Embed Size (px)

Citation preview

E&O and the Personal Auto Insurance Agent

Presented by:Joni R. Fairbrother, CIC, RPLU

Assist. Vice President – Independent Ins. Agents & Brokers of AZ

I am not here to talk doom and gloom

I am not here to talk about making your life more complicated

We work in a great industry with awesome possibilities

Working smart to make you more profitable by avoiding E&O Claims

Some goals for our time together

The number of E&O claims is going down.

Not just in Arizona but across the country

There is some good news!

The severity is through the roof

Average claims settling for more than double what they did in 1996

The bad news is…..

5

What’s going on with Personal Auto E&O in

Arizona

Arizona - Prior to changes in law regarding UM/UIM in early 90’s almost 30% of our E&O claims were from Personal Auto

We now have about 14% of our claims (here in Arizona) come from personal auto

Personal Auto E&O

Prior to about 1992, UM/UIM challenged claims were almost always a loser for agent (if not in loss of the lawsuit – then loss in time and expense in defending)

The rejection forms were just not working very well

So what changed?

The Big I worked very hard to change the law to require a standardized rejection (or acceptance of lower limit) form that would have to be approved by the Arizona Department of Insurance.

The standardized UM/UIM form

ADOI told us – “You worked to change the law, you come up with the form”

Researched nearly every state and contacted almost every personal auto insurance company for samples.

Draft was passed around to E&O defense attorney + many, many stakeholders to edit

Then the hard part came

Arizona Department of Insurance approved the form as the “standard”.

Companies free to come up with their own form BUT had to meet the standard and whatever form used MUST BE FILED with the state. (even if it is the sample from ADOI)

Agents can not use their own form, MUST be the form that the insurance company that you are using filed form.

ADOI approves the form

With the implementation – the standardized form had an immediate positive effect for agents and companies.

A couple of recent stumbling blocks…..

We saw an immediate positive response

See handout for written details.

Arizona Supreme Court Decision made in 2011

Ballesteros - UM/UIM Form was completed

Question before the court is if the form meets the requirements of the law for all – even non-English speaking/reading customers

Ballesteros v. American Standard

The Appellate Court Decision was the VERY frightening issue that we had to deal with

Appellant court sided with Mr. Ballesteros and said agents were required to do “something more”

Say what!!! They didn’t say what “something more” involved – this could have been monumental disaster for agents

Ballesteros v. American Standard

Some details…..

Bilingual agent explained coverage and rejection form was signed.

Mr. Ballesteros claimed that he did not know what he signed.

Argument from Ballesteros was that form should have been in Spanish. (remember – the policy is not in Spanish)

Ballesteros v. American Standard

Big I filed an Amicus Brief (Friend of the Court) to challenge the Appellant Court decision

Many languages spoken in this state – if you had to have a form for each language – impossible situation.

What about illiterate? (functional literate)

