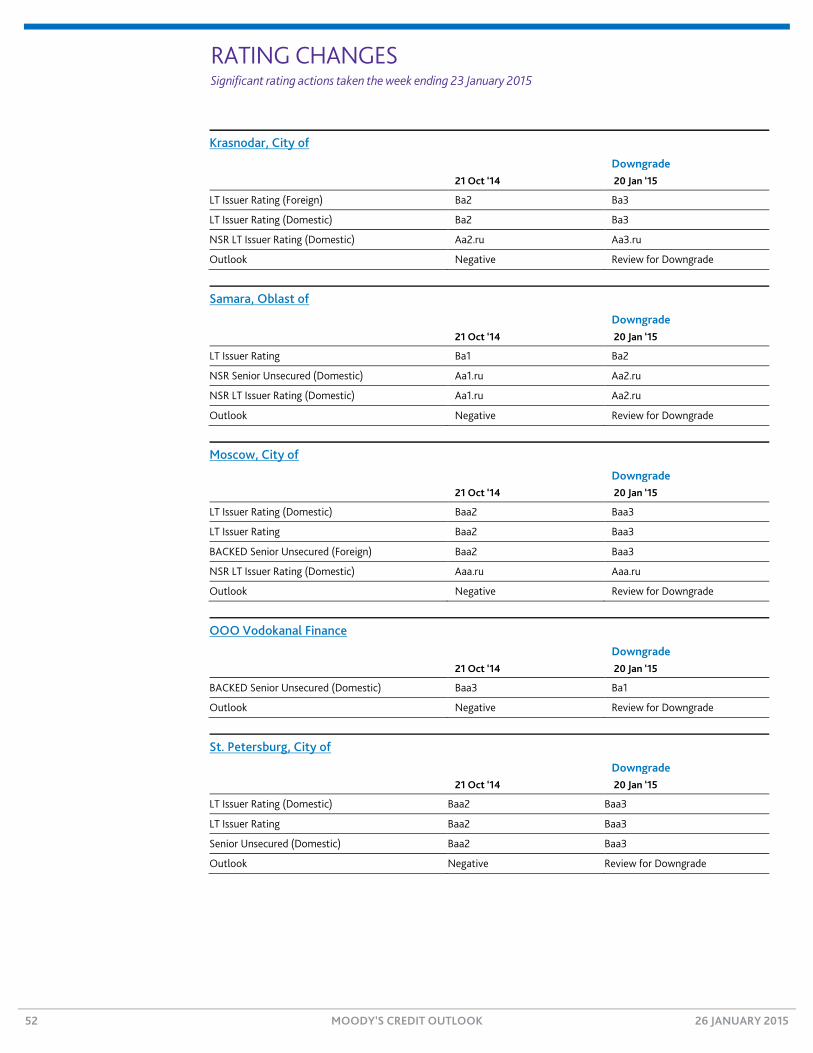

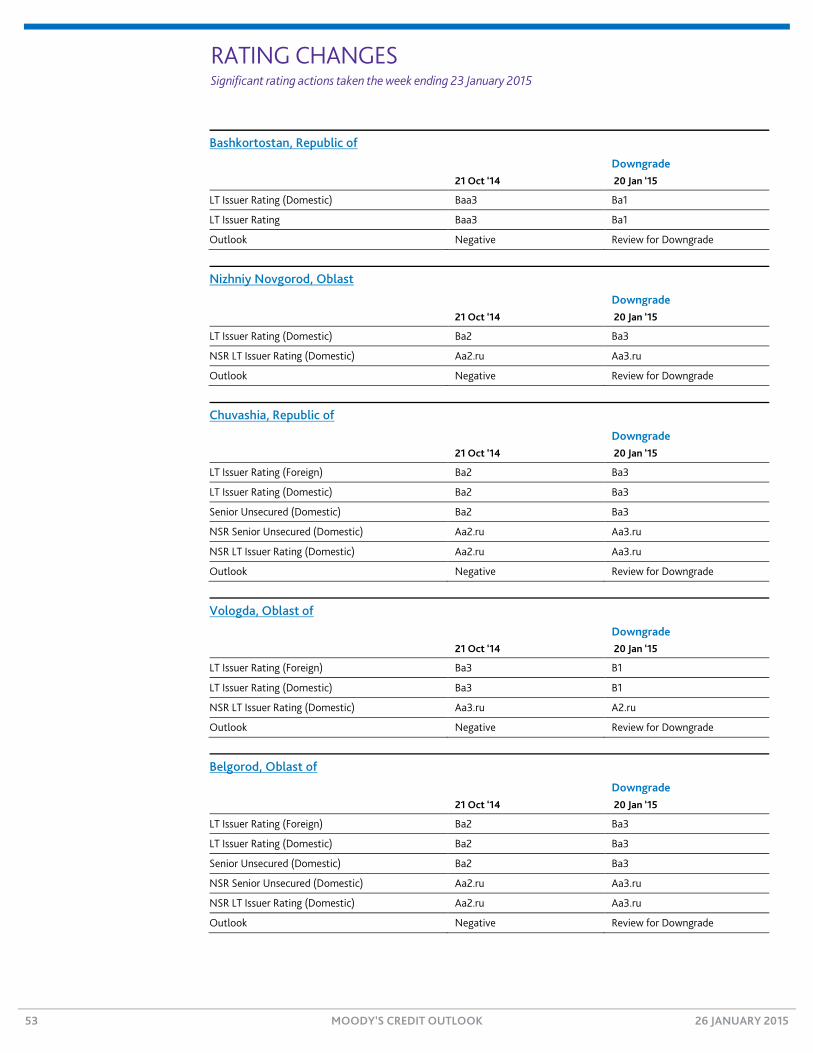

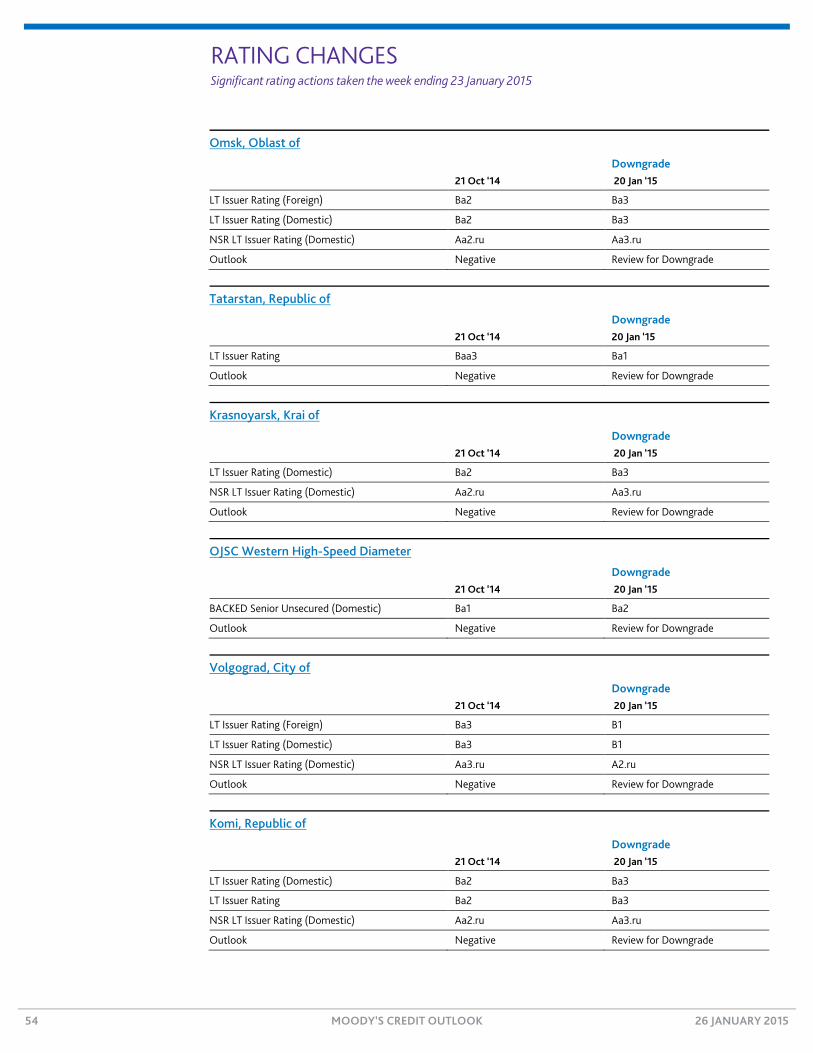

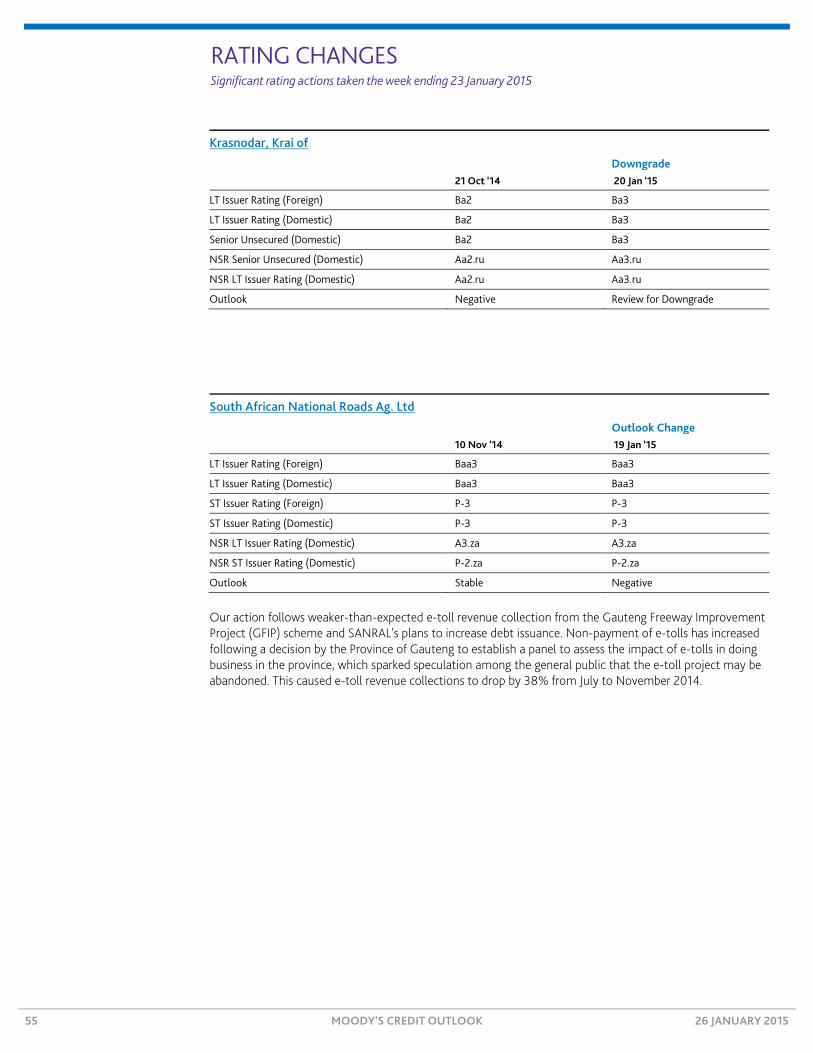

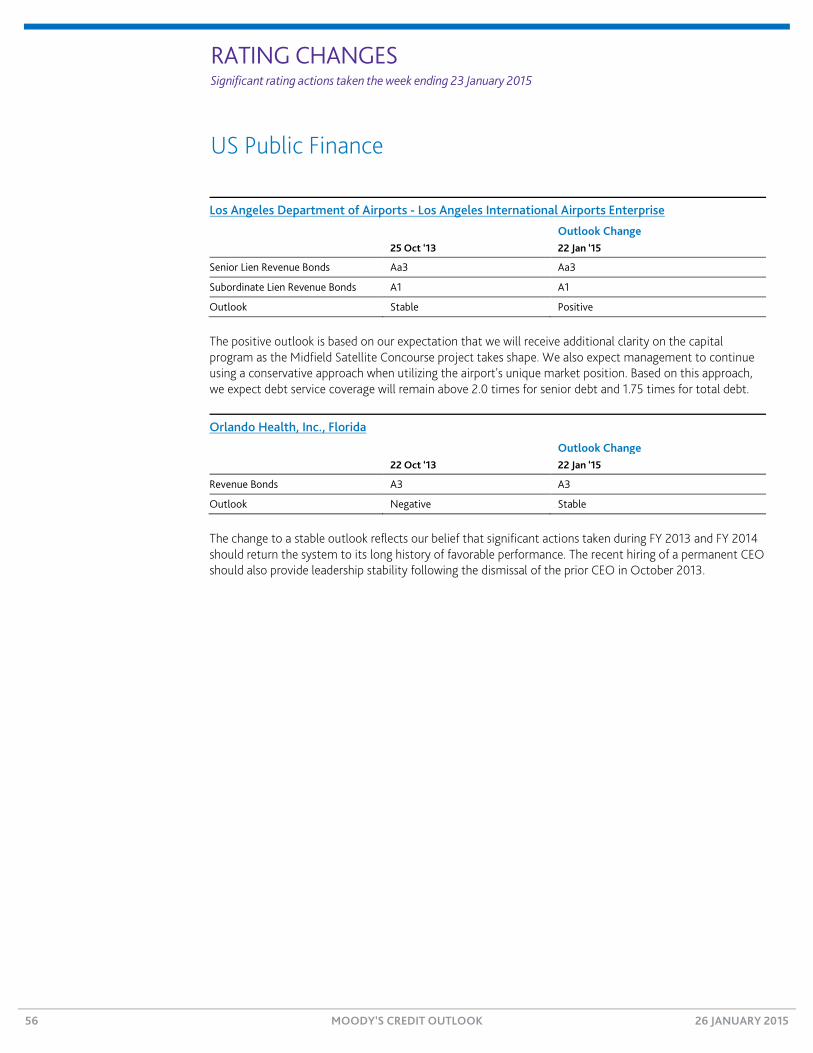

Last week, we downgraded Halcon Resources, Transneft, FGC UES, AHML Insurance, Russian Regional Development Bank, Far Eastern Bank, SB Bank, Sberbank, Agency for Housing Mortgage Lending, Vnesheconombank and 17 Russian regions and cities, and upgraded Derby Healthcare and Slovenia, among other rating actions.

