Embed Size (px)

Citation preview

Place of Britain in a Future Europe Martin Wolf, Associate Editor & Chief Economics Commentator, Financial Times

Oxford Foundation for Law, Justice and Society

Oxford 5th October 2012

Place of Britain in a future Europe

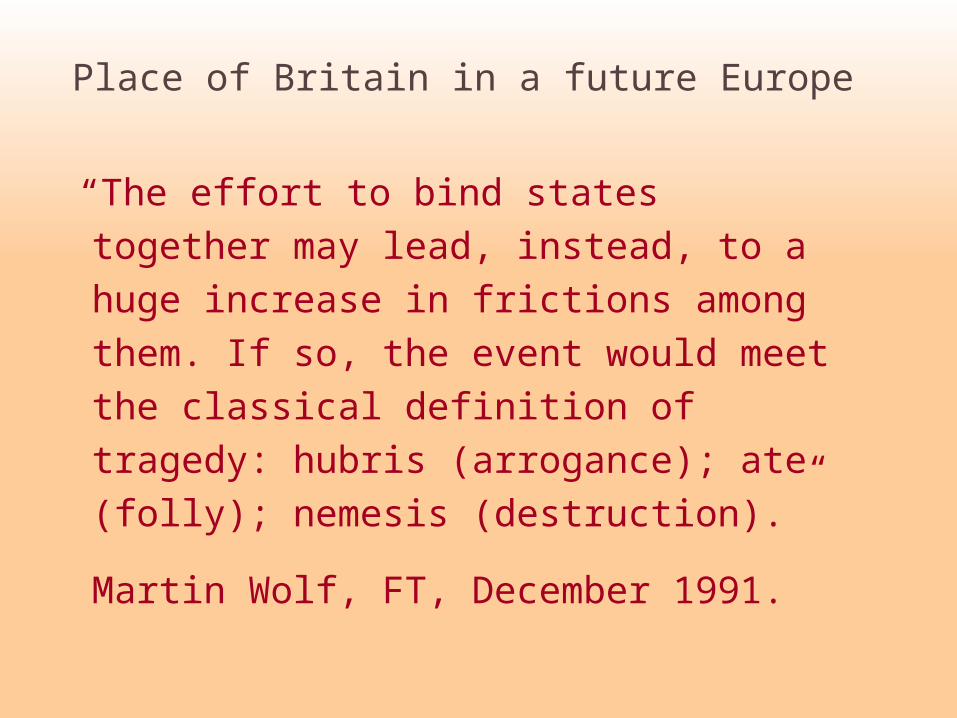

“The effort to bind states together may lead,

instead, to a huge increase in frictions among

them. If so, the event would meet the

classical definition of tragedy:

hubris (arrogance); ate (folly); nemesis

(destruction).”

Martin Wolf, FT, December 1991.

Place of Britain in a future Europe

4

Will the eurozone survive the crisis?

• Eurozone crisis:

– Sources of the crisis

– Symptoms of the crisis

– Solutions to the crisis

• UK in a new European Union

55

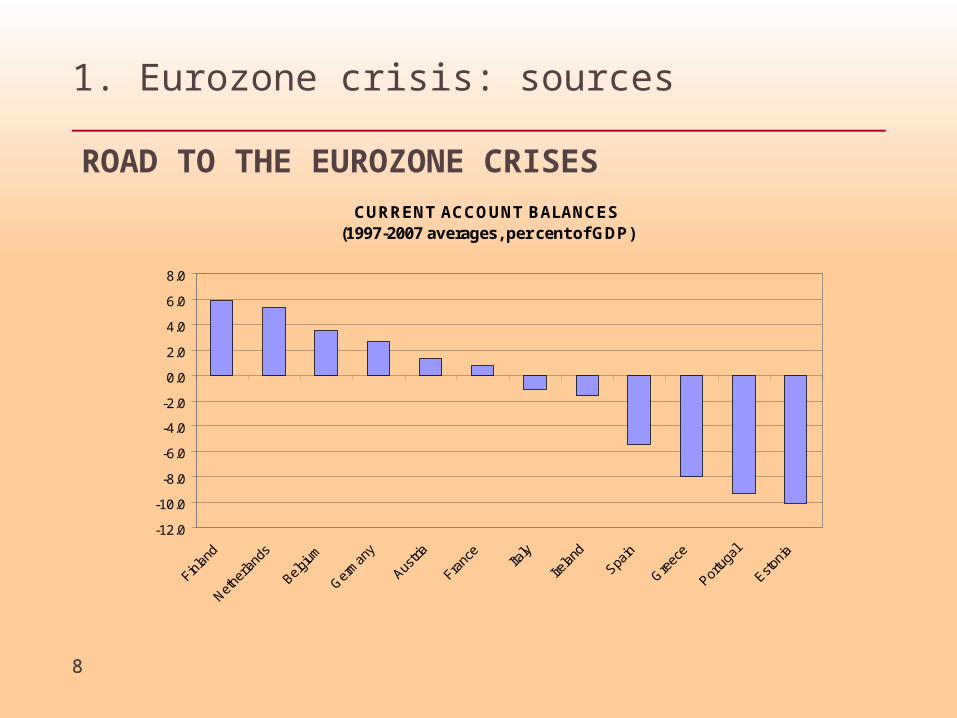

1. Eurozone crisis: sources

• This is not, in its origin, a fiscal crisis, but a balance of payments cum financial crisis.

