Embed Size (px)

Citation preview

PRELIMINARY OFFERING CIRCULAR DATED 17 OCTOBER 2001

U.S.$ll% Loan Participation Notes due 20ll

issued by ABN AMRO Bank (Luxembourg) S.A.on a limited recourse basis for the sole purpose of financing a loan to

OJSC Oil Company Rosneft

The issue price of the U.S.$l l% Loan Participation Notes due 20ll (the ‘‘Notes’’) of ABN AMRO Bank (Luxembourg) S.A. (the ‘‘Bank’’) isl% of their principal amount.

The Notes are limited recourse obligations of the Bank and are being offered for the sole purpose of funding a l year loan (the ‘‘Loan’’) toOJSC Oil Company Rosneft (the ‘‘Borrower’’, the ‘‘Company’’ or ‘‘Rosneft’’) pursuant to a loan agreement (the ‘‘Loan Agreement’’) between theBank and the Borrower. The Notes will be constituted by, be subject to, and have the benefit of, a trust deed dated l 2001 (the ‘‘Trust Deed’’) betweenthe Bank and The Bank of New York, as trustee for the holders of the Notes (the ‘‘Trustee’’). The Bank will, in the Trust Deed, charge in favour of theTrustee for the benefit of the Noteholders (as defined herein) as security for its payment obligations in respect of the Notes (a) its right to principal,interest and additional amounts (if any) as lender under the Loan Agreement and (b) amounts received pursuant to the Loan in an account of the Bank(as described herein), in each case other than certain amounts in respect of Reserved Rights (as defined in ‘‘Terms and Conditions of the Notes’’). TheBank will also assign its administrative rights under the Loan Agreement to the Trustee.

Subject to timely receipt of the relevant amounts in U.S. Dollars from the Borrower (as further described in ‘‘Terms and Conditions of theNotes’’), interest on the Notes is payable semi-annually in arrear, on l and l in each year commencing on l l 2002. In each case where amounts ofprincipal, interest and additional amounts (if any) are stated to be payable in respect of the Notes, the obligation of the Bank to make any such paymentshall constitute an obligation only to pay to Noteholders, on each date upon which such amounts of principal, interest and additional amounts (if any)are due in respect of the Notes, an amount equal to and in the same currency as sums of principal, interest and additional amounts (if any) actuallyreceived by or for the account of the Bank pursuant to the Loan Agreement less any amount in respect of the Reserved Rights. The Bank will have noother financial obligations under the Notes. Noteholders will be deemed to have accepted and agreed that they will be relying solely and exclusively onthe covenant, credit and financial standing of the Borrower in respect of the financial servicing of the Notes.

Payments in respect of the Notes will, except in certain limited circumstances, be made without any deduction or withholding for or on accountof Luxembourg taxes except as required by law. In that event, the Bank will only be required to pay additional amounts to the extent that it receivescorresponding amounts under the Loan Agreement. Payments under the Loan Agreement shall, except in certain limited circumstances, be madewithout any deduction or withholding for or on account of Russian taxes, except as required by law, in which event the Borrower will be obliged toincrease the amounts payable under the Loan Agreement. In certain circumstances the Loan may be prepaid at its principal amount, together withaccrued interest, at the option of the Borrower upon the Borrower being required to increase the amount payable or to pay additional amounts onaccount of Russian or Luxembourg taxes or required to pay additional amounts on account of certain costs incurred by the Bank pursuant to the LoanAgreement. The Bank may (in its own discretion) require the Loan to be prepaid if it becomes unlawful for the Loan or the Notes to remainoutstanding, as set out in the Loan Agreement. In addition, in the event of a Change of Control (as defined in ‘‘Terms and Conditions of the Notes –Redemption and Purchase’’), the holder of a Note may, by exercise of the relevant option, request the Bank to give notice to the Borrower, inaccordance with the provisions of the Loan Agreement, that the Loan be prepaid in an amount representing the aggregate principal amount of theNotes relating to the exercise of such option together with accrued interest. In each case (to the extent that the Bank has actually received the relevantfunds from the Borrower) the payment amount of the relevant Notes (or in the case of a prepayment for tax reasons or illegality, all outstanding Notes)will be prepaid by the Bank together with accrued interest. See ‘‘Loan Agreement – Prepayment – Prepayment for Tax Reasons and Change inCircumstances’’ and ‘‘Terms and Conditions of the Notes – Redemption and Purchase’’.

The Notes will be offered and sold in an offering in the United States to ‘‘qualified institutional buyers’’ (as defined in Rule 144A (‘‘Rule 144A’’)under the United States Securities Act of 1933, as amended (the ‘‘Securities Act’’)) in reliance on Rule 144A and in offshore transactions outside theUnited States in reliance on Regulation S under the Securities Act (‘‘Regulation S’’). See ‘‘Subscription and Sale’’ and ‘‘Form of Notes and TransferRestrictions’’.

Application has been made to list the Notes on the Luxembourg Stock Exchange. Application has also been made for the Notes issued and soldin reliance on Rule 144A to be designated as eligible for trading on PortalSM, a subsidiary of NASDAQ Stock Market, Inc. (‘‘PORTAL’’).

AN INVESTMENT IN THE NOTES INVOLVES A HIGH DEGREE OF RISK. SEE ‘‘RISK FACTORS’’.

THE NOTES HAVE NOT BEEN AND WILL NOT BE REGISTERED UNDER THE SECURITIES ACT, OR ANY STATESECURITIES LAW, AND THE NOTES MAY NOT BE OFFERED OR SOLD WITHIN THE UNITED STATES OR TO, OR FOR THEACCOUNT OR BENEFIT OF, ANY U.S. PERSON (AS SUCH TERMS ARE DEFINED IN REGULATION S), EXCEPT TO QUALIFIEDINSTITUTIONAL BUYERS IN RELIANCE ON THE EXEMPTION FROM THE REGISTRATION REQUIREMENTS OF THESECURITIES ACT PROVIDED BY RULE 144A OR OTHERWISE PURSUANT TO AN EXEMPTION FROM, OR IN A TRANSACTIONNOT SUBJECT TO, THE REGISTRATION REQUIREMENTS OF THE SECURITIES ACT. PROSPECTIVE PURCHASERS OF NOTESARE HEREBY NOTIFIED THAT SELLERS OF NOTES MAY BE RELYING ON THE EXEMPTION FROM THE PROVISIONS OFSECTION 5 OF THE SECURITIES ACT PROVIDED BY RULE 144A. SEE ‘‘FORMS OF NOTES AND TRANSFER RESTRICTIONS’’.

Notes offered and sold outside the United States in reliance on Regulation S (‘‘Unrestricted Notes’’) will be offered and sold in denominationsof U.S.$1,000 or any amount in excess thereof which is an integral multiple of U.S.$1,000, and will be transferable in denominations of U.S.$10,000 orany amount in excess thereof which is an integral multiple of U.S.$1,000. Notes offered and sold to qualified institutional buyers in the United States inreliance on Rule 144A (‘‘Restricted Notes’’) will be offered and sold in denominations of U.S.$1,000 or any amount in excess thereof which is anintegral multiple of U.S.$1,000, and will be transferable in denominations of U.S.$100,000 or any amount in excess thereof which is an integral multipleof U.S.$1,000. Unrestricted Notes will be represented by beneficial interests in an unrestricted global note certificate (the ‘‘Unrestricted Global NoteCertificate’’) in registered form, without interest coupons attached, which will be registered in the name of The Bank of New York Depository(Nominees) Limited as nominee for, and shall be deposited on or about l 2001 (the ‘‘Closing Date’’) with The Bank of New York as commondepositary for, and in respect of interests held through, Euroclear Bank, S.A./N.V., as operator of the Euroclear System (‘‘Euroclear’’) and ClearstreamBanking, societe anonyme (‘‘Clearstream, Luxembourg’’). Restricted Notes will be represented by beneficial interests in a restricted global notecertificate (the ‘‘Restricted Global Note Certificate’’ and together with the Unrestricted Global Note Certificate, the ‘‘Global Note Certificates’’) inregistered form, without interest coupons attached, which will be deposited on or about the Closing Date with The Bank of New York as custodian for,and registered in the name of Cede & Co. as nominee for, The Depository Trust Company (‘‘DTC’’). Interests in the Restricted Global Note Certificatewill be subject to certain restrictions on transfer. See ‘‘Forms of Notes and Transfer Restrictions’’. Beneficial interests in the Global Note Certificateswill be shown on, and transfers thereof will be effected only through, records maintained by DTC, Euroclear and Clearstream, Luxembourg and theirparticipants. Except as described herein, Note Certificates in definitive form will not be issued in exchange for beneficial interests in the Global NoteCertificates.

ABN AMRO DRESDNER KLEINWORT WASSERSTEIN

The date of this Offering Circular is l 2001Th

isP

reli

min

ary

Off

erin

gC

ircu

lar

isb

ein

gd

istr

ibu

ted

for

info

rmat

ion

pu

rpo

ses

on

lyan

dis

sub

ject

toam

end

men

tan

dco

mp

leti

on

.T

his

Pre

lim

inar

yO

ffer

ing

Cir

cula

rd

oes

no

t,an

dis

no

tin

ten

ded

to,

con

stit

ute

or

con

tain

ano

ffer

tose

llan

yo

fth

eN

ote

s.

Other than information relating to the Bank for which no representation or warranty is made by theCompany, the Company, having made all reasonable enquiries, confirms that (i) this Offering Circular (the‘‘Offering Circular’’) contains all information with respect to the Company, the Company and itssubsidiaries, the Loan Agreement and Notes, which is (in the context of the issue, of the Notes) material; (ii)such information is true and accurate in all material respects and is not misleading in any material respect;(iii) any opinions, predictions or intentions expressed in this Offering Circular on the part of the Companyare honestly held or made, have been reached after considering all relevant circumstances, are based uponreasonable assumptions and are not misleading in any material respect; (iv) this Offering Circular does notomit to state any material fact necessary to make such information, opinions, predictions or intentions (inthe context of the issue of the Notes) not misleading in any material respect; and (v) this Offering Circulardoes not contain any untrue statement of a material fact nor does it omit to state any material fact necessaryto make the statements therein, in the light of the circumstance under which they were made, not misleading.Accordingly, save as set out below, the Company accepts responsibility for the information and statementscontained in this Offering Circular other than information relating to the Bank. The Bank acceptsresponsibility for information in respect of itself accordingly. The sections entitled ‘‘Russian Federation –General Overview’’ and ‘‘Overview of the Russian Oil and Gas Industry’’ have been extracted frompublicly available data, and the Company accepts responsibility for accurately extracting such data butaccepts no further responsibility in respect of such information.

No person has been authorised in connection with the offering of the Notes to give any information ormake any representation regarding the Company and the Notes other than as contained in this OfferingCircular. Any such representation or information must not be relied upon as having been authorised by theBank, the Company, the Trustee or the Managers (as defined in ‘‘Subscription and Sale’’). The delivery ofthis Offering Circular at any time does not imply that the information contained in it is correct as of anytime subsequent to its date.

The Managers have not separately verified the information contained in this Offering Circular and donot make any representation or warranty, express or implied, as to the accuracy or completeness of theinformation in this Offering Circular. Each person receiving this Offering Circular acknowledges that suchperson has not relied on the Managers or any person affiliated with any Manager in connection with itsinvestigation of the accuracy of such information or its investment decision. Each person contemplatingmaking an investment in the Notes must make its own investigation and analysis of the creditworthiness ofthe Bank and the Company and its own determination of the suitability of any such investment, withparticular reference to its own investment objectives and experience, and any other factors which may berelevant to it in connection with such investment.

This Offering Circular does not constitute an offer or an invitation by or on behalf of the Bank, theCompany or the Managers to subscribe or purchase, any of the Notes. The distribution of this OfferingCircular and the offer or sale of the Notes in certain jurisdictions is restricted by law. Persons into whosepossession this Offering Circular may come are required by the Bank, the Company and the Managers toinform themselves about and to observe any such restrictions. In particular, the Notes have not beenapproved or disapproved by the U.S. Securities and Exchange Commission, any State securitiescommission in the United States or any other U.S. regulatory authority, nor have any of the foregoingauthorities passed upon or endorsed the merits of the offering of the Notes or the accuracy or adequacy ofthis Offering Circular. Any representation to the contrary is a criminal offence in the United States. Inaddition, the Bank has not authorised any issue of Notes to the public in the United Kingdom within themeaning of the Public Offers of Securities Regulations 1995 (the ‘‘Regulations’’). Notes may not lawfully beoffered or sold to persons in the United Kingdom except in circumstances that do not result in an offer tothe public in the United Kingdom within the meaning of the Regulations or otherwise in compliance with allother applicable provisions of the Regulations. Further information with regard to restrictions on offers andsales of the Notes and the distribution of this Offering Circular is set out under ‘‘Subscription and Sale’’ and‘‘Forms of Notes and Transfer Restrictions’’.

2

TABLE OF CONTENTS

Page

NOTICE TO NEW HAMPSHIRE RESIDENTS...................................................................................... 4

AVAILABLE INFORMATION .................................................................................................................. 4

FORWARD LOOKING STATEMENTS .................................................................................................. 4

ENFORCEABILITY OF JUDGMENTS .................................................................................................... 5

FINANCIAL AND OTHER INFORMATION ........................................................................................ 6

SUMMARY ...................................................................................................................................................... 7

DESCRIPTION OF THE TRANSACTION AND THE SECURITY .................................................. 13

USE OF PROCEEDS...................................................................................................................................... 15

RISK FACTORS .............................................................................................................................................. 16

RUSSIAN FEDERATION-GENERAL OVERVIEW ............................................................................ 30

OVERVIEW OF THE RUSSIAN OIL AND GAS INDUSTRY .......................................................... 32

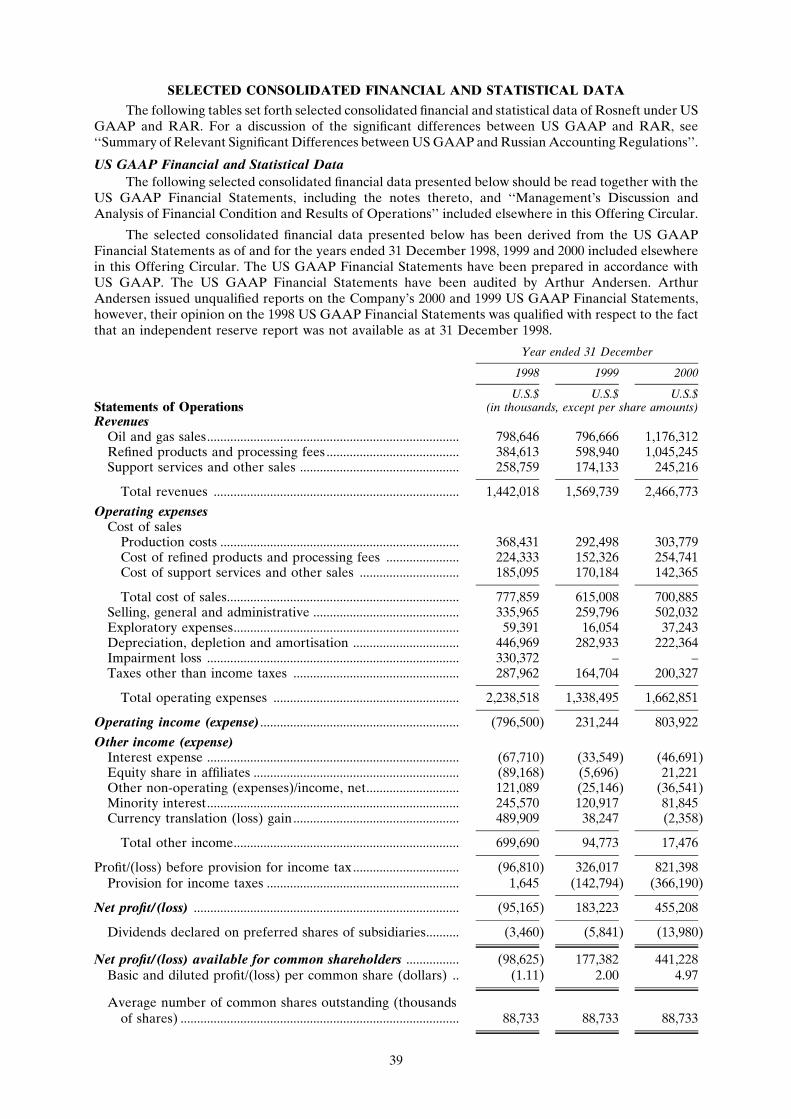

SELECTED CONSOLIDATED FINANCIAL AND STATISTICAL DATA.................................... 39

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIALCONDITION AND RESULTS OF OPERATIONS ................................................................................ 43

