Embed Size (px)

Citation preview

[ C L I E N T N A M E ]

Presentation3

179.31.36

106.107.109

8.144.70

40.44.109

144.28.83

243.165.30

218.70.38

14.116.118

1237395-001.pptx

Conference Call First Quarter 2015 Financial Results

May 04, 2015 1

[ C L I E N T N A M E ]

Agenda

2

[ C L I E N T N A M E ]

Presentation3

179.31.36

106.107.109

8.144.70

40.44.109

144.28.83

243.165.30

218.70.38

14.116.118

1237395-001.pptx

Q1 2015 Milestones

Agenda 179.31.36

106.107.109

8.144.70

40.44.109

144.28.83

243.165.30

218.70.38

14.116.118

Opening Remarks

Q1 2015 Highlights

1

2

3

Operating and Financial Review 4

3

Guidance 5

Q&A 6

[ C L I E N T N A M E ]

Presentation3

179.31.36

106.107.109

8.144.70

40.44.109

144.28.83

243.165.30

218.70.38

14.116.118

1237395-001.pptx

Q1 2015 Highlights 179.31.36

106.107.109

8.144.70

40.44.109

144.28.83

243.165.30

218.70.38

14.116.118

2

4

Revenues and Volume increased 8.5% and 1.7% YoY, respectively. Our key growth drivers for the quarter were Animal Nutrition with an impressive 27.1% YoY jump in sales, and Consumer Goods with a steady increase in revenue of 5.2% YoY

We gained market share in 12 of our 14 categories in Peru in line with our 2014-2015 strategy for organic growth. Consequently, we launched and revamped over 15 new products for our Consumer Goods and B2B businesses, to jointly strengthen our portfolio of new products while continue to boost market share

Gross Profit increased 14.1% in Q1 2015 up to S/. 415.7 million compared to the S/. 364.2 million reported in Q1 2014

EBITDA amounted to S/. 149.5 million, in line with Q1 14’, with EBITDA Margin reaching 9.9%

Net Income reached S/. 19.9 million in Q1 15’ , a decrease of S/. 39.7 million YoY , on the back of: i) net financial expenses of S/. 45.9 million, an increase of S/. 15.7 million YoY, due to increased debt, ii) non-cash expenses of S/. 34.6 million related to FX volatility affecting the time value of our call spread structure, an increase of S/. 40.7 million YoY, iii) FX losses of S/._3.5 million, a reduction of S/. 15.7 YoY, and iv) tax payments of S/. 10.0 million, a reduction of S/. 10.6 million versus Q1 14’

Total debt as of Q1 2015 decreased S/ 162.6 million, a 6.0% versus December 2014, from S/. 2,699.2 million accounted in Q4 2014 to S/. 2,536.6 million in Q1 2015

[ C L I E N T N A M E ]

Presentation3

179.31.36

106.107.109

8.144.70

40.44.109

144.28.83

243.165.30

218.70.38

14.116.118

1237395-001.pptx

Q1 2015 Milestones 179.31.36

106.107.109

8.144.70

40.44.109

144.28.83

243.165.30

218.70.38

14.116.118

3

5

We have materially reduced the position associated with our Q4 14´losses, which is extraordinary and unrelated to our commodities hedging strategy, without incurring in additional significant losses, As of April, we have effectively liquidated the position while we continue to strengthen our controls and processes associated with our commodities hedging strategy

In anticipation to an appreciating US$, Alicorp significantly reduced its exposure to dollar-denominated debt by issuing S/. 500 million in local bonds to repurchase US$107.1 million of its 2023 notes. On February 2015, we concluded a tender offer for our 2023 US$ senior notes with a buyback of US$ 89.2 million. In addition, in March and April we executed additional private repurchases totaling US$ 17.9 million. The local bond issuance and buyback scheme allowed us to simultaneously refinance our existing debt at a lower cost while extending the long-term duration of our consolidated debt to 6.19 years, versus 5.68 years in December 2014.

We concluded a successful capital injection for our Argentina subsidiary totaling US$ 35.0 million. This decision allowed Alicorp to both reduce its interest expense burden in Argentina while refinancing its existing Argentinian peso denominated debt with cheaper Peruvian nuevo sol debt

Alicorp was recognized among the “Best Brand Advertisers in the ANDA 2015 Awards”, as a result of the “Momento de Compartir” campaign, launched as part of our communication strategy roll-out for our mega brand Blanca Flor, in particular for our Ready Mixes and Panettones

[ C L I E N T N A M E ]

