Embed Size (px)

DESCRIPTION

bhghfhg

Citation preview

Stock Price Selection System Using NeuroFuzzy Modelling

Guided by:

Mr.N.Srinivasan

Presented by:

Ramya.T(3111312)

Preeti Singh(3111296)

BONAFIDE

DECLARATION

ABSTRACT

Neural networks have been used for forecasting purposes for some years

now. Often arises the problem of a black-box approach, i.e. after having trained

neural networks to a particular problem, it is almost impossible to analyse them for

how they work. Fuzzy Neuronal Networks allow adding rules to neural networks. This

avoids the black-box-problem. Additionally they are supposed to have a higher

prediction precision in unlike situations. Applying artificial neural network, genetic

algorithm and fuzzy logic for the stock market prediction has attracted much attention

recently, which has better correlated the non quantitative factors with the stock

market performance. However these approaches perform less satisfactorily due to

the memory less nature of the stock market performance. In this paper, we propose

a data compression-based portfolio prediction model hybridized with the fuzzy logic

and genetic algorithm. In the model, the quantifiable microeconomic stock data are

first optimized through the genetic algorithms to generate the most effective

microeconomic data in relation to the stock market performance.

TABLE OF CONTENTS

CHAPTER NO TITLE PAGE NO

1. Introduction 1.1 Overview 1.2 Literature review 1.3 Existing system and its limitations 1.4 Motivation 1.5 Organization of the report

2. Aim and Scope2.1Scope of the project2.2Objectives2.3Existing methodology2.4Problem statement2.5Overview of proposed work

3. Method and algorithms used3.1Hardware requirements3.2Software requirements3.3System design that includes architecture diagram, flow chart UML and

sequence diagram with explanation of each3.4Proposed work

3.4.1 Modules3.4.2 Module description3.4.3 Algorithm with input and output specified

4. Result and discussion and performance analysis4.1Screenshots4.2Description of each screenshots4.3Analysis using graphs and tables

5. Summary and conclusion

6. References

CHAPTER 1

1. Introduction:-

A number of studies have examined the differences between neural networks

and other approaches for modeling and forecasting time series. Especially the

question if no linear models like neural networks can beat linear models have been

an issue for several years. Nevertheless the solution seems still to be unclear when

taking into account the cost - i.e. the computational and methodological expenses. In

this paper two types of neural networks are examined. The first is the classical

neural network approach where a neural network is used to predict the future price of

an asset from the history of the time series itself. The second approach is a family of

quite new neural network models where fuzzy logic is combined with neural

technology to archive higher precision in forecasting and some additional issues.

Fuzzy neural networks provide the possibility to implement rules into neural

network topology; a methodic framework is described in practice fuzzy neural

networks compete with classical neural networks where no extra information is given

than the patterns created out of the time series. An introduction into applying neural

networks for casting financial time series is given. The application of rules allows to

model patterns which occur not very often and are therefore not very likely to be

modeled by a classical neural network. Rules or groups of rules can be modeled

which are specialized on specific situations and circumstances In this paper, a new

data compression-based portfolio prediction model hybridized with genetic algorithm

and fuzzy logic is developed. Traditionally, difference models are applied in the area

of portfolio prediction. Two classical views on the prediction are namely, technical

and quantitative.

The technical view of markets is that the prices are driven by investor

sentiment and that the underlying sequence of prices can be captured and

predicated well using charting techniques. This method studies the action of the

market as a dynamical entity, rather than studying the actual goods in which the

market operator. This is a science of recording the historical market data, such as

prices of stocks and the volume traded, and attempting to predict the future from the

past performance of the function of the underlying security valuation, but also

governed by investor sentiment, health of the economy and many others.

Fuzzy logic has been applied very successfully in many areas where

conventional model based approaches are difficult or not cost-effective to implement.

However, as system complexity increases, reliable fuzzy rules and membership

functions used to describe the system behavior are difficult to determine.

Furthermore, due to the dynamicwhich occur not very often and are therefore not

very likely to be modeled by a classical neural network. Rules or groups of rules can

be modeled which are specialized on specific situations and circumstances In this

paper, a new data compression-based portfolio prediction model hybridized with

genetic algorithm and fuzzy logic is developed. Traditionally, difference models are

applied in the area of portfolio prediction. Two classical views on the prediction are

namely, technical and quantitative.

