Embed Size (px)

Citation preview

MEMBER

HANDBOOK

State of New Jersey

PublicEmployees’Retirement

System

Department of the TreasuryDivision of Pensions and Benefits

July 2005

Public Employees’ Retirement System Handbook

July 2005 i

FOREWORD

The New Jersey Public Employees’ Retirement System (PERS) Member Handbook has been revisedto incorporate changes to the retirement system made since the last version was published in 1997.The PERS Member Handbook provides a summary description of the benefits of the plan and outlinesthe rules and regulations governing the plan. The PERS Member Handbook should provide you withall the information you need about your PERS benefits. It is as accurate as we could make it, howev-er, if there is a conflict with statutes governing the plan or regulations implementing the statutes, thestatutes and regulations will take precedence. Complete terms governing any employee benefit pro-gram are set forth in the New Jersey Statutes Annotated. Regulations, new or amended, are publishedin the New Jersey Register by the State Office of Administrative Law supplementing the New JerseyAdministrative Code. An online version of this handbook containing current updates is available forviewing over the Internet at: www.state.nj.us/treasury/pensions/persman.htm

Separate addenda booklets have been created for the Law Enforcement Officers (LEO), LegislativeRetirement System, Prosecutors Part, and Workers’ Compensation Judges Part of the PERS, whichare components of the PERS, but have significantly different benefits. These addenda are printed sep-arately from the basic PERS Member Handbook since they affect relatively few members. The adden-da are also available for viewing over the Internet.

If you are unsure of or have questions about any aspect of your PERS benefits, you should ask youremployer representative or a counselor at the Division of Pensions and Benefits about them.

Since this is your handbook, we would appreciate any comments or suggestions for improvement thatyou might have. Please send them to the address listed below. An evaluation form is available for youruse on page 35.

Division of Pensions and BenefitsATTN: Publications Unit

P.O. Box 295Trenton, NJ 08625-0295

Public Employees’ Retirement System Handbook

July 2005ii

FOREWORD .................................................... i

CONTACTING THE DIVISION OF PENSIONS AND BENEFITS .......................... iv

DIRECTIONS TO THE DIVISION OF PENSIONS AND BENEFITS .......................... v

PLAN INFORMATION ........................................ vi

THE RETIREMENT SYSTEM .............................. 1PERS Special Employee Groups ................ 1

MEMBERSHIP ................................................ 1Eligibility Criteria ........................................ 1Optional Membership .................................. 2Factors for Ineligibility ................................ 2

ENROLLMENT .................................................. 2Enrollment/Certification of Payroll Deductions .................................................. 2Proof of Age ................................................ 2Contribution Rate ........................................ 3

MULTIPLE & DUAL MEMBERSHIP .................... 3

TRANSFERS .................................................... 3Intrafund Transfer ........................................ 3Interfund Transfer ........................................ 4

SERVICE CREDIT ............................................ 4

VESTING ........................................................ 4

CREDIT FOR MILITARY SERVICE AFTER ENROLLMENT ...................................... 4

PURCHASING SERVICE CREDIT ...................... 5

TYPES OF SERVICEELIGIBLE FOR PURCHASE .............................. 5

Temporary Service .................................... 5Leave of Absence Without Pay .................. 5Former Membership Service ...................... 5Out-of-State Service .................................. 5U.S. Government Service .......................... 6Military Service Before Enrollment ............ 6Military Service After Enrollment ................ 6Uncredited Service .................................... 6Local Retirement System Service .............. 6

IMPORTANT PURCHASE NOTES ...................... 6

COST AND PROCEDURES FOR PURCHASING SERVICE CREDIT ...................... 6

Purchase Rate Chart .................................. 7Partial Purchases ...................................... 7Estimating the Cost of a Purchase ............ 7Rollover for Purchase Payment .................. 8

LOANS ............................................................ 8Internal Revenue Service Requirements ............................................ 9

SUPPLEMENTING YOUR PENSION .................... 10New Jersey State EmployeesDeferred Compensation Plan .................... 10Local Deferred Compensation Plans .......... 10Supplemental Annuity Collective Trust (SACT) .............................. 10

RETIREMENT .................................................. 11Types of Retirement .................................. 11Service Retirement .................................... 11Early Retirement ........................................ 11Veteran Retirement .................................... 11

Definition of a Veteran ............................ 11Establishing Veteran Status .................... 12

Deferred Retirement .................................. 13Ordinary Disability Retirement .................. 14Accidental Disability Retirement ................ 14

OPTIONAL SETTLEMENTS AT RETIREMENT .............................................. 15

Age Limits on Non-spouse Beneficiaries .......................... 17

THE RETIREMENT PROCESS .......................... 176-8 Months Before Retirement .................. 17

Retirement Estimates .............................. 17Retirement Seminars................................ 18

4-6 Months Before Retirement .................. 18Retirement Applications .......................... 18Disability Retirement Applications ............ 18

Approximately 3 Months BeforeRetirement .................................................. 19

State Health Benefits Program Coverage at Retirement .......................... 19

Approximately 2 Months BeforeRetirement .................................................. 19

Unsatisfied Balances:Loans, Purchase Arrears, Shortages ...... 19

State of New JerseyPublic Employees’Retirement SystemTABLE OF CONTENTS

Public Employees’ Retirement System Handbook

July 2005 iii

Approximately 1 Month BeforeRetirement .................................................. 20

Board Approval ........................................ 20COBRA .................................................... 20

AFTER YOUR RETIREMENT DATE .................... 20Statement of Retirement Allowance ........ 20Retirement Checks .................................. 20Change of Address ................................ 20Direct Deposit/Electronic Fund Transfer .......................... 20Withholding Federal and NJ State Income Tax .............................. 20Federal Income Tax After Retirement ...................................... 21NJ State Income Tax After Retirement ...................................... 21Cost-of-Living Adjustment ...................... 21Social Security ........................................ 22

REDUCTION OR SUSPENSION OF YOUR BENEFITS ........................................ 22

Divorce ........................................................ 23Misconduct .................................................. 23

EMPLOYMENT AFTER RETIREMENT ................ 24Returning to Work in a PositionCovered by a State of New Jersey-Administered Retirement System Other than the PERS ................................ 24Returning to a Position Under the PERS .... 24Reenrollment in the PERS ........................ 25Retiring for a Second Time ........................ 25Disability Retirees Restored to Active Service ............................................ 25Disability Retirees -Earnings After Retirement .......................... 25State Health Benefits Program Coverage .................................... 25Social Security Benefits .............................. 25

ACTIVE AND RETIRED DEATH BENEFITS ........ 25Noncontributory and ContributoryGroup Life Insurance .................................. 25Coverage For Active Members .................. 26

Active Group Life Insurance Amounts .................................................. 26

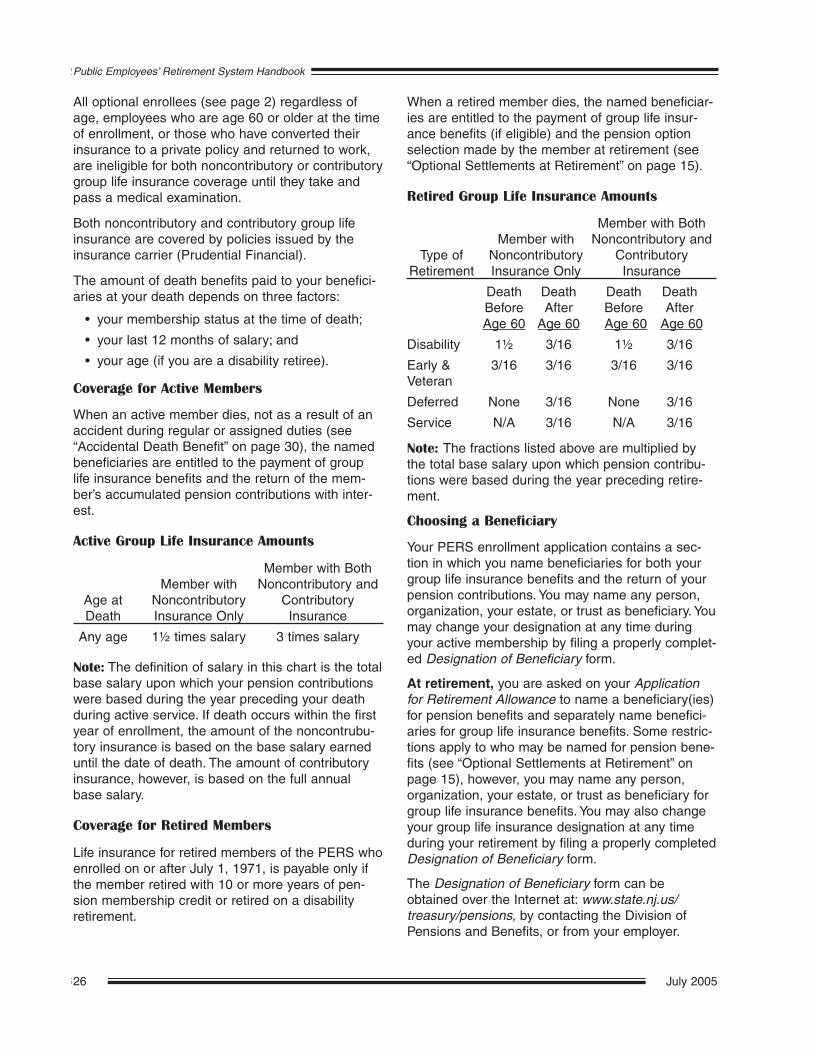

Coverage for Retired Members .................. 26

Retired Group Life Insurance Amounts .................................................. 26

