Embed Size (px)

Citation preview

NIKE U.S. EMPLOYEE HANDBOOK January 15, 2013

2

Disclaimer This current version of the Nike Employee Handbook supersedes and replaces all prior handbooks or other understandings regarding the subjects discussed in the Handbook. These policies are general guidelines and do not form the basis of an employment contract. The Handbook can be changed or modified at any time. Updated versions of the handbook will be posted on the Nike HR Website and at https://nikebenefits.ehr.com as necessary. Printed copies of the handbook are available by calling Nike HR Direct at 1.888.360.6453.

Employment at Nike Employment with Nike is at will as it is not Nike’s practice to enter into employment contracts. Either the employee or Nike may end the employment relationship at any time.

NIKE U.S. EMPLOYEE HANDBOOK January 15, 2013

3

THE NIKE RETIREMENT SAVINGS PLAN

What Is It?

The 401(k) Savings and Profit Sharing Plan for Employees of NIKE, Inc.—the Retirement Savings Plan for short, or the "RSP" as described in this document—is designed to help you meet your future financial goals, with assistance from Nike. This description of the RSP is effective January 1, 2013; any changes to the RSP will be communicated to you in separate updates. As with all Nike benefit programs, this summary is intended to give you an overview of the key plan terms, but the official plan documents are controlling.

The Retirement Savings Plan consists of several types of accounts. Some of them are funded by money that you contribute, and others are funded by Nike. The chart below shows the accounts in the RSP.

Nike > Retirement Savings Plan 401(k) Before-Tax Account After-Tax Account Nike Before-Tax Match Account Profit Sharing Retirement Account Rollover Account Transferred Accounts

401(k) Before-Tax Account and After-Tax Account If you choose to contribute to the RSP, you set aside a portion of your salary each pay period through payroll deductions. Your contributions are deposited into the 401(k) Before-Tax Account and/or After-Tax Account, depending on your election. You choose how to invest your contributions among a variety of investment funds, which gives you flexibility to invest with your individual needs in mind.

Each year, you can contribute up to 50% of your pay from Nike to the RSP, subject to IRS limitations. Contributions to the 401(k) Before-Tax Account reduce your taxable income, giving you a tax break right now. Contributions to the After-Tax Account are made after you pay current taxes. Your entire account balance earns income on a tax-deferred basis until you withdraw the money. Withdrawals from your account are available in certain circumstances while you are still employed by Nike.

Nike Before-Tax Match Account Nike matches a portion of your 401(k) Before-Tax Contributions in the Nike Before-Tax Match Account. This contribution boosts your savings and gives you added incentive to contribute to the Retirement Savings Plan because the Nike Before-Tax Match Contribution is made automatically, up to RSP and legal limits.

Profit Sharing Retirement Account You are automatically enrolled and receive Nike Profit Sharing Contributions when you are eligible (see the “Profit Sharing Retirement Account” section of the handbook). The amount of the contribution is determined each year by Nike's Board of Directors. The Profit Sharing Retirement

NIKE U.S. EMPLOYEE HANDBOOK January 15, 2013

4

Account is invested in a professionally managed diversified investment portfolio. The Profit Sharing Retirement Account begins vesting after you complete two years of vesting service and is fully vested after five years of vesting service.

Rollover Account If you came to work at Nike from another employer, you may have an account in your previous employer's retirement plan. In many cases, you can “roll over” that account into the Retirement Savings Plan, allowing you to continue to invest that account balance on a tax-deferred basis. The Rollover Account is invested according to the elections that you make separately for this account.

Transferred Account If you participated in a plan of an affiliate of Nike that was merged into the Retirement Savings Plan, you may have “Transferred Accounts” in the RSP. Transferred Accounts are invested according to the elections that you make separately for these accounts and may have grandfathered benefit rights and features. If you have questions regarding your Transferred Accounts, please contact the Nike Retirement Plan Center at 800.987.6535.

There are Transferred Accounts attributable to the Cole Haan Retirement Savings Plan (the “Cole Haan Plan”), the Converse, Inc. 401(k) Savings Plan (the “Converse Plan”), the Hurley International LLC, an Oregon Limited Liability Company, Tax Advantaged Plan (the “Hurley Plan”), the Umbro Corp. 401(k) Plan (the “Umbro Plan”), the Salary Reduction Thirft Plan for Employees of Tetra Plastics, Inc., and the Nike Bauer Hockey USA, Inc. 401(k) Plan.

Why Would I Need It?

The Retirement Savings Plan can help you even if retirement is far from your mind. The earlier you start saving money, the less you'll need to set aside later, thanks to compounding earnings and time. The RSP is designed to be a tax-qualified plan under Internal Revenue Code section 401(a). This means that you are able to contribute on a pre-tax basis, and earnings are not taxed on contributions until withdrawal.

This summary describes the terms of the Retirement Savings Plan effective January 1, 2013. This summary was written to provide you with an easy-to-understand explanation of the main features of the RSP and cannot cover every circumstance as it would apply to you. If you would like a more detailed explanation or would like to review the RSP plan document, contact the Nike Retirement Plan Center at 800.987.6535. If there is any important difference between this SPD and the plan document, the plan document will control.

ELIGIBILITY RULES FOR RETIREMENT SAVINGS PLAN (INCLUDING 401k)

To be eligible for the Retirement Savings Plan, you must be an employee of Nike or a participating affiliate. Generally, references to “Nike” in this handbook include participating affiliates. As of January 1, 2013, the participating affiliates are:

Nike, TN., Inc.

Nike International, Ltd.

NIKE U.S. EMPLOYEE HANDBOOK January 15, 2013

5

Nike Retail Services, Inc.

Nike USA, Inc.

Nike IHM, Inc.

Cole Haan

Cole Haan Company Store

Converse, Inc.

Hurley International LLC

The participation rules are different for the different types of accounts under the RSP. See the sections below for information on when you become eligible to begin participation in the various RSP features.

The following groups are not eligible to participate in the RSP:

Employees performing work covered by a collective bargaining agreement, unless the collective bargaining agreement specifically provides for participation in the RSP.

Individuals who are not common-law employees, such as leased employees and individuals designated by Nike as independent contractors.

Employees who work for a Nike affiliate that is not listed above as a participating affiliate. Employees who are designated by Nike as temporary employees (for this purpose a temporary employee is an individual hired for special assignment clerical projects and/or retail sales events) and interns.

Employees who work at the Memphis Apparel Distribution Center and are designated as Seasonal On Call Casual Employee Reserve (SOCCER).

Employees who reside in Puerto Rico and perform services at the company's facilities located in Puerto Rico.

Any individual (whether or not an employee) who performs services for Nike but is not paid through Nike's U.S. payroll.

Foreign nationals (i.e., non-U.S. citizens) working inside or outside of the United States, during any period when the individual is accruing retirement benefits under a retirement plan maintained outside the U.S. funded in whole or in part by Nike or a Nike affiliate.

Please Note: Eligibility is determined based on the classification contained in Nike's payroll records. Classifications or reclassifications imposed by third parties (such as governmental agencies or courts) do not make you eligible for the RSP unless Nike specifically acts to make you eligible.

Service There are several important terms to keep in mind as you consider your service under the RSP.

An "hour of service" is an hour for which you are actually paid or entitled to be paid.

Non-exempt employees receive credit for paid hours actually worked.

Exempt employees receive 190 hours of service for each month in which they work at least one hour, regardless of actual hours worked.

NIKE U.S. EMPLOYEE HANDBOOK January 15, 2013

6

You also may earn up to 501 hours of service per year for paid time when you are not actually working, which includes time spent on approved:

o Paid time off (PTO),

o Holidays,

o Family and/or medical leaves of absence,

o Disability leave, and

o Other leaves of absence specifically approved by Nike if the employee returns or retires within the approved leave period and fulfills all other conditions imposed for the leave.

For eligibility to participate, hours of service include hours you work with Nike or any affiliate. Hours of service with Nike affiliates starts from the date of acquisition of the affiliate by Nike unless you were covered by an affiliate plan that merged into the Nike RSP. In that case, all service recognized under your prior plan is recognized under the RSP. If this applies to you and you have questions regarding your service, please contact the Nike Retirement Plan Center.

Hours of service do not include:

Periods during which you receive payments only under worker's compensation or unemployment compensation laws.

