Embed Size (px)

Citation preview

POST PRIVATIZATION IMPACT ASSESSMENT PRELIMINARY REVIEW OF 4 COMPANIES

October 17, 2006 This publication was produced for review by the United States Agency for International Development. It was prepared by Lionel Knight, Jr.

POST PRIVATIZATION IMPACT ASSESSMENT PRELIMINARY REVIEW OF 4 COMPANIES TECHNICAL ASSISTANCE FOR POLICY REFORM II CONTRACT NUMBER: 263-C-00-05-00063-00 BEARINGPOINT, INC. USAID/EGYPT POLICY AND PRIVATE SECTOR OFFICE OCTOBER 17, 2006 AUTHOR: LIONEL KNIGHT SO 16 POST PRIVATIZATION ASSESSMENT

DISCLAIMER: The author’s views expressed in this publication do not necessarily reflect the views of the United States Agency for International Development or the United States Government.

CONTENTS

I. EXECUTIVE SUMMARY................................................................................... 2

Background and Introduction ................................................................................. 2 Methodology of the Study ...................................................................................... 2 Limitations of the Study.......................................................................................... 3 Overall Conclusions and Findings of the Study ..................................................... 4 Summary of Individual Company Conclusions and Findings .............................. 10

San Stefano Hotel Complex.................................................................... 10 Abu Zaabal fertilizer and chemicals........................................................ 10 National Paper Company........................................................................ 11 Bisco misr................................................................................................ 11

II. SUMMARY OF COMPANY ASSESSMENTS POST–PRIVATIZATION.........................................................................................13

Abu Zaabal Fertilizer & Chemical Company........................................................ 14 Company Background ............................................................................ 15 Privatization History and Information ...................................................... 15 Pre and Post Privatization Trends Analysis............................................ 15 Conclusions and Findings....................................................................... 20

Bisco Misr............................................................................................................. 23 Company Background ............................................................................ 24 Privatization History and Information ...................................................... 24 Pre and Post-Privatization Trends Analysis............................................ 25 Conclusions and Findings:...................................................................... 28

National Paper Co................................................................................................ 29 Company Background ............................................................................ 30 Privatization History and Information ...................................................... 30 Pre and Post Privatization Trends Analysis............................................ 30 Conclusions and Findings....................................................................... 32

San Stefano Hotel ................................................................................................ 33 Background............................................................................................. 34 San Stefano Complex ............................................................................. 35 Privatization Trends Analysis.................................................................. 35 Conclusions and Findings:...................................................................... 36

III. APPENDICES ................................................................................................38 Appendix I- Company Questionnaire................................................................... 39

Post-Privatization Study Questionnaire .................................................. 39 Appendix II- Company Interviewees .................................................................... 44

LIST OF TABLES, GRAPHS AND PHOTOS

I. TABLES Table 1: Privatization Method and New Ownership .......................................... 4

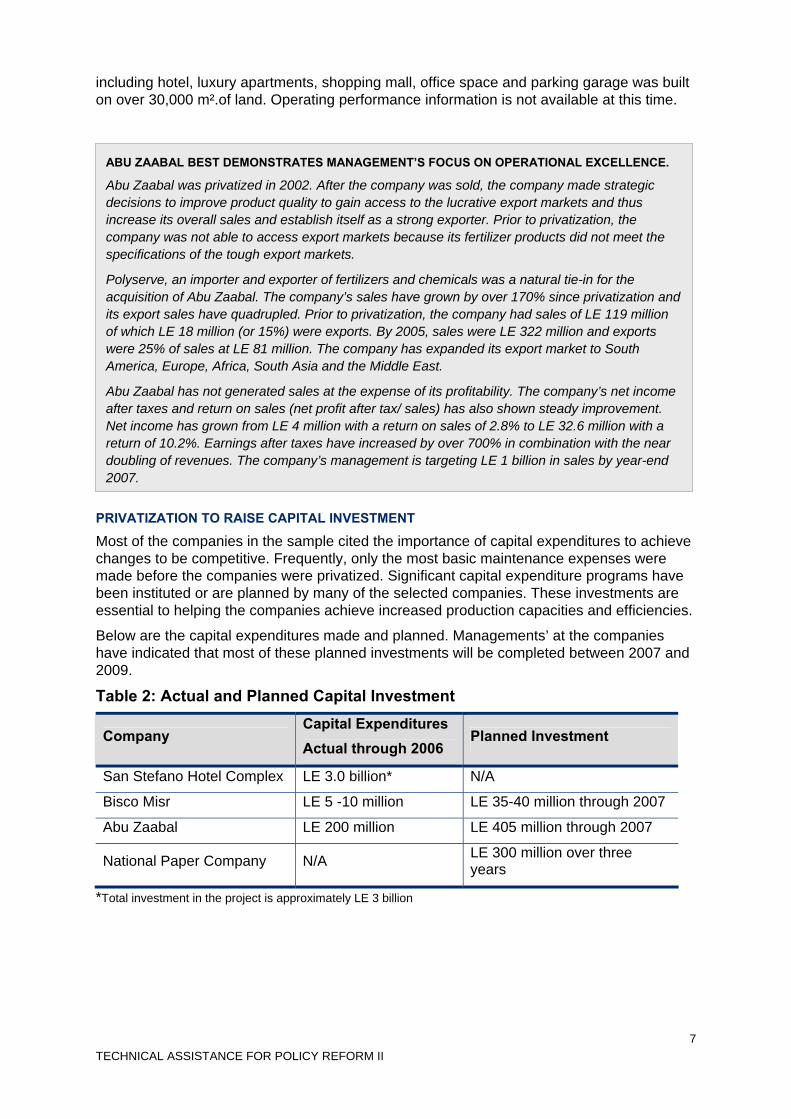

Table 2: Actual and Planned Capital Investment .............................................. 7

Table 3: Initial Sales Proceeds by Company .................................................... 8

Table 4: Revenues and Net Income-Post Privatization .................................. 15

Table 5: Abu Zaabal Revenues by Domestic and Export Sales ..................... 16

Table 6: Abu Zaabal Post Privatization Net Profits and Return on Sales ....... 17

Table 7: Abu Zaabal Key Labor Statistics- Pre and Post- Privatization .......... 18

Table 8: Bisco Key Financial Results.............................................................. 24

Table 9: Bisco Misr Revenues- Pre and Post Privatization............................. 26

Table 10: Bisco Misr Income and Margins Pre and Post Privatization ........... 26

Table 11: National Paper Revenues and Net Income Pre and Post-Privatization……………………………………………………………… ………...31

II. GRAPHS Graph 1: Abu Zaabal Revenues ..................................................................... 16

Graph 2: Abu Zaabal Change in Total Revenues ........................................... 17

Graph 3: Abu Zaabal Profitability .................................................................... 18

Graph 4: Abu Zaabal Impact on Labor............................................................ 19

Graph 5: Abu Zaabal Change in Annual Wages............................................. 19

III. PHOTOS PHOTO1: ABU ZAABAL CO.-SIAB UNIT FOR T.S.P. (TRIPLE TRI CALCIUM PHOSPHATE) .................................................................................................... 21

PHOTO 2: ABU ZAABAL CO.-STORAGE FOR G.S.S.P....................................... 21

PHOTO 3: ABU ZAABAL CO.-FUTURE GRANULATING PLANT (500 TON/DAY) . 21

PHOTO 4: ABU ZAABAL CO.-GRANULATED GSSP FERTILIZER-99% EXPORTED... 22

PHOTO 5: ABU ZAABAL CO.-GRANULATING PLANT- ABU ZAABAL TECHNOLOGY ... 22

PHOTO 6: ABU ZAABAL CO.-GRANULATING MACHINE-NEW EQUIPMENT .............. 22

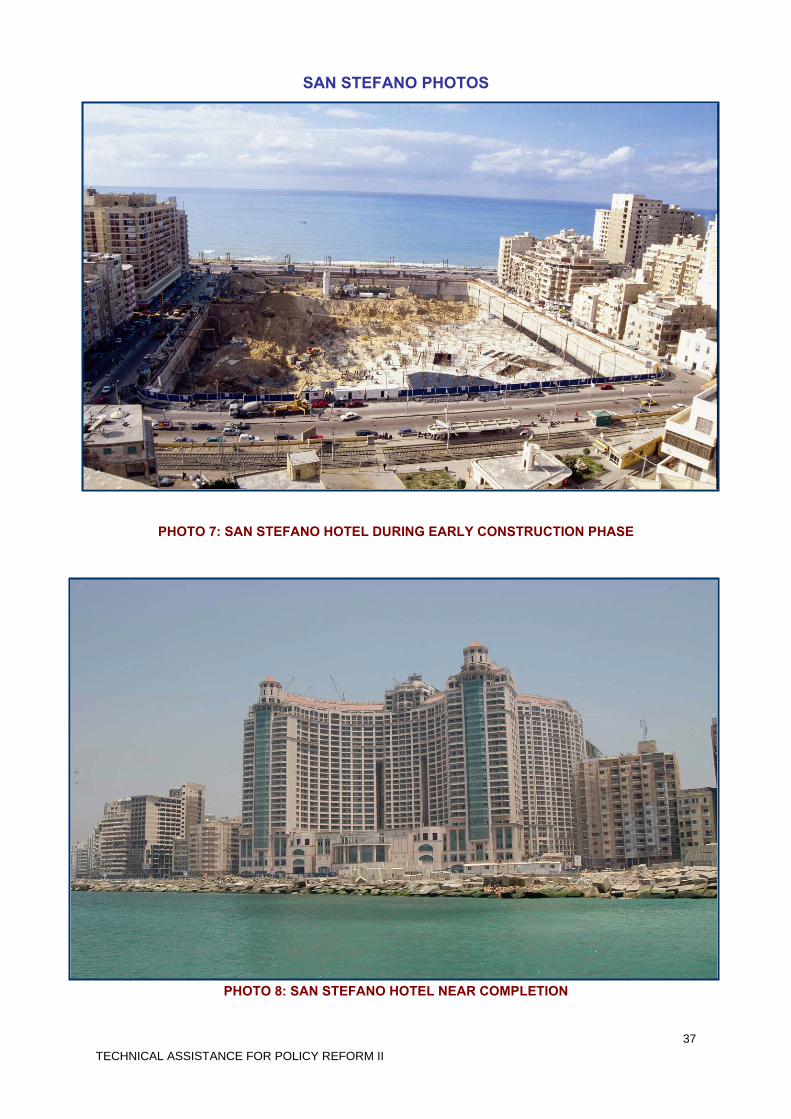

PHOTO 7: SAN STEFANO HOTEL DURING EARLY CONSTRUCTION PHASE ............ 37

PHOTO 8: SAN STEFANO HOTEL NEAR COMPLETION.......................................... 37

TECHNICAL ASSISTANCE FOR POLICY REFORM II 2

I. EXECUTIVE SUMMARY BACKGROUND AND INTRODUCTION The Ministry of Investment (MOI) has asked the United States Agency for International Development (USAID) and the Technical Assistance for Policy Reform Program (TAPR II) to commence a study of 20 privatized entities in order to assess the impact of privatization on these companies. The study will focus on several overall themes that are likely to enable the MOI to assess the changes that have occurred from pre- privatization to post-privatization among the 20 companies. The following are the overall themes on which the study will focus:

1. Strategic focus of the companies;

2. Impact on labor;

3. Operational performance;

4. Capital investment; and

5. Benefits to the Egyptian economy and the Government of Egypt.

These variables were selected because business performances in these essential areas more readily indicate the impact of private ownership on the enterprises and the stakeholders including labor, local communities, business owners, and the government. Significant improvements in these areas can often lead to the necessary “step-change”1 in business performance that enables companies to compete effectively in the global markets.