Choosing a Beneficiary .............................. 26Payment of Group Life Insurance .............. 27Taxation of Group Life Insurance Payments .................................................... 27Group Life Insurance and Leave ofAbsence ...................................................... 27Taxation of Group Life InsurancePremiums .................................................... 27IRS Premium Rates .................................... 28Waiving Noncontributory GroupLife Insurance Over $50,000 ...................... 28

CONVERSION OF GROUP LIFE INSURANCE ................................ 28

Conversion: On Retirement ........................ 29Conversion: Termination of Employment or Leave of Absence ............ 30Conversion: Return to Public Employment ................................................ 30Group Life Insurance CoverageWhile Receiving Workers’Compensation Without Pay ........................ 30

ACCIDENTAL DEATH BENEFIT ........................ 30

WITHDRAWAL FROM THE PENSION FUND ........................................ 31

When Membership Ends ............................ 31Terminating Employment ............................ 31Expired Accounts ...................................... 32Withdrawing Contributions .......................... 33

WORKERS’ COMPENSATION ............................ 33

APPEALS ........................................................ 34

EVALUATION FORM ........................................ 35

Separate Addenda Booklets are also available formembers of the following groups:

LAW ENFORCEMENT OFFICERS (LEO)

LEGISLATIVE RETIREMENT SYSTEM

PROSECUTORS PART OF THE PERS

WORKERS’ COMPENSATION JUDGESPART OF THE PERS

Public Employees’ Retirement System Handbook

July 2005iv

Telephone Numbers:

• For computerized information about your indi-vidual account 24 hours a day, seven days aweek, call our Automated Information Systemat (609) 777-1777. All you need is your SocialSecurity number and a touch-tone phone tohear personalized information about loans,purchase costs, retirement benefits, with-drawals, and your account with the retirementsystem.

• To talk with a counselor about your PublicEmployees’ Retirement System account or theState Health Benefits Program, call (609)292-7524 weekdays between 8:00 a.m. and4:30 p.m. (except State holidays). If you arehearing impaired, call the TDD at (609) 292-7718.

• To speak with a plan representative about theNew Jersey State Employees DeferredCompensation Plan, call (609) 292-3605weekdays between 8:15 a.m. and 4:30 p.m.(except State holidays). Plan representativescan answer your questions about the DeferredCompensation Plan and provide enrollmentand distribution forms.

• To speak with a plan representative about theSupplemental Annuity Collective Trust(SACT), call (609) 633-2031 weekdaysbetween 8:15 a.m. and 4:30 p.m. (exceptState holidays). SACT representatives cananswer your questions about the SACT andprovide enrollment and distribution forms.

• If you are a retired member who needs tochange your mailing address, call (609) 292-MOVE (6683) Monday through Fridaybetween 8:00 a.m. and 4:30 p.m. (exceptState holidays) to change your address overthe telephone. Retirees can also change theiraddress online at: www.state.nj.us/treasury/pensions/changead.htm

Mailing Address:

On all correspondence, be sure to include yourmembership number or Social Security number.

Division of Pensions and BenefitsPO Box 295Trenton, NJ 08625-0295

Counseling Services:

The Division of Pensions and Benefits offers individ-ual counseling services to members of the retire-ment systems and other benefit programs. Noappointments are taken. Counselors are availableMonday through Friday from 7:40 a.m. to 4:00 p.m.The office is located at:

One State Street Square50 West State Street, 1st FloorTrenton, NJ

Directions to the office appear on the next page.

Internet and E-Mail:

Most publications of the Division of Pensions andBenefits may be found on the Internet at:www.state.nj.us/treasury/pensions or you may e-mail the Division at: [email protected]

Member Benefits Online System:

The Member Benefits Online System (MBOS)allows registered PERS members access to theirpension and, if applicable, State Health BenefitProgram account information online. Resourcesavailable through MBOS include: member accountinformation; pension loan estimates and onlineapplication; a retirement calculator; and (if applica-ble) State Deferred Compensation Plan, SACT plan,and State Health Benefits Program account infor-mation. More applications are being added in thenear future.

Before you can begin using MBOS, you must beregistered with MBOS and the MyNewJersey Website. Registration is free.

To begin the MBOS registration process go to:www.state.nj.us/treasury/pensions/mbosregister.htm

Please be sure to read the registration instructions,as the process requires several steps.

CONTACTING THE DIVISION OF PENSIONS AND BENEFITS

Public Employees’ Retirement System Handbook

July 2005 v

The Division of Pensions and Benefits is located at50 West State Street (One State Street Square)which is a half-block east of the State House. Thedirections below will take you to the parking garagenext door to the Division of Pensions and Benefits.You must pay to park in the parking garage.

When leaving the garage, you will be facing theside of One State Street Square. Turn left and walkto the front entrance of the building (on West StateStreet). “Check-in” with the guard in the main lobbywhere you will be directed to the Office of ClientServices.

From Northeast New Jersey via the NJ Turnpike

Take the NJ Turnpike South to Exit 7A. Follow I-195West until it ends, then follow signs for Route 29.After passing through a tunnel and two traffic lights,take the Calhoun Street exit. At the first traffic light,turn right onto West State Street. After passingthrough a traffic light turn left at the next corner ontoChancery Lane. One-half block up is a multilevelparking garage on the left. You must pay to parkhere. See “When leaving the garage” above to getto the office.

From Northeast New Jersey via Route 1

Take Route 1 South toward Trenton. Just north ofTrenton Route 1 splits into two roads. Stay to the left(do not use Route 1 Alternate). From Route 1 takethe Perry Street exit. At the end of the exit ramp,turn left onto Perry Street. At the fourth traffic lightafter turning onto Perry Street turn left onto WarrenStreet. At the second light, turn right onto WestState Street. At the next corner turn right ontoChancery Lane. One-half block up is a multilevelparking garage on the left. You must pay to parkhere. See “When leaving the garage” above to getto the office.

From Northwest New Jersey

Take Route 31 South to I-95 South to Exit 1 (Route29). Follow Route 29 South for five miles to theCalhoun Street exit. At the first traffic light, turn rightonto West State Street. Pass the State House andthe next light. At the next corner, turn left ontoChancery Lane. One-half block up is a multilevelparking garage on the left. You must pay to parkhere. See “When leaving the garage” above to getto the office.

From Southern New Jersey

If using the Turnpike, take exit 7A and follow thedirections from Northeast New Jersey via the NJTurnpike.

If using I-295 North, take exit 60 to Route 29 andfollow the directions for using Route 206 North(below) beginning with Route 29.

If using Route 206 North, about four miles beforereaching center-city Trenton take the I-295 exit but,once on the interstate highway, follow the signs forRoute 29, not I-295. After passing through a tunneland two traffic lights, take the Calhoun Street exit.At the first traffic light, turn right onto West StateStreet. After passing through a traffic light turn leftat the next corner onto Chancery Lane. One-halfblock up is a multilevel parking garage on the left.You must pay to park here. See “When leaving thegarage” to get to the office.

From the New Jersey Shore

Take I-195 West, then follow the directions fromNortheast New Jersey via the NJ Turnpike.

DIRECTIONS TO THE DIVISION OF PENSIONS AND BENEFITS

Public Employees’ Retirement System Handbook

July 2005vi

PLAN INFORMATION

Name of Plan

The Public Employees’ Retirement System of New Jersey.

Administration

The Public Employees’ Retirement System is a defined benefit plan administered by the NewJersey Division of Pensions and Benefits, PO Box 295, Trenton, New Jersey 08625-0295,(609) 292-7524.

Provisions of Law

The Public Employees’ Retirement System was established by New Jersey Statute and canbe found in the New Jersey Statutes Annotated, Title 43, Chapter 15A. Changes in the lawcan only be made by an act of the State Legislature. Rules governing the operation andadministration of the system may be found in Title 17, Chapters 1 and 2 of the New JerseyAdministrative Code.

Funding

The funds used to pay benefits come from three sources: employer contributions, employeecontributions, and investment income from those contributions. All contributions not requiredfor current operations are invested by the State Division of Investment.

Plan Year

For record keeping purposes the plan year is July 1 through June 30.

Service of Legal Process

Legal process may be served on the Director of the Division of Pensions and Benefits, theadministrator of the system.

Employment Rights Not Implied

Membership in the Public Employees’ Retirement System does not give you the right to beretained in the employ of a participating employer, nor does it give you a right of claim to anybenefit you have not accrued under terms of the system.

