Embed Size (px)

Citation preview

NOTICE

$5,000,000*

SILVER CONSOLIDATED SCHOOL DISTRICT NO. 1

GRANT COUNTY, NEW MEXICO

GENERAL OBLIGATION SCHOOL BUILDING BONDS

SERIES 2017

Preliminary Official Statement, subject to completion,

June 9, 2017

The Preliminary Official Statement, dated June 9, 2017 (the "Preliminary Official Statement"),

relating to the above-described bonds (the "Bonds") of the Silver Consolidated School District No. 1 (the

"District"), has been posted as a matter of convenience. The posted version of the Preliminary Official

Statement has been formatted in Adobe Portable Document Format. Although this format should replicate

the Preliminary Official Statement available from the District, appearance may vary for a number of

reasons, including electronic communication difficulties or particular user software or hardware. Using

software other than Adobe Acrobat may cause the Preliminary Official Statement that you view or print to

differ in appearance from the Preliminary Official Statement.

The Preliminary Official Statement and the information contained therein are subject to completion

or amendment or other change without notice. Under no circumstances shall the Preliminary Official

Statement constitute an offer to sell or the solicitation of an offer to buy nor shall there be any sale of the

Bonds in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or

qualification under the securities laws of any such jurisdiction.

For purposes of Rule 15c2-12 promulgated by the Securities and Exchange Commission, the

Preliminary Official Statement alone, and no other document or information on the internet, constitutes the

"Official Statement" that the District has deemed "final" as of its date in respect of the Bonds, except for

certain information permitted to be omitted therefrom.

No person has been authorized to give any information or to make any representations other than

those contained in the Preliminary Official Statement in connection with the offer and sale of the Bonds

and, if given or made, such information or representations must not be relied upon as having been

authorized. The information and expressions of opinion in the Preliminary Official Statement are subject

to change without notice and neither the delivery of the Official Statement nor any sale made thereunder

shall, under any circumstances, create any implication that there has been no change in the affairs of the

District since the date of the Preliminary Official Statement.

By choosing to proceed and view the electronic version of the Preliminary Official Statement, you

acknowledge that you have read and understood this Notice.

Preliminary Official Statement June 9, 2017.

_______________________________ *Preliminary, subject to change

BOOK-ENTRY ONLY MOODY’S RATING: “Baa2” MOODY’S ENHANCED RATING: “Aa2”

BANK QUALIFIED

The delivery of the Bonds is subject to the opinions of Rodey, Dickason, Sloan, Akin, & Robb, P.A., Bond Counsel. On the initial date

of delivery of the Bonds, Rodey, Dickason, Sloan, Akin, & Robb, P.A. will render its opinion that, under existing laws, regulations, rulings, and judicial decisions, and assuming continuing compliance with the covenants described herein, interest on the Bonds is excluded from gross income

for federal income tax purposes and is not a specific preference item for purposes of the federal alternative minimum tax. The interest on the Bonds

may be subject to certain federal taxes imposed only on certain corporations, including imposition of the corporate alternative minimum taxes on a portion of that interest. Also on the initial date of delivery of the Bonds, Bond Counsel will render its opinion that interest on the Bonds is exempt,

under existing law, from personal income taxation by the State of New Mexico. See "Legal Matters" and "Tax Matters" herein for a discussion of

Bond Counsel’s opinion, including a description of certain alternative minimum tax consequences for corporations. See "TAX MATTERS" regarding certain other tax considerations.

$5,000,000*

SILVER CONSOLIDATED SCHOOL DISTRICT NO. 1

GRANT COUNTY, NEW MEXICO

GENERAL OBLIGATION SCHOOL BUILDING BONDS

SERIES 2017

Dated: Date of Delivery Due: August 1, as shown below

The Series 2017 Bonds (the “Bonds”) are issuable as fully registered bonds and, when issued, will be registered in the name of Cede &

Co., as nominee of The Depository Trust Company, New York, New York to which principal and interest payments on the Bonds will be made.

Individual purchases will be made in book-entry form only, in the principal amount of $5,000 or any whole multiple thereof. Purchasers of the Bonds will not receive physical delivery of bond certificates. So long as Cede & Co. is the registered owner of the Bonds, reference herein to the

holders of the Bonds or registered owner of the Bonds shall mean Cede & Co. and shall not mean the Beneficial Owners of the Bonds. So long as Cede & Co. is the registered owner of the Bonds, the principal and interest (first payable on February 1, 2018 and thereafter semiannually on each

August 1 and February 1) are payable to Cede & Co., which will in turn remit such principal and interest to the DTC Participants (as defined herein)

for subsequent disbursement to the Beneficial Owners of the Bonds. See "Book Entry Only System" herein.

The Bonds maturing on and after August 1, 2026 are subject to optional redemption on August 1, 2025, or any date thereafter at par plus

accrued interest to the redemption date.

Proceeds of the Bonds will be used for the purpose of erecting, remodeling, making additions to and furnishing school buildings;

purchasing or improving school grounds, purchasing computer software and hardware for student use in public schools, providing matching funds for capital outlay projects funded pursuant to the Public School Capital Outlay Act; or any combination of these purposes, and to pay the cost of

issuance of the Bonds, and to reimburse the District for expenditures made for the foregoing purposes, said Bonds are to be payable from general

(ad valorem) taxes and to be issued and sold at such time or times upon such terms and conditions as the Board may determine.

MATURITIES, INTEREST RATES AND YIELDS*

Year Maturing Interest Year Maturing Interest

(August 1) Principal Rate Yield Cusip # (August 1) Principal Rate Yield Cusip #

2018 $1,180,000 2028 195,000

2019 130,000 2029 205,000

2020 135,000 2030 215,000

2021 145,000 2031 225,000

2022 150,000 2032 235,000

2023 155,000 2033 245,000

2024 165,000 2034 255,000

2025 170,000 2035 265,000

2026 180,000 2036 275,000

2027 185,000 2037 290,000

The Bonds are offered for delivery when, as, and if issued, subject to the approval of legality by Rodey, Dickason, Sloan, Akin, & Robb,

P.A., Santa Fe, New Mexico, Bond Counsel, and certain other conditions. The written approval of the New Mexico Attorney General of the Bonds

as to form and legality will be supplied. It is expected that the Bonds will be available for delivery through the facilities of The Depository Trust

Company, New York, New York on or about June 30, 2017*.

Dated: June __, 2017

*Preliminary, subject to change.

BAIRD

USE OF INFORMATION IN THIS OFFICIAL STATEMENT

No dealer, salesman or other person has been authorized by the Silver Consolidated School District

No. 1 (the "District") to give any information or to make any statements or representations, other than those

contained in this Official Statement, and, if given or made, such other information, statements or

representations must not be relied upon as having been authorized. This Official Statement does not

constitute an offer to sell or solicitation of an offer to buy any of the Bonds in any jurisdiction in which

such offer or solicitation is not authorized, or in which any person making such offer or solicitation is not

qualified to do so, or to any person to whom it is unlawful to make such offer or solicitation in such

jurisdiction. The information set forth or included in this Official Statement has been provided by the

District and from other sources believed by the District to be reliable. The information and expressions of

opinion herein are subject to change without notice, and neither the delivery of this Official Statement nor

any sale hereunder shall create any implication that there has been no change in the financial condition or

operations of the District described herein since the date hereof. This Official Statement contains, in part,

estimates and matters of opinion that are not intended as statements of fact, and no representation or

warranty is made as to the correctness of such estimates and opinions or that they will be realized.

The Bonds have not been registered under the Securities Act of 1933, in reliance upon exemptions

contained in such Act. The registration and qualification of the Bonds in accordance with applicable

provisions of the securities law of the states in which the Bonds have registered or qualified and the

exemption from registration or qualification in other states cannot be regarded as a recommendation thereof.

Neither the Securities and Exchange Commission nor any other federal, state, municipal or other

governmental entity, nor any agency or department thereof, has passed upon the merits of the Bonds or the

accuracy or completeness of this Official Statement. Any representation to the contrary may be a criminal

offense.

