Embed Size (px)

Citation preview

2012

Glen B. Alleman Niwot Ridge, LLC Copyright © 2012 All Rights Reserved + 1 303 241 9633

[NOTIONAL CAM INTERVIEW QUESTIONS] A collection of CAM interview questions and typical answers based on ANSI-‐748-‐C Earned Value Management processes

Notional Control Account Manager Interview Questions

Niwot Ridge, LLC, Copyright © 2012, All Rights Reserved P a g e | 2

This document provides “notional” questions and answers for Control Account Managers (CAM) during CAM interviews, IBR interviews and DCMA validation and surveillance interviews. The sections are common to all DCMA style programs. The body of this document has sub elements:

«TOP L EVE L S ECT ION»

§ Background information in support of the question and its answer – this is the basis of the activities needed for the CAM interview process. It contains an overview of the guidance, references to the guidance materials, and any external compliance requirements.

! Questions that will be asked during the interview – this is a guide to the types of questions that will be asked by the interviewer or auditor.

" Answers to those questions – these are the sample answers to the questions. In all cases these answers must address the question directly. No further explanation should be provided.

These need to be tailored to the specific needs of the program and the firm’s environment. The Earned Value Management System – System Description is the place to start for this tailoring. As well there should be a set of Program Directive guidance and support work instructions that support the implementation of the System Description and other program execution processes. Since this document is generic in purpose there are some terms that are also generic.

PPM – Program Performance Management – guidance describing the processes used to management programmatic performance. EVMS-‐SD – Earned Value Management System – System Description – guidance for applying Earned Value Management to the program and the source of guidance for the DCMA audits.

Topics in the notional interview guide include:

1. Training – what training materials, course, and guidance should the CAM have had prior to assuming the role of a CAM?

2. Organization – how is the program organized? How does the CAM interact with the program members? Who is the CAM accountable to for the deliverables and reporting?

3. Work Authorization – how is work authorized? How does the CAM know what work he or she is accountable for?

4. Planning – how is the Performance Measurement Baseline represented? How does the CAM know what portions of the PMB he or she is accountable for?

5. Earned Value – how are the Earned Value metrics taken? 6. Change Control – how are changes to the PMB managed? 7. Analysis – what analytical metrics are used to manage the program? 8. Risk – how are programmatic and technical risk managed? 9. Estimate at Completion – what processes are used to produce a credible EAC? 10. Subcontractor Management – how are subcontracts managed by the CAM? 11. Material Management – how is material managed by the CAM?

Notional Control Account Manager Interview Questions

Niwot Ridge, LLC, Copyright © 2012, All Rights Reserved P a g e | 3

Evidence Needed by the CAM Interview support Statement of Work (SOW) for the

accountable Control Accounts and Work Packages

§ Highlight your applicable area of the SOW

Contract Work Breakdown Structure (CWBS) with WBS Dictionary and Exit Criteria for each Work Package and

deliverable

§ WBS dictionary § Highlight your applicable area of the WBS tree § Technical Performance Measures for critical deliverables § Exit criteria for Work Package § Quantifiable Backup Data (QBD) for measures of percent complete

Organization (OBS) § Level II organization charts § CAM organizational charts

Responsibility Assignment Matrix (RAM) § Bring the RAM to the interview § Identify your items in the RAM

Schedules (DID 81861 compliant IMS)

§ Integrated Master Plan (IMP) § Integrated Master Schedule (IMS) § IMS Work Package Level Data § Predecessor and Successor report § Status of Late Starts and Late Finishes § Supplemental or Detailed Schedules

Budget and Work Authorization Documents (WAD)

§ Initial signed WAD § Control Account WADs and any changes from the BCR

Control Account Plans (CAP) / Task and Work Plans

§ Copy of the discrete MS Project reports § Cost system budget distribution by Control Account Report

Requesting Work Authorization Documents

§ Requesting WADs approved and signed § IMS Change Request & Change worksheets

Estimate Change Request (ECR)

§ ECRs § Bottoms up ground rules for changes § Basis of Estimate (BOE) and ETC justification § Staffing charts

Performance Measurement processes § Earned Value data for Work PCKAGES § “redlined” CAPs showing all changes

Actual Cost Physical Percent Complete with QBD

§ Weekly actual reports § Cost system resource code index § Control account instructions

Analysis and Reporting § Variance threshold requirement contained in the Program Directive

§ Variance At Completion (VAC)

Risk Management

§ Outline all technical, schedule, cost, resource, and management process risks.

§ Risk register showing handling processes in the IMS § Risk register showing Management Reserve allocation § Be prepared to provide risk mitigation plans

Notional Control Account Manager Interview Questions

Niwot Ridge, LLC, Copyright © 2012, All Rights Reserved P a g e | 4

«H I S TORY OF TH I S DOCUMENT»

CAM interviews are part of every Earned Value Management System verification and part of every weekly program performance management process. These “notional” questions have been captured over several decades of work within earned value based project and programs, going back to the C/SCSC days before ANSI-‐748A/B/C. The content grows every program I work.

Over time DCMA, Department of Defense, and the Defense Acquisition University have developed guidelines for CAM interviews and Validation and Surveillance processes. These have been incorporated into this guide.

As well hands on Validation and Surveillance experience has shown that the core questions asked and the critical success factors for any program are incorporated in the CAM’s ability to answer – with credible evidence – these questions.

Notional Control Account Manager Interview Questions

Niwot Ridge, LLC, Copyright © 2012, All Rights Reserved P a g e | 5

«THE ABR IDGED VERS ION OF THE CAM INTERV I EW»

General – what is the primary role of the CAM on a weekly project rhythm ! Do you have multiple Control Accounts, or just one? What are they? ! What is the approximate dollar value of your Control Account? ! What is the nature of work in your Control Account? ! How long have you been a Control Account Manager? ! Do you like being a CAM? If not, do you accept the responsibility and function? ! Have you read the EVM System Description? ! Have you read the accompanying Work Instructions? ! Have you read the Program Management Plan (PMP)? ! Demonstrate the contents of your CAM Notebook. ! Have you taken the CAM training provided? Or have you completed an equivalent course? ! What training do you think you need to be effective as a CAM? ! What areas of training

Organizing Your Control Account – does the CAM know who is working on what in the CA? ! Show me your OBS. ! Does your Functional organization align with your OBS? If not, how is it traced to the OBS? ! Who assigns named resources to your Control Account? Can you get whomever you need, or

must you request resources?

Authorizing your Work – does the CAM know what should be worked on and the outcome? ! Who directs, approves, and assigns you to work on a control account? ! Do you have a signed CAP/PWAA? Does the PWAA indicate WBS, title/description of the work,

BAC (in hours or dollars), with Start-‐End dates? ! What paragraphs in your SOW describe your work? Is your work specific or implied? ! What CDRLs apply to your work? ! What DIDs apply to your work? ! How do you authorize work? Demonstrate your CNA artifact and discuss the process. ! How are charge numbers opened and closed? ! Do your planning packages have charge numbers? ! Are actuals collected and charge numbers established at the WP level? Lower? ! Is an approved BCR authorization your to proceed or do you need a revised CAA?

Organizing the Work – does the CAM know what “done” looks like for this CA ! Where is your WBS? Is work decomposed into logical Work Packages from the WBS structure? ! Show me your WBS dictionary? Are all the informational elements present? Does it accurately

reflect the SOW and IMP (or deliverables plan)? ! What is the deliverable for the work done in your Control Account? ! Demonstrate your program level RAM. ! Has the RAM been dollarized? Does each Control Account have an established value?

Notional Control Account Manager Interview Questions

Niwot Ridge, LLC, Copyright © 2012, All Rights Reserved P a g e | 6

! Demonstrate your detailed RAM? ! Demonstrate your Basis of Estimate summary? ! What is your estimating process/tool? ! Demonstrate your CAP?

Schedule – can the CAM brief the order of work needed to get to “Done?” ! Do you have milestone schedule? ! Do you have direct access to the IMS? If not, do you receive a schedule extract? ! Does the deliverables milestone schedule correspond to the IMS? ! Identify your Control Accounts in the IMS. ! What is the frequency of schedule updates? ! What is the process for making a schedule change? Who approves the change and how is it

implemented in the schedule? ! Identify your Work Packages and Planning Packages. Is there visibility of work below the Work

Package level? ! Which milestones relate to your effort? Identify these in your schedules. ! Are your schedules resource loaded? In dollars or hours? At what level? ! Are your forecasts resource loaded? ! If used, explain Rolling Wave planning process, planning packages, and summary level planning

packages. ! Does BCWS on the CAP correspond to BCWS on the IMS and PMB databases?