Our arguments……

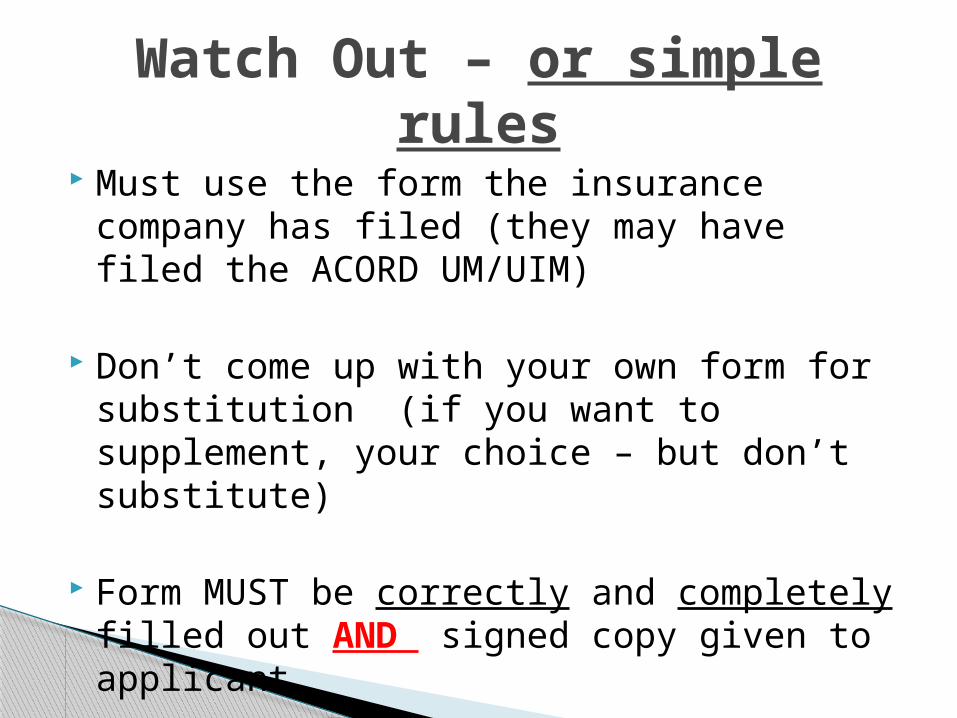

Must use the form the insurance company has filed (they may have filed the ACORD UM/UIM)

Don’t come up with your own form for substitution (if you want to supplement, your choice – but don’t substitute)

Form MUST be correctly and completely filled out AND signed copy given to applicant

Watch Out – or simple rules

Different situation

This decision left a lot of people wondering

Mr. Blevins purchased auto insurance through the 800 number of direct carrier. Recording of Mr. Blevins rejecting coverage but either Mr. Blevins didn’t sign the UM/UIM form or it was lost.

Blevins vs. GEICO

Superior court found in favor of Blevins because the written rejection form could not be produced.

GEICO appealed and Court of Appeals reversed and found in favor of GEICO using the reasoning that Mr. Blevins rejected the coverage himself for himself and the recording proved it.

Blevins vs. GEICO

The decision on this is actually very VERY narrow in scope

Only applied to the person arranging the coverage and no one else that was an “insured”

The court was clear that had there been other “insured’s” the UM/UIM would still have applied

BE VERY CAREFUL

ABSOLUTELY still need to get rejection for every time someone wants reduced or reject UM/UIM coverages.

DO NOT RELY ON PHONE RECORDING

See Blevins bulletin in the back of the handout.

Be very careful….

21

Personal Auto Applications

Correct named insured to match registered owner of the vehicle.◦ Adding a car of a “MVR challenged” relative or

friend to auto policy of a “clean” driver.◦ Not all companies have definition of “Insured”