Research Highlights 57

Last week, we reported on Chinese credits, Italian gaming, European and US high-yield, Southern Pacific Resource, European retail, Swiss corporates, airplane lessors, US banks, Latin American banks, Canadian banks, Spanish banks, global insurers, global financial guarantors, African sovereigns, shadow banking in the West and China, Cuba, Japanese regional and local governments, Pennsylvania school districts, Texas state and local governments, Japanese RMBS, US railcar ABS, global CLOs, solar ABS, Dutch RMBS and Indian RMBS, among other topics.

RECENTLY IN CREDIT OUTLOOK

» Articles in Last Monday’s Credit Outlook 62 » Go to Last Monday’s Credit Outlook

NEWS & ANALYSIS Credit implications of current events

2 MOODY’S CREDIT OUTLOOK 26 JANUARY 2015

Corporates

Clean Harbors’ Planned Carve-Out of Oil and Gas Services Is Credit Negative Last Monday, Clean Harbors, Inc. (Ba2 stable) said that it planned to carve out its oil and gas field services segment into a separate company and add its lodging drill camps business to the new publicly traded entity. The planned transaction is credit negative because it will increase leverage and reduce cash flow available to service debt.

Oil and gas segment revenues and margins have declined over the past year as weakening oil prices have adversely affected demand for its services, a trend that we expect to continue this year. The as-yet-unnamed new company will have annual revenues of $300-$350 million and EBITDA of about $50 million, about 10% of the Clean Harbors’ projections for both 2014 revenue and EBITDA. The transaction may not close for another year and is subject to regulatory, securities law compliance and final approval by Clean Harbors’ board.

The capital structure of the new company has not been established. Clean Harbors has not disclosed the amount of any distribution it may receive from the unit before or upon the initial public offering. The company has indicated that it would redeploy any proceeds about equally between share repurchases and future acquisitions, with no plan to reduce funded debt. As such, Clean Harbors’ leverage would edge higher. A pro forma reduction in trailing EBITDA of $50 million would push debt/EBITDA to about 3.9x from approximately 3.6x in September 2014 and close to the 4.0x threshold we have previously said could pressure the rating.

Clean Harbors said that it plans to launch an initial public offering of shares in the new entity on the Toronto Stock Exchange (the unit generates 60%-70% of its revenues in Canada) and will retain a significant -- and possibly majority -- interest in the company. If it does take a majority stake, and depending on control, the new company would remain consolidated in Clean Harbors’ operating results. However, the new company’s board and management would control operating cash flows, leaving Clean Harbors without direct access to these, other than to any potential dividend payouts or other intercompany arrangements.

Clean Harbors will not apply discontinued operations accounting in 2015 and has included the unit’s results in its initial guidance for 2015, which projects adjusted EBITDA of $530-$570 million, up about 7% from 2014. Upon completion of the carve-out and the loss of the new company’s expected $50 million of EBITDA, Clean Harbors’ 2015 pro forma EBITDA would decline by 7%-8% from its guidance for 2014.

Edwin Wiest Vice President - Senior Credit Officer +1.212.553.1461 [email protected]

This publication does not announce a credit rating action. For any credit ratings referenced in this publication, please see the ratings tab on the issuer/entity page on www.moodys.com for the most updated credit rating action information and rating history.

NEWS & ANALYSIS Credit implications of current events

3 MOODY’S CREDIT OUTLOOK 26 JANUARY 2015

Kinder Morgan Will Buy Hiland Partners, a Credit Positive for Hiland Kinder Morgan Inc. (KMI, Baa3 stable) on Wednesday said it would purchase Hiland Partners LP (B1 review for upgrade) for about $3 billion, including the assumption of the partnership's roughly $1.0 billion of outstanding debt.

The acquisition is credit positive for Hiland, whose ratings we put on review for upgrade because KMI will assume about $1 billion of Hiland’s debt, providing credit support for the small pipeline operator.

For KMI, the largest US midstream energy company in the US, which we project will generate nearly $8 billion of EBITDA in 2015, buying Hiland gives it its initial footprint in the Bakken Shale and helps diversify its crude transportation business, improving its business profile.

Hiland holds a first-mover and premier position in the prolific Bakken Shale, primarily in North Dakota, along with a significant acreage dedication from Continental Resources (Baa3 stable), the largest acreage holder in the Bakken. The recent completion of Hiland’s Double H Pipeline provides a much-needed outlet for crude production in the core of the Bakken region, an area in which it is still economic to drill and produce despite today’s depressed crude oil prices. We expect that about 85% of Hiland’s cash flow will be fee-based.

After its acquisition, depending on the level of explicit credit support KMI provides to Hiland, we would expect at least a one-notch upgrade in Hiland’s B2 senior unsecured note rating. The improvement could be as many as five notches — raising Hiland’s senior unsecured rating to KMI’s Baa3 level — if KMI provides an unconditional guarantee of Hiland’s $975 million of debt. Even without such a guarantee from KMI, Hiland’s credit quality will still get some boost from its affiliation with a much larger and stronger company.

Based on our expectations for Hiland’s 2015 EBITDA, we expect KMI’s purchase multiple for Hiland to be about 13x-14x, but to ultimately decline over the next two years to less than 10x with the further build out of Hiland’s pipeline system.

While initially financed with 100% debt, we expect that KMI will gradually manage down its leverage ratio so that the effect of the Hiland acquisition is credit neutral at worst, and possibly credit positive.

Stuart Miller Vice President - Senior Credit Officer +1.212.553.7991 [email protected]

NEWS & ANALYSIS Credit implications of current events

4 MOODY’S CREDIT OUTLOOK 26 JANUARY 2015

Petrofac Team Wins $4 Billion Oil Project Contract in Kuwait, a Credit Positive Last Tuesday, oil and gas construction company Petrofac Limited (Baa2 negative) announced that its partnership with Greece-based Consolidated Contractors Company (unrated) received a five-year, $4 billion engineering, procurement and construction and operations and maintenance contract from Kuwait Oil Company (KOC, unrated). The award is credit positive because it increases Petrofac’s backlog to a record of approximately $24 billion and is in an area where it has a strong execution track record. The contract also comes at a time when most oil and gas companies are cutting capital expenditures following a steep drop in crude prices. This latest contract highlights the benefit of Petrofac’s long-standing relationship with national oil companies in the Middle East.

The KOC contract is Petrofac’s 11th project in Kuwait, one of the few areas still awarding significant new projects. We expect that exploration and production capital expenditures in North America will decline by 30%-40%, while projects outside of North America will likely decline in 2015 by 10%-20%. Large companies in the Middle East are likely to alter their plans less swiftly because of the longer-term nature of their projects. On the other hand, even Qatar Petroleum (Aa2 stable) recently cancelled its approximately $6 billion Al-Karaana petrochemicals project owing to the current economic climate in the energy industry. We also expect that projects in countries such as Oman are now more likely to be delayed or even cancelled because of the negative effect of Brent crude falling below $50 per barrel.

Petrofac’s award is for the first phase of KOC’s Lower Fars heavy oil development programme, which is located in the north of the country, and involves greenfield and brownfield facilities, associated infrastructure and a production support complex. Heavy crude from the central processing facility will be transported via a 160-kilometer pipeline to South Tank Farm located in Ahmadi, Kuwait. KOC may be able to send the oil to the proposed Al-Zour refinery in the south of Kuwait.

KOC expects the initial phase of the Lower Fars project to produce around 60,000 barrels of oil daily once complete, with the engineering, procurement and construction part scheduled to last for 52 months, including 10 months of commissioning and ramp-up work. The Petrofac team will provide operations and maintenance after it hands over the plant to KOC for a further eight months.

As of 30 September 2014, Petrofac’s backlog was at an all-time high of $21 billion after its most successful year for new awards. However, it has had delays in the Greater Stella and Ticleni projects in its Integrated Energy Services division and expects reduced earnings from the Laggan-Tormore project in the UK in its core Onshore Engineering & Construction business.

We expect the company’s debt/EBITDA to remain at approximately 2.0x through 2015, which is high for its rating considering its recent execution difficulties and the likelihood of a more competitive environment amid lower oil prices and the challenge to continue growing its backlog. However, the KOC award increases Petrofac’s business onshore in the Middle East, where it has a strong execution track record. Petrofac is favoured to receive any award given the industry’s current challenges from lower oil prices.

Douglas Crawford Vice President - Senior Analyst +44.20.7772.5215 [email protected]

NEWS & ANALYSIS Credit implications of current events

5 MOODY’S CREDIT OUTLOOK 26 JANUARY 2015

Telefonica Enters Negotiations to Sell Its UK Subsidiary for £10 Billion, a Credit Positive On 23 January, Telefonica SA (Baa2 negative) announced that it had entered into exclusive negotiations with Hutchison Whampoa Limited (A3 stable) for a possible sale of its UK subsidiary O2 UK (unrated) for around £10.25 billion (€13.5 billion) in cash. The exclusive negotiation period will last several weeks and may or may not result in a final agreement.

A sale as outlined would be credit positive for Telefonica because it would receive around €13.5 billion in cash, part of which the company could use to reduce leverage, increase its capex program, make selective acquisitions within its operating footprint and enhance its shareholder remuneration.

Telefonica has prioritised deleveraging over shareholder remuneration for the past few years. Specifically, management has committed to reduce reported net debt to below €43 billion and has targeted a reported net debt/EBITDA ratio of 2.35x.

However, even if the two companies agree on a deal, the regulatory approval process will be lengthy, delaying debt reduction. We expect substantial regulatory remedies would be imposed as a sale implies reducing the number of mobile players in the UK to three from four. Therefore, the companies do not expect a potential sale to close before 2016. Consequently, any debt reduction from this deal would occur in 2016, leaving Telefonica’s credit metrics broadly unchanged over the next 12 months.

Telefonica’s group revenue is likely to trend toward marginal growth in 2015 and its Moody’s-adjusted EBITDA margin will remain broadly stable at 32%-34% in 2015. We expect lower cash flow ratios, with adjusted retained cash flow/net debt at 19%-20% and free cash flow/net debt below 3%. We also anticipate funds from operations coverage in the 5.0x-6.0x range and an (EBITDA minus capex)/gross interest expense ratio of around 2.5x-3.0x. In terms of leverage, we expect adjusted net debt/EBITDA to remain tightly within our guidance for a Baa2 rating at around 2.8x in 2015.

Our current negative outlook on Telefonica´s ratings reflects the group’s challenging domestic operating environment, which puts pressure on cash-flow-derived financial ratios. Despite the fact that Telefonica’s international diversification enhances its credit profile, the group’s exposure to the domestic market puts it at risk given Spain's contraction in consumer spending.

Carlos Winzer Senior Vice President +34.91.702.6610 [email protected]

NEWS & ANALYSIS Credit implications of current events

6 MOODY’S CREDIT OUTLOOK 26 JANUARY 2015

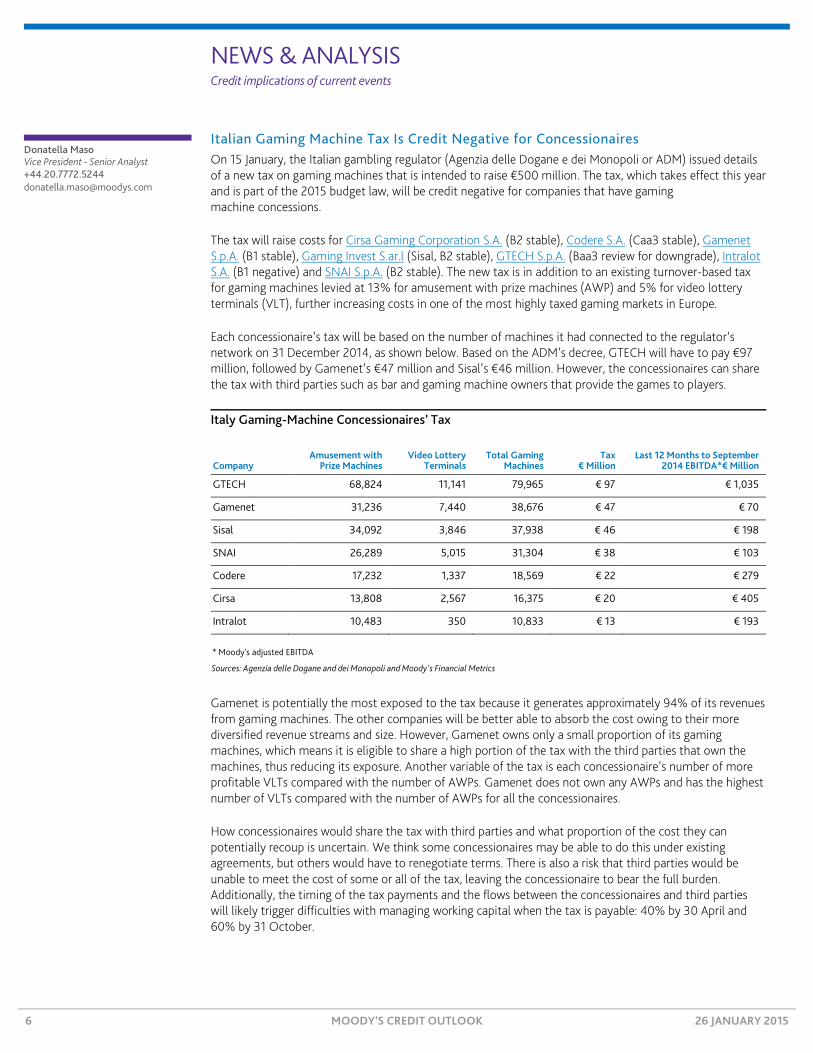

Italian Gaming Machine Tax Is Credit Negative for Concessionaires On 15 January, the Italian gambling regulator (Agenzia delle Dogane e dei Monopoli or ADM) issued details of a new tax on gaming machines that is intended to raise €500 million. The tax, which takes effect this year and is part of the 2015 budget law, will be credit negative for companies that have gaming machine concessions.