The technical view of markets is that the prices are driven by investor

sentiment and that the underlying sequence of prices can be captured and

predicated well using charting techniques. This method studies the action of the

market as a dynamical entity, rather than studying the actual goods in which the

market operator. This is a science of recording the historical market data, such as

prices of stocks and the volume traded, and attempting to predict the future from the

past performance of the function of the underlying security valuation, but also

governed by investor sentiment, health of the economy and many others.

Fuzzy logic has been applied very successfully in many areas where

conventional model based approaches are difficult or not cost-effective to implement.

However, as system complexity increases, reliable fuzzy rules and membership

functions used to describe the system behaviour are difficult to determine.

Furthermore, due to the dynamic nature of economic and financial applications.

Rules and membership functions must beadaptive to the changing environment in

order to continue useful. This article outlines a Stock Market Prediction System

(SMPS) system that extends the neural networks approach to handle fuzzy,

probabilistic and Boolean information. An SPS combines the various advantages of

expert systems, artificial neural systems and fuzzy reasoning. It is designed as

integrated networks architecture, based on a building block called neural gate.

1.1 Overview

Matlab, a Mathworks company in the United States first introduced a set of

numerical analysis and high-performance computing software in 1983. Expanding its

capabilities the version was continually upgraded. Now, the latest version is 2010b

version. It provides a professional level of symbolic computation, word processing,

visual modeling and simulation and real-time control functions. Matlab is a

characteristic of all language features and next generation software development

platform.

Matlab has become suitable for many disciplines and powerful large-scale software.

Most of colleges and universities in Europe and other countries use it. Matlab has

become linear algebra, automatic control theory, mathematical statistics, digital

signal processing, time series analysis, dynamic system simulation and other

advanced courses in the basic teaching tool. In designing the study units and

industrial development sector, Matlab is widely used in research and solve specific

problems. In China, Matlab has received increasing attention in a short time it will

flourish, because no matter which discipline or engineering can be found right from

the Matlab function.

Today's information society, the image is mankind's access to information is one of

the most important sources. With the rapid development of computer technology,

image technology and the continued integration of computer technology to produce

a series of image processing software. Matlab has become internationally

recognized as the best application of technology. With simple programming and data

visualization, it can be seen the operable features.