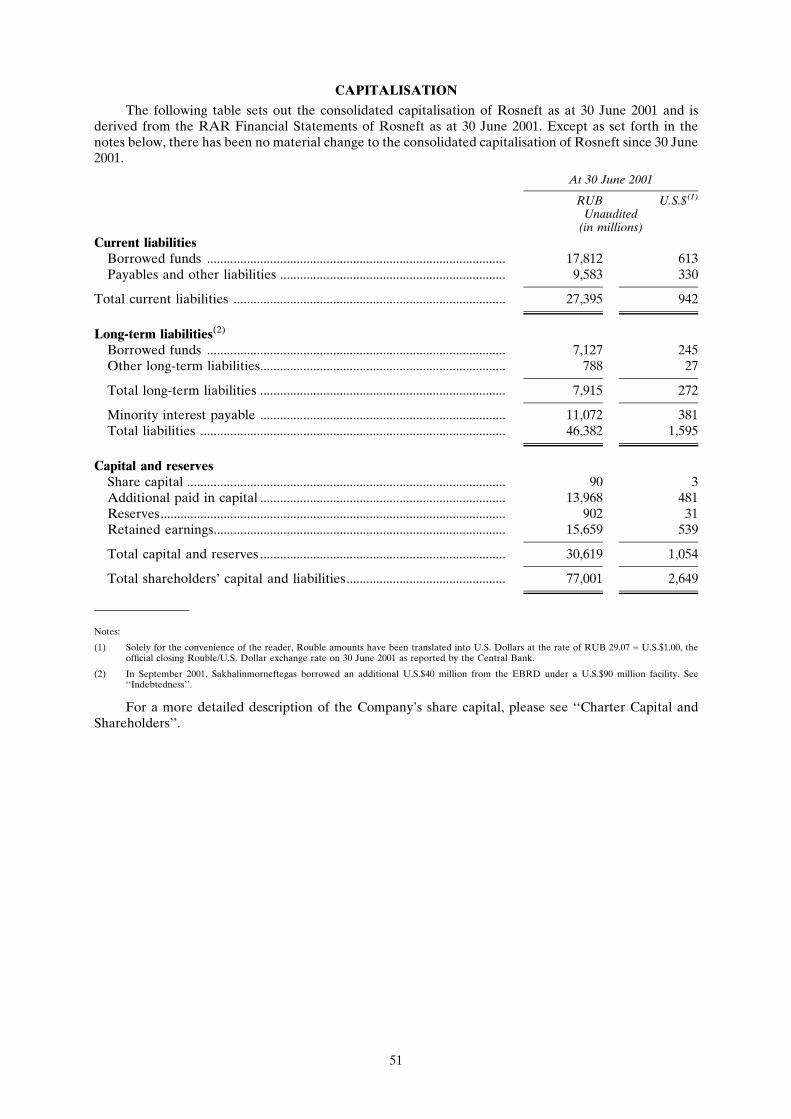

CAPITALISATION ........................................................................................................................................ 51

ROSNEFT.......................................................................................................................................................... 52

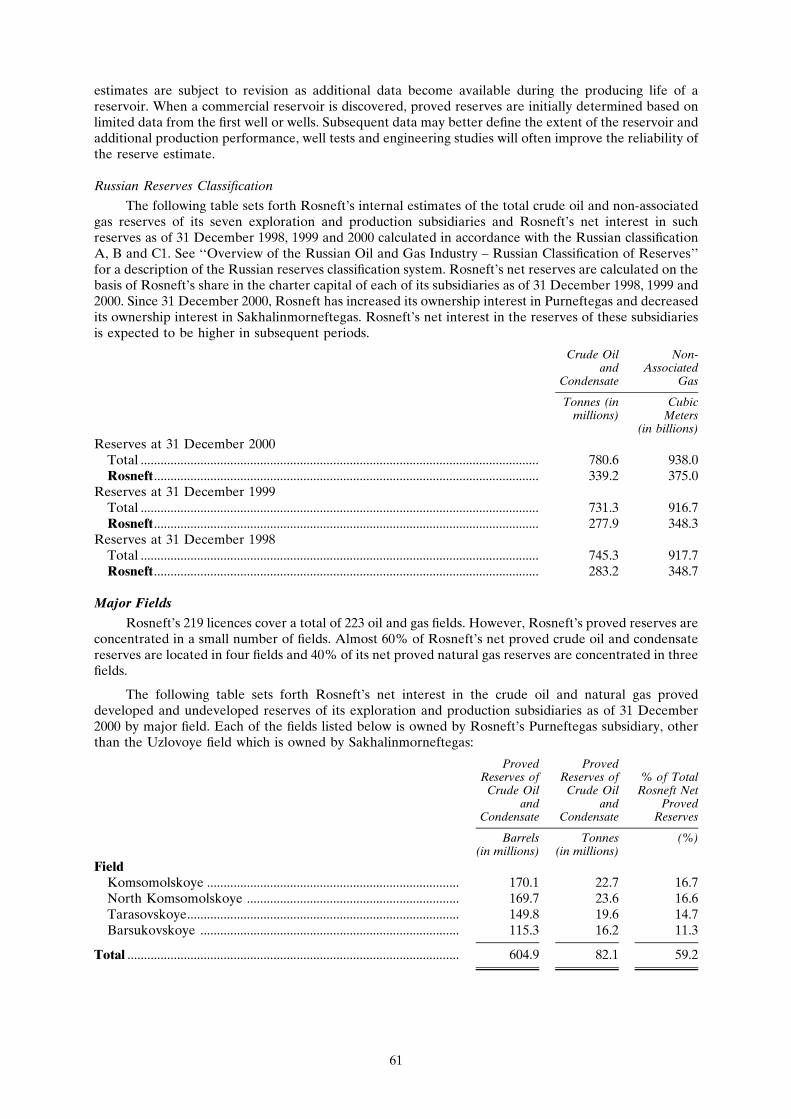

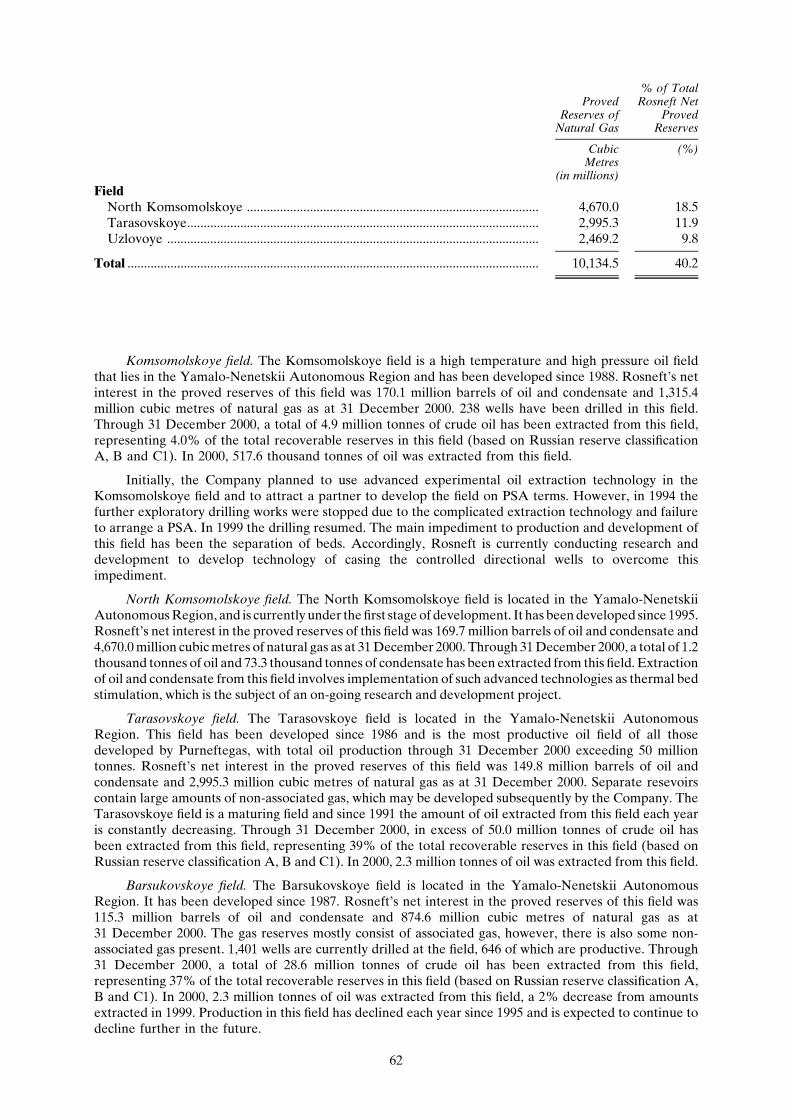

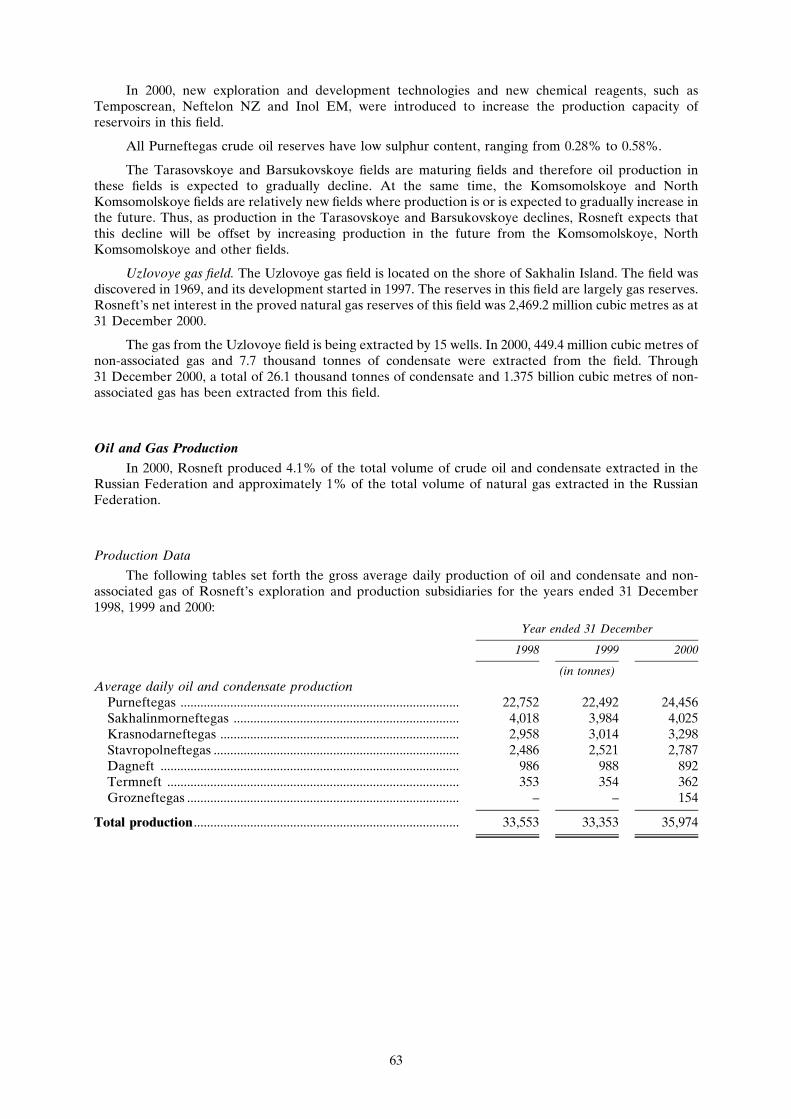

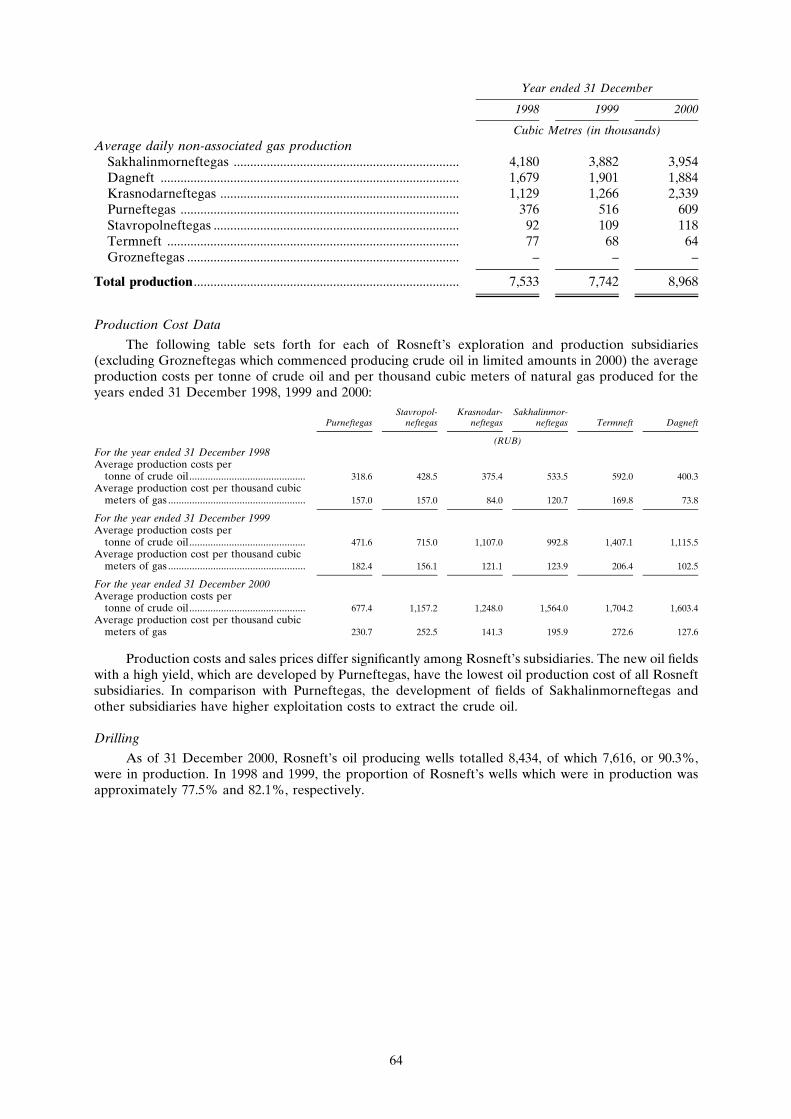

BUSINESS ........................................................................................................................................................ 57

ENVIRONMENTAL MATTERS ................................................................................................................ 77

LABOUR SAFETY ........................................................................................................................................ 78

