Embed Size (px)

Citation preview

Preparing for the Legacy of Your Business

www.berganpaulsen.comTwitter.com/berganpaulsen

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

Preparing for the Legacy of Your Business

About Me• Mike Regan, Assurance Partner• Specialize in tax and audit services for agribusinesses

About Bergan Paulsen• Full-service accounting and business consulting firm• Nearly 100 individuals in five locations • Industry Specialties: Agribusiness, Construction, Dealerships, Small Business,

Health Care, Manufacturing & Distribution, Nonprofit, Real Estate, Transportation

Today’s Agenda• Overview of American Taxpayer Relief Act of 2012• Farm Transition and Estate Planning• Business Succession and Transition

2

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

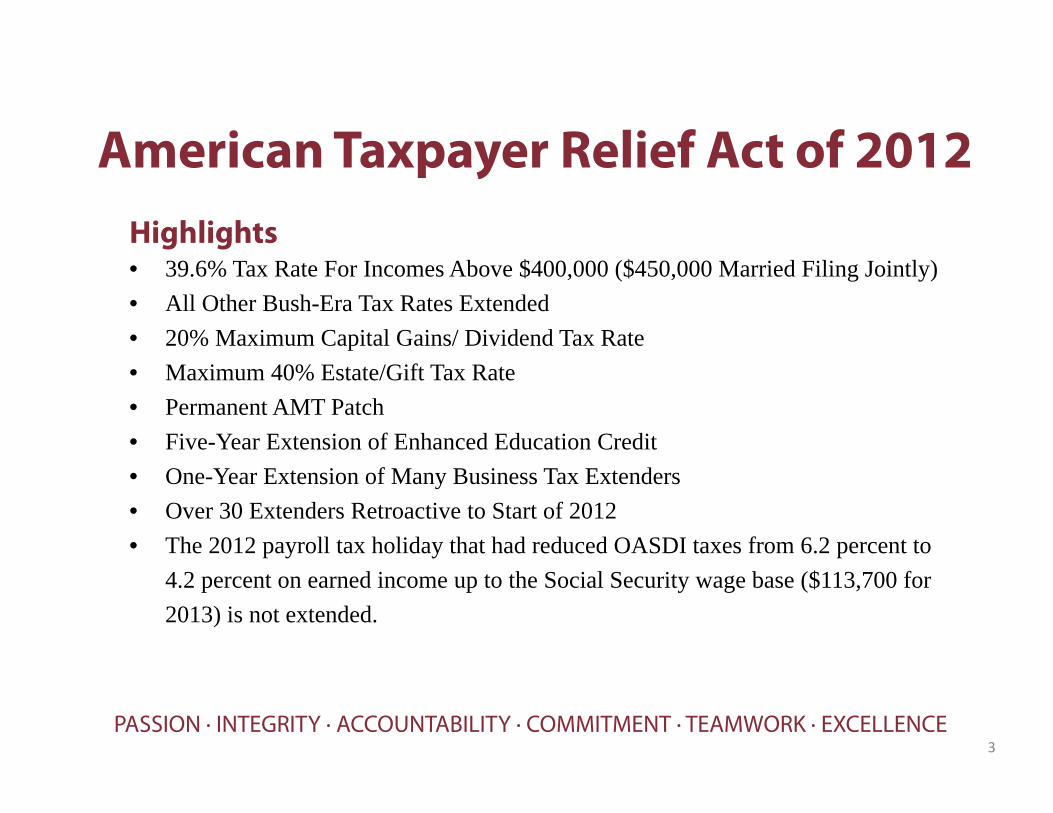

American Taxpayer Relief Act of 2012Highlights• 39.6% Tax Rate For Incomes Above $400,000 ($450,000 Married Filing Jointly)• All Other Bush-Era Tax Rates Extended• 20% Maximum Capital Gains/ Dividend Tax Rate• Maximum 40% Estate/Gift Tax Rate• Permanent AMT Patch• Five-Year Extension of Enhanced Education Credit• One-Year Extension of Many Business Tax Extenders• Over 30 Extenders Retroactive to Start of 2012• The 2012 payroll tax holiday that had reduced OASDI taxes from 6.2 percent to

4.2 percent on earned income up to the Social Security wage base ($113,700 for 2013) is not extended.

3

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

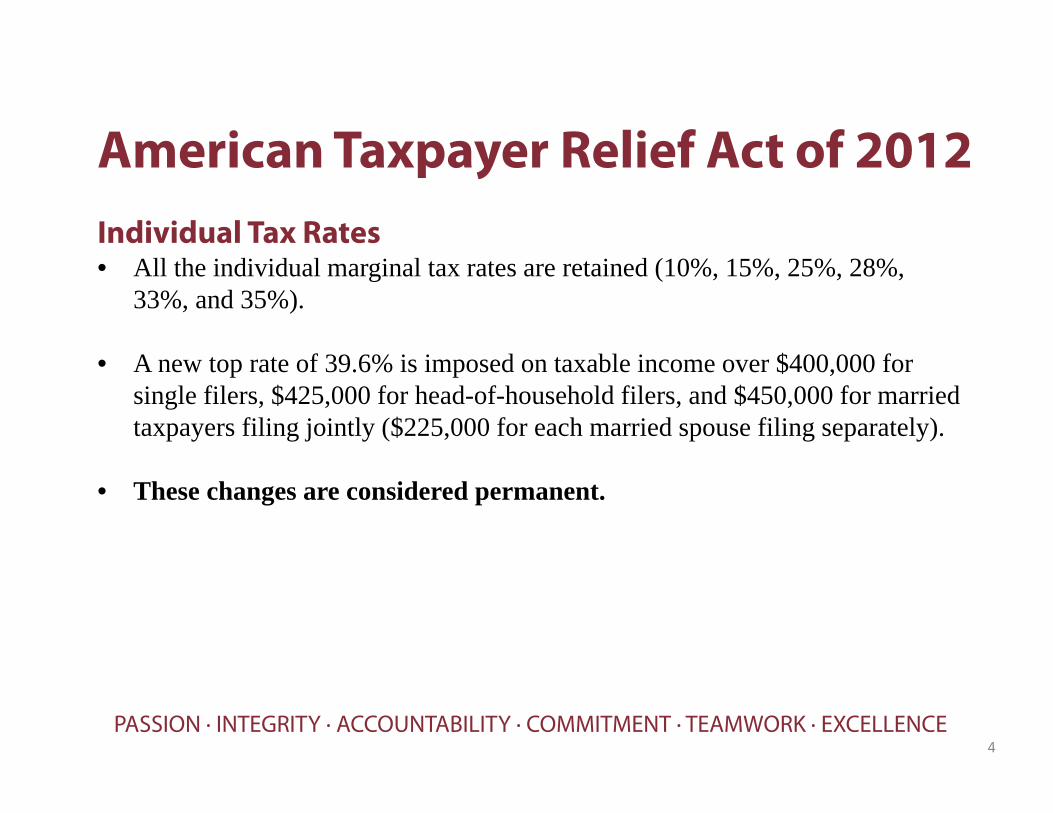

American Taxpayer Relief Act of 2012Individual Tax Rates• All the individual marginal tax rates are retained (10%, 15%, 25%, 28%,

33%, and 35%).

• A new top rate of 39.6% is imposed on taxable income over $400,000 for single filers, $425,000 for head-of-household filers, and $450,000 for married taxpayers filing jointly ($225,000 for each married spouse filing separately).

• These changes are considered permanent.

4

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

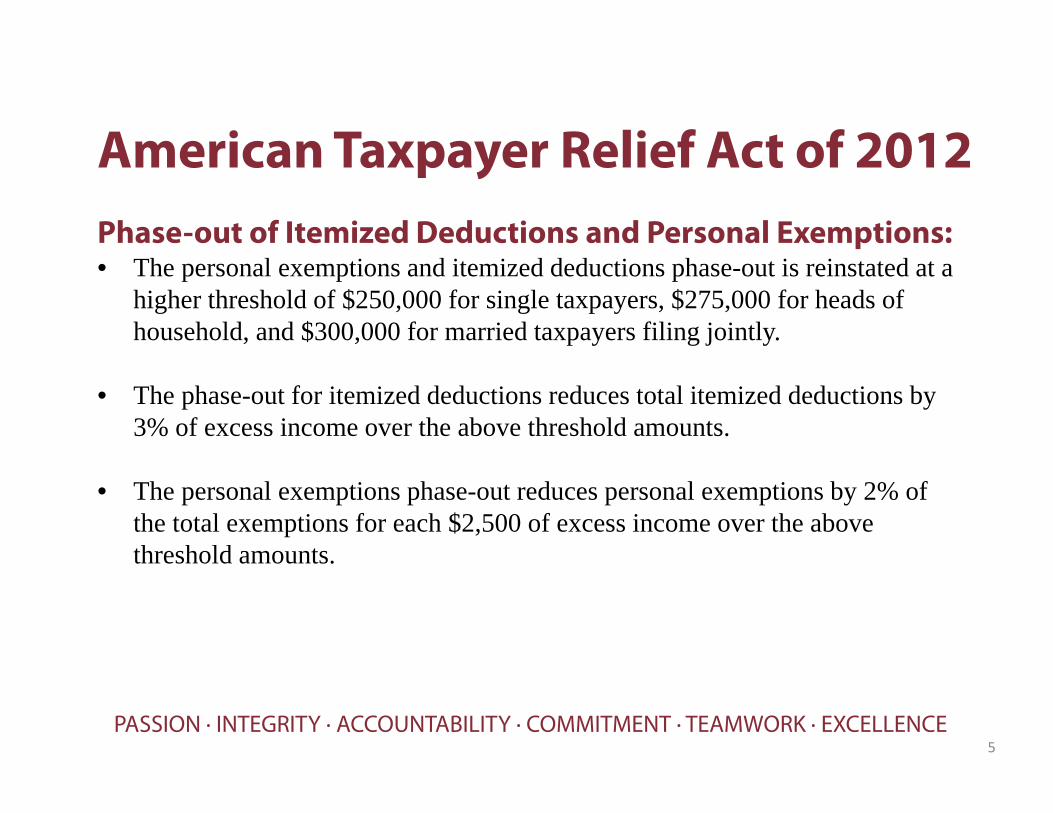

American Taxpayer Relief Act of 2012Phase-out of Itemized Deductions and Personal Exemptions:• The personal exemptions and itemized deductions phase-out is reinstated at a

higher threshold of $250,000 for single taxpayers, $275,000 for heads of household, and $300,000 for married taxpayers filing jointly.

