Embed Size (px)

Citation preview

Page 1

Notes on FDI

By Saul Estrin

Page 2

Outline of Presentation

Context on FDI to Emerging Marketso definitionso scale

The Determinants of FDI

Findings From our Survey

Findings From the Cases

Learning Points

Page 3

Context of FDI to Emerging Markets

Definition of FDI

Role of FDI

Scale of FDI

Page 4

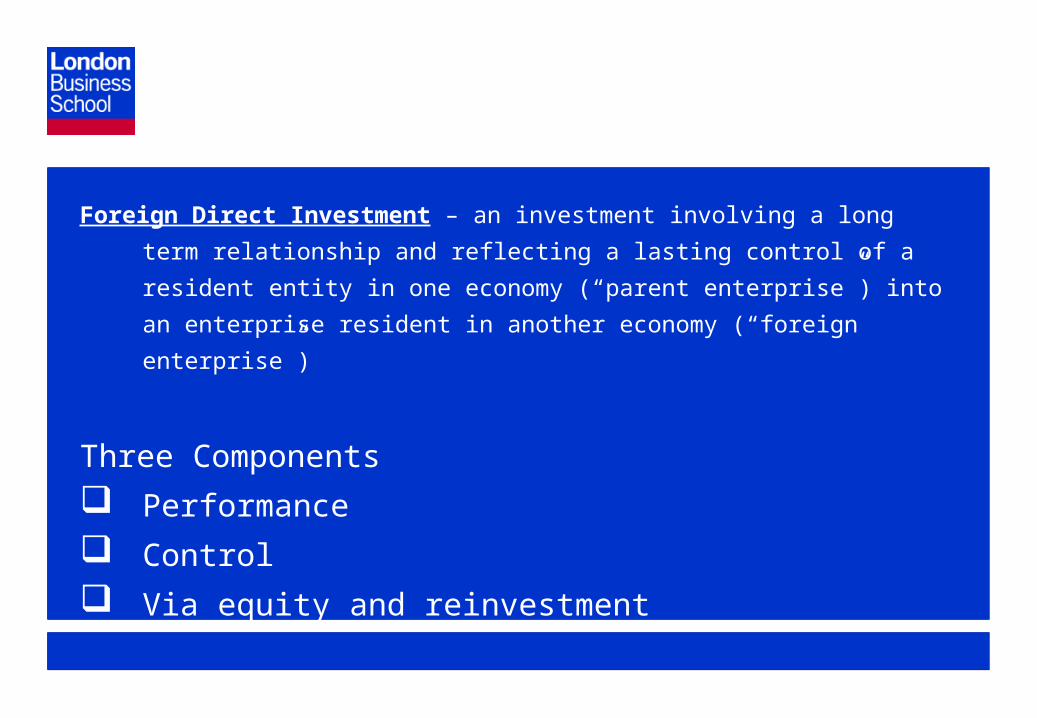

Foreign Direct Investment – an investment involving a long term

relationship and reflecting a lasting control of a resident entity in

one economy (“parent enterprise”) into an enterprise resident in

another economy (“foreign enterprise”)

Three Components

Performance

Control

Via equity and reinvestment

Page 5

Why is FDI Important?

Permits investment to exceed savings without foreign borrowing – source of growth – evidence?

Transfer of technology

Transfer of skills Spillover effects

Transfer of managerial know-how

Integration into world economy

Page 6

Why is FDI Important?cont

But in emerging markets……..

Can lead to dual economy – lack of spillovers

Forward and backward linkages

Can weaken development of local institutions e.g. capital markets

Can lead to increase in domestic monopoly power

Page 7

Table 1 FDI to Whom: Inflows ($bn)

