Embed Size (px)

DESCRIPTION

Option Pricing. Downloads. Today’s work is in: matlab_lec08.m Functions we need today: pricebinomial.m, pricederiv.m. Derivatives. A derivative is any security the payout of which fully depends on another security Underlying is the security on which a derivative’s value depends - PowerPoint PPT Presentation

Citation preview

Option Pricing

Downloads

Today’s work is in: matlab_lec08.m

Functions we need today: pricebinomial.m, pricederiv.m

Derivatives

A derivative is any security the payout of which fully depends on another security

Underlying is the security on which a derivative’s value depends

European Call gives owner the option to buy the underlying at expiry for the strike price

European Put gives owner the option to sell the underlying at expiry for the strike price

Binomial Tree

Arbitrage Pricing (1 period)

Lets make a portfolio that exactly replicates underlying payoff, buy Δ shares of stock, and B dollars of bond

CH = B*Rf+ΔPS(1+σ) CL = B*Rf+ΔPS(1-σ) Solve for B and Δ: Δ=(CH-CL)/(2σPS) and B=(CH-ΔPS(1+σ))/Rf PU= ΔPS+B

pricebinomial.m

function out=pricebinomial(pS,Rf,sigma,Ch,Cl);

D=(Ch-Cl)/(pS*2*sigma);B=(Ch-(1+sigma)*pS*D)/Rf;pC=B+pS*D;out=[pC D];

Price Call

Suppose the price of the underlying is 100 and the volatility is 10%; suppose the risk free rate is 2%

The payoff of a call with strike 100 is 10 in the good state and 0 in the bad state: C=max(P-X,0)

What is the price of this call option?>>pS=100; Rf=1.02; sigma=.1; Ch=10; Cl=0;>>pricebinomial(pS,Rf,sigma,Ch,Cl) Price=5.88, Δ=.5

Larger Trees

The assumption that the world only has two states is unrealistic

However its not unrealistic to assume that the price in one minute can only take on two values

This would imply that in one day, week, year, etc. there are many possible prices, as in the real world

In fact, at the limit, the binomial assumption implies a log-normal distribution of prices at expiry

Binomial Tree (multiperiod)

Tree as matrix

100.0000 108.0000 116.6400 125.9712 0 92.0000 99.3600 107.3088 0 0 99.3600 107.3088 0 0 84.6400 91.4112 0 0 0 107.3088 0 0 0 91.4112 0 0 0 91.4112 0 0 0 77.8688

Prices of Underlying

Recursively define prices forward>>N=3; P=zeros(2^N,N+1);%create a price grid for underlying>>P(1,1)=pS; for i=1:N; for j=1:2^(i-1); P((j-1)*2+1,i+1)=P(j,i)*(1+sigma); P((j-1)*2+2,i+1)=P(j,i)*(1-sigma); %disp([i j i+1 (j-1)*2+1 (j-1)*2+2]); end; end;

Indexing

disp([i j i+1 (j-1)*2+1 (j-1)*2+2]);

1 1 2 1 2 2 1 3 1 2 2 2 3 3 4 3 1 4 1 2 3 2 4 3 4 3 3 4 5 6 3 4 4 7 8

Payout at Expiry

Payout of derivative at expiry is a function of the underlying

European Call: C(:,N+1)=max(P(:,N+1)-X,0); European Put: C(:,N+1)=max(X-P(:,N+1),0); This procedure can price any derivative, as

long as we can define its payout at expiry as a function of the underlying

For example C(:,N+1)=abs(P(:,N+1)-X); would be a type of volatility hedge

Payout at Expiry

Prices of DerivativeRecursively define prices backwards>>X=100; C(:,N+1)=max(P(:,N+1)-X,0); %call option >>for k=1:N; i=N+1-k; for j=1:2^(i-1); Ch=C((j-1)*2+1,i+1); Cl=C((j-1)*2+2,i+1); pStemp=P(j,i); out=pricebinomial(pStemp,Rf,sigma,Ch,Cl); C(j,i)=out(1); %disp([i j i+1 (j-1)*2+1 (j-1)*2+2]); end; end;

Indexing

>>disp([i j i+1 (j-1)*2+1 (j-1)*2+2]);

