Embed Size (px)

Citation preview

FOREWORD

The declaration of the G8 of May 2011 pertaining to the Arab Spring states in its first article: «The changes under way in the Middle East and North Africa (MENA) are historic and have the potential to open the door to the kind of transformation that occurred in Central and Eastern Europe after the fall of the Berlin Wall. The aspiration of people for freedom, human rights, democracy, job opportunities, empowerment and dignity, has led them to take control of their own destinies in a growing number of countries in the region. It resonates with and reinforces our common values ».

Indeed, the wind of change that will embrace the region in the months and years ahead will be momentous and far-reaching. Those countries that have engaged in democratic transitions must resolutely work out economic and social programs that will address the pressing challenges facing their young population viz. unemployment, poverty, and inequitable distribution of income. The expectations of their youth are high, and unless a level of prosperity, or at least anticipation thereof, is achieved the prospect for democratic transition and consolidation may be in jeopardy. In order to accelerate economic growth they must resolutely embark on ambitious investment programs particularly in the labour intensive sectors of the economy. They must also work out intelligent schemes to promote private initiatives and professionalize the business environment in their respec-tive markets. One of the virtues of democracy, if properly pursued, is that it promotes enhanced conditions for private entrepreneurship. In particular, Private Equity can and should play a crucial role in the MENA region as it contributes in the professionalization of the investment climate, the development of SMEs and the acceleration of job creation.

Bar a few exceptions Private Equity remains nascent in the MENA region. The industry remains, by and large, in its infancy throughout the region. The potential is therefore tremendous not only in the traditional areas of private equity such as venture, development or transmission capital but also in other segments of professional investments (e.g. Industry-specific investment funds).

The promotion of Private Equity in MENA will require setting up proper regulatory, legal, judicial and fiscal frameworks while enhancing human capital. It stands a better chance to prosper in those markets where stock exchanges are strong so as to facilitate the formulation and execution of exit strategies. With the right environment and support, private equity and venture capital can help facilitate a flourishing business environ-ment, and will also ultimately contribute in the emergence of a new generation of highly professional and motivated entrepreneurs in the country.

Jaloul AyedMinister of FinanceTunisia

REPORT STEERING COMMITEEAli Arab, Zawya »

Samer Sarraf, Amwal Al Khaleej »Purshotam Ramchandani, Abraaj Capital »Helmut Schuehsler, TVM Capital »Imad Ghandour, Cedar Bridge Partners »Karim Ben Salah, Swicorp »

SPECIAL THANKSSpecial thanks go to our sponsors. Without their support, the development of this report would not be possible.

REPORT SPONSORS:Abraaj Capital »Amwal AlKhaleej »Eastgate Capital Group »Global Capital Management »NBK Capital »Qatar First Investment Bank »Swicorp »Tuninvest »

KPMG Team: Zawya Team: Ali Arab and Lara Ghibril

Thomas SchellenBureau van Dijk: Paul Costers and Amy Morris

table of ContentS

01. iMpoRtant noticeBaSiS of pRepaRation1.1 DEfinitions & AssuMptions1.2 DAtA filtEring1.3

04

02. introDuctory MEssAgEs 07

03. privAtE Equity in thE MEnA rEgionsuMMAry3.1 funDs3.2

Funds raised to date3.2.1 Funds yet to be raised3.2.2 Total active funds3.2.3

inveStMentS3.3 Information limitations3.3.1

DEployMEnt of funDs3.4 rEgionAl focus3.5 sEctor focus3.6 exitS3.7

10

04. survEy of gps of thE MEnA rEgionintroDuction4.1 survEy rEsults4.2

Respondent profile4.2.1 Outlook4.2.2 Types of funds raised4.2.3 Regions and sectors of interest4.2.4 The impact of the financial crisis4.2.5

27

05. ABout thE MEnA privAtE EquityaSSociation

43

06. sponsor profilEs 4507. MEMBErs DirEctory 5608. privAtE Equity & vEnturE cApitAl firMs

in Mena58

impoRtant notiCe1

important notice annual Report

5

impoRtant notiCe1.1 BAsis of prEpArAtion

This report has been prepared based on data provided by the MENA Private Equity Association, and sourced from the Zawya Private Equity Monitor.

Historical data has been updated from that used in the 2009 GVCA report to include full year results for 2010 and to reflect increased disclosure of information in the market. KPMG member firms have not initiated any primary research in relation to this draft report and have not sought to establish or confirm the reliability of the data pro-vided by the MENA Private Equity Association and Zawya.

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is or will continue to be accurate. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

In analysing and determining the parameters of available data, it has been necessary to apply certain criteria, the most significant of which are as follows:

Private equity has been defined to include houses that have a General Partner / Limited Partner structure, »investment companies and quasi-governmental entities that are run by, and operate in the same way as, a private equity house.

Venture capital for the purpose of this report is defined as a fund specifically dedicated to venture capital »investments. This includes funds by Venture Capital Firms, and Venture Funds under Private Equity Firms. This Association is in the process of developing a definition to define Venture Capital in MENA. Accordingly, future references to Venture Capital may change.

Funds managed from MENA but whose focus is to invest solely outside the region are excluded from the fun- »draising and investment totals.

MENA includes Algeria, Bahrain, Egypt, Iraq, Jordan, Kuwait, Lebanon, Libya, Morocco, Oman, Palestine, Qa- »tar, Saudi Arabia, Sudan, Syria, Tunisia, UAE, and Yemen.

Investment size represents the total investment (both the debt and equity portions). However fund size only »considers equity invested, as we have no visibility on debt exposure by funds.

The fund raising totals are the amounts closed/committed for fund raising funds, closed funds, investing funds, »fully vested funds and liquidated funds.

Given the relative nascent state of the industry in MENA, exits have been defined to include partial exits, al- »though simple dilutions have not been included.

1

important notice annual Report

6

1.2 DEfinitions AnD AssuMptions

For analytical purposes, we have considered the following types of funds, as defined by Zawya’s Private Equity monitor:

Announced: » Official launch of funds which are yet to commence fund raising.Rumoured: » Funds expected to announce their intention to commence fund raising.fund raising: » Funds which have been announced and are in the process of raising capital.investing: » Funds which have closed and are actively seeking and/or making investments.fully vested: » Funds that have invested all capital raised. Some of the investments may have divested in this stage but not all.liquidation: » Funds which have divested all investments and have fulfilled all obligations to shareholders.

1.3 DAtA filtEring

The primary data sourced from Zawya has been filtered according to the definitions used in the Emerging Markets Private Equity Association (EMPEA) research methodology.

In particular we have used the following definitions:

Fund Size: In the case of funds yet to make a first close, or where no close information is available, fund size is equivalent to the target amount, and is noted as such. For funds achieving at least one official close, fund size is reported as the capital raised to date, while for funds that have made a final close, the fund size is the total capital raised. All amounts are reported in USD millions. Rumoured funds are excluded.

Currency: Where funds data has been provided in a currency other than USD, exchange rates applied are from the last day of the month in which each close is reported, e.g. first close reported in € on 15 April 2010 would be calculated using the exchange rate for 30 April 2010, taken from publicly available sources.

Funds of funds or secondaries are excluded.

Region: Statistics are based on the ‘market’ approach and funds are categorised based on the intended destination for investments (as defined in a fund’s announced mandate) as opposed to where the private equity firm is located. With regard to multi-region funds, we have included these to the extent that there is a focus on the MENA region. EMPEA methodology is to include only those multi-region funds whose primary intention is to invest in emerging markets. However, the source data does not provide visibility on primary geographic intention.

Funds established with a specific mandate to invest in real estate are excluded from the fundraising, investment and exit totals. The remaining real estate investments relate to funds with mixed investment mandates.

Conventional infrastructure funds, or funds investing directly in greenfield infrastructure projects (e.g. bridges, roads etc.) are excluded from fundraising totals. However, funds that make private equity investments (determined based on target returns) in companies operating in the infrastructure sector are included.

EMPEA does not track or report other alternative asset classes, including hedge funds, real estate funds and con-ventional infrastructure funds. In our analysis we have excluded data from investment-type companies, real estate firms and Sovereign Wealth Funds (SWFs have not been included in the current year analysis).

intRoduCtoRy meSSageS2

8

2

The region is increasing in its dynamism. Its youth have led over the past several months (mostly) positive and peaceful political changes that have radically transformed many countries in the region. The same energized youthful population is also taking control of their economic destiny as well with a surge in entrepreneurship, startups, and venture capital activity. The number of VC deals last year increased over the past two years, and continued growth in this area is expected.

Artificial regional boundaries are also starting to slowly fade away after decades of political fragmentation. Social connectivity and a realization of the need for unity are translating into political and business integration at both grass root and governmental levels. Since 2005, in the wake of the economic boom, increasing cross-border flow of labor, trade, and capital have brought many of the people in the region closer. And the recent political events have proved, beyond doubt, that such integration has progressed further than what most of us have realized: a political event Tunisia has snowballed across a region that shares similar values, challenges, and aspirations. The announcement of expanding the Gulf Cooperation Council to include Morocco and Jordan is another example of the materialization of regional integration.

The birth and evolution of the MENA Private Equity Association (MPEA) epitomize the positive shifts in the region. During its first year, it proved to be an active and constructive facilitator amongst industry participants. It was able to attract 21 members from across the region. It was also able to bridge the gap between the entrepreneurial venture capitalists and the sober private equiteers, allowing both factions to use it as a platform for their activi-ties. It was able to bring in service providers and engage them, without diluting its mission and membership base. It was constructed to be a loose association linked by technology without the rigidity of boards and committees.

These trends will have long-term positive impact on private equity activity. An enlarged common market inhab-ited by a more dynamic population means better investment opportunities. The private equity industry may be pausing to reflect on these changes of 2011. However, it is a pause to see how to clutch on the emerging opportu-nities whilst avoiding short-term risks.

The 2010 Annual Report Steering Committee:

Ali Arab, ZawyaFadi Arbid, Amwal AlKhaleejPurshotam Ramchandani, Abraaj Capital

Annual ReportIntroductory Message

INTRODUCTORY MESSAGE

Helmut Schuehsler, TVM CapitalImad Ghandour, Cedar Bridge PartnersKarim Ben Salah, Swicorp

annual Report

9

kpmg intRoduCtoRy meSSageKPMG is pleased to be associated with the MENA Private Equity Association in, once again, producing the annual report on the private equity and venture capital industries in the Middle Eastern and North African regions.Over the past two to three years, the private equity industry within the region has seen a significant transforma-tion. As a result of the global financial crisis, the industry has experienced a period of consolidation which saw the established funds - those which were able to leverage upon their reputation and proven track record - continue to invest and, in some cases, successfully raise capital in what has been a very challenging environment.

While deal activity continued to be relatively slow in 2010, the region’s private equity firms have continued to focus on their current portfolio in an effort to extract the most value - primarily though operational improvements, debt restructuring and working capital management. The feedback we have received from a number of practitioners in the region suggests that this has had a positive impact on the performance of their portfolio assets and should have a positive impact the eventual exit value.

While the industry in 2010 may not have recovered at the rate that was expected, there were signs that the industry within the MENA region may be on the road to recovery. For example, 2010 saw an increase in funds raised from $1.1 billion in 2009 to $1.3 billion indicating that investors continue to see considerable value in the region. Whilst we recognise the risks posed by the current unrest in some parts of the region, we as a firm remain positive about the longer-term prospects of the industry in MENA.

We would like to note that this report would not have been possible without the efforts of Zawya, the MENAPEA and the members of the Report Steering Committee. We are grateful to them for sharing primary data and industry insights, and we support the efforts of the newly branded Association in furthering the interests of Private Equity in this part of the world.

Dale GregoryPartnerTel: +971 (0) 4 403 0300; Email: [email protected]

kpmg introductory message

KPMG is a global network of professional firms operating in 150 countries with over 138,000 people working in member firms around the world. KPMG in the UAE was established in 1974 and has grown to 900 professional staff led by 30 Partners, across 8 offices in the country. We work closely with our colleagues in offices throughout the MENA region and across the world.

pRivate equity in the mena Region3

annual Report

11

pRivate equity in the mena Region3.1 suMMAry

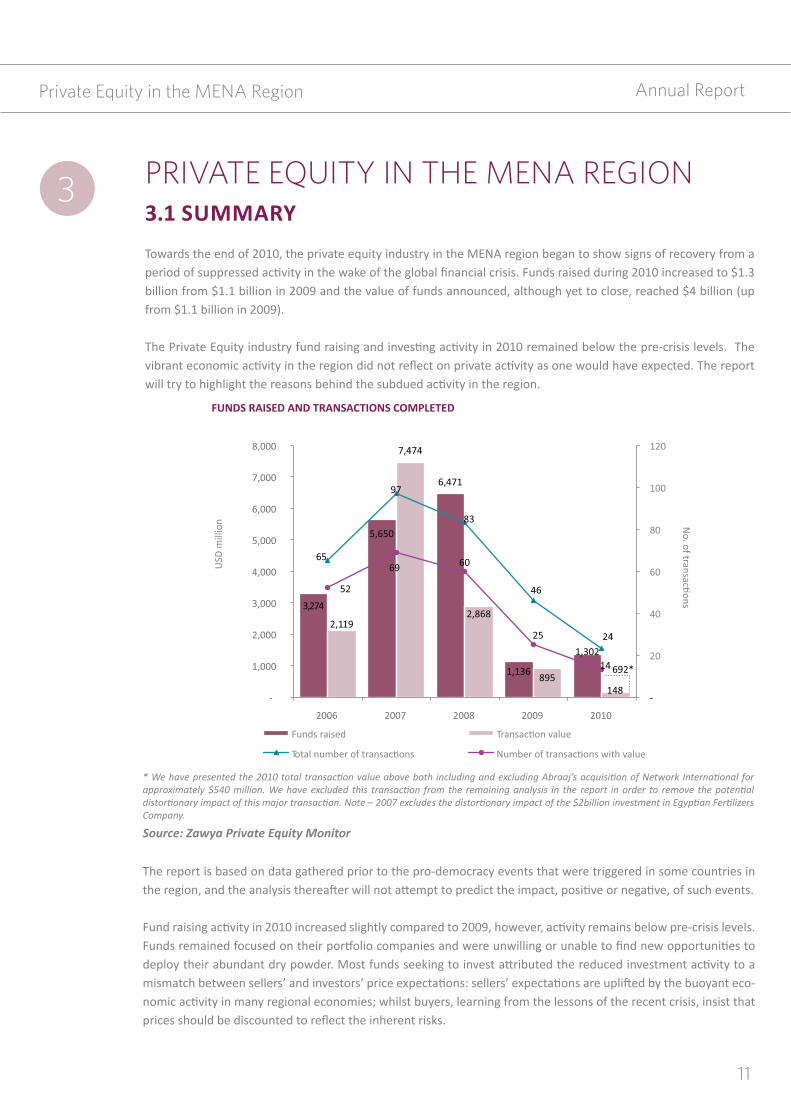

Towards the end of 2010, the private equity industry in the MENA region began to show signs of recovery from a period of suppressed activity in the wake of the global financial crisis. Funds raised during 2010 increased to $1.3 billion from $1.1 billion in 2009 and the value of funds announced, although yet to close, reached $4 billion (up from $1.1 billion in 2009). The Private Equity industry fund raising and investing activity in 2010 remained below the pre-crisis levels. The vibrant economic activity in the region did not reflect on private activity as one would have expected. The report will try to highlight the reasons behind the subdued activity in the region.

