Embed Size (px)

DESCRIPTION

Product Overview and Sales Ideas in Life Insurance. Quick Facts. Quick Facts. Quick Facts. Today we will look at. Whole Life a real sales opportunity…making a 20 pay a 10pay??? Term Insurance in particular T30. Whole Life Case Study for a juvenile. Let’s look at Lisa’s case. - PowerPoint PPT Presentation

Citation preview

Product Overview and Sales Ideas in Life Insurance

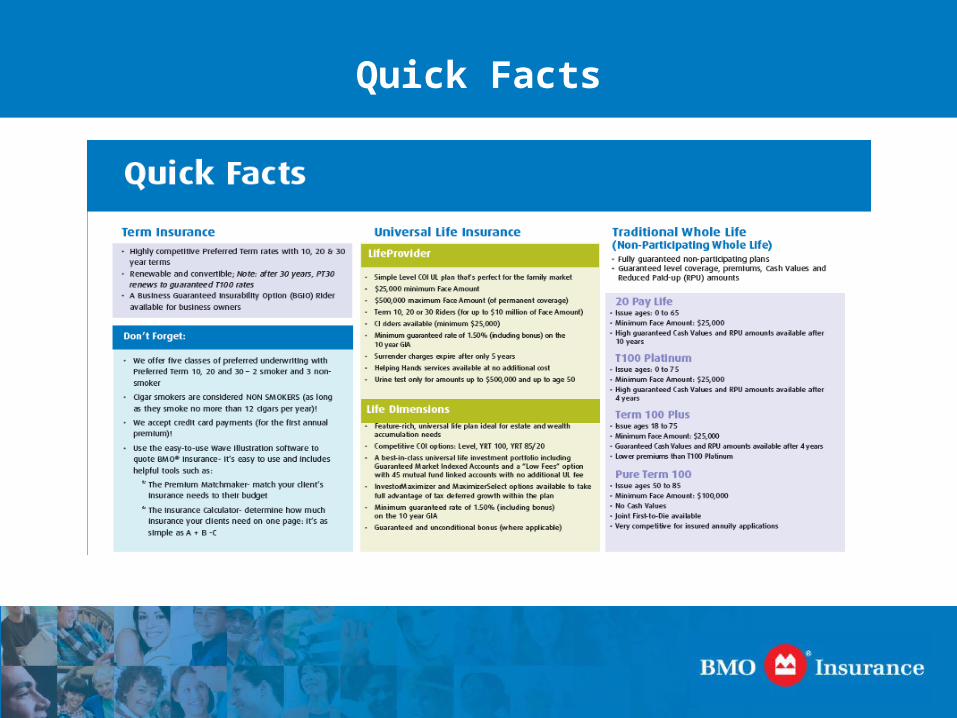

Quick Facts

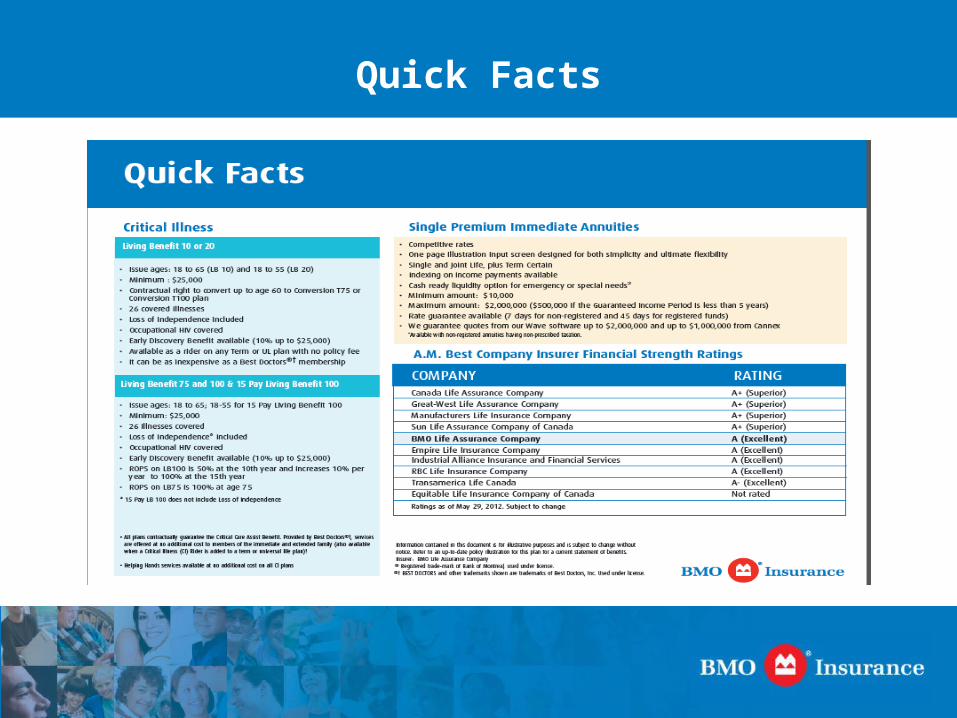

Quick Facts

Quick Facts

Today we will look at

• Whole Life a real sales opportunity…making a 20 pay a 10pay???

• Term Insurance in particular T30

Whole Life Case Study for a juvenile

Let’s look at Lisa’s case

• Lisa is a young 8 year old girl;

• Her father wishes to provide her with a whole

life policy with an insured amount of $30,000;

• He would like that the premium for this policy

be paid up in 10 years;

• An additional amount of insurance may be

required in the future.

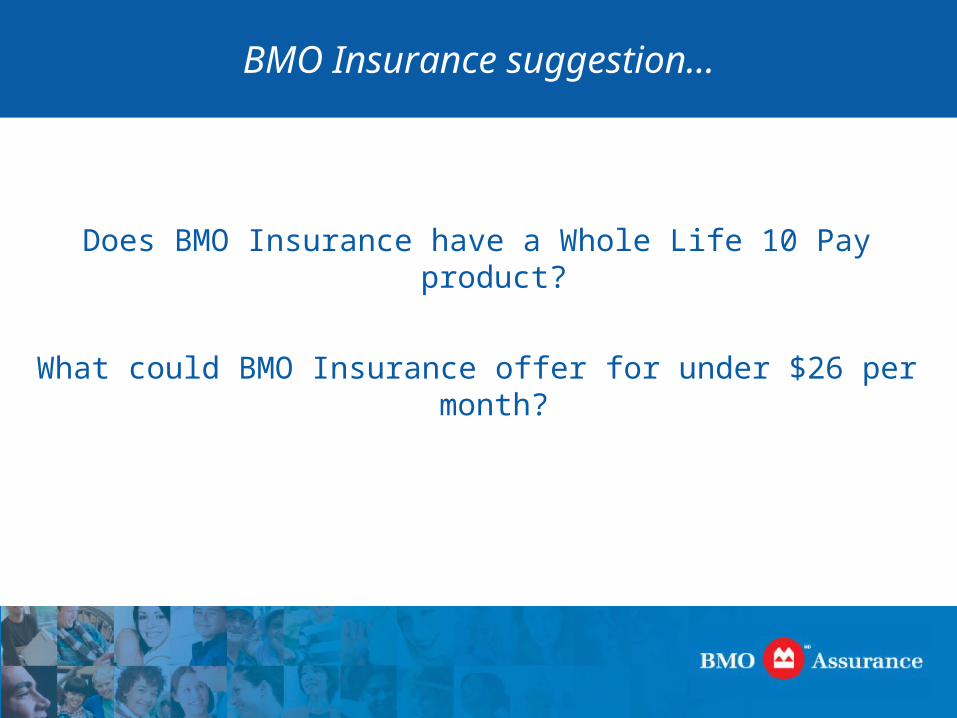

BMO Insurance suggestion...

Does BMO Insurance have a Whole Life 10 Pay product?

What could BMO Insurance offer for under $26 per month?

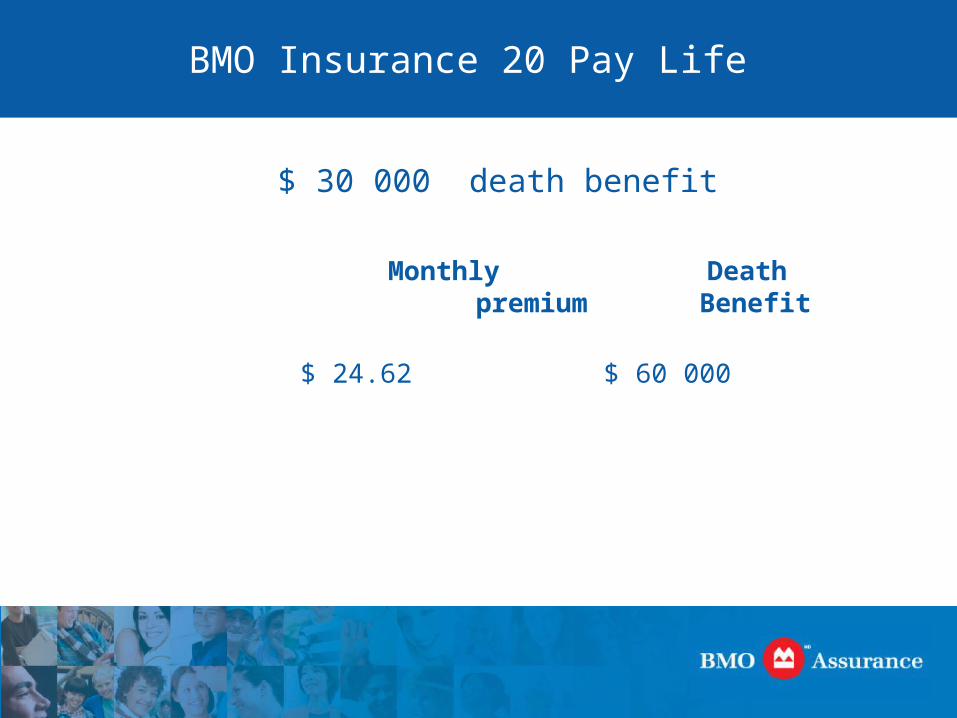

BMO Insurance 20 Pay Life

$ 30 000 death benefit

Monthly Death premium Benefit

$ 24.62 $ 60 000

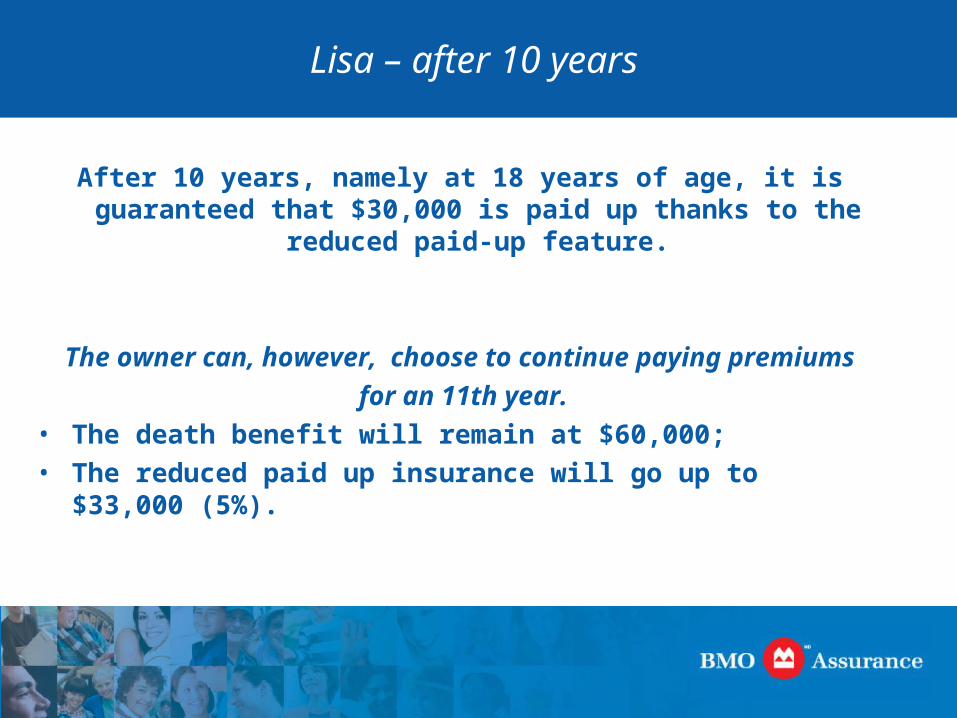

Lisa – after 10 years

After 10 years, namely at 18 years of age, it is guaranteed that $30,000 is paid up thanks to the reduced paid-up feature.