• In the run up to the crisis, there were huge internal capital flows. These opened up current account imbalances and generated huge divergences in competitiveness.

• After 2008, cross-border private financial flows suffered a series of “sudden stops”. These caused, or aggravated, a fiscal crisis.

• The view that this is a fiscal crisis lets creditors blame debtors. This is bad economics and worse politics.

• The correct view that this is a financial crisis puts blame on both creditors and debtors. That is good economics and better politics.

66

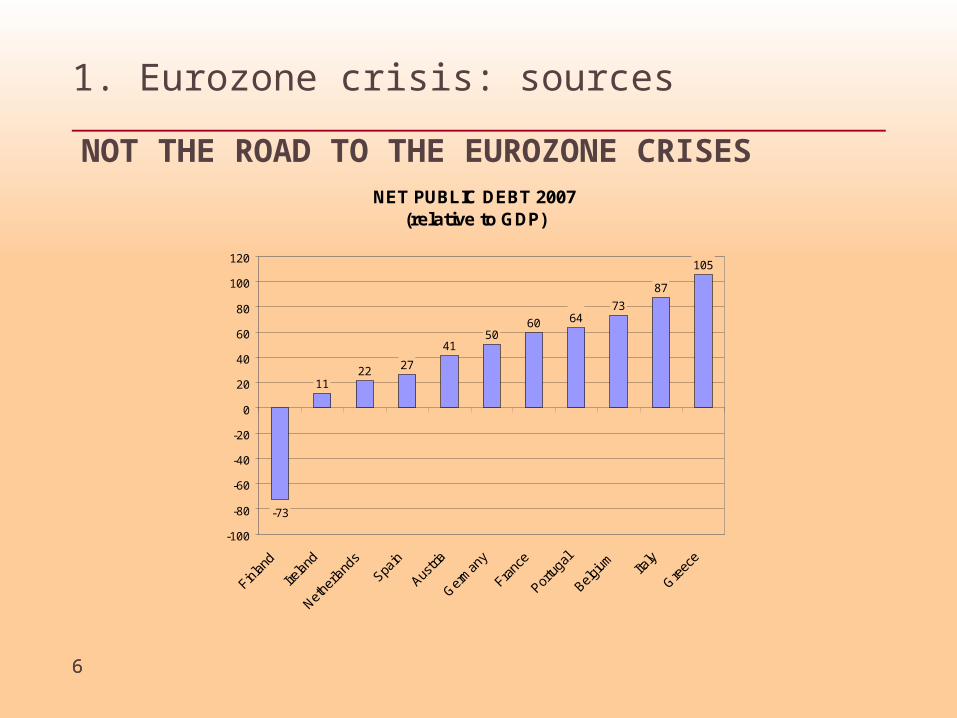

1. Eurozone crisis: sources

NOT THE ROAD TO THE EUROZONE CRISESNET PUBLIC DEBT 2007

(relative to GDP)