Periods for which severance payments are made.

Depending on the purpose of calculating service, your hours are calculated based either on a plan year or an employment year. A "plan year" is the 12-month period beginning on each June 1 and ending on the following May 31.

An "employment year" (12 consecutive months) varies for each employee. Your first employment year is the 12-month period beginning on the day that you are first credited with an hour of service. Subsequent employment years are the 12-month periods beginning on the anniversary of the day you were first credited with an hour of service. For example, if you first reported for work with Nike on July 15, 2012, your first employment year would be from July 15, 2012 to July 14, 2013. Subsequent employment years would be the 12-month period beginning on each subsequent July 15.

Military Leave If you are performing certain military service, you earn hours of service for hours you normally would have worked if you were not on leave.

To receive these hours of service and the other benefits outlined in this section, you must return to work at Nike after the military service within the time period set by law and meet any generally-applicable Nike policies regarding qualifying military leave.

You may also be eligible to “make up" 401(k) Before-Tax Contributions that you would otherwise have been able to make to the RSP had you not been on military service leave. Be aware that such “401(k) Make-Up Contributions” must be made within certain time limits.

Before-Tax Match contributions associated with your 401(k) Make-Up Contributions will be contributed to your account as outlined in the plan document.

NIKE U.S. EMPLOYEE HANDBOOK January 15, 2013

7

Whether or not you decide to contribute 401(k) Make-Up Contributions, any Profit Sharing Contributions you would have been eligible for if you had worked for Nike during the military service will be contributed to your Profit Sharing Retirement Account.

Contact the Nike Retirement Plan Center for more information as soon as you return from military service.

NIKE U.S. EMPLOYEE HANDBOOK January 15, 2013

8

401(k) PLAN

Enrolling in the 401(k) Before-Tax Account and the After-Tax Account If you are an eligible employee, you can elect to start saving in the 401(k) Before-Tax Account and/or the After-Tax Account as early as your first day of employment with Nike. If you want to contribute, you have to make an election—there is no automatic enrollment for your contributions. Payroll deductions start in the first pay period of the month following processing of your enrollment request. If you don't enroll when you are first eligible, you can enroll effective for any subsequent payday as long as your enrollment request is received at least 10 days before the payday.

Before you enroll in the Retirement Savings Plan, you will need to make some important decisions:

How much of your pay you want to save in the RSP,

Whether you want to make 401(k) Before-Tax or After-Tax Contributions or both,

How you want your contributions (including Before-Tax Match Contributions) invested among the Pre-mixed Portfolios, the Core Individual Funds and the Nike Stock Fund, and

Who will receive your account balance if you die.

How to Enroll You may enroll in the Retirement Savings Plan through:

the RSP Internet site at www.resources.hewitt.com/nike, or

the Nike Retirement Plan Center 800.987.6535.

Once you have enrolled in the RSP, you will receive a written confirmation of your RSP elections in the mail. Review it carefully. If there are any errors, please contact the Nike Retirement Plan Center at 800.987.6535

Please note: You automatically participate in the Profit Sharing portion of the RSP when you become eligible for that component of the RSP. You don't have to fill out any forms. See the detailed discussion of the Profit Sharing Retirement Account below.

Contributions to the 401(k) Before-Tax Account and the After-Tax Account

Employee 401(k) Before-Tax Contributions 401(k) Before-Tax Contributions are deducted from your paycheck before your federal, and in

most cases, state and local income taxes are calculated. 401(k) Before-Tax Contributions do not affect your Social Security or Medicare withholding.

You may contribute any whole percentage up to 50% of your pay from Nike to the 401(k) Before-Tax Account, subject to IRS limitations. Pay is described in the section below.

NIKE U.S. EMPLOYEE HANDBOOK January 15, 2013

9

The annual IRS dollar limit on 401(k) Before-Tax Contributions to the Retirement Savings Plan for 2013 is $17,500. This limit includes all before-tax contributions that you make to employer-sponsored qualified 401(k) plans (and 403(b) plans, if you are eligible for that type of plan) for the calendar year. If you participate in the RSP and another plan during the same calendar year, you are responsible for monitoring this limit. Contributions in excess of the limit must be refunded to avoid adverse tax consequences. The IRS may adjust this limit from time to time.

Participants who will reach age 50 by December 31 of the calendar year will be able to make additional "catch-up" contributions for that calendar year over and above the general $17,500 401(k) Before-Tax contributions limit. The maximum catch-up contribution for 2013 is $5,500. The IRS may adjust this limit from time to time.

Once you have made $17,500 (or $23,000 if you will be at least age 50 by December 31, 2013) in 401(k) Before-Tax Contributions during the calendar year, Nike’s payroll system will automatically stop deducting 401(k) Before-Tax Contributions from your pay for the remainder of the calendar year. Deductions for your 401(k) Before-Tax Contributions will then resume at the same percentage with the start of the next calendar year.

After-Tax Contributions You can also contribute up to 3% of your pay from Nike to the After-Tax Account with a total maximum contribution of 50% of pay (the combination of 401(k) Before-Tax and After-Tax Contributions cannot exceed 50% of your pay). These contributions are deducted from your paycheck after federal and any state and local withholding amounts are calculated. Although these contributions do not reduce your current taxable income, your investment earnings will be exempt from tax until distributed. In accordance with federal law, the after-tax contribution level of certain highly compensated employees may be restricted or excess contributions returned.

Making Changes to Your Contributions You can change your contribution amounts at any time during the year, subject to legal limits and the plan maximum contribution percentage. To increase, lower, or stop the amount you contribute to the RSP:

Access the RSP Internet site at www.resources.hewitt.com/nike, or

Call the Nike Retirement Plan Center at 800.987.6535.

Change requests are effective as soon as administratively practicable. Change requests submitted at least 10 business days prior to a payday will generally be effective with the next payday. Change requests submitted less than 10 business days prior to a payday will generally be effective the second payday following the request.

Stopping and Re-Starting Contributions There may be times when you need to stop making 401(k) Before-Tax or After-Tax Contributions to the RSP.

If you are voluntarily stopping your contributions, you need to access the RSP Internet site at www.resources.hewitt.com/nike or call the Nike Retirement Plan Center at 800.987.6535 to set your contribution rate to 0%.

NIKE U.S. EMPLOYEE HANDBOOK January 15, 2013

10

Once you are ready to start contributing to the RSP again, you need to access the RSP Internet site or call the Nike Retirement Plan Center to set your contribution rate and designate your investment choices for future contributions.

Military Service—Make-up Contributions If you are on a qualified military leave, you may be eligible to "make up" 401(k) Before-Tax Contributions that you would otherwise have been able to make to the RSP if you had not been on military service leave. Such 401(k) Make-Up Contributions must be made within five years after you return to work or, if less, within a time period equal to three times the length of your military leave. Investment returns are calculated only from the date of deposit of your 401(k) Make-Up Contributions; there are no investment gains and losses prior to the date that your 401(k) Make-Up Contributions are deposited to the RSP. If you go on military leave, please contact the Nike Retirement Plan Center for a more complete explanation of your rights under the RSP.

Nike Before-Tax Match Contributions When you contribute to your 401(k) Before-Tax Account, Nike adds Before-Tax Match Contributions as well. These are called “Nike Before-Tax Match Contributions.” Nike will match 100% of the first 5% of your pay that you contribute to the account in each payroll period. See below for a description of "pay" for calculating contributions. After-Tax Contributions are not eligible for Nike Before-Tax Match Contributions.

Nike Before-Tax Match Contributions will be made for 401(k) Before-Tax Contributions and will be contributed each payroll period, based on your deferrals and pay from Nike during that pay period. All Before-Tax Match Contributions made by Nike are 100% vested as soon as they are contributed to your account. Should you leave Nike for any reason, you will be eligible to receive the value of those contributions along with the rest of your account balance.

Also, if you return from a qualified military leave and make 401(k) Make-Up Contributions to the RSP, Nike will make Before-Tax Match Contributions on your make-up contributions under the terms and conditions of the RSP in effect during your period of military service.

Please note:

You only receive Nike Before-Tax Match Contributions for pay periods during which you actually contribute to the RSP. This means that if you do not make 401(k) Before-Tax Contributions to the RSP during a given pay period, you will not receive any Nike Before-Tax Match Contributions for that pay period.