that match

Correct Driver List◦ The kids◦ The boyfriend/girlfriend that is a regular driver

Application accuracy

E&O Claims tied to Applications

23

Excluded drivers

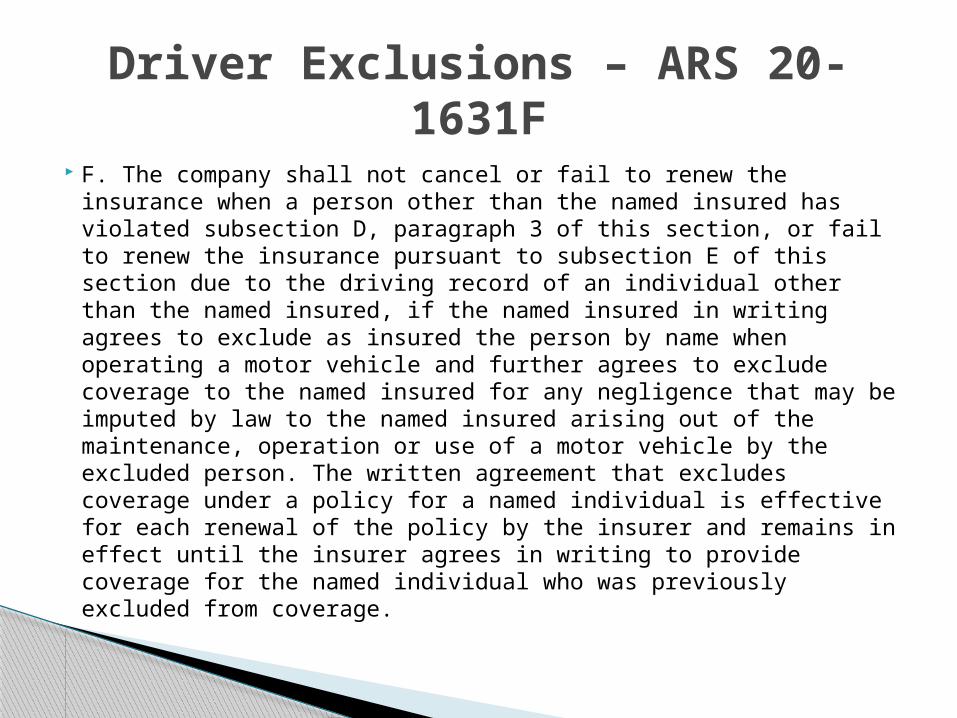

F. The company shall not cancel or fail to renew the insurance when a person other than the named insured has violated subsection D, paragraph 3 of this section, or fail to renew the insurance pursuant to subsection E of this section due to the driving record of an individual other than the named insured, if the named insured in writing agrees to exclude as insured the person by name when operating a motor vehicle and further agrees to exclude coverage to the named insured for any negligence that may be imputed by law to the named insured arising out of the maintenance, operation or use of a motor vehicle by the excluded person. The written agreement that excludes coverage under a policy for a named individual is effective for each renewal of the policy by the insurer and remains in effect until the insurer agrees in writing to provide coverage for the named individual who was previously excluded from coverage.

Driver Exclusions – ARS 20-1631F

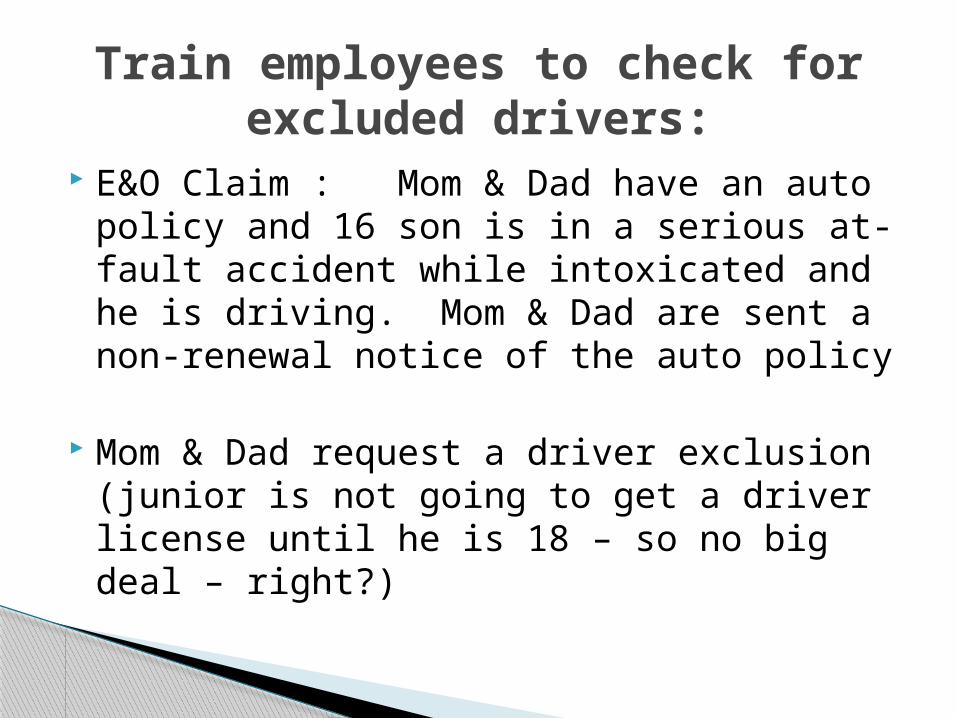

E&O Claim : Mom & Dad have an auto policy and 16 son is in a serious at-fault accident while intoxicated and he is driving. Mom & Dad are sent a non-renewal notice of the auto policy

Mom & Dad request a driver exclusion (junior is not going to get a driver license until he is 18 – so no big deal – right?)

