Embed Size (px)

Citation preview

1

Offshore Renminbi (CNH)

Market: Opportunities Continue to Expand Silicon Valley Bank November 17, 2011

• Ed Sauve, Senior Advisor GFS, Silicon Valley Bank

• Mark Noble, Senior Foreign Exchange Trader, Silicon Valley Bank

• Mike Yahng, Chief Representative, Silicon Valley Bank China

• Paul Kao, Senior Foreign Exchange Trader, Silicon Valley Bank

2

Panelists

3

Agenda

Currency Overview

Offshore RMB (CNH) Market

SVB China Update

Case Studies

China 2012 Outlook

4

Currency Overview Ed Sauve Senior Foreign Global Financial Services

Silicon Valley Bank

• Historically, China has been connected to the world through trade but

not its currency

• Making the renminbi a global currency will…..

– Create a currency link with the world – beyond trade

– Create the opportunity to hold RMB as a link to value (investments)

– Create confidence for China as RMB moves to become a reserve currency

• The RMB trade settlement pilot was originally announced in Dec. 2008

• U.S. financial crisis in 2008 vastly accelerated the PBOC’s plans

− Rising doubts about the willingness of the USD to maintain its value

− Euro is seen as not a good alternative

• China needs to balance its desire to develop a global (appreciating)

currency without impacting its economic (export) engine

5

A Perspective of China and Its Currency

• The official domestic currency of the People’s Republic of China is

the renminbi (RMB)

– Onshore RMB is commonly referred to as CNY

• Onshore RMB structure

− Currency closely held/circulated within China

− FX flows monitored by its central bank (PBoC)

− Local FX hedging vehicles limited in scope

• Global pressure to revalue/appreciate RMB continues to build

– PRC resists freely floating its currency

– Managed float approach preferred

– Long-term goal is to elevate RMB to “reserve currency” status

6

Onshore RMB (CNY)

• In July 2010, PBoC and Hong Kong Monetary Authority (HKMA)

launched the offshore RMB market

− Offshore RMB referred to as CNH

− Seen as a first step toward “internationalizing” China’s currency

• Offshore RMB structure

– Two-way conversions for Hong Kong-based transactions

– Standard FX hedging products available

– CNH spot rates closely linked to CNY

• Trade settlement

− CNH cross-border settlements to/from the Mainland currently restricted

− No settlement restrictions for Hong Kong-based transactions

− Mainland companies expanding CNH capabilities and presence

7

Offshore RMB (CNH)

• Potential international trade changes

– PBoC actively pursuing local companies to invoice in RMB vs. USD

– Cross-border payments must be trade-related to avoid restrictions

– Local currency pricing adjustments possible by accepting FX risk

• Currency risk concerns

− The need for a structured currency risk management program should be

evaluated

− Active cash management practices utilized when parking CNH funds

• New opportunities

– RMB pricing enables U.S. company to control FX risk

– Better clarity for ongoing price movements

– Offshore investment via evolving “dim sum” bond market enhanced

8

Offshore RMB (CNH) Impact for Companies

9

Offshore RMB (CNH) Market Mark Noble Senior Foreign Exchange Trader,

Silicon Valley Bank

Cross-border CNY

settlement

CNH investment products

Movement of CNH into the

Mainland

10

CNH Development Milestones

• August 2011: CNY

settlement scheme

expanded nationwide

• June 2010:

Expanded RMB trade

settlement pilot

scheme to cover 20

provinces and cities.

• October 2011: New guidelines

allowing offshore RMB for FDI

transactions (subject to normal

approvals)

• April 2011: First RMB IPO by

Hui Xian, listed on the Hong

Kong Exchange

• February 2010: HKMA allowed

participating banks to develop

CNY business as long as the

related flows do not entail back

to the mainland

• January 2011: RMB

Overseas Direct Investment

allowing Chinese enterprises

to conduct overseas direct

investment

• August 2010: opened

onshore RMB-denominated

bonds to qualified offshore

institutions to a limited extent

and allowed participating

banks to invest CNY liquidity

in onshore bonds (subject to a

quota)