The owner can, however, choose to continue paying premiums

for an 11th year.• The death benefit will remain at $60,000;• The reduced paid up insurance will go up to $33,000 (5%).

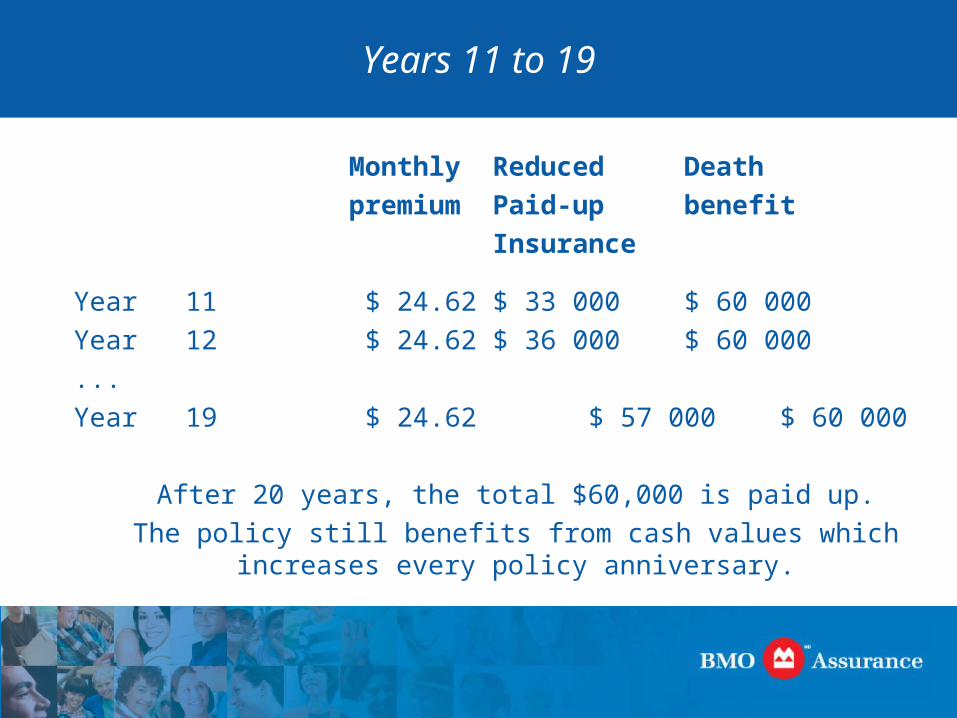

Years 11 to 19

Monthly Reduced Death

premium Paid-up benefit

Insurance

Year 11 $ 24.62 $ 33 000 $ 60 000

Year 12 $ 24.62 $ 36 000 $ 60 000

...

Year 19 $ 24.62 $ 57 000 $ 60 000

After 20 years, the total $60,000 is paid up.

The policy still benefits from cash values which increases every policy anniversary.

After 20 years

Lisa now has a $60,000 policy which is completely paid up.

The premium was lower than the 10 pay policy;

The cash value increases and reaches $60,000 at age 100.

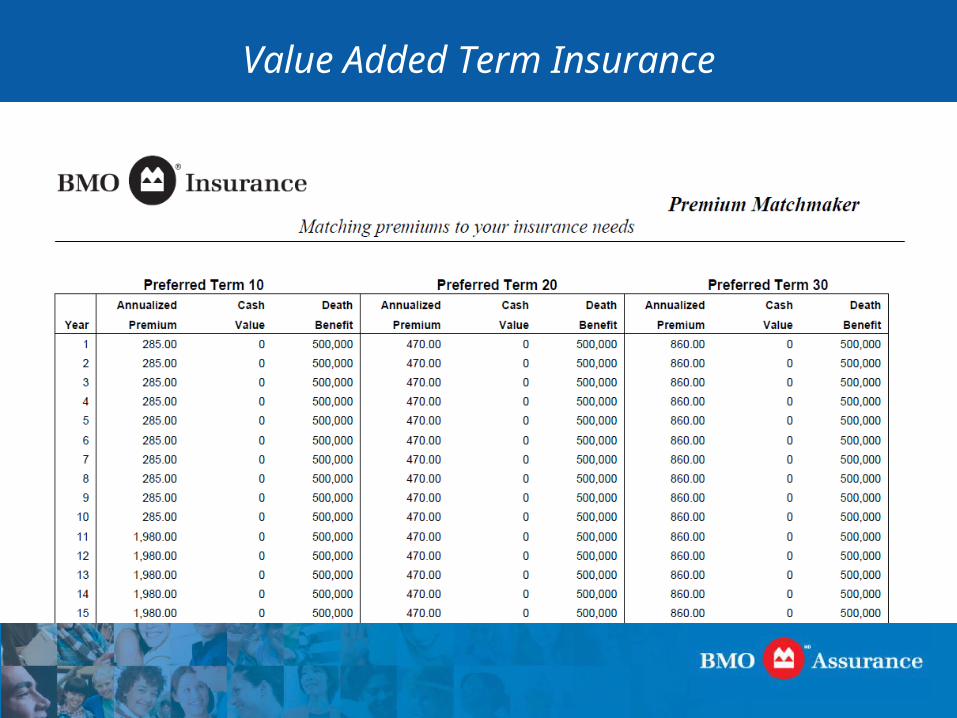

Bmo Insurance Term 30…a value-added term insurance

Value Added Term Insurance

• Alan is a single Dad of two children;

• Alan (35) has a 500,000 insurance need

• He may have a need for insurance at age 65

Value Added Term Insurance

Value Added Term Insurance

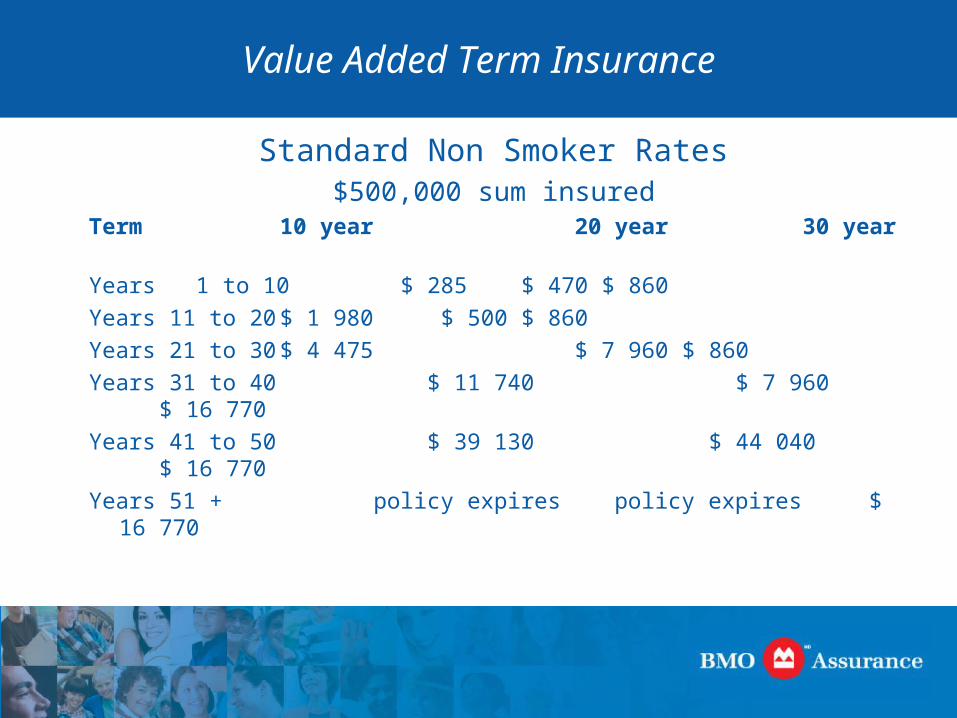

Standard Non Smoker Rates$500,000 sum insured

Term 10 year 20 year 30 year

Years 1 to 10 $ 285 $ 470 $ 860

Years 11 to 20 $ 1 980 $ 500 $ 860

Years 21 to 30 $ 4 475 $ 7 960 $ 860

Years 31 to 40 $ 11 740 $ 7 960 $ 16 770

Years 41 to 50 $ 39 130 $ 44 040 $ 16 770

Years 51 + policy expires policy expires $ 16 770

Value Added Term Insurance

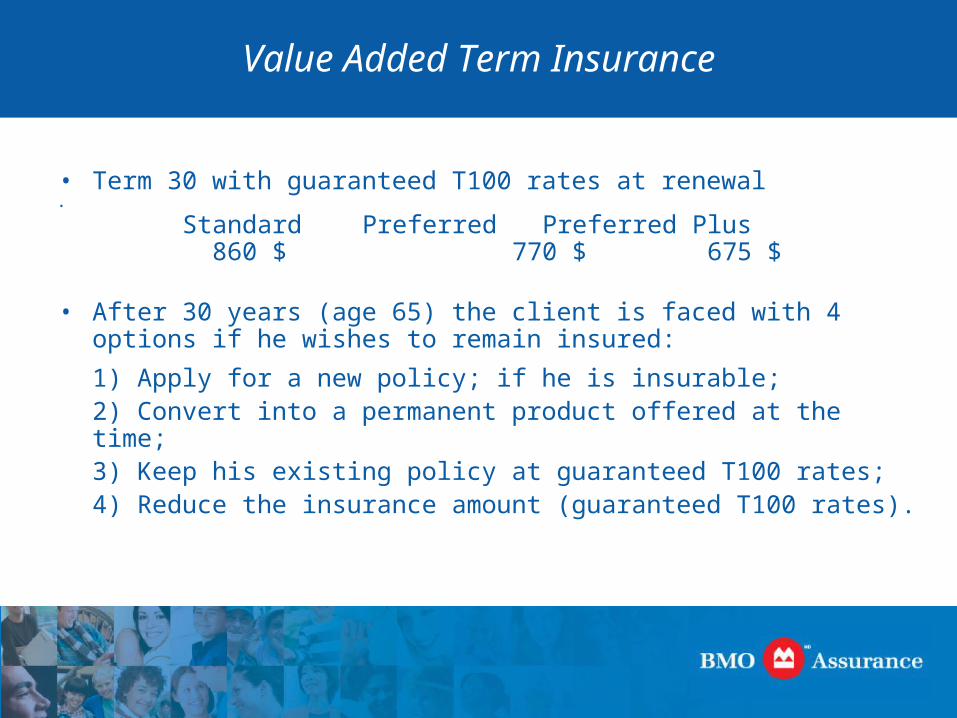

• Term 30 with guaranteed T100 rates at renewal•

Standard Preferred Preferred Plus 860 $ 770 $ 675 $

• After 30 years (age 65) the client is faced with 4 options if he wishes to remain insured:

1) Apply for a new policy; if he is insurable;2) Convert into a permanent product offered at the time;3) Keep his existing policy at guaranteed T100 rates;4) Reduce the insurance amount (guaranteed T100 rates).