LITIGATION.................................................................................................................................................... 79

INSURANCE.................................................................................................................................................... 80

JOINT VENTURES ........................................................................................................................................ 81

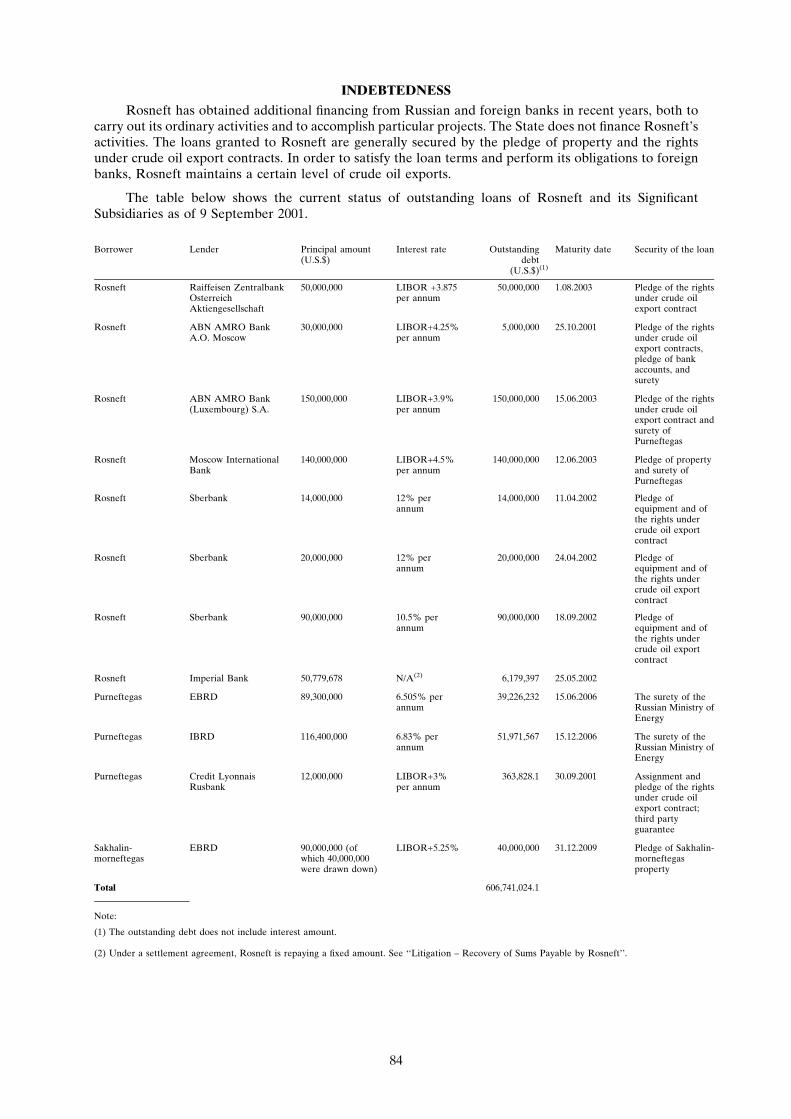

INDEBTEDNESS ............................................................................................................................................ 84

TAXES AND DUTIES ON OIL AND GAS ............................................................................................ 85

CHARTER CAPITAL AND SHAREHOLDERS.................................................................................... 87

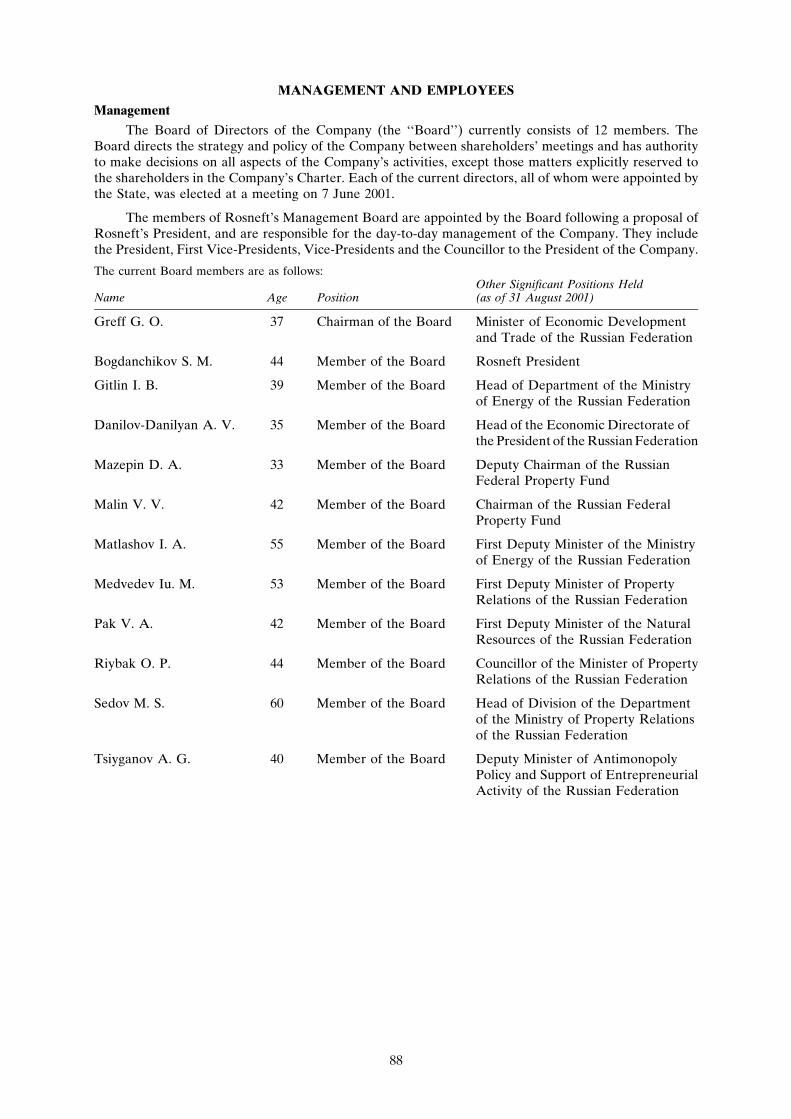

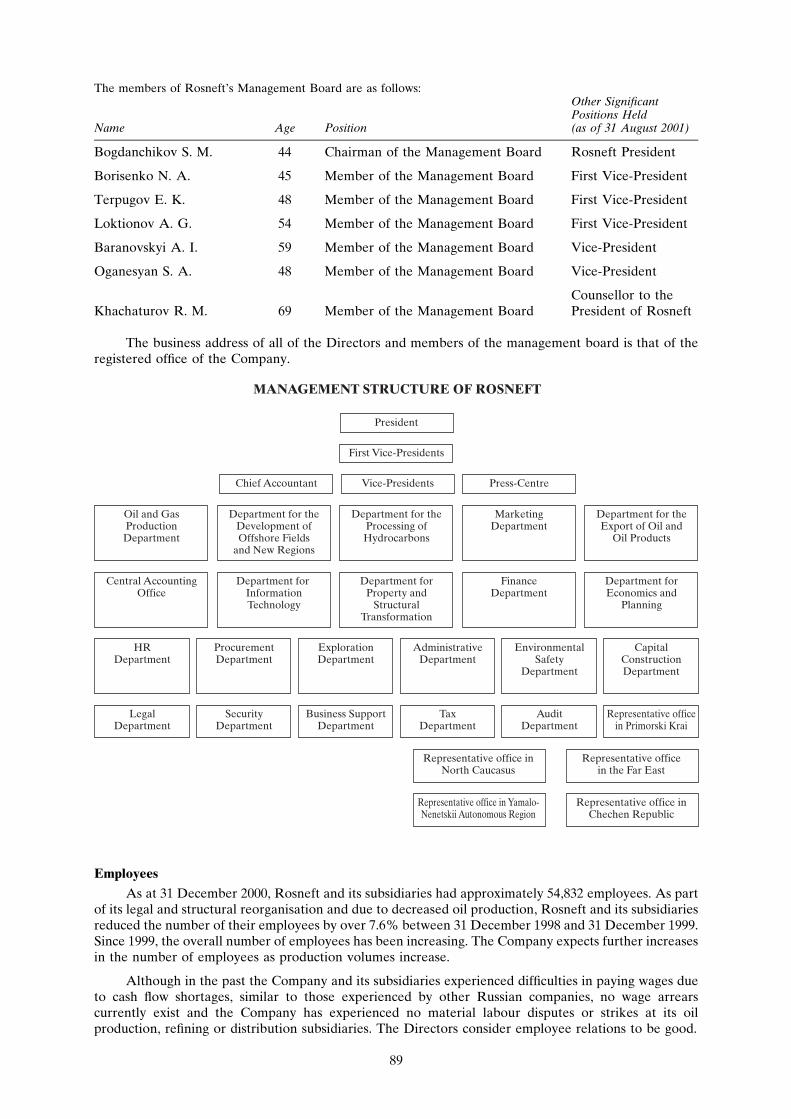

MANAGEMENT AND EMPLOYEES ...................................................................................................... 88

TERMS AND CONDITIONS OF THE NOTES ...................................................................................... 91

SUMMARY OF PROVISIONS OF THE NOTES WHILE IN GLOBAL FORM ............................ 103

LOAN AGREEMENT.................................................................................................................................... 104

ABN AMRO BANK (LUXEMBOURG) S.A. .......................................................................................... 133

TAXATION ...................................................................................................................................................... 134

CERTAIN ERISA CONSIDERATIONS.................................................................................................... 139

FORMS OF NOTES AND TRANSFER RESTRICTIONS.................................................................... 141

SUBSCRIPTION AND SALE ...................................................................................................................... 146

GENERAL INFORMATION ...................................................................................................................... 148

SUMMARY OF RELEVANT SIGNIFICANT DIFFERENCES BETWEENUS GAAP AND RUSSIAN ACCOUNTING REGULATIONS .......................................................... 149

FINANCIAL STATEMENTS AND AUDITORS’ REPORT ................................................................ F-1

APPENDIX A – RAR FINANCIAL STATEMENTS ............................................................................ A-1

3

In connection with this issue, ABN AMRO Bank N.V. may over-allot or effect transactions thatstabilise or maintain the market price of the Notes at a level that might not otherwise prevail. Suchstabilising, if commenced, may be discontinued at any time.

NOTICE TO NEW HAMPSHIRE RESIDENTS

NEITHER THE FACT THAT A REGISTRATION STATEMENT OR AN APPLICATIONFOR A LICENSE HAS BEEN FILED UNDER CHAPTER 421-B OF THE NEW HAMPSHIREREVISED STATUTES WITH THE STATE OF NEW HAMPSHIRE NOR THE FACT THAT ASECURITY IS EFFECTIVELY REGISTERED OR A PERSON IS LICENSED IN THE STATE OFNEW HAMPSHIRE CONSTITUTES A FINDING BY THE SECRETARY OF STATE OF NEWHAMPSHIRE THAT ANY DOCUMENT FILED UNDER RSA 421-B IS TRUE, COMPLETE ANDNOT MISLEADING. NEITHER ANY SUCH FACT NOR THE FACT THAT AN EXEMPTION OREXCEPTION IS AVAILABLE FOR A SECURITY OR TRANSACTION MEANS THAT THESECRETARY OF STATE HAS PASSED IN ANY WAY UPON THE MERITS ORQUALIFICATIONS OF, OR RECOMMENDED OR GIVEN APPROVAL TO, ANY PERSON,SECURITY OR TRANSACTION. IT IS UNLAWFUL TO MAKE, OR CAUSE TO BE MADE, TOANY PROSPECTIVE PURCHASER, CUSTOMER OR CLIENT ANY REPRESENTATIONINCONSISTENT WITH THE PROVISIONS OF THIS PARAGRAPH.

AVAILABLE INFORMATION

Each of the Company and the Bank have agreed that, for so long as any Notes are ‘‘restrictedsecurities’’ within the meaning of Rule 144(a)(3) under the Securities Act, it will, during any period inwhich it is neither subject to Section 13 or 15(d) of the U.S. Securities Exchange Act of 1934 (the‘‘Exchange Act’’) nor exempt from reporting pursuant to Rule 12g3-2(b) thereunder, provide to anyholder or beneficial owner of such restricted securities or to any prospective purchaser of such restrictedsecurities designated by such holder or beneficial owner or to the Trustee for delivery to such holder,beneficial owner or prospective purchaser, in each case upon the request of such holder, beneficial owner,prospective purchaser or Trustee, the information required to be provided by Rule 144A(d)(4) under theSecurities Act.

FORWARD-LOOKING STATEMENTS

This Offering Circular contains forward-looking statements that involve risks and uncertainties, inparticular under ‘‘Management’s Discussion and Analysis of Financial Condition and Results ofOperations’’ and ‘‘Business’’. In some cases, words such as ‘‘believe’’, ‘‘intend’’, ‘‘expect’’, ‘‘anticipate’’,‘‘plan’’, ‘‘target’’ and similar expressions are used to identify forward-looking statements. All statementsother than statements of historical facts, including, among others, statements regarding the Company’sfuture financial position, business strategy, budgets, reserve information, projected levels of capacity andproduction, projected costs, estimates of capital expenditure and plans and objectives of management forfuture operations, are forward-looking statements. Investors should not place undue reliance on theseforward-looking statements. The Company’s actual results could differ materially from those anticipatedin the forward-looking statements for many reasons, including the risks described above and elsewhere inthis Offering Circular.

Although the Company believes that the expectations reflected in the forward-looking statementsare reasonable, no assurance can be given that its future results, level of activity, performance orachievements will meet these expectations. Moreover, neither the Company nor any other personassumes responsibility for the accuracy and completeness of the forward-looking statements. Unlessrequired by law to update these statements, the Company will not necessarily update any of thesestatements after the date of this Offering Circular, either to conform them to actual results or to changesin its expectations.

4

ENFORCEABILITY OF JUDGMENTS

The Company is an open joint stock company organised under the laws of the Russian Federation.None of the directors and executive officers of the Company is a resident of the United States, and all or asubstantial portion of the assets of the Company and such persons are located outside the United States.As a result, it may not be possible for investors to effect service of process within the United States uponthe Company or such persons or to enforce against any of them in the United States courts judgmentsobtained in United States courts, including judgments predicated upon the civil liability provisions of thesecurities laws of the United States or any State or territory within the United States. Russian courts willnot enforce any judgment obtained in a court established in a country other than Russia unless there is atreaty in effect between such country and Russia providing for reciprocal recognition and enforcement ofcourt judgments. If there is such a treaty, Russian courts may nonetheless refuse to recognise and enforcea foreign court judgment on the grounds provided in such treaty and in Russian legislation in effect on thedate on which such recognition and enforcement are sought. It is expected that Russian procedurallegislation may be changed, inter alia, by way of inserting further grounds preventing foreign courtjudgments from being recognised and enforced in Russia.

5

FINANCIAL AND OTHER INFORMATION

This Offering Circular includes audited consolidated financial statements of the Company and itsconsolidated subsidiaries as of and for the years ended 31 December 1998, 1999 and 2000, audited byArthur Andersen ZAO (‘‘Arthur Andersen’’), independent certified public accountants, located at 52/2Kosmodamianskaya nab., 113054 Moscow, Russia. The consolidated financial statements as of and for theyears ended 31 December 1998, 1999 and 2000 (the ‘‘US GAAP Financial Statements’’) have beenprepared in accordance with United States generally accepted accounting principles (‘‘US GAAP’’).Arthur Andersen issued unqualified reports on the Company’s 2000 and 1999 US GAAP FinancialStatements, however, their opinion on the 1998 US GAAP Financial Statements was qualified withrespect to the fact that an independent reserve report was not available as at 31 December 1998. TheCompany does not currently prepare interim consolidated financial statements in accordance with USGAAP.

