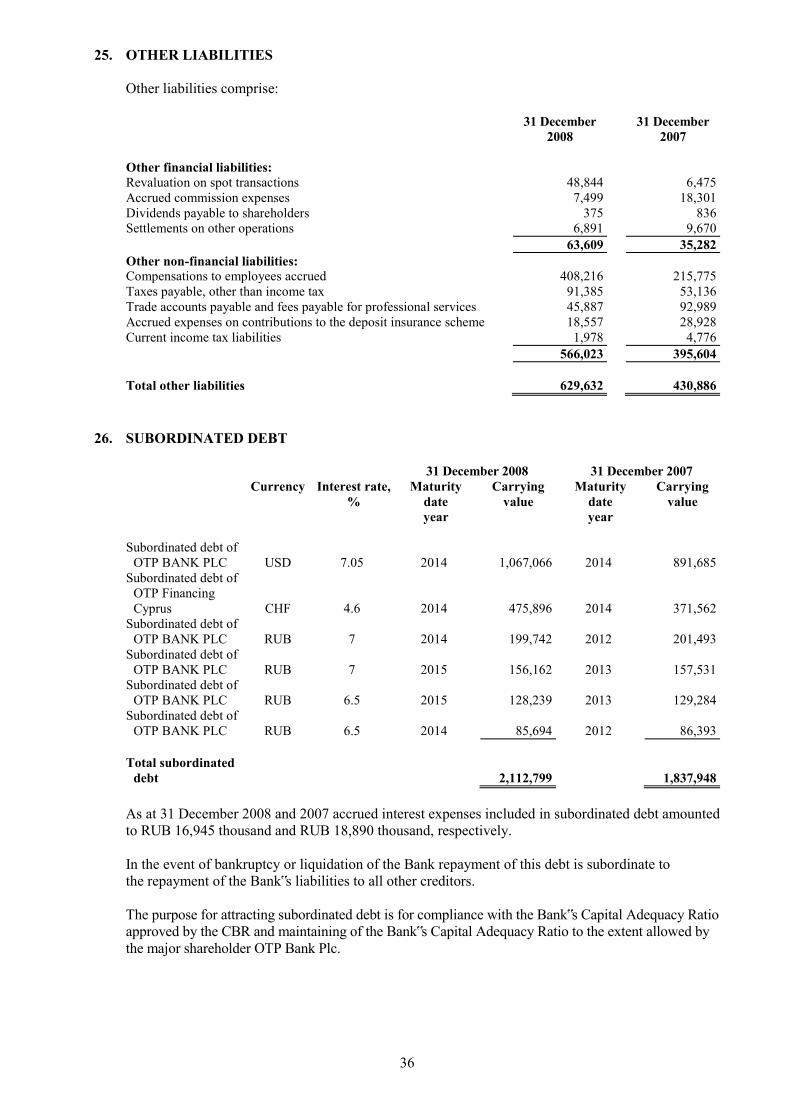

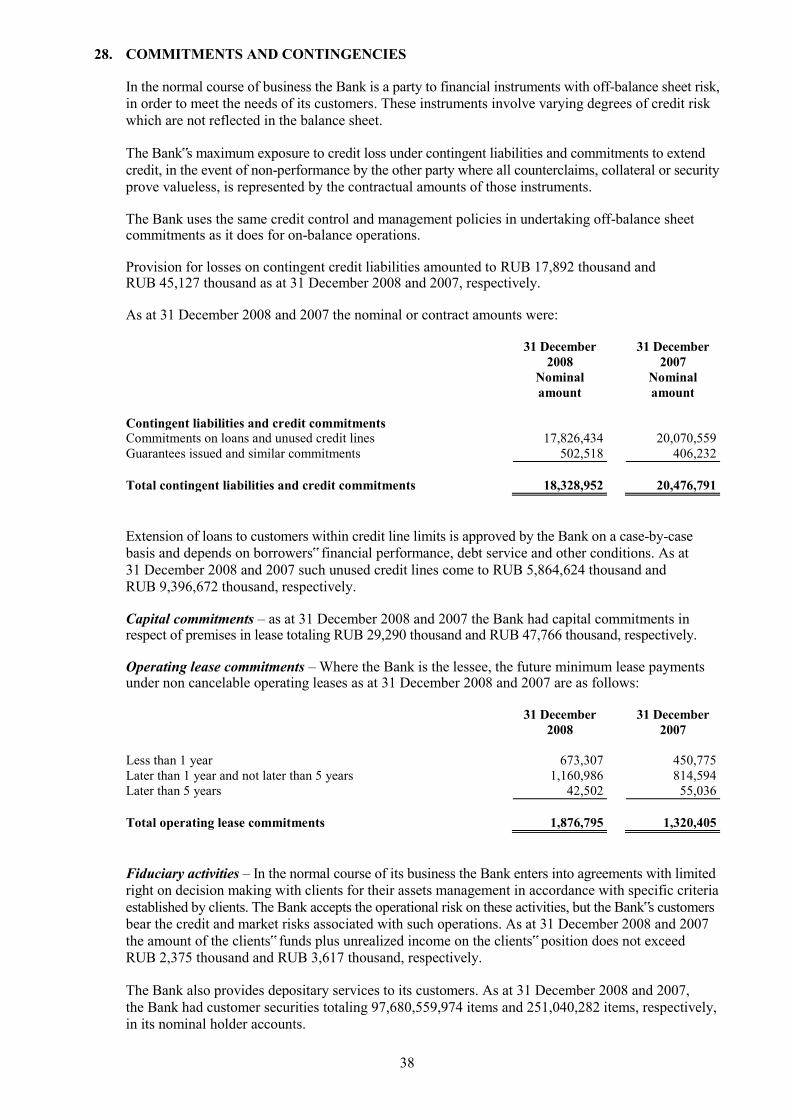

Embed Size (px)

Citation preview

Open Joint Stock Company “OTP Bank” Financial Statements For the Year Ended 31 December 2008

Open Joint Stock Company “OTP Bank” TABLE OF CONTENTS

Page STATEMENT OF MANAGEMENT‟S RESPONSIBILITIES FOR THE PREPARATION AND APPROVAL OF THE FINANCIAL STATEMENTS 1 INDEPENDENT AUDITORS‟ REPORT 2-3 FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2008:

Income statement 4 Balance sheet 5 Statement of changes in equity 6 Statement of cash flows 7-8 Notes to the financial statements 9-57

1

Open Joint Stock Company “OTP Bank” STATEMENT OF MANAGEMENT’S RESPONSIBILITIES FOR THE PREPARATION AND APPROVAL OF THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2008 The following statement, which should be read in conjunction with the independent auditors‟ responsibilities stated in the independent auditors‟ report set out on pages 2-3, is made with a view to distinguishing the respective responsibilities of management and those of the independent auditors in relation to the financial statements of Open Joint Stock Company “OTP Bank”. Management is responsible for the preparation of the financial statements that present fairly the financial position of the Bank as at 31 December 2008, the results of its operations, cash flows and changes in equity for the year then ended, in accordance with International Financial Reporting Standards (“IFRS”). In preparing the financial statements, management is responsible for: Selecting suitable accounting principles and applying them consistently; Making judgments and estimates that are reasonable and prudent; Stating whether IFRS have been followed; and Preparing the financial statements on a going concern basis, unless it is inappropriate

to presume that the Bank will continue in business for the foreseeable future. Management is also responsible for: Designing, implementing and maintaining an effective and sound system of internal controls,

throughout the Bank; Maintaining proper accounting records that disclose, with reasonable accuracy at any time,

the financial position of the Bank, and which enable them to ensure that the financial statements of the Bank comply with IFRS;

Maintaining statutory accounting records in compliance with legislation and accounting standards of the Russian Federation (“RF”);

Taking such steps as are reasonably available to them to safeguard the assets of the Bank; Detecting and preventing fraud, errors and other irregularities. The financial statements for the year ended 31 December 2008 were authorized for issue on 28 May 2009 President of the Bank. On behalf of the Management Board: _________________________ _________________________ President Chief Accountant A.A. Korovin D.I. Karpov 28 May 2009 28 May 2009 Moscow Moscow

INDEPENDENT AUDITORS’ REPORT To the Shareholders and the Board of Directors of Open Joint Stock Company “OTP Bank”: Report on the financial statements We have audited the accompanying financial statements of Open Joint Stock Company “OTP Bank” (the “Bank”), which comprise the balance sheet as at 31 December 2008, the income statement, the statements of changes in equity and cash flows for the year then ended, and a summary of significant accounting policies and other explanatory notes. Management’s responsibility for the financial statements Management of the Bank is responsible for the preparation and fair presentation of these financial statements in accordance with International Financial Reporting Standards. This responsibility includes: designing, implementing and maintaining internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error; selecting and applying appropriate accounting policies; and making accounting estimates that are reasonable in the circumstances. Auditors' responsibility Our responsibility is to express an opinion on reliability of these financial statements based on our audit. We conducted our audit in accordance with International Standards on Auditing. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor‟s judgement, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity‟s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity‟s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

3

Opinion In our opinion, the financial statements present fairly, in all material respects the financial position of the Bank as at 31 December 2008, and its financial performance and cash flows for the year then ended in accordance with International Financial Reporting Standards. 28 May 2009 Moscow

4

Open Joint Stock Company “OTP Bank” INCOME STATEMENT FOR THE YEAR ENDED 31 DECEMBER 2008 (in thousands of Russian rubles)

Notes Year ended

31 December 2008

Year ended 31 December

2007 Interest income 5,30 12,762,139 8,723,453 Interest expense 5,30 (2,736,032) (2,449,320) NET INTEREST INCOME BEFORE PROVISION

FOR IMPAIRMENT LOSSES ON INTEREST BEARING ASSETS 10,026,107 6,274,133

Provision for impairment losses on interest bearing assets 6 (3,897,191) (2,170,202) NET INTEREST INCOME 6,128,916 4,103,931 Net gain/(loss) on financial assets and liabilities

at fair value through profit or loss 7 1,226,138 (34,890) Net (loss)/gain on foreign exchange operations 8,30 (828,952) 163,853 Fee and commission income 9,30 1,857,952 2,232,833 Fee and commission expense 9,30 (441,688) (250,492) Net realized gain on investments available-for-sale - 5,026 Other provisions 6 19,701 (13,255) Other income 10,30 37,696 27,308 NET NON-INTEREST INCOME 1,870,847 2,130,383 OPERATING INCOME 7,999,763 6,234,314 OPERATING EXPENSES 11,30 (6,106,241) (4,635,766) PROFIT BEFORE INCOME TAX 1,893,522 1,598,548 Income tax expense 12 (399,461) (419,496) NET PROFIT 1,494,061 1,179,052 On behalf of the Management Board: _________________________ _________________________ PresidentChief Accountant A.A. Korovin D.I. Karpov 28 May 2009 28 May 2009

Moscow Moscow The notes on pages 9-57 form an integral part of these financial statements.