This Official Statement is "deemed final" by the District for purposes of Rule 15c2-12 of the

Municipal Securities Rulemaking Board. The District has covenanted to provide such annual financial

statements and other information in the manner as may be required by regulations of the Securities and

Exchange Commission or other regulatory body.

IN MAKING AN INVESTMENT DECISION INVESTORS MUST RELY ON THEIR OWN

EXAMINATION OF THE DISTRICT AND THE TERMS OF THE OFFERING, INCLUDING THE

MERITS AND RISKS INVOLVED. THESE SECURITIES HAVE NOT BEEN RECOMMENDED BY

ANY FEDERAL OR STATE SECURITIES COMMISSION OR REGULATORY AUTHORITY.

FURTHERMORE, THE FOREGOING AUTHORITIES HAVE NOT CONFIRMED THE ACCURACY

OR DETERMINED THE ADEQUACY OF THIS DOCUMENT. ANY REPRESENTATION TO THE

CONTRARY IS A CRIMINAL OFFENSE.

This Official Statement contains statements that are "forward-looking statements" as defined in the

Private Securities Litigation Reform Act of 1995. When used in this Official Statement, the words

"estimate," "project," "intend," "expect," and similar expressions are intended to identify forward-looking

statements. Such statements are subject to risks and uncertainties that could cause actual results to differ

materially from those contemplated in such forward-looking statements. Readers are cautioned not to place

undue reliance on these forward-looking statements, which speak only as of the date hereof.

SILVER CONSOLIDATED SCHOOL DISTRICT NO. 1

GRANT COUNTY, NEW MEXICO

2810 N. Swan Street

Silver City, New Mexico 88061

(575) 956-2000

BOARD OF EDUCATION

President Mike McMillan

Vice President Frances Vasquez

Secretary Ashley Montenegro

Member Patrick Cohn

Member Justin Wecks

ADMINISTRATION

Superintendent

Associate Superintendent

Audie Brown

Candy Milam

Director of Finance Michele McCain

MUNICIPAL ADVISOR

George K. Baum & Company

6565 Americas Parkway NE, Suite 860

Albuquerque, New Mexico 87110

(505) 872-2320

BOND COUNSEL

Rodey, Dickason, Sloan, Akin, & Robb, P.A.

201 3rd Street NW, Suite 2200

Albuquerque, New Mexico 87102

(505) 765-5900

PAYING AGENT/REGISTRAR

BOKF, NA

100 Sun Avenue NE, Suite 500

Albuquerque, NM 87109

(505) 222-8447

UNDERWRITER

Robert W. Baird & Co., Inc.

210 University Blvd., Suite 460

Denver, Colorado 80206

(303) 270-6337

i

TABLE OF CONTENTS

Page

INTRODUCTORY INFORMATION .......................................................................................................... 1

SUMMARY INFORMATION ..................................................................................................................... 2

DEBT SERVICE REQUIREMENTS ............................................................................................................ 3

DESCRIPTION OF THE BONDS ............................................................................................................... 4

AUTHORIZATION AND USE OF PROCEEDS ........................................................................................ 4

PAYING AGENT/REGISTRAR .................................................................................................................. 4

PAYMENT OF PRINCIPAL AND INTEREST; RECORD DATE ............................................................ 4

REGISTRATION, TRANSFER AND EXCHANGE .................................................................................. 5

PRIOR REDEMPTION ................................................................................................................................ 5

BOOK ENTRY ONLY SYSTEM ................................................................................................................ 5 General ...................................................................................................................................................... 6

SECURITY AND SOURCE OF PAYMENT .............................................................................................. 7

TAX MATTERS ........................................................................................................................................... 7

NEW MEXICO INCOME TAX OPINION ................................................................................................. 8

QUALIFIED TAX-EXEMPT OBLIGATIONS ........................................................................................... 9

LEGALITY ................................................................................................................................................... 9

REGISTRATION ......................................................................................................................................... 9

LITIGATION ................................................................................................................................................ 9

CONTINUING DISCLOSURE .................................................................................................................. 10 Annual Reports ........................................................................................................................................ 10 Material Event Notices ............................................................................................................................ 10 Availability of Information from MSRB and SID .................................................................................. 11 Limitations and Amendments ................................................................................................................. 11

COMPLIANCE WITH PRIOR UNDERTAKINGS .................................................................................. 11

RATING ..................................................................................................................................................... 12

NEW MEXICO SCHOOL DISTRICT ENHANCEMENT PROGRAM ................................................... 12

TRANSCRIPT AND CLOSING DOCUMENTS ...................................................................................... 12

MUNICIPAL ADVISOR ............................................................................................................................ 13

ii

UNDERWRITING ..................................................................................................................................... 13

ADDITIONAL INFORMATION ............................................................................................................... 13

OFFICIAL STATEMENT CERTIFICATION ........................................................................................... 14

BORROWING CAPACITY ........................................................................................................................ 15

FINANCIAL INFORMATION .................................................................................................................. 16 Reassessment ........................................................................................................................................... 17 Comparison of Assessed Value ............................................................................................................... 18 Assessed Valuation of the Largest Centrally Assessed Taxpayers in the District .................................. 18

TAX RATES ............................................................................................................................................... 18 Yield Control ........................................................................................................................................... 18

TAX DATA ................................................................................................................................................ 19 Method of Tax Collection ....................................................................................................................... 20 Interest On Delinquent Taxes .................................................................................................................. 20 Delinquent Taxes Penalty ........................................................................................................................ 20 Remedies Available for Non-Payment of Taxes ..................................................................................... 21

OUTSTANDING GENERAL OBLIGATION BONDS ............................................................................ 22 Authorized but Unissued General Obligation Bonds .............................................................................. 22

SILVER CONSOLIDATED SCHOOL DISTRICT NO. 1 .......................................................................... 23 General .................................................................................................................................................... 23 Board of Education .................................................................................................................................. 23 Administrative Staff ................................................................................................................................. 23 Enrollment History ................................................................................................................................... 23 Finances of the Educational Program ....................................................................................................... 24 General Fund ........................................................................................................................................... 24

APPENDIX A – General Information – Grant County

APPENDIX B – Form of Opinion of Bond Counsel

APPENDIX C – Excerpt of District’s 2016 Audited Financial Report

APPENDIX D – Form of Continuing Disclosure Undertaking

1

INTRODUCTORY INFORMATION

This Official Statement has been prepared by George K. Baum & Company, employed by the Silver

Consolidated School District No. 1 (the "District") to perform professional services in the capacity of

Municipal Advisor. The purpose of this Official Statement is to provide information concerning the

offering by the District of General Obligation School Building Bonds, Series 2017, dated June 30, 2017*

in the principal amount of $5,000,000* (the "Bonds") approved by the voters at a regular school bond

election held February 7, 2017. All financial and other information presented in this Official Statement has

been obtained from the District, the Grant County Assessor’s and Treasurer’s offices, the State of New

Mexico Public Education Department and other sources which are believed to be reliable, but such

information is not guaranteed as to accuracy or completeness and its inclusion is not to be construed as a

representation on the part of the Board of Education of the District (the “Board”). No person, including

any broker, dealer or salesman, has been authorized to give any information or to make any representations

other than those contained in this Official Statement, and, if given or made, such other information or

representations must not be relied upon as having been authorized by the Board. Any information or

expressions of opinion herein are subject to change without notice and neither the delivery of the Official

Statement nor any supplement to the Official Statement nor any sale hereunder shall, under any

circumstances, create any implication that there has been no change as to the affairs of the District.

*Preliminary, subject to change.

2

SUMMARY INFORMATION

The following information is not a full description of the Bonds and is subject to the more complete

information contained elsewhere in this Official Statement, including the appendices.

Date of Issue: The Bonds are dated June 30, 2017.*

Purpose: Proceeds of the Bonds will be used for the purpose of erecting, remodeling, making

additions to and furnishing school buildings; purchasing or improving school

grounds, purchasing computer software and hardware for student use in public

schools, providing matching funds for capital outlay projects funded pursuant to

the Public School Capital Outlay Act; or any combination of these purposes, and

to pay the cost of issuance of the Bonds, and to reimburse the District for

expenditures made for the foregoing purposes, said Bonds to be payable from

general (ad valorem) taxes and to be issued and sold at such time or times upon

such terms and conditions as the Board may determine.