Accelerated CNH Market Since Mid-2010

• Offshore RMB market continues to be “walled off” from the Mainland

economy via the PRC’s goal to minimize any negative impact

• China continues to maintain tight restrictions via RMB cross-border

– Current Account: Trade settlement is permitted but closely monitored

– Capital Account: Foreign Direct Investment (FDI) must be approved by the

Ministry of Commerce

• No restrictions for offshore (CNH) flows/uses outside of China

• Restrictions apply if a payment crosses the Mainland border

• Restrictions are enforced in China through its local banks

11

Onshore vs. Offshore Overview

• CNH market represents new opportunity for international investors to

gain exposure to RMB

− Trade settlement is still the ultimate goal

− Hong Kong’s “dim sum” bond market growth unprecedented

• Hong Kong is currently the primary offshore RMB financial center

– London and Singapore are seen to follow

• Growth of CNH market linked to rapid increase of RMB-denominated

foreign trade

− Cross-border flows via Hong Kong and the Mainland a catalyst for growth

• RMB denominated financial products continue to evolve

12

CNH Market Characteristics

• Chinese counterparty locations now throughout China

− Previously only 20 designated provinces or cities were allowed

• Chinese counterparty must be approved as a Mainland Designated

Enterprise (MDE) – primarily for trade-related goods

– Established to ensure legitimate participants

13

Trade Settlement Regulations

Import to China (Outbound Payment)

Export From China (Inbound Payment)

Goods No MDE Restrictions MDE Only

Services No MDE Restrictions No MDE Restrictions

• CNH FX market began trading in late July 2010

• As of June 2011, RMB share in world FX trade is less than 1%

– Expected to increase to 5% by 2020

• Normal bid/ask pricing structure applies

− Onshore-to-offshore trading relationship can be volatile

− Market-driven disconnects can happen

• Daily liquidity continues to grow dramatically

– Spot approx. $1.5B

– Forward approx. $1B

• Offshore NDF market continues to reflect deeper appreciation

14

CNH FX Market Overview

15

CNH Trades at a Premium…Most of the Time

Source: Bloomberg and SVB

6.20

6.30

6.40

6.50

6.60

6.70

6.80

6.90

1/4/2010 4/4/2010 7/4/2010 10/4/2010 1/4/2011 4/4/2011 7/4/2011 10/4/2011

CNH CNY

RMB Onshore and Offshore Exchange Rates

16

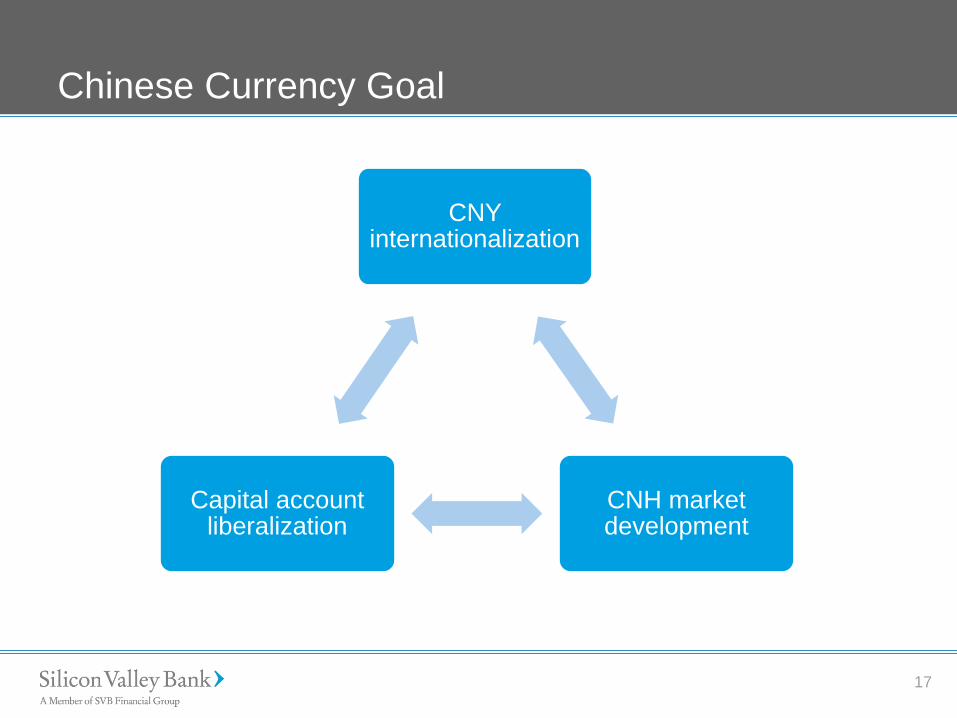

SVB China Update Mike Yahng Chief Representative

Silicon Valley Bank

CNY internationalization

CNH market development

Capital account liberalization

17

Chinese Currency Goal

18

CNY Settlement Grows Rapidly Since Mid-2010

Sources: Reuters

CNY monthly settlement trade volumes grow from less than 20b RMB in June

2010 to more than 150b RMB in May 2011.