5

Open Joint Stock Company “OTP Bank” BALANCE SHEET AS AT 31 DECEMBER 2008 (in thousands of Russian rubles)

Notes 31 December

2008 31 December

2007 ASSETS:

Cash and cash equivalents 13,30 17,065,786 5,465,631 Minimum reserve deposit with the Central Bank of

the Russian Federation 14 49,975 732,333 Financial assets at fair value through profit or loss 15 320,739 6,934,243 Due from banks 16,30 412,588 2,083,071 Loans to customers 17,30 53,762,494 41,347,501 Investments available-for-sale 18,30 1,966,881 1,563,649 Investments held to maturity 19 2,699,695 - Property, plant and equipment and intangible assets 20 2,484,470 2,189,013 Current income tax assets 92,392 19,113 Deferred income tax assets 12 155,069 119,079 Other assets 21,30 372,317 400,786

TOTAL ASSETS 79,382,406 60,854,419 LIABILITIES AND EQUITY LIABILITIES:

Due to banks 22,30 33,471,583 10,394,094 Customer accounts 23,30 32,831,299 41,593,036 Debt securities issued 24 1,308,853 1,214,562 Other provisions 6 18,259 45,966 Deferred income tax liabilities 12 166,017 141,413 Other liabilities 25,30 629,632 430,886 Subordinated debt 26,30 2,112,799 1,837,948

TOTAL LIABILITIES 70,538,442 55,657,905

EQUITY:

Share capital 27 4,265,532 3,765,532 Share premium 27 2,000,000 - Investments available-for-sale fair value reserve (620,277) (255,293) Property, plant and equipment revaluation reserve 526,691 510,915 Retained earnings 2,672,018 1,175,360

TOTAL EQUITY 8,843,964 5,196,514

TOTAL LIABILITIES AND EQUITY 79,382,406 60,854,419 On behalf of the Management Board: _________________________ _________________________ President Chief Accountant A.A. Korovin D.I. Karpov 28 May 2009 28 May 2009

Moscow Moscow The notes on pages 9-57 form an integral part of these financial statements.

6

Open Joint Stock Company “OTP Bank” STATEMENT OF CHANGES IN EQUITY FOR THE YEAR ENDED 31 DECEMBER 2008 (in thousands of Russian rubles) Share

capital Share

premium Investments available-for-

sale fair value

Property and equipment revaluation

reserve

(Accumulated deficit)/

Retained earnings

Total equity

31 December 2006 3,765,532 - - - (3,692) 3,761,840 Fair value adjustment on investments

available-for-sale - - (335,912) - - (335,912) Property, plant and equipment

revaluation - - - 652,328 - 652,328 Deferred income tax recognized directly

in equity - - 80,619 (141,413) - (60,794) Net profit for 2007 - - - - 1,179,052 1,179,052 31 December 2007 3,765,532 - (255,293) 510,915 1,175,360 5,196,514 Fair value adjustment on investments

available-for-sale - - (439,434) - - (439,434) Writing-off property, plant and

equipment revaluation reserve (as a result of disposal) - - - (2,597) 2,597 -

Deferred income tax recognized directly in equity - - 74,450 18,373 - 92,823

Issue of share capital: - ordinary shares and share premium 500,000 2,000,000 - - - 2,500,000 Net profit for 2008 - - - - 1,494,061 1,494,061 31 December 2008 4,265,532 2,000,000 (620,277) 526,691 2,672,018 8,843,964 On behalf of the Management Board: _________________________ _________________________ President Chief Accountant A.A. Korovin D.I. Karpov 28 May 2009 28 May 2009

Moscow Moscow The notes on pages 9-57 form an integral part of these financial statements.

7

Open Joint Stock Company “OTP Bank” STATEMENT OF CASH FLOWS FOR THE YEAR ENDED 31 DECEMBER 2008 (in thousands of Russian rubles) Notes Year ended

31 December 2008

Year ended 31 December

2007 CASH FLOWS FROM OPERATING ACTIVITIES:

Profit before income tax 1,893,522 1,598,548 Adjustments for:

Provision for impairment losses on interest bearing assets 3,897,191 2,170,202 (Recovery of provision)/provision for impairment losses

on other transactions (19,701) 13,255 Fair value adjustment on financial assets held for trading 45,479 164,686 Fair value adjustment on derivative financial instruments 35,094 1,253 Loss from disposal of property, plant and equipment and

intangible assets 18,220 217 Depreciation of property, plant and equipment and

intangible assets 319,757 202,165 Translation loss on foreign exchange operations 836,484 (32,815) Change in interest accruals, net (1,077,260) (1,044,731) Change in noninterest accruals, net 175,182 273,986 Loss on revaluation of property, plant and equipment - 58,515 Income on assets received for free (11,391) -

Cash inflow from operating activities before changes in

operating assets and liabilities 6,112,577 3,405,281

Changes in operating assets and liabilities (Increase)/decrease in operating assets:

Minimum reserve deposit with the Central Bank of Russian Federation 682,358 (33,088)

Due from banks 1,695,163 (1,548,957) Financial assets at fair value through profit or loss 3,707,673 (328,269) Loans to customers (11,774,711) (14,536,975) Other assets 492 (139,150)

Increase/(decrease) in operating liabilities Due to banks and other financial institutions 18,689,444 8,531,626 Customer accounts (9,811,672) 4,984,579 Other liabilities 12,402 24,847 Debt securities issued/(repaid) 84,457 (567,864)

Cash inflow/(outflow) from operating activities

before taxation 9,398,183 (207,970) Income tax paid (393,767) (448,148)

Net cash inflow/(outflow) from operating activities 9,004,416 (656,118)

CASH FLOWS FROM INVESTING ACTIVITIES:

Purchase of property, plant and equipment and intangible assets (635,842) (590,087)

Proceeds on sale of property, plant and equipment and intangible assets 2,408 1,009

Proceeds on sale of investments available-for-sale 6,310 1,406,068 Purchase of investments available-for-sale - (3,219,074)

Net cash outflow from investing activities (627,124) (2,402,084)

8

Open Joint Stock Company “OTP Bank” STATEMENT OF CASH FLOWS (CONTINUED) FOR THE YEAR ENDED 31 DECEMBER 2008 (in thousands of Russian rubles)

Notes Year ended

31 December 2008

Year ended 31 December

2007 CASH FLOWS FROM FINANCING ACTIVITIES:

Subordinated debt - 1,221,639 Dividends paid (461) (6,349) Issue of share capital and share premium 2,500,000 -

Net cash inflow from financing activities 2,499,539 1,215,290

Effect of changes in foreign exchange rate fluctuations

on cash and cash equivalents 723,324 137,504 NET INCREASE/(DECREASE) IN CASH AND

CASH EQUIVALENTS 11,600,155 (1,705,408) CASH AND CASH EQUIVALENTS, beginning of year 13 5,465,631 7,171,039 CASH AND CASH EQUIVALENTS, end of year 13 17,065,786 5,465,631 Interest paid and received by the Bank during the year ended 31 December 2008 amounted to RUB 2,385,387 thousand and RUB 11,560,656 thousand, respectively. Interest paid and received by the Bank during the year ended 31 December 2007 amounted to RUB 2,512,781 thousand and RUB 7,799,651 thousand, respectively. On behalf of the Management Board: _________________________ _________________________ President Chief Accountant A.A. Korovin D.I. Karpov 28 May 2009 28 May 2009

Moscow Moscow The notes on pages 9-57 form an integral part of these financial statements.

