Embed Size (px)

Citation preview

Overview of PAYE reconciliation process and 2007/08 policy changesAnother helpful guide brought to you by South African Revenue Service

Overview of PAYE reconciliation process and 2007/08 policy changes

This guide to the PAYE reconciliation process is not meant to delve into the precise technical and legal detail that is often associated with tax. It should, therefore, not be used as a legal reference.

Should you require additional information concerning any aspect of taxation, you should:• Contact your local SARS office• Contact the National SARS Call Centre on 0860 12 12 18• Visit the SARS website www.sars.gov.za

South African Revenue Service18 July 2008

1

This document is intended to address key questions to help with your 2007/08 PAYE submissions:

What does PAYE reconciliation aim to do? .......................................... 21

What is the overall PAYE process? ....................................................... 32

How do I fill out the PAYE portion of the EMP501? ........................... 43

What is PAYE reconciliation? ............................................................... 64

What if my tax certificates do not match what I have paid SARS? ...... 8

What is not PAYE reconciliation? ........................................................ 7

6

5

Case studies 1: Adjustment for manual certificate issued ..................... 97

Policy changes in 2007/08 tax year .................................................... 11

Case studies 2: Adjustment for late payment commission .................. 10

9

8

What will SARS do once I have submitted my declaration? .............. 1210

Useful terms ........................................................................................ 1311

Who do I contact if I have any questions? .......................................... 1412

2

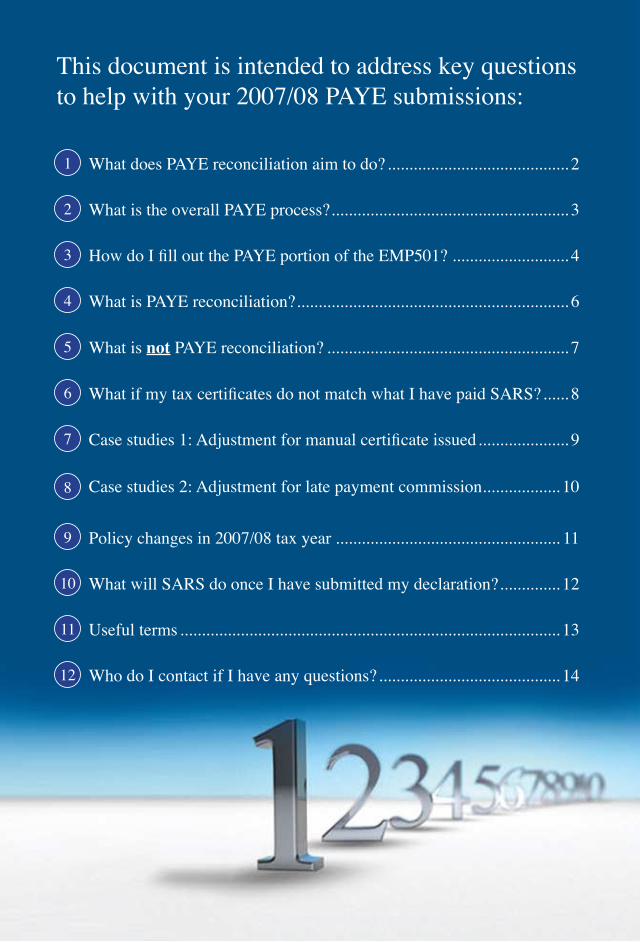

1 What does the PAYE reconciliation aim to do?

A Have I matched my actual PAYE liabilities as declared on the EMP501 with all the IRP5s for the tax year? - Have I accurately reflected the PAYE liabilities on the IRP5s? - Have I made adjustments for all errors?

This will help you

• Exclude liabilities or payments related to certificates issued in prior years

• Identify and resolve any differences between liabilities declared on your EMP201s and actual liabilities based on IRP5s

• Determine what is due to/by SARS for the tax year

2007/08 PAYE reconciliation aims to answer two questions

Why do these questions matter?

B How do I ensure the employee data is correct for accurate pre-population of tax returns? - Have I accurately matched the liabilities to employee records?