0

50

100

150

200

J 2010

A S O N D J 2011

F M A M

CNY settlement trade volumes-RMB bn

• RMB deposits in Hong Kong’s banks have exploded from less than 90B RMB in

June 2010 to more than half a trillion RMB (572B RMB) in Jul 2011.

− Mainly attributed to an increase in RMB receipts by corporate customers through trade

settlement transactions. The number of authorized institutions engaged in RMB

business has increased from 77 in June 2010 to 128 in Jul 2011.

− Also attributed to RMB appreciation expectation

19

Accelerating Growth in CNH Deposits

Source: HKMA

• The CNH bond market has developed at an extraordinary pace since the deregulation of offshore RMB in mid-2010.

− Issuance of offshore RMB bonds in the first half of 2011 stands at 69.4B RMB, (according

to Thomson Reuter’s data), compared to 42.6B RMB in all of 2010

• Still in a preliminary stage. Only RMB 160B of CNH bonds outstanding which grows much slower than CNH deposits demand.

20

High Demand in CNH Bonds

CNH Outstanding Bonds, 160

CNH Deposits, 572

0

100

200

300

400

500

600

700

2008 2009 2010 2011(Jul)

RM

B b

n

Source: HKMA

21

Government Initiatives

• Taking steps towards the internationalization of the RMB − The Chinese authorities have pushed harder for RMB internationalization since the global

financial crisis

− China supports Hong Kong to become an offshore RMB center

• New centers − Likely next candidates would be Singapore or Malaysia, two jurisdictions with relatively

developed financial markets, as well as close commercial and regulatory relationships with China

− Possibly New York and London will also take part in CNH market in future

• RQFII − May start soon (before the end of 2011), with an initial size of 20B RMB, allowing RMB funds

raised in Hong Kong to be invested in the mainland's securities market

− Helps broaden the channels for RMB in the offshore market to flow back to the mainland and the option will first be open to domestic fund managers familiar with the A-share market and subsidiaries of securities companies in Hong Kong

• China may tighten its control over the rapidly growing CNH − Too much RMB flowing back into mainland will impact monetary policy. Controlling inflation

continues to be a top priority

− Rapid growth of CNH deposits may affect confidence in the HKD

22

Case Studies Paul Kao Senior Foreign Exchange Trader,

Silicon Valley Bank

Hedging with CNH

23

Restrictions

• None

• Foreign-based client investing U.S. dollars into China Client profile

• Hedge against CNY appreciation Need

* Non-U.S.-based or non-China- based

Chinese CNY

account

Option 1: MCA Spot contract to

MCA

Option 2: Forward

Purchase forward contract

Option 3: Option Purchase option

contract

Payments to Hong Kong-based Supplier Using CNH

24

Offshore supplier

RMB account

Option 1: FX Send CNH FX wire from USD

DDA

Option 2: MCA

Send CNH from RMB

MCA

• U.S. based client with offshore suppliers Client profile

• Pay offshore supplier in CNH Need

Restrictions

• None

Receivables from Hong Kong-based Buyer in CNH

25

Restrictions

• None

• U.S. based manufacturer selling to an offshore buyer Client profile

• Receive payment in CNH Need

FX trade to client

USD DDA

Option 1: FX Receive RMB FX wire into SVB account

Option 2: MCA Receive RMB

into client’s RMB MCA

Payments to Mainland China Supplier Using CNH

26

• U.S. based client with supplier located in China Client profile

• Pay Chinese supplier in RMB Need Restrictions

• Goods

• MDE

• Approved province

• Services

• SAFE approval

Chinese supplier

RMB account

Option 1: FX Send RMB FX

wire (CNH) from USD

DDA

Option 2: MCA Send RMB wire (CNH) from RMB

MCA

Note: Not yet common but will increase over time

• Economic Outlook

• Government Outlook

• Offshore RMB Outlook

27

China 2012 Outlook

28

Questions?

29

Biographies

30

Ed Sauve

Senior Foreign Exchange Advisor

949.754.0816

Ed Sauve is the senior advisor for the Global Financial Services Group

of Silicon Valley Bank and he has 20 plus years of commercial banking

experience including provision of credit and delivery of a wide variety of

financial services to small business, middle market, institutional and

multi-national companies.

Sauve's international banking experience includes assignments in

London, Middle East and Hong Kong. He opened Middle East Area

Representative office for First Interstate Bank in the United Arab

Emirates and led a program to obtain license to open its bank office in

Beijing, China. Currently he supports the international activities of SVB's

Southern California-based clients.