Presentation3

179.31.36

106.107.109

8.144.70

40.44.109

144.28.83

243.165.30

218.70.38

14.116.118

1237395-001.pptx

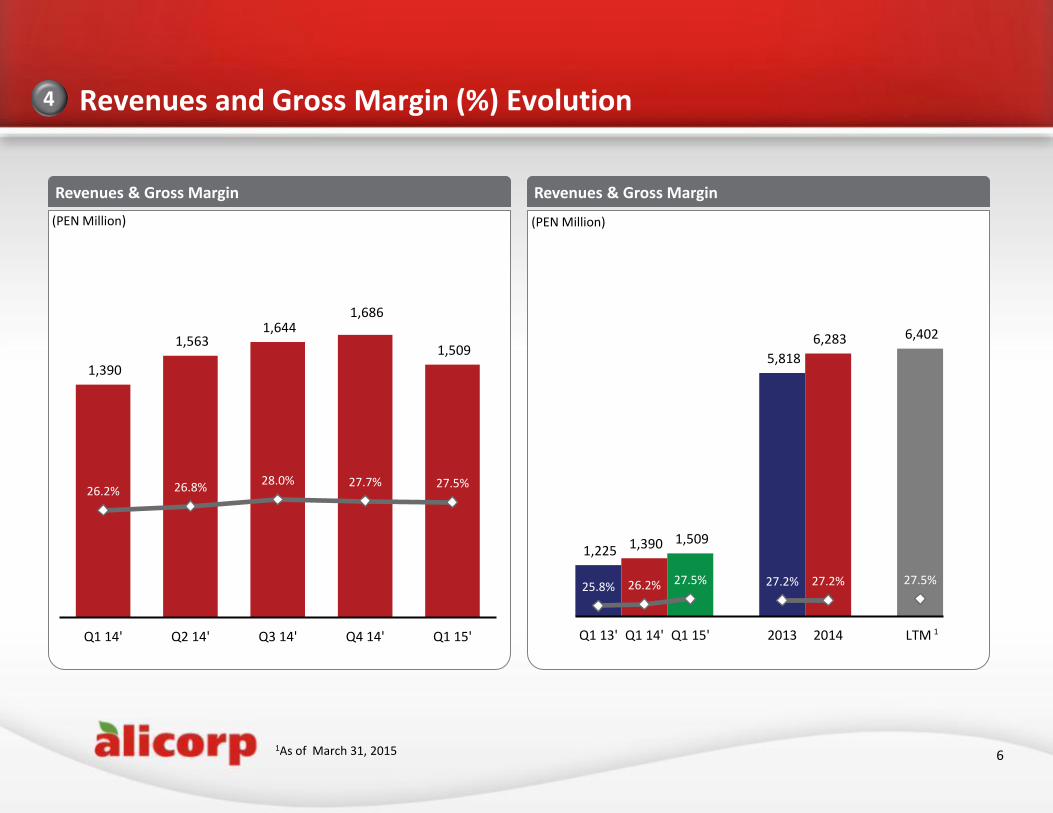

Revenues and Gross Margin (%) Evolution 4

Revenues & Gross Margin Revenues & Gross Margin

(PEN Million) (PEN Million)

6

1,390

1,563 1,644

1,686

1,509

26.2% 26.8% 28.0% 27.7% 27.5%

Q1 14' Q2 14' Q3 14' Q4 14' Q1 15'

1,225 1,390 1,509

5,818

6,283 6,402

25.8% 26.2% 27.5% 27.2% 27.2% 27.5%

Q1 13' Q1 14' Q1 15' 2013 2014 LTM

1As of March 31, 2015

1

[ C L I E N T N A M E ]

Presentation3

179.31.36

106.107.109

8.144.70

40.44.109

144.28.83

243.165.30

218.70.38

14.116.118

1237395-001.pptx

EBITDA and EBITDA Margin (%) Evolution 4

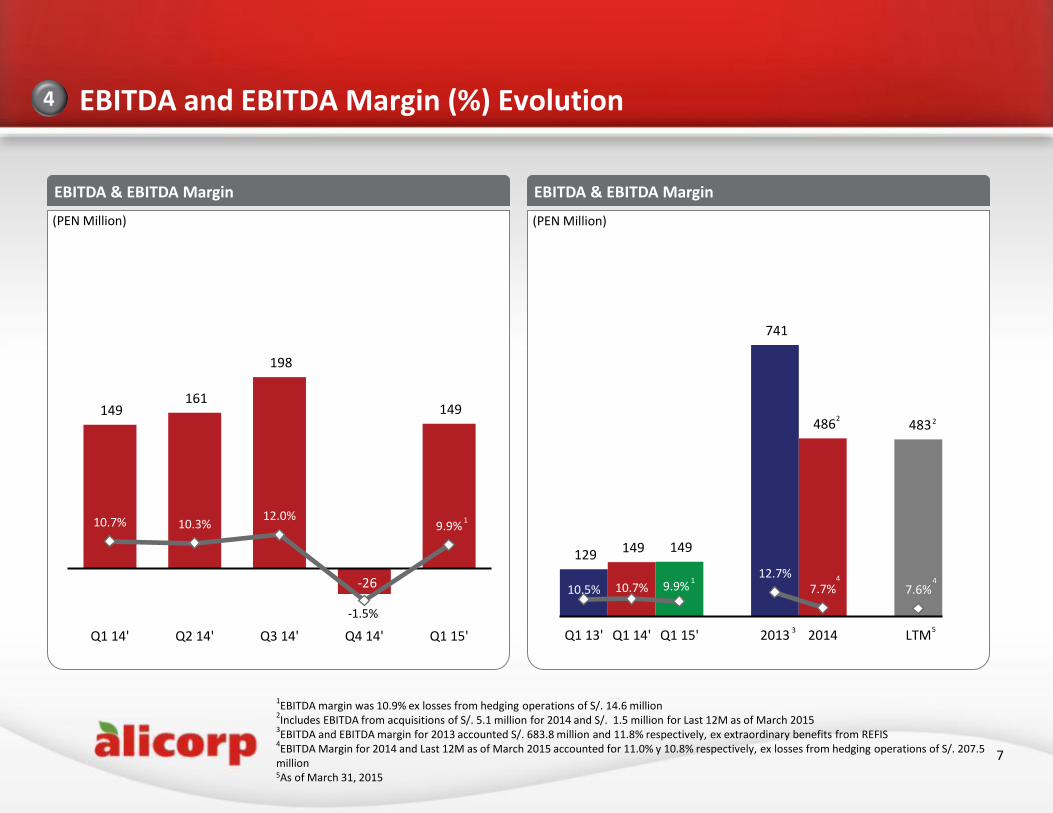

EBITDA & EBITDA Margin EBITDA & EBITDA Margin

(PEN Million) (PEN Million)

7

1EBITDA margin was 10.9% ex losses from hedging operations of S/. 14.6 million

2Includes EBITDA from acquisitions of S/. 5.1 million for 2014 and S/. 1.5 million for Last 12M as of March 2015

3EBITDA and EBITDA margin for 2013 accounted S/. 683.8 million and 11.8% respectively, ex extraordinary benefits from REFIS

4EBITDA Margin for 2014 and Last 12M as of March 2015 accounted for 11.0% y 10.8% respectively, ex losses from hedging operations of S/. 207.5

million 5As of March 31, 2015

149 161

198

-26

149

10.7% 10.3% 12.0%

-1.5%

9.9%

Q1 14' Q2 14' Q3 14' Q4 14' Q1 15'

129 149 149

741

486 483

10.5% 10.7% 9.9% 12.7%

7.7% 7.6%

Q1 13' Q1 14' Q1 15' 2013 2014 LTM3

4

5

2 2

4

1

1

[ C L I E N T N A M E ]

