Embed Size (px)

Citation preview

Overview & Outlook for the P/C Insurance Industry:

Trends, Challenges and Opportunities

Golden Gate RIMS

San Francisco, CA

November 21, 2013

Download at www.iii.org/presentations Robert P. Hartwig, Ph.D., CPCU, President & Economist

Insurance Information Institute 110 William Street New York, NY 10038

Tel: 212.346.5520 Cell: 917.453.1885 [email protected] www.iii.org

2

Presentation Outline

P/C Insurance Industry Financial Overview ROE Growth is Critical

Economic Factors Impacting Growth Regional Analysis

By Line Impacts

Catastrophe Loss Trends

P/C Growth Analysis: $25B+ Annual Increase in DPW Key Line/Region Growth Trends

Reinsurance and the Growth of Alternative Capital

The New Investment Reality The Challenge of Persistently Low Interest Rates

P/C Performance Analysis Combined Ratio Trends and Forecasts

3

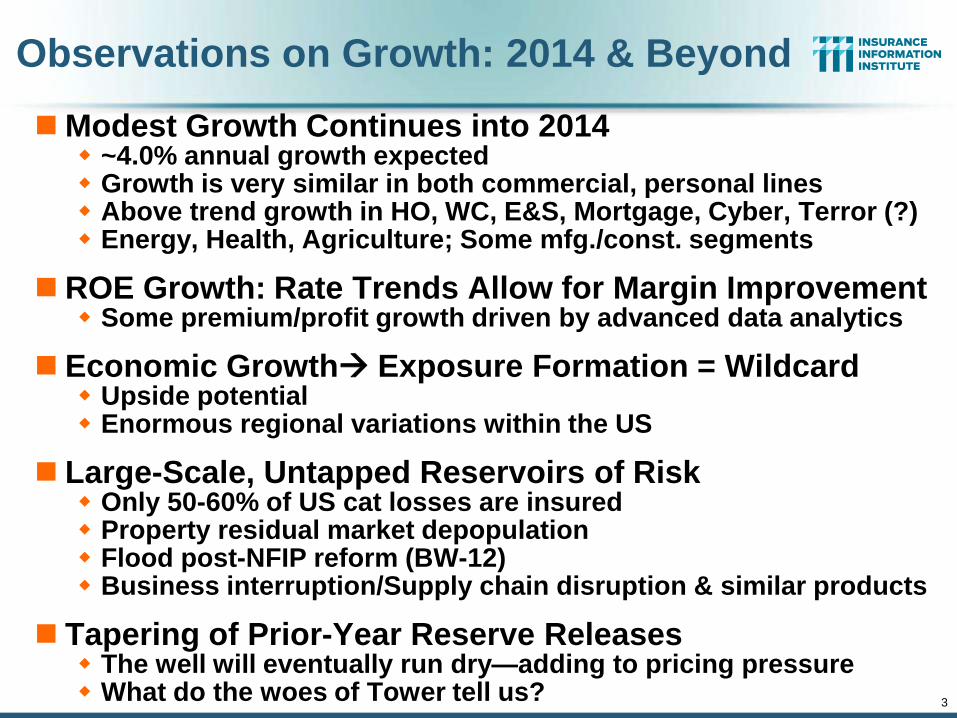

Observations on Growth: 2014 & Beyond

Modest Growth Continues into 2014 ~4.0% annual growth expected Growth is very similar in both commercial, personal lines Above trend growth in HO, WC, E&S, Mortgage, Cyber, Terror (?) Energy, Health, Agriculture; Some mfg./const. segments

ROE Growth: Rate Trends Allow for Margin Improvement Some premium/profit growth driven by advanced data analytics

Economic Growth Exposure Formation = Wildcard Upside potential Enormous regional variations within the US

Large-Scale, Untapped Reservoirs of Risk Only 50-60% of US cat losses are insured Property residual market depopulation Flood post-NFIP reform (BW-12) Business interruption/Supply chain disruption & similar products

Tapering of Prior-Year Reserve Releases The well will eventually run dry—adding to pricing pressure What do the woes of Tower tell us?

4

P/C Insurance Industry Financial Overview

So Far, So Good:

Profit Recovery in 2013 After High CAT Losses in 2011-12

4

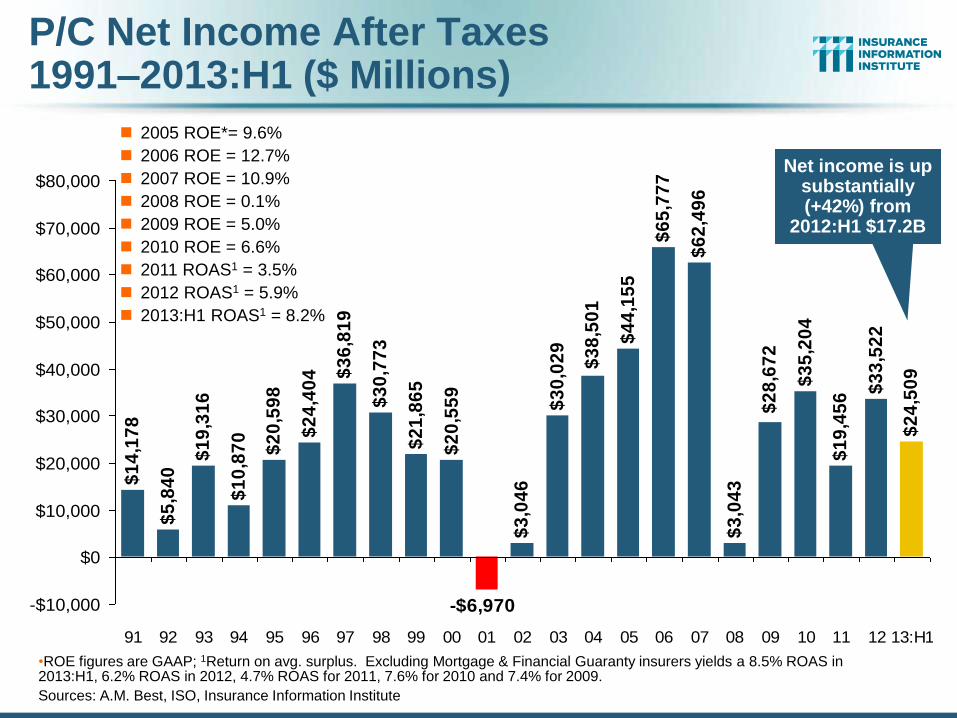

P/C Net Income After Taxes 1991–2013:H1 ($ Millions)

2005 ROE*= 9.6%

2006 ROE = 12.7%

2007 ROE = 10.9%

2008 ROE = 0.1%

2009 ROE = 5.0%

2010 ROE = 6.6%

2011 ROAS1 = 3.5%

2012 ROAS1 = 5.9%

2013:H1 ROAS1 = 8.2%

•ROE figures are GAAP; 1Return on avg. surplus. Excluding Mortgage & Financial Guaranty insurers yields a 8.5% ROAS in 2013:H1, 6.2% ROAS in 2012, 4.7% ROAS for 2011, 7.6% for 2010 and 7.4% for 2009.

Sources: A.M. Best, ISO, Insurance Information Institute

$1

4,1

78

$5

,84

0

$1

9,3

16

$1

0,8

70

$2

0,5

98

$2

4,4

04 $

36

,81

9

$3

0,7

73

$2

1,8

65

$3

,04

6

$3

0,0

29

$6

2,4

96

$3

,04

3

$3

5,2

04

$1

9,4

56

$3

3,5

22

$2

4,5

09

$2

8,6

72

-$6,970

$6

5,7

77

$4

4,1

55

$2

0,5

59

$3

8,5

01

-$10,000

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13:H1

Net income is up substantially (+42%) from

2012:H1 $17.2B

-5%

0%

5%

10%

15%

20%

25%

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

00

01

02

03

04

05

06

07

08

09

10

11

12

13

:H1

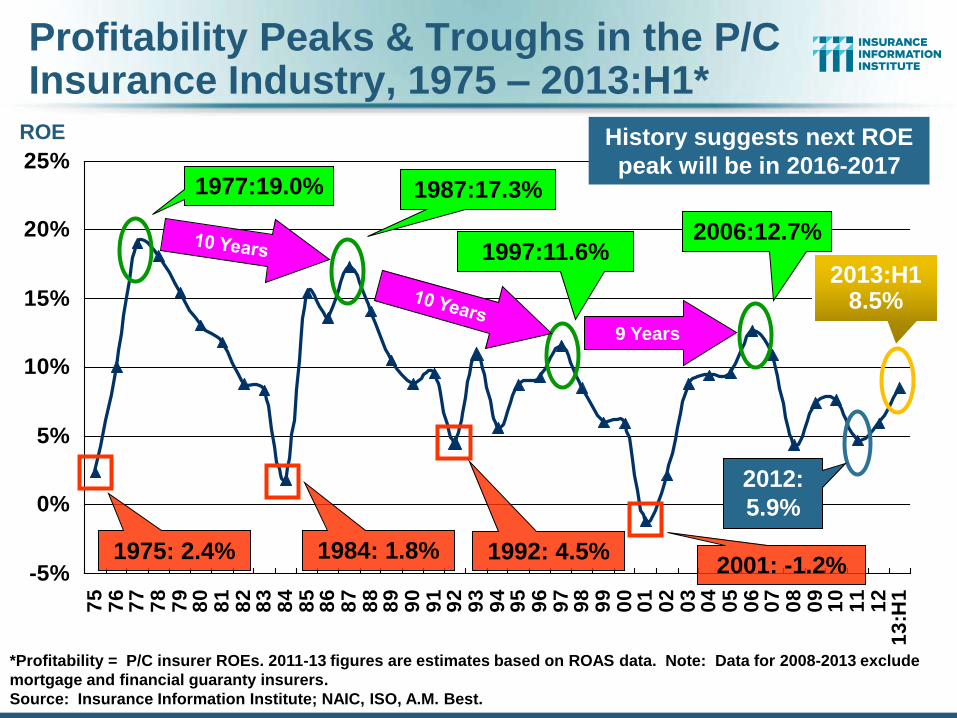

Profitability Peaks & Troughs in the P/C Insurance Industry, 1975 – 2013:H1*

*Profitability = P/C insurer ROEs. 2011-13 figures are estimates based on ROAS data. Note: Data for 2008-2013 exclude

mortgage and financial guaranty insurers.

Source: Insurance Information Institute; NAIC, ISO, A.M. Best.

1977:19.0% 1987:17.3%

1997:11.6%

2006:12.7%

1984: 1.8% 1992: 4.5% 2001: -1.2%

9 Years

2012:

5.9%

History suggests next ROE

peak will be in 2016-2017

ROE

1975: 2.4%

2013:H1 8.5%

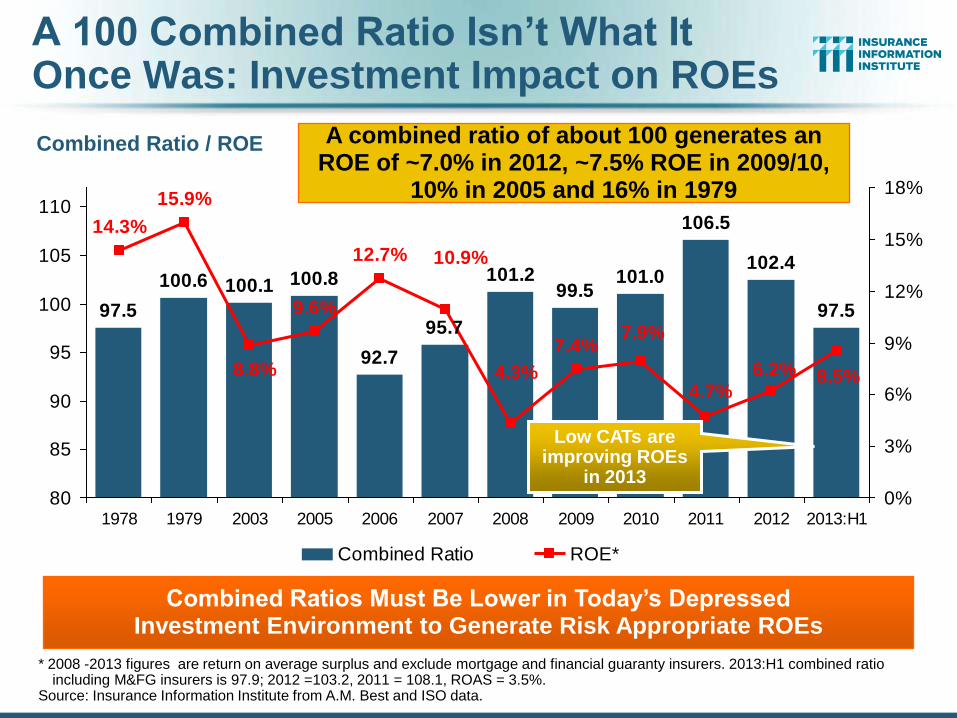

A 100 Combined Ratio Isn’t What It Once Was: Investment Impact on ROEs

Combined Ratio / ROE

* 2008 -2013 figures are return on average surplus and exclude mortgage and financial guaranty insurers. 2013:H1 combined ratio including M&FG insurers is 97.9; 2012 =103.2, 2011 = 108.1, ROAS = 3.5%.

Source: Insurance Information Institute from A.M. Best and ISO data.

97.5

100.6 100.1 100.8

92.7

101.299.5

101.0

97.5

102.4

106.5

95.7

8.5%6.2%4.7%

7.9%7.4%

4.3%

9.6%

15.9%

14.3%

12.7% 10.9%

8.8%

80

85

90

95

100

105

110

1978 1979 2003 2005 2006 2007 2008 2009 2010 2011 2012 2013:H1

0%

3%

6%

9%

12%

15%

18%

Combined Ratio ROE*

Combined Ratios Must Be Lower in Today’s Depressed Investment Environment to Generate Risk Appropriate ROEs

A combined ratio of about 100 generates an ROE of ~7.0% in 2012, ~7.5% ROE in 2009/10,

10% in 2005 and 16% in 1979

Low CATs are improving ROEs

in 2013

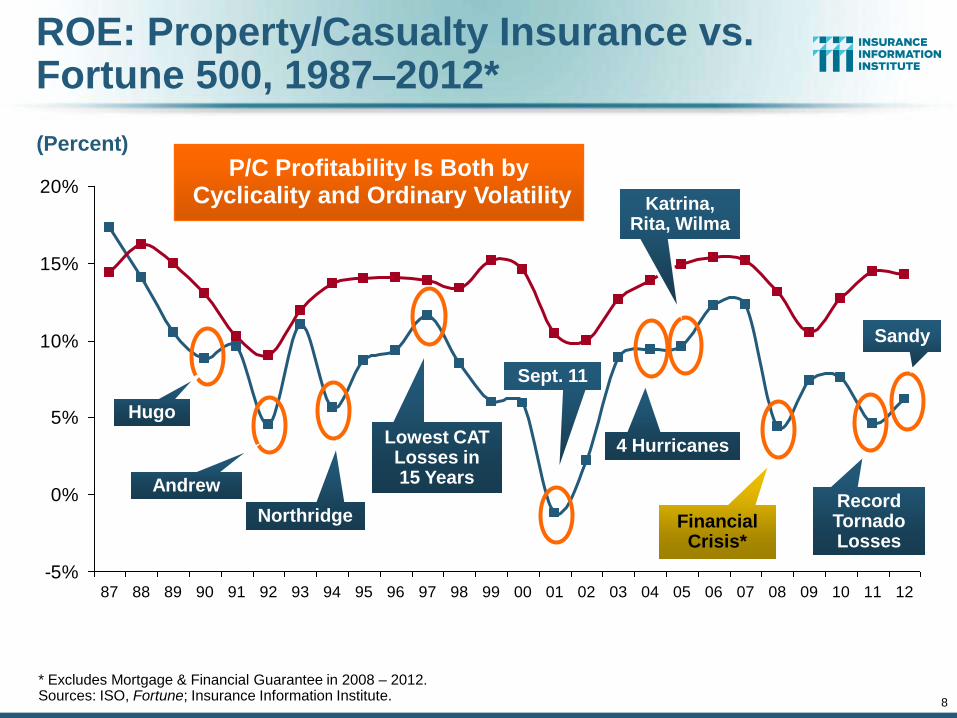

8

ROE: Property/Casualty Insurance vs. Fortune 500, 1987–2012*

* Excludes Mortgage & Financial Guarantee in 2008 – 2012. Sources: ISO, Fortune; Insurance Information Institute.

-5%

0%

5%

10%

15%

20%

87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

P/C Profitability Is Both by Cyclicality and Ordinary Volatility

Hugo

Andrew

Northridge

Lowest CAT Losses in 15 Years

Sept. 11

Katrina, Rita, Wilma

4 Hurricanes

Financial Crisis*

(Percent)

Record Tornado Losses

Sandy

9

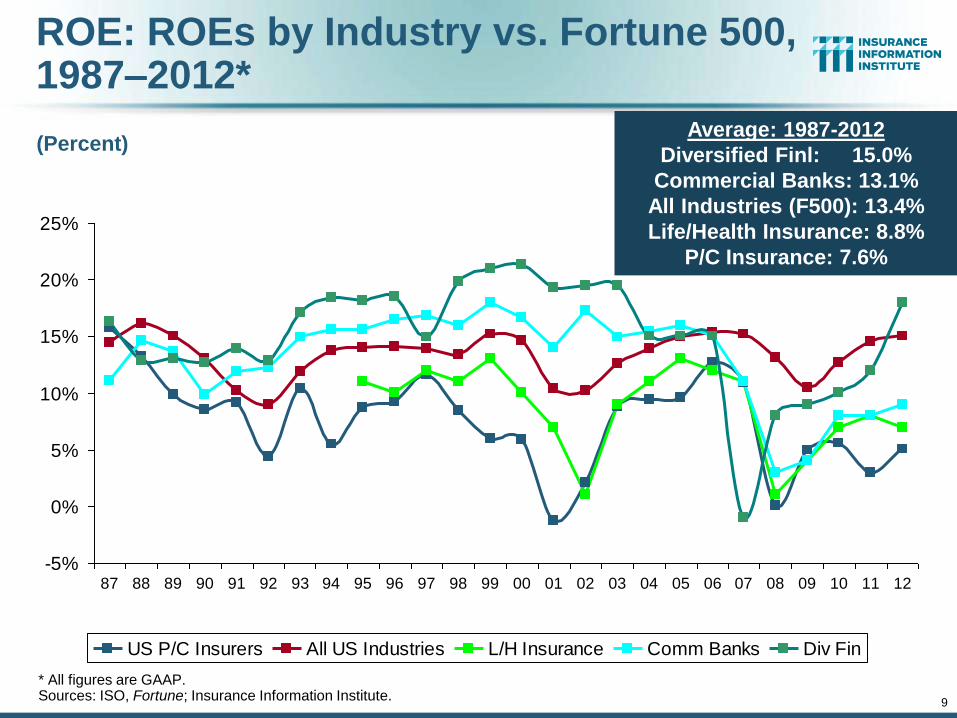

ROE: ROEs by Industry vs. Fortune 500, 1987–2012*

* All figures are GAAP. Sources: ISO, Fortune; Insurance Information Institute.

-5%

0%

5%

10%

15%

20%

25%

87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

US P/C Insurers All US Industries L/H Insurance Comm Banks Div Fin

(Percent) Average: 1987-2012

Diversified Finl: 15.0%

Commercial Banks: 13.1%

All Industries (F500): 13.4%

Life/Health Insurance: 8.8%

P/C Insurance: 7.6%

10

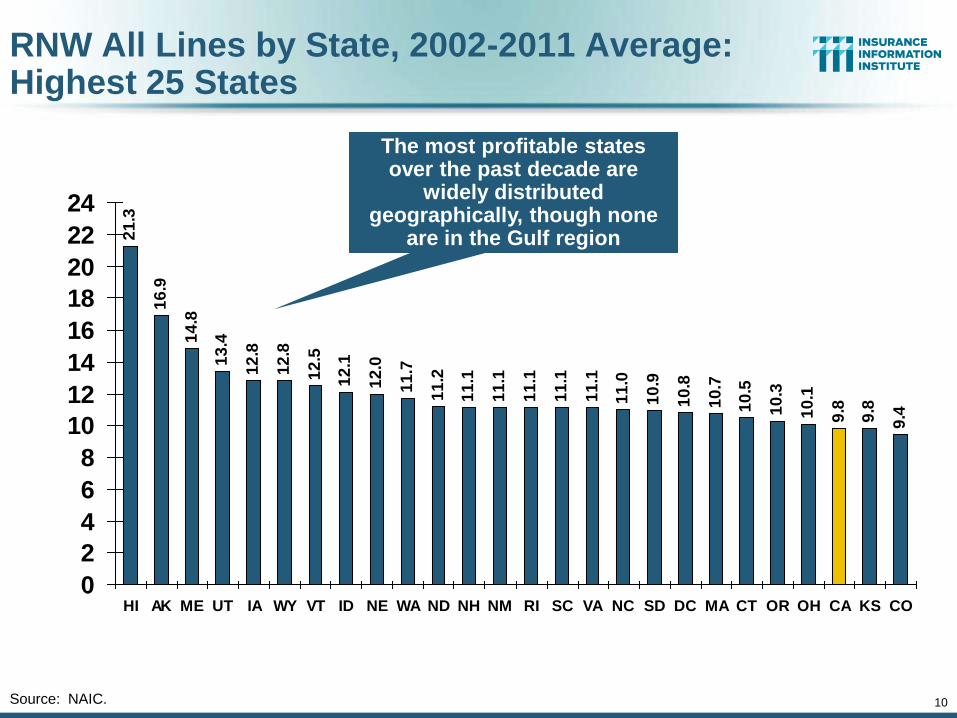

RNW All Lines by State, 2002-2011 Average: Highest 25 States

21

.3

16

.9

14

.8

13

.4

12

.8

12

.8

12

.5

12

.1

12

.0

11

.7

11

.2

11

.1

11

.1

11

.1

11

.1

11

.1

11

.0

10

.9

10

.8

10

.7

10

.5

10

.3

10

.1

9.8

9.8

9.4

0

2

4

6

8

10

12

14

16

18

20

22

24

HI AK ME UT IA WY VT ID NE WA ND NH NM RI SC VA NC SD DC MA CT OR OH CA KS CO

Source: NAIC.