His domestic experience includes management of regional corporate

centers in Los Angeles and the South Bay for Wells Fargo/First

Interstate, as well as regional responsibility for marketing Silicon Valley

Bank's short-term money market capabilities in Southern California. He

has transaction experience in commercial lending, cash management,

corporate finance, short-term money market investments and

international banking.

Mark Noble is a senior foreign exchange advisor with Silicon Valley Bank. He designs custom hedging strategies for clients with complex currency-related issues, advises clients in developing, implementing and monitoring foreign exchange strategies and educates clients in understanding foreign exchange products. Noble has more than 20 years of experience in the financial industry with a dedicated focus on foreign exchanges services and treasury management products. Before joining SVB in 2007, Noble worked for Commonwealth Foreign Exchange and held multiple management positions including director of currency trading and senior manager of financial operations. Noble oversaw daily trading, client treasury management, account reconciliation and the timely delivery of client payments through various global treasury management banks. Over his career, Noble has provided foreign exchange consulting services, executed hedging requirements utilizing spot, forward, swaps and option contracts and coordinated the issuance and maintenance of credit lines. While with a large pharmaceutical firm, Syntex Corporation, he managed many corporate treasury activities from a multi-million dollar foreign exchange risk portfolio, to the development and implementation a foreign exchange module as a part of its internal banking system to facilitate management and mitigate risk. Noble holds a bachelor’s degree in business administration from California State University in Fullerton.

31

Mark Noble

Senior Foreign Exchange Trader

408.654.7711

Mike Yahng is SVB's Chief Representative in China and manages all of

SVB's initiatives and activities in China.

With more than 30 years of experience in international finance and

banking, Yahng joined SVB in 2008 from TianDi Growth Capital where

he was involved with private equity fundraising and investments in

China. Previously he was a managing director for Trinergy Finance, the

interim CEO of Shenzhen Development Bank and CEO of Magically,

Inc. After serving as a lieutenant in the U.S. Navy, Yahng began his

career in banking and spent more than 20 years with Bank of Boston in

a variety of capacities, including managing operations in Greater China.

Yahng received his BA from Yale College and MBA from Harvard

Business School. Yahng sits on the boards of Bank of Hangzhou, UPG,

and First Sino Bank, the only Taiwanese JV Bank in China.

Yahng is based in Shanghai and Hong Kong.

32

Mike Yahng

Chief Representative, China

8621.6143.3818

Paul Kao is a senior foreign exchange trader with Silicon Valley

Bank. With over 15 years experiences in foreign exchange, Kao

provides FX risk management advisory to a portfolio of top-tier Venture

Capital, Private Equity and multi-national high-tech firms. Kao provides

clients with customized FX research and analysis, assisting them in

identifying FX risk, minimizing FX cost and maximizing profits through

spot, forwards, options and structured product markets.

Kao also has extensive experience in international banking, commercial

lending and private banking. Before joining the FX team at SVB, Kao

was a member of Silicon Valley Bank's Northern Technology team,

responsible for underwriting credit facilities to publicly traded technology

companies. Prior to joining SVB, Kao worked for Bank of America,

Private Banking Group, managing a portfolio of high net-worth individual

accounts. Kao also worked in Asia for 5 years for several major money

center banks.

Kao holds a bachelor’s degree in finance from University of North

Carolina at Charlotte and has been a member of Monte Jade Science &

Technology Association since 2002.

33

Paul Kao

Senior Foreign Exchange Trader

408.654.3042

This material, including without limitation the statistical information herein, is provided for informational purposes only. The material is based in part upon information from third-party sources that we believe to be reliable, but which has not been independently verified by us and, as such, we do not represent that the information is accurate or complete. The information should not be viewed as tax, investment, legal or other advice nor is it to be relied on in making an investment or other decision. You should obtain relevant and specific professional advice before making any investment decision. Nothing relating to the material should be construed as a solicitation or offer, or recommendation, to acquire or dispose of any investment or to engage in any other transaction.

©2011 SVB Financial Group. All rights reserved. Silicon Valley Bank is a member of FDIC and

Federal Reserve System. SVB>, SVB>Find a way, SVB Financial Group, and Silicon Valley Bank

are registered trademarks.

SVB Securities is a non-bank affiliate of Silicon Valley Bank and member of SVB Financial

Group. Member FINRA and SIPC. Products offered by SVB Securities are not FDIC insured, are

not deposits or other obligations of Silicon Valley Bank, and may lose value. 1111-0137

34

Disclosures