Embed Size (px)

Citation preview

SELLING CHOCOLATE

OPPORTUNITIES AND CHALLENGES FOR FOOD

MANUFACTURERS

FRANCISCO REDRUELLO

SENIOR FOOD ANALYST

21 NOVEMBER 2012

THE QUESTION

A SNAPSHOT ON CHOCOLATE

CASE STUDIES: BRAZIL AND CHINA

CASE STUDY: US

CASE STUDIES: SPAIN AND UK

KEY CONCLUSIONS

Q&A

© Euromonitor International

3

Money Is Tight… So Is It All Over For Chocolate? THE QUESTION

© Euromonitor International

4

Living In Uncertain Times ECONOMIC UNCERTAINTY

Source: IMF World Economic Outlook. July 2012

+5.2%

+3.8%

+3.3%

2010 2011 *2012

*GDP Growth in 2012 and 2013 is forecasted

+3.6%

*2013

© Euromonitor International

5

Not Only In Developed Economies…ECONOMIC UNCERTAINTY

Eurozone Sentiment Dampened by Debt

Worries

US Unemployment above 8%

Domestic Demand in China Weakens

Economy in Brazil and Argentina Cools Down

THE QUESTION

A SNAPSHOT ON CHOCOLATE

CASE STUDIES: BRAZIL AND CHINA

CASE STUDY: US

CASE STUDIES: SPAIN AND UK

KEY CONCLUSIONS

Q&A

© Euromonitor International

7

-1

0

1

2

3

4

5

6

2007-08 2008-09 2009-10 2010-11 2011-12

Percentage Growth (%)

Chocolate Confectionery. Global Retail Value Growth (%)

Real GDP Growth Chocolate Confectionery*

Chocolate Growth Accelerates In 2012A SNAPSHOT ON CHOCOLATE

* Constant 2012 Prices Fixed 2012 Exchange Rates. Year-on-Year Growth (%). 2012 is partially estimated

© Euromonitor International

8

Asia Pacific12%

Australasia3%

Eastern Europe15%

Latin America11%

Middle East and Africa

4%

North America20%

Western Europe35%

Chocolate Confectionery. Retail Value Sales Breakdown by Region. 2012

1.4

10.3

0.9

4.71.8

1.1

4.3

2011-12 Retail Value Growth (%)*

Emerging Markets Lead Growth A SNAPSHOT ON CHOCOLATE

* Constant 2012 Prices Fixed 2012 Exchange Rates. Year-on-Year Growth (%)

© Euromonitor International

9

Boxed Assortments And Seasonal Chocolate Stand Out A SNAPSHOT ON CHOCOLATE

Alfajores0% Bagged

Selflines/Softlines15%

Boxed Assortments

20%

Chocolate with Toys3%

Countlines26%

Seasonal Chocolate10%

Tablets25%

Other 1%

Chocolate Confectionery. Retail Value Sales Breakdown by Category. 2012

10.12.2

2.6

1.6

2.8

3.1

32011-12 Retail

Value Growth (%)*

-0.5

* Constant 2012 Prices Fixed 2012 Exchange Rates. Year-on-Year Growth (%)

© Euromonitor International

10

0

5,000

10,000

15,000

20,000

25,000

Chocolate Confectionery. Retail Value Sales. (Top Ten Markets) US$ million. 2012

1.9

3.5

Hot Market Opportunities In Brazil And China A SNAPSHOT ON CHOCOLATE

0.9-1.9

14.7 2.30.7

-0.8 1.40.3 8.6

2011-12 Retail Value Growth (%)*

* Constant 2012 Prices Fixed 2012 Exchange Rates. Year-on-Year Growth (%)

© Euromonitor International

11

Supermarkets24%

Hypermarkets14%

Discounters10%

Small Grocery Retailers26%

Other Grocery Retailers

5%

Confectionery specialists

11%

Non-Grocery Retailers

8%

Non-Store Retailing

2%

Chocolate Confectionery. Distribution Breakdown (%). Global Retail Value. 2012

0.5

0.9

0.1-0.6

-0.5

Size Matters… For Chocolate At Least A SNAPSHOT ON CHOCOLATE

-0.5

0.4

2007-12 Percentage Share Point Growth

* Constant 2012 Prices Fixed 2012 Exchange Rates. Year-on-Year Growth (%)