The most profitable states over the past decade are

widely distributed geographically, though none

are in the Gulf region

11

9.0

8.9

8.9

8.5

8.2

8.0

7.8

7.7

7.5

7.1

7.1

7.1

6.9

6.9

6.9

6.0

6.0

5.9

5.4

5.2

4.8

3.9

3.4

1.5

-8.3

-10

.8

-14

-12

-10-8

-6

-4

-2

0

24

6

8

10

WI IN WV MD MN MT FL US NJ AR IL MO AZ PA TX KY NV NY GA MI TN OK DE AL MS LA

Un

em

plo

ym

en

t R

ate

(%

)

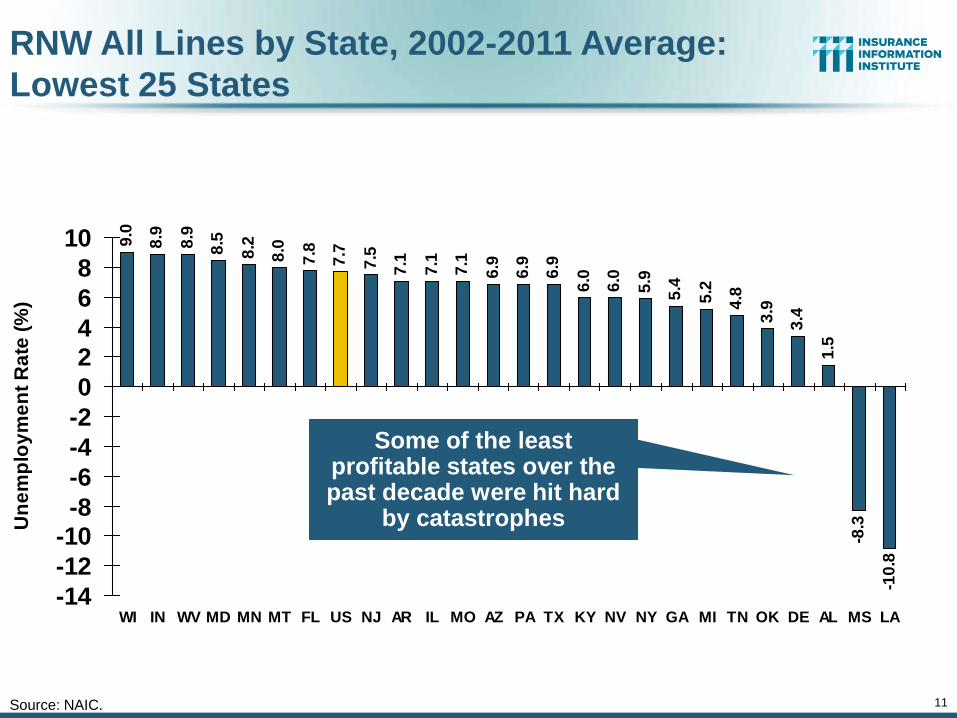

RNW All Lines by State, 2002-2011 Average:

Lowest 25 States

Source: NAIC.

Some of the least profitable states over the past decade were hit hard

by catastrophes

The Strength of the Economy Will Influence P/C Insurer

Growth Opportunities

12

Growth Will Expand Insurer Exposure

Base Across Most Lines

12

13

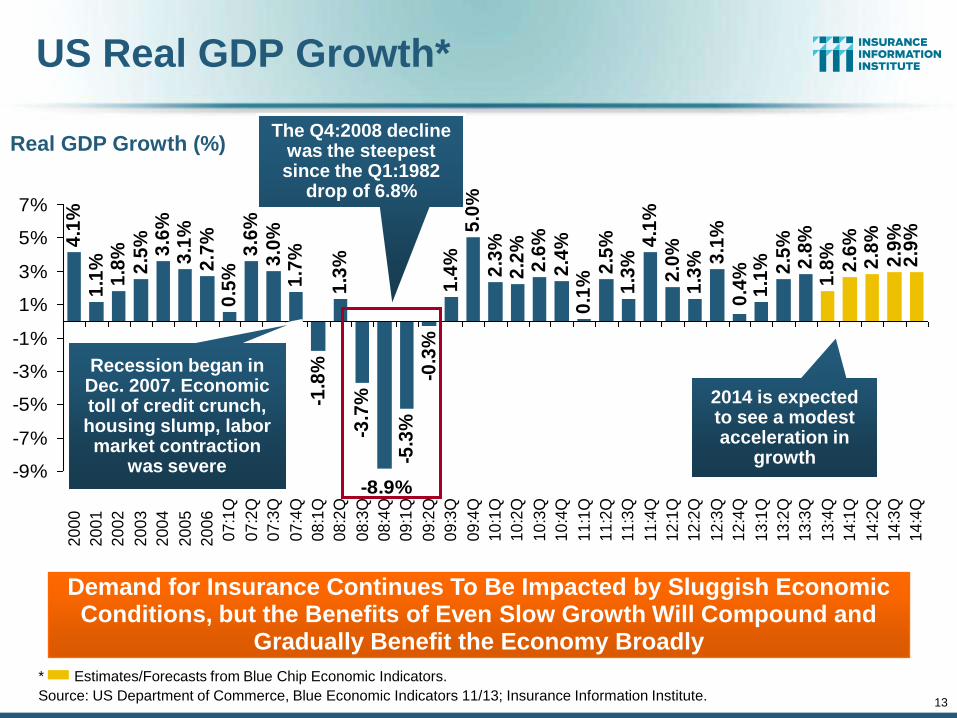

US Real GDP Growth*

* Estimates/Forecasts from Blue Chip Economic Indicators.

Source: US Department of Commerce, Blue Economic Indicators 11/13; Insurance Information Institute.

2.7

%0

.5%

3.6

%3

.0%

1.7

%-1

.8%

1.3

%-3

.7%

-5.3

%-0

.3%

1.4

%5

.0%

2.3

%2

.2%

2.6

%2

.4%

0.1

%2

.5%

1.3

%4

.1%

2.0

%1

.3% 3

.1%

1.1

% 2.5

%2

.8%

1.8

%2

.6%

2.8

%2

.9%

2.9

%

0.4

%

-8.9%

4.1

%1

.1%

1.8

%2

.5% 3.6

%3

.1%

-9%

-7%

-5%

-3%

-1%

1%

3%

5%

7%

2

00

0

2

00

1

2

00

2

2

00

3

2

00

4

2

00

5

2

00

6

07

:1Q

07

:2Q

07

:3Q

07

:4Q

08

:1Q

08

:2Q

08

:3Q

08

:4Q

09

:1Q

09

:2Q

09

:3Q

09

:4Q

10

:1Q

10

:2Q

10

:3Q

10

:4Q

11

:1Q

11

:2Q

11

:3Q

11

:4Q

12

:1Q

12

:2Q

12

:3Q

12

:4Q

13

:1Q

13

:2Q

13

:3Q

13

:4Q

14

:1Q

14

:2Q

14

:3Q

14

:4Q

Demand for Insurance Continues To Be Impacted by Sluggish Economic Conditions, but the Benefits of Even Slow Growth Will Compound and

Gradually Benefit the Economy Broadly

Real GDP Growth (%)

Recession began in Dec. 2007. Economic toll of credit crunch, housing slump, labor market contraction

was severe

The Q4:2008 decline was the steepest since the Q1:1982

drop of 6.8%

2014 is expected to see a modest acceleration in

growth

14

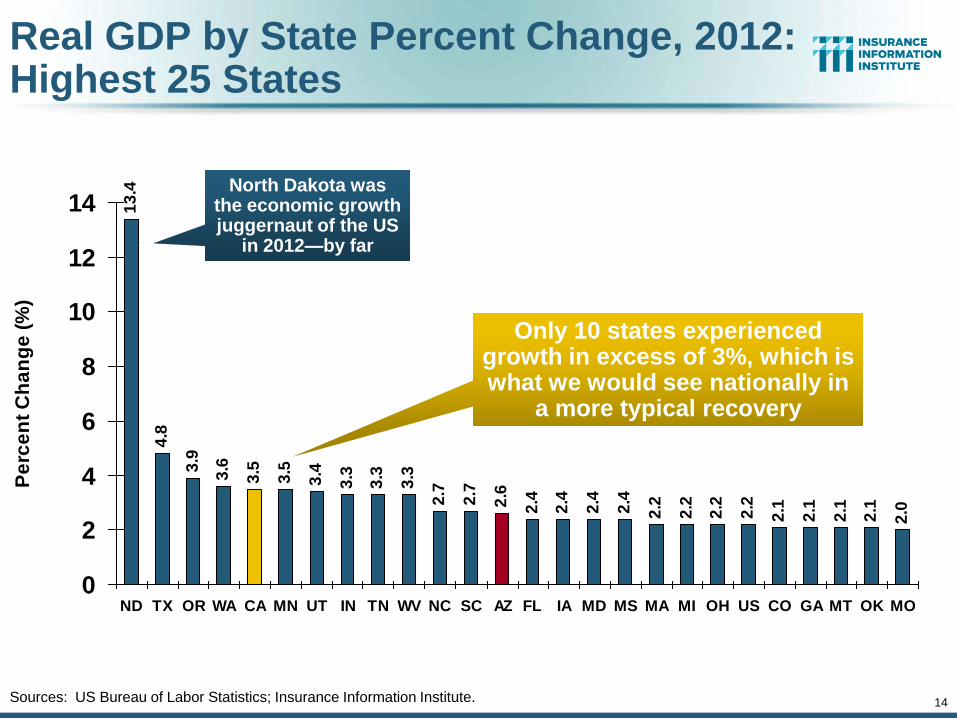

Real GDP by State Percent Change, 2012: Highest 25 States

13

.4

4.8

3.9

3.6

3.5

3.5

3.4

3.3

3.3

3.3

2.7

2.7

2.6

2.4

2.4

2.4

2.4

2.2

2.2

2.2

2.2

2.1

2.1

2.1

2.1

2.0

0

2

4

6

8

10

12

14

ND TX OR WA CA MN UT IN TN WV NC SC AZ FL IA MD MS MA MI OH US CO GA MT OK MO

Pe

rce

nt

Ch

an

ge

(%

)

Sources: US Bureau of Labor Statistics; Insurance Information Institute.

North Dakota was the economic growth juggernaut of the US

in 2012—by far

Only 10 states experienced growth in excess of 3%, which is what we would see nationally in

a more typical recovery

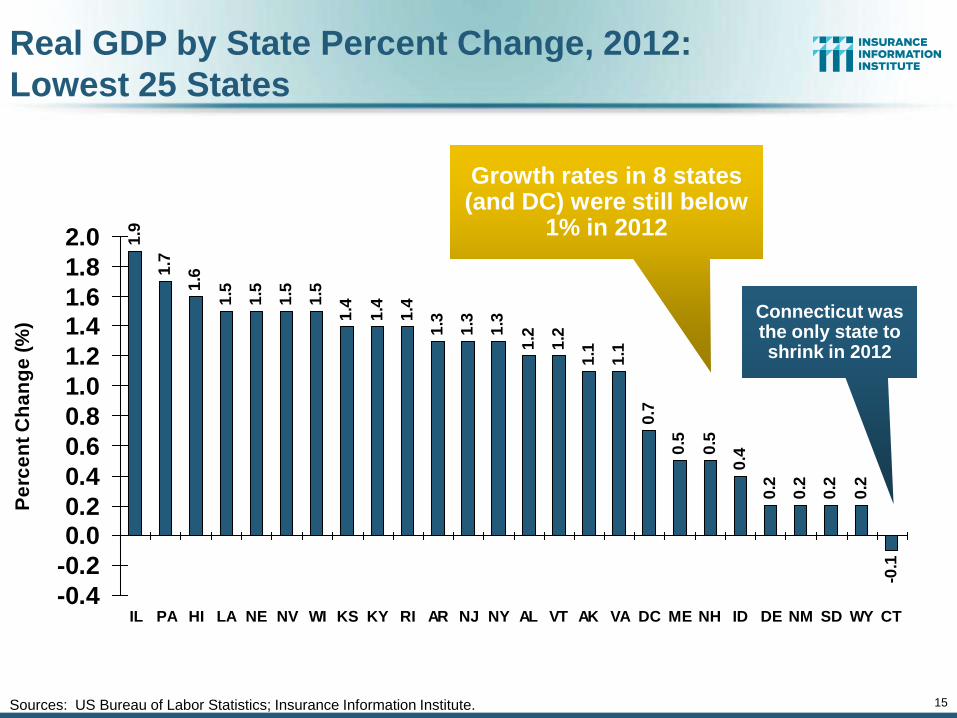

15

1.9

1.7

1.6

1.5

1.5

1.5

1.5

1.4

1.4

1.4

1.3

1.3

1.3

1.2

1.2

1.1

1.1

0.7

0.5

0.5

0.4

0.2

0.2

0.2

0.2

-0.1

-0.4

-0.2

0.00.2

0.4

0.6

0.8

1.0

1.2

1.41.6

1.8

2.0

IL PA HI LA NE NV WI KS KY RI AR NJ NY AL VT AK VA DC ME NH ID DE NM SD WY CT

Pe

rce

nt

Ch

an

ge

(%

)

Real GDP by State Percent Change, 2012:

Lowest 25 States

Sources: US Bureau of Labor Statistics; Insurance Information Institute.

Connecticut was the only state to shrink in 2012

Growth rates in 8 states (and DC) were still below

1% in 2012

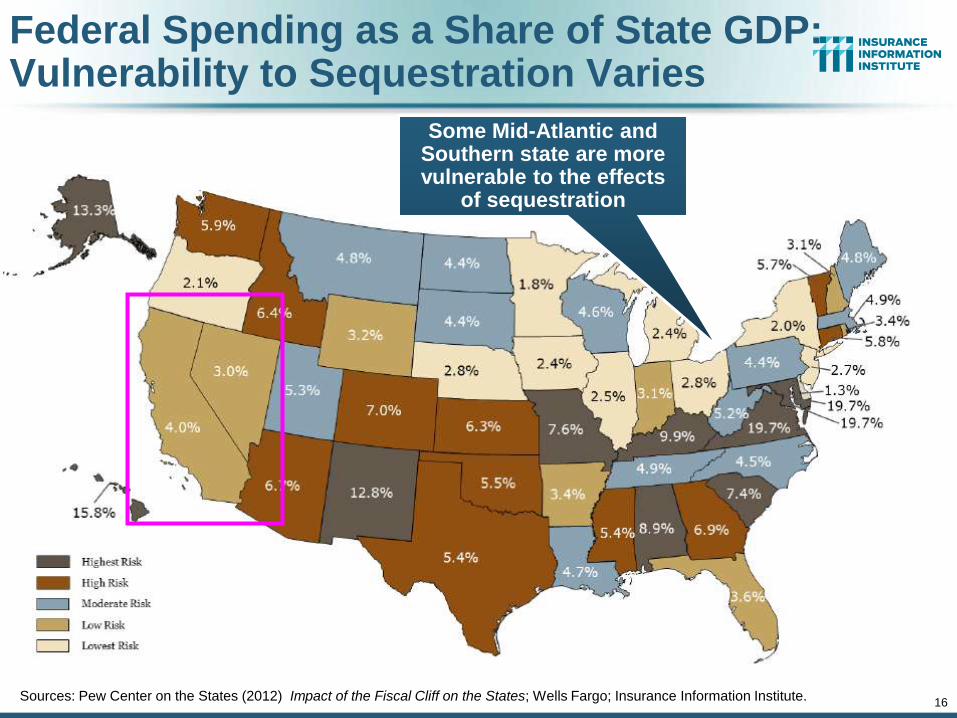

Federal Spending as a Share of State GDP: Vulnerability to Sequestration Varies

Sources: Pew Center on the States (2012) Impact of the Fiscal Cliff on the States; Wells Fargo; Insurance Information Institute. 16

Some Mid-Atlantic and Southern state are more vulnerable to the effects

of sequestration

17

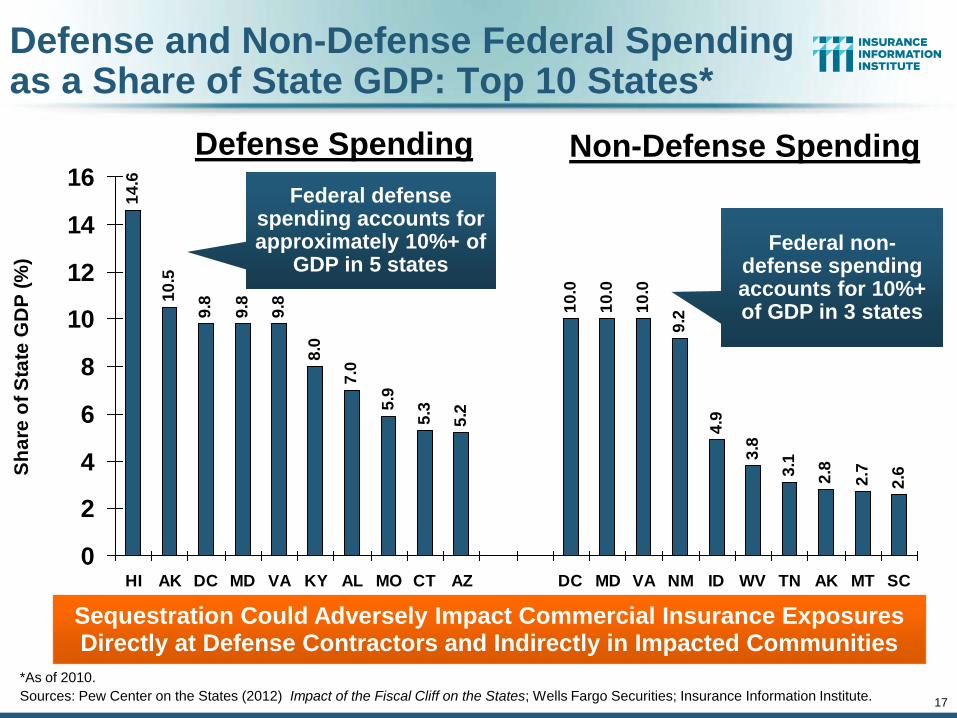

Defense and Non-Defense Federal Spending as a Share of State GDP: Top 10 States*

14

.6

10

.5

9.8

9.8

9.8

8.0

7.0

5.9

5.3

5.2

10

.0

10

.0

10

.0

9.2

4.9

3.8

3.1

2.8

2.7

2.6

0

2

4

6

8

10

12

14

16

HI AK DC MD VA KY AL MO CT AZ DC MD VA NM ID WV TN AK MT SC

Sh

are

of

Sta

te G

DP

(%

)

Federal defense spending accounts for approximately 10%+ of

GDP in 5 states

*As of 2010.

Sources: Pew Center on the States (2012) Impact of the Fiscal Cliff on the States; Wells Fargo Securities; Insurance Information Institute.

Defense Spending Non-Defense Spending

Federal non-defense spending accounts for 10%+ of GDP in 3 states

Sequestration Could Adversely Impact Commercial Insurance Exposures Directly at Defense Contractors and Indirectly in Impacted Communities

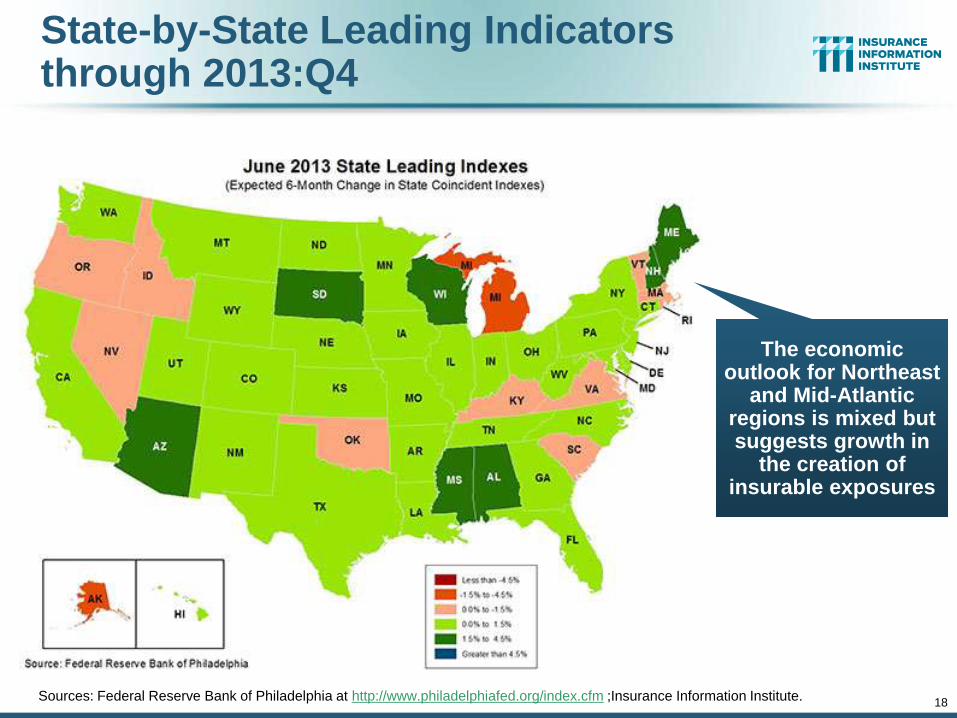

State-by-State Leading Indicators through 2013:Q4

Sources: Federal Reserve Bank of Philadelphia at http://www.philadelphiafed.org/index.cfm ;Insurance Information Institute. 18

The economic outlook for Northeast

and Mid-Atlantic regions is mixed but suggests growth in

the creation of insurable exposures

74

.47

3.6

73

.67

2.2

73

.6 76

67

.86

8.9

68

.26

7.7 7

1.6 74

.57

4.2 7

7.5

67

.5 69

.8 74

.37

1.5

63

.75

5.7 5

9.5

60

.9 64

.16

9.9

75

.07

5.3

76

.27

6.4 79

.37

3.2

72

.3 74

.38

2.6

82

.77

4.5

73

.8 77

.67

8.6

84

.58

4.1

85

.18

2.1

77

.57

3.27

6.4

40

45

50

55

60

65

70

75

80

85

90

Ja

n-1

0

Fe

b-1

0

Ma

r-1

0A

pr-

10

Ma

y-1

0

Ju

n-1

0Ju

l-1

0

Au

g-1

0

Se

p-1

0

Oct-

10

No

v-1

0

De

c-1

0

Ja

n-1

1F

eb

-11

Ma

r-1

1

Ap

r-1

1M

ay-1

1

Ju

n-1

1

Ju

l-1

1A

ug

-11

Se

p-1

1

Oct-

11

No

v-1

1D

ec-1

1

Ja

n-1

2

Fe

b-1

2M

ar-

12

Ap

r-1

2

Ma

y-1

2Ju

n-1

2

Ju

l-1

2

Au

g-1

2O

ct-

12

No

v-1

2

De

c-1

2Ja

n-1

3

Fe

b-1

3

Ma

r-1

3

Ap

r-1

3M

ay-1

3

Ju

n-1

3

Ju

l-1

3A

ug

-13

Se

p-1

3

Oct-

13

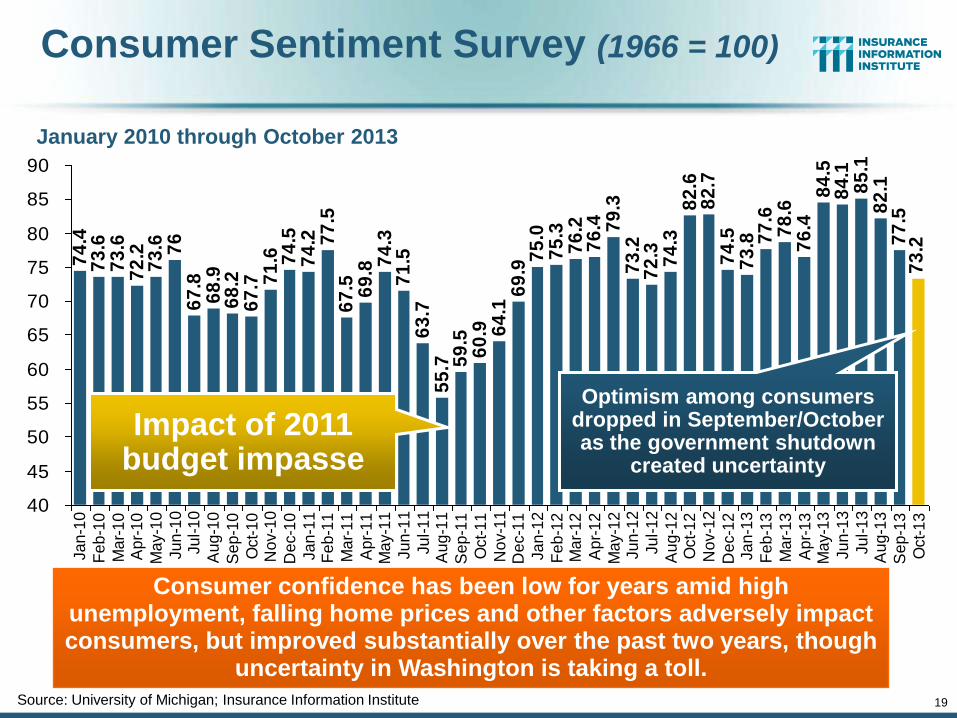

Consumer Sentiment Survey (1966 = 100)

January 2010 through October 2013

Consumer confidence has been low for years amid high unemployment, falling home prices and other factors adversely impact consumers, but improved substantially over the past two years, though

uncertainty in Washington is taking a toll.