Authorization: The Bonds were authorized at a regular election held within the District on

February 7, 2017, and by Resolution of the Board (“Bond Resolution”) adopted on

May 25, 2017, and are issued pursuant to NMSA 1978, Sections 6-15-1 through 6-

15-22, as amended.

Interest Payments: Interest is payable February 1 and August 1, commencing February 1, 2018.

Maturity: The Bonds mature annually on August 1, 2018 through 2037.

Redemption: The Bonds maturing on and after August 1, 2026 are subject to optional

redemption on August 1, 2025, or any date thereafter at par plus accrued interest

to the redemption date.

Security: The Bonds are General Obligation School Building Bonds of the District and are

payable from general ad valorem taxes which may be levied against all taxable

property within the District without limitation as to rate or amount.

Designation: In a resolution authorizing the issuance of the Bonds, the District expects to

designate the Bonds as qualified tax-exempt obligations for purposes of

Section 265(b)(3)(B) of the Internal Revenue Code of 1986, as amended.

Tax Status: Interest on the Bonds is excludable from gross income for federal income tax

purposes and is exempt from taxation by the State of New Mexico. (See “Tax

Matters” herein.)

Delivery: Delivery of the Bonds to the Underwriter is expected on June 30, 2017.*

Registrar/

Paying Agent: BOKF, NA, Albuquerque, New Mexico.

*Preliminary, subject to change.

3

DEBT SERVICE REQUIREMENTS

Series 2017 Bonds* Calendar

Year

Outstanding

Debt Service Principal Interest

Est. Total Debt

Service

2017 $1,475,380

2018 - $1,180,000

2019 - 130,000

2020 - 135,000

2021 - 145,000

2022 - 150,000

2023 - 155,000

2024 - 165,000

2025 - 170,000

2026 - 180,000

2027 - 185,000

2028 - 195,000

2029 - 205,000

2030 - 215,000

2031 - 225,000

2032 - 235,000

2033 - 245,000

2034 - 255,000

2035 - 265,000

2036 - 275,000

2037 - 290,000

(REMAINDER OF PAGE INTENTIONALLY LEFT BLANK)

*Preliminary, subject to change.

4

DESCRIPTION OF THE BONDS

The Bonds will be dated June 30, 2017*, will mature annually on August 1, 2018 through 2037,

and will bear interest at the rates set forth on the cover page of the Final Official Statement.

AUTHORIZATION AND USE OF PROCEEDS

The Bonds are being issued pursuant to the Board's powers under NMSA 1978, Sections 6-15-1

through 6-15-22, as amended and supplemented, the Constitution of the State of New Mexico and other

laws of the State, and the Bond Resolution, and constitute the first installment of $5,000,000 of $20,000,000

of General Obligation School Building Bonds authorized by the qualified voters of the District at a regular

school district election held on February 7, 2017. Pursuant to NMSA 1978, Section 22-18-9, the written

approval of the New Mexico Attorney General will be supplied as to the form and legality of the Bonds.

Proceeds of the Bonds will be used for the purpose of erecting, remodeling, making additions to

and furnishing school buildings; purchasing or improving school grounds, purchasing computer software

and hardware for student use in public schools, providing matching funds for capital outlay projects funded

pursuant to the Public School Capital Outlay Act; or any combination of these purposes, and to pay the cost

of issuance of the Bonds, and to reimburse the District for expenditures made for the foregoing purposes,

said Bonds are to be payable from general (ad valorem) taxes and to be issued and sold at such time or

times upon such terms and conditions as the Board may determine.

PAYING AGENT/REGISTRAR

BOKF, NA, Albuquerque, New Mexico will serve as the Bond Paying Agent/Registrar (the "Paying

Agent/Registrar") for the Bonds.

PAYMENT OF PRINCIPAL AND INTEREST; RECORD DATE

Subject to "Book Entry Only System" below, interest on the Bonds is payable by check mailed on

or before each Interest Payment Date by the Paying Agent/Registrar (defined below) to the registered owner

at the last known address as it appears on the bond registration books (the "Registration Books") kept by

the Paying Agent/Registrar on the Record Date (as defined below), except that the interest on any Bond

payable at the maturity thereof shall be paid only upon presentation of such Bond at the office of the Paying

Agent/Registrar. At the request and expense of a person entitled to a payment of interest on the Bonds,

payment of interest may be made by any other method acceptable to the Paying Agent/Registrar. The

record date (the "Record Date") for the interest payable on any Interest Payment Date is the fifteenth day

of the month next preceding such Interest Payment Date. In the event of a non-payment of interest on a

scheduled payment date, and for 30 days thereafter, a new record date for such interest payment (a "Special

Record Date") will be established by the Paying Agent/Registrar, if and when funds for the payment of

such interest have been received from the District. Notice of the Special Record Date and of the scheduled

payment date of the past due interest (which shall be 15 days after the Special Record Date) shall be sent at

least five business days prior to the Special Record Date by United States mail, first class postage prepaid,

to the address of each registered owner of a Bond appearing on the registration books of the Paying

Agent/Registrar at the close of business on the last business day next preceding the date of mailing of such

notice.

If the date for any payment due on any Bond shall be a Saturday, Sunday, a legal holiday or a day

on which the Paying Agent/Registrar is located is authorized or required by law or executive order to close,

*Preliminary, subject to change.

5

then the date for such payment shall be the next succeeding business day, and payment on such date shall

have the same force and effect as if made on the original date payment was due.

REGISTRATION, TRANSFER AND EXCHANGE

Subject to "Book Entry Only System" below, the Bonds may be transferred, registered and assigned

only on the Registration Books, and such registration and transfer shall be without expense or service charge

to the registered owner, except for any tax or other governmental charges required to be paid with respect

to such registration and transfer. A Bond may be assigned by the execution of an assignment form on the

Bonds or by other instrument of transfer and assignment acceptable to the Paying Agent/Registrar. A new

Bond or Bonds will be delivered by the Paying Agent/Registrar in lieu of the Bond being transferred or

exchanged at the principal corporate trust office of the Paying Agent/Registrar. To the extent possible, new

Bonds issued in an exchange or transfer of Bonds will be delivered to the registered owner or assignee of

the registered owner in not more than three business days after the receipt of the Bonds to be canceled in

the exchange or transfer and the written instrument of transfer or request for exchange duly executed by the

registered owner or its duly authorized agent, in form satisfactory to the Paying Agent/Registrar. New

Bonds registered and delivered in an exchange or transfer shall be in denominations of $5,000 of principal

amount or any integral multiple thereof for any one maturity, shall specify the same maturity date and be

for a like aggregate amount as the Bond or Bonds surrendered for exchange or transfer. Neither the District

nor the Paying Agent/Registrar shall be required to issue, transfer, or exchange any Bond during the period

beginning on the Record Date or Special Record Date and ending on the day subsequent to the next

following Interest Payment Date.

PRIOR REDEMPTION

The Bonds maturing on and after August 1, 2026 are subject to optional redemption on August 1,

2025, or any date thereafter at par plus accrued interest to the redemption date.

BOOK ENTRY ONLY SYSTEM

Unless otherwise noted, the information contained under the caption “General” below has been

provided by The Depository Trust Company ("DTC"). The District makes no representation as to the

accuracy or the completeness of such information. The Beneficial Owners of the Bonds should confirm the

following information with DTC, the Direct Participants or the Indirect Participants.

NEITHER THE DISTRICT NOR THE FISCAL AGENT WILL HAVE RESPONSIBILITY OR

OBLIGATION TO DIRECT PARTICIPANTS, TO INDIRECT PARTICIPANTS, OR TO ANY

BENEFICIAL OWNER WITH RESPECT TO (A) THE ACCURACY OF ANY RECORDS

MAINTAINED BY DTC, ANY DIRECT PARTICIPANT, OR ANY INDIRECT PARTICIPANT; (B)

ANY NOTICE THAT IS PERMITTED OR REQUIRED TO BE GIVEN TO THE OWNERS OF THE

BONDS UNDER THE BOND RESOLUTION; (C) THE SELECTION BY DTC OR ANY DIRECT

PARTICIPANT OR INDIRECT PARTICIPANT OF ANY PERSON TO RECEIVE PAYMENT IN THE

EVENT OF A PARTIAL REDEMPTION OF THE BONDS; (D) THE PAYMENT BY DTC OR ANY

DIRECT PARTICIPANT OR INDIRECT PARTICIPANT OF ANY AMOUNT WITH RESPECT TO

THE PRINCIPAL OR INTEREST DUE WITH RESPECT TO THE OWNER OF THE BONDS; (E) ANY

CONSENT GIVEN OR OTHER ACTION TAKEN BY DTC AS THE OWNERS OF THE BONDS; OR

(F) ANY OTHER MATTER REGARDING DTC.

