Embed Size (px)

Citation preview

Ricardo NegriSecretary of Agriculture, Livestock and

Fisheries

The Argentine Republic

MICA’s 55th Annual Meeting and Conference

San Francisco, California September 28th

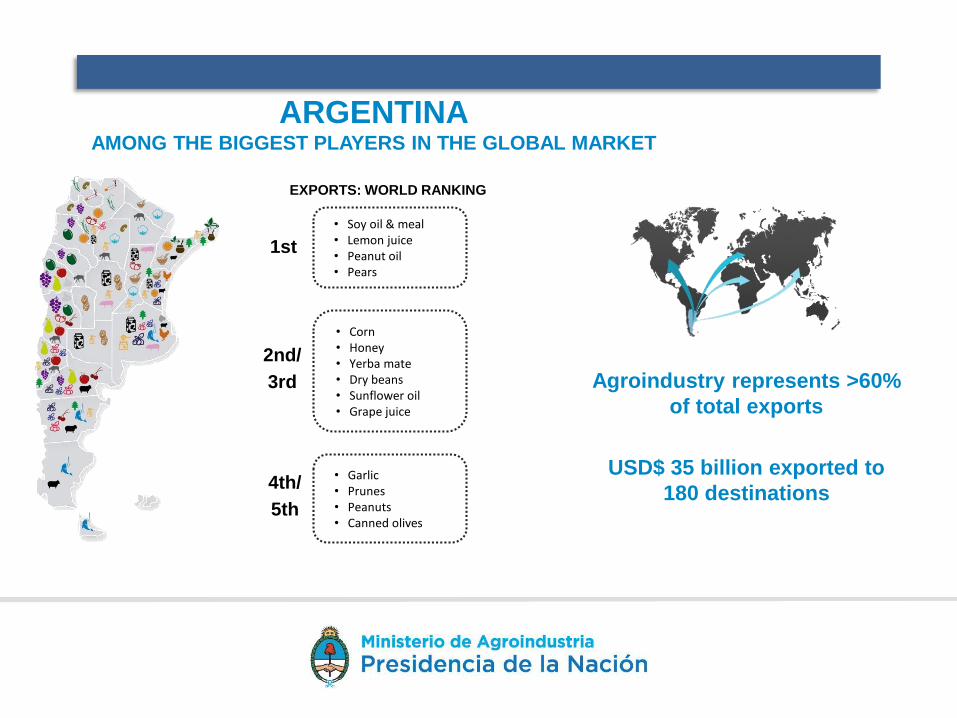

ARGENTINAAMONG THE BIGGEST PLAYERS IN THE GLOBAL MARKET

• Soy oil & meal• Lemon juice• Peanut oil• Pears

• Corn• Honey• Yerba mate• Dry beans• Sunflower oil• Grape juice

• Garlic• Prunes• Peanuts• Canned olives

EXPORTS: WORLD RANKING

1st

4th/

5th

2nd/

3rd Agroindustry represents >60%

of total exports

USD$ 35 billion exported to

180 destinations

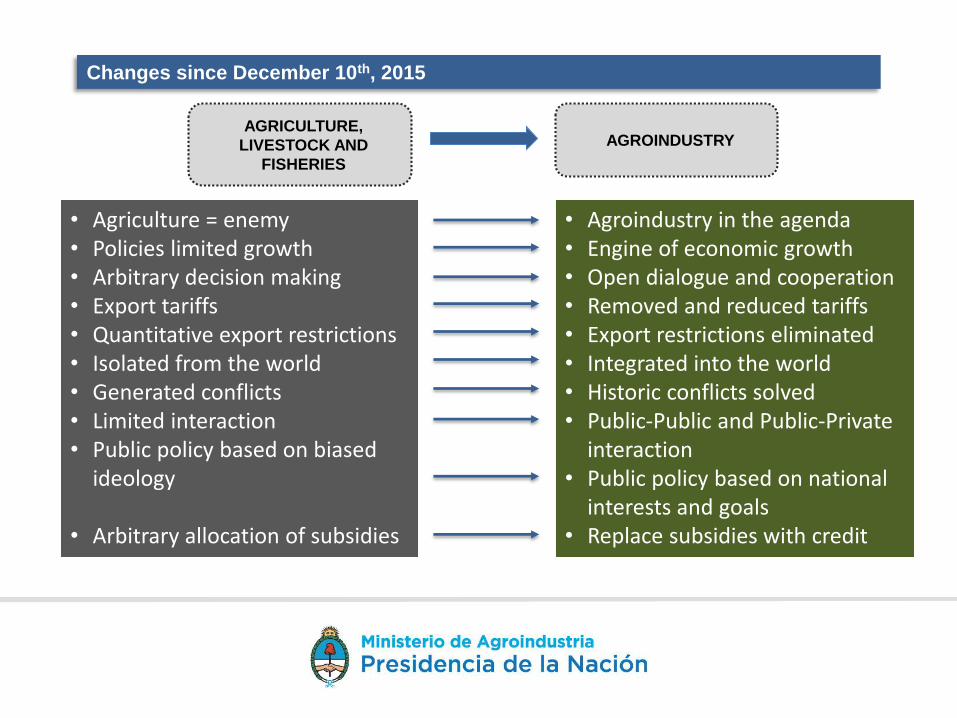

Changes since December 10th, 2015