THE QUESTION

A SNAPSHOT ON CHOCOLATE

CASE STUDIES: BRAZIL AND CHINA

CASE STUDIES: SPAIN AND UK

KEY CONCLUSIONS

Q&A

© Euromonitor International

13

0 750 1,500 2,250

Bagged Selflines/Softlines

Boxed Assortments

Chocolate with Toys

Countlines

Seasonal Chocolate

Tablets

Other ChocolateConfectionery

Chocolate Confectionery in Brazil . Retail Value Sales. US$ Million. 2012

18.1

11.1

13.5

12.4

15.4

�Chocolate benefits from improvement in purchasing power

�Innovation underpins growth of Boxed Assortments

�Filled formats spur demand in tablets

Case Study: Chocolate Confectionery In Brazil CASE STUDIES: BRAZIL AND CHINA

2.7

10.9

2011-12 Retail Value Growth (%)*

* Constant 2012 Prices Fixed 2012 Exchange Rates. Year-on-Year Growth (%)

© Euromonitor International

14

Distribution And Premiumisation Are Key For Success CASE STUDIES: BRAZIL AND CHINA

Hershey benefits from Joint Venture with Pandurata Alimentos

Sonho Valsa

Kraft Foods Brasil

11

11.5

12

Percentage Share (%)

Hershey Co. Retail Value Share (%) in Brazil. Tablets

2010 2012

32

33

34Percentage Share (%)

Kraft Foods Brasil. Retail Value Share (%) in Brazil. Chocolate

Confectionery

2010 2012

© Euromonitor International

15

0 200 400 600 800

Bagged Selflines/Softlines

Boxed Assortments

Countlines

Tablets

Chocolate Confectionery in China. Retail Value Sales. US$ Million. 2012

5

13.9

10

�Countlines benefit from new launches

�Premium chocolate specialists drive growth of Boxed Assortments

�Bagged Selflines bank on ‘affordable snacking ‘trend

Case Study: Chocolate Confectionery In China CASE STUDIES: BRAZIL AND CHINA

6.9

2011-12 Retail Value Growth (%)*

* Constant 2012 Prices Fixed 2012 Exchange Rates. Year-on-Year Growth (%)

© Euromonitor International

16

Crispy Shark Wafer

Nestlé China

Ferrero Rocher

Ferrero China Ltd

Luxury And Positioning Drive Demand In ChinaCASE STUDIES: BRAZIL AND CHINA

16

18

20

22Percentage Share (%)

Ferrero Rocher Group. Retail Value Share (%) in China. Boxed

Assortments

2010 2012

65

70

75

Percentage Share (%)

Nestlé SA. Retail Value Share (%) in China. Countlines

2010 2012

THE QUESTION

A SNAPSHOT ON CHOCOLATE

CASE STUDIES: BRAZIL AND CHINA

CASE STUDY: US

CASE STUDIES: SPAIN AND UK

KEY CONCLUSIONS

Q&A

© Euromonitor International

18

0 2,500 5,000 7,500 10,000

Bagged Selflines/Softlines

Boxed Assortments

Countlines

Seasonal Chocolate

Tablets

Chocolate Confectionery in US . Retail Value Sales. US$ Million. 2012

3.9

3.5

-0.4

�Countlines tap into ‘indulgence on the go’

�Sport events underpin positive growth for Bagged Selflines/ Softlines

Case Study: Chocolate Confectionery In US CASE STUDIES: US

-0.4

0.7

2011-12 Retail Value Growth (%)*

* Constant 2012 Prices Fixed 2012 Exchange Rates. Year-on-Year Growth (%)