9

Open Joint Stock Company “OTP Bank” NOTES TO THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2008 (in thousands of Russian rubles)

1. ORGANIZATION Open Joint Stock Company “OTP Bank” (the “Bank”) was incorporated in the Russian Federation (RF) in 1994. The Bank is regulated by the Central Bank of the Russian Federation (the “CBR”) and conducts its business under general license number 2766 issued on 04 March 2008. The Bank‟s primary business consists of commercial activities to individuals and legal entities, including trading with securities and foreign currencies, and originating loans and guarantees. The registered office of the Bank is located at 45 Pokrovka St., bldg. 1, Moscow 105062, Russian Federation. At the beginning of 2008 the Bank had 5 branches operating in the Russian Federation in Omsk, Novorossiysk, Novosibirsk, St. Petersburg and Zhukovsky. During the year 2008 another 2 branches were registered: “Samarskiy” branch in Samara and “Nizhegorodskiy” branch in Nizhniy Novgorod. Due to the fact that “Nizhegorodskiy” branch received its BIK number only in January 2009, there were no operations in 2008. The Bank is a parent company of a group which consists of the following enterprises: Proportion or ownership

interest, %

Name Country of operation 2008 2007 Type of operation

OJSC “OTP Bank” Russian Federation Parent

company Parent

company Commercial bank Limited Liability Company

“PSF” Russian Federation 100.0 100.0 Financial lease Limited Liability Company

“Gamayun” Russian Federation 100.0 100.0 Catering

Limited Liability Company

“Promfin” Russian Federation 99.2 99.2 Consulting services Limited Liability Company

“Investment company “Promstroyinvest” Russian Federation 99.0 99.0 Investments

Limited Liability Company

“Business-Office” Russian Federation 99.2 99.2 Real estate Limited Liability Company “Audit firm “Consulting-

legal Center” Russian Federation 25.0 25.0 Accounting and audit Because of the fact that the influence of the group members is immaterial consolidated statements of the group are not prepared.

10

As at 31 December 2008 and 2007, the following shareholders owned the issued shares of the Bank:

31 December

2008, % 31 December

2007, % Shareholder First level shareholders: OTP BANK PLC 58.12 51.34 LLC “INVEST OIL” 17.18 19.46 LLC “Megaform Inter” 14.30 16.20 LLC “ALLIANCERESERVE” 5.49 10.22 Other 4.91 2.78 Total 100.00 100.00 Ultimate shareholders: OTP BANK PLC 95.09 97.22 Other 4.91 2.78 Total 100.00 100.00 As OTP BANK PLC holds 100% shares of LLC “INVEST OIL”, “Megaform Inter” and LLC “ALLIANCERESERVE”, as at 31 December 2008 and 31 December 2007 OTP BANK PLC effectively owned 95.09% and 97.22% respectively of the Bank‟s shares, so the Bank is a subsidiary of OTP BANK PLC.

2. BASIS OF PRESENTATION Reporting basis These financial statements of the Bank have been prepared in accordance with International Financial Reporting Standards (“IFRS”) issued by the International Accounting Standards Board (“IASB”) and Interpretations issued by the International Financial Reporting Interpretations Committee (“IFRIC”). These financial statements are presented in thousands of Russian Rubles (“RUB‟000”), unless otherwise indicated. These financial statements have been prepared under the historical cost convention, except for the measurement at fair value of certain financial instruments and measurement of buildings at revalued amounts according to International Accounting Standard (“IAS”) No. 16 “Property, Plant and Equipment”. In accordance with IAS 29 the economy of the Russian Federation was considered to be hyperinflationary during 2002 and prior years. Starting 1 January 2003, the Russian economy is no longer considered to be hyperinflationary and the values of non-monetary assets, liabilities and equity as stated in measuring units as at 31 December 2002 have formed the basis for the amounts carried forward to 1 January 2003. The Bank maintains its accounting records in accordance with Russian Law. These financial statements have been prepared from the Russian statutory accounting records and have been adjusted to conform with IFRS. Entered adjustments include certain reclassifications to reflect the economic substance of underlying transactions including reclassifications of certain assets and liabilities, income and expenses to appropriate financial statement captions. Functional currency The functional currency of the financial statements is the Russian Rubles (RUB).

11

3. SIGNIFICANT ACCOUNTING POLICIES Recognition and measurement of financial instruments The Bank recognizes financial assets and liabilities on its balance sheet when it becomes a party to the contractual obligations of the instrument. Regular way purchases and sales of financial assets and liabilities are recognized using settlement date accounting. Financial assets and liabilities are initially recognized at fair value plus, in the case of a financial asset or financial liability not at fair value through profit or loss, transaction costs that are directly attributable to acquisition or issue of the financial asset or financial liability. The accounting policies for subsequent re-measurement of these items are disclosed in the respective accounting policies set out below. Derecognition of financial assets and liabilities Financial assets A financial asset (or, where applicable a part of a financial asset or part of a group of similar financial assets) is derecognized where:

the rights to receive cash flows from the asset have expired; the Bank has transferred its rights to receive cash flows from the asset, or retained the right to

receive cash flows from the asset, but has assumed an obligation to pay them in full without material delay to a third party under a „pass-through‟ arrangement; and

the Bank either (a) has transferred substantially all the risks and rewards of the asset, or (b) has neither transferred nor retained substantially all the risks and rewards of the asset, but has transferred control of the asset.

A financial asset is derecognized when it has been transferred and the transfer qualifies for derecognition. A transfer requires that the Bank either: (a) transfers the contractual rights to receive the asset‟s cash flows; or (b) retains the right to the asset‟s cash flows but assumes a contractual obligation to pay those cash flows to a third party. After a transfer, the Bank reassesses the extent to which it has retained the risks and rewards of ownership of the transferred asset. If substantially all the risks and rewards have been retained, the asset remains on the balance sheet. If substantially all of the risks and rewards have been transferred, the asset is derecognized. If substantially all the risks and rewards have been neither retained nor transferred, the Bank assesses whether or not is has retained control of the asset. If it has not retained control, the asset is derecognized. Where the Bank has retained control of the asset, it continues to recognize the asset to the extent of its continuing involvement. Financial liabilities A financial liability is derecognized when the obligation is discharged, cancelled, or expires. Where an existing financial liability is replaced by another from the same lender on substantially different terms, or the terms of an existing liability are substantially modified, such an exchange or modification is treated as a de-recognition of the original liability and the recognition of a new liability, and the difference in the respective carrying amounts is recognized in the income statement. Cash and cash equivalents Cash and cash equivalents include cash on hand and current bank accounts. Cash equivalents are short-term, highly liquid investments that are readily convertible to amounts of cash and that are subject to an insignificant risk of change in value. Amounts with any restrictions are not included in cash and cash equivalents. Minimum reserve deposit with the Central Bank of the Russian Federation Minimum reserve deposits with the CBR are deposits with the CBR not used in the day-to-day activities of the Bank. For purposes of determining cash flows, the minimum reserve deposit required by the CBR is not included as a cash equivalent and is reported in a separate balance sheet items.

12

Due from banks In the normal course of business, the Bank maintains advances and deposits for various periods of time with other banks. Due from banks are measured at amortized cost using the effective interest method. Amounts due from credit institutions are carried net of any allowance for impairment losses, if any. Financial assets and liabilities at fair value through profit or loss Financial assets and liabilities at fair value through profit or loss represent derivative instruments or securities acquired principally for the purpose of selling them in the near future, or are part of a portfolio of identified financial instruments that are managed together and for which there is evidence of a recent and actual pattern of short-term profit taking or financial assets/liabilities that upon initial recognition are designated by the bank at fair value through profit or loss. Financial assets and liabilities at fair value through profit or loss are initially recorded and subsequently measured at fair value. The Bank uses quoted market prices to determine fair value for financial assets and liabilities at fair value through profit or loss. The fair value adjustment for financial assets and liabilities at fair value through profit or loss is recognized in the income statement for the period. The Bank enters into derivative financial instruments to manage currency, liquidity risks and for trading purposes. Derivative financial instruments entered into by the Bank include currency futures, short-term interest rate futures and securities futures. Derivative financial instruments that are entered by the Bank are not qualified for hedge accounting. Derivative financial instruments In the normal course of business, the Bank enters into various derivative financial instruments. Derivatives are initially recognized at fair value at the date a derivative contract is entered into and are subsequently re-measured to their fair value at each balance sheet date. The fair values are estimated based on quoted market prices or pricing models that take into account the current market and contractual prices of the underlying instruments and other factors. Derivatives are carried as assets when their fair value is positive and as liabilities when it is negative. Derivatives are included in financial assets and liabilities at fair value through profit or loss in the consolidated balance sheet. Gains and losses resulting from these instruments are included in Net gain/loss from financial assets and liabilities at fair value through profit or loss in the income statement. Derivative instruments embedded in other financial instruments are treated as separate derivatives if their risks and characteristics are not closely related to those of the host contracts and the host contracts are not carried at fair value with unrealized gains and losses reported in income statement. An embedded derivative is a component of a hybrid (combined) financial instrument that includes both the derivative and a host contract, with the effect that some of the cash flows of the combined instrument vary in a similar way to a stand-alone derivative. Repurchase and reverse repurchase agreements In the normal course of business, the Bank enters into sale and repurchase agreements (“repos”) and purchase and sale back agreements (“reverse repos”). Repos and reverse repos are utilized by the Bank as an element of its treasury management and trading business. A repo is an agreement to transfer a financial asset to another party in exchange for cash or other consideration and a concurrent obligation to reacquire the financial assets at a future date for an amount equal to the cash or other consideration exchanged plus interest. These agreements are accounted for as financing transactions. Financial assets sold under repo are retained in the financial statements and consideration received under these agreements is recorded as collateralized deposit received within balances due to banks and customer accounts. Assets purchased under reverse repos are recorded in the financial statements as cash placed on deposit collateralized by securities and other assets and are classified within balances due from banks or loans to customers.