Additionally, this Offering Circular includes consolidated financial statements of the Company andits consolidated subsidiaries as of and for the years ended 31 December 1999 and 2000 and as of and forthe six month periods ended 30 June 2000 and 2001 (the ‘‘RAR Financial Statements’’), included inAppendix A of this Offering Circular. The RAR Financial Statements have been prepared in accordancewith the Regulations of Accounting and Reporting of the Russian Federation (‘‘RAR’’). The RARFinancial Statements as of and for the years ended 31 December 1999 and 2000 have been audited byArthur Andersen. The RAR Financial Statements as of and for the six month periods ended 30 June 2000and 2001 are unaudited.

Prospective investors should note that there are significant differences between US GAAP andRAR. For a discussion of the significant differences between US GAAP and RAR, see ‘‘Summary ofRelevant Significant Differences between US GAAP and Russian Accounting Regulations.’’

In this Offering Circular, all references to ‘‘Roubles’’ and ‘‘RUB’’ are to the lawful currency for thetime being of the Russian Federation and all references to ‘‘U.S. Dollars’’, ‘‘Dollars’’, ‘‘U.S.$’’ and ‘‘$’’are to the lawful currency for the time being of the United States of America.

6

SUMMARY

The following summary should be read in conjunction with, and is qualified in its entirety by referenceto, the more detailed information and financial statements and notes appearing elsewhere in this OfferingCircular. See ‘‘Risk Factors’’ for a discussion of certain factors that should be considered by potentialinvestors prior to an investment in the Notes.

Overview

Rosneft is a vertically integrated petroleum company with upstream, midstream and downstreamoperations based principally in Russia. Rosneft is active in the exploration and development of crude oiland natural gas fields.

As of 31 December 2000, Rosneft had net proved developed and undeveloped reserves in theRussian Federation of approximately 138.9 million tonnes of crude oil and condensate (or 1,021.6 millionbarrels) and 25,182.3 million cubic metres of natural gas (which includes associated and non-associated gas).

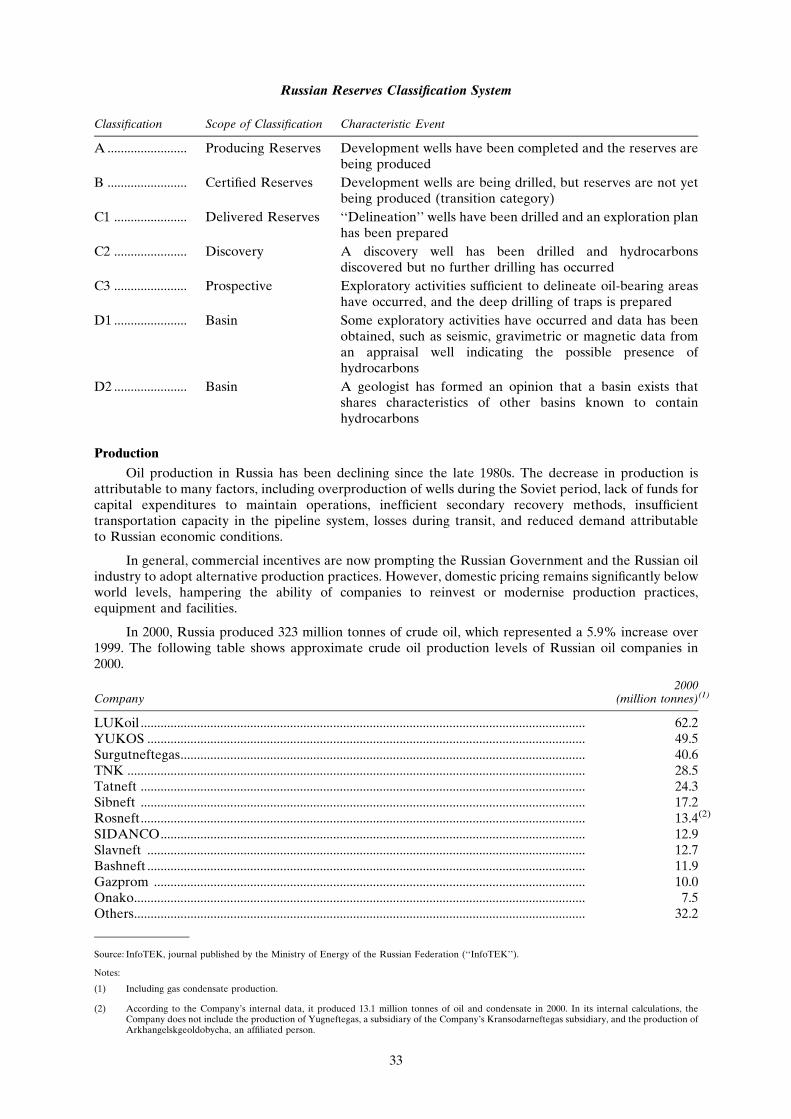

In 2000, Rosneft’s production subsidiaries produced 13,117 thousand tonnes of crude oil andcondensate, representing 4.1% of the total production of crude oil and condensate in the RussianFederation in 2000 and making Rosneft the seventh largest Russian oil producer. In 2000, Rosneftpurchased 76% of the crude oil produced by its subsidiaries. Rosneft also purchases crude oil from otherRussian producers. The oil purchased from Rosneft’s production subsidiaries and third parties is (1)exported, (2) consumed or used internally as feedstock in Rosneft’s refining operations, (3) sold to thirdparties in the Russian Federation and (4) delivered to third party refiners in Russia who process the crudeinto refined products for Rosneft. Rosneft’s share in total Russian exports of crude oil in 2000 was 5.6%.Rosneft produced 5,581.6 million cubic metres of gas in 2000, representing approximately 1% of the totalproduction of natural gas in the Russian Federation. Of the amount, 3,282.5 million cubic metres wasnon-associated gas.

Rosneft is one of the major refiners of petroleum products in the Russian Federation. Rosneftoperates two crude oil refineries and a specialised refinery which produces a number of lubricants andoils. In 2000, Rosneft’s refineries processed 7,097,500 tonnes of crude oil, making Rosneft the tenthlargest refiner in the Russian Federation in 2000 on the basis of crude oil processed. Rosneft’s refineriesproduce gasoline, diesel, jet fuel, fuel oil and other refined products. Rosneft’s two crude oil refineriesoperated at 84% and 62% of capacity, respectively, in 2000. In addition, Rosneft delivers a portion of thecrude oil it purchases from its production subsidiaries to third party refineries that process the crude intorefined products on behalf of Rosneft for a fee. These refined products, together with the refined productoutput from Rosneft’s refineries and refined products purchased from unaffiliated parties, are sold towholesale customers in the Russian Federation, through Rosneft’s retail network of service stations andare also sold for export. Rosneft’s refineries also process crude oil on behalf of other Russian oilproduction companies who pay a processing fee to Rosneft’s refineries for processing their crude oil intorefined products.

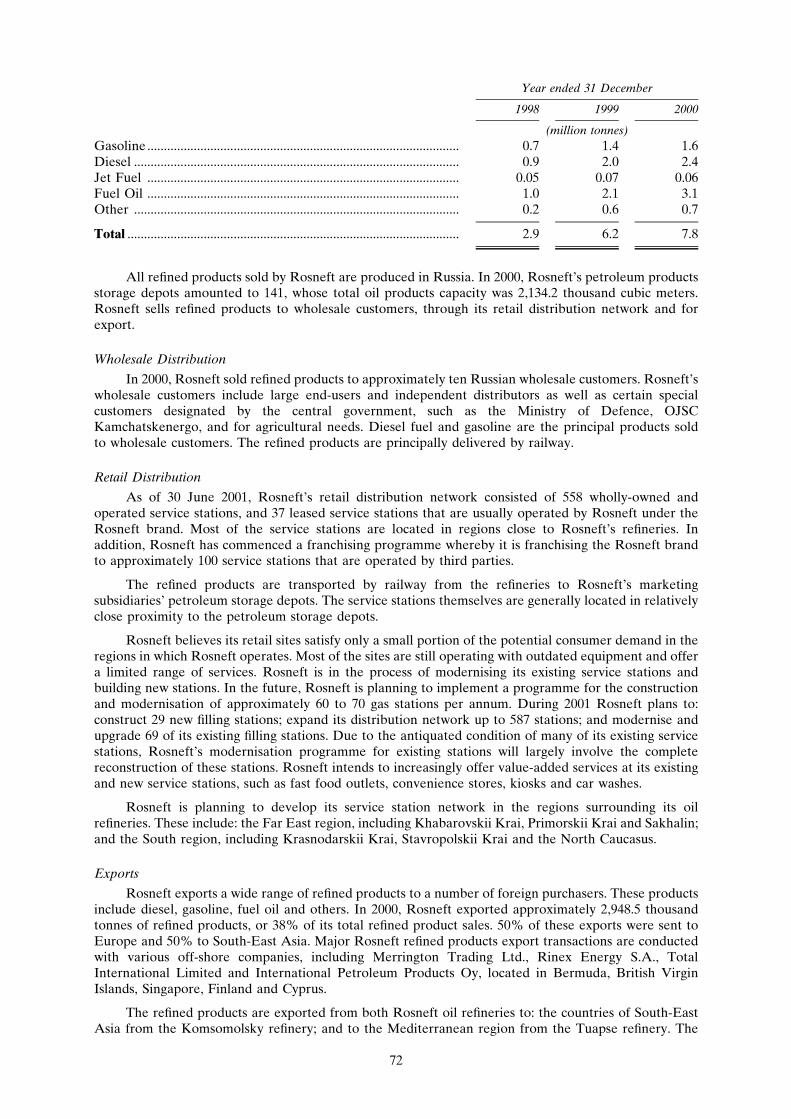

Rosneft has one of the largest distribution networks for refined products in the Russian Federationconsisting of 89 petroleum storage depots and approximately 558 operational retail service stations(which also offer storage services) as of 30 June 2001. Rosneft has also started franchising the Rosneftbrand to approximately 100 service stations that are operated by third parties. This distribution networkcovers 13 constituent entities of the Russian Federation, which are located in Western Siberia, SakhalinIsland, North Caucasus and the Arctic regions of Russia. Rosneft also sells its refined products through itswholesale distribution network.

Business Strategy

Rosneft’s long-term strategy is to reinforce its position as a leading Russian vertically integrated oiland gas company by increasing its production, refining and marketing of oil and gas in Russia anddeveloping its international operations. The key elements of this strategy include the following:

Increasing production of oil and gas in Russia. Rosneft aims to increase its oil and gas production byapproximately 5% per annum by: (i) increasing the yield of its existing fields by recommencingproduction from inactive wells and employing improved extraction and bed stimulation technologies, (ii)improving the efficiency of its producing wells by reducing idle periods and bolstering well maintenanceand workover programmes, (iii) participating in major new oil field development projects, particularly inWestern Siberia and off Sakhalin Island (including through participation in production sharing

7

arrangements and joint ventures with international oil companies to manage operational and financialrisks associated therewith) and (iv) continuing to drill new wells and pursue the acquisition of additionalreserves. In addition, over the next five to ten years Rosneft aims to substantially increase the proportionof its total revenues generated by the production and sale of natural gas, with a particular focus on servingthe growing markets of the Russian Far East, Japan, Korea and China.

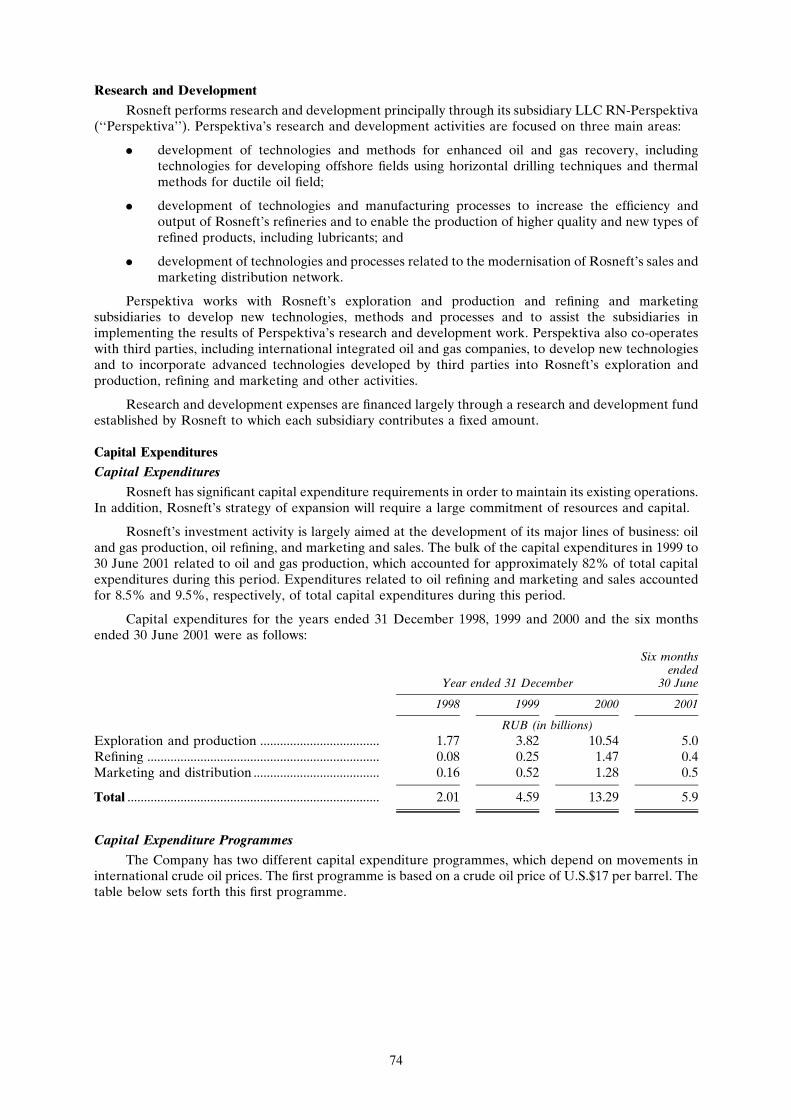

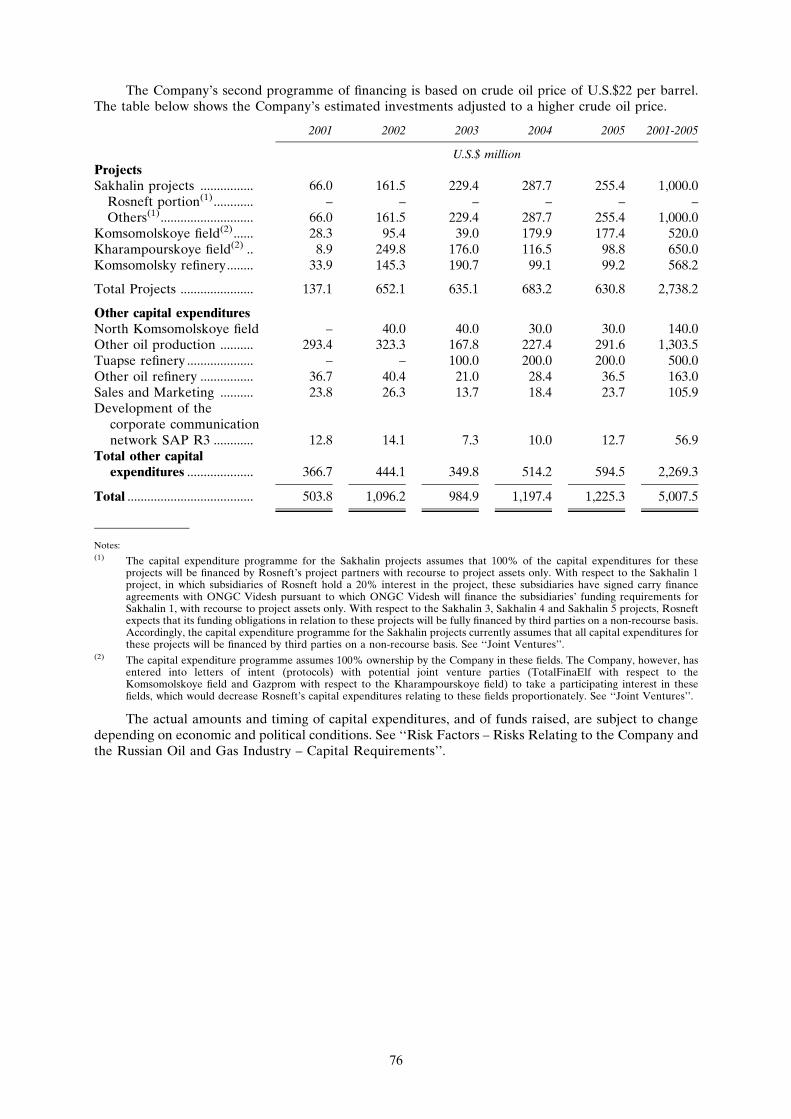

Improving its refining and marketing operations. Rosneft intends to invest substantially in themodernisation of its existing refineries in order to (i) increase refining capacity and improve capacityutilisation, (ii) broaden the range of lighter and higher-value refined products produced and (iii) ensurethat products can meet increasingly stringent environmental requirements in Russian and overseasmarkets. In addition, Rosneft plans to upgrade and expand its network of retail service stations in certainregions in Russia so as to secure additional domestic distribution channels for its expanded refineryoutput and derive additional margins from the sale of refined products. The minimum investmentprogramme is expected to be implemented by Rosneft if the crude oil price does not fall under U.S.$17per barrel, and the maximum planned investment programme is expected to be implemented by Rosneftif the crude oil price maintains a level of U.S.$22 per barrel.