If you contribute large amounts early in the calendar year and reach the IRS 401(k) contribution limit before the end of the calendar year, you will not receive a Nike Before-Tax Match Contribution for any pay period in which you do not make 401(k) Before-Tax Contributions. As a result, there are times where consistently contributing a lower percentage (at least 5% of your pay for each pay period) will result in a higher Before-Tax Match contribution than fluctuating between high percentages and zero contributions within the same year.

Definition of Pay

NIKE U.S. EMPLOYEE HANDBOOK January 15, 2013

11

For purposes of 401(k) Before-Tax Contributions, After-Tax Contributions, and Nike Before-Tax Match Contributions, your pay includes taxable income payable through Nike's U.S. payroll and reported on your Form W-2, such as:

salary,

overtime,

shift differential,

holiday pay,

PTO actually used during the year,

commissions,

most bonuses,

the transfer premium for employees in the Global Transferee Program,

your before-tax contributions to the Nike benefit plans,

your 401(k) Before-Tax Contributions to the RSP, and

gainsharing payments.

Pay (for purposes of the RSP) does not include:

expense reimbursements,

moving expense allowances,

income from the exercise of stock options,

service awards,

severance pay,

relocation pay,

benefit credits,

lump sum payments in lieu of PTO or vacation not taken,

pay for work performed for affiliates not paid through NIKE, Inc. or an adopting affiliate’s payroll,

Long Term Incentive Payments,

NIKE, Inc. Deferred Compensation Plan (DCP) deferrals,

Short Term Disability (STD) and Long Term Disability (LTD) payments, and

other special pay.

Any amounts paid after termination of employment will not be counted for purposes of calculating 401(k) Before-Tax Contributions, After-Tax Contributions, and Nike Before-Tax Match Contributions under the RSP.

The IRS imposes a limit on the annual pay that can be considered for making contributions to the Retirement Savings Plan.

For the plan year ending May 31, 2013, this limit is $250,000. This limit is increasing for the plan year ending May 31, 2014 to $255,000.

NIKE U.S. EMPLOYEE HANDBOOK January 15, 2013

12

The IRS may adjust this limit from time to time.

Note: For employees in the Global Transferee Program, pay also includes the Transfer Premium but excludes other compensation adjustments that are related to an overseas assignment.

Rollovers From Another Plan You may receive a lump sum payment or a qualified partial payment from:

another employer's qualified retirement (foreign accounts or plans do not qualify for rollover to the RSP under current U.S. tax rules), thrift, savings, or stock ownership plan or

a 403(b) tax sheltered annuity or

an eligible section 457 deferred compensation plan sponsored by a state or local governmental employer.

If so, you may be able to roll over (or transfer) that money to the Retirement Savings Plan to keep it protected from current taxes and penalties.

The RSP can only accept rollovers in cash.

Shares of stock and loans from your prior plan cannot be rolled directly into the RSP.

Federal law regulates the timing of rollovers and the types of payments which can be rolled over.

o For example, you can roll over money from an Individual Retirement Account (IRA) only if it originally came from another employer's plan in a non-annuity form and has been kept separate from regular IRA funds (in a rollover or conduit IRA).

o Periodic annuity payments generally are not eligible for rollover treatment.

o Also, the RSP accepts rollovers only of amounts that would be includible in your taxable income if they were not rolled over. Technically, amounts that may be rolled over are known as "eligible rollover distributions'" and the distributing plan or IRA should inform you as to whether they meet these requirements.

o Not all eligible rollover distributions may be accepted by the RSP. Therefore, before requesting a distribution from another plan or IRA, you should check with the Nike Retirement Plan Center to confirm whether an amount is eligible for rollover into the RSP.

If you receive a check made payable to you from your former employer's retirement plan or from a rollover IRA, you must complete a rollover within 60 days of receiving that check, or the money distributed from your old employer's retirement plan or rollover IRA becomes immediately taxable to you and ineligible for rollover.

Amounts which you have contributed directly to your own IRA—and any earnings on those amounts—are not eligible to be rolled over into the RSP.

Nike does not match Rollover Contributions, but they can continue to grow on a tax-deferred basis through your investments.

You decide how you want the funds invested when you transfer the money into the RSP.

Rollover Contribution amounts are always 100% vested and available for withdrawal.

The RSP reserves the right to refuse any rollover contribution that, in the judgment of the Plan Administrator, would jeopardize the RSP's tax qualified status.

NIKE U.S. EMPLOYEE HANDBOOK January 15, 2013

13

If you expect to receive an eligible rollover distribution and want to roll it over to the Retirement Savings Plan, you may:

Request information from the RSP Internet site

Call the Nike Retirement Plan Center at 800.987.6535

Investing in Your Retirement Savings Plan Accounts The investment rules vary depending on the type of RSP account. The following table gives you an overview of the rules, and you can find more details in the sections that follow the table.

401(k) Before-Tax Account You direct the investments After-Tax Account You direct the investments Rollover Account You direct the investments Transferred Account You direct the investments Nike Before-Tax Match Contributions Account You direct the investments Note: Prior to May 13, 2011 participants did not direct the investment of their Nike Before-Tax Contributions. Instead, participants were automatically invested in the Nike Stock Fund, but could transfer out of the fund at any time. Profit Sharing Retirement Account Invested in a diversified account directed by a professional investment manager; you do not direct the investments in this account

Investments You Direct Your account balances in the RSP are held in a trust fund (the Trust) maintained by The Northern Trust Company, the RSP's trustee. Your Retirement Savings Plan accounts grow as you contribute to the RSP and Nike adds Nike Before-Tax Match Contributions. However, your account balances will also increase or decrease based on the performance of the investment options that you select and could be less than the total amount of your contributions. You direct the investment of your accounts from among the offered three Pre-mixed Portfolios, five Core Individual Funds, the Nike Stock Fund and the Schwab Personal Choice Retirement Account (PCRA). The Plan Administrator will follow your investment directions without reviewing them in any way. The information about the RSP’s investment choices that is provided to you by the Plan Administrator should not be considered as investment advice.

Note:

The Retirement Savings Plan is intended to satisfy the requirements of section 404(c) of the Employee Retirement Income Security Act of 1974 (ERISA) and U.S. Department of Labor Regulation section 2550.404c-1.

Under the RSP, you have the responsibility for selecting the funds in which your 401(k) Before-Tax, After-Tax, Rollover, Transferred and Before-Tax Match Contribution Accounts will be invested. Nike, the Retirement Committee, the RSP’s trustee, and other plan fiduciaries are

NIKE U.S. EMPLOYEE HANDBOOK January 15, 2013

14

not responsible for the investment choices you make or any investment losses that may result from your investment choices.

If you terminate from Nike and are subsequently rehired and do not designate an investment alternative, all of your accounts will be invested in the default investment fund specified by the Plan Administrator in accordance with regulations under ERISA section 404(c)(5). The Plan Administrator may change the default investment fund from time to time. The Plan Administrator’s designation of a default investment fund should not be interpreted as a recommendation or endorsement of that fund for you or any other RSP participant.

The performance of investment funds is not guaranteed. Nike, the Retirement Committee, the RSP’s trustee, and other plan fiduciaries are not liable for any losses you may experience due to investment performance.

The Retirement Committee, as Plan Administrator, is the fiduciary responsible for providing you with information about the RSP's investment options and making sure your investment directions are followed. The Retirement Committee’s responsibilities are carried out in conjunction with Nike HR Direct and a third party administrator.

You direct the investment mix of your 401(k) Before-Tax, Nike Before-Tax Match, After-Tax, Rollover and Transferred Accounts when you enroll in the Retirement Savings Plan. You may divide your money among investment options in 1% increments, subject to the limits on investment in the Nike Stock Fund. To change your investment of existing fund balances or future contributions, access the RSP Internet site or call the Nike Retirement Plan Center. Depending on your investment goals, you may select a variety of the three Pre-mixed Portfolios, five Core Individual Funds, and the Nike Stock Fund to meet your risk and reward objectives. When making your investment decisions, remember that:

The Pre-mixed Portfolios, Core Individual Funds, and Nike Stock Fund have varying degrees of risk.

Past returns may not be an accurate forecast of future returns.