Assessing Performance ! Explain and justify the earned value types you use (i.e., 0/100, 50/50, m/s, % complete, LOE). ! What are the technical criteria that support your assessment of performance attained? ! What are your schedule baseline start and finish dates? ! What is the duration of Work Packages? ! Demonstrate how and when status is reported? Trace to month-‐end BCWP

Budget ! What resources are assigned to do the work? ! Do you have named resources or generic resources? ! How is the rate determined for resources? ! Do you have visibility of resource rates? Or do you deal with hours only? ! How are resources assigned to the tasks in your schedule? Do you select resources from a

lookup table? ! Are you responsible for indirect costs? ! Do you have Material, Travel, Sub contractors, Taxes, or ODCs? ! Where are Material, Travel, Sub contractors, Taxes, or ODCs in your schedule? ! Does the BAC in your CAP correspond to your schedule? ! Does the BCWS in your CAP correspond to your schedule? ! Does the resource allocation in your CAP correspond to your schedule?

Notional Control Account Manager Interview Questions

Niwot Ridge, LLC, Copyright © 2012, All Rights Reserved P a g e | 7

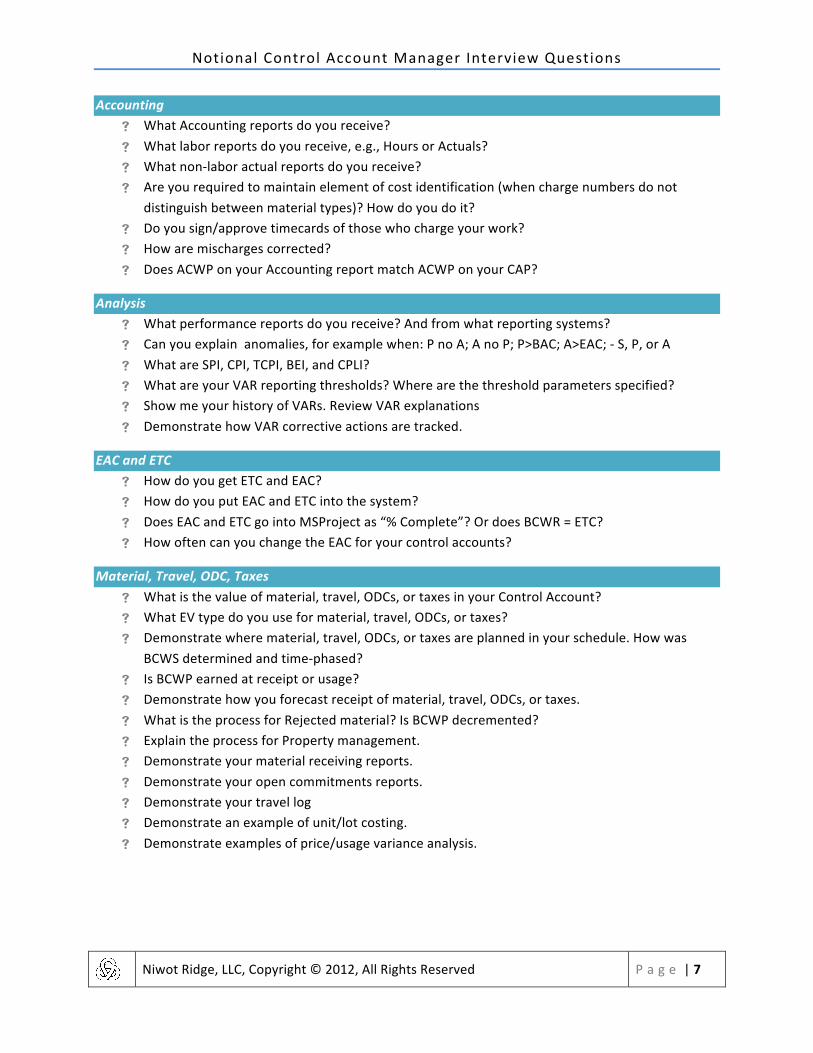

Accounting ! What Accounting reports do you receive? ! What labor reports do you receive, e.g., Hours or Actuals? ! What non-‐labor actual reports do you receive? ! Are you required to maintain element of cost identification (when charge numbers do not

distinguish between material types)? How do you do it? ! Do you sign/approve timecards of those who charge your work? ! How are mischarges corrected? ! Does ACWP on your Accounting report match ACWP on your CAP?

Analysis ! What performance reports do you receive? And from what reporting systems? ! Can you explain anomalies, for example when: P no A; A no P; P>BAC; A>EAC; -‐ S, P, or A ! What are SPI, CPI, TCPI, BEI, and CPLI? ! What are your VAR reporting thresholds? Where are the threshold parameters specified? ! Show me your history of VARs. Review VAR explanations ! Demonstrate how VAR corrective actions are tracked.

EAC and ETC ! How do you get ETC and EAC? ! How do you put EAC and ETC into the system? ! Does EAC and ETC go into MSProject as “% Complete”? Or does BCWR = ETC? ! How often can you change the EAC for your control accounts?

Material, Travel, ODC, Taxes ! What is the value of material, travel, ODCs, or taxes in your Control Account? ! What EV type do you use for material, travel, ODCs, or taxes? ! Demonstrate where material, travel, ODCs, or taxes are planned in your schedule. How was

BCWS determined and time-‐phased? ! Is BCWP earned at receipt or usage? ! Demonstrate how you forecast receipt of material, travel, ODCs, or taxes. ! What is the process for Rejected material? Is BCWP decremented? ! Explain the process for Property management. ! Demonstrate your material receiving reports. ! Demonstrate your open commitments reports. ! Demonstrate your travel log ! Demonstrate an example of unit/lot costing. ! Demonstrate examples of price/usage variance analysis.

Notional Control Account Manager Interview Questions

Niwot Ridge, LLC, Copyright © 2012, All Rights Reserved P a g e | 8

Subcontracts ! Do you manage any subcontractors? ! Demonstrate your major subcontracts in the WBS dictionary. ! What is the nature of the sub-‐contracted effort? Labor hours or a clearly defined deliverable? ! What type of contract drives the sub-‐contracted effort? T&M, Firm Fixed Price? ! Explain flow down requirements for subcontractor EVMS. Full EVMS with certification; EVMS

compliance only; no EVMS? ! Trace subcontract effort in the IMS. ! What is the basis for assessing subcontractor performance? ! What is the basis for assessing ETC of sub-‐contracted effort? ! Where is the subcontract effort indicated in the CAP? ! Explain process for accrual of an estimated ACWP for sub-‐contracted work. ! Have you visited your subcontractor? Show me results of your reviews. ! What formal performance reporting requirements do you receive from subs? ! Is the sub-‐contracted effort formally observed and evaluated?

Change Control ! How often do you change your baseline? ! How do changes get submitted and approved? Explain the BCR process. ! Have you had a change? Explain. Demonstrate your BCR. Demonstrate before and after in your

IMS and on your CAP. ! Where are the documents that support your baseline changes? ! Are your BCRs (Budget Change Request) signed? ! Under what circumstances can you request Management Reserve? ! How is your management reserve calculated? ! Do you have Contingency Reserve (i.e., slack or float)?

Risk ! What tool do you use to identify risk? ! What tool do you use to track and report risk? ! What tool do you use to quantify risk assessment? ! System Description requires Risk added to EAC when probability reaches 80%. How do CAMs

determine 80% probability? ! How are Risks recorded and indicated on Risk Registry? ! How do you nominate Risks to be put on Risk Registry? ! How do you escalate Risks? ! How do you close out Risks? ! Demonstrate your Risks? ! What are your risk areas? Cost? Schedule? Technical?

Notional Control Account Manager Interview Questions

Niwot Ridge, LLC, Copyright © 2012, All Rights Reserved P a g e | 9

Accrual of Estimated Actuals ! What do you accrue on a regular basis? ! Who does the accrual of estimated actuals? ! Where is the record/artifact of accruals? ! Where is the CAM documentation kept that validates accrual? ! Who does the monthly reversal process? ! How is the reversal process performed? ! What documentation do you retain to justify the accrual of estimated actual?

Notional Control Account Manager Interview Questions

Niwot Ridge, LLC, Copyright © 2012, All Rights Reserved P a g e | 10

«TRA IN ING»

§ Training processes are the core of CAM success. This training must include the mechanics of the EVMS as well as the governance process applied to Control Accounts

! When did you last receive PP&C or CAM training?

" Our formal EVM System Description is the starting point for our training. The CAM notebook training covers the use of all materials we need to do our job as a CAM, guided by the EVM System Description.

«ORGAN I ZAT ION»

§ Define the authorized work elements for the program. A work breakdown structure (WBS), tailored for effective internal management control, and is commonly used in this process.

§ Identify the program organizational structure including the major subcontractors responsible for accomplishing the authorized work, and define the organizational elements in which work will be planned and controlled.

§ Provide for the integration of the company’s planning, scheduling, budgeting, work authorization and cost accumulation processes with each other, and as appropriate, the program work breakdown structure and the program organizational structure.

§ Identify the company organization or function responsible for controlling overhead (indirect costs).