Developing its international and other operations. With a view to broadening its reserve base,Rosneft will seek to identify international opportunities and to participate, together with foreign jointventure partners, in the exploration and development of oil and gas fields outside Russia. In the longterm, Rosneft may consider investing in other fuel and energy businesses in Russia with a view tostrengthening its overall position in the Russian energy market.

Enhancing financial controls and improving efficiency of corporate governance. Rosneft intends toimprove its financial controls and risk management so as to be able to manage more precisely theoperational and financial risks associated with its business. In addition, Rosneft will seek to ensure that itslenders and investors benefit from financial and accounting transparency (through the adoption ofinternational accounting practices by all members of its group and more regular consolidated financialreporting). Rosneft also intends to improve the flexibility of its corporate organisational structure,improve its investment planning system, introduce a cost management and financial risk managementsystem and install a SAP R/3 corporate management information system.

Developing new technologies. Rosneft plans to continue investing in proprietary research anddevelopment projects and to otherwise seek out new technologies which will enable it to improve oil andgas production, ensure maintenance of high standards of environmental safety and reduce the negativeimpact on the environment of exploration and production activities.

Summary Consolidated Financial and Statistical Data

The following tables set forth summary consolidated financial and statistical data of Rosneft underUS GAAP and RAR. For a discussion of the significant differences between US GAAP and RAR, see‘‘Summary of Relevant Significant Differences between US GAAP and Russian AccountingRegulations’’.

US GAAP Financial and Statistical Data

The following summary consolidated financial data presented below should be read together withthe US GAAP Financial Statements, including the notes thereto, and ‘‘Management’s Discussion andAnalysis of Financial Condition and Results of Operations’’ included elsewhere in this Offering Circular.

The summary consolidated financial data presented below has been derived from the US GAAPFinancial Statements as of and for the years ended 31 December 1998, 1999 and 2000 included elsewherein this Offering Circular. The US GAAP Financial Statements have been prepared in accordance withUS GAAP. The US GAAP Financial Statements have been audited by Arthur Andersen. ArthurAndersen issued unqualified reports on the Company’s 2000 and 1999 US GAAP Financial Statements,however, their opinion on the 1998 US GAAP Financial Statements was qualified with respect to the factthat an independent reserve report was not available as at 31 December 1998.

8

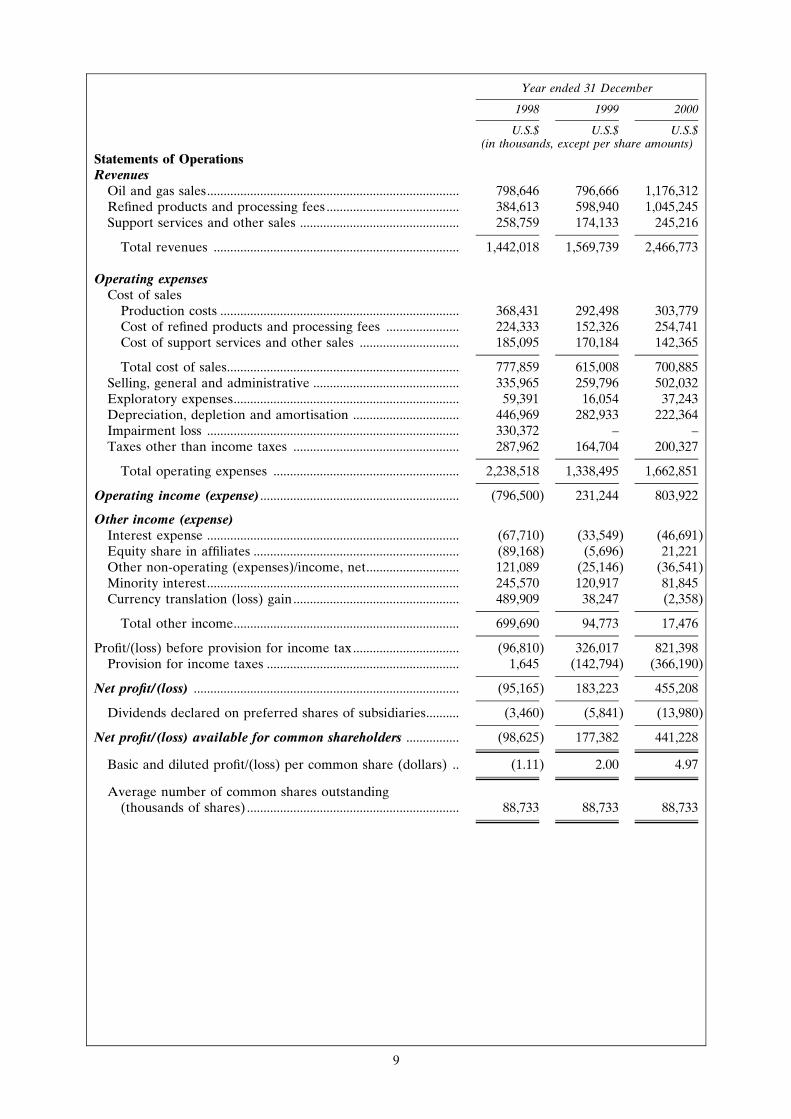

Year ended 31 December

1998 1999 2000

U.S.$ U.S.$ U.S.$(in thousands, except per share amounts)

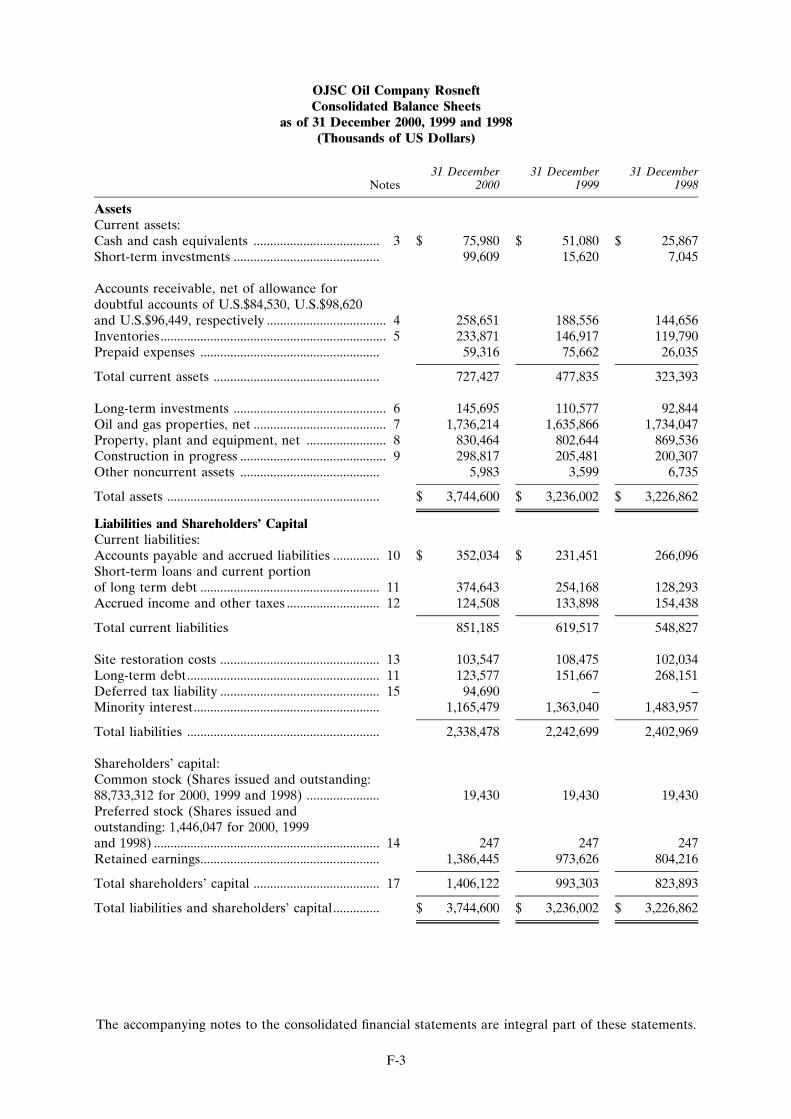

Statements of OperationsRevenues

Oil and gas sales............................................................................ 798,646 796,666 1,176,312Refined products and processing fees ........................................ 384,613 598,940 1,045,245Support services and other sales ................................................ 258,759 174,133 245,216

Total revenues .......................................................................... 1,442,018 1,569,739 2,466,773

Operating expensesCost of sales

Production costs ........................................................................ 368,431 292,498 303,779Cost of refined products and processing fees ...................... 224,333 152,326 254,741Cost of support services and other sales .............................. 185,095 170,184 142,365

Total cost of sales...................................................................... 777,859 615,008 700,885Selling, general and administrative ............................................ 335,965 259,796 502,032Exploratory expenses.................................................................... 59,391 16,054 37,243Depreciation, depletion and amortisation ................................ 446,969 282,933 222,364Impairment loss ............................................................................ 330,372 – –Taxes other than income taxes .................................................. 287,962 164,704 200,327

Total operating expenses ........................................................ 2,238,518 1,338,495 1,662,851

Operating income (expense) ............................................................ (796,500) 231,244 803,922

Other income (expense)Interest expense ............................................................................ (67,710) (33,549) (46,691)Equity share in affiliates .............................................................. (89,168) (5,696) 21,221Other non-operating (expenses)/income, net............................ 121,089 (25,146) (36,541)Minority interest............................................................................ 245,570 120,917 81,845Currency translation (loss) gain.................................................. 489,909 38,247 (2,358)

Total other income.................................................................... 699,690 94,773 17,476

Profit/(loss) before provision for income tax ................................ (96,810) 326,017 821,398Provision for income taxes .......................................................... 1,645 (142,794) (366,190)

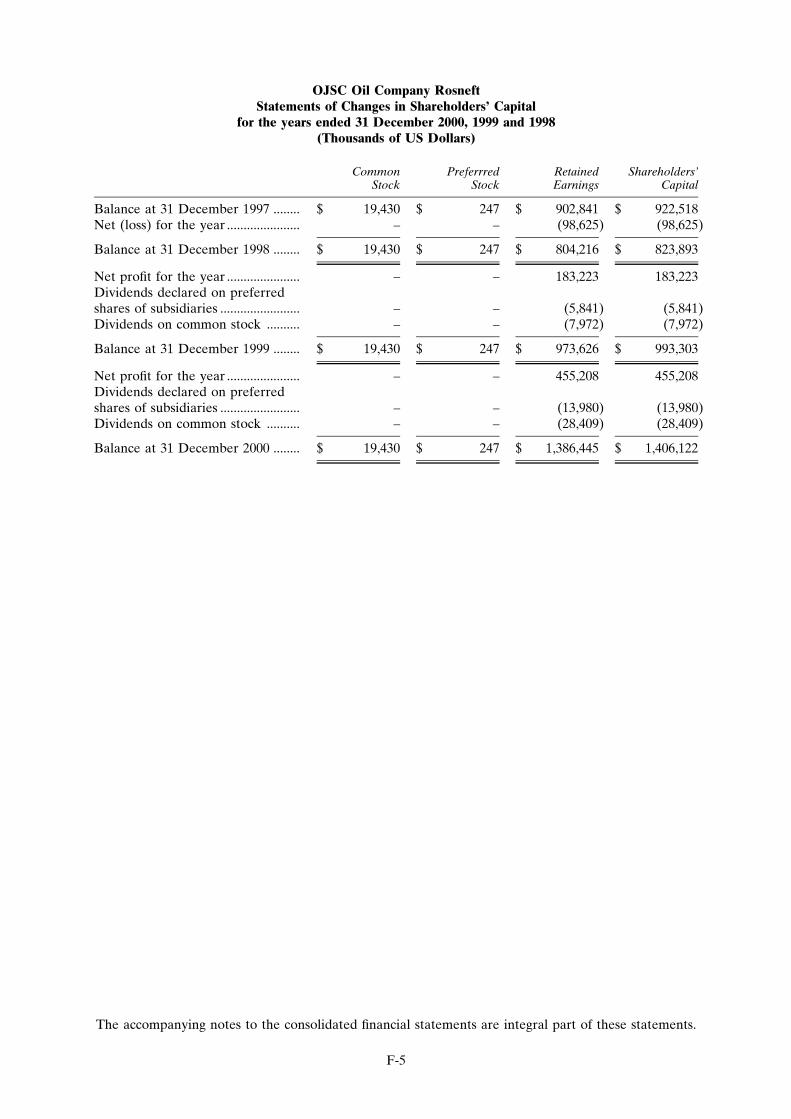

Net profit/(loss) ................................................................................ (95,165) 183,223 455,208

Dividends declared on preferred shares of subsidiaries.......... (3,460) (5,841) (13,980)

Net profit/(loss) available for common shareholders ................ (98,625) 177,382 441,228

Basic and diluted profit/(loss) per common share (dollars) .. (1.11) 2.00 4.97

Average number of common shares outstanding(thousands of shares) ................................................................ 88,733 88,733 88,733