-73

1122 27

4150

60 6473

87

105

-100

-80

-60

-40

-20

0

20

40

60

80

100

120

Finlan

d

Irela

nd

Nethe

rland

s

Spain

Austri

a

Ger

man

y

Franc

e

Portu

gal

Belgiu

mIta

ly

Gre

ece

77

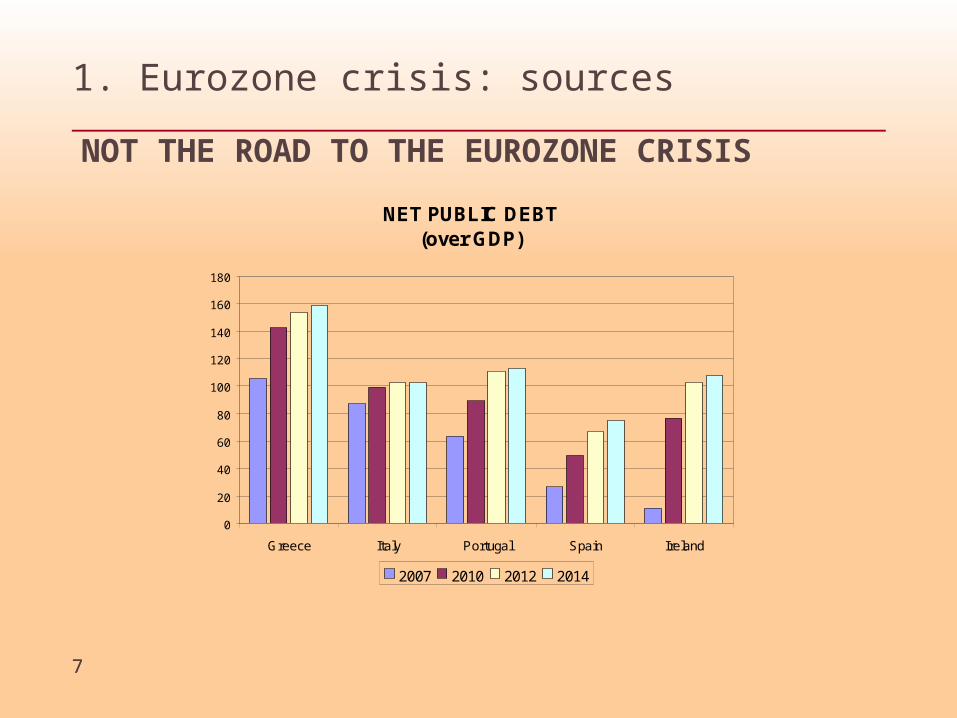

1. Eurozone crisis: sources

NOT THE ROAD TO THE EUROZONE CRISIS

NET PUBLIC DEBT(over GDP)

0

20

40

60

80

100

120

140

160

180

Greece Italy Portugal Spain Ireland

2007 2010 2012 2014

Source: IMF WEO database April 2012

88

1. Eurozone crisis: sources

CURRENT ACCOUNT BALANCES(1997-2007 averages, per cent of GDP)