Value Added Term Insurance

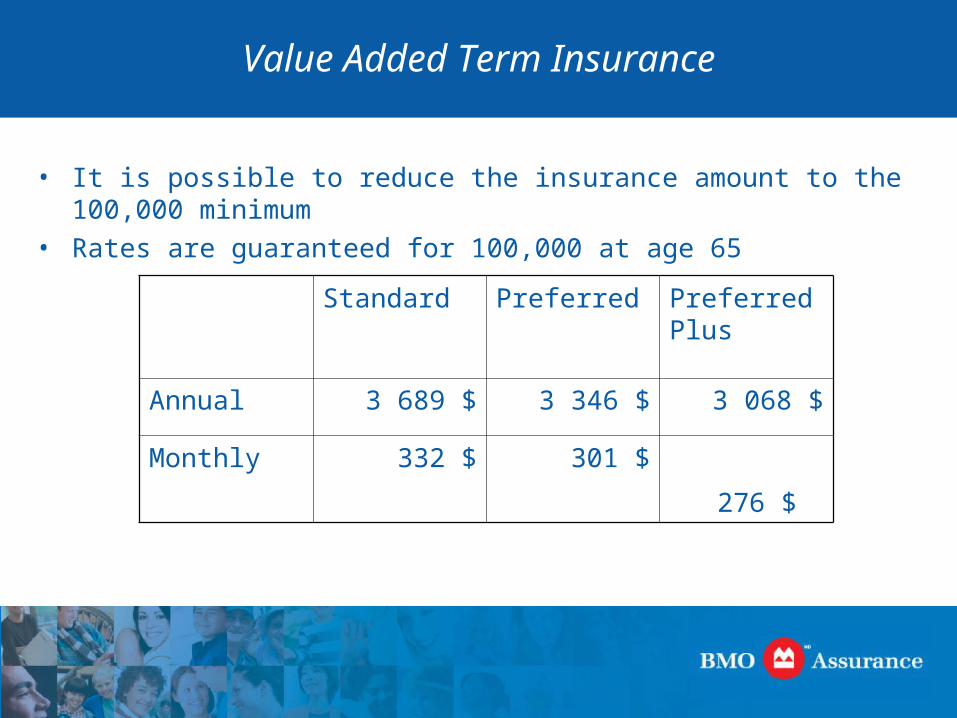

Standard Preferred Preferred Plus

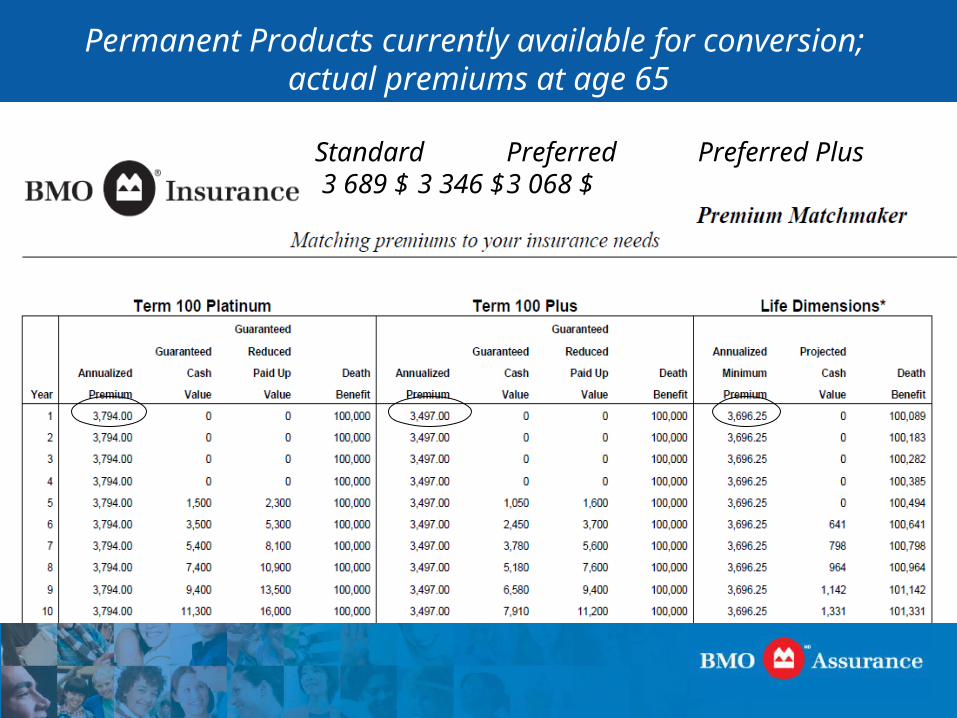

Annual 3 689 $ 3 346 $ 3 068 $

Monthly 332 $ 301 $ 276 $

• It is possible to reduce the insurance amount to the 100,000 minimum• Rates are guaranteed for 100,000 at age 65

Permanent Products currently available for conversion; actual premiums at age 65

Standard Preferred Preferred Plus 3 689 $ 3 346 $ 3 068 $

Standard Preferred Preferred Plus 3 689 $ 3 346 $ 3 068 $

Value Added Term Insurance…In other words..

• If we were to use a house analogy:

– Term insurance is like renting

– Permanent insurance is like owning

– BMO’s Term 30…

…like renting with the option to buy at a

guaranteed price!

Term or Perm?

The age-old question…

Case Study

• Male 45 NS

• Has an insurance need for the next 20 years;

• There is a possibility that the need may become permanent;

• The client has strong cash flows and he loves getting a deal!

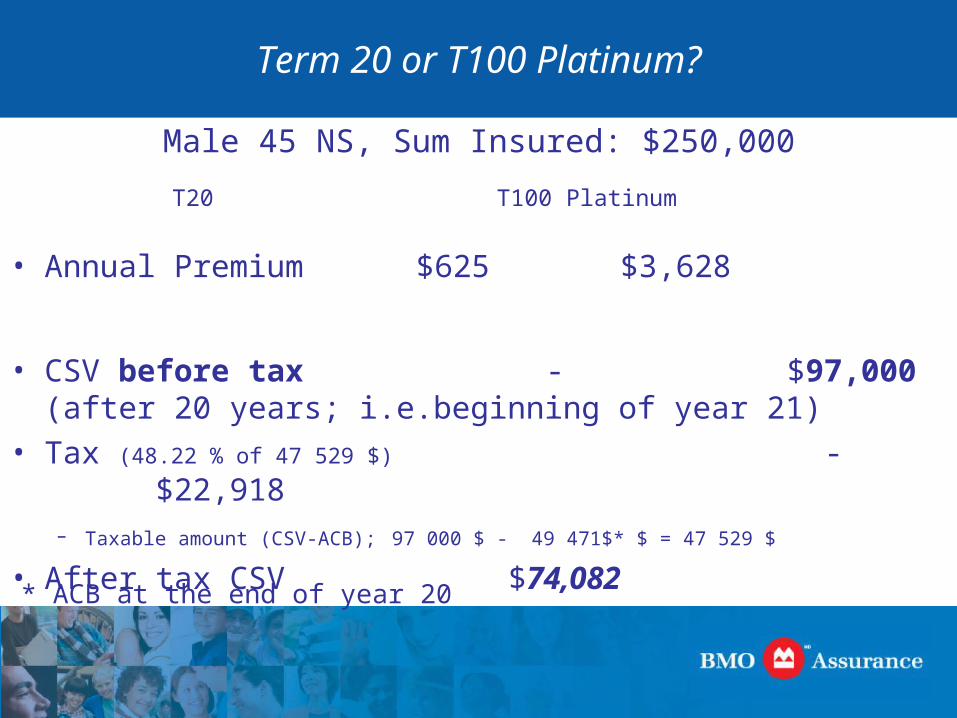

Term 20 or T100 Platinum?

T20 T100 Platinum

• Annual Premium $625 $3,628

• CSV before tax - $97,000 (after 20 years; i.e.beginning of year 21)

• Tax (48.22 % of 47 529 $) - $22,918 – Taxable amount (CSV-ACB); 97 000 $ - 49 471$* $ = 47 529 $

• After tax CSV $74,082

Male 45 NS, Sum Insured: $250,000

* ACB at the end of year 20

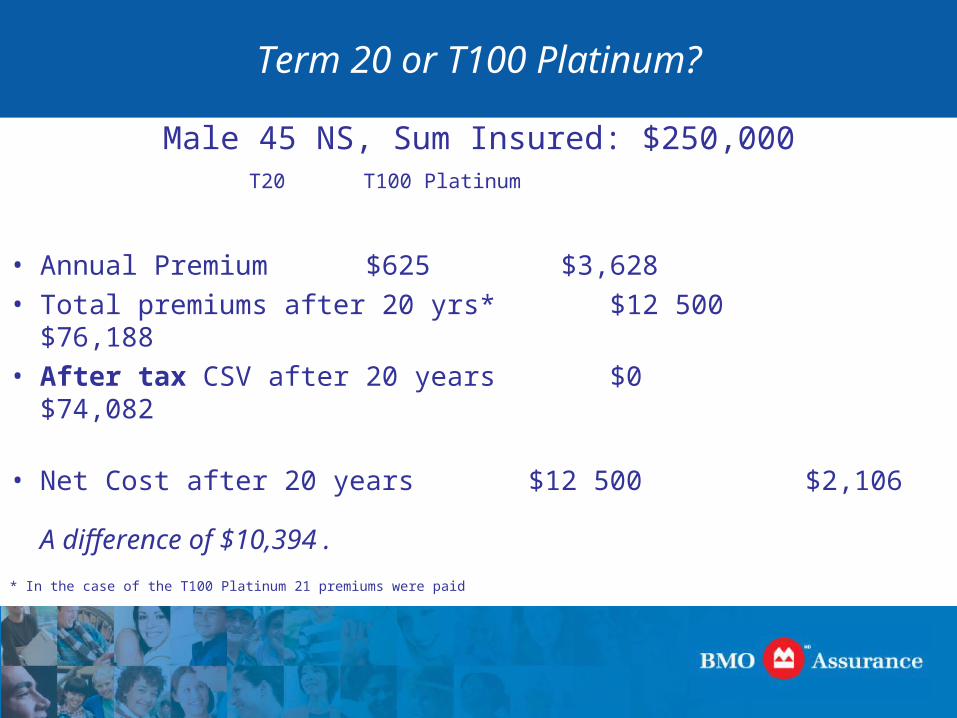

Term 20 or T100 Platinum?

T20 T100 Platinum

• Annual Premium $625 $3,628 • Total premiums after 20 yrs* $12 500 $76,188• After tax CSV after 20 years $0 $74,082

• Net Cost after 20 years $12 500 $2,106

A difference of $10,394 .