• Agriculture = enemy• Policies limited growth• Arbitrary decision making• Export tariffs • Quantitative export restrictions• Isolated from the world• Generated conflicts• Limited interaction• Public policy based on biased

ideology

• Arbitrary allocation of subsidies

• Agroindustry in the agenda• Engine of economic growth• Open dialogue and cooperation • Removed and reduced tariffs• Export restrictions eliminated• Integrated into the world• Historic conflicts solved• Public-Public and Public-Private

interaction• Public policy based on national

interests and goals• Replace subsidies with credit

AGRICULTURE,

LIVESTOCK AND

FISHERIES

AGROINDUSTRY

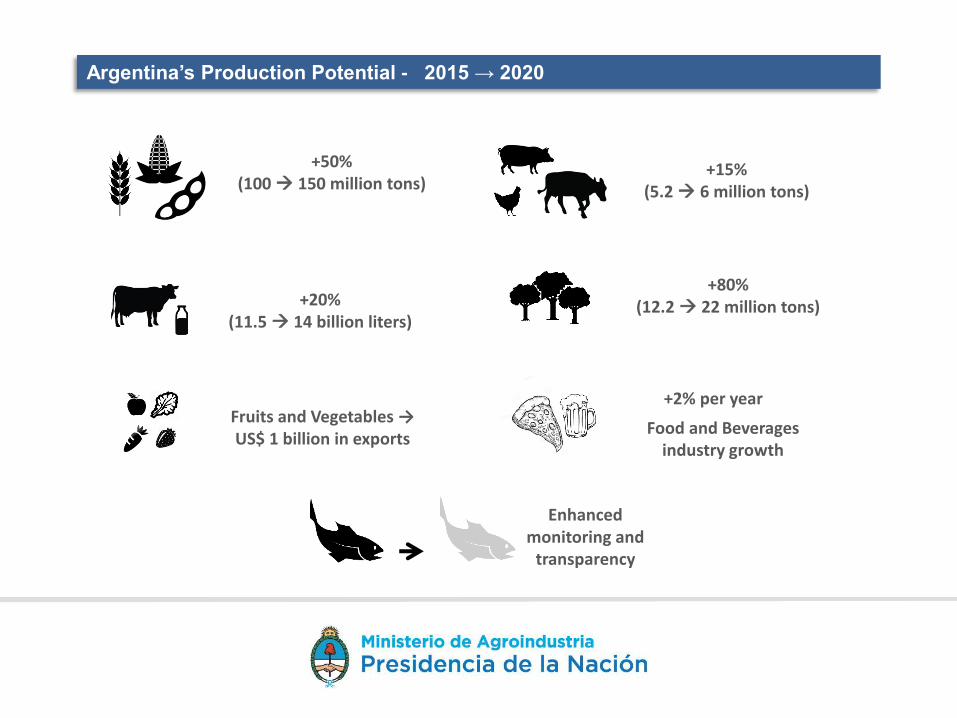

Argentina’s Production Potential - 2015 → 2020

+50%(100 150 million tons)

+20% (11.5 14 billion liters)

+15% (5.2 6 million tons)