Presentation3

179.31.36

106.107.109

8.144.70

40.44.109

144.28.83

243.165.30

218.70.38

14.116.118

1237395-001.pptx

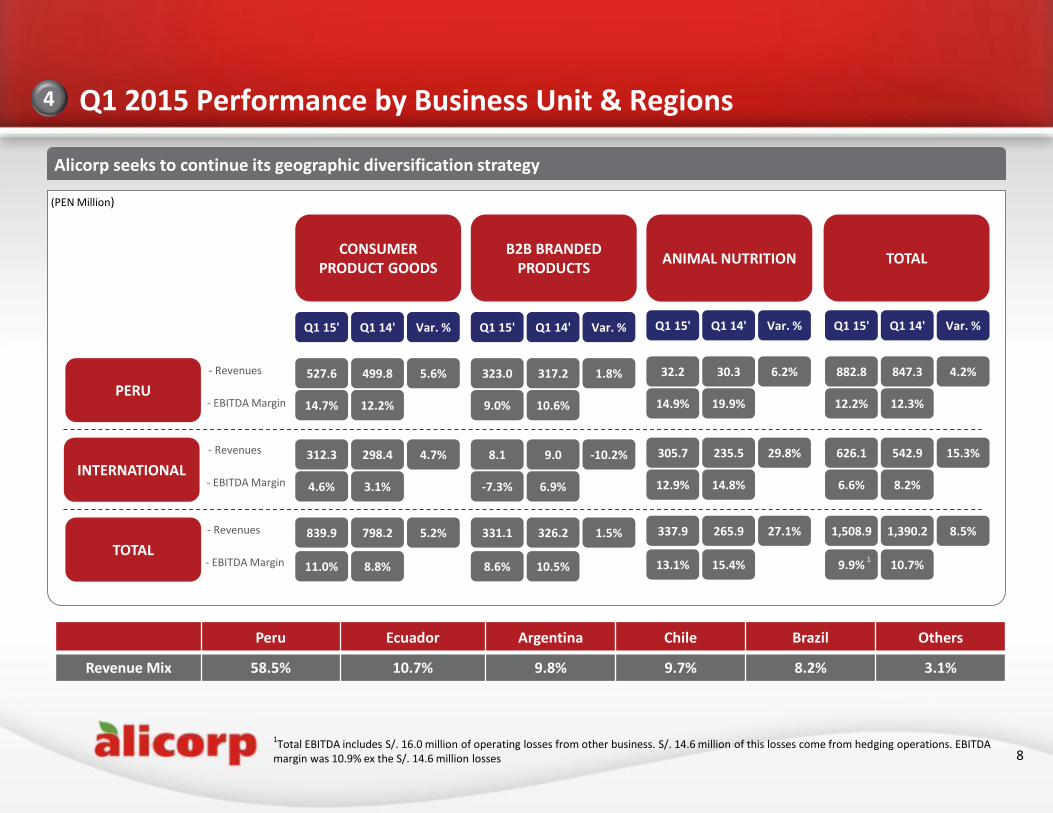

Q1 2015 Performance by Business Unit & Regions 4

Alicorp seeks to continue its geographic diversification strategy

Peru Ecuador Argentina Chile Brazil Others

Revenue Mix 58.5% 10.7% 9.8% 9.7% 8.2% 3.1%

(PEN Million)

8

PERU

INTERNATIONAL

TOTAL

CONSUMER PRODUCT GOODS

B2B BRANDED PRODUCTS

ANIMAL NUTRITION

TOTAL

- Revenues

- EBITDA Margin

- Revenues

- EBITDA Margin

- Revenues

- EBITDA Margin

Q1 14' Q1 15' Var. % Q1 14' Q1 15' Var. % Q1 14' Q1 15' Var. % Q1 14' Q1 15' Var. %

499.8 527.6 5.6%

12.2% 14.7%

298.4 312.3 4.7%

3.1% 4.6%

798.2 839.9 5.2%

8.8% 11.0%

317.2 323.0 1.8%

10.6% 9.0%

9.0 8.1 -10.2%

6.9% -7.3%

326.2 331.1 1.5%

10.5% 8.6%

30.3 32.2 6.2%

19.9% 14.9%

235.5 305.7 29.8%

14.8% 12.9%

265.9 337.9 27.1%

15.4% 13.1%

847.3 882.8 4.2%

12.3% 12.2%

542.9 626.1 15.3%

8.2% 6.6%

1,390.2 1,508.9 8.5%

10.7% 9.9%

1Total EBITDA includes S/. 16.0 million of operating losses from other business. S/. 14.6 million of this losses come from hedging operations. EBITDA

margin was 10.9% ex the S/. 14.6 million losses

1

[ C L I E N T N A M E ]