This interim-preliminary report presents four of the 20 privatized entities that will be part of the post privatization assessment.

METHODOLOGY OF THE STUDY

With the assistance of the MOI and Sector Holding Companies, TAPR II contacted five companies that had been privatized between 1996 and 2005. The companies were selected based on the willingness of the companies to meet with the TAPR II team to discuss their post-privatization experiences, provide necessary information and the belief that their experiences would represent the overall or typical experiences of many privatized companies. The companies were chosen from the food, chemical, and tourism sectors.

After explaining the purpose of the study with the respective companies, TAPR II sent questionnaires to the companies that outlined the range of questions that would be asked in the interviews. The TAPR II team then followed up and held interviews with the management of the companies to gain additional information and insights that could not be answered adequately in the questionnaire. Most of the interviews were open and management were generally cooperative in the meetings, although time constraints and quality of information provided limited the ability of the TAPR II team to conduct more in-depth analysis of the selected companies. The companies are:

Tourism and Cinemas Holding Company • San Stefano Hotel (privatized in 1998)

Chemical Industries Holding Company • Abu Zaabal Fertilizers and Chemicals (privatized in 2002) • National Paper Company (privatized in 2005)

Food Holding Company • Bisco Misr (privatized in 2005)

1“Step-change” refers to the high rate of change and level of investments (capital, human, equipment, etc.) that must be made by companies operating in transitional economies to compete effectively in global markets.

TECHNICAL ASSISTANCE FOR POLICY REFORM II 3

LIMITATIONS OF THE STUDY The time allotted for the data gathering of this study was September 12 to October 19, 2006. Thus, the assessment is constrained by the short timeframe to complete the company studies in time to meet the MOI deadline and the availability of company management. All the interviews were conducted in the company headquarters where the TAPR II personnel conducting the interviews were not able to engage in site visits to observe the company operations. As private enterprises, not all companies were open to answering all the questions that were posed and most did not complete the questionnaire that was sent to them at the time of this report.

Much of the information contained herein is based exclusively on interviews with management and from financial data collected from the privatized companies, the holding companies and the Ministry of Investment. The financial information provided has not been verified nor have the accounting standards used been reviewed. The four company snap shots have been reviewed by their respective managements for accuracy of the data presented and authorized for publication.

The financial data is presented using current prices and has not been adjusted for inflation or foreign exchange fluctuations.

The following section highlights the overall conclusions of this post-privatization impact assessment. The conclusions will focus on the five key themes of the study and will use the example from the sample companies to demonstrate successful aspects of privatization.

TECHNICAL ASSISTANCE FOR POLICY REFORM II 4

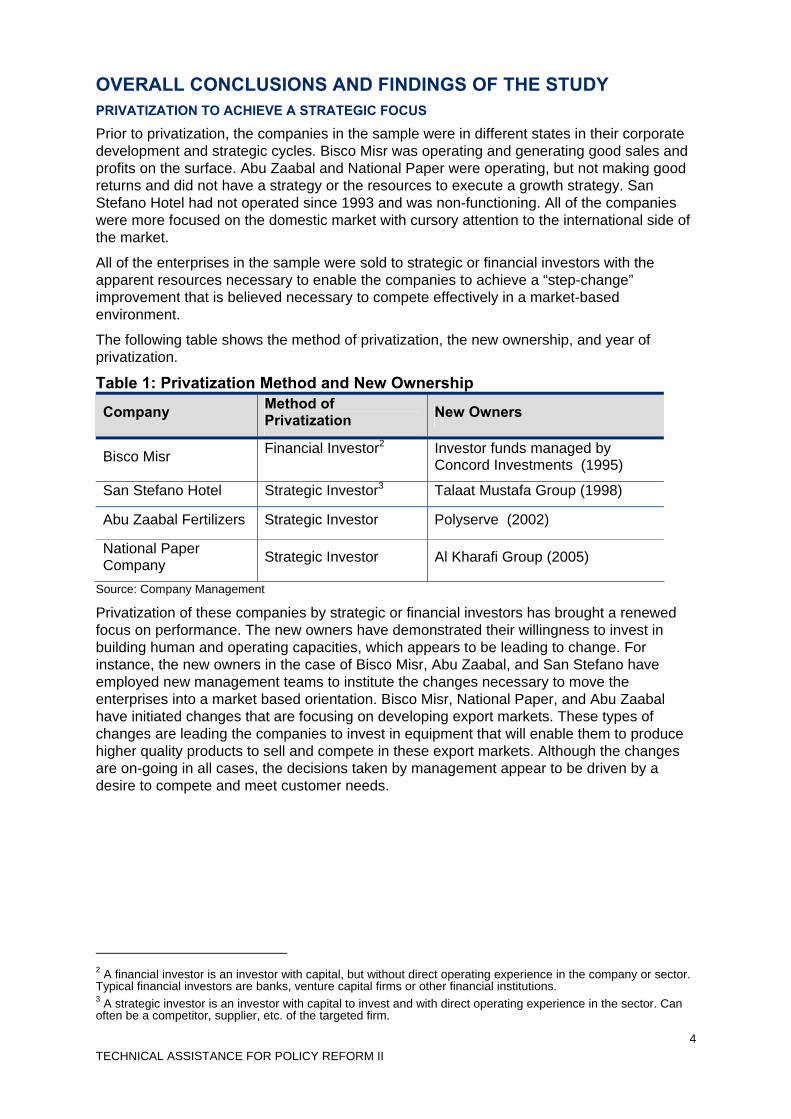

OVERALL CONCLUSIONS AND FINDINGS OF THE STUDY PRIVATIZATION TO ACHIEVE A STRATEGIC FOCUS

Prior to privatization, the companies in the sample were in different states in their corporate development and strategic cycles. Bisco Misr was operating and generating good sales and profits on the surface. Abu Zaabal and National Paper were operating, but not making good returns and did not have a strategy or the resources to execute a growth strategy. San Stefano Hotel had not operated since 1993 and was non-functioning. All of the companies were more focused on the domestic market with cursory attention to the international side of the market.

All of the enterprises in the sample were sold to strategic or financial investors with the apparent resources necessary to enable the companies to achieve a “step-change” improvement that is believed necessary to compete effectively in a market-based environment. The following table shows the method of privatization, the new ownership, and year of privatization.

Table 1: Privatization Method and New Ownership

Company Method of Privatization New Owners

Bisco Misr Financial Investor2 Investor funds managed by Concord Investments (1995)

San Stefano Hotel Strategic Investor3 Talaat Mustafa Group (1998)

Abu Zaabal Fertilizers Strategic Investor Polyserve (2002)

National Paper Company Strategic Investor Al Kharafi Group (2005)

Source: Company Management

Privatization of these companies by strategic or financial investors has brought a renewed focus on performance. The new owners have demonstrated their willingness to invest in building human and operating capacities, which appears to be leading to change. For instance, the new owners in the case of Bisco Misr, Abu Zaabal, and San Stefano have employed new management teams to institute the changes necessary to move the enterprises into a market based orientation. Bisco Misr, National Paper, and Abu Zaabal have initiated changes that are focusing on developing export markets. These types of changes are leading the companies to invest in equipment that will enable them to produce higher quality products to sell and compete in these export markets. Although the changes are on-going in all cases, the decisions taken by management appear to be driven by a desire to compete and meet customer needs.

2 A financial investor is an investor with capital, but without direct operating experience in the company or sector. Typical financial investors are banks, venture capital firms or other financial institutions. 3 A strategic investor is an investor with capital to invest and with direct operating experience in the sector. Can often be a competitor, supplier, etc. of the targeted firm.

TECHNICAL ASSISTANCE FOR POLICY REFORM II 5

PRIVATIZATION TO ENHANCE WORKERS WELFARE

The workers in all the privatized companies of the sample appear to have benefited from private ownership. The numbers of workers in two of the four companies (National Paper and Abu Zaabal) increased from pre-privatization levels. San Stefano Hotel, which was not operating prior to privatization, has generated hundreds of jobs during the construction phase of the complex. With the opening of the mall in July 2006, mall workers and shop employees have been hired. The hotel, which is due to open in December 2006, will also provide jobs. Only Bisco Misr has shown a decline in workers from 2,750 workers, pre-privatization to about 2,400 after privatization. The company has hired about 72 new workers in its marketing and sales functions.

All companies reported increased wages ranging from 25%-35% since privatization. The total compensation packages often included health care benefits and incentive bonus awards. Increased levels of training have been an integral part of all the new managements focus. Training has focused on prepping workers for competing in the global market place. Training topics have covered sales, marketing, quality control, and information technology. None of the companies reported any labor discord or actions, even in environments where the company instituted layoffs. Those companies that instituted early retirement programs, the programs and severance packages were according to the law.