Source: University of Michigan; Insurance Information Institute

Optimism among consumers dropped in September/October as the government shutdown

created uncertainty

19

Impact of 2011 budget impasse

20

16

.9

16

.5

16

.1

13

.2

10

.4

11

.6

12

.7

14

.4

15

.5 16

.1

16

.0

16

.2

16

.2

16

.2

16

.216

.9

16

.617

.1

17

.5

17

.8

17

.4

9

10

11

12

13

14

15

16

17

18

19

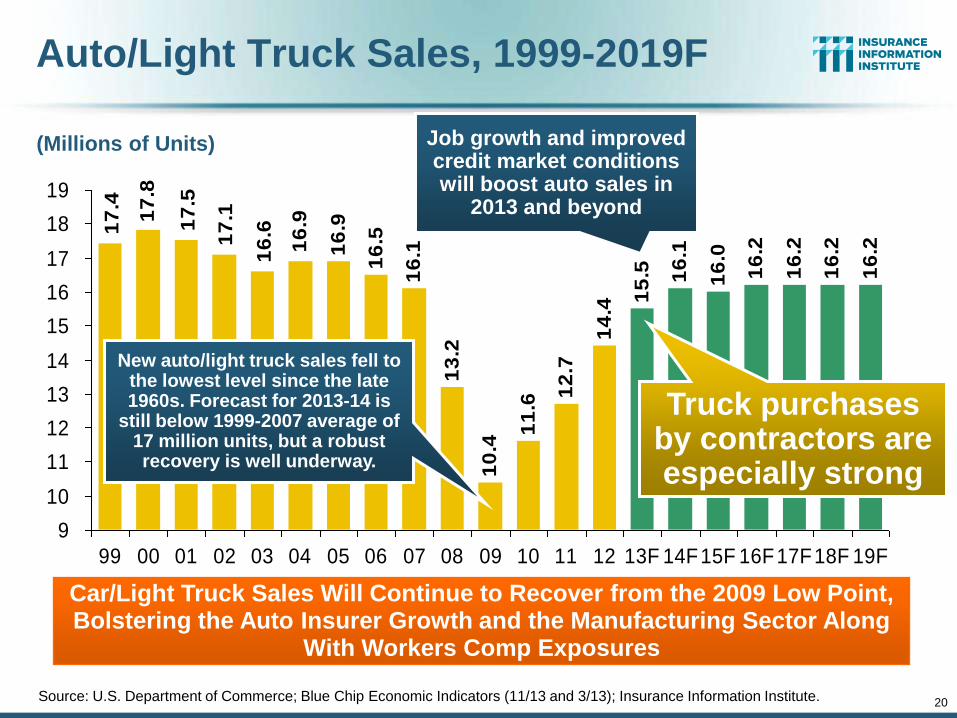

99 00 01 02 03 04 05 06 07 08 09 10 11 12 13F 14F15F 16F17F18F 19F

(Millions of Units)

Auto/Light Truck Sales, 1999-2019F

Source: U.S. Department of Commerce; Blue Chip Economic Indicators (11/13 and 3/13); Insurance Information Institute.

Car/Light Truck Sales Will Continue to Recover from the 2009 Low Point, Bolstering the Auto Insurer Growth and the Manufacturing Sector Along

With Workers Comp Exposures

New auto/light truck sales fell to the lowest level since the late 1960s. Forecast for 2013-14 is

still below 1999-2007 average of 17 million units, but a robust recovery is well underway.

Job growth and improved credit market conditions will boost auto sales in

2013 and beyond

Truck purchases by contractors are especially strong

21

16%

18%

20%

22%

24%

26%

28%

30%

01 02 03 04 05 06 07 08 09 10 11 12E 13F 14F

$125

$135

$145

$155

$165

$175

$185

$195

% of registered cars under 3 years old Auto Ins Direct Pms$ Billions

Personal Auto Insurance Direct Written Premiums vs. Recently-Registered Cars

Sources: AIPSO Facts (various issues); SNL Financial; Conning Research & Consulting, Property-Casualty Forecast and Analysis, First Quarter 2012; Insurance Information Institute.

PP DWP, flat from 2004-2009, is rising again. Conning forecasts growth at 3.5% in 2013 and 4.0% in 2014.

Average age of registered cars rose as fewer new cars were bought (and

insured)

In 2004-07 no growth in

PP DWP despite

strong new car/truck

sales New car/truck sales grow to 14-15M/year

4%/yr growth forecast for PP

DWP from recovering

new car/truck sales

22

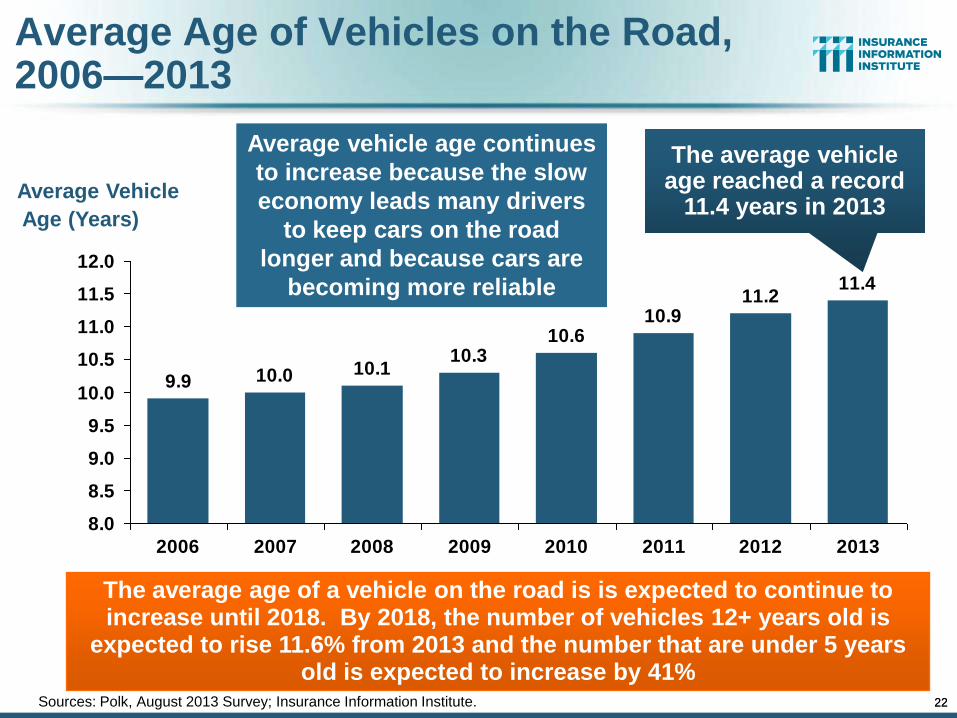

Average Age of Vehicles on the Road, 2006—2013

11.211.4

10.910.6

10.310.110.09.9

8.0

8.5

9.0

9.5

10.0

10.5

11.0

11.5

12.0

2006 2007 2008 2009 2010 2011 2012 2013

Sources: Polk, August 2013 Survey; Insurance Information Institute.

Average Vehicle

Age (Years)

The average age of a vehicle on the road is is expected to continue to increase until 2018. By 2018, the number of vehicles 12+ years old is

expected to rise 11.6% from 2013 and the number that are under 5 years old is expected to increase by 41%

The average vehicle age reached a record

11.4 years in 2013

22

Average vehicle age continues

to increase because the slow

economy leads many drivers

to keep cars on the road

longer and because cars are

becoming more reliable

23

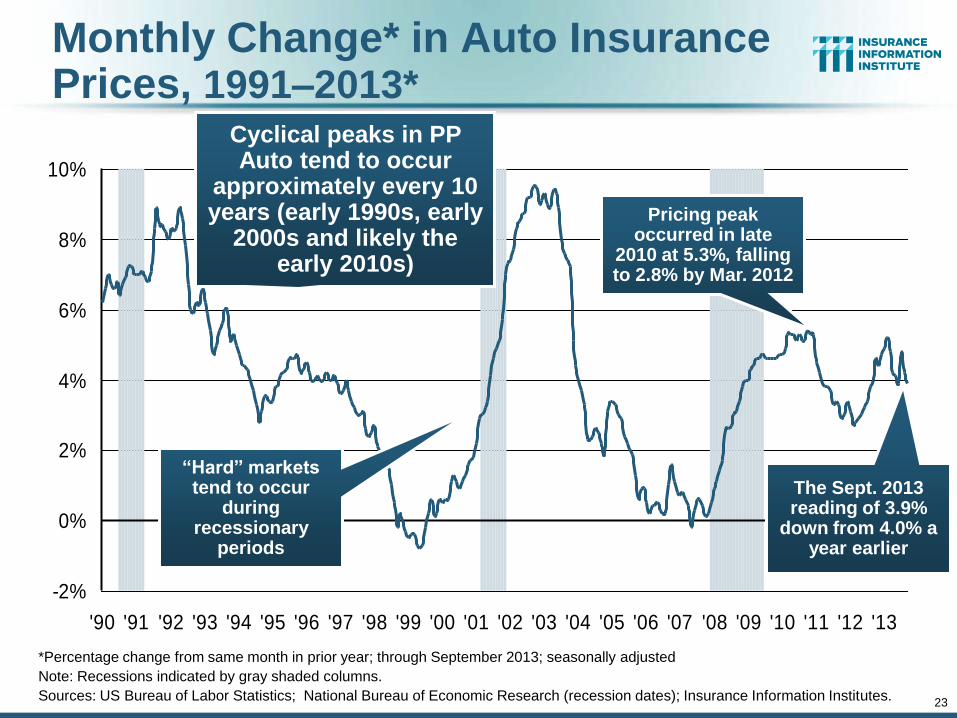

Monthly Change* in Auto Insurance Prices, 1991–2013*

*Percentage change from same month in prior year; through September 2013; seasonally adjusted

Note: Recessions indicated by gray shaded columns.

Sources: US Bureau of Labor Statistics; National Bureau of Economic Research (recession dates); Insurance Information Institutes.

-2%

0%

2%

4%

6%

8%

10%

'90 '91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13

Cyclical peaks in PP Auto tend to occur

approximately every 10 years (early 1990s, early

2000s and likely the early 2010s)

“Hard” markets tend to occur

during recessionary

periods

Pricing peak occurred in late

2010 at 5.3%, falling to 2.8% by Mar. 2012

The Sept. 2013 reading of 3.9%

down from 4.0% a year earlier

24

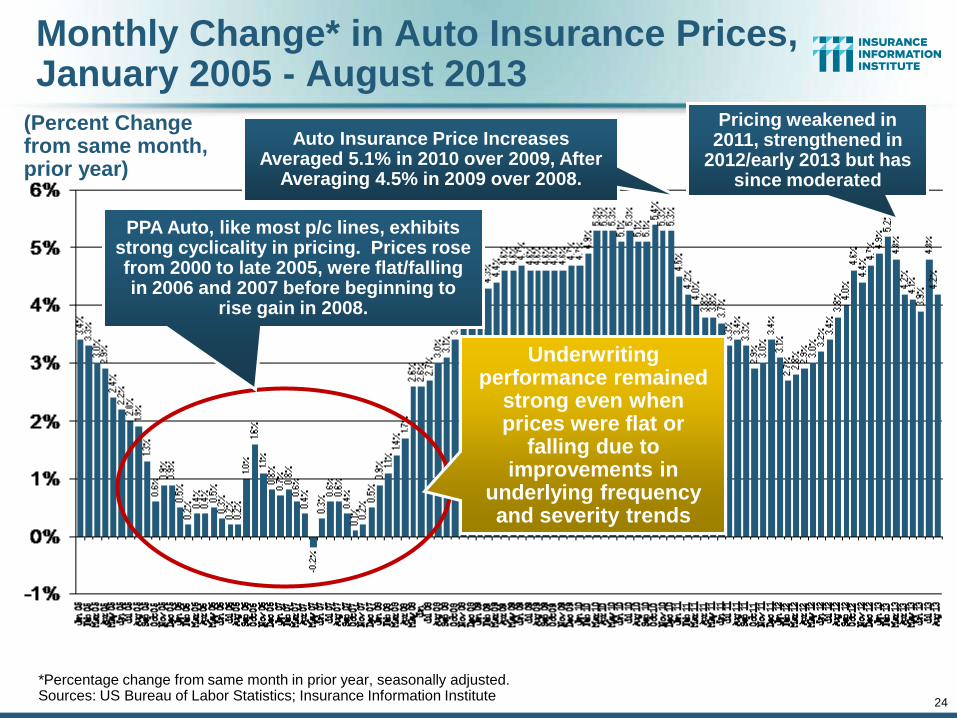

Monthly Change* in Auto Insurance Prices, January 2005 - August 2013

(Percent Change from same month, prior year)

*Percentage change from same month in prior year, seasonally adjusted. Sources: US Bureau of Labor Statistics; Insurance Information Institute

Auto Insurance Price Increases Averaged 5.1% in 2010 over 2009, After

Averaging 4.5% in 2009 over 2008.

Underwriting performance remained

strong even when prices were flat or

falling due to improvements in

underlying frequency and severity trends

PPA Auto, like most p/c lines, exhibits strong cyclicality in pricing. Prices rose from 2000 to late 2005, were flat/falling in 2006 and 2007 before beginning to

rise gain in 2008.

Pricing weakened in 2011, strengthened in

2012/early 2013 but has since moderated

25

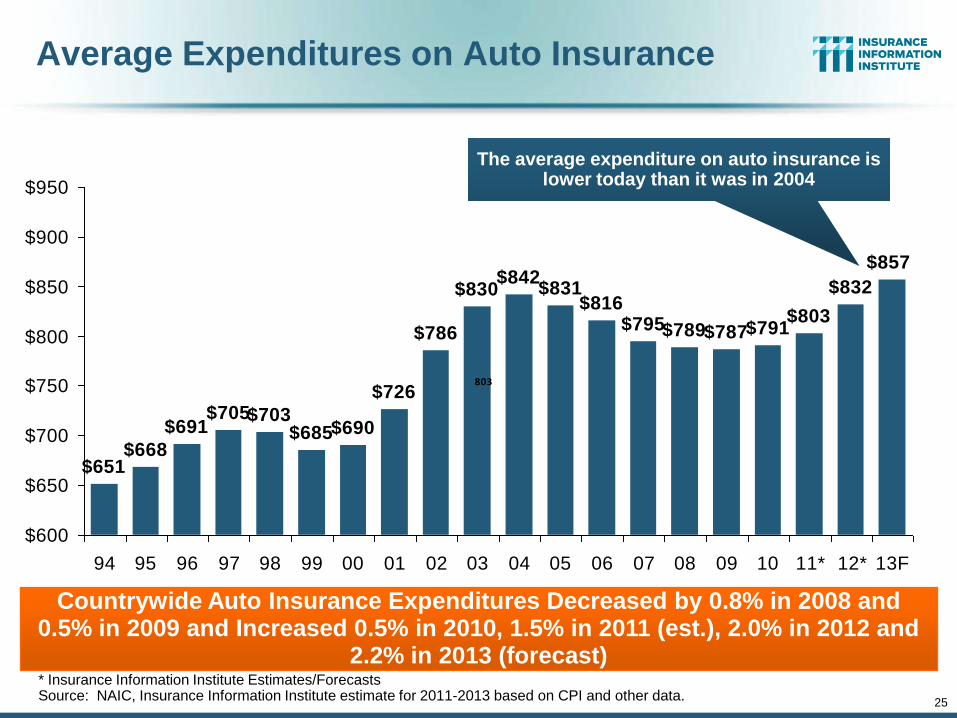

Average Expenditures on Auto Insurance

$651$668

$691$705

$726

$786

$830$842

$831$816

$795$789$787$791$803

$832

$857

$690$685$703

$600

$650

$700

$750

$800

$850

$900

$950

94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11* 12* 13F

803

Countrywide Auto Insurance Expenditures Decreased by 0.8% in 2008 and 0.5% in 2009 and Increased 0.5% in 2010, 1.5% in 2011 (est.), 2.0% in 2012 and

2.2% in 2013 (forecast) * Insurance Information Institute Estimates/Forecasts Source: NAIC, Insurance Information Institute estimate for 2011-2013 based on CPI and other data.

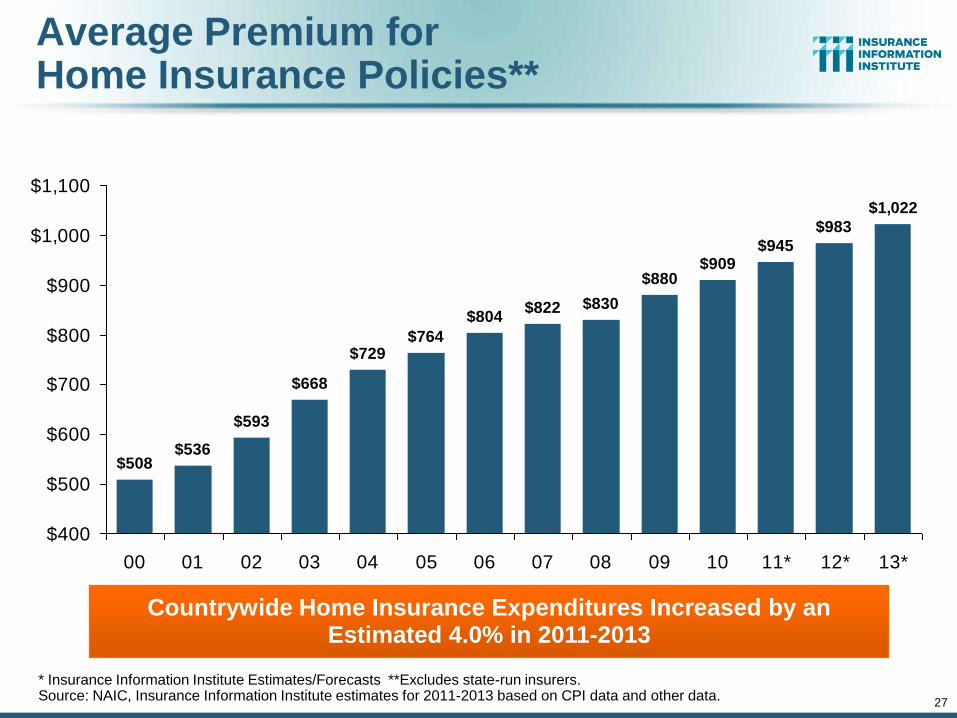

The average expenditure on auto insurance is lower today than it was in 2004

26

(Millions of Units)

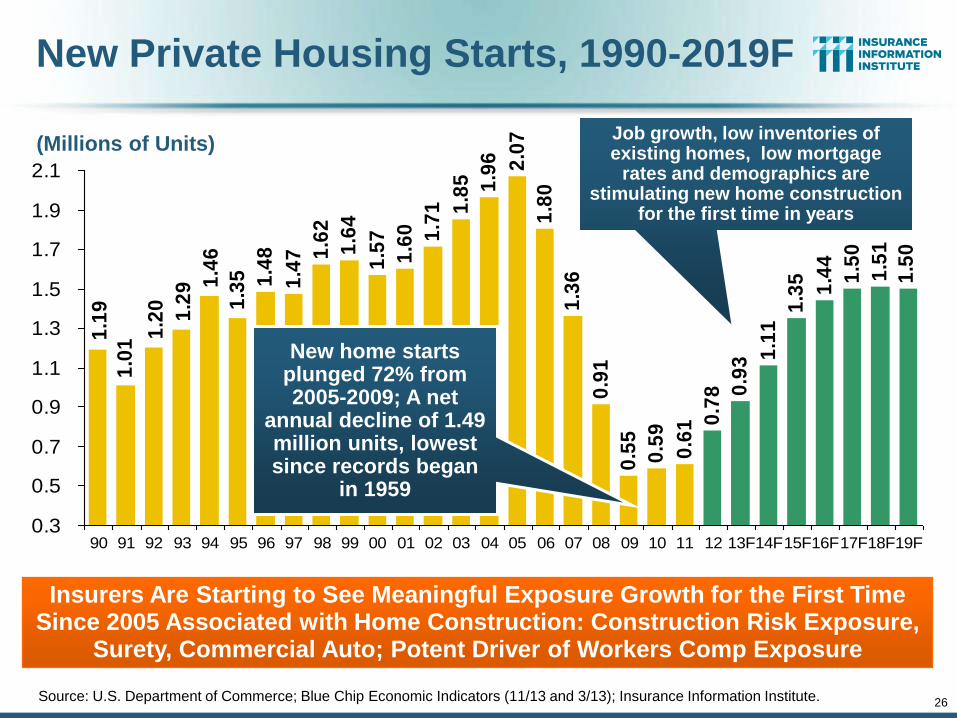

New Private Housing Starts, 1990-2019F

1.4

8

1.4

7 1.6

2

1.6

4

1.5

7

1.6

0 1.7

1 1.8

5 1.9

6 2.0

7

1.8

0

1.3

6

0.9

1

0.5

5

0.5

9

0.6

1 0.7

8 0.9

3 1.1

1

1.3

5

1.4

4

1.5

0

1.5

1

1.5

0

1.3

51.4

6

1.2

9

1.2

0

1.0

11.1

9

0.3

0.5

0.7

0.9

1.1

1.3

1.5

1.7

1.9

2.1

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13F14F15F16F17F18F19F

Source: U.S. Department of Commerce; Blue Chip Economic Indicators (11/13 and 3/13); Insurance Information Institute.

Insurers Are Starting to See Meaningful Exposure Growth for the First Time Since 2005 Associated with Home Construction: Construction Risk Exposure,

Surety, Commercial Auto; Potent Driver of Workers Comp Exposure

New home starts plunged 72% from 2005-2009; A net

annual decline of 1.49 million units, lowest since records began

in 1959

Job growth, low inventories of existing homes, low mortgage

rates and demographics are stimulating new home construction

for the first time in years

27

Average Premium for Home Insurance Policies**

* Insurance Information Institute Estimates/Forecasts **Excludes state-run insurers. Source: NAIC, Insurance Information Institute estimates for 2011-2013 based on CPI data and other data.