Presentation3

179.31.36

106.107.109

8.144.70

40.44.109

144.28.83

243.165.30

218.70.38

14.116.118

1237395-001.pptx

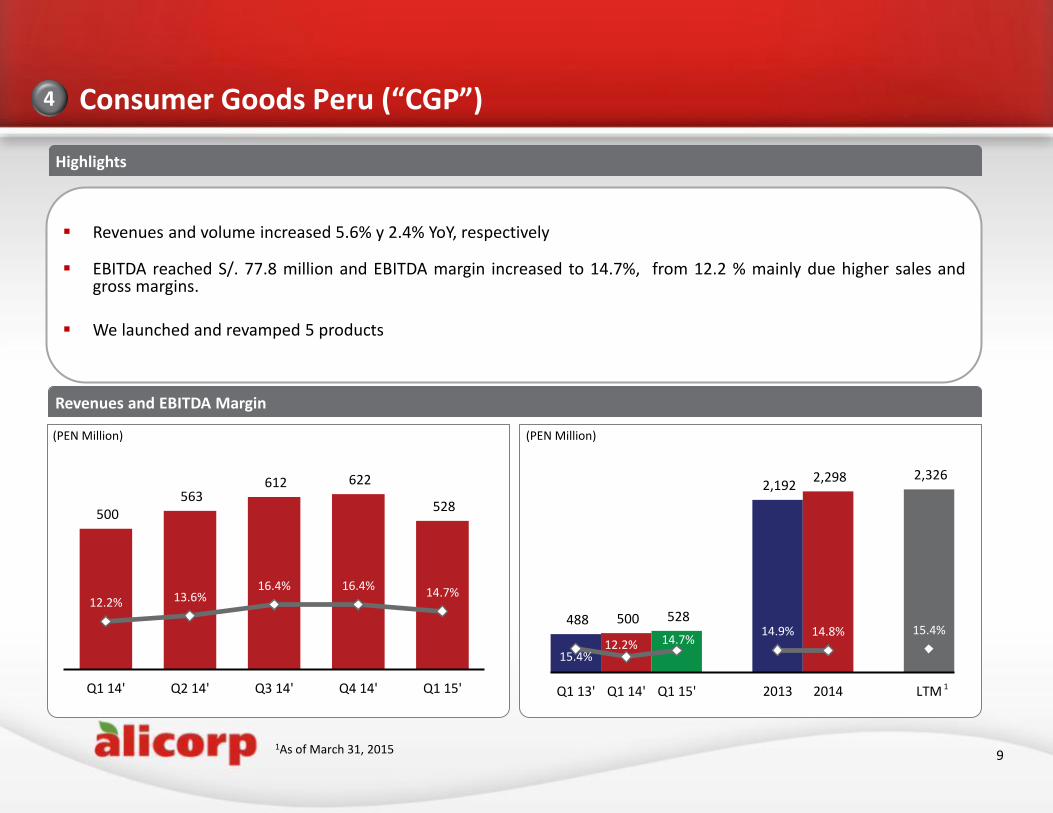

Consumer Goods Peru (“CGP”) 4

Revenues and volume increased 5.6% y 2.4% YoY, respectively

EBITDA reached S/. 77.8 million and EBITDA margin increased to 14.7%, from 12.2 % mainly due higher sales and gross margins.

We launched and revamped 5 products

Revenues and EBITDA Margin

Highlights

(PEN Million) (PEN Million)

9

1

2

500 563

612 622

528

12.2% 13.6% 16.4% 16.4%

14.7%

Q1 14' Q2 14' Q3 14' Q4 14' Q1 15'

488 500 528

2,192 2,298 2,326

15.4% 12.2% 14.7%

14.9% 14.8% 15.4%

Q1 13' Q1 14' Q1 15' 2013 2014 LTM

1As of March 31, 2015

1

[ C L I E N T N A M E ]

Presentation3

179.31.36

106.107.109

8.144.70

40.44.109

144.28.83

243.165.30

218.70.38

14.116.118

1237395-001.pptx

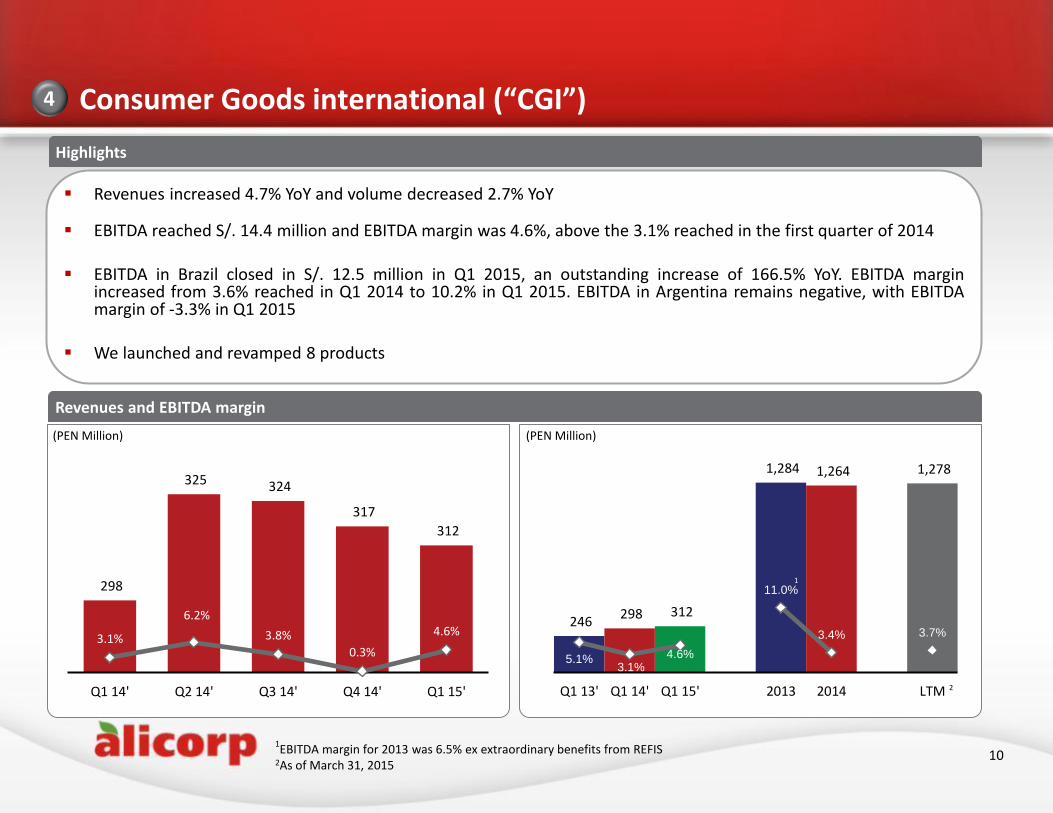

Consumer Goods international (“CGI”) 4

Revenues increased 4.7% YoY and volume decreased 2.7% YoY

EBITDA reached S/. 14.4 million and EBITDA margin was 4.6%, above the 3.1% reached in the first quarter of 2014

EBITDA in Brazil closed in S/. 12.5 million in Q1 2015, an outstanding increase of 166.5% YoY. EBITDA margin increased from 3.6% reached in Q1 2014 to 10.2% in Q1 2015. EBITDA in Argentina remains negative, with EBITDA margin of -3.3% in Q1 2015

We launched and revamped 8 products

Revenues and EBITDA margin

Highlights

(PEN Million) (PEN Million)

10

2

2

298

325 324

317

312

3.1%

6.2%

3.8%

0.3%

4.6%

Q1 14' Q2 14' Q3 14' Q4 14' Q1 15'

246 298 312

1,284 1,264 1,278

5.1% 3.1%

4.6%

11.0%

3.4% 3.7%

Q1 13' Q1 14' Q1 15' 2013 2014 LTM

1EBITDA margin for 2013 was 6.5% ex extraordinary benefits from REFIS

2As of March 31, 2015

1

[ C L I E N T N A M E ]

