Embed Size (px)

Citation preview

VALUATION AND PRICING OF EQUITY SECURITIES IN AN EMERGING STOCK MARKET: EVIDENCE FROM THE NIGERIAN BANKING SECTOR

A THESIS SUBMITTED TO THE DEPARTMENT OF

FACULTY OF

1

NWUDE CHUKE EMMANUEL PG/Ph.D/2000/31748

VALUATION AND PRICING OF EQUITY SECURITIES IN AN EMERGING STOCK MARKET: EVIDENCE FROM THE NIGERIAN BANKING SECTOR

Business Administration

A THESIS SUBMITTED TO THE DEPARTMENT OF BANKING AND FINANCE

FACULTY OF BUSINESS ADMINISTRATION, UNIVERSITY OF NIGERIA ENUGU

CAMPUS

Webmaster Digitally Signed by Webmaster’s Name DN : CN = Webmaster’s name O= University of Nigeria, NsukkaOU = Innovation Centre

2010

UNIVERSITY OF NIGERIA

VALUATION AND PRICING OF EQUITY SECURITIES IN AN EMERGING STOCK MARKET: EVIDENCE FROM THE NIGERIAN BANKING SECTOR

BANKING AND FINANCE,

, UNIVERSITY OF NIGERIA ENUGU

DN : CN = Webmaster’s name O= University of Nigeria, Nsukka

UNIVERSITY OF NIGERIA

2

VALUATION AND PRICING OF EQUITY SECURITIES IN AN EMERGING STOCK MARKET: EVIDENCE FROM THE NIGERIAN BANKING SECTOR

BY NWUDE CHUKE EMMANUEL

PG/Ph.D/2000/31748

DEPARTMENT OF BANKING AND FINANCE FACULTY OF BUSINESS ADMINISTRATION

UNIVERSITY OF NIGERIA NSUKKA ENUGU CAMPUS

APRIL 2010

3

VALUATION AND PRICING OF EQUITY SECURITIES IN AN EMERGING STOCK MARKET: EVIDENCE FROM THE NIGERIAN BANKING SECTOR

BY NWUDE CHUKE EMMANUEL PG/Ph.D/2000/31748 A thesis submitted to the Department of Banking and Finance, Faculty of Business Administration, University of Nigeria Enugu campus, in fulfilment of the requirements for the award of a Doctor of Philosophy(Ph.D) Degree in Finance DEPARTMENT OF BANKING AND FINANCE FACULTY OF BUSINESS ADMINISTRATION UNIVERSITY OF NIGERIA ENUGU CAMPUS SUPERVISOR: PROF. C. U. UCHE APRIL 2010

4

APPROVAL

Nwude Chuke Emmanuel, a postgraduate student in the Department of Banking and Finance,

Faculty of Business Administration, University of Nigeria, Enugu campus, with registration

number PG/Ph.D/2000/31748 has satisfactorily completed the requirements for the award of

Doctor of Philosophy in Finance.

This thesis has been approved for the Department of Banking and Finance, Faculty of

Business Administration, University of Nigeria, Enugu Campus.

BY

Professor C. U. Uche Mrs N. J. Modebe Supervisor Head of Department

Professor S. I. Owualah Dr U. J. F. Ewurum External Examiner Internal Examiner

5

CERTIFICATION I, Nwude Chuke Emmanuel, a postgraduate student in the Department of Banking and Finance, Faculty of Business Administration, University of Nigeria, Enugu campus, with registration number PG/Ph.D/2000/31748 carried out this research work on “Valuation and Pricing of Equity Securities in an Emerging Stock Market: Evidence from the Nigerian Banking Sector” in fulfilment of the requirements for the award of Doctor of Philosophy in Finance. The work embodied in this thesis is original and has not been submitted in part or full for any

other Diploma or Degree of this or any other University.

Chuke E. Nwude Student

6

DEDICATION

This research is dedicated to Almighty God, the Fountain of knowledge, my Cornerstone, my

Creator, my Protector, my Shield, the Solid Rock on which I stand and the Everlasting God

whose gifts are irrevocable. He has shown Himself strong in my life, as He does for all whose

hearts are perfect towards Him. To you God alone is all the glory.

7

ACKNOWLEDGEMENTS First, I give glory and praise to God for His enabling grace that made it possible for me to

complete this work despite all odds. I am sincerely grateful to my supervisors, Professor

Chibuike Ugochukwu Uche and Dr A. M. O. Anyafo (of blessed memory) for their

contributions without which this work would not have been a success. I would like to thank

Professor Chibuike Ugochukwu Uche in a special way, for incisively inspiring research in

this direction and for his invaluable suggestions in the course of this work. His sacrifices

ensured and insured the completion of this work. In the same vein, I express my profound

gratitude to our erudite first professor of finance University of Nigeria Nsukka ever produced,

in the person of Professor F. O. Okafor, for his incalculable sacrifice to ensure continuity in

academic excellence in the Department in particular and the Faculty of Business

Administration in general, for his understanding, assistance and moral support in all my

academic endeavours.

Equally worthy of mention are Prof Ikechukwu Nwosu, Professor (Mrs) D. Nnoli, Dr U. J. F.

Ewurum, Dr (Mrs) Eby Ogamba, Dr J.U.J Onwumere, Dr (Mrs) Justie Nnabuko, Dr I. C. O.

Nwaizugbo who normally called to know what was holding me from completing my work,

which they know I have the capacity. I am particularly appreciative of your interests that

urged me on to complete this work.

My thanks go to Professor David Webb of London School of Economics and Political

Science, Professor Olaseni Akintola-Bello of Arbitrage Consulting Group Lagos, Professor

W. I. C. Iyiegbuniwe and HRH Professor Sunday Owualah both of Department of Banking

and Finance, University of Lagos, for their invaluable contributions in this work.

I also wish to express my profound gratitude to the Dean, Faculty of Business

Administration, Professor Uche Modum, and the Head, Department of Banking and Finance,

Mrs Nwanne J. Modebe, for their understanding, assistance and moral support.

Finally, I wish to acknowledge the support of my dear God-sent wife Comie, and children,

KC, Somtie, Chisom, Dinma-baby, for their prayers, patience and understanding for the time

I had to stay away from their cherished company to see to the tidying up of this work.