3

The report is based on data gathered prior to the pro-democracy events that were triggered in some countries in the region, and the analysis thereafter will not attempt to predict the impact, positive or negative, of such events.

Fund raising activity in 2010 increased slightly compared to 2009, however, activity remains below pre-crisis levels. Funds remained focused on their portfolio companies and were unwilling or unable to find new opportunities to deploy their abundant dry powder. Most funds seeking to invest attributed the reduced investment activity to a mismatch between sellers’ and investors’ price expectations: sellers’ expectations are uplifted by the buoyant eco-nomic activity in many regional economies; whilst buyers, learning from the lessons of the recent crisis, insist that prices should be discounted to reflect the inherent risks.

private equity in the mena Region

* We have presented the 2010 total transaction value above both including and excluding Abraaj’s acquisition of Network International for approximately $540 million. We have excluded this transaction from the remaining analysis in the report in order to remove the potential distortionary impact of this major transaction. Note – 2007 excludes the distortionary impact of the $2billion investment in Egyptian Fertilizers Company.

Source: Zawya Private Equity Monitor

annual Report

12

2010 also saw significant growth in the venture capital industry. Four separate venture or growth capital funds successfully raised $340 million (representing an increase from zero funds raised in 2009 and approximately $129 million in 2008). For the first time, the proportion to the total was significant: it represented 26 percent of the total funds raised and approximately 50 percent of investments completed.

As in previous years, the core regional economies of Saudi Arabia, Turkey, Egypt, and UAE were the destination of the majority of the investment. In response to the economic environment, fund managers have continued to focus on investing in defensive and non-cyclical sectors such as healthcare and power and utilities. In line with this trend, we are seeing more focused investment strategies adopted by some fund managers.

private equity in the mena Region

annual Report

13

3.2 funDs

3.2.1 funDs rAisED to DAtE

Raising capital continued to be a challenge for fund managers in 2010. However, 2010 did see a marginal increase in total value of funds raised from $1.1 billion in 2009 to $1.3 billion, suggesting that the tide may have turned and confidence may be returning to the investor community.

2010 saw eight funds successfully raise capital totaling $1.3 billion. In contrast to the industry peak in 2007 and 2008, the comparatively low number of funds successfully raising capital means the region has become a less com-petitive environment for fund managers and potential investors. This is also mirrored in the investment arena with the general feedback received from fund managers suggesting a significant increase in the portion of proprietary transactions and less reliance on auctions.

Source: Zawya Private Equity Monitor

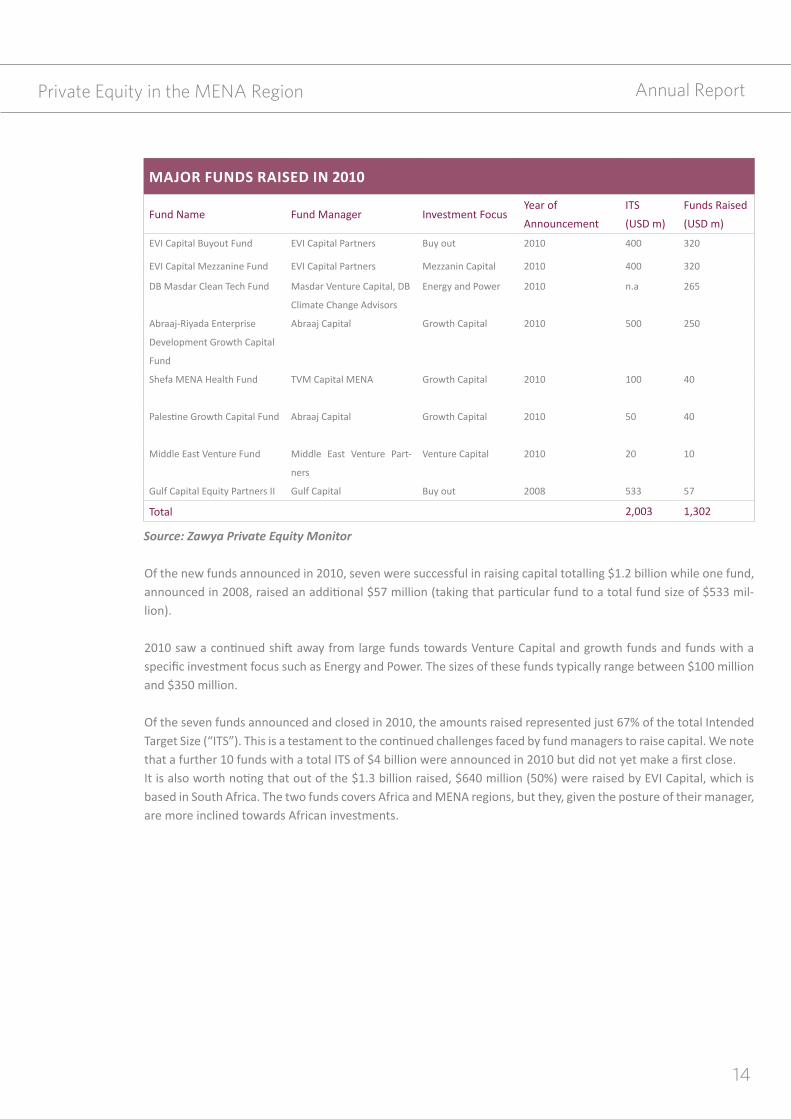

Cumulative funds under management grew to $22.3 billion in 2010. The table following details which funds successfully raised capital during 2010.

Source: Zawya Private Equity Monitor

private equity in the mena Region

Annual Report

14

MAJOR FUNDS RAISED IN 2010

Fund Name Fund Manager Investment FocusYear of

Announcement

ITS

(USD m)

Funds Raised

(USD m)

EVI Capital Buyout Fund EVI Capital Partners Buy out 2010 400 320

EVI Capital Mezzanine Fund EVI Capital Partners Mezzanin Capital 2010 400 320

DB Masdar Clean Tech Fund Masdar Venture Capital, DB

Climate Change Advisors

Energy and Power 2010 n.a 265

Abraaj-Riyada Enterprise

Development Growth Capital

Fund

Abraaj Capital Growth Capital 2010 500 250

Shefa MENA Health Fund TVM Capital MENA Growth Capital 2010 100 40

Abraaj Capital Growth Capital 2010 50 40

Middle East Venture Fund Middle East Venture Part-

ners

Venture Capital 2010 20 10

Gulf Capital Equity Partners II Gulf Capital Buy out 2008 533 57

Total 2,003 1,302

Of the new funds announced in 2010, seven were successful in raising capital totalling $1.2 billion while one fund, -

lion).

specific investment focus such as Energy and Power. The sizes of these funds typically range between $100 million and $350 million.

Of the seven funds announced and closed in 2010, the amounts raised represented just 67% of the total Intended

that a further 10 funds with a total ITS of $4 billion were announced in 2010 but did not yet make a first close.

based in South Africa. The two funds covers Africa and MENA regions, but they, given the posture of their manager, are more inclined towards African investments.

Source: Zawya Private Equity Monitor

Private Equity in the MENA Region

annual Report

15

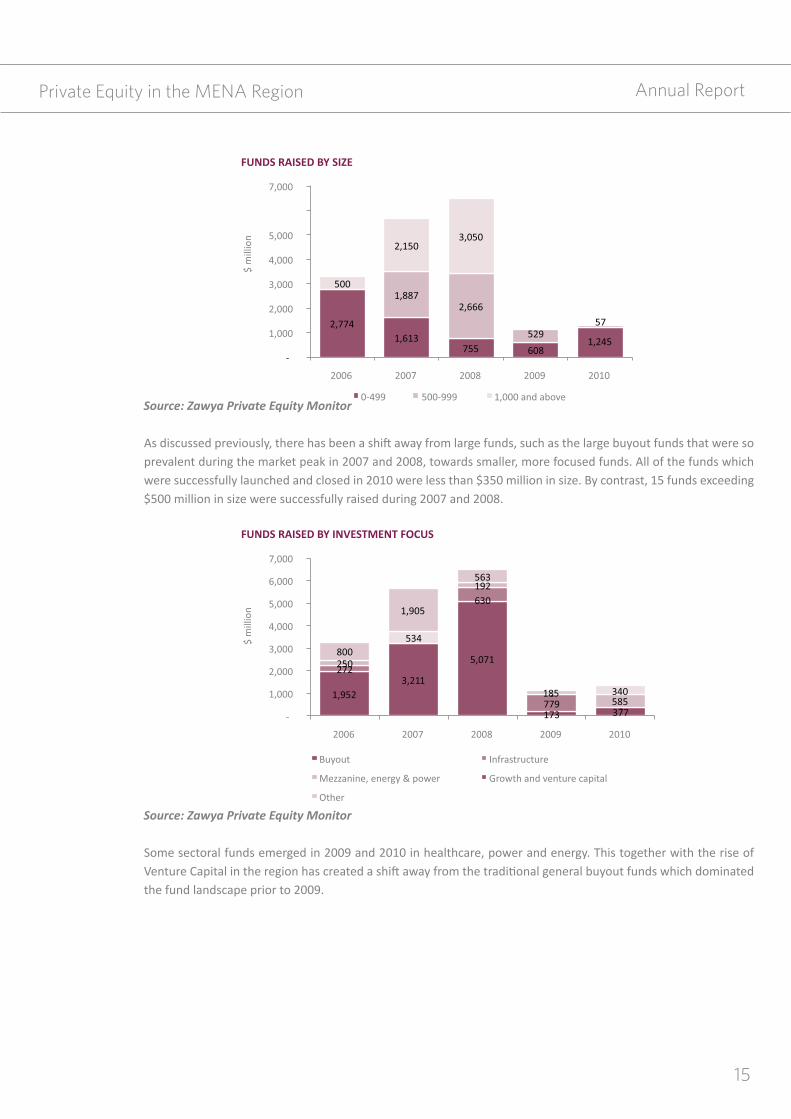

As discussed previously, there has been a shift away from large funds, such as the large buyout funds that were so prevalent during the market peak in 2007 and 2008, towards smaller, more focused funds. All of the funds which were successfully launched and closed in 2010 were less than $350 million in size. By contrast, 15 funds exceeding $500 million in size were successfully raised during 2007 and 2008.

