Embed Size (px)

DESCRIPTION

PORTFOLIO COMMITTEE MEETING FUTURE OF DENEL SAAB AEROSTRUCTURES (PTY) LTD 24 MAY 2011. DENEL SAAB AEROSTRUCTURES (PTY) LTD (DSA) Vision:The reliable African link in the global aerostructures supply chain - PowerPoint PPT Presentation

Citation preview

PORTFOLIO COMMITTEE MEETING

FUTURE OF DENEL SAAB

AEROSTRUCTURES (PTY) LTD

24 MAY 2011

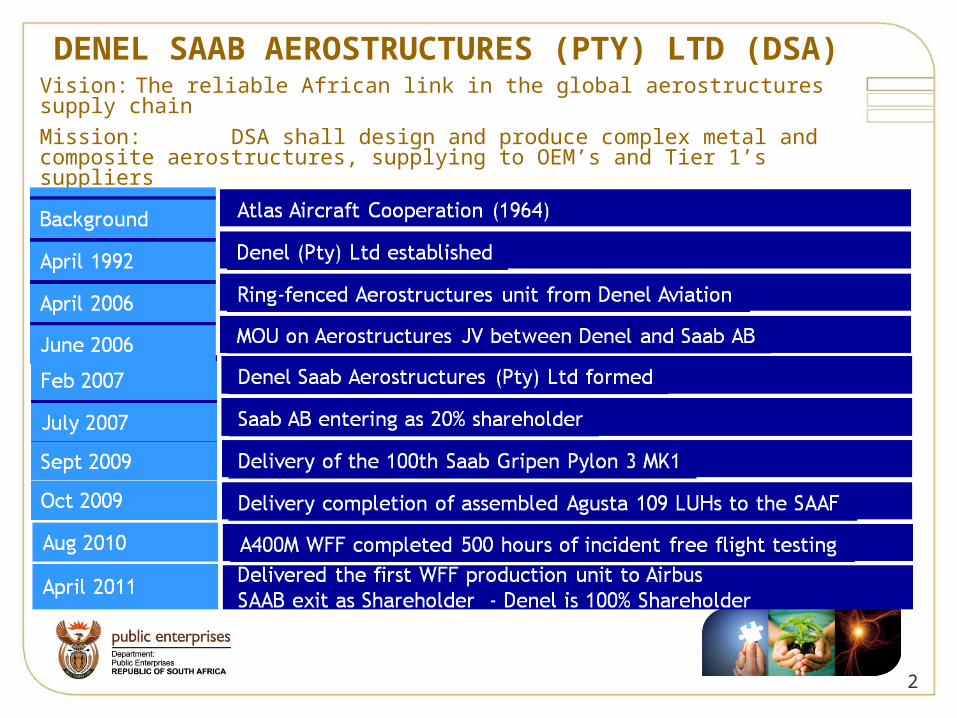

DSA Vision, Mission and MilestonesDENEL SAAB AEROSTRUCTURES (PTY) LTD (DSA)

Vision: The reliable African link in the global aerostructures supply chain

Mission: DSA shall design and produce complex metal and composite aerostructures, supplying to OEM’s and Tier 1’s suppliers