1991-1996 1997 1998 1999 2000 2001 2002

World 254 482 686 1079 1393 824 651

Developing Countries 92 193 191 230 246 209 162

Developing Share (%) 36 40 28 21 18 25 25

Africa 5 11 9 12 8 19 11

Latin America 27 73 82 108 93 84 56

Asia 59 109 100 108 142 107 95

Central & Eastern Europe 8 19 22 25 26 25 29

Page 8

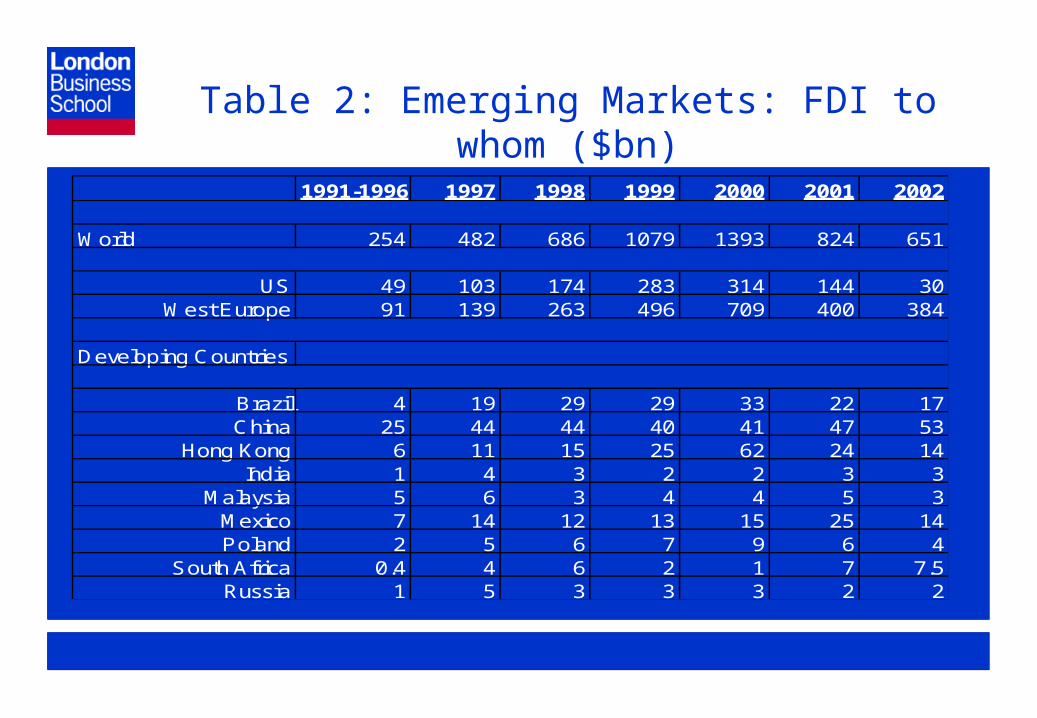

Table 2: Emerging Markets: FDI to whom ($bn)

1991-1996 1997 1998 1999 2000 2001 2002

World 254 482 686 1079 1393 824 651

US 49 103 174 283 314 144 30West Europe 91 139 263 496 709 400 384

Developing Countries

Brazil 4 19 29 29 33 22 17China 25 44 44 40 41 47 53

Hong Kong 6 11 15 25 62 24 14India 1 4 3 2 2 3 3

Malaysia 5 6 3 4 4 5 3Mexico 7 14 12 13 15 25 14Poland 2 5 6 7 9 6 4

South Africa 0.4 4 6 2 1 7 7.5Russia 1 5 3 3 3 2 2

Page 9

Table 3 Outflows: Major Countries ($bn)

1991-1996 1997 1998 1999 2000 2001 2002

World Developed Economies 280 477 683 1096 1200 711 647240 396 631 1021 1098 660 600

US 67 96 131 209 143 104 120West Europe 140 244 437 771 872 487 411

Developing Countries 39 77 50 73 99 47 43

Brazil 0.5 1.1 2.8 1.7 2.3 -2.6 2.5

Hong Kong 17 24 17 19 59 11 18

Russia 0.5 3 1 2 3 3 3

Page 10

Reasons for FDI - OLI Paradigm

FDI occurs when three sets of determining factors occur simultaneously:

O – Ownership-specific advantages of firms;

L - Location advantages of host countries;

I - Internalisation - firms able to exploit O and L advantages through

internalisation rather than via the market;

o If firm only has O, it will rely on exports, licenses and sale of patents

in foreign market.

o If it has O and I, it will invest directly abroad.

o L advantage of the host country determines where.