-12.0

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

Finlan

d

Nethe

rland

s

Belgium

Germ

any

Austri

a

Franc

eIta

ly

Irelan

d

Spain

Greec

e

Portu

gal

Estonia

ROAD TO THE EUROZONE CRISES

99

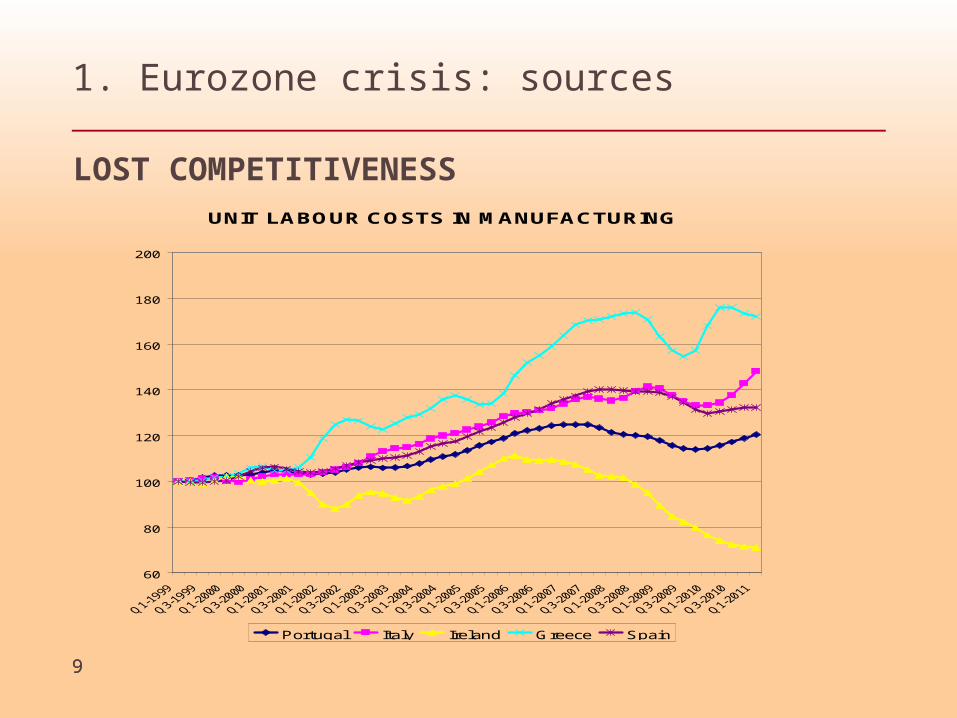

1. Eurozone crisis: sources

LOST COMPETITIVENESSUNIT LABOUR COSTS IN MANUFACTURING

60

80

100

120

140

160

180

200

Portugal Italy Ireland Greece Spain

10

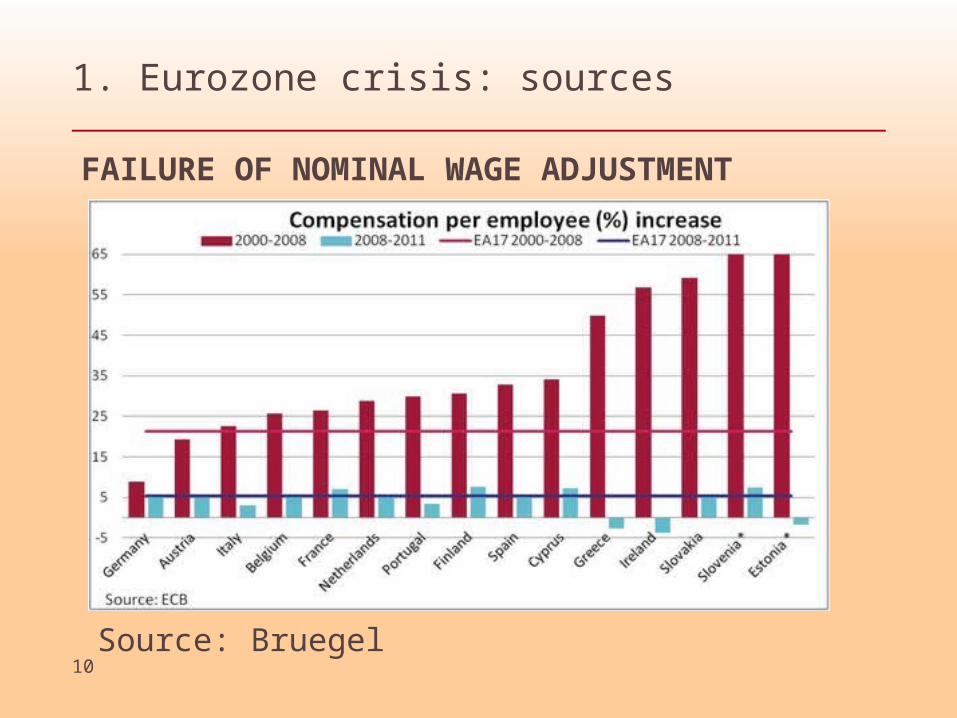

1. Eurozone crisis: sources

FAILURE OF NOMINAL WAGE ADJUSTMENT

Source: Bruegel

11

1. Eurozone crisis: sources

• Why were proponents of the eurozone unaware of the danger of cross-border financial flows and current account imbalances?

– They thought these flows were the purpose of the exercise;

– They thought currency risk was the only danger; and

– They thought they had eliminated currency risk.

• They were wrong:

– Currency risk is not the only danger and

– Currency risk cannot be eliminated, so long as the possibility of secession remains. It will re-emerge as credit risk.

11

12

1. Eurozone crisis: sources

• Even regions within countries can suffer the consequences of current account imbalances:

– These will show up as regional recessions;

– But, for regions within countries, mechanisms for handling the worst consequences of regional “busts” exist:

• Support of the financial system;

• Fiscal transfers; and

• Labour mobility.

– These work adequately.

12

13

1. Eurozone crisis: sources

• Eurozone member countries do not have such mechanisms of support.

• They are in a gold-standard type of mechanism: the adjustment mechanism was depression.

• It never seemed plausible that this could work – or would be allowed to work.

• As a senior Italian official told me: “we are not Latvia”.

13

14

1. Eurozone crisis: sources

• They did have a central bank, which helped. But, as Spain has discovered, support from the European Central Bank is not the same as having one’s own central bank.

• The contrast between Spain and the UK is striking. They have similar fiscal situations, but totally different interest rates on public debt.

• The explanation for this divergence between the two countries is liquidity, currency and default risk.

14

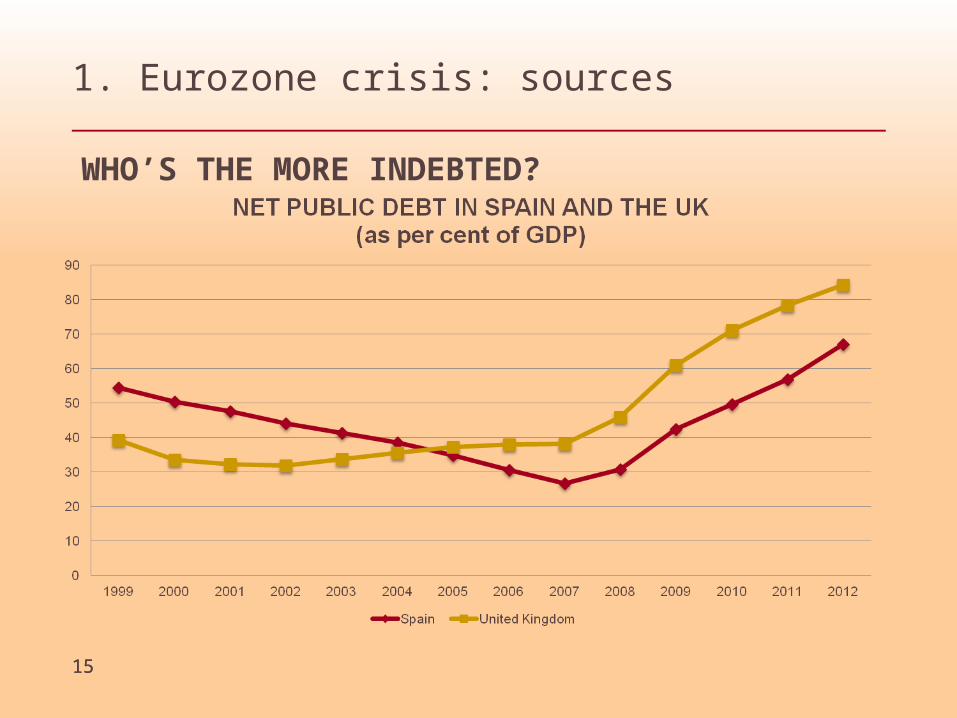

15

1. Eurozone crisis: sources

15

WHO’S THE MORE INDEBTED?