BISCO MISR BEST EXEMPLIFIES THE NEEDED SHIFT IN STRATEGIC FOCUS

Prior to privatization, Bisco Misr focused its efforts on selling its products to the bid-oriented government or public market. Its products were sold to schools, the Army and other governmental agencies. The sales volume was high but the quality of the sales was low because the company was prevented from passing on increased costs by the term of its government contracts. Overall, the profit margins from the government sales were low due to the controlled and fixed priced nature of its contracts with the government.

The new management instituted a strategy that would impact the company long-term. The management decided to exit the government market and focus on the private market. This meant that the company would forego its high sales volumes in the short run and would enter a very competitive market that had the potential to generate greater profits since they would be able to raise prices as costs increased. The company believes that its products have been a part of the community for many years and have strong brand recognition in Egypt. This should enable Bisco Misr to compete well in the Egyptian market. The company also decided to focus on the export markets to take advantage of the “brand” awareness that the company believes it enjoys in the Arab markets in general.

The strategy of orienting itself to the private market has forced the company to improve the quality of its product, produce a product that the customer is willing to pay for, and introduce a more marketing and sales focused approach. These changes require hiring a more professionally oriented workforce, increased training of existing workers, new investment in production facilities, quality orientation, etc. To this end, the new owner brought in a globally experienced management team to make the strategic transition. Although early in the process, the new management appears to be making decisions that are likely to benefit the company over the long-term and should lead to a better positioned and more profitable company.

TECHNICAL ASSISTANCE FOR POLICY REFORM II 6

PRIVATIZATION TO RAISE OPERATIONAL PERFORMANCE

Operational performance involves assessing the company’s ability to expand its markets, increase its revenues, manage its costs, and generate profits. Abu Zaabal has been privatized for nearly four years and has a successful performance record to date with substantial increases in sales and profits. Nevertheless, Bisco Misr and National Paper Company, both privatized within the past 15-18 months, are in the process of implementing strategic changes; thus it is too early to show meaningful change. Bisco Misr and National Paper’s managements are in the process of making changes that should positively impact the performance of the companies in the long term, but may in the short term cause revenues and profits to decline. Despite these performances, the decisions taken by management should, in all likelihood, bode well for the future of the enterprises. San Stefano Hotel, although sold in 1998, will not open and operate as a new hotel complex until December 2006. The original hotel building was razed and a brand new hotel complex

NATIONAL PAPER, BISCO MISR, AND ABU ZAABAL REPRESENT INSTANCES WHERE PRIVATIZATION HAS BROUGHT BENEFITS TO THE WORKERS.

National Paper is one of the oldest paper producing companies in Egypt. The company was surviving in the short run, but its future without an investor was not good. Worker productivity was considered low by management and evidenced by low production levels. The company was then acquired by Al Kharafi Group, a major international Kuwaiti-based conglomerate.

The new owner is now undertaking a technical review of the company before it decides on how it will spend the LE 300 million in planned capital expenditure. In the meantime, the new owner has increased the number of workers from 970 to 1060 and decided to invest in the workers. They have given the workers 25% salary increases across the board. In addition, they have given the workers health care benefits that are superior to what they would have received under the government ownership complete with the ability to use any hospital for treatments, and accidental injury insurance coverage of up to LE 50,000 for accidents that occur inside or outside the plant. Management believes that this level of trust in the workers has already shown benefits to the company with increases of production in a six-month period from 32,500 tons to 35,600 tons. Management believes the turnaround is due to improved morale as a result of the investment by the new owner.

Bisco Misr is an interesting case of dealing with redundant labor and a weak work ethic. The new management wanted to take the company in a different direction that would rely on the employees becoming more market-oriented and responsive to the consumer. Since not everyone would be able to make that transition, the company instituted an early retirement program that offered a lump-sum payment for those who were eligible. In addition those employees who were not eligible for early retirement, but were not able to work in the new environment were given attractive severance packages. The remaining employees were given 35% increases across the board and extensive training. Further, the company has hired about 72 new employees in the marketing and sales are and is planning on new employees with skills in information technology (IT) and finance. Although Bisco Misr has had layoffs, it has rewarded remaining employees with increased salaries and investments in worker training to develop the skills needed to compete in its new markets.

Abu Zaabal’s management has indicated that prior to privatization the company has experienced declines in the number of worker from 1992 to 2002. Post privatization, the company has invested in new equipment and technology leading to increases in sales and profit. The result is that post-privatization (2002-2006), the company has increased: its overall workforce by 27% from 1,216 to 1,546 employees; and the average wage per employee by about 46% from LE 13,000 to LE 19,000 per year.

TECHNICAL ASSISTANCE FOR POLICY REFORM II 7

including hotel, luxury apartments, shopping mall, office space and parking garage was built on over 30,000 m².of land. Operating performance information is not available at this time.

PRIVATIZATION TO RAISE CAPITAL INVESTMENT

Most of the companies in the sample cited the importance of capital expenditures to achieve changes to be competitive. Frequently, only the most basic maintenance expenses were made before the companies were privatized. Significant capital expenditure programs have been instituted or are planned by many of the selected companies. These investments are essential to helping the companies achieve increased production capacities and efficiencies.

Below are the capital expenditures made and planned. Managements’ at the companies have indicated that most of these planned investments will be completed between 2007 and 2009. Table 2: Actual and Planned Capital Investment

*Total investment in the project is approximately LE 3 billion

Company Capital Expenditures Actual through 2006

Planned Investment

San Stefano Hotel Complex LE 3.0 billion* N/A

Bisco Misr LE 5 -10 million LE 35-40 million through 2007

Abu Zaabal LE 200 million LE 405 million through 2007

National Paper Company N/A LE 300 million over three years

ABU ZAABAL BEST DEMONSTRATES MANAGEMENT’S FOCUS ON OPERATIONAL EXCELLENCE.

Abu Zaabal was privatized in 2002. After the company was sold, the company made strategic decisions to improve product quality to gain access to the lucrative export markets and thus increase its overall sales and establish itself as a strong exporter. Prior to privatization, the company was not able to access export markets because its fertilizer products did not meet the specifications of the tough export markets.

Polyserve, an importer and exporter of fertilizers and chemicals was a natural tie-in for the acquisition of Abu Zaabal. The company’s sales have grown by over 170% since privatization and its export sales have quadrupled. Prior to privatization, the company had sales of LE 119 million of which LE 18 million (or 15%) were exports. By 2005, sales were LE 322 million and exports were 25% of sales at LE 81 million. The company has expanded its export market to South America, Europe, Africa, South Asia and the Middle East.

Abu Zaabal has not generated sales at the expense of its profitability. The company’s net income after taxes and return on sales (net profit after tax/ sales) has also shown steady improvement. Net income has grown from LE 4 million with a return on sales of 2.8% to LE 32.6 million with a return of 10.2%. Earnings after taxes have increased by over 700% in combination with the near doubling of revenues. The company’s management is targeting LE 1 billion in sales by year-end 2007.

TECHNICAL ASSISTANCE FOR POLICY REFORM II 8

BENEFITS TO THE EGYPTIAN ECONOMY AND GOVERNMENT

The benefits of privatization to the Egyptian economy and the Government of Egypt have been varied. In all cases (in our sample), the government was able to sell a company that was a marginal performer and place them in the hands of strong owners. The government was able to generate respectable sales proceeds and often commitments for investment (see table 2) and worker retention.

Below is a table that highlights the proceeds generated from the sale of the four company sample.

Table 3: Initial Sales Proceeds by Company

*Source: Chemical Industry Holding Company, includes lease amount, shares sale, and inventory;

** Food Industry Holding Company;

***Source: Company Management; and

**** Company Management, includes LE 50 Million of sales tax on the construction contract.

New owners have been able to turn around companies that were marginal and often a fiscal burden to the government. The companies are now in a position to increase employment, generate profits, expand their markets domestically and overseas, and lead to renewed economic development in the areas that they operate. These will ultimately lead to greater tax revenue generation for the government.

The cost of not privatizing these enterprises is believed to be high. Private ownership shows that the companies are more profitable or are on the way to being more profitable than under government ownership. The levels of capital expenditures would likely not have been available while under government control and the timing required to approve these

Company Initial Sales Proceeds

Abu Zaabal LE 267.0 million*

Bisco Misr LE 220.0 million**

National Paper Co. LE 135.0 million***

San Stefano Hotel LE 320.0 million****

Total LE 942.0 million

ABU ZAABAL SHOWS HOW PRIVATIZATION CAN LEAD TO ACCESS TO MUCH NEEDED CAPITAL EXPENDITURES.

Prior to privatization, Abu Zaabal had only minimal capital expenditures in its business. According to management, the company was producing for the domestic market and the quality of the products and plant capacities did not allow for export sales The company was acquired by Polyserve, an Egyptian fertilizer and chemical trading company that was seeking a producer to lock in its supply. Under new private ownership, Abu Zaabal was the recipient of an extensive plan to invest up to LE 405 million to increase the capacities in its fertilizer, sulphuric acid, and phosphoric acids product groups. Through 2006, Abu Zaabal management has invested about LE 200 million for capacity expansion, modernization, quality and environmental expenditures. Management believes that these increased capacities as well as quality improvements are the drivers for the increased level export sales of the company.

Company management has also indicated its expectation to generate revenues of approximately LE 1 billion by year end 2007. This challenging goal would likely not be attainable without the investments in new equipment, modernized technology, and increased capacity.

TECHNICAL ASSISTANCE FOR POLICY REFORM II 9

expenditures would have made the companies more vulnerable to competition. In short, the companies in our sample are in a better position to exceed their possibilities than under government control.

SAN STEFANO HOTEL’S TRANSFORMATION UNDER THE OWNERSHIP OF TALAAT MUSTAFA GROUP DEMONSTRATES THE FULL BENEFITS OF PRIVATIZATION TO THE GOVERNMENT AND THE ECONOMY OF EGYPT.

San Stefano Hotel was a historical hotel placed in a prime location in Alexandria on about 30,367 m² of the Corniche. The hotel ceased to operate in 1993 and was in a derelict condition. The government was not generating tax revenues on the property nor was there any employment from the hotel. When the government was willing to be flexible and allow the construction of a high rise building, the government created an environment that enabled potential investors to offer significantly greater amounts for the purchase of the building and the land. Talaat Mustafa Group (TMG) offered to pay LE 270 million for the purchase of the building and land and an additional LE 50 million for sales taxes.* TMG’s proposal ultimately has provided approximately LE 2.5 billion in additional investment in infrastructure and new facilities for a total commitment of approximately LE 3 billion.