Benefits and provisions of the Public Employees’ Retirement System are subject to changes by the legis-lature, courts, and other officials. While this booklet outlines the benefit and contribution schedules of thePublic Employees’ Retirement System, it is not a final statement. Complete terms governing any employ-ee benefit program are set forth in the New Jersey Statutes Annotated. Regulations, new or amended, arepublished in the New Jersey Register by the State Office of Administrative Law supplementing the NewJersey Administrative Code.

PUBLIC EMPLOYEES’ RETIREMENT SYSTEM (PERS)

as of July 2005

THE RETIREMENT SYSTEM

The State of New Jersey established the PublicEmployees’ Retirement System (PERS) in 1955after the repeal of the laws that created the formerState Employees’ Retirement System. The Divisionof Pensions and Benefits is assigned all administra-tive functions of the retirement system except forinvestment.

The PERS Board of Trustees has the responsibilityfor the proper operation of the retirement system.The Board consists of six employee representatives,the State Treasurer, and two individuals appointedby the Governor with the advice and consent of theSenate. The Board meets once a month. A PERSmember who wishes to be a candidate for thePERS Board of Trustees must be nominated bypetitions bearing the signatures of 500 active mem-bers. Nominating petition forms, together withinstructions for filing, are available upon writtenrequest to the Secretary of the PERS Board ofTrustees, Division of Pensions and Benefits, PO Box295, Trenton, New Jersey 08625-0295.

The purpose of this handbook is to provide you withinformation about the retirement system to assistyou in making decisions concerning your future andyour family’s future. If you have questions concern-ing your retirement system benefits, please seepage iv for information on contacting the Division ofPensions and Benefits.

An online version of this handbook containing cur-rent updates is available for viewing over theInternet at: www.state.nj.us/treasury/pensions/persman.htm Be sure to check the Division ofPensions and Benefits Internet home page at:www.state.nj.us/treasury/pensions for PERS relatedforms, fact sheets, and news of any new develop-ments affecting the PERS.

PERS Special Employee Groups

The information contained in this handbook appliesto the majority of the members enrolled in thePERS. However, certain members of the PERSqualify for enrollment into special employee groups:

• Law Enforcement Officers (LEO)

• Prosecutors Part of the PERS

• State Legislative Retirement System (LRS) ofthe PERS

• Workers’ Compensation Judges (WCJ) Part ofthe PERS

Members of these special employee groups shouldalso see the PERS Handbook Addendum specific totheir employee group for exceptions to the regularPERS rules and benefits. These exceptions are alsonoted under the section headings in this handbook.

MEMBERSHIP(LEO, LRS, Prosecutors Part, and

WCJ members see addendum)

Eligibility Criteria

Enrollment rules and regulations are described ingeneral terms in this handbook and may not coverall situations. If you have been a public employee forseveral years, you should be aware that presentrules and regulations governing enrollment in theretirement system may differ from past rules andregulations. If you have specific questions concern-ing your date of enrollment, you may wish to contactthe Division of Pensions and Benefits for additionalinformation.

Membership in the retirement system is generallyrequired as a condition of employment for mostemployees of the State, or any county, municipality,school district, or public agency. You are required toenroll in the PERS if:

• you are employed on a regular basis in aposition covered by Social Security; and

• your annual salary is $1,500 or more; and

• you are not required to be a member of anyother State or local government retirementsystem on the basis of the same position;

or if:

• you are receiving a monthly retirementallowance from the PERS and you earn morethan $15,000 annually from any PERS-cov-ered employment (see “Exceptions” on page24); or

• you retired on a PERS disability retirementand earn more than $1,500 annually from anyPERS-covered employment (see page 25 foradditional information).

Although most employees are required to enroll inthe retirement system when hired, in someinstances you may not qualify for enrollment in thesystem until up to one year from your date ofemployment.

July 2005 1

Public Employees’ Retirement System Handbook

EXAMPLE 1: If you are hired as a temporary or pro-visional employee by an employer covered by CivilService you would not be eligible for enrollment untilyour 13th month of employment (or the date you arepermanently appointed to your position — Date ofRegular Appointment).

EXAMPLE 2: If you are an adjunct faculty member ata State or County college/university you would beenrolled immediately if you are already a member ofthe PERS due to other employment, otherwise, youwould not be eligible for enrollment until the start ofyour third consecutive semester of teaching.

Optional Membership

Membership in the retirement system is optionalfor:

• non-veteran elected officials. (Elected officialswho qualify as veterans must enroll in theretirement system. See page 11 for a defini-tion of “veteran”.)

• full-time non-veterans hired prior to July 1,1966 or the date of adoption of the retirementsystem by the employer, whichever is earlier.

• part-time non-veterans hired prior to July 1,1966.

• part-time school crossing guards receivingperiodic benefits from the federal government(whether military or civilian pension, includingSocial Security) unless the employee is previ-ously retired from the PERS.

• employees hired prior to September 10, 1991who are receiving monthly retirementallowances from another state.

• special service employees hired under thefederal Older American Community ServiceEmployment Act.

If you choose the option of joining the retirementsystem, you cannot withdraw your funds until youend your employment.

Factors for Ineligibility

You cannot join the PERS if:

• you are a provisional or temporary employeecovered by Civil Service with less than 12months of continuous service.

• you do not earn at least $1,500 annually.

• you are not covered by Social Security.

• you are a seasonal employee.

• you are a retired member of PERS who hasreturned to public employment and your annu-al salary from all PERS covered employmentis not expected to exceed $15,000.

• you are retired and receiving a monthly retire-ment allowance from another public retire-ment system in New Jersey.

• you are employed under the Job TrainingPartnership Act (JTPA) or its successor pro-gram established under the WorkforceInvestment Act of 1998 (WIA) and are paiddirectly from federal JTPA or WIA funds.

If you are in doubt about the eligibility of a position,write to the Division of Pensions and Benefits for anadministrative determination.

ENROLLMENT (Prosecutors Part members see addendum)

Enrollment/Certification of Payroll Deductions

Both you and your employer must complete anEnrollment Application for you to enroll in the retire-ment system. Your employer will send the completedapplication to the Division of Pensions and Benefitsfor processing. When processing is complete, youand your employer will receive a Certification ofPayroll Deductions showing the date deductions willbegin, your rate of contribution, and any backdeductions due.

You may wish to keep the Certification of PayrollDeductions on file with your other important papersso that you have a record of your enrollment in theretirement system.

Proof of Age

All members of the PERS must provide documenta-tion that proves their age before retiring. You shouldattach evidence of your proof of age to your enroll-ment application; however, do not delay sending theenrollment application if proof of age is not readilyavailable. Acceptable evidence of your age includesa photocopy of:

• your birth certificate;

• your passport;

• naturalization or immigration papers;

• certain other records including baptismalrecords or school records, or

• an affidavit from an older family member.

July 20052

Public Employees’ Retirement System Handbook

Contribution Rate

The full rate of PERS employee contributions is fivepercent of base salary (Prosecutors Part memberspay a rate of 8.5 percent). The full rate of contribu-tion is established by the statutes governing thePERS.

Your contribution rate is applied to your base salaryto determine your pension deductions. Base salarydoes not include overtime, bonuses, or money youreceive as an adjustment before retirement. Yourpension contributions are deducted from your salaryeach payday and reported to the PERS by youremployer.

Temporary Reductions — The State Treasurer hasthe right under State law to make temporary reduc-tions in the contribution rate. Reductions in the fullcontribution rate are considered temporary and areauthorized by the Treasurer on a year-to-year basisprovided there are sufficient excess assets in thepension fund.

When authorized reductions are in effect, theemployer will take regular pension deductions at thereduced contribution rate, however, all voluntarydeductions (loan repayments, purchases) remainbased upon the full rate of five percent (except forProsecutors Part members, see addendum).

The pension deduction shown on the Certification ofPayroll Deductions for new employees alwaysreflects the full five percent rate even if a reductionis in effect.

Pensionable Maximum — Since the PERS is a“qualified” pension plan under the provisions of theInternal Revenue Code, Section 401(a)(17), the cur-rent federal ceiling on pensionable compensation($210,000 for 2005) applies to the base salaries ofPERS members.

Tax Deferral — Since January 1987, all mandatorypension contributions to the PERS have been feder-ally tax deferred. Under the 414(h) provisions of theInternal Revenue Code this reduces your grosswages subject to federal income tax. Purchases ofservice credit are voluntary pension contributionsand are not tax deferred unless funded by a rolloverfrom another tax-deferred plan (see “Rollover forPurchase Payment” on page 8).

MULTIPLE & DUAL MEMBERSHIP

Multiple Membership — You are considered a mul-tiple member if you are employed and reported to

the retirement fund by more than one PERS partici-pating employer.

EXAMPLE: If you are a plumbing inspector workingfor more than one municipality, you are enrolled asan employee of each public employer. All of yourbase salaries are posted to your PERS account andconsolidated in calculating your retirement benefit.In terms of service credit, however, no more than 12months of service credit will be given for any calen-dar or fiscal year.

You are required to file an Enrollment Applicationwhen hired by your first PERS employer. If youaccept PERS covered employment from a secondemployer (or subsequent employers), the newemployer should submit a Report of Transfer indicat-ing “Multiple Enrollment” in the space provided atthe top of the form.