13

In the event that assets purchased under reverse repo are sold to third parties, the results are recorded with the gain or loss included in net gains/(losses) on respective assets. Any related income or expense arising from the pricing difference between purchase and sale of the underlying assets is recognized as interest income or expense. Loans to customers Loans to customers are non-derivative assets with fixed or determinable payments that are not quoted in an active market, other than those classified in other categories of financial assets. Loans granted by the Bank are initially recognized at fair value plus related transaction costs. Where the fair value of consideration given does not equal the fair value of the loan, for example where the loan is issued at lower than market rates, the difference between the fair value of consideration given and the fair value of the loan is recognized as a loss on initial recognition of the loan and included in the income statement. Subsequently, loans are carried at amortized cost using the effective interest method. Loans to customers are carried net of any allowance for impairment losses. Write off of loans and advances Loans and advances are written off against the allowance for impairment losses when deemed uncollectible. Loans and advances are written off after management has exercised all possibilities available to collect amounts due to the Bank and after the Bank has sold all available collateral. Excess funds upon such sale are repaid to the borrower. Loans and advances may be also written off on basis of Board of Directors order when the following conditions are simultaneously met: The main loan is due for more than two years; There are no cash flows under the contract for more than two years. Allowance for impairment losses The Bank accounts for impairment of financial assets when there is objective evidence that a financial asset or group of financial assets is impaired. Impairment losses are measured as the difference between carrying amounts and the present value of expected future cash flows, including amounts recoverable from guarantees and collateral, discounted at the financial asset‟s original effective interest rate, for financial assets which are carried at amortized cost. If in a subsequent period the amount of impairment losses decreases and the decrease can be related objectively to an event occurring after the impairment was recognized, the previously recognized impairment loss is reversed. For the financial assets carried at cost, the impairment losses are measured as the difference between the carrying amount of the financial asset and present value of the estimated future cash flows discounted using the current market interest rate for a similar financial instrument. Such impairment losses are not reversed. The determination of impairment losses is based on the analysis of risk assets and reflects the amount which, in the judgement of the management, is adequate to provide for losses incurred. Provisions are created as a result of an individual appraisal of risk assets for financial assets that are individually significant, and an individual or collective assessment for financial assets that are not individually significant. The change in impairment losses is charged to the profit and loss and the total of impairment losses is deducted in arriving at assets as shown in the balance sheet. Factors that the Bank considers in determining whether it has objective evidence that an impairment loss has been incurred include information about the debtors‟ or issuers‟ liquidity, solvency and business and financial risk exposures, levels of the trends in delinquencies for similar financial assets, national and local economic trends and conditions, and the fair value of collateral and guarantees. These and other factors may, either individually or taken together, provide sufficient objective evidence that an impairment loss has been incurred in a financial asset or group of financial assets.

14

It should be understood that estimates of losses involve an exercise of judgement, while it is possible that in particular periods the Bank may sustain losses, which are substantial relative to the allowance for impairment losses, it is judgement of management that the allowance for impairment losses is adequate to absorb losses incurred on the risk assets. Investments available-for-sale Investments available-for-sale represent debt and equity investments that are intended to be held for an indefinite period of time. Such securities are initially recorded at fair value. Subsequently the securities are measured at fair value, with such re-measurement recognized directly in equity until sold when gain/loss previously recorded in equity is recycled through the income statement. Impairment losses, foreign exchange gains or losses and interest income accrued using the effective interest method are recognized directly in the income statement. The Bank uses quoted market prices to determine the fair value for the Bank‟s investments available-for-sale. If the market for investments is not active, the Bank establishes fair value by using valuation techniques. Valuation techniques include using recent arm‟s length market transactions between knowledgeable, willing parties, reference to the current fair value of another instrument that is substantially the same, discounted cash flow analysis and option pricing models. If there is a valuation technique commonly used by market participants to price the instrument and that technique has been demonstrated to provide reliable estimates of prices obtained in actual market transactions, the Bank uses that technique. Dividends received on investments available-for-sale are included in dividend income in the income statement. Non-marketable debt and equity securities are stated at amortized cost and cost, respectively, less impairment losses, if any, unless fair value can be reliably measured. When there is objective evidence that such securities have been impaired, the cumulative loss previously recognized in equity is removed from equity and recognized in the income statement for the period. Reversals of such impairment losses on debt instruments, which are objectively related to events occurring after the impairment, are recognized in the income statement for the period. Reversals of such impairment losses on equity instruments are not recognized in the income statement. Investments held to maturity Investments held to maturity are debt securities with determinable or fixed payments. The Bank has the positive intent and ability to hold them to maturity. Such securities are carried at amortized cost using the effective interest method, less any allowance for impairment. Amortized discounts are recognized in interest income over the period to maturity using the effective interest method. Property, plant and equipment and intangible assets Property, plant and equipment (except buildings) and intangible assets, acquired after 1 January 2003 are disclosed in financial statements at historical cost less accumulated depreciation and any recognized impairment loss, if any. Property, plant and equipment and intangible assets, acquired before 1 January 2003 are disclosed in financial statements at historical cost restated for inflation less accumulated depreciation and any recognized impairment loss, if any. Depreciation is charged on the carrying value of property, plant and equipment and intangible assets and is designed to write off assets over their useful economic lives. Depreciation is calculated on a straight line basis at the following annual prescribed rates:

Buildings and constructions 2.5%-20% Furniture and equipment 3.3%-52.2% Motor vehicles 9.8%-32.4% Intangible assets 10% - 80.0%

Leasehold improvements are amortized over the lease agreement conditions. Expenses related to repairs and renewals are charged when incurred and included in operating expenses unless they qualify for capitalization.

15

The carrying amount of property, plant and equipment and intangible assets are reviewed at each balance sheet date to assess whether they are recorded in excess of their recoverable amount. Impairment loss is recognized in the respective period and is included in operating expenses. After the recognition of an impairment loss the depreciation charge for property, plant and equipment is adjusted in future periods to allocate the assets‟ revised carrying value, less its residual value (if any), on a systematic basis over its remaining useful life. Buildings are stated in the balance sheet at their revalued amounts, being the fair value at the date of revaluation, determined from market-based evidence by appraisal undertaken by professional independent appraisers, less any subsequent accumulated depreciation and subsequent accumulated impairment losses. Revaluation are performed with sufficient regularly such that the carrying amount does not differ materially from that which would be determined using fair values at the balance sheet date. Any revaluation increase arising on the revaluation of such buildings is credited to the property, plant and equipment revaluation reserve, except to the extent that it reverses a revaluation decrease for the same asset previously recognized as an expense in which case the increase is credited to the income statement to the extent of the decrease previously charged. A decrease in carring amount arising on the revaluation is charged as an expense to the extent that it exceeds the balance, if any, held in the revaluation reserve relating to a previous revaluation of that asset. Depreciation on revalued buildings is charged to income statement. On the subsequent sale or retirement of a revalued property, the attributable revaluation surplus remaining in the revaluation reserve is transferred directly to retained earnings. Taxation Income tax expense represents the sum of the current and deferred tax expense. The current tax expense is based on taxable profit for the year. Taxable profit differs from net profit before tax as reported in the income statement because it excludes items of income or expense that are taxable or deductible in other years and it further excludes items that are never taxable or deductible. The Bank‟s current tax expense is calculated using tax rates that have been enacted during the reporting period. Deferred tax is the tax expected to be payable or recoverable on differences between the carrying amounts of assets and liabilities in the financial statements and the corresponding tax bases used in the computation of taxable profit, and is accounted for using the balance sheet liability method. Deferred tax liabilities are generally recognized for all taxable temporary differences and deferred tax assets are recognized to the extent that it is probable that taxable profits will be available against which deductible temporary differences can be utilized. Such assets and liabilities are not recognized if the temporary difference arises from goodwill or from the initial recognition (other than in a business combination) of other assets and liabilities in a transaction that affects neither the tax profit nor the accounting profit. The carrying amount of deferred tax assets is reviewed at each balance sheet date and reduced to the extent that it is no longer probable that sufficient taxable profits will be available to allow all or part of the asset to be recovered. Deferred tax is calculated at the tax rates that are expected to apply in the period when the liability is settled or the asset is realized. Deferred tax is charged or credited in the income statement, except when it relates to items charged or credited directly to equity, in which case the deferred tax is also dealt with in equity.

16

Deferred income tax assets and deferred income tax liabilities are offset and reported net on the balance sheet if: The Bank has a legally enforceable right to set off current income tax assets against current

income tax liabilities; and Deferred income tax assets and the deferred income tax liabilities relate to income taxes levied

by the same taxation authority on the same taxable entity. The Russian Federation also has various other taxes, which are assessed on the Bank‟s activities apart from income tax. These taxes are included as a component of operating expenses in the income statement. Due to banks, customer accounts, debt securities issued, subordinated debt Due to banks, customer accounts, debt securities issued and subordinated debt are initially recognized at fair value. Subsequently, amounts due are stated at amortized cost and any difference between net proceeds and the redemption value is recognized in the income statement over the period of the borrowings, using the effective interest method as interest expenses. Other provisions Other provisions are recognized when the Bank has a present legal or constructive obligation as a result of past events (determined by legal standards or deemed), it is probable that an outflow of resources embodying economic benefits will be required to settle the obligation and a reliable estimate of the obligation can be made. Financial guarantees Financial guarantees issued by the Bank are credit insurance that provides for specified payments to be made to reimburse to the holder for a loss it incurs because a specified debtor fails to make payment when due under the original or modified terms of a debt instrument. Such financial guarantee contracts are initially recognized at fair value. Subsequently they are measured at the higher of (a) the amount recognized as a provision in accordance with IAS 37 “Provisions, Contingent Liabilities and Contingent Assets”; and (b) the amount initially recognized less, where appropriate, cumulative amortization of initial premium revenue received over the financial guarantee contracts or letter of credit issued. Share capital and share premium Contributions to share capital made before 1 January 2003 are recognized at their cost restated for inflation. Contributions to share capital made after 1 January 2003 are recognized at cost. Share premium represents the excess of contributions over the nominal value of the shares issued. Dividends on ordinary shares are recognized in equity as a reduction in the period in which they are declared. Dividends that are declared after the balance sheet date are treated as a subsequent event under IAS 10 “Events after the Balance Sheet Date” (“IAS 10”) and disclosed accordingly. Retirement and other benefit obligations In accordance with the requirements of the Russian legislation, state pension system provides for the calculation of current payments by the employer as a percentage of current total payment to staff. This expense is charged in the period in which the related salaries are earned. The Bank does not have any pension arrangements separate from the state pension system of the Russian Federation. In addition, the Bank has no post-retirement benefits or other significant compensated benefits requiring accrual. Recognition of income and expense Interest income and expense are recognized on an accrual basis using the effective interest method. The effective interest method is a method of calculating the amortized cost of a financial asset or a financial liability (or group of financial assets or financial liabilities) and of allocating the interest income or interest expense over the relevant period. The effective interest rate is the rate that exactly discounts estimated future cash payments or receipts through the expected life of the financial instrument or, when appropriate, a shorter period to the net carrying amount of the financial asset or financial liability.