The Egyptian economy has benefited from the employment generation during the construction phase of the hotel complex and should enjoy the benefits of employment generation once the entire complex is open for business. The government should expect potential tax revenues from the hotel, mall, office spaces, and sales of residential facilities. The Alexandria area will have a strong anchor investment that might encourage other similar investments in the area. For instance, TMG invested in the infrastructure of the area by widening the Corniche to improve traffic conditions. The government has followed suite and widened other parts of the Corniche, enhancing a larger section of the roadway. San Stefano is a potential huge success for the government, the economy and the city of Alexandria.

*TMG indicated that if a high rise building had not been allowed, their offer for the building would have been in the LE 70 million range.

TECHNICAL ASSISTANCE FOR POLICY REFORM II 10

The section below presents a more detailed case by case summary of findings from our interviews with the companies.

SUMMARY OF INDIVIDUAL COMPANY CONCLUSIONS AND FINDINGS SAN STEFANO HOTEL COMPLEX

• San Stefano is an excellent example of privatization in Egypt. The Holding Company for Tourism and Cinema has taken a non-performing asset and sold it via a transparent public tender to a first class investor for LE 320 million. The government showed flexibility in allowing the construction of a high-rise building which garnered greater interest from the potential investors. The winning investor, Talaat Moustafa Group (TMG) had the vision, capital, and know-how to invest and create a truly first class complex that will likely enhance an area of the Alexandria Corniche for a long time.

• The total investment for the San Stefano Complex will approach LE 3 billion and will consist of a new luxury five-star hotel managed by the Four Seasons Group; 900 luxury apartments, a luxury mall, commercial spaces, and underground parking. The shopping mall opened in July 2006 and the attached hotel will open in December 2006. More than half of the luxury apartments have been sold.

• TMG attracted the internationally recognized hotel and hospitality operator, Four Seasons Group, to manage the hotel and will thus assure the investment meets international five-star standards.

• Construction of the complex provided employment for about 4,000 workers. Additional jobs will emerge post construction through the hotel, shopping mall and commercial facilities of about 2,200 workers.

• The hotel is located in a strategic location in Alexandria and should serve as a key anchor for other investment in the area as well as a means of wider local economic development.

• An international hotel manager like the Four Seasons Group should bring management skills and training of staff that could provide an upgrade of the overall hotel services in the area.

• The impact on local economic development will likely extend beyond the Complex to its suppliers and other local businesses. The Egyptian economy should benefit from increased jobs, improved infrastructure, enhanced workforce skills, and generation of tax revenues.

• Building the hotel has resulted in infrastructure improvement in Alexandria. For example, expansion of the Corniche in front of the hotel has led the city of Alexandria to further widen the rest of the Corniche and improve the traffic flow in the area.

ABU ZAABAL FERTILIZER AND CHEMICALS

• Polyserve acquired Abu Zaabal via a two-step lease and purchase transaction that generated LE 267 million for the Egyptian government in leasing and sales proceeds.

• The acquisition of Abu Zaabal by a strategic investor like Polyserve with knowledge of the fertilizer and chemicals production, distribution and sales has enabled the company to gain access to export markets to increase sales; and to financial capital for necessary investments to increase its production capacities and quality of products.

• The company now has access to new markets both domestically and internationally. This is reflected in the strong sales increases in both the domestic and export markets. Overall sales have increased by over 170% and international sales have quadrupled since privatization.

TECHNICAL ASSISTANCE FOR POLICY REFORM II 11

• Prior to privatization, Abu Zaabal had little investment in its production assets. In about four years of privatization, Abu Zaabal has invested approximately LE 200 million to increase production capacities. The company is planning to spend up to LE 405 million in strategic capital investments to increase capacities, improve productivity and quality, and address environmental challenges.

• The additional capacities and quality improvements will likely be contributors to help achieve management’s goal of LE 1 billion sales by 2007.

• From pre-privatization (2002) to 2005, the company increased its overall workforce by 27% from 1,216 to 1,546 employees. The company also increased the average wage per employee by about 46% from LE 13,000 to LE 19,000 per year.

NATIONAL PAPER COMPANY

• Government of Egypt sold 100% of National Paper Company to the international Kuwaiti-owned conglomerate Al Kharafi Group for LE 135 million in 2005.

• Privatization of National Paper Company is early in the process to fully evaluate the impact, but the acquisition should be positive for the future of the company.

• National Paper’s acquisition by the Al Kharafi Group will expose the company to a world class organization that will enhance the company’s access to capital, new markets, and management expertise.

• National Paper has old equipment, some dating back to its founding in 1934. The company has not been able to make investments above routine maintenance in the recent past. Al Kharafi Group has committed to invest LE 300 million to modernize the equipment, thus enabling the company to compete internationally with higher quality product offerings.

• National Paper under the ownership of Al Kharafi has increased the number of workers from 970 to 1060 and is investing in the employees of the company by offering 25% salary increases, attractive health care benefits, accident insurance, bonus for performance, and training. Management believes the workers are becoming more productive, increasing production in six months from 32,500 tons to 35,600 tons.

BISCO MISR • The Government of Egypt sold 100% of Bisco Misr and has generated LE 220 million

in sales proceeds from its two- tranche sales of its interests. • Bisco Misr was “fully” privatized when a 36.9% block of government-owned shares

were tendered and sold to the financial investor with funds managed by Concord Investment Funds.

• The new professional management team has made strategic changes in the target markets of the company. The change in strategy has led to short-term reductions in revenue and profits, but will lead to long-term profit generation.

• Management is focusing its domestic sales on the private market and is exiting the low margin high volume public/governmental bid market.

• The company is utilizing its regional brand recognition to focus on developing export sales in the Arab world and Africa.

• After privatization, the company planned to invest approximately LE 50 million through 2007 in capital expenditures. To date, Bisco Misr has invested about LE 33 million for increased production and quality, overdue maintenance, and distribution/sales facilities.

• Management has written-down non-saleable inventory and old unusable packaging, sacrificing short-term profit for long-term viability and cleaning up its balance sheet.

TECHNICAL ASSISTANCE FOR POLICY REFORM II 12

• Management instituted an early retirement program to reduce excess employees who were eligible. Several hundred have taken advantage of the program. The remaining employees have received 35% raises, training, and professional growth opportunities in a potentially significant player in the regional food industry sector.

• Despite the early retirement program and layoffs, the company has added employees with skills in marketing, sales, finance, and IT to enhance the company’s new market/customer driven focus. To this end, Bisco Misr has hired 72 people in the marketing and sales function.

TECHNICAL ASSISTANCE FOR POLICY REFORM II 13

II. SUMMARY OF COMPANY ASSESSMENTS POST–PRIVATIZATION

TECHNICAL ASSISTANCE FOR POLICY REFORM II 14

ABU ZAABAL FERTILIZER & CHEMICAL COMPANY

مصنع إنتاج حامض الكبريتيك

Information contained within is sourced from discussions with the company management and from data provided by the company, the Holding Company for Chemical Industries and the Office of the Ministry of Investment unless otherwise footnoted.

FUTURE SULPHURIC ACID FACTORY

TECHNICAL ASSISTANCE FOR POLICY REFORM II 15

COMPANY BACKGROUND Abu Zaabal Fertilizer and Chemical (Abu Zaabal) was established in 1947. The company is based in Cairo with chemical and fertilizer operations located in the greater Cairo area and Alexandria. The company was organized to produce and sell fertilizers as well as sulphuric and phosphoric acids. The company sells its products both domestically and exports to the Middle East, Africa, Europe, South Asia, and South America. The company was privatized in March 2002 initially through a lease arrangement of Abu Zaabal’s factory to Polyserve that eventually led to the sale of the company to Polyserve.

Polyserve was established in March 1995 as an Egyptian importer and exporter of fertilizer and chemical products. Polyserve acquired Abu Zaabal to augment its fertilizer and chemical trading activities with a producer of fertilizers and chemicals. The acquisition enabled Abu Zaabal to increase its sales in the local market and bolster its presence in the export market. The company currently employs about 1,500 employees. Below are the revenues and profits of the company since privatization.

Table 4: Revenues and Net Income-Post Privatization

Source: Company Management

PRIVATIZATION HISTORY AND INFORMATION Abu Zaabal’s was privatized in a two step process that involved an initial lease arrangement (with an option to buy) for the use of the company’s facilities that was then followed by an outright purchase of the company’s shares and inventory. Polyserve entered into a government-approved three-year lease arrangement with Abu Zaabal on February 11, 2002. The arrangement enabled Polyserve to lease and operate the factories of Abu Zaabal. Polyserve was to pay an initial leasing fee and then quarterly payments. About two years into the lease, Polyserve decided to forgo the last year of the lease and acquire Abu Zaabal outright by purchasing 99% of the company’s shares in February 2005. In addition to the payment for the shares of the company and inventory, Polyserve agreed to provide 40% of the markets’ need (farmers) for fertilizer and 50% of the government’s need for sulphuric acid that would be used for water purification. In addition, Polyserve was to improve the production facilities, rectify the environmental concerns of the company, maintain the workforce and improve product quality. Polyserve paid LE 267 million for Abu Zaabal including lease payments, shares purchase, and inventory. Polyserve owns 99% of the shares of Abu Zaabal and 1% is owned by others.

