Embed Size (px)

Citation preview

Occupational Fraud – Background & Statistics

Risk Management Considerations

Best Practices & Tips

The use of one’s occupation for personal

enrichment through deliberate misuse or

misapplication of the employing

organization’s resources or assets

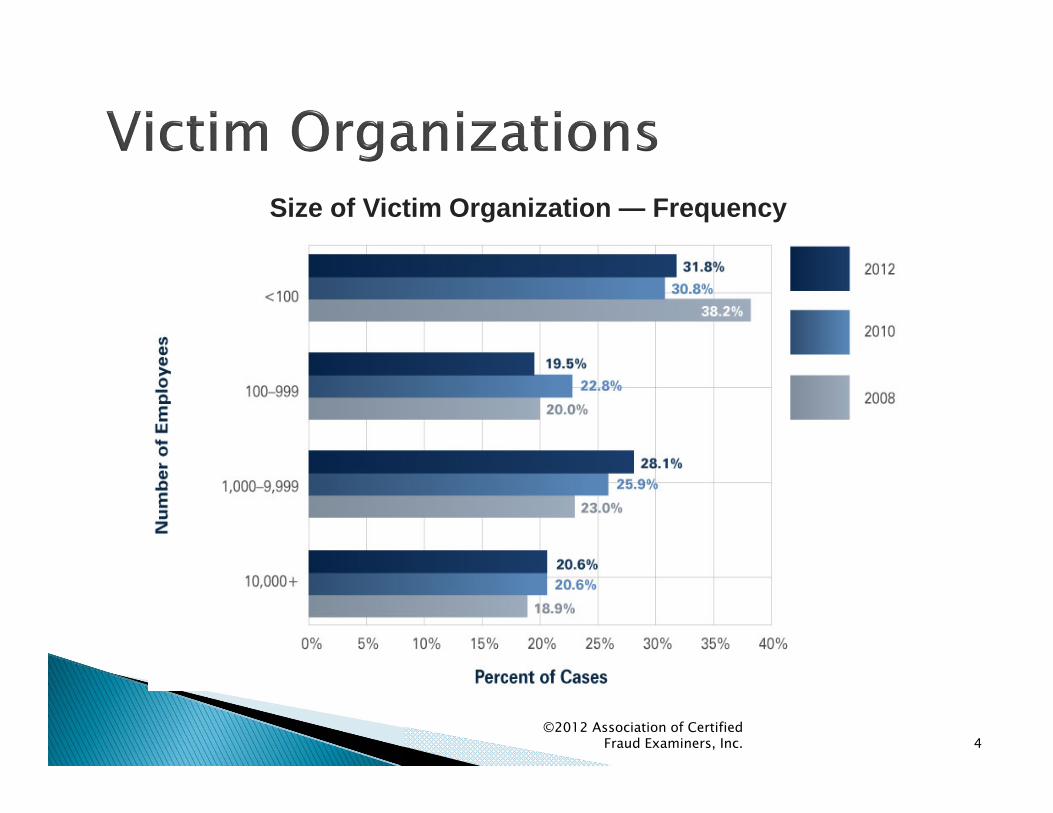