While you always own 100% of your 401(k) Before-Tax, After-Tax, Nike Before-Tax Match

Contributions and Rollover Accounts, their values may increase or decrease depending on your investment choices. You have many choices for investing your 401(k) Before-Tax, After-Tax, Nike Before-Tax Match Contributions, and Rollover Accounts. The RSP offers three Pre-mixed Portfolios and five Core Individual Funds managed by professional investment managers, the Nike Stock Fund, and a brokerage window choice known as the Schwab Personal Choice Retirement Account® (PCRA), which allows you to expand your investment options.

In addition to the information provided under “Investment Options” below, you have a right to receive the following information available in the Investment Performance Update (mailed to you with your quarterly statement) and Quarterly Fund Data Sheets and upon request:

Information about the value of shares or units held in the various investment alternatives for your account.

Information about the value of each fund and the past and current investment performance of the fund.

A description of each fund’s annual operating expenses.

Copies of the financial statements and/or reports on the funds and of any other materials relating to the funds that are provided to the Plan Administrator.

A list of the underlying assets of each investment fund and the value of each asset.

NIKE U.S. EMPLOYEE HANDBOOK January 15, 2013

15

To receive any of this information, please refer to Quarterly Fund Data Sheets located in the 401k Plan Details section on the Nike Intranet site or you may request them from the RSP Internet site at www.resources.hewitt.com/nike or through the Nike Retirement Plan Center at 800.987.6535. A written request may also be sent to the Plan Administrator at the address listed in the “Administrative Facts” section of the Nike U.S. Employee Handbook.

Investment Options Following are summaries of your current investment choices. For more details on the funds, please refer to the Quarterly Fund Data Sheets (available through the RSP Internet site or from the Nike Retirement Plan Center.) The data sheets include important information including material about fund managers, portfolios, performance history, and investment management fees. The first three options are Pre-mixed Portfolios, the next five described below (i.e., the funds other than the Schwab PCRA) are sometimes referred to in this summary as the “Core Individual Funds.” Finally, there is the Nike Stock Fund.

Two Approaches

There are two different approaches to investing in your Retirement Savings Plan accounts. The first approach is for investors who prefer the simplicity of investing in one fund choice that is professionally managed and covers all major asset classes. The Pre-mixed Portfolios are designed for these investors. The Pre-mixed Portfolios provide three different combinations of the various investment funds to create a choice of funds with either a conservative, moderate, or aggressive investment style. It is important to note that the Pre-mixed Portfolios are made up of the same funds as the Core Individual Funds. Note: The Nike Stock Fund is not in the Pre-mixed Portfolios; if you want to invest in the Nike Stock Fund (subject to limitations discussed below), you must select the Nike Stock Fund in addition to your designated Pre-mixed Portfolio. The second approach is for investors who prefer to customize their accounts. Customizing your Retirement Savings Plan account takes more effort than choosing a Pre-mixed Portfolio. If you choose a customized approach, you direct investment into the mix of funds that you believe are appropriate investments for your personal situation.

Pre-mixed Portfolios Conservative Pre-mixed Portfolio invests more in conservative fixed assets (stable value

and bonds) than in stocks. This Conservative Portfolio will likely experience less up and down price movement than a more aggressive portfolio, but will also have a lower long-term return potential.

Moderate Pre-mixed Portfolio invests in a balance of conservative fixed assets (stable value and bonds) and stocks. This Moderate Portfolio will likely experience a moderate long-term return potential with more up and down price movement than the Conservative Portfolio.

Aggressive Pre-mixed Portfolio invests most of its money in the stock market. The Aggressive Portfolio will tend to have a higher long-term return potential, but will also likely experience more up and down price movement than the other two portfolios.

Core Individual Funds Stable Value Fund invests in contracts issued by insurance companies and other financial

institutions, which pay interest in exchange for the use of your money. While this type of

NIKE U.S. EMPLOYEE HANDBOOK January 15, 2013

16

investment is designed to minimize risk, there is still a chance that an insurance company or bank may default, causing a loss. Because stable value investments can be safer than both stocks and bonds, you can expect to earn less from them over the long run.

Bond Fund invests in corporate and government bonds. When you purchase a bond, you are lending money to a company or government entity. In addition to paying back the original loan amount, bond issuers also pay interest, which usually remains fixed throughout the term of the bond. Even though the interest rate may be constant, bonds aren't risk-free. This is because the value of a bond changes with external interest rates. Generally, when external interest rates drop, the value of a bond goes up (and vice versa). In addition, it is possible that the bond issuer may default on its obligations, i.e., be unable to repay the principal loan amount and/or the interest. So, while bonds are usually less volatile than stocks, there is still the possibility of loss.

Large Company Stock Fund invests in established, recognized large U.S. companies. Generally, these are companies with a market capitalization of over $3 billion.

Small Company Stock Fund invests in small U.S. companies. These companies typically rely on fewer product lines and/or innovative new products and strategies, which presents the opportunity for greater growth but also the risk that these companies could fail.

International Company Stock Fund invests in equity opportunities in the Americas, Europe, Asia, and some emerging markets. Currency value changes and foreign politics may affect returns and increase the volatility of this type of fund.

Nike Stock Fund The Nike Stock Fund is invested in Nike Class B Common Stock, giving Retirement Savings Plan participants who elect to invest in the Nike Stock Fund ownership in Nike, Inc. Any dividends paid on Nike stock held in your account are credited to your account and invested in additional shares of Class B Common Stock. It is important to note that individual stocks are inherently subject to more risk than a diversified portfolio of holdings.

The RSP’s trustee is responsible for exercising any voting rights that attach to shares of Nike Class B Common Stock held in your accounts. The trustee acts as a fiduciary in exercising those rights and must act in the best interests of RSP participants and beneficiaries. Note that the Nike Stock Fund is unitized with a small cash reserve, and the value of the fund may be affected by the cash reserve, income earned on the cash, and other trust activities that generally account for small differences in the rate of return compared to direct purchase of Nike stock. Your balance in the Nike Stock Fund is expressed in equivalent shares, to learn more please visit the RSP Web site at www.resources.hewitt.com/nike and go to Manage Investments where you will find information on how equivalent shares are calculated in the Answer Center (select the link for Unit Accounting).

There are two separate and distinct limits with respect to how you may elect to invest in the Nike Stock Fund. The first limit applies to directing the investment of your future contributions, and the second limit applies to changes in the investment of your existing accounts.

Future Investments: You can invest up to 10% of your future 401(k) Before-Tax and After-Tax Contributions, Nike Before-Tax Match Contributions, and Rollover Contributions into the Nike Stock Fund.

o For example, assume your 401(k) eligible earnings are $1,000 per pay period, your 401(k) Before-Tax Contribution rate is 5% and you elect 10% of your future payroll contributions into the Nike Stock Fund:

NIKE U.S. EMPLOYEE HANDBOOK January 15, 2013

17

Your Before-Tax Contributions into the Nike Stock Fund is $5 ($1,000 x 5% x 10% limit)

Nike Before-Tax Match into the Nike Stock Fund is also $5 ($1,000 x 5% x 10% limit)

Total of $10 invested into the Nike Stock Fund each pay period

Current Investments: While you may elect to diversify and transfer out of the Nike Stock Fund at any time, you may only direct the investment of your existing accounts into the Nike Stock Fund if the current percentage invested in the fund is 20% or less of your RSP account balance*. Your investment in the Nike Stock Fund will not automatically be reduced to 20% of your current account balance*. There is no limit on the total amount of stock you can accumulate in the Nike Stock Fund, you may contribute up to 10% of your future contributions (see above) into the fund even if the fund is 20% or more of your current account balance*. The market price used to calculate your Nike Stock Fund balance will be the closing price on the New York Stock Exchange for Nike Class B Common Stock from the previous trading day. There are two ways to manage your existing account balances that you direct on the RSP Web site.

o Fund to Fund Transfer: Allows you to direct the existing investment in a fund(s) to another fund(s).

o Redistribute Current Balance Among Funds: Allows you to select the percentage you want invested in each fund. The RSP Web site will calculate the amounts to move between existing funds to equal the percentages you have designated. If you use this method, the Nike Stock Fund percentage must equate to 20% or less of your RSP account balance*. Therefore, if your existing Nike Stock Fund balance is greater than the 20%, you will be required to lower your investment to an amount that results in Nike Stock Fund being no more than 20% or less of your RSP account balance*. If you do not want to decrease your existing Nike Stock Fund balance, then you must use the Fund to Fund Transfer method.

o Note for participants with a balance in the Schwab Personal Choice Retirement Account (PCRA): While the PCRA account is not displayed on the Fund to Fund Transfer or Redistribute Current Balance Among Funds pages on the RSP Web site, the system will include your PCRA balance in the calculation of the 20% limit (the PCRA balance used in the calculation will be from the close of the previous business day).