Presentation3

179.31.36

106.107.109

8.144.70

40.44.109

144.28.83

243.165.30

218.70.38

14.116.118

1237395-001.pptx

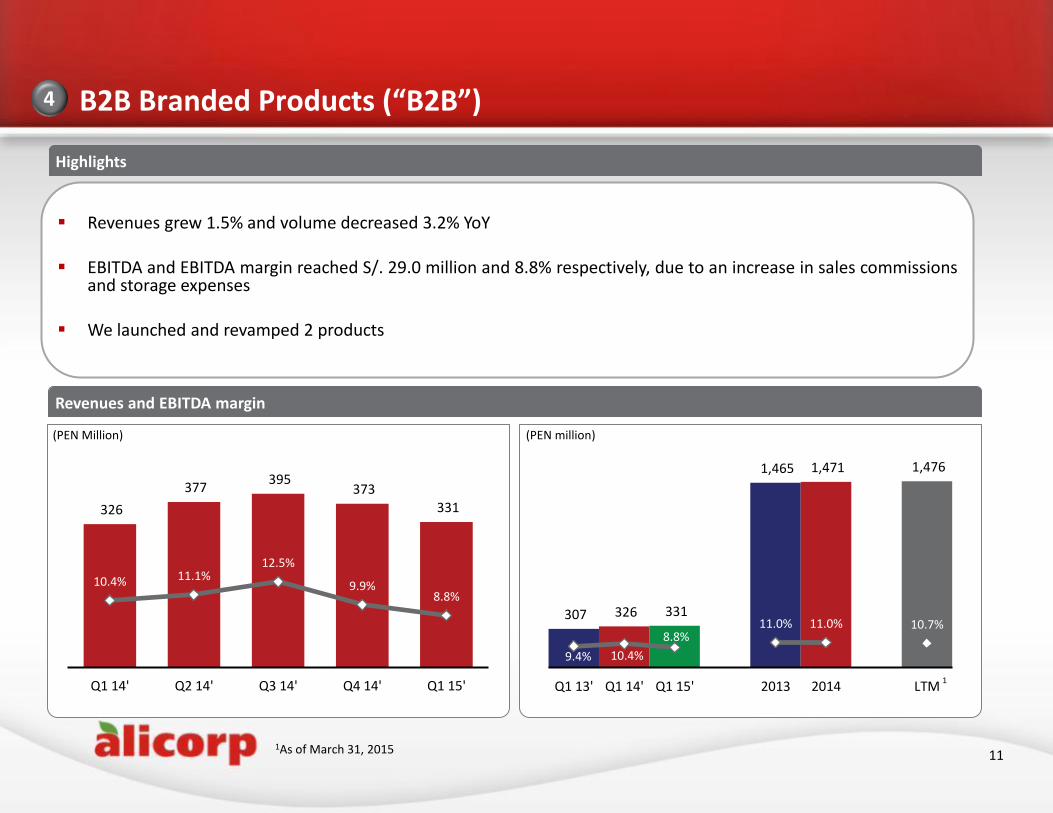

B2B Branded Products (“B2B”) 4

Revenues grew 1.5% and volume decreased 3.2% YoY

EBITDA and EBITDA margin reached S/. 29.0 million and 8.8% respectively, due to an increase in sales commissions and storage expenses

We launched and revamped 2 products

Revenues and EBITDA margin

Highlights

(PEN Million) (PEN million)

11

326

377 395

373 331

10.4% 11.1% 12.5%

9.9% 8.8%

Q1 14' Q2 14' Q3 14' Q4 14' Q1 15'

307 326 331

1,465 1,471 1,476

9.4% 10.4%

8.8% 11.0% 11.0% 10.7%

Q1 13' Q1 14' Q1 15' 2013 2014 LTM1

1As of March 31, 2015

[ C L I E N T N A M E ]

Presentation3

179.31.36

106.107.109

8.144.70

40.44.109

144.28.83

243.165.30

218.70.38

14.116.118

1237395-001.pptx

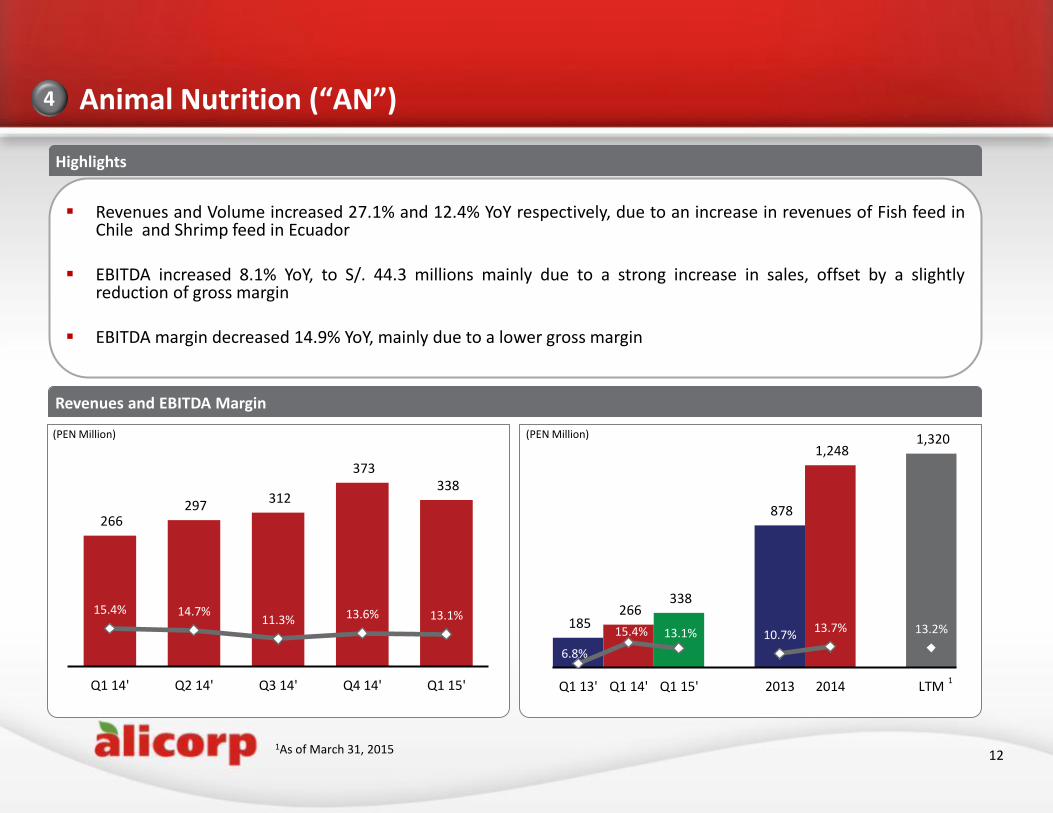

Animal Nutrition (“AN”) 4

Revenues and Volume increased 27.1% and 12.4% YoY respectively, due to an increase in revenues of Fish feed in Chile and Shrimp feed in Ecuador