PRE AND POST PRIVATIZATION TRENDS ANALYSIS REVENUES

Abu Zaabal produces and sells fertilizer products, sulphuric and phosphoric acids to both the local domestic and export markets. Following privatization, overall revenues increased by 170% through 2005. Through its access to Polyserve’s international markets, the company has quadrupled its export sales and is now selling into markets in South America, Europe, Middle East and Africa, and South Asia. When the company completes it

LE (000) 2002 2003 2004 2005

Revenues 143,078 194,335 263,448 321,531

Net Income 4,020 5,974 16,996 32,608

TECHNICAL ASSISTANCE FOR POLICY REFORM II 16

101,208

18,023

121,920

21,158

150,810

43,54

5

187,794

75,65

4

239,821

81,71

0

0

50,000

100,000

150,000

200,000

250,000

Rev

enue

s in

LE (0

00)

Pre-Priv

atizat

ion

2002

* (10

mon

ths)

2003

2004

2005

Years

Domestic Sales Export Sales

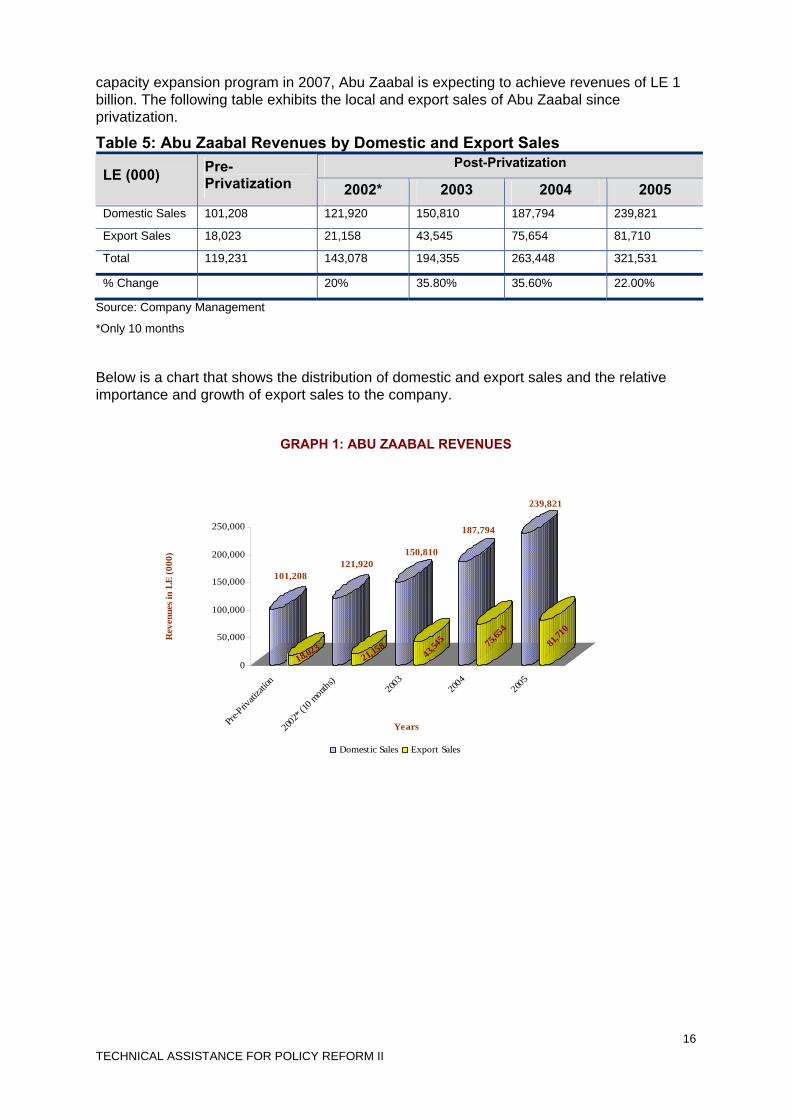

capacity expansion program in 2007, Abu Zaabal is expecting to achieve revenues of LE 1 billion. The following table exhibits the local and export sales of Abu Zaabal since privatization.

Table 5: Abu Zaabal Revenues by Domestic and Export Sales Post-Privatization

LE (000) Pre-Privatization 2002* 2003 2004 2005

Domestic Sales 101,208 121,920 150,810 187,794 239,821

Export Sales 18,023 21,158 43,545 75,654 81,710

Total 119,231 143,078 194,355 263,448 321,531

% Change 20% 35.80% 35.60% 22.00%

Source: Company Management

*Only 10 months

Below is a chart that shows the distribution of domestic and export sales and the relative importance and growth of export sales to the company.

GRAPH 1: ABU ZAABAL REVENUES

TECHNICAL ASSISTANCE FOR POLICY REFORM II 17

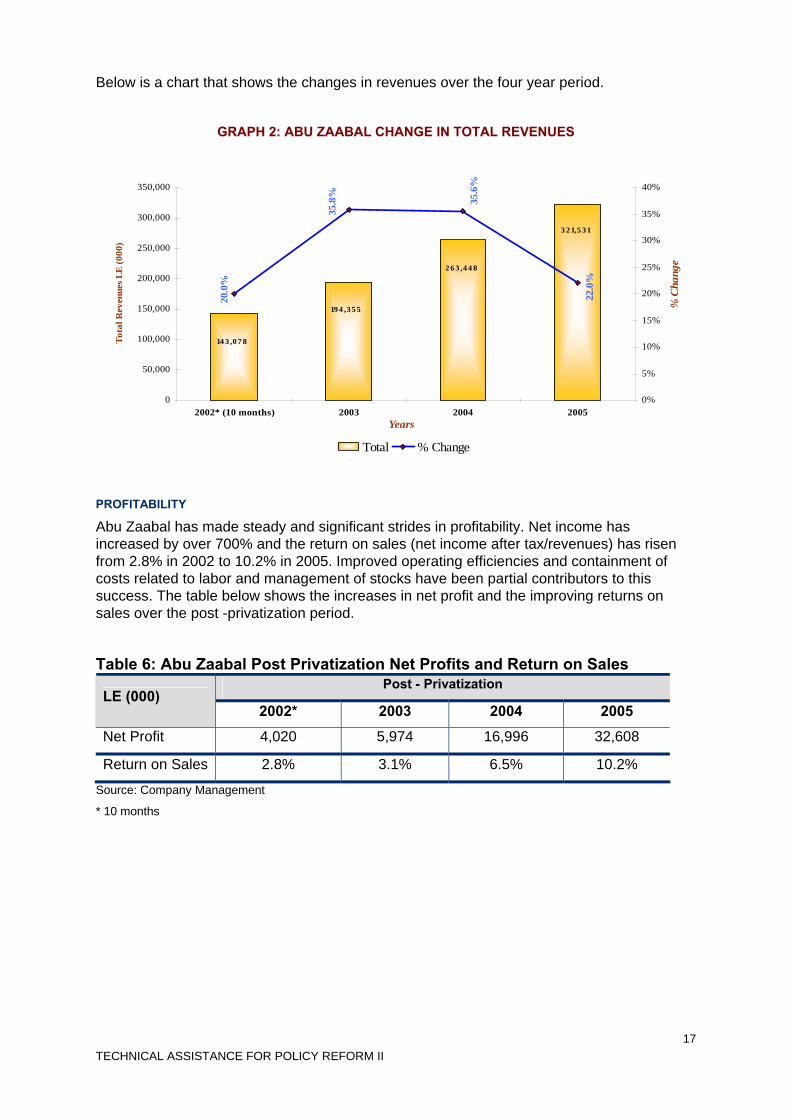

Below is a chart that shows the changes in revenues over the four year period.

GRAPH 2: ABU ZAABAL CHANGE IN TOTAL REVENUES

14 3 ,0 7 8

19 4 ,3 5 5

2 6 3 ,4 4 8

3 2 1,5 3 120

.0%

22.0

%

35.6

%

35.8

%

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

2002* (10 months) 2003 2004 2005Years

Tota

l Rev

enue

s LE

(000

)

0%

5%

10%

15%

20%

25%

30%

35%

40%

% C

hang

e

Total % Change

PROFITABILITY

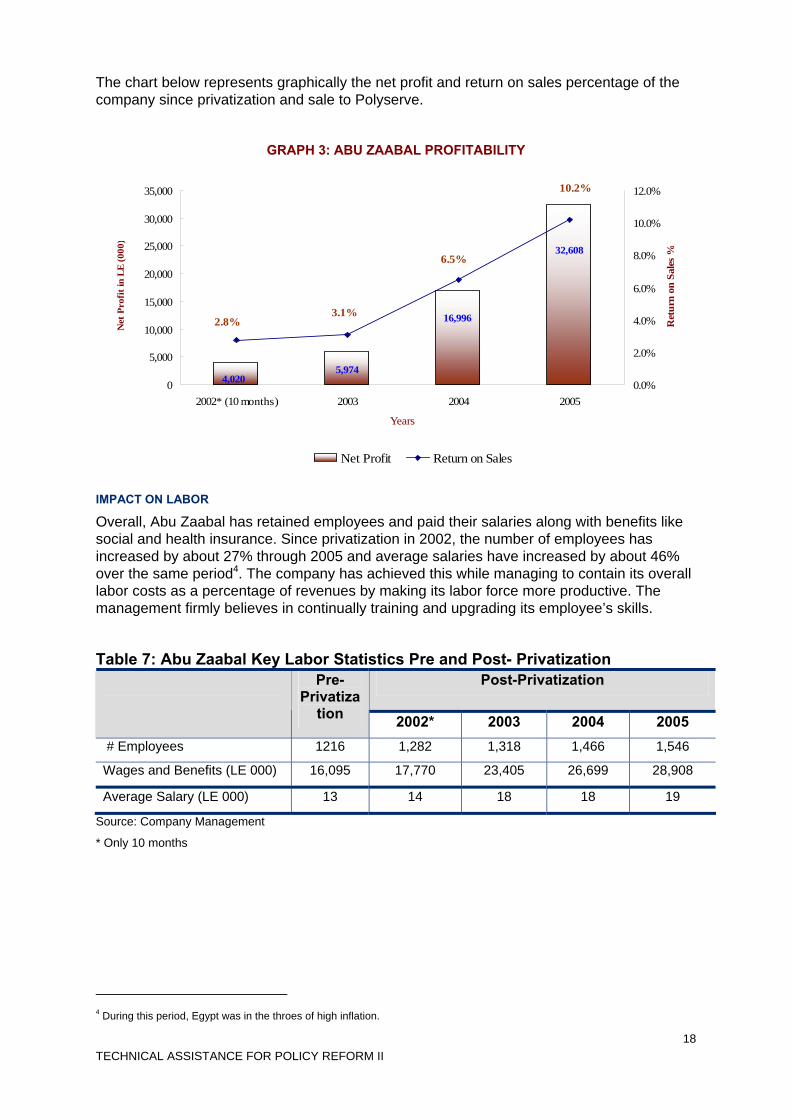

Abu Zaabal has made steady and significant strides in profitability. Net income has increased by over 700% and the return on sales (net income after tax/revenues) has risen from 2.8% in 2002 to 10.2% in 2005. Improved operating efficiencies and containment of costs related to labor and management of stocks have been partial contributors to this success. The table below shows the increases in net profit and the improving returns on sales over the post -privatization period.