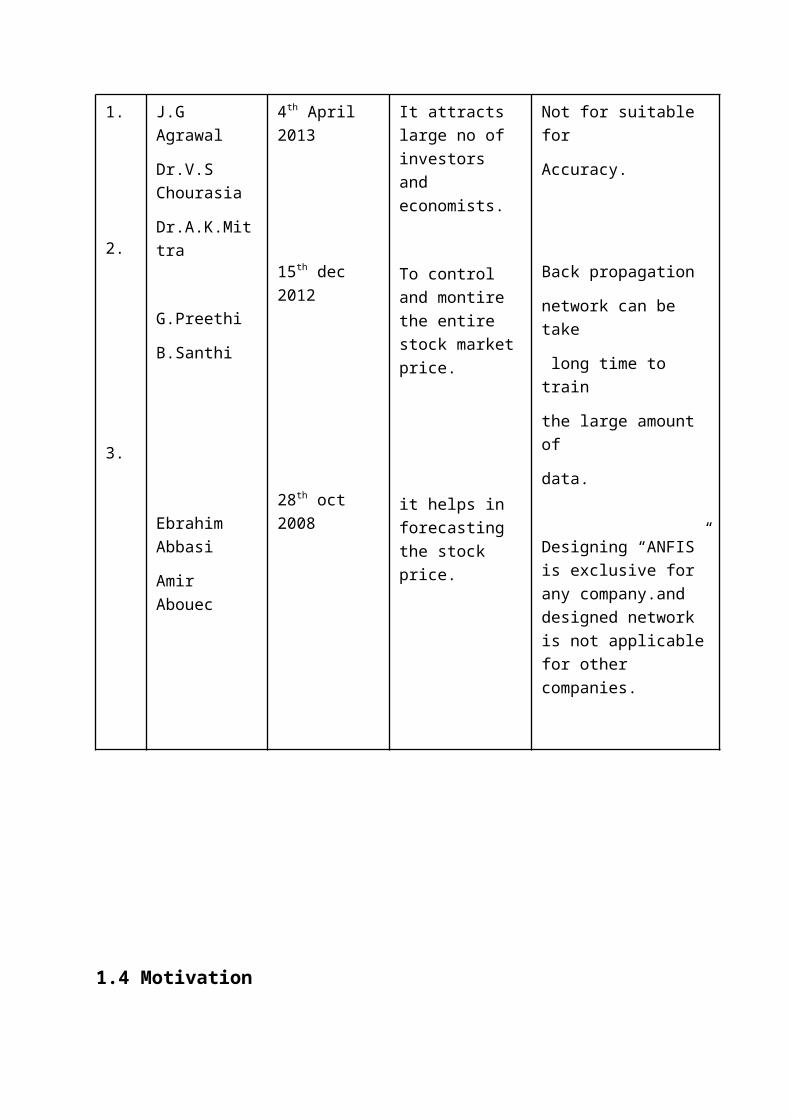

1.2 Literature review

SNO Name of the Author

Year of publication

Advantages Disadvantages

1.

2.

3.

J.G Agrawal

Dr.V.S Chourasia

Dr.A.K.Mittra

G.Preethi

B.Santhi

Ebrahim Abbasi

Amir Abouec

4th April 2013

15th dec 2012

28th oct 2008

It attracts large no of investors and economists.

To control and montire the entire stock market price.

it helps in forecasting the stock price.

Not for suitable for

Accuracy.

Back propagation

network can be take

long time to train

the large amount of

data.

Designing “ANFIS” is exclusive for any company.and designed network is not applicable for other companies.

1.4 Motivation

The Existing methods to predict stock price can have uncertainity due to non

linear data overtime. Stock price prediction accurancy can be improved with neuro

fuzzy modelling and by looking into real time entities such as news, management

strategies and government decisions. In order to improve the accurancy a new

approach based on Neuro fuzzy and by looking into real time entities can be

incorporated

In this paper, a new data compression-based portfolio prediction model

hybridized with genetic algorithm and fuzzy logic is developed. Traditionally,

difference models are applied in the area of portfolio prediction. Two classical views

on the predictionare namely, technical and quantitative. The technical view of

markets is that the prices are driven by investor sentiment and that the underlying

sequence of prices can be captured and predicated well using charting techniques.

In this paper, we mainly discuss steps and methods of using neural network to

predict stock market, including sampling principles, principles of determining the

number of node in hidden layers. Then the previous stock market performance with

the effective stock data and the fuzzified microeconomic data are processed based

on the context-based modeling and vector quantization. Finally, the prediction of the

stock market performance with the stock data is defuzzified using the fuzzification

model to produce a portfolio performance prediction. The major concern of the study

is to develop a system that can predict future prices in the stock markets by taking

samples of past prices. The developed system seems to work acceptable.

Experiments show that obtained forecasts have about 70% accuracy; this result can

be seen as satisfying for such difficult task.

1.5 Organizationof the report

CHAPTER 2

2.Aim and scope

2.1 Scope of the project

After an extensive literature survey all the drawbacks of the existing system

have been noted and plans and methodologies to overcome those limitations. The

Scope of the project carries the aim and view of the project.

2.2 Objective

To predict the future stock price.

Implementing Fuzzy Rule and Neural Network Modeling for high accuracy.

Suggestions to the user about time dependent information about the stock.