© Euromonitor International

19

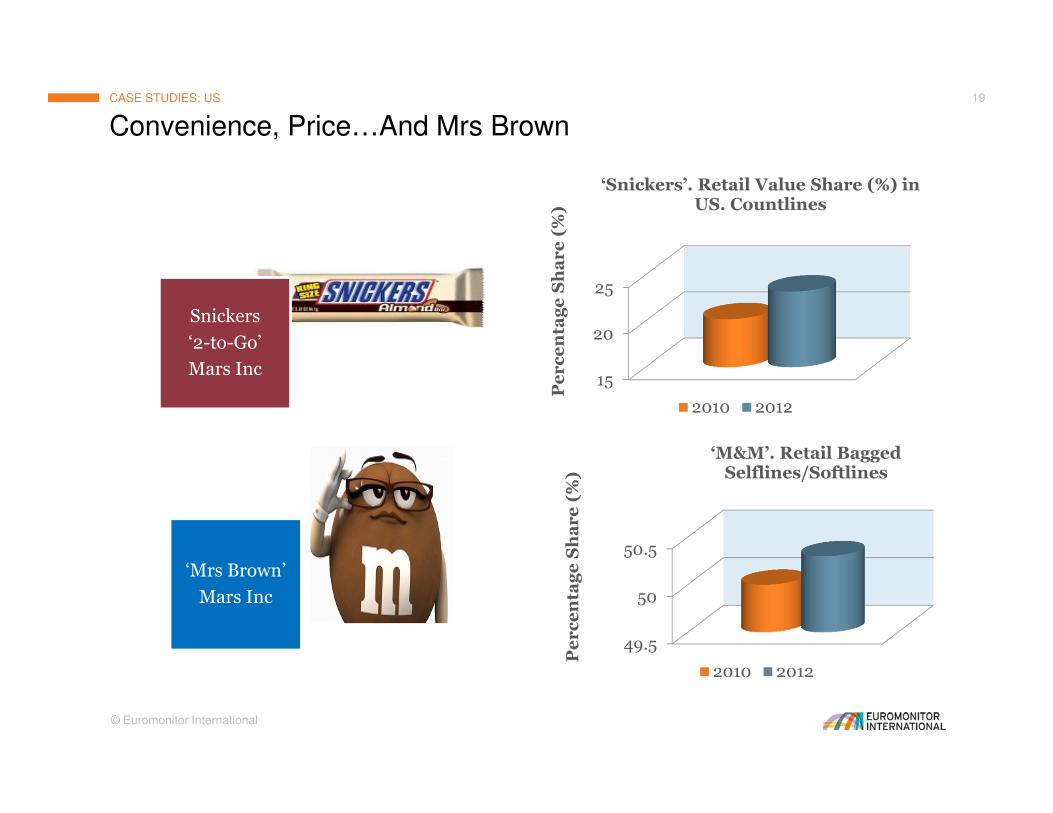

Convenience, Price…And Mrs BrownCASE STUDIES: US

Snickers

‘2-to-Go’

Mars Inc

‘Mrs Brown’

Mars Inc

15

20

25

Percentage Share (%)

‘Snickers’. Retail Value Share (%) in US. Countlines

2010 2012

49.5

50

50.5

Percentage Share (%)

‘M&M’. Retail Bagged Selflines/Softlines

2010 2012

THE QUESTION

A SNAPSHOT ON CHOCOLATE

CASE STUDIES: BRAZIL AND CHINA

CASE STUDY: US

CASE STUDIES: SPAIN AND UK

KEY CONCLUSIONS

Q&A

© Euromonitor International

21

0 200 400 600

Bagged Selflines/Softlines

Boxed Assortments

Chocolate with Toys

Countlines

Seasonal Chocolate

Tablets

Other ChocolateConfectionery

Chocolate Confectionery in Spain . Retail Value Sales. US$ Million. 2012

-0.9

-2.9

-0.6

-1.1

4

�Chocolate snacking benefits from longer working-hours

�Low retail unit prices underpin growth of Bagged Selflines/ Softlines and Countlines

Case Study: Chocolate Confectionery In Spain CASE STUDIES: SPAIN

-1.1

0.7

2011-12 Retail Value Growth (%)*

* Constant 2012 Prices Fixed 2012 Exchange Rates. Year-on-Year Growth (%)