*RSP Account Balance: For purposes of the 20% limitation described above, the account balance includes only those accounts where you direct the investment (i.e., excludes the Profit Sharing Account, if applicable).

Nike stock diversification: All participants have the opportunity to move amounts invested in the Nike Stock Fund, including Nike Before-Tax Match Contributions made before May 13, 2011, into the Core Individual Funds or Pre-Mixed Portfolios within the Retirement Savings Plan. The same Core Individual Funds, Pre-Mixed Portfolios and Nike Stock Fund (limits apply) are options for amounts subject to your investment direction. This gives you control over investment of your RSP accounts by providing the option to diversify investments and move amounts in the Nike Stock Fund into Core Individual Funds or Pre-mixed Portfolios, each with different investment risk and reward characteristics.

NIKE U.S. EMPLOYEE HANDBOOK January 15, 2013

18

Up to 100% of your balance invested in the Nike Stock Fund may be transferred into any of the investment options available under the RSP at any time.

To diversify from the Nike Stock Fund, submit your request by:

Accessing the RSP Web site at www.resources.hewitt.com/nike, or

Calling the Nike Retirement Plan Center at 800.987.6535

For each of the investment options, refer to the Quarterly Fund Data Sheets located on the Nike HR Website (go to Human Resources, then under Benefits select 401(k) Plan Details), or you may request a free copy from the RSP Web site at www.resources.hewitt.com/nike or through the Nike Retirement Plan Center at 800.987.6535. The Quarterly Fund Data Sheets provide more information on how the options compare in risk and reward characteristics in determining the best fit for your situation.

The Schwab Personal Choice Retirement Account® (PCRA) The Schwab Personal Choice Retirement Account® (PCRA) is an investment choice within the RSP that is set up through Charles Schwab. Through the PCRA you are able to invest in mutual funds other than the three Pre-mixed Portfolios, five Core Individual Funds and the Nike Stock Fund that are offered within the RSP. This gives you a wider range of investment options. There are fees that will be charged directly to your PCRA, based on the transactions that you instruct Charles Schwab to make. Note: Your investments in the Nike Stock Fund and Profit Sharing Fund are not eligible for transfer to the PCRA.

Opening a PCRA

There are two ways to request the Retirement Savings Plan PCRA Enrollment Kit to open an account in the PCRA:

From the RSP Internet site at www.resources.hewitt.com/nike, and

From the Nike Retirement Plan Center at 800.987.6535.

The information in the Retirement Savings Plan PCRA Enrollment Kit from Charles Schwab will include:

Limited Power of Attorney (LPOA) form (this form must be completed and returned to the Nike Retirement Plan Center before your account will be opened).

Access to mutual funds available through the account.

A handbook containing information on how to place trade orders and access information about your account.

Information on the fees that will be charged to your account as a result of the investment instructions you provide to Charles Schwab.

Once your completed LPOA form is received by the Nike Retirement Plan Center, it will be forwarded to Schwab, and your PCRA will be opened shortly thereafter (in approximately 10 days).

Transferring money to the PCRA

Once your PCRA is opened, you can transfer money from your Pre-mixed Portfolios and/or five Core Individual Funds within the Retirement Savings Plan to the PCRA for investing.

NIKE U.S. EMPLOYEE HANDBOOK January 15, 2013

19

You will need to access the RSP Internet site or call the Nike Retirement Plan Center to start the process.

You must indicate how much money (in whole dollars) you wish to transfer from each of the Core Individual Funds to your PCRA.

This money will then be transferred to your PCRA and, once the transaction settles (it may take two or three days), it will initially be held in the Schwab Money Market Fund.*

The minimum that can be transferred from your Pre-mixed Portfolios and/or five Core Individual Funds to your PCRA at any time is $1,000. In addition, you must leave at least $250 in your Pre-mixed Portfolios and/or five Core Individual Funds at the time that you make the transfer.

To invest within your PCRA, you must contact Charles Schwab directly. Charles Schwab will provide you with instructions about how to place trade orders in your PCRA, along with a list of available mutual funds. The Charles Schwab fund list will provide you with important details specific to each mutual fund that you can invest in, such as minimum investment requirements, fund-level fees and any other fees or commissions associated with the purchase or sale of each fund. For more information visit www.schwab.com or call 888.393.7272.

Charles Schwab will send you confirmations of all trades within your PCRA. They will also provide you with a detailed statement of your PCRA account balance and activity at the end of each calendar quarter (March 31, June 30, September 30, and December 31) and for each month there is transaction activity in your PCRA.

The RSP Internet site and the Nike Retirement Plan Center will be updated daily with the total amount invested in your PCRA, but will not provide you with mutual fund level detail. As a result, you should review your PCRA statements carefully.

*An investment in the Schwab Money Market Fund is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency. Although the Schwab Money Market Fund seeks to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in the Schwab Money Market Fund.

Your Investment Earnings and Statements Your share in any given investment fund depends on the amount of your investments, your account activity, and actual fund value changes. Investment returns are posted to your accounts each business day. Nike Class B Common Stock dividends on the Nike Stock Fund are credited to your accounts when paid.

Each plan quarter, you will receive a statement which shows in the current balances of your Retirement Savings Plan accounts and related fee and expense detail. You will also receive an annual fee disclosure statement with information on the RSP’s investment options, fees and other expenses. Access the RSP Internet site or call the Nike Retirement Plan Center at 800.987.6535 for more up-to-date account balances, or to see an online statement. Quarterly Fund Data Sheets are also available in the 401K Plan Details section of the Nike Intranet site as well as through the RSP Internet site and the Nike Retirement Plan Center.

Making Changes to Your Retirement Savings Plan Investments By accessing the RSP Internet site or calling the Nike Retirement Plan Center, you can switch where you invest current balances or future contributions. You can make changes on a daily basis;

NIKE U.S. EMPLOYEE HANDBOOK January 15, 2013

20

however, in certain instances the changes will not take effect until the next business day following the day you make the changes. See "Investment changes for your current account balance" below, for more details on the timing of transactions to change your investment directions for your existing account balance. Although the RSP recordkeeping system is capable of tracking daily investment changes, this does not imply that daily trading of your RSP account is a sound investment strategy.

Changing how you invest your future contributions and your existing account balances are two unrelated transactions. You must complete a separate request for each transaction.

Investment changes for your future contributions

You may change your investment elections for future contributions at any time. When you make a change, it will affect the investment of all contributions that are made to your account from that time forward until you make another change.

This change will not impact the investment direction of your existing account balance.

When you make a change, you may direct your future contributions to any mix of the three Pre-mixed Portfolios, the five Core Individual Funds and the Nike Stock Fund in 1% increments. However, the Nike Stock Fund is limited to a maximum of 10%.

Note: you cannot direct future contributions directly to the PCRA; see the section titled “Schwab Personal Choice Retirement Account® (PCRA)” (above) for information on using the PCRA.

Investment changes for your current account balance

You may change the investment mix of the value of your existing account balance at any time by accessing the RSP Internet site or calling the Nike Retirement Plan Center at 800.987.6535. You have two ways to make this change:

Fund to Fund Transfer: Allows you to direct the existing investment in a fund(s) to another fund(s).

o Note: You may only direct the investment of your existing accounts into the Nike Stock Fund if the current percentage invested in the fund is 20% or less of your RSP account balance*.

Redistribute Current Balance Among Funds: Allows you to select the percentage you want invested in each fund. The RSP Web site will calculate the amounts to move between existing funds to equal the percentages you have designated.

Note: If you use this method and have an existing balance in the Nike Stock Fund, the percentage of the fund must equate to 20% or less of your RSP account balance*. Therefore, if your existing Nike Stock Fund balance is greater than the 20%, you will be required to lower your investment to an amount that results in Nike Stock Fund being no more than 20% or less of your RSP account balance*. If you do not want to decrease your existing Nike Stock Fund balance, then you must use the Fund to Fund Transfer method.