9

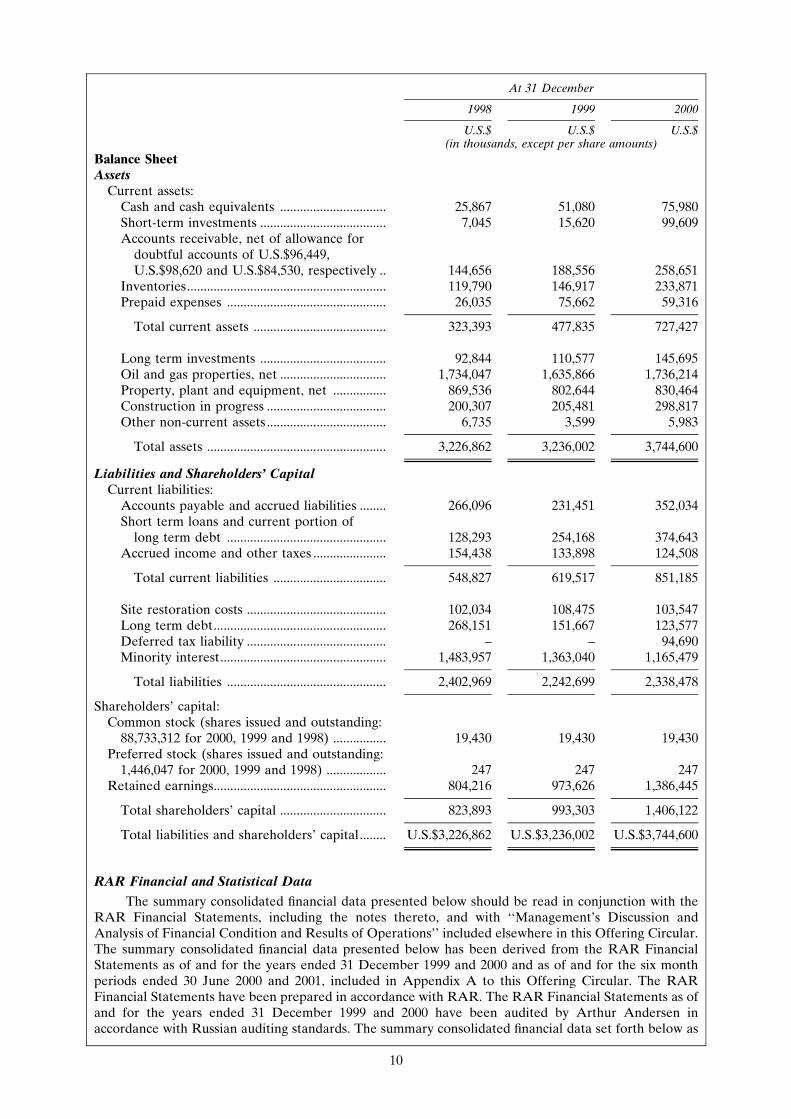

At 31 December

1998 1999 2000

U.S.$ U.S.$ U.S.$(in thousands, except per share amounts)

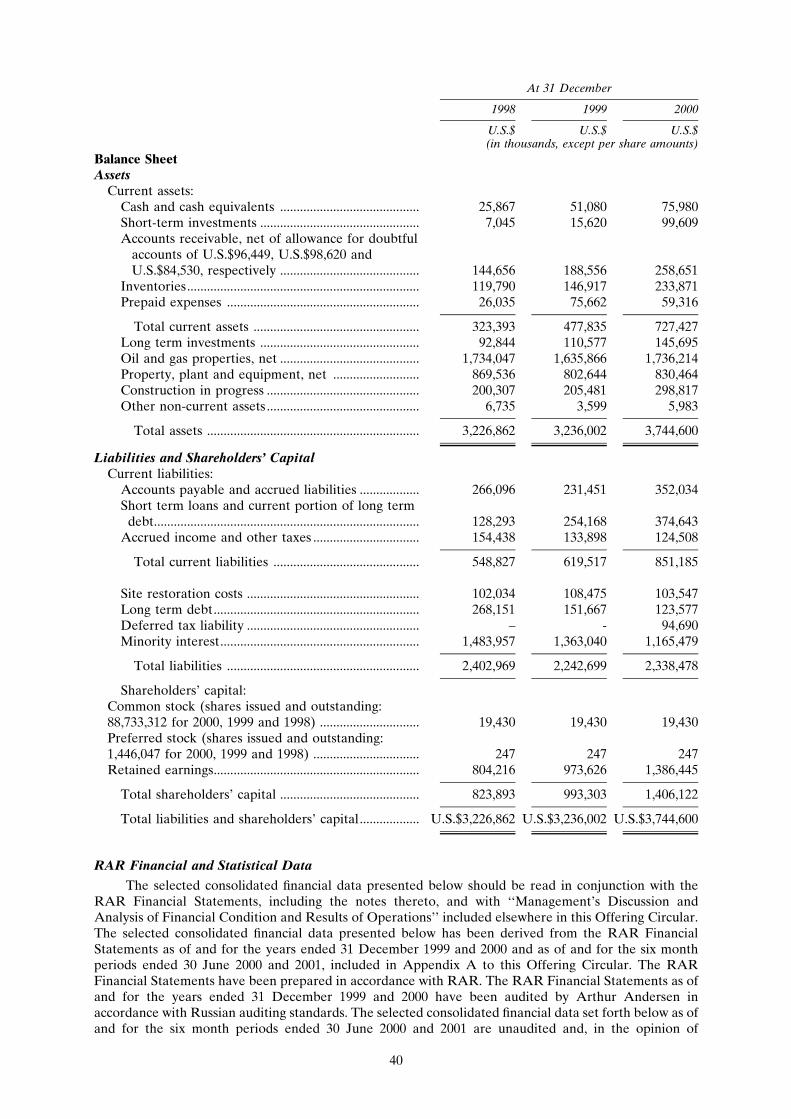

Balance SheetAssets

Current assets:Cash and cash equivalents ................................ 25,867 51,080 75,980Short-term investments ...................................... 7,045 15,620 99,609Accounts receivable, net of allowance for

doubtful accounts of U.S.$96,449,U.S.$98,620 and U.S.$84,530, respectively .. 144,656 188,556 258,651

Inventories............................................................ 119,790 146,917 233,871Prepaid expenses ................................................ 26,035 75,662 59,316

Total current assets ........................................ 323,393 477,835 727,427

Long term investments ...................................... 92,844 110,577 145,695Oil and gas properties, net ................................ 1,734,047 1,635,866 1,736,214Property, plant and equipment, net ................ 869,536 802,644 830,464Construction in progress .................................... 200,307 205,481 298,817Other non-current assets .................................... 6,735 3,599 5,983

Total assets ...................................................... 3,226,862 3,236,002 3,744,600

Liabilities and Shareholders’ CapitalCurrent liabilities:

Accounts payable and accrued liabilities ........ 266,096 231,451 352,034Short term loans and current portion of

long term debt ................................................ 128,293 254,168 374,643Accrued income and other taxes ...................... 154,438 133,898 124,508

Total current liabilities .................................. 548,827 619,517 851,185

Site restoration costs .......................................... 102,034 108,475 103,547Long term debt.................................................... 268,151 151,667 123,577Deferred tax liability .......................................... – – 94,690Minority interest.................................................. 1,483,957 1,363,040 1,165,479

Total liabilities ................................................ 2,402,969 2,242,699 2,338,478

Shareholders’ capital:Common stock (shares issued and outstanding:

88,733,312 for 2000, 1999 and 1998) ................ 19,430 19,430 19,430Preferred stock (shares issued and outstanding:

1,446,047 for 2000, 1999 and 1998) .................. 247 247 247Retained earnings.................................................... 804,216 973,626 1,386,445

Total shareholders’ capital ................................ 823,893 993,303 1,406,122

Total liabilities and shareholders’ capital........ U.S.$3,226,862 U.S.$3,236,002 U.S.$3,744,600

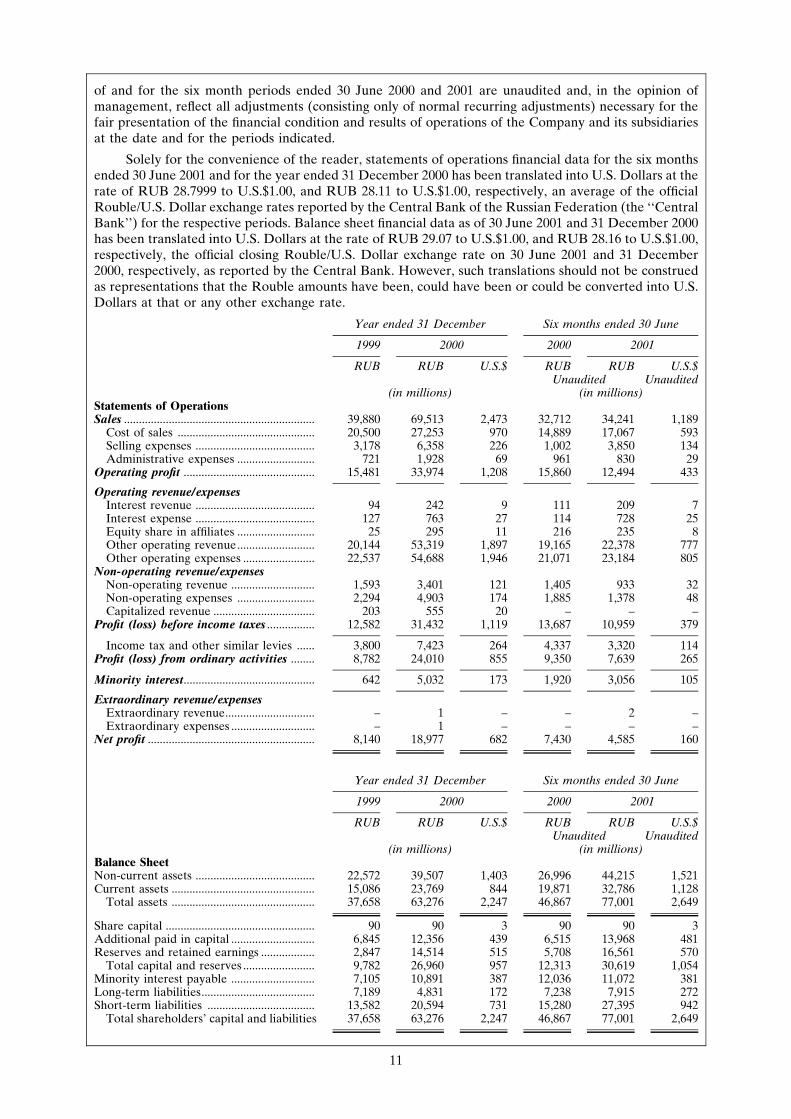

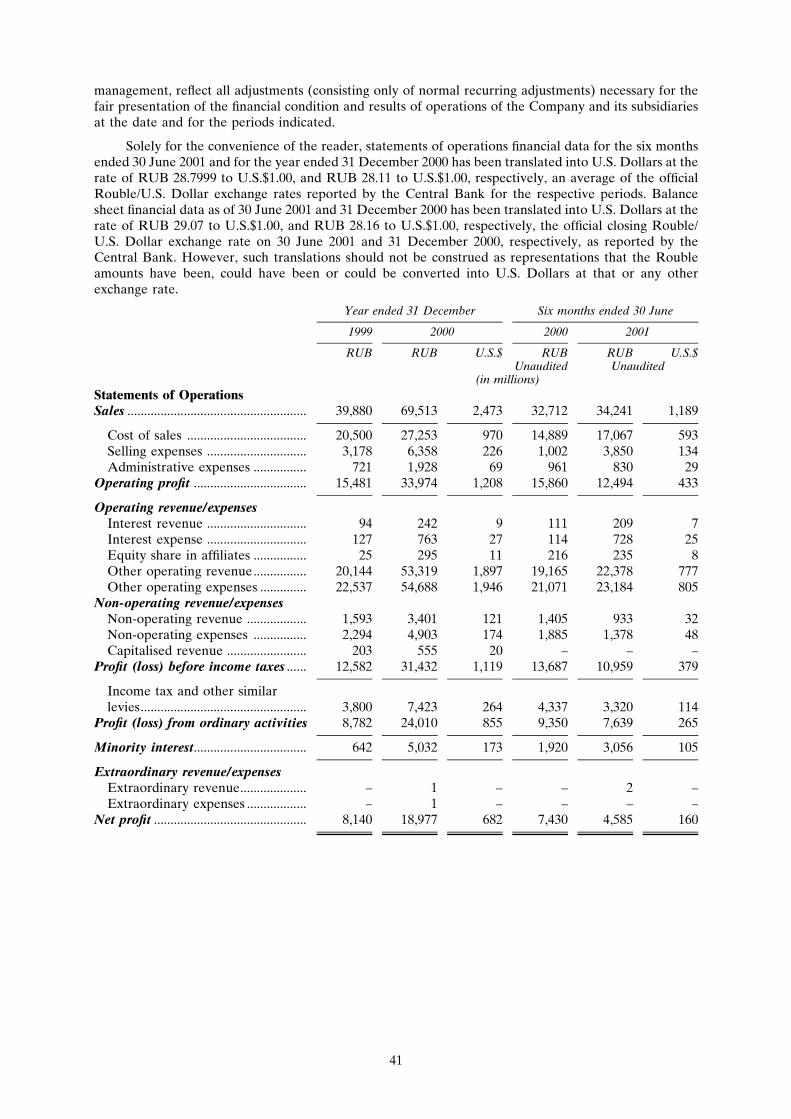

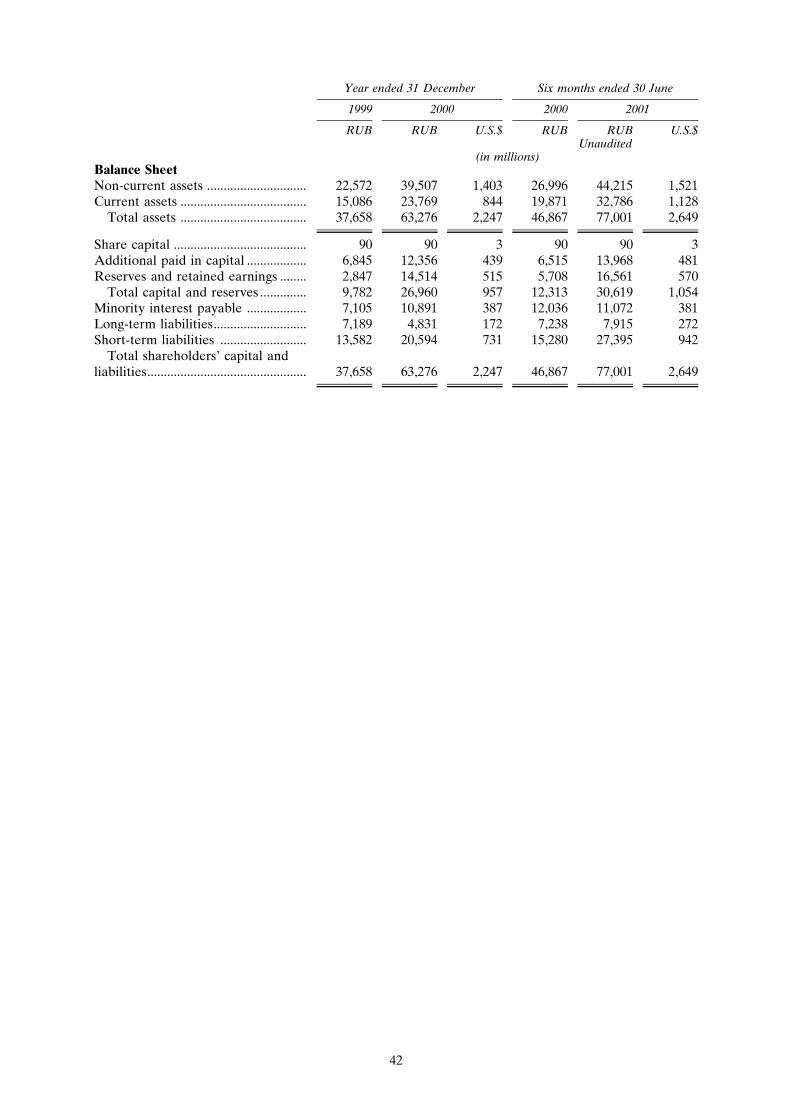

RAR Financial and Statistical Data

The summary consolidated financial data presented below should be read in conjunction with theRAR Financial Statements, including the notes thereto, and with ‘‘Management’s Discussion andAnalysis of Financial Condition and Results of Operations’’ included elsewhere in this Offering Circular.The summary consolidated financial data presented below has been derived from the RAR FinancialStatements as of and for the years ended 31 December 1999 and 2000 and as of and for the six monthperiods ended 30 June 2000 and 2001, included in Appendix A to this Offering Circular. The RARFinancial Statements have been prepared in accordance with RAR. The RAR Financial Statements as ofand for the years ended 31 December 1999 and 2000 have been audited by Arthur Andersen inaccordance with Russian auditing standards. The summary consolidated financial data set forth below as

10

of and for the six month periods ended 30 June 2000 and 2001 are unaudited and, in the opinion ofmanagement, reflect all adjustments (consisting only of normal recurring adjustments) necessary for thefair presentation of the financial condition and results of operations of the Company and its subsidiariesat the date and for the periods indicated.