This will help you

• Reconcile your 'to be issued' IRP5s with the taxes withheld

• Issue accurate IRP5s to your employees for 2007/08 tax year

You will not be allowed to issue IRP5s to your employees if you are not reconciled for tax year 2007/08

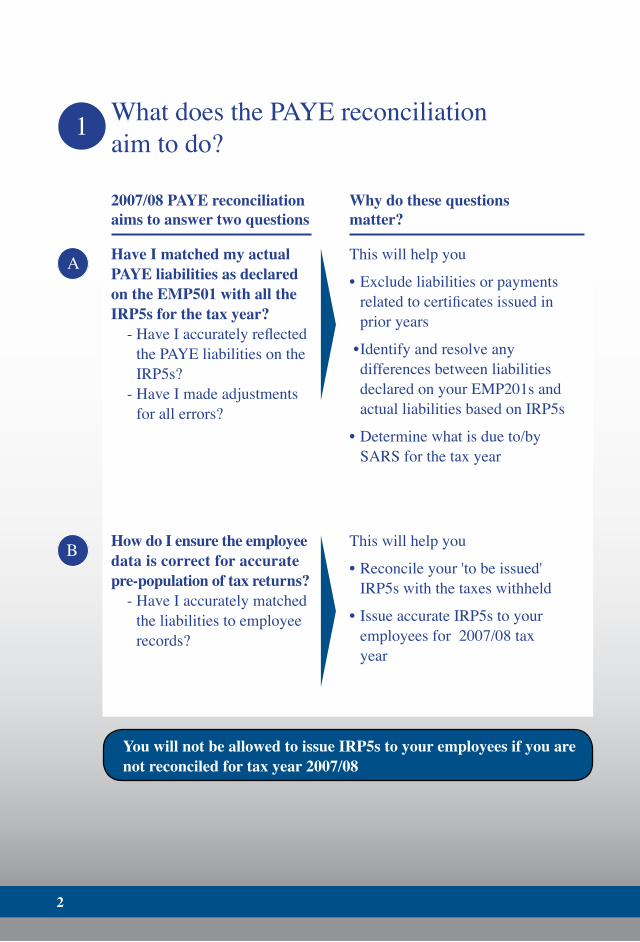

3

Submit the reconciled declaration

Match the computed liability in step 3 to the liabilities and pay-ments and adjust for errors

Compute actual annual liability as per IRP5s to be issued

3

4

5

2 Submit monthly declaration and pay withheld liabilities

2 What is the overall PAYE process?

What does the employer do?

• Run the monthly payroll to determine your current declarations and monthly liabilities

• Declare this liability on form EMP201 and submit it together with the payment to SARS by the 7th of the month following the month of employee remuneration

• Compute the actual liabilities for transactions in the 2007/08 tax year based on your annual payroll: - Imported as a CSV - Manual certificates issued

• Remove liabilities or payments relating to certificates issued in prior years• Reconcile the actual declared 2007/08 liabilities and payments to the certificates to be issued this year• Account for the differences

• Submit your signed EMP501 and associated payroll data to SARS by August 29, 2008• Pay any adjustments owing to SARSNote: The employer will be liable to pay any adjustment owing to SARS

1 Run monthly payroll

4

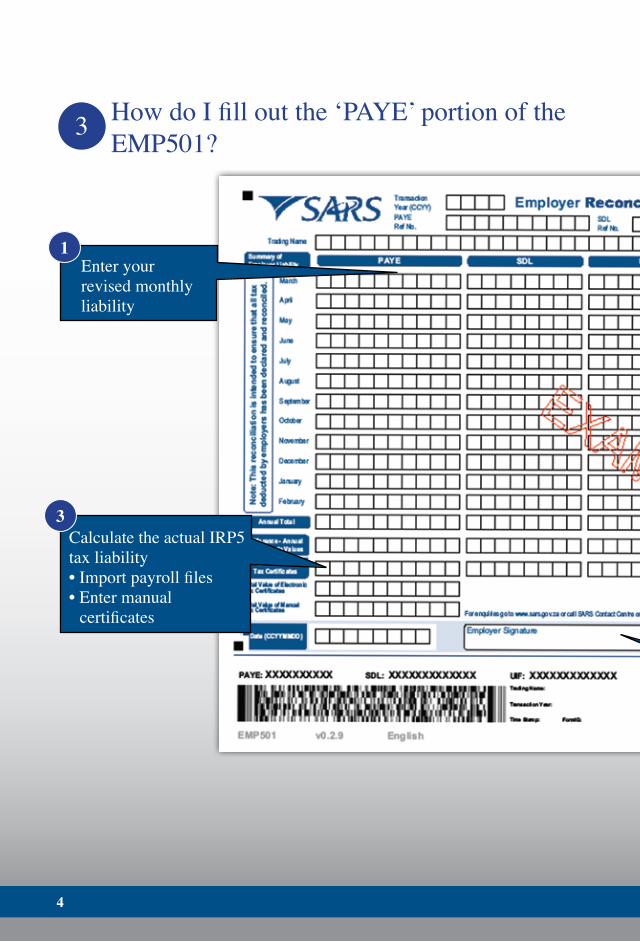

3 How do I fill out the ‘PAYE’ portion of the EMP501?

Enter your revised monthly liability

1

Calculate the actual IRP5 tax liability • Import payroll files• Enter manual certificates