Table 6: Abu Zaabal Post Privatization Net Profits and Return on Sales

Post - Privatization LE (000)

2002* 2003 2004 2005 Net Profit 4,020 5,974 16,996 32,608

Return on Sales 2.8% 3.1% 6.5% 10.2%

Source: Company Management

* 10 months

TECHNICAL ASSISTANCE FOR POLICY REFORM II 18

The chart below represents graphically the net profit and return on sales percentage of the company since privatization and sale to Polyserve.

GRAPH 3: ABU ZAABAL PROFITABILITY

16,996

32,608

5,9744,020

2.8%3.1%

6.5%

10.2%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Years

Net

Pro

fit in

LE

(000

)

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

2002* (10 months) 2003 2004 2005

Ret

urn

on S

ales

%

Net Profit Return on Sales

IMPACT ON LABOR

Overall, Abu Zaabal has retained employees and paid their salaries along with benefits like social and health insurance. Since privatization in 2002, the number of employees has increased by about 27% through 2005 and average salaries have increased by about 46% over the same period4. The company has achieved this while managing to contain its overall labor costs as a percentage of revenues by making its labor force more productive. The management firmly believes in continually training and upgrading its employee’s skills.

Table 7: Abu Zaabal Key Labor Statistics Pre and Post- Privatization

Post-Privatization

Pre-Privatiza

tion 2002* 2003 2004 2005 # Employees 1216 1,282 1,318 1,466 1,546

Wages and Benefits (LE 000) 16,095 17,770 23,405 26,699 28,908

Average Salary (LE 000) 13 14 18 18 19

Source: Company Management

* Only 10 months

4 During this period, Egypt was in the throes of high inflation.

TECHNICAL ASSISTANCE FOR POLICY REFORM II 19

GRAPH 4: ABU ZAABAL IMPACT ON LABOR NUMBERS

1216

1,5461,4661,3181,282

0

500

1000

1500

2000

Pre-Privatization 2002* 2003 2004 2005

Years

Num

ber

of E

mpl

oyee

s

GRAPH 5: ABU ZAABAL CHANGE IN ANNUAL WAGES

16,09517,770

23,40526,699

28,908

19,000

13,000 14,000

18,000 18,000

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Pre-Privatization 2002* 2003 2004 2005

Years

Wag

es in

LE

(000

)

Ave

rage

Sal

arie

s in

LE

Wages & benefits Average Salary

t

CAPITAL EXPENDITURES

Abu Zaabal has invested about LE 200 million in capital expenditures through 2006. The expenditures have been for maintenance, cost reduction, product expansion and energy reduction costs. The company is in the process of investing up to LE 405 million in capital expenditures to increase capacities in fertilizers, sulphuric acids, and phosphoric acids and to make necessary environmental expenditures to resolve sewage, gas expulsion, and dust removal. The costs of the environmental investments are estimated at LE 26 million. The new capacities are expected to generate sales of LE 1 billion by 2007. MARKET DEVELOPMENT

Abu Zaabal has generated significant increases in sales both domestically and internationally. The company has made a concerted effort to develop its export markets and has entered into several new markets such as Brazil, Argentina, Italy, Greece, Turkey, Tanzania, Sudan, Syria, Saudi Arabia, Yemen, Sri Lanka and Bangladesh.

TECHNICAL ASSISTANCE FOR POLICY REFORM II 20

SUPPLY CHAIN IMPROVEMENTS

No significant changes are noted in the supply chain. The company engages in long-term supply contracts of 5-10 years with some as long as 30 years to lock in the quantities of materials. Prices are negotiated according to the market. The company indicated that they did not engage in hedging. NEW MANAGEMENT TECHNIQUES/SKILLS

Senior level management at Abu Zaabal was replaced by the management of Polyserve. While management at the operational levels has been retained, consultants were engaged to advise the company on human resource management, technical design, and production. This has led the company to make capital investments to increase capacity and productivity. BENEFITS TO THE EGYPTIAN ECONOMY AND GOVERNMENT

The privatization of Abu Zaabal has been successful by many measures including revenues, earning, labor increases in wages, job security and skills development. The company’s improved profitability potentially brings additional tax revenues and relieves the additional burden of “managing” an enterprise. The increased level of employment helps to develop productive citizens who will add to the local community through their purchasing power.

CONCLUSIONS AND FINDINGS • Polyserve acquired Abu Zaabal via a two-step lease and purchase transaction that

generated LE 267 million for the Egyptian government in leasing and sales proceeds. • The acquisition of Abu Zaabal by a strategic investor like Polyserve, with knowledge

of the fertilizer and chemical production, distribution, and sales has enabled the company to gain access to export markets to increase sales; and, financial capital for necessary investments to increase its production capacities.

• The company now has access to new markets both domestically and internationally. This is reflected in the strong sales increases in both the domestic and export markets. Overall sales in 2005 have increased by over 170% to LE 321 million and international sales have quadrupled to LE 81.7 million since privatization.

• Through 2006, Abu Zaabal has invested approximately LE 200 million in new capital expenditures to increase production capacities. The Company is planning up to LE 405 million in strategic capital investments which is being made to increase capacities, improve productivity, quality, and clean up environmental challenges.

• The additional capacities and quality improvements will likely help the management to achieve their sales target of LE 1 billion by 2007.

• By 2005, the company increased its overall workforce by 27% from pre-privatization levels (1,216 to1,546 people) and also increased the average wage per employee by about 46% from LE 13,000 to LE 19,000 per year.

TECHNICAL ASSISTANCE FOR POLICY REFORM II 21

ABU ZAABAL PLANT PHOTOS

PHOTO 1: SIAB UNIT FOR T.S.P. (TRIPLE TRI CALCIUM PHOSPHATE)

PHOTO 2: STORAGE FOR G.S.S.P

PHOTO 3: FUTURE GRANULATING PLANT (500 TON/DAY)

TECHNICAL ASSISTANCE FOR POLICY REFORM II 22

PHOTO 4: GRANULATED GSSP FERTILIZER-99% EXPORTED

PHOTO 5: GRANULATING PLANT- ABU ZAABAL TECHNOLOGY

PHOTO 6: GRANULATING MACHINE-NEW EQUIPMENT

TECHNICAL ASSISTANCE FOR POLICY REFORM II 23

BISCO MISR

Information contained within is sourced from discussions with the company management and from data provided by the company, the Holding Company for Food or the Office of the Ministry of Investment unless otherwise footnoted.

TECHNICAL ASSISTANCE FOR POLICY REFORM II 24

COMPANY BACKGROUND Bisco Misr, established in 1957, is the oldest and second largest player in the Egyptian biscuit manufacturing sector. The company was organized to make the full range of confectionary products including a variety of biscuits, cakes, sweets, chewing gum, toffee, cereals, chocolates, licorice and mints. The company sells its products both locally and internationally. The company has three manufacturing facilities and currently employs about 2,400 people.

The company was “fully” privatized in 2005 when a 36.9% block of government owned shares were tendered and sold to an investor. The successful bidder was the financial investor, Concord Investment Funds and funds managed by Concord Investment Funds. The new management team that was installed has implemented several changes that will likely produce strong results over the long run.

Table 8: Bisco Misr Financial Results

Source: Company Management and “Beltone Financial” brokerage report dated 2 March 2006

*Plan through 2007 including maintenance expenses.

PRIVATIZATION HISTORY AND INFORMATION In the first phase of Bisco Misr’s privatization, the government initially sold a 20% stake to the Cairo and Alexandria Stock Exchange (CASE) while retaining an 80% stake in the company. In the second phase, the government sold an additional 50% of its 80% stake to the CASE over a period of years (1999-2005) resulting in a technically privatized the company. Although the company was privatized, the government remained the largest single shareholder with about a 36.9% holding. Thus, the government continued to retain effective “control” of the company. In the third phase, the Holding Company of the Food Industry sold the remaining 36.9% stake in the company to financial investors in February 2005 via a public tender. The shares were purchased at full market price and had no requirements or restrictions regarding capital investment and retention of labor.

5 EBITDA is defined as earnings before interest, taxes, depreciation, and amortization 6 Capex is defined as capital expenditures

Pre-Privatization Post-Privatization

2003 2004 2005 2006 (estimate)

Revenues LE 116.5 million LE 117.2 million LE 141 million LE 140 million

EBITDA5 LE 18 million LE 12 million LE 22 million N/A

Net Income LE 26 million LE 22 million LE 22 million LE 3.5 million

Capex6 LE 3.2 million LE 1.0 million LE 50 million*

TECHNICAL ASSISTANCE FOR POLICY REFORM II 25

PRE AND POST-PRIVATIZATION TRENDS ANALYSIS PRE-PRIVATIZATION SITUATION SUMMARY

Bisco Misr was an established provider of biscuits and confectionaries with a strong market presence in Egypt. The company focused its offerings to the middle and low income groups and generated most of its sales from the “public” or government market including public schools, the Army, and other Egyptian institutions. The company exported its products to foreign markets in the Arab world and Africa. Bisco Misr’s sales performance was flat during the 2003-2004 timeframe. Net income after taxes was strong and liquidity excellent. The company operates three plants and has 11 production lines and three oven heaters. Prior to privatization, the company spent little capital for new production capacities, modernization or maintenance of its core business assets, investing approximately LE 4.2 million in the 2003-2004 periods. However, the company invested about LE 45 million in a portfolio of companies stocks that enabled Bisco Misr to report stronger non-operating income that permitted the company to report less taxable income.

Bisco Misr was fully privatized in February 2005 and a new management team was installed in the April-May 2005 time frame. Although the new management team has not been in place long enough to see the full results of their actions, the decisions taken should only improve the long-term prospects of the company. Below are some of the essential strategic decisions taken by the management team:

• Focus away from the low margin public sector market (public schools and other Egyptian governmental institutions) to the private sector market;

• Become more consumer oriented by developing a focus on marketing and sales; • Grow its exports and develop additional markets in the Arab world and Africa, • Make needed capital expenditures to increase production capacities and efficiencies. • Invest in training; • Reduce the number of employees to reduce operational costs and invest in the

remaining employees through higher wages and training; • Develop a focus and orientation on marketing and sales, finance and IT; and • Hire new employees with skills in marketing, sales and finance.