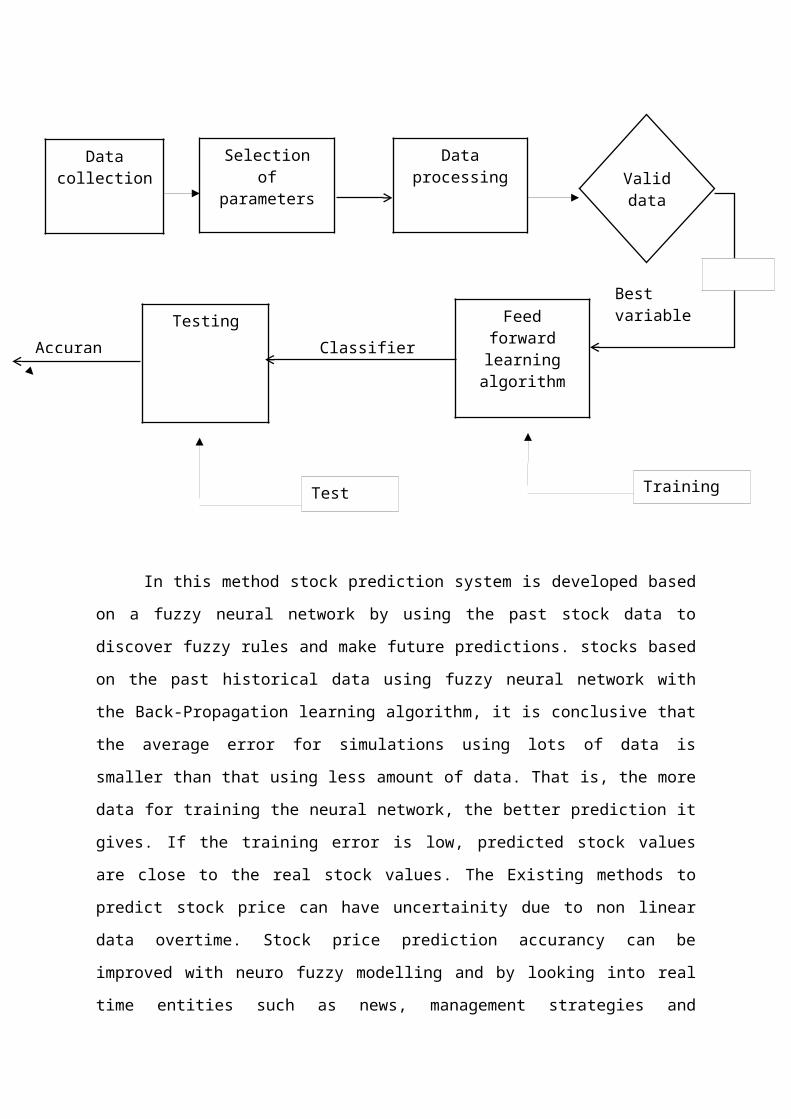

2.3 Existing system and its limitations

No

In this method stock prediction system is developed based on a fuzzy neural

network by using the past stock data to discover fuzzy rules and make future

predictions. stocks based on the past historical data using fuzzy neural network with

the Back-Propagation learning algorithm, it is conclusive that the average error for

Data collection

Selection of parameters

Data processing Valid

data

Feed forward learning algorithm

TestingClassifier

Best variable

Accurancy

Training dataTest data

Yes

simulations using lots of data is smaller than that using less amount of data. That is,

the more data for training the neural network, the better prediction it gives. If the

training error is low, predicted stock values are close to the real stock values. The

Existing methods to predict stock price can have uncertainity due to non linear data

overtime. Stock price prediction accurancy can be improved with neuro fuzzy

modelling and by looking into real time entities such as news, management

strategies and government decisions. In order to improve the accurancy a new

approach based on Neuro fuzzy and by looking into real time entities can be

incorported.

Disadvantages:

High future price

Accuracy is low

2.4 Problem Statement

Stock price predeiction

2.5 Overview of Proposed Methodology

Matlab, a Mathworks company in the United States first introduced a set of

numerical analysis and high-performance computing software in 1983. Expanding its

capabilities,the version was continually upgraded. Now, the latest version is 2010b

version. It provides a professional level of symbolic computation, word processing,

visual modeling and simulation and real-time control functions. Matlab is a

characteristic of all language features and next generation software development

platform.

Matlab has become suitable for many disciplines and powerful large-scale

software. Most of colleges and universities in Europe and other countries use it.

Matlab has become linear algebra, automatic control theory, mathematical statistics,

digital signal processing, time series analysis, dynamic system simulation and other

advanced courses in the basic teaching tool. In designing the study units and

industrial development sector, Matlab is widely used in research and solve specific

problems. In China, Matlab has received increasing attention in a short time it will

flourish, because no matter which discipline or engineering can be found right from

the Matlab function.

Today's information society, the image is mankind's access to information is

one of the most important sources. With the rapid development of computer

technology, image technology and the continued integration of computer technology

to produce a series of image processing software. Matlab has become internationally

recognized as the best application of technology. With simple programming and data

visualization, it can be seen the operable features.