* In the case of the T100 Platinum 21 premiums were paid

Male 45 NS, Sum Insured: $250,000

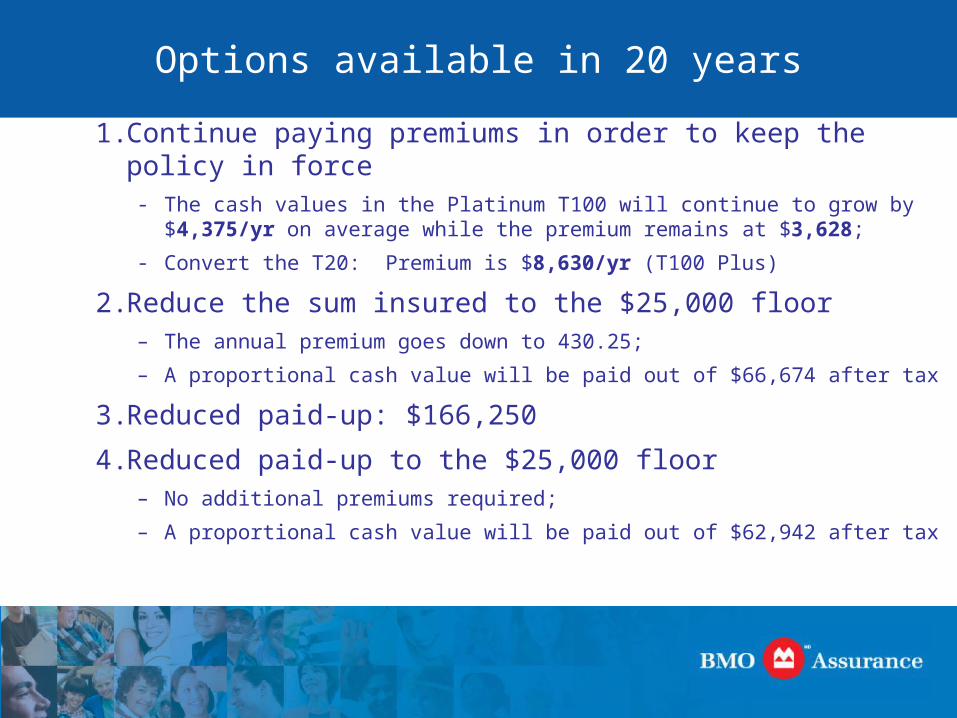

Options available in 20 years

1. Continue paying premiums in order to keep the policy in force- The cash values in the Platinum T100 will continue to grow by $4,375/yr

on average while the premium remains at $3,628;

- Convert the T20: Premium is $8,630/yr (T100 Plus)

2. Reduce the sum insured to the $25,000 floor– The annual premium goes down to 430.25;

– A proportional cash value will be paid out of $66,674 after tax

3. Reduced paid-up: $166,250

4. Reduced paid-up to the $25,000 floor– No additional premiums required;

– A proportional cash value will be paid out of $62,942 after tax

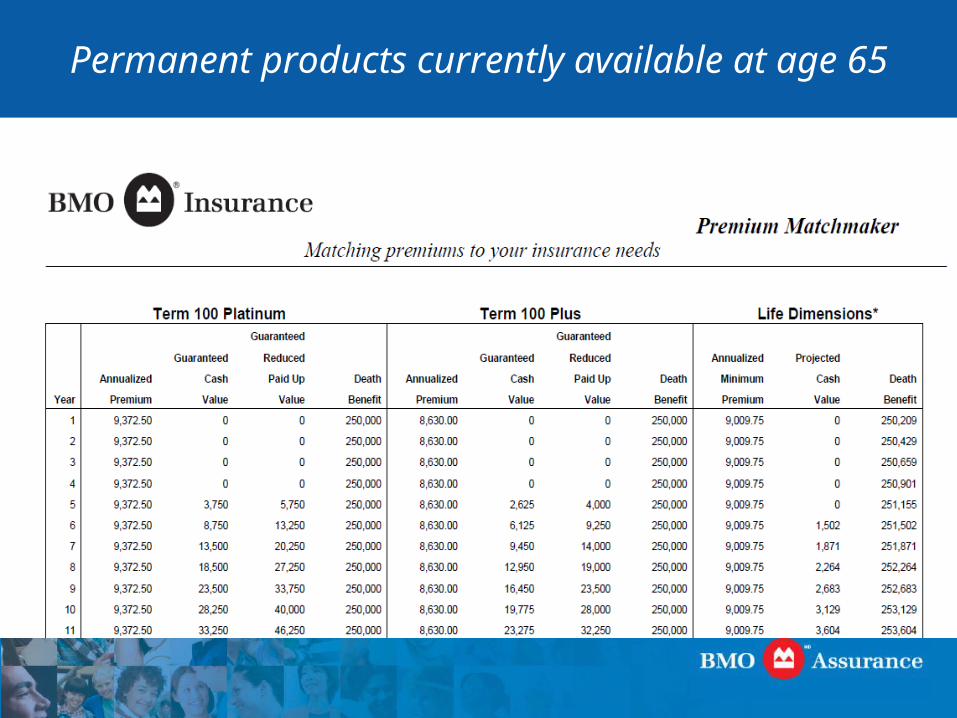

Permanent products currently available at age 65

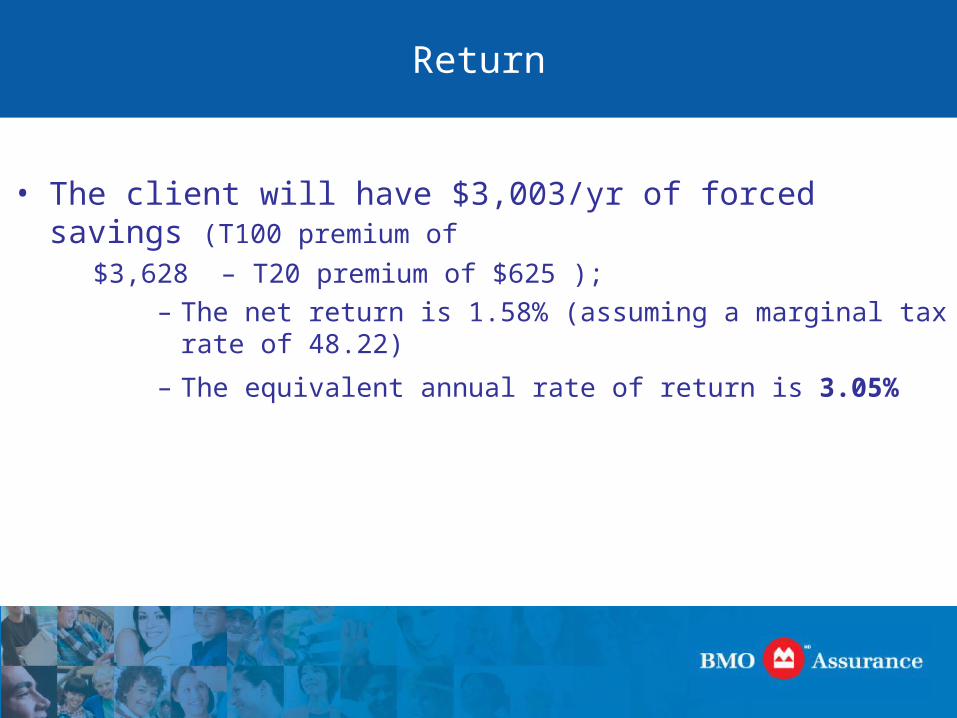

Return

• The client will have $3,003/yr of forced savings (T100 premium of

$3,628 – T20 premium of $625 );– The net return is 1.58% (assuming a marginal tax rate of 48.22)

– The equivalent annual rate of return is 3.05%

Conversion Considerations

Products currently available for Conversion

• Life Dimension Universal Life• T100 Platinum• T100 Plus• 20 Pay

Important:

Currently, Pure Term 100 and Life Provider Universal Life products are not available for conversion.