§ Provide for integration of the program work breakdown structure and the program organizational structure in a manner that permits cost and schedule performance measurement by elements of either or both structures as needed.

! Show your organizational chart and describe your responsibilities

" Be prepared to show application organizational charts with traceability from the highest level program organization to the lowest level where resources support your work scope.

" Highlight this traceability from the highest to the lowest level. Be prepared to discuss your roles and responsibilities as reference on your applicable organizational chart.

! Where is your scope of work defined?

§ This information is defined in the Statement of Work (SOW) and WBS Dictionary. § The WBS Dictionary is correlated with each WBS element to the SOW tasks. § The WBS Dictionary describes the effort, and the Control Accounts through with the effort will

be accomplished.

" Be prepared to show the SOW and WBS dictionary. " Explain their use as they apply to your Control Accounts. " Highlight your applicable SOW and WBS dictionary paragraphs.

Notional Control Account Manager Interview Questions

Niwot Ridge, LLC, Copyright © 2012, All Rights Reserved P a g e | 11

" Show the IMP matrix and explain its logic.

! Do you own or support any of the Events, Accomplishments, or Criteria in the IMP?

§ Systems Engineering is responsible for the development of the Integrated Master Plan (IMP) Matrix. The IMP Matrix is an event driven plan of Program Events (PE), Significant Accomplishments (SA), Accomplishment Criteria (AC), and Process Definition (process narratives) which encompass the scope of your program activities. The IMP defines WHAT and HOW – but not WHEN (scheduled dates).

" Be prepared to show the IMP Matrix, explain that the IMP Matrix contains Program Events (PE), Significant Accomplishments (SA), and Accomplishment Criteria (AC).

" Be prepared to show and explain those PE’s, SA’s and the AC as they pertain to your Work Package, its scope, the Control Accounts and how they relate and trace to the Integrated Master Schedule (IMS). High light your applicable IMP PE’s, SA’s and the AC in the IMP Matrix.

! What WBS elements are you responsible for?

§ The WBS tree reflects the WBS elements for which you are responsible.

" Be prepared to show the applicable WBS elements with traceability from the lowest level to the highest level of the WBS Tree.

" Highlight traceability from the lowest to the highest level.

! Show your responsibility Assignment Matrix (RAM)

§ The Responsibility Assignment Matrix (RAM) is the intersection of the Organization Breakdown Structure (OBS) and the Work Breakdown Structure (WBS) responsibilities.

" Be prepared to show the intersection with your Control Accounts as reflected on the RAM. " Understand all components contained in the RAM that pertain to your Control Accounts. " Highlight your applicable Control Account data.

! How many Control Accounts do you have and what are their total budgets?

" Identify the Control Accounts on the RAM for data traces " Identify your Control Accounts on the RAM and be prepared to show the Budget At Completion

(BAC) for each Control Account (burdened and direct dollars). " Show how the BAC for each Control Account is reflected on the current month Control Account

Organizational Performance Report (CA OPR).

Notional Control Account Manager Interview Questions

Niwot Ridge, LLC, Copyright © 2012, All Rights Reserved P a g e | 12

«WORK AUTHOR I ZAT ION»

§ Maintaining the proper sequence of work package execution is critical to the generation of credible Earned Value Management data. Work preformed out of sequence either has not budget assigned for that period of performance or has budget assigned but no work be performed or some combination.

§ In both cases the Earned Value number cannot represent the proper progress of the project.

! What authorizes you to begin your work? Are the appropriate signatures present?

§ Operation Directives (Program Directives or other firm dependence names) provide the Program with the Authorization to Proceed (ATP).

" Be prepared to show this OD (PD) as well as any other OD’s (PD’s) that authorize contract changes which impact your Control Accounts. Identify appropriate approval signatures.

" The work authorization process triggers the planning, scheduling, budgeting, and performance of work form the total program level through the responsible organizational structure to the Control Account level.

" The Work Authorization process begins with an OD (PD) issues by the Contracts Organization. The OD (PD) authorizes the program to issues a Work Authorization Document (WAD) that defines all authorized work elements on the program.

" Once the OD (PD) has been issued, authorizing work to commence on a contract or contract change, all program work subsequently must be authorized or directed by a WAD.

! Identify the key elements on the Work Authorization Document (WAD)

" The WAD contains the following key elements " Scope of the work to be performed in terms of activities and deliverables " Schedule of the work packages that performance the work " Budget for each Work Package " Period of Performance for the collective Work Packages " Approval processes for this work and the release of the funding

! Show how you can trace the key work elements on the latest approved WAD?

" The following key elements of the latest approved WAD are: " Scope to SOW/WBS Dictionary or equivalent " Budget on WAD to the Cost Control System – the Budget Distribution Reports " Validate that the WAD is consistent with the period performance on the Integrated Master

Schedule (IMS), baseline date and revision number " Provider a description of each of these documents and the processes used to create and

management them

Notional Control Account Manager Interview Questions

Niwot Ridge, LLC, Copyright © 2012, All Rights Reserved P a g e | 13

! Does the Control Account period of performance on the WAD match the start and end dates for the time phased resources in your Control Account Plan?

" Be prepared to trace the period of performance for each Control Account budget referenced on the current approved WAD to the applicable IMS time–phases Control Account / task period of performance. Ensure all dates can be reconciled.

! Do the Control Account periods of performance match the schedule time spans in the IMS?

" Be prepared to trace the period of performance for each Control Account budget referenced on the most current approved WAD to the applicable IMS time–phased Control Account / task period of performance. Ensure all dates reconcile.

" Be prepared to justify the budget and the Earned Value methods selected.

«P LANN ING»

§ Schedule the authorized work in a manner, which describes the sequence of work and identifies significant task interdependencies required to meet the requirements of the program.

§ Identify physical products, milestones, technical performance goals, or other indicators that will be used to measure progress.

§ Establish and maintain a time-‐phased budget baseline, at the Control Account level, against which program performance can be measured. Budget for far-‐term efforts may be held in higher level accounts until an appropriate time for allocation at the Control Account level. Initial budgets established for performance measurement will be based on either internal management goals or the external customer negotiated target cost including estimates for authorized but undefinitized work. On government contracts, if an over target baseline is used for performance measurement reporting purposes; prior notification must be provided to the customer.

§ Establish budgets for authorized work with identification of significant cost elements (labor, material, etc.) as needed for internal management and for control of subcontractors.

§ To the extent it is practical to identify the authorized work in discrete work packages, establish budgets for this work in terms of dollars, hours, or other measurable units. Where the entire Control Account is not subdivided into work packages, identify the far term effort in larger planning packages for budget and scheduling purposes.

§ Provide that the sum of all work package budgets plus planning package budgets within a Control Account equals the Control Account budget.

§ Identify and control level of effort activity by time-‐phased budgets established for this purpose. Only that effort which is unmeasurable or for which measurement is impractical may be classified as Level of Effort.

§ Establish overhead budgets for each significant organizational component of the company for expenses that will become indirect costs. Reflect in the program budgets, at the appropriate

Notional Control Account Manager Interview Questions

Niwot Ridge, LLC, Copyright © 2012, All Rights Reserved P a g e | 14

level, the amounts in overhead pools that are planned to be allocated to the program as indirect costs.

§ Identify management reserves and undistributed budget. § Assure that the program target cost goal is reconciled with the sum of all internal program

budgets and management reserves.

! What key supporting documentation do you use to establish and plan your tasks?

" Budgets are based on negotiated proposal values less Management Reserve (MR). the CAM plans and spreads the BCWS received according to how the scope of work will be accomplished as defined in the Statement of Work (SOW) and the WBS dictionary, and consistent with the Integrated Master Plan (IMP) and Integrated Master Schedule (IMS).

" The WBS Dictionary correlates WBS elements to the SOW tasks, and provides a description of the effort. Control Accounts and tasks are developed by the CAMs form the SOW and WBS. The program IMS establishes the periods of performance, work tasks, and milestones (if needed).

! How do you time phase the budget for the tasks?

" Based on the documentation provided above (SOW, WBS, IMP/IMS), you as the CAM must provide a time phased budget baseline for each Control Account Work Package and the activities within those Work packages contained in the IMS.

! Do you have any Level of Effort (LOE)

" BCWP for LOE’s is earned through the passage of time and is not based on work accomplished. BCWP always equals BCWS through the current period.

" Each CAM may have Control Accounts that are classified as totally LOE or Control Accounts that may only have some LOE effort. Be prepared to justify why you have LOE Control Account(s) or LOE tasks contained with a Control Account. Explain why they are not measureable.

! What is the recommended ratio of LOE to discrete budget in a Control Account classified as discrete?

" As stated in the Program Directive (PD), the recommended ratio of LOE to discrete budget within a Control Account is not to exceed some predefined value. This is typically 10% to 20% of the burdened dollar Budget at Completion (BAC).