8

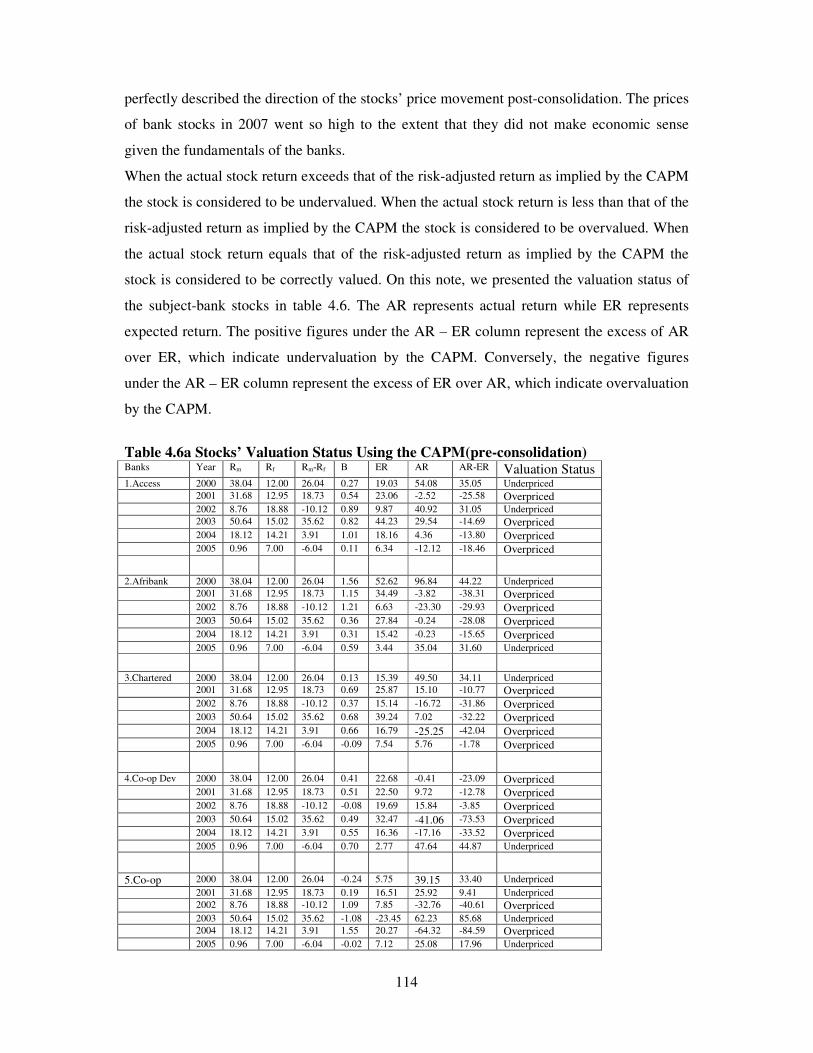

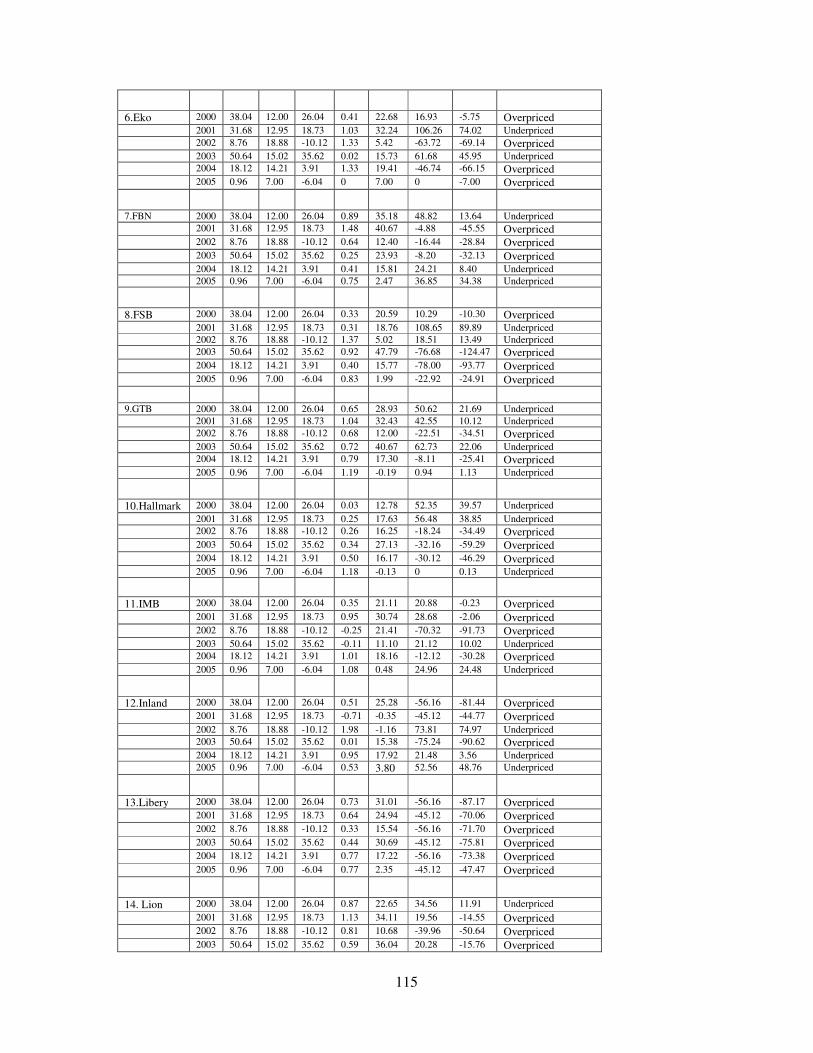

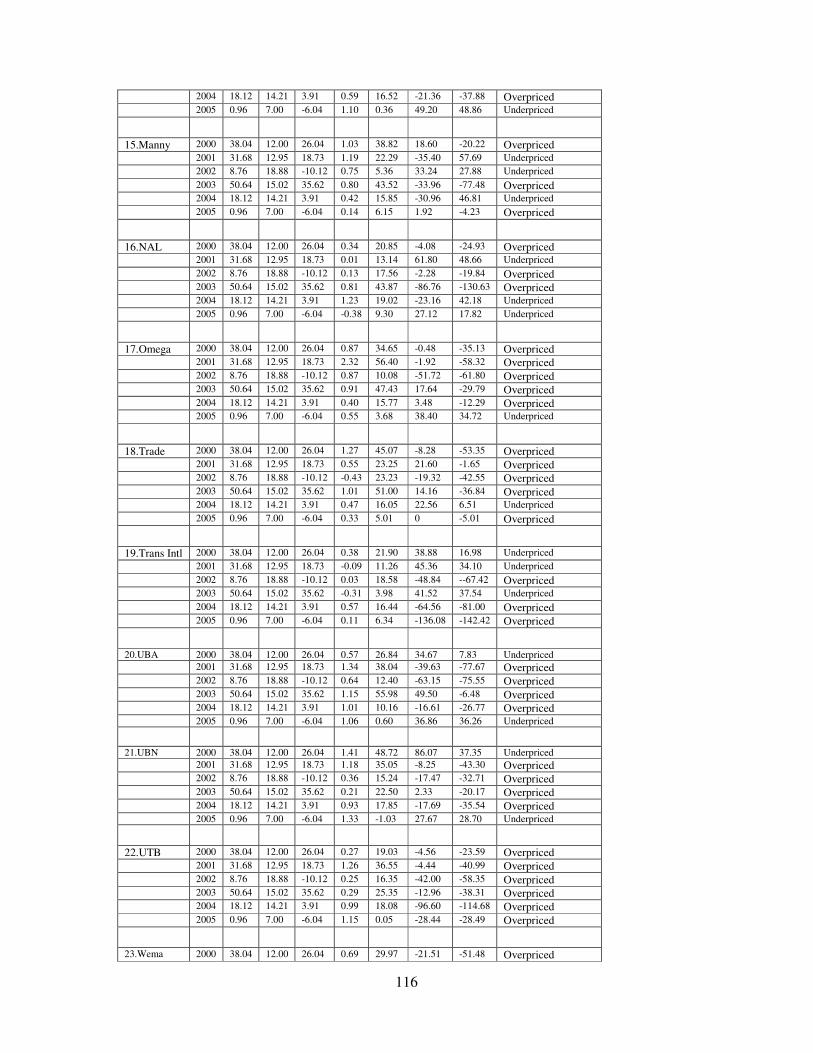

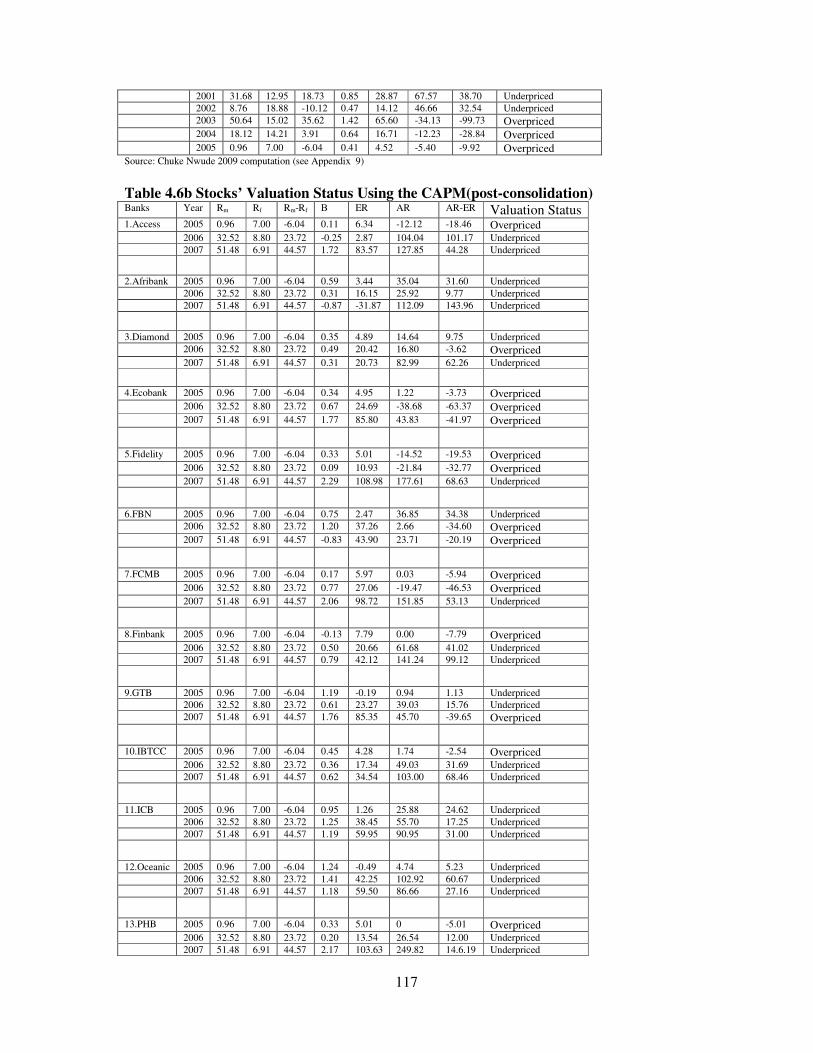

ABSTRACT In finance, there is widespread agreement that the Capital Asset Pricing Model (CAPM) and Whitbeck-Kisor Model (WKM) are good predictors of share price movements in stock markets. While the above assertion had been empirically validated in several stock markets in developed economies, there have been few such studies in the stock markets of developing economies like Nigeria. Such studies have now become imperative given the recent developments that have seen the Nigerian stock market capitalization increasing from N276, 111,743,197.30 on January 2, 1998 to N10, 180,292,984,225.00 on December 31, 2007 without a relative increase in the volume of stocks being traded. To this effect, the major objective of this study is to examine the relevance of some of the established models that guide stock price movements in the Nigerian context. For this study, particular reference is placed on the banking sector, which dominates other sectors in terms of market capitalization and volume traded in the Nigerian Stock Exchange market. Data for this research were collected mainly from secondary sources such as audited annual reports of sampled banks, periodicals, various publications of Central Bank of Nigeria such as annual reports and statistical bulletins, Daily official lists and statistical year books of Nigerian Stock Exchange, different publications of Securities and Exchange Commission and Nigerian Deposit Insurance Corporation. The data set for the study consists of all the 23 pre-consolidation and 20 out of the 21 post-consolidation bank equity stocks quoted on the Nigerian Stock Exchange. Spring bank was not included because it has not published any financial statements after the bank consolidation exercise. The study covered an eight year period (2000-2007), pre and post bank consolidation periods. Three hypotheses were tested using the Capital Asset Pricing Model (CAPM) and Whitbeck-Kisor Model (WKM), multiple linear regression model, and Pearson product moment correlation coefficient. The findings of the study show that the application of the Capital Asset Pricing Model(CAPM) to Nigerian banking sector data indicate that 100 percent of the banking stocks were either undervalued or overvalued while zero percent were correctly valued. The application of the Whitbeck-Kisor Model (WKM) to Nigerian banking sector data shows that 4.4 percent of the banking stocks were correctly valued while the remaining 95.6 percent were either undervalued or overvalued. Hence none of the tested models guided the valuation and pricing of equity securities in the Nigerian Stock Exchange market from 2000-2007. There was no statistically significant relationship between the price-earnings ratio and the level of earnings growth, dividend payout ratio, and the variability of earnings of the sampled stocks in the Nigerian Stock Exchange market from 2000-2007.

9

TABLE OF CONTENTS Title fly i Title Page ii Approval iii Certification iv Dedication v Acknowledgements vi Abstract vii Table of contents viii CHAPTER ONE: INTRODUCTION

1.1 Background of Study 1 1.2 Statement of Problem 9 1.3 Objectives of Study 10 1.4 Research Questions 11 1.5 Statements of Research Hypotheses 11 1.6 Scope of Study 11 1.7 Significance of Study 12 1.8 Limitations of the Study 14 References 15 CHAPTER TWO: REVIEW OF RELATED LITERATURE 2.1Theoretical Concepts 19 2.1.1The Concept of Value 19 2.1.2 Approaches to common stocks valuation 22 2.1.2.1 The Discounted cash Flow (DCF) Valuation 22 2.1.2.2 Dividend Discount Model (DDM) 24 2.1.2.3 Free Cash Flow Discount Model (FCFDM) 27 2.1.2.4 Relative Valuation Approach 29 2.1.2.5 Earnings Multiplier (P/E ratio) Model 29 2.1.2.6 Price/Earnings to Growth Rate ratio (PEG) 30 2.1.2.7 Price/Book Value (PBV) 31 2.1.2.8 Price/Sales ratio (PSR) 31