$508$536

$593

$668

$822 $830

$880$909

$945

$983

$1,022

$804

$764$729

$400

$500

$600

$700

$800

$900

$1,000

$1,100

00 01 02 03 04 05 06 07 08 09 10 11* 12* 13*

Countrywide Home Insurance Expenditures Increased by an Estimated 4.0% in 2011-2013

28

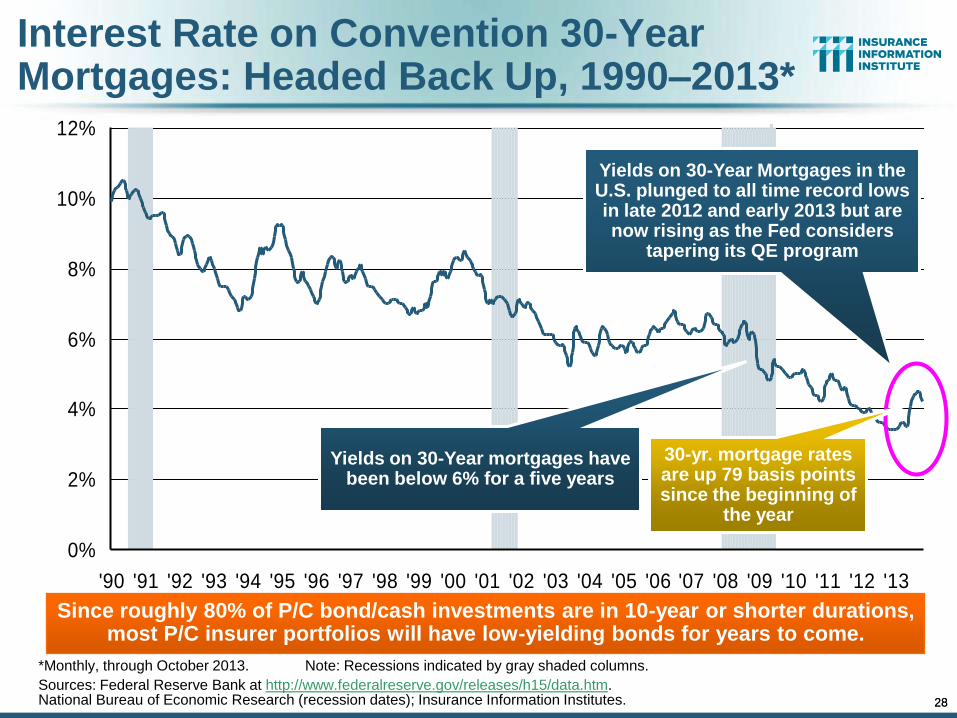

Interest Rate on Convention 30-Year Mortgages: Headed Back Up, 1990–2013*

*Monthly, through October 2013. Note: Recessions indicated by gray shaded columns.

Sources: Federal Reserve Bank at http://www.federalreserve.gov/releases/h15/data.htm. National Bureau of Economic Research (recession dates); Insurance Information Institutes.

0%

2%

4%

6%

8%

10%

12%

'90 '91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13

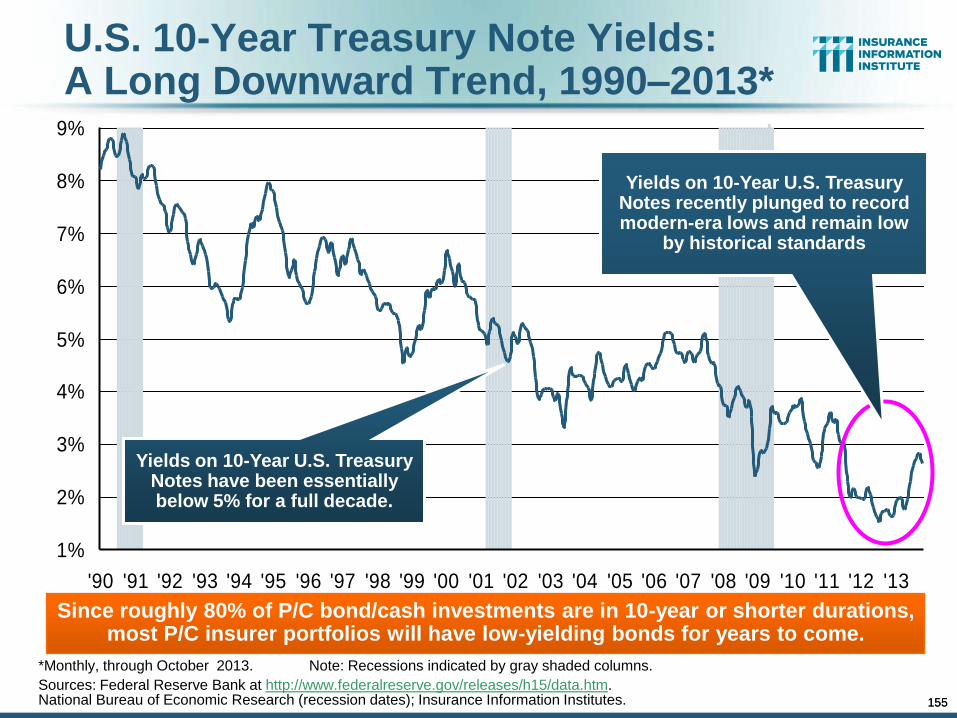

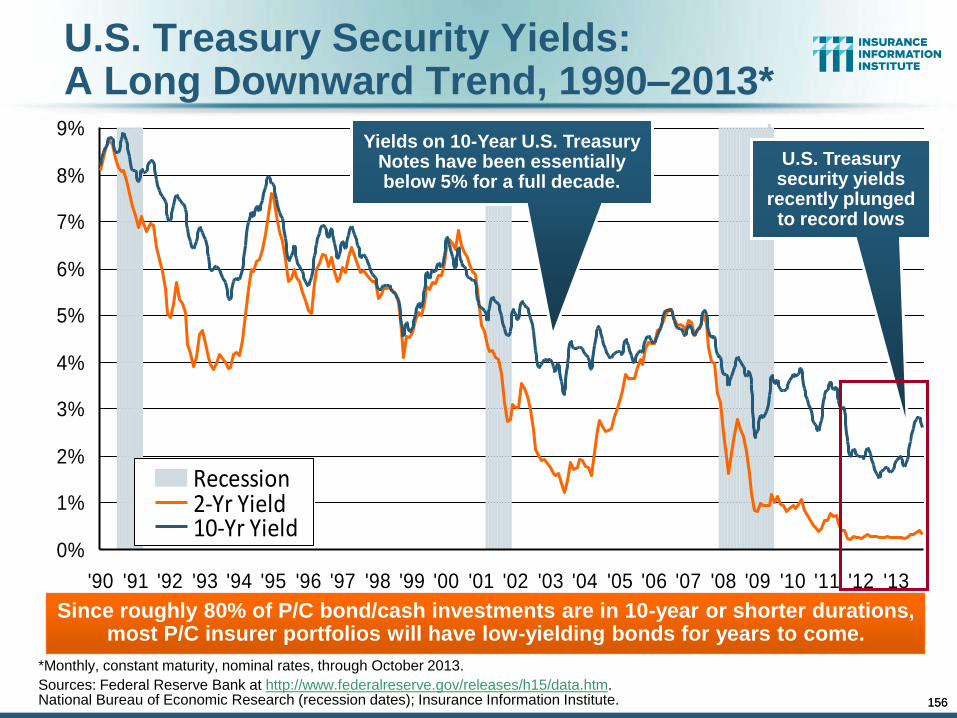

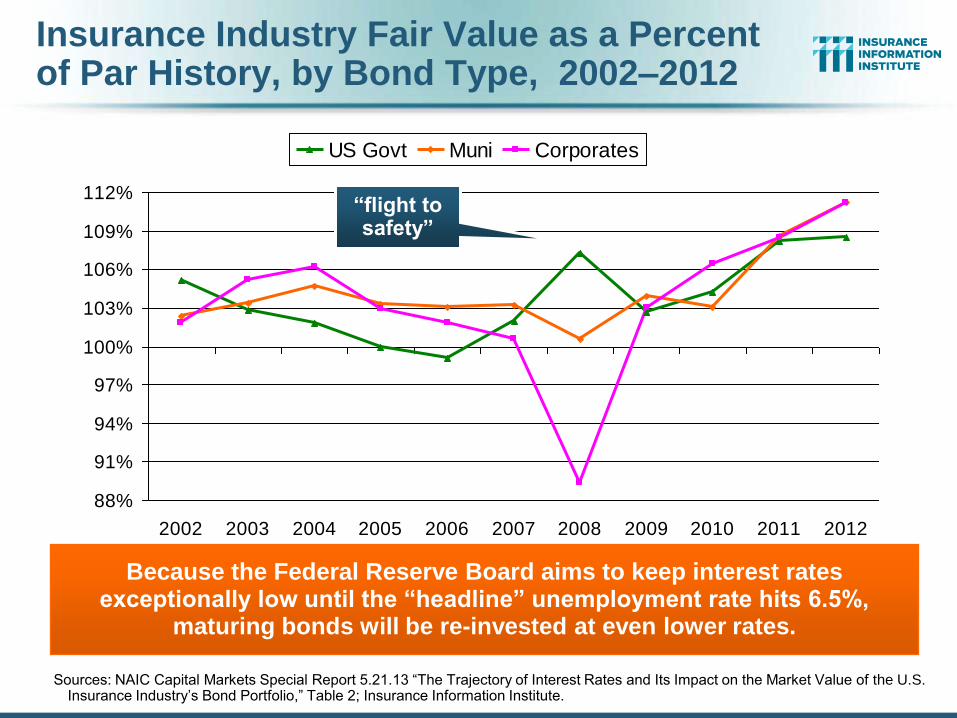

Yields on 30-Year mortgages have been below 6% for a five years

Since roughly 80% of P/C bond/cash investments are in 10-year or shorter durations, most P/C insurer portfolios will have low-yielding bonds for years to come.

Yields on 30-Year Mortgages in the U.S. plunged to all time record lows in late 2012 and early 2013 but are now rising as the Fed considers

tapering its QE program

28

30-yr. mortgage rates are up 79 basis points since the beginning of

the year

29

Mortgage Interest Rates Will Rise as Expectations Over the Fed’s Tapering of QE3 Persist; Still Low by Historical Standards

3.3

4%

3.4

0%

3.3

8%

3.4

2%

3.5

3%

3.5

3%

3.5

3%

3.5

6%

3.5

1%

3.5

2%

3.6

3%

3.5

4%

3.5

7%

3.5

4%

3.4

3%

3.4

1%

3.4

0%

3.3

5%

3.4

2%

3.5

1%

3.5

9% 3

.81

%3

.91

%3

.98

%3

.93

%4

.46

%4

.29

%4

.51

%4

.37

%4

.31

%4

.39

%4

.40

%4

.40

% 4.5

8%

4.5

1%

4.5

7%

4.5

7%

4.5

0%

4.3

2%

4.2

2%

4.2

3%

4.2

8%

4.1

3%

4.1

0%

4.1

6% 4

.35

%

3.0%

3.2%

3.4%

3.6%

3.8%

4.0%

4.2%

4.4%

4.6%

4.8%

03-J

an

10-J

an

17-J

an

24-J

an

31-J

an

07-F

eb

14-F

eb

21-F

eb

28-F

eb

07-M

ar

14-M

ar

21-M

ar

28-M

ar

04-A

pr

11-A

pr

18-A

pr

25-A

pr

02-M

ay

09-M

ay

16-M

ay

23-M

ay

30-M

ay

06-J

un

13-J

un

20-J

un

27-J

un

04-J

ul

11-J

ul

18-J

ul

25-J

ul

01-A

ug

08-A

ug

15-A

ug

22-A

ug

29-A

ug

05-S

ep

12-S

ep

19-S

ep

26-S

ep

03-O

ct

10-O

ct

17-O

ct

24-O

ct

31-O

ct

07-N

ov

14-N

ov

30-year mortgage rates were up sharply from their

lows earlier in the year

30-Year Mortgages in 2013 Are Rising: What Will Be the Impact on Construction?

*Weekly through November 14, 2013.

Sources: Federal Reserve Bank at http://www.federalreserve.gov/releases/h15/data.htm.; Insurance Information Institutes.

30

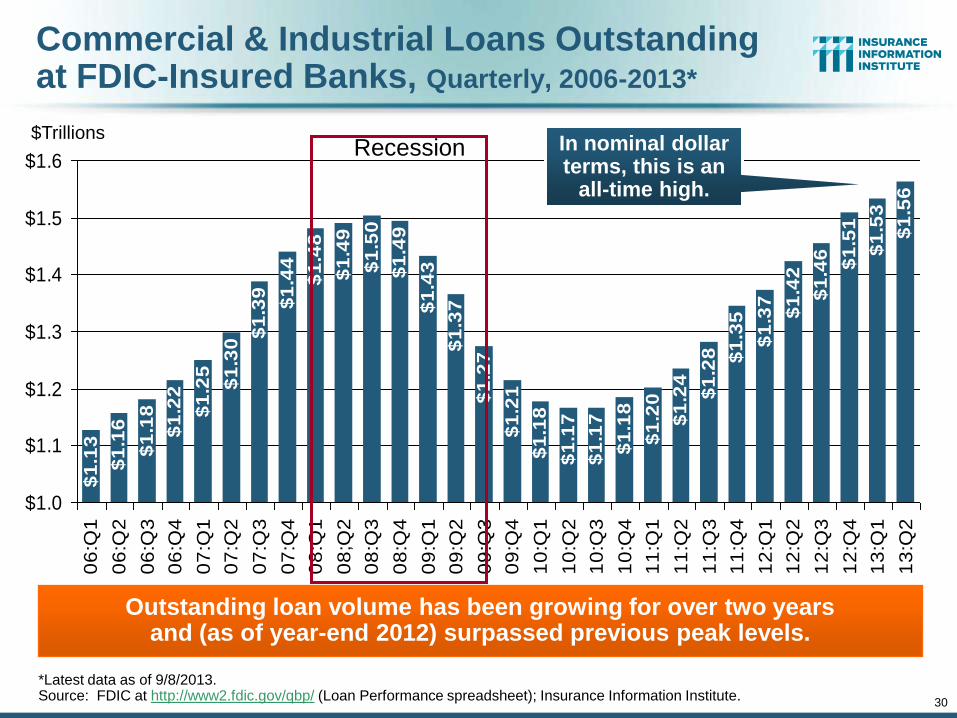

Commercial & Industrial Loans Outstanding at FDIC-Insured Banks, Quarterly, 2006-2013*

$1

.16

$1

.18

$1

.22

$1

.44

$1

.48

$1

.49

$1

.50

$1

.49

$1

.43

$1

.37

$1

.27

$1

.21

$1

.18

$1

.17

$1

.17

$1

.18

$1

.20

$1

.24

$1

.28 $1

.35

$1

.37

$1

.42

$1

.46

$1

.51

$1

.53

$1

.56

$1

.13

$1

.25

$1

.30

$1

.39

$1.0

$1.1

$1.2

$1.3

$1.4

$1.5

$1.6

06

:Q1

06

:Q2

06

:Q3

06

:Q4

07

:Q1

07

:Q2

07

:Q3

07

:Q4

08

:Q1

08

;Q2

08

:Q3

08

:Q4

09

:Q1

09

:Q2

09

:Q3

09

:Q4

10

:Q1

10

:Q2

10

:Q3

10

:Q4

11

:Q1

11

:Q2

11

:Q3

11

:Q4

12

:Q1

12

:Q2

12

:Q3

12

:Q4

13

:Q1

13

:Q2

Outstanding loan volume has been growing for over two years and (as of year-end 2012) surpassed previous peak levels.

*Latest data as of 9/8/2013. Source: FDIC at http://www2.fdic.gov/qbp/ (Loan Performance spreadsheet); Insurance Information Institute.

$Trillions In nominal dollar terms, this is an

all-time high.

Recession

31

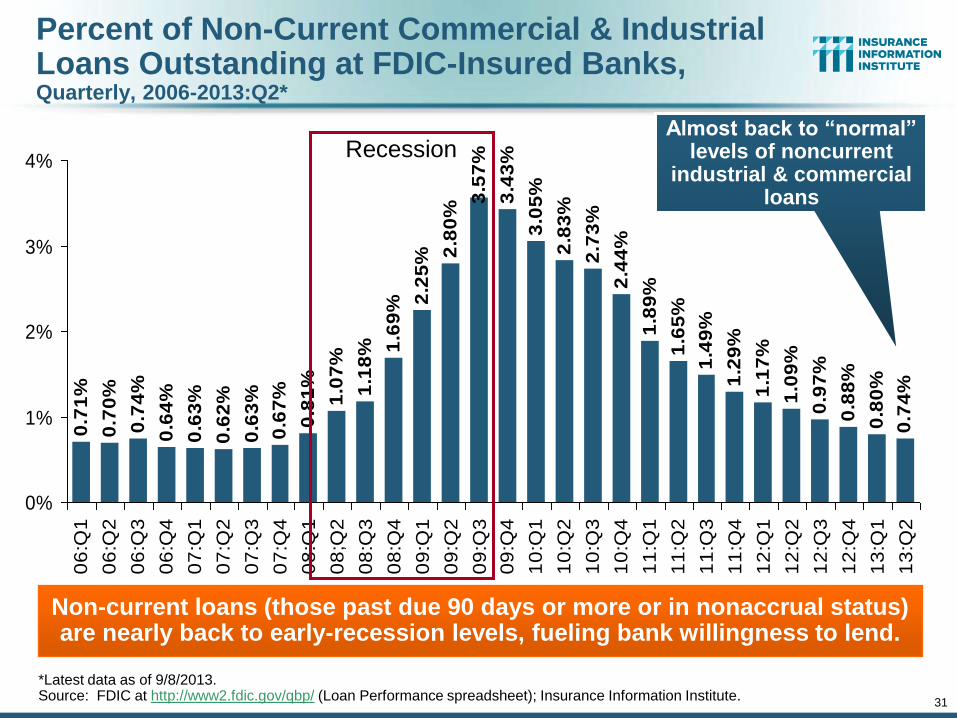

Percent of Non-Current Commercial & Industrial Loans Outstanding at FDIC-Insured Banks, Quarterly, 2006-2013:Q2*

0.7

0%

0.7

4%

0.6

4%

0.6

7%

0.8

1%

1.0

7%

1.1

8% 1

.69

% 2.2

5% 2

.80

%

3.5

7%

3.4

3%

3.0

5%

2.8

3%

2.7

3%

2.4

4%

1.8

9%

1.6

5%

1.4

9%

1.2

9%

1.1

7%

1.0

9%

0.9

7%

0.8

8%

0.8

0%

0.7

4%

0.7

1%

0.6

3%

0.6

2%

0.6

3%

0%

1%

2%

3%

4%

06

:Q1

06

:Q2

06

:Q3

06

:Q4

07

:Q1

07

:Q2

07

:Q3

07

:Q4

08

:Q1

08

;Q2

08

:Q3

08

:Q4

09

:Q1

09

:Q2

09

:Q3

09

:Q4

10

:Q1

10

:Q2

10

:Q3

10

:Q4

11

:Q1

11

:Q2

11

:Q3

11

:Q4

12

:Q1

12

:Q2

12

:Q3

12

:Q4

13

:Q1

13

:Q2

Non-current loans (those past due 90 days or more or in nonaccrual status) are nearly back to early-recession levels, fueling bank willingness to lend.

*Latest data as of 9/8/2013. Source: FDIC at http://www2.fdic.gov/qbp/ (Loan Performance spreadsheet); Insurance Information Institute.

Almost back to “normal” levels of noncurrent

industrial & commercial loans

Recession

CONSTRUCTION INDUSTRY OVERVIEW & OUTLOOK

32

The Construction Sector Is Critical to the Economy and the P/C Insurance Industry

32

33

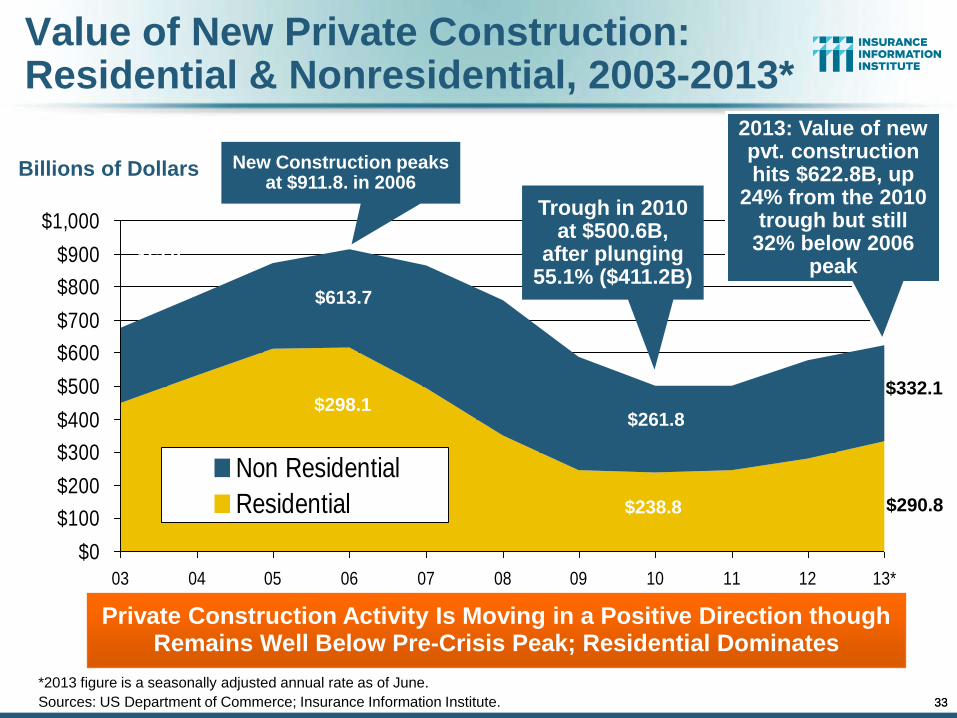

Value of New Private Construction: Residential & Nonresidential, 2003-2013*

Billions of Dollars

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

$1,000

03 04 05 06 07 08 09 10 11 12 13*

Non Residential

Residential

Private Construction Activity Is Moving in a Positive Direction though Remains Well Below Pre-Crisis Peak; Residential Dominates

$298.1

$15.0

$613.7

New Construction peaks at $911.8. in 2006

Trough in 2010 at $500.6B,

after plunging 55.1% ($411.2B)

2013: Value of new pvt. construction hits $622.8B, up

24% from the 2010 trough but still

32% below 2006 peak

33

$261.8

$238.8

$332.1

$290.8

*2013 figure is a seasonally adjusted annual rate as of June.

Sources: US Department of Commerce; Insurance Information Institute.

34

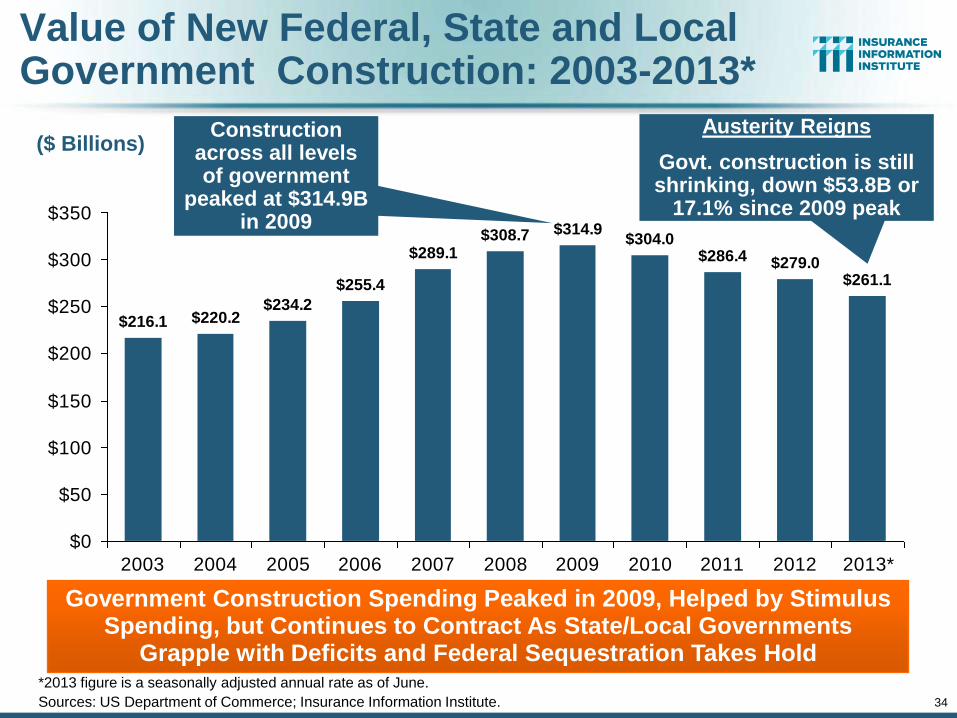

$314.9$304.0

$286.4 $279.0$261.1

$216.1 $220.2$234.2

$255.4

$289.1$308.7

$0

$50

$100

$150

$200

$250

$300

$350

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013*

($ Billions)

Government Construction Spending Peaked in 2009, Helped by Stimulus Spending, but Continues to Contract As State/Local Governments

Grapple with Deficits and Federal Sequestration Takes Hold

Value of New Federal, State and Local Government Construction: 2003-2013*

*2013 figure is a seasonally adjusted annual rate as of June.