Chapter 3

3.Methods and algorithm used

3.1 Hardware requirements

Processor Type : Pentium -IV

Speed : 2.4 GHZ

Ram : 128 MB RAM

Hard disk : 20 GB HD

3.2 Software requirements

Operating System : Windows 7

Software Programming Package : Matlab R2013a

3.3 System design that includes architecture diagram

11

3.4 Proposed work

In this paper, a new data compression-based portfolio prediction model

hybridized with genetic algorithm and fuzzy logic is developed. Traditionally,

difference models are applied in the area of portfolio prediction. Two classical views

on the prediction are namely, technical and quantitative. The technical view of

markets is that the prices are driven by investor sentiment and that the underlying

sequence of prices can be captured and predicated well using charting techniques. In

this paper, we mainly discuss steps and methods of using neural network to predict

stock market, including sampling principles, principles of determining the number of

node in hidden layers. Then the previous stock market performance with the effective

stock data and the fuzzified microeconomic data are processed based on the context-

based modeling and vector quantization. Finally, the prediction of the stock market

performance with the stock data is defuzzified using the fuzzification model to

produce a portfolio performance prediction. The major concern of the study is to

develop a system that can predict future prices in the stock markets by taking samples

of past prices. The developed system seems to work acceptable. Experiments show

that obtained forecasts have about 70% accuracy; this result can be seen as satisfying

for such difficult task.

3.4.1 Modules• Construct the classifier

• KNN classifier

• Cross validation classifier

• Draw a circle around the 10 nearest neighbours

• Data clustering

• Training Data

3.4.2 Modules description

3.4.3 Algorithm with input and

output specifiedAn n-input-1-output fuzzy neural network has m fuzzy IF-THEN rules which are

described by

IF x1 is A1kand … and xn is An

k THEN y is B

k,

where x i and y are input and output fuzzy linguistic variables, respectively. Fuzzy linguistic

values Aikand B

kare defined by fuzzy membership functions as follows,

μA k

i ( xi )=exp [−(xi−a i

k

σ ik )2]

(1)

μBk( y )=exp[−( y−bk

ηk )2 ] (2)

the n-input-1-output fuzzy neural network with simple fuzzy reasoning is defined below:

f ( x1 ,. .. , xn )=∑k=1

mbk [∏i=1

nμ A

ik( xi )]

∑k=1

m[∏i=1

nμ

A ik( x i) ] (3)

Given n-dimensional input data vectors xp (i.e., xp = (x1p, x2

p,……, xnp))and one-dimensional

output data vector yp for p=1,2,...,N, (i.e., N training data sets). The energy function for p is

defined by

E p=12[ f ( x1

p , . .. , xnp )− y p ]2

(4)

For simplicity, let E and fp

denote Ep

and f ( x1p , .. . , xn

p ) , respectively. After training the

centers of output membership functions (

∂ EP

∂ bk), the widths of output membership functions(

∂ EP

∂ δk), the centers of input membership functions(

∂ EP

∂ ak) and the centers of input

membership functions(

∂ EP

∂σ k), then we obtain the training algorithm [5 -7]:

bk( t +1)=bk ( t )−θ∂ EP

∂bk|t

(5) σ k( t +1)=σk ( t )−θ

∂ EP

∂ σ k|t

(6)

ak( t +1)=ak ( t )−θ∂ EP

∂ ak|t

(7) ηk( t+1)=ηk( t )−θ

∂ EP

∂ηk|t

(8)

Where, is the learning rate and t=0,1,2,…

The main steps using the learning algorithm as follows:

Step 1: Present an input data sample, compute the corresponding output;

Step 2: Compute the error between the output(s) and the actual target(s);

Step 3: The connection weights and membership functions are adjusted;

Step 4: At a fixed number of epochs, delete useless rule and membership function nodes, and

add in new ones;

Step 5: IF Error > Tolerance THEN go to Step 1 ELSE stop.

When the error level drops to below the user-specified tolerance, the final

interconnection weights reflect the changes in the initial fuzzy rules and membership

functions. If the resulting weight of a rule is close to zero, the rule can be safely removed

from the rule base, since it is insignificant compared to others. Also, the shape and position of

the membership functions in the Fuzzification and Defuzzification Layers can be fine tuned

by adjusting the parameters of the neurons in these layers, during the training process.

CHAPTER 44.Result and discussion and performance analysis

The Hybrid Time Lagged Network (HTLN) has been tested with stock series of various

companies listed on the main board of the Kuala Lumpur Stock Exchange to analyse their

behaviours with respect to the varying degree of chaos in the input series [21]. In addition,

the performance of HTLN is compared with two standard networks for stock predictions.