! In the current rolling wave, do you have any discrete Control Accounts with more LOE than allowed?

" No. Ensure that any LOE effort within a discrete Control Account does not exceed the stated PD guidance. If discrete Control Accounts do exceed this guidance, then the LOE effort should be extracted and a new separate LOE Control Account developed.

Notional Control Account Manager Interview Questions

Niwot Ridge, LLC, Copyright © 2012, All Rights Reserved P a g e | 15

! Are all your LOE Control Accounts detail planned through completion?

" Yes. All LOE effort has been planned through completion " When the current program has multiple rolling wave periods – Discrete work scope must be

planned through the current rolling wave period. Future rolling wave periods must be contained in discrete planning packages.

" These must be “detail planned” at least 30 days prior to the start of the next rolling wave period of performance.

! Do you have the current approved version of the Integrated Master Schedule and know how your work packages and planning packages support the major program events and milestones?

" Be prepared to trace the period of performance for each Control Account work package and its work activities references in the Control Account Plan (CAP) to the applicable Program Events referenced in the program Integrate Master Schedule or master Milestones contained in the Program IMS.

" Ensure all dates reconcile. " Be able to justify the budget and Earned Value methods selected for each Work Package and

Planning Package.

! Is the task / milestone exit criteria clearly defined? Either separately documented or embedded in the task description.

" A Task Entry and Exit (TEC) must be established for each discrete work package. If the task descriptions in the IMS are at such a detailed level that clearly defines the exit criteria closure, then no additional exit criteria documentation is required.

" Be prepared to show and explain the TECs referenced on the IMS that support your Control Account tasks. Also be prepared to show the entrance and exit criteria for each discrete Control Account work package. Explain how they were derived.

! For the current planning period, what is your total LOE versus Discrete in dollars and hours?

" Be prepared to identify the Budget At Completion (BAC) in burdened dollars and hours for all current LOE effort contained in your Control Accounts. Divide the dollar amount by the total of all current open Control Accounts Budget At Completion. This will provide the LOE versus Discrete percent ratio.

! Trace a task(s) from your IMS to your Control Account Plan (CAP) for both total and time phase resources

" Be prepared to trace the period of performance for each Control Account budget referenced on the current approved WAD to the applicable IMS time phased Control Account or task period of performance. Ensure all dates and resources allocated reconcile with the current rolling wave period.

Notional Control Account Manager Interview Questions

Niwot Ridge, LLC, Copyright © 2012, All Rights Reserved P a g e | 16

! Show an example that you have predecessors and successors identified within your organization or Integrated Product Team (IPT) and between other organizations or IPTs.

" A series or network of activities which are required to accomplish a task are linked together with logical predecessors and successor relationships must provide for the identification of the critical path(s). Each discrete activity has an output predecessor which is linked to an input or successor activity. This defining activity relationship enables the process to assess progress within the network. Be prepared to show an example of how your predecessor/successor activities are indentified with your organization or Integrated Product Team (IPT) are dependent or linked between other organizations or IPTs predecessors and successor activities. Program Planning and Controls can provide predecessor and successor reports to help clarify your response.

! If you are responsible for any major subcontracts or intercompany work transfers, where is it reflected in your IMS?

" Be prepared to show the major subcontracting and inter-‐company work transfer authorization (IWTA) effort reflected in the IMS and how your tasks support the major events and milestones.

! If you are responsible for any high value material, where is it reflected in your IMS?

" Be prepared to show any high value material effort reflected on the IMS. Explain how your tasks support the major events and milestones.

! Are any of your tasks on the program or IPT critical path?

" If yes, be prepared to show which tasks are contained on the critical path. " The critical path is defined as the longest computed path through a program schedule network.

The critical path represents scheduled activities with the highest risk and the least margin for error.

! Do you have any special requirements because you are on the critical path?

" Yes. Any schedule activities that are contained on the critical path will have increased management visibility and must be statused weekly for impacts to the program.

! What are the most critical areas of your work effort?

" Identify areas in your work scope which you consider the most critical. Explain why.

! What is your schedule reserve?

§ Schedule reserve is generally expressed as float. Float is the amount of time an activity can slip before it affects another activity finish date. It is the difference between when the activity can happen and when the activity must happen. Positive float (reserve) should be conserved and managed. Negative float indicates activities that must be reworked to meet the event schedule. Events may be milestones or deliverables. If the total float is less than or equal to zero (0), then

Notional Control Account Manager Interview Questions

Niwot Ridge, LLC, Copyright © 2012, All Rights Reserved P a g e | 17

there may be a critical condition in the schedule. Schedule reserve is indentified on the IMS network by Control Account or task, or by the IMS schedule reserve reports.

" Be prepared to describe the schedule reserve for the Control Accounts you’re accountable for and how that schedule margin was arrived at.

" Be prepared to describe how you measure the erosion of the schedule margin as the program progresses and whether the remaining schedule margin is sufficient to protect the deliverable dates in the IMS.

! Do you have resources allocated for your float or schedule reserve?

" No. schedule reserve, or float, does not have a defined work scope. Resources may be allocated to tasks when a behind schedule condition occurs (which may cause negative schedule reserve or float). If this occurs, additional resources may be applied to the task to help mitigate schedule degradation. This situation most likely will result in a cost overrun condition and may require additional resources or estimates to be applied. This should not be view3ed as the best solution.

! Do you status your IMS detail tasks weekly?

" Yes. Control account task activities schedule in the IMS are statused weekly which includes accomplishments, forecasts (late or early) and all schedule changes and revisions.

! Do you track late starts and late finishes?

" Be prepared to show the status of late starts and late finishes which occurred during last week. This data can be obtained from the metric produced by the Program Planning and Controls staff.

! Validate that the month-‐end schedule progress for a Control Account taken in the IMS is consistent with the cost system.

" Be prepared to reconcile the current month Earned Value (BCWP) values contained in the monthly Organizational Performance Report (OPR) with the Control Account and task Earned Value (BCWP) contained the IMS.

! Do you have approved, documented, discrete criteria for all percent complete work packages and or tasks that exceed 45 workdays in length?

§ Percent Complete Earned Value method is based on objective (not subjective) criteria and is used for tasks where the measured accomplishment is for equal value products or services. Each lower level task should be less than two months in duration and must have a start and completion along with associated time phased resource plan.

" Be prepared to show the approved documents and the discrete criteria for all percent complete work. The percent complete evidence can be in the form of actual deliverables or in a document showing how you would calculate this percent complete.

Notional Control Account Manager Interview Questions

Niwot Ridge, LLC, Copyright © 2012, All Rights Reserved P a g e | 18

" Remember, CAM opinion is no acceptable as a measure of percent complete – only tangible evidence can be used.

! Do you have supplemental schedules? Do they support the IMS?

§ In some cases CAMs may feel the need to maintain lower level detailed schedules that support Control Accounts and tasks. These lower level schedules are not contained in the IMS, but are supportive in monitoring Control Accounts and tasks scheduled performance.

" If this is the case, be prepared to show how this lower level of detail is traceable to the IMS and the PMB.

«EARNED VA LUE»

§ Record direct costs in a manner consistent with the budgets in a formal system controlled by the general books of account.

§ When a work breakdown structure is used, summarize direct costs from Control Accounts into the work breakdown structure without allocation of a single Control Account to two or more work breakdown structure elements.

§ Summarize direct costs from the Control Accounts into the contractor’s organizational elements without allocation of a single Control Account to two or more organizational elements.

§ Record all indirect costs that will be allocated to the contract. § Identify unit costs, equivalent unit’s costs, or lot costs when needed. § For EVMS, the material accounting system will provide for:

• Accurate cost accumulation and assignment of costs to Control Accounts in a manner consistent with the budgets using recognized, acceptable, costing techniques.

• Cost performance measurement at the point in time most suitable for the category of material involved, but no earlier than the time of progress payments or actual receipt of material.

§ Full accountability of all material purchased for the program including the residual inventory

! What Earned Value techniques are approved for use on this program?

" The Program Directive (PD) defines the Earned Value techniques approved for use on this program.

" Be prepared to provide a copy of the Program Directive which contains the approved Earned Value techniques.

! How is Earned Value taken for your work? Task Level, Work Package Level?

" Earned Value for your Control Account tasks are determined as the task level based on the Earned Value methods selected. Earned Value also is taken consistent with how the work is planned.

Notional Control Account Manager Interview Questions

Niwot Ridge, LLC, Copyright © 2012, All Rights Reserved P a g e | 19

" Be prepared to discuss each Control Account task Earned Value technique and the method selected for determining earned Value.

! Is the Earned Value technique or method chosen appropriately for the specific task or work package?

" Be prepared to provide a rational for selecting the earned value method for each task. Explain why the earned value methods selected are appropriate.

! Do you have any apportioned effort?

" An apportioned earned value method is used for efforts like quality assurance which can be identified and measured with the completion of an assembly, a manufacturing process, or a portion thereof.