Fruits and Vegetables → US$ 1 billion in exports

Enhanced monitoring and

transparency

Food and Beverages industry growth

+80% (12.2 22 million tons)

+2% per year

Argentina

Beef Production

Increase competitiveness and transparency in the

domestic market

Simplify rules and tax regulations

Enhance transportation

system

Agroindustrial Policy

Agroindustrial Policy

Our goals

Increase market

access

Simplify export

requirements

Promote bilateral

negotiations

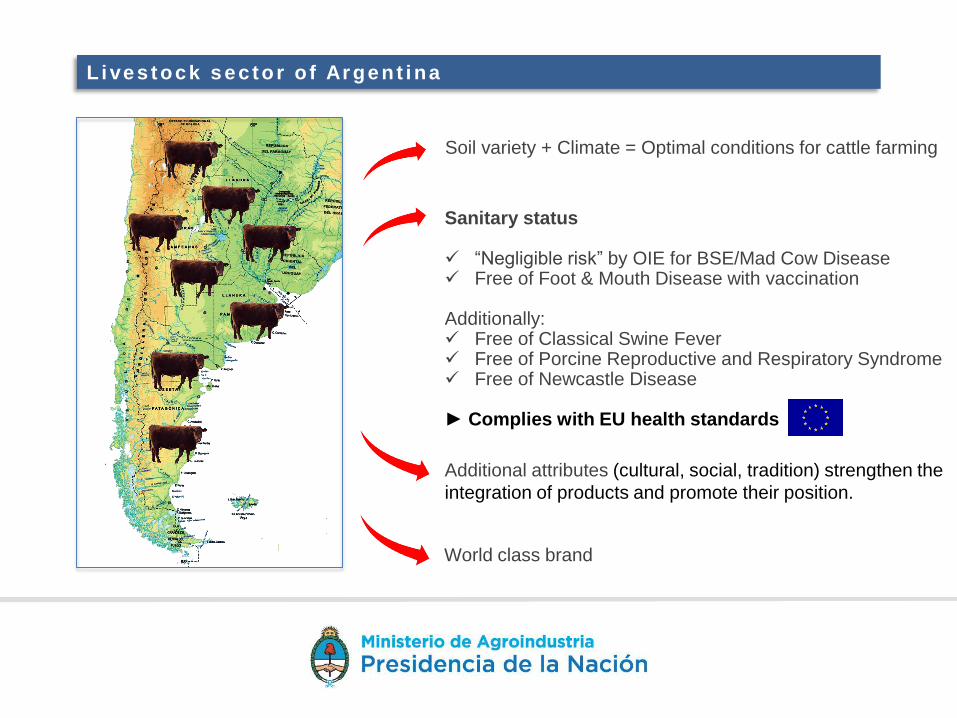

Lives tock sec tor o f Argent ina

Additional attributes (cultural, social, tradition) strengthen the

integration of products and promote their position.

Soil variety + Climate = Optimal conditions for cattle farming

Sanitary status

“Negligible risk” by OIE for BSE/Mad Cow Disease Free of Foot & Mouth Disease with vaccination

Additionally: Free of Classical Swine Fever Free of Porcine Reproductive and Respiratory Syndrome Free of Newcastle Disease

