Embed Size (px)

DESCRIPTION

non profit organization

Citation preview

7/21/2019 NPO - Govact

http://slidepdf.com/reader/full/npo-govact 1/5

7/21/2019 NPO - Govact

http://slidepdf.com/reader/full/npo-govact 2/5

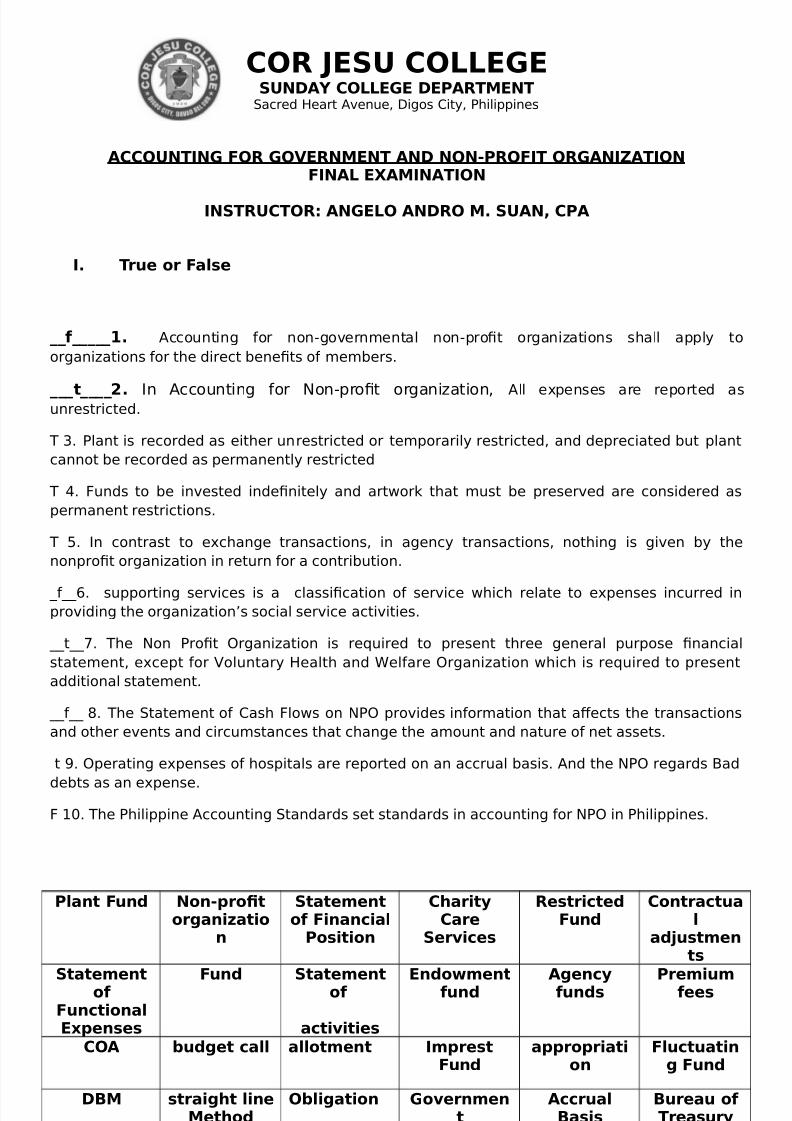

COR JESU COLLEGESUNDAY COLLEGE DEPARTMENT

9acred $eart Avenue, :igos !ity, 2hilippines

ACCOUNTING OR GO!ERNMENT AND NON"PROIT ORGANI#ATIONINAL E$AMINATION

INSTRUCTOR: ANGELO ANDRO M% SUAN& CPA

I% True 'r a(se

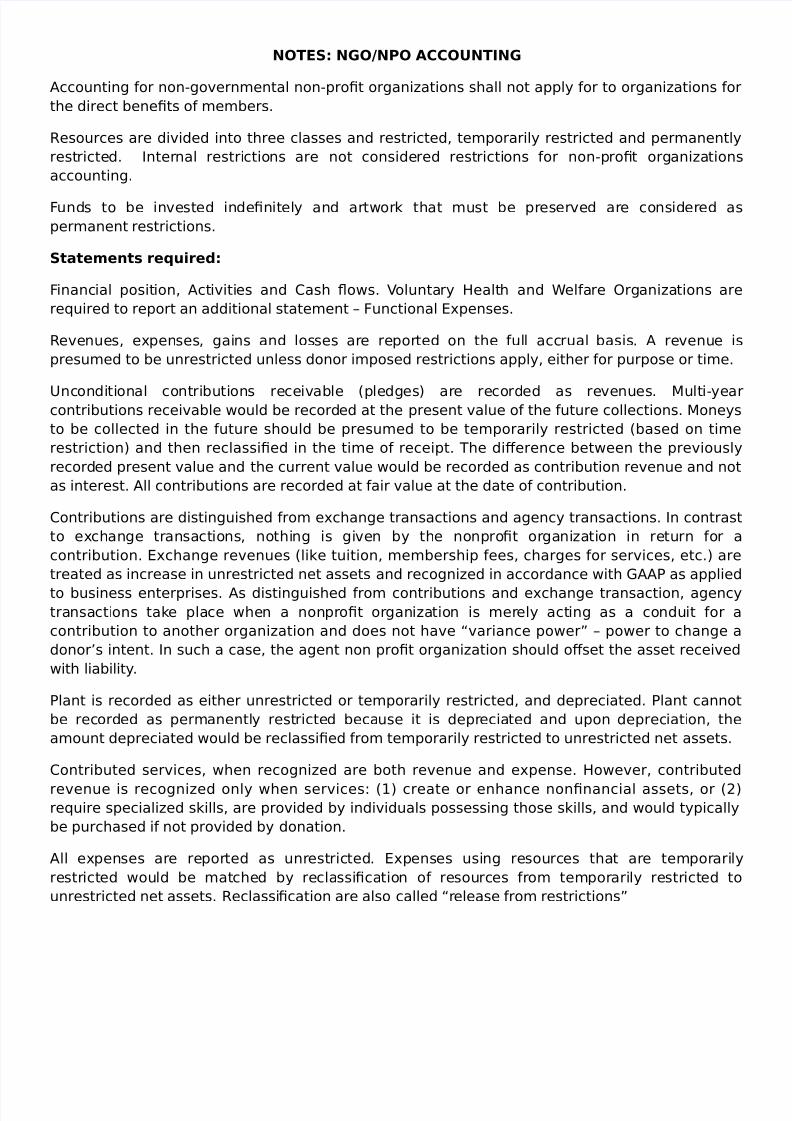

))*)))))+% Accounting for non-governmental non-prot organizations shall apply to

organizations for the direct benets of members.

)))t)))),% In Accounting for ;on-prot organization, All e*penses are reported asunrestricted.

/ <. 2lant is recorded as either unrestricted or temporarily restricted, and depreciated but plant

cannot be recorded as permanently restricted

/ =. Funds to be invested indenitely and artwor that must be preserved are considered as

permanent restrictions.

/ >. In contrast to e*change transactions, in agency transactions, nothing is given by the

nonprot organization in return for a contribution.

?f??@. supporting services is a classication of service which relate to e*penses incurred inproviding the organization5s social service activities.

??t??. /he ;on 2rot &rganization is re'uired to present three general purpose nancial

statement, e*cept for #oluntary $ealth and %elfare &rganization which is re'uired to present

additional statement.

??f?? B. /he 9tatement of !ash Flows on ;2& provides information that a0ects the transactions

and other events and circumstances that change the amount and nature of net assets.

t C. &perating e*penses of hospitals are reported on an accrual basis. And the ;2& regards Dad

debts as an e*pense.

F 7E. /he 2hilippine Accounting 9tandards set standards in accounting for ;2& in 2hilippines.

P(ant und N'n"-r'.t'rani0ati'

