Embed Size (px)

Citation preview

Connecticut Pro Bono LITC Project Training for LITC Volunteers

PART I: WORKING A LITC CASES .......................................................................... 1

SUBSECTION A: TYPES OF CASES AND ISSUES VOLUNTEERS WILL BE ASKED TO HANDLE...................................................................................................... 1

A. EXAMINATIONS (AUDITS)........................................................................................... 2 B. EIC CERTIFICATION PROGRAM................................................................................ 3 C. EMPLOYEES VS. INDEPENDENT CONTRACTORS........................................................ 4 D. NONFILERS .............................................................................................................. 4 E. INNOCENT SPOUSE RELIEF ....................................................................................... 5 F. CANCELLATION OF INDEBTEDNESS INCOME ............................................................ 5 G. COLLECTION OF TAX DEBT...................................................................................... 6 H. UNITED STATES TAX COURT LITIGATION ................................................................ 7

SUBSECTION B: WORKING WITH LOW-INCOME TAXPAYERS ................... 7

A. CHARACTERISTICS OF LOW INCOME TAXPAYER POPULATION................................. 9 B. SKILLS FOR INTERVIEWING LOW-INCOME TAXPAYERS.......................................... 14

SUBSECTION C: FAMILY STATUS AUDITS......................................................... 24

A. REVIEW OF RULES FOR CLAIMING HEAD OF HOUSEHOLD FILING STATUS.............. 24 B. REVIEW OF RULES FOR CLAIMING DEPENDENCY EXEMPTIONS. (SEE ALSO IRS

PUBLICATION 501, WWW.IRS.GOV) ................................................................................ 27 C. REVIEW OF RULES FOR CLAIMING EARNED INCOME CREDIT (SEE ALSO IRS

PUBLICATION 596 WWW.IRS.GOV) ................................................................................. 32 D. OVERVIEW OF RULES FOR CLAIMING CHILD TAX CREDIT ........................................ 34 E. POINTS AT WHICH A TAXPAYER’S CLAIM OF EIC, HOH OR DX MIGHT BE

QUESTIONED: ................................................................................................................. 35

Part I: Working a LITC Cases

Subsection A: Types of Cases and Issues Volunteers will be asked to handle.

As a volunteer, you will most probably be involved in assisting low-income

taxpayers in the following kinds of cases: (1) audits (examinations) of past-filed

tax returns, especially returns on which the client claimed head-of-household

filing status, dependency exemptions for children, the child tax credit, and/or the

earned income tax credit; (2) EIC Certification or recertification; (3) examinations

of returns on which clients reported income and expenses from being self-

1

Connecticut Pro Bono LITC Project Training for LITC Volunteers employed; (4) requests for advice by a client who has not filed a tax return for

prior year(s) and need to do so now (e.g., wants to become a citizen, wants to

buy a home, or needs to show returns to borrow money), so-called Voluntary

Disclosure; (5) clients who want to get relief from a joint income tax liability of a

former spouse by claiming innocent spouse relief; (6) clients who have been

notified by the IRS that they have income after a debt has been cancelled; (7)

clients who are facing collection action by the IRS (filing of a tax lien or issuance

of a levy); and (8) litigation before the United States Tax Court.

Below are short descriptions of these categories. Today’s training will

touch on many of them in much more detail.

A. Examinations (Audits)

Low-income taxpayers are often the targets of examinations (audits) by

the Internal Revenue Service as a result of increased scrutiny of the earned

income credit (“EIC”), a refundable credit that is available to low-income working

taxpayers. As a result, many of the clients asking for assistance will be in

various stages of having the IRS review filed tax returns or the IRS freezing a

current refund because of the disallowance of the EIC in a prior year. Most of

the reviews are done by correspondence, which may test your patience. This

training will give you some practical advice for handling the more frustrating parts

of these kinds of audits. See Appendix 1, Handouts for EIC Representation.

2

Connecticut Pro Bono LITC Project Training for LITC Volunteers B. EIC Certification Program

The IRS has been heavily auditing taxpayers who claim the earned

income credit (EIC). These audits involve sending IRS notices, which are very

difficult for literate persons to understand never mind low literacy, ESL or Limited

English Proficiency (LEP) taxpayers. As a result of that audit activity, the IRS

estimates that as high as 25% of the taxpayers who claim the EIC may not be

entitled to it. To verify this, the IRS is piloted a program aimed at having

taxpayers who claim children for purposes of the EIC prove that they lived with

them for more than 6 months during 2004. This is one of the statutory

requirements for the EIC. Under the program, 8,200 randomly selected taxpayers

in Hartford County (4,100 in the City of Hartford alone) were asked to send in

form affidavits or third party letters to the IRS. The IRS would not release the EIC

portion of the selected taxpayers’ refunds unless the proper documentation was

submitted and accepted. A report on the effect of the program indicates that the

certification requirement in fact discouraged taxpayers who may have been

eligible from actually claiming the EIC. Any taxpayer who was included in the

program sample group who either did not submit sufficient documentation or did

not participate faces problems for 2005. If the taxpayer files and claims the EIC

for 2005 (which is likely to happen because the taxpayer will think that since he

or she has not been contacted this year to certify that everything is fine) will be

disallowed the EIC for 2005 and most likely will be audited. This is where

representation may make a very large difference.

3

Connecticut Pro Bono LITC Project Training for LITC Volunteers C. Employees vs. Independent Contractors

Low-income taxpayers are also often targets of employers who want to

avoid the requirement of withholding taxes and paying FICA. These taxpayers

are often told at the end of the year that the employer will report their “wages” as

self-employment income. This leaves these taxpayers with a large tax liability for

the “self employment taxes” and penalties for not paying estimated taxes.