Train employees to check for excluded drivers:

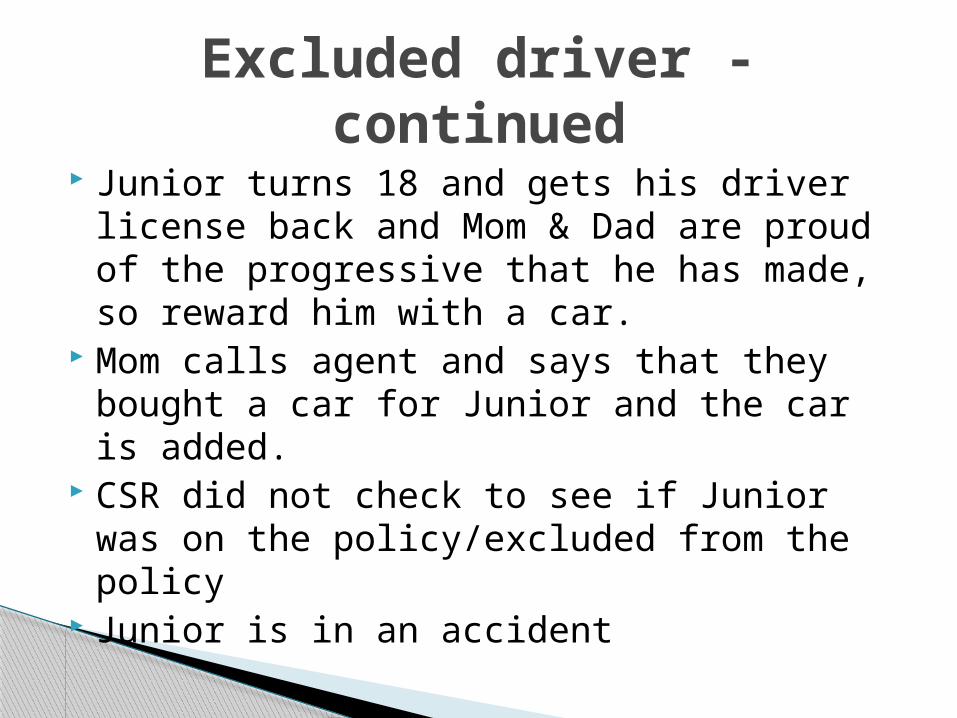

Junior turns 18 and gets his driver license back and Mom & Dad are proud of the progressive that he has made, so reward him with a car.

Mom calls agent and says that they bought a car for Junior and the car is added.