6

General

The Depository Trust Company (“DTC”), New York, NY, will act as securities depository for the

Bonds. The Bonds will be issued as fully-registered securities registered in the name of Cede & Co. (DTC’s

partnership nominee) or such other name as may be requested by an authorized representative of DTC. One

fully-registered Bond certificate will be issued for each maturity of the Bonds, in the aggregate principal

amount of such maturity, and will be deposited with DTC.

DTC, the world’s largest securities depository, is a limited-purpose trust company organized under

the New York Banking Law, a “banking organization” within the meaning of the New York Banking Law,

a member of the Federal Reserve System, a “clearing corporation” within the meaning of the New York

Uniform Commercial Code, and a “clearing agency” registered pursuant to the provisions of Section 17A

of the Securities Exchange Act of 1934. DTC holds and provides asset servicing for over 3.5 million issues

of U.S. and non-U.S. equity issues, corporate and municipal debt issues, and money market instruments

(from over 100 countries) that DTC’s participants (“Direct Participants”) deposit with DTC. DTC also

facilitates the post-trade settlement among Direct Participants of sales and other securities transactions in

deposited securities, through electronic computerized book-entry transfers and pledges between Direct

Participants’ accounts. This eliminates the need for physical movement of securities certificates. Direct

Participants include both U.S. and non-U.S. securities brokers and dealers, banks, trust companies, clearing

corporations, and certain other organizations. DTC is a wholly-owned subsidiary of the Depository Trust

& Clearing Corporation (“DTCC”). DTCC is the holding company for DTC, National Securities Clearing

Corporation and Fixed Income Clearing Corporation, all of which are registered clearing agencies. DTCC

is owned by the users of its regulated subsidiaries. Access to the DTC system is also available to others

such as both U.S. and non-U.S. securities brokers and dealers, banks, trust companies, and clearing

corporations that clear through or maintain a custodial relationship with a Direct Participant, either directly

or indirectly (“Indirect Participants”). DTC has a Standard & Poor’s rating of AA+. The DTC Rules

applicable to Direct Participants are on file with the Securities and Exchange Commission. More

information about DTC can be found at www.dtcc.com. The District undertakes no responsibility for and

makes no representations as to the accuracy or the completeness of the content of such material contained

on that website as described in the preceding sentence including, but not limited to, updates of such

information or links to other Internet sites accessed through the aforementioned website.

Purchases of the Bonds under the DTC system must be made by or through Direct or Indirect

Participants, which will receive a credit for the Bonds on DTC’s records. The ownership interest of each

actual purchaser of each Bond (“Beneficial Owner”) is in turn to be recorded on the Direct and Indirect

Participants’ records. Beneficial Owners will not receive written confirmation from DTC of their purchase.

Beneficial Owners are, however, expected to receive written confirmations providing details of the

transaction, as well as periodic statements of their holdings, from the Direct or Indirect Participant through

which the Beneficial Owner entered into the transaction. Transfers of ownership interests in the Bonds are

to be accomplished by entries made on the books of Direct and Indirect Participants acting on behalf of

Beneficial Owners. Beneficial Owners will not receive certificates representing their ownership interests in

the Bonds, except in the event that use of book-entry system for the Bonds is discontinued.

To facilitate subsequent transfers, all Bonds deposited by Direct Participants with DTC are

registered in the name of DTC’s partnership nominee, Cede & Co. or such other name as may be requested

by an authorized representative of DTC. The deposit of Bonds with DTC and their registration in the name

of Cede & Co. or such other DTC nominee do not affect any change in beneficial ownership. DTC has no

knowledge of the actual Beneficial Owners of the Bonds; DTC’s records reflect only the identity of Direct

Participants to whose accounts such Bonds are credited, which may or may not be the Beneficial Owners.

The Direct and Indirect Participants will remain responsible for keeping account of their holdings on behalf

of their customers.

7

Conveyance of notices and other communications by DTC to Direct Participants, by Direct

Participants to Indirect Participants, and by Direct Participants and Indirect Participants to Beneficial

Owners will be governed by arrangements among them, subject to any statutory or regulatory requirements

as may be in effect from time to time.

While the Bonds are in the book-entry only system, redemption notices will be sent to DTC. If less

than all of the Bonds are being redeemed, DTC’s practice is to determine by lot the amount of the interest

of each Direct Participant in such issue to be redeemed.

Neither DTC nor Cede & Co. (nor any other DTC nominee) will consent or vote with respect to

the Bonds unless authorized by a Direct Participant in accordance with DTC’s MMI Procedures. Under its

usual procedures, DTC mails an Omnibus Proxy to the District as soon as possible after the record date.

The Omnibus Proxy assigns Cede & Co.’s consenting or voting rights to those Direct Participants to whose

accounts the Bonds are credited on the record date (identified in a listing attached to the Omnibus Proxy).

Redemption proceeds, distributions, and dividend payments on the Bonds will be made to Cede &

Co., or such other nominee as may be requested by an authorized representative of DTC. DTC’s practice is

to credit Direct Participants’ accounts, upon DTC’s receipt of funds and corresponding detail information

from the District or agent on payable date in accordance with their respective holdings shown on DTC’s

records. Payments by Participants to Beneficial Owners will be governed by standing instructions and

customary practices, as is the case with securities held for the accounts of customers in bearer form or

registered in “street name,” and will be the responsibility of such Participant and not of DTC, agent, or the

District, subject to any statutory or regulatory requirements as may be in effect from time to time. Payment

of redemption proceeds, distributions, and dividend payments to Cede & Co. (or such other nominee as

may be requested by an authorized representative of DTC) is the responsibility of the District or agent,

disbursement of such payments to Direct Participants will be the responsibility of DTC, and disbursement

of such payments to the Beneficial Owners will be the responsibility of Direct and Indirect Participants.

DTC may discontinue providing its services as depository with respect to the Bonds at any time by

giving reasonable notice to the District. Under such circumstances, in the event that a successor depository

is not obtained, certificates representing the Bonds are required to be printed and delivered.

The District may decide to discontinue the use of the system of book-entry transfers through DTC

(or a successor securities depository). In that event, certificates representing the Bonds will be printed and

delivered to DTC.

The information in this Official Statement concerning DTC and DTC’s book-entry system has been

obtained from sources that the District believes to be reliable, but neither the District nor the Underwriter

takes any responsibility for the accuracy thereof.

SECURITY AND SOURCE OF PAYMENT

The Bonds are a general obligation of the District. Annual ad valorem taxes will be levied on all

taxable property within the District without limitation as to rate or amount for the purpose of paying

principal and interest on the Bonds.

TAX MATTERS

In the opinion of Rodey, Dickason, Sloan, Akin, & Robb, P.A., Bond Counsel, to be delivered at

the time of the original issuance of the Bonds, under existing laws, regulations, rulings and judicial

8

decisions, the interest on the Bonds is excludable from gross income for federal income tax purposes. Bond

Counsel is further of the opinion that the interest on the Bonds is exempt from taxation by the State and its

political subdivisions.

The Internal Revenue Code of 1986, as amended (the “Code”), imposes various restrictions,

conditions and requirements relating to the exclusion from gross income for federal tax purposes of interest

on obligations, such as the Bonds. The District has covenanted in the Resolution to comply with certain

guidelines designed to assure that interest on the Bonds will not become includible in gross income. Failure

to comply with these covenants may result in the interest on the Bonds being included in gross income from

the date of issue of the Bonds. The opinion of Bond Counsel assumes compliance with such covenants.