Once you have established multiple membership,you will be classified as a multiple member for yourentire membership. Multiple members cannot with-draw or begin to collect retirement benefits until theyhave retired from or terminated every position cov-ered by the PERS.

Dual Membership — You are considered a dualmember if you are a member of more than oneNew Jersey State-administered retirement systemat the same time.

EXAMPLE: If you are a State employee enrolled inthe PERS and an educator enrolled in the Teachers’Pension and Annuity Fund (TPAF), you are a dualmember.

When establishing dual membership, EnrollmentApplications are filed by each employer with the dif-ferent retirement systems.

Unlike a multiple member, a dual member’s contri-butions and service credit are kept separate.Benefits will be paid separately from each retire-ment system in the event of death, retirement, orwithdrawal.

TRANSFERS (Prosecutors Part members see addendum)

Intrafund Transfer

An Intrafund Transfer is the transfer of your accountfrom one PERS employer to another PERS employ-er. If you terminate your current position covered bythe PERS and accept a position also covered by thePERS, your new employer should file a Report ofTransfer form with the Division of Pensions and

July 2005 3

Public Employees’ Retirement System Handbook

Benefits, provided you have not withdrawn yourmembership or your account has not expired (see“Withdrawal from the Pension Fund” on page 31).

If you meet the criteria listed above, you are imme-diately eligible to continue your same membershipin the PERS with the new employer.

If you are a multiple member (see the definition ofa “multiple member” on page 3), your new employershould indicate “Multiple Enrollment” by checkingthe box provided at the top of the Report of Transfer.

Interfund Transfer

An Interfund Transfer is the transfer of your accountfrom a PERS employer to employment covered by adifferent New Jersey State-administered retirementsystem (or vice versa). If you terminate your currentposition covered by the PERS and accept a positioncovered by a different New Jersey State-adminis-tered retirement system, you may transfer your con-tributions and service credit to the new retirementsystem provided:

• you have not withdrawn your membership oryour account has not expired (see“Withdrawal from the Pension Fund” on page31);

• you are not a dual member with more thanthree years of concurrent service in theTeachers’ Pension and Annuity Fund* or withany concurrent service in any other retirementsystem (see the definition of a “dual member”on page 3); and

• you meet the eligibility requirements of thesecond retirement system.

If you are interested in transferring your member-ship account, an enrollment application for the newsystem and an Application for Interfund Transfershould be submitted by your employer to theDivision of Pensions and Benefits when you meetthe eligibility requirements of the new retirementsystem.

SERVICE CREDIT(Prosecutors Part members see addendum)

Since retirement benefits are based in part on accu-mulated service credit, it is important that youreceive the appropriate amount of credit for theamount of time you work. You receive one month ofservice credit for each month you make a full pen-sion contribution.

• Employees whose employers report serviceand contributions biweekly will receive onepay period of service credit for each pay peri-od a full pension contribution is made.

• Employees paid on a ten-month contract fromSeptember through June will receive credit forthe July and August that preceded September,if a full month’s pension deduction is taken forSeptember.

VESTING(LEO, LRS, and Prosecutors Part members

see addendum)

You are vested in the PERS after you have attained10 years of service credit.

Being vested in the PERS means that you are guar-anteed the right to receive a retirement benefitwhen you reach age 60.

• If you are vested and terminate your employ-ment before retiring, your pension account willremain open pending either a return to cov-ered employment, your filing for a DeferredRetirement to be effective at age 60 (seepage 13 — you must file a retirement applica-tion prior to receipt of any benefits), or yourwithdrawal from the pension system (seepage 31).

• If you are not vested and you terminateemployment before retiring, your options varydepending on the nature of your terminationand/or your age at the time of your termina-tion (see “Terminating Employment” on page31).

CREDIT FOR MILITARY SERVICE AFTER ENROLLMENT

The federal Uniformed Services Employment andReemployment Rights Act of 1994 (USERRA) pro-vides that a member who leaves employment toserve on active duty is entitled to certain pensionrights upon return to employment with the same

July 20054

Public Employees’ Retirement System Handbook

*A PERS member with three years or less of con-current service in a Teachers’ Pension and AnnuityFund account may, under certain conditions, trans-fer all service credit from one fund to the other, lessany concurrent service credit.

employer. The time in military service is to count, forvesting and retirement eligibility purposes, asthough the employee had not left. However, themember will, at a minimum, have to make the pen-sion contributions normally required to have the mili-tary service time included in the calculation of theretirement benefit.

When an employee returns from uniformed militaryservice to PERS covered employment within thetime frames specified under USERRA, the employershould notify the Division of Pensions and Benefitsno later than 30 days after the employee’s return bysubmitting a Request for USERRA-Eligible Serviceform. Once notified, the Division will annotate theemployee’s pension account to reflect the USERRAcredit for benefits eligibility and will provide theemployee with a quotation for the cost for purchas-ing the pension service credit so that it countstoward the calculation of benefits.

PURCHASING SERVICE CREDIT

Since your retirement allowance is based in part onthe amount of service credit posted to your accountat the time of retirement, it may help you to pur-chase additional service credit if you are eligible todo so. Only active members of the retirement sys-tems are permitted to purchase service credit. Anactive member is one who has not retired or with-drawn, and who has made a contribution to theretirement system within two years of the purchaserequest. In no case can you receive more than oneyear of service credit for any calendar or fiscal year.A dual member (see page 3) cannot purchase con-current service from any other retirement system.

TYPES OF SERVICE ELIGIBLE FOR PURCHASE

(Prosecutors Part members see addendum)

If a type of service is not listed below, it is not eligi-ble for purchase.

Temporary Service – Members are eligible to pur-chase service credit for temporary or provisionalemployment provided the employment was continu-ous and immediately preceded a permanent or reg-ular appointment in a position covered by thePERS.

• Members are allowed to purchase temporaryservice rendered under a former membershipin a New Jersey State-administered retire-ment system.

• Part-time, hourly, and substitute service maybe eligible for purchase.

• Service through the Job Training PartnershipAct (JTPA), and its successor program estab-lished under the Workforce Investment Act of1998, is not eligible.

Leave of Absence Without Pay – Members are eli-gible to purchase service credit for official leaves ofabsence without pay. The amount of time eligible forpurchase depends on the “type of leave” that wastaken.

• up to two years may be purchased for leavestaken for personal illness;

• up to three months may be purchased forleaves taken for personal reasons.

• Maternity leave is considered personal ill-ness.*

• Child care leave is eligible for purchase as aleave for personal reasons.

A leave of absence without pay under a formermembership in a New Jersey State-administeredretirement system may be eligible for purchase.

If a member who is employed 10 months per yeargoes on an approved leave for personal reasons forthe months of May, June, and/or September, themember will be allowed to purchase credit for themonths of July and August as part of the leave ofabsence — up to a maximum of five months.

Former Membership Service – Members may pur-chase all service credited under a previous mem-bership in a New Jersey State-administered retire-ment system (PERS, TPAF, PFRS, SPRS) whichhas been terminated after two continuous years ofinactivity in accordance with statute or by withdrawalby the member of the contributions made undersuch membership.

Out-of-State Service – Members are eligible to pur-chase up to 10 years of service credit for publicemployment rendered with any state, county, munic-ipality, school district, or public agency outside theState of New Jersey, provided the service renderedwould have been eligible for membership in a New

July 2005 5

Public Employees’ Retirement System Handbook

*A certification from a physician that a member wasdisabled due to pregnancy and a resulting disabilityfor the period in excess of three months is required.Otherwise, three months is the maximum period ofpurchase for maternity.

Jersey administered retirement system had theservice been rendered as a public employee in thisstate. This service is only eligible for purchase if themember is not receiving nor eligible to receiveretirement benefits from the out-of-state public pen-sion fund.

U.S. Government Service – Members are eligible topurchase up to 10 years of service credit for civilianservice rendered with the U.S. government if thepublic employment would have been eligible forcredit in a State of New Jersey-administered retire-ment system had the service been rendered as apublic employee in this state. This service is only eli-gible for purchase if the member is not receiving noreligible to receive retirement benefits from the feder-al government based in whole or in part on thisservice.

Military Service Before Enrollment – Membersmay purchase service credit for up to 10 years ofactive military service rendered prior to enrollmentprovided the member is not receiving nor eligible toreceive a military pension or a pension from anyother state or local source for such military service.

Active military service eligible for purchase meansfull-time duty in the active military service of theUnited States and includes full-time training duty,annual training duty, and attendance, while in theactive military service, at a school designated as aservice school by law or by the Secretary of the mil-itary department concerned. It cannot include peri-ods of service of less than 30 days. It does notinclude weekend drills or annual summer training ofa national guard or reserve unit or time spent as acadet or midshipman at one of the military acade-mies.

Active military service that has been combined withreserve component service to qualify for a militarypension as a reserve component member may beeligible for purchase.

If you qualify as a veteran, you may be eligible topurchase an additional five years of military service(see “Important Purchase Notes” at right).