EBITDA increased 8.1% YoY, to S/. 44.3 millions mainly due to a strong increase in sales, offset by a slightly reduction of gross margin

EBITDA margin decreased 14.9% YoY, mainly due to a lower gross margin

Revenues and EBITDA Margin

Highlights

(PEN Million) (PEN Million)

12

266 297

312

373 338

15.4% 14.7% 11.3% 13.6% 13.1%

Q1 14' Q2 14' Q3 14' Q4 14' Q1 15'

185 266

338

878

1,248 1,320

6.8%

15.4% 13.1% 10.7% 13.7% 13.2%

Q1 13' Q1 14' Q1 15' 2013 2014 LTM1

1As of March 31, 2015

[ C L I E N T N A M E ]

Presentation3

179.31.36

106.107.109

8.144.70

40.44.109

144.28.83

243.165.30

218.70.38

14.116.118

1237395-001.pptx

Debt Metrics

Net Debt

Q4 2014 Q1 2015

Current Debt

Non-Current Debt

Var. %

Total Indebtedness

(-) Cash

Net Debt

Debt Breakdown by currency3

1Includes EBITDA from acquisitions

2Net Debt / EBITDA for Q4 2014 and Q1 2015 were 3.75x and 3.51x respectively, ex losses from hedging operation of S/. 207.5 million during 2014

3Debt after swap as of March 31, 2015 4Debt excluding amortized cost

(PEN Million)

13

937.0 571.6 -39.0%

1,762.2 1,965.1 11.5%

2,699.2 2,536.6 -6.0%

99.5 112.2 12.8%

2,599.7 2,424.4 -6.7%

4

18%

65%

5%

12%

USD

PEN

BRL

ARS

Net Debt / EBITDA1

Maturity Profile as of March 20154

534

174

116

33

566

111

290

22

1,062

50 100 100 100 100 50

2015 2016 2017 2018 2023 2024 2025 2026 2027 2028 2029 2030

Mil

lare

s International Bonds Local Bonds Bank Loans(PEN Million)

2.53x 2.70x

3.24x 3.64x

5.35x 5.02x

Q4 13' Q1 14' Q2 14' Q3 14' Q4 14' Q1 15'

2,424

483

1,893

747

2,057

761

2,403

741

2,732

750

2,600

486

Net Debt EBITDA

2 2

[ C L I E N T N A M E ]

Presentation3

179.31.36

106.107.109

8.144.70

40.44.109

144.28.83

243.165.30

218.70.38

14.116.118

1237395-001.pptx

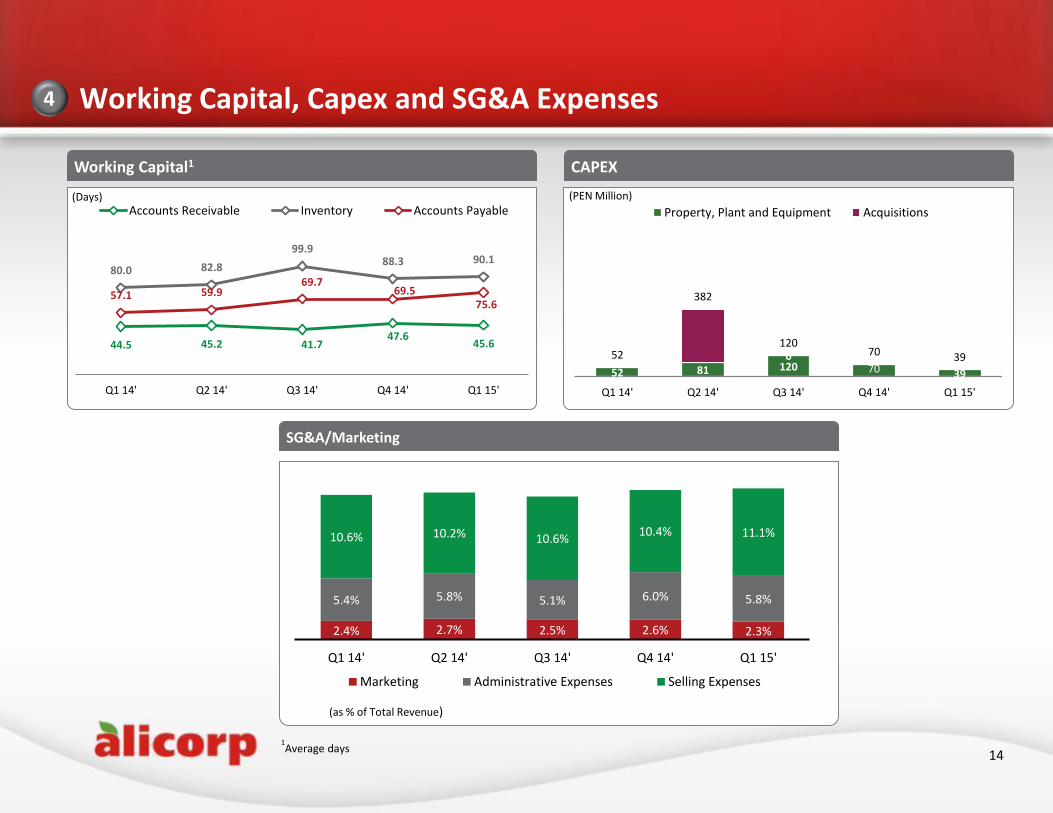

Working Capital, Capex and SG&A Expenses 4

14

Working Capital1

(Days)

CAPEX

(PEN Million)