Sources: US Department of Commerce; Insurance Information Institute.

Construction across all levels of government

peaked at $314.9B in 2009

Austerity Reigns

Govt. construction is still shrinking, down $53.8B or

17.1% since 2009 peak

35

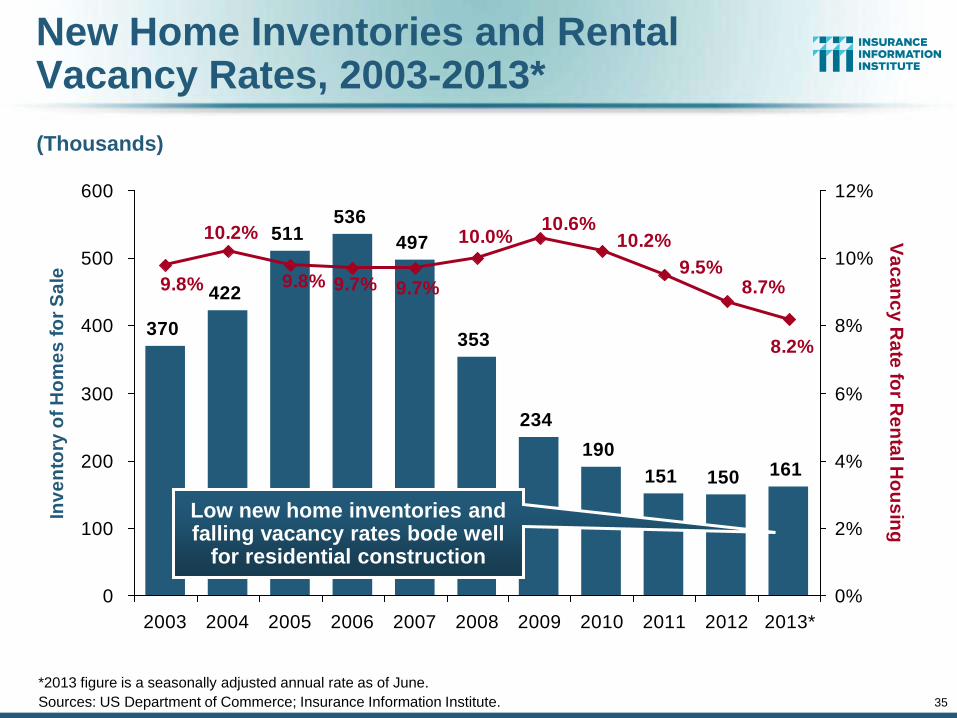

New Home Inventories and Rental Vacancy Rates, 2003-2013*

370

422

511536

497

353

234

190

151 150 161

8.2%

8.7%9.5%

10.2%10.6%

10.0%

9.7%9.7%9.8%

10.2%

9.8%

0

100

200

300

400

500

600

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013*

Inv

en

tory

of

Ho

me

s f

or

Sa

le

0%

2%

4%

6%

8%

10%

12%

Va

ca

nc

y R

ate

for R

en

tal H

ou

sin

g

(Thousands)

Low new home inventories and falling vacancy rates bode well

for residential construction

*2013 figure is a seasonally adjusted annual rate as of June.

Sources: US Department of Commerce; Insurance Information Institute.

36

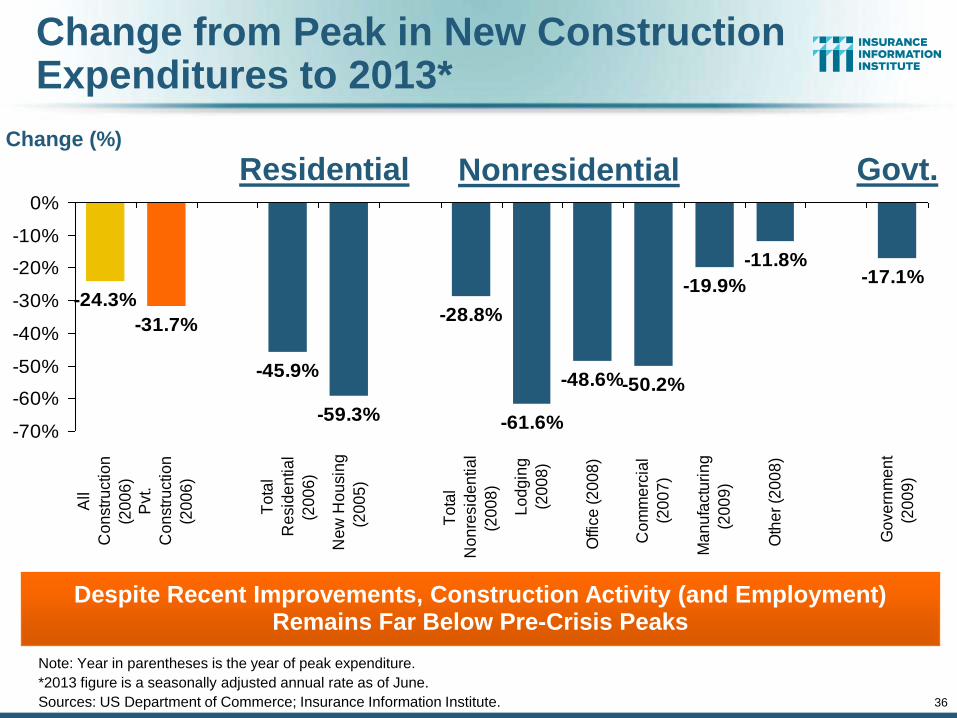

Change from Peak in New Construction Expenditures to 2013*

-28.8%

-61.6%

-48.6%-50.2%

-19.9%

-11.8%-17.1%

-24.3%

-31.7%

-45.9%

-59.3%-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

All

Co

nstr

uctio

n

(20

06

)

Pvt.

Co

nstr

uctio

n

(20

06

)

To

tal

Re

sid

en

tia

l

(20

06

)

Ne

w H

ou

sin

g

(20

05

)

To

tal

No

nre

sid

en

tia

l

(20

08

)

Lo

dg

ing

(20

08

)

Offic

e (

20

08

)

Co

mm

erc

ial

(20

07

)

Ma

nu

factu

rin

g

(20

09

)

Oth

er

(20

08

)

Go

ve

rnm

en

t

(20

09

)

Despite Recent Improvements, Construction Activity (and Employment) Remains Far Below Pre-Crisis Peaks

Change (%)

Note: Year in parentheses is the year of peak expenditure.

*2013 figure is a seasonally adjusted annual rate as of June.

Sources: US Department of Commerce; Insurance Information Institute.

Residential Nonresidential Govt.

37

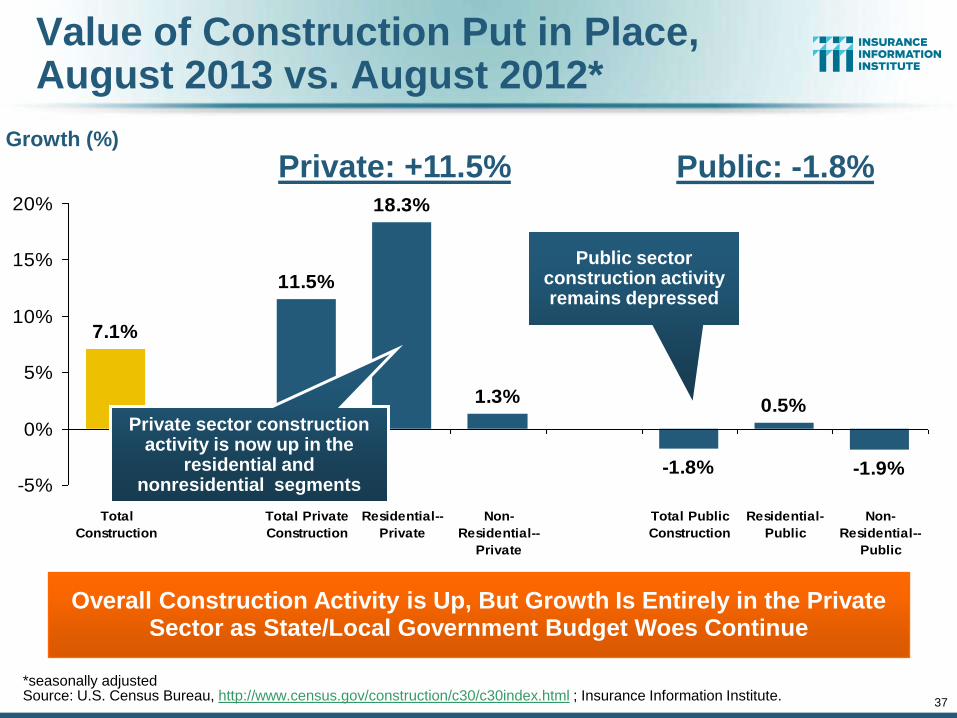

Value of Construction Put in Place, August 2013 vs. August 2012*

-1.8%

0.5%

-1.9%

7.1%

11.5%

18.3%

1.3%

-5%

0%

5%

10%

15%

20%

Total

Construction

Total Private

Construction

Residential--

Private

Non-

Residential--

Private

Total Public

Construction

Residential-

Public

Non-

Residential--

Public

Overall Construction Activity is Up, But Growth Is Entirely in the Private Sector as State/Local Government Budget Woes Continue

Growth (%)

Private sector construction activity is now up in the

residential and nonresidential segments

*seasonally adjusted Source: U.S. Census Bureau, http://www.census.gov/construction/c30/c30index.html ; Insurance Information Institute.

Private: +11.5% Public: -1.8%

Public sector construction activity remains depressed

38

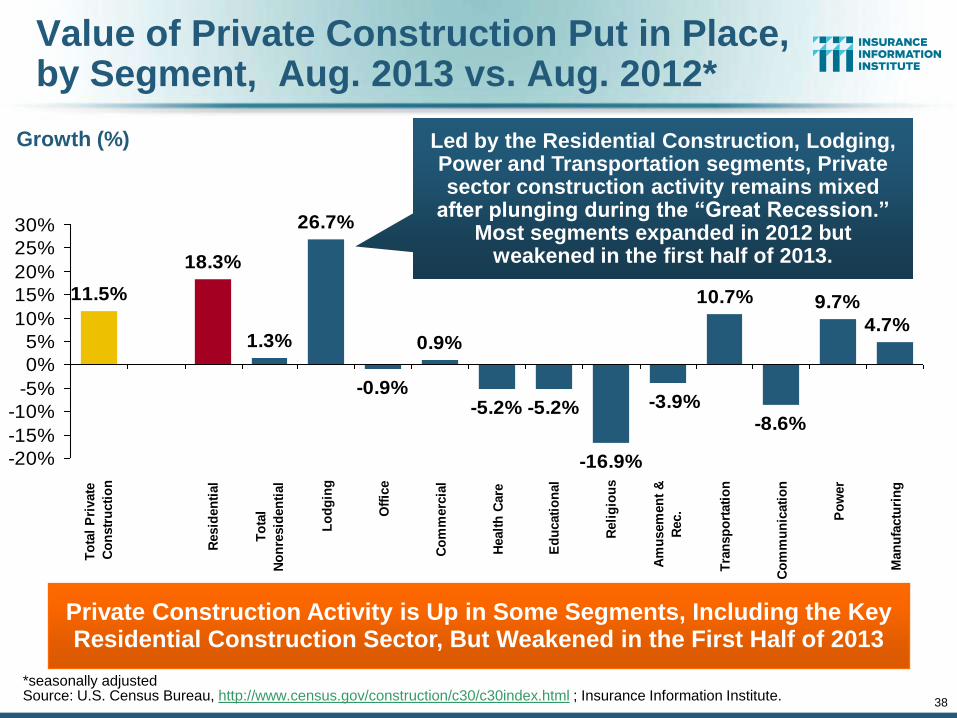

Value of Private Construction Put in Place, by Segment, Aug. 2013 vs. Aug. 2012*

0.9%

-5.2% -5.2%

-16.9%

10.7%

-8.6%

9.7%

4.7%

-3.9%

11.5%

18.3%

1.3%

26.7%

-0.9%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

To

tal

Pri

vate

Co

nstr

ucti

on

Resid

en

tial

To

tal

No

nre

sid

en

tial

Lo

dg

ing

Off

ice

Co

mm

erc

ial

Healt

h C

are

Ed

ucati

on

al

Reli

gio

us

Am

usem

en

t &

Rec.

Tra

nsp

ort

ati

on

Co

mm

un

icati

on

Po

wer

Man

ufa

ctu

rin

g

Private Construction Activity is Up in Some Segments, Including the Key Residential Construction Sector, But Weakened in the First Half of 2013

Growth (%) Led by the Residential Construction, Lodging, Power and Transportation segments, Private sector construction activity remains mixed

after plunging during the “Great Recession.” Most segments expanded in 2012 but

weakened in the first half of 2013.

*seasonally adjusted Source: U.S. Census Bureau, http://www.census.gov/construction/c30/c30index.html ; Insurance Information Institute.

39

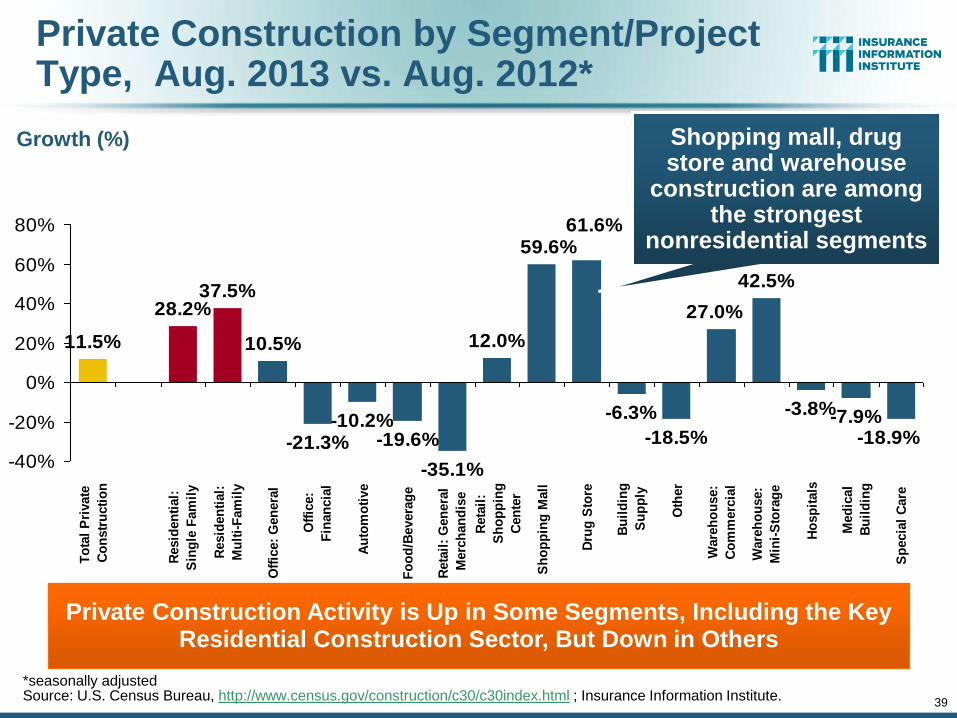

Private Construction by Segment/Project Type, Aug. 2013 vs. Aug. 2012*

-10.2%-19.6%

-35.1%

12.0%

-6.3%

-18.5%

42.5%

-3.8%-7.9%-18.9%

61.6%

27.0%

59.6%

11.5%

28.2%37.5%

10.5%

-21.3%-40%

-20%

0%

20%

40%

60%

80%

To

tal

Pri

vate

Co

nstr

ucti

on

Resid

en

tial:

Sin

gle

Fam

ily

Resid

en

tial:

Mu

lti-

Fam

ily

Off

ice:

Gen

era

l

Off

ice:

Fin

an

cia

l

Au

tom

oti

ve

Fo

od

/Bevera

ge

Reta

il:

Gen

era

l

Merc

han

dis

e

Reta

il:

Sh

op

pin

g

Cen

ter

Sh

op

pin

g M

all

Dru

g S

tore

Bu

ild

ing

Su

pp

ly

Oth

er

Ware

ho

use:

Co

mm

erc

ial

Ware

ho

use:

Min

i-S

tora

ge

Ho

sp

itals

Med

ical

Bu

ild

ing

Sp

ecia

l C

are

Private Construction Activity is Up in Some Segments, Including the Key Residential Construction Sector, But Down in Others

Growth (%) Shopping mall, drug store and warehouse

construction are among the strongest

nonresidential segments

*seasonally adjusted Source: U.S. Census Bureau, http://www.census.gov/construction/c30/c30index.html ; Insurance Information Institute.

40

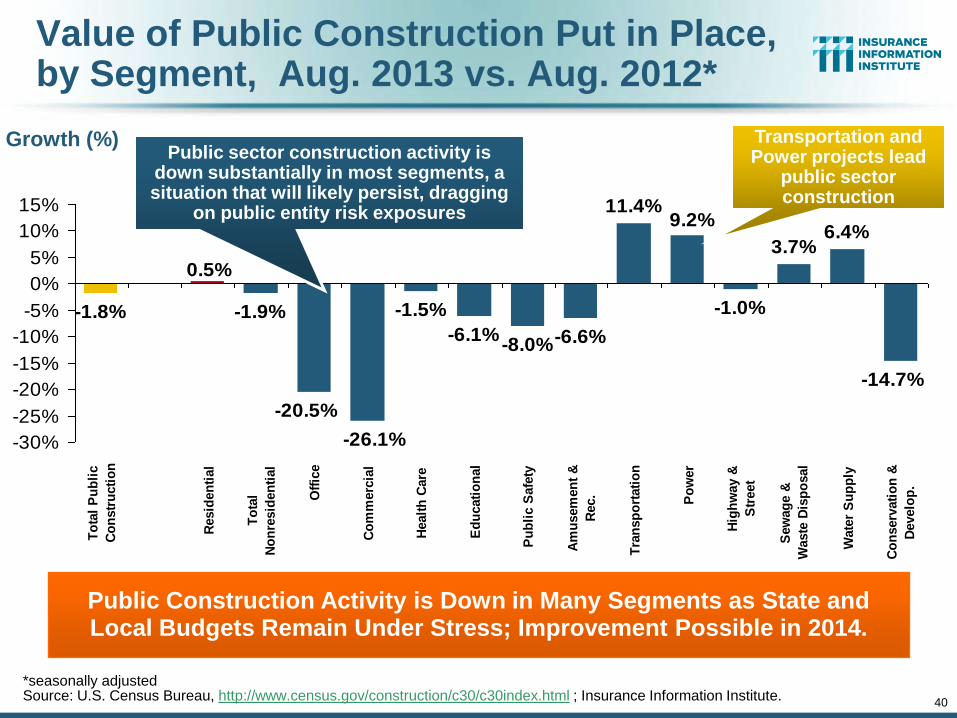

Value of Public Construction Put in Place, by Segment, Aug. 2013 vs. Aug. 2012*

-1.5%

-6.1%-8.0%-6.6%

11.4%

-1.0%

3.7%6.4%

-14.7%

9.2%

-1.8%

0.5%

-1.9%

-20.5%

-26.1%-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

To

tal

Pu

bli

c

Co

nstr

ucti

on

Resid

en

tial

To

tal

No

nre

sid

en

tial

Off

ice

Co

mm

erc

ial

Healt

h C

are

Ed

ucati

on

al

Pu

bli

c S

afe

ty

Am

usem

en

t &

Rec.

Tra

nsp

ort

ati

on

Po

wer

Hig

hw

ay &

Str

eet

Sew

ag

e &

Waste

Dis

po

sal

Wate

r S

up

ply

Co

nserv

ati

on

&

Develo

p.

Public Construction Activity is Down in Many Segments as State and Local Budgets Remain Under Stress; Improvement Possible in 2014.

Growth (%)

*seasonally adjusted Source: U.S. Census Bureau, http://www.census.gov/construction/c30/c30index.html ; Insurance Information Institute.

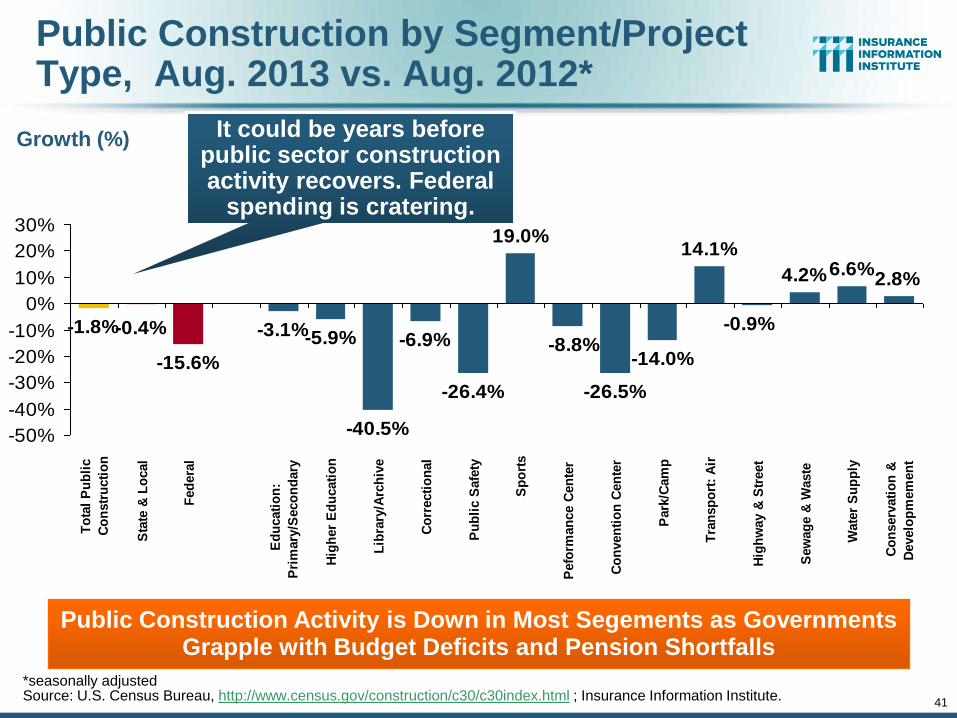

Public sector construction activity is down substantially in most segments, a situation that will likely persist, dragging

on public entity risk exposures

Transportation and Power projects lead

public sector construction

41

Public Construction by Segment/Project Type, Aug. 2013 vs. Aug. 2012*

-40.5%

-6.9%

-26.4%

19.0%

-26.5%

-14.0%

14.1%

4.2%6.6%2.8%

-5.9%-3.1%

-15.6%

-0.4%-1.8%-8.8%

-0.9%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

To

tal

Pu

bli

c

Co

nstr

ucti

on

Sta

te &

Lo

cal

Fed

era

l

Ed

ucati

on

:

Pri

mary

/Seco

nd

ary

Hig

her

Ed

ucati

on

Lib

rary

/Arc

hiv

e

Co

rrecti

on

al

Pu

bli

c S

afe

ty

Sp

ort

s

Pefo

rman

ce C

en

ter

Co

nven

tio

n C

en

ter

Park

/Cam

p

Tra

nsp

ort

: A

ir

Hig

hw

ay &

Str

eet

Sew

ag

e &

Waste

Wate

r S

up

ply

Co

nserv

ati

on

&

Develo

pm

em

en

t

Public Construction Activity is Down in Most Segements as Governments Grapple with Budget Deficits and Pension Shortfalls

Growth (%) It could be years before public sector construction activity recovers. Federal

spending is cratering.