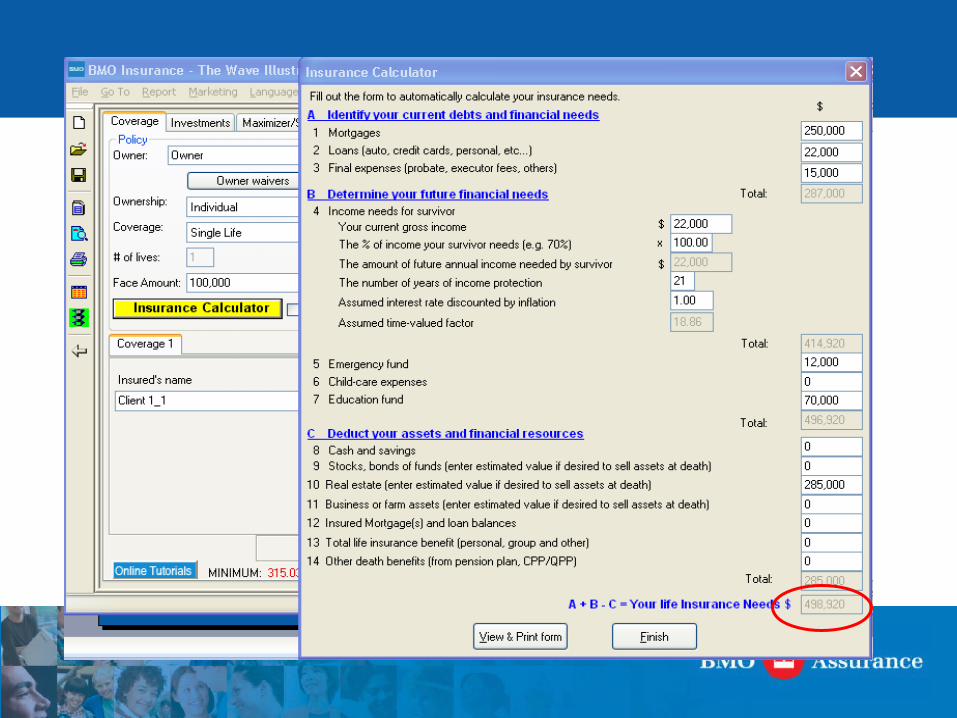

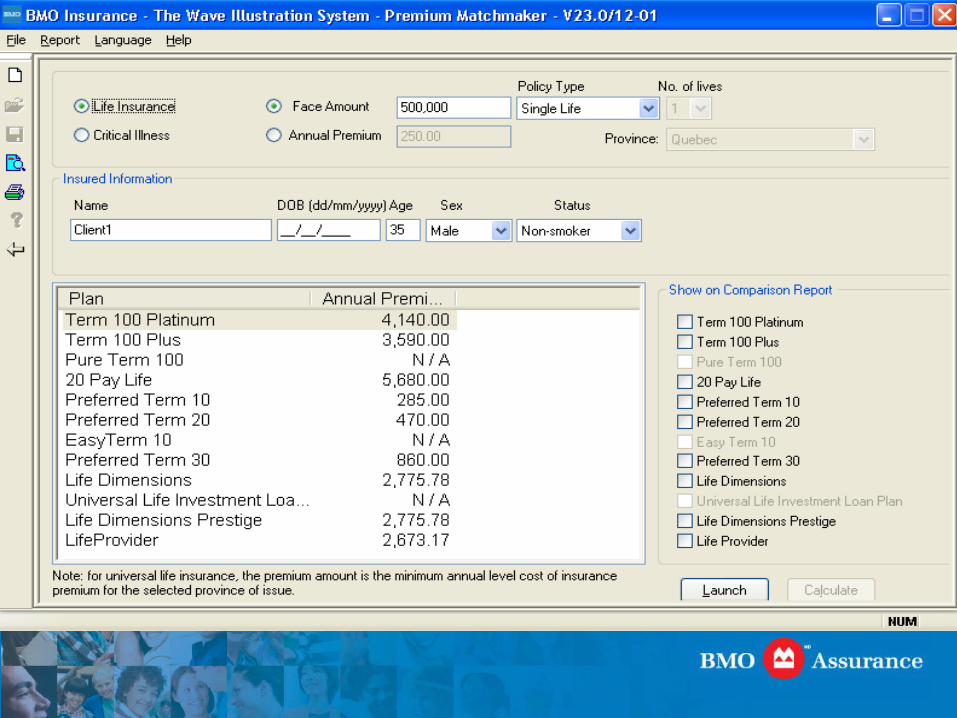

Wave Software

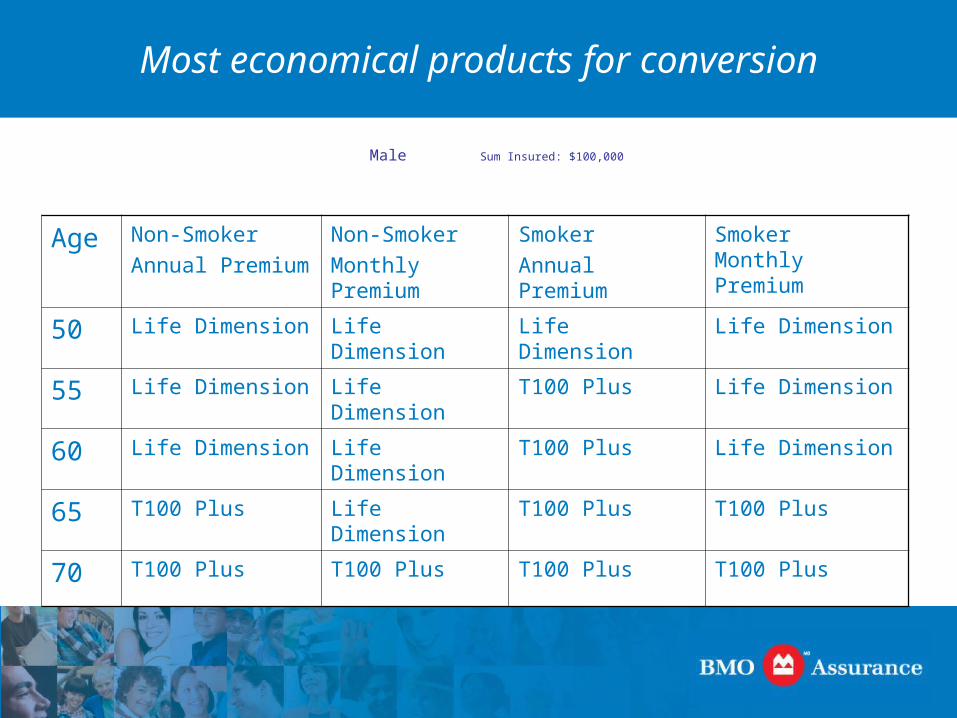

Most economical products for conversion

Male Sum Insured: $100,000

Age Non-Smoker

Annual Premium

Non-Smoker

Monthly Premium

Smoker

Annual Premium

Smoker Monthly Premium

50 Life Dimension Life Dimension Life Dimension Life Dimension

55 Life Dimension Life Dimension T100 Plus Life Dimension

60 Life Dimension Life Dimension T100 Plus Life Dimension

65 T100 Plus Life Dimension T100 Plus T100 Plus

70 T100 Plus T100 Plus T100 Plus T100 Plus

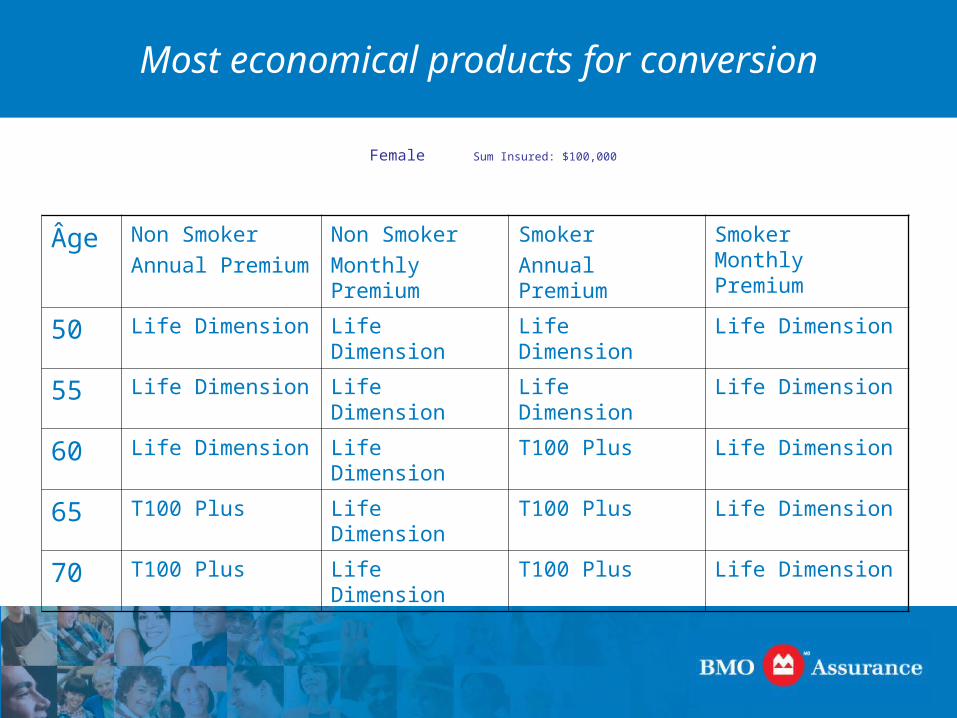

Most economical products for conversion

Female Sum Insured: $100,000

Âge Non Smoker

Annual Premium

Non Smoker

Monthly Premium

Smoker

Annual Premium

SmokerMonthly Premium

50 Life Dimension Life Dimension Life Dimension Life Dimension

55 Life Dimension Life Dimension Life Dimension Life Dimension

60 Life Dimension Life Dimension T100 Plus Life Dimension

65 T100 Plus Life Dimension T100 Plus Life Dimension

70 T100 Plus Life Dimension T100 Plus Life Dimension

Insured Annuity with a twist

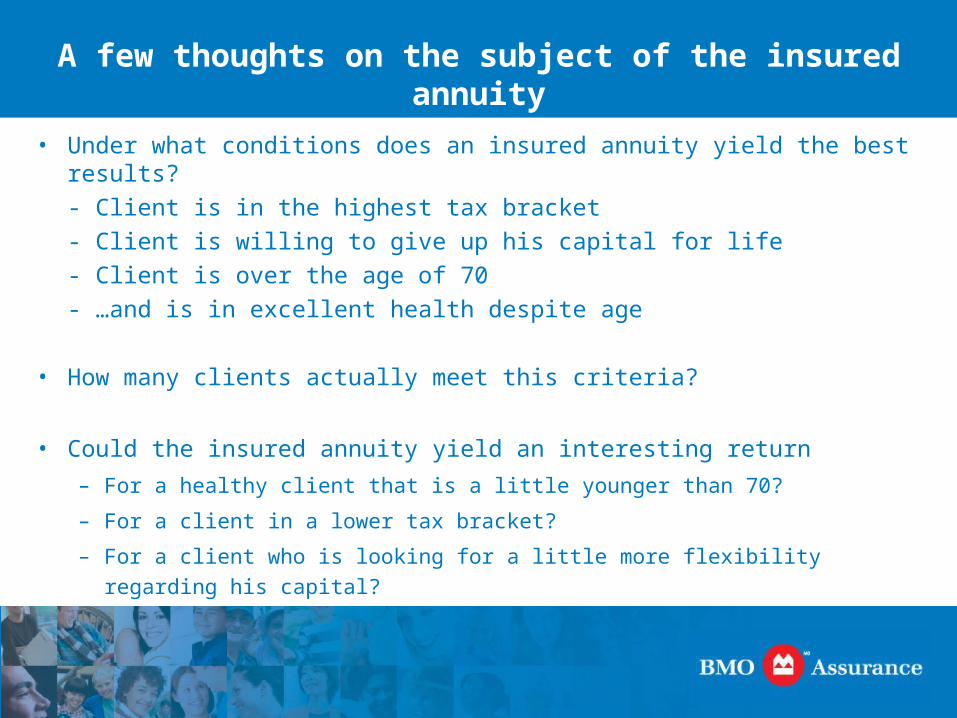

A few thoughts on the subject of the insured annuity

• Under what conditions does an insured annuity yield the best results?

- Client is in the highest tax bracket

- Client is willing to give up his capital for life

- Client is over the age of 70

- …and is in excellent health despite age

• How many clients actually meet this criteria?

• Could the insured annuity yield an interesting return

– For a healthy client that is a little younger than 70?

– For a client in a lower tax bracket?

– For a client who is looking for a little more flexibility regarding his capital?

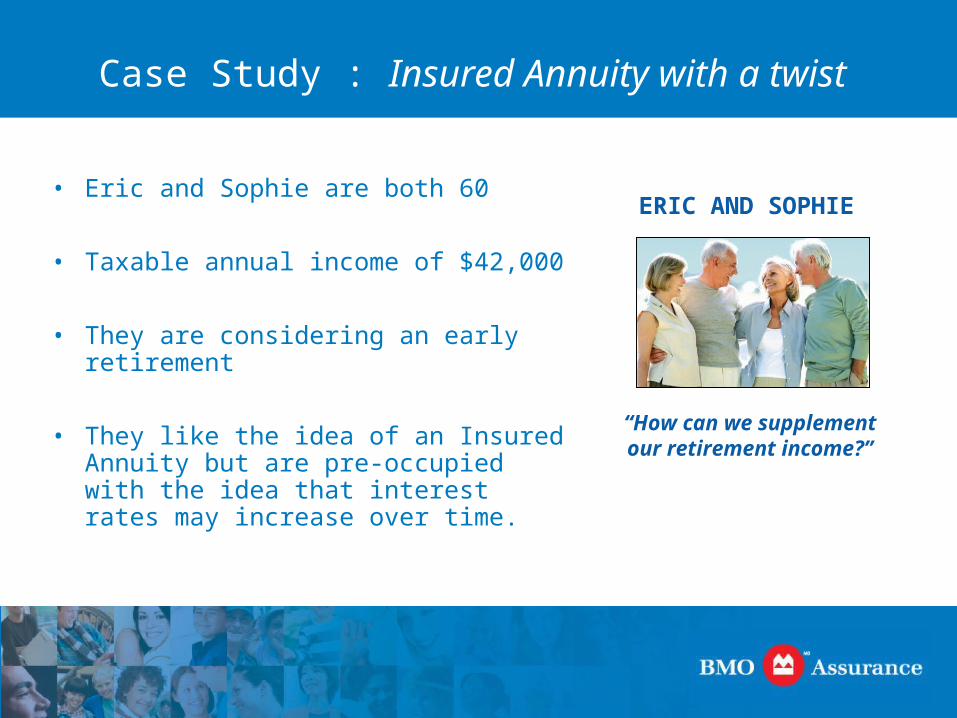

Case Study : Insured Annuity with a twist

• Eric and Sophie are both 60

• Taxable annual income of $42,000

• They are considering an early retirement

• They like the idea of an Insured Annuity but are pre-occupied with the idea that interest rates may increase over time.