The tax will raise costs for Cirsa Gaming Corporation S.A. (B2 stable), Codere S.A. (Caa3 stable), Gamenet S.p.A. (B1 stable), Gaming Invest S.ar.l (Sisal, B2 stable), GTECH S.p.A. (Baa3 review for downgrade), Intralot S.A. (B1 negative) and SNAI S.p.A. (B2 stable). The new tax is in addition to an existing turnover-based tax for gaming machines levied at 13% for amusement with prize machines (AWP) and 5% for video lottery terminals (VLT), further increasing costs in one of the most highly taxed gaming markets in Europe.

Each concessionaire’s tax will be based on the number of machines it had connected to the regulator’s network on 31 December 2014, as shown below. Based on the ADM’s decree, GTECH will have to pay €97 million, followed by Gamenet’s €47 million and Sisal’s €46 million. However, the concessionaires can share the tax with third parties such as bar and gaming machine owners that provide the games to players.

Italy Gaming-Machine Concessionaires’ Tax

Company Amusement with

Prize Machines Video Lottery

Terminals Total Gaming

Machines Tax

€ Million Last 12 Months to September

2014 EBITDA*€ Million

GTECH 68,824 11,141 79,965 € 97 € 1,035

Gamenet 31,236 7,440 38,676 € 47 € 70

Sisal 34,092 3,846 37,938 € 46 € 198

SNAI 26,289 5,015 31,304 € 38 € 103

Codere 17,232 1,337 18,569 € 22 € 279

Cirsa 13,808 2,567 16,375 € 20 € 405

Intralot 10,483 350 10,833 € 13 € 193

* Moody's adjusted EBITDA

Sources: Agenzia delle Dogane and dei Monopoli and Moody's Financial Metrics

Gamenet is potentially the most exposed to the tax because it generates approximately 94% of its revenues from gaming machines. The other companies will be better able to absorb the cost owing to their more diversified revenue streams and size. However, Gamenet owns only a small proportion of its gaming machines, which means it is eligible to share a high portion of the tax with the third parties that own the machines, thus reducing its exposure. Another variable of the tax is each concessionaire’s number of more profitable VLTs compared with the number of AWPs. Gamenet does not own any AWPs and has the highest number of VLTs compared with the number of AWPs for all the concessionaires.

How concessionaires would share the tax with third parties and what proportion of the cost they can potentially recoup is uncertain. We think some concessionaires may be able to do this under existing agreements, but others would have to renegotiate terms. There is also a risk that third parties would be unable to meet the cost of some or all of the tax, leaving the concessionaire to bear the full burden. Additionally, the timing of the tax payments and the flows between the concessionaires and third parties will likely trigger difficulties with managing working capital when the tax is payable: 40% by 30 April and 60% by 31 October.

Donatella Maso Vice President - Senior Analyst +44.20.7772.5244 [email protected]

NEWS & ANALYSIS Credit implications of current events

7 MOODY’S CREDIT OUTLOOK 26 JANUARY 2015

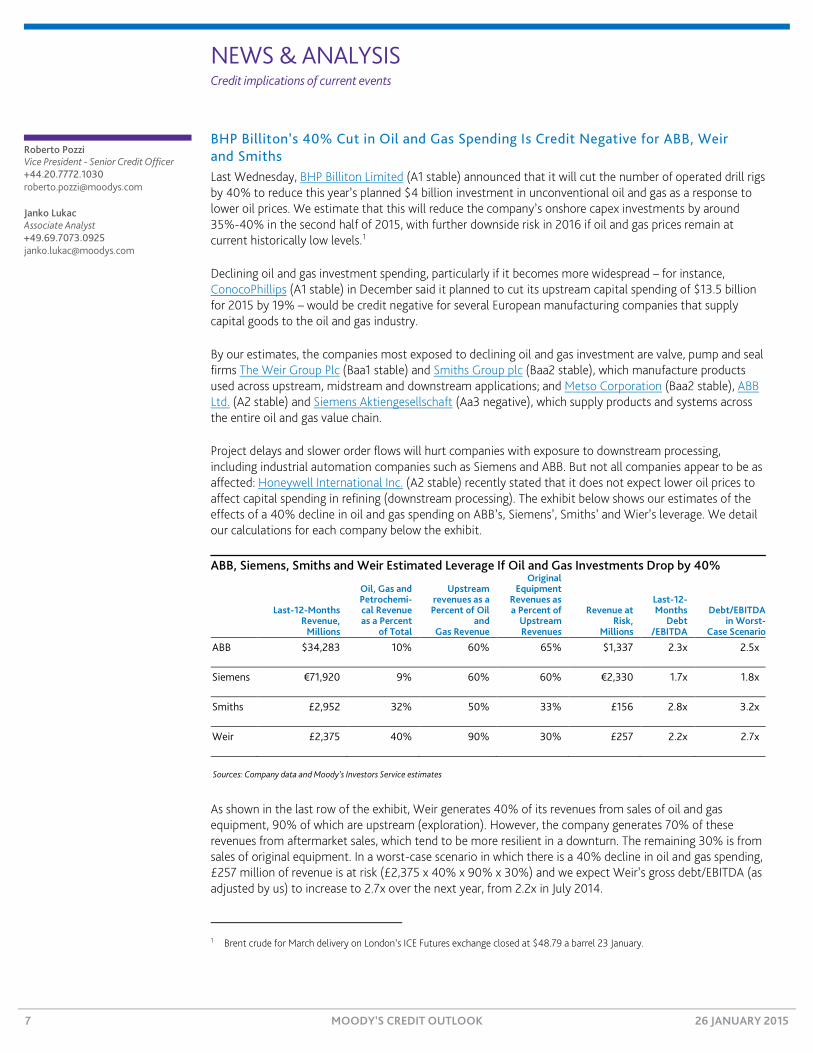

BHP Billiton’s 40% Cut in Oil and Gas Spending Is Credit Negative for ABB, Weir and Smiths Last Wednesday, BHP Billiton Limited (A1 stable) announced that it will cut the number of operated drill rigs by 40% to reduce this year’s planned $4 billion investment in unconventional oil and gas as a response to lower oil prices. We estimate that this will reduce the company’s onshore capex investments by around 35%-40% in the second half of 2015, with further downside risk in 2016 if oil and gas prices remain at current historically low levels.1

Declining oil and gas investment spending, particularly if it becomes more widespread – for instance, ConocoPhillips (A1 stable) in December said it planned to cut its upstream capital spending of $13.5 billion for 2015 by 19% – would be credit negative for several European manufacturing companies that supply capital goods to the oil and gas industry.

By our estimates, the companies most exposed to declining oil and gas investment are valve, pump and seal firms The Weir Group Plc (Baa1 stable) and Smiths Group plc (Baa2 stable), which manufacture products used across upstream, midstream and downstream applications; and Metso Corporation (Baa2 stable), ABB Ltd. (A2 stable) and Siemens Aktiengesellschaft (Aa3 negative), which supply products and systems across the entire oil and gas value chain.

Project delays and slower order flows will hurt companies with exposure to downstream processing, including industrial automation companies such as Siemens and ABB. But not all companies appear to be as affected: Honeywell International Inc. (A2 stable) recently stated that it does not expect lower oil prices to affect capital spending in refining (downstream processing). The exhibit below shows our estimates of the effects of a 40% decline in oil and gas spending on ABB’s, Siemens’, Smiths’ and Wier’s leverage. We detail our calculations for each company below the exhibit.

ABB, Siemens, Smiths and Weir Estimated Leverage If Oil and Gas Investments Drop by 40%

Last-12-Months Revenue,

Millions

Oil, Gas and Petrochemi-cal Revenue as a Percent

of Total

Upstream revenues as a

Percent of Oil and

Gas Revenue

Original Equipment

Revenues as a Percent of

Upstream Revenues

Revenue at Risk,

Millions

Last-12-Months

Debt /EBITDA

Debt/EBITDA in Worst-

Case Scenario

ABB $34,283 10% 60% 65% $1,337 2.3x 2.5x

Siemens €71,920 9% 60% 60% €2,330 1.7x 1.8x

Smiths £2,952 32% 50% 33% £156 2.8x 3.2x

Weir £2,375 40% 90% 30% £257 2.2x 2.7x

Sources: Company data and Moody’s Investors Service estimates

As shown in the last row of the exhibit, Weir generates 40% of its revenues from sales of oil and gas equipment, 90% of which are upstream (exploration). However, the company generates 70% of these revenues from aftermarket sales, which tend to be more resilient in a downturn. The remaining 30% is from sales of original equipment. In a worst-case scenario in which there is a 40% decline in oil and gas spending, £257 million of revenue is at risk (£2,375 x 40% x 90% x 30%) and we expect Weir’s gross debt/EBITDA (as adjusted by us) to increase to 2.7x over the next year, from 2.2x in July 2014.

1 Brent crude for March delivery on London’s ICE Futures exchange closed at $48.79 a barrel 23 January.

Roberto Pozzi Vice President - Senior Credit Officer +44.20.7772.1030 [email protected]

Janko Lukac Associate Analyst +49.69.7073.0925 [email protected]

NEWS & ANALYSIS Credit implications of current events

8 MOODY’S CREDIT OUTLOOK 26 JANUARY 2015

We expect Smiths’ debt/EBITDA to deteriorate to 3.2x under the same worst-case scenario, from 2.8x as of July 2014. We estimate that 32% of Smiths revenue comes from oil and gas equipment and 50% of that from upstream, while the rest comes from refining and petrochemicals operations. One third of this exposure is from sales of original equipment, which will be affected by lower oil prices, while the remainder is aftermarket sales, which will be unaffected.

We estimate that 10% of ABB’s revenues come from sales of oil and gas equipment, mostly from ABB’s Process Automation segment. Of that amount, 60% is from equipment sold upstream, of which around 65% is original equipment. In a worst-case scenario, we expect ABB’s debt/EBITDA to deteriorate to 2.5x from 2.3x in September 2014.

Diversification should help Siemens offset much of the weakness in its energy units following significant investments in oil and gas equipment last year. We expect Siemens to generate 10% of sales from oil and gas equipment, including revenues from Dresser-Rand Group Inc. (Ba2 review for upgrade), which Siemens is in the process of acquiring. Sixty-percent of Siemens oil and gas equipment sales are in the upstream segment, which will most likely be affected by spending cuts. Considering that aftermarket constitutes around 40% of Siemens’ oil and gas revenue, we expect the company’s debt/EBITDA to increase to 1.8x from 1.7x in September 2014 in a worst-case scenario using the same 40% decline in oil and gas revenues.

NEWS & ANALYSIS Credit implications of current events

9 MOODY’S CREDIT OUTLOOK 26 JANUARY 2015

GPT Group’s Redemption of Exchangeable Securities Is Credit Positive Last Wednesday, The GPT Group (A3 stable) announced that it had entered into an agreement with an affiliate of Singapore-based sovereign wealth fund GIC (unrated) to fully redeem the exchangeable securities that the company had issued during the height of the global financial crisis. GPT will redeem the securities for AUD325 million, plus accrued distribution, and will fully fund the redemption with an equity raise. The transaction is credit positive for GPT because it replaces high-cost capital with ordinary equity. Moreover, the transaction further demonstrates the company’s conservative financial policies and commitment to solid credit metrics.

The exchangeable securities, which have a face value of AUD250 million, are an expensive perpetual instrument with a fixed distribution rate of 10% per year. This has resulted in an annual distribution of AUD25 million since the company issued the securities in November 2008, compared with an ordinary equity distribution rate of about 5.6% for 2014. Moreover, the replacement of exchangeable securities with ordinary equity points to the company now having more permanent equity on its balance sheet and provides additional flexibility around distributions.

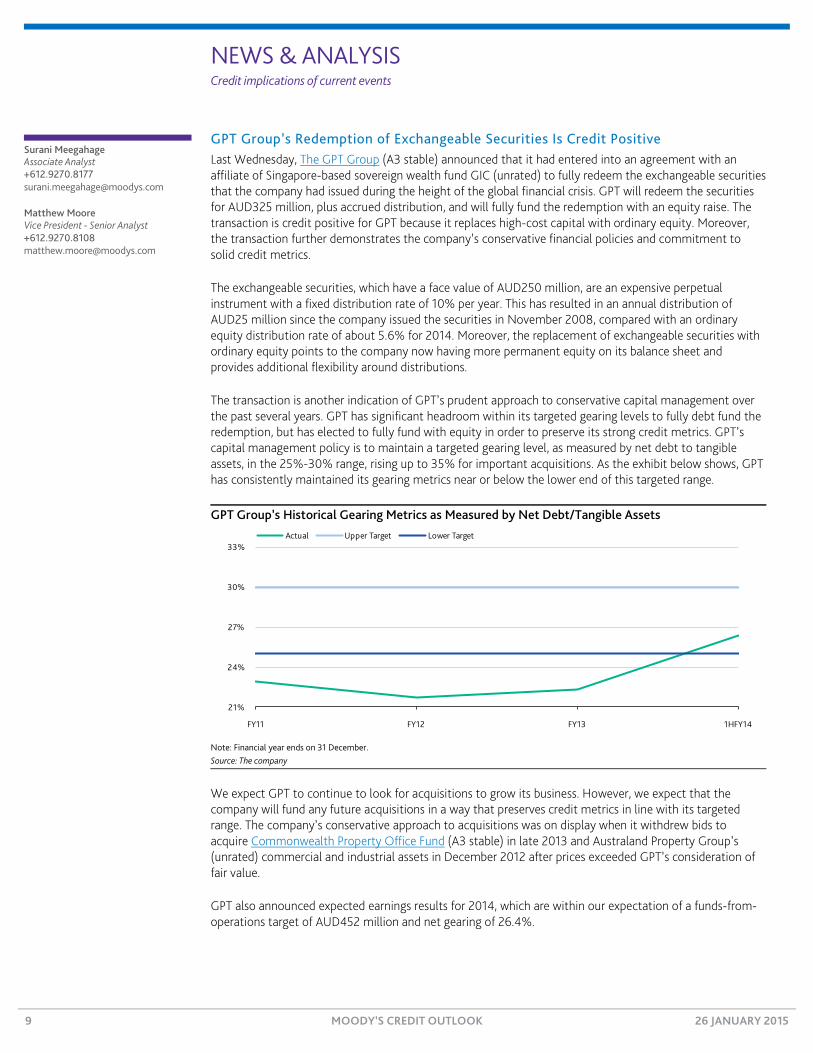

The transaction is another indication of GPT’s prudent approach to conservative capital management over the past several years. GPT has significant headroom within its targeted gearing levels to fully debt fund the redemption, but has elected to fully fund with equity in order to preserve its strong credit metrics. GPT’s capital management policy is to maintain a targeted gearing level, as measured by net debt to tangible assets, in the 25%-30% range, rising up to 35% for important acquisitions. As the exhibit below shows, GPT has consistently maintained its gearing metrics near or below the lower end of this targeted range.