They are the supervised Multilayer Perceptron network known as

Time Lagged Feed-forward Network (TLFN) and unsupervised Kohonen network known as

Highly Granular Unsupervised Time Lagged Network (HGUTLN) [21]. As the algorithms

intend to be used by traders for stock trading, the performance analysis is carried out for the

three neural network algorithms based on the stock trading performance.

best performance and the error factor increases geometrically with m, the degree of prediction

attempted.

The Hybrid Time Lagged Network (HTLN) has been tested with stock series of various

companies listed on the main board of the Kuala Lumpur Stock Exchange to analyse

behaviours with respect to the varying degree of chaos in the input series [21]. In addition,

the performance of HTLN is compared with two standard networks for stock predictions.

They are the supervised Multilayer Perceptron network known as

Time Lagged Feed-forward Network (TLFN) and unsupervised Kohonen network known as

Highly Granular Unsupervised Time Lagged Network (HGUTLN) [21]. As the algorithms

intend to be used by traders for stock trading, the performance analysis is carried out for the

three neural network algorithms based on the stock trading performance.

In this section, the trading performance of Diversif (Diversified Resources Berhad) and

Carlsberg (Carlsberg Brewery Malaysia Berhad) is used as examples to illustrate the

performance of the three neural networks. The reasons for showing these two stocks over the

others is the interesting nature of its stock price series including a few steep turns and lots of

different turning points in the price series.

4.1 Screenshots

4.2 Descrption for each screen shots

4.3 Analsis using graphs and tables

The performance of the TLFN, HGUTLN and HTLN networks based on the trading of

Diversif and Carlsberg stocks with initial starting value of 10,000 RM. In the figures, two

types of curves are shown. Liquid Cash indicates the cash values and Portfolio Value

indicates the cash and stock values. As shown in Fig. 7 and Fig. 8, it can be seen that the

hybrid HTLN network performs the best in terms of both the prediction quality and the

amount of profits generated. It gives a very stable performance and is not disturbed by the

chaotic nature of data. The supervised TLFN network performs with reasonable amount of

accuracy in terms of prediction. However, it can be thrown off balance if the input series is

very chaotic in nature. The unsupervised HGUTLN network performs the worst of the three

in terms of prediction quality. It has a lagging behaviour with respect to the input temporal

series.

The financial market different from a lot of physical systems like we know the weather is that

the financial market is a sort of complex feedback mechanism. What people expect prices to

be affects the prices they observe and then the prices they observe then affects how they are

going to form their expectations about what the prices will be in the next period. The market

is basically an uncertain beast or an uncertain institution, it’s an institution where people

trade risk, swap risk, and that’s why it’s there. And so if it were possible to predict it there

would be no risk. In individuals, I think there cannot be any publicly available system to

predict a financial market. On the other hand, neural networks have been found useful in

stock price prediction [1-2]. Both feedforward and recurrent neural networks have been

investigated and good results have been obtained. That means the prediction software would

be very useful to assist individuals in reaching a final decision. In this paper, assuming that it

is possible to predict markets, a prediction system is developed using fuzzy neural networks

with a learning algorithm to predict the future stock values. The system consists of several

neural networks modules. These models are all used to learn the relationships between

different technical and economical indices and the decision to buy or sell stocks. The inputs

to the networks are technical and economic indices. The output of the system is the decision

to buy and sell. There are several neural network methods for stock prediction, such as Time

Series method, Recurrent neural network and Feed-forward neural network method, etc. [2].

When compared to these techniques, Fuzzy neural network is a very useful and effective

method to process, which is explained in the later sections.

The learning algorithm is used to train the networks. Before learning starts, tolerances are

defined for the output units. During learning, the weights are updated only when the output

errors exceed the tolerances. The learning data for which the output errors do not exceed the

tolerances are eliminated from the training data sets. The input data to each network are the

moving averages of the weekly averaged data which are obtained directly by using a Java

program from the website. The output simulation data is also the average values of the

weekly stock data.

Time series forecasting analyzes past data and projects estimates of future data values.