16

1. Eurozone crisis: sources

16

WHO’S THE MORE INDEBTED?

17

1. Eurozone crisis: sources

• The conclusion is that high-income countries embedded inside a currency union are more vulnerable to balance of payments cum financial crises than countries with floating exchange rates and their own central banks.

• They are more like emerging countries with exceptionally hard exchange-rate pegs.

• The idea that eliminating currency crises would eliminate crises was a gigantic error.

• The currency union replaced the brief currency crises of the exchange-rate mechanism with long-running solvency, employment and political crises.

17

18

1. Eurozone crisis: symptoms

• The symptoms of the crisis include:

– Dwindling cross-border finance, capital flight and bank runs;

– Private retrenchment, collapsing GDP and soaring unemployment;

– Exorbitant bond yields in deficit countries;

– Tighter links between domestic banks and their governments;

– Political and economic stress; and

– Rising political friction.

18

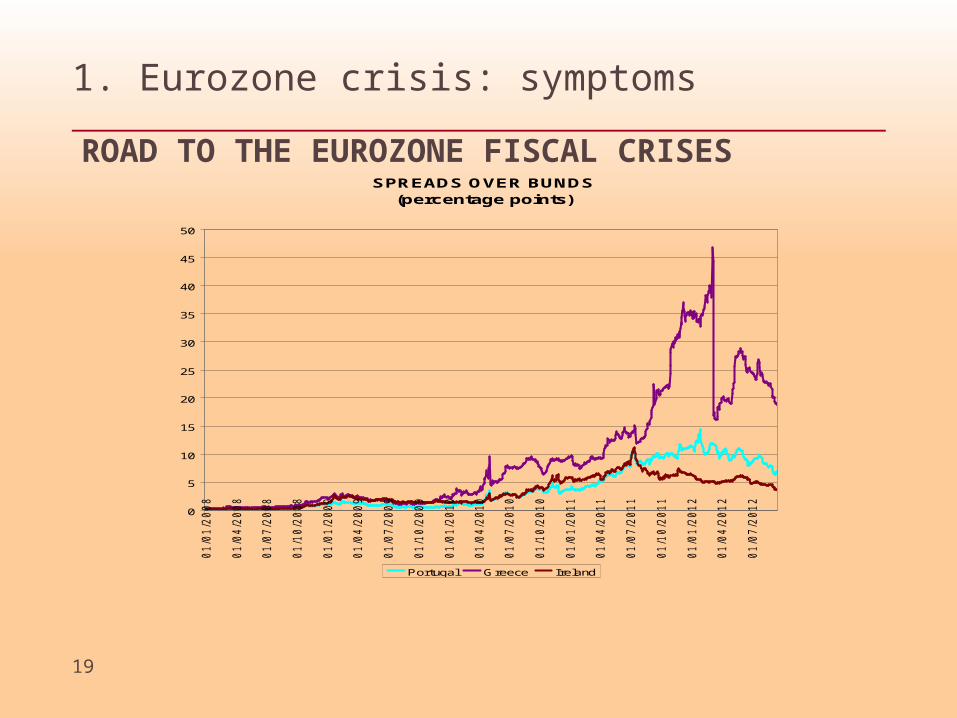

19

1. Eurozone crisis: symptoms

ROAD TO THE EUROZONE FISCAL CRISESSPREADS OVER BUNDS

(percentage points)