2

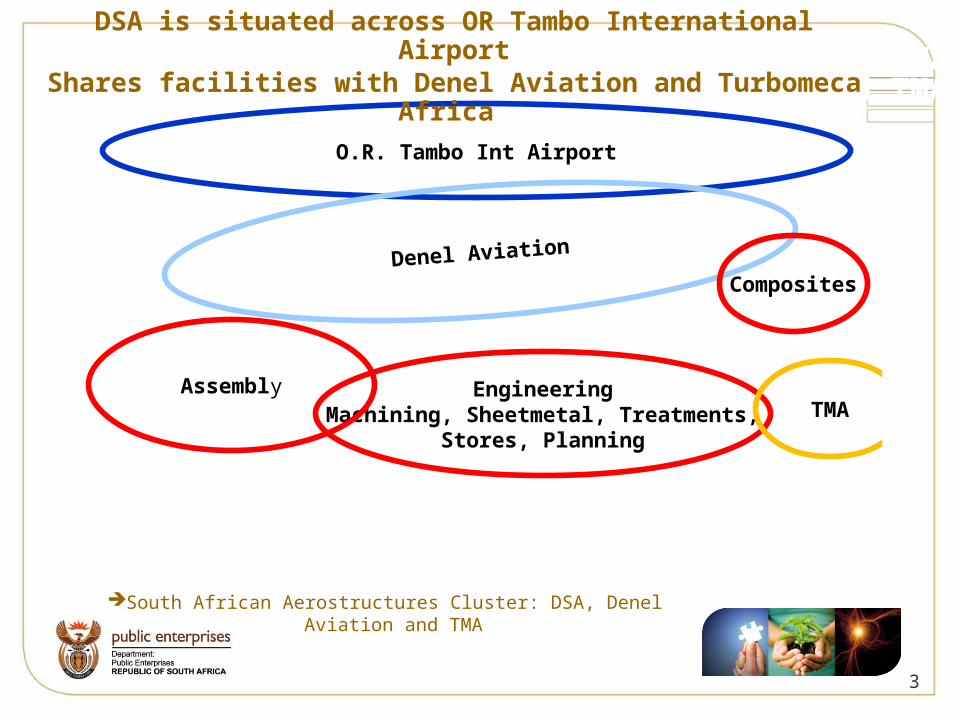

DDSAdDSADSA is situated across OR Ta

Share facilities with Denel Aviation and TMA

EngineeringMachining, Sheetmetal, Treatments,

Stores, Planning

Assembly

O.R. Tambo Int Airport

Denel Aviation

Composites

TMA

South African Aerostructures Cluster: DSA, Denel Aviation and TMA

DSA is situated across OR Tambo International AirportShares facilities with Denel Aviation and Turbomeca

Africa

3

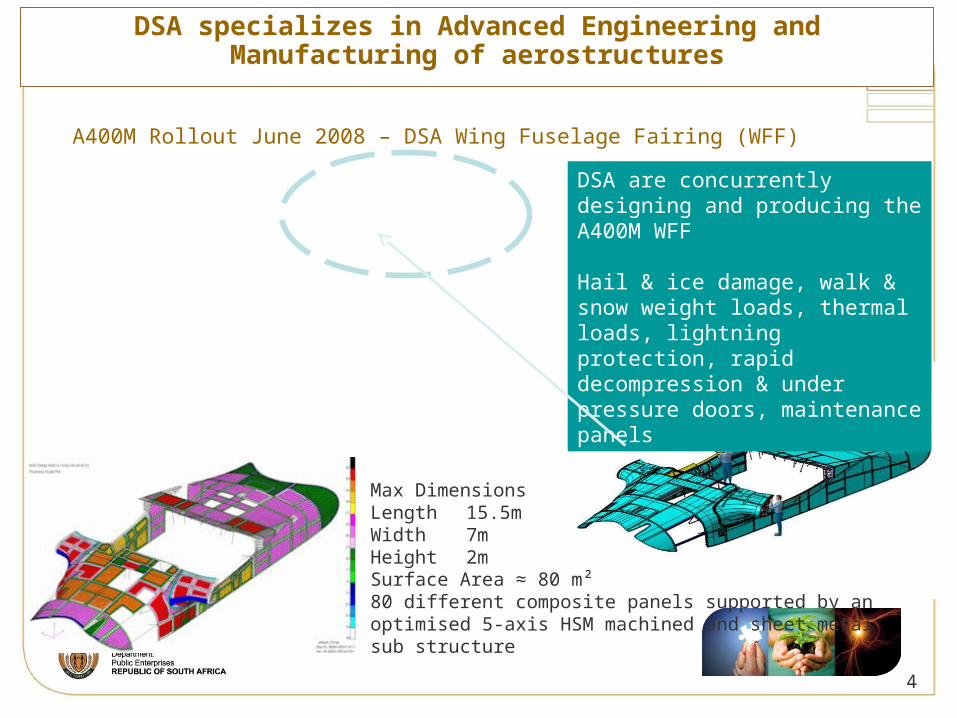

Max DimensionsLength 15.5mWidth 7mHeight 2mSurface Area ≈ 80 m²80 different composite panels supported by an optimised 5-axis HSM machined and sheet metal sub structure