GPT Group’s Historical Gearing Metrics as Measured by Net Debt/Tangible Assets

Note: Financial year ends on 31 December. Source: The company

We expect GPT to continue to look for acquisitions to grow its business. However, we expect that the company will fund any future acquisitions in a way that preserves credit metrics in line with its targeted range. The company’s conservative approach to acquisitions was on display when it withdrew bids to acquire Commonwealth Property Office Fund (A3 stable) in late 2013 and Australand Property Group’s (unrated) commercial and industrial assets in December 2012 after prices exceeded GPT’s consideration of fair value.

GPT also announced expected earnings results for 2014, which are within our expectation of a funds-from-operations target of AUD452 million and net gearing of 26.4%.

21%

24%

27%

30%

33%

FY11 FY12 FY13 1HFY14

Actual Upper Target Lower Target

Surani Meegahage Associate Analyst +612.9270.8177 [email protected]

Matthew Moore Vice President - Senior Analyst +612.9270.8108 [email protected]

NEWS & ANALYSIS Credit implications of current events

10 MOODY’S CREDIT OUTLOOK 26 JANUARY 2015

CITIC Limited and CITIC Group Will Benefit from Itochu’s and Charoen Pokphand’s Equity Investment On 20 January, Japan-based Itochu Corporation (Baa1 review for downgrade) and Thailand-based Charoen Pokphand Group Company Limited (CPG, unrated) announced that they will buy a 20% stake in Hong Kong-based CITIC Limited (A3 stable) for a total of HKD80 billion ($10.4 billion).

The investment is credit positive for CITIC Limited and CITIC Group Corporation (A3 stable) because it will strengthen their financial and business profiles. The investment is credit negative for Itochu and we put its ratings on review for downgrade.

Pending shareholder and regulatory approvals, Itochu and CPG will invest through a 50-50 joint venture by subscribing to CITIC Limited’s convertible preferred shares for around HKD45.92 billion; and by acquiring about 10% of CITIC Limited from CITIC Group for around HKD34.37 billion.

Upon completion of the transactions and the full conversion of the preferred shares into common shares, the Itochu-CPG joint venture will own around a 20% stake in CITIC Limited. CITIC Group’s total ownership share in CITIC Limited will fall to around 60% from 78%.

We expect that CITIC Limited will use the HKD45.92 billion of proceeds to support business growth and to repay debt. Assuming half of the HKD45.92 billion is used to repay debt, we estimate that CITIC Limited’s reported consolidated debt/capitalization ratio would fall to around 36% from 40% at end of first- half 2014.

CITIC Group’s cash proceeds of HKD34.37 billion will strengthen its liquidity. The company will also have an enlarged equity basis from the transactions. Assuming half of the HKD45.92 billion is used to repay debt and capital gain or loss from the stake transfer, we estimate that CITIC Group’s reported consolidated debt/capitalization ratio would fall to around 44% from 48% at end of 2013.

The strategic alliance between CITIC Limited, Itochu and CPG will enhance CITIC Group and CITIC Limited’s business profiles, given that the three companies are the leading conglomerates in their respective home bases. CITIC Limited will also be able to access business opportunities outside of China and the introduction of new third-party shareholders in CITIC Limited will help improve the government-related entity’s corporate governance and operational efficiency. The transactions follow CITIC Group and CITIC Limited’s restructuring last year, which we viewed as a pilot for the introduction of government reforms to improve the operations of state-owned enterprises.

The transactions have no immediate effect on CITIC Group and CITIC Limited’s ratings because part of the proceeds will likely be used to fund the companies’ growth, rather than for debt repayment. The dilution of CITIC Group’s stake in CITIC Limited to 60% will not materially weaken the parent’s support for CITIC Limited, nor the strong support that CITIC Group is likely to receive from the government of China (Aa3 stable) in times of need.

Kai Hu Vice President - Senior Credit Officer +86.21.6101.0553 [email protected]

NEWS & ANALYSIS Credit implications of current events

11 MOODY’S CREDIT OUTLOOK 26 JANUARY 2015

Itochu’s ¥600 Billion Investment in CITIC Limited Is Credit Negative Last Tuesday, Itochu Corporation (Baa1 review for downgrade), a leading Japanese trading company, announced that it and Charoen Pokphand Group Company Limited (CPG, unrated) had agreed to jointly invest in CITIC Limited (A3 stable) by acquiring a 20% stake. The total value of the proposed strategic investment, which the companies will complete using a 50-50 joint investment vehicle, is HKD80 billion ($10.4 billion), of which Itochu’s investment will be HKD40 billion.

The investment is credit negative for Itochu because the transaction, if successfully concluded, would involve a significant cash outlay for Itochu and would likely put material negative pressure on the company’s free cash flow and leverage. Consequently, we put Itochu’s ratings on review for downgrade.

The transaction cost of approximately ¥600 billion equals about 26% of Itochu’s total shareholders’ equity as of 30 September 2014 and will be the largest single investment in the company’s more than 150-year history. Assuming that the investment will be fully funded by additional borrowing and not offset by other asset sales, Itochu’s gross debt will increase by 20% to ¥3.6 trillion from around ¥3.0 trillion as of the end of September 2014.

Also, Itochu will be exposed to the refinancing risk of CPG because as part of the capital participation plan, Itochu will initially grant a shareholder loan to the investment vehicle for the acquisition cost that will include a part of the funding portion for CPG.

The investment’s positive benefits include increasing Itochu’s business diversification and further strengthening its position in China and other Asia markets. Among major Japanese trading companies, Itochu has a long history of investing in China, and has a strong presence there. Nevertheless, whether Itochu will be able to generate sufficient returns from this deal within a reasonable time frame to pay back its investment remains uncertain, as does the rate of deleveraging that will occur from the flow of dividends. As a result, if this investment does not generate synergy and cash flow levels that meet the company’s expectations, Itochu may need to pare back the effect of its investment in CITIC by paying down debt through sales of existing assets.

Maki Hanatate Vice President - Senior Credit Officer +81.3.5408.4029 [email protected]

NEWS & ANALYSIS Credit implications of current events

12 MOODY’S CREDIT OUTLOOK 26 JANUARY 2015

Infrastructure

Argentina’s Provinces Agree to Freeze Electricity Tariffs Until December, a Credit Negative On 15 January, Argentina’s Ministry of Infrastructure announced the incorporation of the Province of Salta to the Electricity Convergence Federal Plan, extending the plan from 2014. Including Salta, 16 of Argentina’s 23 provinces agreed with federal authorities to freeze electricity distribution tariffs until December this year. While the provincial distribution companies agree to freeze tariffs, the federal plan aims to periodically compensate their increased costs and expenses owing to high inflation that is not transferred to end consumers.

The agreement will add volatility to the cash flows of Argentina’s electric distribution companies because we expect that payments from the federal compensation program will be regularly delayed compared to direct and timely collections from consumers. For example, we estimate federal compensation payments to Empresa Distribuidora de Electricidad Salta (EDESA, Caa1 negative), are around 15% of total revenues.

In addition, the agreement negatively affects transparency in the electricity distribution sector, curtails the autonomy of provincial regulators and increases federal government discretion in provincial regulations. Provincial regulators have historically been more supportive and predictable than federal regulators. Provincial regulators’ cost-monitoring mechanisms and tariff-rate reviews periodically allowed tariff increases, enabling provincial electric distribution companies to sustain their margins and cash flows. This situation differed substantially from the tariff regulation of federal electric distribution companies, which have been frozen since 2007. The freeze has resulted in federal electric distribution companies being unable to cover their operating costs and reducing investments in the network. However, the plan aims to provide resources for higher federal investments in infrastructure to improve the quality of the distribution network.

The Electricity Convergence Federal Plan program, originally implemented in the second quarter of 2014, established that the provinces should follow the federal government electricity policy of not increasing electric distribution tariffs until the end of that year. The federal government will compensate the companies to help them cope with their increased costs and required CAPEX.

The federal cost-compensation plan has, until now, properly balanced provincial electric distribution companies growing operating costs and higher capex. This has been the case for EDESA, which was able to sustain its margins and capex requirements within the convergence program. However, we expect that Argentina’s inflationary pressures in 2015 and very weak growth, which we expect to be flat this year and 1% in 2016, will make it difficult for the federal government to maintain these payments.

So far, for 2015, the participating provinces are Formosa (Caa2 negative), Mendoza (Caa2 negative), Buenos Aires (Caa2 negative), and Jujuy, Santa Cruz, Tierra del Fuego, Neuquén, Santiago del Estero, La Rioja, Entre Ríos, Tucumán, Misiones, San Juan, La Pampa, Catamarca and Salta (all unrated). As in 2014, we expect that the remaining seven provinces will follow.

Christián Hermann Associate Analyst +54.11.5129.2616 [email protected]

NEWS & ANALYSIS Credit implications of current events

13 MOODY’S CREDIT OUTLOOK 26 JANUARY 2015

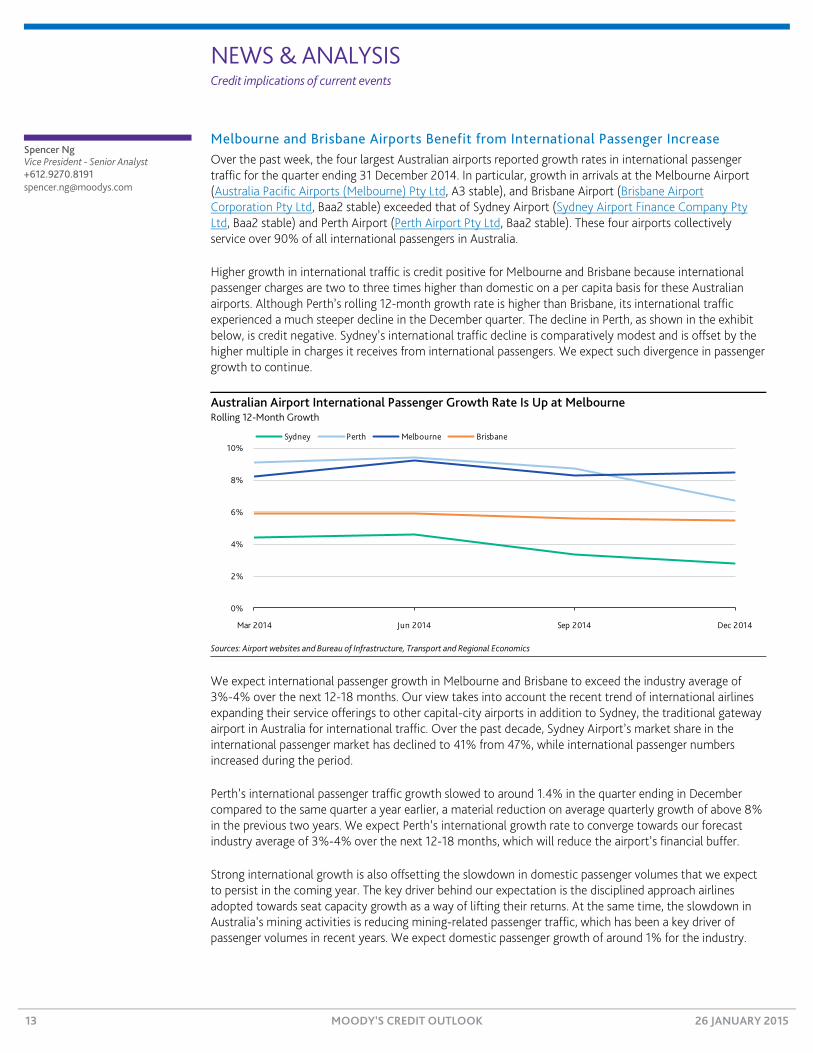

Melbourne and Brisbane Airports Benefit from International Passenger Increase Over the past week, the four largest Australian airports reported growth rates in international passenger traffic for the quarter ending 31 December 2014. In particular, growth in arrivals at the Melbourne Airport (Australia Pacific Airports (Melbourne) Pty Ltd, A3 stable), and Brisbane Airport (Brisbane Airport Corporation Pty Ltd, Baa2 stable) exceeded that of Sydney Airport (Sydney Airport Finance Company Pty Ltd, Baa2 stable) and Perth Airport (Perth Airport Pty Ltd, Baa2 stable). These four airports collectively service over 90% of all international passengers in Australia.

Higher growth in international traffic is credit positive for Melbourne and Brisbane because international passenger charges are two to three times higher than domestic on a per capita basis for these Australian airports. Although Perth’s rolling 12-month growth rate is higher than Brisbane, its international traffic experienced a much steeper decline in the December quarter. The decline in Perth, as shown in the exhibit below, is credit negative. Sydney’s international traffic decline is comparatively modest and is offset by the higher multiple in charges it receives from international passengers. We expect such divergence in passenger growth to continue.

Australian Airport International Passenger Growth Rate Is Up at Melbourne Rolling 12-Month Growth

Sources: Airport websites and Bureau of Infrastructure, Transport and Regional Economics

We expect international passenger growth in Melbourne and Brisbane to exceed the industry average of 3%-4% over the next 12-18 months. Our view takes into account the recent trend of international airlines expanding their service offerings to other capital-city airports in addition to Sydney, the traditional gateway airport in Australia for international traffic. Over the past decade, Sydney Airport’s market share in the international passenger market has declined to 41% from 47%, while international passenger numbers increased during the period.