Source: Zawya Private Equity Monitor

Source: Zawya Private Equity Monitor

Some sectoral funds emerged in 2009 and 2010 in healthcare, power and energy. This together with the rise of Venture Capital in the region has created a shift away from the traditional general buyout funds which dominated the fund landscape prior to 2009.

private equity in the mena Region

16

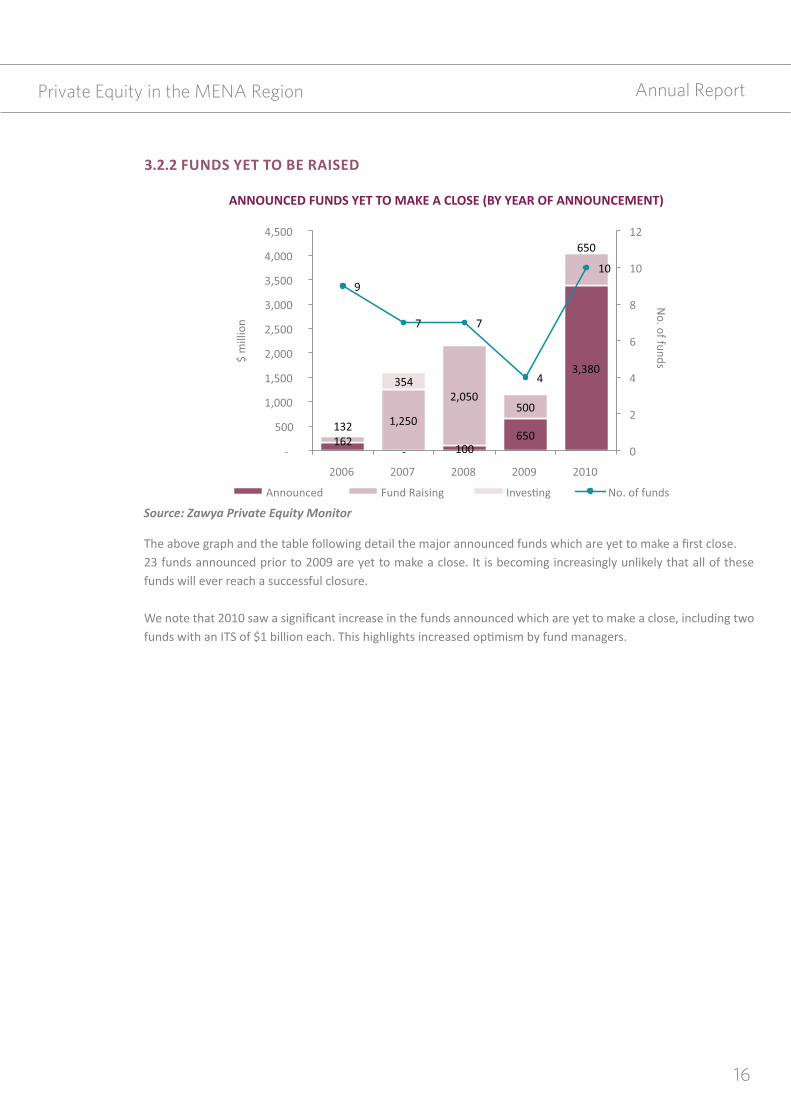

3.2.2 FUNDS YET TO BE RAISED

The above graph and the table following detail the major announced funds which are yet to make a first close.23 funds announced prior to 2009 are yet to make a close. It is becoming increasingly unlikely that all of these funds will ever reach a successful closure.

We note that 2010 saw a significant increase in the funds announced which are yet to make a close, including two

Source: Zawya Private Equity Monitor

Annual ReportPrivate Equity in the MENA Region

annual Report

17

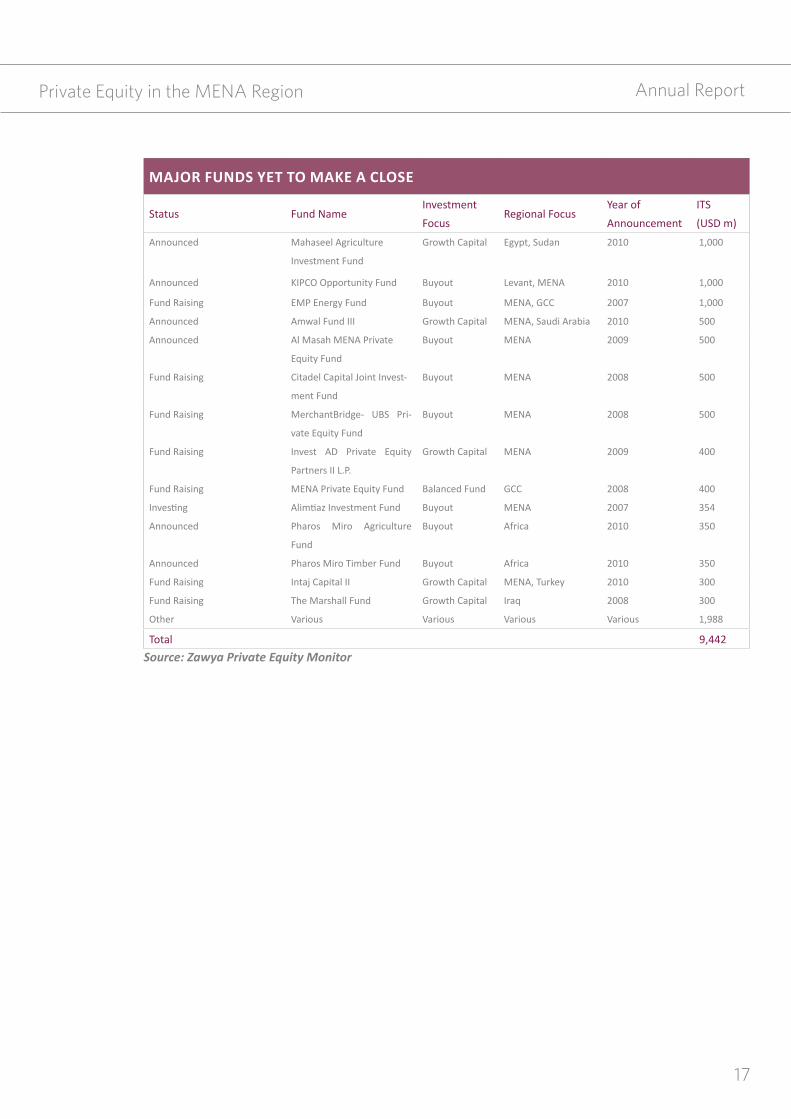

MAjor funDs yEt to MAkE A closE

Status Fund NameInvestment

FocusRegional Focus

Year of

Announcement

ITS

(USD m)

Announced Mahaseel Agriculture

Investment Fund

Growth Capital Egypt, Sudan 2010 1,000

Announced KIPCO Opportunity Fund Buyout Levant, MENA 2010 1,000

Fund Raising EMP Energy Fund Buyout MENA, GCC 2007 1,000

Announced Amwal Fund III Growth Capital MENA, Saudi Arabia 2010 500

Announced Al Masah MENA Private

Equity Fund

Buyout MENA 2009 500

Fund Raising Citadel Capital Joint Invest-

ment Fund

Buyout MENA 2008 500

Fund Raising MerchantBridge- UBS Pri-

vate Equity Fund

Buyout MENA 2008 500

Fund Raising Invest AD Private Equity

Partners II L.P.

Growth Capital MENA 2009 400

Fund Raising MENA Private Equity Fund Balanced Fund GCC 2008 400

Investing Alimtiaz Investment Fund Buyout MENA 2007 354

Announced Pharos Miro Agriculture

Fund

Buyout Africa 2010 350

Announced Pharos Miro Timber Fund Buyout Africa 2010 350

Fund Raising Intaj Capital II Growth Capital MENA, Turkey 2010 300

Fund Raising The Marshall Fund Growth Capital Iraq 2008 300

Other Various Various Various Various 1,988

Total 9,442

Source: Zawya Private Equity Monitor

private equity in the mena Region

annual Report

18

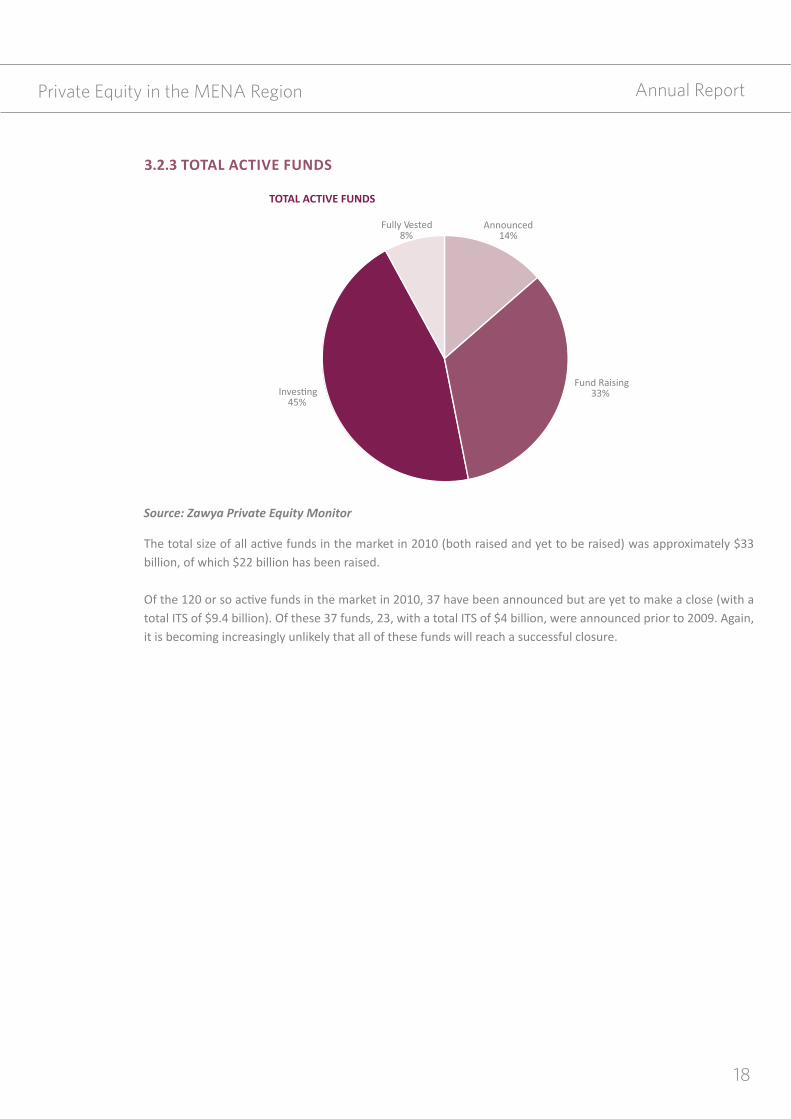

3.2.3 totAl ActivE funDs

The total size of all active funds in the market in 2010 (both raised and yet to be raised) was approximately $33 billion, of which $22 billion has been raised.

Of the 120 or so active funds in the market in 2010, 37 have been announced but are yet to make a close (with a total ITS of $9.4 billion). Of these 37 funds, 23, with a total ITS of $4 billion, were announced prior to 2009. Again, it is becoming increasingly unlikely that all of these funds will reach a successful closure.

Source: Zawya Private Equity Monitor

private equity in the mena Region

Annual Report

19

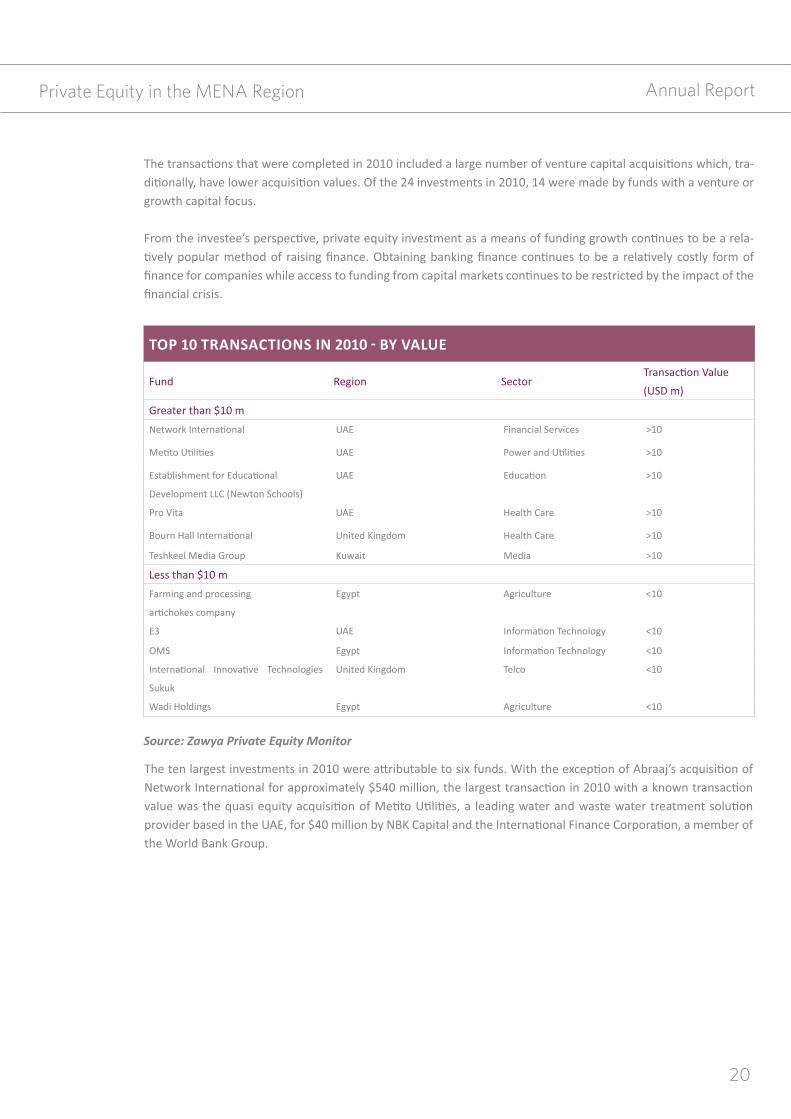

3.3 INVESTMENTS

3.3.1 INFORMATION LIMITATIONS

Furthermore, in some cases where investments are publically announced, private equity houses have not revealed

for analysis purposes based on available market intelligence.

the fund.