©2012 Association of Certified Fraud Examiners, Inc. 4

Size of Victim Organization — Frequency

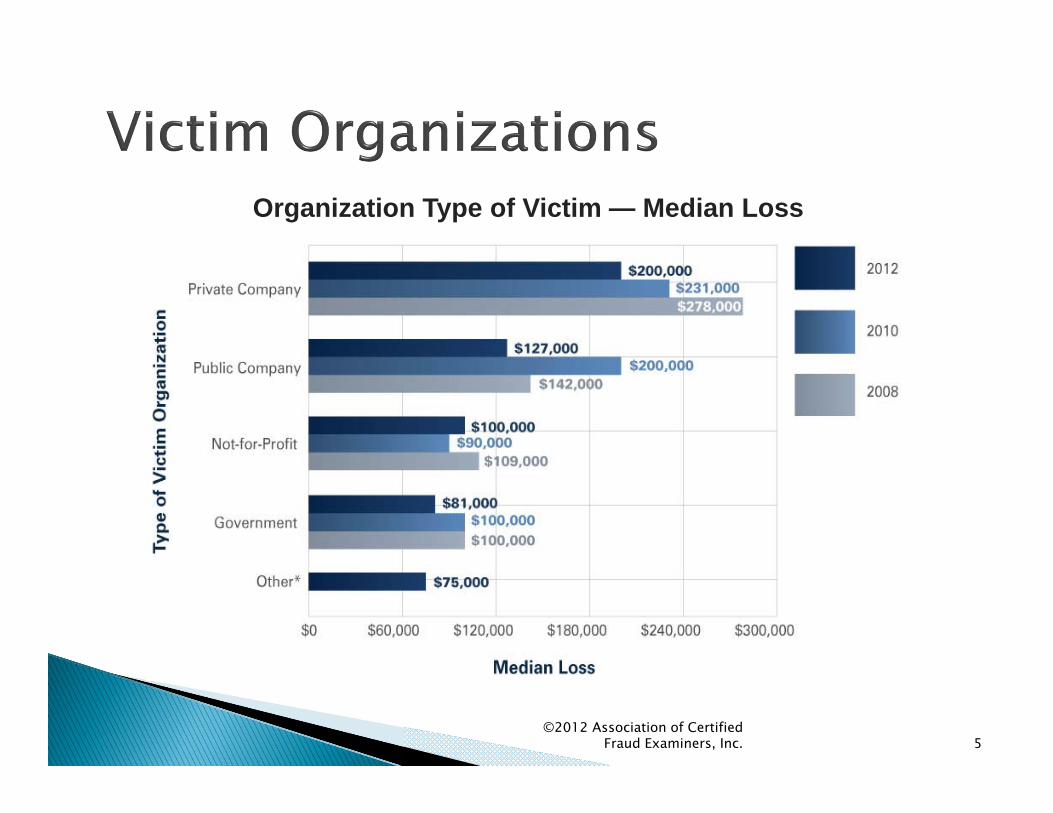

©2012 Association of Certified Fraud Examiners, Inc. 5

Organization Type of Victim — Median Loss

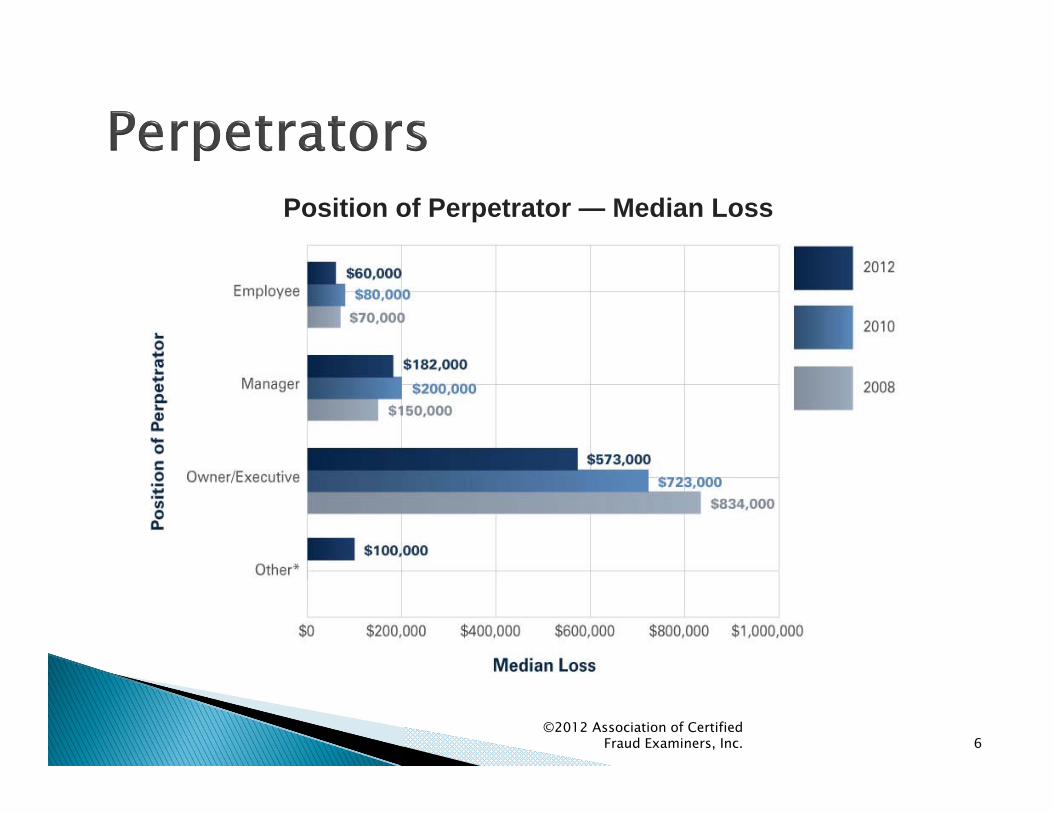