3 1 4 1 2 3 2 4 3 4 3 3 4 5 6 3 4 4 7 8 2 1 3 1 2 2 2 3 3 4 1 1 2 1 2

pricederiv.m

function out=pricederiv(pS,Rf,sigmaAgg,X,N)sigma=sigmaAgg/sqrt(N); Rf=Rf^(1/N); %define sigma, Rf for shorter periodC=zeros(2^N,N+1); P=zeros(2^N,N+1); %initialize price vectorsP(1,1)=pS;for i=1:N; %create price grid for underlying for j=1:2^(i-1); P((j-1)*2+1,i+1)=P(j,i)*(1+sigma); P((j-1)*2+2,i+1)=P(j,i)*(1-sigma); end;end;C(:,N+1)=max(P(:,N+1)-X,0); %a european call for k=1:N; %create price grid for option i=N+1-k; for j=1:2^(i-1); Ch=C((j-1)*2+1,i+1); Cl=C((j-1)*2+2,i+1); pStemp=P(j,i); x=pricebinomial(pStemp,Rf,sigma,Ch,Cl); C(j,i)=x(1); end;end;out=C(1,1);

Investigating N

>>pS=100; Rf=1.02; sigmaAgg=.3; X=100; B-S value of this call is 12.8

http://www.blobek.com/black-scholes.html >>for N=1:15; out(N,1)=N; out(N,2)=pricederiv(pS,Rf,sigmaAgg,X,N); end;>>plot(out(:,1),out(:,2)); This converges to B-S as N grows!

Convergence to B-S Price

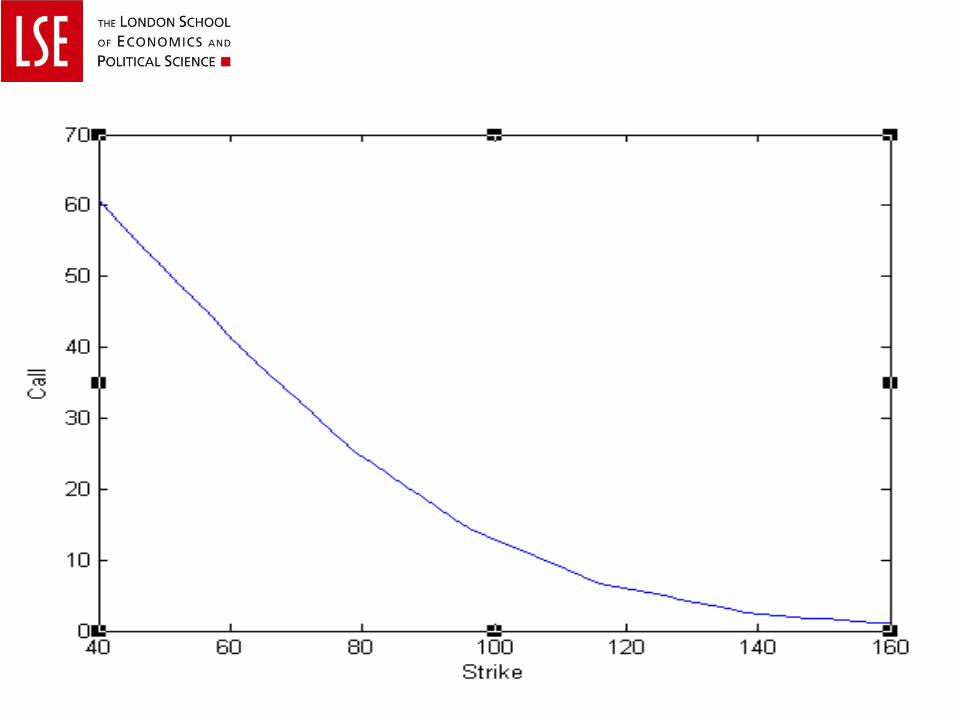

Investigating Strike Price

>>pS=100; Rf=1.02; sigmaAgg=.3; N=10;>>for i=1:50; X=40+120*(i-1)/(50-1); out(i,1)=X; out(i,2)=pricederiv(pS,Rf,sigmaAgg,X,N); end;>>plot(out(:,1),out(:,2));>>xlabel('Strike'); ylabel('Call');

InvestigatingUnderlying Price

>>X=100; Rf=1.02; sigmaAgg=.3; N=10;>>for i=1:50; pS=40+120*(i-1)/(50-1); out(i,1)=pS; out(i,2)=pricederiv(pS,Rf,sigmaAgg,X,N); end;>>plot(out(:,1),out(:,2));>>xlabel('Price'); ylabel('Call');

Investigating sigma

>>X=100; Rf=1.02; pS=100; N=10;>>for i=1:50; sigmaAgg=.01+.8*(i-1)/(50-1); out(i,1)=sigmaAgg; out(i,2)=pricederiv(pS,Rf,sigmaAgg,X,N); end;>>plot(out(:,1),out(:,2));>>xlabel('Sigma'); ylabel('Call');