Basically, this method attempts to model a nonlinear function by a recurrence relation derived

from past values. The recurrence relation can then be used to predict new values in the time

series, which hopefully will be good approximations of the actual values. There are two basic

types of time series forecasting: univariate and multivariate. Univariate models, like Box-

Jenkins, contain only one variable in the recurrence equation. The equations used in the

model contain past values of moving averages and prices. Box-Jenkins is good for short-term

forecasting but requires a lot of data, and it is a complicated process to determine the

appropriate model equations and parameters. Multivariate models are univariate models

expanded to "discover casual factors that affect the behavior of the data." [3-4]. As the name

suggests, these models contain more than one variable in their equations. Regression analysis

is a multivariate model, which has been frequently compared with neural networks. Overall,

time series forecasting provides reasonable accuracy over short periods of time, but the

accuracy of time series forecasting diminishes sharply as the length of prediction increases.

Many other computer-based techniques have been employed to forecast the stock market.

They range from charting programs to sophisticated expert systems. Fuzzy logic has also

been used. Expert systems process knowledge sequentially and formulate it into rules. They

can be used to formulate trading rules based on technical indicators. In this capacity, expert

systems can be used in conjunction with neural networks to predict the market. In such a

combined system, the neural network can perform its prediction, while the expert system

could validate the prediction based on its well-known trading rules. The advantage of expert

systems is that they can explain how they derive their results. With neural networks, it is

difficult to analyze the importance of input data and how the network derived its results.

However, neural networks are faster because they execute in parallel and are more fault

tolerant.

The major problem with applying expert systems to the stock market is the difficultly

in formulating knowledge of the markets because we ourselves do not completely understand

them. Neural fuzzy networks have an advantage over expert systems because they can extract

rules without having them explicitly formalized. In a highly chaotic and only partially

understood environment, such as the stock market, this is an important factor. It is hard to

extract information from experts and formalize it in a way usable by expert systems. Expert

systems are only good within their domain of knowledge and do not work well when there is

missing or incomplete information. Neural networks handle dynamic data better and can

generalize and make "educated guesses." Thus, neural networks are more suited to the stock

market environment than expert systems. In the wide variety of different models presented so

far, each model has its own benefits and shortcomings. The best way is that these methods

work best when employed together. The major benefit of using a fuzzy neural network then is

for the network to learn how to use these methods in combination effectively, and hopefully

learn how the market behaves as a factor of our collective consciousness.

CHAPTER 5

5 Summary and conclusion

In this paper, we mainly discuss steps and methods of using neural network to predict stock

market, including sampling principles, principles of determining the number of node in

hidden layers. Then the previous stock market performance with the effective stock data and

the fuzzified microeconomic data are processed based on the context-based modeling and

vector quantization. Finally, the prediction of the stock market performance with the stock

data is defuzzified using the fuzzification model to produce a portfolio performance

prediction. The major concern of the study is to develop a system that can predict future

prices in the stock markets by taking samples of past prices. The developed system seems to

work acceptable. Experiments show that obtained forecasts have about 70% accuracy; this

result can be seen as satisfying for such difficult task.

REFERENCES[1][Hie941] Y. Hiemstra. Linear Regression versus Backpropagation to PredictQuarterly

Excess Returns In: Pmceedings of the “Neuml Networks in the Capital Markets 1994”,

Pasadena, CA, 1994.

[2][JK95] J. Ledermann, R. A. Klein. Virtual %ding. Probus Publishing, 1995.

[3][Ras97] M. Rut. Application of Fuzzy Neural Networks on Financial Problems In:

Proceedings of the NAFIpS’97, Syracuse, NY, 1997.

[4]B.Vanstone and G. Finnie, "An Empirical Methodology for Developing Stockmarket

Trading Systems using Artificial Neural Networks,"Expert Systems with Applications,

vol. In Press, 2008.

[5]C.M. Huang, Q. Bi, G.S. Stiles, and R. W. Harris. Fast full search equivalent

encoding algorithms for image compression using quantization. IEEE Transactions

[6]Pamela C.Cosman, Eve A. Riskin, Rbert M. Gray, Combining Vector Quantization

and Histogram Equalization, BULB Journals, Information Processing & Management.

Vol. 28 Number 6, 1992 pp. 68 1-686

[7]G. S. Atsalakis and K. P.Valavanis, "Surveying stock market forecasting techniques -

part ii: Soft computing methods," Expert Systems with Applications, vol. In Press,

Corrected Proof, 2008.

[8] A. P. N. Refenes, A. N. Burgess, and Y. Bentz, "Neural networks in financial

engineering: A study in methodology," IEEE Transactions on Neural Networks, vol. 8(6),

pp. 1222 - 1267, 1997.