Sometimes you can help these clients convince the IRS that the employer

misclassified them as a self-employed individual, thereby reducing their total tax

liability. See Appendix 2, Handouts for Independent Contractor/Self-Employed

Clients

D. Nonfilers

Low-income taxpayers are often more likely than other parts of the

population to experience personal problems and tragedies, the magnitude of

which may prevent them from filing their tax returns. A large percentage of low-

income taxpayers suffer from physical and mental health issues, which may

require hospitalization and make them unable to prepare and file returns. Also,

low-income taxpayers may move frequently making it difficult to keep necessary

documents to file tax returns. Finally, low-income taxpayers often see

themselves as victims and may lack the education and skills to be able to carry

out what many of us may see as the surmountable task of filing a tax return.

Many of these clients might never catch up with their filing requirements until

some other life event requires them to file. For example, a client may decide to

start a small business to try to get off the public assistance track. To qualify for a

4

Connecticut Pro Bono LITC Project Training for LITC Volunteers small business loan or a bank loan, the client may need to produce tax returns.

Or, a client may need to get financial aid to pursue an education and need tax

returns to apply for the aid. The IRS has a voluntary disclosure policy under that

encourages taxpayers to come forward and file before they are under

examination. See Appendix 3, Handouts for Nonfiler Clients

E. Innocent Spouse Relief

Married taxpayers may elect to file a joint income tax return. Doing so

often qualifies the taxpayers for lower tax rates. However, once a joint return is

filed, any unpaid tax liability or any additional tax liability that the IRS discovers is

the liability of each spouse individually. Spouses who have suffered from

spousal abuse or who are kept in the dark about their husband’s or wife’s tax

cheating may qualify for relief from the joint liability, either in whole or in part. To

do this, a client must file for innocent spouse relief. The path to innocent spouse

relief is fraught with traps for the unwary and good legal representation is often

the difference between success and failure. When a taxpayer who requests

innocent spouse relief is not represented early in the process, he or she may still

have a chance litigating a denial and you may be asked to get involved at this

stage. See Appendix 4, Handouts for Clients Claiming Innocent Spouse Relief

F. Cancellation of Indebtedness Income

Many low-income taxpayers are victims of predatory lending. These

lenders often foreclose on debts, leaving clients not only with worse credit ratings

but income in the form of cancellation of indebtedness. This is reported to the

5

Connecticut Pro Bono LITC Project Training for LITC Volunteers IRS and the IRS then makes an assessment of additional tax. For example, a

client may have been lured into a car loan with very little down, but with an

interest rate that makes it impossible to make payments over 36 months. If the

client defaults on the loan and the car is repossessed, the value of the car at the

time of repossession is often no where near the loan balance. The lender will

then issue a Form 1099 to the client when tax filing season rolls about, showing

cancellation of indebtedness income of the difference between the payoff amount

of the loan and the value of the car. However, a very little known defense to this

is showing that at the end of the year in which the debt was cancelled, the client

was insolvent. Proving insolvency will relieve the client of all tax liability. Also, if

a client files for bankruptcy and the debt is discharged, then the client does not

have cancellation of indebtedness income.

G. Collection of Tax Debt

Collection of tax debts is only one of many times that a low-income

taxpayer is pursued for past debts. As a result, your client, out of fear or

embarrassment, may ignore the preliminary notices sent by the IRS. Such

notices usually give taxpayers ways to try to work out payment of the debt or

even challenge the debt. Instead, you may first get involved when a client has

received notice that a lien has been filed or that his or her wages or bank account

will be levied. In 1998, Congress passed measures that give taxpayers some

due process rights when it comes to collection of tax debts. You will learn about

these and ways to help clients who face economic hardship to get immediate

6

Connecticut Pro Bono LITC Project Training for LITC Volunteers relief from IRS collection measures. See Appendix 5, Handouts for Clients

Seeking Collection Help.

H. United States Tax Court Litigation

Finally, many low-income taxpayers are unable to resolve their matters

before the issuance of a notice of deficiency. With this notice, they are told of

their rights to litigate before the United States Tax Court without having to pay

the tax debt first. Those taxpayers who exercise these rights will file petitions

(complaints) with the Tax Court and set in motion litigation. Tax Court litigation is

very unique. However, like many other forms of litigation, settlement is very much

encouraged and we will discuss how to go about doing this. See Appendix 6,

“Representing Clients Before the United States Tax Court” prepared by The

Community Tax Law Project and reproduced for educational purposes and use

by New Hampshire Pro Bono Referral Project volunteers.

Subsection B: Working with Low-Income Taxpayers

As an attorney, most of your professional life is spent interviewing people

(clients, witnesses, experts, etc.), communicating (either verbally or in writing),

and assisting clients. Much of what you do for the pro bono project will be the

same. What will be different, however, is that for many of you interviewing,

communicating and counseling low-income taxpayers will present challenges that

you may not have faced.

7

Connecticut Pro Bono LITC Project Training for LITC Volunteers

The model of lawyering that is most practiced today, and the one that is

generally taught in United States law schools, is the model of client-centered

counseling. Under this model, a lawyer and client collaborate in a client’s

representation. The lawyer engages the client in the process, understanding

that the client has a better command of the facts, that it is the client’s goals and

objectives that must be met, not the lawyer’s ego, and that full disclosure makes

for the best representation.

Under this model, gathering facts from a client involves using both open-

ended and closed-ended questions in a way that obtains as much of a time-line

as possible. It also involves taking the “temperature” of the client each time you

meet to see if the client’s situation has changed or his or her goals have

changed. Characteristics of a client that make it difficult of a client to develop a

rapport with you, to articulate or advocate his or her views, or to understand your

“language” all impact on how effectively you can engage in effective fact

gathering.

Under this model, there is a difference between advising a client and

counseling a client. Counseling involves empowering the client and assisting

them in making a decision. Advising the client involves telling them what you

would do in a similar situation or a discrete piece of advice. Again,

characteristics of a client that make it difficult for the client to choose will frustrate

counseling.

At the risk of stereotyping, there are characteristics common to low-

income taxpayers that will test some of your assumptions about your client’s

8

Connecticut Pro Bono LITC Project Training for LITC Volunteers

ability to understand, to make choices, and to follow through. This part of the

training will provide you with a window into the lives of low-income taxpayers that

hopefully will help you be more effective fact gatherers, communicators and

counselors.1

A. Characteristics of Low Income Taxpayer Population

The following is a list of certain characteristics that are more frequently

found in low-income taxpayer population.2 It does not mean that your clients will

exhibit some or all of these characteristics and does not mean that some of the

characteristics are not found in middle-income and high-income taxpaying

populations. Below we will discuss in more detail how these characteristics might

impact you when you go about gathering information from your client or

counseling him or her.