Bond Counsel has opined that the interest on the Bonds is not a specific preference item for

purposes of the alternative minimum tax provisions contained in the Code; however, interest on the Bonds

will be included in the adjusted current earnings of certain corporations in the calculation of alternative

minimum tax.

To the extent the issue price of any maturity of the Bonds is less than the amount to be paid at

maturity of such Bonds (excluding amounts stated to be interest and payable at least annually over the term

of such Bonds), the difference constitutes “original issue discount,” the accrual of which, to the extent

properly allocable to each Beneficial Owner thereof, is treated as interest on the Bonds which is excluded

from gross income for federal income tax purposes. Beneficial Owners of the Bonds should consult their

own tax advisors with respect to the tax consequences of ownership of Bonds with original issue discount,

including the treatment of Beneficial Owners who do not purchase such Bonds in the original offering to

the public at the first price at which a substantial amount of such Bonds is sold to the public.

Prospective purchasers of the Bonds should be aware that ownership of the Bonds may result in

collateral federal income tax consequences to certain taxpayers, including, without limitation, financial

institutions, property and casualty insurance companies, individual recipients of Social Security or Railroad

Retirement benefits, certain S corporations with “excess net passive income,” foreign corporations subject

to the branch profits tax, life insurance companies and taxpayers who may be deemed to have incurred or

continued indebtedness to purchase or carry or have paid or incurred certain expenses allocable to the

Bonds. Bond Counsel does not express any opinion regarding such collateral tax consequences. Prospective

purchasers of the Bonds should consult their tax advisors regarding collateral federal income tax

consequences.

The opinion of Bond Counsel is based on existing law, which is subject to change. Such opinion

is further based on factual representations made to Bond Counsel as of the date thereof. Bond Counsel

assumes no duty to update or supplement its opinion to reflect any facts or circumstances that may thereafter

come to its attention, or to reflect any changes in law that may thereafter occur or become effective.

Moreover, the opinion of Bond Counsel is not a guarantee of a particular result, and is not binding on the

IRS or the courts; rather, such opinion represents its professional judgment based on its review of existing

law, and in reliance on the representations and covenants that it deems relevant to such opinion.

NEW MEXICO INCOME TAX OPINION

On the date of initial delivery of the Bonds, Rodey, Dickason, Sloan, Akin, & Robb, P.A. will

render its opinion that interest on the Bonds will be excluded from net income for purposes of New

Mexico state income tax. Rodey, Dickason, Sloan, Akin, & Robb, P.A. expresses no opinion as to any

other federal, state or local tax consequences. (See the Forms of Opinion of Bond Counsel in Appendix

B.)

9

QUALIFIED TAX-EXEMPT OBLIGATIONS

The District intends to designate the Bonds as Qualified Tax-Exempt Obligations. Section 265(a)

of the Internal Revenue Code of 1986 (the “Code”) provides, in pertinent part, that interest paid or incurred

by a taxpayer, including a "financial institution," on indebtedness incurred or continued to purchase or carry

tax-exempt obligations is not deductible by such taxpayer in determining taxable income. Section 265(b)

of the Code provides an exception to the disallowance of such deduction for any interest expense paid or

incurred on indebtedness of a taxpayer which is a "financial institution" allocable to tax-exempt obligations,

other than "private activity bonds," which are designated by a "qualified small issuer" as "qualified tax-

exempt obligations." A "qualified small issuer" is any governmental issuer (together with any subordinate

issuers) who issues no more than $10,000,000 of tax-exempt obligations during the calendar year. Section

265(b)(5) of the Code defines the term "financial institution" as referring to any corporation described in

Section 585(a)(2) of the Code, or any person accepting deposits from the public in the ordinary course of

such person's trade or business which is subject to federal or state supervision as a financial institution.

LEGALITY

Rodey, Dickason, Sloan, Akin, & Robb, P.A., Albuquerque, New Mexico has been retained as

Bond Counsel to the District ("Bond Counsel"). Bond Counsel will provide an unqualified opinion that the

Bonds are legally issued under New Mexico law and that the interest income from the Bonds is exempt

from Federal and State of New Mexico income taxes. Bond Counsel was not requested to and did not take

part in the preparation of the Official Statement nor has it undertaken to independently verify any of the

information contained herein. Bond Counsel has no responsibility for the accuracy or completeness of any

information furnished in connection with any offer or sale of the Bonds, but such counsel prepared in

cooperation with other persons and are partially responsible for the Official Notice of Meeting and Sale

adopted by the Board on May 25, 2017. The legal fees to be paid to Bond Counsel for services rendered in

connection with the issuance of the Bonds are contingent in part upon the sale and delivery of the Bonds.

REGISTRATION

The Bonds have not been registered under the Federal Securities Act of 1933 or the Securities

Exchange Act of 1934, both as amended, in reliance upon the exemptions provided thereunder by

Sections 3(a)(2) and 3(a)(12), respectively, for the issuance and sale of the Bonds; nor have the Bonds been

qualified under the Securities Act of New Mexico. The District assumes no responsibility for qualification

of the Bonds under the securities laws of any jurisdiction in which the Bonds may be sold, assigned,

pledged, hypothecated or otherwise transferred. This disclaimer of responsibility for qualification for sale

or other disposition of the Bonds shall not be construed as an interpretation of any kind with regard to the

availability of any exemption from securities registration provisions.

LITIGATION

There is not now pending or threatened, to the best of the knowledge of the District, any litigation

restraining or enjoining the issuance or delivery of the Bonds or questioning or affecting the validity of the

Bonds or the proceedings or authority under which they are to be issued. Neither the creation, organization

or existence, nor the title of a quorum of the present Board members or other officers of the District to their

respective offices, is being questioned. At the time of delivery of the Bonds, the District will deliver a no-

litigation certificate to that effect.

10

CONTINUING DISCLOSURE

The District has made the following agreement for the benefit of the holders and beneficial owners

of the Bonds. The District is required to observe the agreement for so long as it remains obligated to

advance funds to pay the Bonds. Under the agreement, the District will be obligated to provide certain

updated financial information and operating data annually, and timely notice of specified material events,

to certain information vendors. This information will be available to securities brokers and others who

subscribe to receive the information from the vendors.

Annual Reports

The District will provide certain updated financial information and operating data to certain

information vendors annually. The information to be updated includes all quantitative financial information

and operating data with respect to the District of the general type included in this Official Statement under

the headings “TAX RATES”, “SILVER CONSOLIDATED SCHOOL DISTRICT NO. 1”, "FINANCIAL

INFORMATION - “Direct and Overlapping G.O. Bond Debt Ratios”, and “Analysis of Assessed

Valuations,” and in Appendix C. The District will update and provide this information by March 31 of

each fiscal year beginning in 2018. The District will provide the updated information and operating data

to the Municipal Securities Rulemaking Boards (the “MSRB”) Electronic Market Access System

(“EMMA”).

The District may provide updated information in full text or may incorporate by reference certain

other publicly available documents, as permitted by SEC Rule 15c2-12. The updated information will

include audited financial statements, if the District commissions an audit and it is completed by the required

time. If audited financial statements are not available by the required time, the District will provide

unaudited financial statements by the required time, and will provide audited financial statements when and

if the audit report becomes available. Any such financial statements will be prepared in accordance with

the accounting principles described in Appendix C or such other accounting principles as the District may

be required to employ from time to time pursuant to state law or regulation.

The District's current fiscal year end is June 30th. Accordingly, it must provide updated financial

information and operating data by March 31 in each year, unless the District changes its fiscal year. If the

District changes its fiscal year, it will notify MSRB and any SID of the change.