*seasonally adjusted Source: U.S. Census Bureau, http://www.census.gov/construction/c30/c30index.html ; Insurance Information Institute.

42

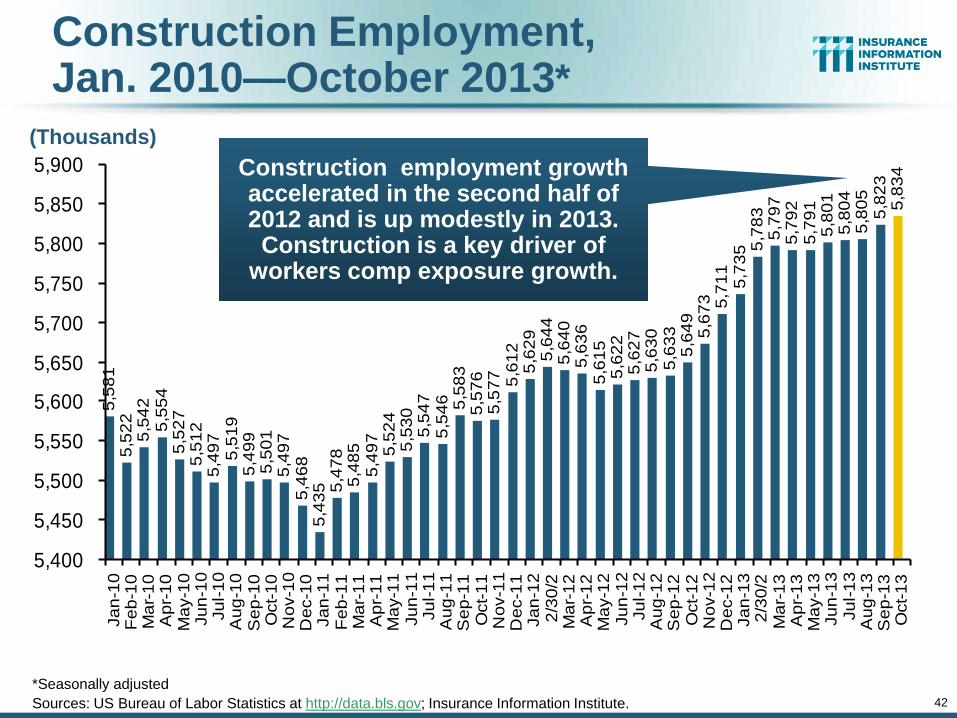

Construction Employment, Jan. 2010—October 2013*

*Seasonally adjusted

Sources: US Bureau of Labor Statistics at http://data.bls.gov; Insurance Information Institute.

5,5

81

5,5

22

5,5

42

5,5

54

5,5

27

5,5

12

5,4

97

5,5

19

5,4

99

5,5

01

5,4

97

5,4

68

5,4

35 5

,47

85

,48

55

,49

75

,52

45

,53

05

,54

75

,54

6 5,5

83

5,5

76

5,5

77 5,6

12

5,6

29

5,6

44

5,6

40

5,6

36

5,6

15

5,6

22

5,6

27

5,6

30

5,6

33

5,6

49

5,6

73 5,7

11

5,7

35 5

,78

35

,79

75

,79

25

,79

15

,80

15

,80

45

,80

55

,82

35

,83

4

5,400

5,450

5,500

5,550

5,600

5,650

5,700

5,750

5,800

5,850

5,900

Ja

n-1

0F

eb

-10

Ma

r-1

0A

pr-

10

Ma

y-1

0Ju

n-1

0Ju

l-1

0A

ug

-10

Se

p-1

0O

ct-

10

No

v-1

0D

ec-1

0Ja

n-1

1F

eb

-11

Ma

r-1

1A

pr-

11

Ma

y-1

1Ju

n-1

1Ju

l-1

1A

ug

-11

Se

p-1

1O

ct-

11

No

v-1

1D

ec-1

1Ja

n-1

22

/30

/2M

ar-

12

Ap

r-1

2M

ay-1

2Ju

n-1

2Ju

l-1

2A

ug

-12

Se

p-1

2O

ct-

12

No

v-1

2D

ec-1

2Ja

n-1

32

/30

/2M

ar-

13

Ap

r-1

3M

ay-1

3Ju

n-1

3Ju

l-1

3A

ug

-13

Se

p-1

3O

ct-

13

Construction employment growth accelerated in the second half of 2012 and is up modestly in 2013. Construction is a key driver of

workers comp exposure growth.

(Thousands)

43

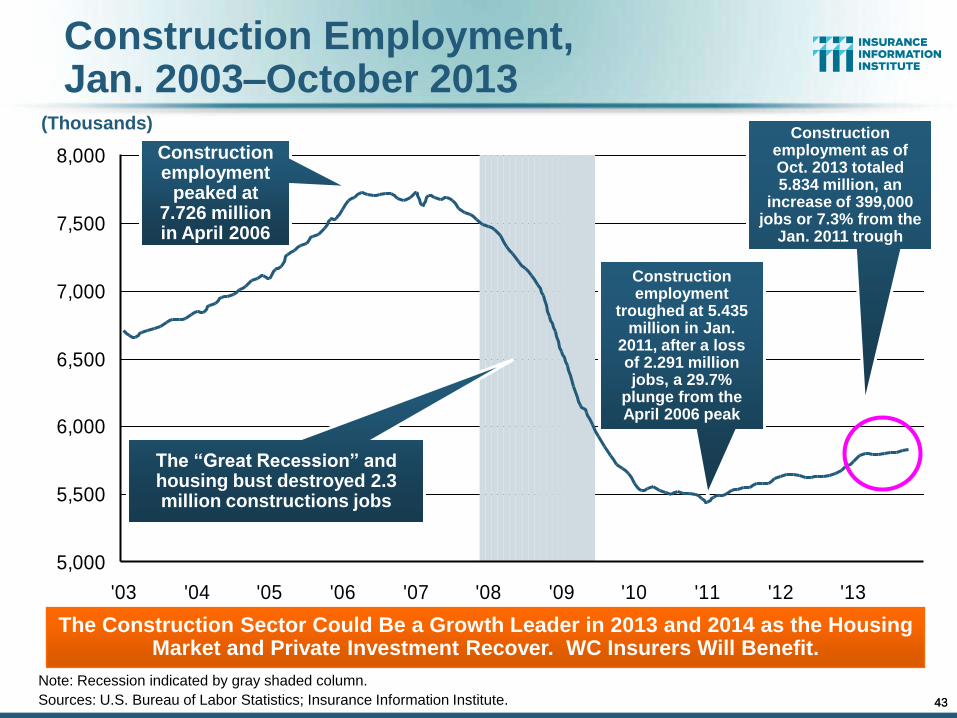

Construction Employment, Jan. 2003–October 2013

Note: Recession indicated by gray shaded column.

Sources: U.S. Bureau of Labor Statistics; Insurance Information Institute.

5,000

5,500

6,000

6,500

7,000

7,500

8,000

'03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13

The “Great Recession” and housing bust destroyed 2.3 million constructions jobs

The Construction Sector Could Be a Growth Leader in 2013 and 2014 as the Housing Market and Private Investment Recover. WC Insurers Will Benefit.

Construction employment

troughed at 5.435 million in Jan.

2011, after a loss of 2.291 million jobs, a 29.7%

plunge from the April 2006 peak

43

Construction employment

peaked at 7.726 million in April 2006

(Thousands) Construction

employment as of Oct. 2013 totaled 5.834 million, an

increase of 399,000 jobs or 7.3% from the

Jan. 2011 trough

44

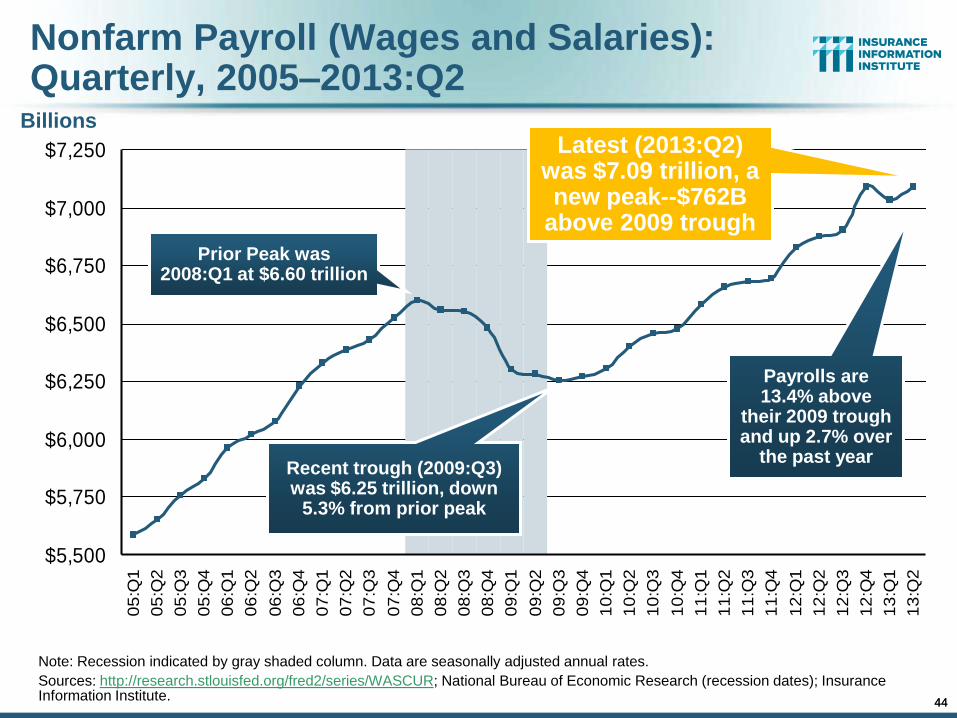

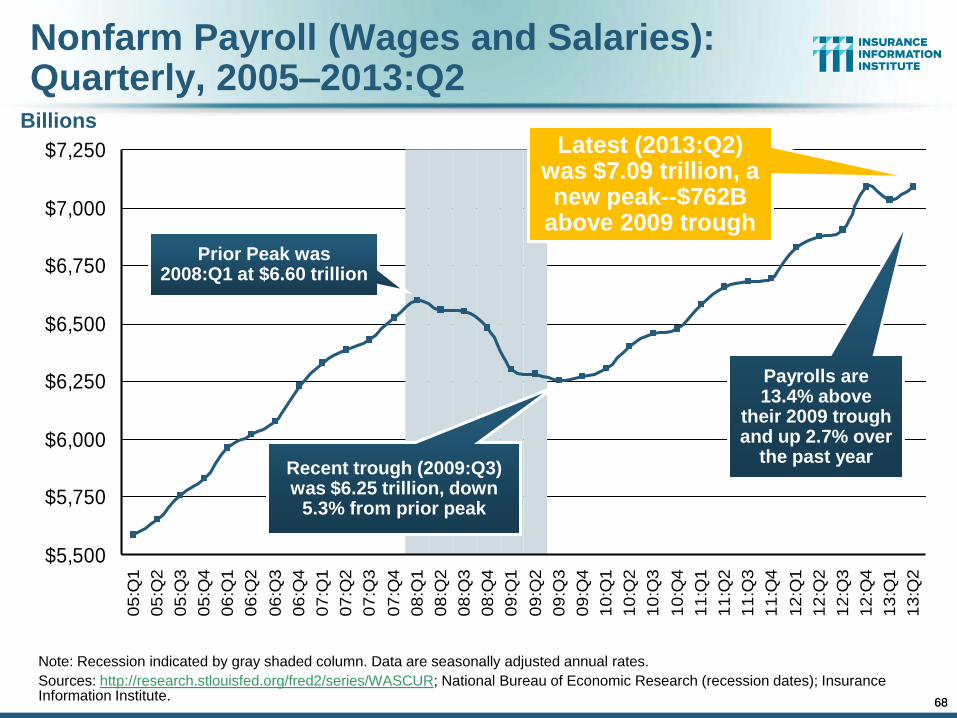

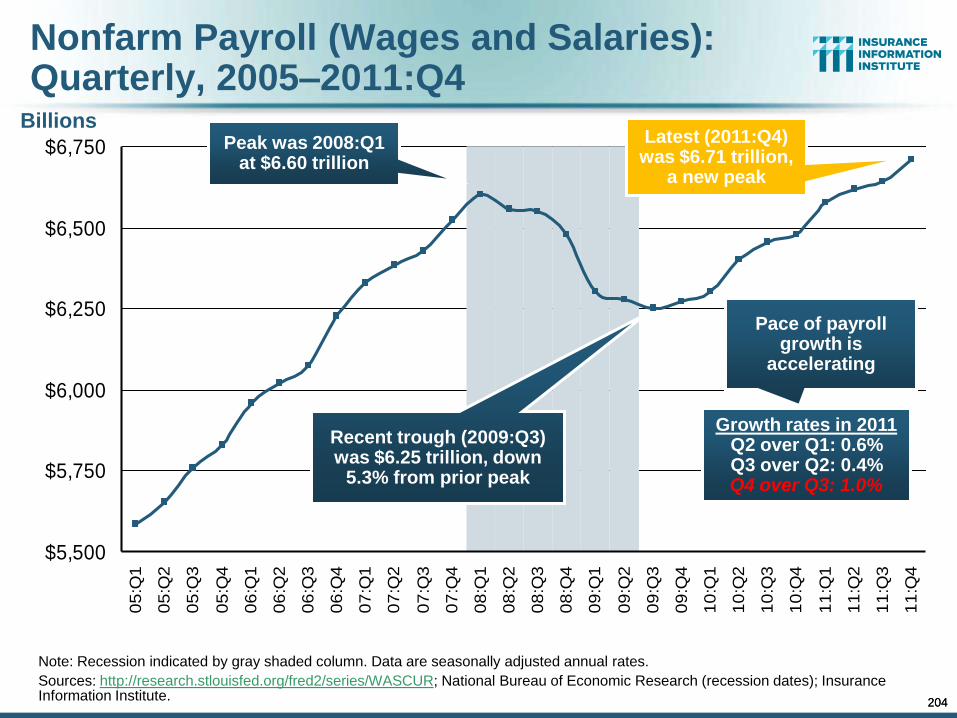

Nonfarm Payroll (Wages and Salaries): Quarterly, 2005–2013:Q2

Note: Recession indicated by gray shaded column. Data are seasonally adjusted annual rates.

Sources: http://research.stlouisfed.org/fred2/series/WASCUR; National Bureau of Economic Research (recession dates); Insurance Information Institute.

Billions

$5,500

$5,750

$6,000

$6,250

$6,500

$6,750

$7,000

$7,2500

5:Q

1

05

:Q2

05

:Q3

05

:Q4

06

:Q1

06

:Q2

06

:Q3

06

:Q4

07

:Q1

07

:Q2

07

:Q3

07

:Q4

08

:Q1

08

:Q2

08

:Q3

08

:Q4

09

:Q1

09

:Q2

09

:Q3

09

:Q4

10

:Q1

10

:Q2

10

:Q3

10

:Q4

11

:Q1

11

:Q2

11

:Q3

11

:Q4

12

:Q1

12

:Q2

12

:Q3

12

:Q4

13

:Q1

13

:Q2

Prior Peak was 2008:Q1 at $6.60 trillion

Latest (2013:Q2) was $7.09 trillion, a new peak--$762B

above 2009 trough

Recent trough (2009:Q3) was $6.25 trillion, down

5.3% from prior peak

Payrolls are 13.4% above

their 2009 trough and up 2.7% over

the past year

44

58

.35

7.1

60

.45

9.6

57

.85

5.3

55

.15

5.2

55

.3 56

.9 58

.25

8.5 6

0.8

61

.45

9.7

59

.75

4.2 5

5.8

51

.4 52

.55

2.5

51

.85

2.2 53

.1 54

.15

1.9 53

.35

4.1

52

.55

0.2

50

.55

0.7

51

.65

1.7

49

.95

0.2

53

.1 54

.2

50

.74

9.0 5

0.9

55

.45

5.7

56

.25

6.4

51

.3

40

45

50

55

60

65

Ja

n-1

0F

eb

-10

Ma

r-1

0A

pr-

10

Ma

y-1

0

Ju

n-1

0Ju

l-1

0A

ug

-10

Se

p-1

0

Oct-

10

No

v-1

0D

ec-1

0

Ja

n-1

1F

eb

-11

Ma

r-1

1A

pr-

11

Ma

y-1

1Ju

n-1

1Ju

l-1

1

Au

g-1

1S

ep

-11

Oct-

11

No

v-1

1

De

c-1

1Ja

n-1

2F

eb

-12

Ma

r-1

2

Ap

r-1

2M

ay-1

2Ju

n-1

2

Ju

l-1

2A

ug

-12

Se

p-1

2O

ct-

12

No

v-1

2D

ec-1

2Ja

n-1

3

Fe

b-1

3M

ar-

13

Ap

r-1

3M

ay-1

3

Ju

n-1

3Ju

l-1

3A

ug

-13

Se

p-1

3O

ct-

13

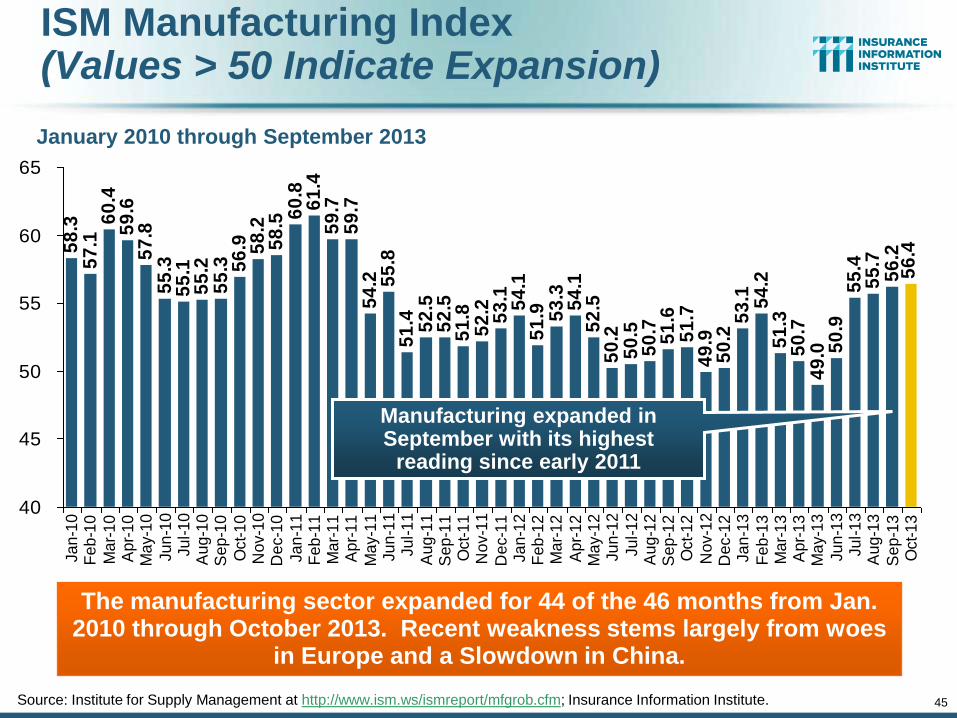

ISM Manufacturing Index (Values > 50 Indicate Expansion)

January 2010 through September 2013

The manufacturing sector expanded for 44 of the 46 months from Jan. 2010 through October 2013. Recent weakness stems largely from woes

in Europe and a Slowdown in China.

Source: Institute for Supply Management at http://www.ism.ws/ismreport/mfgrob.cfm; Insurance Information Institute.

Manufacturing expanded in September with its highest

reading since early 2011

45

46

$200,000

$300,000

$400,000

$500,000

Jan-

92

Jan-

93

Jan-

94

Jan-

95

Jan-

96

Jan-

97

Jan-

98

Jan-

99

Jan-

00

Jan 01

Jan 02

Jan 03

Jan 04

Jan 05

Jan 06

Jan 07

Jan 08

Jan 09

Jan 10

Jan 11

Jan 12

Jan 13

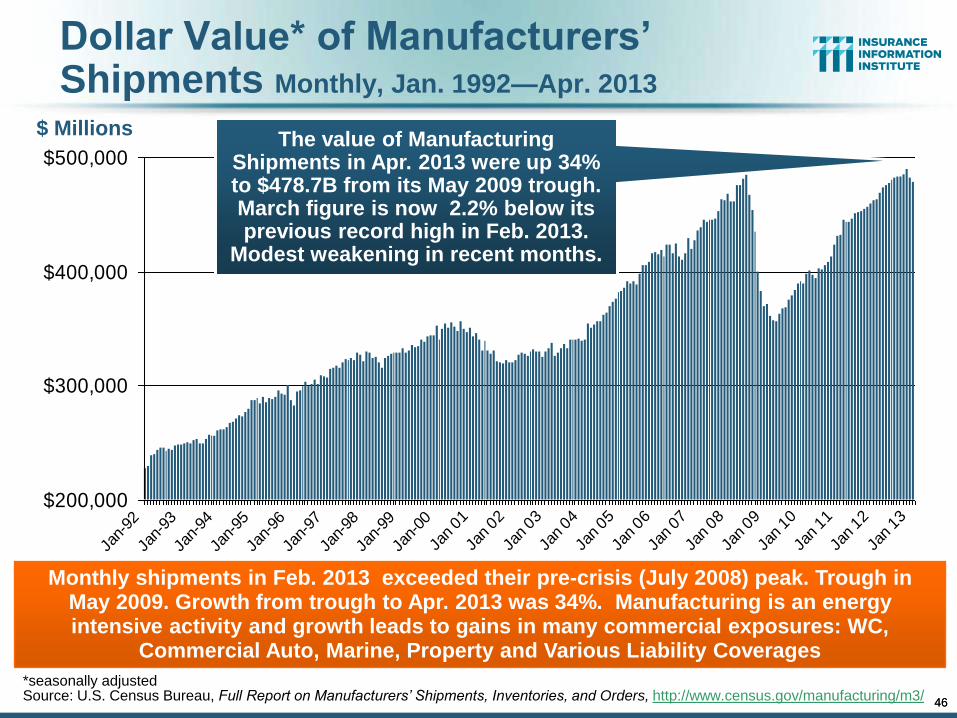

Dollar Value* of Manufacturers’ Shipments Monthly, Jan. 1992—Apr. 2013

*seasonally adjusted Source: U.S. Census Bureau, Full Report on Manufacturers’ Shipments, Inventories, and Orders, http://www.census.gov/manufacturing/m3/

Monthly shipments in Feb. 2013 exceeded their pre-crisis (July 2008) peak. Trough in May 2009. Growth from trough to Apr. 2013 was 34%. Manufacturing is an energy intensive activity and growth leads to gains in many commercial exposures: WC,

Commercial Auto, Marine, Property and Various Liability Coverages

The value of Manufacturing Shipments in Apr. 2013 were up 34% to $478.7B from its May 2009 trough. March figure is now 2.2% below its previous record high in Feb. 2013.

Modest weakening in recent months.