• The phase-out for itemized deductions reduces total itemized deductions by 3% of excess income over the above threshold amounts.

• The personal exemptions phase-out reduces personal exemptions by 2% of the total exemptions for each $2,500 of excess income over the above threshold amounts.

5

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

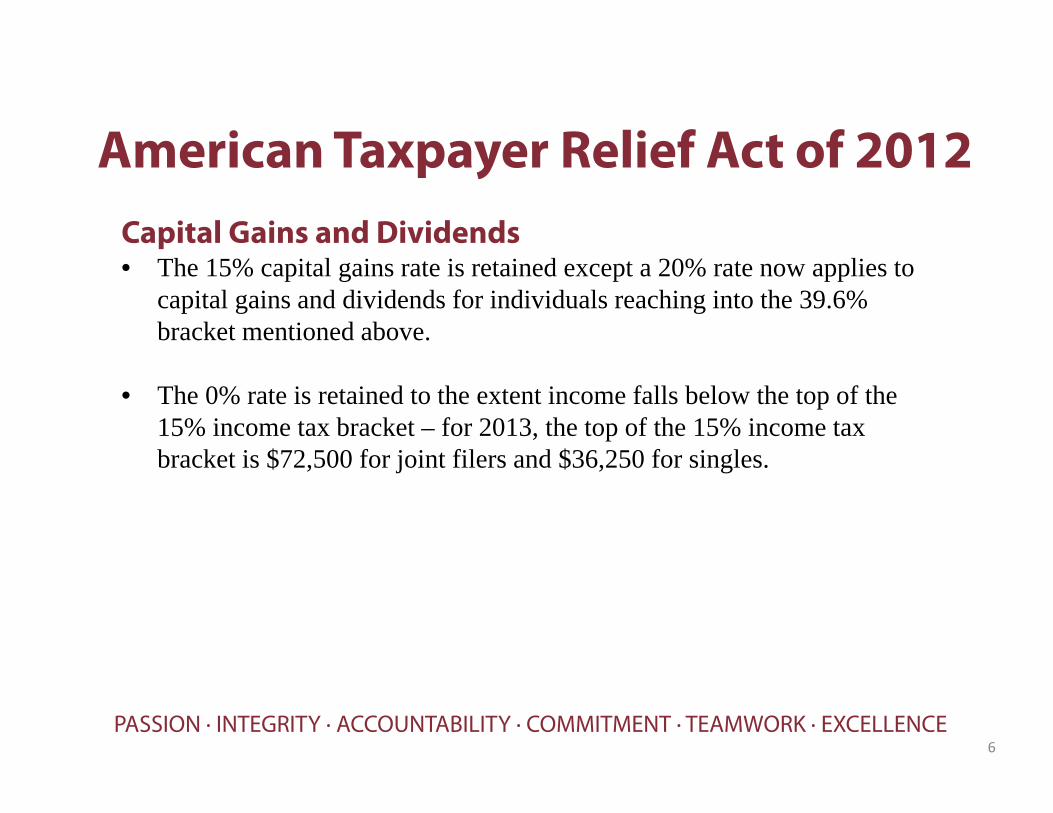

American Taxpayer Relief Act of 2012Capital Gains and Dividends• The 15% capital gains rate is retained except a 20% rate now applies to

capital gains and dividends for individuals reaching into the 39.6% bracket mentioned above.

• The 0% rate is retained to the extent income falls below the top of the 15% income tax bracket – for 2013, the top of the 15% income tax bracket is $72,500 for joint filers and $36,250 for singles.

6

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

American Taxpayer Relief Act of 2012Alternative Minimum Tax (AMT)• The exemption amount for the AMT on individuals is permanently

indexed for inflation.

• For 2012, the exemption amounts are $78,750 for married taxpayers filing jointly and $50,600 for single filers.

• Relief from AMT for nonrefundable credits is retained.

7

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

American Taxpayer Relief Act of 2012Estate and Gift Tax• The estate and gift tax exclusion amount is retained at $5 million

indexed for inflation ($5.12 million in 2012 and $5.25 million for 2013), but the top tax rate increases permanently from 35% to 40% effective January 1, 2013.

• The estate tax “portability” election, under which, if an election is made, the surviving spouse’s exemption amount is increased by the deceased spouse’s unused exemption amount, was made permanent by the act. To elect portability, the estate of the first deceased spouse must file an estate tax return by the due date of that return, even if the estate would not otherwise be required to file an estate tax return.

8

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

American Taxpayer Relief Act of 2012Individual Extension Provisions• The American opportunity tax credit for qualified tuition and other

expenses of higher education will now run through 2017.• The following are retroactively patched to 2012 and extended one year

through 2013:o Deduction for up to $250 for elementary and secondary school

teacherso Deduction of mortgage insurance premiums as qualified residence

interesto Deduction for state and local sales taxes paid in lieu of state and local

income taxes paido Above-the-line deduction for up to $4,000 of higher-education-

related-expenseso Exclusion from income for Qualified Charitable Distributions from

an IRA to a charity

9

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

American Taxpayer Relief Act of 2012Business Tax Extenders• Extended through 2013 the credit for increasing research and

development activities, which expired at the end of 2011.

• Expensing amounts under Sec. 179 are changed to $500,000 for 2012 and 2013 with a $2 million investment limit.

• Increased expensing amounts under Sec. 179 are extended through 2013.

• The availability of an additional 50% first-year bonus depreciation was extended for one year and now generally applies to property placed in service before January 1, 2014.

10

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

American Taxpayer Relief Act of 2012Business Tax Extenders, Cont’d.• The following were extended through 2013, and in some cases modified:

o The Work Opportunity Tax Credit was extended through 2013o 15 year straight-line cost recovery for qualified leasehold

improvements, qualified restaurant buildings and improvements, and qualified retail improvements

o Temporary exclusion of 100% of gain on certain small business stocko Reduction in S corporation recognition period for built-in gains taxo For tax years beginning in 2012 and 2013, the S corporation

recognition period for built-in gains tax is reduced to 5 years

11

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

American Taxpayer Relief Act of 2012Energy Tax Extenders• Extends and in some cases modifies the following energy credits that

expired at the end of 2011:o Credit for energy-efficient existing homeso Cellulosic biofuel producer credito Incentives for biodiesel and renewable dieselo Credits with respect to facilities producing energy from certain

renewable resourceso Credit for energy-efficient new homeso Alternative fuels excise tax credits

12

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

Affordable Care Act of 2010Additional taxes go into effect in 2013• Net investment income tax

o 3.8% net investment income tax applies to individuals (and estates/trusts) with net investment income and if modified adjusted gross income is above certain thresholds of $200,000 for single and head of household filers and $250,000 for married filing jointly.

o Net investment income include interest, dividends, capital gain, rental and royalty income, and passive business income.

• Additional medicare taxo 0.9% additional medicare tax applies to an individual’s wages and

self-employment income that exceeds a threshold amount based on an individual’s filing status. $200,000 for single and head of household filers and $250,000 for married filing jointly.

• Reporting employer provided health insurance on Form W-2 (code DD)

13

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

Farm Transition and Estate PlanningTrends in Agriculture• Like the rest of the population, farmers are aging.

o Average age of farm operator is age 57o Fastest growing segment is those over age 65o This aging trend suggests an increased need for planning as farmers

reach an age when transition must occur because of death, disability, or retirement

• We are not replacing aging farmers with beginning farmers.o As the country’s farmers get older there are fewer people standing in

line to take their placeo For every one farmer and rancher under the age of 25, there are five

who are age 75 and older

14

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

Farm Transition and Estate PlanningTrends in Agriculture• Families need to encourage young people to enter farming as an

occupation.• Increasing number of women involved in production agriculture and as ag

professionals• ISU Beginning Farmer Center conducts beginning farmer programs and

business succession programs – www.extension.iastate.edu/bfc• Beginning Farmer Tax Credit Program – Iowa income tax credit

authorized by the Iowa Ag Development Authority for asset owners leasing land to beginning farmers whereby the owner may provide a better lease rate due to the savings received from the tax credit. Tax credit is 5% of cash rental or 15% of crop share rental