Solely for the convenience of the reader, statements of operations financial data for the six monthsended 30 June 2001 and for the year ended 31 December 2000 has been translated into U.S. Dollars at therate of RUB 28.7999 to U.S.$1.00, and RUB 28.11 to U.S.$1.00, respectively, an average of the officialRouble/U.S. Dollar exchange rates reported by the Central Bank of the Russian Federation (the ‘‘CentralBank’’) for the respective periods. Balance sheet financial data as of 30 June 2001 and 31 December 2000has been translated into U.S. Dollars at the rate of RUB 29.07 to U.S.$1.00, and RUB 28.16 to U.S.$1.00,respectively, the official closing Rouble/U.S. Dollar exchange rate on 30 June 2001 and 31 December2000, respectively, as reported by the Central Bank. However, such translations should not be construedas representations that the Rouble amounts have been, could have been or could be converted into U.S.Dollars at that or any other exchange rate.

Year ended 31 December Six months ended 30 June

1999 2000 2000 2001

RUB RUB U.S.$ RUB RUB U.S.$Unaudited Unaudited

(in millions) (in millions)Statements of OperationsSales ................................................................ 39,880 69,513 2,473 32,712 34,241 1,189

Cost of sales .............................................. 20,500 27,253 970 14,889 17,067 593Selling expenses ........................................ 3,178 6,358 226 1,002 3,850 134Administrative expenses .......................... 721 1,928 69 961 830 29

Operating profit ............................................ 15,481 33,974 1,208 15,860 12,494 433

Operating revenue/expensesInterest revenue ........................................ 94 242 9 111 209 7Interest expense ........................................ 127 763 27 114 728 25Equity share in affiliates .......................... 25 295 11 216 235 8Other operating revenue.......................... 20,144 53,319 1,897 19,165 22,378 777Other operating expenses ........................ 22,537 54,688 1,946 21,071 23,184 805

Non-operating revenue/expensesNon-operating revenue ............................ 1,593 3,401 121 1,405 933 32Non-operating expenses .......................... 2,294 4,903 174 1,885 1,378 48Capitalized revenue .................................. 203 555 20 – – –

Profit (loss) before income taxes ................ 12,582 31,432 1,119 13,687 10,959 379

Income tax and other similar levies ...... 3,800 7,423 264 4,337 3,320 114Profit (loss) from ordinary activities ........ 8,782 24,010 855 9,350 7,639 265

Minority interest............................................ 642 5,032 173 1,920 3,056 105

Extraordinary revenue/expensesExtraordinary revenue.............................. – 1 – – 2 –Extraordinary expenses ............................ – 1 – – – –

Net profit ........................................................ 8,140 18,977 682 7,430 4,585 160

Year ended 31 December Six months ended 30 June

1999 2000 2000 2001

RUB RUB U.S.$ RUB RUB U.S.$Unaudited Unaudited

(in millions) (in millions)Balance SheetNon-current assets ........................................ 22,572 39,507 1,403 26,996 44,215 1,521Current assets ................................................ 15,086 23,769 844 19,871 32,786 1,128

Total assets ................................................ 37,658 63,276 2,247 46,867 77,001 2,649

Share capital .................................................. 90 90 3 90 90 3Additional paid in capital ............................ 6,845 12,356 439 6,515 13,968 481Reserves and retained earnings .................. 2,847 14,514 515 5,708 16,561 570

Total capital and reserves ........................ 9,782 26,960 957 12,313 30,619 1,054Minority interest payable ............................ 7,105 10,891 387 12,036 11,072 381Long-term liabilities...................................... 7,189 4,831 172 7,238 7,915 272Short-term liabilities .................................... 13,582 20,594 731 15,280 27,395 942

Total shareholders’ capital and liabilities 37,658 63,276 2,247 46,867 77,001 2,649

11

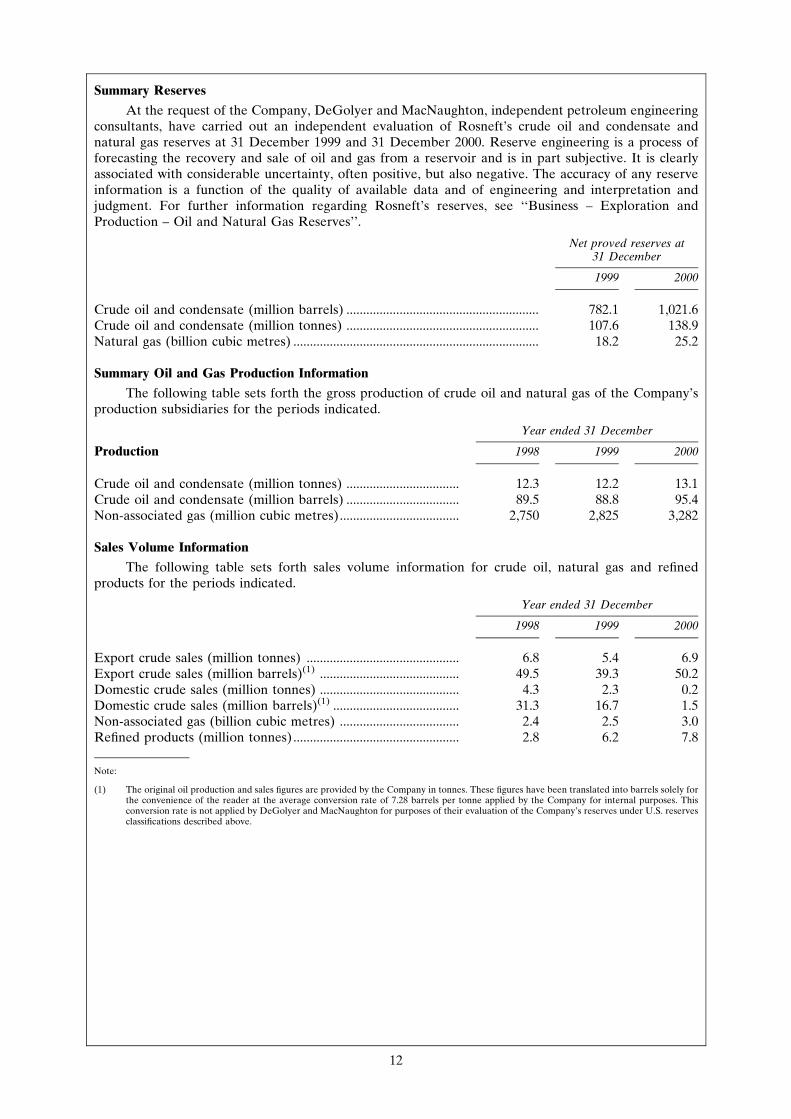

Summary Reserves

At the request of the Company, DeGolyer and MacNaughton, independent petroleum engineeringconsultants, have carried out an independent evaluation of Rosneft’s crude oil and condensate andnatural gas reserves at 31 December 1999 and 31 December 2000. Reserve engineering is a process offorecasting the recovery and sale of oil and gas from a reservoir and is in part subjective. It is clearlyassociated with considerable uncertainty, often positive, but also negative. The accuracy of any reserveinformation is a function of the quality of available data and of engineering and interpretation andjudgment. For further information regarding Rosneft’s reserves, see ‘‘Business – Exploration andProduction – Oil and Natural Gas Reserves’’.

Net proved reserves at31 December

1999 2000

Crude oil and condensate (million barrels) .......................................................... 782.1 1,021.6Crude oil and condensate (million tonnes) .......................................................... 107.6 138.9Natural gas (billion cubic metres) .......................................................................... 18.2 25.2

Summary Oil and Gas Production Information

The following table sets forth the gross production of crude oil and natural gas of the Company’sproduction subsidiaries for the periods indicated.

Year ended 31 December

Production 1998 1999 2000

Crude oil and condensate (million tonnes) .................................. 12.3 12.2 13.1Crude oil and condensate (million barrels) .................................. 89.5 88.8 95.4Non-associated gas (million cubic metres).................................... 2,750 2,825 3,282

Sales Volume Information

The following table sets forth sales volume information for crude oil, natural gas and refinedproducts for the periods indicated.

Year ended 31 December

1998 1999 2000

Export crude sales (million tonnes) .............................................. 6.8 5.4 6.9Export crude sales (million barrels)(1) .......................................... 49.5 39.3 50.2Domestic crude sales (million tonnes) .......................................... 4.3 2.3 0.2Domestic crude sales (million barrels)(1) ...................................... 31.3 16.7 1.5Non-associated gas (billion cubic metres) .................................... 2.4 2.5 3.0Refined products (million tonnes) .................................................. 2.8 6.2 7.8

Note:

(1) The original oil production and sales figures are provided by the Company in tonnes. These figures have been translated into barrels solely forthe convenience of the reader at the average conversion rate of 7.28 barrels per tonne applied by the Company for internal purposes. Thisconversion rate is not applied by DeGolyer and MacNaughton for purposes of their evaluation of the Company’s reserves under U.S. reservesclassifications described above.

12

DESCRIPTION OF THE TRANSACTION AND THE SECURITY

The following summary description should be read in conjunction with, and is qualified in its entiretyby, the Terms and Conditions of the Notes and the provisions of the Loan Agreement appearing elsewherein this Offering Circular.

The transaction will be structured as a loan to Rosneft by the Bank. The Bank will issue the Noteswhich will be limited recourse loan participation notes issued for the sole purpose of funding the Loan toRosneft. The Notes will be constituted by, be subject to, and have the benefit of, the Trust Deed. Theobligations of the Bank to make payments under the Notes shall constitute an obligation only to pay tothe Noteholders an amount equal to and in the same currency as sums of principal, interest and/oradditional amounts (if any) actually received by or for the account of the Bank pursuant to the LoanAgreement less any amount in respect of the Reserved Rights (as further described under ‘‘Terms andConditions of the Notes’’).

As provided in the Trust Deed, the Bank will charge in favour of the Trustee for the benefit of theNoteholders as security for its payment obligations in respect of the Notes (a) its rights to principal,interest and additional amounts (if any) as lender under the Loan Agreement and (b) amounts receivedpursuant to the Loan in an account with The Bank of New York, in the name of the Bank together withthe debt represented thereby (other than interest from time to time earned thereon) (the ‘‘Account’’), ineach case other than certain amounts in respect of the Reserved Rights. The Bank will assign certainadministrative rights under the Loan Agreement to the Trustee. The Borrower will be obliged to makepayments under the Loan (other than in respect of the Reserved Rights) to the Bank in accordance withthe terms of the Loan Agreement to the Account.

The Bank will covenant not to agree to any amendments to or any modification or waiver of, orauthorise or any breach or potential breach of, the terms of the Loan Agreement unless the Trustee hasgiven its prior written consent (except in relation to the Reserved Rights). The Bank will further agree toact at all times in accordance with any instructions of the Trustee from time to time with respect to theLoan Agreement (subject to being indemnified and/or secured to its satisfaction), save as otherwiseprovided in the Trust Deed and except in relation to the Reserved Rights. Any amendments,modifications, waivers or authorisations made with the Trustee’s consent shall be notified to theNoteholders in accordance with Condition 12 (Notices) of the Terms and Conditions relating to the Notesand shall be binding on the Noteholders.

The security under the Trust Deed will become enforceable upon the occurrence of a RelevantEvent, as further described in the Terms and Conditions of the Notes.

Payments in respect of the Notes will, except in certain limited circumstances, be made without anydeduction or withholding for or on account of Luxembourg taxes except as required by law. See ‘‘Termsand Conditions of the Notes – Taxation’’. In that event, the Bank will only be required to pay additionalamounts to the extent that it receives corresponding amounts under the Loan Agreement. The LoanAgreement provides for the Borrower to pay such corresponding amounts in these circumstances. Inaddition, payments under the Loan Agreement shall, except in certain limited circumstances, be madewithout any deduction or withholding for or on account of Russian taxes, except as required by law, inwhich event the Borrower will be obliged to increase the amounts payable under the Loan Agreement.See ‘‘Risk Factors – Risks Relating to the Notes – Taxation’’.

In certain circumstances (including in certain circumstances following enforcement of the securityupon a Relevant Event) the Loan may be prepaid at its principal amount, together with accrued interest,at the option of the Borrower upon the Borrower being required to increase the amount payable or to payadditional amounts on account of Russian or Luxembourg taxes pursuant to the Loan Agreement orrequired to pay additional amounts on account of certain costs incurred by the Bank. The Bank may (inits own discretion) require the Loan to be prepaid if it becomes unlawful for the Loan or the Notes to

13

remain outstanding, as set out in the Loan Agreement. In addition, in the event of a Change of Control(as defined in ‘‘Terms and Conditions of the Notes – Redemption and Purchase’’), the holder of a Notemay, by exercise of the relevant option, request the Bank to give notice to the Borrower, in accordancewith the provisions of the Loan Agreement, that the Loan be prepaid in an amount representing theaggregate principal amount of the Notes relating to the exercise of such option together with accruedinterest. In each case (to the extent that the Bank has actually received the relevant funds from theBorrower) the payment amount of the relevant Notes (or in the case of a prepayment for tax reasons orillegality, all outstanding Notes) will be prepaid by the Bank together with accrued interest. See ‘‘RiskFactors – Risk Factors Relating to the Notes – Taxation’’, ‘‘Loan Agreement – Prepayment – Prepaymentfor Tax Reasons and Change in Circumstances’’ and ‘‘Terms and Conditions of the Notes – Redemptionand Purchase’’.

The Borrower has agreed and the Noteholders will be deemed to have acknowledged, accepted andagreed that the Bank is entitled to deduct the Bank’s and Trustee’s expenses, the Managers’ commissionsand certain other expenses from the advance to be made to the Borrower pursuant to the LoanAgreement.

14

USE OF PROCEEDS

The proceeds from the offering of the Notes will be used by the Bank for the sole purpose offinancing the Loan. The net proceeds of the Loan, expected to amount to approximately U.S.$l, will beused by Rosneft for general corporate purposes, including (1) to increase production of oil and gas and toincrease oil and gas reserves; (2) to increase the quality of the refined products produced by Rosneft,upgrade its refining operations and expand its retail distribution network. See also ‘‘Business – Strategy’’and ‘‘Business – Capital Expenditures’’.

15

RISK FACTORS

Investment in the Notes involves a high degree of risk. Potential investors should carefully review thisentire Offering Circular and in particular should consider all the risks inherent in making such aninvestment, including the risk factors set forth below, before making a decision to invest. These risk factors,individually or together, could have a material adverse effect on the Company.