Perth’s international passenger traffic growth slowed to around 1.4% in the quarter ending in December compared to the same quarter a year earlier, a material reduction on average quarterly growth of above 8% in the previous two years. We expect Perth’s international growth rate to converge towards our forecast industry average of 3%-4% over the next 12-18 months, which will reduce the airport’s financial buffer.

Strong international growth is also offsetting the slowdown in domestic passenger volumes that we expect to persist in the coming year. The key driver behind our expectation is the disciplined approach airlines adopted towards seat capacity growth as a way of lifting their returns. At the same time, the slowdown in Australia’s mining activities is reducing mining-related passenger traffic, which has been a key driver of passenger volumes in recent years. We expect domestic passenger growth of around 1% for the industry.

0%

2%

4%

6%

8%

10%

Mar 2014 Jun 2014 Sep 2014 Dec 2014

Sydney Perth Melbourne Brisbane

Spencer Ng Vice President - Senior Analyst +612.9270.8191 [email protected]

NEWS & ANALYSIS Credit implications of current events

14 MOODY’S CREDIT OUTLOOK 26 JANUARY 2015

Continued growth in international passenger traffic will also support Melbourne and Brisbane airports’ ability to maintain their financial profiles by generating the revenues they require to help fund their substantial capital programs. Over the next five years, both of these airports have plans to undertake major capital expansion projects that include terminal expansions and development of new runways that could commence after 2018 at an aggregate capital cost of more than AUD3 billion.

A material source of risk to our expectations – both upside and downside – is the effect of a lower Australian dollar on international passenger traffic. Over the past six months, the Australian dollar has declined, and was USD0.79 on 23 January, down from a peak of around USD0.95. A weaker currency increases Australia’s attractiveness to international visitors which should benefit the airports. While overseas travel by Australians could decline as a result of the softer currency, there is likely to be an increase in domestic flights, which should partly offset that effect.

NEWS & ANALYSIS Credit implications of current events

15 MOODY’S CREDIT OUTLOOK 26 JANUARY 2015

Banks

Surprise Canadian Rate Cut Is Credit Negative for Banks On Wednesday, the Bank of Canada unexpectedly cut the overnight lending rate 25 basis points to 0.75%, its first rate change since September 2010. The rate cut is credit negative for Canadian banks because it will pressure already-compressed net interest margins.

The rate cut comes as Canadian banks are already facing margin compression as a result of persistently low interest rates. Net interest margins, which measure the difference between interest income and interest expense relative to interest-earning assets, have been on a downward trend and will be further subdued as a result of this cut. Canadian banks are also facing profitability headwinds as a result of declining oil prices, weak trading revenue and slowing growth in consumer lending.

Although the 25 basis point rate cut is modest, most market participants expected the central bank’s next move to be a rate increase, tightening monetary policy amid rising home prices and debt burdens for Canadian households. In the Monetary Policy Report released on Wednesday, the central bank said that although the sharp drop in oil prices has provided some anticipated boost to economic growth outside the energy sector, there is considerable uncertainty around the outlook. The central bank views the rate cut as insurance against the downside risks associated with the oil price shock on the inflation outlook and financial stability.

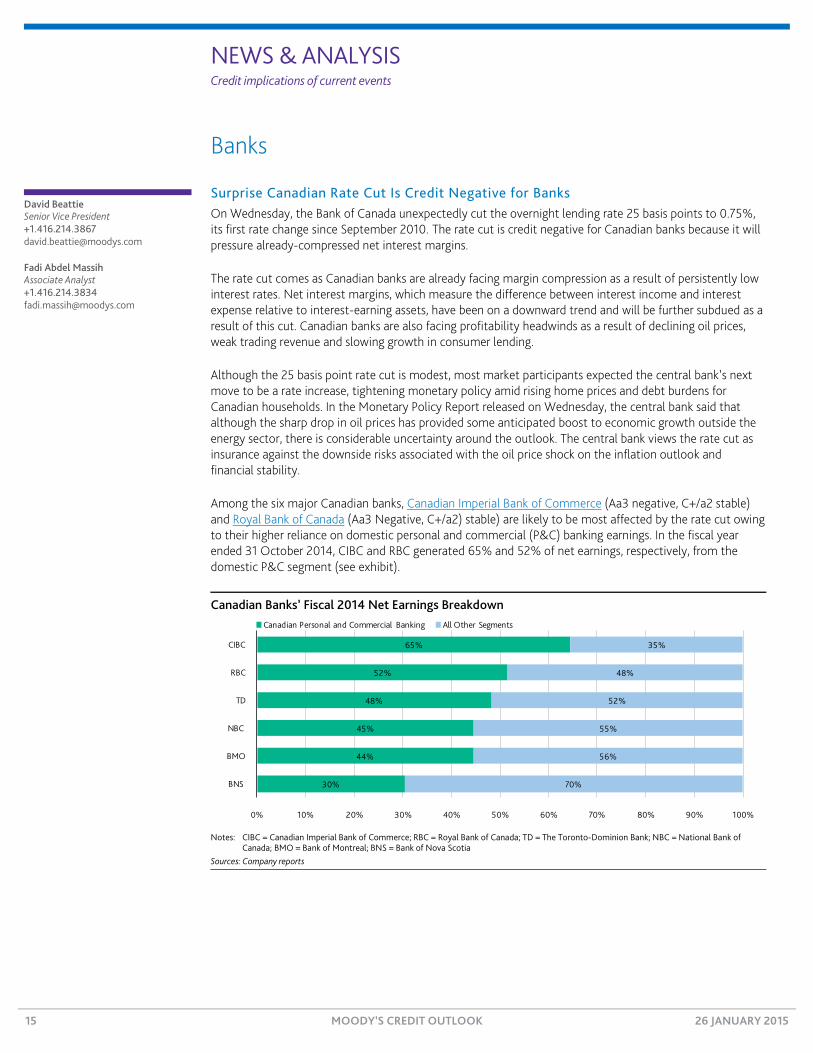

Among the six major Canadian banks, Canadian Imperial Bank of Commerce (Aa3 negative, C+/a2 stable) and Royal Bank of Canada (Aa3 Negative, C+/a2) stable) are likely to be most affected by the rate cut owing to their higher reliance on domestic personal and commercial (P&C) banking earnings. In the fiscal year ended 31 October 2014, CIBC and RBC generated 65% and 52% of net earnings, respectively, from the domestic P&C segment (see exhibit).

Canadian Banks’ Fiscal 2014 Net Earnings Breakdown

Notes: CIBC = Canadian Imperial Bank of Commerce; RBC = Royal Bank of Canada; TD = The Toronto-Dominion Bank; NBC = National Bank of Canada; BMO = Bank of Montreal; BNS = Bank of Nova Scotia Sources: Company reports

30%

44%

45%

48%

52%

65%

70%

56%

55%

52%

48%

35%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

BNS

BMO

NBC

TD

RBC

CIBC

Canadian Personal and Commercial Banking All Other Segments

David Beattie Senior Vice President +1.416.214.3867 [email protected]

Fadi Abdel Massih Associate Analyst +1.416.214.3834 [email protected]

NEWS & ANALYSIS Credit implications of current events

16 MOODY’S CREDIT OUTLOOK 26 JANUARY 2015

RBC’s Acquisition of City National Is Credit Negative Last Thursday, the Royal Bank of Canada (RBC, Aa3 negative, C+/a2 stable2) announced the acquisition of City National Corporation (CN, A3 stable) and its subsidiary City National Bank (A2 stable, C+/a2 stable) for approximately $5.4 billion, comprising $2.7 billion in cash and around 44 million RBC common shares. This acquisition outside of RBC’s strong Canadian base market, and in the more competitive US regional banking market, is credit negative for RBC because it dilutes the bank’s core strength. In addition, given that the purchase price is at a 26% acquisition premium (21.0x 2015 consensus earnings per share and 2.6x third-quarter 2014 tangible book value per share), RBC has paid a full price for this asset.

The growth-seeking acquisition of CN marks RBC’s re-entry into US regional banking after its 2012 exit. The bank’s renewed strategy to expand outside its core Canadian market stems primarily from lower growth prospects in Canada. The acquisition of a banking platform in the US will also enable RBC to cross-sell with its US wealth management franchise, now the eighth largest in the US.

CN’s major credit challenge has been its low profitability compared with peers, which will dilute RBC’s key credit strength: the stable and recurring earnings power of its domestic personal and commercial franchise, where it has scale and pricing power. Although CN has only 3.4% of RBC’s assets and 2.2% of its net income, there is significant execution risk in the bank’s strategy to reenter the highly competitive US regional banking market, which will depend on continued growth, cost savings and successful cross-selling.

Despite the strategic objectives of the transaction, we believe RBC will find it difficult to build a scalable platform for growing its US banking and wealth management business. CN is a Los Angeles-based private bank and commercial lender concentrated in California and focused on high-net-worth clients. Given CN’s relatively small geographic footprint and the limited scope of its business, we believe that RBC will likely need to make further acquisitions in the credit-dilutive US market to achieve its stated aims.

The search for growth opportunities is a challenge for all banks in the mature Canadian market, which in addition to slowing loan growth must contend with persistently low interest rates that constrain margins. However, the high risk-adjusted profitability of the banks’ domestic operations makes them more favorable from a credit perspective than external acquisitions such as RBC’s purchase of CN.

2 The bank ratings shown in this report are the banks’ deposit ratings, their standalone bank financial strength ratings/baseline credit

assessments and the corresponding rating outlooks.

David Beattie Senior Vice President +1.416.214.3867 [email protected]

NEWS & ANALYSIS Credit implications of current events

17 MOODY’S CREDIT OUTLOOK 26 JANUARY 2015

Banca Popolare di Milano Will Benefit from Italy’s Reform of Cooperative Banks Last Tuesday, the Italian Council of Ministers approved a new law to reform the cooperative bank (Banche Popolari) sector. Pending parliamentary approval, the law would require those cooperative banks with more than €8 billion in assets to convert to joint-stock companies, which implies the removal of the one-vote-per-shareholder governance rule.

Removal of the one-vote-per-shareholder rule (regardless of the number of shares held) would be credit positive for Banca Popolare di Milano S.C.a r.l. (B1 negative, E+/b2 stable3) because the rule has afforded employees and small shareholders in Banca Popolare di Milano significant influence. The employees and shareholders have so far elected the majority of the bank’s surveillance board and constrained the bank’s ability to remedy corporate governance shortcomings and implement best practices, all of which would strengthen its credit quality.

The risks associated with Banca Popolare di Milano's current corporate governance structure weigh on its creditworthiness and were publicly acknowledged by the bank in April 2011 after a Bank of Italy inspection revealed governance weaknesses. Banca Popolare di Milano subsequently made various attempts to change its corporate governance structure, some of which failed. Because this reform will oblige Banca Popolare di Milano to convert to a joint-stock company with voting rights distributed according to market rules, giving institutional investors in Banca Popolare di Milano more influence, it is credit positive. The rebalancing of power will facilitate the successful implementation of the bank’s strategic plan, which aims to cope with the challenges of Italy’s still-weak domestic operating environment.

We do not think the reform will have a credit effect on other Italian cooperative banks. The mandatory conversion into joint-stock companies and improved governance rules will not necessarily translate into a material improvement of those banks’ credit profile. Becoming a joint-stock company will broaden access to capital, although we have seen that the legal status of a cooperative bank does not diminish investor appetite for their capital, as demonstrated by the large acceptance of recent capital increases made by these banks. Neither has the one-vote-per-shareholder structure significantly jeopardised the corporate strategy of the Italian cooperative banks, with the exception of Banca Popolare di Milano. Therefore, we do not expect significant positive developments in terms of corporate governance after this rule is removed.

The reform also paves the way for further consolidation within the Italian banking system. Although overall we think any move toward consolidation will improve credit quality, there is no guarantee that future mergers involving cooperative banks would be executed in a way to ensure the emergence of stronger banking groups.

3 The bank ratings shown are Banca Popolare di Milano’s deposit rating, its standalone bank financial strength rating/baseline credit

assessment and the corresponding rating outlooks.

London +44.20.7772.5454

NEWS & ANALYSIS Credit implications of current events

18 MOODY’S CREDIT OUTLOOK 26 JANUARY 2015

China’s Tighter Regulations of Banks’ Entrusted Loans Is Credit Positive On 16 January, the China Banking Regulatory Commission (CBRC), China’s bank regulator, published a request for comment on guidance for managing commercial banks’ fast-growing entrusted loan business. Entrusted loan were originally loans organized by an agent bank between borrowers and lenders. The bank collects loan principal and interest, for which it charges a handling fee, but the bank does not assume any credit risk. However, Chinese banks are increasingly taking more risks through the assumption of payment and repayment responsibilities, providing guarantees and channeling funds to risky non-loan assets.

The draft guidance is credit positive for China’s banks and establishes detailed regulation on entrusted loans where there had been none. The new guidance will help curb the systemic risk that entrusted loans pose to the banking system. Specifically, the draft guidance stipulates that funds can only come from principal lenders rather than the banks, and cannot be channeled to investment in equities, bonds, derivatives or wealth management products, invested in companies or used in other products or projects the government prohibits.