n

Statement'* inan1ia(

P'siti'n

C2arit3Care

Ser4i1es

Restri1tedund

C'ntra1tua(

ad5ustments

Statement'* un1ti'na(E6-enses

und Statement'*

a1ti4ities

End'7ment*und Aen13*unds Premium*ees

COA 8udet 1a(( a(('tment Im-restund

a--r'-riati'n

(u1tuatin und

D9M strai2t (ineMet2'd

O8(iati'n G'4ernment

A11rua(9asis

9ureau '* Treasur3

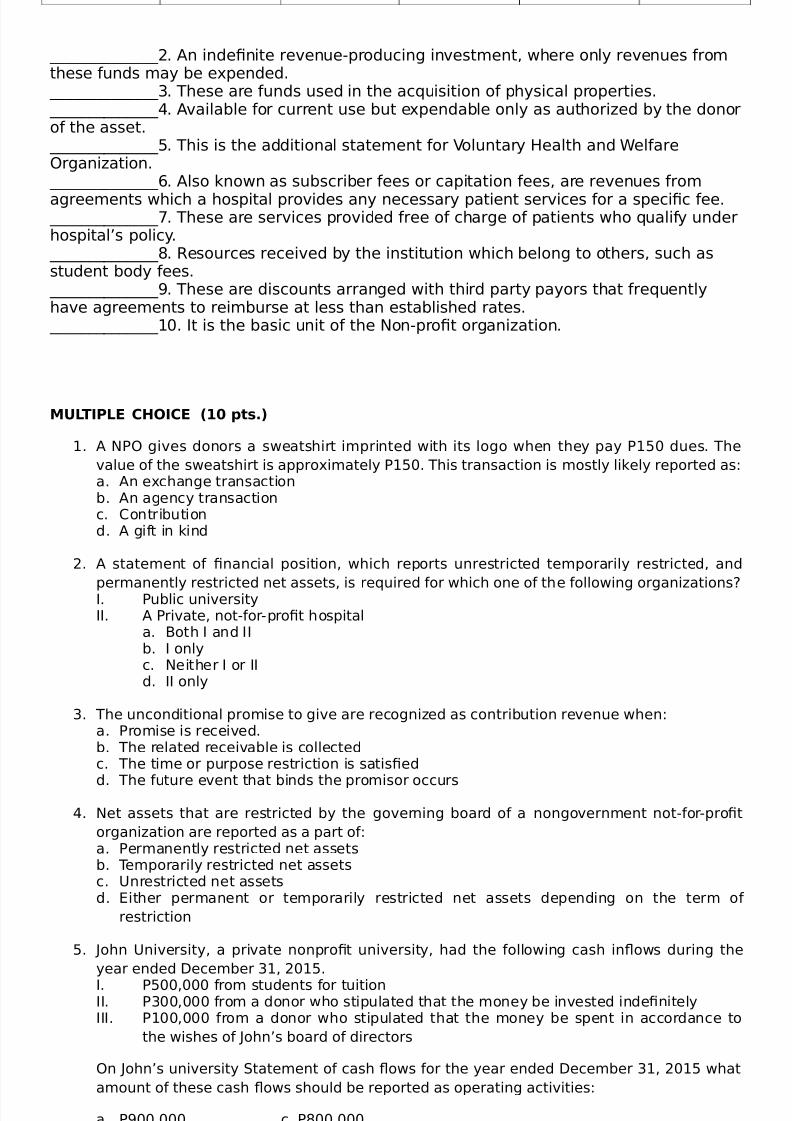

Identi.1ati'n:

??????????????7. Is a non-stoc corporation that is organized for the benet of the publicas a whole rather than for the benet of an individual proprietor.

7/21/2019 NPO - Govact

http://slidepdf.com/reader/full/npo-govact 3/5

??????????????8. An indenite revenue-producing investment, where only revenues fromthese funds may be e*pended. ??????????????<. /hese are funds used in the ac'uisition of physical properties. ??????????????=. Available for current use but e*pendable only as authorized by the donorof the asset. ??????????????>. /his is the additional statement for #oluntary $ealth and %elfare&rganization. ??????????????@. Also nown as subscriber fees or capitation fees, are revenues from

agreements which a hospital provides any necessary patient services for a specic fee. ??????????????. /hese are services provided free of charge of patients who 'ualify underhospital5s policy. ??????????????B. Resources received by the institution which belong to others, such asstudent body fees. ??????????????C. /hese are discounts arranged with third party payors that fre'uentlyhave agreements to reimburse at less than established rates. ??????????????7E. It is the basic unit of the ;on-prot organization.

MULTIPLE COICE ;+< -ts%=

7. A ;2& gives donors a sweatshirt imprinted with its logo when they pay 27>E dues. /he

value of the sweatshirt is appro*imately 27>E. /his transaction is mostly liely reported as6a. An e*change transactionb. An agency transactionc. !ontributiond. A gift in ind

8. A statement of nancial position, which reports unrestricted temporarily restricted, and

permanently restricted net assets, is re'uired for which one of the following organizationsI. 2ublic universityII. A 2rivate, not-for-prot hospital

a. Doth I and IIb. I onlyc. ;either I or IId. II only

<. /he unconditional promise to give are recognized as contribution revenue when6a. 2romise is received.b. /he related receivable is collectedc. /he time or purpose restriction is satised

d. /he future event that binds the promisor occurs

=. ;et assets that are restricted by the governing board of a nongovernment not-for-prot

organization are reported as a part of6a. 2ermanently restricted net assetsb. /emporarily restricted net assetsc. +nrestricted net assetsd. )ither permanent or temporarily restricted net assets depending on the term of

restriction

>. Gohn +niversity, a private nonprot university, had the following cash in"ows during the

year ended :ecember <7, 8E7>.