Material Event Notices

The District will also provide timely notices of certain events to certain information vendors. The

District will provide notice of any of the following events with respect to the Bonds, if such event is material

to a decision to purchase or sell Bonds or Certificates, respectively: (1) principal and interest payment

delinquencies; (2) non-payment related defaults; (3) unscheduled draws on debt service reserves reflecting

financial difficulties; (4) unscheduled draws on credit enhancements reflecting financial difficulties;

(5) substitution of credit or liquidity providers, or their failure to perform; (6) adverse tax opinions or events

affecting the tax-exempt status of the Bonds; (7) modifications to rights of holders of the Bonds; (8) Bond

calls; (9) defeasances; (10) release, substitution or sale of property securing repayment of the Bonds;

(11) rating changes; (12) bankruptcy, insolvency, receivership or a similar event with respect to the District

or an obligated person; (13) the consummation of a merger, consolidation, or acquisition involving an

obligated person or the sale of all or substantially all of the assets of the obligated person, other than in the

ordinary course of business, the entry into a definitive agreement to undertake such an action or the

termination of a definitive agreement relating to any such actions, other than pursuant to its terms, if

material; (14) appointment of a successor or additional trustee, or a change of name of a trustee, if material,

and (15) Tender offers. In addition, the District will provide, within 10 days, notice of any failure by the

11

District to provide information, data or financial statements in accordance with its agreement described

above under "Annual Reports." The District will provide each notice described in this paragraph to the

MSRB.

Availability of Information from MSRB and SID

The District has agreed to provide the foregoing information only to the MSRB and any SID. The

information will be available to holders of Bonds only if the holders comply with the procedures and pay

the charges established by such information vendors or obtain the information through securities brokers

who do so.

No SID has been designated in New Mexico at this time.

Limitations and Amendments

The District has agreed to update information and to provide notices of material events only as

described above. The District has not agreed to provide other information that may be relevant or material

to a complete presentation of its financial results of operations, condition or prospects or agreed to update

any information that is provided, except as described above. The District makes no representation or

warranty concerning such information or concerning its usefulness to a decision to invest in or sell bonds

at any future date. The District disclaims any contractual or tort liability for damages resulting in whole or

in part from any breach of its continuing disclosure agreement or from any statement made pursuant to its

agreement, although holders of Bonds may seek a writ of mandamus to compel the District to comply with

its agreement.

This continuing disclosure agreement may be amended by the District from time to time to adapt

to changed circumstances that arise from a change in legal requirements, a change in law or a change in the

identity, nature, status or type of operations of the District, but only if (1) the provisions, as so amended,

would have permitted an underwriter to purchase or sell Bonds or Certificates in the primary offering of

the Bonds in compliance with the Rule, taking into account any amendments or interpretations of the Rule

since such offering as well as such changed circumstances and (2) either (a) the Holders of a majority in

aggregate principal amount (or any greater amount required by any other provision of the Resolution that

authorizes such an amendment) of the outstanding Bonds consent to such amendment or (b) a person that

is unaffiliated with the District (such as nationally recognized bond counsel) determined that such

amendment will not materially impair the interest of the Holders and beneficial owners of the Bonds. The

District may also amend or repeal the provisions of this continuing disclosure agreement if the SEC amends

or repeals the applicable provision of the Rule or a court of final jurisdiction enters judgment that such

provisions of the Rule are invalid, but only if and to the extent that the provisions of this sentence would

not prevent an underwriter from lawfully purchasing or selling bonds in the primary offering of the Bonds.

COMPLIANCE WITH PRIOR UNDERTAKINGS

Pursuant to Securities and Exchange Commission Rule 15c2-12, the District will undertake to

provide certain ongoing disclosure, including annual operating data and financial information, audited

financial statements and notices of the occurrence of certain material events.

The District previously has entered into such undertakings pursuant to such Rule with respect to

bonds previously issued by it. The District’s continuing disclosure undertakings provide that while the

Series 2005 Bonds are outstanding, the District will provide certain annual financial information to the

national securities repositories within six months after the end of each fiscal year. The District failed to file

its audited financials and financial operating information for the Fiscal Year 2012 within six months of the

12

end of the fiscal year. The District made its 2012 audited financials and financial operating filings available

on EMMA on March 21, 2013.

The District has entered into a written agreement with George K. Baum & Company for limited

clerical and ministerial assistance to help the District meet certain of its continuing disclosure filing

obligations. Those limited clerical and ministerial services include reminders of filing dates and, upon

request by the District, assistance with the process of posting information with the MSRB.

RATING

Moody’s Investors Services, Inc. has assigned its municipal bond rating of “Baa2” (stable outlook)

to the Bonds. In addition, Moody’s Investors Services, Inc. has assigned an “Aa2” (negative outlook)

enhanced rating to the Bonds based on the New Mexico School District Enhancement Program. The ratings

reflect only the view of Moody’s Investors Services, Inc., and an explanation of the significance of such

ratings may be obtained only from Moody’s Investors Services, Inc., 99 Church Street, New York, New

York 10003. There is no assurance that such ratings will continue for any given period of time or that it

will not be revised downward or withdrawn entirely by Moody’s Investors Services, Inc. if, in its judgment,

circumstances warrant. Any such downward revision or withdrawal of the ratings may have an adverse

effect on the market price of the Bonds.

NEW MEXICO SCHOOL DISTRICT ENHANCEMENT PROGRAM

The New Mexico Legislature amended NMSA 1978, Section 22-18-13 in the first session of 2007,

which became effective on March 30, 2007, and is applicable to general obligation bonds issued after such

date. Section 22-18-13 provides that if the District’s Paying Agent notifies the Department of Finance and

Administration on the business day immediately prior to the payment date that a bond payment has not

been received, the Department of Finance and Administration shall forward the amount necessary to make

the payment due on the bonds to the Paying Agent. Such amount will be withheld by the Department of

Finance and Administration from the District’s monthly State Equalization Guarantee distribution (see

“Finances of the Educational Program – State Equalization Guarantee”). If the amount of the next

succeeding distribution is insufficient to pay the amount due, the Department of Finance and Administration

shall withhold amounts from each succeeding payment of the State Equalization Guarantee distribution,

including payments to be made in succeeding fiscal years, but no more than 12 consecutive months of

payments, until the total amount of principal and interest is withheld. Withholding of the State Equalization

Guarantee distribution may affect the District’s ability to continue to operate.

Section 22-18-13 requires filing the Bond Resolution, bond offering documents and contact

information for the Paying Agent with the Department of Finance and Administration. Failure to file such

information will not invalidate the obligation of the State Treasurer to pay the bond payment and withhold

the State Equalization distribution.

Moody’s Investors Service, Inc. has assigned an “Aa2” (negative outlook) rating to New Mexico’s

School District Enhancement Program. By request, Moody’s has assigned the “Aa2” (negative outlook)

rating to school district bonds upon verification of a requirement in the authorizing bond resolution that an

independent, third-party paying agent will be appointed and maintained. Notwithstanding this fact, the

Bonds are qualified and do receive the benefit of the New Mexico School District Enhancement Program.

TRANSCRIPT AND CLOSING DOCUMENTS

A complete transcript of proceedings and a no-litigation certificate (described above under

"Litigation") will be delivered by the District to the purchaser when the Bonds are delivered. The District

13

will at that time also provide a certificate issued by the District relating to the accuracy and completeness

of this Official Statement.

MUNICIPAL ADVISOR

George K. Baum & Company has been retained as Municipal Advisor to the District to assist in the

issuance of the Bonds. In this capacity, the Municipal Advisor has compiled certain data relating to the

Bonds that is contained in this Official Statement. The Municipal Advisor has not independently verified

any of the data contained herein or conducted a detailed investigation of the affairs of the District to

determine the accuracy or completeness of this Official Statement. Because of its limited participation, the

Municipal Advisor assumes no responsibility for the accuracy or completeness of any of the information

contained herein. The fee of the Municipal Advisor for services with respect to the Bonds is contingent

upon the issuance and sale of the Bonds.

The Municipal Advisor has provided the following sentence for inclusion in this Official Statement:

The Municipal Advisor has reviewed the information in this Official Statement in accordance with, and as

part of, its responsibilities to the District and, as applicable, to investors under the federal securities laws as

applied to the facts and circumstances of this transaction, but the Municipal Advisor does not guarantee the

accuracy or completeness of such information.