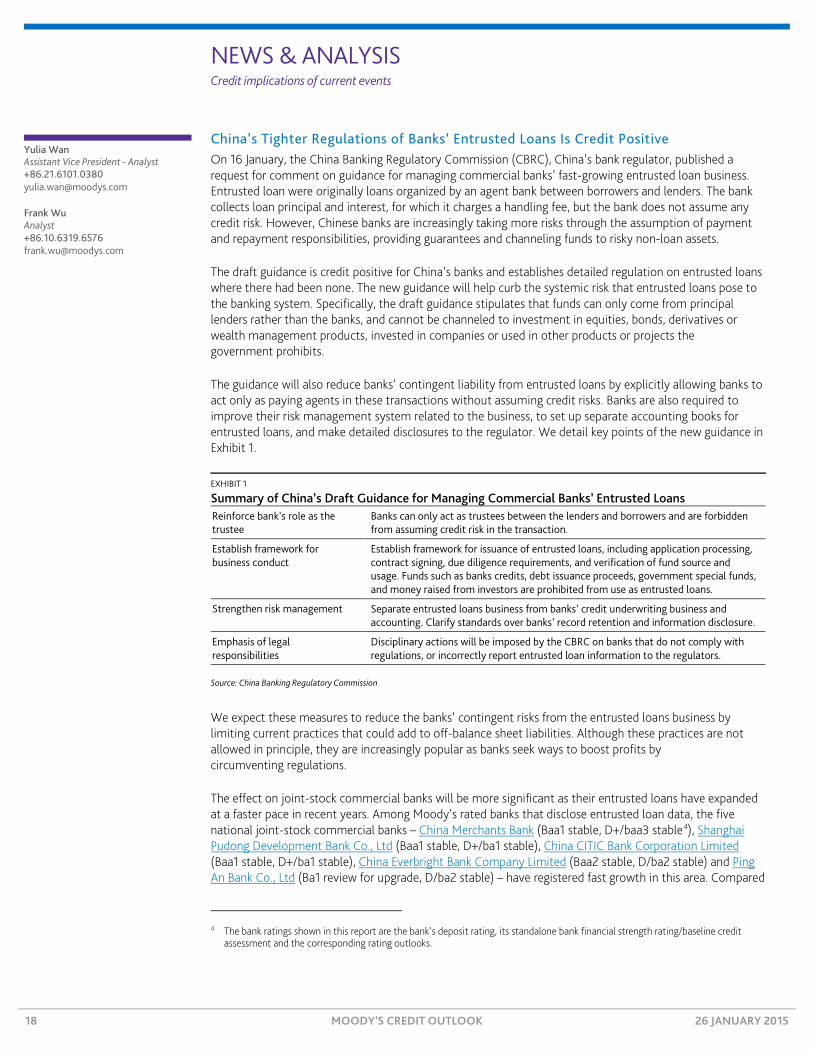

The guidance will also reduce banks’ contingent liability from entrusted loans by explicitly allowing banks to act only as paying agents in these transactions without assuming credit risks. Banks are also required to improve their risk management system related to the business, to set up separate accounting books for entrusted loans, and make detailed disclosures to the regulator. We detail key points of the new guidance in Exhibit 1.

EXHIBIT 1

Summary of China’s Draft Guidance for Managing Commercial Banks’ Entrusted Loans Reinforce bank’s role as the trustee

Banks can only act as trustees between the lenders and borrowers and are forbidden from assuming credit risk in the transaction.

Establish framework for business conduct

Establish framework for issuance of entrusted loans, including application processing, contract signing, due diligence requirements, and verification of fund source and usage. Funds such as banks credits, debt issuance proceeds, government special funds, and money raised from investors are prohibited from use as entrusted loans.

Strengthen risk management Separate entrusted loans business from banks’ credit underwriting business and accounting. Clarify standards over banks’ record retention and information disclosure.

Emphasis of legal responsibilities

Disciplinary actions will be imposed by the CBRC on banks that do not comply with regulations, or incorrectly report entrusted loan information to the regulators.

Source: China Banking Regulatory Commission

We expect these measures to reduce the banks’ contingent risks from the entrusted loans business by limiting current practices that could add to off-balance sheet liabilities. Although these practices are not allowed in principle, they are increasingly popular as banks seek ways to boost profits by circumventing regulations.

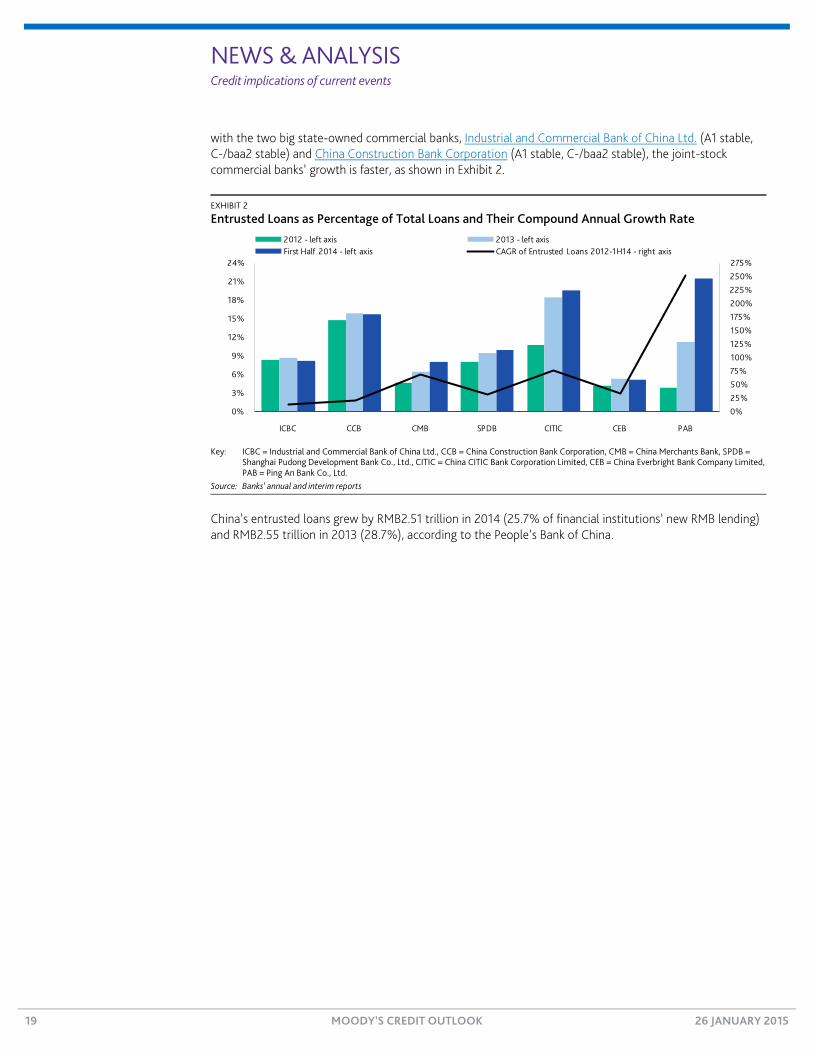

The effect on joint-stock commercial banks will be more significant as their entrusted loans have expanded at a faster pace in recent years. Among Moody’s rated banks that disclose entrusted loan data, the five national joint-stock commercial banks – China Merchants Bank (Baa1 stable, D+/baa3 stable4), Shanghai Pudong Development Bank Co., Ltd (Baa1 stable, D+/ba1 stable), China CITIC Bank Corporation Limited (Baa1 stable, D+/ba1 stable), China Everbright Bank Company Limited (Baa2 stable, D/ba2 stable) and Ping An Bank Co., Ltd (Ba1 review for upgrade, D/ba2 stable) – have registered fast growth in this area. Compared

4 The bank ratings shown in this report are the bank’s deposit rating, its standalone bank financial strength rating/baseline credit

assessment and the corresponding rating outlooks.

Yulia Wan Assistant Vice President - Analyst +86.21.6101.0380 [email protected]

Frank Wu Analyst +86.10.6319.6576 [email protected]

NEWS & ANALYSIS Credit implications of current events

19 MOODY’S CREDIT OUTLOOK 26 JANUARY 2015

with the two big state-owned commercial banks, Industrial and Commercial Bank of China Ltd. (A1 stable, C-/baa2 stable) and China Construction Bank Corporation (A1 stable, C-/baa2 stable), the joint-stock commercial banks’ growth is faster, as shown in Exhibit 2.

EXHIBIT 2

Entrusted Loans as Percentage of Total Loans and Their Compound Annual Growth Rate

Key: ICBC = Industrial and Commercial Bank of China Ltd., CCB = China Construction Bank Corporation, CMB = China Merchants Bank, SPDB = Shanghai Pudong Development Bank Co., Ltd., CITIC = China CITIC Bank Corporation Limited, CEB = China Everbright Bank Company Limited, PAB = Ping An Bank Co., Ltd. Source: Banks’ annual and interim reports

China’s entrusted loans grew by RMB2.51 trillion in 2014 (25.7% of financial institutions’ new RMB lending) and RMB2.55 trillion in 2013 (28.7%), according to the People’s Bank of China.

0%

25%

50%

75%

100%

125%

150%

175%

200%

225%

250%

275%

0%

3%

6%

9%

12%

15%

18%

21%

24%

ICBC CCB CMB SPDB CITIC CEB PAB

2012 - left axis 2013 - left axisFirst Half 2014 - left axis CAGR of Entrusted Loans 2012-1H14 - right axis

NEWS & ANALYSIS Credit implications of current events

20 MOODY’S CREDIT OUTLOOK 26 JANUARY 2015

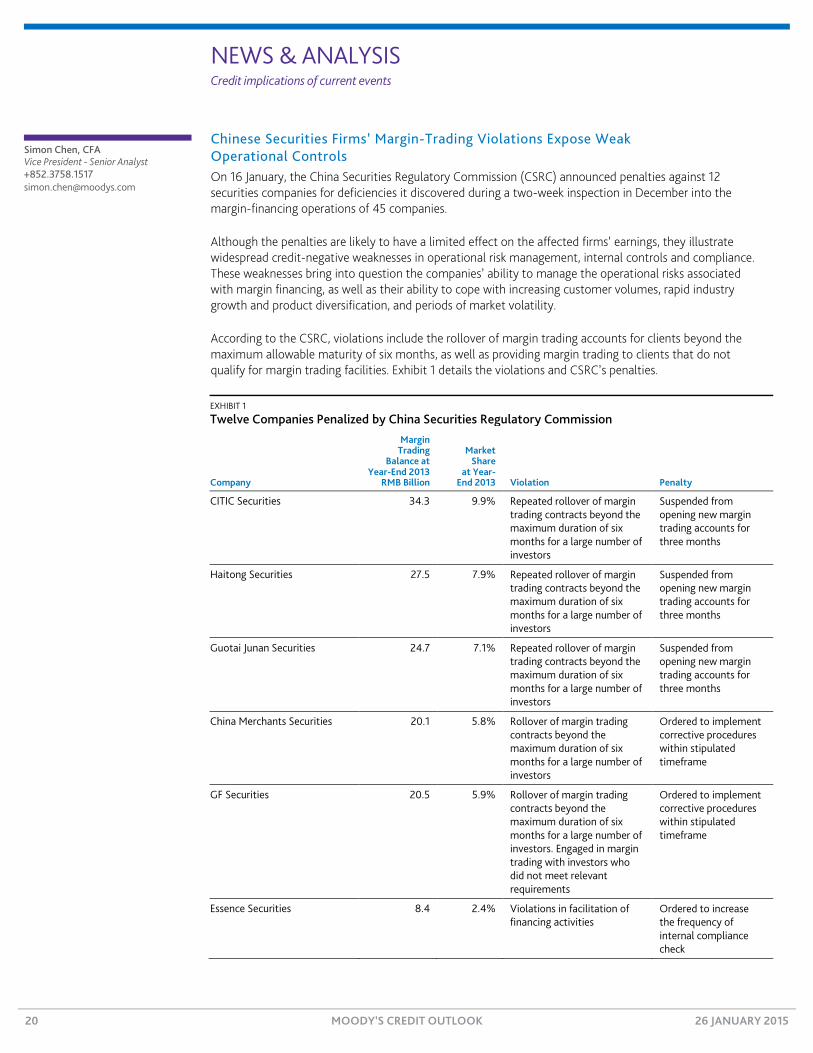

Chinese Securities Firms’ Margin-Trading Violations Expose Weak Operational Controls On 16 January, the China Securities Regulatory Commission (CSRC) announced penalties against 12 securities companies for deficiencies it discovered during a two-week inspection in December into the margin-financing operations of 45 companies.

Although the penalties are likely to have a limited effect on the affected firms’ earnings, they illustrate widespread credit-negative weaknesses in operational risk management, internal controls and compliance. These weaknesses bring into question the companies’ ability to manage the operational risks associated with margin financing, as well as their ability to cope with increasing customer volumes, rapid industry growth and product diversification, and periods of market volatility.

According to the CSRC, violations include the rollover of margin trading accounts for clients beyond the maximum allowable maturity of six months, as well as providing margin trading to clients that do not qualify for margin trading facilities. Exhibit 1 details the violations and CSRC’s penalties.

EXHIBIT 1

Twelve Companies Penalized by China Securities Regulatory Commission

Company

Margin Trading

Balance at Year-End 2013

RMB Billion

Market Share

at Year- End 2013 Violation Penalty

CITIC Securities 34.3 9.9% Repeated rollover of margin trading contracts beyond the maximum duration of six months for a large number of investors

Suspended from opening new margin trading accounts for three months

Haitong Securities 27.5 7.9% Repeated rollover of margin trading contracts beyond the maximum duration of six months for a large number of investors

Suspended from opening new margin trading accounts for three months

Guotai Junan Securities 24.7 7.1% Repeated rollover of margin trading contracts beyond the maximum duration of six months for a large number of investors

Suspended from opening new margin trading accounts for three months

China Merchants Securities 20.1 5.8% Rollover of margin trading contracts beyond the maximum duration of six months for a large number of investors

Ordered to implement corrective procedures within stipulated timeframe

GF Securities 20.5 5.9% Rollover of margin trading contracts beyond the maximum duration of six months for a large number of investors. Engaged in margin trading with investors who did not meet relevant requirements

Ordered to implement corrective procedures within stipulated timeframe

Essence Securities 8.4 2.4% Violations in facilitation of financing activities

Ordered to increase the frequency of internal compliance check

Simon Chen, CFA Vice President - Senior Analyst +852.3758.1517 [email protected]