" If you have selected an apportioned earned value method, be able to explain the BCWP of the base or parent account. Parent apportioned accounts must have the same start and completion date. Apportioned accounts must have discrete effort as a base and not LOE. BCWP for the apportioned account is expressed as the same percentage of its Budget At Completion (BAC) as the BCWP calculated for the base account or work task.

«CHANGE CONTROL»

§ Incorporate authorized changes in a timely manner, recording the effects of such changes in budgets and schedules. In the directed effort prior to negotiation of a change, base such revisions on the amount estimated and budgeted to the program organizations.

§ Reconcile current budgets to prior budgets in terms of changes to the authorized work and internal replanning in the detail needed by management for effective control.

§ Control retroactive changes to records pertaining to work performed that would change previously reported amounts for actual costs, Earned Value, or budgets. Adjustments should be made only for correction of errors, routine accounting adjustments, effects of customer or management directed changes, or to improve the baseline integrity and accuracy of performance measurement data.

§ Prevent revisions to the program budget except for authorized changes. § Document changes to the performance measurement baseline.

! What is the process you must follow to make a change to your baseline budget?

§ The process for baseline change control is described in the Earned Value Management Systems Description. It should read something like this…

" There are essentially situations that permit the Performance Measurement Baseline (PMB) to change: externally directed contract changes, formal reprogramming, and internal replanning. Each situation is defines and described in the EVMS SD.

Notional Control Account Manager Interview Questions

Niwot Ridge, LLC, Copyright © 2012, All Rights Reserved P a g e | 20

" Externally directed contract changes and formal reprogramming are the only conditions that permit a change to the Contract Budget Base (CBB) and both require permission from the customer.

" If changes to the PMB are within the constraints of the contract then internal replanning is permitted subject to the limitation of the EVMS SD.

" The internal budget replanning process should following this approach: The CAM requests a change to a Control Account(s) level budget through a Requesting WAD and reviews the request with the Program Planning and Controls lead for determination of any impact to the IMS. If it is determined that the change will impact the IMS, then the process for internal schedule replanning must be followed.

" Typically this internal replanning process follows these steps (1) Intermediate Management and the Change Control Board (CCB) approve or deny the request. Approved requests are sent to the Program Planning and Control Lead for approval (2) The PP&C Lead reviews and approves or denies the request; (3) if the requesting WAD is disputed or involves Management Reserve distribution, the Program Manager makes the final determination of approval; (4) If the changes are to occur within two accounting period beyond the current accounting period, the Program Manager or Business Deputy notifies the customer in writing of the change; (5) If the change is approved, the WAD is sent to the CAM. The CAM revises the detailed schedules and prepares an Estimate To Complete (ETC). PP&C inputs the data into the cost and schedule tools. If the CAM states in the Comments Section of the Requesting WAD that this ETC is equal to the change to the time phased BCWS (budget), then no Estimate Change Request (ECR) is required. If the ETC is different than the time phased BCWS on the Requesting WAD, then the CAM must submit an ECR.

! What is the process you must follow to make a change to your baseline schedule? Where is this documented?

" The internal schedule replanning process is usually described in the EVMS Systems Description. This usually is described as follows:

" The CAM submits a Request for IMS Change for and the accompanying IMS Change Request Worksheet to the Schedule Review Board (SRB). The SRB includes the IPT and organizational scheduler, intermediate management and the CAM. The SRB determines of the change is minor or major. Guidelines for the classification of changes is usually described in the EVMS System Description.

" If the change is determined minor, then the forms are sent to the Program Master Scheduler for review. Of the Program Master Scheduler approves the request, the approved forms are sent to the Schedule Review Board (SRB) and evaluated. Of the SRB approves the change, and then it may be implemented.

" If the change is determined major by the SRB and the Program Master Scheduler, then the forms are sent to the Change Control Board (CCB) for review. If the CCB approves the change, the change may be implemented.

Notional Control Account Manager Interview Questions

Niwot Ridge, LLC, Copyright © 2012, All Rights Reserved P a g e | 21

" If approved changes are to occur within two accounting periods beyond the current accounting period, the Program Manager or Business Deputy notifies the customer in writing of the change.

" As soon as practical WAD(s) are updated to reflect the schedule change.

! What was the last change to one of your Control Accounts?

" Be prepared to describe this change, the reason for the change " Be able to show the latest revised IMS resulting from the change and the affected Control

Accounts and any Work Packages affected by the change. " If no changes were made to the work packages, describe the process used to make a change.

! Were any changes performed in the last 60 days?

" Walk through the last change you made to a Control Account. " If no changes were made, describe the process used to make a change

! Were all appropriate documents used to process the change?

" Show the requesting WAD or IMS change request involved.

! What is the difference between the classes of change defined in your change control management system?

" Class 1 changes are usually out of scope to the contract. Class I changes are customer directed (authorized negotiated work scope or authorized unpriced work scope). All contract baseline changes must be authorized by a Program Directive (PD) or Operations Directive (OD) and directed by Work Authorization Documents (WAD)

" Class 2 changes are in scope to the contract but out of scope to the CAM or Control Account. Class 2 changes are classified to internal revisions to the baseline. They are either within the baseline scope or are changes to the baseline scope which requires a transfer from Management Reserve (MR).

! Were the changes performed in a timely manner?

" Changes to the baseline must be accomplished in a timely manner. Revisions to the budget and schedule must be completed and input to the cost and schedule tool within 60 calendar days after authorization of a change. Work authorizing documents and schedules must be amended where appropriate

! What is the acceptable use of management reserve?

" The acceptable use of Management Reserve (MR) is described in the EVMS Systems Description and a sample is stated below

" Management Reserve (MR) is a budget account established by Program Management for use in accommodating growth in the current work scope, rate changes, and other program unknowns. MR must be held for current and future needs. Because it is a control tool, actual and Earned

Notional Control Account Manager Interview Questions

Niwot Ridge, LLC, Copyright © 2012, All Rights Reserved P a g e | 22

Value are never allocated to the MR account. It must be not allocated to offset accumulated overruns or underruns. MR is not a contingency that can be eliminated from contract prices during subsequent negotiations. It must not be used to absorb the cost of out-‐of-‐scope contract changes. The customer must not view this budget reserve as a source of funding for added work scope.

" In some instances the Program Manager may elect to add work scope to what has already been authorized and budgeted and / or CAMs may wish to request MR funds. For example: there may be a change in the number of components or an insignificant amount of budget transfer accompanying a transfer in work scope. New or revised work must be judged to be within the scope of the existing contract. Technical breakthroughs or improved manufacturing processes may allow previously authorized and budgeted work to be canceled or reduced in scope. In these cases, budgets may be transferred to MR from the affected Control Accounts. WADs and schedules must be prepared or revised as necessary. Budgets must be issued through an approved WAD and charge numbers opened or closed as necessary. Consideration of potential liens or givebacks to MR must be given as well

" Changes to overhead or General and Administrative (G&A) rates can have a significant impact on budgets. Revised reporting could be significantly different from the existing rates affecting budgets. When the effect of a burden rate change is so great that the budget becomes unrealistic, MR may be used to compensate for the rate change.

! What would you do of your requests for additional resources were denied?

" If a Requesting Work Authorization Document (WAD) initiated by the CAM requesting additional resources was denied, then the CAM must (1) maintain a copy of the denied WAD to reflect additional budget was requested and disapproved; (2) initiate and submit and Estimate Change Request (ECR) from to identify the resources required for the appropriate Control Account and to revise the Estimate To Complete (ETC).

! Who initiates requests for opening and closing charge numbers?

" You do. CAMs must request new WBS charge numbers be opened for controls accounts that are scheduled to commence in the near future. WBS charge numbers are opened or closed by authorized Program Planning and Controls staff using an appropriate charge number form.

! Is it permissible to make changes to the Budgeted Cost of Work Scheduled or Actual Cost of Work Performed?

" Yes, but under limited conditions. Retroactive changes to Budgeted Cost for Work Scheduled (BCWS) may be made only to correct clerical errors or to make customer authorized changes. Routine accounting adjustments to cumulative BCWS can be accomplished only through a current month adjustment and not retroactively.

" Retroactive changes to actual cost may not be made except for correction of clerical errors or normal accounting adjustments. Adjustments must be reflected in the accounting records for the

Notional Control Account Manager Interview Questions

Niwot Ridge, LLC, Copyright © 2012, All Rights Reserved P a g e | 23

month the adjustments are made. The categories of adjustments are: (1) non labor, (2) labor current year, (3) labor prior year.

«ANALYS I S »

§ At least on a monthly basis, generate the following information at the Control Account and other levels as necessary for management control using actual cost data from, or reconcilable with, the accounting system:

♦ Comparison of the amount of planned budget and the amount of budget earned for work accomplished. This comparison provides the schedule variance.