► Complies with EU health standards

World class brand

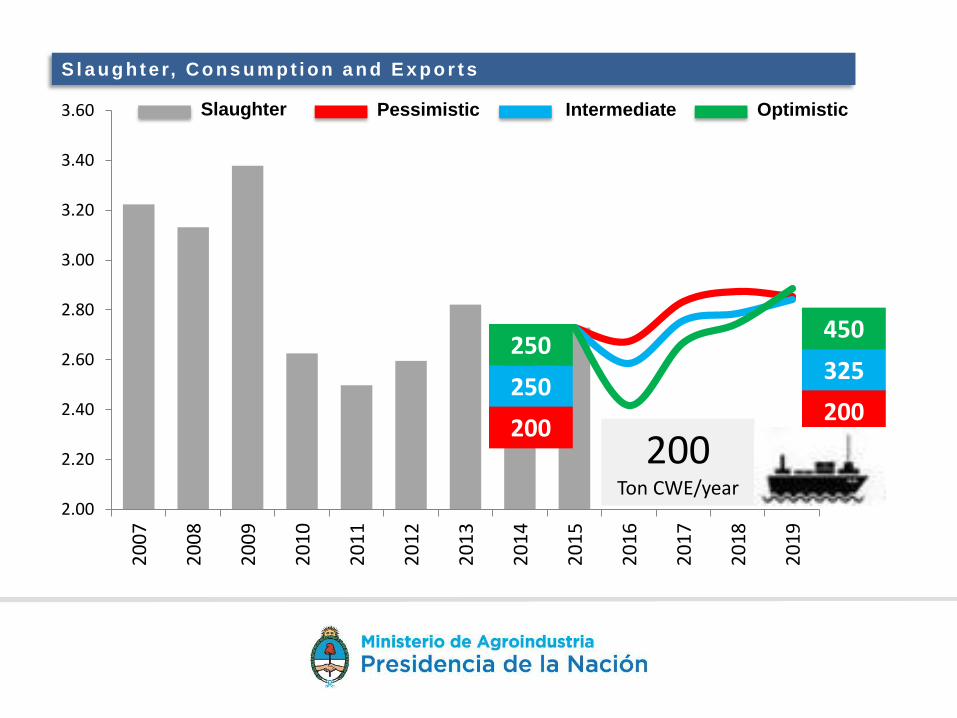

S l a u g ht e r, C o n s u m p t i o n a n d E x p o r t s

2.00

2.20

2.40

2.60

2.80

3.00

3.20

3.40

3.60

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

Slaughter

250

250

200200

Ton CWE/year

325

450

200

Pessimistic Intermediate Optimistic

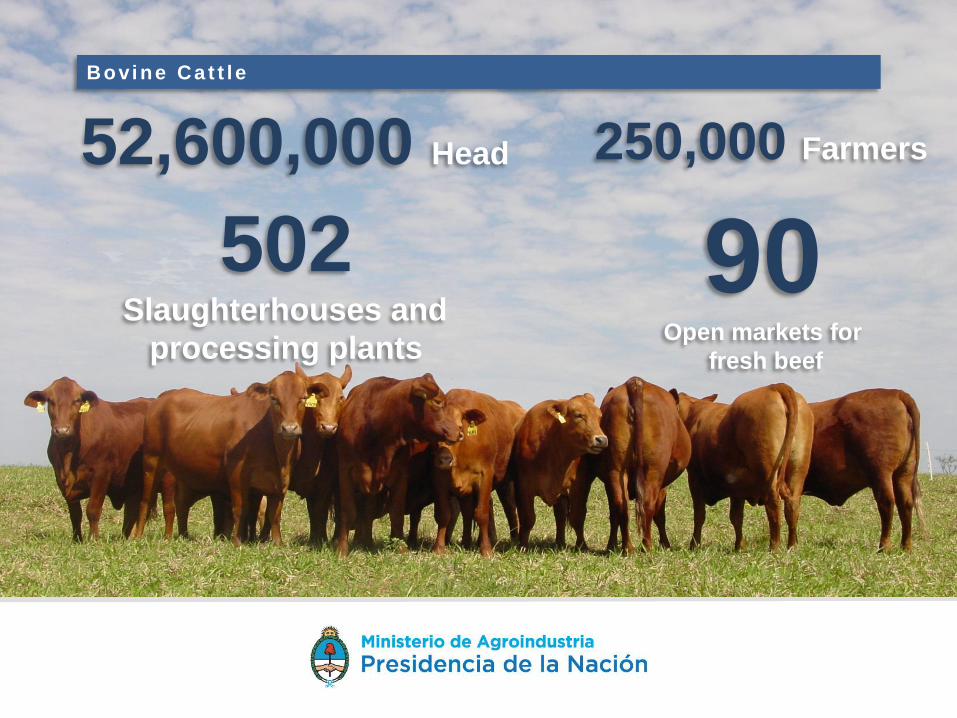