1. Many low-income taxpayers do not have strong organizational skills.

Many low-income taxpayers are low-income because of a lack of

education or undiagnosed or treated learning disabilities. This may make it

difficult for them to organize documents or their thoughts. Further, many low-

income taxpayers live hectic lives, primarily focused on meeting the basic needs

for them and their families. Many have other competing demands on their time-

keeping a shelter over their heads, feeding their family, coping with substance

1 This part of the training has been taken from training materials that Diana Leyden assisted in developing to train IRS customer service representatives in the Kansas City Mo. Service Center (Campus) who were handling the EIC certification process. 2 I recommend reading the following two books to help understand low-income taxpayers: Nickled and Dimed, On (Not) Getting By in America, Barbara Ehrenreich; The Working Poor: Invisible in America, David Shipler. ;

9

Connecticut Pro Bono LITC Project Training for LITC Volunteers abuse or mental health problems, getting medical care without medical

insurance- demands that may not be as pressing or difficult to handle for more

affluent taxpayers. So, requests to obtain documents and organize them may

not be fulfilled and you may need to be more proactive in doing so.

2. Low-income taxpayers do not keep good records.

Many low-income taxpayers experience disruption in their housing. They

may be homeless for a period of time. They may move frequently. They may be

fearful of or distrust the government and for that reason, do not keep records.

Thus, in your job of substantiating tax benefits or claims, where documentation is

essential, you may not be able to rely upon you client to produce the

documentation. You may need to contact third parties and to do so, may need to

secure authorization from you client so the third party will share the client

information with you.

3. Low-income taxpayers keep irregular work hours.

Often, to make ends meet, low-income taxpayers cobble together several

low-paying jobs. These jobs may require them to work odd shifts or be on call.

Many employers of low-paying jobs do not allow employees time to make calls or

to use work phones. This may make it difficult to reach them by phone or

schedule appointments during a normal work day.

4. Low-income taxpayer may delay in getting in touch with you.

Experience has shown that there are often significant delays in

communicating with low-income taxpayers. Even though the client may have

10

Connecticut Pro Bono LITC Project Training for LITC Volunteers contacted the Pro Bono Project coordinator and said that they had a serious

problem in need of immediate attention, you may find that you need to make

several calls before the client and you speak. Why? It may be difficult for the

taxpayer to get to a phone due to irregular work hours, or it may be difficult for

the client to get transportation or child care to attend a meeting. Be persistent

and creative. Is it possible for the client to bring a child in and have the child stay

in a nearby room with a coloring book or toys? Can the client bring a relative or

friend to watch the child at your office? Can you meet in a local library in a

closed room for the first meeting if your office is not on a bus line?

5. Low-income taxpayers often experience financial difficulties.

Living at the edge of poverty often means that there are necessary

choices- foods today or the phone or electric bill. Phone service may be

discontinued, leaving you no way to contact your client. Some of the

documentation you will need to prove the family status issues may not be

available because of nonpayment of bills. Concern and stress over keeping a

family fed and clothed may make it difficult for a client to focus on his or her

matter.

6. Low-income taxpayers rely more heavily on cash to pay bills.

Low-income taxpayers may not have bank accounts for a variety of

reasons. They may have bad credit, may have misused checking accounts in the

past, or may be distrustful of banks. This will make obtaining proof of support and

expenses for family status cases or for financial statements for offers in

11

Connecticut Pro Bono LITC Project Training for LITC Volunteers compromise difficult. You may also find that these clients are the victims of

predatory lenders, using paycheck cashers and paying exorbitant fees for money

orders.

7. Low-income taxpayer may live in non-traditional housing.

Low-income taxpayers may not be able to afford apartments without

sharing the expenses with friends and relatives. Language problems (either not

speaking English as a first language or having low-proficiency in English) and

cultural norms concerning extended families may be behind the nontraditional

housing patterns. This may make it difficult to prove your client actually lives in

an apartment for purposes of the earned income credit because his or her name

is not on the lease and the landlord does not know he or she resides there. Or,

due to the nontraditional nature of the housing, records for the client’s children

may not reflect the actual address. For example, your client may live with her

children in a homeless shelter, but she is too embarrassed about that to list that

address in the children’s school records.

8. Low-income taxpayers use free medical clinics and emergency rooms for

medical care.

When the need to document health care is necessary, it may be difficult to

find a primary care physician. Low-income taxpayers may rarely be seen by the

same physician because of the lack of health care insurance. An overstressed

emergency care resident or physician may not get the correct information about

12

Connecticut Pro Bono LITC Project Training for LITC Volunteers the child of a low-income taxpayer, but that may be one of the only forms of proof

of the child’s address.

13

Connecticut Pro Bono LITC Project Training for LITC Volunteers

9. Low-income taxpayers rely upon oral testimony in other areas for purposes of

proving entitlement to benefits.

Oral testimony is a primary means for low-income taxpayers to establish

eligibility for public assistance or social services. In a tax audit, oral testimony

may not be allowed or have any credibility. Also, rational and logical proffers of

proof- affidavits from neighbors or friends- may not be accepted by the IRS,

causing you and your client high levels of frustration.

B. Skills for Interviewing Low-Income Taxpayers

The focus of this part of the training session will be on identifying and

understanding the key skills that will make you more effective in gathering

information from a low-income taxpayer.

1. Overview of Interviewing Skills and Techniques: There are 3 main goals of

interviewing:

a. Developing a rapport and trust with the Client. Getting a client to

relax and feel able to trust you is the key to obtaining accurate information

and understanding the client’s goals. When you are representing a client

with a different economic and social background, you will need to

recognize what barriers (inhibitors) may make it difficult to develop a

rapport. You will need to use some tools (facilitators) to help overcome

these barriers.