Military Service After Enrollment – Under therequirements of the federal Uniformed ServicesEmployment and Reemployment Rights Act of 1994(USERRA), members may receive credit for militaryservice rendered after October 13, 1994 (see page4). However, USERRA eligible service will only beused to determine eligibility for benefits. The calcu-lation of retirement benefits will not use the USER-

RA eligible service unless the employee pays therequired pension contributions for the period of mili-tary service.

Note: There is a time sensitive element to this pur-chase (see page 4).

Uncredited Service – Members may purchase anyregular employment with a public employer in NewJersey for which the member does not now haveretirement credit. This is credit for time when themember should have been enrolled, but was not.

Local Retirement System Service – Members maypurchase service credit established within a localretirement system in New Jersey if they were ineligi-ble to transfer that service to the PERS upon with-drawal from the local retirement system. This serv-ice is only eligible for purchase if the member is notreceiving nor eligible to receive retirement benefitsfrom that public pension fund.

IMPORTANT PURCHASE NOTES

• If you qualify as a non-veteran, you are eligi-ble to purchase an aggregate of 10 years ofservice credit for work outside New Jersey(Out-of-State, Military, and U.S. GovernmentService).

• If you qualify as a military veteran (see“Definition of a Veteran” on page 11), you maybe eligible to purchase an additional fiveyears of military service rendered during peri-ods of war for an aggregate of 15 years ofservice outside New Jersey (Out-of-State,Military, and U.S. Government Service).

• To qualify for an Ordinary DisabilityRetirement, members need 10 years of NewJersey service; therefore, the purchase ofU.S. Government, Out-of-State, or MilitaryService cannot be used to qualify for this typeof retirement.

• Purchases of service credit are voluntary pen-sion contributions and are not tax deferredunless funded by a rollover from another tax-deferred plan (see “Rollover for PurchasePayment” on page 8).

COST AND PROCEDURES FOR PURCHASING SERVICE CREDIT

You may obtain a quotation of the cost for purchas-ing additional service credit by submitting anApplication to Purchase Service Credit to the

July 20056

Public Employees’ Retirement System Handbook

Division of Pensions and Benefits. This applicationis available from your employer, by writing to theDivision of Pensions and Benefits, or over theInternet at: www.state.nj.us/treasury/pensions

You can receive an estimate of the cost of purchas-ing service credit by calling the AutomatedInformation System at (609) 777-1777 or by usingthe online Purchase Calculator which can be foundon the Division of Pensions and Benefits’ Internetsite.

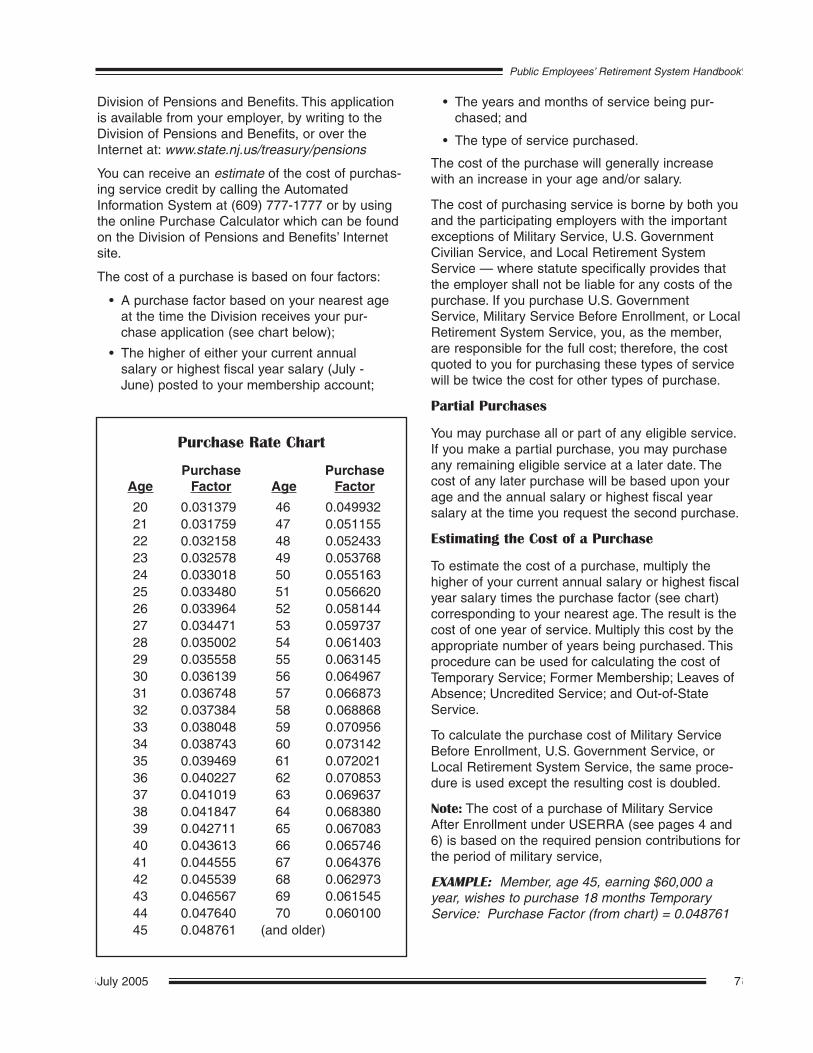

The cost of a purchase is based on four factors:

• A purchase factor based on your nearest ageat the time the Division receives your pur-chase application (see chart below);

• The higher of either your current annualsalary or highest fiscal year salary (July -June) posted to your membership account;

• The years and months of service being pur-chased; and

• The type of service purchased.

The cost of the purchase will generally increasewith an increase in your age and/or salary.

The cost of purchasing service is borne by both youand the participating employers with the importantexceptions of Military Service, U.S. GovernmentCivilian Service, and Local Retirement SystemService — where statute specifically provides thatthe employer shall not be liable for any costs of thepurchase. If you purchase U.S. GovernmentService, Military Service Before Enrollment, or LocalRetirement System Service, you, as the member,are responsible for the full cost; therefore, the costquoted to you for purchasing these types of servicewill be twice the cost for other types of purchase.

Partial Purchases

You may purchase all or part of any eligible service.If you make a partial purchase, you may purchaseany remaining eligible service at a later date. Thecost of any later purchase will be based upon yourage and the annual salary or highest fiscal yearsalary at the time you request the second purchase.

Estimating the Cost of a Purchase

To estimate the cost of a purchase, multiply thehigher of your current annual salary or highest fiscalyear salary times the purchase factor (see chart)corresponding to your nearest age. The result is thecost of one year of service. Multiply this cost by theappropriate number of years being purchased. Thisprocedure can be used for calculating the cost ofTemporary Service; Former Membership; Leaves ofAbsence; Uncredited Service; and Out-of-StateService.

To calculate the purchase cost of Military ServiceBefore Enrollment, U.S. Government Service, orLocal Retirement System Service, the same proce-dure is used except the resulting cost is doubled.

Note: The cost of a purchase of Military ServiceAfter Enrollment under USERRA (see pages 4 and6) is based on the required pension contributions forthe period of military service,

EXAMPLE: Member, age 45, earning $60,000 ayear, wishes to purchase 18 months TemporaryService: Purchase Factor (from chart) = 0.048761

July 2005 7

Public Employees’ Retirement System Handbook

Purchase Rate Chart

Purchase PurchaseAge Factor Age Factor

20 0.031379 46 0.04993221 0.031759 47 0.05115522 0.032158 48 0.05243323 0.032578 49 0.05376824 0.033018 50 0.05516325 0.033480 51 0.05662026 0.033964 52 0.05814427 0.034471 53 0.05973728 0.035002 54 0.06140329 0.035558 55 0.06314530 0.036139 56 0.06496731 0.036748 57 0.06687332 0.037384 58 0.06886833 0.038048 59 0.07095634 0.038743 60 0.07314235 0.039469 61 0.07202136 0.040227 62 0.07085337 0.041019 63 0.06963738 0.041847 64 0.06838039 0.042711 65 0.06708340 0.043613 66 0.06574641 0.044555 67 0.06437642 0.045539 68 0.06297343 0.046567 69 0.06154544 0.047640 70 0.06010045 0.048761 (and older)