NEWS & ANALYSIS Credit implications of current events

21 MOODY’S CREDIT OUTLOOK 26 JANUARY 2015

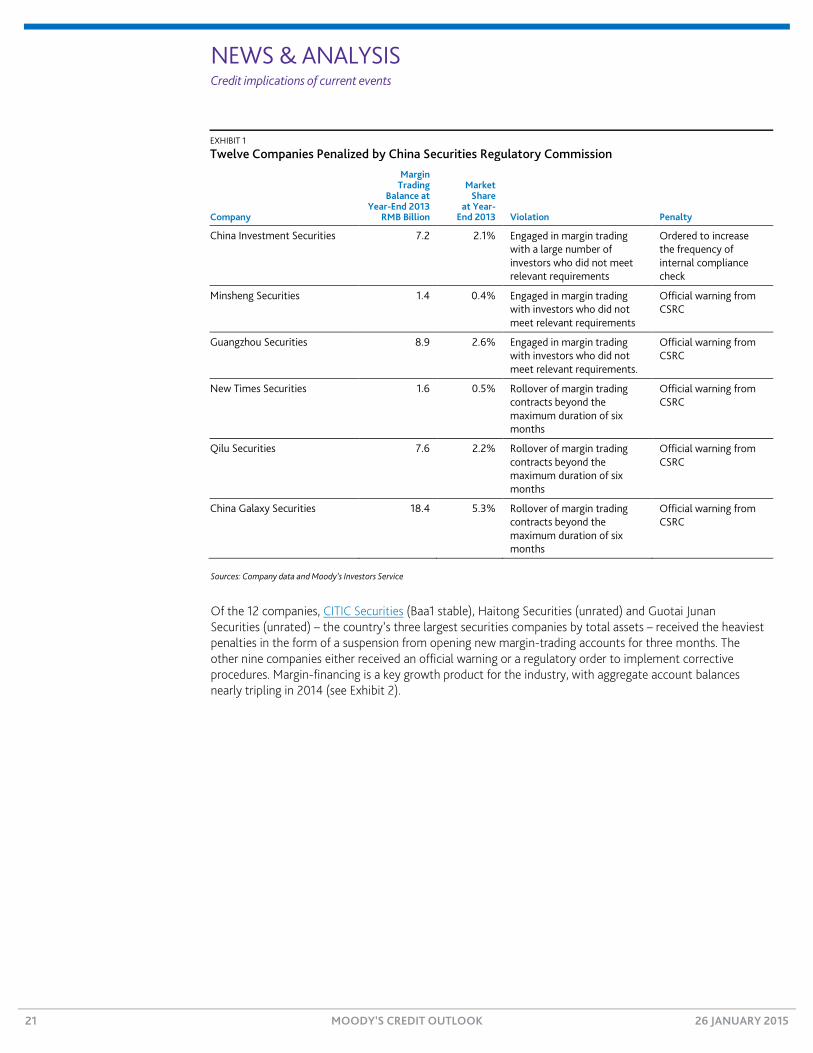

EXHIBIT 1

Twelve Companies Penalized by China Securities Regulatory Commission

Company

Margin Trading

Balance at Year-End 2013

RMB Billion

Market Share

at Year- End 2013 Violation Penalty

China Investment Securities 7.2 2.1% Engaged in margin trading with a large number of investors who did not meet relevant requirements

Ordered to increase the frequency of internal compliance check

Minsheng Securities 1.4 0.4% Engaged in margin trading with investors who did not meet relevant requirements

Official warning from CSRC

Guangzhou Securities 8.9 2.6% Engaged in margin trading with investors who did not meet relevant requirements.

Official warning from CSRC

New Times Securities 1.6 0.5% Rollover of margin trading contracts beyond the maximum duration of six months

Official warning from CSRC

Qilu Securities 7.6 2.2% Rollover of margin trading contracts beyond the maximum duration of six months

Official warning from CSRC

China Galaxy Securities 18.4 5.3% Rollover of margin trading contracts beyond the maximum duration of six months

Official warning from CSRC

Sources: Company data and Moody’s Investors Service

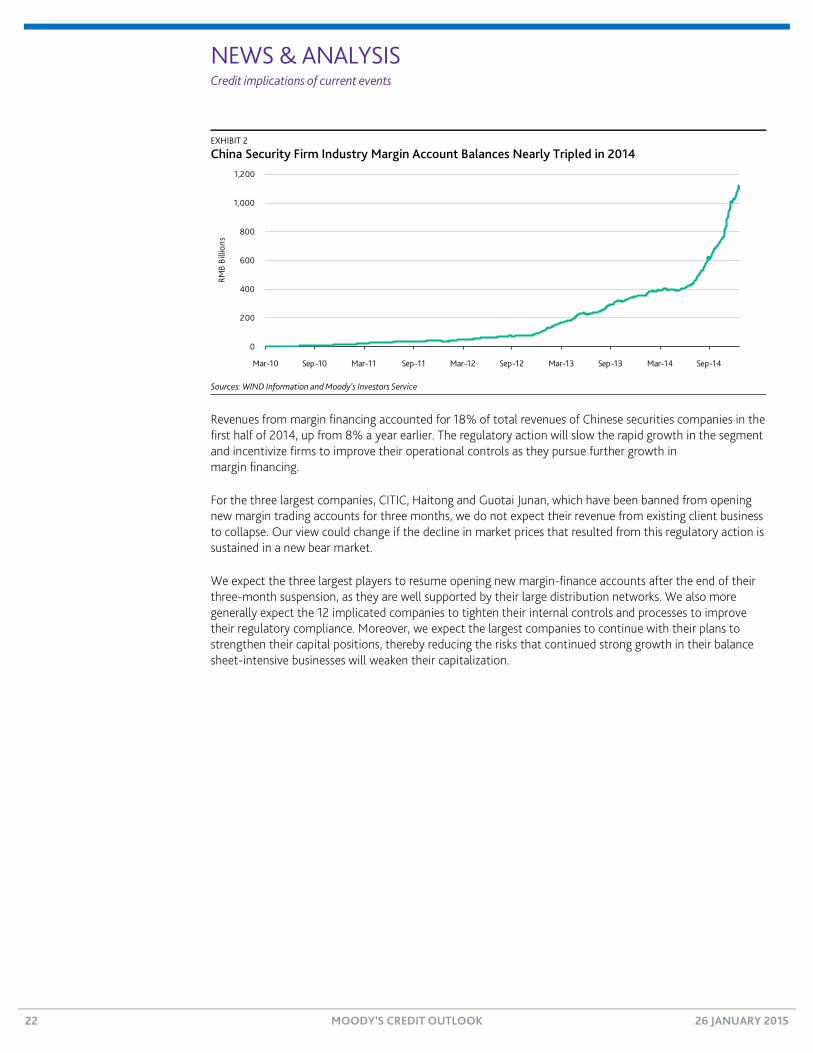

Of the 12 companies, CITIC Securities (Baa1 stable), Haitong Securities (unrated) and Guotai Junan Securities (unrated) – the country’s three largest securities companies by total assets – received the heaviest penalties in the form of a suspension from opening new margin-trading accounts for three months. The other nine companies either received an official warning or a regulatory order to implement corrective procedures. Margin-financing is a key growth product for the industry, with aggregate account balances nearly tripling in 2014 (see Exhibit 2).

NEWS & ANALYSIS Credit implications of current events

22 MOODY’S CREDIT OUTLOOK 26 JANUARY 2015

EXHIBIT 2

China Security Firm Industry Margin Account Balances Nearly Tripled in 2014

Sources: WIND Information and Moody’s Investors Service

Revenues from margin financing accounted for 18% of total revenues of Chinese securities companies in the first half of 2014, up from 8% a year earlier. The regulatory action will slow the rapid growth in the segment and incentivize firms to improve their operational controls as they pursue further growth in margin financing.

For the three largest companies, CITIC, Haitong and Guotai Junan, which have been banned from opening new margin trading accounts for three months, we do not expect their revenue from existing client business to collapse. Our view could change if the decline in market prices that resulted from this regulatory action is sustained in a new bear market.

We expect the three largest players to resume opening new margin-finance accounts after the end of their three-month suspension, as they are well supported by their large distribution networks. We also more generally expect the 12 implicated companies to tighten their internal controls and processes to improve their regulatory compliance. Moreover, we expect the largest companies to continue with their plans to strengthen their capital positions, thereby reducing the risks that continued strong growth in their balance sheet-intensive businesses will weaken their capitalization.

0

200

400

600

800

1,000

1,200

Mar-10 Sep-10 Mar-11 Sep-11 Mar-12 Sep-12 Mar-13 Sep-13 Mar-14 Sep-14

RMB

Billi

ons

NEWS & ANALYSIS Credit implications of current events

23 MOODY’S CREDIT OUTLOOK 26 JANUARY 2015

Hong Kong’s Proposed Resolution Regime for Financial Institutions Is Credit Negative for Unsecured Creditors Last Wednesday, the Hong Kong government published a second-round consultation paper on its proposed resolution regime for Hong Kong financial institutions. The consultation paper, which underscores the government’s intention to limit the use of public funds in the resolution of distressed financial institutions, contains responses to feedback to the first-round consultation published in January 2014, as well as implementation details for the resolution regime. Details in the consultation paper weaken the likelihood of government support, and are thus credit negative for unsecured creditors of Hong Kong banks and insurance companies.

In particular, the latest consultation notes that the Hong Kong Monetary Authority has already begun to roll out its recovery planning requirements for local banks and states clearly that recovery plans should be proportionate to the nature, scale and complexity of a bank’s operations. The authorities also propose that they be vested with powers to require banks’ affiliated entities to provide essential services in resolution to ensure operational continuity. We see these as further steps by regulators to reduce obstacles to the resolution of distressed banks, and they should facilitate the resolution of banks without government support.

The government also stated its intention to publish further details on the implementation of total loss-absorbing capacity (TLAC) requirements for Hong Kong banks in a third round of consultation. The Financial Stability Board has yet to finalize details on TLAC requirements for global systemically important financial institutions. An implementation of TLAC requirements in Hong Kong could increase authorities’ ability to bail-in bank creditors without causing disruptions to the broader financial system and economic activity.

Nevertheless, the government has also elaborated on proposed safeguards to creditors in the resolution of distressed financial institutions. The consultation reiterated the government’s aim to preserve priority of claims for creditors and shareholders in resolutions, and the principle that no creditors would be worse off in resolution than in liquidation. The proposed regime provides creditors with a compensation mechanism whereby independent third-party valuations would be used to determine whether compensation is due to creditors as a result of resolution action, with such funds to be furnished by the industry. Creditors, shareholders and government authorities will also have the ability to appeal the valuation outcome to a resolution compensation tribunal.

The consultation paper also specifies the types of liabilities to be excluded from bail-ins, including protected deposits, insurance policyholder claims protected by insolvency funds, secured and collateralized liabilities and interbank liabilities with maturities of less than seven days. Given that secured liabilities such as repos would be excluded from potential bail-ins, we expect financial institutions to shift more of their counterparty transactions to secured lending, especially during times of stress, which should provide their claims with more seniority than unsecured creditors in resolutions.

Sonny Hsu Vice President - Senior Analyst +852.3758.1363 [email protected]

NEWS & ANALYSIS Credit implications of current events

24 MOODY’S CREDIT OUTLOOK 26 JANUARY 2015

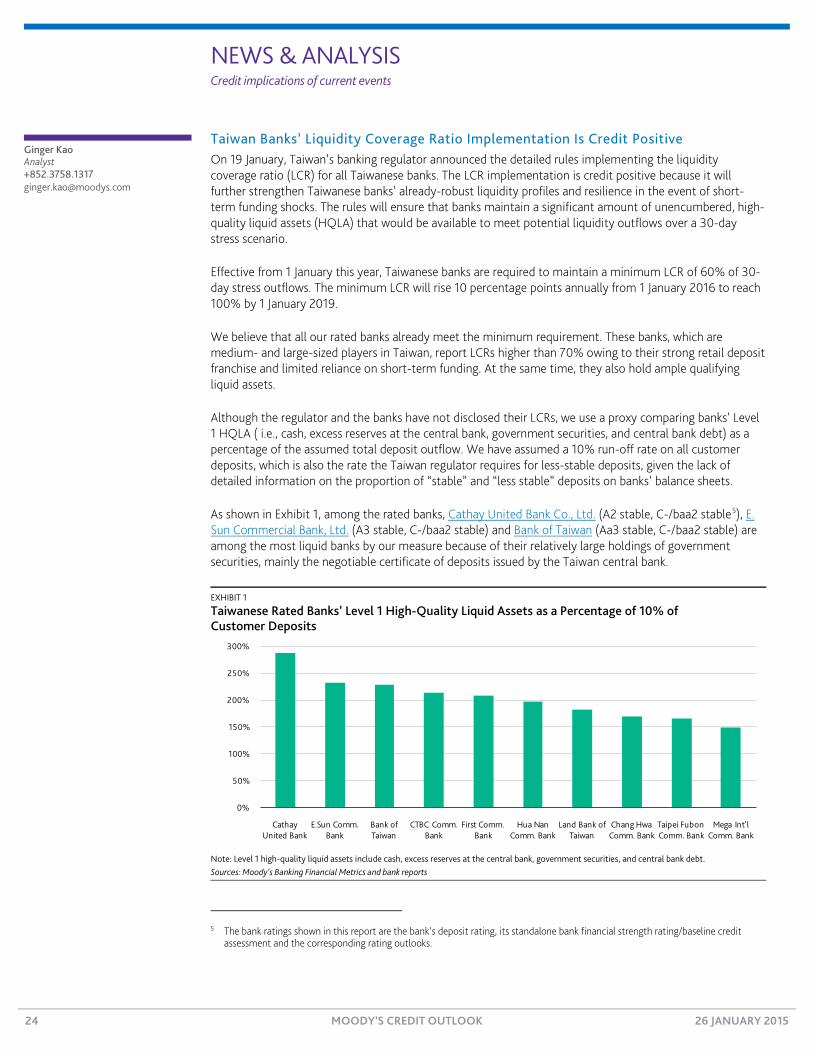

Taiwan Banks’ Liquidity Coverage Ratio Implementation Is Credit Positive On 19 January, Taiwan’s banking regulator announced the detailed rules implementing the liquidity coverage ratio (LCR) for all Taiwanese banks. The LCR implementation is credit positive because it will further strengthen Taiwanese banks’ already-robust liquidity profiles and resilience in the event of short-term funding shocks. The rules will ensure that banks maintain a significant amount of unencumbered, high-quality liquid assets (HQLA) that would be available to meet potential liquidity outflows over a 30-day stress scenario.

Effective from 1 January this year, Taiwanese banks are required to maintain a minimum LCR of 60% of 30-day stress outflows. The minimum LCR will rise 10 percentage points annually from 1 January 2016 to reach 100% by 1 January 2019.