17

Once a financial asset or a group of similar financial assets has been written down (partly written down) as a result of an impairment loss, interest income is thereafter recognized using the rate of interest used to discount the future cash flows for the purpose of measuring the impairment loss. Interest earned on assets at fair value is classified as interest income. Loan origination fees are deferred, together with the related direct costs, and recognized as an adjustment to the effective interest rate of the loan. Where it is probable that a loan commitment will lead to a specific lending arrangement, the loan commitment fees are deferred, together with the related direct costs, and recognized as an adjustment to the effective interest rate of the resulting loan. Where it is unlikely that a loan commitment will lead to a specific lending arrangement, the loan commitment fees are recognized in the income statement over the remaining period of the loan commitment. Where a loan commitment expires without resulting in a loan, the loan commitment fee is recognized in the income statement on expiry. Loan servicing fees are recognized as revenue as the services are provided. All other commissions are recognized when services are provided. Other income/expenses are recognized to the extent of gain/loss and in the period, when arised. Foreign currency translation Monetary assets and liabilities denominated in foreign currencies and translated into RUB at the appropriate spot rates of exchange established by the Central Bank of the Russian Federation at the balance sheet date. Foreign currency transactions are accounted for at the exchange rates prevailing at the date of the transaction. Profit and losses arising from these translations are included in net gain on foreign exchange operations. Rates of exchange The exchange rates used by the Bank in the preparation of the financial statements as at year-end are as follows: 31 December

2008 31 December

2007 RUB/US Dollar 29.3804 24.5462 RUB/Euro 41.4411 35.9332 Offset of financial assets and liabilities Financial assets and liabilities are offset and reported net on the balance sheet when the Bank has a legally enforceable right to set off the recognized amounts and the Bank intends either to settle on a net basis or to realize the asset and settle the liability simultaneously. In accounting for a transfer of a financial asset that does not qualify for de-recognition, the Bank does not offset the transferred asset and the associated liability. Fiduciary activities The Bank provides trustee services to its customers. The Bank also provides depositary services to its customers which include transactions with securities on their depositary accounts. Assets accepted and liabilities incurred under the fiduciary activities are not included in the Bank‟s financial statements. The Bank accepts the operational risk on these activities, but the Bank‟s customers bear the credit and market risks associated with such operations.

18

Areas of significant management judgments and sources of estimation uncertaincy The preparation of financial statements in accordance with IFRS requires the management of the Bank to make estimates and assumptions that affect the reported amounts of the assets and liabilities of the Bank, disclosure of contingent assets and liabilities as at the reporting date and reporting amounts of income and expenses. Actual results could differ from those estimates and assumptions. Estimates that are particularly susceptible to change relate to the provisions for impairment losses and the fair value of financial instruments. The following estimates and judgements are considered to be important for presentation of a financial condition of the Bank. Loans to customers are measured at amortized cost less allowance for impairment losses. The estimation of allowance for impairment losses involves an exercise of significant judgement. The Bank estimates allowances for impairment losses with the objective of maintaining balance sheet provisions at a level believed by management to be sufficient to absorb losses incurred in the Bank‟s loan portfolio. The calculation of provisions on impaired loans is based on the likehood of the assets being written off and the estimated loss on such a write-off. These assessments are made using statistical techniques based on historical experience. These determinations are supplemented by the application of management judgement. The Bank considers accounting estimates related to provisions for loans to be key sources of estimation uncertainly because: (i) they are highly susceptible to change from period to period as the assumptions about future default rates and valuation of losses relating to impaired loans and advances are based on recent performance experience, and (ii) any significant difference between the Bank‟s estimated losses (as reflected in the provisions) and actual losses will require the Bank to take provisions which could have a material impact on its future income statement and its balance sheet. The Bank‟s assumptions about estimated losses are based on past performance, past customer behaviour, the credit quality of recent underwritten business and general economic conditions, which are not necessarily an indication of future losses. Certain property (buildings) is measured at revalued amounts. The date of the latest appraisal was 31 December 2007 year. Investments available-for-sale are measured at fair value less impairment losses. The estimation of impairment losses involves the exercise of significant management judgement. The accounting policy for the impairment of financial instruments is discussed in Note 3 below. A deferred tax asset is recognized for all deductible temporary differences to the extent that it is probable that taxable profit will be available against which the deductible temporary differences can be offset. Estimation of probabilities is based on management estimation of future taxable profit and involves the exercise of significant management judgement from the Bank. Taxation is discussed in Notes 12 and 28. Adoption of new and revised standards In the current year, the Bank has adopted all of the new and revised Standards and Interpretations issued by the IASB and IFRIC of the IASB that are relevant to its operations and effective for annual reporting periods ending on 31 December 2008. The adoption of these new and revised Standards and Interpretations has not resulted in changes to the Bank‟s accounting policies that have affected the amounts reported for the current or prior years, except the amendments to IAS 39 “Financial Instruments: Recognition and Measurement” and IFRS 7, “Financial Instruments: Disclosures” titled “Reclassification of Financial Assets”.

19

Amendments to IAS 39, “Financial Instruments: Recognition and Measurement”, and IFRS 7, “Financial Instruments: Disclosures”, titled “Reclassification of Financial Assets” – On 13 October 2008 IASB issued amendments to IAS 39 and IFRS 7 which permits certain reclassifications of non-derivative financial assets (other than those designated as at fair value through profit or loss at initial recognition under the fair value option) out of the fair value through profit or loss category and also allow reclassification of financial assets from the available for sale category to the loans and receivables category in particular circumstances. The amendments to IFRS 7 introduce additional disclosure requirements if an entity has reclassified financial assets in accordance with the amendments to IAS 39. The amendments are effective as of 13 October 2008 and in certain circumstances can be applied retrospectively from 1 July 2008. The information about the effect of accepted adjustments is presented in notes 15 and 18.

4. RECLASSIFICATIONS Reclassifications Certain reclassifications have been made to the financial statements as at 31 December 2007 and for the year then ended to conform to the presentation as at 31 December 2008 and for the year then ended as current year presentation provides better view of the financial position of the Bank. Nature of reclassification Amount

(RUB’000) Balance

sheet/Income statement line as per the previous

report

Balance sheet/Income

statement line as per current

report

Reclassification of commissions on financial market operations

13,340

Net gain on financial assets and liabilities at fair value

through profit or loss

Fee and commission

expense

Reclassification of income from the services of

processing, storing and copying of documents, trust operations 4,816

Other income

Fee and commission

income Reclassification of commissions for money

transfer services, cash-settlement services and operations where acting as an intermediary 46,681

Operating expenses

Fee and commission

expense

20

5. NET INTEREST INCOME Year ended

31 December 2008

Year ended 31 December

2007 Interest income comprises: Interest income on assets carried at amortized cost: 12,296,046 8,116,670

- interest income on impaired financial assets 11,213,642 6,931,800 - interest income on unimpaired financial assets 1,082,404 1,184,870

Interest income on financial assets at fair value 466,093 606,783 Total interest income 12,762,139 8,723,453 Interest income on assets carried at amortized cost comprises:

Interest on loans to customers 12,059,440 7,966,781 Interest on investments held-to-maturity 142,991 289 Interest on due from banks 93,615 149,600

Total interest income on financial assets carried at amortized cost 12,296,046 8,116,670 Interest income on financial assets at fair value:

Interest income on financial assets recognized at fair value through profit or loss 282,610 533,892

Interest income on financial assets available-for-sale 183,483 72,891 Total interest income on financial assets at fair value 466,093 606,783 Interest expense comprises: Interest on financial liabilities carried at amortized cost 2,736,032 2,449,320 Total interest expense 2,736,032 2,449,320 Interest expense on financial liabilities carried at amortized cost

comprise: Interest on customer accounts 1,537,378 2,023,235 Interest on deposits from banks 1,013,359 251,835 Interest on subordinated debt 120,064 77,182 Interest on debt securities issued 65,231 97,068