DSA are concurrently designing and producing the A400M WFF

Hail & ice damage, walk & snow weight loads, thermal loads, lightning protection, rapid decompression & under pressure doors, maintenance panels

A400M Rollout June 2008 – DSA Wing Fuselage Fairing (WFF)

DSA specializes in Advanced Engineering and Manufacturing of aerostructures

4

5

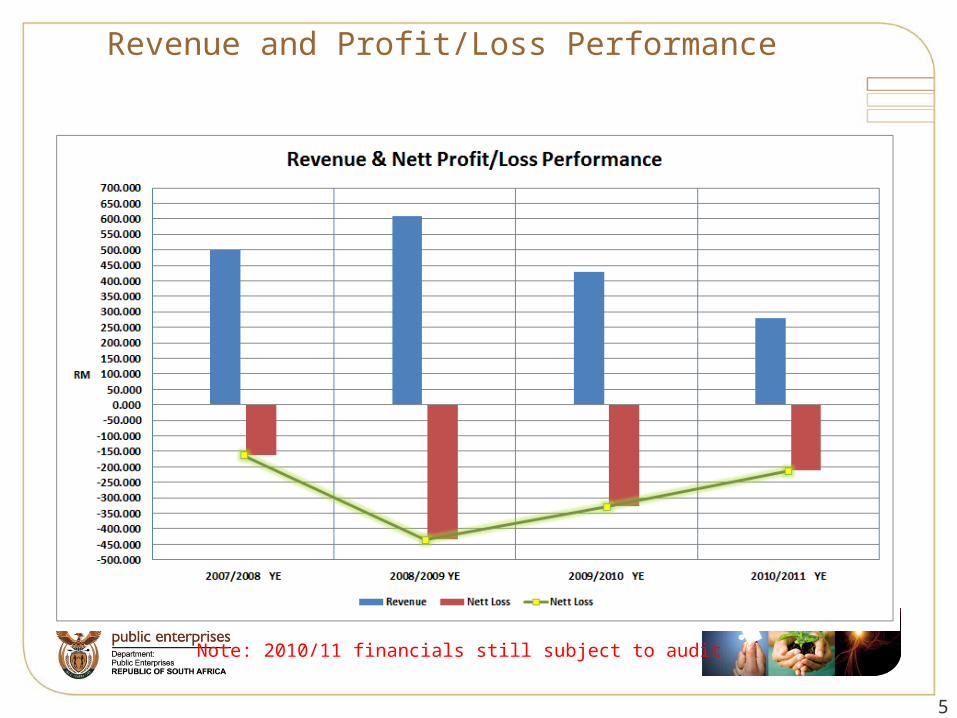

DSA Revenue and Profit/Loss Performance

Note: 2010/11 financials still subject to audit

Current Status

Status:• DSA remains loss-making and a key strategic challenge to Denel (EBIT Feb 2011 – (R259m); March 2010 – (R283m) and March 2009 – (R444m)• SAAB has exited the business in April 2011. SAAB owned 20% of the business since 2007.• Improved performance for 2010/2011 expected – Audit is in progress

Restructuring:During the year under review, DSA exceeded Sales, Cash and EBIT performance targets

through restructuring of the business including:

• Significantly reducing labour costs.

• Significant improvement in financial management and governance.

• Reducing rental costs through space optimisation.

• Implementing shared services with Denel Aviation and outsourcing non-core activities.

• Transferring the steel-heat treatment facility to TMA.

• Audited improvement in climate survey from 65% to 74%.

Operations:The operational turnaround of the business continues with a marked improvement in

delivery and quality. Airbus in particular has expressed satisfaction with DSA’s performance against key milestones on the A400M programme. Margins on all contracts however remain under pressure and are currently unacceptable.