©2012 Association of Certified Fraud Examiners, Inc. 6

Position of Perpetrator — Median Loss

Assessment

Reduction◦ Preventative

◦ Detective

Transfer

Acceptance

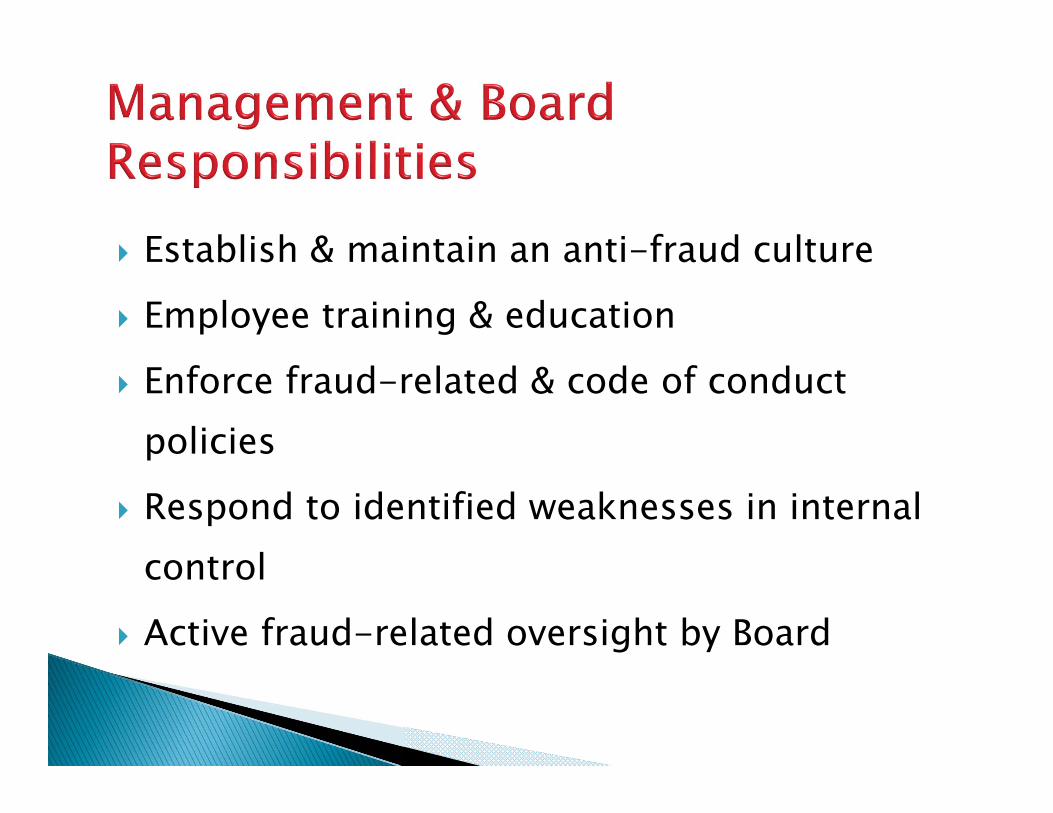

Establish & maintain an anti-fraud culture

Employee training & education

Enforce fraud-related & code of conduct policies