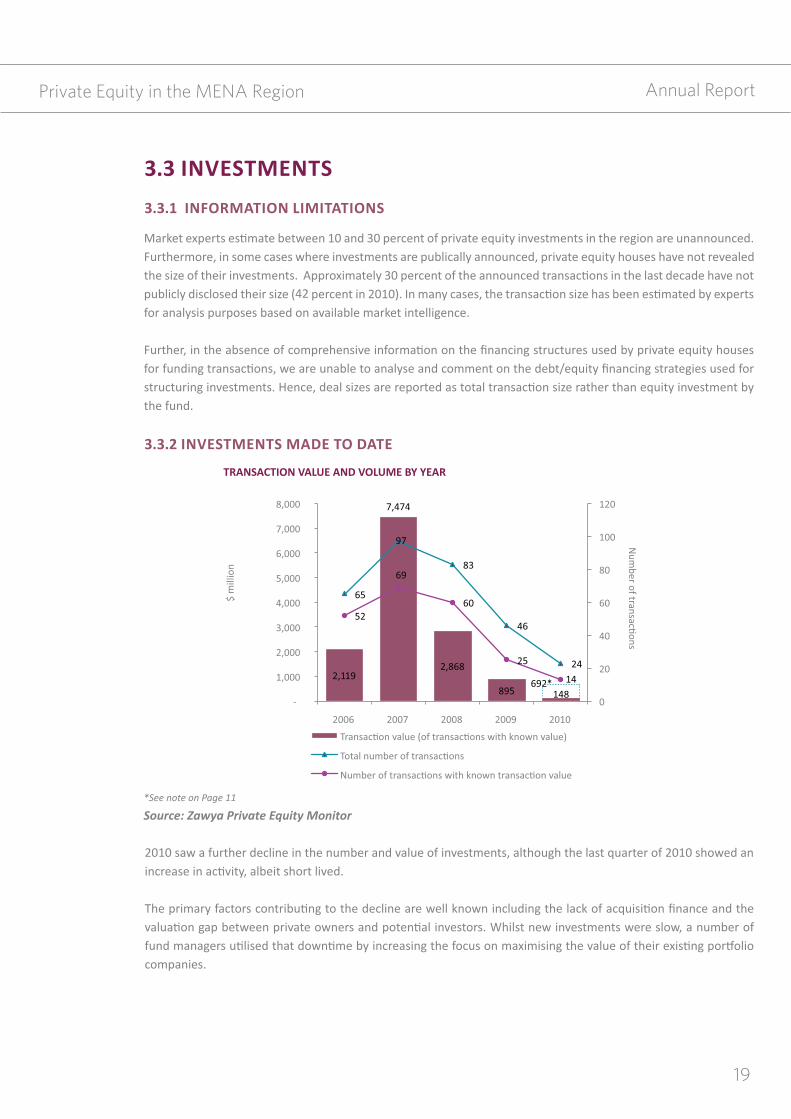

2010 saw a further decline in the number and value of investments, although the last quarter of 2010 showed an

companies.

*See note on Page 11

Source: Zawya Private Equity Monitor

3.3.2 INVESTMENTS MADE TO DATE

Private Equity in the MENA Region

42

20

-

growth capital focus.

-

financial crisis.

Source: Zawya Private Equity Monitor

TOP 10 TRANSA BY VALUE

Fund Region Sector(USD m)

Greater than $10 m

UAE Financial Services >10

UAE >10

Development LLC (Newton Schools)

UAE >10

Pro Vita UAE Health Care >10

United Kingdom Health Care >10

Teshkeel Media Group Kuwait Media >10

Less than $10 m

Farming and processing Egypt Agriculture <10

E3 UAE <10

OMS Egypt <10

Sukuk

United Kingdom Telco <10

Wadi Holdings Egypt Agriculture <10

the World Bank Group.

Annual ReportPrivate Equity in the MENA Region

21

Annual ReportPrivate Equity in the MENA Region

The average size of an investment continued to decline in 2010 to $11 million from $36 million in 2009. Of the known transaction values, the vast majority were less than $20 million.

While limited access to and the increased cost of financial leverage continues to restrict the ability of funds to complete large transactions, the private equity industry is showing an increasing appetite for investing into SMEs and venture capital businesses.

22

3.4 DEPLOYMENT OF FUNDS

» »

widen the gap further. »

life of the fund. »

Source: Zawya Private Equity Monitor

When analysing the level of deployed funds in the MENA region, it is important to reiterate that a significant por-

We also note that the level of available funds largely depends on the fund managers’ ability to call on the amount of funds raised. Nevertheless, it appears as though the fund raising cycle is running well ahead of the deployment

have grown to several billion dollars since 2006.)

Annual ReportPrivate Equity in the MENA Region

23

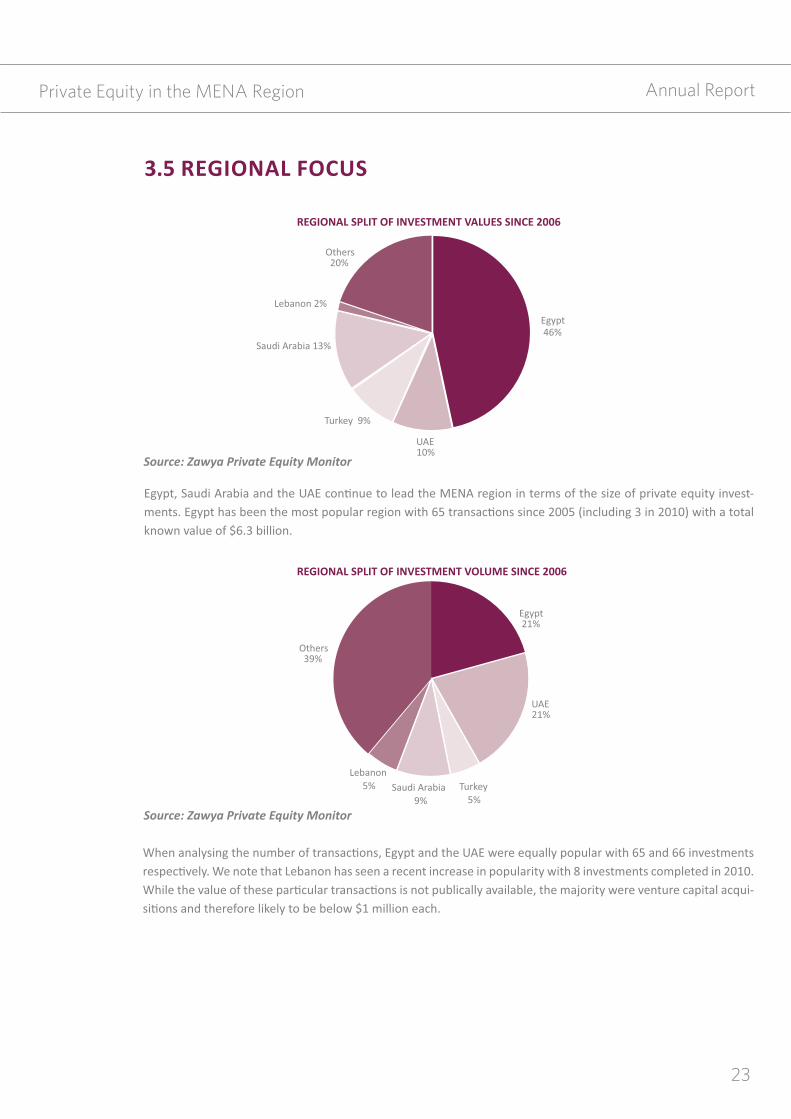

3.5 REGIONAL FOCUS

-

known value of $6.3 billion.

Source: Zawya Private Equity Monitor

Source: Zawya Private Equity Monitor

-

Annual ReportPrivate Equity in the MENA Region

46%

annual Report

24

Source: Zawya Private Equity Monitor

Turkey, in line with Egypt, enjoys the benefits of a large and fast-growing population, strong local demand, and proven resilience to the global financial crisis. However, political uncertainty around the region continues to have a short-term negative impact on investor sentiment.

While the portion of investments in Saudi Arabia increased year on year from 2007 to 2009, only one private eq-uity transaction was completed in the country in 2010. However, given the size of the economy in Saudi Arabia (the largest economy in terms of GDP in the Middle East), the country is expected to benefit from relatively significant private equity investment in the years to come.

The UAE continues to be a popular destination for fund managers and, given the size and dynamic nature of the economy, it is expected to remain amongst the top destinations for years to come.

3.6 sEctor focus

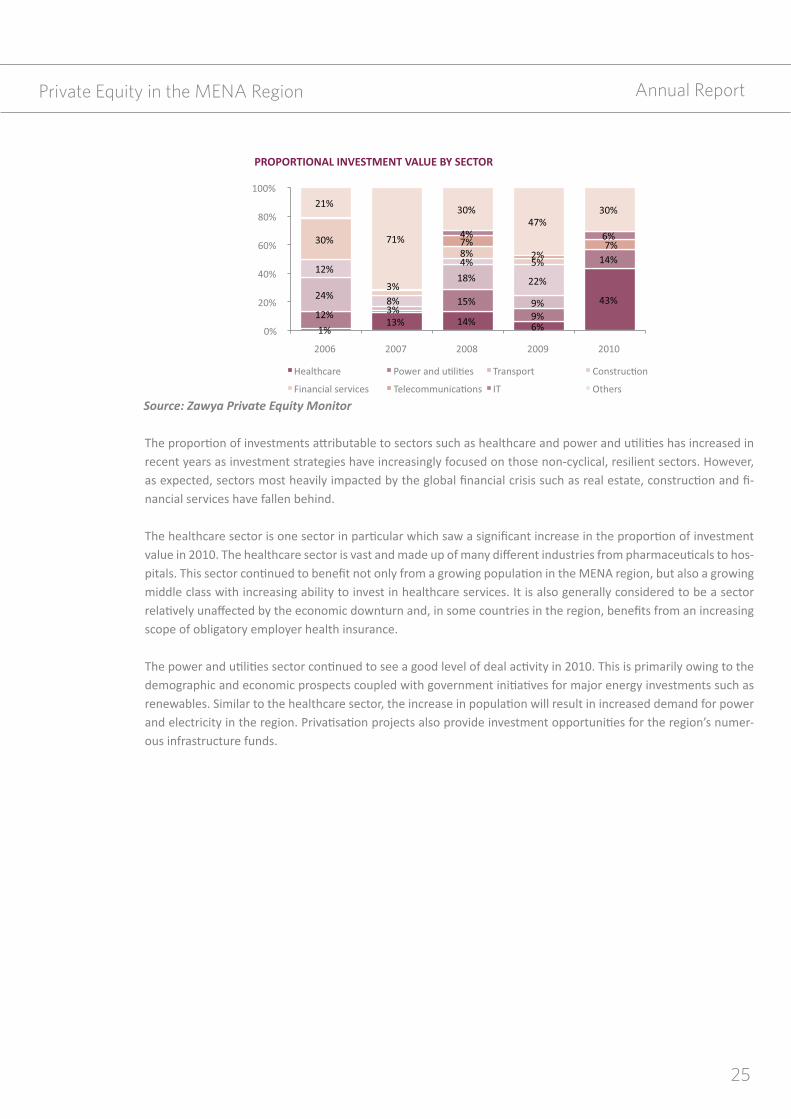

Source: Zawya Private Equity Monitor

Based on investment value, the most attractive sectors in 2010 were the healthcare and power and utilities sectors which collectively accounted for 57% of the total transaction value ($84 million of the total $148 million).

private equity in the mena Region

annual Report

25

Source: Zawya Private Equity Monitor

The proportion of investments attributable to sectors such as healthcare and power and utilities has increased in recent years as investment strategies have increasingly focused on those non-cyclical, resilient sectors. However, as expected, sectors most heavily impacted by the global financial crisis such as real estate, construction and fi-nancial services have fallen behind.

The healthcare sector is one sector in particular which saw a significant increase in the proportion of investment value in 2010. The healthcare sector is vast and made up of many different industries from pharmaceuticals to hos-pitals. This sector continued to benefit not only from a growing population in the MENA region, but also a growing middle class with increasing ability to invest in healthcare services. It is also generally considered to be a sector relatively unaffected by the economic downturn and, in some countries in the region, benefits from an increasing scope of obligatory employer health insurance.

The power and utilities sector continued to see a good level of deal activity in 2010. This is primarily owing to the demographic and economic prospects coupled with government initiatives for major energy investments such as renewables. Similar to the healthcare sector, the increase in population will result in increased demand for power and electricity in the region. Privatisation projects also provide investment opportunities for the region’s numer-ous infrastructure funds.

private equity in the mena Region

annual Report

26

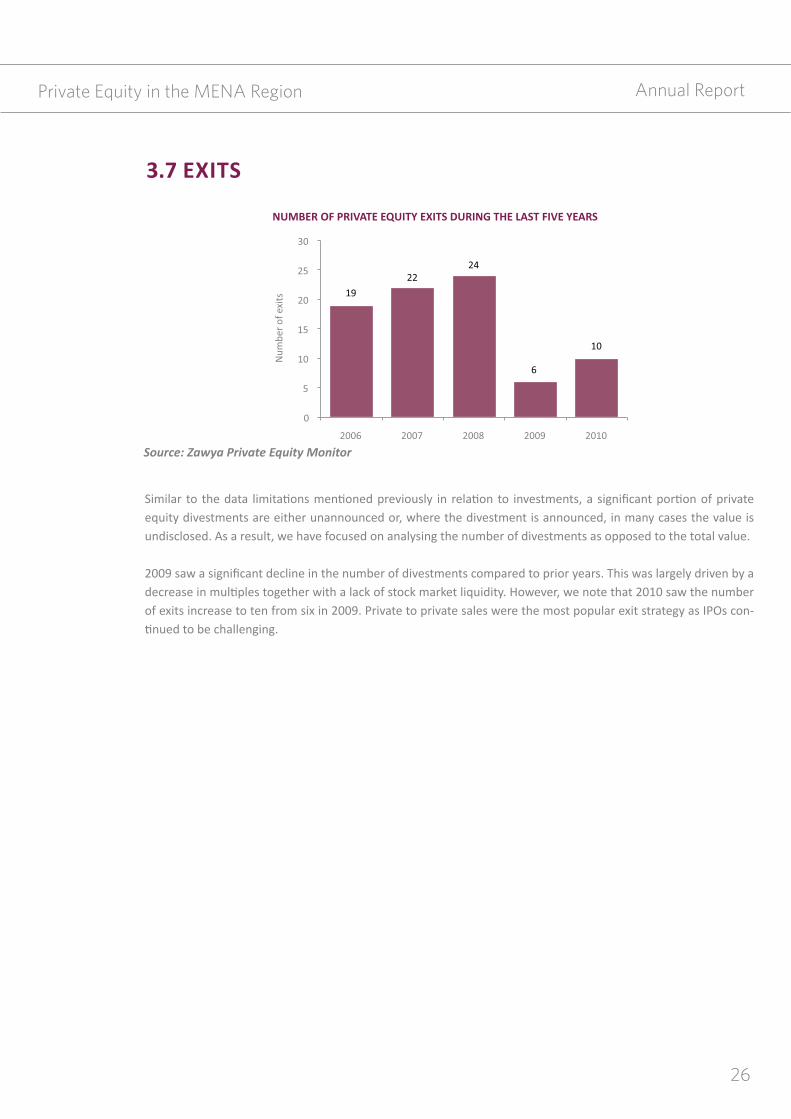

Source: Zawya Private Equity Monitor

Similar to the data limitations mentioned previously in relation to investments, a significant portion of private equity divestments are either unannounced or, where the divestment is announced, in many cases the value is undisclosed. As a result, we have focused on analysing the number of divestments as opposed to the total value.