Current Status

6

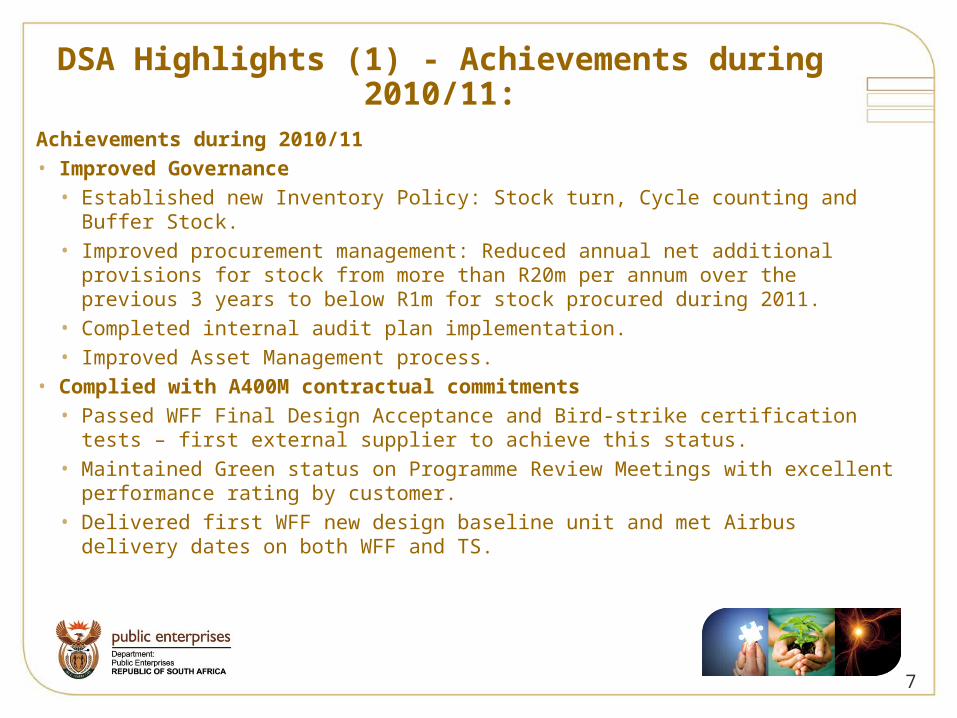

DSA Highlights (1) - Achievements during 2010/11:

Achievements during 2010/11• Improved Governance

• Established new Inventory Policy: Stock turn, Cycle counting and Buffer Stock.

• Improved procurement management: Reduced annual net additional provisions for stock from more than R20m per annum over the previous 3 years to below R1m for stock procured during 2011.

• Completed internal audit plan implementation.• Improved Asset Management process.

• Complied with A400M contractual commitments • Passed WFF Final Design Acceptance and Bird-strike certification tests – first

external supplier to achieve this status.• Maintained Green status on Programme Review Meetings with excellent

performance rating by customer.• Delivered first WFF new design baseline unit and met Airbus delivery dates

on both WFF and TS.