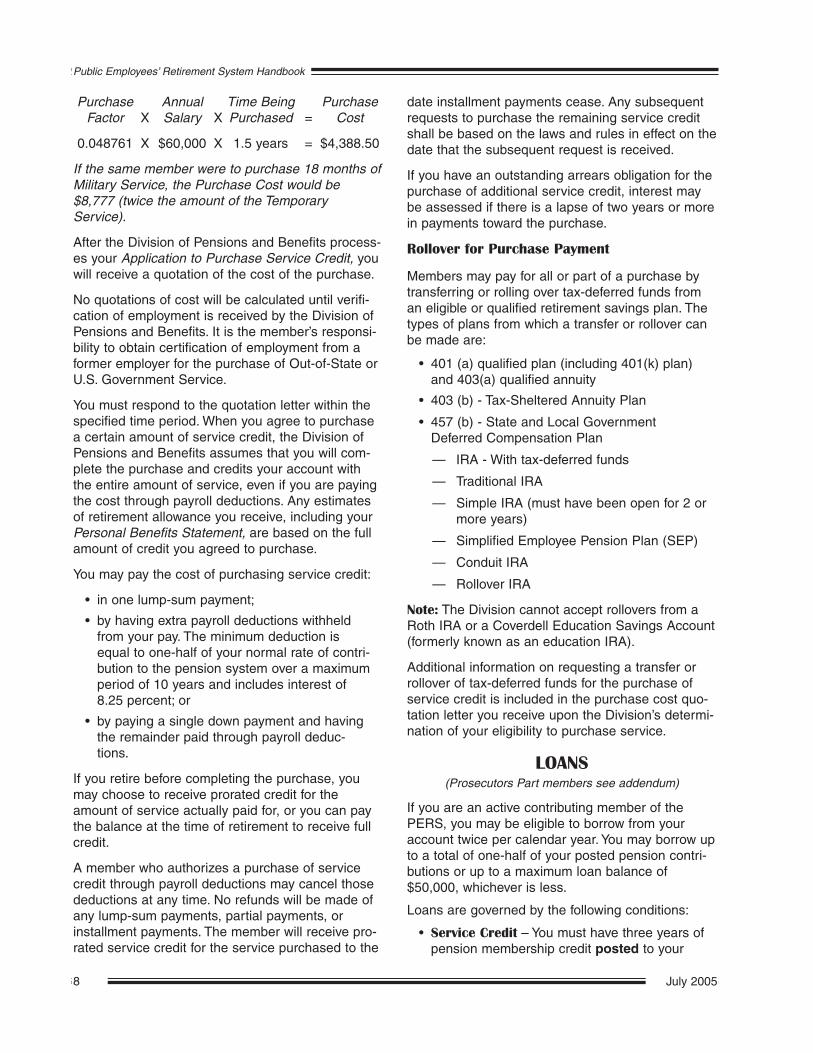

Purchase Annual Time Being PurchaseFactor X Salary X Purchased = Cost

0.048761 X $60,000 X 1.5 years = $4,388.50

If the same member were to purchase 18 months ofMilitary Service, the Purchase Cost would be$8,777 (twice the amount of the TemporaryService).

After the Division of Pensions and Benefits process-es your Application to Purchase Service Credit, youwill receive a quotation of the cost of the purchase.

No quotations of cost will be calculated until verifi-cation of employment is received by the Division ofPensions and Benefits. It is the member’s responsi-bility to obtain certification of employment from aformer employer for the purchase of Out-of-State orU.S. Government Service.

You must respond to the quotation letter within thespecified time period. When you agree to purchasea certain amount of service credit, the Division ofPensions and Benefits assumes that you will com-plete the purchase and credits your account withthe entire amount of service, even if you are payingthe cost through payroll deductions. Any estimatesof retirement allowance you receive, including yourPersonal Benefits Statement, are based on the fullamount of credit you agreed to purchase.

You may pay the cost of purchasing service credit:

• in one lump-sum payment;

• by having extra payroll deductions withheldfrom your pay. The minimum deduction isequal to one-half of your normal rate of contri-bution to the pension system over a maximumperiod of 10 years and includes interest of8.25 percent; or

• by paying a single down payment and havingthe remainder paid through payroll deduc-tions.

If you retire before completing the purchase, youmay choose to receive prorated credit for theamount of service actually paid for, or you can paythe balance at the time of retirement to receive fullcredit.

A member who authorizes a purchase of servicecredit through payroll deductions may cancel thosedeductions at any time. No refunds will be made ofany lump-sum payments, partial payments, orinstallment payments. The member will receive pro-rated service credit for the service purchased to the

date installment payments cease. Any subsequentrequests to purchase the remaining service creditshall be based on the laws and rules in effect on thedate that the subsequent request is received.

If you have an outstanding arrears obligation for thepurchase of additional service credit, interest maybe assessed if there is a lapse of two years or morein payments toward the purchase.

Rollover for Purchase Payment

Members may pay for all or part of a purchase bytransferring or rolling over tax-deferred funds froman eligible or qualified retirement savings plan. Thetypes of plans from which a transfer or rollover canbe made are:

• 401 (a) qualified plan (including 401(k) plan)and 403(a) qualified annuity

• 403 (b) - Tax-Sheltered Annuity Plan

• 457 (b) - State and Local GovernmentDeferred Compensation Plan

— IRA - With tax-deferred funds

— Traditional IRA

— Simple IRA (must have been open for 2 ormore years)

— Simplified Employee Pension Plan (SEP)

— Conduit IRA

— Rollover IRA

Note: The Division cannot accept rollovers from aRoth IRA or a Coverdell Education Savings Account(formerly known as an education IRA).

Additional information on requesting a transfer orrollover of tax-deferred funds for the purchase ofservice credit is included in the purchase cost quo-tation letter you receive upon the Division’s determi-nation of your eligibility to purchase service.

LOANS(Prosecutors Part members see addendum)

If you are an active contributing member of thePERS, you may be eligible to borrow from youraccount twice per calendar year. You may borrow upto a total of one-half of your posted pension contri-butions or up to a maximum loan balance of$50,000, whichever is less.

Loans are governed by the following conditions:

• Service Credit – You must have three years ofpension membership credit posted to your

July 20058

Public Employees’ Retirement System Handbook

pension fund account. Pension contributionsare posted to your account on a quarterlybasis. It normally takes 60 days after the endof a quarter for your contributions to be post-ed to your account. For example, if youenrolled in the pension fund on January 1,2005, you would not have three years postedto your account until March, 2008.

• Loan Amount – The minimum amount youmay borrow is $50, and loan amounts thenincrease in increments of $10. The maximumyou may borrow is one-half of your contribu-tions that are posted to your account, up to amaximum loan balance of $50,000, whicheveris less. You may learn the amount you mayborrow by calling the Automated InformationSystem at (609) 777-1777.

• Loan Repayment – The maximum time periodover which a loan may be repaid is five years.The minimum deduction toward the repay-ment of a loan is equal to the full pensioncontribution rate of five percent of salary atthe time of your request. The maximum allow-able deduction toward the repayment of yourloan is 25 percent of your base salary. Theminimum loan repayment amount will be simi-lar whether you borrow $500 or $5,000; how-ever, the repayment of a larger loan will con-tinue for a longer period of time than for asmaller loan.

If you have an outstanding loan balance andtake a subsequent loan, the Internal RevenueService requires that the new combined loanbalance must be repaid within five years ofthe date of the first loan (see “InternalRevenue Service Requirements” at right).

You may learn the minimum deduction towardthe repayment of a loan by calling theAutomated Information System at (609) 777-1777.

• Interest – Interest is charged at the rate offour percent per year on the declining bal-ance.

• Number of Loans Per Year – You may borrowtwice in any calendar year. This is determinedby the date of the check, not the date of therequest. For example, if you made a requestfor a loan on December 24th but the checkwas dated January 5th, the loan would beyour first for the new year.

• Return to Payroll – If you have been out of

work without pay within the last six months,your employer must complete the bottom por-tion of the Loan Application to certify that youhave returned to employment.

• For Loans Made Prior to January 1, 2002 –If you are out of work without pay after loanpayments are set up, no loan payments willbe made until you return to work though inter-est will continue to accrue.

• For Loans Made After January 1, 2002 –See the Internal Revenue Service require-ments for loan repayment which are detailedin the next section.

You may obtain a Loan Application from youremployer, or you may download an application overthe Internet at: www.state.nj.us/treasury/pensions

You may apply for a loan regardless of your age. Ifyou retire before repaying the outstanding balanceof your loan, your loan payments will be carried intoretirement. That is, your pension allowance will bereduced by the same monthly amount you werepaying towards your loan just prior to retirement.You may also repay your outstanding loan balancein one lump sum prior to retirement.

If you die before repaying your loan (either before orafter retirement), the outstanding balance will bededucted from the proceeds of any benefits beingpaid to your beneficiaries.

If you terminate employment and withdraw yourcontributions before repaying your loan, all yourcontributions less the loan balance will be returnedto you (see “Internal Revenue ServiceRequirements” below).

The Automated Information System, at (609) 777-1777, gives you complete access to information youmay need about loans. It will tell you if you are eligi-ble to borrow, how much you can borrow, and whenyour check will be sent if you have filed an applica-tion for a loan. It will also allow you to model differ-ent loan and repayment amounts before you applyfor a loan or provide you with the balance on anexisting loan as of the last quarterly posting.

Internal Revenue Service (IRS) Requirements

Internal Revenue Code Section 72(p) requires thatloan balances cannot exceed $50,000 and must berepaid within five years. Furthermore, if you take asubsequent loan (or loans) and your original loanbalance is not completely paid off, the repaymentperiod will remain five years from the date of the

July 2005 9

Public Employees’ Retirement System Handbook

first loan. The repayment rules on subsequentloans may result in either a substantial increase inyour repayment amount or may even limit theamount that you can borrow if the payroll deduc-tions to repay the loan exceeds the 25 percent ofbase salary restriction on loan repayments.