14

Connecticut Pro Bono LITC Project Training for LITC Volunteers

b. Maximizing Information Gathering. With a paying client, the client has

an incentive to get you the information as efficiently as possible to avoid

large legal fees. With a pro bono client, you need to have an incentive to

get the information as efficiently as possible because you client may not

be able to afford to meet with you as often as you like.

c. Obtaining a general idea of the client’s problem and or questions

in an efficient manner.. Low-income taxpayers may lack good

communication skills or be distrustful of professionals. This may make it

difficult to get a general idea of the client’s problems or his or her

questions. You may need to use open-ended questions rather than close-

ended or leading questions to get the information you need. Also, many

low income taxpayers have difficulty getting off time from work to attend

meetings and so you may need to be more efficient in obtaining

information during a face-to-face meeting or may need to develop different

skills for obtaining information by telephone.

2. Developing Rapport:

Developing a rapport and/or trust there are two factors at work: Inhibitors

(things that work against this goal) and facilitators (things that help reach the

goal.)

a. What are kinds of inhibitors?

15

Connecticut Pro Bono LITC Project Training for LITC Volunteers

(i) Language (Can you communicate with the taxpayer? Does the

taxpayer speak understandable English?

(ii) Trauma on the part of the taxpayer. Perhaps dealing with the IRS is

extremely frightening because of prior bad experiences with government officials.

Perhaps the tax problem is the result of personal trauma- e.g., a taxpayer

claiming innocent spouse relief may be a domestic violence victim. Tell them that

you are there to help them.

(iii) Embarrassment. Perhaps they were formerly a middle-class

taxpayer with a good job, who fell upon hard times. Confessing that they are

now low-income and that they are on public assistance may be extremely

embarrassing. Tell them that it is ok and develop a rapport. If possible, try to

assure them by explaining a time in your life when you were embarrassed about

asking for help.

(iv) Seeing you, the attorney, as an authority figure. Keep your voice

should be soft and friendly.

(v) Culture, age, social or dialect barriers. Proper attitude is all it takes

to overcome this barrier.

(vi) Memory. Clients, who are substance abusers or even survivors of

chemotherapy, may have memory trouble. Develop mechanisms for helping the

client relate to time. For example, if a client has children, try using the grades the

16

Connecticut Pro Bono LITC Project Training for LITC Volunteers children were in during the tax years as a trigger for remembering what

happened during those years.

(vii)`Fear. Keep assuring the client you are there to help and that you are

bound to keep their information confidential.

b. What are facilitators?

(i) Showing empathy and respect. Sympathize with your Client. Put

yourself in his or her shoes. What would you do differently?

(ii) Active Listening. Be patient and understanding and listen with your

eyes and heart as well as your ears.

(iii) Speak Slowly and Use Less Complex Language. Speak “their

language” if you can. Use less complex language. For example,

instead of using the verb “verify” us “prove” or “show”.

(iv) Ask clear and well-organized questions. Be as detailed as

necessary to obtain the heart of the problem or question.

(v) Exhibit patience. Develop techniques for defusing your frustration.

Practice phrases that might be kinder ways of conveying frustration.

E.g., I realize that this is very upsetting for you and you really want

your refund. I am annoyed at the IRS too. Together I think we can

convince them you are due your refund. But to do that I really need

your help. We must get [name of document.] I know you have tried.

Let’s put our heads together and see how we can work together to

get it.

17

Connecticut Pro Bono LITC Project Training for LITC Volunteers c. What is active listening?

(i) Listening to what the client has said before responding.

(ii) Restating an answer to see if what your heard is what the taxpayer intended to say.

d. Exercise to show active listening- variation on 20 questions. We will do an

exercise with audience participation aimed at showing the advantages of

active listening and open- and closed-ended questions.

e. Identifying common inhibitors of low-income taxpayers that may make information

gathering more challenging:

(i) Mental health issues

(ii) Literacy issues-both inability to read and to comprehend

(iii) Con artists types

(iv) English as a second language

(v) Transiency

(vi) Rigid work schedules

(vii) Low-self esteem and inability to be assertive

(viii) Many other problems take center stage-financial, social, and

emotional.

(ix) Fear of government

(x) Anger and feeling of being “had by the system”

18

Connecticut Pro Bono LITC Project Training for LITC Volunteers

f. Identifying facilitators that make information gathering with low-income

taxpayers easier:

(i) Active listening/sympathetic ear.

(ii) Talking slowly.

(iii) Empathy

(iv) Being polite

(v) Validating concerns

(vi) Tone of voice

(vii) General attitude of wanting to help

(viii) Humor

(ix) Refraining from being or coming across as judgmental

3. Communicating

The biggest mistake that is made in trying to communicate is that the

communicator makes unarticulated assumptions. Many times this is more

pronounced when a technical subject is involved, such as taxes. Another

big mistake, especially common with telephonic communications, is the

misinterpretation of the tone and/or responses by a client. The inability of

the communicator to observe body language reduces considerably the

ability to read the recipient of the communication. Add to these problems

gaps due to cultural or social differences between a communicator and a

client and there are many chances for miscommunication. This part of the

presentation will identify some common problems you face in

communicating with low-income taxpayers and some techniques for

19

Connecticut Pro Bono LITC Project Training for LITC Volunteers overcoming those problems. There are 4 steps to being effective when

communicating with people with different cultural or social backgrounds

than you.

a. First, identify similarities and differences with the Client.

(i) For example, is the client a single parent? Are you a

single parent or married?

(ii) Does the client speak English as a first language? Do

you?

(iii) Does the client live in a rural or urban area? What kind

of area do you live in?

(iv) Is the client young or old? Male or female?

b. Second, identify the client’s behaviors and responses to your

questions or comments. (Does the client know about the U.S. tax

systems? Does he know the consequences for not complying with

IRS notices? Does the client react to sarcasm?)

c. Third, identify cultural and/or social beliefs or habits that the

client subscribes to, especially with respect to responding to the

government and how they are different from your beliefs and

responses.

d. Fourth, recognize your biases and stereotypes and take action to

reduce stress that might trigger these- for example, if a client does

not answer a question the 2nd or 3rd time you ask it, have a

20

Connecticut Pro Bono LITC Project Training for LITC Volunteers

mechanism for distressing- counting to 5, humor, excuse yourself

from the room for a moment.

e. Practical Advice.