2.1.2.9 Price/Cash Flow Multiple 31

2.1.2.10 Enterprise Value to Sales (EVS) ratio 31

2.1.2.11 EV/EBITDA (EVE) ratio 32

2.1.2.12 Subscription-member-based Valuation 32

2.1.2.13 Models for setting the offer price 32

2.1.2.14 Dividend based Value 32

2.1.2.15 Net Asset based Value 33

2.1.2.16 Relative Value 33

2.1.2.17 Net Book Value of Asset per share 33

2.1.2.18 Current Cost of Asset per share 34

2.1.2.19 Number of Years Purchase of Earnings 34

2.1.2.20 Price/Earnings Multiplier 34

10

2.1.2.21 Liquidation Value 35

2.1.2.22 Replacement Value 35

2.1.2.23 Stock price relative to Treasury bonds 35

2.1.2.24 Stock price relative to equity value per share 35

2.1.2.25 With Constant Growth Dividend Trend to Perpetuity 36

2.1.2.26 Using variable Dividend Model (for a definite period) 38

2.1.2.27 Non-Growth, Non-plough back, Constant Dividend 38

2.1.3 Sentiments that Affect Stock Value 39

2.1.3.1 Investors Preferences 39

2.1.3.2 Fundamental Analysis 40

2.1.3.3 Technical Analysis 40

2.1.3.4 Random Walk Hypothesis 40

2.1.3.5 Noise Trading 41

2.1.3.6 The Efficient Market Hypothesis 41

2.2 Survey of Related Studies 42

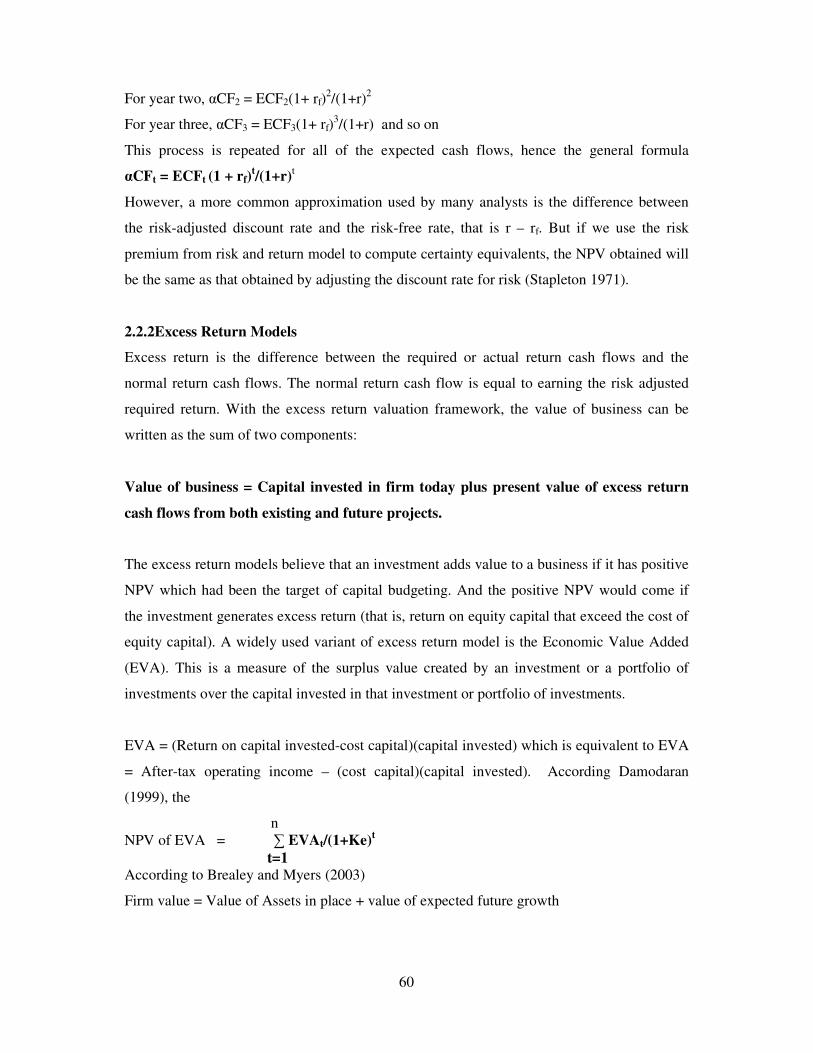

2.2.0 Earnings Models 47

2.2.1 Certainty Equivalent Models 48

2.2.2 Excess Return Models 49

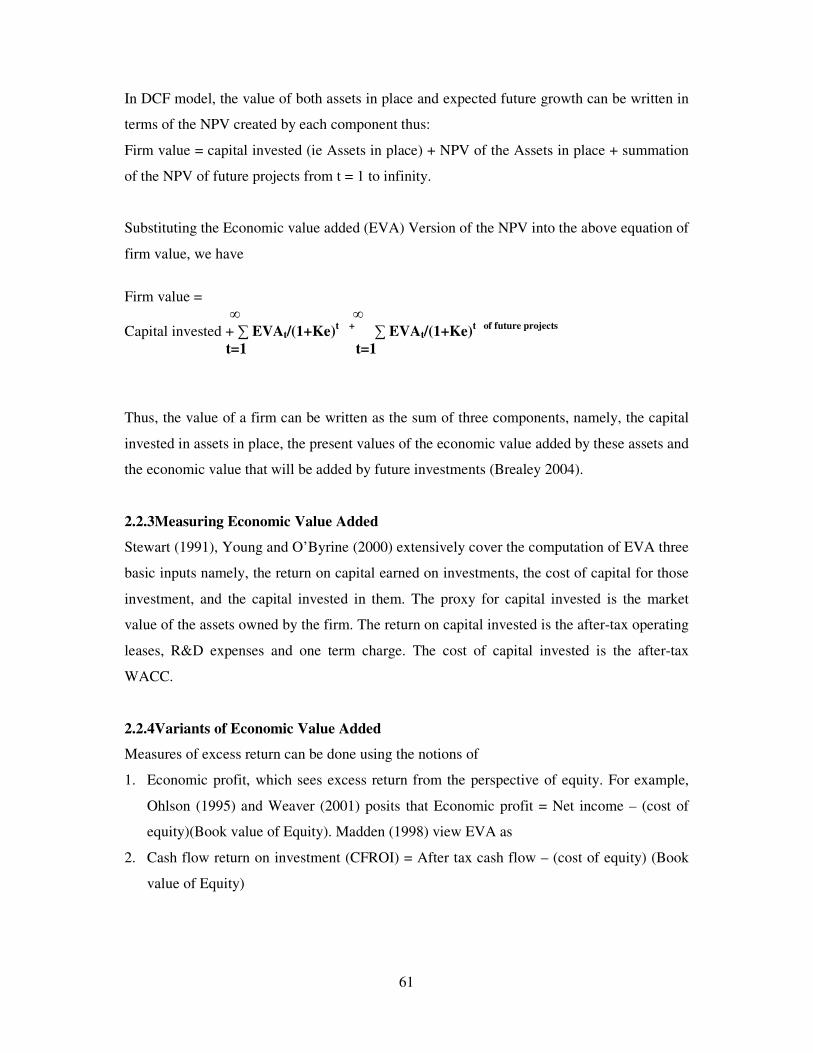

2.2.3 Measuring Economic Value Added 50

2.2.4 Variants of Economic Value Added 50

2.2.5 Adjusted Present Value (APV) Models 51

2.2.6 Variants of APV 53

2.2.7 Asset Based Valuation 53

2.2.8 Accounting Valuations 53

2.2.8.1 Book Value Based Valuation 53

2.2.8.2 Book Value plus Earnings Valuation Model 54

2.2.8.3 Fair Value Accounting 55

2.2.8.4 Liquidation Valuation 55

2.2.9 Relative Valuation 56

2.2.10 Determinants of Multiples 58

2.2.11 Comparable Firms 60

2.2.12 Valuation Based on P/E ratio: Determination of P/E ratio 63

2.2.13 Sector regressions 65

2.2.14 Market Regression 66

11

2.2.15 Estimation of Fundamentals 66

2.2.15.1 Estimation of beta coefficient 66

2.2.15.2 The CAPM 68

2.3 Conclusion 70

References 72

CHAPTER THREE: RESEARCH METHODOLOGY

3.0 Introduction 82 3.1Theoretical framework for the Study 82 3.2 Research Design 83 3.3 Nature and Sources of Data 84 3.4 Population and Sample 84 3.5 Valuation Methodology 85 3.6 Model specifications 86 3.6.1 Application of CAPM to Nigerian banking Industry Data 86 3.6.1.1 Estimating the Expected Rate of Return 86 3.6.1.2 Estimating the Risk-free Rate 86 3.6.1.3 Estimating the Beta Coefficient 87 3.6.1.4 Estimating the Market Return 87 3.6.1.5 Estimating the Actual Rates of Return of an Asset 88 3.6.1.6 Geometric Mean 89 3.6.1.7 Assessment of Level of Variation 90 3.6.2 Application of KWM to Nigerian Banking Industry Data 90 3.6.2.1 Estimating Normal P/E ratio 90 3.7 Summary 91 References 94 CHAPTER FOUR: DATA PRESENTATION AND ANALYSIS 4.0 Introduction 96 4.1 Data Presentation 96 4.2 Data Analysis 101 4.3 Test of Hypotheses 114 CHAPTER FIVE: SUMMARY OF FINDINGS, CONCLUSIONS AND RECOMMENDATIONS 5.0 Introduction 118 5.1 Summary of Findings 118 5.2 Conclusions 126 5.3 Recommendations 128 Appendix 130 Bibliography 186

12

CHAPTER ONE

INTRODUCTION

1.1 BACKGROUND OF STUDY

Research is an organized enquiry or investigation into any subject or area of interest with the

aim of providing information for solving identified problem(s). It can be a revision of

accepted theories or laws in the light of new facts or practical application of such new or

revised theories or laws. It can also be a collection of information about a particular subject.

Research is all about facts and logic. A research interest can come up from various sources

such as contemporary events, areas of further research as indicated in past researched works,

comments in journal articles, discussions, and assertions that are subject to validation.

Research interest can also be sparked off by phenomena characterized by controversy and

need investigation to find out more.

In finance, there is widespread agreement that the Capital Asset Pricing Model (CAPM) and

Whitbeck-Kisor Model (WKM) are good predictors of share price movements in stock

markets. While the above assertion had been empirically validated in several stock markets in

developed economies, there have been few such studies in the stock markets of developing

economies like Nigeria. Such studies have now become imperative given the recent

developments that have seen the Nigerian stock market capitalization increasing from N276,

111,743,197.30 on January 2, 1998 to N10, 180,292,984,225.00 on December 31, 2007

without a relative increase in the volume of stocks being traded. The fluctuations in stock

prices at times do not make economic sense given the economic reality of the companies.

Sometimes stock prices went ahead of what the underlying business would earn, just as

sometimes they fell below. The model that guides this cycle is quite hazy and there is need to

unravel the mystery surrounding the issue of share price movement.The mystery surrounding

share price movement can be captured in the following analysis.

A share of common stock represents a unit of ownership position in a company. The ordinary

shareholders are entitled to vote on important matters regarding the company, to vote on the

membership of the Board of Directors and receive dividends when declared. In the event of

13

liquidation of the firm, the ordinary shareholders will receive a pro-rata share of the assets

remaining after the creditors and preferred stockholders had been paid off. To invest on

common stock, there is need to ascertain its value abinitio. This leads us to the question, what

is the value of a share of a company?

This seemingly straight forward issue has been the source of endless difficulty and

controversy in finance. One answer is clear of course, which is that the value of a share is the

price it commands in the stock market. That is true enough, but not very satisfactory. Share

prices move around erratically often for no apparent reason.