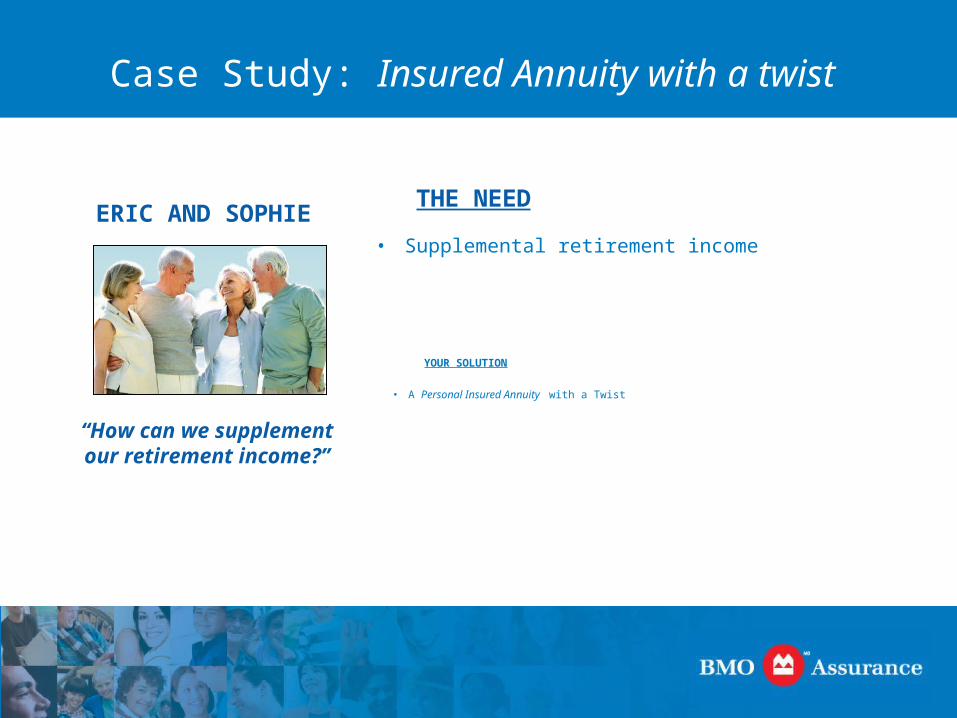

“How can we supplement our retirement income?”

ERIC AND SOPHIE

Case Study: Insured Annuity with a twist

YOUR SOLUTION

• A Personal Insured Annuity with a Twist

“How can we supplement our retirement income?”

ERIC AND SOPHIETHE NEED

• Supplemental retirement income

Case Study: Insured Annuity with a twist

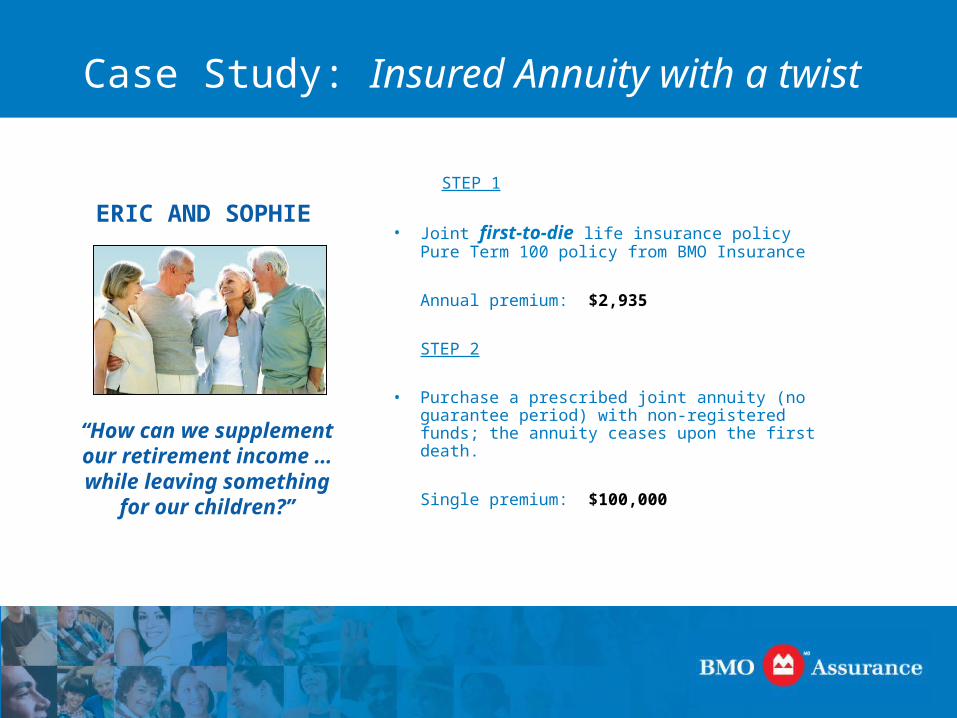

STEP 1

• Joint first-to-die life insurance policy Pure Term 100 policy from BMO Insurance

Annual premium: $2,935

STEP 2

• Purchase a prescribed joint annuity (no guarantee period) with non-registered funds; the annuity ceases upon the first death.

Single premium: $100,000

“How can we supplement our retirement income … while leaving something

for our children?”

ERIC AND SOPHIE

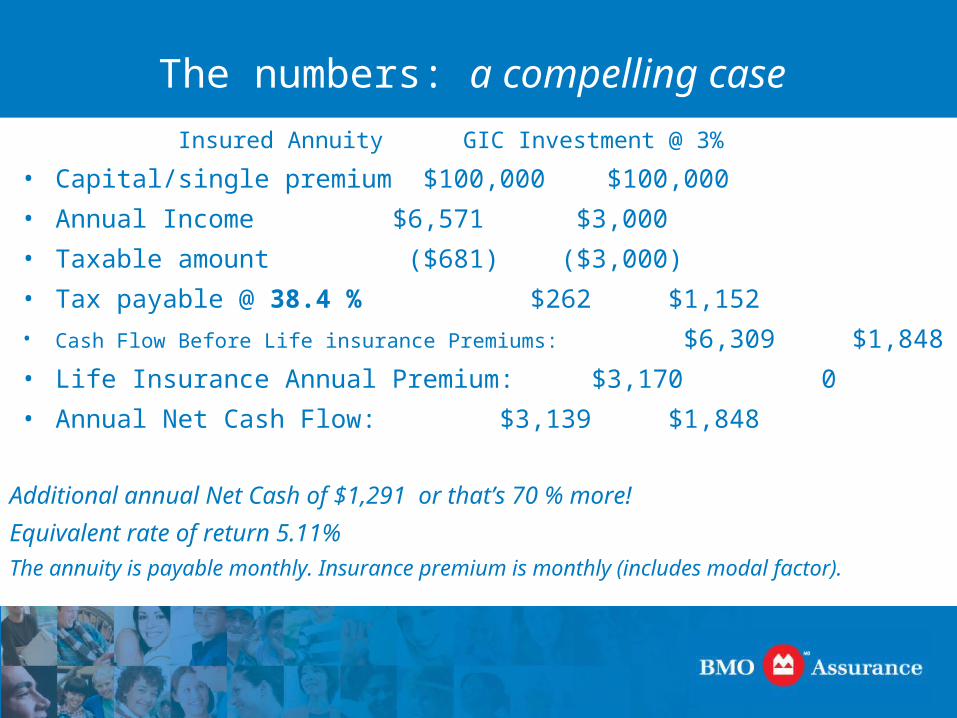

The numbers: a compelling case

Insured Annuity GIC Investment @ 3%

• Capital/single premium $100,000 $100,000

• Annual Income $6,571 $3,000

• Taxable amount ($681) ($3,000)

• Tax payable @ 38.4 % $262 $1,152

• Cash Flow Before Life insurance Premiums: $6,309 $1,848

• Life Insurance Annual Premium: $3,170 0

• Annual Net Cash Flow: $3,139 $1,848

Additional annual Net Cash of $1,291 or that’s 70 % more!

Equivalent rate of return 5.11%

The annuity is payable monthly. Insurance premium is monthly (includes modal factor).

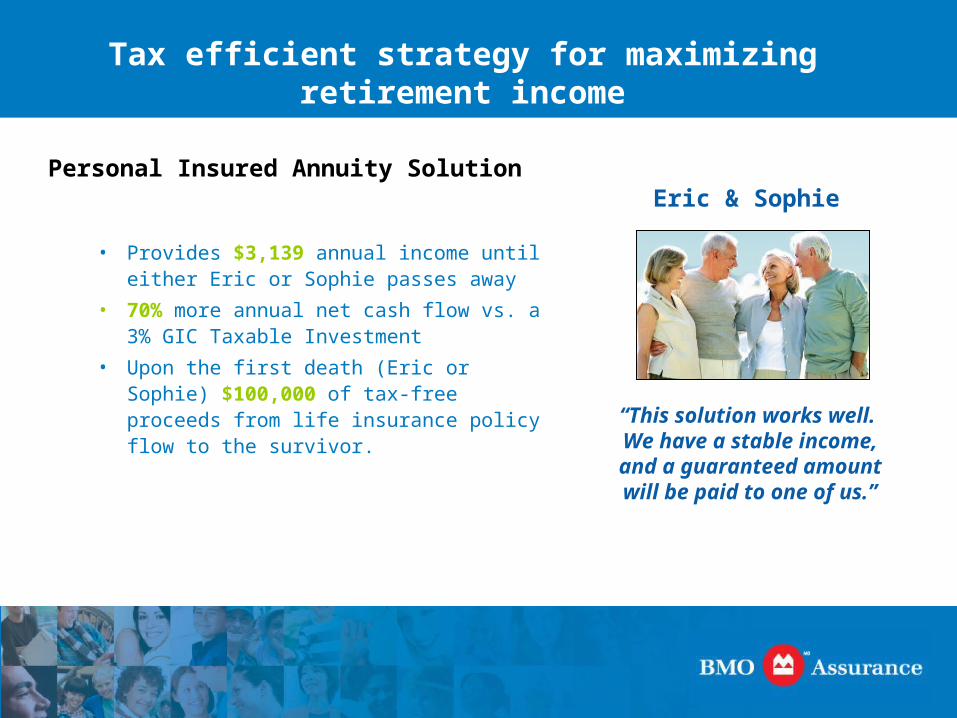

Tax efficient strategy for maximizing retirement income

• Provides $3,139 annual income until either Eric or Sophie passes away

• 70% more annual net cash flow vs. a 3% GIC Taxable Investment

• Upon the first death (Eric or Sophie) $100,000 of tax-free proceeds from life insurance policy flow to the survivor.

“This solution works well. We have a stable income, and a guaranteed amount will be paid to one of us.”