Page 11

Main Economic Determinants of FDI

Type of FDI

Market Seeking;

Resource Seeking

Efficiency Seeking;

Determinants

market size;

market growth;

access to global/regional markets;

raw materials; oil, gas,minerals,timber

cost of resources and assets, e.g. labour, skills,

technology.

input costs e.g. transport, communication;

Page 12

Overview of Research Project

Study of FDI in Egypt, India, South Africa and Vietnam

Surveys of FDI subsidiaries – 600+ firms

12 cases (four per country)

Summarise comparative findings from survey and case results

Page 13

Our Countries

Very different in size, history, institutions

Similar in “level of” development

Similar in scale of FDI

Page 14

in million US$

South Africa 49 -5 -8 -42 -19 380 1241 818 3817 561 1502 888 6653India 113 236 155 233 574 973 2144 2525 3619 2633 2168 2319 3404Egypt 926 734 352 459 493 1256 598 636 887 1065 2919 1235 510Vietnam* 5 16 32 385 523 1936 2336 1803 2587 1700 1484 1289 1300

2001

Note: we use the latest available revision of the data, i.e. WIR 2002 for datafor 1996 onwards. * In the case of Vietnam, this involves a considerabledownward adjustment of the data from 1996 onwards, compared to the datareported in the WIR 2001.

Source: United Nations: World Investment Report annual 1994 to2002.

1982 – 89 (annual average)

97 98 99 200093 94 95 9690 91 92

Table 1.1: FDI in Emerging Markets

Page 15

Table 1.2 Key economic and social data in Egypt, India, South Africa and Vietnam

Sources: IMF: International Financial Statistics; World Bank: Development Report, Competitiveness Indicators; UN: Human Development Report, various years.

1990 2000 1990 1990

52 64 835 34

926 1.49 377 3.325

66.9 62.9

55.3 57.2

0.642 0.577

115 124

28.7 37.8

20.2 6.6

42.7 27.7

17 28

86 32

21 4

493 158

Vietnam

2000 2000 1990 2000

Egypt India S.Africa

66 79Population, million 1.016 43

78 390GDP per capita, US$ 460 3.02

53.7 53.9 50.3 67.8Life expectancy at birth ** 52.1 50.3

Adult literacy rate 85.3 93.4

HDI index 0.574 0.511 0.714 0.695 0.605 0.688

HDI rank na na na 107 na 109

Gini index *** na na na 59.3 na 36.1

Tertiary enrolment rates, % **** 15.8 6.1 13.2 18.9 1.9 4.1

Urban population, % of total ** 43.5 21.3 48 56.9 18.8 24.1

Agriculture % of GDP 19 31 5 4 37 26

32Phone lines (# per 1000 people) 30 6

10Mobile phones (# per 1000 people) na na

274Scientists and engineers in R&D per million peoplena na na 992 na

na 190 na

93 114 1

Notes * averages over the 1990-1995 and 1996-2000, ** data refer to 1975 and 1999, *** Gini coefficient refers to different years between 1993 and 1998, **** data refer to 1990 and 1995 .