SG&A/Marketing

44.5 45.2 41.7 47.6

45.6

80.0 82.8

99.9 88.3 90.1

57.1 59.9 69.7

69.5 75.6

Q1 14' Q2 14' Q3 14' Q4 14' Q1 15'

Accounts Receivable Inventory Accounts Payable

2.4% 2.7% 2.5% 2.6% 2.3%

5.4% 5.8% 5.1% 6.0% 5.8%

10.6% 10.2% 10.6% 10.4% 11.1%

Q1 14' Q2 14' Q3 14' Q4 14' Q1 15'

Marketing Administrative Expenses Selling Expenses

52 81 120 70 39

0 52

382

120 70 39

Q1 14' Q2 14' Q3 14' Q4 14' Q1 15'

Mill

ares

Property, Plant and Equipment Acquisitions

(as % of Total Revenue)

1Average days

[ C L I E N T N A M E ]

Presentation3

179.31.36

106.107.109

8.144.70

40.44.109

144.28.83

243.165.30

218.70.38

14.116.118

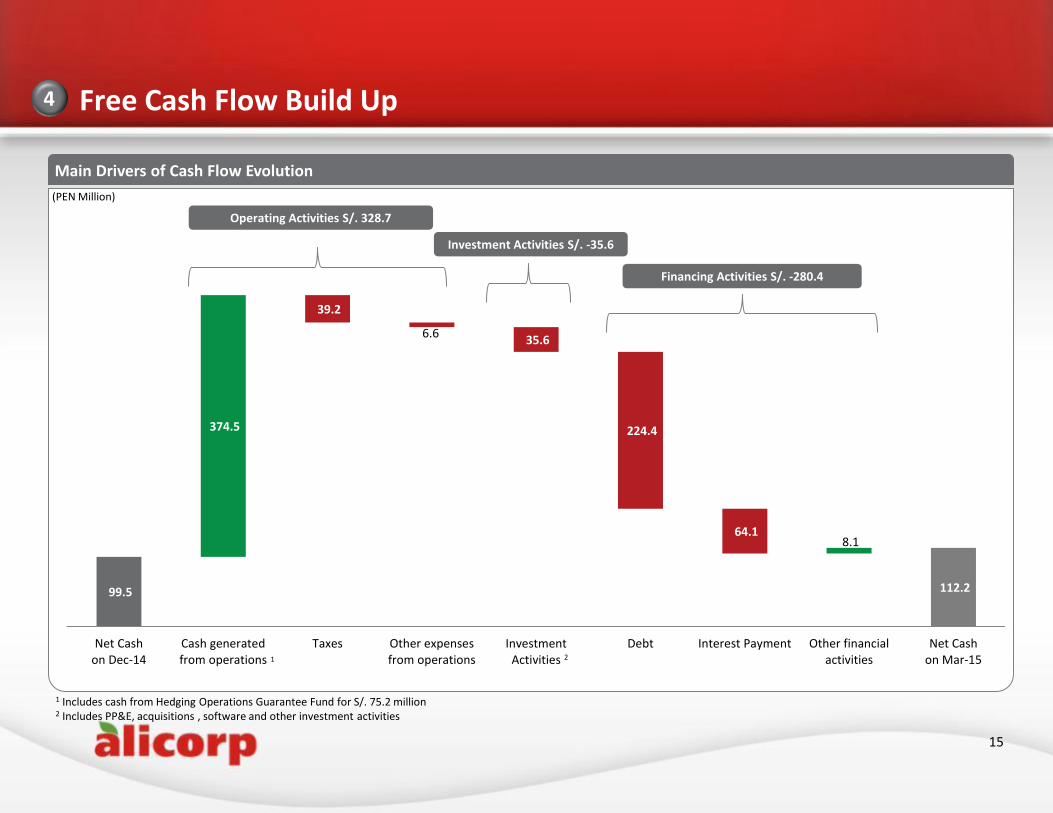

1237395-001.pptx

99.5

587.8

112.2

374.5

-

-

- 8.1

39.2

6.6 35.6

224.4

64.1

Net Cashon Dec-14

Cash generatedfrom operations

Taxes Other expensesfrom operations

InvestmentActivities

Debt Interest Payment Other financialactivities

Net Cashon Mar-15

4

15

Main Drivers of Cash Flow Evolution

Free Cash Flow Build Up

(PEN Million)

1 Includes cash from Hedging Operations Guarantee Fund for S/. 75.2 million 2 Includes PP&E, acquisitions , software and other investment activities

Operating Activities S/. 328.7

Financing Activities S/. -280.4

Investment Activities S/. -35.6

1 2

[ C L I E N T N A M E ]