2009 saw a significant decline in the number of divestments compared to prior years. This was largely driven by a decrease in multiples together with a lack of stock market liquidity. However, we note that 2010 saw the number of exits increase to ten from six in 2009. Private to private sales were the most popular exit strategy as IPOs con-tinued to be challenging.

3.7 Exits

private equity in the mena Region

SuRvey of gpS of the mena Region4

Annual Report

28

SURVEY OF GPS OF THE MENA REGION4.1 INTRODUCTION

first quarter of 2011 with the aim of obtaining a greater understanding of the private equity environment in the

-parisons are made for previous years, these comparisons refer to earlier GVCA surveys.

METHODOLOGY

MENA region (including the top 10 PE houses based on funds under management). The firms surveyed have invest-ments in a breadth of industries with a wide geographical reach.

SCOPE OF THE SURVEY

and outlook for 2011.

PROFILE OF THE RESPONDENTSThe majority of the respondents established their private equity firms within the last five years with approximately

percent of responding firms have less than $500 million worth of assets under management.

FUTURE OUTLOOK

managers in the region.

Consistent with what is seen in the 2010 data when the average size of funds raised was approximately $160 mil-lion, 71 percent of the respondents believe that the average size of the funds raised in 2011 will be less than $250 million. Many respondents believe that the notable resurgence in growth capital and increased focus on venture

areas of focus will prove to be the most popular.

5

Survey of GPS of the MENA Region

54

annual Report

29

4.2 survEy rEsults

4.2.1 rEsponDEnt profilE

When was the company Established?

Of the 25 private equity firms in the MENA region who took part in the survey, six were established in the last two years (with 16 established in the last 5 years). This reflects the nascent nature of the industry in the region compared to more developed markets such as the US and European markets. It is interesting that three of the respondents were set up in the last year, despite the challenging environment.

Who owns the fund management company?

Of the respondents, 71 percent stated that management hold, at least, some ownership in the fund management company with 38% majority owned by management.

Survey of gpS of the mena Region

annual Report

30

how many funds have you managed since establishment?

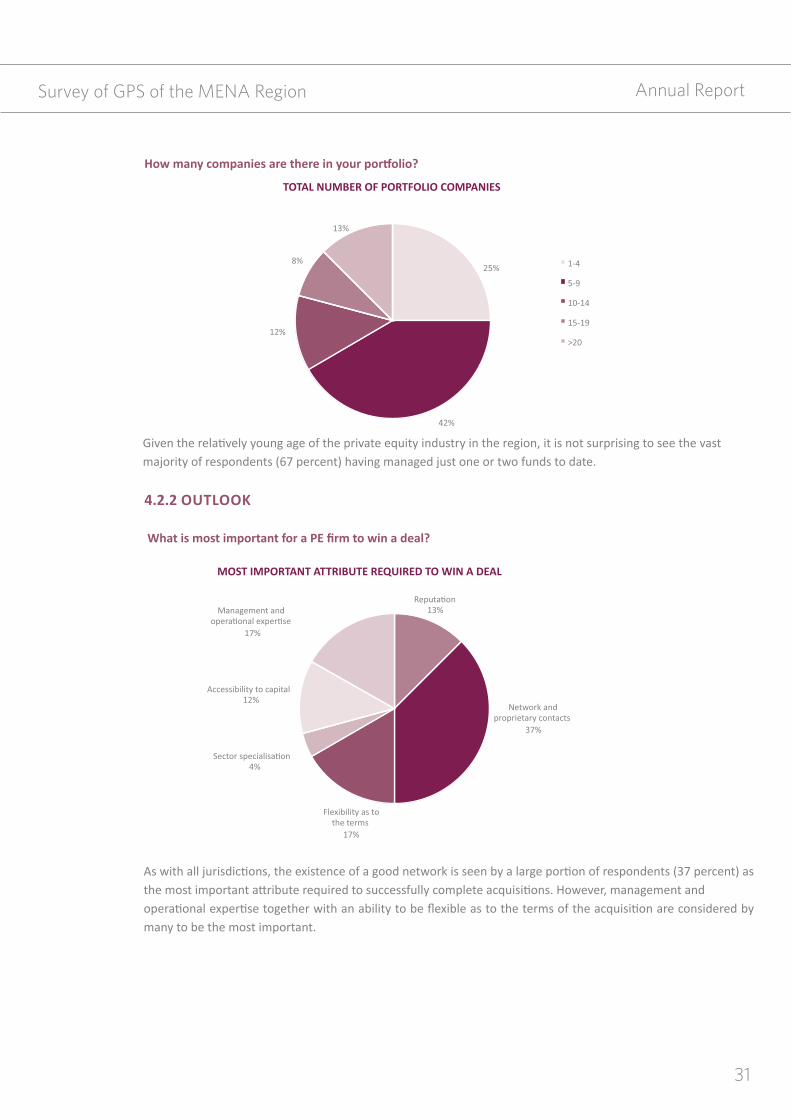

Given the relatively young age of the private equity industry in the region, it is not surprising to see the vast major-ity of respondents (67 percent) having managed just one or two funds to date.

54 percent of responding firms have less than $500 million worth of assets under management.

What is the total value of assets under management?

Survey of gpS of the mena Region

annual Report

31

how many companies are there in your portfolio?

Given the relatively young age of the private equity industry in the region, it is not surprising to see the vast majority of respondents (67 percent) having managed just one or two funds to date.

4.2.2 outlook

What is most important for a pE firm to win a deal?

As with all jurisdictions, the existence of a good network is seen by a large portion of respondents (37 percent) as the most important attribute required to successfully complete acquisitions. However, management and operational expertise together with an ability to be flexible as to the terms of the acquisition are considered by many to be the most important.

Survey of gpS of the mena Region

annual Report

32

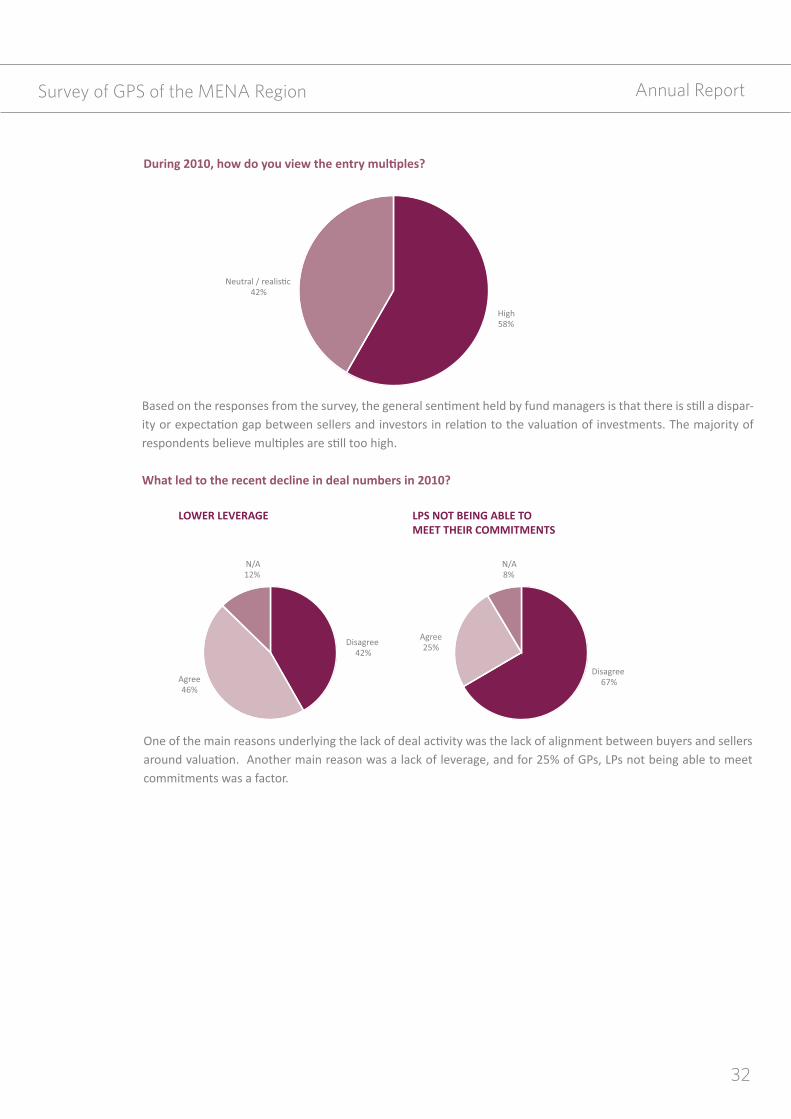

During 2010, how do you view the entry multiples?

Based on the responses from the survey, the general sentiment held by fund managers is that there is still a dispar-ity or expectation gap between sellers and investors in relation to the valuation of investments. The majority of respondents believe multiples are still too high.

Survey of gpS of the mena Region

What led to the recent decline in deal numbers in 2010?

One of the main reasons underlying the lack of deal activity was the lack of alignment between buyers and sellers around valuation. Another main reason was a lack of leverage, and for 25% of GPs, LPs not being able to meet commitments was a factor.

annual Report

33

pArticipAnts WErE AskED to ExprEss thEir opinion ABout thE futurE of privAtE Equity in thE MEnA rEgion.

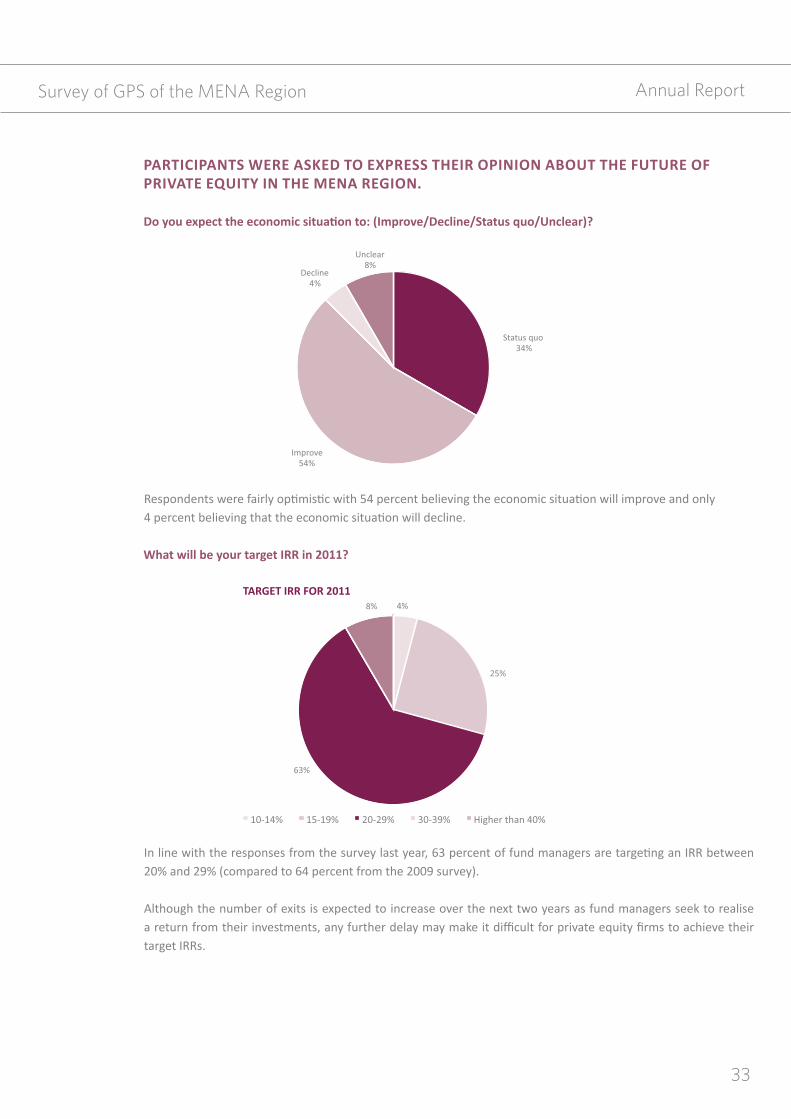

Do you expect the economic situation to: (improve/Decline/status quo/unclear)?