Page 16

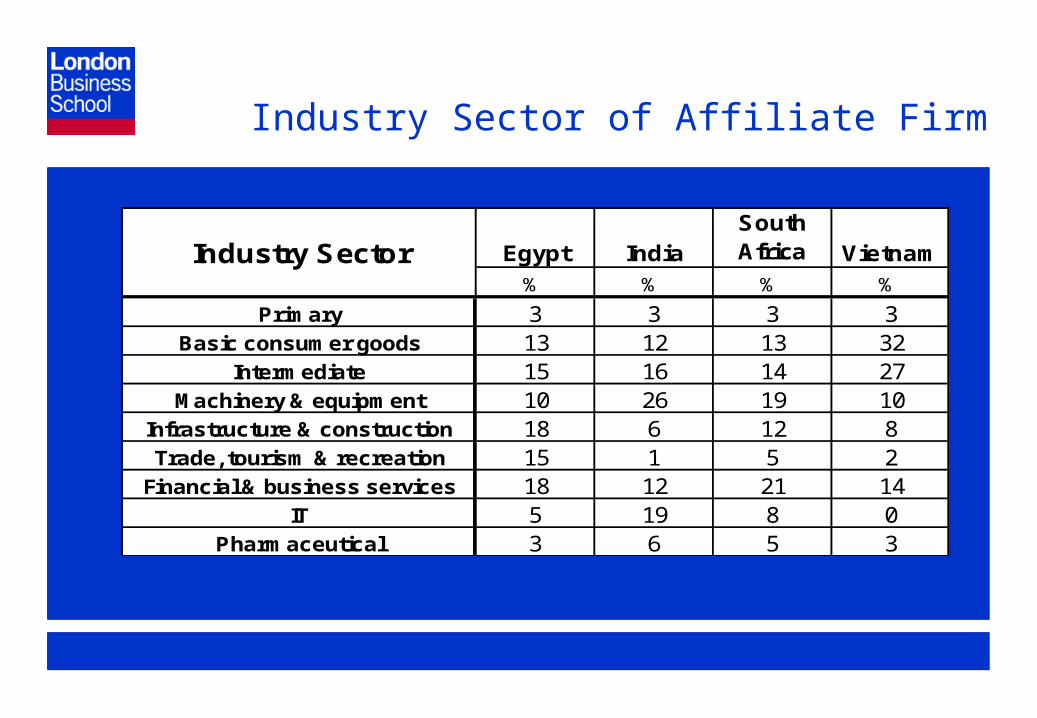

Industry Sector Egypt IndiaSouth Africa Vietnam

% % % %

Primary 3 3 3 3Basic consumer goods 13 12 13 32

Intermediate 15 16 14 27Machinery & equipment 10 26 19 10

Infrastructure & construction 18 6 12 8Trade, tourism & recreation 15 1 5 2

Financial & business services 18 12 21 14IT 5 19 8 0

Pharmaceutical 3 6 5 3

Industry Sector of Affiliate Firm

Page 17

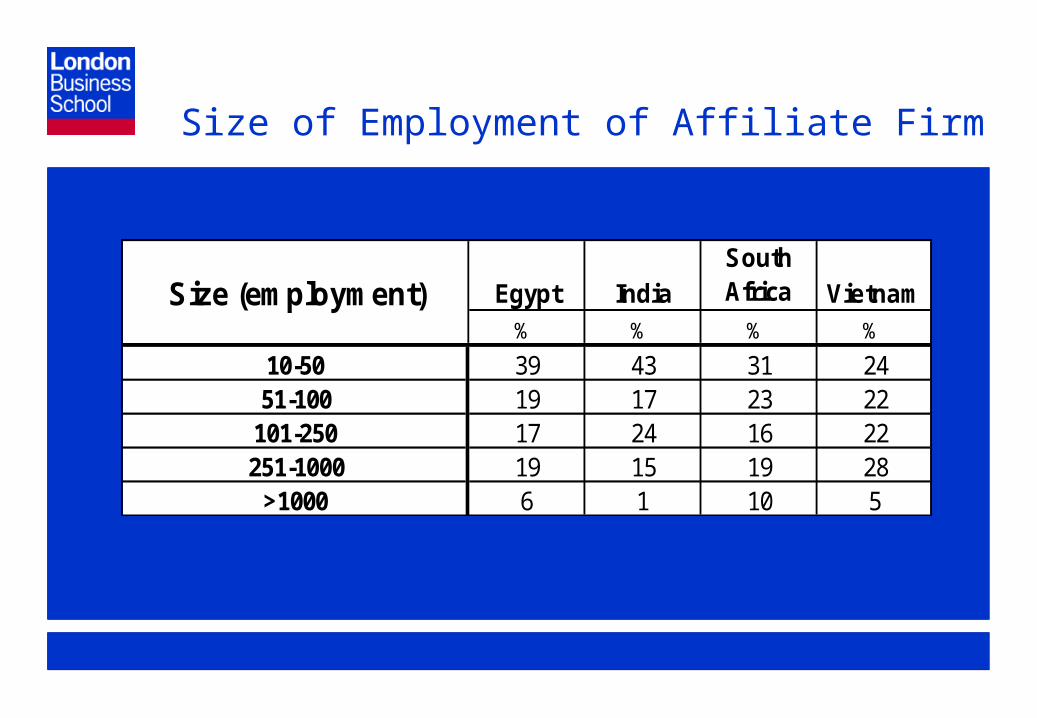

Size (employment) Egypt IndiaSouth Africa Vietnam

% % % %

10-50 39 43 31 2451-100 19 17 23 22

101-250 17 24 16 22251-1000 19 15 19 28

>1000 6 1 10 5

Size of Employment of Affiliate Firm

Page 18

Home Regions Egypt IndiaSouth Africa Vietnam

% % % %

North America 19 29 23 5Europe 43 48 57 15

Japan & East Asia 2 17 14 78MENA 33 2 0 1

Other (incl. Australia) 2 2 6 2

Geographic Regions of Parent Firms

Page 19

Global Employment Egypt IndiaSouth Africa Vietnam

% % % %

< 1000 32 38 19 351000 – 10,000 28 36 31 33

10,000 – 100,000 21 21 40 27> 100,000 19 5 10 5

Global Employment of Parent Firm

Page 20

Mode of Entry Egypt IndiaSouth Africa Vietnam

% % % %

Greenfield 47 36 32 55Joint Venture 37 52 22 33Acquisition 5 4 32 2

Partial Acquisition 12 8 14 11

Mode of Entry

Page 21

T6

Market Focus (initial and current) Initial Current Initial Current Initial Current Initial Current

1 % of Exported Product 22 27 38 39 18 26 49 50

2 Regional Market 10 12 5 7 3 9 25 243 Global Market 10 10 21 21 11 14 18 204 Other Affiliates of the Parent 3 4 12 10 4 3 7 6

Egypt India South Africa Vietnam

% % % %

Domestic Markets vs Exports

Page 22

0 10 20 30 40 50 60

Technology

Marketing

Management

Machinery

Equity

Distribution networks

Business networks

Brands

PercentageVietnam South Africa India Egypt

Figure 5: Critical Resources Chosen

Page 23

0 10 20 30 40 50 60 70 80 90 100

Technology

Marketing

Management

Machinery

Equity

Distribution networks

Business networks

Brands

PercentageVietnam South Africa India Egypt

Figure 5a: Local Firm Source of Resource

Page 24

0 10 20 30 40 50 60 70 80 90 100

Technology

Marketing

Management

Machinery

Equity

Distribution networks

Business networks

Brands

PercentageVietnam South Africa India Egypt

Figure 5b: Foreign Parent Source of Resource

Page 25