3

5

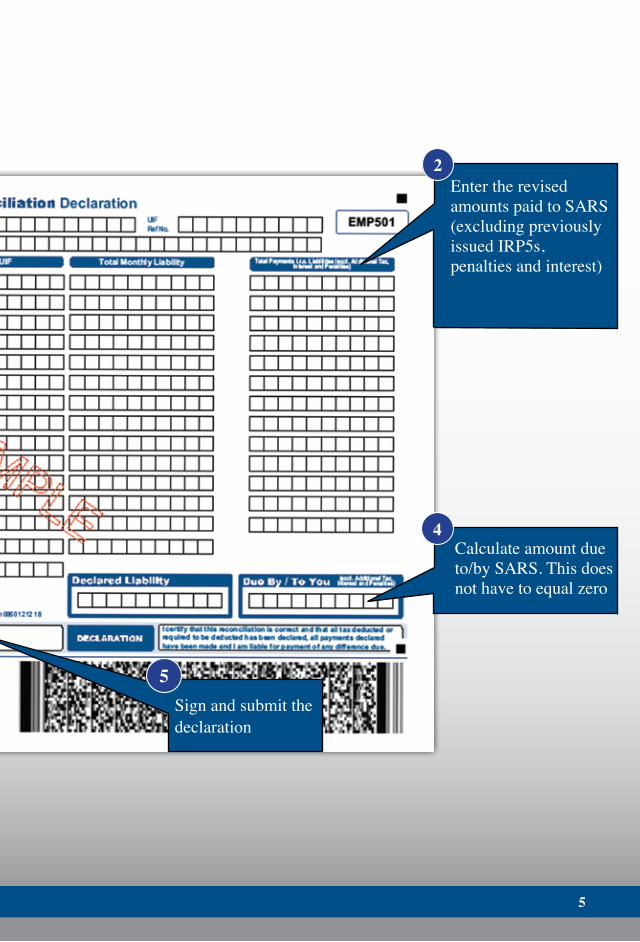

5Sign and submit the declaration

Calculate amount due to/by SARS. This does not have to equal zero

4

Enter the revised amounts paid to SARS(excluding previously issued IRP5s, penalties and interest)

2

6

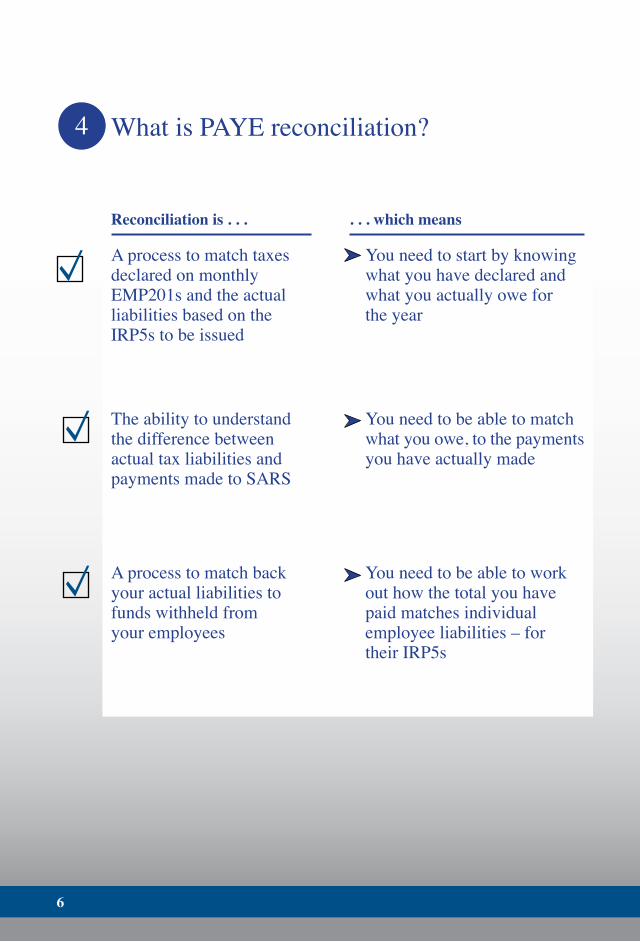

4 What is PAYE reconciliation?

Reconciliation is . . . . . . which means

A process to match taxes declared on monthly EMP201s and the actual liabilities based on the IRP5s to be issued