The proponents of the Efficient Market Hypothesis (EMH), which was spearheaded by Fama

(1970), supported by Patell and Wolfson (1984), Seyhun (1986), Gosnell, Keown and

Pinkerton (1996), are of the view that share prices fully and fairly reflect all relevant

available information about the stock. They submit that the market efficiency can be weak,

semi-strong or strong. In its weak form, share prices reflect all past or historic information. In

its semi-strong form, share prices reflect all publicly available information including past

information. It is strong if share prices reflect all past, publicly and privately (insider)

available information. Wherever and whenever it is possible to use insider information (by

the privileged investors) before it becomes available to the market, to buy and sell shares and

make above normal profits, the market is deemed not to be an efficient one. Fama (1991)

asserts that under the weak form, future prices can be predicted using historical accounting

information or macroeconomic variables.

In a semi-strong efficient market, the share price of a company quickly responds to new

information relating to that company. The share prices quoted on the stock exchange are

therefore always-fair prices, reflecting all information about a company that is relevant to

buying and selling. The share price will factor in past company performance, expected

company performance, the quality of management team, the way the company might respond

to changes in the economic environment such as a rise in interest rate, inflation etc.

Another form of capital market efficiency is operational efficiency, which means that

transaction costs are low enough as to encourage investors to trade freely on shares. If a stock

market is operationally efficient, the timing of new issues of equity will be immaterial

because the price paid for the new equity will always be a fair one.

14

The EMH became controversial when some anomalies were detected in the behavior of stock

market prices as evidenced by a number of research findings. Rozett and Kinney (1976),

using stocks quoted on the New York Stock Exchange (NYSE), documented stocks prices for

the period 1904 – 1974 and discovered that on the average, the return for the month of

January was generally 3.48% higher than other months as compared to 0.42% for the other

months. Later studies carried out by Bhardwaj and Brooks (1992) for 1977 – 1986 periods,

Reinganum (1983) for the1961 – 1990 period, also identified the same market anomaly which

they have termed “January effect”. French (1980) analyzed the daily stocks returns for the

period 1953- 1977, and found that there is a tendency for returns to be negative on Mondays

whereas they were positive on other days of the week. He noted that these negative returns

were caused only by the weekend effect and not by a general closed market effect. Therefore,

he suggested that for a trading to be profitable in such situation, one should adopt the strategy

of buying stocks on Mondays and selling them on Friday. Agrawal and Tandon (1994) found

significantly negative returns on Monday in nine countries and on Tuesday in eight countries,

yet large and positive returns on Friday in 17 of the 18 countries studied, up to 1987.

Lakonishok and Maberly (1990) also documented the same effect. They termed this scenario

‘Weekend effect’ or Monday effect.

Cadsby and Ratner (1992) came up with evidence from USA, UK, France, and Japan to show

that stock returns are significantly higher at the last and first day of the month. Haugen and

Lakonishok (1989) assert that US stock returns are significantly higher on the last and first

three trading days of the month. Ariel (1987) found that stock returns were higher on the last

day of the month. They termed this scenario “turn of the month effect”.

Ariel (1987), Cadsby and Ratner (1992), and Brockman and Michayluk (1998) documented a

“pre-holiday effect” where, on the average, stock returns were higher the day before a

holiday than on other trading days.

Apart from the calendar effects, Banz (1981) supported by Reinganum (1983) in his analysis

of 1936–1975 period revealed that excess returns would have been earned by holding the

stocks of low capitalization companies otherwise called the “small size firms”. Reinganum

(1983) provided evidence that the risk adjusted annual return of small firms were greater than

15

20%. This is termed “small-size firm effect”. Fama and French (1995) found that market and

size factors in earnings help explain market and size factors in returns.

Basu (1977) opined that stocks of low P/E companies earned a premium for investors during

1957-1971 period and an investor who held the low P/E ratio portfolio earned higher returns

than an investor who held the entire sample of stocks. Dechow, Hutton and Sloan (1999)

documented that short-sellers position themselves in stocks of firms with low P/E ratios since

they are known to have commensurate future returns in terms of dividend income and price

appreciation.

Debondt and Thaler (1985,1987) presented evidence that is consistent with the fact that stock

prices overreact to changes in current earnings. They reported positive estimated abnormal

stock returns for portfolios that previously generated inferior earnings performance. This line

of thought generates “over/under reaction of stock prices to earnings announcement”.

Harris and Gurel (1986), Seyhun (1990) found a surprising increase in share prices (up to

3%) on the announcement of a stock’s inclusion into the Standard and Poor(S&P) 500 index

and this they called the “S&P index effect”.

The influence of phenomena such as snow, rain, sunshine, and cloudy weather which put

people in different moods, choices and judgements as discovered in NYSE (Hirshleifer and

Shumay 2001) created anomalies which cannot be explained within the existing paradigm of

EMH. Efficient Market Hypothesis (EMH) propounds that information is instantaneously

reflected in stock prices. This clearly suggested that information alone is not moving the

stock prices. Hirshleifer and Shumay (2001) found that stock market daily stock returns are

positively correlated with sunshine in almost all the 26 countries they analysed their data

from 1982-1997. This they have termed the “weather effect”

John Maynard Keynes (1936) views stock market as a “Casino” guided by “animal spirit” of

investors with short-run speculative motives, who are disinterested in assessing the present

value of future dividends or holding on investment for a significant period but rather

interested in estimating the short-run price movements. As a result, shareholders are

increasingly concerned with short term gains and have very short-term planning horizons.

EMH and Keynes have two extreme views of the stock market. EMH is flawed on the ground

that it is not guided by a complete knowledge of factors governing the decision. It fails to

16

provide a realistic framework for the formation of expectations, given the uncertainty factor.

Keynes is of the opinion that, to make a rational decision would involve knowledge of future

income flows, the appropriate discount rate, both of which are unknowable. And this creates

insufficient knowledge for one to make a forecast of investment yields. He submitted that the

future is uncertain and can never be determined, while EMH maintains that in the real world

the investors are only faced with risk and not uncertainty. To drive his point home, Keynes

came up with an analogy. In his analogy he likened the stock market to a beauty contest

where the goal of any investor is to pick the girl that others would consider prettiest rather

than choosing the one he/she thinks is prettiest. Hence the individual tends to conform to the

behaviour of the majority. And what may be irrational at the individual level now becomes

rational or the convention in Keynesian analysis.

The examination of share price movements with respect to the movements in the fundamental

variables, in order to ascertain the rationality of market behaviour is called the volatility tests.

The first two studies which applied these tests were those by Shiller (1981), LeRoy and

Porter (1981) and these spawned a series of articles. Shiller tested a model in which stock

prices are the present discounted value of future dividends. LeRoy and Porter (1981) used a

similar analysis for the bond market. These studies revealed significant volatility in both the

stock and bond markets. Shiller (1981) suggested that if fluctuations in actual prices are

greater than those implied by changes in the fundamental variables affecting the prices, the

difference would arise as a result of fads (i.e. waves of optimistic or pessimistic market

psychology). Schwert (1989) tested for relationship between volatility in stocks return and

economic activity. He found increased volatility in financial asset returns during recessions,

which would suggest that operating leverage tended to increase during recessions. He also

found increased volatility in period during which the proportion of new debt issues to new

equity issues was more than a firm’s long term existing financing mix. This may be

interpreted as evidence of financial leverage affecting volatility. These results of excess

volatility in the stock market have been confirmed by Cochrane (1991), West (1988),

Campbell and Shiller (1988), Mankiw, Romer and Shapiro (1985). However the tests have

been criticized, largely on methodological grounds by Marsh and Merton (1987).

Poterba and Summers (1988:23-26) posit that there are two types of investors in the market –

namely the rational speculators or arbitrageurs who trade on the basis of valid information

and noise traders who trade on the basis of imperfect information. Imperfect information

17

driven investors cause prices to deviate from their equilibrium, while arbitragers play the

crucial role of stabilizing prices by diluting such shifts in prices. They assert that perfect

arbitrage under EMH is unrealistic as a result of fundamental risk and unpredictable future

resale price. Given the limited arbitrage they argue that security prices do not merely respond

to information but also to changes in expectations or sentiments which are not fully justified

information. Investors’ trading strategies such as trend chasing, tracking possible indicators

of demand constitute “noise” rather than rational evaluation of information, make no sense if

prices respond only to fundamental news and not to investor demand. But they make perfect

sense in a world where investor sentiments move prices and so predicting changes in this

sentiment pays. Black (1986) argues that noise traders play a useful role in promoting

transactions and thus influencing prices and informed traders like to trade with noise traders

who provide liquidity. Therefore so long as risk is rewarded and there is limited arbitrage it is

unlikely that market forces would eliminate noise traders and maintain efficient prices.

On models of human behaviour that effect market behaviour, there were attempts to explain

the persistence of anomalies rooted in human and social psychology. On this note, it is a well

known fact that individuals have limited information processing capacity, exhibit systematic

bias in information processing, are prone to make mistakes, and rely on the opinion of others.

Kahneman and Tversky (1986) argue that when faced with the complex task of assigning

probabilities to uncertain outcomes individuals often tend to use cognitive heuristics, which

often lead to systematic biases. Rabin and Thaler (2001) show that the failure of expected

utility theory of risk aversion is due to its failure to recognize the psychological principles

underlining decision tasks. Shiller (1981) attributes the movements in stock prices to social

movements and suggests that the final opinion of individual investors may largely reflect the

opinion of a larger group. This type of “follow the crowd or social fads” approach is bound

to cause excessive volatility in the stock market, with very little rational or logical

explanation. Grinblatt and Keloharju (2001) assert that custom, language, and culture

influence stock trades.

Huberman and Regeve (2001) posit that how and not when information is released can cause

stock price reactions. They exemplify this with the news about a firm which developed a cure

for cancer. Although the news (information) had been published a few months earlier in

multiple media outlets, the stock price more than quadrupled the day after receiving public

18

attention in the New York Times. Although there was no new information presented, the

form in which it was presented caused a permanent price rise.

It is obvious that the EMH has stimulated a plethora of studies that looked among other

things, at the reaction of the stock market to the announcement of various events such as

earnings(Ball and Brown 1968), stock splits(Fama, Fisher, Jensen and Roll 1969), capital

expenditure(McConnell and Muscrella 1985), diverstitures (Klein 1986), and takeovers

(Jensen and Ruback 1983). The usefulness or relevance of the information was judged based

on the market activity associated with a particular event. Most of the EMH researches in the

seventies focused on predicting prices from past prices while those of the eighties and

nineties looked critically at the possibility of forecasting prices based on variables such as

dividend yield (Fama and French 1992), P/E ratios (Campbell and Shiller 1988), term

structure variables (Harvery 1991), and the inadequacies of the CAPM (Cutter et al 1989:

Haugen and Baker 1996). Researchers repeatedly challenged the studies based on EMH by

raising critical questions such as: Can the movement in stock prices be fully attributed to the

announcement of events? Do public announcements affect prices at all? And what could be

some other factors affecting price movements? Cutter, Poterba and Summers (1989) argue

that most price movements for individual stocks cannot be traced to public announcements.

Haugen and Baker (1996), in their analysis of determinants of returns in United States of

America, United Kingdom, Japan, France, and Germany conclude that none of the factors

related to sensitivities of macroeconomic variables seem to be important determinants of

expected stock returns.