*RSP Account Balance: For purposes of the 20% limitation described above, the account balance includes only those accounts where you direct the investment (i.e., excludes the Profit Sharing Account, if applicable).

For a transaction to occur on the day of your call, the call must be completed prior to market close – generally 1 p.m. Pacific Time. If your call is completed after market close, the

NIKE U.S. EMPLOYEE HANDBOOK January 15, 2013

21

transaction will occur at the close of the next business day (for this purpose, "business day" means any day that the New York Stock Exchange is open and trading).

Note: For the Nike Stock Fund the market price used to calculate your Nike Stock Fund balance will be the closing price from the previous trading day. If you transfer or redistribute into or out of the Nike Stock Fund, the market price will be the closing price at the end of the current trading day.

ACCESSING YOUR 401(k) BEFORE-TAX, AFTER-TAX, ROLLOVER AND TRANSFERRED ACCOUNT BALANCE

Loans The Retirement Savings Plan is designed to help you save for your retirement years. However, there may be times when you feel that you have a more immediate financial need. The Retirement Savings Plan includes a loan program that may be able to help.

If you have an account in the Retirement Savings Plan with employee contributions (either 401(k) Before-Tax, After-Tax, or Rollover Contributions), you can borrow from your account by applying for a loan from the money in your account. Transferred Accounts comprised of employee contributions, including Roth Contributions, will also be available for a loan. Funds in the Nike Before-Tax Match Contributions Account and the Profit Sharing Retirement Account are not available for loans.

The Retirement Savings Plan allows participants to have up to two loans outstanding at any time.

There are two kinds of loans available:

General purpose loans (these loans must be repaid within 5 years of the date the loan is taken)

Primary residence loans (these loans must be repaid within 10 years of the date the loan is taken)

Points to consider when deciding whether or not to take a loan

If you leave employment with Nike for any reason, your outstanding loan balance becomes immediately due and payable in full. If not repaid within the time frame indicated on the Separation of Employment Notice that will be sent to you, the unpaid balance becomes a taxable distribution and may also be subject to a 10% penalty tax.

A loan may change the earnings on your account, since the money you borrow is no longer invested with the rest of your account. Although you pay interest on the loan amount, the interest you pay on your loan may differ from the gain/loss that money would have received if it had remained invested according to your investment elections.

Taking out a loan will reduce the amount available to you for withdrawals until you repay the loan in full.

How the loan money comes out of your account

When you take a loan from your account, the money will come out in the following order:

After-Tax Account

NIKE U.S. EMPLOYEE HANDBOOK January 15, 2013

22

Rollover Account

401(k) Before-Tax Account

Transferred Account (including Roth Account), if applicable

Within each account, your loan will be treated as having been made on a pro-rata basis from each of the investment funds you selected for the investment of your account. When the money is paid back into your account, it is repaid in the reverse order from how it came out (first to your 401(k) Before-Tax Account, then your Rollover Account, and finally your After-Tax Account) except your Transferred Account is always paid last. As the loan payments go back into your account, they will be invested in the same manner as you are currently investing your future contributions.

Example

Current Balances 401(k) Before-Tax Account $8,000 After-Tax Account $1,500 Rollover Account $3,000 Total $12,500 Employee takes a $6,000 loan. The $6,000 will be borrowed from the accounts in this order:

First: After-Tax Account

Next: Rollover Account

Last: 401(k) Before-Tax Account

$1,500

$3,000

$1,500 Repayment of the loan will be in the following order:

First: 401(k) Before-Tax Account

Next: Rollover Account

Last: After-Tax Account

$1,500

$3,000

$1,500

Interest on your loan

You will pay a fixed interest rate established when you request a loan. Your interest rate will equal the prime lending rate + 1%, and will be fixed for the life of your loan. An exception may apply if you are on qualified military leave; contact the Nike Retirement Plan Center at 800.987.6535 if this may apply to you.

How much can you borrow?

The minimum loan is $1,000.

The maximum loan is the lesser of 50% of your vested account balance, limited to the amount in your 401(k) Before-Tax, After-Tax, Rollover and Transferred (employee contributions only) Accounts or $50,000 reduced by the highest aggregate loan balance in the preceding 12 months (even if the loan was previously paid off).

You cannot borrow more than the total amount in your 401(k) Before-Tax, After-Tax, Rollover and Transferred (employee contributions only) Accounts.

NIKE U.S. EMPLOYEE HANDBOOK January 15, 2013

23

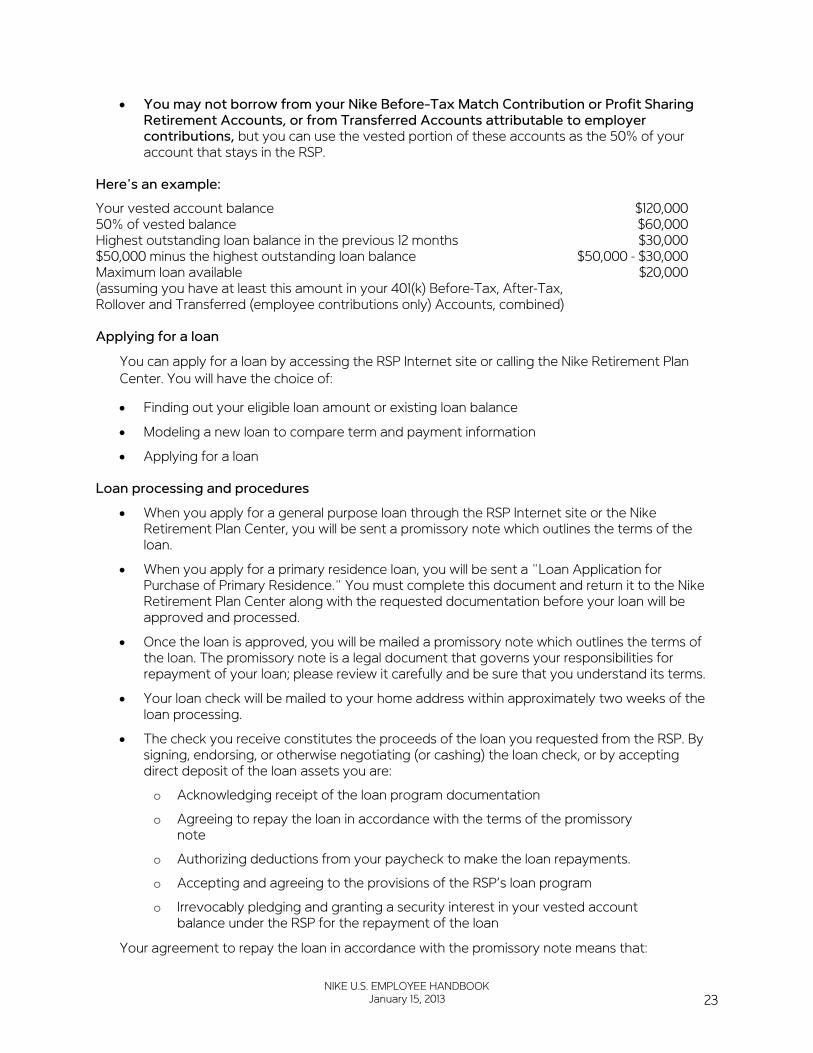

You may not borrow from your Nike Before-Tax Match Contribution or Profit Sharing Retirement Accounts, or from Transferred Accounts attributable to employer contributions, but you can use the vested portion of these accounts as the 50% of your account that stays in the RSP.

Here's an example:

Your vested account balance $120,000 50% of vested balance $60,000 Highest outstanding loan balance in the previous 12 months $30,000 $50,000 minus the highest outstanding loan balance $50,000 - $30,000 Maximum loan available $20,000 (assuming you have at least this amount in your 401(k) Before-Tax, After-Tax, Rollover and Transferred (employee contributions only) Accounts, combined)

Applying for a loan

You can apply for a loan by accessing the RSP Internet site or calling the Nike Retirement Plan Center. You will have the choice of:

Finding out your eligible loan amount or existing loan balance

Modeling a new loan to compare term and payment information

Applying for a loan

Loan processing and procedures

When you apply for a general purpose loan through the RSP Internet site or the Nike Retirement Plan Center, you will be sent a promissory note which outlines the terms of the loan.