Total interest expense on financial liabilities carried at

amortized cost 2,736,032 2,449,320 Net interest income before provision for impairment losses on

interest bearing financial assets 10,026,107 6,274,133

6. ALLOWANCE FOR IMPAIRMENT LOSSES AND OTHER PROVISIONS The movements in allowance for impairment losses on interest bearing assets were as follows: Loans to

customers Investments

available-for-sale

Total

31 December 2006 3,203,305 25 3,203,330 Provision / (recovery) of provision 2,170,205 (3) 2,170,202 Loans written off against allowance (13,780) - (13,780) Recovery of loans previously written off 7,204 - 7,204 31 December 2007 5,366,934 22 5,366,956 Provision 3,897,191 - 3,897,191 Loans written off against allowance (3,232,791) - (3,232,791) Recovery of loans previously written off 46,834 - 46,834 31 December 2008 6,078,168 22 6,078,190

21

The movements in other allowances were as follows: Other

assets Provisions for commitments

on loans

Legal proceedings

Total

31 December 2006 12,499 34,812 - 47,311 Provision 2,101 10,315 839 13,255 Assets written off against allowance (410) - - (410) 31 December 2007 14,190 45,127 839 60,156 Provision/(recovery of provision) 8,006 (27,235) (472) (19,701) Assets written off against allowance (71) - - (71) 31 December 2008 22,125 17,892 367 40,384

7. NET GAIN/(LOSS) ON FINANCIAL ASSETS AND LIABILITIES AT FAIR VALUE THROUGH PROFIT OR LOSS Net gain/ (loss) on financial assets and liabilities at fair value through profit or loss comprises: Year ended

31 December 2008

Year ended 31 December

2007 Net (loss)/gain on financial assets and liabilities held-for-trading (26,022) 9,166 Net gain/(loss) on operations with derivative financial instruments 1,252,160 (44,056) Total net gain/(loss) on financial assets and liabilities at fair value

through profit or loss 1,226,138 (34,890) Net (loss)/gain on operations with financial assets held-for-trading

comprises: Realized gain on trading operations 19,457 173,852 Unrealized expense on fair value adjustment (45,479) (164,686)

Total net (loss)/gain on operations with financial assets and

liabilities held for trading (26,022) 9,166 The Bank enters into derivative financial instruments to manage currency and liquidity risks and such financial instruments are held primarily for trading purposes.

8. NET (LOSS)/GAIN ON FOREIGN EXCHANGE OPERATIONS Net (loss)/gain on foreign exchange operations comprise: Year ended

31 December 2008

Year ended 31 December

2007 Dealing, net 7,532 131,038 Translation differences, net (836,484) 32,815 Total net (loss)/gain on foreign exchange operations (828,952) 163,853

22

9. FEE AND COMMISSION INCOME AND EXPENSE Fee and commission income and expense comprise: Year ended

31 December 2008

Year ended 31 December

2007 Fee and commission income: Cash and settlement operations 669,558 602,833 Plastic cards operations 585,472 773,371 Operations where acting as an intermediary 254,808 242,377 Foreign exchange operations 127,396 341,977 Use of Client-Bank system 71,909 75,148 Currency control agent‟s functions 51,298 115,462 Attracting of clients service for insurance companies 40,219 19,553 Cash collection operations 27,254 24,723 Documentary operations 9,204 10,820 Typography, storage and copying of documents 6,502 5,701 Banknote transactions 3,776 2,436 Provision of services through automated information system 1,453 1,587 Broker‟s commission 1,302 2,510 Other 7,801 14,335 Total fee and commission income 1,857,952 2,232,833 Fee and commission expense: Plastic cards operations 180,974 154,336 Operations where acting as an intermediary 139,431 32,003 Operations on financial markets, including deals with securities 50,964 13,341 Settlement transactions and money transfer 49,367 32,200 Banknote transactions 13,581 7,462 Depository services 3,237 4,548 Cash collection operations 1,669 4,075 Counter-guarantees 1,483 1,736 Registrar‟s fee 871 564 Other 111 227 Total fee and commission expense 441,688 250,492

10. OTHER INCOME Other income comprises: Year ended

31 December 2008

Year ended 31 December

2007 Safe deposit boxes rental income 12,892 11,326 Gains on VISA shares received for free 11,391 - Gains on deposit interest recalculation in case of termination of

the contracts before the maturity date 7,787 - Property lease income 901 635 Fines and penalties received 846 473 Income from write-off of accounts payable 723 925 Gain on transactions with own promissory notes 125 191 Income of disposal of property not attributed to property,

plant and equipment 99 70 Refund of re-registration of the Bank‟s shares - 3,050 Refund of mandatory proposal for treasury stock acquisition - 1,726 Other 2,932 8,912 Total other income 37,696 27,308

23

11. OPERATING EXPENSES Operating expenses comprise: Year ended

31 December 2008

Year ended 31 December

2007 Staff costs 3,080,292 2,260,556 Operating leases 700,091 502,376 Unified social tax 531,290 419,575 Postal and telecommunications costs, informational systems 328,708 181,692 Depreciation and amortization charges on property, plant and

equipment and intangible assets 319,757 202,165 Other taxes and duties 306,280 209,253 Advertising costs 168,325 87,515 Stationery and inventory expenses 110,359 59,721 Repairs and maintenance of premises 104,590 71,560 Deposit insurance 102,653 162,109 Security expenses 90,807 58,229 Business trip expenses 40,492 36,229 Repairs and maintenance of other property 32,692 63,483 Repairs and maintenance of vehicles 23,752 10,346 Inventories not included in property and equipment 21,962 38,441 Information and consulting services 19,279 95,181 Loss from fixed assets disposal 18,220 217 Insurance expenses 12,155 5,504 Expenses related to the paperwork 12,087 6,803 Rights of use of intellectual property 11,138 12,474 Transport expenses 10,742 18,536 Realtor services 10,155 7,675 Auditing services 8,361 7,604 Representation expenses 6,844 760 Penalties and fines 2,202 10,586 Recruitment 2,163 4,288 Outdoor advertising expenses 1,988 1,209 Charity and sponsorship expenses 1,741 3,769 Subscription to print issues and professional literature 1,472 2,159 Membership fee 1,270 966 Revaluation loss on fixed assets - 58,515 Other expenses 24,374 36,270 Total operating expenses 6,106,241 4,635,766

12. INCOME TAXES The Bank provides for taxes based on the tax accounts maintained and prepared in accordance with the tax regulations of the Russian Federation where the Bank and its subsidiaries operate, which may differ from IFRS. The Bank is subject to certain permanent tax differences due to the non-tax deductibility of certain expenses and a tax free regime for certain income. Deferred taxes reflect the net tax effects of temporary differences between the carrying amounts of assets and liabilities for financial reporting purposes and the amounts used for tax purposes. Temporary differences as at 31 December 2008 and 2007 relate mostly to different methods of income and expense recognition as well as to recorded values of certain assets. The tax rate used for the 2008 and 2007 reconciliations below is the corporate tax rate of 24% payable by corporate entities in the Russian Federation on taxable profits under tax law in that jurisdiction. In November 2008, an amendment to the Tax Code was enacted to reduce the corporate income tax rate from 24% to 20% effective from 1 January 2009. Current year Russian income tax is measured at 24% in 2008 and 2007 of the assessable profit for the year. Starting from 31 December 2008 deferred taxes are measured at 20% (2007: 24%).

24

Temporary differences as at 31 December 2008 and 2007 comprise: 31 December

2008 31 December

2007 Deductible temporary differences: Loans to customers 464,093 146,491 Investments available-for-sale 154,141 336,062 Other liabilities and other provisions 107,134 121,112 Other assets 60,009 12,447 Investments held to maturity 8,513 - Debt securities issued 4,829 13,757 Financial assets at fair value through profit and loss - 155,707 Total deductible temporary differences 798,719 785,576 Taxable temporary differences: Property, plant and equipment and intangible assets 852,866 815,761 Financial assets at fair value through profit and loss 595 - Due from banks - 8,452 Total taxable temporary differences 853,461 824,213 Net deferred tax (liability)/asset at the statutory tax rate (20%/24%) (42,977) 51,521 Less: unrecognized deferred tax receivable - (13,061) Net deferred income tax (liability)/asset (42,977) 38,460 Net deferred tax (liability)/asset (42,977) 38,460 Relationships between tax expenses and accounting profit for the years ended 31 December 2008 and 2007 are explained as follows: 31 December

2008 31 December

2007 Profit before income tax 1,893,522 1,598,548 Tax at the statutory tax rate (24 %) 454,445 383,652 Change in unrecognized deferred tax recievables (13,061) (82,201) Tax effect of permanent differences – non deductable tax expenses 35,844 118,045 Effect of change in income tax rates (8,595) - Revise of income tax base for 2007, in 2008 (69,172) - Income tax expense 399,461 419,496 Current income tax expense 318,024 457,956 Change in the deferred tax expense 81,437 (38,460) Income tax expense 399,461 419,496

31 December

2008 31 December

2007 Beginning of the period – Deferred income tax assets 119,079 - Beginning of the period – Deferred income tax liabilities (141,413) - Changes in deferred tax liabilities and assets recognized in

the income statement (81,437) 38,460 Changes in deferred income tax assets recognized in equity 74,450 80,619 Changes in deferred income tax liabilities recognized in equity 18,373 (141,413) End of the period - Deferred income tax assets 155,069 119,079 End of the period – Deferred income tax liabilities (166,017) (141,413)

25

13. CASH AND CASH EQUIVALENTS 31 December

2008 31 December

2007 Balances with the Central Bank of the Russian Federation

(excluding minimum reserve deposits with the Central bank of the Russian Federation) 7,251,044 1,721,502

Cash in correspondent accounts and accounts in non-bank credit institutions 6,759,745 1,375,073

Cash 3,054,997 2,369,056 Total cash and cash equivalents 17,065,786 5,465,631

14. MINIMUM RESERVE DEPOSITS WITH THE CENTRAL BANK OF THE RUSSIAN FEDERATION As at 31 December 2008 and 2007 minimum reserve deposits with the Central Bank of the Russian Federation amounted to RUB 49,975 thousand and RUB 732,333 thousand, respectively. The Bank is required to maintain minimum reserve deposits with the CBR at all times.