0 5 10 15 20 25 30 35 40

Technology

Marketing

Management

Machinery

Equity

Distribution networks

Business networks

Brands

PercentageVietnam South Africa India Egypt

Figure 5c: Other Local Source of Resource

Page 26

0 0.5 1 1.5 2 2.5 3 3.5 4 4.5

Executive management

Professionals

Operations management

Skilled non-managementlabour

Mean RankEgypt Mean Rank India Mean Rank South Africa Mean Rank Vietnam Mean Rank

Figure 6: Labour Market Evaluation - by Country

Page 27

0 0.5 1 1.5 2 2.5 3 3.5 4 4.5 5

Utility reliablility

IT& telecom reliability

Competent professionals

Real estate

Machinery & equipment

Raw material & components

Mean RankEgypt Mean Rank India Mean Rank South Africa Mean Rank Vietnam Mean Rank

Figure 7: Local Inputs - by Country

Page 28

0 0.5 1 1.5 2 2.5 3 3.5 4 4.5

Business license

Real estate

Visa & work permit

Environment regulations

General legal frameworks

Predictability

Central government

Provincial government

Local government

Mean RankEgypt Mean Rank India Mean Rank South Africa Mean Rank Vietnam Mean Rank

Figure 8: Institutional Environments - by Country

Page 29

0 0.5 1 1.5 2 2.5 3 3.5 4 4.5

Revenue Growth

Profitability

Productivity

Mean Rank

Vietnam South Africa India Egypt

Figure 9: Performance - by Country

Page 30

Lesson from Survey

Most FDI small – not a motor of employment creation

Local familiarity, experience and integration to regional trading blocks very important

High proportion of FDI is market - seeking

Entry mode mainly greenfield and JV

Contribution of key resources mainly from foreign firms

Business environment particularly weak in terms of institutions and policy

Page 31

Table 1: Sectoral Distribution of Case Studies

Egypt India South Africa Vietnam

Services ECMS ABN Amro ABN Amro ---

Food &

Beverages

Manufacturing,

intermediate

products

Manufacturing, final products

(Telecom)

Heinz

( ketchup)

----

GlaxoSmithKline

(pharmaceuticals)

(banking)

Barcardi-Martini

(spirits)

Packaging

(packaging)

-----

ABN Amro

(banking)

---

NGK/Behr

(autmotive suppliers)

EST

SEAB/Carlsberg

(brewing)

ABB

(Electrical

components)

Honda

(motorcycles)

Page 32

Findings from Cases

Global strategies are prime drivers of FDI Promote global or regional supply base, e.g.