Presentation3

179.31.36

106.107.109

8.144.70

40.44.109

144.28.83

243.165.30

218.70.38

14.116.118

1237395-001.pptx

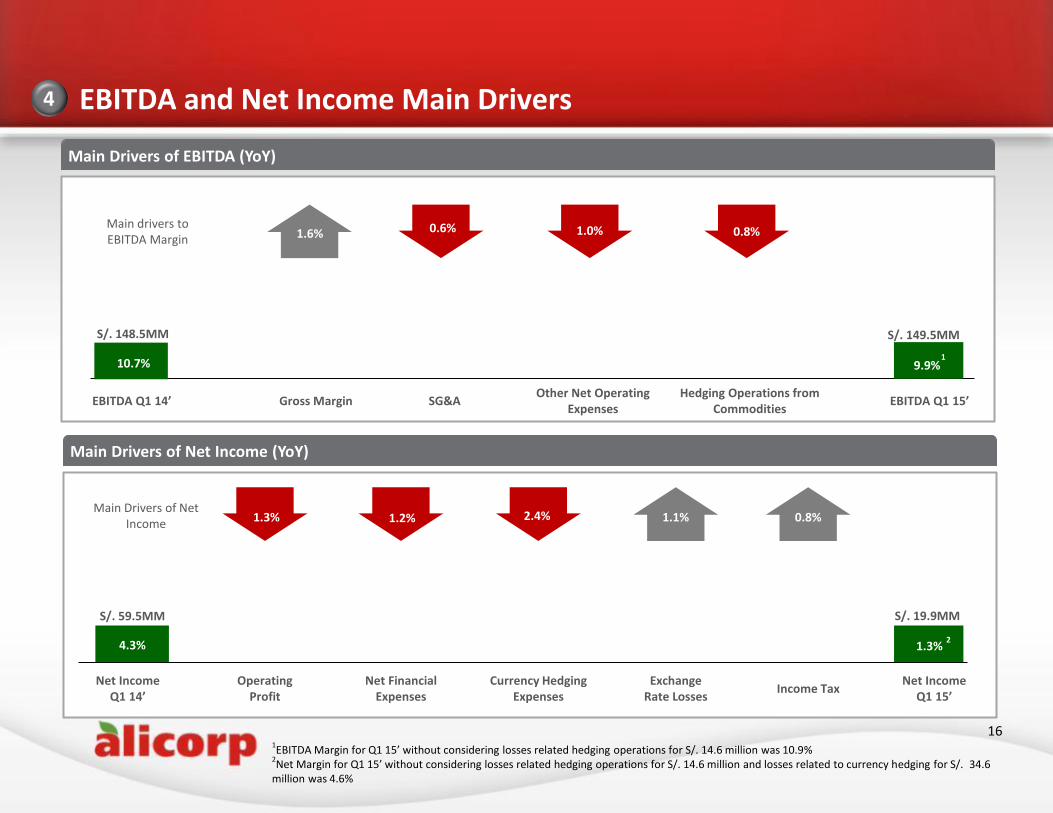

EBITDA and Net Income Main Drivers

Main Drivers of EBITDA (YoY)

16

4

1EBITDA Margin for Q1 15’ without considering losses related hedging operations for S/. 14.6 million was 10.9%

2Net Margin for Q1 15’ without considering losses related hedging operations for S/. 14.6 million and losses related to currency hedging for S/._34.6

million was 4.6%

SG&A Other Net Operating

Expenses Gross Margin

Main drivers to EBITDA Margin

Hedging Operations from Commodities

% 1.6% 0.6% 1.0% 0.8%

EBITDA Q1 14’

10.7%

S/. 148.5MM

EBITDA Q1 15’

S/. 149.5MM

9.9% 1

Main Drivers of Net Income (YoY)

1.3% 1.2%

Net Income Q1 15’

S/. 59.5MM S/. 19.9MM

Net Income Q1 14’

4.3% 1.3%

Operating Profit

Net Financial Expenses

Exchange Rate Losses

Income Tax

1.1% 2.4%

Currency Hedging Expenses

0.8%

2

Main Drivers of Net Income

[ C L I E N T N A M E ]

Presentation3

179.31.36

106.107.109

8.144.70

40.44.109

144.28.83

243.165.30

218.70.38

14.116.118

1237395-001.pptx

Guidance 2015 179.31.36

106.107.109

8.144.70

40.44.109

144.28.83

243.165.30

218.70.38

14.116.118

5

17

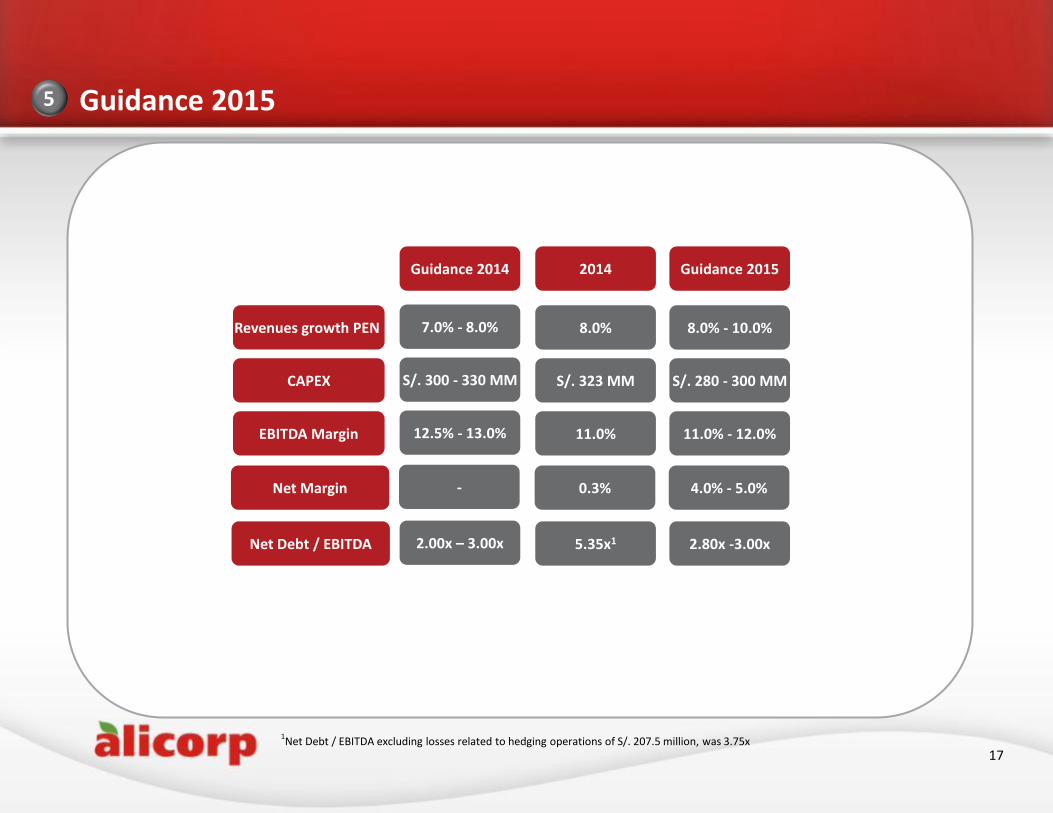

1Net Debt / EBITDA excluding losses related to hedging operations of S/. 207.5 million, was 3.75x

2014 Guidance 2014

8.0% 7.0% - 8.0%

11.0%

12.5% - 13.0%

S/. 323 MM S/. 300 - 330 MM

Revenues growth PEN

EBITDA Margin

CAPEX

5.35x1 2.00x – 3.00x Net Debt / EBITDA

Guidance 2015

8.0% - 10.0%

11.0% - 12.0%

S/. 280 - 300 MM

2.80x -3.00x

0.3% - Net Margin 4.0% - 5.0%

[ C L I E N T N A M E ]

Q&A

18