$ Millions

46

47

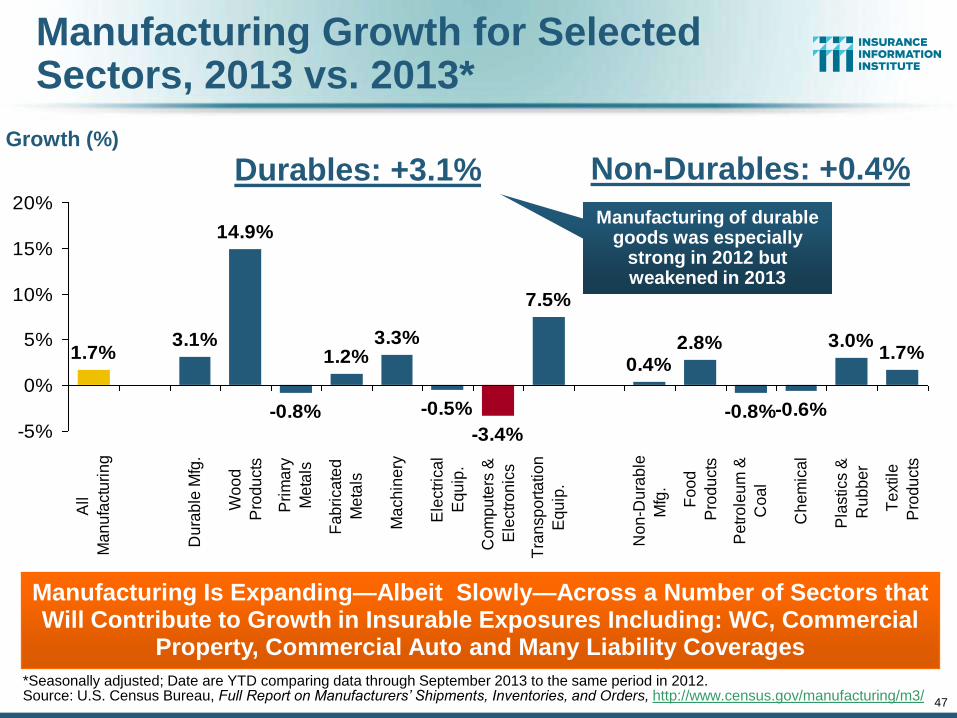

Manufacturing Growth for Selected Sectors, 2013 vs. 2013*

3.3%

-0.5%

-3.4%

7.5%

0.4%2.8%

-0.8%-0.6%

3.0%1.7%1.7%

3.1%

14.9%

-0.8%

1.2%

-5%

0%

5%

10%

15%

20%

All

Ma

nu

factu

rin

g

Du

rab

le M

fg.

Wo

od

Pro

du

cts

Pri

ma

ry

Me

tals

Fa

bri

ca

ted

Me

tals

Ma

ch

ine

ry

Ele

ctr

ica

l

Eq

uip

.

Co

mp

ute

rs &

Ele

ctr

on

ics

Tra

nsp

ort

atio

n

Eq

uip

.

No

n-D

ura

ble

Mfg

.

Fo

od

Pro

du

cts

Pe

tro

leu

m &

Co

al

Ch

em

ica

l

Pla

stics &

Ru

bb

er

Te

xtile

Pro

du

cts

Manufacturing Is Expanding—Albeit Slowly—Across a Number of Sectors that Will Contribute to Growth in Insurable Exposures Including: WC, Commercial

Property, Commercial Auto and Many Liability Coverages

Growth (%)

Manufacturing of durable goods was especially

strong in 2012 but weakened in 2013

*Seasonally adjusted; Date are YTD comparing data through September 2013 to the same period in 2012. Source: U.S. Census Bureau, Full Report on Manufacturers’ Shipments, Inventories, and Orders, http://www.census.gov/manufacturing/m3/

Durables: +3.1% Non-Durables: +0.4%

66%

68%

70%

72%

74%

76%

78%

80%

82%

Mar

01

Jun 0

1

Sep

Dec

Mar

02

Jun 0

2

Sep

Dec

Mar

03

Jun 0

3

Sep

Dec

Mar

04

Jun 0

4

Sep

Dec

Mar

05

Jun 0

5

Sep

Dec

Mar

06

Jun 0

6

Sep

Dec

Mar

07

Jun 0

7

Sep

Dec

Mar

08

Jun 0

8

Sep

Dec

Mar

09

Jun 0

9

Sep

Dec

Mar

10

Jun 1

0

Sep

Dec

Mar

11

Jun 1

1

Sep

Dec

Mar

12

Jun 1

2

Sep

Dec

Mar

13

Jun 1

3

Sep

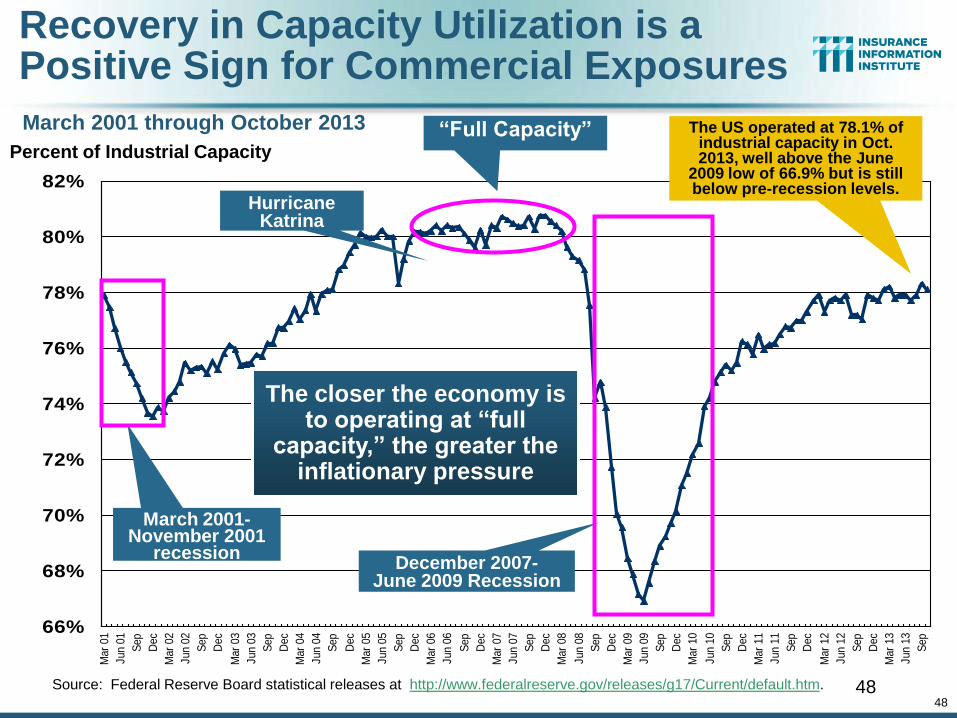

Recovery in Capacity Utilization is a Positive Sign for Commercial Exposures

Source: Federal Reserve Board statistical releases at http://www.federalreserve.gov/releases/g17/Current/default.htm. 48

Percent of Industrial Capacity

Hurricane Katrina

March 2001-November 2001

recession

“Full Capacity”

The closer the economy is to operating at “full

capacity,” the greater the inflationary pressure

The US operated at 78.1% of industrial capacity in Oct. 2013, well above the June

2009 low of 66.9% but is still below pre-recession levels.

December 2007- June 2009 Recession

March 2001 through October 2013

48

49

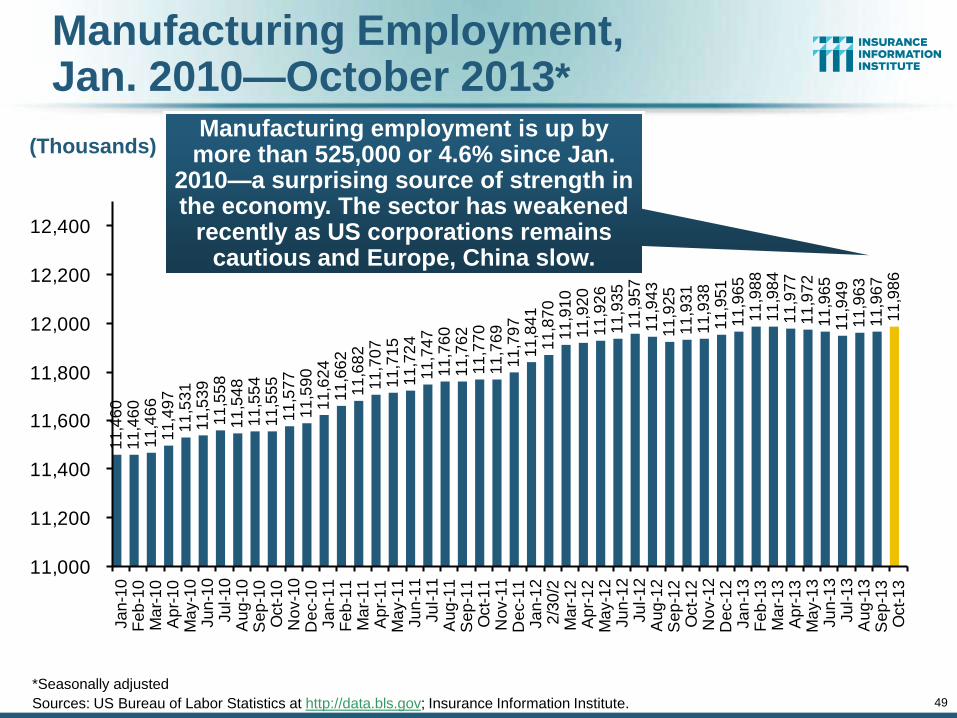

Manufacturing Employment, Jan. 2010—October 2013*

11

,46

01

1,4

60

11

,46

61

1,4

97

11

,53

11

1,5

39

11

,55

81

1,5

48

11

,55

41

1,5

55

11

,57

71

1,5

90

11

,62

41

1,6

62

11

,68

21

1,7

07

11

,71

51

1,7

24

11

,74

71

1,7

60

11

,76

21

1,7

70

11

,76

91

1,7

97

11

,84

11

1,8

70

11

,91

01

1,9

20

11

,92

61

1,9

35

11

,95

71

1,9

43

11

,92

51

1,9

31

11

,93

81

1,9

51

11

,96

51

1,9

88

11

,98

41

1,9

77

11

,97

21

1,9

65

11

,94

91

1,9

63

11

,96

71

1,9

86

11,000

11,200

11,400

11,600

11,800

12,000

12,200

12,400

Ja

n-1

0F

eb

-10

Ma

r-1

0A

pr-

10

Ma

y-1

0Ju

n-1

0Ju

l-1

0A

ug

-10

Se

p-1

0O

ct-

10

No

v-1

0D

ec-1

0Ja

n-1

1F

eb

-11

Ma

r-1

1A

pr-

11

Ma

y-1

1Ju

n-1

1Ju

l-1

1A

ug

-11

Se

p-1

1O

ct-

11

No

v-1

1D

ec-1

1Ja

n-1

22

/30

/2M

ar-

12

Ap

r-1

2M

ay-1

2Ju

n-1

2Ju

l-1

2A

ug

-12

Se

p-1

2O

ct-

12

No

v-1

2D

ec-1

2Ja

n-1

3F

eb

-13

Ma

r-1

3A

pr-

13

Ma

y-1

3Ju

n-1

3Ju

l-1

3A

ug

-13

Se

p-1

3O

ct-

13

Manufacturing employment is up by more than 525,000 or 4.6% since Jan.

2010—a surprising source of strength in the economy. The sector has weakened

recently as US corporations remains cautious and Europe, China slow.

*Seasonally adjusted

Sources: US Bureau of Labor Statistics at http://data.bls.gov; Insurance Information Institute.

(Thousands)

50

.7 52

.7 54

.15

4.6

54

.85

3.5

53

.75

2.8 53

.95

4.6 56 5

7.1 5

9.4

59

.75

6.3

54

.45

3.3

53

.45

3.8

52

.65

2.6

52

.65

2.6

53

.05

6.8

56

.15

5.0

53

.75

4.1

52

.75

2.9 54

.3 55

.25

4.8

54

.85

5.7

55

.25

6.0

53

.15

3.7

52

.25

6.0

58

.65

4.4 55

.5

54

.4

40

45

50

55

60

65

Ja

n-1

0F

eb

-10

Ma

r-1

0A

pr-

10

Ma

y-1

0

Ju

n-1

0Ju

l-1

0A

ug

-10

Se

p-1

0

Oct-

10

No

v-1

0D

ec-1

0

Ja

n-1

1F

eb

-11

Ma

r-1

1A

pr-

11

Ma

y-1

1Ju

n-1

1Ju

l-1

1

Au

g-1

1S

ep

-11

Oct-

11

No

v-1

1

De

c-1

1Ja

n-1

2F

eb

-12

Ma

r-1

2

Ap

r-1

2M

ay-1

2Ju

n-1

2

Ju

l-1

2A

ug

-12

Se

p-1

2O

ct-

12

No

v-1

2D

ec-1

2Ja

n-1

3

Fe

b-1

3M

ar-

13

Ap

r-1

3M

ay-1

3

Ju

n-1

3Ju

l-1

3A

ug

-13

Se

p-1

3O

ct-

13

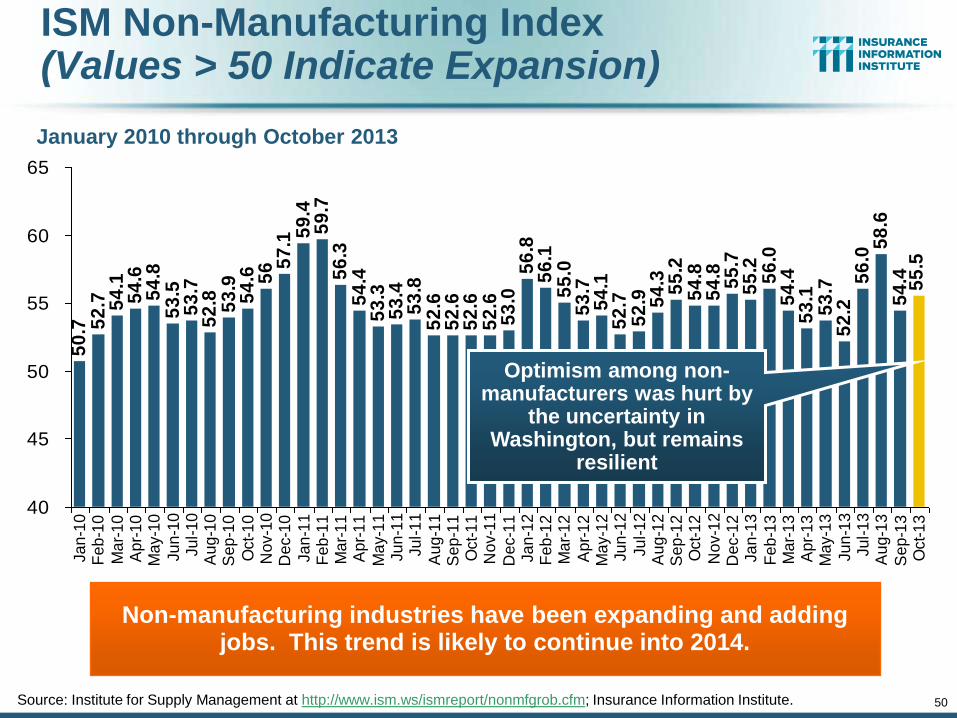

ISM Non-Manufacturing Index (Values > 50 Indicate Expansion)

January 2010 through October 2013

Non-manufacturing industries have been expanding and adding jobs. This trend is likely to continue into 2014.

Source: Institute for Supply Management at http://www.ism.ws/ismreport/nonmfgrob.cfm; Insurance Information Institute.

Optimism among non-manufacturers was hurt by

the uncertainty in Washington, but remains

resilient

50

51

43

,69

4

48

,12

5

69

,30

0

62

,43

6

64

,00

4

71

,27

7

81

,23

5

82

,44

6

63

,85

3

63

,23

5

64

,85

3

71

,54

9

70

,64

3

62

,30

4

52

,37

4

51

,95

9

53

,54

9

54

,02

7

44

,36

7

37

,88

4

35

,47

2

40

,09

9

38

,54

0

35

,03

7

34

,31

7

39

,20

1

19

,69

5

28

,32

2

43

,54

6

60

,83

7

56

,28

2

47

,80

6

40

,07

5

34

,89

2

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

00

01

02

03

04

05

06

07

08

09

10

11

12

13

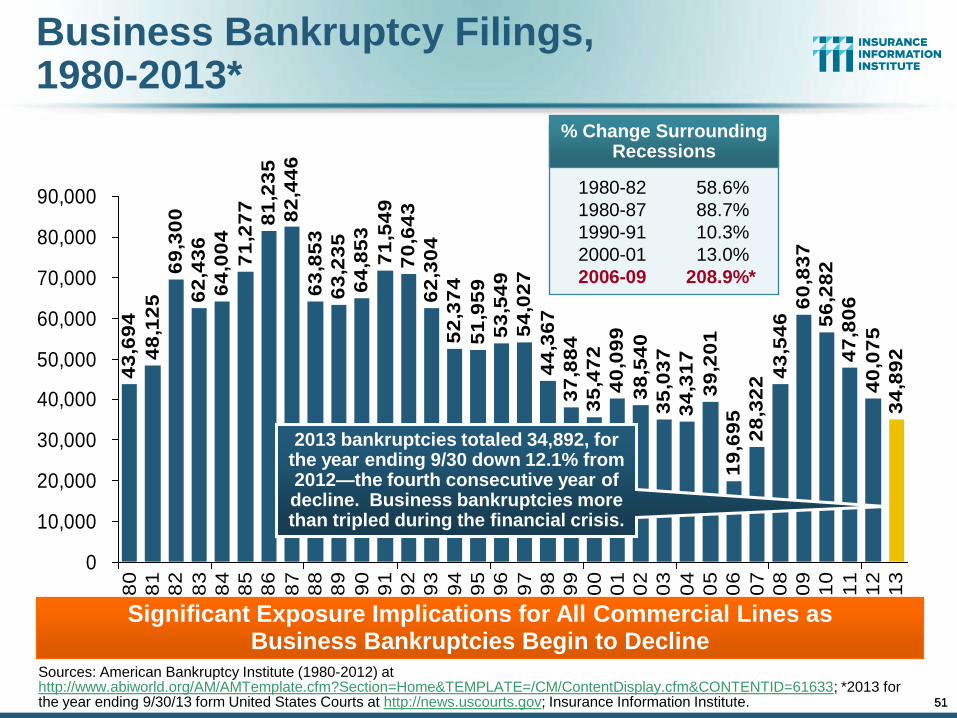

Business Bankruptcy Filings, 1980-2013*

Sources: American Bankruptcy Institute (1980-2012) at http://www.abiworld.org/AM/AMTemplate.cfm?Section=Home&TEMPLATE=/CM/ContentDisplay.cfm&CONTENTID=61633; *2013 for the year ending 9/30/13 form United States Courts at http://news.uscourts.gov; Insurance Information Institute.

Significant Exposure Implications for All Commercial Lines as Business Bankruptcies Begin to Decline

2013 bankruptcies totaled 34,892, for the year ending 9/30 down 12.1% from 2012—the fourth consecutive year of decline. Business bankruptcies more than tripled during the financial crisis.

% Change Surrounding Recessions

1980-82 58.6%

1980-87 88.7%

1990-91 10.3%

2000-01 13.0%

2006-09 208.9%*

51

52

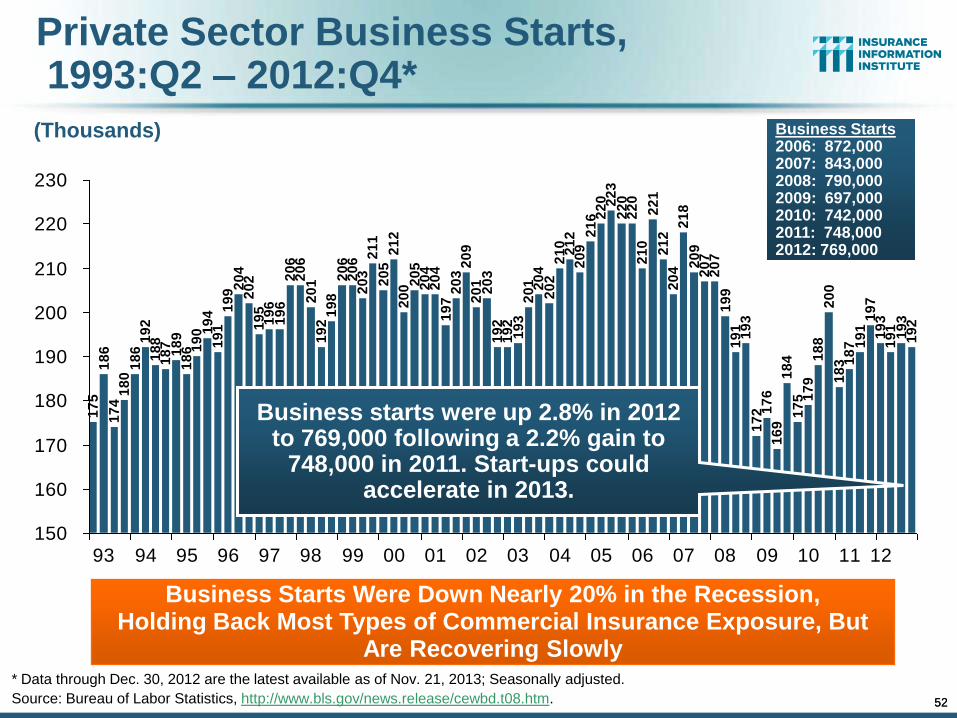

Private Sector Business Starts, 1993:Q2 – 2012:Q4*

17

51

86

17

41

80

18

61

92

18

81

87

18

91

86 1

90 1

94

19

11

99 2

04

20

21

95

19

61

96

20

62

06

20

11

92

19

82

06

20

62

03

21

12

05

21

22

00 2

05

20

42

04

19

72

03

20

92

01

19

21

92

19

32

01 20

42

02

21

02

12

20

92

16 2

20 22

32

20

22

02

10

22

12

12

20

42

18

20

92

07

20

71

99

19

11

93

17

2 17

61

69

18

41

75 1

79

18

82

00

18

3 18

7 19

11

97

19

31

91

19

31

92

20

3

150

160

170

180

190

200

210

220

230

93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

Business Starts Were Down Nearly 20% in the Recession, Holding Back Most Types of Commercial Insurance Exposure, But

Are Recovering Slowly * Data through Dec. 30, 2012 are the latest available as of Nov. 21, 2013; Seasonally adjusted.

Source: Bureau of Labor Statistics, http://www.bls.gov/news.release/cewbd.t08.htm.

(Thousands)

Business starts were up 2.8% in 2012 to 769,000 following a 2.2% gain to

748,000 in 2011. Start-ups could accelerate in 2013.