15

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

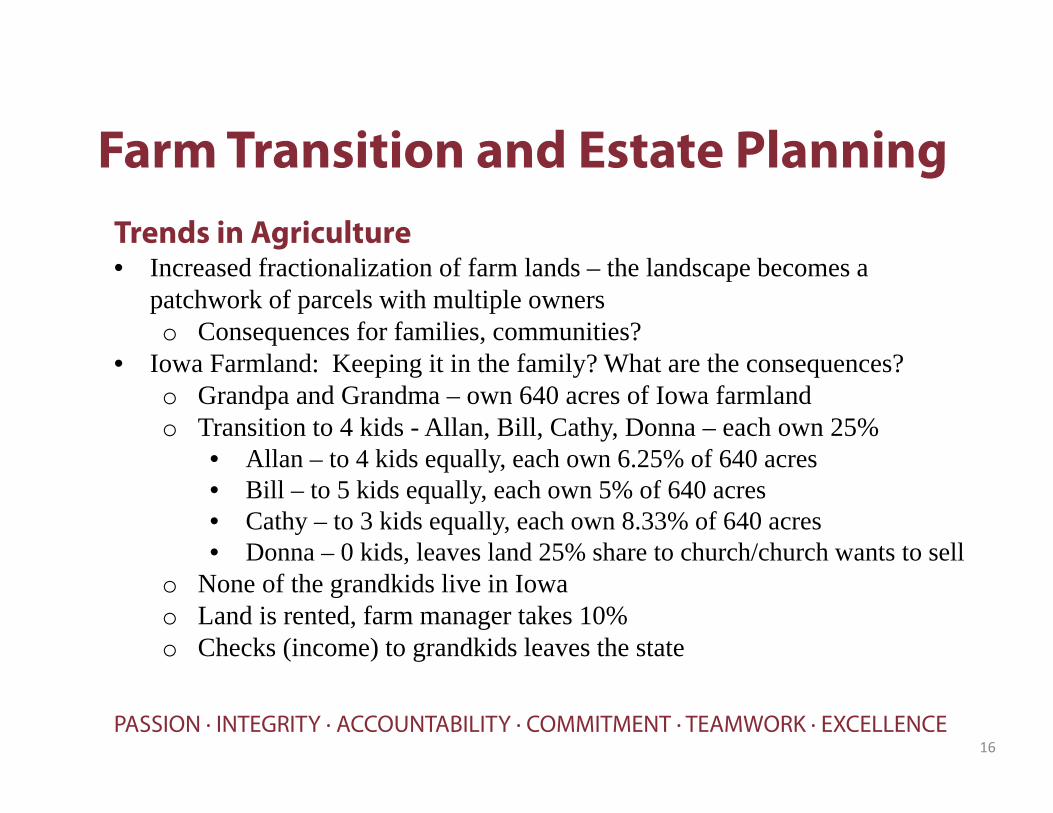

Farm Transition and Estate PlanningTrends in Agriculture• Increased fractionalization of farm lands – the landscape becomes a

patchwork of parcels with multiple ownerso Consequences for families, communities?

• Iowa Farmland: Keeping it in the family? What are the consequences?o Grandpa and Grandma – own 640 acres of Iowa farmland o Transition to 4 kids - Allan, Bill, Cathy, Donna – each own 25%

• Allan – to 4 kids equally, each own 6.25% of 640 acres• Bill – to 5 kids equally, each own 5% of 640 acres• Cathy – to 3 kids equally, each own 8.33% of 640 acres• Donna – 0 kids, leaves land 25% share to church/church wants to sell

o None of the grandkids live in Iowao Land is rented, farm manager takes 10%o Checks (income) to grandkids leaves the state

16

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

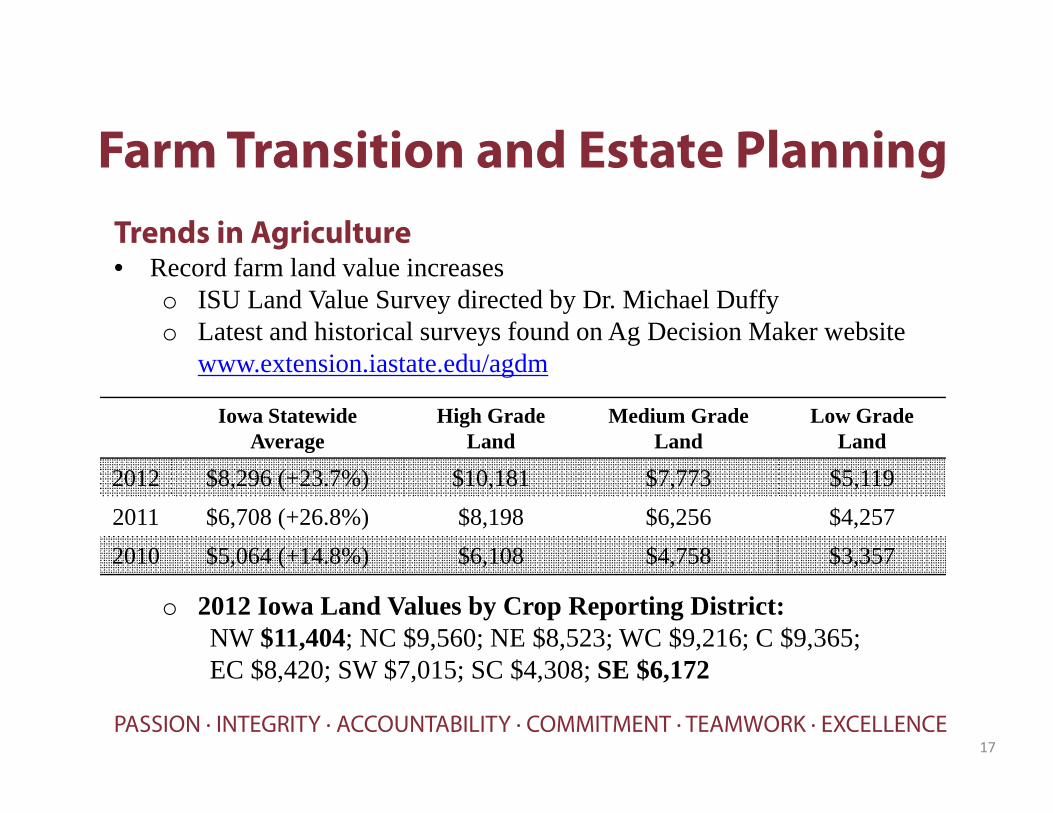

Farm Transition and Estate PlanningTrends in Agriculture• Record farm land value increases

o ISU Land Value Survey directed by Dr. Michael Duffyo Latest and historical surveys found on Ag Decision Maker website

www.extension.iastate.edu/agdm

o 2012 Iowa Land Values by Crop Reporting District:NW $11,404; NC $9,560; NE $8,523; WC $9,216; C $9,365; EC $8,420; SW $7,015; SC $4,308; SE $6,172

17

Iowa Statewide Average

High Grade Land

Medium Grade Land

Low Grade Land

2012 $8,296 (+23.7%) $10,181 $7,773 $5,1192011 $6,708 (+26.8%) $8,198 $6,256 $4,2572010 $5,064 (+14.8%) $6,108 $4,758 $3,357

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

Farm Transition and Estate PlanningTrends in Agriculture• What is driving record farm land value increases and what could

influence land prices in the future?o Highly correlated with record farm incomeo Low interest rate economic environmento Change in investor demand and change in investment alternativeso Government policies – ethanol mandateo Crop input costs – rising costso Performance of the economyo International demand – rising world population/middle classo Weather conditions

18

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

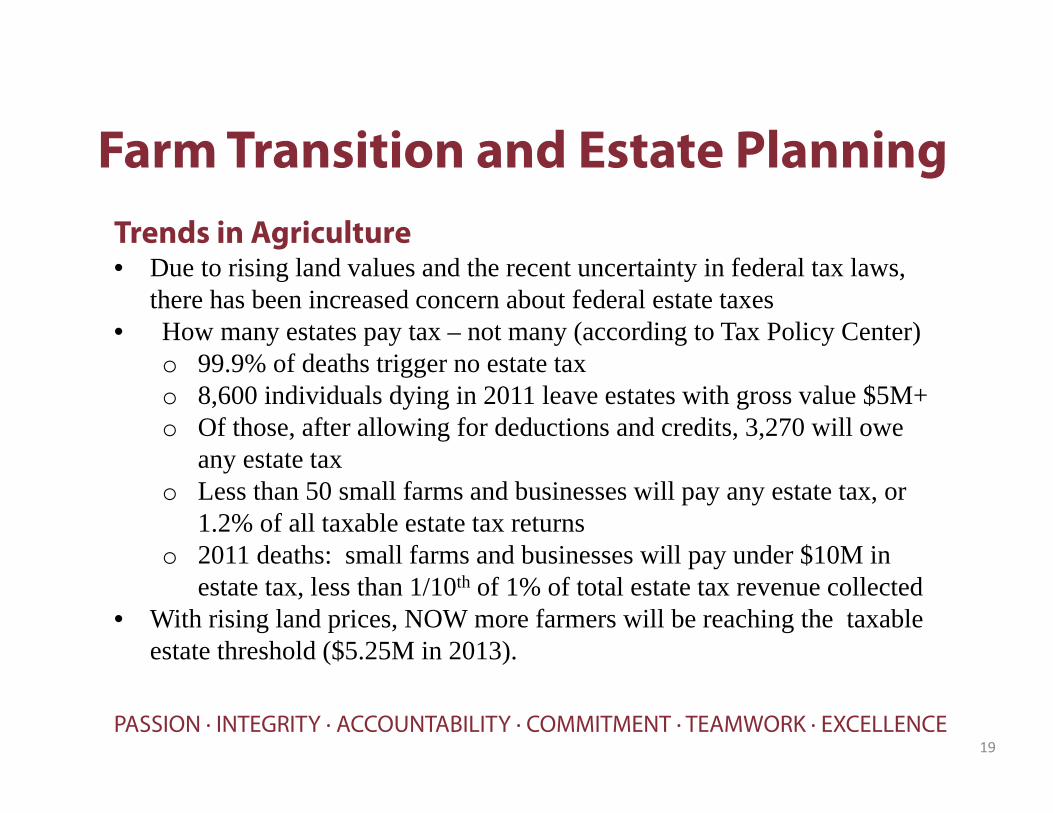

Farm Transition and Estate PlanningTrends in Agriculture• Due to rising land values and the recent uncertainty in federal tax laws,

there has been increased concern about federal estate taxes• How many estates pay tax – not many (according to Tax Policy Center)

o 99.9% of deaths trigger no estate taxo 8,600 individuals dying in 2011 leave estates with gross value $5M+o Of those, after allowing for deductions and credits, 3,270 will owe

any estate taxo Less than 50 small farms and businesses will pay any estate tax, or

1.2% of all taxable estate tax returnso 2011 deaths: small farms and businesses will pay under $10M in

estate tax, less than 1/10th of 1% of total estate tax revenue collected• With rising land prices, NOW more farmers will be reaching the taxable

estate threshold ($5.25M in 2013).