The EMH contributed immensely to the understanding of the securities market but there are

growing discontentments with the hypothesis. Presently, the stock market is subject to waves

of optimistic and pessimistic sentiments even when no objective evidence exists for such

sentiment, and stock price movements are caused largely by changes in the perception of

ignorant speculators, tinted with a significant degree of order and coherence infused by the

institutional and social structures.

The Fundamentalists opine that the political developments in an economy, macro economic

indicators, assets markets and the financial news of the companies and the industries

determine why, when and where prices will move in the market. The political developments

include level of confidence in a nation’s government, the climate of stability and the level of

19

certainty in implementing policies and programs. Macroeconomic indicators include growth

rate as measured by GDP, interest rates, inflation, unemployment, money supply, foreign

exchange reserves and productivity, and the recall of borrowed money on margin account.

Asset market comprise of stocks, bonds and real estate. Financial news of the entity that

issued the security includes the history of past performances of the entity with respect to EPS,

DPS, capital appreciation etc. Trend is made from the past records upon which the likely

future trend in price per share is determined.

The Technicalists or Chartists believe on the examination of past price patterns/trends,

volumes, values, number of deals with charts and formulae to predict future price

movements, buying and selling opportunities and assessing the extent of market turnarounds.

It can be on intraday basis such as some minute’s intervals, hourly intervals. It could also be

on interday basis such as weekly, monthly, quarterly or yearly basis. Some tools used for

technical analysis include stochastic indicators, moving averages and ratios.

The Random Walk Hypothesis proponents opine that changes in share price occurs at random

and there is no relationship between past share prices and future share prices. That past share

price contains no information about the direction of future share price and the information on

new share price appears in random fashion.

In equity valuation, there are many approaches. There are the asset based valuation

approaches and income based valuation approaches. The asset based valuation approach is

based on the principle of substitution in the sense that no rational investor will pay more for

the business assets than the cost of procuring the assets of similar economic utility. The

market approach is rooted in the economic principle of competition in the sense that in a free

market, the supply and demand forces will drive the price of business assets to certain

equilibrium.

Tuller (1990) noted that everyone has his own theory about the most equitable and accurate

method of valuation, and that each business interest naturally tends to favour the valuation

method that best suits his own self-interests. He says that finance companies value a business

at what the assets will bring at liquidation auction. Investment bankers and venture capitalists

interested in rapid appreciation and high returns on their investment, value a business at

discounted future cash flow. He argues that the value of assets might be interesting to know,

20

but hardly anyone buys a business only for its balance sheet assets. The whole purpose is to

make money, and most buyers feel that they should be able to generate at least as much cash

in the future as the business yielded in the past. Based on this perception, many buyers view

DCF method as the most relevant of all valuation methods for it tells them what the business

has historically provided to its owners in terms of cash. This method typically takes financial

data from the company’s previous 3 years in drawing its conclusions.

Johansen (2000) submits that balance sheet based valuations are most often employed when

the business under examination generates most of its earnings from its assets. In this case the

balance sheet method highly favoured is the Current-market-value-adjusted assets values as

listed on the balance sheet on historical cost levels. The quest to unravel the mystery

surrounding share price movement in the stock market in Nigeria sparked off the interest to

research on the valuation and pricing of securities in a developing economy like ours, with

special interest on banking stocks.

1.2 STATEMENT OF THE PROBLEM

There seems to be no clear-cut method of fixing share prices in the Nigerian stock exchange.

The appropriate valuation and pricing of securities have remained problematic in Nigerian

stock market especially with respect to bank shares. Banks, as we know, are the major

financier of other sectors and hence banking stock prices should influence the price of stocks

in other sectors. According to Damodaran (2006), valuation is at the heart of what we do in

finance. In corporate finance, we consider how best to increase firm value by changing its

investment, financing and dividend decisions. In portfolio management, we expend resources

trying to find firms that trade at less than their true value and then hope to generate profits as

prices converge on true value. In studying whether markets are efficient, we analyze whether

market prices deviate from true value, and if so, how quickly they revert to true value.

Valuation is important not only from the perspective of corporate management but also from

the viewpoints of investors, the regulatory authorities and the Government. For an investor, it

represents a pivotal area around which sensible investment and financing decisions revolve.

The profitability of trading on financial instruments depends on proper valuation. Therefore

when deciding on the investment structure of an investor, valuation has to be assigned due

consideration. In Nigeria, many investors were enticed into investment in shares as they saw

others getting rich through investment in shares. This of course created higher share prices.

This process continued until economic reality was left far behind. At some point, the bubble

21

bursted and stock prices fall, and vice versa. The astronomical stock prices at times do not

make economic sense given the economic reality of the companies. Sometimes stock prices

get ahead of what the underlying businesses will earn, just as sometimes they fall below.

The proponents of the Efficient Market Hypothesis (EMH), which was spearheaded by Fama

(1970), supported by Patell and Wolfson(1984), Seyhun(1986), Gosnell, Keown and

Pinkerton(1996), are of the view that share prices fully and fairly reflect all relevant available

information about the stock. However the problem was that EMH became controversial when

some anomalies were detected in the stock market (Rozett and Kinney (1976); Bhardwaj and

Brooks (1992): Reinganum (1983); Agrawal and Tandon (1994); Lakonishok and Maberly

(1990); Cadsby and Ratner (1992); Haugen and Lakonishok (1989); Ariel (1987); Cadsby

and Ratner (1992), and Brockman and Michayluk (1998); Banz (1981); Hirshleifer and

Shumay (2001); John Maynard Keynes (1936); etc

Many prior empirical researches have posited that stock prices should be fixed based on

either earnings or net assets value or some combination of the two Damodaran (2006),

Buchanam (2000), Medaglia (1999), Slee (1999), Tuller (1990), Yegge (1996), and Johansen

(2000); etc. In the Nigerian case the method of fixing equity share prices in the secondary

arm of the capital market is not quit clear. A much more pertinent issue, however, is that

most of the earlier research works on these models were focused on firms listed on developed

stock markets. Not much has been done to establish the model that guides share pricing in

emerging stock market setting, especially in Nigeria. And given the apparent difference

between the developed market economies and the emerging market economics, the impact of

these models on share valuation is likely to vary. Therefore the main challenge of this study

is to investigate the model that best explains the price movement in the Nigerian stock

exchange.

1.3 OBJECTIVES OF THE STUDY

In finance, there is widespread agreement that the Capital Asset Pricing Model (CAPM) and

Whitbeck-Kisor Model (WKM) are good predictors of share price movements in stock

markets. While the above assertion had been empirically validated in several stock markets in

developed economies, there have been few such studies in the stock markets of developing

economies like Nigeria. Such studies have now become imperative given the recent

22

developments that have seen the Nigerian stock market capitalization increasing from

N276,111,743,197.30 on January 2, 1998 to N10,180,292,984,225.00 on December 31, 2007

without a relative increase in the volume of stocks being traded. To this effect, the major

objective of this study is to examine the relevance of some of the established models that

guide stock price movements in the Nigerian context. For this study, particular reference was

placed on the banking sector. In achieving this, the following specific objectives were

addressed.

1. To apply the Capital Asset Pricing Model (CAPM) to the Nigerian banking sector data

and from the results infer whether banking stocks were correctly priced, underpriced or

overpriced as at the time of the forecast.

2. To apply the Whitbeck-Kisor Model (WKM) to the Nigerian banking sector data and

from the results infer whether banking stocks were correctly priced, underpriced or

overpriced as at the time of the forecast

3. To identify from the two established valuation models the one that better describes the

price movement of banking stocks in Nigerian Stock Exchange market.

1.4 RESEARCH QUESTIONS

In addressing these objectives, the study seeks to answer the following questions:

1. From the perspective of the Capital Asset Pricing Model (CAPM), are the subject-banks

stocks correctly valued, undervalued, or overvalued by the market?

2. From the perspective of the Whitbeck-Kisor Model (WKM), are the subject-banks

stocks correctly price, underpriced, or overpriced by the market?

3. Which of the valuation models better explains the price movement of the subject-banks’

stocks in the Nigerian stock exchange?

1.5 STATEMENT OF RESEARCH HYPOTHESIS

To achieve the above objectives, following propositions were formulated in null hypotheses

for the study.

HO1: From the perspective of the Capital Asset Pricing Model (CAPM), the subject-banks

stocks were not correctly valued.

HO2: From the perspective of the Whitbeck-Kisor Model (WKM), the subject-banks stocks

were not correctly valued.

HO3: None of the valuation models guides the valuation and pricing of ordinary shares of the

subject-banks in the Nigerian stock exchange.

23

1.6 SCOPE OF THE STUDY

Companies quoted on the Nigerian stock market are segregated into many sectors but the area

of interest to the researcher is the banking sector. The decision to research only on banking

stocks is informed by the fact that banks are the major financier of other sectors and hence

banking stock prices should influence the price of stocks in other sectors. The banking sector

also dominates other sectors in terms of market capitalization and volume of equity traded in

the market. Therefore, the findings and conclusions to be derived from this work were as

related to the banking stocks in Nigeria. The study covers the period of eight years (2000-

2007), comprising 96 months. This period was selected to cover both the pre and post

consolidation era in the banking sector in Nigeria. The study covers only banking stocks

pricing in the secondary arm of the Nigerian stock market.

In line with the objective of the study, data from the Nigerian stock exchange was collected

and utilized to validate the existence of a relationship between banking stock price movement

and the models under study in an emerging market setting. In doing this, daily official price

lists of the exchange and the annual reports of the banks were collected over the period,

January 2000 to December 2007. Only banks listed on the exchange between years 2000 to

2007 and remained listed up to 2007 were selected for this study. This period was selected for

our study because it was a relatively stable period in Nigeria as it was fairly free from major

political factors that could upturn the capital market so adversely.

1.7 SIGNIFICANCE OF THE STUDY

The relevance of valuation can be capture in the work of Damodaran (2006) who concludes

that valuation is at the heart of what we do in finance. For example, in order to know whether

there is increase in firm value due to its investment and financing decisions, valuation of the

firm is necessary. To identify and buy stocks that trade at less than their true value so that the

investor can make profit when the prices converge on true value, valuation of the firm is

necessary. Valuation is also necessary when there is need to investigate whether market

prices deviate from true value, and if so, how quickly they revert to true value, in order to

ascertain the level of efficiency of the stock market; when a private company wishes to go

24

public by obtaining a stock exchange quotation; when some companies have a proposal for

merger or takeover; and when there is need to have a basis for levying relevant taxes, for

instance, capital gains tax, capital transfer tax, stamp duty, etc

Again, prior empirical studies generally focused on firms listed on developed stock markets,

with only very little done on emerging markets, especially the Nigerian stock market.