Eric & SophiePersonal Insured Annuity Solution

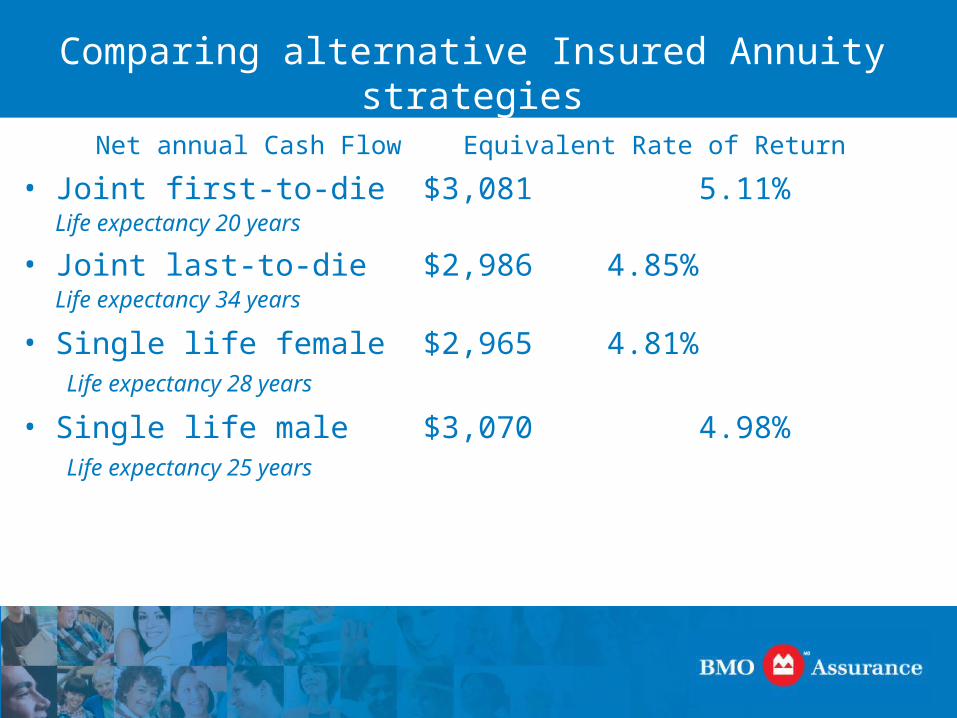

Comparing alternative Insured Annuity strategies

Net annual Cash Flow Equivalent Rate of

Return

• Joint first-to-die $3,081 5.11%Life expectancy 20 years

• Joint last-to-die $2,986 4.85%Life expectancy 34 years

• Single life female $2,965 4.81%Life expectancy 28 years

• Single life male $3,070 4.98%Life expectancy 25 years

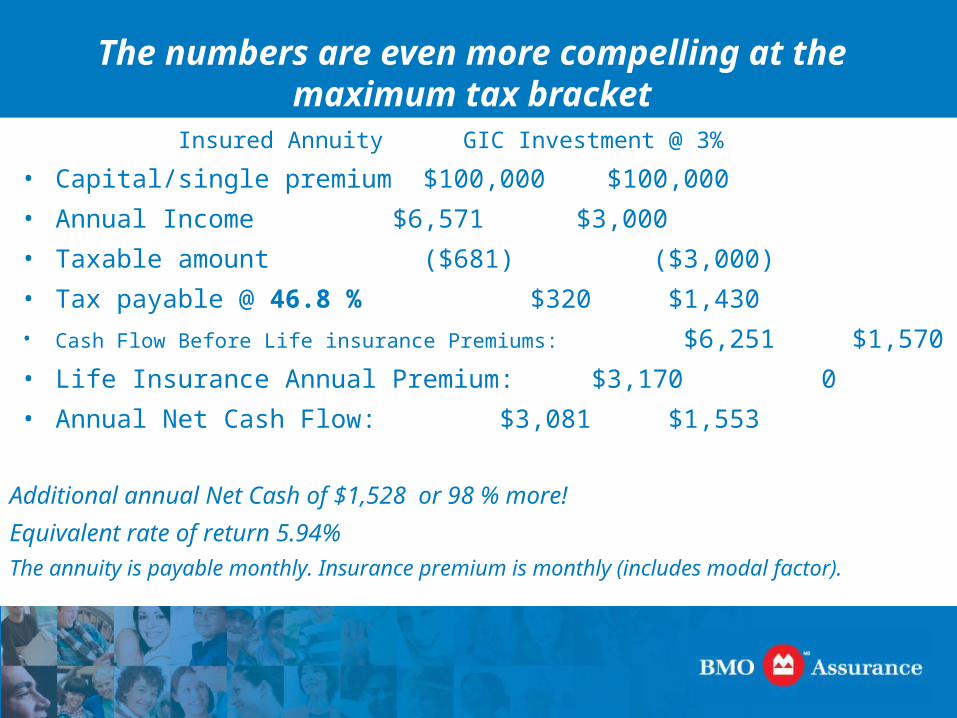

The numbers are even more compelling at the maximum tax bracket

Insured Annuity GIC Investment @ 3%

• Capital/single premium $100,000 $100,000

• Annual Income $6,571 $3,000

• Taxable amount ($681) ($3,000)

• Tax payable @ 46.8 % $320 $1,430

• Cash Flow Before Life insurance Premiums: $6,251 $1,570

• Life Insurance Annual Premium: $3,170 0

• Annual Net Cash Flow: $3,081 $1,553

Additional annual Net Cash of $1,528 or 98 % more!

Equivalent rate of return 5.94%

The annuity is payable monthly. Insurance premium is monthly (includes modal factor).

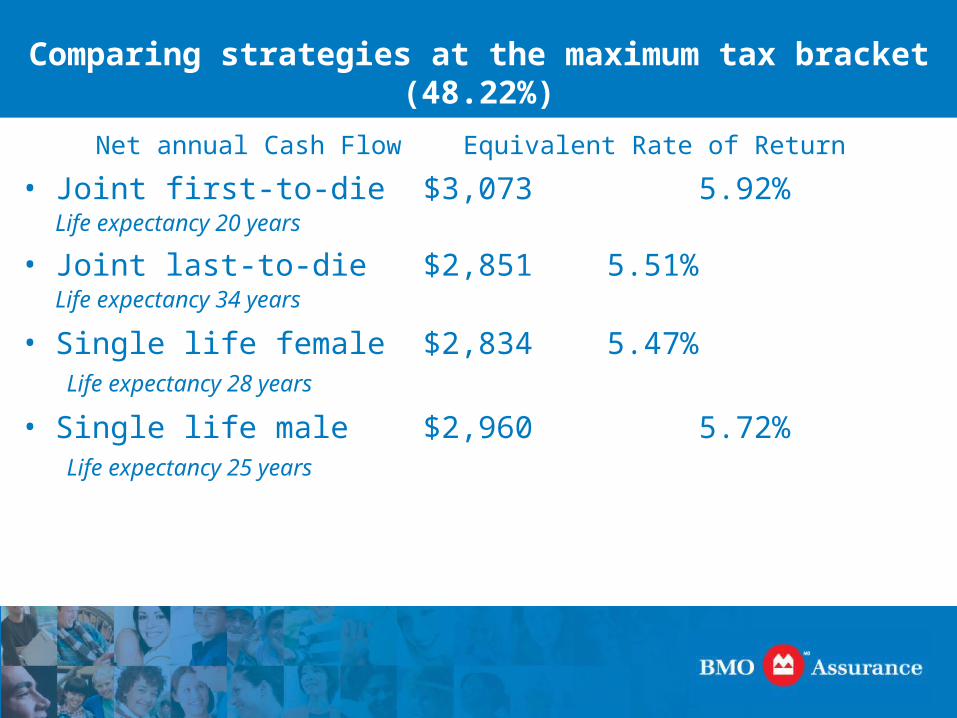

Comparing strategies at the maximum tax bracket (48.22%)

Net annual Cash Flow Equivalent Rate of

Return

• Joint first-to-die $3,073 5.92%Life expectancy 20 years

• Joint last-to-die $2,851 5.51%Life expectancy 34 years

• Single life female $2,834 5.47%Life expectancy 28 years

• Single life male $2,960 5.72%Life expectancy 25 years

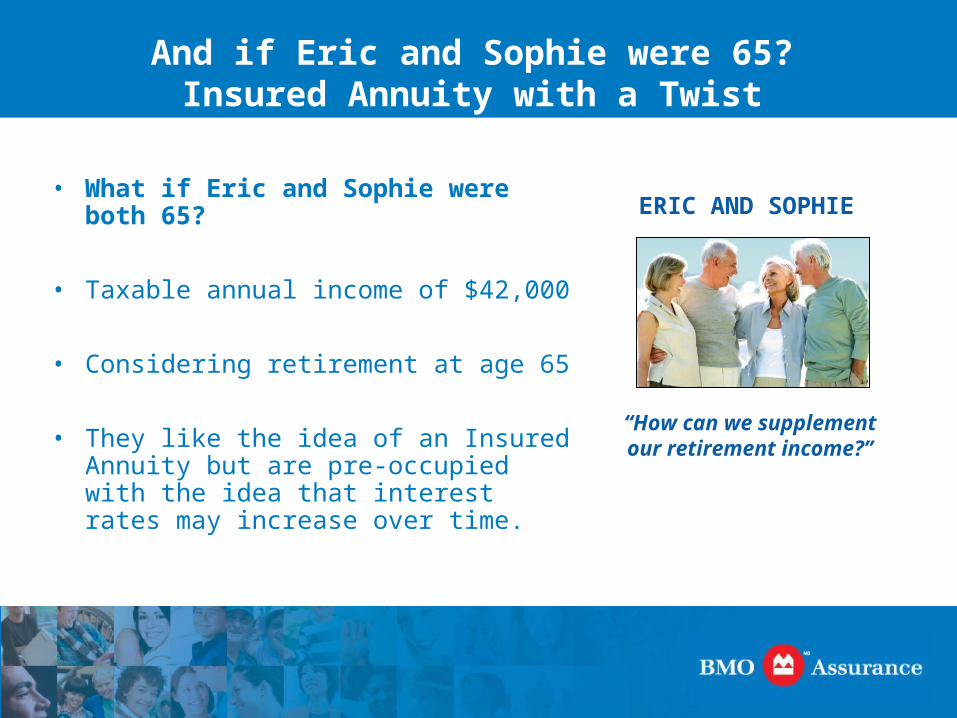

And if Eric and Sophie were 65?Insured Annuity with a Twist

• What if Eric and Sophie were both 65?

• Taxable annual income of $42,000

• Considering retirement at age 65

• They like the idea of an Insured Annuity but are pre-occupied with the idea that interest rates may increase over time.

“How can we supplement our retirement income?”

ERIC AND SOPHIE

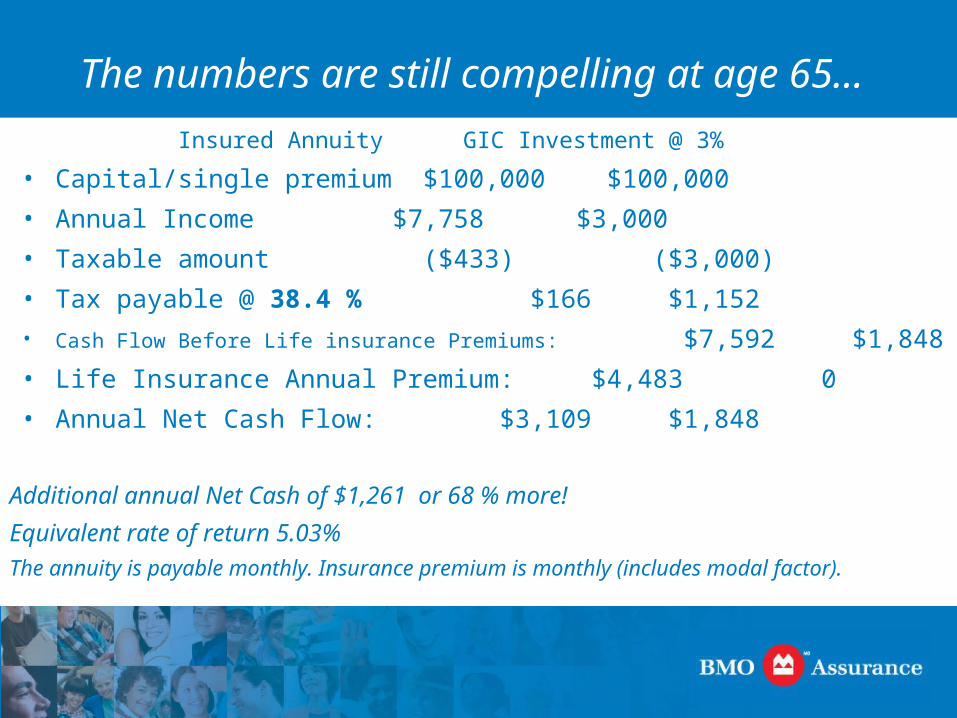

The numbers are still compelling at age 65…

Insured Annuity GIC Investment @ 3%

• Capital/single premium $100,000 $100,000

• Annual Income $7,758 $3,000

• Taxable amount ($433) ($3,000)

• Tax payable @ 38.4 % $166 $1,152

• Cash Flow Before Life insurance Premiums: $7,592 $1,848

• Life Insurance Annual Premium: $4,483 0

• Annual Net Cash Flow: $3,109 $1,848

Additional annual Net Cash of $1,261 or 68 % more!