0

5

10

15

20

25

30

35

40

45

50

01/0

1/2

008

01/0

4/2

008

01/0

7/2

008

01/1

0/2

008

01/0

1/2

009

01/0

4/2

009

01/0

7/2

009

01/1

0/2

009

01/0

1/2

010

01/0

4/2

010

01/0

7/2

010

01/1

0/2

010

01/0

1/2

011

01/0

4/2

011

01/0

7/2

011

01/1

0/2

011

01/0

1/2

012

01/0

4/2

012

01/0

7/2

012

Portugal Greece Ireland

20

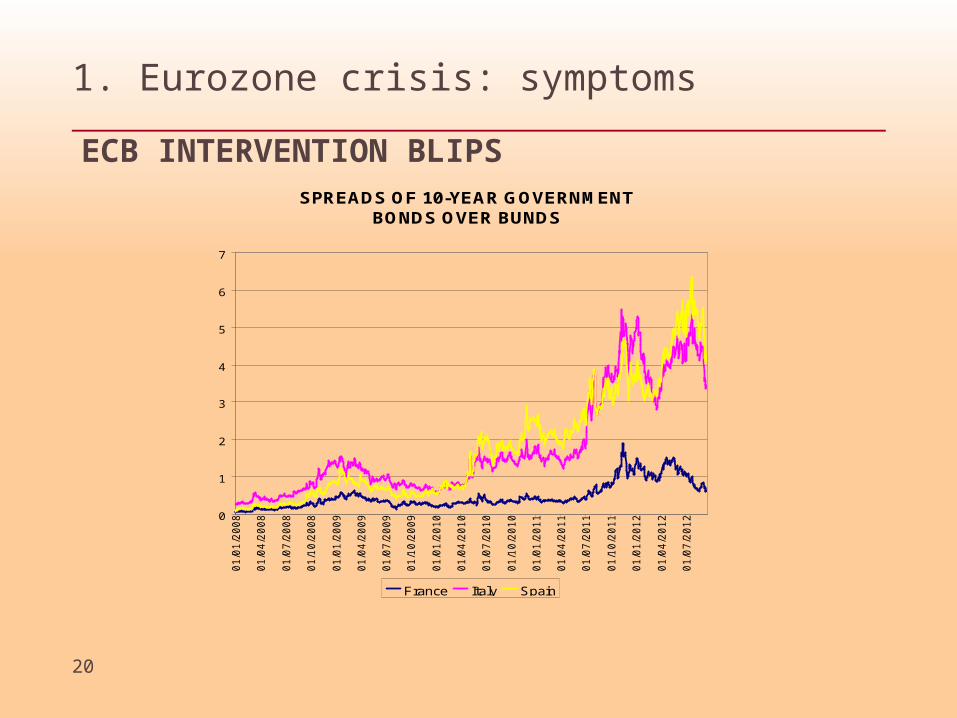

1. Eurozone crisis: symptoms

ECB INTERVENTION BLIPSSPREADS OF 10-YEAR GOVERNMENT

BONDS OVER BUNDS

0

1

2

3

4

5

6

7

01

/01

/20

08

01

/04

/20

08

01

/07

/20

08

01

/10

/20

08

01

/01

/20

09

01

/04

/20

09

01

/07

/20

09

01

/10

/20

09

01

/01

/20

10

01

/04

/20

10

01

/07

/20

10

01

/10

/20

10

01

/01

/20

11

01

/04

/20

11

01

/07

/20

11

01

/10

/20

11

01

/01

/20

12

01

/04

/20

12

01

/07

/20

12

France Italy Spain

21

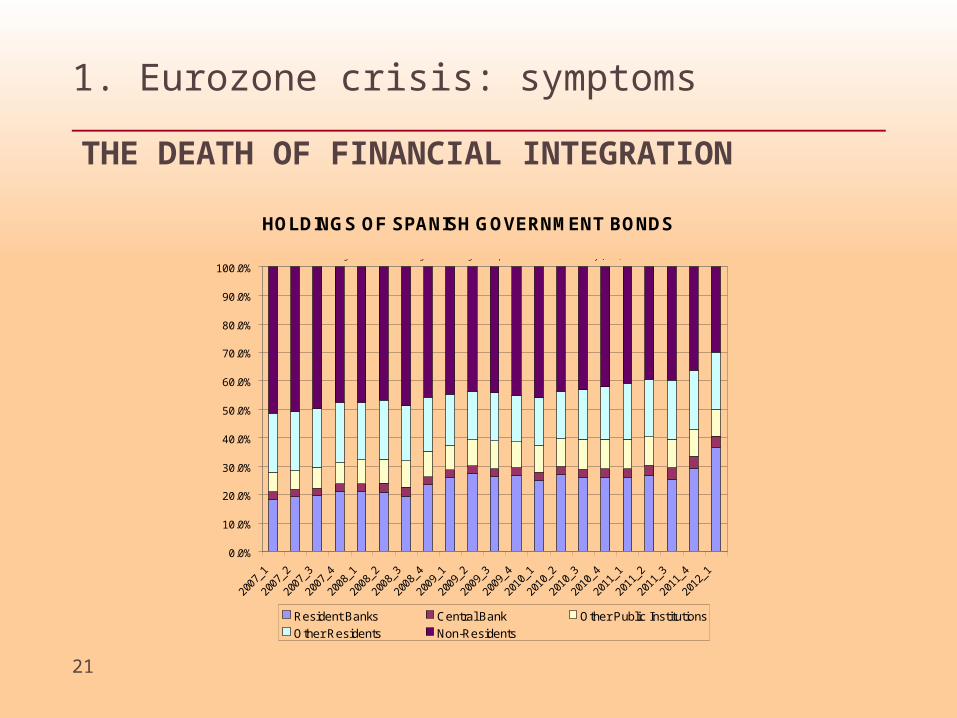

1. Eurozone crisis: symptoms

HOLDINGS OF SPANISH GOVERNMENT BONDS

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

2007

_1

2007

_2

2007

_3

2007

_4

2008

_1

2008

_2

2008

_3

2008

_4

2009

_1

2009

_2

2009

_3

2009

_4

2010

_1

2010

_2

2010

_3

2010

_4

2011

_1

2011

_2

2011

_3

2011

_4

2012

_1

Resident Banks Central Bank Other Public Institutions

Other Residents Non-Residents

Bruegel database of sovereign bond holdings developed in Merler and Pisani-Ferry (2012)