(i) Recognize the tremendous gap between your level of

education/expertise in tax and the level of education of the

client.

(ii) Avoid language that implicates authority.

(iii) Practice different ways of explaining tax concepts.

(iv) Keep an open mind- think of different reasons for

responses.

(v) Don’t be reluctant to reword responses to make sure the

client understands what you are saying.

(vi) Invite questions by the client and invite him or her to tell

you when s/he is confused. (If you have any doubts that the

client knows or understands, ask the client to tell you their

understanding of the conversation)

(vi) Be patient (Always)

21

Connecticut Pro Bono LITC Project Training for LITC Volunteers

4. Counseling

One of the most important roles you will play is assisting a low-income

taxpayer to develop a way to make an informed decision about how to proceed

and to develop a game plan for following through. 6 steps to helping:

a. Identify the problem and make sure that both you and the client see the same problem.

b. Evaluate with the client the information you have gathered.

c. Cooperate to generate potential solutions to the problem.

d. Encourage the client to evaluate each potential solution.

e. Encourage the client to choose the best solution.

f. Develop a plan to act on the solution.

g. Practice Tips.

(i) Explain what kind of information a particular type of

document is trying to prove.

(ii) Brainstorm with the taxpayer about alternative forms of

acceptable proof.

(iii) Explain why certain documents might have to be

combined with other documents to prove eligibility- e.g., a divorce

order might prove that the taxpayer has custody of the parties’

minor children, but would need to be coupled with a marital

dissolution agreement or parenting plan listing the specific names

of the children or school records might show residence for part of

22

Connecticut Pro Bono LITC Project Training for LITC Volunteers

the year, but would need to be coupled with the school records for

the other part of the year to meet the residence requirement.

(iv) If a client says he or she can’t get a particular type of

document, use empathy and try to determine what the barriers to

getting the document are and whether such barriers can be

overcome, especially if the client can get assistance from a trusted

advisor. Be prepared to suggest alternative sources of proof.

(v) Be flexible in setting guidelines.

(vi) Be aware of cultural differences in meanings of

documentation- if you are not clear that a client has the same

meaning as you as to what a document is, ask the client to explain

what he or she thinks it is.

(vii) Identify and show sensitivity to barriers, whether or not they

seem real to you. For example, if a client says they cannot get a

school record or affidavit from the school, using the parallel

universe technique, think about possible reasons why and discuss

them with the client. A low-income taxpayer may not have

registered a child in the school using his address because he lives

outside of the school district. Can the client get an affidavit from

the person whose address he used about the fact that the client

picks up the child everyday from school.

23

Connecticut Pro Bono LITC Project Training for LITC Volunteers Subsection C: Family Status Audits

A typical low-income taxpayer with children will file a tax return claiming

head of household filing status, dependency exemptions for children, the child

tax credit and the earned income credit. Such a return is likely to be audited

(examined) for two reasons: (1) it is part of the ongoing investigation into whether

the earned income credit has a higher fraud claim rate that other tax deductions

or credits; or (2) some other taxpayer, either related or not, has claimed the same

child or children as dependents or for purpose of the EIC.

To help you assist clients facing such audits, it is first useful to know the

rules for claiming these tax benefits. Second, it is useful to understand the

process by which the IRS reviews a return and processes information submitted

on behalf of a taxpayer. Third, it is useful to know some tried and true methods

for obtaining proof that will more likely than not be accepted by the IRS. Fourth,

and finally, it is important to know what appeal rights you have and how to use

the Taxpayer Advocate in these kinds of audits.

The following discussion of the rules apply to years PRIOR TO 2005.

Most of the cases you will be handling involve prior years.

A. Review of rules for claiming Head of Household Filing Status.

If a taxpayer is able to claim head of household filing status, then s/he will

get a larger standard deduction. This can help considerably in reducing the

taxpayer’s taxable income to zero and is therefore an important benefit.

Requirements for claiming Head of Household:

24

Connecticut Pro Bono LITC Project Training for LITC Volunteers 1. As of December 31st of the tax year, taxpayer must be either (1) unmarried

or divorced; or (2) if still legally married, not have lived with the spouse for any

time during the last 6 months of the year (July1-December 31);

2. Have maintained a home as the principal place of abode of either a

biological (or adopted) child or a person who the taxpayer can claim as a

dependent and that child or dependent lived there for MORE THAN 6 months

during the calendar year;

3. Paid with his or her own funds (not public assistance; not child support)

MORE THAN 50% of the total of the following costs of maintaining the home for

EACH and EVERY MONTH during the calendar year:

Rent (if client owns the house, ONLY the mortgage interest, not

principal)

Utilities (e.g., gas, electric, water, sewer, phone (cell phone if that is

the only phone), sometimes cable;

Groceries (not dining out)

Repairs made by client to the home and not reimbursed by landlord

Homeowners or renters insurance

Property taxes.

Special Rules/Special Circumstances:

Temporary Absence: If a child or dependent for whom the house is maintained is

temporarily absent, it will not count against the 6 month period. Examples: Child

attends school; child is in the military; child is in detention facility; child is

hospitalized.

25

Connecticut Pro Bono LITC Project Training for LITC Volunteers Household within a House. Courts have held, and now the IRS accepts, the rare

instances where more than one family lives within one physical home. It takes a

lot of documentation, but is it possible to prove that the portion of the house

expenses allocated to the physical space occupied by one family are the correct

starting point for total expenses. Example: Taxpayer and her child live in a 2

bedroom apartment with a relative. The relative does not care for the child and

has a different work schedule. You may be able to prove that one half of the

apartment is the proper household and look only to that portion of the expenses.