Equivalent rate of return 5.03%

The annuity is payable monthly. Insurance premium is monthly (includes modal factor).

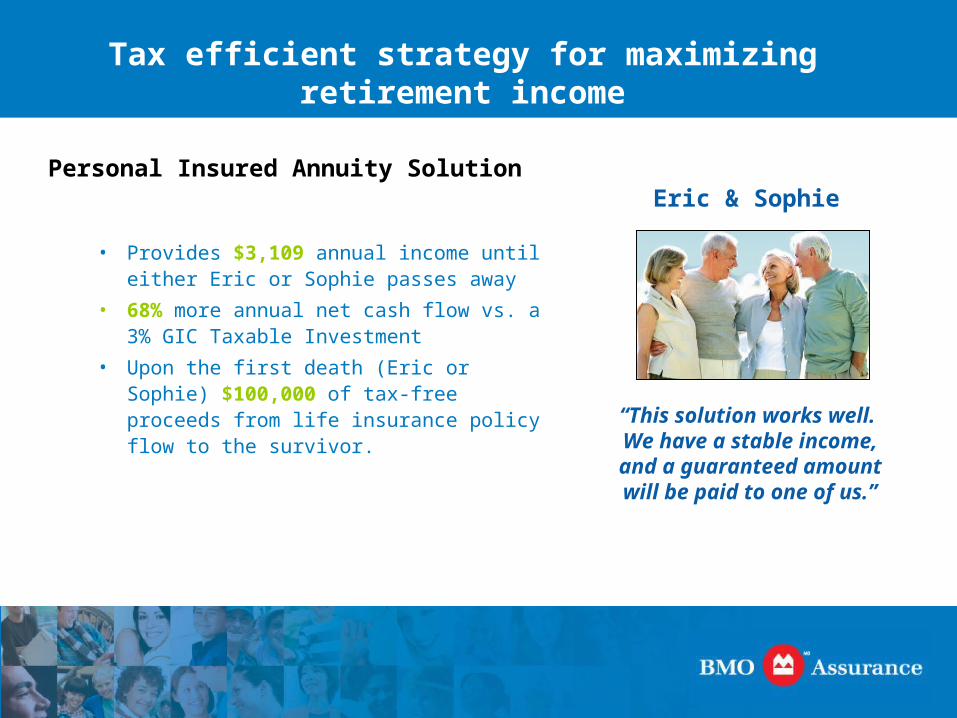

Tax efficient strategy for maximizing retirement income

• Provides $3,109 annual income until either Eric or Sophie passes away

• 68% more annual net cash flow vs. a 3% GIC Taxable Investment

• Upon the first death (Eric or Sophie) $100,000 of tax-free proceeds from life insurance policy flow to the survivor.

“This solution works well. We have a stable income, and a guaranteed amount will be paid to one of us.”

Eric & SophiePersonal Insured Annuity Solution

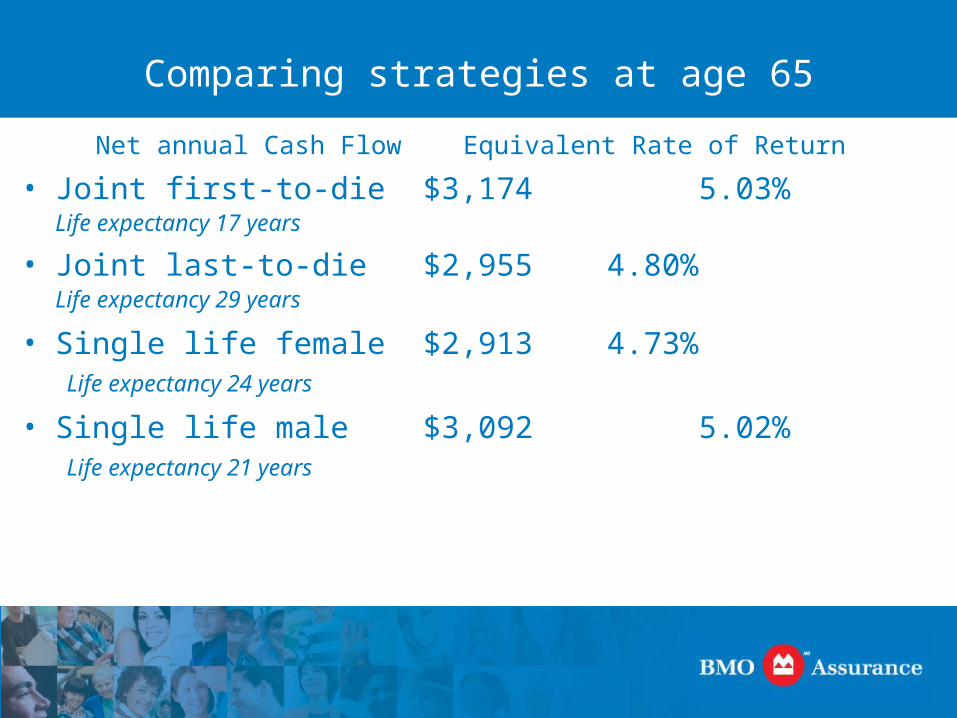

Comparing strategies at age 65

Net annual Cash Flow Equivalent Rate of

Return

• Joint first-to-die $3,174 5.03%Life expectancy 17 years

• Joint last-to-die $2,955 4.80%Life expectancy 29 years

• Single life female $2,913 4.73%Life expectancy 24 years

• Single life male $3,092 5.02%Life expectancy 21 years

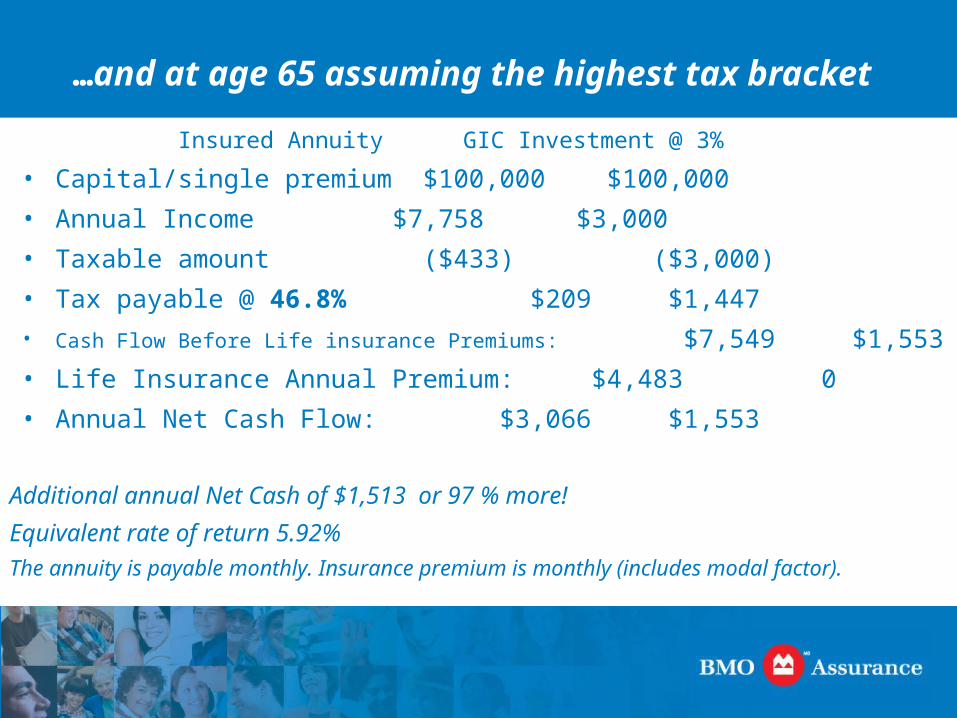

…and at age 65 assuming the highest tax bracket

Insured Annuity GIC Investment @ 3%

• Capital/single premium $100,000 $100,000

• Annual Income $7,758 $3,000

• Taxable amount ($433) ($3,000)

• Tax payable @ 46.8% $209 $1,447

• Cash Flow Before Life insurance Premiums: $7,549 $1,553

• Life Insurance Annual Premium: $4,483 0

• Annual Net Cash Flow: $3,066 $1,553

Additional annual Net Cash of $1,513 or 97 % more!

Equivalent rate of return 5.92%

The annuity is payable monthly. Insurance premium is monthly (includes modal factor).

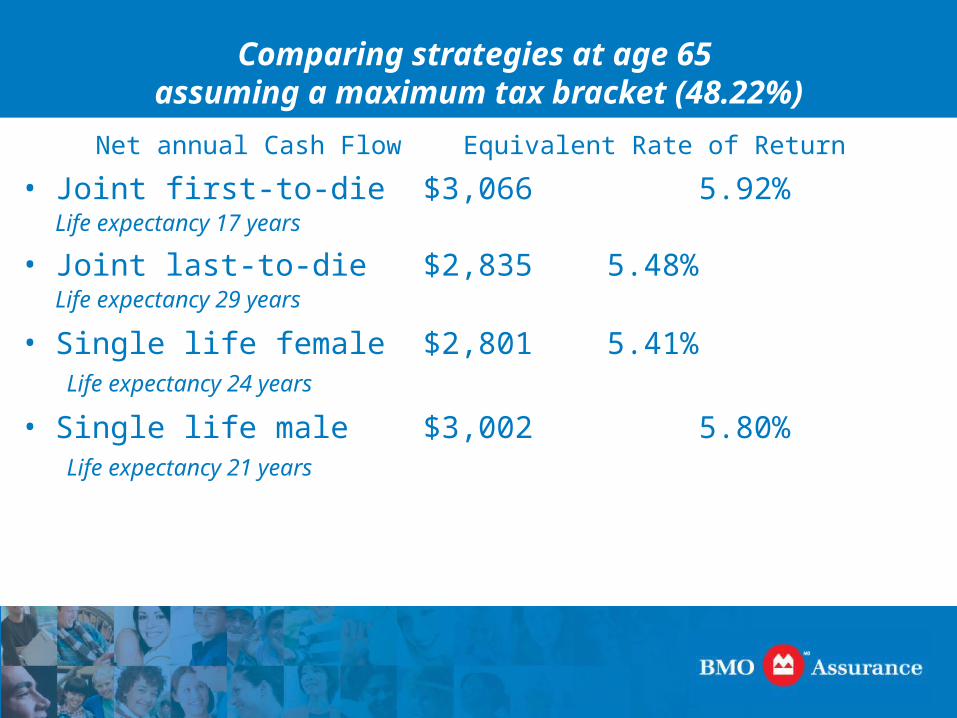

Comparing strategies at age 65 assuming a maximum tax bracket (48.22%)

Net annual Cash Flow Equivalent Rate of

Return

• Joint first-to-die $3,066 5.92%Life expectancy 17 years

• Joint last-to-die $2,835 5.48%Life expectancy 29 years

• Single life female $2,801 5.41%Life expectancy 24 years

• Single life male $3,002 5.80%Life expectancy 21 years