19

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

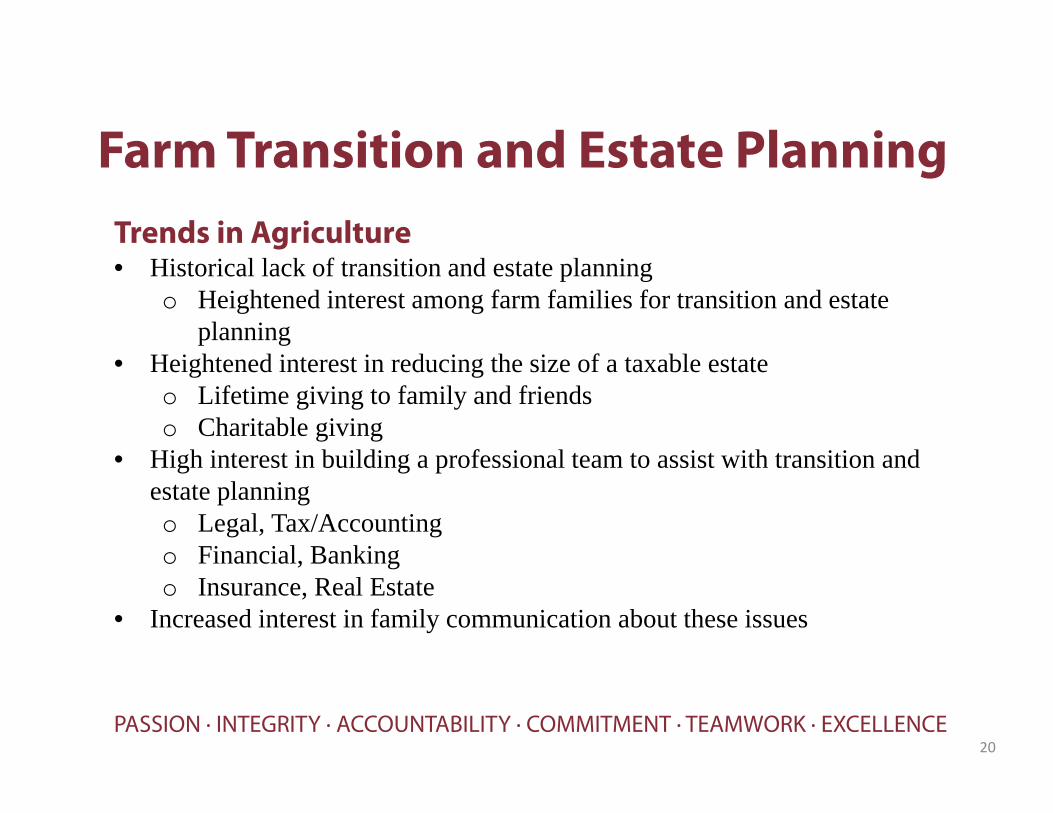

Farm Transition and Estate PlanningTrends in Agriculture• Historical lack of transition and estate planning

o Heightened interest among farm families for transition and estate planning

• Heightened interest in reducing the size of a taxable estateo Lifetime giving to family and friendso Charitable giving

• High interest in building a professional team to assist with transition and estate planningo Legal, Tax/Accounting o Financial, Banking o Insurance, Real Estate

• Increased interest in family communication about these issues

20

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

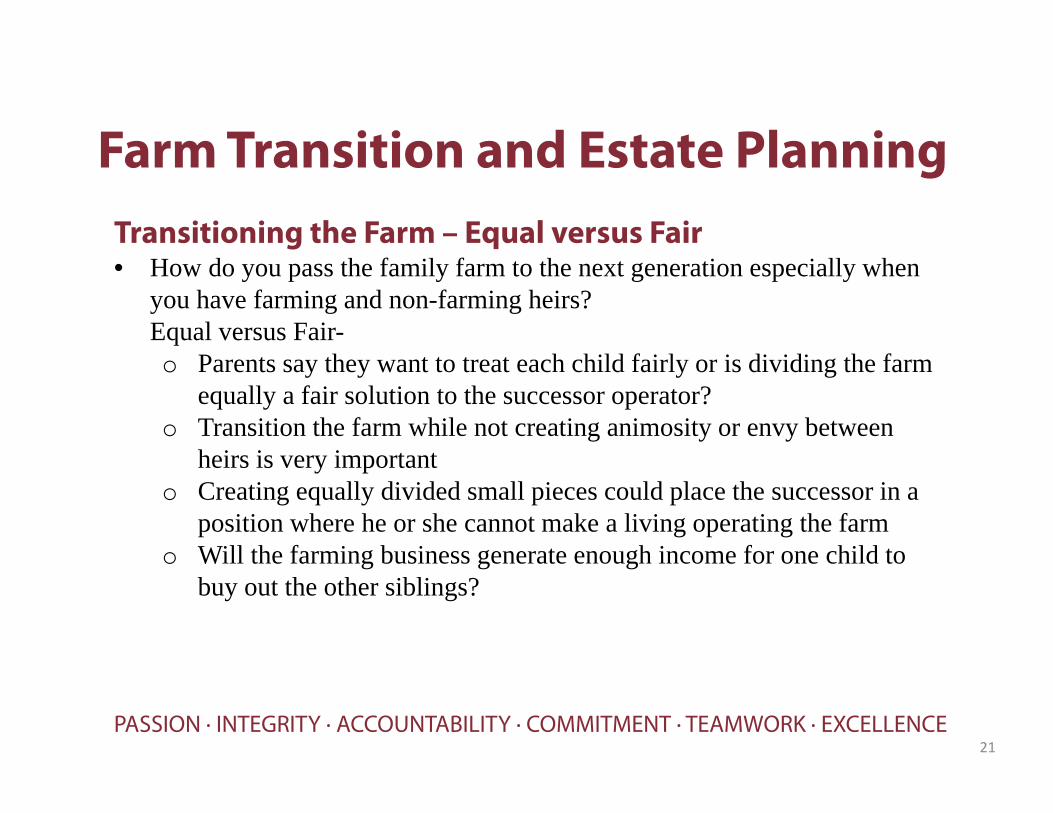

Farm Transition and Estate PlanningTransitioning the Farm – Equal versus Fair• How do you pass the family farm to the next generation especially when

you have farming and non-farming heirs?Equal versus Fair-o Parents say they want to treat each child fairly or is dividing the farm

equally a fair solution to the successor operator? o Transition the farm while not creating animosity or envy between

heirs is very importanto Creating equally divided small pieces could place the successor in a

position where he or she cannot make a living operating the farmo Will the farming business generate enough income for one child to

buy out the other siblings?

21

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

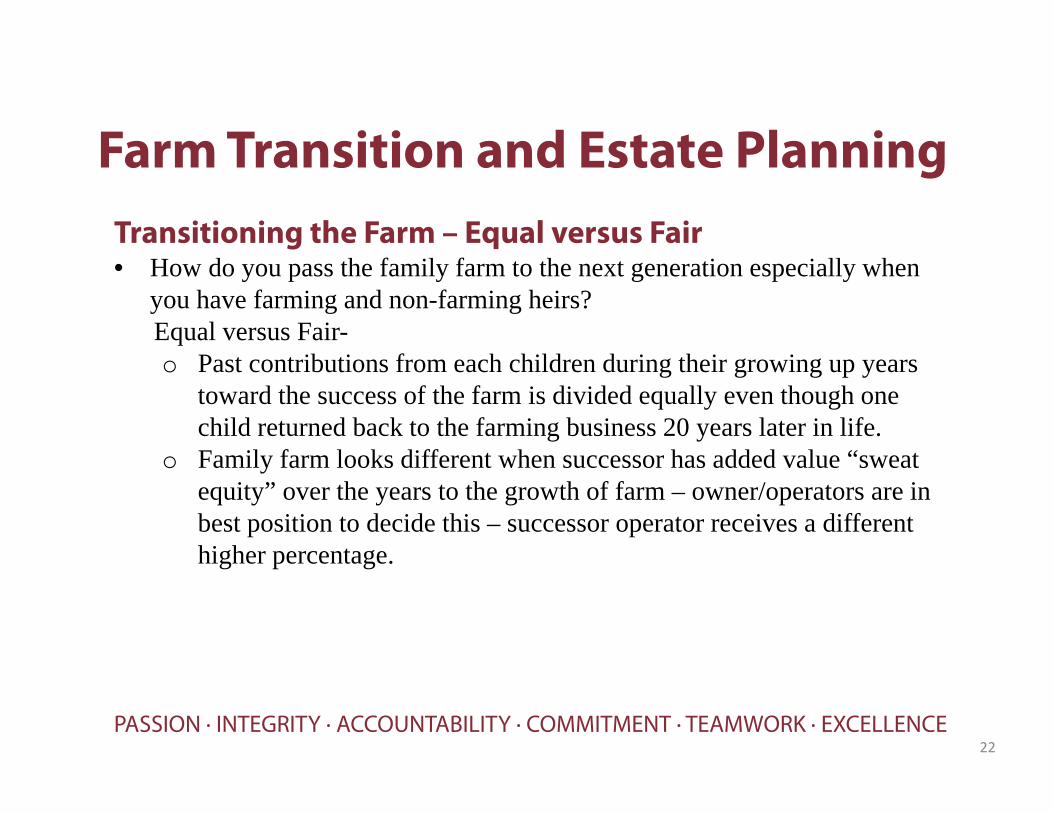

Farm Transition and Estate PlanningTransitioning the Farm – Equal versus Fair• How do you pass the family farm to the next generation especially when

you have farming and non-farming heirs?Equal versus Fair-o Past contributions from each children during their growing up years

toward the success of the farm is divided equally even though one child returned back to the farming business 20 years later in life.

o Family farm looks different when successor has added value “sweat equity” over the years to the growth of farm – owner/operators are in best position to decide this – successor operator receives a different higher percentage.