♦ Comparison of the amount of the budget earned the actual (applied where appropriate) direct costs for the same work. This comparison provides the cost variance.

§ Identify, at least monthly, the significant differences between both planned and actual schedule performance and planned and actual cost performance, and provide the reasons for the variances in the detail needed by program management.

§ Identify budgeted and applied (or actual) indirect costs at the level and frequency needed by management for effective control, along with the reasons for any significant variances.

§ Summarize the data elements and associated variances through the program organization and/or work breakdown structure to support management needs and any customer reporting specified in the contract.

§ Implement managerial actions taken as the result of Earned Value information. § Develop revised estimates of cost at completion based on performance to date, commitment

values for material, and estimates of future conditions. Compare this information with the performance measurement baseline to identify variances at completion important to company management and any applicable customer reporting requirements including statements of funding requirements.

! Show how you monitor who charges your Control Account

" By using the Systems, Applications, Products data processing (SAP) or equivalent weekly actual cost reports. These reports are generated and distributed weekly by Cost Management and Program Controls. Each CAM must review the SAP actual cost reports on a weekly basis and assess proper charging practices. If resources aren’t recognized or incorrect charging practices occur, a Current Year Labor Cost Transfer form must be completed and submitted to correct any charging anomalies.

! How does Earned Value get into the cost accounting system? How do you verify what was submitted?

" The Program Directive defines the Earned Value techniques approved for use on the program. Earned Value for your Control Account tasks is based on the Earned Value methods selected. Earned Value is taken consistent with how the work is planned.

Notional Control Account Manager Interview Questions

Niwot Ridge, LLC, Copyright © 2012, All Rights Reserved P a g e | 24

" On a monthly basis (month-‐end) Program Planning and Controls and the CAM assess each work package and the tasks in the Work Package to assure progress and Earned Value is taken in accordance with the method selected.

" After this process is complete the planning tool’s Earned Value is uploaded to the Cost Management system for pricing and cost analysis. Once the Cost System has been uploaded the Organizational Performance Reports (OPR) are generated to validate the Earned Value taken.

! How do you use weekly labor actual reports and organizational performance reports?

" Actual cost reports are generated and distributed weekly by PP&C. each CAM must review these actual cost reports on a weekly basis to assess the impacts to current and cumulative cost variances by Control Account.

" Organizational Performance Reports are generated from the Cost System each month-‐end to reflect BCWS, BCWP, ACWP, Schedule Variance, Cost Variance, and Variance at Completion for the current period, cumulative to date and at completion data by Control Account and by resource.

! What weekly and monthly meetings do you attend where your schedule and cost performance is discussed?

§ Schedule review meetings are held weekly and monthly as outlined in a Business Rhythms Calendar. During these meetings each CAM must present schedule progress and monthly performance, schedule metric reports, risks, risk mitigation plans, etc. CAMs must be prepared to discuss all details relating to any problems and proposed resolutions concerning their Control Accounts.

§ CAMs and Program Managers must review schedule status at the Weekly Program Control meeting. This meeting is an internal review in which the Technical and Intermediate Managers, and CAMs present schedule information to the Program Manager.

" Be prepared to discuss other pertinent business meeting where your scope of performance is reviewed.

! Show your latest variance analysis report. Has it been reviewed and approved?

§ This report is provided from the Cost Management System and used as required. § With this report the CAM can speak directly to the performance of the Control Account and the

Work Packages that make up the CA

" Be prepared to explain variances or trending thresholds that determine how you take corrective actions for your Control Account.

! Is the root cause of the variance drivers clearly and accurately identified?

" Be prepared to explain the root causes of any variances shown in the Variance Analysis Report

Notional Control Account Manager Interview Questions

Niwot Ridge, LLC, Copyright © 2012, All Rights Reserved P a g e | 25

! Has the impact to other Control Accounts or the program been identified?

" Be prepared to explain the impacts to other Control Accounts and the Program.

! If recoverable, has a corrective action plan been identified?

" Be prepared to explain your corrective action plan.

! Does the schedule variance correlate with the schedule status?

" Be prepared to explain how the schedule variance is correlated with the schedule status.

! Who reviewed and approves the variance analysis reports?

" The approval signatures for a Control Account variance analysis for are: (a) The Control Account Manager (CAM); (b) the Intermediate Manager or Business Manager; (c) the Program Manager or Director.

! How do you use the organizations performance reports or their equivalents?

" Organizational Performance Reports (OPRs) are generated from the Cost Management System each month end to reflect BCWS, BCWP, ACWP, schedule variance, cost variance, and variance at completion for the current period and cumulative to date and at completion data by Control Account.

" The OPR is the official Cost Management System document used to identify and status all variance analyses for each Control Account. Be prepared to provide the OPR for all your Control Accounts. Be able to explain all variance calculations and indices referenced along with their impacts to your Control Accounts.

" Some type of Performance Management Fact Sheet contain all variance analyses, indices and percentage calculations must be contained in your CAM Notebook

! Show and explain your CPI and SPI values that support your TCPI values?

" Be prepared to show your CPI and SPI values from the Cost Management System performance reports and how they support the To Complete Performance Index.

! What drives your variances?

" The following are explanations that must be considered tin order to address properly favorable or unfavorable cost and schedule performance measurement variance analysis problem statements:

" Cost Variance – problem statement (favorable or unfavorable) " BCWP > BCWS – favorable variance explanations " The task is less complex and will be completed earlier than planned " Early effort has been confined to tasks which are less complex than those that follow " The task has been overstaffed early in order to recognize the establishment of a higher priority

Notional Control Account Manager Interview Questions

Niwot Ridge, LLC, Copyright © 2012, All Rights Reserved P a g e | 26

" Deliverables of hardware have been accomplished in advance of need date " Earned Value may be incorrect and require an adjustment in the next reporting period " The plan is time phased poorly and the current status is not reflective of what is really happening " BCWP < BCWS – unfavorable variance explanation " The task is more complex than originally planned " Early effort has been more complex than the effort that follows " Delays in staffing have slowed progress " Hardware deliverables are late " Design of rework activities has delayed progress " Software deliverables are late " Data from another organization (drawings or technical analysis) has been late " Additional requirements have been established or changed " Higher priority has been establishes on other work " The plan is time phased poorly " Schedule Variance – favorable or unfavorable explanations " The complexity of the task is less than originally estimated " The less complex tasks have been completed early " The task is primarily LOE and not been fully staffed " The plan is time phased poorly " BCWP < BCWS – unfavorable " The task is more complex than originally planned " The more complex tasks have been complete early " Program priorities have resulted in application of resources in an inefficient manner – more

overtime or additional staffing " Delays in receipt of data have resulted in implementation of workarounds to make schedule.

More overtime or additional staffing " Changes, redesign, additional requirements, or out-‐of-‐scope effort " The plan is time phased poorly " Rate or usage variance

«R I SK»

§ DID 81650 calls out a Statistical Risk Analysis (SRA) for the Integrated Master Schedule (IMS). § The risk management of the technical aspects of the program should be included in the IMS as

well. § Technical risk management is guided by the specific procurement agency, but DoD Risk

Management is the starting document.

Notional Control Account Manager Interview Questions

Niwot Ridge, LLC, Copyright © 2012, All Rights Reserved P a g e | 27

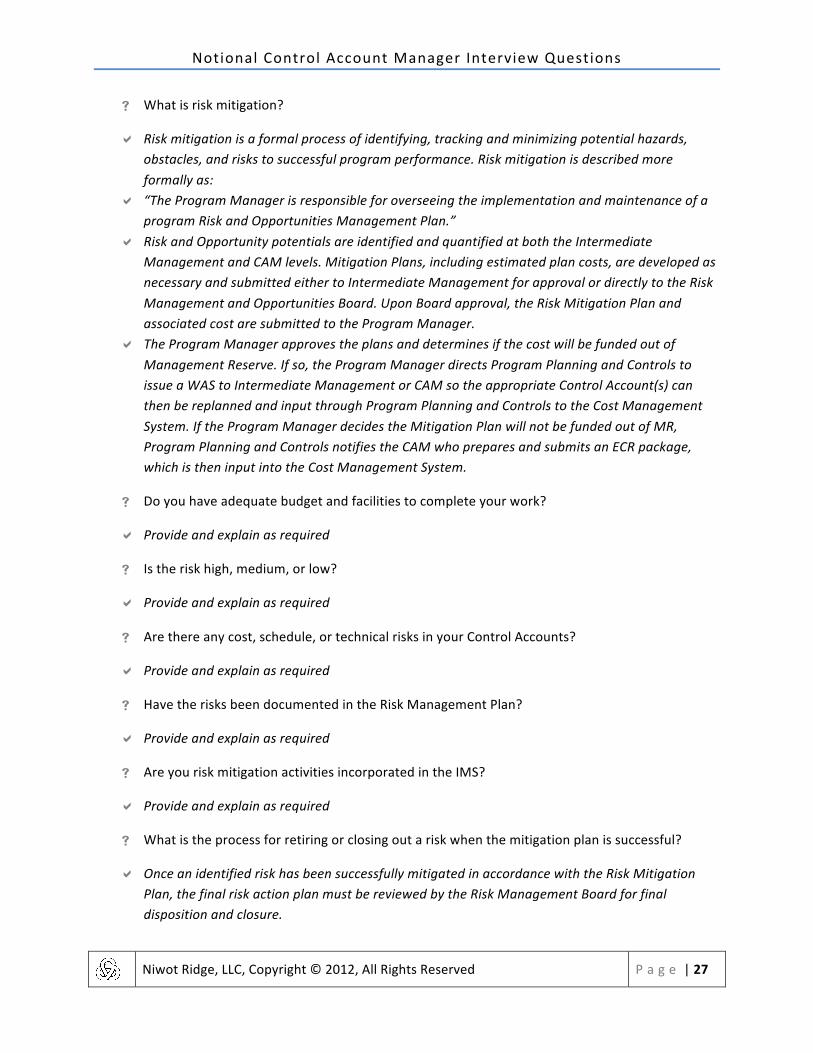

! What is risk mitigation?