7

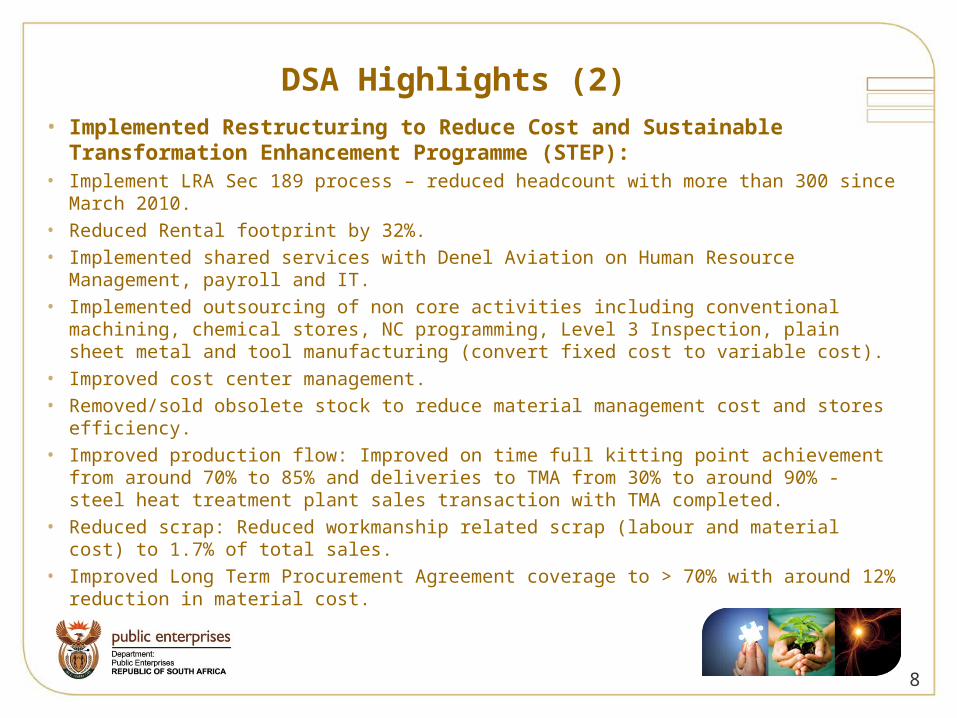

DSA Highlights (2)• Implemented Restructuring to Reduce Cost and Sustainable

Transformation Enhancement Programme (STEP):• Implement LRA Sec 189 process – reduced headcount with more than 300 since March

2010.• Reduced Rental footprint by 32%.• Implemented shared services with Denel Aviation on Human Resource Management,

payroll and IT.• Implemented outsourcing of non core activities including conventional machining,

chemical stores, NC programming, Level 3 Inspection, plain sheet metal and tool manufacturing (convert fixed cost to variable cost).

• Improved cost center management.• Removed/sold obsolete stock to reduce material management cost and stores

efficiency.• Improved production flow: Improved on time full kitting point achievement from around

70% to 85% and deliveries to TMA from 30% to around 90% - steel heat treatment plant sales transaction with TMA completed.

• Reduced scrap: Reduced workmanship related scrap (labour and material cost) to 1.7% of total sales.

• Improved Long Term Procurement Agreement coverage to > 70% with around 12% reduction in material cost.