© Euromonitor International

22

‘Dare To Show Your Soft Side’CASE STUDIES: SPAIN

Milka

‘Dare To Show Your Soft Side’

Kraft Foods España

‘Kit Kat Mini’

Nestle SA

8.4

8.6

8.8

Percentage Share (%)

‘Milka’. Retail Value Share (%) in Spain. Tablets

2010 2012

29

29.5

30Percentage Share (%)

‘Kit Kat’. Retail Value Share (%) in Spain. Countlines

2010 2012

© Euromonitor International

23

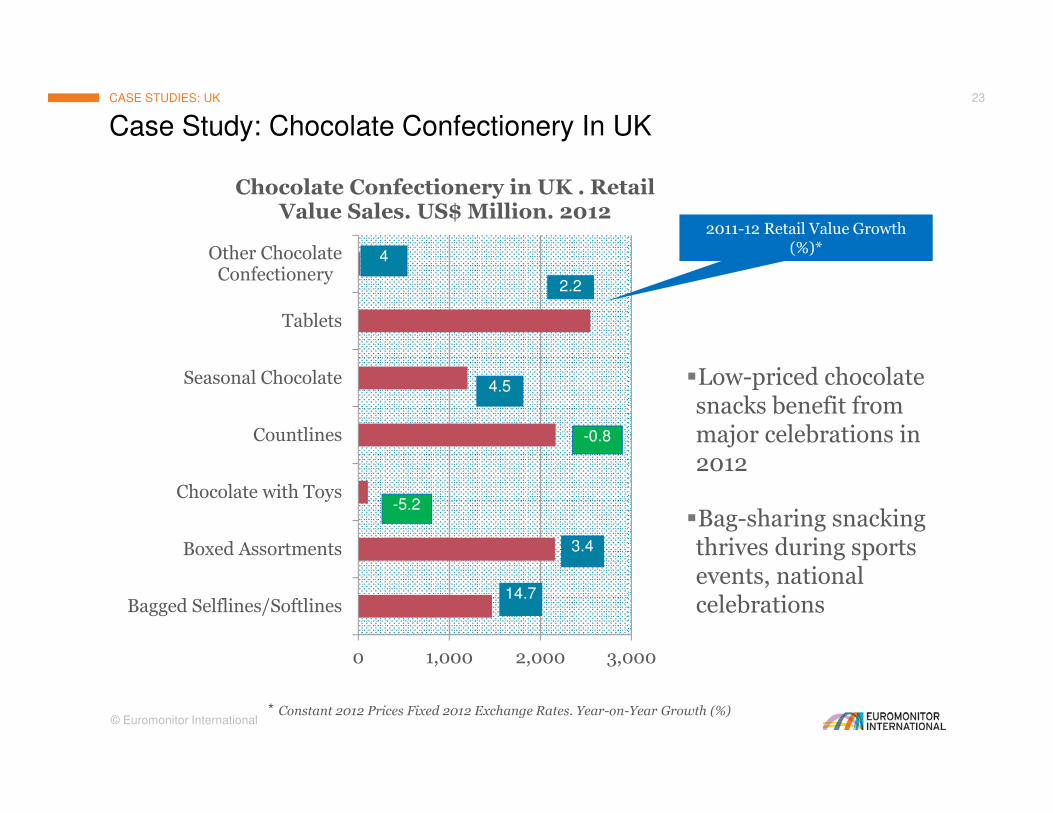

0 1,000 2,000 3,000

Bagged Selflines/Softlines

Boxed Assortments

Chocolate with Toys

Countlines

Seasonal Chocolate

Tablets

Other ChocolateConfectionery

Chocolate Confectionery in UK . Retail Value Sales. US$ Million. 2012

-0.8

3.4

�Low-priced chocolate snacks benefit from major celebrations in 2012

�Bag-sharing snacking thrives during sports events, national celebrations

Case Study: Chocolate Confectionery In UK CASE STUDIES: UK

4

2.2

4.5

-5.2

14.7

2011-12 Retail Value Growth (%)*

* Constant 2012 Prices Fixed 2012 Exchange Rates. Year-on-Year Growth (%)