Respondents were fairly optimistic with 54 percent believing the economic situation will improve and only 4 percent believing that the economic situation will decline.

What will be your target irr in 2011?

In line with the responses from the survey last year, 63 percent of fund managers are targeting an IRR between 20% and 29% (compared to 64 percent from the 2009 survey).

Although the number of exits is expected to increase over the next two years as fund managers seek to realise a return from their investments, any further delay may make it difficult for private equity firms to achieve their target IRRs.

Survey of gpS of the mena Region

annual Report

34

What will be the most attractive exit routes during 2011?

While IPOs continue to be seen as challenging, trade sales are considered to be the most attractive exit strategy according to 75 percent of respondents (an increase from 64 percent of respondents in our last survey). It is in-teresting to note that just 13 percent of respondents believe that sales to other private equity firms will be the most attractive exit option in 2011, suggesting that the secondary market is still not as developed as it is in other regions.

Survey of gpS of the mena Region

annual Report

35

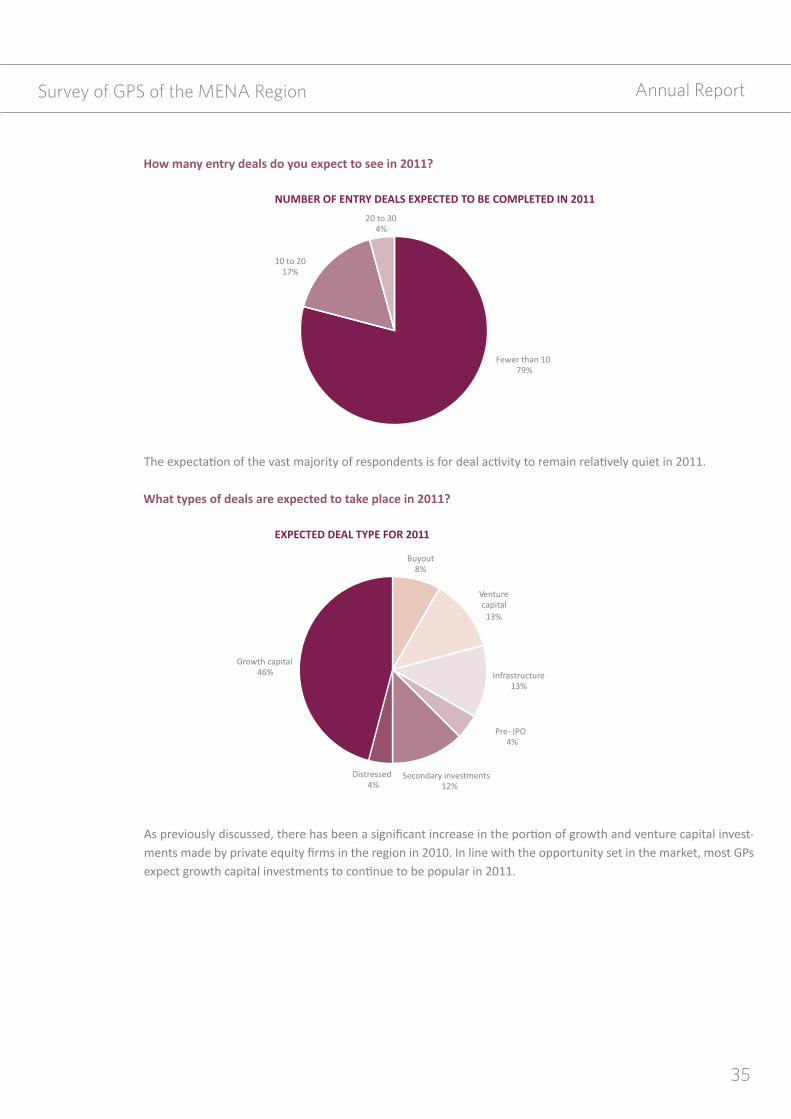

how many entry deals do you expect to see in 2011?

The expectation of the vast majority of respondents is for deal activity to remain relatively quiet in 2011.

What types of deals are expected to take place in 2011?

As previously discussed, there has been a significant increase in the portion of growth and venture capital invest-ments made by private equity firms in the region in 2010. In line with the opportunity set in the market, most GPs expect growth capital investments to continue to be popular in 2011.

Survey of gpS of the mena Region

annual Report

36

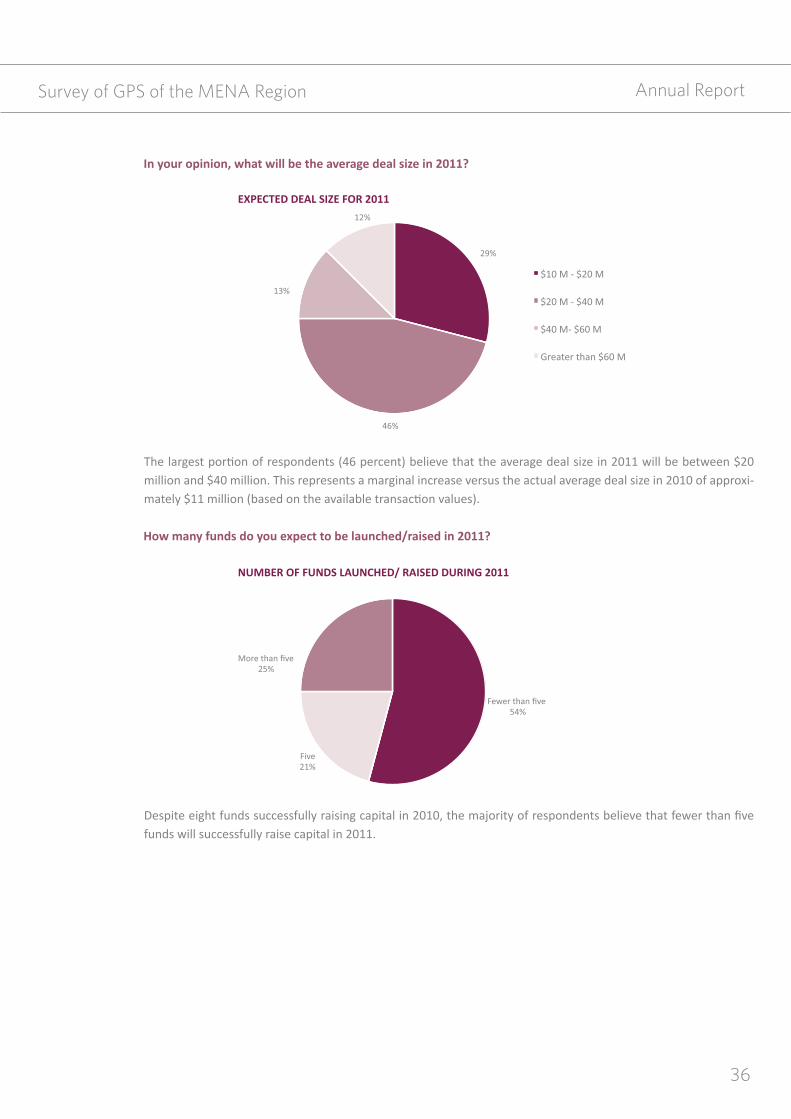

in your opinion, what will be the average deal size in 2011?

The largest portion of respondents (46 percent) believe that the average deal size in 2011 will be between $20 million and $40 million. This represents a marginal increase versus the actual average deal size in 2010 of approxi-mately $11 million (based on the available transaction values).

how many funds do you expect to be launched/raised in 2011?

Despite eight funds successfully raising capital in 2010, the majority of respondents believe that fewer than five funds will successfully raise capital in 2011.

Survey of gpS of the mena Region

annual Report

37

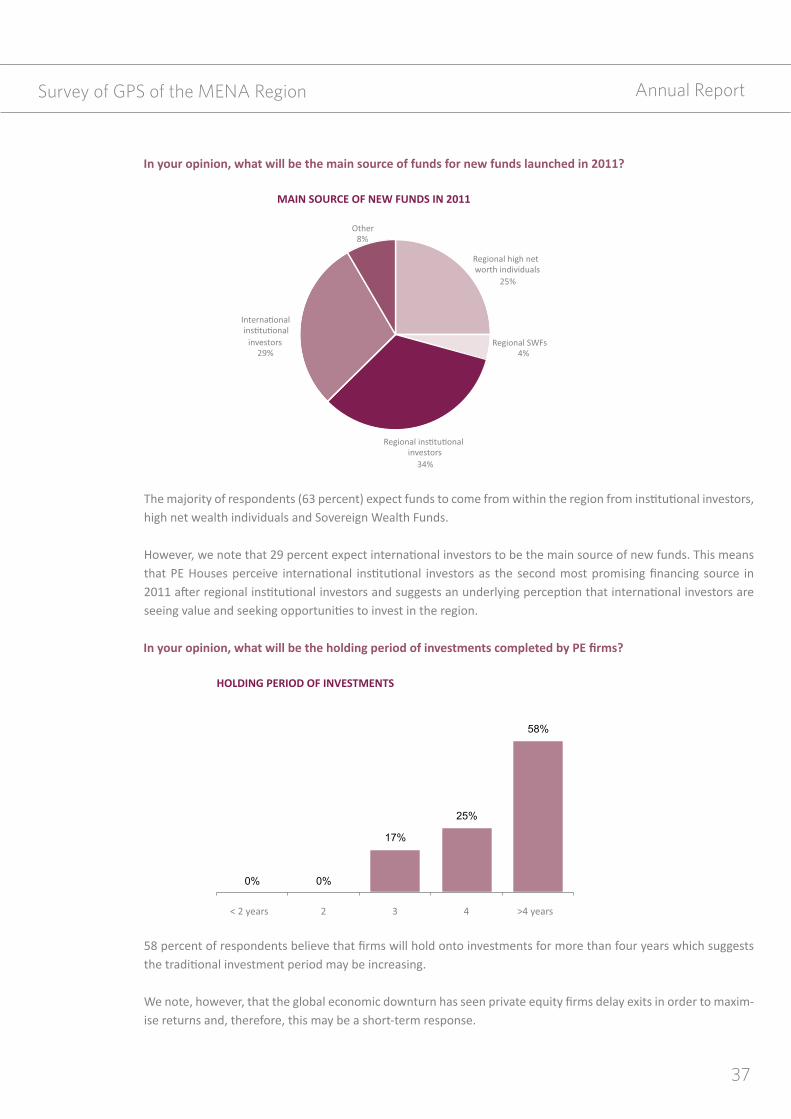

in your opinion, what will be the main source of funds for new funds launched in 2011?

The majority of respondents (63 percent) expect funds to come from within the region from institutional investors, high net wealth individuals and Sovereign Wealth Funds.

However, we note that 29 percent expect international investors to be the main source of new funds. This means that PE Houses perceive international institutional investors as the second most promising financing source in 2011 after regional institutional investors and suggests an underlying perception that international investors are seeing value and seeking opportunities to invest in the region.

in your opinion, what will be the holding period of investments completed by pE firms?

58 percent of respondents believe that firms will hold onto investments for more than four years which suggests the traditional investment period may be increasing.

We note, however, that the global economic downturn has seen private equity firms delay exits in order to maxim-ise returns and, therefore, this may be a short-term response.

Survey of gpS of the mena Region

annual Report

38

how many exit deals do you expect in 2011?

Half of the respondents believe that deal activity will continue to be slow with fewer than five exits expected in 2011.

in 2011…

While 75 percent of respondents express their confidence that LPs will be able to meet their expectations in 2011, this is despite an expectation that deal values will not come down.

Survey of gpS of the mena Region

annual Report

39

What are the main challenges in 2011 for MEnA private Equity industry?

40 percent of respondents believe that at lack of quality investment opportunities and the prevalence of high valu-ations will be the major challenges to the industry in the MENA region.

What is the most important role of pE firms in their portfolio companies?

PE firms themselves see it as their most important roles to provide both operational and strategic planning ad-vice and support to their portfolio companies. This is a departure from the 2009 survey in which 32 percent of respondents named providing financial advice and support as the most important role.