22

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

Farm Transition and Estate PlanningSpecial Use Valuation• Remember the importance of Special Use Valuation for family farm land

o Farm land – a special use value, or tax break for family farmso Decedent or a member of decedent’s family must have materially

participated in the farm businesso Land must pass to qualified heir, such as spouse or lineal descendent

or ascendanto Must maintain status for at least 10 years following the death, i.e land

stays in the family and is not soldo Possible to reduce the value of the real property portion of qualifying

estates by 40% to 70%, up to maximum $1,070,000 for 2013

23

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

Farm Transition and Estate PlanningGifting of Assets During Your Lifetime• Annual gifting under the exclusion amount ($14,000 in 2013)

o Husband and spouse may jointly gift $28,000 to each child and still remain under the annual gift exclusion amount

• Gifting minority interests - valuation discounts on taxable estates o John Doe has $20M of assets in his name, transfers assets to LLC and

gifts spouse 1% of assets. John Doe can take 20% valuation discount for lack of marketability to arrive at a taxable estate of $16M.

o John Doe has $20M of assets in his name, transfers assets to LLC, and gifts spouse 49% and 2% to two kids, and retains 49% thereby lacking voting control. John Doe can take 35% valuation discount for lack of control and lack of marketability to arrive at a taxable estate of $13M.

24

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

Farm Transition and Estate PlanningGifting of Assets During Your Lifetime• Lifetime gifting

o Any amount of lifetime gift that is made that exceeds the annual exclusion amount ($14,000 in 2013) uses part of the estate/gift tax exemption amount ($5.25 million in 2013).

o Said another way, if you use your estate/gift tax exemption amount during your lifetime, it will not be available for your estate.

o Ideally the best asset to make a lifetime gift is an asset that will have significant appreciation between the date of the gift and the date of death. All of the appreciation is removed from the estate.

25

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

Farm Transition and Estate PlanningGifting of Assets During Your Lifetime• Lifetime gifting

o What is the current market value of the estate? If the estate will not be subject to estate tax, it is better to hold assets until death to get the stepped up cost basis. Inherited assets from an estate have a cost basis to the heirs equal to the market value at date of death.

o What is the cost basis of the land? Cost basis to the donee transfers from the original owner, so if the asset is going to be sold soon after the gift triggering a taxable gain, gifting may not be best thing to do.

o Will the value of the farm land continue to appreciate? Generally you do not want to gift land at high value, you want to gift at low value and remove appreciation from estate.

o Do parents need some income from the land? If so, not best to gift.o Consideration of family farm limited liability company? This can

accomplish family farm management, transfer of units through LLC annual exclusion gifts, and keep some income with parents.

26

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

Farm Transition and Estate PlanningGifting of Assets During Your Lifetime• Grantor trust – living trust or revocable trust

o Allows the grantor, the individual who establishes the trust, to have control over the trust assets and receive income created from the trust

o Freezes valuation of assets at time granted to trust yet grantor (i.e. parents) retain control of the assets during the life of the trust

o Assets held within the trust will pass directly to the beneficiaries named in the trust agreement and not be subject to probate court.

o Because there is no wait time in probate, the trust’s beneficiaries can have immediate benefit from assets in the trust

o Cost of trust administration is less than other types of trusts that have to go through probate

o Assets funded into the trust will still be considered to be your own personal assets for creditor and estate tax purposes

27

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

Farm Transition and Estate PlanningGifting of Assets During Your Lifetime• Irrevocable trusts - benefits

o Estate tax reduction - this type of trust is used to remove the value of property from a person’s estate so that the property cannot be taxed when the person dies. In other words, the person who transfers assets into an irrevocable trust is giving over these assets to the trustee and beneficiaries so that the person no longer owns the assets.

o Provide asset protection – the trustmaker is giving up complete control over and access to the trust assets and therefore, the trust assets cannot be reached by creditors of the trustmaker.

o Charitable estate planning – if trustmaker makes the initial transfer of assets into a charitable trust while still alive, then the trustmaker will receive a charitable income tax deduction in the year the transfer is made.

28

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

Business Succession and TransitionBusiness Entity Selection• Sole Proprietorship • Partnership • Corporation• S Corporation• Limited Liability Company (LLC)

29

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

Business Succession and TransitionBusiness Entity Selection• Sole Proprietorship – Schedule C or Schedule F

o Advantages:• Easy to form and simple to operate• Easy to sell assets• Fewer administrative burdens• All taxation to owner

o Disadvantages:• Limited source of capital.• No limited liability for owner.• No continuity past proprietor• All net earnings subject to self-employment tax

30

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

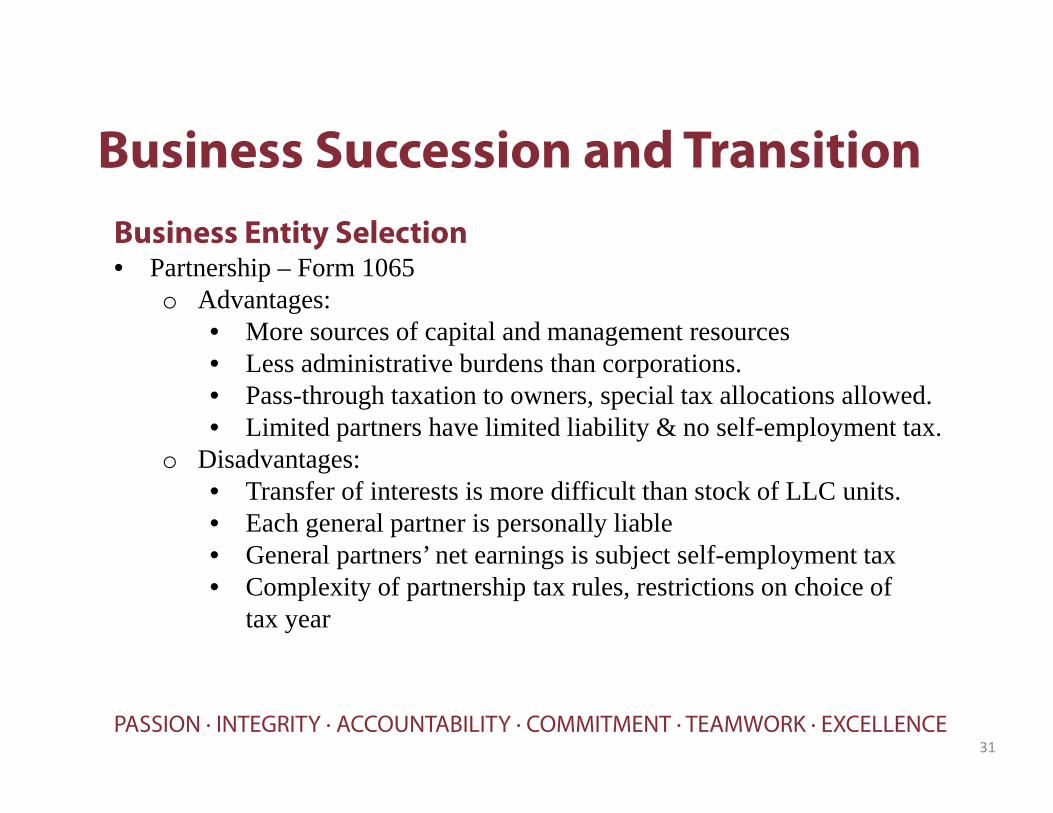

Business Succession and TransitionBusiness Entity Selection• Partnership – Form 1065

o Advantages:• More sources of capital and management resources• Less administrative burdens than corporations.• Pass-through taxation to owners, special tax allocations allowed.• Limited partners have limited liability & no self-employment tax.

o Disadvantages:• Transfer of interests is more difficult than stock of LLC units.• Each general partner is personally liable• General partners’ net earnings is subject self-employment tax• Complexity of partnership tax rules, restrictions on choice of

tax year

31

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

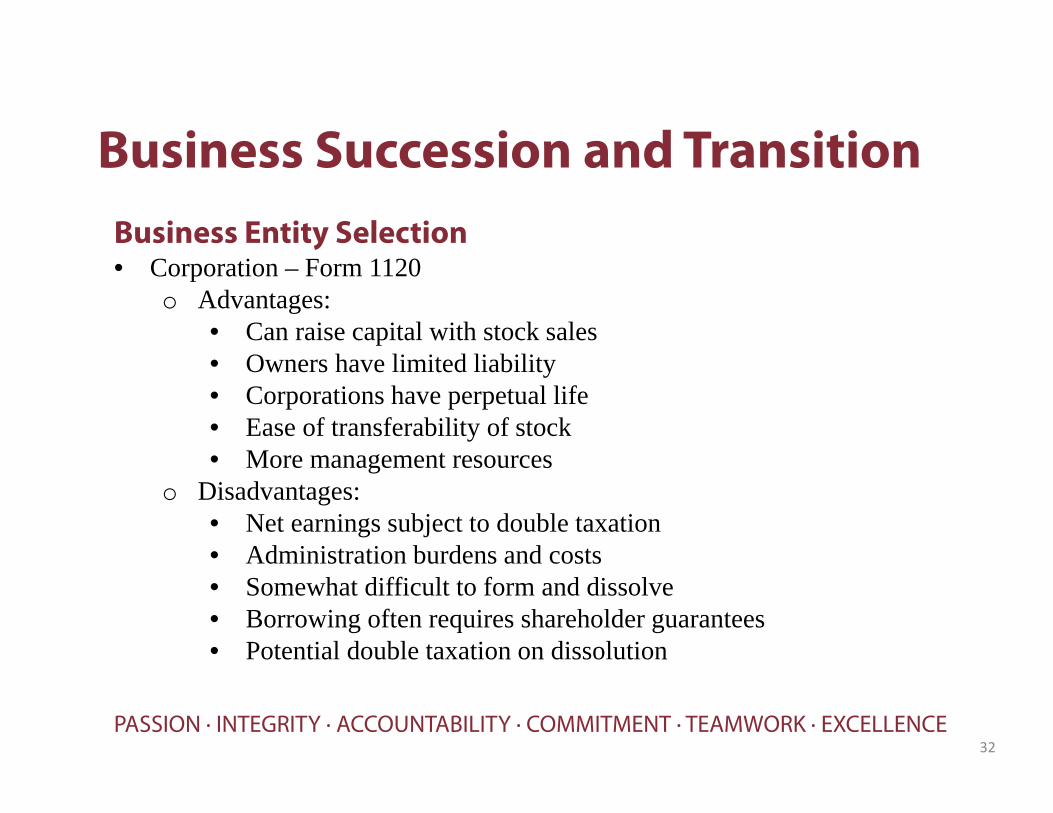

Business Succession and TransitionBusiness Entity Selection• Corporation – Form 1120

o Advantages:• Can raise capital with stock sales• Owners have limited liability• Corporations have perpetual life• Ease of transferability of stock• More management resources

o Disadvantages:• Net earnings subject to double taxation• Administration burdens and costs• Somewhat difficult to form and dissolve• Borrowing often requires shareholder guarantees• Potential double taxation on dissolution