Risks Relating to the Russian Federation

Rosneft is a vertically-integrated petroleum company with upstream, midstream and downstreamoperations based primarily in Russia, and virtually all of its assets are located on Russian territory. Set outbelow is a brief description of some of the risks incurred by investing in Russia, although the list is not anexhaustive one.

Political and Social Risks

In recent years, Russia has been undergoing a substantial political transformation from a centrallycontrolled command economy under communist rule to a pluralist market-oriented democracy. Therecan be no assurance that the political and economic reforms necessary to complete such a transformationwill continue. In its current relatively nascent stage, the Russian political system is vulnerable to thepopulation’s dissatisfaction with reform, social and ethnic unrest and changes in governmental policies,any of which could have a material adverse effect on Rosneft and its ability to meet its obligations underthe Loan.

During this transformation, legislation has been enacted to protect private property againstexpropriation and nationalisation. However, due to the lack of experience in enforcing these provisions inthe short time they have been in effect and due to potential political changes in the future, there can be noassurance that such provisions would be enforced in the event of an attempted expropriation ornationalisation. Expropriation or nationalisation of any substantial assets of the Rosneft group orportions thereof, potentially without adequate compensation, would have a material adverse effect onRosneft.

The Russian Government has been highly unstable, having experienced four changes in primeminister since March 1998, as well as the resignation of former President Yeltsin on 31 December 1999and the subsequent election of President Putin on 26 March 2000. The various government institutionsand the relations between them, as well as the Russian Government’s policies and the political leaderswho formulate and implement them, are subject to rapid change. Any major changes in, or rejection of,current policies favouring political and economic reform by the Russian Government may have amaterial adverse effect on Rosneft.

Russia is a federation of republics, territories, regions, districts, cities of federal importance, andautonomous areas. The delineation of authority among the constituent entities of the Russian Federationand federal government authorities is often uncertain and at times contested. Lack of consensus betweenlocal and regional authorities and the Russian Government often results in the enactment of conflictinglegislation at various levels, and may result in political instability. This lack of consensus may havenegative economic effects on Rosneft, which could be material to its ability to meet its financialobligations.

In addition, ethnic, religious, historical and other divisions have, on occasion, given rise to tensionsand, in certain cases, military conflict. Russian military and paramilitary forces have been engaged inChechnya in the recent past and continue to maintain a presence there. The spread of violence, or itsintensification, could have significant political consequences. These include the imposition of a state ofemergency in some parts or throughout the Russian Federation. These events could materially adverselyaffect the investment environment in Russia.

The failure of many Russian companies to pay full salaries on a regular and timely basis, and thefailure of salaries and benefits to keep pace with the increasing cost of living, could lead in the future tolabour and social unrest. This may have political, social and economic consequences, such as increasedsupport for a renewal of centralised authority, increased nationalism with restrictions on foreigninvolvement in the Russian economy and increased violence, any of which could have a material adverseeffect on Rosneft.

The privatisation of the oil and gas industry in Russia, which is a vital sector of the nationaleconomy, continues to be a source of political controversy. There can be no assurance that currentgovernment policies liberalising control over the oil and gas industry will endure. Furthermore, control

16

over natural resources such as oil and gas and their exploitation remains an issue between the federalauthorities and the regions. The Company’s operations could be materially affected by the increasedpolitical independence of the regions in which it conducts its operations or through which its natural gas,crude oil or refined products are transported.

Economic Risks

Simultaneously with the enactment of political reforms, the Russian Government has beenattempting to implement policies of economic reform and stabilisation. These policies have involvedliberalising prices, reducing defence expenditures and subsidies, privatising state-owned enterprises,reforming the tax and bankruptcy systems, and introducing legal structures designed to facilitate private,market-based activities, foreign trade and investment.

Despite the implemented reform policies the Russian economy has been characterised by decliningindustrial production, significant inflation, an unstable but managed currency, rising unemployment andunderemployment, high government debt relative to gross domestic product, high levels of corporateinsolvency with little recourse to restructuring or liquidation in bankruptcy proceedings, a weak bankingsystem, widespread tax evasion, and the impoverishment of a large portion of the Russian population.

Additionally, the events and aftermath of 17 August 1998 – the Russian Government’s default on itsshort-term Rouble-denominated treasury bills and other Rouble-denominated securities, theabandonment of the Rouble corridor by the Central Bank and the temporary moratorium on certainhard-currency payments – led to a severe devaluation of the Rouble, a sharp increase in the rate ofinflation, the significant deterioration of the country’s banking system, significant defaults on hardcurrency obligations, a dramatic decline in the prices of Russian debt and equity securities, and aninability to raise funds on international capital markets.

While the Russian economy has improved in a number of areas since 1998, it is impossible toestimate how long the impact of the August 1998 events will be felt or to quantify the impact they mayhave on Rosneft.

The prospect exists of widespread bankruptcy, mass unemployment and the collapse of certainsectors of the Russian economy. Moreover, there is a lack of consensus as to the scope, content and paceof economic and political reform. No assurance can be given that reform policies will continue to beimplemented and, if implemented, will be successful, that Russia will remain receptive to foreign tradeand investment, or that the economy in Russia will improve. Any failure of the current policies ofeconomic reform and stabilisation could have a material adverse effect on the operations of Rosneft.

Funding from International Organisations; Access to the International Capital Markets

Russia in the past has received substantial financial assistance from several foreign governments andinternational organisations, including the International Monetary Fund. No assurance can be given thatany such financing will be further provided to Russia. If such financial assistance is eliminated, economicdevelopment in Russia may be adversely affected.

Moreover, due to defaults on certain obligations and other factors, the Russian Government may beunable to raise funds on international capital markets, which may lead to direct or indirect monetaryfinancing of the budget deficit, putting further pressure on inflation and the value of the Russian Rouble.

The considerable external debt of Russia, as well as the failure to obtain funding from foreigngovernments and international organisations, or increased rates of inflation or devaluation arising fromthe need to resort to monetary financing of the budget deficit in the absence of access to the internationalcapital markets, could materially adversely affect the country and lead to economic downturns.

Lack of Liquidity

Russian businesses have a limited history of operating in free-market conditions and have hadlimited experience (compared with Western companies) of entering into and performing contractualobligations. Russian businesses, when compared to Western, are often characterised by management thatlacks experience in responding to changing market conditions and limited capital resources with which todevelop their operations. In addition, Russia has a limited infrastructure to support a market system.Communications, banks and other financial infrastructure are less well developed and less well regulatedthan their Western counterparts.

17

Russian companies face significant liquidity problems due to a limited supply of domestic savings,few foreign sources of funds, high taxes, limited lending by the banking sector to the industrial sector andother factors. Many Russian companies cannot make timely payments for goods or services and owe largeamounts of overdue federal and local taxes, as well as wages to employees. Many Russian companieshave also resorted to paying their debts or accepting settlement of accounts receivable through barterarrangements or through the use of promissory notes.

These problems were aggravated by the 1995 Russian banking crisis and by the impact on theRussian banking system of the events of August 1998. This further impaired the ability of the bankingsector to act as a consistent source of liquidity to Russian companies. An intensification of liquidityproblems or a further deterioration of the Russian banking system could have a material adverse effecton the Company’s operations and financial performance.

Legal Risks

Risks associated with the Russian legal system include, inter alia: (i) the untested nature of theindependence of the judiciary and its immunity from economic, political or nationalistic influences; (ii)inconsistencies among laws, Presidential decrees, and Government and ministerial orders and resolutions;(iii) the lack of judicial or administrative guidance on interpreting the applicable rules; (iv) a high degreeof discretion on the part of governmental authorities; (v) conflicting local, regional and federal rules andregulations; (vi) the relative inexperience of judges and courts in interpreting new legal norms; and (vii)the unpredictability of enforcement of foreign judgments and foreign arbitral awards.

The laws in Russia regulating ownership, control and corporate governance of Russian companiesare relatively new and, by and large, have not yet been tested in the courts. Disclosure and reportingrequirements do not guarantee that material information will always be available and antifraud andinsider trading legislation is generally rudimentary. The concept of fiduciary duties on the part of themanagement or directors to their companies or the shareholders is not well developed.

In addition, substantive amendments to several fundamental Russian laws (including those relatingto the tax regime, corporations and licensing) have recently been adopted and will shortly becomeeffective. The recent nature of much of Russian legislation, the lack of consensus about the scope, contentand pace of economic and political reform, and the rapid evolution of the Russian legal system in waysthat may not always coincide with market developments may result in ambiguities, inconsistencies andanomalies, the enactment of laws and regulations without a clear constitutional or legislative basis, andultimately in investment risks that do not exist in more developed legal systems. Therefore, no assurancecan be given that the development or implementation or application of legislation (includingGovernment resolutions or Presidential decrees) will not have a material adverse effect on foreigninvestors (or private investors generally).

The existing business culture in Russia continues to be influenced by attitudes formed in the periodof the Soviet planned economy, in which survival often depended on finding ways to avoid the impositionof (often arbitrarily applied) laws and regulations. As a result, the commitment of business people,Government officials and agencies, and the judicial system to abide by legal requirements and negotiatedagreements is still uncertain.

Many Russian laws are structured in a way that provides for significant administrative discretion inapplication and enforcement. Reliable texts of laws and regulations at the regional and local levels maynot be available, and usually are not updated or catalogued. As a result, applicable law is often difficult toascertain and apply, even after reasonable effort. Russia does not have a judicial system based onprecedents. In addition, the laws are subject to different and changing interpretations and administrativeapplications. As a result of these factors, even the best efforts to comply with the laws may not alwaysresult in full compliance.

Russian laws often provide general statements of principles rather than a specific guide toimplementation, and Government officials may be delegated or exercise broad authority to determinematters of significance. Such authority may be exercised in an unpredictable way and effective appealprocesses may not be available. In addition, breaches of Russian law, especially in the area of currencycontrol, may involve severe penalties and consequences that could be considered as disproportionate tothe violation committed.

The independence of the judicial system and its immunity from economic, political and nationalisticinfluences in Russia remains largely untested. Judges and courts are generally inexperienced in the areasof business and corporate law. Judicial precedents generally have no binding effect on subsequent

18

decisions. Not all Russian legislation and court decisions are readily available to the public or organisedin a manner that facilitates understanding. The Russian judicial system can be slow. All of these factorsmake judicial decisions in Russia difficult to predict and effective redress uncertain. Additionally, courtclaims are often used to further political aims. Additionally, court decisions are not always enforced orfollowed by law-enforcement agencies. There is no guarantee that the proposed judicial reform aimed atbalancing the rights of private parties and governmental authorities in courts and reducing grounds for re-litigation of decided cases will be implemented and succeed in building a reliable and independentjudicial system.

Foreign Court Judgments or Arbitral Awards

The Russian Federation is not a party to any multilateral or bilateral treaties with most Westernjurisdictions for the mutual enforcement of court judgments. Consequently, should a judgment beobtained from a court in any of such jurisdictions it is highly unlikely to be given direct effect in Russiancourts. However, the Russian Federation (as successor to the Soviet Union) is a party to the 1958 NewYork Convention on the Recognition and Enforcement of Foreign Arbitral Awards and the LoanAgreement contains a provision allowing for arbitration of disputes. A foreign arbitral award obtained ina state which is party to that Convention should be recognised and enforced by a Russian court (subjectto the qualifications provided for in the Convention and compliance with Russian civil procedureregulations and other procedures and requirements established by Russian legislation). It is expected thatRussian procedural legislation will be changed, inter alia, by way of introducing further groundspreventing foreign court judgments and arbitral awards from being recognised and enforced in Russia. Inpractice, reliance upon international treaties may meet with resistance or a lack of understanding on thepart of Russian court or other officials, thereby introducing delay and unpredictability into the process ofenforcing any foreign judgment or any foreign arbitral award in the Russian Federation.

Exchange Rates, Exchange Controls and Repatriation Restrictions

In recent years, the Rouble has experienced a significant depreciation relative to the U.S. Dollar. Inthe middle of August 1998, the value of the Rouble against the U.S. Dollar fell by more than 300% inseveral days. Before August 1998 the Central Bank had been trying to support the Rouble within acertain band. However, after the significant August 1998 devaluation of the Rouble, the band wascancelled. The ability of the Russian Government and the Central Bank to reduce the volatility of theRouble will depend on many political and economic factors, including their ability to control inflation andthe availability of foreign currency. Furthermore, uncertainties exist with respect to the continuation ofthe Central Bank’s current policy.

The Rouble is not convertible outside Russia. A market exists within Russia for the conversion ofRoubles into other currencies, but it is limited in size and is subject to rules limiting the purposes forwhich conversion may be effected. There can be no assurance that such a market will continueindefinitely. Currently, 50% of foreign currency revenues from export sales must be converted intoRoubles. The relative stability of the exchange rate of the Rouble against the U.S. Dollar since 1999 hasmitigated risks associated with forced conversion, but no assurance can be given that such stability willcontinue. Moreover, the banking system in Russia is not as developed as its Western counterparts, andconsiderable delays may occur in the transfer of funds within, and the remittance of funds out of, Russia.

While the current policy of the Russian Government is to allow the repatriation by foreign investorsof profits earned in Roubles, there are restrictions on such repatriation. Rouble proceeds from certainoperations of foreign investors are required to be frozen for 365 days before they may be converted intohard currency.

Lack of Official Data Reliability

Official statistics and other data published by Russian federal, regional and local governments, andfederal agencies are substantially less complete or reliable than those of Western countries, and there canbe no assurance that the official sources from which certain of the information set forth herein has beendrawn are reliable or complete. Official statistics may also be produced on different bases than those usedin Western countries. Any discussion of matters relating to Russia herein must therefore be subject touncertainty due to concerns about the completeness or reliability of available official and publicinformation.

19

Risks Relating to the Company and the Russian Oil and Gas Industry

Uncertainties in Estimates of Oil and Gas Reserves

There are numerous uncertainties inherent in estimating quantities of proved reserves and inprojecting future rates of production and the timing of development expenditures, including many factorsbeyond the control of the Company. The reserves data included in this Offering Circular, which is derivedfrom the Reserves Reports (as defined in ‘‘Business – Exploration and Production – Oil and Natural GasReserves’’), as well as Rosneft’s internal estimates of its reserves included herein, represent onlyestimates and should not be construed as exact quantities. Estimating oil and gas reserves is a subjectiveprocess and estimates of different engineers often vary significantly. In addition, results of drilling, testingand production subsequent to the date of an estimate generally result in revisions to that estimate.Accordingly, reserves estimates may be materially different from the quantities of crude oil that areultimately recovered and, if recovered, the revenue therefrom could be less and the costs related theretocould be more than estimated amounts. The significance of such estimates is highly dependent upon theaccuracy of the assumptions on which they were based, the quality of the information available and theability to verify such information against industry standards. The reserves evaluations carried out byDeGolyer and MacNaughton were based on production data, prices, costs, ownership, geological andengineering data, and other information provided by the Company and accepted without independentverification. The Reserves Reports assume, among other things, that the future development of theCompany’s oil fields and the future marketability of the Company’s oil will be similar to pastdevelopment and marketability. These economic assumptions may prove to be incorrect. In particular,the Russian economy is more unstable and subject to more significant and sudden changes than theeconomies of many other countries, and thus economic assumptions in Russia are subject to a significantdegree of uncertainty. Potential investors should not place undue reliance on the forward-lookingstatements in the Reserves Reports or on comparisons of similar reports concerning companiesestablished in places with more mature economic systems.

Failure to Acquire or Find and Develop Additional Reserves