Since the new management has changed the fiscal year end from June 30 to December 31, a direct financial comparison is not feasible at this time. REVENUES

According to management, estimated 2006 revenues will be flat due to management’s focus on quality private sector sales rather than the higher volume public sector. The makeup of the sales, however, is expected to be significantly changed. In 2005, the company generated about 70% of its sales from private market and exports, and 30% from the public market. The company has already changed its focus to generating its revenues exclusively from the private and export markets (away from the pursuit of government contracts) where it will be freer to increase prices. The company currently sells to 17 countries in Africa and the Arab world. Although exports have been relatively small at LE 2 million, the company expects a 33% year on year increase in exports in 2006 due to its renewed focus on foreign sales. The company currently has 283 SKUs (stock keeping units) in its product portfolio. Management believes that some of its SKUs will have limited attraction and less potential for growth in the private market place. Thus, Bisco Misr will rationalize the SKUs with little potential growth or profitability.

These decisions taken together will initially dampen revenues, but will produce more profitable and sustainable revenues in the long run. The new management team is demonstrating its expertise by its willingness to forgo short-term gain in the interest of long-term viability. Management has hired consultants to provide assistance in setting its strategic

TECHNICAL ASSISTANCE FOR POLICY REFORM II 26

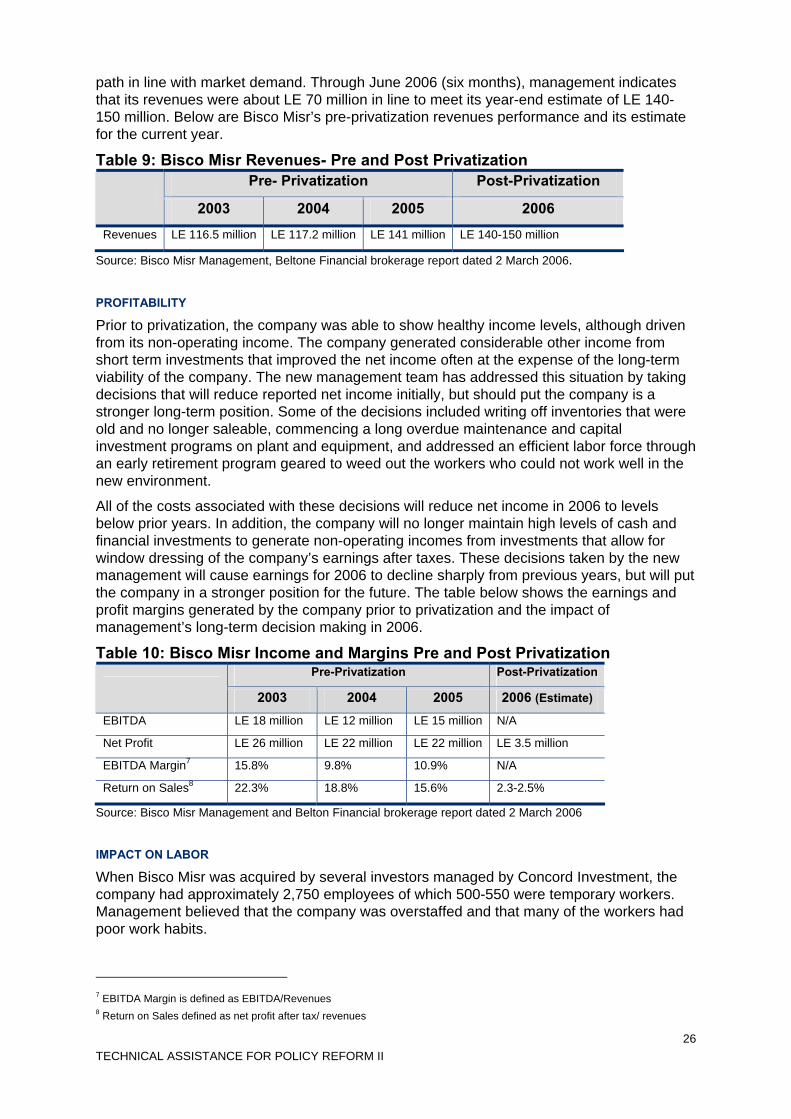

path in line with market demand. Through June 2006 (six months), management indicates that its revenues were about LE 70 million in line to meet its year-end estimate of LE 140-150 million. Below are Bisco Misr’s pre-privatization revenues performance and its estimate for the current year.

Table 9: Bisco Misr Revenues- Pre and Post Privatization Pre- Privatization Post-Privatization

2003 2004 2005 2006

Revenues LE 116.5 million LE 117.2 million LE 141 million LE 140-150 million

Source: Bisco Misr Management, Beltone Financial brokerage report dated 2 March 2006. PROFITABILITY

Prior to privatization, the company was able to show healthy income levels, although driven from its non-operating income. The company generated considerable other income from short term investments that improved the net income often at the expense of the long-term viability of the company. The new management team has addressed this situation by taking decisions that will reduce reported net income initially, but should put the company is a stronger long-term position. Some of the decisions included writing off inventories that were old and no longer saleable, commencing a long overdue maintenance and capital investment programs on plant and equipment, and addressed an efficient labor force through an early retirement program geared to weed out the workers who could not work well in the new environment.

All of the costs associated with these decisions will reduce net income in 2006 to levels below prior years. In addition, the company will no longer maintain high levels of cash and financial investments to generate non-operating incomes from investments that allow for window dressing of the company’s earnings after taxes. These decisions taken by the new management will cause earnings for 2006 to decline sharply from previous years, but will put the company in a stronger position for the future. The table below shows the earnings and profit margins generated by the company prior to privatization and the impact of management’s long-term decision making in 2006.

Table 10: Bisco Misr Income and Margins Pre and Post Privatization Pre-Privatization Post-Privatization

2003 2004 2005 2006 (Estimate)

EBITDA LE 18 million LE 12 million LE 15 million N/A

Net Profit LE 26 million LE 22 million LE 22 million LE 3.5 million

EBITDA Margin7 15.8% 9.8% 10.9% N/A

Return on Sales8 22.3% 18.8% 15.6% 2.3-2.5%

Source: Bisco Misr Management and Belton Financial brokerage report dated 2 March 2006

IMPACT ON LABOR

When Bisco Misr was acquired by several investors managed by Concord Investment, the company had approximately 2,750 employees of which 500-550 were temporary workers. Management believed that the company was overstaffed and that many of the workers had poor work habits.

7 EBITDA Margin is defined as EBITDA/Revenues 8 Return on Sales defined as net profit after tax/ revenues

TECHNICAL ASSISTANCE FOR POLICY REFORM II 27

Management engaged in a program to reverse this situation. First, the company instituted new standards and practices for all employees. Those employees who could not meet the new standards were encouraged to leave or have been asked to leave with separation pay. Second, the company offered an early retirement program with a lump sum payment structure. To date, about 470 workers chose the early retirement option, and the company has allocated about LE 5 million to implement the early retirement program. The remaining workers were given a 35% increase in salaries, training (marketing and sales), and were introduced to a new work ethic. Despite the cuts, the company has hired about 72 new staff members in the areas that it hopes to build for its future sales and ability to perform in the competitive private market. These areas include sales and marketing, finance, and information technology (IT). Today, the company has about 2,400 employees, but management concedes that it might need to further reduce its workforce. The management team has indicated that despite the reductions in workforce, the company has not suffered from labor discord. Management believes that its work reduction programs have been attractive to the workers who have taken them. CAPITAL EXPENDITURES

In its strategic plan, the company plans to make capital expenditures of about LE 50 million through 2007. The company will invest about LE 40 million to upgrade and add new biscuit production lines and to construct new outlets for sales and distribution. Management expects these investments to expand capacity, efficiency, improve quality and simplify the distribution of its products. The remaining LE 10 million in capital has been planned for renovation since the former management team neglected to make adequate investments in the company’s production assets. To date, management has spent about LE 33 million of which LE 8 million has been for renovation and maintenance expenses. MARKET DEVELOPMENT

The market strategy of the new management is to develop the private market which it believes is more profitable than the government/public contract-bid end of the market. The company has prepared for this new focus by hiring marketing and sales people and providing training to orient existing employees to this new way of thinking. The new management will spend about LE 2.7 million in fiscal year 2006 on marketing, advertising and promotion, a substantial increase from prior management. SUPPLY CHAIN IMPROVEMENTS

Several changes have been implemented by the new management team which will improve the company’s supply chain relationship including: • Establishing a list of approved suppliers; • Setting up a procurement system that is linked to sales and production; • Setting specific quality standards for raw material well in advance; and • Paying suppliers according to negotiated terms and conditions.

NEW MANAGEMENT TECHNIQUES/SKILLS

The new investor replaced the entire management team in all key functions except production and quality control. The new CEO, formerly the Managing Director of Novartis, brings with him experience in IT, sales and marketing. The financial function will also be enhanced by hiring new and appropriate staff to augment the CFO function. The new management team brings a new level of professionalism and performance orientation that they received from their prior experiences working in private sector companies. It is too early to evaluate the new management’s performance, but they appear to have taken decisions that will ultimately enhance Bisco Misr’s future performance.

TECHNICAL ASSISTANCE FOR POLICY REFORM II 28

BENEFITS TO THE EGYPTIAN ECONOMY AND GOVERNMENT

The Government of Egypt was able to sell its interest in Bisco Misr and generate approximately LE 220 million in proceeds. Egyptian economy will benefit from the sale of Bisco Misr through the introduction of modern management techniques, improvement of product quality, training of workforce and access to new competitive markets. With the company’s focus on maximizing operating income from the core business rather than investment income, the government may be more likely to receive a source of tax revenue. This example will in all likelihood become a beacon for other companies to become more market-oriented.

CONCLUSIONS AND FINDINGS: Given the relatively recent acquisition of Bisco Misr by an anchor investor, it is too early to assess the long term trends and outcomes of Bisco Misr’s privatization. The company and its new management team have made substantial changes in strategy and operations that bode well for the company’s long term viability, despite the short-term and one-time reduction in net income from prior years. Some of the advantages of privatization for Bisco Misr include:

• The Food Industry Holding Company was able to sell its interest in Bisco Misr and generate approximately LE 220 million in sales proceeds.

• The new professional management team has made strategic changes in the target market of the company. The change in strategy has led to short-term reductions in revenue and profits, but management believes the decisions will lead to long-term profit generation.

• Management is focusing its domestic sales on the private market and is exiting the low margin high volume public/governmental bid market.

• The company is utilizing its regional brand recognition to focus on developing export sales in the Arab world and Africa.