How does this help? If all the expenses paid are considered the relative might be

considered as paying for more than 50% of the expenses. If only the taxpayer’s

expenses are considered, it will probably be easier to prove that the taxpayer

paid for more than 50% of his or her allocable expenses.

What if Client cannot get records for every month of the year? May be able to

combine an affidavit of the client with partial records to prove that the records

approximate what every month’s expenses were and that he or she paid them for

every month.

What if Client lives in subsidized housing? For head of household, the actual

amount PAID counts as the expense. This creates a difference between client

living in low-income housing and Sec. 8 housing. In low-income housing, a client

pays below market rate, but the difference between market and what the client

pays is not paid by any third party. So, in that case, the total amount the client

pays is the total amount paid and the client pays 100% of the rent.

26

Connecticut Pro Bono LITC Project Training for LITC Volunteers In Section 8 (HUD) housing, however, there are two payments- amounts the

client pays based on his or her income and an amount paid by the federal

government to the landlord. Often when section 8 housing is involved, the client

will NOT be found to pay for more than one-half of the costs of maintaining the

home if he or she pays for less than 50% of the rent.

See Appendix for charts and sample spreadsheets to help organize facts in Head

of Household cases.

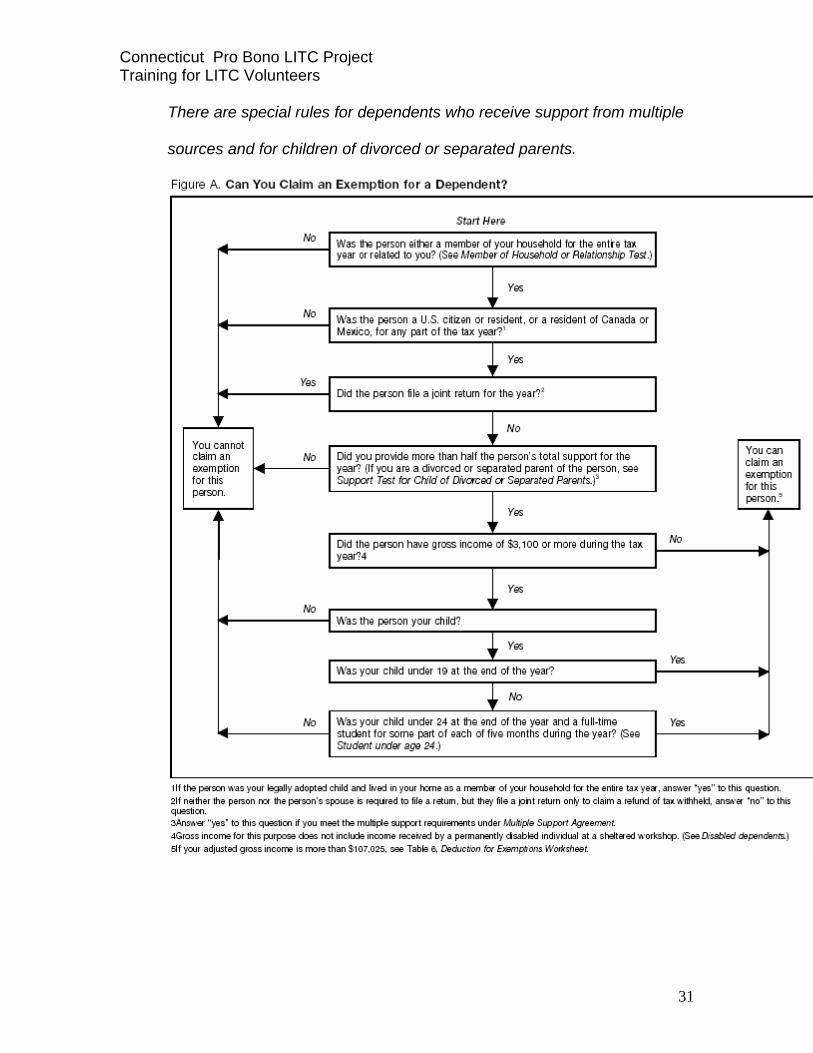

B. Review of Rules for claiming Dependency Exemptions. (See also IRS Publication 501, www.irs.gov)3

Like the head of household filing status standard deduction, taxpayers

reduce their taxable incomes for each dependency exemption claimed. A

taxpayer will automatically qualify for an exemption for him or herself and if a joint

return is filed, for the spouse. To claim a dependency exemption for other people,

however, all of the five dependency tests must be met. (*A taxpayer cannot claim

a person as a dependent if the person can be claimed as a dependent on

another taxpayer's return):

1. Relationship/ Member of Household Test. A claimed dependent

must either (a) be a relative as described below; OR (2) be a person who lived

with the taxpayer for the ENTIRE calendar year as a member of the household.

a. Relationship Test

3 The rules for claiming a dependent changed some what for tax years 2005 and after as a result of the adoption of a uniform definition of qualifying child. At the time of publication of this training materials new training materials for teaching about this had not been completed. Further, what is taught in these materials will apply to tax years 2004 and before, the focus of many cases you will be handling as the IRS audits prior years.

27

Connecticut Pro Bono LITC Project Training for LITC Volunteers

Taxpayers will meet this test for the following relatives if the

relatives meet the requirements of the relationship test:

• child

• parent

• brother/sister

• stepparent

• stepchild

• stepbrother/stepsister

• half brother/half sister

• grandparent

• grandchild

• son-in-law/daughter-in-law

• mother-in-law/father-in-law

• brother-in-law/sister-in-law

If related by blood, relatives also include

• uncle/aunt and

• niece/nephew

Other considerations:

• Cousins do not meet the relationship test.

• Relatives do not have to be members of the taxpayer's household.

• Relationships established by marriage are not ended by death or

divorce. For example, a daughter-in-law is a relative to her in-law parents

even after the death of their son (her husband).

28

Connecticut Pro Bono LITC Project Training for LITC Volunteers

b. Member of Household Test

Taxpayers will meet this test for any person who is not a relative

under the above rules who lives with the taxpayer as a member of

the household for the entire year.

• The dependent does not have to be related to the taxpayer.