Besides, there are not many published evidence of empirical studies on the Nigerian stock

exchange that have vigorously tested the relationship between the stock price movement and

the models under study. However, with the clear differences in market microstructure,

information communication technology development, and other control environment in

Nigeria on one hand, and the developed markets on the other hand, the relationship between

the stock price movement and the models is likely to vary. Therefore there is need to

empirically test the relevance of the models on stock pricing in the Nigerian Stock exchange,

given its peculiarities. Furthermore, because of the divergent empirical results of the earlier

studies, it is important to investigate how best the models describe the stock price movement

in Nigeria in order to validate the existence of any relationship between the models and the

stock pricing in Nigeria.

Valuation is important not only from the perspective of corporate management but also from

the viewpoints of the operators in the stock market. Therefore, it is expected that the findings

of our study should assist operators in the Nigerian stock exchange in their investment

decisions. More importantly, it should be useful in guiding policy makers at the exchange to

formulate policies on equity share pricing so as to restore investors confidence in the market.

When the investors’ confidence is restored, trading activities can increase. Certainly, with an

increased trading volume at the exchange, the overall gross domestic product of the nation is

bound to increase, as more income will be generated by the investors. For an investor, it

represents a pivotal area around which sensible investment and financing decisions revolve.

The profitability of trading on financial instruments depends on proper valuation. Therefore

when deciding on the investment structure of an investor, the findings from this study

become helpful to the investor. When deciding on which stock to transact in order to have a

justifiable reward valuation is needful. This work will bring to light and remind potential

investors the valuation status of the Nigerian banking stocks. This knowledge will help them

to make informed investment and financing decisions that can enhance their investment

value, which is a sure way to wealth creation and poverty eradication.

25

This study will undoubtedly provide a basis upon which other researchers in the capital

market issues can explore other sectors of the market.

1.8 LIMITATIONS OF THE STUDY

One major limitation of this study is the unavailability of complete data for 2008 and 2009.

The inclusion of the two years data would have made the work a more recent study and

perhaps would have generated a better result. Another limitation that caused the delay in

finishing this work has to do with the difficulties encountered in the course of collection of

the required data from the Nigerian stock exchange and the company registrars of the banks.

It is surprising to know that majority of the company registrars do not keep proper custody of

the annual reports of the banks and other companies under their care. This made it impossible

for the researcher to collect all the annual reports in one visit. Likewise, the Nigerian stock

exchange. The Nigerian stock exchange has incomplete records when it comes to the annual

reports of listed companies. These many visits to the various registrars and the Nigerian stock

exchange posed a serious problem and challenge in that our purse had to be stretched beyond

measure to pay for the data required for the research.

26

References

Agrawal, A. and Tandon, K. (1994), “Anomalies or Illusions? Evidence from Stock Markets in Eighteen Countries”, Journal of International Money and Finance, Vol.13, 83-106. Ariel, R. A. (1987), “A monthly Effect in Stock Return”, Journal of Financial Economics, Vol.18, 161-174. Ball, R. J. and Brown, P. (1968), ‘An Empirical Evaluation of Accounting Income Numbers’ Journal of Accounting Research, vol.16, 159-178. Banz, R. (1981), “The Relationship between Return and Market Value of Common Stock,” Journal of Financial Economics, March, 3 – 18. Basu, S. (1977), “Investment Performance of Common Stocks in Relation to their Price- Earnings Ratios: A Test of the Efficient Market Hypothesis,” Journal of Finance 32, 663-82. Bhardwaj, R.K., and Brooks, L.D. (1992) “The January Anomaly: Effects of Low Share Price Transaction costs and bid-ask Bias.” Journal of Finance 47 January, 553-575. Black F. (1986), ‘Noise’ Journal of Finance, Vol.41, 529-543. Brennan, M.J.and Subvahmanya, A. (1995), “Investment Analysis and Adjustment of Stock Prices to Common Information”, Review Financial Studies, Vol.6, 799-824. Brockman, P. and Michayluk, D. (1998) “The Persistent Holiday Effective: Additional Evidence, Applied Economic Letters 5, 205-209.

Buchanam, D. (2000), ‘Business Valuators Must Dig Behind the Hype’ Washington Business Journal, September 15. Cadsby, B. and Ratner, M. (1992), ‘Turn of the Month and Pre-holiday Effect on Stock Returns: Some International Evidence’ Journal of Banking and Finance 16, 497-509. Campbell, J.Y. and Shiller, R.J. (1988), ‘Cointegration and Tests of Present Value Models’ Journal of Political Economy Vol.95, 1062- 1088. Cochrance, J.H. (1991) “Volatility Tests and Efficient Market: A Review Essay”, Journal of Monetary Economics Vol.27, 463-485. Cutler, D.M.; Poterba, M. and Summers, L.H. (1989), ‘What moves stock prices’ Journal of Portfolio Management, Vol. 15, 4-12. Damodaran, A. (2006), ‘Damodaran on valuation’ 2ed, York, John Wiley & sons.

27

DeBondt, W. F. and Thaler, R. H. (1985), “Does the Stock Market Overreact”. Journal of Finance, July 793-805. DeBondt, W. F. and Thaler, R. H. (1987), “Further Evidence of Investor Overreaction and Stock-Market Seasonality”Journal of Finance,42, 557-81. DeBondt, W.E.M. and Thaler, R. H. (1987) “Further Evidence on Investor Overreaction and Stock Market Seasonality”, Journal of Finance, Vol.47, 427-465. Dechow, P. M.; Hutton, A. P.; Sloan R. G. (1999), “An Empirical Assessment of the Residual Income Valuation model” Journal of Accounting and Economics vol.26, 1-34. Fama, E.F. (1965), “The Behavour of Stock Market Prices,” Journal of Business 38, 34-105. Fama, E.F. (1970), ‘Efficient Capital Markets: A Review of Theory and Empirical Work,” Journal of Finance 25 (May 1970): 383 417. Fama, E. F. (1991) “Efficient Capital Markets: II Journal of Finance December, 1575-1617. Fama, E. F. (1991), “Stock Returns, Real Activity, Inflation and Money,” American Economic Review 71, No.2, June, 545-565. Fama, E. F and French, K. R. (1995), ‘Size and book-to-market factors in earnings and returns’ Journal of Finance, Vol. 50, 131-155. Fama, E. F. and French, K. R. (1992), ‘The cross-Section of Expected Returns’ Journal Of Finance Vol. 47, 427 – 466. Fama, E. F.; Fisher L.; Jensen M. and Roll R. (1969),“The Adjustment of stock prices to new Information”International Economic Review, Vol.10, No.1(February), 1-21. French, K. R. (1980), “Risk, Return and Equilibrium”, Journal of Political Economy 79 (January/February 1971): 30-55. Gordon, M. J. (1962) “The Savings, Investment and Valuation of a Corporation”, Review of Economics and Statistics, vol.10, p. 37. Gosnell, T.F.; Keown, A. J.; Pinkerton, J.M. (1996), ‘The Intraday Speed of Stock Price Adjustment to Major Dividend Changes: Bid- Ask Bounce and Order Flow Imbalances’ Journal of Banking and Finance, Vol.20, 247-266. Grinblatt, M. and Keloharju, M. (2001), ‘How Distance, Language, and Culture Influence Stockholdings and Trades’ Journal of Finance, Vol. 56, 1053-1073. Haris, L. and Gurel, H. (1986), ‘Price and Volume Effects Associated with Changes in the S&P 500 List: New Evidence for the existence of Price Pressure’ Journal of Finance, Vol.41, 815-829. Harvey, C.R. (1991), ‘The World Price of Covariance Risk’ Journal of Finance, vol.46, 815-829.

28

Hirshleifer, D. and Shumway, T. (2001), ‘Good Day Sunshine: Stock Returns and the Wealth’ Journal of Finance SSRN Working Paper. Huberman and Regeve (2001), ‘Contagious Speculation and a Cure for Caneer: A nonevent that made stock prices soar’, Journal of Finance, vol.56, 387-396. Jensen, M. and Ruback R.S. (1983), ‘The Market Corporate Control: The Scientific Evidence’ Journal of Financial Economics, Vol.11, 5-50. Johansen, J. A. (2000), ‘How to buy or sell a business’, Small Business Administration. Kahneman, D. and Tvversky, A. (1986), ‘Choices, Values, and Frames’ American Psychologist, 341-350. Keynes, J. M. (1936), “The General Theory of Employment’, London, Macmillan. Klein, A. (1986), ‘The Timing and Substance of Divestiture announcements: Individual, Simultaneous and Cumulative Effects’ Journal of Finance, vol.41, 685-696. Lakonishok, J. and Edwin, M. (1990), “The Weekend Effect: Trading Patterns of Individual and Institutional Investors”, Journal of Finance 45, March, 231-243. LeRoy, S.F. and Porter, R.D. (1981), “The Present Value relation: Tests based or Implied variance bonds’ Econometrica, Vol.49, 555-574. Mankiv, N. G.; Romer, D.; Shapiro, M. D. (1985), ‘An Unbiased reexamination of Stock Market Volatility’ Journal of Finance, vol. 40, 677-687. Marsh, T.A. and Merton R.C. (1987), “Dividend Behaviour for aggregate Stock Markets”, Journal of Business, Vol.60, 1-40. McConnell, J. J. and Muscarella, C. J. (1985), “Corporate Capital expenditure decisions and the market Value of the Firm” Journal of Financial Economics, Vol.14, 399-422. Patell, J. and Wolfson, M. (1984), ‘The Intraday Speed of Adjustment of Stock Prices to Earnings and Dividend Announcements’ Journal of Financial Economics, Vol.13, 223-252. Rabin, M. and Thaler, R. H. (2001), Anomalies: Risk Aversion’ Journal of Economic Perspectives, vol.15, 219-232. Reinganum, M. R. (1983), ‘Portfolio Strategies for Small Caps Vs Large’, Journal of Portfolio Management. Winter 29-36. Rosett, M. S. and Kinney, W. R. (1976), “Capital Market Seasonality: The Case of Stock Returns” Journal of Financial Economics 3, 378-402. Schwert, G.W. (1989), “Why Does Stock Volatility Change Over Time?” Journal of Finance, Vol-44, No.5 (December), 1115-1153.

29

Seyhun, N. (1990), ‘Overreaction of Fundamentals: Some Lessons from Insiders Response to the market Crash of 1987’Journal of Finance, Vol.45, 1363-1388. Seyhun, N. (1986), ‘Insiders’ Profits, Cost of Trading and market Efficient’ Journal of Financial Economics, Vol.16, 189-212. Shiller, R. J. (1981), “Do Stock Prices Move Too Much to be Justified by Subsequent Change in Dividend”, American Economic Review, Vol.71, 421-436. Slee, R. (1999), ‘How Much is Your Small Business Worth to a Roll-Up? Triangle Business Journal, August 20. Tuller, L. W. (1990), ‘Getting Out: A Step-by step Guide to Selling a Business or Professional Practice, Liberty Hall. . West, K. D. (1988), ‘Dividend Innovations and Stock Price Volatility’ Econometrica, Vol.56, 37-61. Yegge, W. M. (1996), ‘A Basic Guide to Buying and Selling a company, John Wiley.