8

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

900.0

12/2009 03/2010 06/2010 09/2010 12/2010 03/2011 06/2011

Rm

DSA Completed Headcount Reduction

LABOUR COST R'm

Employee Analysis

Job CategoryHeads

May 2011

Senior Management 7

Management 37

Engineer 25

Technical 85

Planner 20

Artisan 113

Operator 35

Administrative 55

Apprentice 20

Total 397

9

No o

f p

eop

le

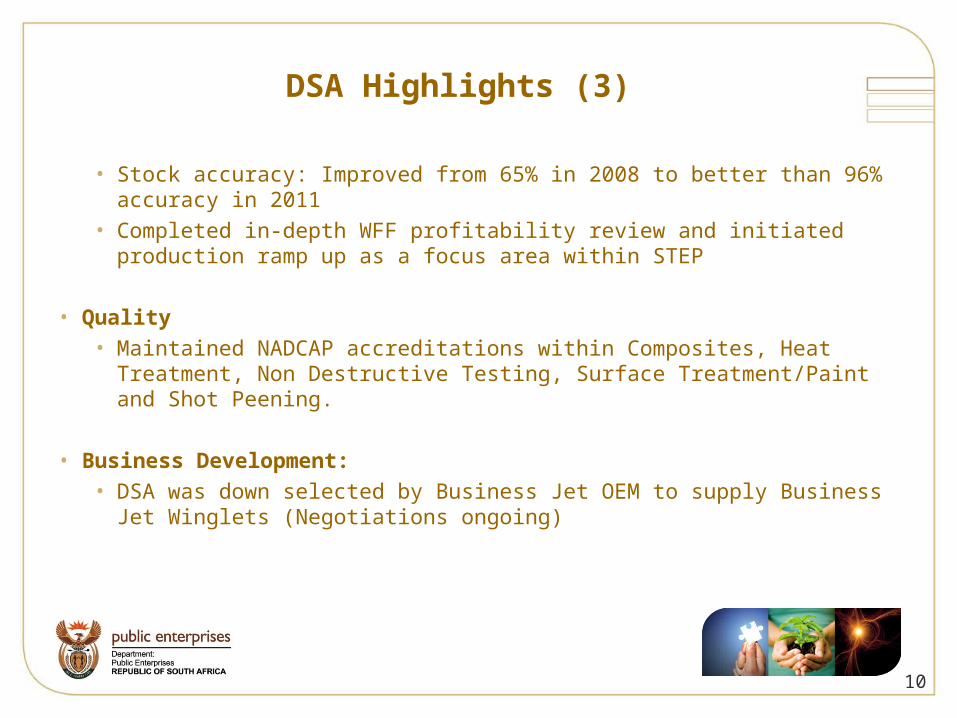

DSA Highlights (3)

• Stock accuracy: Improved from 65% in 2008 to better than 96% accuracy in 2011

• Completed in-depth WFF profitability review and initiated production ramp up as a focus area within STEP

• Quality• Maintained NADCAP accreditations within Composites, Heat Treatment,

Non Destructive Testing, Surface Treatment/Paint and Shot Peening.

• Business Development:• DSA was down selected by Business Jet OEM to supply Business Jet

Winglets (Negotiations ongoing)

10

Strategic Scenarios

• Domestic Transfer to Aerosud

• Aerosud submitted an unsolicited conditional proposal to acquire DSA in December 2010.

• Discussions are on-going.

• Further announcements can be made once the discussions have been finalised.

• Revised Business Plan (in Process)

The latest DSA revised business plan includes the following key interventions:

• Building a robust revenue pipeline. International OEM’s targeted:

• Spirit Aerosystems

• Hondajet

• Gulfstream

• Lockheed Martin

• Contract negotiations with key customers

• Cash flow management

• Improving balance sheet solvency

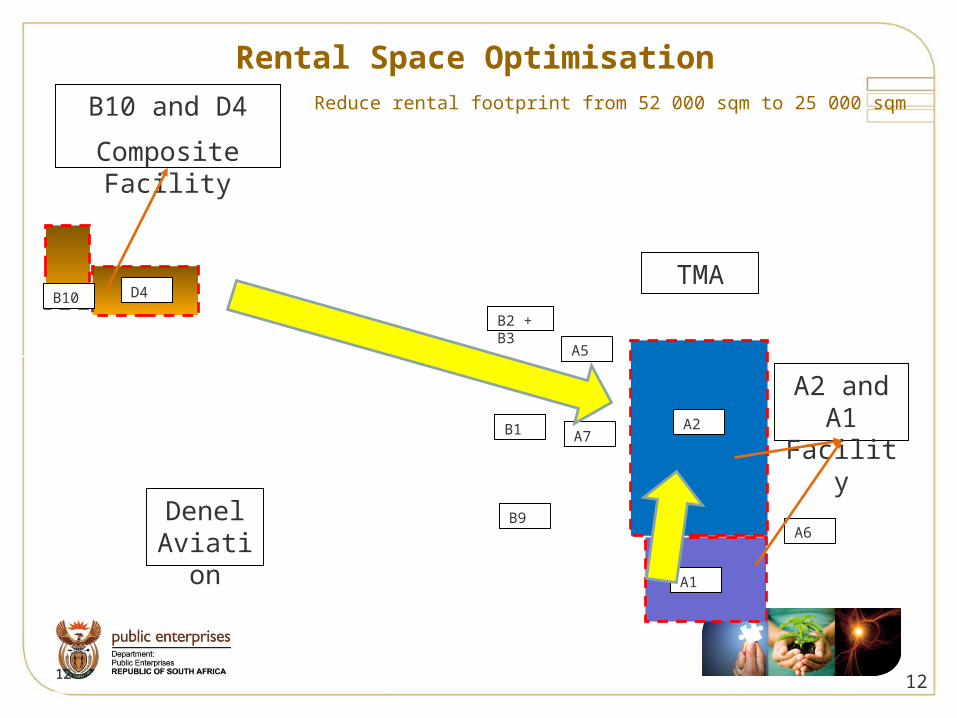

• A further reduction in the rental footprint from 52 000m2 to 25 000m2 through consolidating all activities into the A2 building including the composites facility.