You need to start by knowing what you have declared and what you actually owe for the year

The ability to understand the difference between actual tax liabilities and payments made to SARS

You need to be able to match what you owe, to the payments you have actually made

A process to match back your actual liabilities to funds withheld from your employees

You need to be able to work out how the total you have paid matches individual employee liabilities – for their IRP5s

7

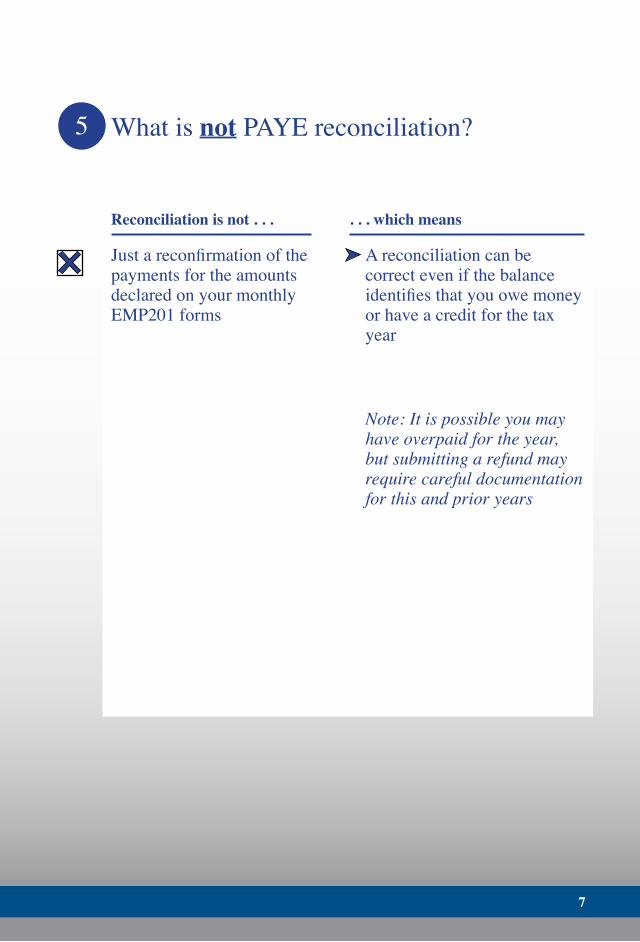

5 What is not PAYE reconciliation?

Reconciliation is not . . . . . . which means

Just a reconfirmation of the payments for the amounts declared on your monthly EMP201 forms

A reconciliation can be correct even if the balance identifies that you owe money or have a credit for the tax year

Note: It is possible you may have overpaid for the year, but submitting a refund may require careful documentation for this and prior years

8

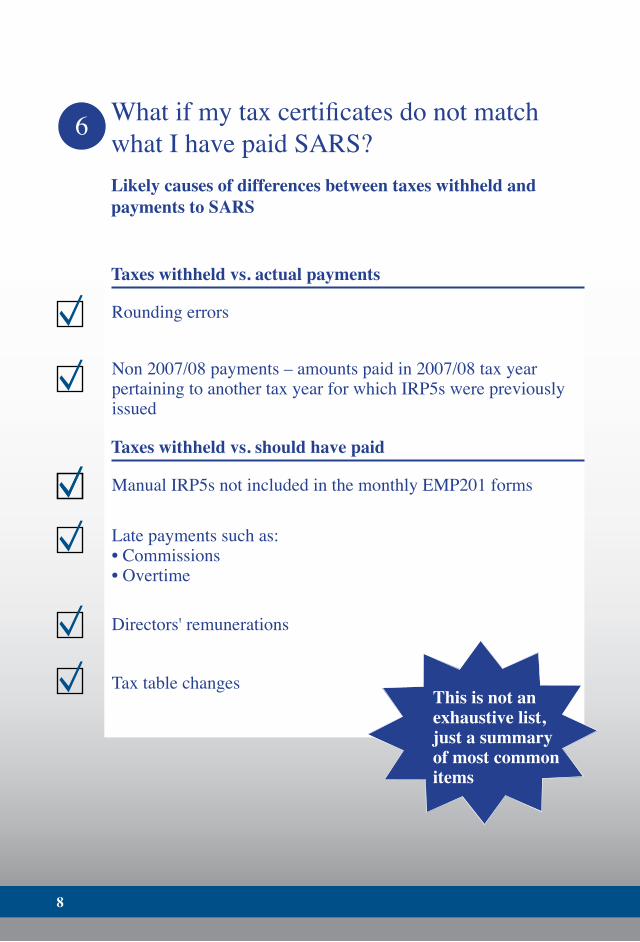

6 What if my tax certificates do not match what I have paid SARS?Likely causes of differences between taxes withheld and payments to SARS