Respond to identified weaknesses in internal control

Active fraud-related oversight by Board

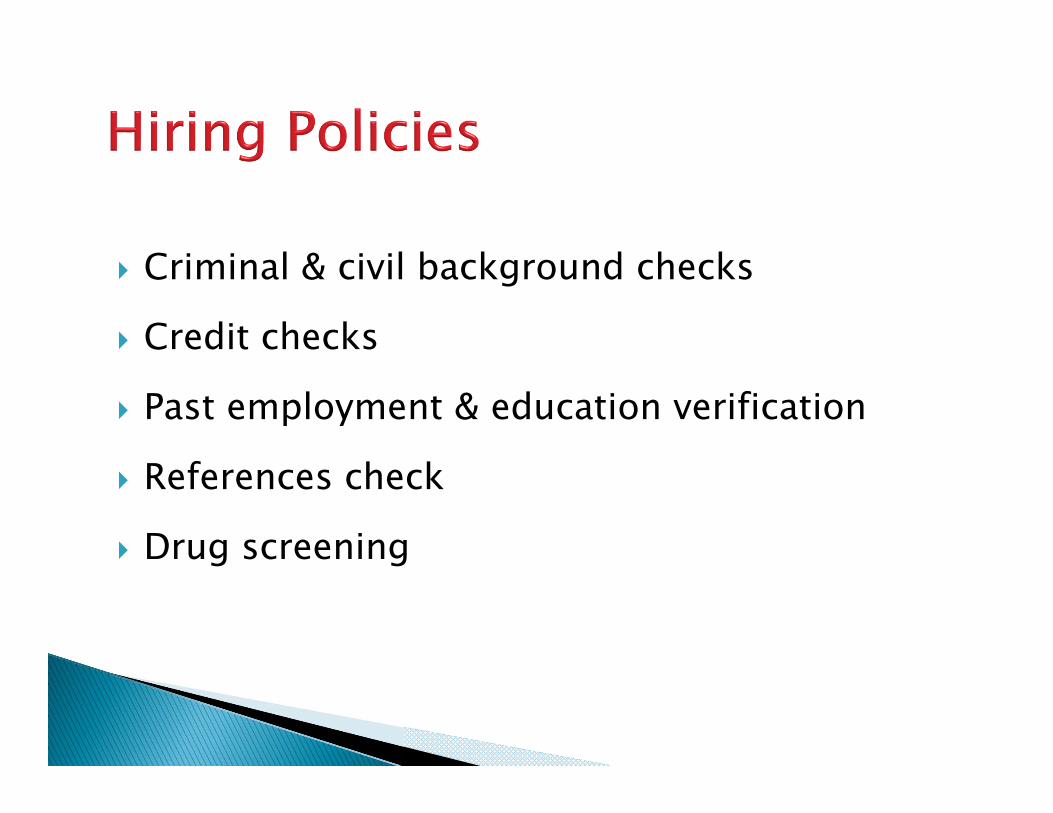

Criminal & civil background checks

Credit checks

Past employment & education verification

References check

Drug screening

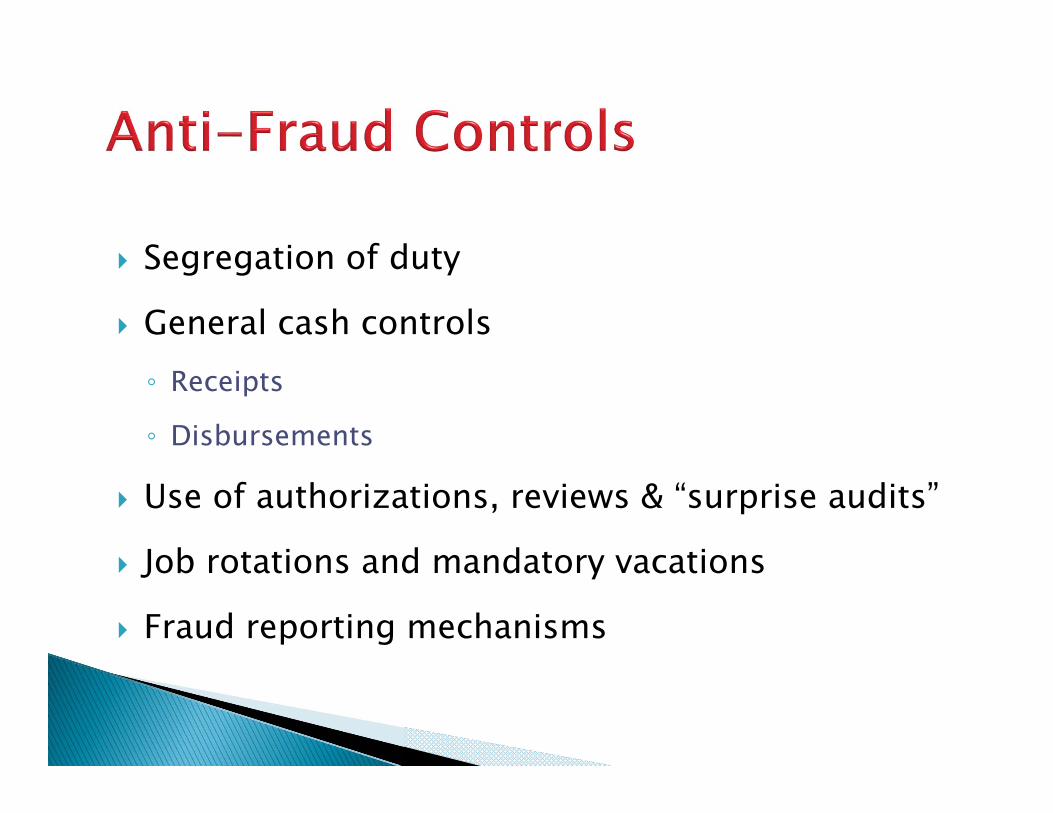

Segregation of duty