• The dependent must live with the taxpayer all year except for

temporary absences. (Temporary absences include attending

school, taking vacations, and staying in the hospital.)

• The relationship between the taxpayer and the dependent must

not violate local laws

2. Citizen or Resident Test. Taxpayers will meet this test for persons

who are, for some part of the year,

• U.S. citizens or residents, or

• Residents of Canada or Mexico. (Odd rule and is strictly applied.

E.g., a resident of Guatamala does NOT qualify as a dependent,

but a resident of Mexico does.)

3. Joint Return Test. Taxpayers will meet this test for persons who are:

• unmarried,

• married but do not file a joint return, or

• married and file a joint return only to claim a refund of withheld

tax; neither would have a tax liability on separate returns; neither the

dependent nor spouse can claim personal exemptions on their joint return.

29

Connecticut Pro Bono LITC Project Training for LITC Volunteers

4. Gross Income Test. Taxpayers will meet this test for persons whose

gross incomes are less than the exemption amount. In 2004, the

exemption amount was $3,050.

Gross Income

• is all taxable income in the form of money, property, and services;

• includes unemployment compensation and certain scholarships; and

• does not include welfare benefits and nontaxable Social Security

benefits.

The gross income test does not apply if the taxpayer's child is under

• 19 years of age as of December 31st of the tax year, or

• 24 years of age as of December 31st of the tax year and was a full-time

student during that tax year.

5. Support Test. Did the taxpayer provide more than half of a person's

total support for the entire year? Total support items include:

• food, clothing, shelter, education, medical and dental care, recreation,

and transportation; and

• welfare, food stamps, and housing provided by the state.

Compare the dollar value of the support provided by the taxpayer with the

total support the person received from all sources.

The gross income test considers the dependent's taxable income.

The support test considers all income, taxable and nontaxable.

30

Connecticut Pro Bono LITC Project Training for LITC Volunteers

There are special rules for dependents who receive support from multiple

sources and for children of divorced or separated parents.

31

Connecticut Pro Bono LITC Project Training for LITC Volunteers

C. Review of Rules for Claiming Earned Income Credit (See also IRS Publication 596 www.irs.gov)

The earned income credit, or EIC, is a refundable credit for workers who

meet certain requirements and file a tax return. This means that if a taxpayer

owes no tax, but qualifies for the EIC, the entire amount of the EIC is issued as a

tax refund. Persons with or without a qualifying child may claim the EIC, but

persons with so-called qualifying children get a larger credit.

For tax year 2004, the maximum credit is $2,604 for persons with one

qualifying child, and $4,300 for persons with two or more qualifying children.

The maximum credit is $390 for persons without a qualifying child. To claim the

earned income credit, the taxpayer must:

1. Have earned income. For 2004, earned income includes all

income from employment, but only if it is includible in gross income. Examples of

earned income are wages, salaries, tips, and other taxable employee

compensation. Earned income also includes net earnings from self-employment.

Earned income does not include amounts such as pensions and annuities,

welfare benefits, unemployment compensation, worker's compensation benefits,

or social security benefits. (For tax years before 2002, the definition was

different, so you must consult the Internal Revenue Code to determine if certain

payments are included in earned income.)

2. Must have a valid social security number (not ITIN) for the

taxpayer, taxpayer spouse if filing a joint return, and all qualifying

children.

32

Connecticut Pro Bono LITC Project Training for LITC Volunteers

3. Must file a joint return if married. A taxpayer who is married but who

has lived apart from his or her spouse all of the last 6 months of the tax

year, may be considered as “not married” even if he or she is not

divorced or separated and eligible to claim the EIC if he or she files

head of household. To do this, however, see below for rules regarding

head of household.

4. Must not have investment income of more than statutory

limit.($2,650 for 2004) Investment income includes taxable interest,

tax exempt interest, dividend income, capital gain net income, certain

income from rents or royalties, and certain income from passive

activities. It does not include gains from selling business assets.

5. If claiming children as qualifying children, must be able to show:

a. Age- Child must be younger than 19 as of December 31st of

the tax year, unless the child is a full-time student (in which case the child

must be under the age of 24 at the end of the tax year) or completely

disabled.

b. Relationship- Child must be the biological or adopted child

of the taxpayer, sister, brother, stepsister, stepbrother or a descendent

(e.g., niece or nephew) that the taxpayer treats as his or her own child, or

if a “foster child” must have been placed with the taxpayer by an

authorized placement agency.

33

Connecticut Pro Bono LITC Project Training for LITC Volunteers

c. Residency- The child must have lived with the taxpayer for more than

6 months- i.e., 183 days or more. The taxpayer and child need not live

in a house or apartment- time spent in a shelter or with relatives

counts. The exact counting of days together may be very important for

this part of the rule. If the child lives with both a taxpayer and another

person to whom the child meets the qualifying child test. (Special rules

apply to military personnel.) Temporary absences from the home,

such as due to illness, education, military service, do not count as time

away from the home.

6. If not claiming qualifying children:

a. Must be 25 or older, but under age 65 at the end of the tax year.

b. No one else can claim the taxpayer as a dependent.

c. The taxpayer’s principal place of abode must have been in the U.S.

for more than half of the tax year. (Puerto Rico is NOT considered to be the U.S.

for purposes of this test.)

D. Overview of Rules for Claiming Child Tax Credit Generally, if a taxpayer qualifies for the dependency exemption for a child,

then the taxpayer can claim the child tax credit for that child. For 2004, the

amount of the child tax credit is $1,000 per child and in some cases, some of the

child tax credit is a refundable credit.