Taxes withheld vs. actual payments

Rounding errors

Non 2007/08 payments – amounts paid in 2007/08 tax year pertaining to another tax year for which IRP5s were previously issued

Taxes withheld vs. should have paid

Manual IRP5s not included in the monthly EMP201 forms

Late payments such as: • Commissions• Overtime

Tax table changes

Directors' remunerations

This is not an exhaustive list, just a summary of most common items

9

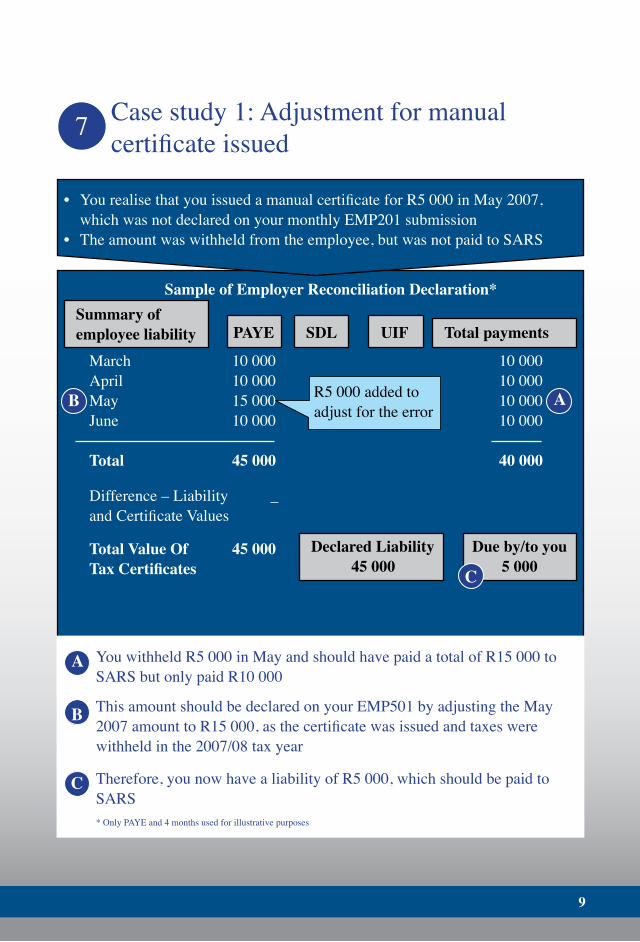

7 Case study 1: Adjustment for manual certificate issued

• You realise that you issued a manual certificate for R5 000 in May 2007, which was not declared on your monthly EMP201 submission• The amount was withheld from the employee, but was not paid to SARS

PAYE SDL UIFSummary of employee liability

Sample of Employer Reconciliation Declaration*

Total payments

Due by/to you5 000

Declared Liability45 000

MarchAprilMayJune

Total

Difference – Liability and Certificate Values

Total Value Of Tax Certificates

10 00010 00015 00010 000

45 000

45 000

–

10 00010 00010 00010 000

40 000

A

You withheld R5 000 in May and should have paid a total of R15 000 to SARS but only paid R10 000

A

This amount should be declared on your EMP501 by adjusting the May 2007 amount to R15 000, as the certificate was issued and taxes were withheld in the 2007/08 tax year