THE DEATH OF FINANCIAL INTEGRATION

22

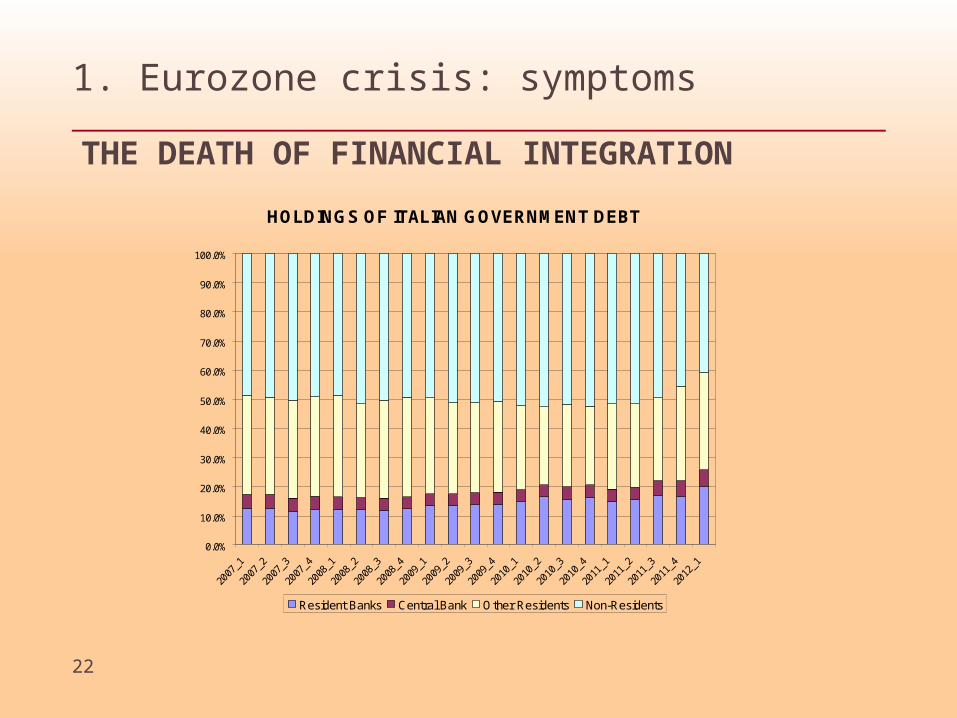

1. Eurozone crisis: symptoms

THE DEATH OF FINANCIAL INTEGRATION

HOLDINGS OF ITALIAN GOVERNMENT DEBT

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

2007

_1

2007

_2

2007

_3

2007

_4

2008

_1

2008

_2

2008

_3

2008

_4

2009

_1

2009

_2

2009

_3

2009

_4

2010

_1

2010

_2

2010

_3

2010

_4

2011

_1

2011

_2

2011

_3

2011

_4

2012

_1

Resident Banks Central Bank Other Residents Non-Residents

Bruegel database of sovereign bond holdings developed in Merler and Pisani-Ferry (2012)