We believe that all our rated banks already meet the minimum requirement. These banks, which are medium- and large-sized players in Taiwan, report LCRs higher than 70% owing to their strong retail deposit franchise and limited reliance on short-term funding. At the same time, they also hold ample qualifying liquid assets.

Although the regulator and the banks have not disclosed their LCRs, we use a proxy comparing banks’ Level 1 HQLA ( i.e., cash, excess reserves at the central bank, government securities, and central bank debt) as a percentage of the assumed total deposit outflow. We have assumed a 10% run-off rate on all customer deposits, which is also the rate the Taiwan regulator requires for less-stable deposits, given the lack of detailed information on the proportion of “stable” and “less stable” deposits on banks’ balance sheets.

As shown in Exhibit 1, among the rated banks, Cathay United Bank Co., Ltd. (A2 stable, C-/baa2 stable5), E. Sun Commercial Bank, Ltd. (A3 stable, C-/baa2 stable) and Bank of Taiwan (Aa3 stable, C-/baa2 stable) are among the most liquid banks by our measure because of their relatively large holdings of government securities, mainly the negotiable certificate of deposits issued by the Taiwan central bank.

EXHIBIT 1

Taiwanese Rated Banks’ Level 1 High-Quality Liquid Assets as a Percentage of 10% of Customer Deposits

Note: Level 1 high-quality liquid assets include cash, excess reserves at the central bank, government securities, and central bank debt. Sources: Moody’s Banking Financial Metrics and bank reports

5 The bank ratings shown in this report are the bank’s deposit rating, its standalone bank financial strength rating/baseline credit

assessment and the corresponding rating outlooks.

0%

50%

100%

150%

200%

250%

300%

Cathay United Bank

E.Sun Comm. Bank

Bank of Taiwan

CTBC Comm. Bank

First Comm. Bank

Hua Nan Comm. Bank

Land Bank of Taiwan

Chang Hwa Comm. Bank

Taipei Fubon Comm. Bank

Mega Int'l Comm. Bank

Ginger Kao Analyst +852.3758.1317 [email protected]

NEWS & ANALYSIS Credit implications of current events

25 MOODY’S CREDIT OUTLOOK 26 JANUARY 2015

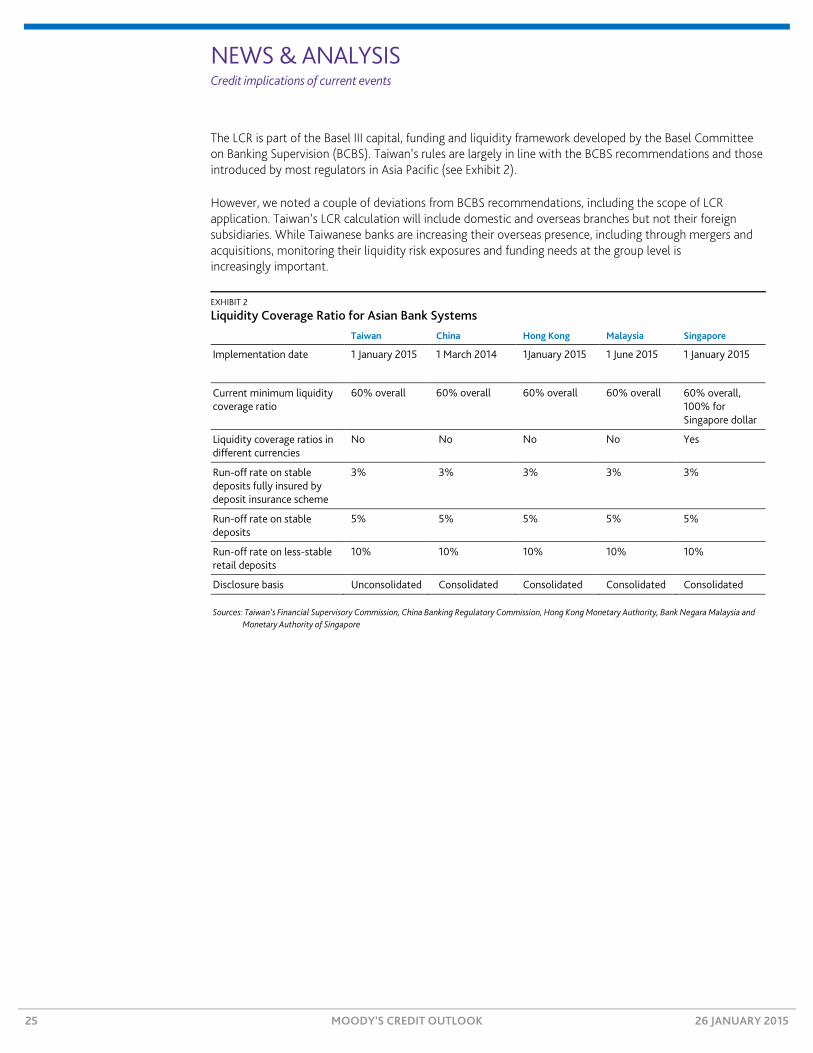

The LCR is part of the Basel III capital, funding and liquidity framework developed by the Basel Committee on Banking Supervision (BCBS). Taiwan’s rules are largely in line with the BCBS recommendations and those introduced by most regulators in Asia Pacific (see Exhibit 2).

However, we noted a couple of deviations from BCBS recommendations, including the scope of LCR application. Taiwan’s LCR calculation will include domestic and overseas branches but not their foreign subsidiaries. While Taiwanese banks are increasing their overseas presence, including through mergers and acquisitions, monitoring their liquidity risk exposures and funding needs at the group level is increasingly important.

EXHIBIT 2

Liquidity Coverage Ratio for Asian Bank Systems

Taiwan China Hong Kong Malaysia Singapore

Implementation date 1 January 2015 1 March 2014 1January 2015 1 June 2015 1 January 2015

Current minimum liquidity coverage ratio

60% overall 60% overall 60% overall 60% overall 60% overall, 100% for Singapore dollar

Liquidity coverage ratios in different currencies

No No No No Yes

Run-off rate on stable deposits fully insured by deposit insurance scheme

3% 3% 3% 3% 3%

Run-off rate on stable deposits

5% 5% 5% 5% 5%

Run-off rate on less-stable retail deposits

10% 10% 10% 10% 10%

Disclosure basis Unconsolidated Consolidated Consolidated Consolidated Consolidated

Sources: Taiwan’s Financial Supervisory Commission, China Banking Regulatory Commission, Hong Kong Monetary Authority, Bank Negara Malaysia and Monetary Authority of Singapore

NEWS & ANALYSIS Credit implications of current events

26 MOODY’S CREDIT OUTLOOK 26 JANUARY 2015

Metropolitan Bank & Trust’s Proposed Rights Issue Is Credit Positive Last Wednesday, Metropolitan Bank & Trust Company (MBT, Baa2 stable, C-/baa2 stable6) announced that it had received board approval to conduct a rights issue of up to PHP32 billion ($725 million). The proposed rights issue, the timing of which is subject to regulatory approvals and market conditions, is credit positive for MBT because it will bolster its capital ratios and maintain them above Basel III regulatory requirements.

In addition, the capital raise will provide additional buffer for the bank to comply with domestic systemically important banks (D-SIBs) Tier 1 capital requirements that will be phased in between 2017 and 2019. The rights issue will also allow the bank to comply with stringent stress test requirements for Philippine banks with large real estate exposures.7

The capital increase will also support MBT’s accelerating credit growth, which has been robust in the past few years, especially in the bank’s key focus areas of the middle market, small and midsize enterprise and retail segments.

This proposed rights issue follows a series of steps that the bank has undertaken to boost its capital base. MBT raised PHP16 billion of Basel III-compliant Tier 2 subordinated debt in March last year, and PHP6.5 billion in August. The exhibit below shows MBT’s common equity Tier 1 capital ratios, accounting for the capital raise and 20% credit growth in 2015.

Metropolitan Bank & Trust’s Pro-Forma Common Equity Tier 1 Capital Ratio

Sources: The bank and Moody’s Investors Service calculations

The bank also sold non-core assets to boost its capital base, including its 30% stake in Toyota Motor Philippines to GT Capital in December 2012-January 2013 and its 40% stake in Global Business Power Corporation via two tranches in October 2013; 20% to Orix Corporation (Baa2 stable) and 20% to Meralco PowerGen (unrated). In August 2014, MBT and subsidiary Philippine Savings Bank (unrated) sold their 15% and 25% stakes, respectively, in Toyota Financial Services Philippines Corporation to GT Capital.

These corporate actions are positive as the sales will free up capital in preparation for business growth and higher capital requirements under the new Basel III regime. These disposals also allow MBT to avoid punitive deductions to its Tier 1 capital calculation that results from equity investments in non-financial entities under Basel III.

6 The ratings shown are MBT’s deposit rating, its standalone bank financial strength rating/baseline credit assessment and the

corresponding rating outlooks. 7 See Philippine Banks’ New Real Estate Stress Test Is Credit Positive, 10 July 2014.

14.2%

12.1%

15.4%

13.2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

End 2013 Actual Sep 2014 Actual Sep 2014 Pro-Forma Capital Raise End-2015 Projected

Minimum CET1Ratio Required: 8.5%

Daphne Cheng Analyst +65.6398.8339 [email protected]

NEWS & ANALYSIS Credit implications of current events

27 MOODY’S CREDIT OUTLOOK 26 JANUARY 2015

India Reduces Banks’ Loan-Pricing Flexibility, a Credit Negative for Consumer Lenders On 19 January, the Reserve Bank of India (RBI) instituted norms requiring banks to outline the framework they use to set spreads on loans above their benchmark lending rates. The new requirements are credit negative because they will reduce banks’ discretion to price loans at higher spreads to correspond to market conditions and each borrower’s creditworthiness.

The norms are likely to most affect consumer loan pricing given that retail borrowers tend to have less pricing power than large industrial borrowers and banks have been most able to take advantage of market inefficiencies in the retail loan segment. Within the retail segment, pricing in the mortgage segment is likely to be the most affected as it is in this segment that banks have resorted to differential pricing the most. Among our rated Indian banks, ICICI Bank Limited (Baa3 stable, D+/baa3 stable8) and Axis Bank Ltd (Baa3 stable, D+/baa3 stable) have a high share of mortgage loans in their overall loan books, as shown in the exhibit below.

Share of Mortgage and Retail Loans in Total Loans - March 2014

Notes: AXIS = Axis Bank Ltd (Baa3 stable, D+/baa3 stable), HDFC = HDFC Bank Ltd (Baa3 stable, D+/baa3 stable), ICICI = ICICI Bank Ltd Baa3 stable, D+/baa3 stable), BOB = Bank of Baroda (Baa3 stable, D/ba2 negative), BOI = Bank of India (Baa3 stable, D/ba2 negative), CAN = Canara Bank (Baa2 stable, D/ba2 negative), IOB = Indian Overseas Bank (Baa3 stable, E+/ba2 stable). Figures are reported on a net advances basis. CBI = Central Bank of India (Baa3 negative, E+/b3 negative), OBC = Oriental Bank of Commerce (Baa3 stable, D-/ba2 negative), PNB = Punjab National Bank (Baa3 stable, D-/ba3 stable), SBI = State Bank of India (Baa2 stable, D+/ba1 negative), SYN = Syndicate Bank (Baa3 stable, D/ba2 negative), UBI = Union Bank of India (Baa3 stable, D/ba2 negative). Figures are reported on a gross advances basis. Sources: Company financial statements and presentations and Moody's Banking Financial Metrics

Indian banks are required to set a base lending rate that is a function of the bank’s cost of funding, operating costs and cost of capital. Although banks are not allowed to lend at rates below their base rate, they have latitude in how they charge a premium or spread on individual loans, depending on market conditions and the credit quality of the specific borrower.

RBI’s concern about the transparency and fairness of how banks determine loan spreads mainly relate to the downward stickiness of lending rates (i.e., lending rates not declining commensurately with other interest rates), discriminatory treatment of old borrowers versus new borrowers and arbitrary changes in spreads. Bank spreads are a function of product-specific operating costs, credit risk premium, the loan tenor and qualitative factors such as competitive intensity and pricing power. The regulator has been concerned that arbitrary inclusion of these qualitative factors into product pricing can lead to spread disparities among customers. The new norms address this by requiring banks to have a board-approved policy delineating the

8 The bank ratings shown in this report are the bank’s deposit rating, its standalone bank financial strength rating/baseline credit

assessment and the corresponding rating outlooks.

20.9% 19.4%

11.3%

6.6% 6.5% 6.4% 5.9% 5.5% 5.1% 4.9% 4.8% 3.5% 2.0%

39.0%

30.7%

19.2%

10.7% 11.1%

49.4%

15.1%11.9%

11.5% 11.6% 10.8% 9.7%8.0%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

ICICI AXIS SBI UBI CAN HDFC CBI SYN OBC BOB PNB IOB BOI

Housing Loans as Percent of Total Advances Retail Advances as Percent of Total Advances

Srikanth Vadlamani Vice President - Senior Credit Officer +65.6398.8336 [email protected]

NEWS & ANALYSIS Credit implications of current events

28 MOODY’S CREDIT OUTLOOK 26 JANUARY 2015

spread components. We expect this to reduce the arbitrariness in determining spreads for specific customers.

Moreover, the spread charged to an existing borrower may not be increased except on account of deterioration in the borrower’s risk profile or when market interest rates for that particular loan tenor have increased. If a bank decides to change its spreads because of a change in market interest rates for a particular loan tenor, the change will also be applied to all the bank’s borrowers at that particular tenor.

NEWS & ANALYSIS Credit implications of current events

29 MOODY’S CREDIT OUTLOOK 26 JANUARY 2015

Insurers

Alliant Buys QBE US Agencies, Joining Credit-Negative Trend of Highly Levered Broker Acquisitions On 20 January, Alliant Holdings I, LLC (B3 stable) agreed to acquire QBE US Agencies, a subsidiary of Australian insurance group QBE Insurance Group Limited (Baa2 stable), for a total consideration of as much as $300 million. We view the transaction as complementary to Alliant’s strategy, but credit negative because of its sizeable debt financing and execution risk. The companies expect the sale, which extends a long run of mergers and acquisitions among insurance brokers, to close in February.