General cash controls◦ Receipts

◦ Disbursements

Use of authorizations, reviews & “surprise audits”

Job rotations and mandatory vacations

Fraud reporting mechanisms

©2012 Association of Certified Fraud Examiners, Inc. 12

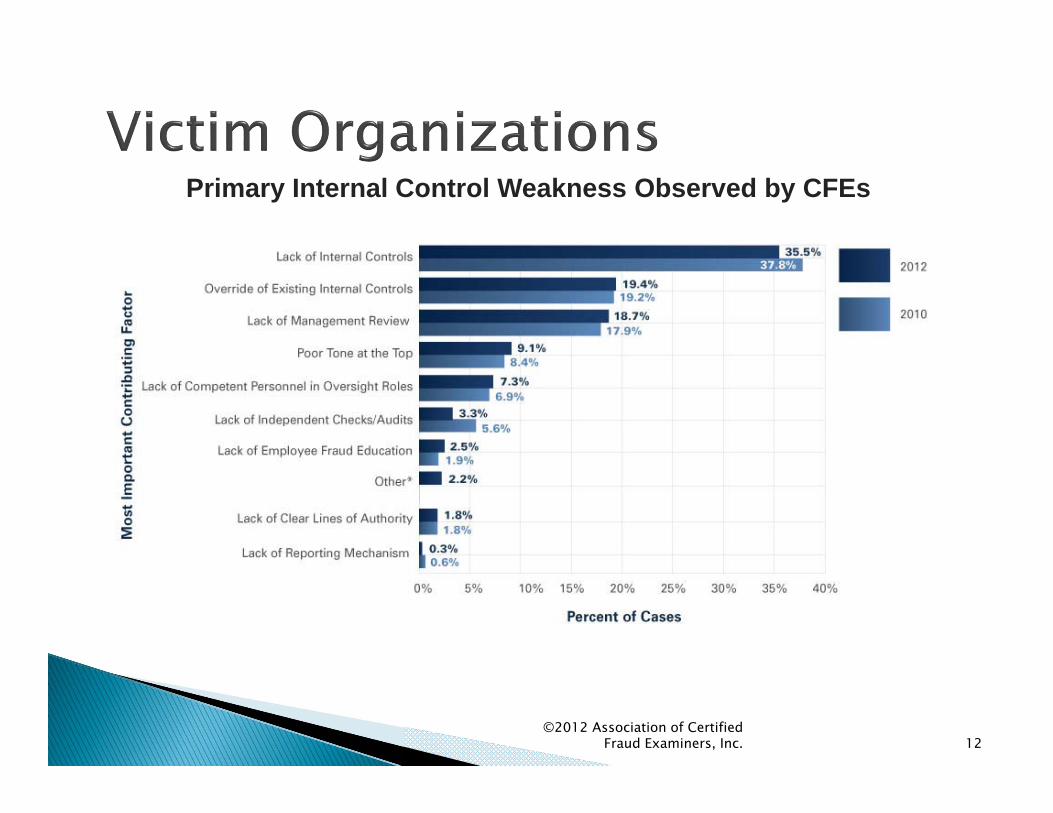

Primary Internal Control Weakness Observed by CFEs