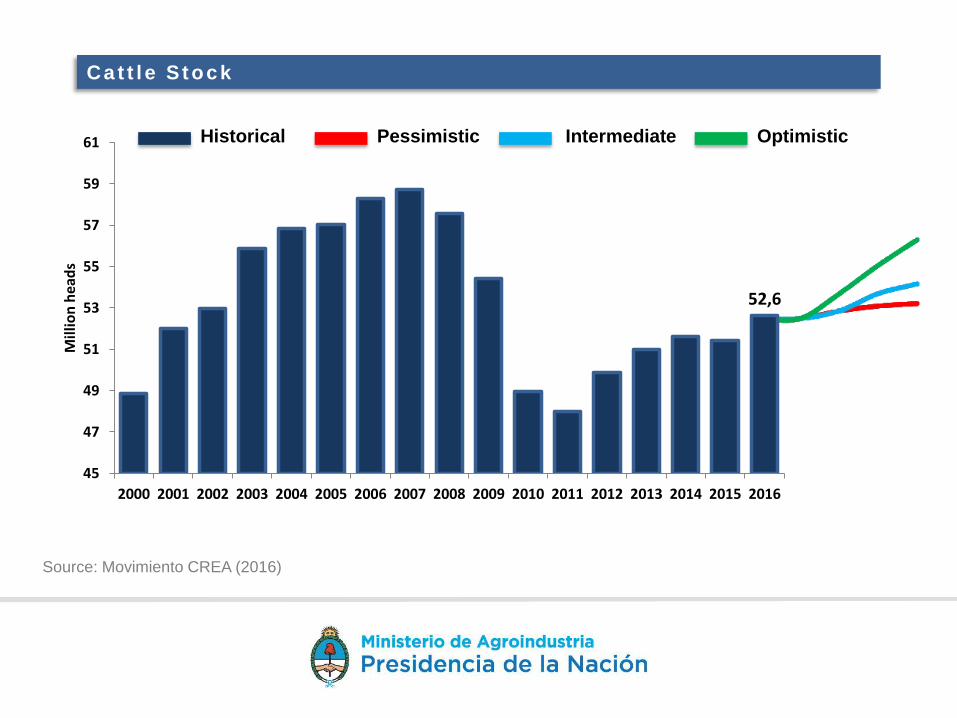

52,600,000 Head

Bovine Ca t t l e

250,000 Farmers

502Slaughterhouses and

processing plants

90Open markets for

fresh beef

Cat t l e S tock

52,6

45

47

49

51

53

55

57

59

61

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Mill

ion

hea

ds

Pessimistic Intermediate OptimisticHistorical

Source: Movimiento CREA (2016)