I. 2>EE,EEE from students for tuitionII. 2<EE,EEE from a donor who stipulated that the money be invested indenitelyIII. 27EE,EEE from a donor who stipulated that the money be spent in accordance to

the wishes of Gohn5s board of directors

&n Gohn5s university 9tatement of cash "ows for the year ended :ecember <7, 8E7> what

amount of these cash "ows should be reported as operating activities6

a. 2CEE,EEE c. 2BEE,EEEb. 2=EE,EEE d. 2@EE,EEE

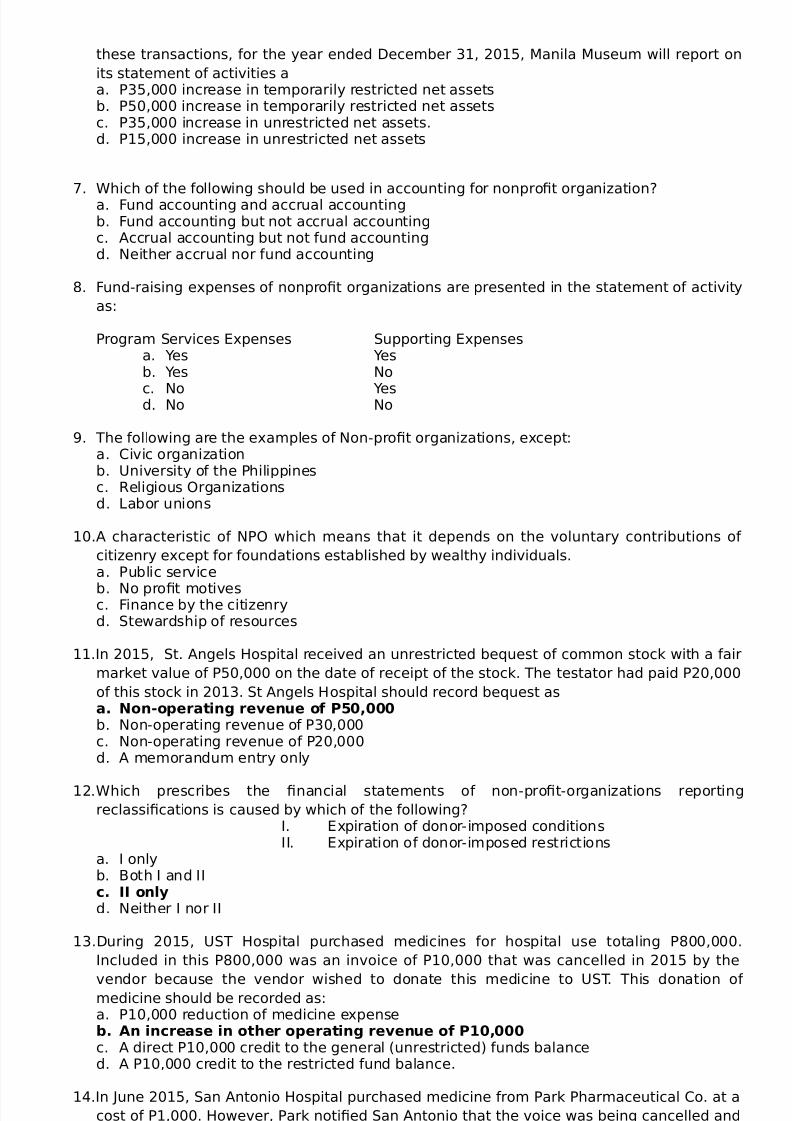

@. anila useum, a non prot organization received contributions restricted for research

totaling 2>E,EEE in 8E7=. Assume that the 2>E,EEE was not e*pensed in 8E7=. /hese

contributions were used to purchase 2<>,EEE of research e'uipment in 8E7>. As a result of

7/21/2019 NPO - Govact

http://slidepdf.com/reader/full/npo-govact 4/5

these transactions, for the year ended :ecember <7, 8E7>, anila useum will report on

its statement of activities aa. 2<>,EEE increase in temporarily restricted net assetsb. 2>E,EEE increase in temporarily restricted net assetsc. 2<>,EEE increase in unrestricted net assets.d. 27>,EEE increase in unrestricted net assets

. %hich of the following should be used in accounting for nonprot organizationa. Fund accounting and accrual accountingb. Fund accounting but not accrual accountingc. Accrual accounting but not fund accountingd. ;either accrual nor fund accounting