Survey of gpS of the mena Region

annual Report

40

in 2011…

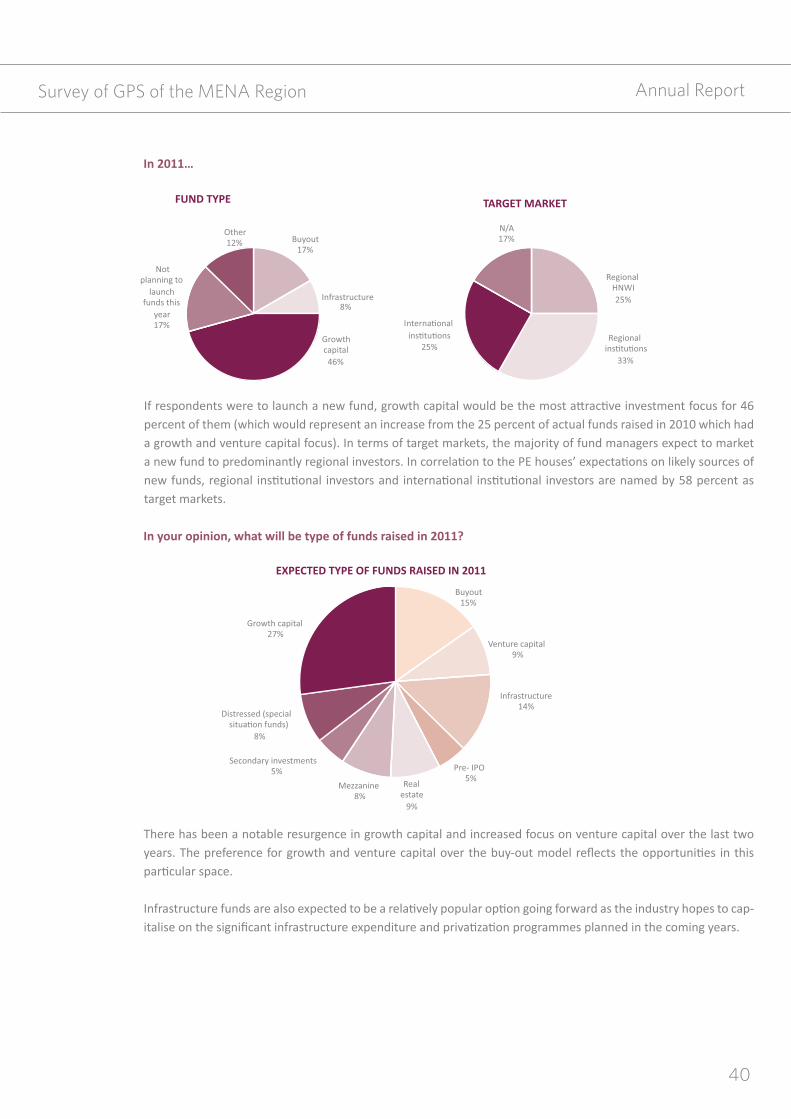

If respondents were to launch a new fund, growth capital would be the most attractive investment focus for 46 percent of them (which would represent an increase from the 25 percent of actual funds raised in 2010 which had a growth and venture capital focus). In terms of target markets, the majority of fund managers expect to market a new fund to predominantly regional investors. In correlation to the PE houses’ expectations on likely sources of new funds, regional institutional investors and international institutional investors are named by 58 percent as target markets.

in your opinion, what will be type of funds raised in 2011?

There has been a notable resurgence in growth capital and increased focus on venture capital over the last two years. The preference for growth and venture capital over the buy-out model reflects the opportunities in this particular space. Infrastructure funds are also expected to be a relatively popular option going forward as the industry hopes to cap-italise on the significant infrastructure expenditure and privatization programmes planned in the coming years.

Survey of gpS of the mena Region

annual Report

41

4.2.4 rEgions AnD sEctors of intErEst

The GCC, Jordan, Egypt and North Africa are specific regions of focus for the respondents going forward. Reasons frequently cited for PE investor interest in those markets include the large population growth, growing middle class and the level of anticipated government spending. However, we note that the survey was completed prior to the recent developments in the political situation in the region and therefore may not necessarily capture the current sentiment of investors.

We also note that Lebanon saw an increase in deal activity in 2010 and, according to the respondents to the sur-vey, remains an attractive market going forward.

The focus in 2010 was clearly on defensive sectors such as healthcare which are seen to offer non-cyclical low risk income streams. From the responses to our survey, this focus on defensive sectors continues to be a popular investment strategy going forward.

Survey of gpS of the mena Region

annual Report

42

4.2.5 thE iMpAct of thE finAnciAl crisis

how did the economic turmoil affect your portfolio companies?

While it is expected that margins, sales and profits would be impacted by the global recession, it is interesting that approximately one quarter of respondents said that the economic downturn had no effect on their portfolio companies.

We do note, however, that a number of responding fund managers have had to reassess their strategies with 13 percent of respondents having delayed or cancelled new expansion or investment plans and 8 percent having delayed IPOs.

Survey of gpS of the mena Region

about the mena pRivate equity aSSoCiation

5

annual Report

44

mena pRivate equity aSSoCiation

The MENA Private Equity Association is a non-profit entity committed to supporting and developing the private equity and venture capital industry in the Middle East and North Africa.

The Association aims to foster greater communication within the region’s private equity and venture capital net-work and facilitate knowledge sharing in order to encourage overall economic growth, and will actively promote the industry’s successes to local stakeholders and build trust with investors, regulators and the public regionally and internationally.

www.menapea.com

about the mena private equity association

SponSoR pRofileS6

annual Report

46

Zawya

Over 800,000 professionals from around the world, rely on Zawya to find and connect to the right investment opportunities in the Middle East and North Africa region. Backed by our team of in-house private equity and sovereign wealth fund analysts, Zawya’s PE solutions let you shape the right private equity strategy and stay ahead of regional SWF developments. Our comprehensive range of solutions provides a wide variety of unique online content, features and tools, including:

• Zawya’s Private Equity Monitor, which empowers PE professionals with the most com-prehensive coverage of the asset class, including unbiased research, in-depth analysis, and the latest news and intelligence. It allows you to gain sharp insight into private equity fund performance by comparing against similar funds, identifying potential minority interest op-portunities, as well as examiningthe latest transactions, rates, sizes, and IRRs. Members can also determine performance trends, compare the values of entry and exit deals, as well as gauge investor appetite by re-viewing the areas of funds being raised, closing sizes, sectors, and countries of investment.• As IPOs are a popular exit strategy for Private Equity Managers in the region, the IPO Moni-tor brings together historical analysis, activity monitoring, and a pipeline of deals for the IPO asset class. Strengthening members’ understanding the industry & market appetites, and keeping track of what lies ahead in Corporate Arabia’s quest to go public. Additionally, Zawya members can review portfolio details, identify where the bigger players are investing, and gain clear insight on the trends andbehaviors of the region’s Sovereign Wealth Funds through our dedicated coverage of SWF activity.• Zawya’s Corporate Monitor service, the cornerstone of our solutions, combines the names and contact details of 120,000+ senior officers with a comprehensive database of over 14,000 public and private companies based in the Middle East. Members can build custom-ized company lists, aswell as compare and contrast company profiles by sector, market size, and ownership. Simi-larly, third-party research provided in the Research Monitor offers greater understanding of the overall state of the target company’s market, sector, and macro-economic context.• With a team of on-the-ground journalists stationed throughout the region, Zawya Dow Jones Live News, an exclusive partnership with Dow Jones Newswires, delivers unique and insightful stories to help you better identify, assess and connect to the right finance and investment opportunities in the Middle East. In addition, more than 200 regional and in-ternational news sources are aggregated by our in-house editorial team, offering maximum exposure and clarity on the asset class.• The Zawya Network (ZN), our exclusive private network for premium members, offers us-ers the ability to quickly connect, engage, and transact with like-minded professionals. Forge valuable relationships, engage in variety of discussions, identify new oportunities, and tap in to the knowledge and experience of the regional and international investment community.

Sponsors’ profiles

annual Report

47

abRaaj Capital

Abraaj Capital is the leading alternative asset management group in the Middle East, North Africa and South Asia (MENASA). Since inception in 2002, we have raised over US$ 7 billion and distributed almost US$ 3 billion to our investors. Based in Dubai, the Abraaj Group oper-ates nine additional offices in Amman, Beirut, Cairo, Istanbul, Karachi, Mumbai, Ramallah, Riyadh and Singapore.

The group has made more than 40 investments in 11 countries across the MENASA region and has achieved 21 exits. More than 70 world-class investment and operating profession-als work for the group. Abraaj Capital Funds have holdings in 30 companies, including some of the region’s most prominent - such as Air Arabia, the region’s leading low-cost carrier; Acibadem Healthcare Group, Turkey’s leading privately owned hospital operator; and Al Borg Laboratories, the Middle East’s biggest privately owned medical-testing laboratory company.

Abraaj Capital has won many regional and international awards, including six consecutive years as ‘Middle Eastern Private Equity Firm of the Year’ from London-based Private Equity International. Abraaj Capital was awarded the ranking of top private equity firm in emerging markets worldwide from Private Equity International in 2011.

Abraaj Capital Ltd., a member of the Abraaj Group, is licensed by the Dubai Financial Serv-ices Authority. The group is also an associate member of the European Venture Capital Association.

Sponsors’ profiles

annual Report

48

amwal alkhaleej

Amwal AlKhaleej is a leading regional private equity firm which started its operations in 2005 and that has approximately USD 700 million of assets under management. It is the first and only private equity firm to be headquartered in Riyadh, Saudi Arabia. Amwal AlKhaleej also operates in Cairo and Dubai. The three-office presence staffed with local and on-the-ground experienced investment professionals provides the firm with local origination and execution capabilities. Its founders and management team also include some of the most well-known merchant names and investment professionals in the MENA region.

Amwal AlKhaleej is focused on delivering extraordinary results that are consistent, absolute, and deliver market-outperforming returns. The firm emphasizes ethics and transparency as it unlocks the long-term potential of its investments. While open to opportunities across the region, Amwal AlKhaleej focuses on sectors where it can create exceptional value and partners with regional companies that have strong, committed management teams seeking growth.

Amwal AlKhaleej specializes in taking influential minority and majority stakes in growing companies across sectors in the MENA region. It has investments in several high calibre com-panies including Rowad Schools, Gulf Insulation Group, Maritime Industrial Services, Samay Hills, Arab Cotton Ginning, Al-Tayyar Travel Group, Dubai Contracting Group, Right Angle Media and Contact Cars. The firm’s indigenous investment team is composed of internation-ally trained local talent that has a thorough understanding of the region’s business, cultural, legal and social landscapes. They also have a proven track-record for delivering high value returns, strategic growth and management support with integrity.

In addition, the firm is committed to thought leadership. Working with various academics, practitioners, and industry experts, it regularly contributes to a wide range of white papers and articles that reflect its perspective on private equity in the Middle East, and contributes to the intellectual capital of the industry.

Amwal AlKhaleej offers an “Absolute Advantage” to its partners by creating superior results that have a sweeping impact on businesses. Through teamwork and a shared vision, it gives businesses a unique advantage by designing, supporting and deploying initiatives that foster long-term value creation for its investee companies and all stakeholders. For more information please visit www.amwalalkhaleej.com

Sponsors’ profiles

annual Report

49

eaStgate Capital gRoup

The Eastgate Capital Group is the private equity arm of NCB Capital and was founded in 2006. Eastgate Capital Group Limited (“Eastgate”) is regulated by the Dubai Financial Serv-ices Authority.

Eastgate’s mandate is to source, structure, and invest in attractive private equity and real estate opportunities across emerging markets, with a particular focus on the Middle East and North Africa (MENA) region. Eastgate currently has close to USD 600 million of commit-ments under management of which it has invested close to USD 300 million in 11 transac-tions across 6 countries.

Eastgate MENA Direct Equity Fund (the “MENA Fund”), the core product of Eastgate, targets Shariah compliant direct equity investments in growth companies across the MENA and Tur-key region with a particular emphasis on Saudi Arabia. The MENA Fund targets investments in less cyclical consumer-centric sectors that are expected to benefit from favourable dy-namics in the target countries while being relatively resilient to potential macro-economic shocks. The MENA Fund has made investments in the education, pharmaceutical, health-care, and gold jewellery manufacturing & distribution sectors.

Eastgate targets to create and capture outstanding value for its investors by blending crea-tive insights, exceptional talent, and capital.

Sponsors’ profiles

annual Report

50

global Capital management

Global Capital Management Ltd., the alternative asset management arm of Global Invest-ment House, is a leading private equity asset management firm in the Middle East & North Africa (MENA) region managing around USD2.5billion on behalf of its clients.

Global Capital Management has one of the largest private equity teams in MENA with 30 professionals comprising 9 nationalities; providing ‘local’ perspective for deals in all target regions. The team has cumulative work experience of over 250 years ranging from private equity & venture capital, investment banking, transaction advisory, credit rating and audit. The team is based out of four locations - Kuwait, UAE, Turkey and Egypt.

Global Capital Management’s achievements have been recognized at product and deal level through awards such as “Fund of the Year” for 2007 and 2008, “Private Equity Deal of the Year” for 2008 by Terrapin. It was also ranked among top 150 Private Equity firms in the World by Private Equity International and top 20 in Asia by PEI Asia in 2009 and 2010.

Sponsors’ profiles

annual Report

51

global Capital management

Established in 2005, NBK Capital focuses on offering a diversified range of innovative financial prod-ucts and services to clients.

With a highly professional team of over 170 professionals leveraging world-class experience and ex-pertise of investment, NBK Capital delivers creative financial solutions through its four divisions – Al-ternative Investments, Asset Management, Brokerage & Research, and Investment Banking.

NBK Capital has advised on over USD 7.4 billion in financing transactions and USD 2.5 billion in M&A transactions during the past two years. The company’s assets under management currently stand at just over USD 6.5 billion across regional and international funds.

Innovative products, objective research, creative thinking, timely implementation and excellence in service have seen NBK Capital being recognized as “Best Investment Bank in the Middle East” for 2009 by The Banker, and as “Best Investment Bank in Kuwait” for 2009 by Global Finance and for 2009 and 2010 by Euromoney.

As the investment banking subsidiary of National Bank of Kuwait (NBK), the highest-rated bank in the Middle East, NBK Capital combines the strengths, resources and global network of one of the largest and oldest financial institutions in the country with best-in-class investment structuring and execu-tion, on a broad array of financial strategies, to consistently deliver integrated value added solutions.

Operating regionally from Kuwait, Dubai, Istanbul and Cairo, NBK Capital prides itself on a reach and scale that is global, a focus that is regional and a service level that always remains personal.

nbk Capital

Sponsors’ profiles

annual Report

52

qataR fiRSt inveStment bank

Qatar First Investment Bank (QFIB) is a pioneering Islamic investment bank well positioned to work across the broader GCC and MENA region. It launched in 2009 with an authorized capital of QAR 3.65 billion (US$ 1 billion) and a paid up capital of QAR 1.6 billion (US$ 430 million).