" Risk mitigation is a formal process of identifying, tracking and minimizing potential hazards, obstacles, and risks to successful program performance. Risk mitigation is described more formally as:

" “The Program Manager is responsible for overseeing the implementation and maintenance of a program Risk and Opportunities Management Plan.”

" Risk and Opportunity potentials are identified and quantified at both the Intermediate Management and CAM levels. Mitigation Plans, including estimated plan costs, are developed as necessary and submitted either to Intermediate Management for approval or directly to the Risk Management and Opportunities Board. Upon Board approval, the Risk Mitigation Plan and associated cost are submitted to the Program Manager.

" The Program Manager approves the plans and determines if the cost will be funded out of Management Reserve. If so, the Program Manager directs Program Planning and Controls to issue a WAS to Intermediate Management or CAM so the appropriate Control Account(s) can then be replanned and input through Program Planning and Controls to the Cost Management System. If the Program Manager decides the Mitigation Plan will not be funded out of MR, Program Planning and Controls notifies the CAM who prepares and submits an ECR package, which is then input into the Cost Management System.

! Do you have adequate budget and facilities to complete your work?

" Provide and explain as required

! Is the risk high, medium, or low?

" Provide and explain as required

! Are there any cost, schedule, or technical risks in your Control Accounts?

" Provide and explain as required

! Have the risks been documented in the Risk Management Plan?

" Provide and explain as required

! Are you risk mitigation activities incorporated in the IMS?

" Provide and explain as required

! What is the process for retiring or closing out a risk when the mitigation plan is successful?

" Once an identified risk has been successfully mitigated in accordance with the Risk Mitigation Plan, the final risk action plan must be reviewed by the Risk Management Board for final disposition and closure.

Notional Control Account Manager Interview Questions

Niwot Ridge, LLC, Copyright © 2012, All Rights Reserved P a g e | 28

! What is the process for retiring or closing out a risk when the mitigation plan is unsuccessful?

" If an identified risk has not been mitigated completely in accordance with the Risk Mitigation Plan, then the Risk Management Board must review the mitigation plan actions taken and make appropriate adjustments as needed (mitigation plans, mitigation times, etc.). The Risk Management Board may simply accept the risk level as is and continue to monitor as appropriate. These actions could result in additional revisions to the Control Account Baseline. This change may require a WAD or an Estimate Change Request

! Have resources been provided for the mitigation plans?

" Identify any resources that have been provided for the mitigation plans. If none have been provided, explain why?

! Where critical skills exist, are you sufficiently staffed in these areas? Do you have succession planning for these critical areas?

" Provide and explain as required

«EST IMATE AT COMPLET ION ( EAC ) »

! Describe the process you use to update your EAC and what documentation is used?

§ The acceptance process for updating the Estimate To Complete (ETC) and Estimate At Completion (EAC) are described in the published Earned Value Management System Description and summarized below

§ “Every month CAMs review the Control Account cost and schedule data and assess the ETC and EAC of each Control Account. CAMs make an assessment based on the historical performance of the accounts current metrics and future projections.”

§ “The projections should consider potential process improvements, risk assessments, and other applicable factors that may affect remaining work. The EAC is updates in the cost tool as Actual Cost for Work Performed (ACWP) replaces ETC. It is recommended that this occur monthly. If not monthly than quarterly. If the current ACWP is different from the current ETC minor perturbations will result in the EAC. If the customer mandates a stable EAC, then a log must be maintained to reconcile internal EAC values and customer reported EACs.

§ Where Control Account ETC changes are required, the CAM generates and redlines a time phased ETC. The change request form is completed, or other documentation that contains the appropriate data elements are attached to the form. The Change Request is then submitted to Program Controls for review

Notional Control Account Manager Interview Questions

Niwot Ridge, LLC, Copyright © 2012, All Rights Reserved P a g e | 29

! How do you update your Estimate to Compete (ETC)? When was the ETC last updated?

" The Estimate At Completion should be reviewed monthly and updated as appropriate. Provide the rationale for the latest ETC and EAC revisions.

! Show documentation of that update and rationale for the new ETC numbers.

" Provide and explain as required.

! Who reviews and approves your ETC?

" The CAM, Program Controls, and the Program Manager

! Do the cost and schedule variances support the EAC?

" If you have experienced unfavorable cost or schedule variances and have not revised your EAC and ETC values, then the following actions should be taken:

" Compare the CPI percent against the TCPI percentage. Of the delta value is less than X% then your EAC is considered credible. The Independent Estimate At Completion (IEAC) indices are used to assess the validity of the range and to evaluate the realism of the projected EAC.

! How often is a comprehensive EAC (CEAC) performed?

§ Each program should performance a Comprehensive Estimate At Completion (CEAC) using a “bottoms up” method at least annually. This date should be defined in the Program Directive.

" Be prepared to answer which data has been chosen for your program.

! If a CEAC was performed, show your memo with the ground rules from Program Control?

" Be prepared to describe what ground rules are used for the CEAC, who participants in the CEAC, and how the program Performance Measurement Baseline (PMB) is adjusted using the output of the CEAC.

«SUBCONTRACTOR MANAGEMENT»

§ Do any of your Control Accounts contain subcontractor effort? If so, answer the following questions:

! What scope is the subcontract responsible for?

" Subcontracts and or inter-‐company work transfer agreements (IWTAs) scope is based on negotiated or documented contracted work. Be prepared to discuss your subcontract / IWTA contract type and work scope and be prepared to provide the Statement of Work (SOW) and work authorization for each subcontract / IWTA

Notional Control Account Manager Interview Questions

Niwot Ridge, LLC, Copyright © 2012, All Rights Reserved P a g e | 30

! How does the subcontractor receive authorizations for scope, schedule, and resources from the prime?

§ Subcontractor and IWTA direction is provided by the contract administration organization through a negotiated contract or a contract modification to amend or change work scope, schedule, and resources.

! What reporting requirements have been levied on the subcontractors?

§ Any nonrecurring or development subcontract that is larger than $25M and not Firm Fixed Price (FFP), has a Cost Performance Report (CPR) requirement. A non-‐FFP sub-‐contract larger than $10M, but less than $25M, has a modified Cost Performance Report (MCPR) requirement. The Non-‐FFP subcontracts under $10M have minor reporting requirements although if considered a high cost, schedule, or technical risk a MCPR is required. Firm Fixed Price contracts fall into two categories: Delivery and Support / Level of Effort

" Be prepared to provide copies of the latest reporting documentation pertaining to your subcontracts / IWTAs

! Are the subcontractor’s schedules status weekly?

" Provide and explain as required

! How are the resources planned for the subcontractors (BCWS spreads for the subcontractor work packages)

§ The budget information should represent the cost baseline negotiated or proposed. The BCWS must be time-‐phased consistent with the baseline schedule spans negotiated with each subcontractor, and should be reconciled to the reporting requirement documentation (CPR, MCPR) with the cost management system. Regardless of the Program Performance Management system applied to the subcontractor, the Program Performance Management data must be reviewed for logic, consistently, and validity

§ For minor subcontracts the CAM uses the IMS information and the time phased budget to plan and status the effort in the PPM cost management tool. The BCWS in input into the PPM Cost Tool and planned by the CAM using the time phased data in conjunction with the schedules tasks. The subcontractor’s scheduled tasks are given as associated dollar value using the appropriate Earned Value techniques allowed in the PPM cost tool. The recommended technciques for minor subcontarcts is Percent Complete method. It provide a means to gain partial earnings, thereby minimizing erroneous cost and schedule variances.

! Is the BCWS time phased with the baseline schedule plans?