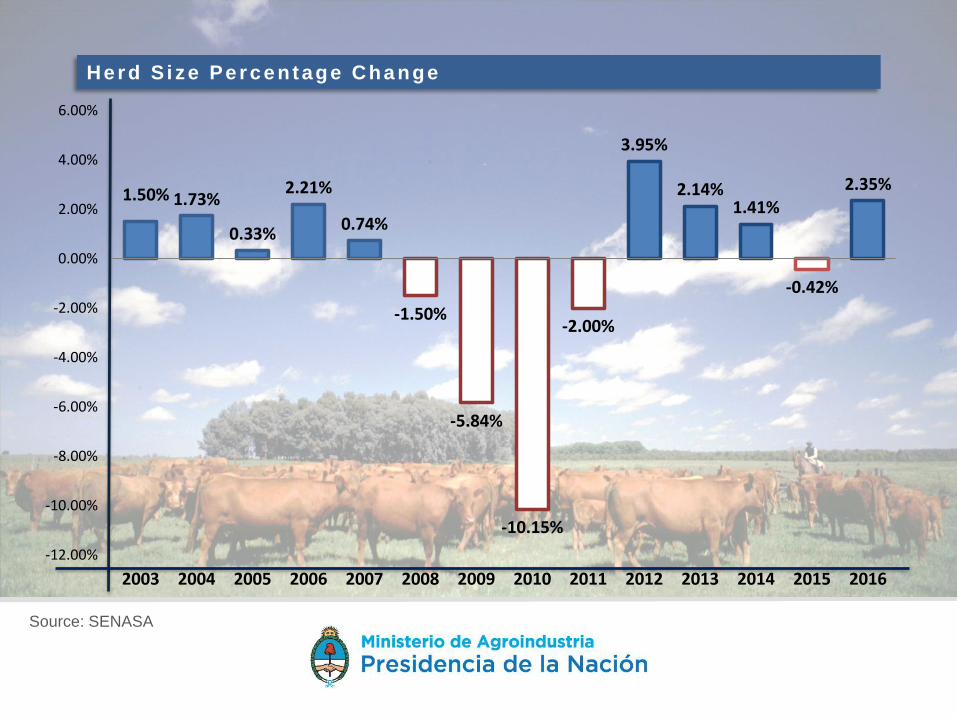

Herd S i ze Percentage Change

1.50% 1.73%

0.33%

2.21%

0.74%

-1.50%

-5.84%

-10.15%

-2.00%

3.95%

2.14%1.41%

-0.42%

2.35%

-12.00%

-10.00%

-8.00%

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Source: SENASA

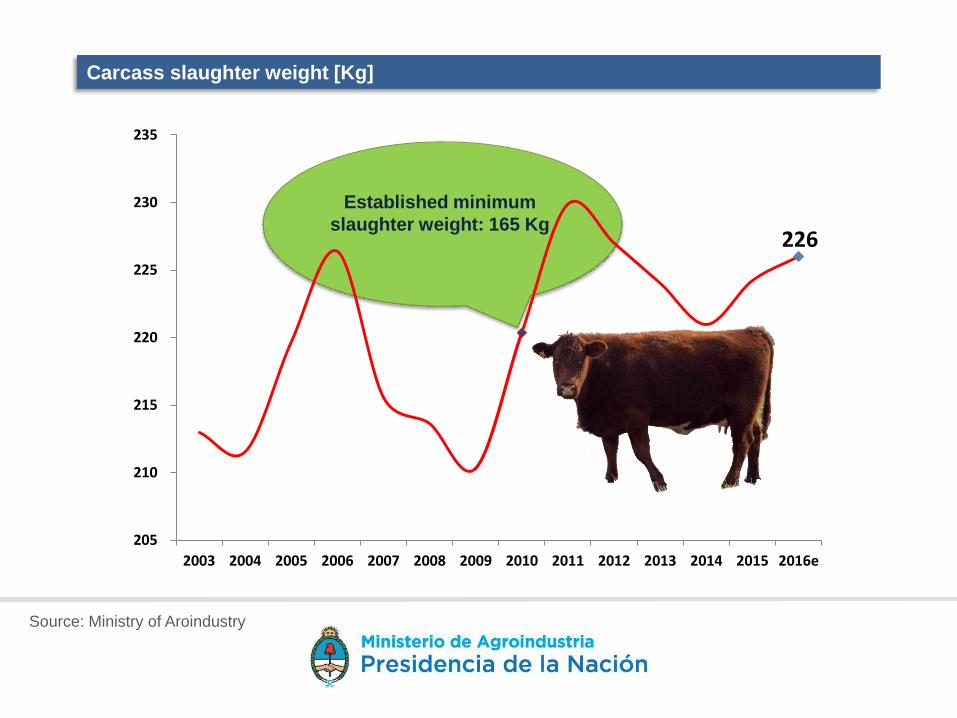

Carcass slaughter weight [Kg]