15. FINANCIAL ASSETS AT FAIR VALUE THROUGH PROFIT OR LOSS In accordance with amendments to IAS 39 and IFRS 7 management of the Bank on 31 October 2008 decided to reclassify starting from 1 July 2008 debt securities from financial assets at fair value through profit and loss to investments available-for-sale and investments held to maturity. As at 1 July 2008 the total amount of reclassified securities was RUB 2,823,920 thousand. As at 1 July 2008 the total amount of expected cash flows from reclassified securities was RUB 3,890,310 thousand, and effective interest rates were measured from 5.06% to 10.89% per annum. If reclassification was not performed, unrealized loss on fair value of these securities totaling RUB 574,029 thousand have been included in income statement for the year ended 31 December 2008. Financial assets at fair value through profit or loss comprise: 31 December 31 December 2008 2007 Financial assets held for trading:

Debt securities 320,739 6,934,243 Total financial assets held for trading 320,739 6,934,243 Total financial assets at fair value through profit or loss 320,739 6,934,243

26

Financial assets recognized at fair value through loss or profit comprise: 31 December 2008 31 December 2007 Interest

to nominal, % Fair value Interest

to nominal, % Fair value Debt securities: Government bonds: Federal loan bonds 6-9 320,739 5.8-10 1,135,924 320,739 1,135,924 Eurobonds: Moscow City Hall - 5.06 616,562 CJSC “International Industrial Bank” - 9-9.5 362,749 CJSC “TsUN LenSpetsSMU” - 9.75 281,841 CJSC JSCB “Gazbank” - 9.75 280,076 OJSC “Promsvyazbank” - 8.75 264,391 Kazakhgold Group Ltd (Kazakhstan) - 9.38 203,375 OJSC AK “Transneft” - 5.67 192,072 TNK-ВР Holding - 6.63 183,783 OJSC “Sibacadembank” - 8.30 175,939 LLC “Slavinvestbank” - 9.88 62,026 LLC “Mirax Group” - 9.45 53,799 NAK “Naftogaz Ukraine” - 8.13 48,494 OJSC “Astana Finance” - 7.88 35,554 OJSC “Kazanorgsintez” - 9.25 24,556 - 2,785,217 Corporate bonds: LLC “Alliance-Finance” - 8.75 500,550 OJSC “Moscow Credit Bank” - 9.50 458,429 OJSC “SKB-Bank” - 9.75 415,236 JSCB “Uniastrum Bank” (LLC) - 10.9-11 347,000 CJSC CB “KEDR” - 11.15 214,116 OJSC BANK “ST. PETERSBURG” - 9 187,670 CJSC “Bank Russky Standart” - 8.25 87,787 - 2,210,788 Municipal bonds: Administration of the Republic of Karelia - 8.15 400 - 400 Promissory notes of Russian banks: LLC “SLAVINVESTBANK” - 11.68-11.73 396,141 CJSC JSCB “Russ-Bank” - 11.99-12.07 322,736 OJSC “Dalnevostochny Bank” - 10.51-10.58 83,037 - 801,914 Total debt securities 320,739 6,934,243 Total financial assets held for trading 320,739 6,934,243

27

Derivative financial instruments comprise: 31 December 2008 31 December 2007 Nominal

amount, (RUB ’000)

Net fair value

(RUB ‘000)

Nominal amount,

(RUB ’000)

Net fair value

(RUB ‘000) Asset Liability Asset Liability Derivative

financial instruments:

Foreign currency contracts

Futures 1,359,977 - - 5,726,093 - 614 Total 1,359,977 - - 5,726,093 - 614 As at 31 December 2008 and 2007 included in financial assets at fair value through profit or loss is accrued interest income on debt securities amounting to RUB 6,488 thousand and RUB 93,379 thousand, respectively. As at 31 December 2007 the use of Federal loan bonds with carrying value of RUB 592,913 thousand, bonds of OJSC “Bank St.-Petersburg” with carrying value of RUB 129,767 thousand, and bonds of OJSC “Moscow Credit Bank” with carrying value of RUB 398,164 thousand were restricted, as collateral represented by these securities enables the Bank to use the one-day and automatic overdraft loans when making transfer payments through the correspondent accounts with the CBR. As at 31 December 2008 included in financial assets at fair value through profit or loss are Federal loan bonds amounting to RUB 320,739 thousand, which were pledged as collateral under repurchase agreements with CBR.

16. DUE FROM BANKS Due from banks comprise: 31 December

2008 31 December

2007 Due from banks 412,588 1,668,290 Loans under reverse repurchase agreements - 414,781 Total due from banks 412,588 2,083,071 As at 31 December 2008 and 2007 accrued interest income of 3,148 thousand RUB and 3,403 thousand RUB, respectively was included in the balances due from banks. As at 31 December 2008 and 2007 the maximum credit risk exposure on due from banks amounted to RUB 412,588 thousand and RUB 2,083,071 thousand, respectively. Fair value of assets pledged and carrying value of loans under reverse repurchase agreements as at 31 December 2008 and 2007 are presented as follows: 31 December 2008 31 December 2007 Carrying value

of loans Fair value of

collateral Carrying value

of loans Fair value of

collateral Shares of Russian companies: OJSC “MMC “Norilsk Nickel” - - 180,137 202,459 OJSC “RAO UES of Russia” - - 125,087 140,177 OJSC “Gazprom” - - 55,028 62,757 OJSC “VTB” - - 54,529 62,200 Total - - 414,781 467,593

28

17. LOANS TO CUSTOMERS Loans to customers comprise: 31 December

2008 31 December

2007 Loans to customers 59,840,205 44,318,404 Loans under reverse repurchase agreements 457 2,396,031 59,840,662 46,714,435 Less: allowance for impairment losses (6,078,168) (5,366,934) Total loans to customers 53,762,494 41,347,501 As at 31 December 2008 and 2007 accrued interest income less allowance for imparement losses included in loans to customers amounted to RUB 930,627 thousand and RUB 649,868 thousand, respectively. Movements in allowances for impairment losses for the years ended 31 December 2008 and 2007 are disclosed in Note 6. The table below summarizes the amount of loans secured by collateral, rather than the fair value of the collateral itself: 31 December

2008 31 December

2007 Unsecured loans 29,005,066 27,574,926 Loans collateralized by pledge of real estate 21,409,849 10,271,971 Loans collateralized by pledge of vehicles 4,728,963 2,620,877 Loans collateralized by pledge of goods in turnover 3,044,629 2,311,856 Loans collateralized by other property 911,416 1,158,196 Loans collateralized by pledge of the Bank‟s promissory notes 471,421 154,131 Loans collateralized by pledge of inventories 116,217 21,913 Loans collateralized by pledge of cash 70,262 87,486 Loans collateralized by pledge of securities 20,472 2,461,393 Loans collateralized by other collateral 62,367 51,686 59,840,662 46,714,435 Less: allowance for impairment losses (6,078,168) (5,366,934) Total loans to customers 53,762,494 41,347,501 31 December

2008 31 December

2007 Analysis by sector: Individuals 43,272,867 32,167,208 Trade 4,682,275 3,298,806 Real estate and rent 4,046,080 2,079,136 Construction 3,327,180 2,577,478 Manufacturing 2,164,302 2,093,486 Agriculture 744,367 570,004 Government authorities 503,347 258,253 Finance and operating leases 309,207 209,005 Services 285,719 513,318 Transport 149,844 117,780 Science 94,016 54,744 Publishing and printing 68,745 43,591 Finance 62,830 2,531,535 Oil & gas production, refining and transportation - 48,192 Other 129,883 151,899 59,840,662 46,714,435 Less: allowance for impairment losses (6,078,168) (5,366,934) Total loans to customers 53,762,494 41,347,501

29

During the year ended 31 December 2007 the Bank received financial assets by taking possession of collateral it held as security with carring amount of RUB 62 thousand. As at 31 December 2007 such assets were not included in Property and equipment balance due to selling. There were no such cases in 2008. Loans to individuals comprise the following products: 31 December

2008 31 December

2007 Consumer loans 18,647,115 18,619,365 Mortgage loans 9,563,984 2,297,238 Plastic cards overdraft loans 8,427,450 6,281,196 Car loans 3,379,547 1,493,335 Entrepreneurs 1,523,211 1,693,105 Other 1,731,560 1,782,969 43,272,867 32,167,208 Less: allowance for impairment losses (5,613,767) (4,957,989) Total loans to individuals 37,659,100 27,209,219 As at 31 December 2008 and 2007 the Bank granted loans to 5 and 3 borrowers/groups of related borrowers totaling RUB 6,219,327 thousand and RUB 2,276,524 thousand, respectively, which individually exceeded 10% of the Bank‟s equity. As at 31 December 2008 and 2007 nearly all loans were granted to companies and individuals whose business activity is within the Russian Federation, which represents a significant geographical concentration in one region. As at 31 December 2008 and 2007 loans to 10 borrowers/groups of related borrowers totaled 14.20% (RUB 8,496,931 thousand) and 10.72% (RUB 5,008,841 thousand), respectively, in the loan portfolio. As at 31 December 2008 and 2007 a maximum credit risk exposure on loans to customers amounted to RUB 53,762,494 thousand and RUB 41,347,501 thousand, respectively. As at 31 December 2008 and 2007 a maximum credit risk exposure on loan commitments and overdrafts extended by the Bank to its customers amounted to RUB 5,694,793 thousand and RUB 9,358,033 thousand, respectively. As at 31 December 2008 and 2007 loans to customers included loans in amount of RUB 205,742 thousand and RUB 237,207 thousand, respectively, whose terms have been renegotiated. Otherwise these loans would be past due or impaired. As at 31 December 2008 and 2007 loans to customers included loans in amount of RUB 5,526,740 thousand and RUB 7,307,003 thousand, respectively, that were individually determined to be impaired. As at 31 December 2008 and 2007 such loans were collateralized by Bank‟s promissory notes, real estate, vehicles, equipment, goods in turnover and other assets types of collateral with a fair value of RUB 8,409,383 thousand and RUB 9,023,507 thousand, respectively.