" Be prepared to provide copies of your sibcontracts or IWTAs latest budget milestone plans and reporting documentation, and show traceability to the applicable Control Account

Notional Control Account Manager Interview Questions

Niwot Ridge, LLC, Copyright © 2012, All Rights Reserved P a g e | 31

! Can you trace the budget from the Work Authorization to the Control Account Plans, to the subcontractors?

" Be prepared to provide traceability for each subcontractor / IWTA Work Authorization Document (WAD) that provides scope, schedule, budget, period of performance, and approvals to the applicable PPM cost report and control account plan.

! Can you trace the schedule from the subcontractor’s schedule to the Control Account Plan, to the IMS?

" Be prepared to provide copies of your subcontract / IWTA latest milestone plans and reporting documentation and provide traceability to the program IMS

! How do you determine BCWP for each subcontractor?

§ Subcontract Earned Value Budgeted Cost for Work Performed (BCWP) is taken from the CPR or MCPR. This value is represented at cost, but appropriate fee must be added. BCWP is handled based on the contract type and fee type. Once the appropriate fee is added to the cost, BCWP form the subcontract CPR or MCPR data is then input into the PPM Cost Tool.

" As a CAM you must provide a sanity check to ensure that the Earned Value represented in the subcontract reports is accurate and that progress has been assessed properly based on your knowledge of the work being performed.

" For minor subcontract effort the CAM must update progress and Earned Value monthly on both an IMS and on the Work Packages listed on the CAP worksheets. Immediately upon receipt of the subcontractor’s status and schedule data, the CAM must determine the current Earned Value (BCWP) by using the appropriate approved technique.

" IWTAs are handled in the same fashion as previously described. The only difference between subcontracts and IWTAs is that no fee is added.

! What are the thresholds for generating a variance analysis report for the subcontractors?

§ Variance Analysis thresholds for subcontracts and IWTAs must be the same as, or are greater than, customer directed variance analysis reporting requirements. It is imperative that the subcontract or IWTA cost and schedule variances, and Variance At Completion (VAC) thresholds are assessed and reported in the same manner as the prime contractor in order to provide uniform CPR Format 5 variance analysis narratives and corrective actions.

§ There are two primary methods of variance analysis required by most customers: variance drivers or traditional dollar and or percentage thresholds. If the customer requires the variance driver method, then the subcontractor should also be required to use this method. If the traditional dollar and or percentage method is required , the program should flow down that same percentage but reduce the dollar amount. Non-‐FFP subcontractor’s value data in the PPM tool system includes fee, which increases the subcontractor’s values by as much as 5% to 15%/

Notional Control Account Manager Interview Questions

Niwot Ridge, LLC, Copyright © 2012, All Rights Reserved P a g e | 32

as such, tighter variance thresholds should be given to the subcontractor, and these should be documented in the variance reporting thresholds section of the PPM Program Directive.

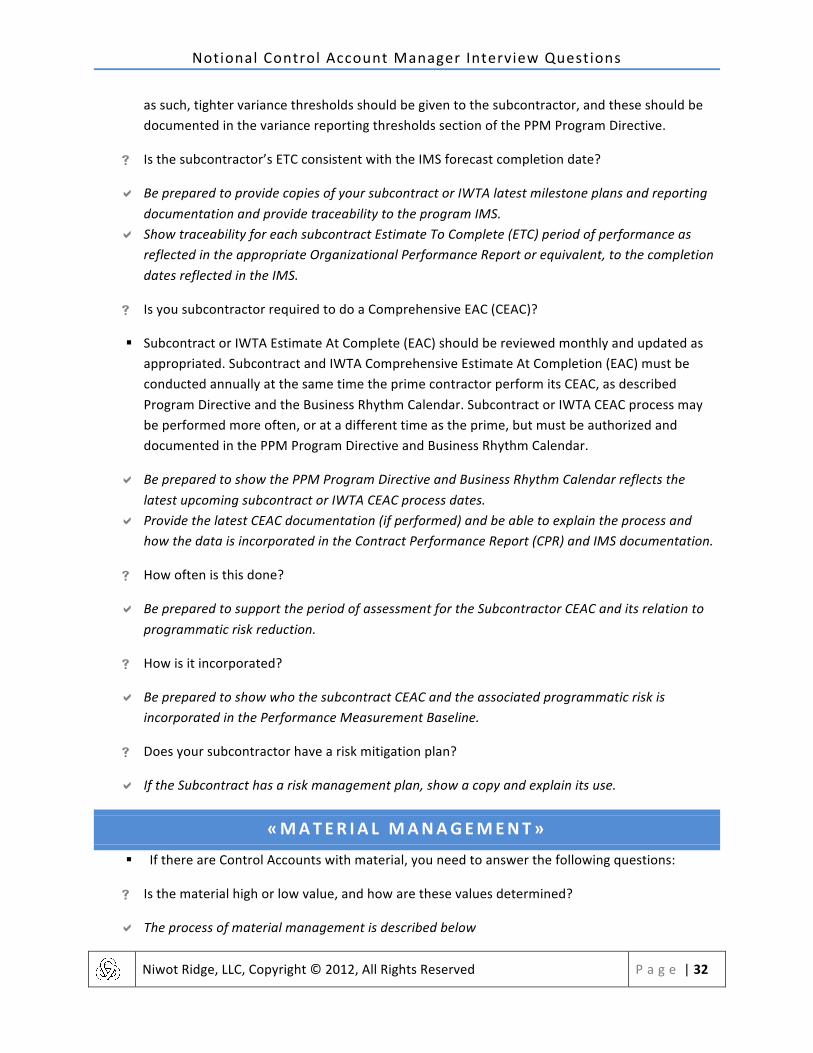

! Is the subcontractor’s ETC consistent with the IMS forecast completion date?

" Be prepared to provide copies of your subcontract or IWTA latest milestone plans and reporting documentation and provide traceability to the program IMS.

" Show traceability for each subcontract Estimate To Complete (ETC) period of performance as reflected in the appropriate Organizational Performance Report or equivalent, to the completion dates reflected in the IMS.

! Is you subcontractor required to do a Comprehensive EAC (CEAC)?

§ Subcontract or IWTA Estimate At Complete (EAC) should be reviewed monthly and updated as appropriated. Subcontract and IWTA Comprehensive Estimate At Completion (EAC) must be conducted annually at the same time the prime contractor perform its CEAC, as described Program Directive and the Business Rhythm Calendar. Subcontract or IWTA CEAC process may be performed more often, or at a different time as the prime, but must be authorized and documented in the PPM Program Directive and Business Rhythm Calendar.

" Be prepared to show the PPM Program Directive and Business Rhythm Calendar reflects the latest upcoming subcontract or IWTA CEAC process dates.

" Provide the latest CEAC documentation (if performed) and be able to explain the process and how the data is incorporated in the Contract Performance Report (CPR) and IMS documentation.

! How often is this done?

" Be prepared to support the period of assessment for the Subcontractor CEAC and its relation to programmatic risk reduction.

! How is it incorporated?

" Be prepared to show who the subcontract CEAC and the associated programmatic risk is incorporated in the Performance Measurement Baseline.

! Does your subcontractor have a risk mitigation plan?

" If the Subcontract has a risk management plan, show a copy and explain its use.

«MATER IA L MANAGEMENT»

§ If there are Control Accounts with material, you need to answer the following questions:

! Is the material high or low value, and how are these values determined?

" The process of material management is described below

Notional Control Account Manager Interview Questions

Niwot Ridge, LLC, Copyright © 2012, All Rights Reserved P a g e | 33

§ “Initially material budgets can be placed in planning packages until specific material requirements are identified (by purchase requisition, purchase order, development Bill of Materials, or material lists). As requirements are identified, budgets are converted into tasks with schedules and estimated or know costs. For the purpose of performance management there are generally three type of material: direct charge, inventory, and miscellaneous material. BCWS and BCWP are handled differently for each category.”

§ “If a program does not utilize a Materials Requirements Plan (MRP) system for tracking direct or inventory material, it must be tracked using high-‐dollar-‐value or high-‐quantity level that warrants planning and statusing by part number because of its criticality to the program. The definition of “high dollar or high quantity” must be defined in the Program Directive. High Value Material is to be planned discretely while low value material may be planned as Level of Effort.”

" Be prepared to explain how the program determine “high” and “low” value material requirements, and provide the definition referenced in the Program Directive.

! How do you plan your material? Is it listed by Bill of Materials or an equivalent?

§ BCWS for Direct Charge Material: typically Direct Charge Material is represented by estimated (of not yet negotiated) pt negotiated values time-‐phased by month; and based on milestone schedules, on expected receipt of hardware to the point-‐of-‐use, or on a monthly percentage.

§ In determining the BCWS methodology consideration should be given to program requirements, the subcontractor / purchase order type of the contract and the payment terms (milestones, payment on delivery, etc.). Tasks should be primarily considered “discrete effort” and planned as such, using any of the Earned Value techniques defined in the Program Directive.