2323

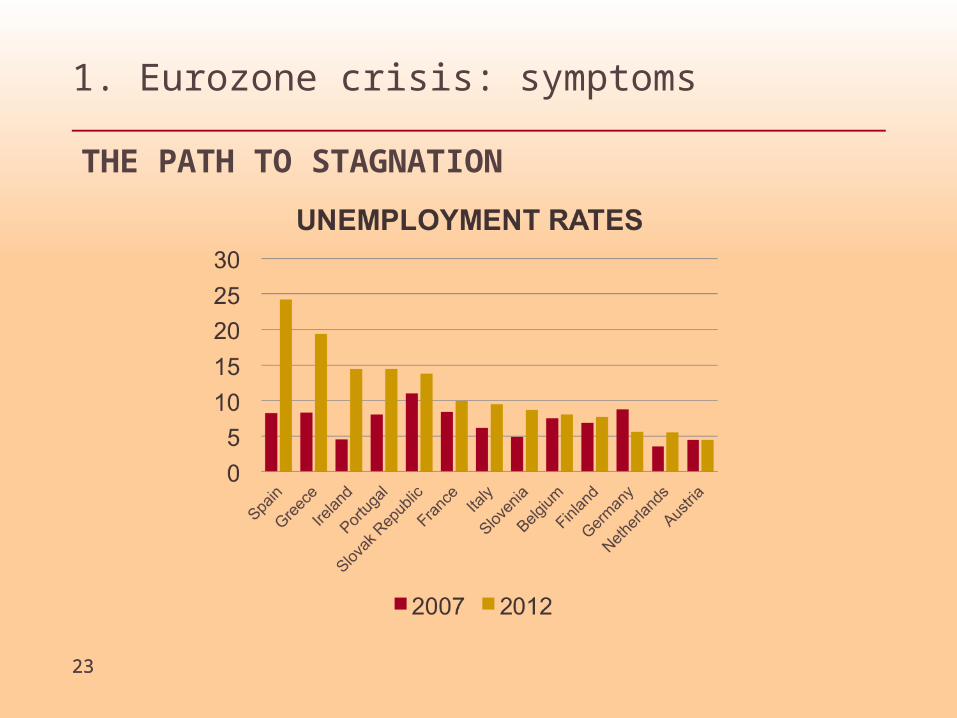

1. Eurozone crisis: symptoms

THE PATH TO STAGNATION

24

1. Eurozone crisis: solutions

• How is the eurozone going to resolve its crisis?

• I see two scenarios: the catastrophic and the painful:

– Partial or complete break-up; or

– An extended and painful period of adjustment, via depression and structural reform.

2525

1. Eurozone crisis: solutions

• Here are the challenges to be met if the currency union is to survive:

1. Debt write-offs: to clear up the legacy costs of the poorly structured and managed currency union, Mark I.

2. Financing: to prevent financial, fiscal and economic collapses. By “financing”, I mean an ability to maintain a working financial system and maintenance of manageable costs of government funding.

3. Adjustment: structural reforms and divergent inflation across the eurozone, with higher inflation and stronger final demand in core countries. This will take at least 5-10 years.

26

1. Eurozone crisis: solutions

• In the long term, the euro zone needs to be a minimum federal union

• This should include:

– A banking union: this would be possible, without fiscal backup, if (and only if) banks could be resolved without budgetary support.

– An adequate safety net: Eurobonds are one way to do this; and a bigger European Stability Mechanism, plus European Central Bank support, is another. A permanent large-scale “transfer union” is indeed undesirable.

– A supportive central bank.

• The fiscal compact cannot be a binding constraint.

27

1. Eurozone crisis: solutions

• Willingness to act was substantial, once it became obvious that the original design had failed. But willingness to act has also been insufficient.

• The obstacles to action are of three kinds:

– Economic: it is hard to make this work;

– Ideological: the difference in economic perspectives are large; and

– Political: the countries and peoples do not like one another very much and do not identify with one another very much.

• Such reforms also raise huge questions about political legitimacy.

• It will be a bad marriage or a messy divorce.

28

2. Britain in a new Europe

• What does this mean for Britain?

• It means fundamental change in relations with the rest of the EU, for sure.

• But the nature of the fundamental change depends on the outcome for the eurozone over which Britain has little, if any, influence.

• The way I analyse this question is as follows:

– The status quo in the eurozone is untenable;

– Thus, the eurozone will either fragment, so becoming more homogeneous, or it will become much more integrated.

29

2. Britain in a new Europe

• If the eurozone fragments, it will either survive, in large part, or disappear altogether;

– If it survives, in part, it might do so in one big block (minus, say, Greece) or after the exit of creditor nations (led by Germany) or after the exit of a group of debtor nations;

– If it breaks up, in whole or in part, the EU will be in a legal limbo, since members are required to be in the eurozone;

– The UK will need to decide on where it would fit into an EU that would follow a partial or complete break up of the eurozone.

30

2. Britain in a new Europe

• If the eurozone stays together, it will have to become a banking union, which will force it to become a fiscal union, in some part:

– This will require more fiscal and financial discipline and more fiscal and financial support.

– That would transform Britain’s position, since the questions that most affect it will increasingly be decided within a new quasi-federal Eurozone grouping. That is particularly true of financial regulation.

31

2. Britain in a new Europe

• What would the options for Britain then be?

– Joining the eurozone.

– Staying inside the EU and accepting the outcome of Eurozone decisions, over which Britain might have little influence.

– Seeking to move into the European Economic Area, while accepting that it would have no influence on single market regulation (including on finance).

– This would also put the UK outside the common agricultural policy, common fisheries policy, co-operation over justice and home affairs, the common foreign and security policy and full budgetary demands.

– Moving into EFTA.

– But what would the response of other members be to these options?

32

2. Britain in a new Europe

• Political implications are worth thinking about:

– We are talking about massive upheavals in relations among members of the Eurozone and members of the EU;

– One possibility is that if the Eurozone became more federal, the UK would break up (or at least be more likely to break up). Similar developments seem likely in other EU members (Spain?);

– The big point is that the future of the EU would become wildly unpredictable