-

8/4/2019 Outlook for Gas Demand & Supply by 2020

1/16

CONFERENCE ON NATURAL GAS TRANSIT AND

STORAGE IN SOUTHEST EUROPE, 31 MAY - 1 JUNE 2002

Outlook for Gas Demand

and Supply to 2020

Dr. Fatih Birol

International Energy Agency

CONFERENCE ON NATURAL GAS TRANSIT AND

STORAGE IN SOUTHEST EUROPE, 31 MAY - 1 JUNE 2002

Outlook for Gas Demand

and Supply to 2020

Dr. Fatih Birol

International Energy Agency

-

8/4/2019 Outlook for Gas Demand & Supply by 2020

2/16

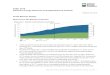

WorldEnergyOutlook2001

Insights

0

100

200

300

400

500

600

700

1980 1990 1999 2010 2020

Mtoe

Power generation& heat

Res/commercial/transport

Industry

The power sector is the main driver of gas demand

growth to 2020, but other sector contribute too

-

8/4/2019 Outlook for Gas Demand & Supply by 2020

3/16

WorldEnergyOutlook2001

Insights

0

500

1000

15002000

2500

3000

3500

4000

4500

5000

1971 2000 2010 2020

TWh

Other renewables

Hydro

Nuclear

GasOil

Coal

Most of the increase in power generation over 2000-

2020 comes from gas

-

8/4/2019 Outlook for Gas Demand & Supply by 2020

4/16

WorldEnergyOutlook2001

Insights

0

1

2

3

45

6

Coal Gas Nuclear

cen

tsperkWh

Investment O&M Fuel

Gas is most competitive fuel for power & tighter/new

emission rules will increase its edge over coal

-

8/4/2019 Outlook for Gas Demand & Supply by 2020

5/16

WorldEnergyOutlook2001

Insights

0

100

200

300

400

500

600

700

800

900

1980 1990 2000 2010 2020

bcm

Net imports

Indigenous

prodn

Most of the regions additional gas needs will have

to be imported

-

8/4/2019 Outlook for Gas Demand & Supply by 2020

6/16

WorldEnergyOutlook2001

Insights

Economic activity and industrial

production Impact of liberalisation on gas prices

relative to oil products

Competitiveness of gas in powergeneration

Distributed generation - would favour gas National & EU

policies...

-

8/4/2019 Outlook for Gas Demand & Supply by 2020

7/16

-

8/4/2019 Outlook for Gas Demand & Supply by 2020

8/16

WorldEnergyOutlook2001

Insights

Nuclear policies will determine gas

demand at the margin Diverging trends across Europe:

u Phase out agreed in Germany, Sweden &

Belgium - but how quickly?u New plant approved in Finland

u New EPR reactor design under developmentin France

u Long-term option in UK (Energy White Paperend-2002/early

2003)

-

8/4/2019 Outlook for Gas Demand & Supply by 2020

9/16

WorldEnergyOutlook2001

Insights

Gas demand poised for rapid growth

Power generation is key driver Major uncertainties

regarding:

u nuclear/renewables policies

u technology/costs

u gas price relative to other fuels

-

8/4/2019 Outlook for Gas Demand & Supply by 2020

10/16

WorldEnergyOutlook2001

Insights Potential New Gas Supply ChainsPotential New Gas Supply

Chains

Expanding pipeline networks and new LNG projects

will promote regional & global gas market integration

North America

Latin America

Europe

FSU

Africa Middle East

Asia/Pacific

Pipeline LNG

-

8/4/2019 Outlook for Gas Demand & Supply by 2020

11/16

WorldEnergyOutlook2001

Insights

Ultimate remaining resources (including

proven reserves) are an estimated 453 - 527 tcm

World total: 164 tcm at 1 January 2001

56.7

58.5

6.4

11.6

14.9

7.7

8.2

-

8/4/2019 Outlook for Gas Demand & Supply by 2020

12/16

WorldEnergyOutlook2001

Insights

0

10

20

30

40

50

Russia Iran Qatar Saudi UAE Iraq Turkmen Kazakh Uzbek Kuw ait

Azer

Rserves(tcm)

0

100

200

300

400

500

600

700

Reserves/p

roductionratio(yea

rs)

Reserves R/P ratio

Russia and Iran between them hold around half of

world proven reserves of conventional natural gas

-

8/4/2019 Outlook for Gas Demand & Supply by 2020

13/16

WorldEnergyOutlook2001

Insights

-10 10 30 50 70

Azerbaijan

Turkmenistan

Iraq

Bahrain

Oman

UAE

Iran

BcmInland consumption Net exports

Russia is by the far the largest producer (404 bcm) and

net exporter (180 bcm - entirely to Europe)

NOT INCLUDING RUSSIA

-

8/4/2019 Outlook for Gas Demand & Supply by 2020

14/16

WorldEnergyOutlook2001

Insights

All Caspian/Gulf producers could potentially supply more gas

to

Turkey and beyond but costs vary

URKEYT

YRI AS

EORGIAG

EBANONL

SRAELI

ORDANJ

RAQI

OLDOVAM

OMANIAR

ERM ANYG

RANCEF

PAINS

LGERIAAYBIAL

GYPTE

KRAIN EU

USTRI AA

ROATIACLOVANI AS

TALYI

REECEG

OUGOSY .

OS

ERZ

B . &

H .

YROMFLBANIAA

WITS .

ELGIUMB

UXL .

ETHN .NITED

INGDOM

U

K

Z

EP

C .

R .LOVAKI AS

ULGARI AB

UNISIAT

From

Volga-Urals

From

Caspian

FromAzerbaijan,Turkmenistan

&Iran

LNG

from Qatarand other Middle East

From

Iraq

From

Qatar

AUDI RABIAS A

UNGARYH

OLANDP

-

8/4/2019 Outlook for Gas Demand & Supply by 2020

15/16

WorldEnergyOutlook2001

Insights ($/Mbtu)

0 0.5 1 1.5 2 2.5 3 3.5

TURKMENISTAN (via Tky/Bulg./Rom./Hung./Aust.)

IRAN (v ia Tky/Bulg./Rom./Hung./Aust.)

0 0.5 1 1.5 2 2.5 3 3.5

IRAQ (direct)

AZERBIJAN (via Georgia)

IRAN (direct)

TURKMENISTAN (via Iran)

RUSSIA - CASPIAN (Bluestream expansion)

QATAR (via S.Arabia/Jordan/Syria)

Transport Production Transit fees

0 0.5 1 1.5 2 2.5 3 3.5

LIBYA (direct subsea)

QATAR (LNG through Suez

Canal)

Delivered to German Border

Delivered to Italy

Delivered to Turkey

-

8/4/2019 Outlook for Gas Demand & Supply by 2020

16/16

WorldEnergyOutlook2001

Insights

Several low-cost supply options to Turkey

But geopolitical risks/market barriers in producer &transit

countries

Surplus Turkish-bought gas will have to competeagainst LNG &

piped gas from N.Africa, Russiaand Norway in S & W Europe

Caspian and Gulf important options to diversifysupplies to SE

Europe