UNDERWRITING

The Bonds are being purchased by Robert W. Baird & Co., Inc. (the “Underwriter”) pursuant to a

Bond Purchase Agreement dated June __, 2017. The Underwriter has agreed, subject to certain conditions,

to purchase the Bonds from the District at a price of $_______ (representing the par amount of the Bonds

of $5,000,000*, [plus a net original issue premium] [less a net original issue discount] of $_______, less an

Underwriter’s discount of $________. The Bond Purchase Agreement provides that the Underwriter will

purchase all of the Bonds if any are purchased, the obligation to make such purchase being subject to certain

terms and conditions set forth in the Bond Purchase Agreement, including approval of certain legal matters

by counsel and certain other conditions.

The Underwriter has reviewed the information in this Official Statement pursuant to its

responsibilities to investors under federal securities laws, but the Underwriter does not guarantee the

accuracy or completeness of such information.

The prices at which the Bonds are offered to the public (and the yields resulting therefrom) may

vary from the initial public offering prices appearing on the cover page of this Official Statement. In

addition, the Underwriter may allow commissions or discounts from such initial offering prices to dealers

and others.

ADDITIONAL INFORMATION

Information concerning the Bonds, including the District's Official Statement, may be obtained

from the District's Municipal Advisor, George K. Baum & Company, 6565 Americas Parkway, Suite 860,

Albuquerque, New Mexico 87110. The Official Statement is deemed final by the District for purposes of

SEC Rule 15c2-12(b)(1) except for the omission of the following information: the offering price, interest

rate, selling compensation, aggregate principal amount, principal amount per maturity, delivery dates, any

other terms or provisions required by an issuer of such securities to be specified in a competitive bid, ratings,

other terms of the Bonds depending on such matters, and the identity of the underwriter(s).

14

The District will provide the Final Official Statement and any amendments or supplements thereto

and will undertake all other obligations as contemplated by Rule 15c12-12 of the Securities and Exchange

Commission.

OFFICIAL STATEMENT CERTIFICATION

As of the date hereof this Official Statement is true to the best of my knowledge, complete and

correct in all material respects, and does not include any untrue statement of a material fact or omit to state

a material fact necessary in order to make the statements made herein, in light of the circumstances under

which they are made, not misleading.

The preparation of this Official Statement and its distribution has been authorized by the District.

The Official Statement is hereby duly approved by the District as of the date on the cover page hereof.

SILVER CONSOLIDATED SCHOOL DISTRICT NO. 1

/s/

President, Board of Education

/s/

Secretary, Board of Education

15

BORROWING CAPACITY

2016 Final Limitation (6% x $579,238,305*) $34,754,298

Less: Outstanding Direct General Obligation School Building Bonds (1,420,000)

Less: 2017 Bonds (5,000,000)**

Unused Borrowing Capacity $28,334,298

*Source: New Mexico Public Education Department.

**Preliminary, subject to change.

(REMAINDER OF PAGE INTENTIONALLY LEFT BLANK)

16

FINANCIAL INFORMATION

Actual and Assessed Valuations

2016 Estimated Actual Valuation $1,737,714,915 (1) 2016 Final Assessed Valuation $579,238,305 (2)

Outstanding Direct Debt $1,420,000

Plus: 2017 Bonds 5,000,000*

Total Direct Debt $6,420,000

Overlapping G.O. Bonded Indebtedness

Taxing Body

2016 Final

Assessed Valuation

Bonded Debt

Percentage

Applicable

Net Amount

State of New Mexico $56,608,163,615 $326,755,000 1.02% $3,343,493

Grant County 841,061,500 2,845,000 68.87% 1,959,349

Town of Silver City 207,101,984 - 0 - 100.00% - 0 -

Total Overlapping Debt $5,302,842

Total Direct and Overlapping Debt $11,722,842

Direct and Overlapping G.O. Bond Debt Ratios

Direct Debt to Assessed Value 1.11%

Direct and Overlapping Debt to Assessed Value 2.02%

Direct Debt to Actual Valuation 0.37%

Direct and Overlapping Debt to Actual Valuation 0.67%

Per Capita Direct Debt (3) $301

Per Capita Direct and Overlapping Debt $549

Per Capita Assessed Valuation $27,139

Per Capita Actual Valuation $81,418

(1) Estimated Actual Valuation is calculated by multiplying estimated assessed value times three plus

estimated exemptions.

(2) New Mexico assessed values represent 33-1/3% (the maximum assessment ratio permitted by the New

Mexico Constitution) of the actual property value after deduction of certain exemptions. Property tax levies

are based upon the certified assessed valuation.

(3) Estimated District population is 21,343 (Source: Statistical Atlas).

*Preliminary, subject to change.

17

DEBT LIMITATIONS

Article IX, Section 11 of the New Mexico Constitution and NMSA 1978, Section 22-18-1, as

amended, limit the power of the District to incur general obligation debt extending beyond the fiscal year

(e.g., by issuing additional bonds) in three ways:

1. The District can only incur such debt for the purpose of erecting, remodeling, making additions to

and furnishing school buildings, or purchasing or improving school grounds, and purchasing

computer software and hardware for student use in public schools, providing matching funds for

capital outlay projects funded pursuant to the Public School Capital Outlay Act, or any combination

of these purposes, and to pay the cost of issuance of the bonds, and to reimburse the District for

expenditures made for the foregoing purposes, as well as to pay all legal, financial and other

necessary costs connected with the sale and issuance of the Bonds.

2. The District must submit any proposition to create such a debt to a vote of the qualified electors of

the District, and a majority of those voting must vote in favor of creating the debt.

3. The total direct general obligation indebtedness of the District may not exceed 6% of the assessed

valuation of the taxable property within the District, as shown by the last preceding general

assessment.

ANALYSIS OF ASSESSED VALUATION

Assessed Valuation of property within the District is calculated as follows: of the total estimated

actual valuation of all taxable property in the District, 33-1/3% is legally subject to ad valorem taxes. After

deduction of certain personal exemptions, the certified 2016 final assessed valuation is $579,238,305. The

actual value of personal property within the District is determined by the Grant County Assessor, and is

divided into Residential, Non-Residential and Oil, Gas and Copper categories. The actual value of

corporate property within the District is determined by the New Mexico State Property Tax Department.

The analysis of the District's Assessed Valuation for the past five years is as follows:

Tax Year Residential Non-Residential Oil, Gas & Copper Total

2016 $337,050,712 $174,234,661 $67,952,932 $579,238,305

2015 333,397,250 172,973,963 76,185,210 582,556,423

2014 331,526,666 174,130,023 77,376,444 583,033,133

2013 322,005,607 177,119,853 74,000,400 573,125,860

2012 312,203,906 171,535,094 66,325,797 550,064,797

Source: New Mexico Public Education Department.

Reassessment

New Mexico has a state-wide property reassessment program. The program's objective is to keep

property values close to their market values so that there will be a high correlation between the value of a

property and its share of the tax burden. The first reassessment under this present program was in 1986,

and such reassessments continue to occur biannually in the even numbered years.

18

Comparison of Assessed Value

Tax Year Grant County District Assessed Value

2016 $841,061,500 $579,238,305 2015 822,204,992 582,556,423 2014 791,414,221 583,033,133 2013 748,601,307 573,125,860 2012 702,741,153 550,064,797

Source: New Mexico Public Education Department and New Mexico Department of Finance and Administration.

Assessed Valuation of the Largest Centrally Assessed Taxpayers in the District

Taxpayer

2016

Assessed Valuation

Union Pacific $15,226,113

PNM Electric 5,792,922

El Paso Natural Gas 4,714,837

NM Gas Company 2,957,773

SFFP 2,688,435

Western Telephone 1,842,199

QWEST 1,325,255

Level 3 Communication 1,324,049

WNM Communication Corp. 1,007,874

Lordsburg Minerals 1,060,256

Source: New Mexico Department of Taxation and Revenue.

TAX RATES

Yield Control

NMSA 1978, Section 7-37-7.1 limits the allowable increase in property taxes from the preceding

year. Specifically, no rate shall be set or assessment imposed which will produce current tax revenues in

excess of the prior year's tax revenues, plus a percent that is determined by a growth control factor. The

growth control factor is the sum of (1) the growth in the assessed valuation due to net new additions to the

property tax rolls, expressed as a percent of the prior year's assessed ("G"), and (2) the percentage change, not

in excess of 5%, in the annual business indicator index between the prior calendar year and the year next

preceding the prior calendar year ("I"). The resulting yield control equation is:

Current tax revenues = prior tax revenues X (G + I)

Where:

G is never less than 100%, and

I is never less than 0% nor more than 5%.