B

Therefore, you now have a liability of R5 000, which should be paid to SARS

C

C

B R5 000 added to adjust for the error

* Only PAYE and 4 months used for illustrative purposes

10

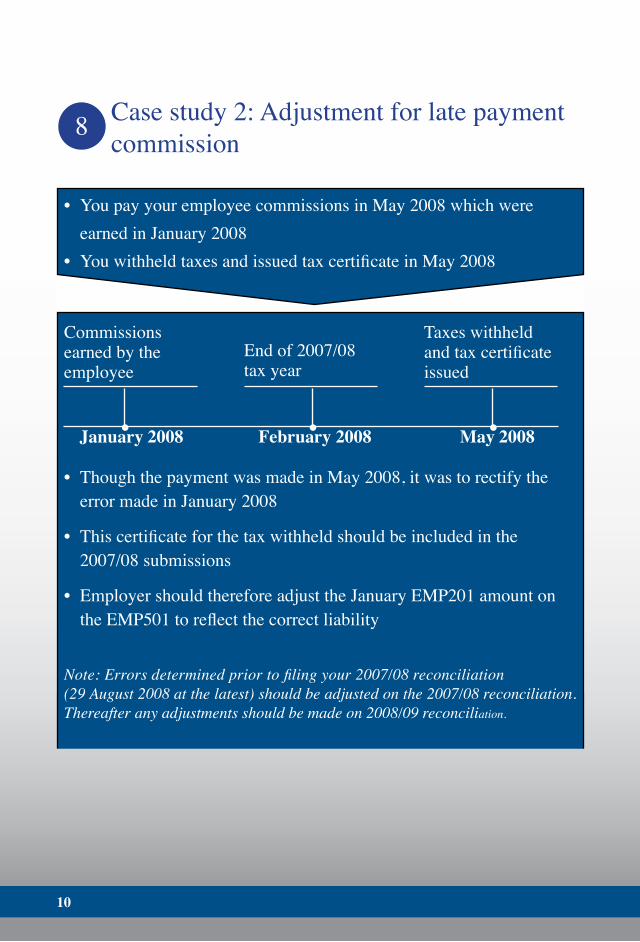

8 Case study 2: Adjustment for late payment commission

• Though the payment was made in May 2008, it was to rectify the error made in January 2008

• This certificate for the tax withheld should be included in the 2007/08 submissions

• Employer should therefore adjust the January EMP201 amount on the EMP501 to reflect the correct liability

Note: Errors determined prior to filing your 2007/08 reconciliation (29 August 2008 at the latest) should be adjusted on the 2007/08 reconciliation. Thereafter any adjustments should be made on 2008/09 reconciliation.

Commissions earned by the employee

End of 2007/08 tax year

Taxes withheld and tax certificate issued

January 2008 February 2008 May 2008

• You pay your employee commissions in May 2008 which were earned in January 2008• You withheld taxes and issued tax certificate in May 2008

11

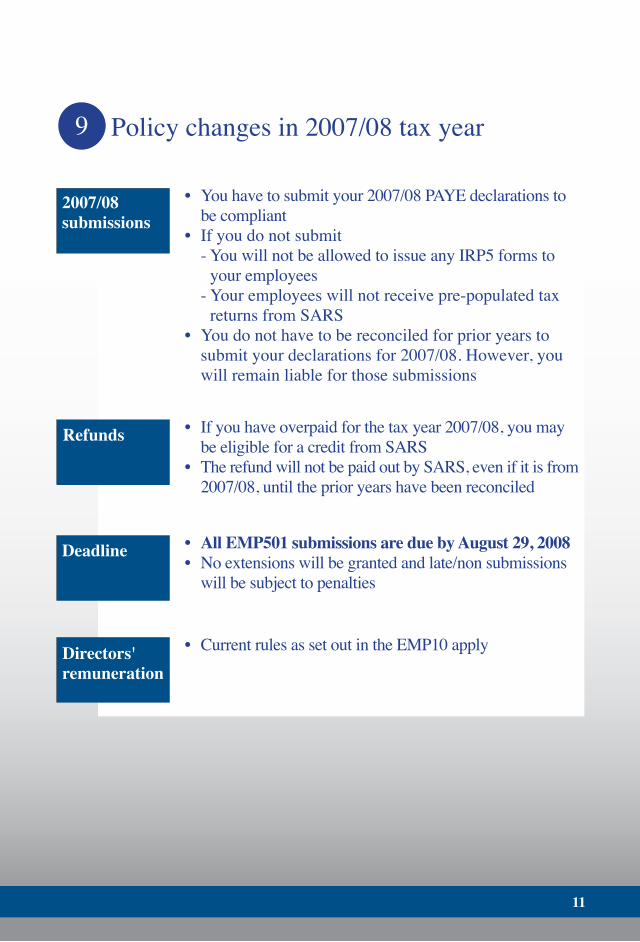

9 Policy changes in 2007/08 tax year

2007/08 submissions

• You have to submit your 2007/08 PAYE declarations to be compliant • If you do not submit - You will not be allowed to issue any IRP5 forms to your employees - Your employees will not receive pre-populated tax returns from SARS• You do not have to be reconciled for prior years to submit your declarations for 2007/08. However, you will remain liable for those submissions