© Euromonitor International

24

All You Need Is Sharing…CASE STUDIES: UK

Green & Black’s

‘Tasting Collection’

Green & Blacks Ltd

‘Bitsa Wispa’

April 2012

Cadbury UK Ltd

0

2.5

5

Percentage Share (%)

‘Green & Black’s’. Retail Value Share (%) in UK. Tablets

2010 2012

0

2

4Percentage Share (%)

‘Bitsa Wispa’. Retail Value Share (%) in UK. Selflines/Softlines

2010 2012

THE QUESTION

A SNAPSHOT ON CHOCOLATE

CASE STUDIES: BRAZIL AND CHINA

CASE STUDY: US

CASE STUDIES: SPAIN AND UK

KEY CONCLUSIONS

Q&A

© Euromonitor International

26

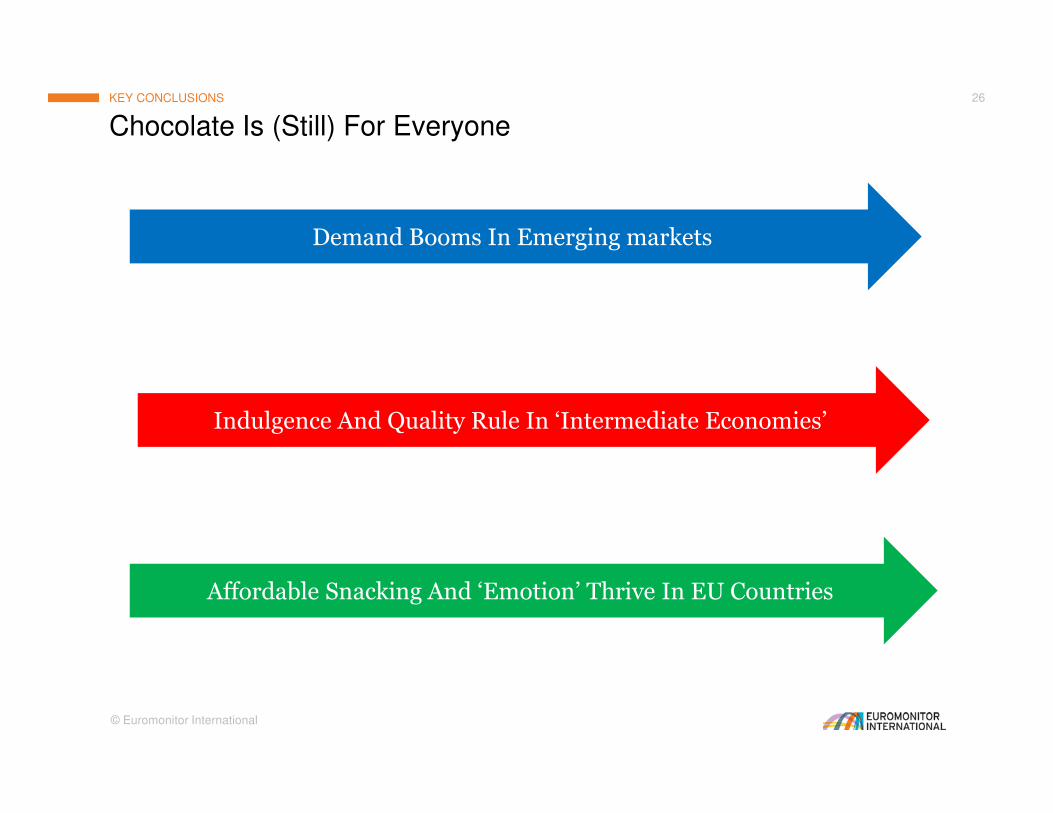

Chocolate Is (Still) For Everyone KEY CONCLUSIONS

Demand Booms In Emerging markets

Indulgence And Quality Rule In ‘Intermediate Economies’

Affordable Snacking And ‘Emotion’ Thrive In EU Countries

© Euromonitor International

27

Money Is Tight… So Is It All Over For Chocolate? THE QUESTION

© Euromonitor International

28

Money Is Never Tight For Chocolate!THE QUESTION