QFIB is unique in Qatar, simultaneously independent and central to the market, providing clients and counterparties with access to one of the region’s deepest pools of capital. Adopt-ing an investment strategy that centres on sector and geographical diversification, QFIB focuses on sectors that benefit from key drivers of economic change; these include the en-ergy, financial services, industrials, real estate and health care services. Since its inception, QFIB has executed seven transactions in five different sectors across three geographies and exited one investment.

QFIB offers Principle Investments, Asset Management and Corporate Finance Advisory serv-ices. Relationships drive QFIB’s dynamic business strategy; the management team has an entrepreneurial outlook that encourages innovation and creativity in meeting client needs. The Bank’s medium to long-term view ensures clients can benefit from the leadership’s in-sight and connections.

QFIB operates to the highest of international business regulatory standards and corporate governance. The first independent Shari’ah compliant investment bank is licensed by the Qatar Financial Centre Regulatory Authority (QFCRA) and is ISO 27001 certified.

Sponsors’ profiles

annual Report

53

qataR fiRSt inveStment bank SwiCoRp

Swicorp is a leading corporate finance advisory, private equity and principal investment firm with a specific regional focus on the Middle East and North Africa (MENA) region.

Founded in 1987 and licensed by the Capital Market Authority of the Kingdom of Saudi Arabia, and the Dubai Financial Service Authority of the United Arab Emirates, Swicorp has an extensive track record of pioneering M&A and Advisory transactions across the MENA re-gion over the last 20 years. Headquartered in Riyadh with regional offices in Jeddah, Geneva, Tunis, Dubai and Algiers, the firm has over 100 employees across its offices and activities, including 30 private equity professionals from both within and outside the region.

Since the launch of its private equity activities in 2004, Swicorp has established itself among the leading private equity managers in the MENA region, with nearly US$1.4 billion currently under management across two separate investment programs, including Intaj Capital and Swicorp Joussour.

Intaj Capital is a pan-MENA focused private equity fund investing in companies operating in sectors driven directly or indirectly by growth in consumer demand. Sectors include consum-er goods, retail, food and beverage, media and communications, consumer financial serv-ices, healthcare and consumer-facing construction materials, among others. Intaj pursues two main investment strategies for building a platform of value creation in its portfolio com-panies: growth and buy & build investments. Intaj Capital I, the first fund launched in 2005, invested US$187 million, US$290 million including co-investments from limited partners, in eight investments across seven countries, well diversified in terms of both geographic coverage and sectors. Intaj Capital II, which represents the second private equity vehicle of the Intaj franchise, had a first closing in September 2010 with commitments from leading international institutional LPs.

Joussour was founded in 2005 with US$1 billion in capital commitments. Joussour focuses on large-scale investments in the energy sector, petrochemicals and ancillary businesses to the petrochemical industry, and energy-intensive sectors, through greenfields and joint ventures with international partners or buy-out/relocation of international players in the sector.

Sponsors’ profiles

annual Report

54

tuninveSt-afRiCinveSt

Tuninvest-AfricInvest Group was founded in 1994 and is part of a full fledged investment boutique, Integra Partners (www.integra-partners.com) which offers in addition to Pri-vate Equity: Brokerage, Asset Management and Corporate Finance services.

Tuninvest-AfricInvest Group is today a leading private equity firms in North and sub-Sa-haran Africa with over $550 million of assets under management across 11 PE funds and sponsored by prestigious DFIs, private and institutional investors.The covered and targeted region evolved during the life of the Group from Tunisia for the first generation of funds with relatively small investments, to the Maghreb region (Maghreb Private Equity Funds I & II) and Sub-Saharan Africa (AfricInvest Funds I & II and AfricInvest Financial Sector Fund) with larger investments. The Group is now launching its third generation of Funds with the initiation of Maghreb Private Equity Fund III, a new North African Initiative.

Tuninvest–AfricInvest Group relies on a team of 35 highly skilled investment profession-als with over 120 years of cumulative PE experience, operating out of 6 offices (Tunis, Casablanca, Algiers, Lagos, Abidjan and Nairobi).

The Group has made 90 investments across several sectors and realized over 40 exits generating above market IRRs. The Group has made significant contribution to the eco-nomic development of its target countries through the growth and profitability achieved by its portfolio companies.

The Group is the co-founder of the African Venture Capital Association (www.avcanet.com) and a member of the Euromed Capital Forum (www.euromed-capital.com).

Sponsors’ profiles

annual Report

55

exeCutive

Executive is a monthly business magazine that offers its readers in-depth and forward think-ing analysis, solid reporting and punchy opinion on Middle East and North Africa’s com-merce, economy and finance as well as regular industry surveys, regional market data and global economic trends.

Since its launch in 1998, Executive’s passion for business, its inside access and uncanny fore-sight has earned it the highest plaudits, where its readers choose it for its unbiased editorial line and comprehensive analysis.

From Morocco to Iraq, Executive has a solid network of the best business and economic analysts, experts, and reporters to provide what is arguably the most authoritative business writing in the Middle East.

For more information, please visit www.executive-magazine.com<http://www.executive-magazine.com/> or call us on 00 961 1 611696

Sponsors’ profiles

mena pRivate equity aSSoCiation membeRS diReCtoRy

7

Annual Report

57

Abraaj CapitalDubai, UAE

Egypt, Jordan, KSA, Lebanon,

Pakistan, Singapore, Turkey

+971 4 5064400

www.abraaj.com

EFG Hermes PrivateEquity

Cairo, Egypt

UAE

+971 4 364 1961

www.efg-hermes.com

New Silk Route

Dubai, UAE

India, USA

+971 4 3211772

www.nsrpartners.com

SwicorpRiyadh, KSA

Algeria,Tunisia, UAE

Switzerland

+966 1 211 0737

www.swicorp.com

Amwal AlKhaleejRiyadh, KSA

Egypt, UAE

+966 1 216 4666

www.amwalalkhaleej.com

Gulf CapitalAbu Dhabi, UAE

+971 2 671 6060

www.gulfcapital.com

Doha, Qatar

+974 4 483333

www.qfib.com.qa

Tunis, Tunisia

Algeria, Ivory Coast, Kenya,

Morocco, Nigeria

+21671189800

www.tuninvest.com

Capital Trust GroupBeirut, Lebanon

UK, USA

+961 1 368968

www.capitaltrustltd.com

Investcorp BankManama, Bahrain

UK, USA

+973 1 753 2000

www.investcorp.com

ReAya HoldingJeddah, KSA

+966 2 6676777

www.reayaholding.com

TVM CapitalDubai, UAE

Germany, USA

www.tvm-capital.ae

Cedar Bridge PartnersCairo, Egypt

UAE

www.cedar-bridge.com

Levant CapitalDubai, UAE

+971 4 331 9788

www.levantcapital.com

Riyada Enterprise DevelopmentDubai, UAE

Egypt, Jordan,

+971 4 5064400

www.riyada.com

Citadel CapitalCairo, Egypt

Algeria, Kenya

+202 2 7914440

www.citadelcapital.com

Malaz CapitalRiyadh, KSA

+966 1 4601644

www.malazcapital.com

SaffarDubai, UAE

+971 4 3735777

www.saffar.com

Eastgate Capital GroupDubai, UAE

+971 4 329 7171

www.eastgategroup.com

NBK CapitalKuwait

Egypt, Turkey, UAE

+965 2 2246900

ww.nbkcapital.com

SEDCOJeddah, KSA

UAE

+971 4 3637166

www.sedco.com

Mena Private Equity Association Members Directory

Qatar FirstInvestment Bank

TunInvest–AfricInvestGroup

Growth Capital

pRivate equity & ventuRe Capital fiRmS in mena

8

annual Report

59

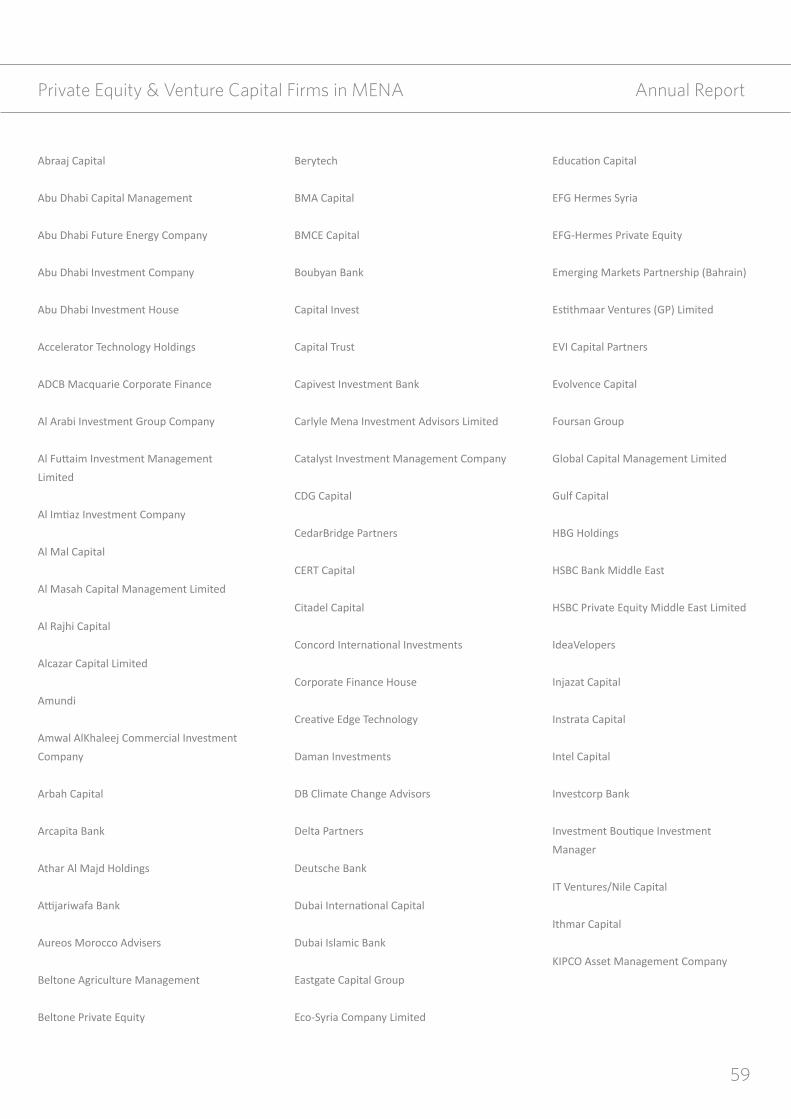

Abraaj Capital

Abu Dhabi Capital Management

Abu Dhabi Future Energy Company

Abu Dhabi Investment Company

Abu Dhabi Investment House

Accelerator Technology Holdings

ADCB Macquarie Corporate Finance

Al Arabi Investment Group Company

Al Futtaim Investment Management

Limited

Al Imtiaz Investment Company

Al Mal Capital

Al Masah Capital Management Limited

Al Rajhi Capital

Alcazar Capital Limited

Amundi

Amwal AlKhaleej Commercial Investment

Company

Arbah Capital

Arcapita Bank

Athar Al Majd Holdings

Attijariwafa Bank

Aureos Morocco Advisers

Beltone Agriculture Management

Beltone Private Equity

Berytech

BMA Capital

BMCE Capital

Boubyan Bank

Capital Invest

Capital Trust

Capivest Investment Bank

Carlyle Mena Investment Advisors Limited

Catalyst Investment Management Company

CDG Capital

CedarBridge Partners

CERT Capital

Citadel Capital

Concord International Investments

Corporate Finance House

Creative Edge Technology

Daman Investments

DB Climate Change Advisors

Delta Partners

Deutsche Bank

Dubai International Capital

Dubai Islamic Bank

Eastgate Capital Group

Eco-Syria Company Limited

Education Capital

EFG Hermes Syria

EFG-Hermes Private Equity

Emerging Markets Partnership (Bahrain)

Estithmaar Ventures (GP) Limited

EVI Capital Partners

Evolvence Capital

Foursan Group

Global Capital Management Limited

Gulf Capital

HBG Holdings

HSBC Bank Middle East

HSBC Private Equity Middle East Limited

IdeaVelopers

Injazat Capital

Instrata Capital

Intel Capital

Investcorp Bank

Investment Boutique Investment

Manager

IT Ventures/Nile Capital

Ithmar Capital

KIPCO Asset Management Company

private equity & venture Capital firms in mena

annual Report

60

KKR

Kuwait Finance and Investment Company

Kuwait Finance House

Kuwait Finance House Bahrain

Kuwait Financial Centre

Kuwait Investment Company

Levant Capital Limited

Malaz Capital

Manara Equity Partners

Marshall Fund Capital Advisors

Masdar Venture Capital

MENA Advisors Limited

MerchantBridge and Co

Middle East Capital Group

Middle East Venture Partners

Millennium Private Equity

Minah Partners

Moroccan Information Technopark Com

pany

NBK Capital Limited

New Enterprise East Investments

Upline Investments

Pharos Financial Advisors Limited

Unicorn Investment Bank

Venture Capital Bank

Viveris Management

PrimeCorp (France)

Qatar Capital Partners

RAIS (Netherlands)

Rasmala Holdings Limited

Riyada Enterprise Development

Riva y Garcia Financial Group

Sabre Abraaj Management Company

Saffar

Sawari Ventures

Saham Group

SHUAA Capital

SHUAA Capital Saudi Arabia

SHUAA Partners

Siparex Group

Siraj Capital Dubai Limited

Siraj Fund Management Company

Sphinx Private Equity Management

Swicorp

The Financial Corporation Company

The National Investor

Tuareg Capital

TunInvest-AficInvest

TVM Capital MENA

private equity & venture Capital firms in mena