30

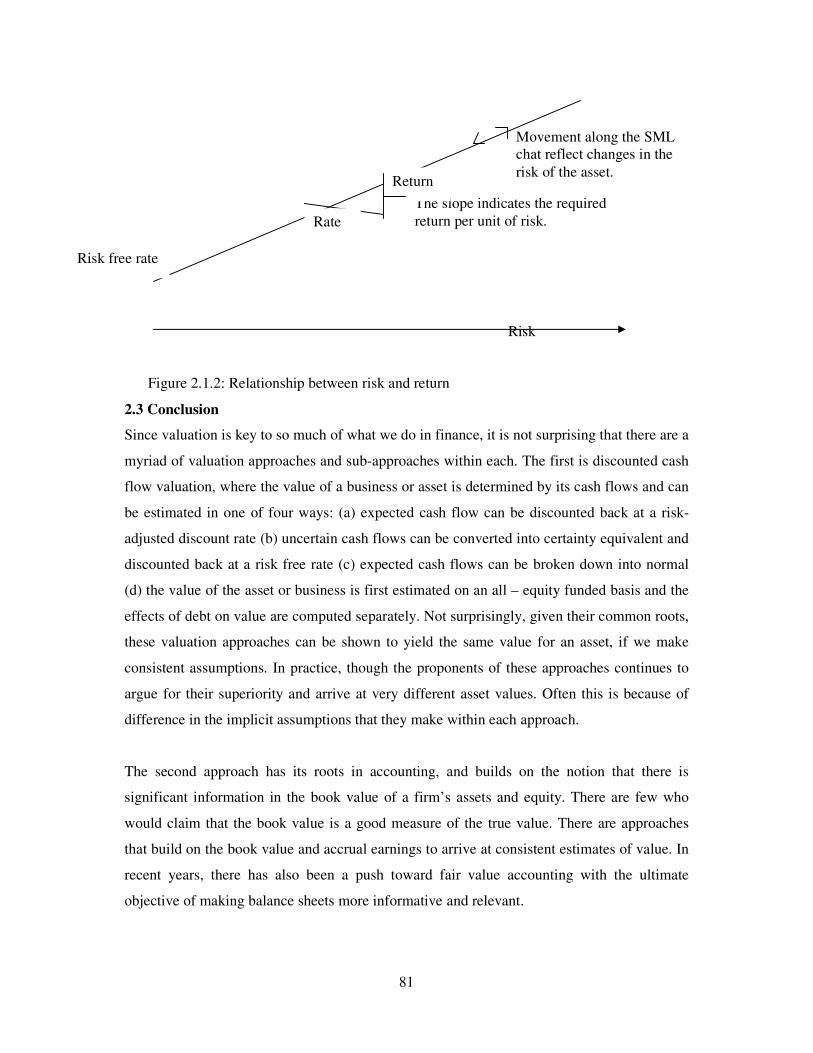

CHAPTER TWO

REVIEW OF RELATED LITERATURE

2.1THEORITICAL CONCEPTS

2.1.1The Concept of Value

Valuation is a process and a set of procedures used to estimate the economic value of an asset

or liability. Valuation lies at the heart of much of what we do in finance, be it market

efficiency, corporate governance, merger and acquisition transactions, financial reporting,

taxable events to determine the proper tax liability, litigations, wills and estates, divorce

settlements, business analysis or comparison of different investment analysis, decision rules

in capital budgeting. It is used by financial market participants to determine the price they are

willing to pay or receive to consummate a sale of an asset or a business. There are many

concepts of value.

For example, the transaction value of a firm is the market value of the firm equity plus the

market value of the firm preferred stock plus the value of the firm debt plus the transaction

fees, minus the cash balances and market securities, all these measured at the close of

transaction (Kaplan and Ruback, 1995).The value of an asset is the price that a

knowledgeable and willing buyer pays to a knowledgeable and willing seller. Book value is

the asset historical cost less its accumulated depreciation. Market value is the price of an asset

as determined in a competitive market place. Intrinsic value is the present value of the

expected future cash flows discounted at the decision maker’s required rate of return. The

result of a value calculation under the income approach is generally the fair market value of

the subject company since the entire benefit stream of the subject company is more often

valued. Valuation is the first step towards intelligent investing. Before an intelligent investor

sets out to buy or sell stocks, he should have had an idea of what value the stock should

command.

In the case of a share of common stock which represents a unit of ownership position in a

company, the ordinary shareholders have entitlements to receive dividends, which constitute

cash flows to them. There is value attached to each unit. In the event of liquidation of the

31

firm, the ordinary shareholders will receive a pro-rata share of the assets remaining after the

creditors and preferred stockholders had been paid off. For equitable sharing of the assets

there is need for proper valuation. In stock investments, stock valuation models are designed

to identify undervalued and overvalued securities (Akintola-Bello, 2004:177). They indicate

which sector seem relatively attractive or unattractive and should therefore be bought or sold

as the case may be. An undervalued security is one whose price is judged to be less than it

would be if investors had the same perception of the company as that produced by the use of

the valuation model. Conversely, an overvalued security is one whose market price is greater

than it would be if all investors had the same perception of the company as that provided by

the model and noncyclical business. To invest on common stock, there is need to ascertain its

value abinitio. This leads us to the question ‘What is the value of a share of a company?

This innocent-seeming question is a source of endless difficulty and controversy in finance.

One answer is clear, of course. The value of a share is the price it commands in the stock

market. That is true enough, but not very satisfying. Economic principles and common sense

suggest that two basic components namely income flow to shareholders through dividends

and capital appreciation and the rate of return should be the motive forces propelling share

price. However, investors do not know what those income flows would be year by year from

now until the end of time. Had it been they would know, they would simply discount each to

its present value and add up the series infinitely to get the share value. Nevertheless, the

world is more complicated than this. Therefore, the first component of valuation calls for an

income flow forecast of which a scope of error and disagreement is already vast. At times not

all earning will be paid out as dividends immediately. A growing number of firms do not pay

dividends at all. In this case a more plausible measure of income flow becomes the earnings,

that is, the profit. The value of the firm can still be expected to grow due to reinvestment of

retained earnings. This growth, in turn, will be reflected in a rising share price. So one can

think of earnings yield (E/P) as the engine that drives both dividends and capital gains, the

two forms in which shareholders receive most of their income from shares.

The earnings measures of value have been faulted on the ground that earnings is an

accountant’s concept and a clever finance man can make a company’s earnings come out at

whatever he likes. Consequently, they prefer measures less prone to manipulation, such as

sales or cash flow, which comes in various shapes and sizes. Still others prefer to look at the

32

value of a firm’s net assets. None of these measures is perfect. The best course may be to

weigh all of them.

Shareholders are entitled to a share of all dividends in perpetuity. Even if the company’s

stock does not currently have a dividend yield, chances are that at some point in the future

there could be some sort of dividend. A company can repurchase its own shares using its

excess cash, rather than paying out dividends to shareholder. This effectively drives up the

stock price by providing a buyer as well as improving EPS by decreasing the number of

shares outstanding. Mature, cash flow positive companies tend to be much more liberal with

share repurchase as opposed to dividends simply because dividends to shareholders are taxed

twice.

In equity valuation, there are many approaches. There are the asset based valuation

approaches and income based valuation approaches. The asset based valuation approach is

based on the principle of substitution in the sense that no rational investor will pay more for

the business assets than the cost of procuring the assets of similar economic utility. The

market approach is rooted in the economic principle of competition in the sense that in a free

market, the supply and demand forces will drive the price of business assets to certain

equilibrium.

Tuller (1990) noted that everyone has his own theory about the most equitable and accurate

method of valuation, and that each business interest naturally tends to favour the valuation

method that best suits his own self-interests. He says that finance companies value a business

at what the assets will bring at liquidation auction. Investment bankers and venture capitalists

interested in rapid appreciation and high returns on their investment, value a business at

discounted future cash flow. He argues that the value of assets might be interesting to know,

but hardly anyone buys a business only for its balance sheet assets. The whole purpose is to

make money, and most buyers feel that they should be able to generate at least as much cash

in the future as the business yielded in the past. Based on this perception, many buyers view

DCF method as the most relevant of all valuation methods for it tells them what the business

has historically provided to its owners in terms of cash. This method typically takes financial

data from the company’s previous 3 years in drawing its conclusions.

33

Johansen (2000) submits that balance sheet based valuations are most often employed when

the business under examination generates most of its earnings from its assets. In this case, the

balance sheet method highly favoured is the Current-market-value-adjusted assets values as

listed on the balance sheet on historical cost levels

2.1.2 Approaches to Common Stocks Valuation

Traditionally, an enterprise can be valued based on either its earnings or its net assets value or

some combination of the two. In equity valuation, various techniques, assembled under two

major approaches have been devised over time (Damodaran 2006; Buchanam 2000; Medaglia

1999; Slee 1999; Tuller 1990; Yegge 1996; and Johansen 2000). The approaches are (1) the

Discounted Cash Flow valuation techniques, where the value of the stock is estimated based

upon the present value of some measure of cash flow, which can be dividends, operating

(firm) free cash flow, or the equity free cash flow; and (2) the relative valuation techniques,

where the value of stock is estimated based upon its current price relative to variables

considered to be significant to valuation, such as earnings, cash flow, book value, or sales.

Hence, approaches to equity valuation can taken any of two forms:

1 2

Discounted Cash Flow Techniques Relative Valuation Techniques

-Present Value of Dividends -Price/Earnings (P/E) ratio

-Present Value of Firm Free Cash Flow -Price/Cash Flow (P/CF) ratio

-Present Value of Equity Free Cash Flow -Price/Book Value (P/BV) ratio

-Price/Sales (P/S) ratio

Most analysts may be aware of these techniques and their inputs but what makes a superior

analyst is the acceptance level of the estimates of the inputs such as the growth rate of the

variables (dividends, earnings, cash flow, or sales), the discount rate and the determination of

the values of the variables. The basic valuation techniques under each approach are hereunder

discussed.

2.1.2.1The Discounted Cash Flow (DCF) Valuation Approach

Following the stock market crash of 1929 in the United States of America (USA) investors

became wary of relying on reported earnings or any measure of value apart from cash. This is

because tangible assets value gradually became less well correlated with the total value of the

company as determined by the stock market. That is, the tangible assets value was dropping

34

towards less than one-fifth of the total corporate value, which means that intangible assets

such as customer relationships, patents, proprietary business models, channels, etc, are the

remaining four-fifth. As a result of this situation, Burr- Williams (1938) in his text on ‘The

Theory of Investment value’ became the first to articulate the DCF as a valuation method for

stocks/financial assets, projects or company using the concept of time value of money.

Though, Fisher (1930) in his text on “The Theory of interest” also expressed the DCF method

in modern economic terms but not related to stock’s valuation. The first book to explicitly

connect the present value concept with dividends was The Theory of Investment Value by

Burr -Williams (1938) where he states that ‘A stock is worth the present value of all the

dividends ever to be paid upon it, no more, no less…. Present earnings, outlook, financial

condition, and capitalization should bear upon the price of a stock only as they assist buyers

and sellers in estimating future dividends’. Graham (1934) used a series of screening

measures that include low PE, high dividend yields, reasonable growth and low risk that

highlighted stocks that would be undervalued using a dividend discount model.