The annual business indicator index is defined as the "annual implicit price deflator index for state

and local government purchases of goods and services, as published in the United States Department of

Commerce monthly publication entitled 'Summary of Current Business' or any successor publication for the

calendar year." The yield control formula applies to both residential and non-residential property, but the

calculations for each property class are made separately. In addition, the yield control formula applies to any

19

authorized operating levy but not to any debt service levy. To the extent that the reassessment program, as

discussed under "Reassessment" above, increased property values, the yield control formula operated to limit

the growth in tax revenues resulting solely from reassessment, while not directly limiting the increase in tax

revenues due to net new additions to the property tax rolls.

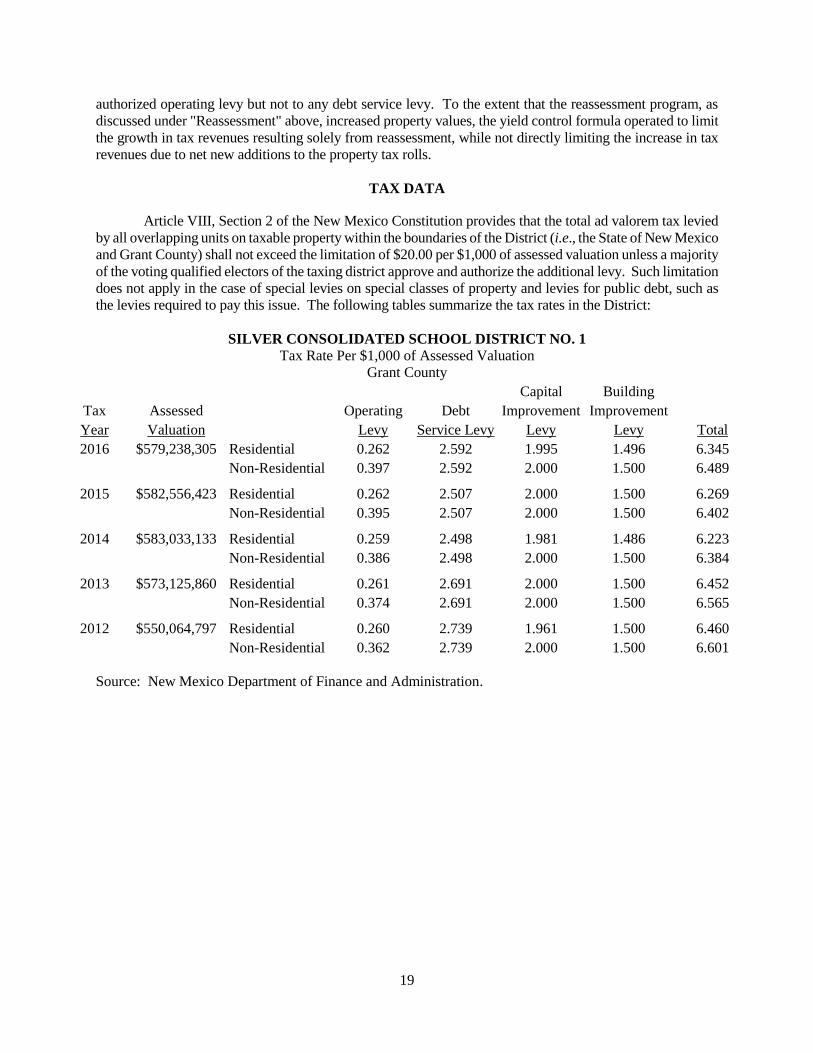

TAX DATA

Article VIII, Section 2 of the New Mexico Constitution provides that the total ad valorem tax levied

by all overlapping units on taxable property within the boundaries of the District (i.e., the State of New Mexico

and Grant County) shall not exceed the limitation of $20.00 per $1,000 of assessed valuation unless a majority

of the voting qualified electors of the taxing district approve and authorize the additional levy. Such limitation

does not apply in the case of special levies on special classes of property and levies for public debt, such as

the levies required to pay this issue. The following tables summarize the tax rates in the District:

SILVER CONSOLIDATED SCHOOL DISTRICT NO. 1 Tax Rate Per $1,000 of Assessed Valuation

Grant County

Capital Building Tax Assessed Operating Debt Improvement Improvement Year Valuation Levy Service Levy Levy Levy Total

2016 $579,238,305 Residential 0.262 2.592 1.995 1.496 6.345

Non-Residential 0.397 2.592 2.000 1.500 6.489

2015 $582,556,423 Residential 0.262 2.507 2.000 1.500 6.269

Non-Residential 0.395 2.507 2.000 1.500 6.402

2014 $583,033,133 Residential 0.259 2.498 1.981 1.486 6.223

Non-Residential 0.386 2.498 2.000 1.500 6.384

2013 $573,125,860 Residential 0.261 2.691 2.000 1.500 6.452

Non-Residential 0.374 2.691 2.000 1.500 6.565

2012 $550,064,797 Residential 0.260 2.739 1.961 1.500 6.460

Non-Residential 0.362 2.739 2.000 1.500 6.601

Source: New Mexico Department of Finance and Administration.

20

SILVER CONSOLIDATED SCHOOL DISTRICT TAX RATES - TOTAL

District Tax Rates – Total

2012 2013 2014 2015 2016

R* NR** R* NR** R* NR** R* NR** R* NR**

State of New Mexico 1.360 1.360 1.360 1.360 1.360 1.360 1.360 1.360 1.360 1.360

Grant County 7.794 13.360 7.504 13.044 7.414 13.019 7.472 12.988 7.452 12.988

Town of Silver City 1.398 2.553 2.728 3.887 2.647 2.924 2.675 3.063 2.661 3.104

Silver Schools 6.460 6.601 6.452 6.565 6.223 6.384 6.269 6.402 6.345 6.489

Historical Summary of Tax Rates for Bonds

2012 2013 2014 2015 2016

R* NR** R* NR** R* NR** R* NR** R* NR**

State of New Mexico 1.360 1.360 1.360 1.360 1.360 1.360 1.360 1.360 1.360 1.360

Grant County 1.510 1.510 1.194 1.194 1.169 1.169 1.138 1.138 1.138 1.138

Town of Silver City 0.328 0.328 0.662 0.662 0.000 0.000 0.000 0.000 0.000 0.000

Silver Schools 2.739 2.739 2.691 2.691 2.498 2.498 2.507 2.507 2.592 2.592

*Residential

**Non-Residential

Source: State of New Mexico Department of Finance and Administration.

Method of Tax Collection

Current taxes for all units of government are collected by the Grant County Treasurer and distributed

monthly to the various political subdivisions to which they are due.

Property taxes are payable to the Grant County Treasurer in two equal annual installments. The first

annual installment is due on November 10 and becomes delinquent on December 10. The second annual

installment is due on April 10 and becomes delinquent on May 10. Pursuant to NMSA 1978, Section 7-38-

46, property taxes are delinquent 30 days after the date on which they are due.

Interest On Delinquent Taxes

Pursuant to NMSA 1978, Section 7-38-49, if property taxes are not paid for any reason within thirty

(30) days after the date they are due, interest on the unpaid taxes shall accrue from the thirtieth day after

they are due until the date they are paid. Interest accrues at the rate of one percent (1%) per month or any

fraction of a month.

Delinquent Taxes Penalty

Pursuant to NMSA 1978, Section 7-38-50, if property taxes become delinquent, a penalty of one

percent (1%) of the delinquent tax for each month or any portion of a month they remain unpaid shall be

imposed, but the total penalty shall not exceed five percent (5%) of the delinquent taxes. The minimum

penalty imposed is $5.00. A county can suspend application of the minimum penalty requirement for any

tax year.

21

If property taxes become delinquent because of an intent to defraud by the property owner, fifty

percent (50%) of the property taxes due or fifty dollars ($50.00), whichever is greater, shall be added as a

penalty.

Remedies Available for Non-Payment of Taxes

Pursuant to NMSA 1978, Section 7-38-47, property taxes are the personal obligation of the person