CSR did not check to see if Junior was on the policy/excluded from the policy

Junior is in an accident

Excluded driver - continued

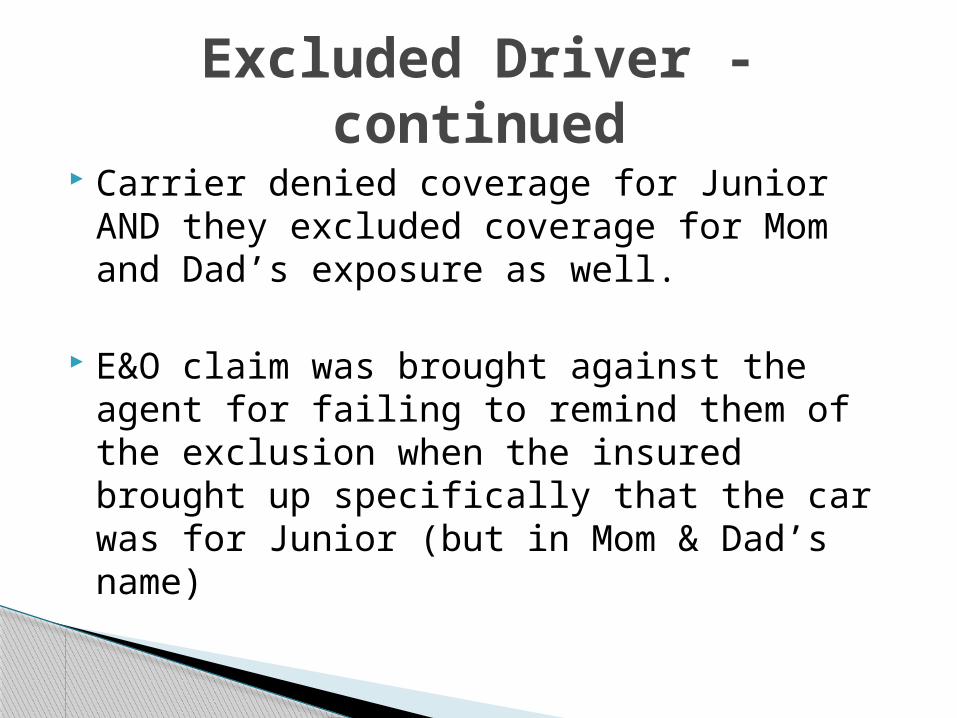

Carrier denied coverage for Junior AND they excluded coverage for Mom and Dad’s exposure as well.

E&O claim was brought against the agent for failing to remind them of the exclusion when the insured brought up specifically that the car was for Junior (but in Mom & Dad’s name)

Excluded Driver - continued

With an excluded driver endorsement, the excluded driver has no coverage (and Named Insured has no coverage if excluded driver is driving) BUT…….

Excluded driver is STILL an “insured”.

Don’t forget – still some coverage for excluded driver

UM/UIM when riding (not driving) a car of the named insured (i.e. parents)

UM/UIM when passenger of some other vehicle

UM/UIM when pedestrian / bike riding

Medical payment (if not driving)

Giving permission to someone else to drive an insured vehicle.

Coverage that still follows excluded driver…..

30

Newly Acquired Auto

ISO – standard auto policy allows liability on the broadest terms until the end of the policy period.

ISO - 14 days physical damage as long as physical damage coverage is already on the policy.

ISO – 4 days of physical damage coverage for newly acquired that no physical damage is on the current policy ($500 ded applies)

Newly Acquired Auto

Each company files their own forms – it is critical that you / your staff chart newly acquired automatic coverage (or lack of) for each company.

Mercury policy says…….

Easy target area for bad information going out to customers.

Not all companies follow ISO

Tell your customers to report newly acquired vehicles immediately.

Tell your customers to report new drivers immediately

Suggestion……

34

Cancellations

To follow-up or not follow-up – that is the question.

Non-pay customer – should an agent follow-up with customers when a notice of cancellation is sent out?

BEING CONSISTENT IS THE KEY

Cancellations

All staff needs to work under the same rule/procedure regarding cancellations and reinstatements.

Don’t promise reinstatements unless verified by company first --- the company may have a general practice of reinstatement, but final decision is always theirs.

Cancellation continued….

Don’t accept money from a client who comes in to pay on a cancelled policy until you first verify with company.

“Reasonable expectation” could attach if they walk out of your office after paying you.

Cancellation continued….

39

Claims – not the E&O type

Most personal lines companies request that the insured report the claim directly to them.

If you do take claim information – remember to let the insurance company claims department do their job.

Claims – not the E&O type

Insured calls you… “What if……..” or “I wanted to tell you about this thing, but I don’t want you to report it to the insurance company”

BE CAREFUL --- information reported to you is information reported to the insurance company (most every time)

Claims

Third party calls you and tells you that your customer caused an accident?

What can you tell them?

What can’t you tell them?

Don’t let third party pressure you into giving out more information than you should.

TRAIN STAFF ABOUT 3RD PARTY CALLS

Third Party Report of claim

43

Standard of Care

E&O claims are generally based on negligence. (sometime contractual)

In a claim of negligence – you look to the definition of negligence ……

Standard Of Care

To do or the failure to do what a reasonable and prudent person would do under similar circumstances.