In the second half of 19th century, the growth of railroads in the US called for new tools to

analyze long-term investments with significant cash outflows and cash inflows later. A civil

engineer, Wellington (1887) notes the importance of time value of money and argued that the

present value of future cash flows should be compared to the cost of up-front investment. He

was followed by a Southern Bell engineer, Pennell (1914), who developed present value

equations for annuities, to examine whether to install new machinery or retain old equipment.

He says that the DCF is what amount someone is willing to pay today in order to receive the

anticipated cash flows of future periods. Bohm-Bawerk (1903) provided an explicit example

of present value calculations using the example of a house purchase with twenty annual

installments payments.

Fisher (1907 & 1930) suggested four alternative approaches for analyzing investments, which

he claimed would yield the same results. He argued that when confronted with multiple

investments, one should pick the investment (a) that has the highest present value at the

market interest rate; (b) where the present value of the benefits exceeded the present value of

the costs the most: (c) with the ‘rate of return on sacrifice’ that most exceeds the market

interest rate or (d) that, when compared to the next most costly investment, yields a rate of

return over cost that exceeds that market interest rate. The first two approaches represent the

35

NPV rule, the third is a variant of the IRR approach and the last is the marginal rate of return

approach.

All the views expressed above describe the DCF models, which is also called the absolute

value models. The absolute value models determine the value of a firm based on all its

expected future cash flows discounted to the present value. The discount is based on an

opportunity cost of capital, which is sometimes called a discount rate, and is expressed as a

percentage. The DCF gained popularity as a valuation method for stocks after the 1929 stock

market crash. It is considered a strong tool because it concentrates on cash generation

potential of a business.

There are four variants of DCF models in practice, and theorists have long argued about the

advantages and disadvantages of each. In the first place, the equity free cash flows on an

asset(or business) are discounted at a required rate of return to arrive at the value of the asset.

In the second place, the expected equity free cash flows are first adjusted for risk to arrive at

risk-adjusted to certainty-equivalent cash flows, which are then discounted at the risk-free

rate, to estimate the value of a risky asset. In the third place, is the Adjusted Present Value

(APV), where a business is valued first without the effects of debt using the firm free cash

flows and later consider the marginal effected of borrowed money on the firm value. Finally,

we can value a business as a function of the excess returns (ie economic value added) we

expect it to generate on its investments. The various useable cash flows are

1. Equity free cash flows (ECF) discounted at cost of equity

2. Certainty-equivalent-equity free cash flows (CEFCF) discounted at risk-free rate;

3. Firm free cash flows (FFCF) discounted at the WACC before tax (ie the adjusted

present value approach)

4. Excess returns (ie economic profit) discounted at the required return to equity;

In all these, we have the equity – approach and the entity – approach. The equity-approach

uses flows to equity while the entity – approach uses total firm free cash flows that accrue to

both debt and equity holders.

2.1.2.2Dividend Discount Model (DDM)

According to Terry and Keith (2007: 20-21) one technique for valuing equities is to calculate

the present value of all the expected future dividends, (Williams 1938; Gordon 1962; Fuller

and Hsia 1984). Damodaran (2006) reasoned that when investors buy stock in publicly traded

36

companies, they generally expect to get two types of cash flows namely, the dividends during

the holding period and an expected price at the end of the holding period, and since the

expected price is itself determined by future dividends, the value of a stock is the present

value of dividends through infinity. By this view, a share price is calculated with reference to

estimated future annual dividend payments in perpetuity, based on the assumptions of infinite

stock holding period, since the company is assumed to last forever.

Although, equity values are generally considered to be a function of expected future earnings,

the dividend discounted models treat dividends as a proxy for earnings and thus account for

future earnings implicitly. This is acceptable given that a firm may either pay out what is

earned or may reinvest those earnings within the firm. If the earnings are reinvested and an

increasing dividend policy is assumed, future dividends will be greater than current

dividends. Thus dividend will grow as long as some profits are ploughed back into the

business. Based on this conception, they submit that the theoretical price of a share for a

definite holding period n can be obtained from

Po = D1/1+k+D1(1+g2)/(1+k)2 + D1(1+g2)(1+g3)/(1+k)3 +-------+D1(1+g2)*--

*(1+gn)(1+k)n ……………………………………..2.1

Where

Po = the theoretical price of a share

Di = the dividend per share due at the end of period i

gi = the growth rate of dividends or earnings in period i

k = the risk adjusted rate of return required by the market, ie, the rate used by the market to

discount the future cash flows.

As earnings can be reinvested in the business or paid out as dividends, D = E(1-b), which

transformed the above expression into

Po = E1(1-b)/1+k+E1(1-b)(1+g2)/(1+k)2 + E1(1-b)(1+g2)(1+g3)/(1+k)3 +-------

+E1(1-b)(1+g2)*--*(1+gn)(1+k)n …………………2.2

Where

E1 = earnings in period i

b = the retention ratio

Equation (2.2) assumes that the retention ratio, b, is constant, but it may not be so. In a world

that assumes no external financing, g is the product of the retention ratio, b, and the return on

37

equity, r. Thus, g = rb. If external funding is used, growth would be enhanced by the returns

of the externally funded projects, thus g = r(b+f), where f represents the external funding as a

proportion of earnings.

The theoretical price of a share for indefinite holding period can be obtained from

� Value per share = �Dt/(1+Ke)t from t =1 to infinity t=1

� Value per share = �DO(1+g)t/(1+Ke)t from t =1 to infinity t=1

= DO(1+g)/ Ke ……………… 2.3

where Dt = Expected dividends per share in period t

Ke = cost of equity

g = perpetual constant dividend growth rate

This equation 2.3 is the Discount Dividend Model(DDM) to infinity. When the objective is

to derive a share value from estimated future dividend payments on the share, this model is

used. It derived its strength from the fact that dividends are more relevant to an investor in a

minority shareholding than either earnings or asset values. The DCF recognizes the time

value of the cash flows, which is a plus for it. However, it is unsuitable for valuations where

the shareholder has a controlling interest in the company and can dictate dividends/retentions

policy. In addition, the expectations of future dividend growth might be inaccurate.

Since projections of dividends cannot be made in perpetuity and publicly traded firms can last

forever, at least in theory, several versions of the dividend discount model have been

developed based upon different assumptions about future growth. In a stable-growth firm that

pays out what it can afford to in dividends, Durand (1957) and Gordon (1962) opine that the

Value per share = D(1+g) Ke – g …………………. 2.4

where

D(1+g) = expected dividends in the next time period

Ke = cost of equity

g = expected growth rate in perpetuity

38

This model is flawed because no firm can grow at stable rate forever and it is expected that

dividends and earnings growth must be equal, which is also not realistic. To handle this

abnormality, a two-stage growth model that allows for an initial phase where the growth rate

is not a stable growth rate and a subsequent steady state where the growth rate is stable and

expected to remain so for the long-term, was developed thus:

n Value per share = �Dt/(1+Ke)t + {Dn+1/(Ke-g)}/(1+Ke)n ….. 2.5 t=1

where

Dt = expected dividends per share in period t

g = the stable dividend growth rate after n years

While the proponents of this model would argue that, using a steady state payout ratio, for

firms that pay little or no dividends, is likely to cause only small errors in the valuation; the

model is quite limited in its application.

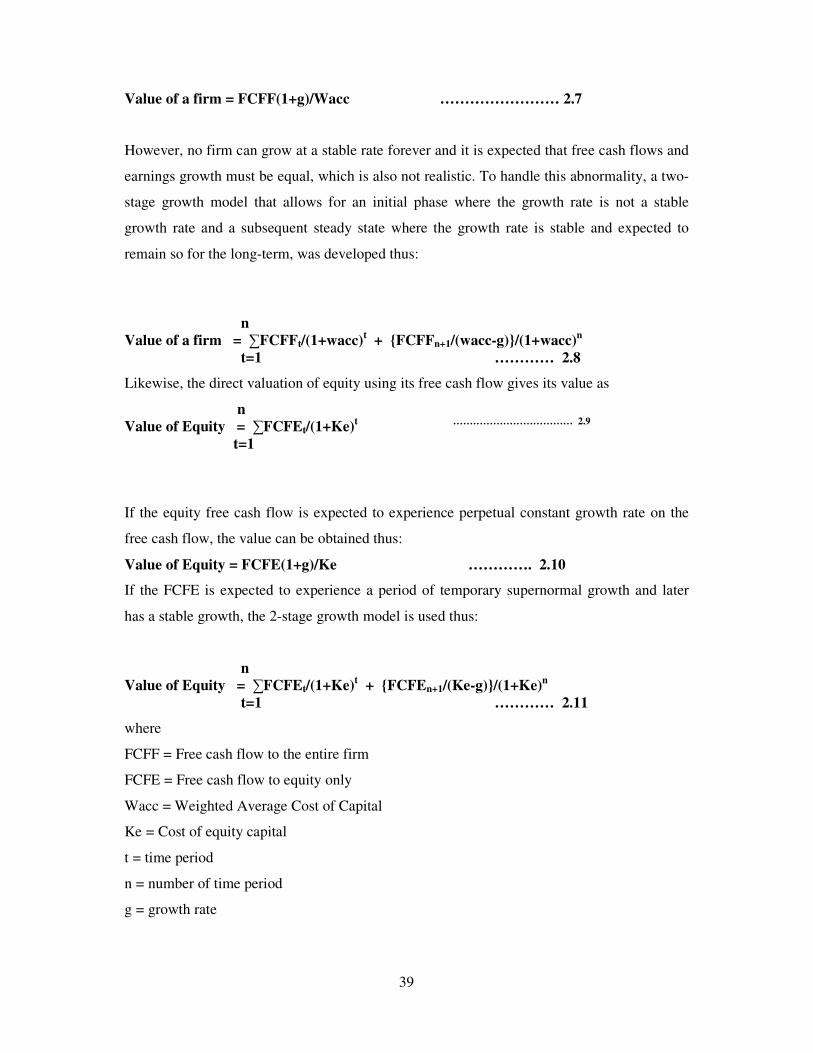

2.1.2.3Free Cash Flow Discount Model (FCFDM)

Damodaran (2006) submits that the value of an asset is a function of the expected cash flows

on that asset and that asset with high and predictable cash flows should have higher values

than the asset with low and volatile cash flows. Free Cash Flow can be Free Cash Flow to the

entire firm (FCFF) or Free Cash Flow to equity only (FCFE). The FCFF is one prior to the

payment of interest to the debt holders and deducting funds needed for capital expenditures.

If the total firm’s operating free cash flow is used, the appropriate discount rate to use is the

wacc. The total discounted value of the FCFF minus the value of debt gives the value of

equity. The value of a firm is equal to the present value of all cash flows during the forecast

period. That is,

n Value of a firm = �FCFFt/(1+wacc)t ……………………. 2.6 t=1

If the firm’s free cash flow is expected to experience perpetual constant growth rate, the value

can be obtained thus:

39