-

8/6/2019 PPT_Sec C_Group 11

1/17

Fiscal PolicyFiscal Policy

&&Current AccountCurrent Account

Submitted by:Group 11Section C

Harsh AgrawalMadhumitha JPankaj AroraPraveen TrivediSneha

HingoraniTirtheshwar Banerjee

-

8/6/2019 PPT_Sec C_Group 11

2/17

IntroductionIntroduction To what extent fiscal adjustment

can

contribute to resolving externalimbalances?

Post liberalization trajectory of the country

Relationship between various parameters of

fiscal policy and the current account.

-

8/6/2019 PPT_Sec C_Group 11

3/17

Fiscal PolicyFiscal Policy

-

8/6/2019 PPT_Sec C_Group 11

4/17

Current AccountCurrent Account

-

8/6/2019 PPT_Sec C_Group 11

5/17

Theoretical StudyTheoretical StudyMajor factors through which

fiscal policy affects currentaccount:

-

8/6/2019 PPT_Sec C_Group 11

6/17

Tax and current accountTax and current account

(

Am

oun

t

in

th

ou

sa

nd

)

cr

or

es

-

8/6/2019 PPT_Sec C_Group 11

7/17

Government Expenditure andGovernment Expenditure andcurrent

accountcurrent account

(

Am

oun

t

in

th

ou

sa

nd

)

cr

or

es

-

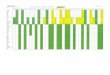

8/6/2019 PPT_Sec C_Group 11

8/17

AnalysisAnalysisWe took the previous 20 year data of all 5

parameters of fiscalpolicy (described in previous slides) and got

the equation tocalculate Net Current Account is as follows:

NCA = -68444.6 -1.066 Td+ 0.90 Ti -0.419 Rex + 0.853 Cex +0.700

S

Finding - Revenue- expenditure (Rex) and subsidy(S) ; and

indirect

(Ti) and direct taxes (Td) are highly correlated.

In such case there will be error in distinguishing the

independenteffect of each variable.

-

8/6/2019 PPT_Sec C_Group 11

9/17

AnalysisAnalysis

A lso th e sig n ifica n ce le v e lo f v a ria b le su b sid y

S U B S ID Y w a s b e y o n

.a cce p ta b le lim its

,H e n ce W e ig n o re d th e sub sid y v a ria b le a n d u

sed to ta lta x v a ria b le

.co m b in in g d ire ct an d in d ire ct va ria b le

-

8/6/2019 PPT_Sec C_Group 11

10/17

We performed the regression again and derived theequation

as:

NCA = -12573.3 -.074 T - 0.212 Rex+ 1.292 Cex

A n a ly sis

-

8/6/2019 PPT_Sec C_Group 11

11/17

Now we studied the impact of fiscal policy variables on

majoringredients (Merchandise and Invisible account) of net

currentbalance. (Again performed the regression twice for it.)

The effect of capital expenditure, revenue expenditure and

totaltax

on merchandise output can be described as:

MA = 32160-.481 T - 0.264 Rex+ 1.579 Cex

And on the invisibles account as:

IA = -44733.9+.407 T + 0.052 Rex 0.287 Cex

A n a ly sis

-

8/6/2019 PPT_Sec C_Group 11

12/17

-R e g re ssio n M e rch a n d ise-R e g re ssio n M e rch a n d

ise

A c c o u n tA c c o u n t

-

8/6/2019 PPT_Sec C_Group 11

13/17

-R e g re ssio n In v isib le-R e g re ssio n In v isib le

A c c o u n tA c c o u n t

-

8/6/2019 PPT_Sec C_Group 11

14/17

ConclusionConclusion Association between fiscal policy and the

emergence or

unwinding of large external imbalances is limited. Changesin

fiscal policy are indeed associated with changes in thecurrent

account, but the relationship is far less than one-for-one.

Tax, which constitutes direct and indirect tax, has very

lesssignificance in determining the change in the total

currentaccount (as a whole) of India.

but when we decompose the constituents of current accountas

merchandise account and invisible account and find thesignificance

of tax in determining them, we find it to besubstantial.

-

8/6/2019 PPT_Sec C_Group 11

15/17

Conclusion - Effect onConclusion - Effect onMerchandise and

invisible accountMerchandise and invisible account

Total Tax and capital expenditure are most critical

indetermining the Total Merchandise value and

individualaccount.

Revenue expenditure is not much accurate predictor for

these accounts. If Total tax increases by 1%, total merchandise

value

decreases by 0.481%, whereas invisible account increasesby

0.407%.

if Capital expenditure increases by 1%, total

merchandiseincreases by 1.579% whereas invisible account

decreasesby 0.287%.

-

8/6/2019 PPT_Sec C_Group 11

16/17

Thank YouThank You

-

8/6/2019 PPT_Sec C_Group 11

17/17

Merchandised and invisible Merchandised and invisible

improved regressionimproved regression

M e rch a n d ised

A c c o u n t

In v isib le

A c c o u n t