226

205

210

215

220

225

230

235

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016e

Established minimum

slaughter weight: 165 Kg

Source: Ministry of Aroindustry

Argentina

Beef Exports

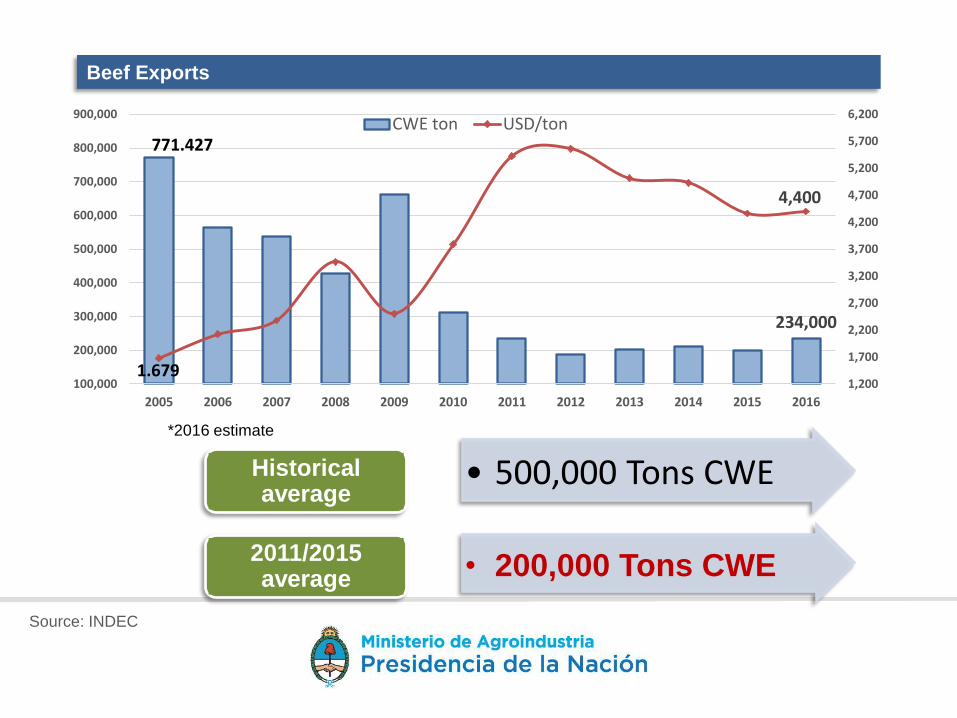

Beef Exports

234,000

4,400

1,200

1,700

2,200

2,700

3,200

3,700

4,200

4,700

5,200

5,700

6,200

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

CWE ton USD/ton771.427

1.679

*2016 estimate

• 500,000 Tons CWEHistorical average

• 200,000 Tons CWE2011/2015 average

Source: INDEC

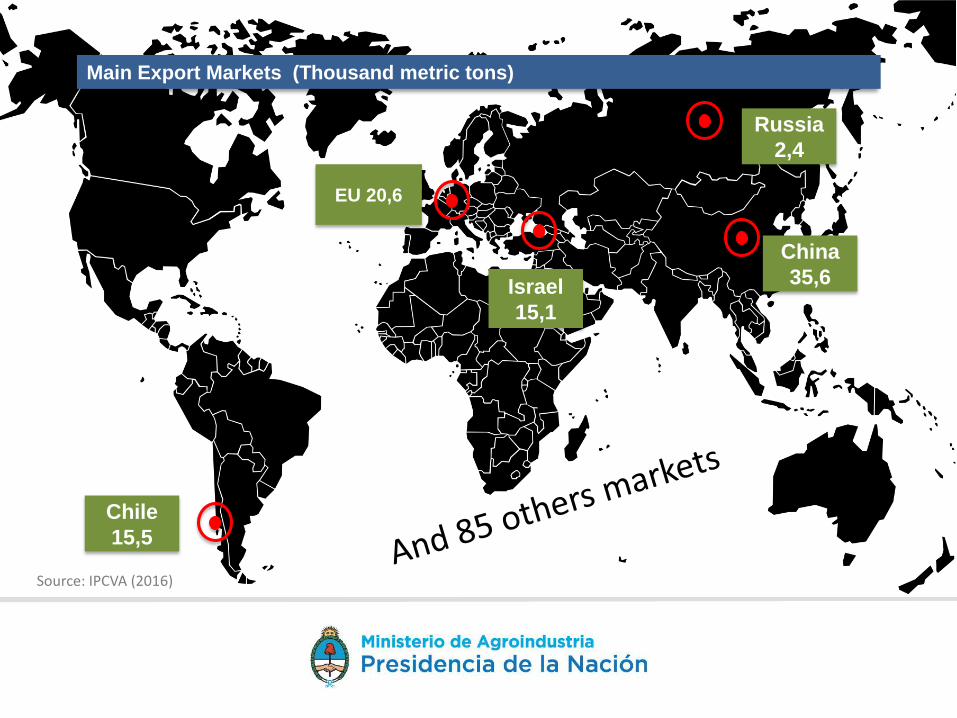

Main Export Markets (Thousand metric tons)

EU 20,6

Russia

2,4

China

35,6Israel

15,1

Chile

15,5

Source: IPCVA (2016)

Main goals

OPEN

and in the future: South Korea, Japan, Mexico

Increase exports

Betternegotiations

to increase trade

new markets

United States

Canada(Chilled and Frozen)

![Porcine Epidemic Diarrhea [Autosaved]](https://img.pdfslide.net/doc/110x75/577c808c1a28abe054a92a69/porcine-epidemic-diarrhea-autosaved.jpg)