• Further outsourcing of non core activities to reduce fix costs to variable costs.

Strategic Scenarios

11

Rental Space Optimisation

12

A2 and A1 Facility

12

D4B10

B10 and D4

Composite Facility

B2 + B3

A5

A7

A1

A6

A2B1

B9

Reduce rental footprint from 52 000 sqm to 25 000 sqm

TMA

Denel Aviation

12

13

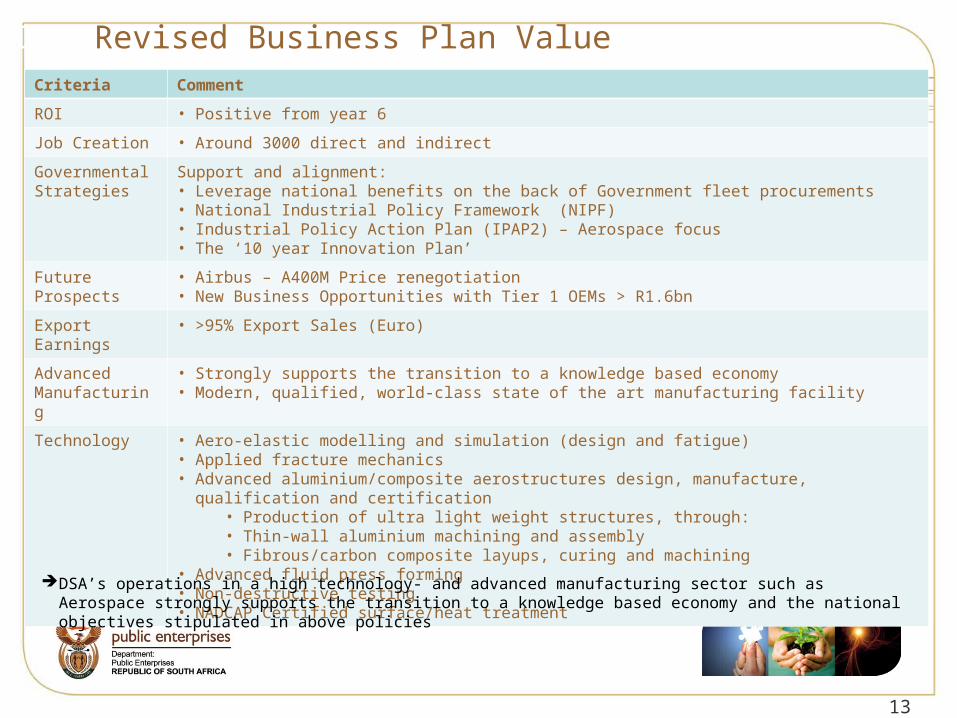

DSA Revised Business Plan ValueCriteria Comment

ROI • Positive from year 6

Job Creation • Around 3000 direct and indirect

Governmental Strategies

Support and alignment:• Leverage national benefits on the back of Government fleet procurements• National Industrial Policy Framework (NIPF)• Industrial Policy Action Plan (IPAP2) – Aerospace focus• The ‘10 year Innovation Plan’

Future Prospects

• Airbus – A400M Price renegotiation• New Business Opportunities with Tier 1 OEMs > R1.6bn

Export Earnings

• >95% Export Sales (Euro)

Advanced Manufacturing

• Strongly supports the transition to a knowledge based economy • Modern, qualified, world-class state of the art manufacturing facility

Technology • Aero-elastic modelling and simulation (design and fatigue)• Applied fracture mechanics• Advanced aluminium/composite aerostructures design, manufacture, qualification and

certification • Production of ultra light weight structures, through:• Thin-wall aluminium machining and assembly• Fibrous/carbon composite layups, curing and machining