The IRS regulations also require members to maketimely payments toward outstanding loan balances.While it is your employer’s responsibility to withholdloan deductions from your salary, if you are out ofwork without pay, your employer has no salary fromwhich to take deductions. Members who leave pay-roll with an outstanding loan balance will be notifiedafter six months of nonpayment and offered theoption of paying off the entire loan balance or mak-ing loan repayment through a monthly personalbilling. Failure to repay the loan as scheduled(through either lump-sum payment, personal billing,or return to payroll) will result in the unpaid loan bal-ance being declared in default. If a loan is in default,the loan balance is declared a taxable or “deemeddistribution” and will be reported to the IRS. For thetax year in which the default occurs, the Division ofPensions and Benefits will send you a Form 1099-Rfor tax filing purposes in January of the followingyear. You will be required to include the portion ofthe loan representing before-tax contribution asincome on your federal return. In addition, if you areunder age 59½, you will be required to pay an addi-tional ten percent tax for taking an early pensiondistribution.

If you default on your loan, it will be your responsi-bility to make an estimated tax payment to the IRSto cover your tax liability on the deemed distribution;no withholding will be deducted from your accountby the Division.

If you resume your loan repayments after thedefault, the payments received will be posted toyour account as already-taxed contributions that willincrease the nontaxable portion of your pension atretirement. A deemed distribution cannot be can-celled by resuming your loan payments or repayingthe loan in full prior to the end of the tax year inwhich the default occurs. Please note that, unlike anormal pension distribution, a loan treated as a dis-tribution cannot be rolled over to an IRA or otherqualified retirement plan.

SUPPLEMENTING YOUR PENSION

In addition to your regular pension contributions,there are other opportunities to supplement yourretirement income and possibly set aside money ona tax-deferred basis.

New Jersey State Employees DeferredCompensation Plan

If you are an employee of the State, you may be eli-gible for the New Jersey State Employees DeferredCompensation Plan (IRC Section 457). Contribu-tions to the plan are not subject to federal incometax until you take a distribution from the plan, eitherat retirement or termination before retirement. Themain benefits of the plan are to help you save onfederal income tax now and to supplement yourretirement income through investments.

Brochures on investment options and other perti-nent information are available by calling (609) 292-3605 or by writing to: Division of Pensions andBenefits, New Jersey State Employees DeferredCompensation Plan, PO Box 295, Trenton, NJ08625-0295.

Local Deferred Compensation Plans

PERS members employed by a municipality, county,or board of education may also be eligible to con-tribute to an IRC Section 457 deferred compensa-tion plan. Contact your employer to see if this typeof plan is available to you.

Supplemental Annuity Collective Trust (SACT)

The Supplemental Annuity Collective Trust (SACT)is a voluntary investment program that providesretirement income separate from, and in addition to,your basic pension plan. Your contributions areinvested conservatively in the stock market. Theprogram consists of two separate plans. The SACT-Regular Plan is available to all actively contributingmembers of a New Jersey State-administered retire-ment system. Contributions to this plan are madeafter deductions for federal income tax. The SACT-Tax Sheltered Plan (IRC Section 403(b)) is availableto actively contributing members of public educa-tional institutions. Contributions to this plan aremade before deductions for federal income tax.

SACT brochures and enrollment packets are avail-able by calling (609) 633-2031 or by writing to:Division of Pensions and Benefits, SupplementalAnnuity Collective Trust, PO Box 295, Trenton, NJ08625-0295.

July 200510

Public Employees’ Retirement System Handbook

RETIREMENT(LEO, LRS, Prosecutors Part, and

WCJ members see addendum)

All applications for retirement must be received bythe Division of Pensions and Benefits prior to theeffective date of the retirement. It is the member’sresponsibility to ensure the receipt of the retire-ment application and any other required documen-tation.

Types of Retirement

There are several types of retirement for which youmay qualify.

Service Retirement

Service Retirement is available to members uponreaching age 60 or older. No minimum amount ofpension membership credit is required.

The formula to calculate the maximum annual pen-sion is:

Years of Service X Final Average = Maximum55 Salary Annual

Allowance

FOR EXAMPLE: A member with 22 years of servicewould receive 22/55 or 40% of Final AverageSalary. You receive a slightly higher percentage foreach additional month of service.

‘Years of Service’ means the years and months ofpension service credited to your account —including purchased service credit. It does not nec-essarily mean years and months of employment.

‘Salary’ means the base salary on which your pen-sion contributions are based. It does not includeextra pay for overtime or money given in anticipationof your retirement. Nor does it include amounts paidfor housing, clothing, or uniform allowances.

‘Final Average Salary’ means your average salaryfor the three years immediately preceding yourretirement (either 36 months for employees with 12-month contracts or 30 months for employees with10-month contracts). If your three last years are notyour highest years of salary, your allowance may becalculated using your three highest fiscal years (July1 to June 30) of salary. If this is the case, pleaseindicate on your retirement application that you hadhigher fiscal years of salary.

Early Retirement

Early Retirement is available to members who have

25 years or more of pension membership creditbefore reaching age 60. The benefit is calculatedusing the Service Retirement formula; however, ifyou retire before age 55, your allowance is perma-nently reduced 1/4 of 1 percent for each monthunder that age (three percent per year). For exam-ple, if you retire at age 54, you will receive 97 per-cent of your full retirement allowance.

Here are other reduction factor examples:

Reduction ReductionAge Factor Age Factor54 .97 50 .8553 .94 49 .8252 .91 48 .7951 .88 47 .76

Veteran Retirement

Veteran Retirement is available to qualified militaryveterans who remain in active employment until theeffective date of retirement and who meet the mini-mum age and pension service credit requirementsfor a Veteran Retirement as of their retirement date.

A qualified military veteran may retire with:

• 25 years of service credit at age 55 or older;or

• 20 years of service credit at age 60 or older;or

• 35 years of service credit at age 55 or older.

• Veterans meeting the age requirement withbetween 20 and 34 years of service credit willretire with an annual benefit equal to 54.5 per-cent of the salary upon which pension contri-butions were based during the last year ofemployment or highest 12 consecutivemonths of base salary.

• Veterans with 35 or more years of servicecredit at age 55 or older are entitled to anannual allowance based on the following for-mula:

Years of Service X Highest 12 = Maximum55 Consecutive Annual

Months of Salary Allowance

Veteran members may retire on a ServiceRetirement if that provides a higher benefit.

Definition of a Veteran — A veteran is a personwho holds an honorable discharge from the militaryservice of the United States who served during the

July 2005 11

Public Employees’ Retirement System Handbook

following periods:

• World War II – September 16, 1940 toDecember 31, 1946

• Korean Conflict – June 23, 1950 to January31, 1955

• Lebanon Crisis – July 1, 1958 to November 1,1958

• Vietnam Conflict – December 31, 1960 to May7, 1975

• Lebanon Peacekeeping Mission – September26, 1982 to December 1, 1987

• Grenada Peacekeeping Mission – October 23,1983 to November 21, 1983

• Panama Peacekeeping Mission – December20, 1989 to January 31, 1990

• Operation Desert Shield/Storm – August 2,1990 to February 28, 1991

• Operation Northern Watch/Southern Watch –August 27, 1992 to May 1, 2003

• Operation Restore Hope in Somalia –December 5, 1992 to March 31, 1994

• Operations Joint Endeavor/Joint Guard-Republic of Bosnia and Herzegovina –November 20, 1995 to June 20, 1998

• Operation Enduring Freedom – September11, 2001 to present

• Operation Iraqi Freedom – March 19, 2003 topresent

Veteran status can be granted for World War II, theKorean Conflict, or the Vietnam Conflict as long asthe member had at least 90 days of continuousactive military service, of which at least one day fellwithin the dates listed above. Any honorably dis-charged member of the American Merchant Marinewho served at least 90 days between September16, 1940 and December 31, 1946 also qualifies forveteran status.

Service with the Women’s Army Auxiliary Corps(WAAC) and Women’s Army Corps (WAC) may alsoqualify for veteran status.

For veteran status for the listed missions/operationsafter Vietnam, the member must have served atleast 14 days in the country or region or on shipspatrolling in the territorial waters of these nations.

• If the start of the member's service began onor after the beginning date of the war era, vet-eran status will be granted as long as any one

of the 14 days of service fell on or within thedates listed above.

• If the start of the member's service was priorto the beginning date of the war era, then themember must have served all 14 days in thearea within the dates specified for the conflictin order to be granted veteran status.

If the veteran was discharged because of a service-incurred disability during a period of conflict, the 90or 14-day requirement for service is waived. AbsentWithout Leave (AWOL) periods must be deductedfrom active service and if this reduces the activeservice to less than the 90 or 14-day servicerequirement, veteran status will be denied.

Veteran status cannot be granted if an individualreceived a dishonorable discharge, a dischargefrom the draft, disenrollment from the Coast GuardReserve, or a discharge from the reserve with noevidence of active service in time of war.