Refunds • If you have overpaid for the tax year 2007/08, you may be eligible for a credit from SARS• The refund will not be paid out by SARS, even if it is from 2007/08, until the prior years have been reconciled

Deadline • All EMP501 submissions are due by August 29, 2008• No extensions will be granted and late/non submissions will be subject to penalties

Directors' remuneration

• Current rules as set out in the EMP10 apply

12

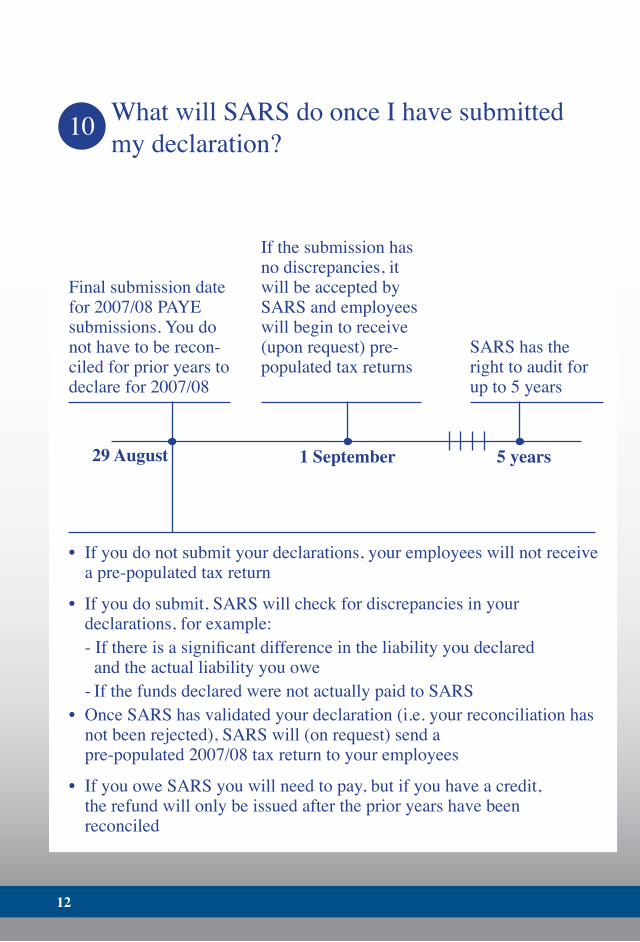

• If you do not submit your declarations, your employees will not receive a pre-populated tax return

• If you do submit, SARS will check for discrepancies in your declarations, for example: - If there is a significant difference in the liability you declared and the actual liability you owe - If the funds declared were not actually paid to SARS• Once SARS has validated your declaration (i.e. your reconciliation has not been rejected), SARS will (on request) send a pre-populated 2007/08 tax return to your employees

• If you owe SARS you will need to pay, but if you have a credit, the refund will only be issued after the prior years have been reconciled

Final submission date for 2007/08 PAYE submissions. You do not have to be recon-ciled for prior years to declare for 2007/08

If the submission has no discrepancies, it will be accepted by SARS and employees will begin to receive (upon request) pre-populated tax returns