32

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

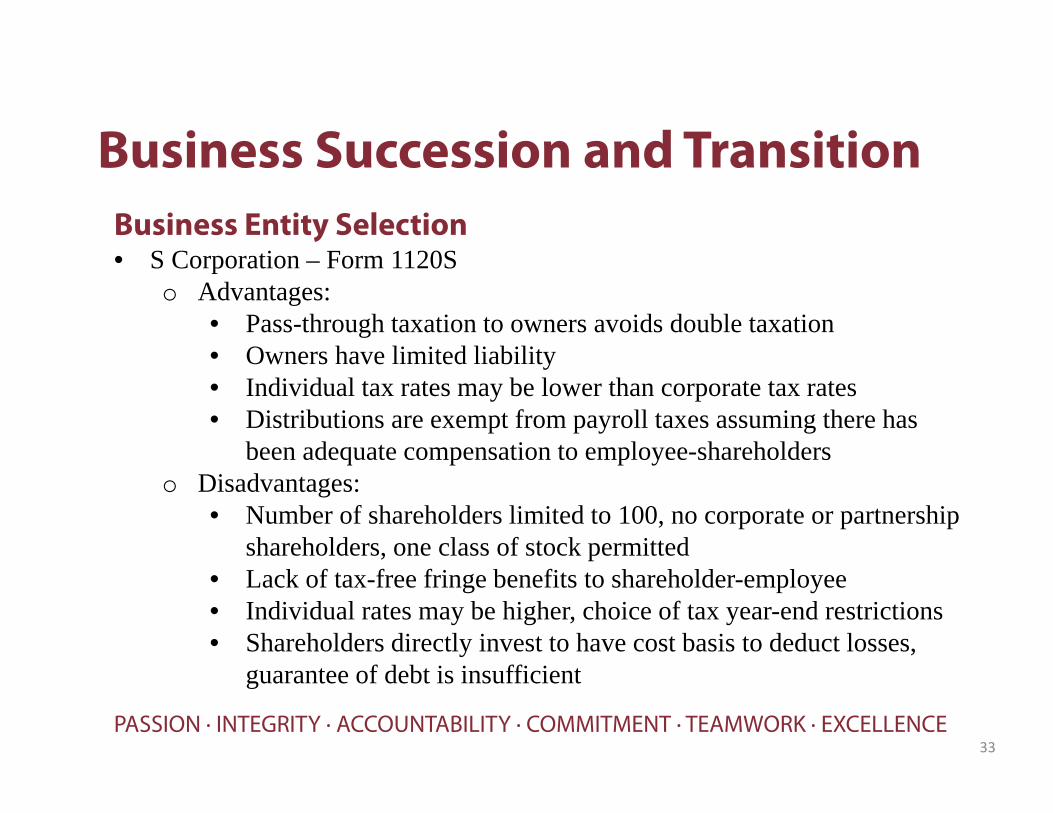

Business Succession and TransitionBusiness Entity Selection• S Corporation – Form 1120S

o Advantages:• Pass-through taxation to owners avoids double taxation• Owners have limited liability• Individual tax rates may be lower than corporate tax rates• Distributions are exempt from payroll taxes assuming there has

been adequate compensation to employee-shareholderso Disadvantages:

• Number of shareholders limited to 100, no corporate or partnership shareholders, one class of stock permitted

• Lack of tax-free fringe benefits to shareholder-employee• Individual rates may be higher, choice of tax year-end restrictions• Shareholders directly invest to have cost basis to deduct losses,

guarantee of debt is insufficient

33

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

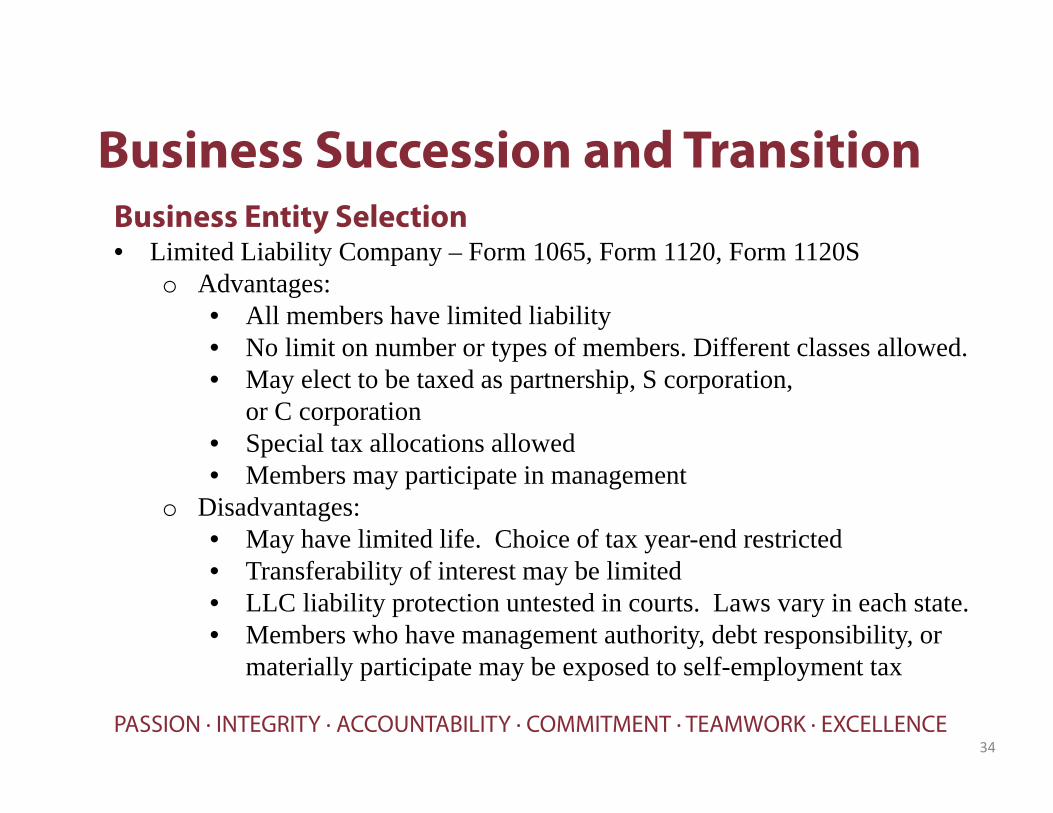

Business Succession and TransitionBusiness Entity Selection• Limited Liability Company – Form 1065, Form 1120, Form 1120S

o Advantages:• All members have limited liability• No limit on number or types of members. Different classes allowed.• May elect to be taxed as partnership, S corporation,

or C corporation• Special tax allocations allowed• Members may participate in management

o Disadvantages:• May have limited life. Choice of tax year-end restricted• Transferability of interest may be limited• LLC liability protection untested in courts. Laws vary in each state.• Members who have management authority, debt responsibility, or

materially participate may be exposed to self-employment tax

34

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

Business Succession and TransitionInternal and External Transition Options• Every individual’s goals are different as one approaches retirement• Sit down with individual to determine long-term ownership and

employment goals – two separate issues• If transfer company, what does the individual plan to do with their time• Develop family members to manage business

35

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

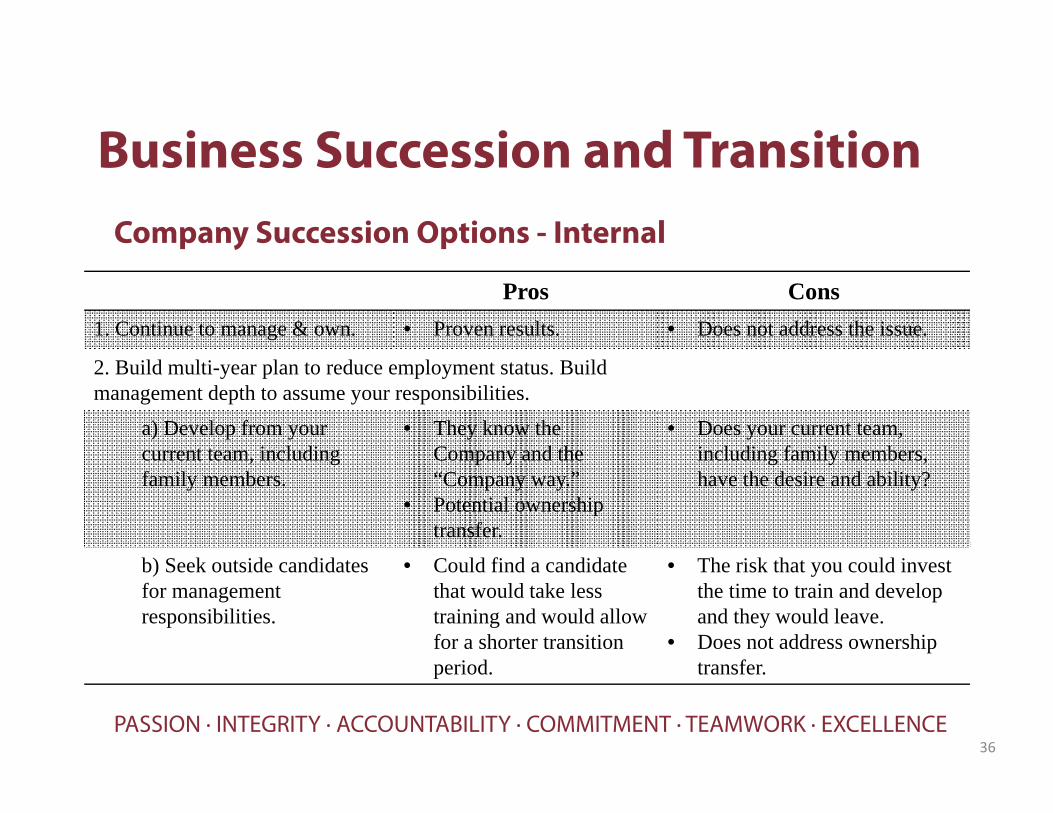

Business Succession and TransitionCompany Succession Options - Internal

36

Pros Cons1. Continue to manage & own. • Proven results. • Does not address the issue.