• The company is investing approximately LE 50 million over the next three years in capital expenditures. To date, Bisco Misr has invested about LE 33 million for increased production and quality, overdue maintenance, and distribution/sales facilities.

• Management has written-off non-saleable inventory and old unusable packaging, sacrificing short-term profit for long-term viability and clean up of its balance sheet.

• Management instituted an early retirement program to reduce excess employees who were eligible. Several hundred have taken advantage of the program. The remaining employees have received 35% raises, training, and professional growth opportunities with a potentially significant player in the regional food industry sector.

• Despite the early retirement program and layoffs, the company has added 72 employees with skills in marketing, sales, finance, and IT to enhance the company’s new market/customer driven focus.

TECHNICAL ASSISTANCE FOR POLICY REFORM II 29

NATIONAL PAPER CO.

Information contained within is sourced from discussions with the company management and from data provided by the company management, the Holding Company for Chemical Industries and the Ministry of Investment unless otherwise footnoted.

TECHNICAL ASSISTANCE FOR POLICY REFORM II 30

COMPANY BACKGROUND National Paper Co. is the oldest paper company in Egypt. Based in Alexandria, the company was established in 1934 to produce various paper products; and was changed to a public company in 1961. In July 2005, it was privatized through the tender and sale of 100% of the company’s shares to the Al Kharafi Group, a Kuwaiti based international conglomerate. The company is a producer of special use papers that have unique market niches including: brown papers used to make boxes, paper used for cement bags (the only cement bag producer in the Middle East), industrial wrapping paper, textile cones, and insulated paper used in high tension electrical wires. PRIVATIZATION HISTORY AND INFORMATION National Paper Co. was privatized in July 2005 following a public tender and sale of 100% of the shares of the company to the Al Kharafi Group. The Al Kharafi Group is a Kuwaiti based international conglomerate with global operations and annual revenues exceeding $3.9 billion (Forbes 500). The group is over 100 years old with interests in engineering and construction, food industries and agricultural business, banking and investments, manufacturing and industry, real estate and infrastructure development tourism, leisure and hospitality and aviation services. The company is one of the most active and diversified operations in the Arab world and plans to expand its interests in the region.

In addition to paying LE 135 million for 100% of National Paper, Al Kharafi has committed to investing LE 300 million to replace the old equipment of the company. To date, few changes in management are apparent, but changes have been made in the human resources area that will be discussed below.

PRE AND POST PRIVATIZATION TRENDS ANALYSIS PRE- PRIVATIZATION SITUATION SUMMARY

Management indicated that the company was generating moderate revenues and profitable prior to privatization. The company was impeded from further development and growth by its old machinery and equipment and the lack of capital necessary to invest adequately in the company. The management team also understood that without the help of an investor with the ability to make necessary capital investments, the company would be able to survive in the short run but its ability to continue to compete in the market over the long term would be severely restricted. Thus, management was supportive of the privatization of the company. REVENUES AND INCOME

Below are the revenues and net income for National Paper Co. prior to privatization. The management of the company was not allowed to disclose post-privatization financial information without permission from the new owner, thus the information is gleaned from management discussions.

TECHNICAL ASSISTANCE FOR POLICY REFORM II 31

Table 11: National Paper Revenues and Net Income Pre and Post-Privatization

Source: Company Management

*Management was not able to provide financial information pending permission from Al Kharafi Group.

IMPACT ON LABOR

The impact of privatization on the National Paper employees has been very positive. All of the staff across the board received 25% salary increases and a bonus program has been initiated. Salaries have gone from LE 19.2 million to LE 20.4 million. Computer training has been implemented for many employees in the company. In addition, the employees were given health insurance that allows them to use any hospital that the individual employee prefers. The company is paying 90% of the cost of health insurance and the employee the remaining 10%. Accident insurance has also been offered to the workers covering accidents occurring both inside and outside the company facilities, with coverage up to LE 50,000 per worker. The number of employees has increased from about 970 to 1,060 employees. CAPITAL EXPENDITURES

National Paper has six production lines for producing different types of paper. All of the machines are old. Some of the machines were bought second hand in 1934 from Europe. The capacities of machines are 20-25 tons per day. Prior to privatization, only maintenance level expenses were undertaken. Under the new ownership, the company will be upgrading the equipment, resulting in increased production levels in the 300-325 ton per day range. The company anticipates spending in the area of LE 300 million. The company has recently completed a technical study and anticipates starting the implementation of the investments by year end 2007. MARKET DEVELOPMENT

In the past National Paper’s sales were principally in the local Egyptian market with very small sums of exports ranging in the 100-200 ton per year range. Just prior to privatization, the company began focusing its efforts on sales to international markets in the region. The company achieved about 2,000 tons of exports. Since privatization, the company has exported about 3,500 tons of paper in just a few months to Turkey and other Arab countries. NEW MANAGEMENT TECHNIQUES/SKILLS

The acquisition of National Paper by Al Kharafi is still in its early stages. Al Kharafi has been moving slowly to implement changes. There have been few management changes, but more changes are expected as the new owners complete its technical review. BENEFITS TO THE EGYPTIAN ECONOMY AND GOVERNMENT

The sale of National Paper Co. to Al Kharafi Group has enabled the government to raise LE 135 million from the sale of the company. In addition, Al Kharafi Group has committed to invest an additional LE 300 million in much needed investment to modernize the company’s equipment. Finally, the payment of enhanced employee health and accident benefits by the company also provides a cost savings to the government.

Pre- Privatization Post- Privatization LE (000)

2003 2004 2005* 2006*

Revenues LE 105,429 LE 120,613 N/A N/A

Net Income LE 10,671 LE 18,958 N/A N/A

TECHNICAL ASSISTANCE FOR POLICY REFORM II 32

CONCLUSIONS AND FINDINGS • Government of Egypt sold 100% of National Paper Company to the international

Kuwaiti owned conglomerate Al Kharafi Group for LE 135 million. • It is too early in the privatization process of National Paper Company to fully evaluate

the impact, but the acquisition should be positive for the future of the company. • National Paper’s acquisition by the Al Kharafi Group will expose the company to a

world class organization that will enhance the company’s access to capital, new markets, and management expertise.

• Al Kharafi Group has committed to invest LE 300 million in new capital to modernize the equipment that will enable the company to compete internationally with a high quality product offering and to expand its capacities for the first time in decades.

• National Paper under the ownership of Al Kharafi Group has increased the number of workers from 970 to 1060 and is willing to invest in the employees of the company by offering 25% salary increases, attractive healthcare benefits, accident insurance, bonus for performance, and training. As a result, workers are becoming more productive, increasing production in six months from 32,500 tons to 35,600 tons.

TECHNICAL ASSISTANCE FOR POLICY REFORM II 33

SAN STEFANO HOTEL

SAN STEFANO HOTEL CIRCA EARLY 20TH CENTURY

Information contained within is sourced from discussions with the company management and from data provided by the company, the Holding Company for Tourism and Cinema and the Office of the Ministry of Investment unless otherwise footnoted.

TECHNICAL ASSISTANCE FOR POLICY REFORM II 34

BACKGROUND San Stefano Hotel was established in the beginning of the 20th Century in Alexandria on a land area of 30,367 square meters. The three-star hotel had a capacity of 132 rooms. Unfortunately, due to a lack of investment over the years, the building lost its luster and the hotel has been closed since 1993.

In 1998, after unsuccessful attempts to tender the property, the Holding Company for Tourism and Cinema launched a competitive tender to sell the property that allowed the potential investors to construct a high rise hotel complex, encouraging investors to make higher offers than the prior tenders. Talaat Moustafa Group (TMG) was successful in winning the competitive bid against other potential investors. TMG’s bid was approximately LE 270 million for the building and the land. TMG’s bid included the construction of a complex that would include the hotel, luxury residences, a mall and parking garage. Since winning the bid, TMG has invested over LE 2.5 billion for the demolition and total rebuilding of the San Stefano Hotel Complex. The San Stefano Hotel will be managed by Four Seasons Resort Hotels as a five-star hotel and will open in December 2006. In addition to the hotel and127 luxury suites, the complex will include about 945 luxury apartments, a luxury shopping mall, office space, and an underground parking facility. The shopping mall was inaugurated in July 2006 and about 60% of the apartments have been sold. PRIVATIZATION PROCESS

The San Stefano hotel was a challenging hotel property for the government to privatize. The government initiated a number of tenders but the amounts offered were not acceptable to the government. The lack of acceptable bids could be attributed to the fact that the government would not allow a high rise building to be built, which impacted the amounts that potential bidders were willing to offer. In April 1998, the government agreed to tender the hotel and in this case allow the potential bidders to present proposals that would allow for a high rise building in the area. Potential bidders understood that the old San Stefano building would require demolition a new facility built in its place. The government’s tender required the establishment of a five-star hotel utilizing the name of the old hotel and including conference room facilities, game rooms and showroom.

Talaat Moustafa Group and a group of other Arab and Egyptian investors formed the Arab Co. for Hotels & Tourism Investment and submitted the successful bid of approximately LE 270 million for the land and the building plus LE 50 million for sales tax on the construction contract. The winning bid included the development and construction of a luxury five-star Four Seasons managed hotel, luxury apartments, luxury shopping mall, business offices and underground parking for 2,400 vehicles. The Hotel Complex envisioned by TMG will transform the Alexandria Corniche, and will likely become an anchor for the redevelopment and modernization of tourism in Alexandria. BACKGROUND ON TALAAT MOUSTAFA GROUP

Talaat Moustafa Group is an Egyptian real estate developer that operates in the field of real estate and tourism; contracting and building materials manufacturing; agricultural and agriculture products; and general investments. The company is capitalized 51% by the Talaat Moustafa Group and 49% by other Arab and international investors. The San Stefano Complex is among the group’s largest tourism projects.

TECHNICAL ASSISTANCE FOR POLICY REFORM II 35

SAN STEFANO COMPLEX San Stefano Company for Real Estate Investment was incorporated in 1998 under Law 159/1981 as an Egyptian Joint Stock Company developing communities and selling, renting and using residential units, with issued capital of LE 250 million and raised several times in order to face the financing requirements of the Company. San Stefano Company for Real Estate Investment has 24 shareholders including Talaat Moustafa Group, Misr Insurance Co., the National Bank of Egypt, Arab Joint Investment Co. et al.