SARS has the right to audit for up to 5 years

10 What will SARS do once I have submitted my declaration?

29 August 1 September 5 years

13

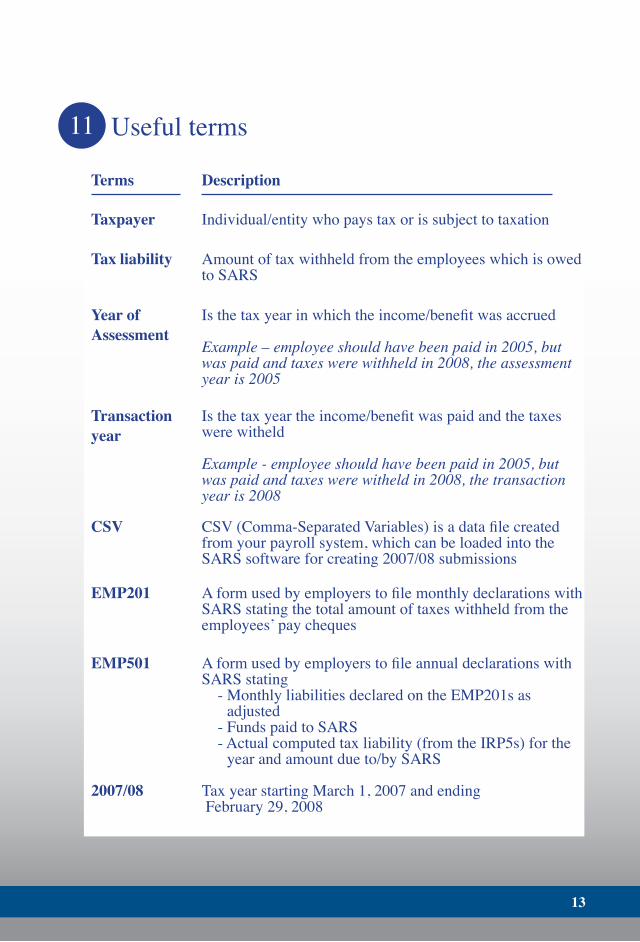

11 Useful terms

Terms

Taxpayer Individual/entity who pays tax or is subject to taxation

Tax liability Amount of tax withheld from the employees which is owed to SARS

Transaction year

Is the tax year the income/benefit was paid and the taxes were witheld

Example - employee should have been paid in 2005, but was paid and taxes were witheld in 2008, the transaction year is 2008

Year of Assessment

Is the tax year in which the income/benefit was accrued Example – employee should have been paid in 2005, but was paid and taxes were withheld in 2008, the assessment year is 2005

CSV CSV (Comma-Separated Variables) is a data file created from your payroll system, which can be loaded into the SARS software for creating 2007/08 submissions

EMP201 A form used by employers to file monthly declarations with SARS stating the total amount of taxes withheld from the employees’ pay cheques

EMP501 A form used by employers to file annual declarations with SARS stating - Monthly liabilities declared on the EMP201s as adjusted - Funds paid to SARS - Actual computed tax liability (from the IRP5s) for the year and amount due to/by SARS

2007/08 Tax year starting March 1, 2007 and ending February 29, 2008

Description

14

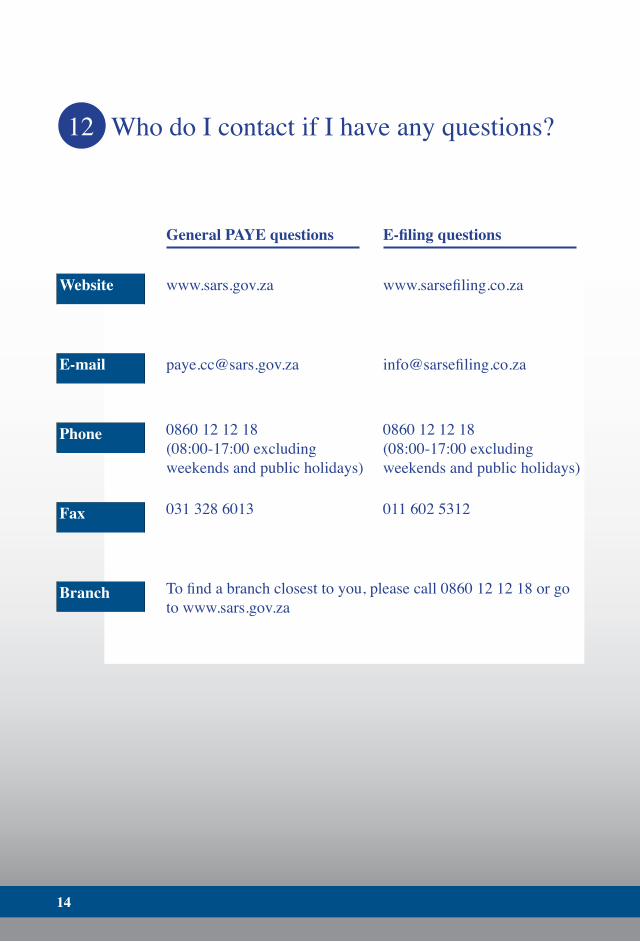

12 Who do I contact if I have any questions?

General PAYE questions E-filing questions

www.sars.gov.za www.sarsefiling.co.zaWebsite

[email protected] [email protected]

0860 12 12 18(08:00-17:00 excluding weekends and public holidays)

0860 12 12 18(08:00-17:00 excluding weekends and public holidays)

Phone

031 328 6013 011 602 5312Fax

To find a branch closest to you, please call 0860 12 12 18 or go to www.sars.gov.za

Branch

NOTES

NOTES

Lehae La SARS, 299 Bronkhorst Street, Nieuw Muckleneuk 0181, Private Bag X923, Pretoria, 0001, South Africa

Telephone: +27 12 422 4000, Fax: +27 12 422 5181, Web: www.sars.gov.za