34

Connecticut Pro Bono LITC Project Training for LITC Volunteers E. Points at which a taxpayer’s claim of EIC, HOH or DX might be questioned:

1. Upon the filing of a return. If a taxpayer files a return electronically,

the return may not be accepted for electronic riling because the IRS

has an “indicator” (a computer code) indicating that the taxpayer

cannot claim the EIC. This may happen if:

a. For a prior year, the taxpayer’s return was examined and the

IRS disallowed the EIC. This could have happened because

the taxpayer was contacted to provide supporting

information and either did not provide it or provided

insufficient information. It could also happen if the taxpayer

simply did not respond to the request. The IRS would treat

the taxpayer as not eligible for the EIC. If that happens, the

taxpayer is required to “recertify” the next year he or she

claims by filing a Form 8832. To fix this, you can have the

taxpayer submit the form. However, there is a catch 22

because once the taxpayer submits the form, then the

current year’s return will be examined for, among other

things, qualification for the EIC.

b. Someone else claimed a child or children your client claimed

as either dependents or EIC.

c. Your client is listed on a state registry for child support as the

noncustodial parent. Circumstances may have changed and

35

Connecticut Pro Bono LITC Project Training for LITC Volunteers

you client may now be the custodial parent or his or her child

may have lived with him or her for more than 6 months

despite the custodial agreement.

d. Your client or his or her child has an invalid social security

number. Many undocumented workers obtain social security

cards through friends, employers or even flea markets to

enable them to work. They are not, however, eligible to have

a social security number because they do not have green

card immigration status or permanent residency status. In

this case, they are not entitled to claim the EIC.

e. Your client was part of a test group for certification or

precertification an required to submit documents to the IRS

certifying that his or her child(ren) satisfied the residency test

prior to filing his or her return.

2. The IRS has paid out a refund attributable to the EIC, has

subsequently determined that the taxpayer is not entitled to it, and

is now trying to collect it. At this point, if you can establish that your

taxpayer in fact correctly claimed the EIC, you can get rid of this

liability through an audit reconsideration request. See Appendix 8.

3. EIC Certification Program. (See Appendix 1)

F. Practice Points for Obtaining Information to prove these benefits.

36

Connecticut Pro Bono LITC Project Training for LITC Volunteers 1. Residency of a child. You may need to get more than one

document the combined effect of which is to show that a third party’s records had

the same address for the child as the address of the taxpayer. Examples of

types of documents you should obtain:

a. Letters from schools or preschools on the organization’s letterhead

listing the name and social security number (if in the organization’s records) of

the child and indicating the address of record for the child and the period that is

covered. See Appendix # 1 for sample letter.

b. Letters from physician, medical clinics, or hospitals listing the name

and social security number (if in the organization’s records) of the child and

indicating the address of record for the child and the period that is covered. See

Appendix # for sample letter.

c. Leases for apartments showing the address of the apartment and

the name of the taxpayer and all children listed as living in the apartment.

d. Copies of utility bills or other third party providers showing the

taxpayer’s name and address for a period of more than 6 months.

e. Affidavit from other trustworthy third parties attesting to the fact that

a child lived with the taxpayer for a known period- e.g., priests, rabbi, imam,

ministers, day care providers, social workers, etc. Usually the IRS does give any

weight to letters from neighbors or relatives, even though they might be the best

persons to attest to this fact.

2. Relationship and age of the child. If a child was born in the U.S. and

the taxpayer is named as a parent on the birth certificate, the IRS can

37

Connecticut Pro Bono LITC Project Training for LITC Volunteers independently verify this and you do not need to send in a birth certificate. If the

child was born outside of the U.S. and is not a citizen or has a social security

number, you will probably need to submit a copy of the birth certificate from the

foreign country.

3. Divorced or separated parents and dependency exemptions.

Currently, and apparently unbeknownst to many family law practitioners,

provisions in a divorce decree, separate maintenance agreement or separation

agreement have no control over who can claim a dependency exemption.

Instead, the parent who has custody of a child for the greater part of the year can

claim the child as a dependent unless that parent signs a Form 8832 that the

noncustodial parent attaches to and files with his or her return.

3. Costs of Maintaining a Home. Tricky part of this tax benefit is that the

taxpayer must be able to show that for each and every month for the entire tax

year, he or she paid for more than 50% of the costs of maintaining the home.

Costs are defined in the regulations to be limited to the following: rent, if an

apartment or mortgage interest (not principal) if a home, utilities, food consumed

on the premises (i.e., groceries, but not amounts spent eating out), repairs to the

home paid for by the taxpayer, property taxes, and homeowners or renters

insurance. The costs, however, are limited to actual costs. So, if for one month a

taxpayer did not pay utilities or was behind in rent, there is not imputed the usual

costs for that month.

a. The difference between low-income housing and Section 8 housing.

Low-income housing is usually understood to mean housing for which a taxpayer

38

Connecticut Pro Bono LITC Project Training for LITC Volunteers qualifies due to low income and which is housing developed and provided by a

state or municipal housing authority for a below-market rent. In this kind of

housing, there are not any subsidy payments to third parties. The housing

authority is able to rent the units out at below market usually due to favorable

housing credits or loans for this type of housing. The total amount of the rent paid

is the amount paid by the taxpayer/tenant. In contrast, Sec. 8 housing is a

federal subsidy program administered by HUD. Private landlords rent to low-

income taxpayers who pay the landlords part of the fair rental value, the rest of

the fmv rental payment being paid by HUD. In this case, the total fmv is the

amount of the cost of the housing. If the taxpayer pays less than 50% of the fmv,

there may be a difficulty in showing that the total costs of maintaining a home is

paid for by the taxpayer.

b. Less than perfect documentation for all 12 months. Many times

taxpayers may not have receipts for all expenses needed to prove HOH or DX.

You may be able to cajole a company into giving you the records, but be aware

that many utility companies and providers charge for statements. Sometimes

utility companies are willing to give a listing of total payments received without

charge. You may be successful in combining several months’ worth of

statements or receipts with an affidavit by the taxpayer that to the best of his or

her knowledge she incurred similar expenses for the remaining months and

extrapolate to determine yearly totals.

c. The role of public assistance and child support in determining eligibility

for head of household. Both the IRS and courts have held that payments by

39

Connecticut Pro Bono LITC Project Training for LITC Volunteers

40

governments or other parents in the form of assistance (e.g., food stamps, cash

assistance, child support) must be treated as payments made by third parties,

not the taxpayer, for purposes of determining who provides more than one-half of

the support of dependents or who pays for the costs of maintaining a home.