2. Build multi-year plan to reduce employment status. Build management depth to assume your responsibilities.

a) Develop from your current team, including family members.

• They know the Company and the “Company way.”

• Potential ownership transfer.

• Does your current team, including family members, have the desire and ability?

b) Seek outside candidates for management responsibilities.

• Could find a candidate that would take less training and would allow for a shorter transition period.

• The risk that you could invest the time to train and develop and they would leave.

• Does not address ownership transfer.

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

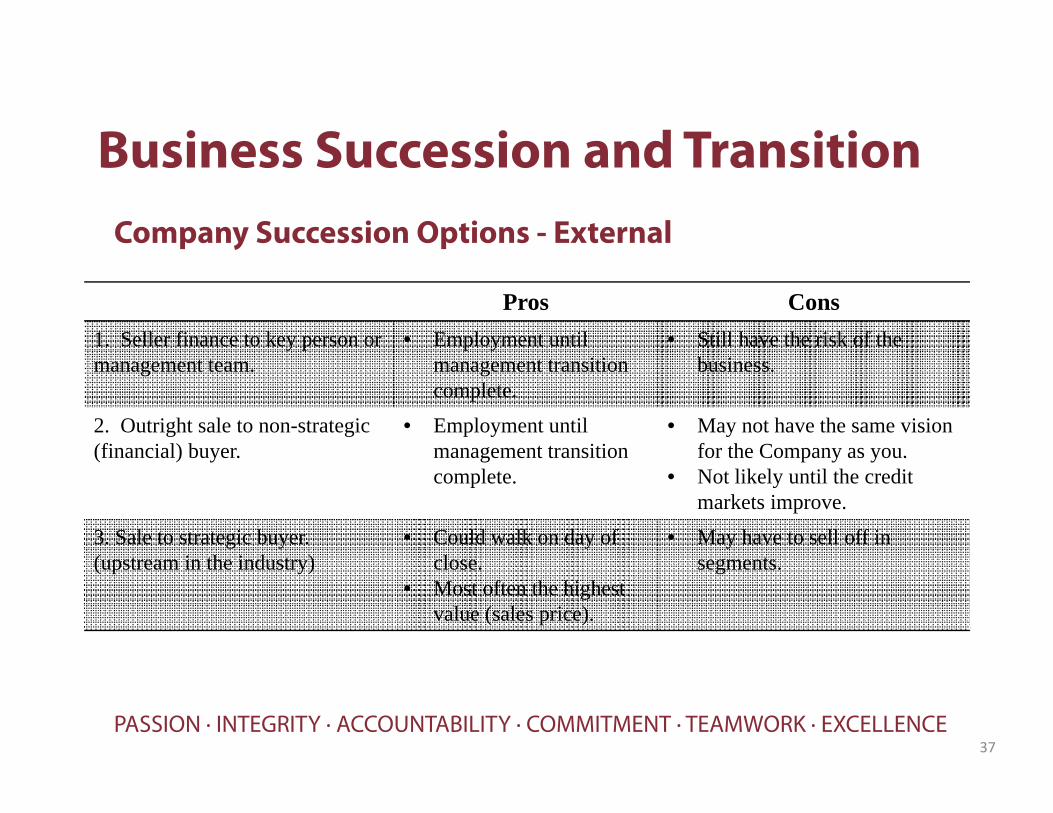

Business Succession and TransitionCompany Succession Options - External

37

Pros Cons1. Seller finance to key person or management team.

• Employment until management transition complete.

• Still have the risk of the business.

2. Outright sale to non-strategic (financial) buyer.

• Employment until management transition complete.

• May not have the same vision for the Company as you.

• Not likely until the credit markets improve.

3. Sale to strategic buyer. (upstream in the industry)

• Could walk on day of close.

• Most often the highest value (sales price).

• May have to sell off in segments.

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

Business Succession and TransitionCorporate Stock vs Asset Sale• A prospective buyer offers to purchase a small corporation’s assets, while

the owners of a small corporation want to sell their stock. The buyer and seller cannot both structure the sale entirely to their advantage.

38

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

Business Succession and TransitionCorporate Stock vs Asset Sale• Seller’s perspective-

o Sellers pay less tax by selling stock rather than assets. Lower capital gain tax rates apply to the entire gain if stock is sold

o Sellers of assets realize gains that are subject to depreciation recapture which may be taxed at higher ordinary tax rates.

o Sellers of assets must value each asset and allocate the sales price among the assets sold and generally incur higher professional fees for appraisals, income tax preparation, and legal services

o Sellers may be able to negotiate a higher sales price if willing to sell assets rather than stock

39

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

Business Succession and TransitionCorporate Stock vs Asset Sale• Buyer’s perspective-

o Buyers of assets can depreciate individual assets used in a businesso Buyers of stock cannot depreciate its cost, seller’s tax basis remainso Buyers of stock must assume successor liability for debts and actions

of the predecessor without adequate information to quantify the risk

40

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

Business Succession and TransitionCorporate Stock vs Asset Sale• Goodwill – excess of price paid over the value of the “hard assets”

o Sellers of assets prefer more value be placed on goodwill and less on equipment and inventory to reduce ordinary income and increase capital gains whereby capital gains are taxed at lower rate rates

o Buyers of assets prefer less value be placed on goodwill and more on equipment and inventory to increase rapidly realized depreciation and cost of good sold deductions

o Form 8594 filed by buyer and seller on agreed-upon asset allocation

41

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

Business Succession and TransitionCorporate Stock vs Asset Sale• S Corporations - IRC Section 338(h) (10) election

o Allows a corporation acquiring 80% or more of the stock of the target corporation to make a tax election to treat a stock purchase as a purchase of the target corporation’s assets

o S Corporation is deemed to have sold its assets at market valueo The gain on the sale of the assets would pass-through on the final S

Corporation tax return and K-1s and be reported by the shareholder on their personal tax return, thereby increasing their cost basis in the S corporation stock

o The shareholder then realizes a capital gain or loss on the final liquidating distribution based on the difference between the amount of the liquidating distribution and the increased cost basis in the S corporation stock

o Buyer is able to depreciate the individual assets used in a business

42

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

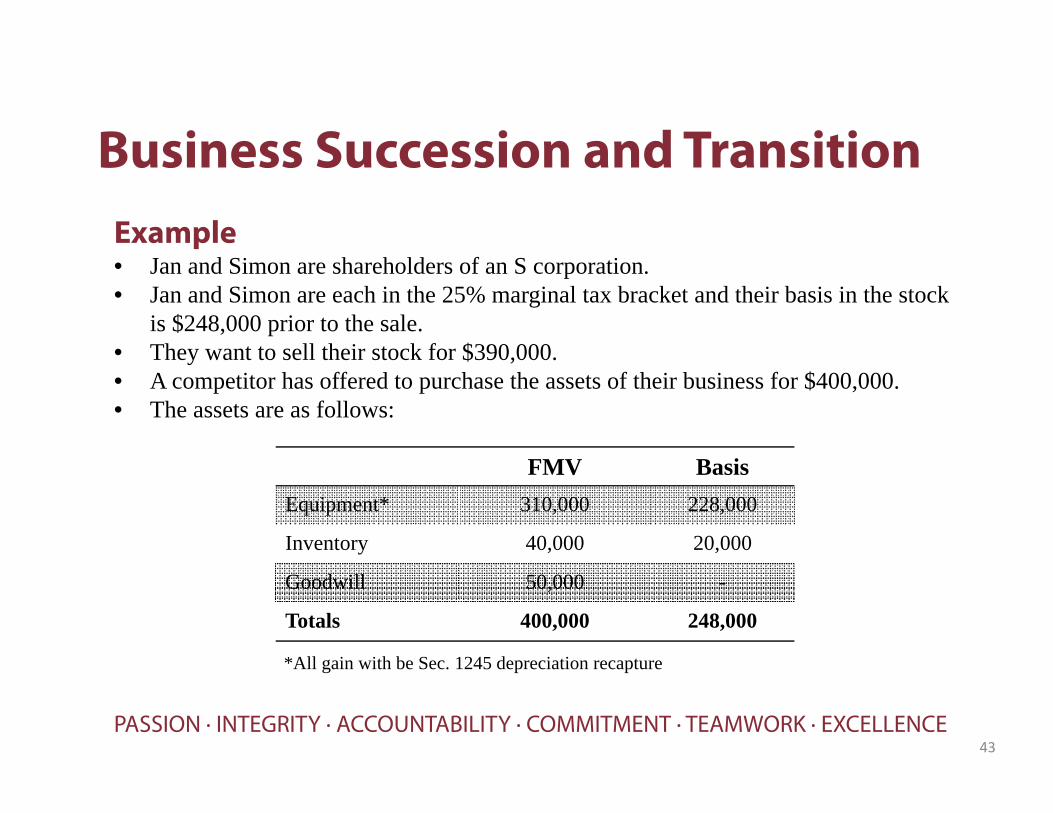

Business Succession and TransitionExample• Jan and Simon are shareholders of an S corporation. • Jan and Simon are each in the 25% marginal tax bracket and their basis in the stock

is $248,000 prior to the sale.• They want to sell their stock for $390,000.• A competitor has offered to purchase the assets of their business for $400,000.• The assets are as follows:

43

FMV BasisEquipment* 310,000 228,000

Inventory 40,000 20,000

Goodwill 50,000 -

Totals 400,000 248,000

*All gain with be Sec. 1245 depreciation recapture

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

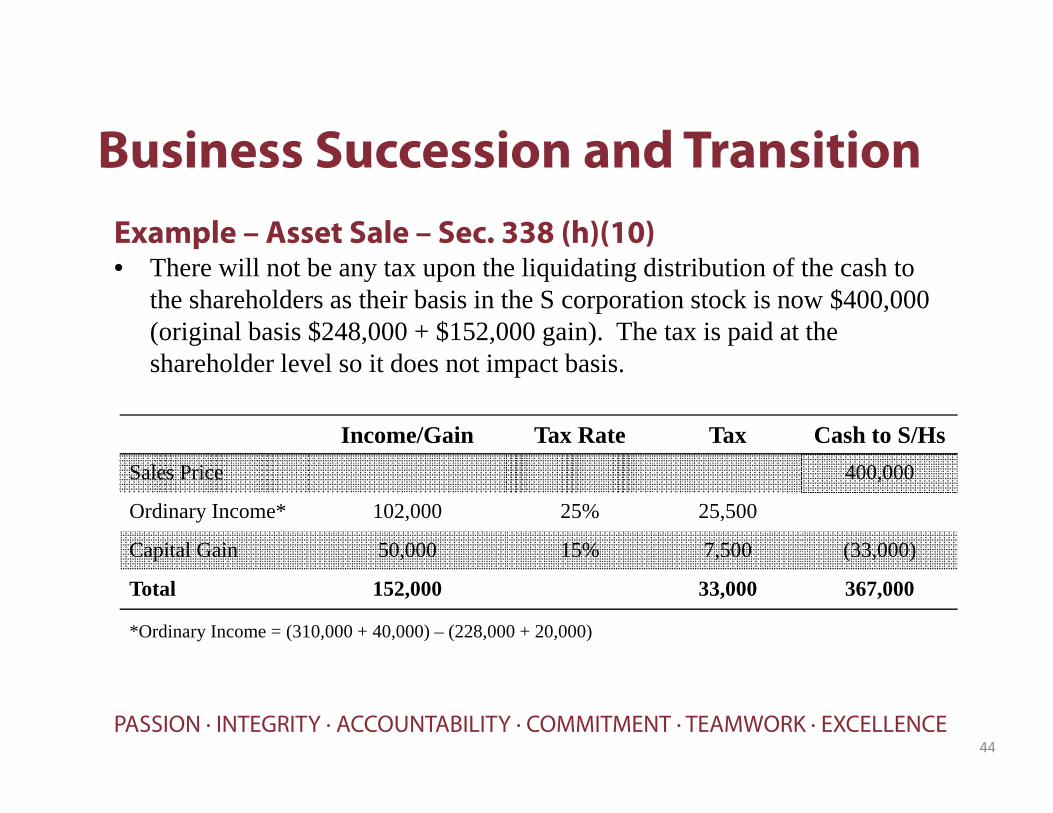

Business Succession and TransitionExample – Asset Sale – Sec. 338 (h)(10)• There will not be any tax upon the liquidating distribution of the cash to

the shareholders as their basis in the S corporation stock is now $400,000 (original basis $248,000 + $152,000 gain). The tax is paid at the shareholder level so it does not impact basis.

44

Income/Gain Tax Rate Tax Cash to S/HsSales Price 400,000

Ordinary Income* 102,000 25% 25,500

Capital Gain 50,000 15% 7,500 (33,000)

Total 152,000 33,000 367,000

*Ordinary Income = (310,000 + 40,000) – (228,000 + 20,000)

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

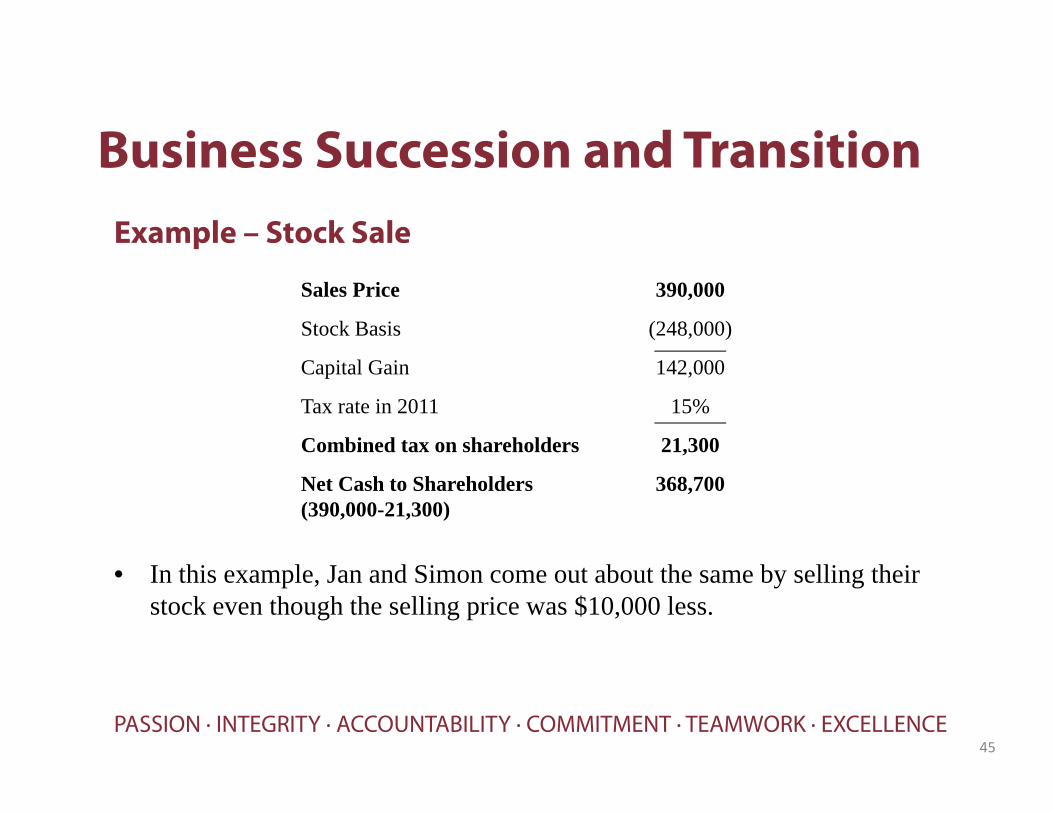

Business Succession and TransitionExample – Stock Sale

• In this example, Jan and Simon come out about the same by selling their stock even though the selling price was $10,000 less.

45

Sales Price 390,000

Stock Basis (248,000)

Capital Gain 142,000

Tax rate in 2011 15%

Combined tax on shareholders 21,300

Net Cash to Shareholders (390,000-21,300)

368,700

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

Business Succession and TransitionEmployee Stock Ownership Plans (ESOPs)• ESOP is an employee qualified retirement plan designed to invest in the

employer’s stock. ESOP may also borrow money and enter into transactions with related parties to acquire the employer’s stock.

• ESOPs serve the following corporate finance objectives:o Borrowing at reduced after-tax cost – greater cash flowo Refinancing existing bank debt, repaying new debt with pre-tax

dollars (i.e. principal debt payment is a tax deduction).o Solving ownership succession issueso Eliminating federal income tax at corporate and shareholder levelso Estate planning and charitable givingo Facilitating an acquisition or divestiture/spin-off of a division to a

company owned by the employeeso Providing employees with incentives for productivity

46

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

Business Succession and TransitionEmployee Stock Ownership Plans (ESOPs)• ESOPs federal and state tax incentives

o ESOP share of corporation’s net earnings are tax deferred since the plan is a qualified retirement plan

o Recently enacted Iowa tax incentive – 50% of the gain from the sale of stock to an ESOP is excluded from Iowa taxation

47

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

Business Succession and TransitionEmployee Stock Ownership Plans (ESOPs)• ESOPs have several limitations:

o Plan does not work well with a smaller employment baseo Plan does not work well if company is highly leveragedo Plan is costly to operate – appraisals, stock buy-backs. o Company is required to be appraised annually by qualified appraisero Costs to buy back stock when people leave and are due a distributiono Tax rules are complex. Tax rules different for S vs C Corporations

48

PASSION · INTEGRITY · ACCOUNTABILITY · COMMITMENT · TEAMWORK · EXCELLENCE

Business Succession and TransitionCorporate Reorganizations• In general, IRC Section 368 tax-free reorganization treatment means

neither the corporations involved nor their shareholders recognize taxable income or loss on the exchanges of stock and assets occurring during the reorganization plano Statutory merger or consolidation (Type A)o Acquisition by one corporation of the property of another corporation

by means of exchanging its stock for stock (Type B)o Acquisition by one corporation of the property of another corporation

by means of exchange its stock for property (Type C)o Transfer by corporation of its assets to a corporation if the transferor

controls the corporation to which assets are transferred (Type D)o Recapitalization (Type E)

49

GET MORE THAN BEAN COUNTERS.

Get MORE for Your Business At Every Stage.www.berganpaulsen.com

Mike ReganAssurance Partner, [email protected]