When you apply for a primary residence loan, you will be sent a "Loan Application for Purchase of Primary Residence." You must complete this document and return it to the Nike Retirement Plan Center along with the requested documentation before your loan will be approved and processed.

Once the loan is approved, you will be mailed a promissory note which outlines the terms of the loan. The promissory note is a legal document that governs your responsibilities for repayment of your loan; please review it carefully and be sure that you understand its terms.

Your loan check will be mailed to your home address within approximately two weeks of the loan processing.

The check you receive constitutes the proceeds of the loan you requested from the RSP. By signing, endorsing, or otherwise negotiating (or cashing) the loan check, or by accepting direct deposit of the loan assets you are:

o Acknowledging receipt of the loan program documentation

o Agreeing to repay the loan in accordance with the terms of the promissory note

o Authorizing deductions from your paycheck to make the loan repayments.

o Accepting and agreeing to the provisions of the RSP’s loan program

o Irrevocably pledging and granting a security interest in your vested account balance under the RSP for the repayment of the loan

Your agreement to repay the loan in accordance with the promissory note means that:

NIKE U.S. EMPLOYEE HANDBOOK January 15, 2013

24

o You agree that your loan payments (including interest and any finance charges) will be made by payroll deduction as provided in the payment schedule.

o You assign and grant to the RSP a security interest of up to 50% of your account balance as security for prompt and full repayment of the loan.

o If the loan is for a period of greater than five years, you certify that the purpose of the loan is for the purchase of your principal residence.

Repaying your loan

Your loan payments will start as soon as administratively possible and will be deducted from your paycheck on an after-tax basis.

Prepaying your loan

You may prepay your loan in full at any time. Partial repayments are not permitted and will be returned to you.

To prepay your loan, you will need to access the RSP Internet site at www.resources.hewitt.com/nike or call the Nike Retirement Plan Center at 800.987.6535. You will be sent the payoff amount as of the end of each of the next three calendar months. It is important that you follow the instructions that you receive exactly in order to correctly prepay your loan.

If you default on your loan

A default on a loan from the Retirement Savings Plan triggers a taxable event because the loan amount is treated as a deemed distribution from your Retirement Savings Plan account. If you default on a loan, the amount of the default will be reported to the IRS as a taxable distribution in the year the default occurs. In addition to ordinary income taxes, you may have to pay the additional 10% penalty tax on the amount of the deemed distribution. You will receive a Form 1099-R for the year of the default showing that you have received this distribution from the RSP. It is your responsibility to report the income to the IRS and pay the appropriate taxes and any applicable penalties that are assessed as a result.

If you leave the company

All outstanding loans become due and payable in full immediately following your termination of employment from Nike (including cases of layoff or reduction in force). Note that transfer from Nike to or from a participating affiliate will not cause your loan to become due.

Once the Plan Administrator is notified of the termination of your employment, you will be sent a Separation of Employment Notice that includes specific information on how and when to repay your loan in order to avoid a taxable distribution from the RSP. If you do not repay your loan balance within the stated time period, your loan will become a taxable distribution to you at that time and may be subject to tax penalties.

Loans while on approved leave of absence

If you go on a leave of absence up to 12 months, no loan payments will be required during your approved leave. You have the following options to repay your loan:

Continue to pay your loan repayment by requesting monthly loan coupons; or

NIKE U.S. EMPLOYEE HANDBOOK January 15, 2013

25

Suspend your loan payments during the leave.

o If you suspend your loan repayments during your leave, when you return from the leave, your loan will automatically be reamortized, extending the term of your loan to take into account the payments you missed during your leave. The new repayment term cannot exceed IRS limits on loan terms – five years for general purpose loans and ten years for primary residence loans. If your loan term cannot be extended, your repayment deductions amount will be increased to incorporate payments missed during your leave. When you return to work, new deduction amounts will be based on the revised loan schedule. The revised schedule will take into account the missed payments during the time you did not make any loan payments. Contact the Nike Retirement Plan Center for more information on making loan repayments during your leave.

You also have the option to make a one-time balloon payment for the repayments missed during your leave. If you would like to make a balloon payment, please contact the Nike Retirement Plan Center prior to your return from leave to make arrangements.

If your leave continues for more than 12-months, you will be required to begin making manual loan repayments beginning with the 13th month of your leave. You will receive information regarding how to begin making manual loan repayments. If the loan repayment amount is not received when due, the outstanding loan amount will default and permanently reduce your account balance. In addition, the outstanding loan amount will be treated as a distribution and may be subject to tax and penalty, and will continue to be treated as an active loan until the outstanding loan amount is paid in full. This means that the defaulted loan will continue to count toward one of the two loans available to you.

In cases of a qualified military leave, loan repayments are suspended for the period of leave, even if the leave is longer than 12 months, and the final due date of the loan is also extended by the period of military leave. For more information on loans while on military leave, contact the Nike Retirement Plan Center.

Withdrawals Before Termination of Employment The Retirement Savings Plan’s objective is to help you supplement your retirement income. But if you need access to your money before you retire, there are ways to make withdrawals from your account while you are still an active employee. For information on distributions after your employment with Nike ends, see the section titled “When You Leave Nike.”

If you have an After-Tax Contributions Account or Rollover Account in the RSP and you are an active employee, you may withdraw all or part of the After-Tax Contributions Account or Rollover Account while you are still employed. The rules are described at the end of this section.

If you have a Before-Tax Match Contributions Account, you may not withdraw any amounts from this account before you terminate employment, unless you become disabled. For purposes of the RSP, you are disabled if, as a result of a physical or mental illness or injury, you are unable to perform the material duties or essential functions of your occupation. The determination is made by the Plan Administrator, which may rely on medical experts of its choosing.

You may take an in-service distribution of all of your vested accounts, including your Before-Tax Contribution Account, your Nike Before-Tax Match Contribution Account, and your Transferred Account when you reach age 59½ or you become disabled (as defined above).

NIKE U.S. EMPLOYEE HANDBOOK January 15, 2013

26

You may take an in-service distribution from your Before-Tax Contribution Account or Transferred Accounts attributable to employee contributions before age 59 1/2 if you have a financial hardship. Additional in-service withdrawal rights for participants on qualifying military leave apply to certain Transferred Accounts attributable to employee contributions. For more information, please contact the Nike Retirement Plan Center.

Financial Hardship Withdrawal Rules "Financial hardship" is an immediate and heavy financial need that cannot be met from any other available source, including Retirement Savings Plan loans and withdrawal of After-Tax and Rollover Contributions. “Dependent” for purposes of a hardship withdrawal is defined in Internal Revenue Code section 152 (generally those who you may claim as dependents on your federal tax return). Hardship withdrawals are available only to meet the following financial situations:

Medical expenses for you or your dependents that are not covered by a medical plan or other insurance, and that would be deductible under Internal Revenue Code section 213 (ignoring the 7.5% of adjusted gross income test).

Purchase of your primary residence (i.e., a down payment and closing costs, but not mortgage payments).

Post-high school tuition and related fees for you, your spouse, or dependents for the next 12 months.

Payment to prevent foreclosure on (or eviction from) your primary residence.

Funeral expenses for your spouse or your parents or your children or your dependents.

Repair of damage to your principal residence not compensated for by insurance that would qualify for the casualty deduction under Internal Revenue Code section 165 without regard to whether the loss exceeds 10% of adjusted gross income (examples include damage caused by fire, theft or storm).

Expenses caused by natural disasters where relief is granted by the IRS, such as for expenses related to Hurricane Sandy.

Here are the rules that govern hardship withdrawals:

You must take the maximum loans available to you from the RSP (if you are eligible) before you can request a hardship withdrawal.

You must withdraw all currently available distributions from the RSP, including After-Tax Contributions and Rollover Contributions, before you can request a hardship withdrawal.

Your contributions to the 401(k) Before-Tax Account must stop for 6 months after the date you receive the hardship withdrawal. After the 6 month suspension period is over, you may resume making 401(k) Before-Tax Contributions up to the annual limits permitted under the RSP.

You can withdraw your 401(k) Before-Tax Contributions only. Earnings on your 401(k) Before-Tax Contributions cannot be withdrawn.