Veteran status cannot be granted if the individualservice was:

• State Militia;

• Student training corps during World War II;

• Army of the Allies but not as a citizen of theUnited States at the time of such service;

• Military service during peacetime;

• Military service for training purposes. Also,courses of education and training under theArmy Specialized Training Program or theNavy College;

• Training Program where the courses were acontinuation of the individual’s civilian coursesand were pursued to completion;

• As a cadet or midshipman at one of the serv-ice academies; or

• Any military service performed pursuant to theprovisions of Section 511(d) of Title 10,United States Code, pursuant to enlistment inthe Army National Guard or as a reserve forservice in the Army Reserve, Naval Reserve,Air Force Reserve, Marine Corps or CoastGuard Reserve.

Establishing Veteran Status — Individuals wishingto establish veteran status with the retirement sys-tem should submit a photocopy of their dischargepapers (Form DD 214) showing both their inductionand discharge dates to:

July 200512

Public Employees’ Retirement System Handbook

NJ Department of Military and Veterans AffairsATTN: DVP-VBBPO Box 340Trenton, NJ 08625-0340

Since the NJ Department of Military and VeteransAffairs also makes determinations of veteran's pref-erence for Civil Service and property tax appeals, anote should be attached to say that the discharge isbeing sent for pension purposes. Include youraddress on the note.

Deferred Retirement

Deferred Retirement is available to members whohave at least 10 years of service credit and are notyet 60 years of age when they terminate employ-ment. The retirement would be effective on the firstof the month after attaining age 60. The benefit iscalculated using the Service Retirement formula.

You may apply for a Deferred Retirement when youterminate covered employment or at any time priorto age 60. You must file an Application forRetirement Allowance for the retirement to takeeffect. Under no circumstances can a retirementbecome effective prior to the date the application isreceived by the Division of Pensions and Benefits. Ifa member is removed from employment for cause,the member will be ineligible for DeferredRetirement.

At any time before your Deferred Retirementbecomes effective, you may change your mind andapply for a lump-sum withdrawal of all your pensioncontributions instead. Once you cancel yourDeferred Retirement and withdraw your contribu-tions, all the rights and privileges of membership inthe retirement system end.

Please note the following important informationabout your life insurance, health care coverage,loans, and purchase arrears if you are considering aDeferred Retirement:

• Life Insurance — Your life insurance cover-age will end 31 days after you terminateemployment and will not be in effect until yourDeferred Retirement becomes payable. If youdie before your Deferred Retirement becomeseffective, the last named beneficiary willreceive a return of your pension contributions.There is no life insurance benefit under thesecircumstances. However, during the 31-dayperiod after you terminate employment you

may convert your group life insurance cover-age to a private policy with the PrudentialFinancial. For more information see“Conversion: On Retirement” on page 29.

• Health Benefits — PERS members with lessthan 25 years of service credit who are elect-ing a Deferred Retirement cannot normallytransfer their active health care coverage tothe retired group of the State Health BenefitsProgram (SHBP); however, those electingDeferred Retirement may be eligible for con-tinuation of SHBP coverage under the federallegislation called COBRA* for up to 18 monthsif they were covered by the SHBP just prior toterminating employment. If the actual retire-ment commences while the 18 months ofCOBRA coverage is in effect, the retiree maythen transfer from the COBRA coverage andcontinue the SHBP coverage into retirement.If the 18 months of COBRA coverage endsbefore the retirement commences, the mem-ber will not be entitled to maintain health cov-erage through the SHBP. Participants shouldcontact their employer to see if they qualify forCOBRA continuation.

PERS members with 25 or more years ofservice credit who were employed by aschool board or a county college, are eligi-ble for employer-paid health benefits, and whoelect Deferred Retirement are eligible forSHBP coverage when the DeferredRetirement becomes effective at age 60 orlater.

• Loans — If you terminate employment, failureto repay a pension loan as scheduled mayresult in the unpaid loan balance beingdeclared a taxable distribution that will bereported to the IRS. See page 9 for moreinformation about the IRS regulations regard-ing the repayment of pension loans.

• Purchase Arrears — If you have an outstand-ing arrears obligation for the purchase of addi-tional service credit, interest may be assessedif there is a lapse in payments of two years ormore. For purchases authorized afterSeptember 8, 1998, the purchase will be can-celed after two years with no payments andthe service credit prorated. Members return-

July 2005 13

Public Employees’ Retirement System Handbook

*The Consolidated Omnibus Budget ReconciliationAct (COBRA) of 1985.

ing to employment can have the original pur-chase resumed.

• Supplemental Compensation on Retirement(SCOR) — State employees who retire on aDeferred Retirement are not eligible for pay-ment for unused sick days under the SCORprogram. See your payroll administrator formore information.

Ordinary Disability Retirement

To qualify for an Ordinary Disability Retirement youmust:

• have an active pension account. i.e. you musthave had at least one pension contributioncredited to your account within the past twoyears. If more than two years have elapsedsince the last contribution and you terminatedemployment because you were totally andpermanently disabled and continue to be dis-abled for the same reason(s), special rulesapply; contact the Division of Pensions andBenefits for more information;

• have 10 or more years of New Jersey servicecredit (Out-of-State, Military, and U.S.Government civilian service purchases cannotbe used to attain the 10 years);

• be considered totally and permanently dis-abled (you must prove that you are physicallyor mentally incapacitated from performingyour normal or assigned job duties with nopossibility of significant improvement); and

• submit medical reports certifying your disabili-ty.

Note: If the medical documentation suppliedby you is not sufficient to support your claimof disability, you may be examined by physi-cians selected by the retirement system. Theexamination will be scheduled by the Divisionof Pensions and Benefits — at no cost to you.All medical information is confidential andonly for use by the PERS Board ofTrustees in evaluating your application.

If you qualify for an Ordinary Disability Retirement,the annual benefit is equal to 43.6 percent of yourFinal Average Salary (FAS) or 1.64 percent of yourFAS for each year of service credit, whichever pro-vides the higher benefit.

The application process begins by filing theApplication for Disability Retirement with theDivision of Pensions and Benefits (see “Disability

Retirement Applications” on page 18). The applica-tion contains forms for your physician(s) to completeand a form for the release of hospital records relat-ed to your disability. The application requires corrob-oration of your condition by at least two medicalsources. The more complete the application, thefaster it can be evaluated, although the process maytake six months or more.

It is the applicant’s responsibility to arrange forall physicians’ statements and hospital recordsto be sent to the Division.

Your employer has the right to apply for an involun-tary disability retirement on your behalf.

Once the Board approves a member for a disabilityretirement allowance, the member’s retirementapplication cannot be withdrawn, canceled, oramended (except to change your retirement optionselection provided that you file written notice withthe Division of pensions and Benefits within 30 daysof the date of the Board’s approval or your retire-ment date, whichever is later; otherwise, the retire-ment option will remain and cannot be changed forany reason thereafter).

Approval for Workers’ Compensation or SocialSecurity Disability benefits has no bearing on yourapplication for Ordinary Disability Retirement fromthe PERS. However, if you are approved forOrdinary Disability Retirement benefits and receivea Workers’ Compensation award, your Workers’Compensation award may be reduced by theamount of your Ordinary Disability Retirement bene-fit. If you have any questions concerning this issue,please contact the Division of Workers’Compensation at (609) 292-2515 or send e-mail to:[email protected]

Accidental Disability Retirement

To qualify for an Accidental Disability Retirementyou must:

• be an active member of the PERS on the dateof the “traumatic event” (see definition onpage 15) and at the time you file your applica-tion for retirement;

• be considered totally and permanently dis-abled (you must prove that you are physicallyor mentally incapacitated from performingyour normal or assigned job duties with nopossibility of significant improvement) as aresult of a “traumatic event” that happenedduring and as a direct result of carrying outyour regular or assigned job duties;

July 200514

Public Employees’ Retirement System Handbook

• file an Application for Disability Retirementwithin five years of the date of the “traumaticevent”; and

• be examined by physicians selected by theretirement system. The examination will bescheduled by the Division of Pensions andBenefits — at no cost to you. All medicalinformation is confidential and used onlyby the PERS Board of Trustees in review-ing your claim.

If you qualify for Accidental Disability, your annualretirement allowance will be 72.7 percent of yoursalary at the time of the “traumatic event”.

‘TRAUMATIC EVENT’ has been defined by the courtsas one in which the worker is involuntarily exposedto a violent level of force or impact which is notbrought into motion by the worker. To be eligible forAccidental Disability benefits, the applicant mustdemonstrate that:

• the injury was not induced by normal workeffort;

• the worker met involuntarily with the objectthat was the source of the harm; and

• the source of the injury was a violent oruncontrollable power.

The following would not be considered “traumaticevent”s:

• Slip and fall cases, no force or power origi-nates anywhere except from the person fallingand the gravitational force on the person isnot considered “great”;

• A worker who injures his wrist when a jack-hammer twists in his hand is not injured as adirect result of a great rush of force or uncon-trollable power;

• A member’s heart attack, although the resultof job stress and tension, is not considered a“traumatic event”.

If you apply for Accidental Disability and are foundby the Board of Trustees to be totally and perma-nently disabled but not as a result of a “traumaticevent”, you may be retired on an Ordinary Disabilityif you have the required service credit (see page14).

The application process begins by filing theApplication for Disability Retirement with theDivision of Pensions and Benefits (see “Disability