30

Carrying value of loans under reverse repurchase agreements and fair value of assets pledged as at 31 December 2008 and 2007 are presented as follows: 31 December 2008 31 December 2007 Carrying value

of loans Fair value of

collateral Carrying value

of loans Fair value of

collateral Corporate shares OJSC “Surgutneftegaz” 243 242 81,318 91,396 OJSC “NK Rosneft” 132 132 20,604 23,539 OJSC “Gazprom” 62 62 254,307 288,789 OJSC “NK Lukoil” 12 12 14,929 16,810 JSB “Sberbank” (OJSC) 8 8 296,202 336,930 OJSC RAO “UES of Russia” - - 476,161 532,256 OJSC “Rostelecom” - - 250,456 291,579 VTB Bank (OJSC) - - 174,307 200,432 OJSC AK “Transneft” - - 60,386 68,776 OJSC “MMC “Norilsk Nickel” - - 27,231 30,727 OJSC “Tatneft” - - 19,492 22,202 OAO “Uralsvyazinform” - - 8,800 9,847 OJSC “POLYUS GOLD” - - 4,063 4,531 OJSC “MTS” - - 2,039 2,379 OJSC “Severstal” - - 33 33 Total corporate shares 457 456 1,690,328 1,920,226 Promissory notes of

Russian banks OJSC “ALFA-BANK” - - 223,127 227,903 JSCB “MDM-BANK” (OJSC) - - 151,908 154,103 OJSC “JSB BARS” BANK - - 147,115 150,537 OJSC “ROSSELKHOZBANK” - - 90,142 92,160 OJSC “Nomos-Bank” - - 46,902 48,097 OJSC JSCB “Moscow Bank for

Reconstruction and Development” - - 46,509 47,573 Total promissory notes

of Russian banks - - 705,703 720,373 Total 457 456 2,396,031 2,640,599

18. INVESTMENTS AVAILABLE FOR SALE In accordance with amendments to IAS 39 and IFRS 7 management of the Bank on 31 October 2008 decided to reclassify, starting from 1 July 2008, debt securities from investments available-for-sale to investments held to maturity. As at 1 July 2008 the total amount of reclassified securities was RUB 1,549,239 thousand. As at 1 July 2008 the total amount of expected cash flows from reclassified securities was RUB 2,647,143 thousand, and effective interest rates were from 10.85% to 17.79% per annum. If reclassification was not performed, an unrealized loss on fair value of these securities totaling RUB 811,947 thousand should have been recognized for the year ended 31 December 2008. Investments available-for-sale comprise: 31 December

2008 31 December

2007 Debt securities 1,947,833 1,550,969 Equity securities 19,048 12,680 Total investments available for sale 1,966,881 1,563,649

31

31 December 2008 31 December 2007

Interest to

nominal, % Fair value Interest to

nominal, % Fair value

Debt securities Eurobonds: Moscow City Hall 5.06 475,321 - - CJSC JSCB “Gazbank” 9.75 335,235 - - CJSC “TsUN LenSpetsSMU” 9.75 244,939 - - OJSC “Sibacadembank” 8.30 215,443 - - JSCB “Promsvyazbank” (CJSC) 8.75 154,602 - - OJSC AK “Transneft” 5.67 149,984 - - TNK-ВР Holding 6.63 124,197 - - CJSC “International Industrial

Bank” 9-9.5 116,938 - - LLC “Slavinvestbank” 9.88 77,121 - - LLC “Mirax Group” 9.45 54,053 - - JSC “Temirbank” - - 9.50 739,257 LLC AKB “Alliance Bank” - - 7.88-9.75 709,117 JSC Center Credit - - 8.63 102,595 Total Eurobonds 1,947,833 1,550,969 Promissory notes: OJSC “Rossiysky Credit Bank” 2.74-2.82 22 2.74-2.82 22 Less allowance for impairment

losses (22) (22) Total promissory notes: - - Total debt securities 1,947,833 1,550,969 31 December 2008 31 December 2007

Ownership,

% Amount Ownership,

% Amount

Equity securities Ordinary shares and equity interest LLC “PSF” 100 12,543 100 12,543 VISA Inc. - 6,364 - - Other - 141 - 137 Total equity securities 19,048 12,680 Total securities available-for-sale 1,966,881 1,563,649 Movements in allowances for impairment losses for the years ended 31 December 2008 and 2007 are disclosed in Note 6. As at 31 December 2008 and 2007 included in securities available-for-sale was accrued interest income of RUB 58,078 thousand and RUB 77,230 thousand, respectively. As at 31 December 2008 included in securities available-for-sale is eurobonds amounting to RUB 904,104 thousand, which were pledged as collateral under repurchase agreements with CBR.

32

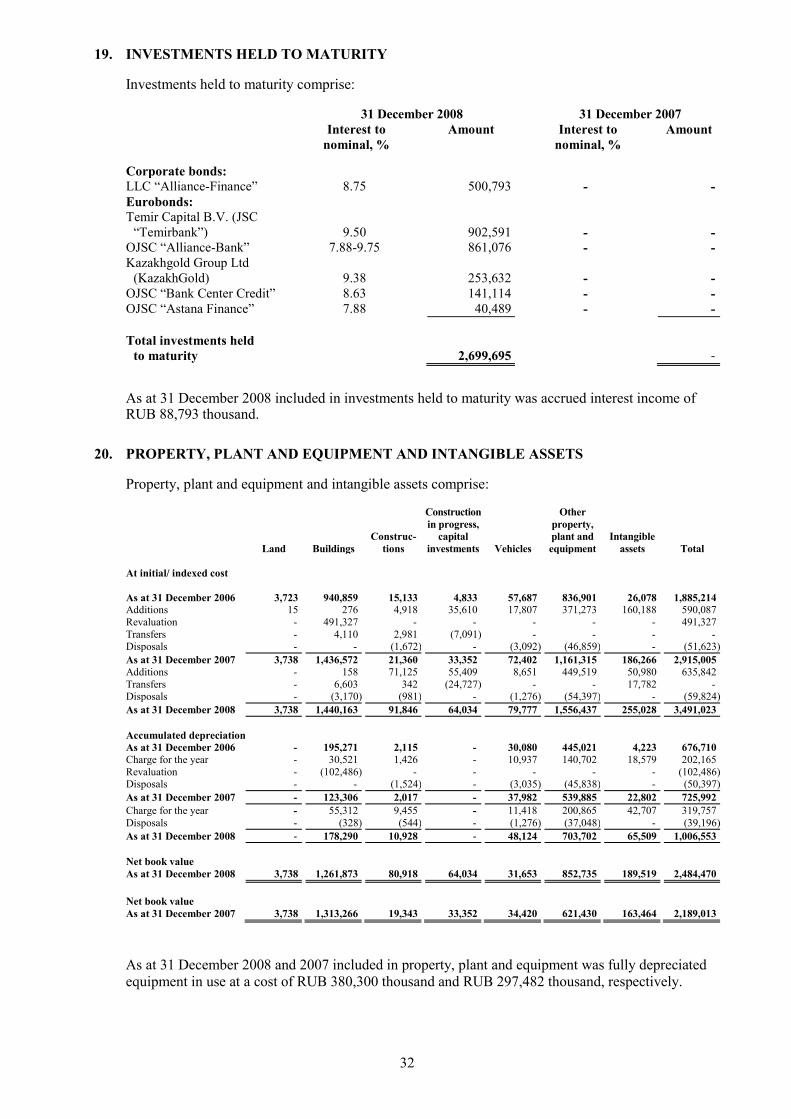

19. INVESTMENTS HELD TO MATURITY Investments held to maturity comprise: 31 December 2008 31 December 2007 Interest to

nominal, % Amount

Interest to

nominal, % Amount

Corporate bonds: LLC “Alliance-Finance” 8.75 500,793 - - Eurobonds: Temir Capital B.V. (JSC

“Temirbank”) 9.50 902,591 - - OJSC “Alliance-Bank” 7.88-9.75 861,076 - - Kazakhgold Group Ltd

(KazakhGold) 9.38 253,632 - - OJSC “Bank Center Credit” 8.63 141,114 - - OJSC “Astana Finance” 7.88 40,489 - - Total investments held

to maturity 2,699,695 - As at 31 December 2008 included in investments held to maturity was accrued interest income of RUB 88,793 thousand.

20. PROPERTY, PLANT AND EQUIPMENT AND INTANGIBLE ASSETS Property, plant and equipment and intangible assets comprise:

Land

Buildings

Construc-tions

Construction in progress,

capital investments

Vehicles

Other property, plant and equipment

Intangible assets