Honda Extend market research, e.g. Carlsberg Follow customers e.g. Ziton Follow competitors , e.g. NGK Impact of institutions usually not general but

specific, but a few, e.g.• Impact of labour law in India, Egypt• Bureaucracy in Egypt• Visas in South Africa

Page 33

Findings from Cases cont

FDI given opportunity by liberalisation/privatisation

Regional factors in country significant determinants of location e.g. Vietnam, India.

Page 34

Capital Markets

Acquisitions rare because capital markets are not well developed in emerging markets. Explains differences between South Africa and others

Privatisation, capital market development and FDI related e.g. Vietnam or India

Need “supply” of acquisition targets

Page 35

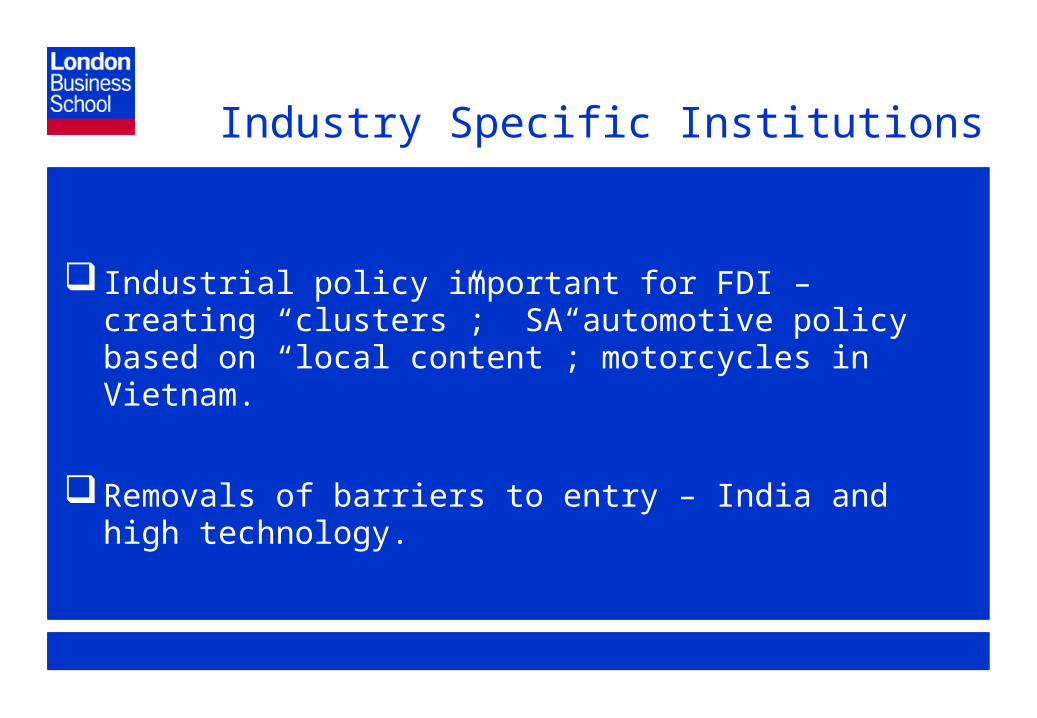

Industry Specific Institutions

Industrial policy important for FDI – creating “clusters”; SA automotive policy based on “local content”; motorcycles in Vietnam.

Removals of barriers to entry – India and high technology.

Page 36

Conclusions From Research

FDI to emerging markets increasing and likely to do so even more

Firms solve the problem of how to operate in institutionally weaker environments – size, entry mode

Global strategies are important but so are regional ones

Spillover benefits greater from acquisitions but integration into global market also relevant

![Curso de Aperturas Abiertas. Panov & Estrin [63]](https://img.pdfslide.net/doc/110x75/577cdbb11a28ab9e78a8d1db/curso-de-aperturas-abiertas-panov-estrin-63.jpg)