B. Fund-raising e*penses of nonprot organizations are presented in the statement of activity

as6

2rogram 9ervices )*penses 9upporting )*pensesa. Hes Hesb. Hes ;o

c. ;o Hesd. ;o ;o

C. /he following are the e*amples of ;on-prot organizations, e*cept6a. !ivic organizationb. +niversity of the 2hilippinesc. Religious &rganizationsd. abor unions

7E.A characteristic of ;2& which means that it depends on the voluntary contributions of

citizenry e*cept for foundations established by wealthy individuals.a. 2ublic service

b. ;o prot motivesc. Finance by the citizenryd. 9tewardship of resources

77.In 8E7>, 9t. Angels $ospital received an unrestricted be'uest of common stoc with a fair

maret value of 2>E,EEE on the date of receipt of the stoc. /he testator had paid 28E,EEE

of this stoc in 8E7<. 9t Angels $ospital should record be'uest asa% N'n"'-eratin re4enue '* P><&<<<b. ;on-operating revenue of 2<E,EEEc. ;on-operating revenue of 28E,EEEd. A memorandum entry only

78.%hich prescribes the nancial statements of non-prot-organizations reporting

reclassications is caused by which of the followingI. )*piration of donor-imposed conditionsII. )*piration of donor-imposed restrictions

a. I onlyb. Doth I and II1% II 'n(3d. ;either I nor II

7<.:uring 8E7>, +9/ $ospital purchased medicines for hospital use totaling 2BEE,EEE.

Included in this 2BEE,EEE was an invoice of 27E,EEE that was cancelled in 8E7> by the

vendor because the vendor wished to donate this medicine to +9/. /his donation of medicine should be recorded as6a. 27E,EEE reduction of medicine e*pense8% An in1rease in 't2er '-eratin re4enue '* P+<&<<<c. A direct 27E,EEE credit to the general unrestricted funds balanced. A 27E,EEE credit to the restricted fund balance.

7=.In Gune 8E7>, 9an Antonio $ospital purchased medicine from 2ar 2harmaceutical !o. at a

cost of 27,EEE. $owever, 2ar notied 9an Antonio that the voice was being cancelled and

that the medicines were being donated to 9an Antonio. 9an Antonio should record this

donation of medicines as

a% Ot2er '-eratin re4enue '* P+&<<<b. A 27,EEE credit to operating e*pensesc. A 27,EEE credit to non-operating e*pensesd. A memorandum entry only

7/21/2019 NPO - Govact

http://slidepdf.com/reader/full/npo-govact 5/5

7>.%illiams $ospital, a nonprot hospital aJliated with a religious group reported the

following information for the year ended :ecember <7, 8E7>6

1ross patient service revenue at the hospital5s full established rates 2CBE,EEEDad :ebts e*pense 7E,EEE!ontractual AdKustments with third-party payors 7EE,EEEAllowance for discounts to hospital employees 7>,EEE

&n the hospital5s statement of operations for the year ended :ecember <7, 8E77,

what amount should be reported as net patient service revenues.

a. 2B@>,EEEb. 2BBE,EEEc. 2B>>,EEEd. 2C>>,EEE

2ro Forma )ntries6

Pr'8(em +: 's-ita(s

1ross patient service before charity care or contractual adKustments 28EE,EEE!harity !are for poor and indigent persons patients 7>,EEE!ontractual adKustment allowed to 2hilhealth patients <E,EEE2rovision for doubtful accounts <E,EEE

Re'uired67. Record gross receipt patient revenue8. Record contractual adKustments allowed to 2hilhealth<. Record the provision of doubtful accounts

Pr'8(em ,: P(ede

A non-prot organization received unconditional pledges totaling to <EE,EEE in a fund raisingdrive. 7EL of the pledges are considered to be doubtful of collection. ae the following Kournalentries6

7. Record pledges received8. Record the 7EL provision for doubtful pledges

Pr'8(em ?: C'((ees and Uni4ersities

1ross /uition fees 2>EE,EEE /uition waivers provided under fellowship program >E,EEE2rovision for doubtful accounts >L 8>,EEE

ae the following Kournal entries67. Record educational and general tuition fees8. Record tuition waivers<. Record provision for doubtful accounts

![NPOnpo-cncp.org/files/activity_index/第18回日本NPO学会年次大会発表と... · 3 13 [npo - net:00458] NPO 3 3 11 Green Hill NPO NPO CERT NPO 月 「 地 域 の リ ス ク](https://img.pdfslide.net/doc/110x75/6049ebeac34dbc54af20b039/nponpo-cncporgfilesactivityindexc18oenpoce.jpg)