You can only withdraw enough money to meet your demonstrated financial need, which can include amounts necessary to pay federal, state, and local taxes that you expect to have to pay because of the hardship withdrawal.

You cannot withdraw Profit Sharing Retirement Account or your Before-Tax Match Contribution Account funds until you reach age 59 1/2, even due to financial hardship.

NIKE U.S. EMPLOYEE HANDBOOK January 15, 2013

27

Hardship withdrawals are subject to income taxes. The withdrawal may also be subject to a 10% IRS "early withdrawal penalty" if you receive a hardship withdrawal before you reach age 59½. Hardship withdrawals are not eligible for rollover.

Your withdrawal will be deducted proportionately from each of the investment funds in which your 401(k) Before-Tax and/or Transferred Accounts are invested at the time of withdrawal.

Special rules may apply to withdrawal of Transferred Accounts. Please contact the Nike Retirement Plan Center for more information if this applies to you.

Special rules may apply to withdrawals for expenses caused by natural disasters in accordance with IRS guidance.

To apply for a hardship withdrawal:

You may request a hardship withdrawal form by accessing the RSP Internet site or by contacting the Nike Retirement Plan Center at 800.987.6535.

You must submit the completed form and supporting documentation to the Nike Retirement Plan Center.

You will need to provide documentation verifying the amount needed to meet your financial hardship.

Your withdrawal cannot exceed the amount needed to meet your immediate financial need.

IRS regulations provide that a hardship withdrawal may include amounts for the payment of federal and state taxes on the withdrawal if you so request.

After-Tax and Rollover Account Withdrawal Rules The rules for After-Tax and Rollover Account withdrawals are less restrictive than those for withdrawals from 401(k) Before-Tax Accounts:

You can take a withdrawal from your After-Tax or Rollover Account (including earnings) for any reason.

You cannot withdraw any of the Nike After-Tax Match Contributions contributed before June 1, 2000 on your After-Tax Contributions until you reach age 59 1/2, retire or leave Nike.

The minimum after-tax withdrawal amount is $500. The maximum withdrawal is limited to your After-Tax and Rollover Account balances on the day the withdrawal is processed.

When you make an after-tax or rollover withdrawal, you withdraw both After-Tax and Rollover Contributions and tax-deferred investment earnings in proportion to what is in your account.

You'll pay regular income taxes on a withdrawal from your Rollover Account. You’ll only pay income taxes on a withdrawal from your After-Tax Account to the extent you did not already pay tax. If you’re under age 59½, you will also pay the 10% IRS early withdrawal penalty on the earnings portion of the withdrawal.

Age 59 1/2 Withdrawals If you reach age 59 1/2 and remain employed by Nike, you may request withdrawal of all of your vested accounts. The withdrawal will occur from your accounts in the following order:

NIKE U.S. EMPLOYEE HANDBOOK January 15, 2013

28

After-Tax Contribution Account

Transferred Account attributable to Roth Contributions from the Cole Haan Plan

Rollover Contribution Account

Transferred Account attributable to Roth Rollover Contributions from the Cole Haan Plan

Before-Tax Contribution Account (unmatched)

Before-Tax Contribution Account (matched)

After-Tax Match Contribution Account

Vested Match Account

Nike Before-Tax Match Contribution Account

Transferred Accounts attributable to profit sharing contributions under the Cole Haan Plan

Nike Profit Sharing Retirement Account

Withdrawals After Termination of Employment See discussion under the heading “When You Leave Nike.”

Profit Sharing Retirement Account The Profit Sharing Retirement Account is a key Nike contribution to your future.

Only Nike makes contributions to your Profit Sharing Retirement Account. You do not contribute anything to this account. Each year, Nike's Board of Directors determines the Profit Sharing Contribution amount (if any) based on Nike's annual financial performance and business considerations. Nike's Board of Directors has complete discretion to determine whether to make a Profit Sharing Contribution for a particular year.

Eligibility If Nike makes a Profit Sharing Contribution for a plan year, you will receive a portion of the contribution if you are eligible. Eligibility is based on your service, which is described in more detail below. To be eligible, you must be an eligible employee (as described above under the heading “Eligibility Rules for the Retirement Savings Plan”) and satisfy the following:

You must complete 1,000 hours of service in at least one “employment year” (12 consecutive months) to become an RSP participant for Profit Sharing Contribution purposes. Your participation date is the June 1 (or subsequent business day if June 1 falls on a weekend) that occurs during the first employment year when you complete 1,000 hours of service with Nike or any Nike affiliate. For example, if you are hired on September 1, 2010 and complete 1,000 hours by August 31, 2011, your participation date is June 1, 2011. You must still satisfy the additional plan year service requirements to receive an allocation of Nike’s Profit Sharing Contribution for that plan year.

Once you are an RSP participant for Profit Sharing Contribution purposes, to receive a contribution for any given plan year, you must complete 1,000 or more hours of service with Nike or a participating affiliate during the plan year. Hours of service with a Nike affiliate who has not adopted the RSP do not count for this purpose. You must also be employed by Nike

NIKE U.S. EMPLOYEE HANDBOOK January 15, 2013

29

or any Nike affiliate on the last business day (usually May 31) of the plan year for which contributions are made.

Once you satisfy the initial eligibility requirements for the Profit Sharing Retirement Account, you do not have to satisfy them again. If you terminate employment and are later rehired, you will be eligible to receive a Profit Sharing Contribution if you complete 1,000 or more hours of service with Nike or a participating affiliate during the plan year of rehire and are employed by Nike or any Nike affiliate on the last business day (usually May 31) of the plan year of rehire. However, if you terminate employment prior to satisfying the initial eligibility requirements for Profit Sharing Contribution purposes and are later rehired, you will be treated as a new employee for purposes of satisfying the eligibility requirements.

Service You need to be familiar with the following terms to determine how much service you have under the RSP.

An "hour of service" is an hour for which you are actually paid or entitled to be paid.

Employees paid by the hour (non-exempt employees) receive credit for paid hours actually worked.

Salaried employees (exempt employees) receive 190 hours of service for each month in which they work at least one hour, regardless of actual hours worked.

You also may earn up to 501 hours of service per year for paid time when you are not actually working, including time spent on approved:

o Paid time off (PTO)

o Holidays

o Family and/or medical leaves of absence

o Disability leave

o Other leaves of absence specifically approved by Nike if the employee returns or retires within the approved leave period and fulfills all other conditions imposed for the leave.

For eligibility to participate, hours of service include hours you work with Nike or any affiliate. For contribution purposes, hours of service only includes hours of service with Nike or a participating affiliate. Hours of service with Nike affiliates starts from the date of acquisition of the affiliate by Nike unless you were covered by an affiliate plan that merged into the Nike RSP. In that case, all service recognized under your prior plan is recognized under the RSP. If this applies to you and you have questions regarding your service, please contact the Nike Retirement Plan Center.

Hours of service do not include:

Periods during which you receive payments only under worker's compensation or unemployment compensation laws.

Periods for which severance payments are made.

If you are in qualified military service, you earn hours of service for hours you normally would have worked. To receive these hours of service, you must return to work at Nike after your military service within the time period set by law. These hours of service are not limited to 501 hours of service per year spent on qualified military service leave.

NIKE U.S. EMPLOYEE HANDBOOK January 15, 2013

30

As indicated above, depending on the purpose for calculating service, your hours are calculated based either on a plan year or an employment year. A "plan year" is the 12-month period beginning on each June 1 and ending on the following May 31.

An "employment year" (12 consecutive months) varies for each employee. The first employment year is the 12-month period beginning on the day that you are first credited with an hour of service. Subsequent employment years are the 12-month periods beginning on the anniversary of the day you were first credited with an hour of service. For example, if you first reported for work with Nike on July 15, 2012, your first employment year would be from July 15, 2012 to July 14, 2013. Subsequent employment years would be the 12-month period beginning on each subsequent July 15.

Calculating Your Share Here's how your allocation of the Profit Sharing Contribution is calculated:

Nike's Board of Directors decides on a total Profit Sharing Contribution.

Your share of the total is based on your pay as a percentage of the total pay for all eligible employees. All eligible participants receive the same percentage of pay as an allocation of the Profit Sharing Contribution.