In an E&O claim – the reasonable and prudent person is a reasonable and prudent “agent”

Definition of Negligence

State laws

Duties owed to insurance companies

Duties owed to the agent’s or broker’s customers

Duties owed to third parties

Who do we owe a Standard of Care?

Unfair Trade Practices◦ Misrepresenting terms of a policy◦ Making false or misleading statements◦ Misrepresenting the financial condition of an

insurer◦ Using the title of a policy to misrepresent its

true nature◦ Inducing a policyholder to forfeit or surrender a

policy based on misrepresentations◦ Using false advertising

Duties to the State

Unfair Trade Practices (cont’d)◦ Defaming an insurance company◦ Falsifying records or documents◦ Selling or offering securities as an inducement

to buy insurance◦ Discriminating against individuals in policy

terms or based on geographic location or age of property

◦ Making a rebate or giving something as an inducement to buy insurance

State laws

◦Comply with terms of the agency agreement

◦Follow all underwriting guidelines provided to the agency

◦Accurately disclose all known risks and material information

Agent duties to a company

Obtain the coverage requested by the customer

Carry out customer’s instructions

Advise the customer when you can’t

Duties to your customers

Determining the other party’s insurable interest and protecting it

Advising other parties of failure to obtain coverage

Using a sufficient degree of skill and care in performing duties to a third party

Duties to Third Parties

If you make a promise by advertisement, in writing or orally – you MUST live up to your promise.

Watch out for overpromise…..

Do what you promise …..

53

“The insurance company for ALL your insurance needs” (ad from an insurance agency – not company)

Yellow page ad’s / Website – slogans that can hurt

54

“We can cover ABSOLUTELY ALL of your insurance needs” (from an agency that is not licensed to sell L&H)

Yellow page ad’s / Website – slogans that can hurt

55

Insurance Consultant – Insurance Expert Witness – Insurance Instructor – I know what you need for insurance protection

Yellow page ad’s Website – slogans that can hurt

56

Facts of similar cases have different outcomes in different jurisdictions

Legal relationship with client depends upon the services performed AND PROMISED

The Legal System

57

Agent’s liability grows with the authority granted by the customer (just handle this for me)

No bright lines to determine when a special relationship begins

Social, ethical, & legal responsibilities are linked

The Legal System

58

File Documentation

59

File Documentation

The file (paper or electronic) is the “story” of what happens on every account

Each step in the process must be documented

“Activities” used in automated files

60

What Constitutes Proper Documentation?

Who initiated the contact? What was the substance of the

conversation? What action is to be taken? What are the next steps? What documents are involved and

where should they be kept?

61

Those darn E&O Claims

An attorney calls your office staff to ask about information from the customer file.

ASK TO HAVE QUESTIONS IN WRITING

An attorney asks for copies of correspondence, copy of the application, etc.

Polite, professional “no” – questions/requests in writing

If you have a POSSIBLE E&O claim

Someone asks you for a recorded statement Polite, professional “no” – questions/requests

in writing

In a court room for a civil case – you don’t have a right to remain silent – BUT DO SO until someone can help you

If you have a POSSIBLE E&O claim

Get your E&O carrier to help you answer.

DO NOT carry on conversations and freely supply third parties with information from your file.

When you receive a demand or request of information

DON’T admit liability – to the insured or the insured’s insurance company

Be empathetic, but watch what you say

Don’t discuss your E&O coverage with anyone, and don’t provide copies

Don’t offer to pay the claim yourself.

NOTIFY your E&O carrier

Caveats

Stress Time lost

◦ Preparing loss notice◦ Producing documents◦ Completing interrogatories◦ Meeting with attorneys◦ Practice deposition◦ Giving depositions◦ Sitting in on witness depositions◦ Going to trial or participating in settlement conferences

What to Expect with E&O Claim

We want to help you with your E&O coverage.

Please call on our office with questions.

My card with contact information at your table.

We want to help

QUESTIONS – about anything we talked about this morning?

QUESTIONS – on any topic we DIDN’T talk about this morning.

QUESTIONS???

For inviting me to speak to you today about a subject that I am very passionate about.

Thanks Mercury!!