Business Starts 2006: 872,000 2007: 843,000 2008: 790,000 2009: 697,000 2010: 742,000 2011: 748,000 2012: 769,000

52

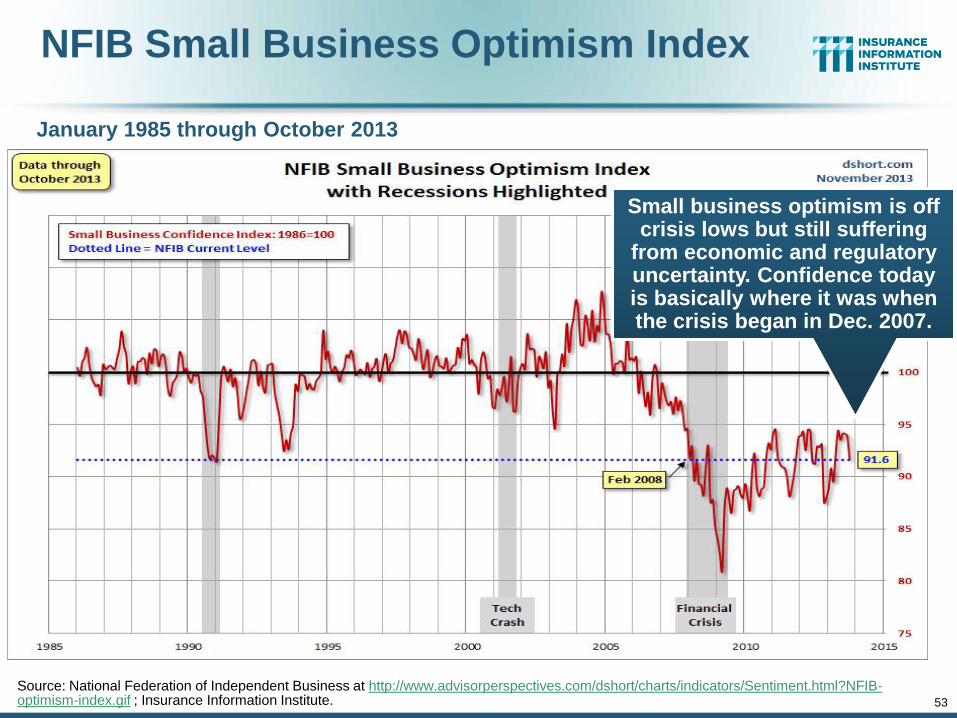

NFIB Small Business Optimism Index

January 1985 through October 2013

Source: National Federation of Independent Business at http://www.advisorperspectives.com/dshort/charts/indicators/Sentiment.html?NFIB-optimism-index.gif ; Insurance Information Institute. 53

Small business optimism is off crisis lows but still suffering

from economic and regulatory uncertainty. Confidence today is basically where it was when the crisis began in Dec. 2007.

54

12 Industries for the Next 10 Years: Insurance Solutions Needed

Export-Oriented Industries

Health Sciences

Health Care

Energy (Traditional)

Alternative Energy

Petrochemical

Agriculture

Natural Resources

Technology (incl. Biotechnology)

Light Manufacturing

Insourced Manufacturing

Many industries are

poised for growth, though

insurers’ ability to

capitalize on these

industries varies widely

Shipping (Rail, Marine, Trucking, Pipelines)

55

Labor Market Trends

Massive Job Losses Sapped the Economy and Commercial/Personal

Lines Exposure, But Trend is Improving

55

56

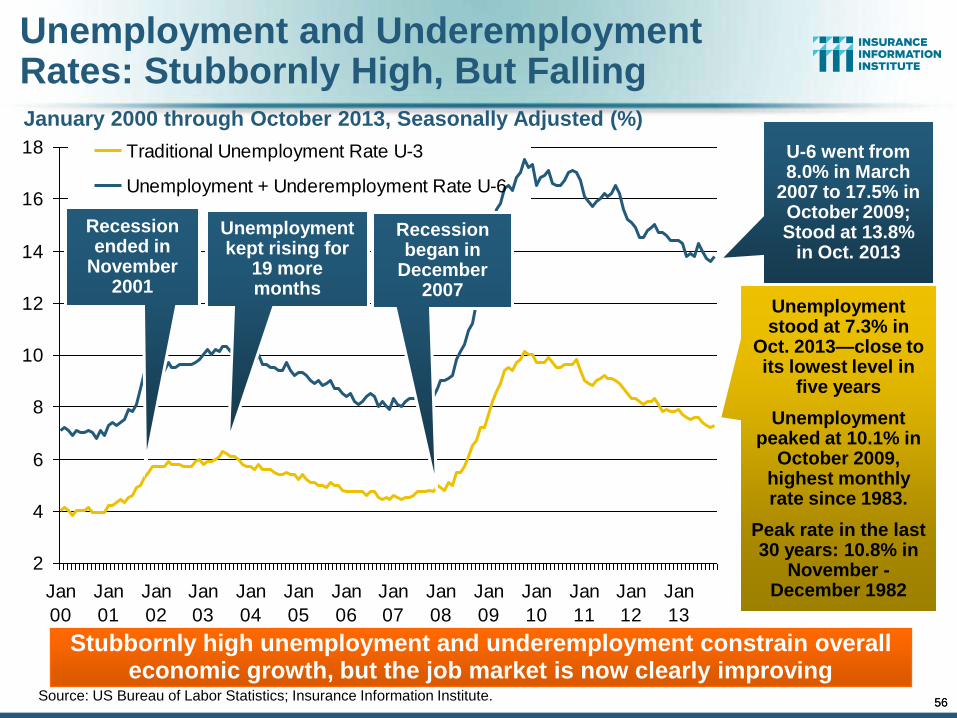

Unemployment and Underemployment Rates: Stubbornly High, But Falling

2

4

6

8

10

12

14

16

18

Jan

00

Jan

01

Jan

02

Jan

03

Jan

04

Jan

05

Jan

06

Jan

07

Jan

08

Jan

09

Jan

10

Jan

11

Jan

12

Jan

13

Traditional Unemployment Rate U-3

Unemployment + Underemployment Rate U-6

Unemployment stood at 7.3% in

Oct. 2013—close to its lowest level in

five years

Unemployment peaked at 10.1% in

October 2009, highest monthly rate since 1983.

Peak rate in the last 30 years: 10.8% in

November - December 1982

Source: US Bureau of Labor Statistics; Insurance Information Institute.

U-6 went from 8.0% in March

2007 to 17.5% in October 2009; Stood at 13.8%

in Oct. 2013

January 2000 through October 2013, Seasonally Adjusted (%)

Recession ended in

November 2001

Unemployment kept rising for

19 more months

Recession began in

December 2007

Stubbornly high unemployment and underemployment constrain overall economic growth, but the job market is now clearly improving

56

22

75

41

68

50

12

36

61

-79

24 6

8 74

51

2-1

14

-10

5-2

22

-21

9-2

03

-26

7-2

69

-42

9-4

84

-78

6 -70

1-8

21

-69

2-8

12

-82

1-2

88

-44

2-2

82 -2

22 -1

62

-23

3-3

4-1

67

-17

-26

17

01

02

94 10

31

29

11

3 18

81

54

11

48

02

43

22

33

03

18

31

77

20

61

29

25

61

74

19

7 24

9 32

32

65

20

81

20 15

27

81

77

13

11

18

21

7 25

62

24

16

43

19

15

4 18

81

87

19

41

00

20

71

50 2

12

11

1

(1,000)

(800)

(600)

(400)

(200)

0

200

400

Ja

n-0

7F

eb

-07

Ma

r-0

7A

pr-

07

Ma

y-0

7Ju

n-0

7Ju

l-0

7A

ug

-07

Se

p-0

7O

ct-

07

No

v-0

7D

ec-0

7Ja

n-0

8F

eb

-08

Ma

r-0

8A

pr-

08

Ma

y-0

8Ju

n-0

8Ju

l-0

8A

ug

-08

Se

p-0

8O

ct-

08

No

v-0

8D

ec-0

8Ja

n-0

9F

eb

-09

Ma

r-0

9A

pr-

09

Ma

y-0

9Ju

n-0

9Ju

l-0

9A

ug

-09

Se

p-0

9O

ct-

09

No

v-0

9D

ec-0

9Ja

n-1

0F

eb

-10

Ma

r-1

0A

pr-

10

Ma

y-1

0Ju

n-1

0Ju

l-1

0A

ug

-10

Se

p-1

0O

ct-

10

No

v-1

0D

ec-1

0Ja

n-1

1F

eb

-11

Ma

r-1

1A

pr-

11

Ma

y-1

1Ju

n-1

1Ju

l-1

1A

ug

-11

Se

p-1

1O

ct-

11

No

v-1

1D

ec-1

1Ja

n-1

2F

eb

-12

Ma

r-1

2A

pr-

12

Ma

y-1

2Ju

n-1

2Ju

l-1

2A

ug

-12

Se

p-1

2O

ct-

12

No

v-1

2D

ec-1

2Ja

n-1

3F

eb

-13

Ma

r-1

3A

pr-

13

Ma

y-1

3Ju

n-1

3Ju

l-1

3A

ug

-13

Se

p-1

3O

ct-

13

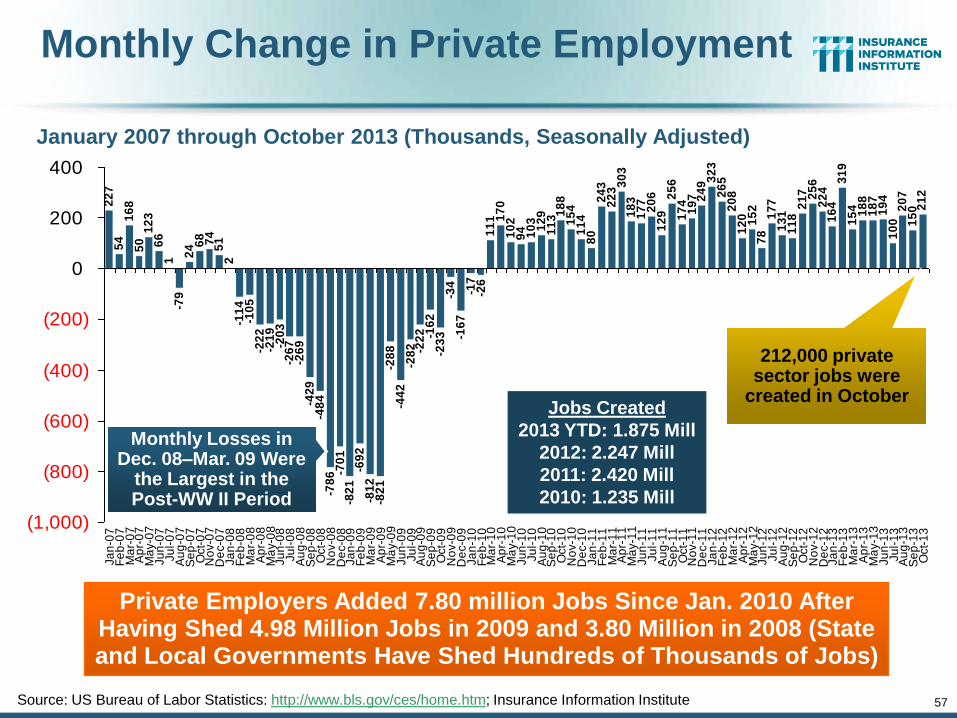

Monthly Change in Private Employment

January 2007 through October 2013 (Thousands, Seasonally Adjusted)

Private Employers Added 7.80 million Jobs Since Jan. 2010 After Having Shed 4.98 Million Jobs in 2009 and 3.80 Million in 2008 (State and Local Governments Have Shed Hundreds of Thousands of Jobs)

Source: US Bureau of Labor Statistics: http://www.bls.gov/ces/home.htm; Insurance Information Institute

Monthly Losses in Dec. 08–Mar. 09 Were

the Largest in the Post-WW II Period

212,000 private sector jobs were

created in October

57

Jobs Created

2013 YTD: 1.875 Mill

2012: 2.247 Mill

2011: 2.420 Mill

2010: 1.235 Mill

0.0

51

0.0

53

-0.0

61

-0.1

66

-0.3

88

-0.6

07

-0.8

10

-1.0

77

-1.3

46

-1.7

75

-2.2

59

-3.0

45

-3.7

46

-4.5

67

-5.2

59

-6.0

71

-6.8

92

-7.1

80

-7.6

22

-7.9

04

-8.1

26

-8.2

88

-8.5

21

-8.5

55

-8.7

22

-8.7

39

-8.7

65

-8.6

54

-8.4

84

-8.3

82

-8.2

88

-8.1

85

-8.0

56

-7.9

43

-7.7

55

-7.6

01

-7.4

87

-7.4

07

-6.9

41

-6.6

38

-6.4

55

-6.2

78

-6.0

72

-5.9

43

-5.6

87

-5.5

13

-5.3

16

-5.0

67

-4.7

44

-4.4

79

-4.2

71

-4.1

51

-3.9

99

-3.9

21

-3.7

44

-3.6

13

-3.4

95

-3.2

78

-3.0

22

-2.7

98

-2.6

34

-2.3

15

-2.1

61

-1.9

73

-1.7

86

-1.5

92

-1.4

92

-1.2

85

-1.1

35

-0.9

23

-7.1

64

-10

-8

-6

-4

-2

0

2

De

c-0

7Ja

n-0

8F

eb

-08

Ma

r-0

8A

pr-

08

Ma

y-0

8Ju

n-0

8Ju

l-0

8A

ug

-08

Se

p-0

8O

ct-

08

No

v-0

8D

ec-0

8Ja

n-0

9F

eb

-09

Ma

r-0

9A

pr-

09

Ma

y-0

9Ju

n-0

9Ju

l-0

9A

ug

-09

Se

p-0

9O

ct-

09

No

v-0

9D

ec-0

9Ja

n-1

0F

eb

-10

Ma

r-1

0A

pr-

10

Ma

y-1

0Ju

n-1

0Ju

l-1

0A

ug

-10

Se

p-1

0O

ct-

10

No

v-1

0D

ec-1

0Ja

n-1

1F

eb

-11

Ma

r-1

1A

pr-

11

Ma

y-1

1Ju

n-1

1Ju

l-1

1A

ug

-11

Se

p-1

1O

ct-

11

No

v-1

1D

ec-1

1Ja

n-1

2F

eb

-12

Ma

r-1

2A

pr-

12

Ma

y-1

2Ju

n-1

2Ju

l-1

2A

ug

-12

Se

p-1

2O

ct-

12

No

v-1

2D

ec-1

2Ja

n-1

3F

eb

-13

Ma

r-1

3A

pr-

13

Ma

y-1

3Ju

n-1

3Ju

l-1

3A

ug

-13

Se

p-1

3O

ct-

13

Millio

ns

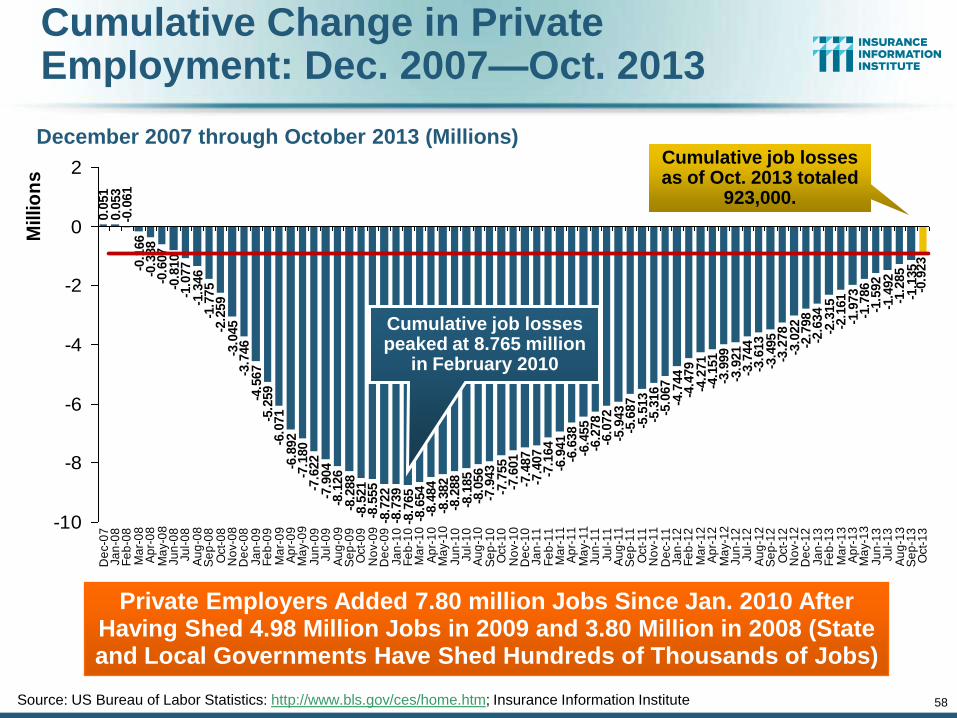

Cumulative Change in Private Employment: Dec. 2007—Oct. 2013

December 2007 through October 2013 (Millions)

Source: US Bureau of Labor Statistics: http://www.bls.gov/ces/home.htm; Insurance Information Institute

Cumulative job losses peaked at 8.765 million

in February 2010

Cumulative job losses as of Oct. 2013 totaled

923,000.

58

Private Employers Added 7.80 million Jobs Since Jan. 2010 After Having Shed 4.98 Million Jobs in 2009 and 3.80 Million in 2008 (State and Local Governments Have Shed Hundreds of Thousands of Jobs)

-0.0

17

-0.0

43

0.0

68

0.2

38

0.3

40

0.4

34

0.5

37

0.6

66

0.7

79

0.9

67

1.1

21

1.2

35

1.3

15

1.5

58

1.7

81

2.0

84

2.2

67

2.4

44

2.6

50

2.7

79

3.0

35

3.2

09

3.4

06

3.6

55

3.9

78

4.2

43

4.4

51

4.5

71

4.7

23

4.8

01

4.9

78

5.1

09

5.2

27

5.4

44

5.7

00

5.9

24

6.0

88

6.4

07

6.7

49

6.9

36

7.1

30

7.2

30

7.4

37

7.5

87

7.7

99

6.5

61

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

Jan-1

0

Feb-1

0

Mar-

10

Apr-

10

May-1

0

Jun-1

0

Jul-10

Aug-1

0

Sep-1

0

Oct-

10

Nov-1

0

Dec-1

0

Jan-1

1

Feb-1

1

Mar-

11

Apr-

11

May-1

1

Jun-1

1

Jul-11

Aug-1

1

Sep-1

1

Oct-

11

Nov-1

1

Dec-1

1

Jan-1

2

Feb-1

2

Mar-

12

Apr-

12

May-1

2

Jun-1

2

Jul-12

Aug-1

2

Sep-1

2

Oct-

12

Nov-1

2

Dec-1

2

Jan-1

3

Feb-1

3

Mar-

13

Apr-

13

May-1

3

Jun-1

3

Jul-13

Aug-1

3

Millio

ns

Cumulative Change in Private Sector Employment: Jan. 2010—October 2013

January 2010 through October 2013* (Millions)

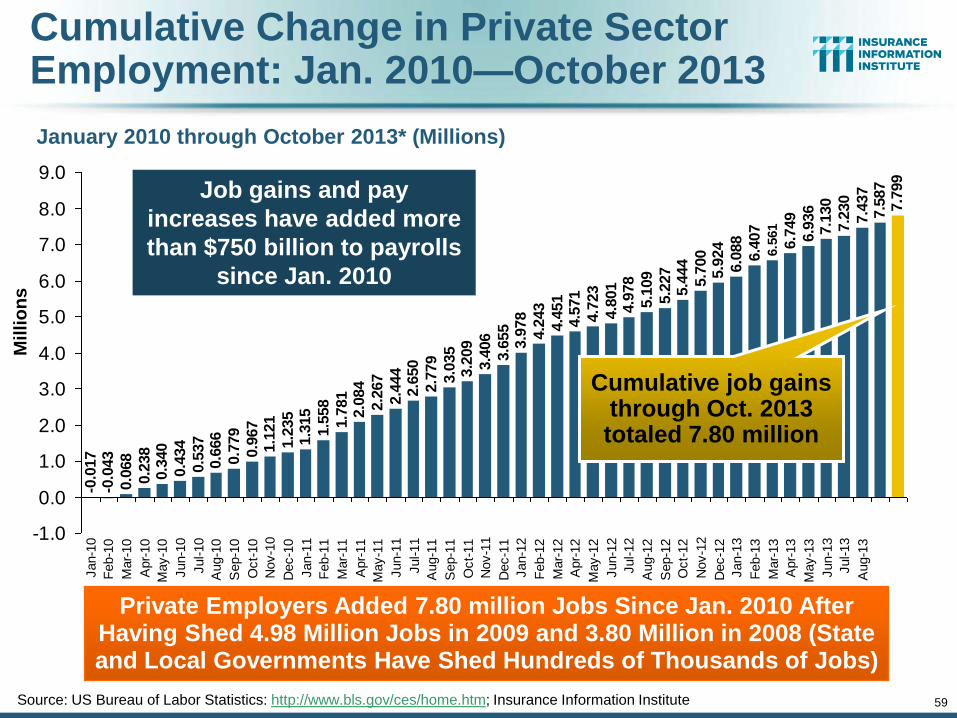

Source: US Bureau of Labor Statistics: http://www.bls.gov/ces/home.htm; Insurance Information Institute

Cumulative job gains through Oct. 2013 totaled 7.80 million

59

Job gains and pay

increases have added more

than $750 billion to payrolls

since Jan. 2010

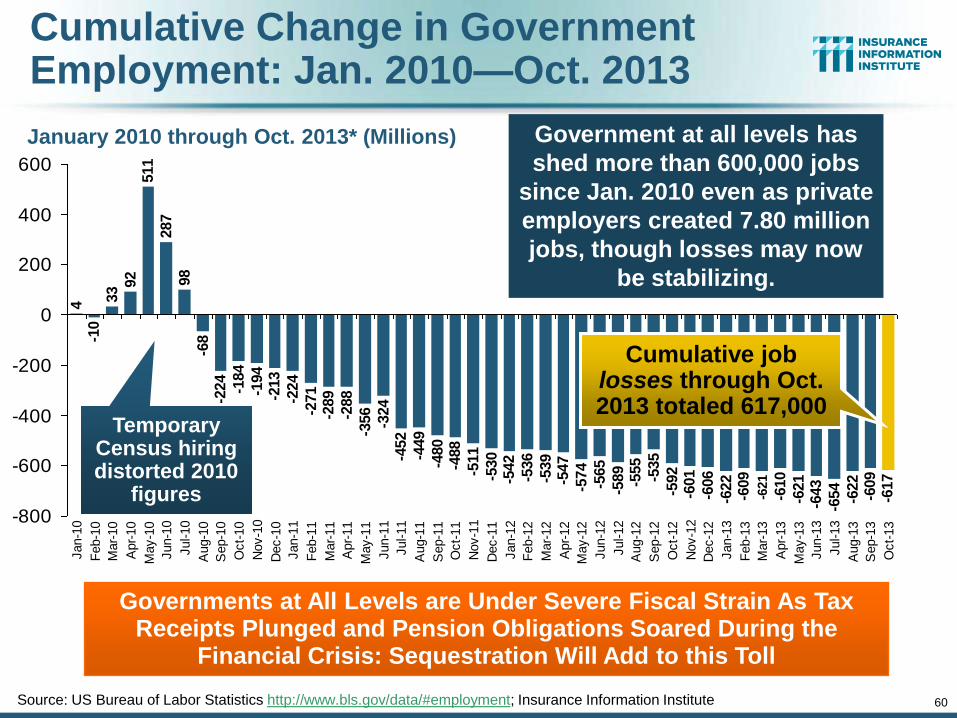

Private Employers Added 7.80 million Jobs Since Jan. 2010 After Having Shed 4.98 Million Jobs in 2009 and 3.80 Million in 2008 (State and Local Governments Have Shed Hundreds of Thousands of Jobs)

4-1

0

33 9

2511

287

98

-68

-224

-184

-194

-213

-224

-271

-289

-288

-356

-324

-452

-449

-480

-488

-511

-530

-542

-536

-539

-547

-574

-565

-589

-555

-535

-592

-601

-606

-622

-609

-610

-621

-643

-654

-622

-609

-617

-621

-800

-600

-400

-200

0

200

400

600

Jan-1

0

Feb-1

0

Mar-

10

Apr-

10

May-1

0