• Advanced fluid press forming• Non-destructive testing• NADCAP Certified surface/heat treatment

DSA’s operations in a high technology- and advanced manufacturing sector such as Aerospace strongly supports the transition to a knowledge based economy and the national objectives stipulated in above policies

13

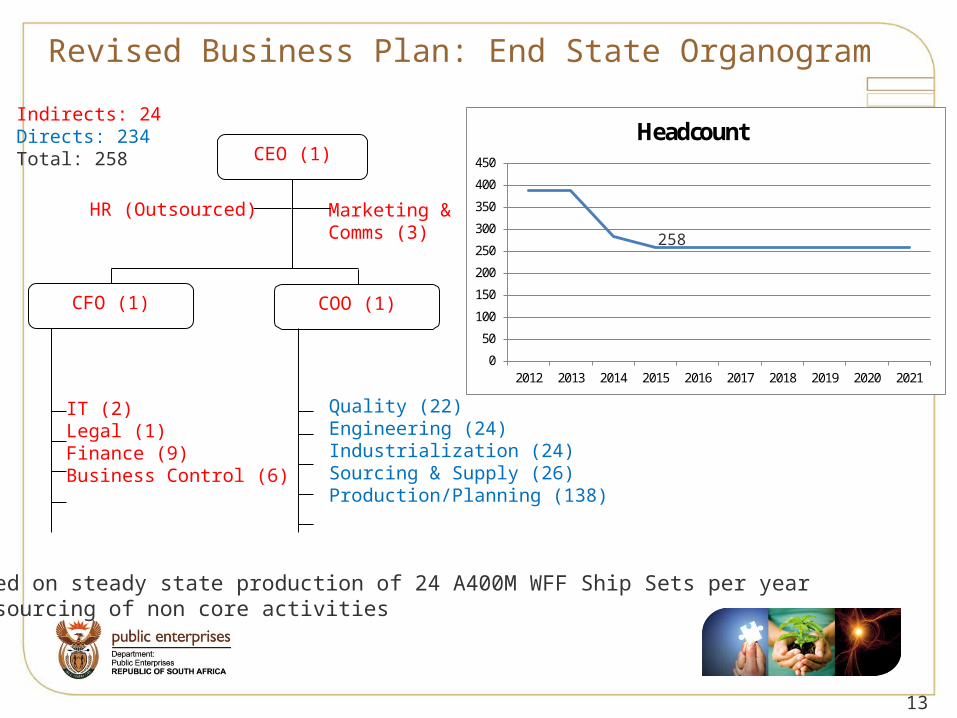

Revised Business Plan: End State Organogram

CEO (1)

COO (1)

Marketing &Comms (3)

Indirects: 24Directs: 234Total: 258

CFO (1)

IT (2)Legal (1)Finance (9)Business Control (6)

Quality (22)Engineering (24)Industrialization (24)Sourcing & Supply (26)Production/Planning (138)

• Based on steady state production of 24 A400M WFF Ship Sets per year• Outsourcing of non core activities

HR (Outsourced)

0

50

100

150

200

250

300

350

400

450

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Headcount 7F

258

A40

• DSA’s total economic impact is conservatively estimated to be:• Around 3000 jobs• R760 million consumer revenue• R180 million in taxes• Around R400 million of future export revenue per annum.

• IPAP 2 2011/12 – 13/14 released by the DTI in April 2011 has identified Advanced materials and Aerospace under Cluster 3 – Sectors with Potential for Long-Term Advanced Capabilities:

• Aerospace and Defence sector profile is a critical and pervasive generator of new technologies and is crucial to future innovation in South Africa.

• Significant progress has been achieved in developing recognition by and confidence from global original equipment manufacturers (OEM’s) in aerospace.

• With DSA’ operating in a high technology- and advanced manufacturing sector such as Aerospace, falls within the ambit of IPAP 2 long term advanced manufacturing capabilities

DSA Economic Impact

15

Way Forward

• Discussions with Aerosud continuing

• Implementation of revised business plan

• Funding for DSA remains a critical issue

16

THANK YOU