Embed Size (px)

Citation preview

This

by copyright

material may be protected

17 U.S. 285

Profiting from technological innovation:Implications for integration, collaboration,licensing and public policy

David J. TEECE *

School of Business Administration, of California, Berkeley, CA 94720, U.S.A.

Final version received June 1986

This paper attempts to explain why innovating firms oftenfail to obtain significant economic returns from an innovation,while customers, imitators and other industry participants be- nefit. Business strategy particularly as it relates to the firm’sdecision to integrate and collaborate is shown to be animportant factor. The paper demonstrates that when imitationis easy, markets don’t work well, and the profits from innova-tion may accrue to the owners of certain complementary assets,rather than to the developers of the intellectual property. Thisspeaks to the need, in certain cases, for the innovating firm toestablish a prior position in these complementary assets. Thepaper also indicates that innovators with new products andprocesses which provide value to consumers may sometimes beso ill positioned in the market that they necessarily will fail.The analysis provides a theoretical foundation for the proposi-tion that manufacturing often matters. particularly to innovat-ing nations. Innovating firms without the requisite ing and related capacities may die, even though they are thebest at innovation. Implications for trade policy and domesticeconomic policy are examined.

* I thank Raphael Harvey Brooks, Chris Therese Flaherty, Richard Gilbert, Heather MelHorwitch, David Carl Jacobsen, Michael Porter,Gary Richard Rumelt, Raymond Vernon and Sid-ney Winter for helpful discussions relating to the subjectmatter of this paper. Three anonymous referees also pro-vided valuable criticisms. I gratefully acknowledge thefinancial support of the National Science Foundation un-der grant no. SRS-8410556 to the Center for Research inManagement, University of California Berkeley. Earlierversions of this paper were presented at a National Academyof Engineering Symposium titled “World Technologies andNational Sovereignty,” February 1986, and at a conferenceon innovation at the University of Venice, March 1986.

Research Policy 15 (1986) 285-305North-Holland

It is quite common for innovators those firmswhich are first to commercialize a new product orprocess in the market to lament the fact thatcompetitors/imitators have profited more fromthe innovation than the firm first to commercializeit! Since it is often held that being first to marketis a source of strategic advantage, the clear ex-istence and persistence of this phenomenon mayappear perplexing if not troubling. The aim of thisarticle is to explain why a fast second or even aslow third might outperform the innovator. Themessage is particularly pertinent to those scienceand engineering driven companies that harbor themistaken illusion that developing new productswhich meet customer needs will ensure fabuloussuccess. It may possibly do so for the product, butnot for the innovator.

In this paper, a framework is offered whichidentifies the factors which determine who winsfrom innovation: the firm which is first to market,follower firms, or firms that have related capabili-ties that the innovator needs. The follower firmsmay or may not be imitators in the narrow senseof the term, although they sometimes are. Theframework appears to have utility for explainingthe share of the profits from innovation accruingto the innovator compared to its followers andsuppliers (see fig. as well as for explaining avariety of interfirm activities such as joint ven-tures, coproduction agreements, cross distributionarrangements, and technology licensing. Implica-tions for strategic management, public policy, andinternational trade and investment are then dis-cussed.

Elsevier Science Publishers B.V. (North-Holland)

2 8 6

What determines the share of profits captured by theinnovatof?

Fig. 1. Explaining the distribution of the profits from innova-tion.

2. The phenomenon

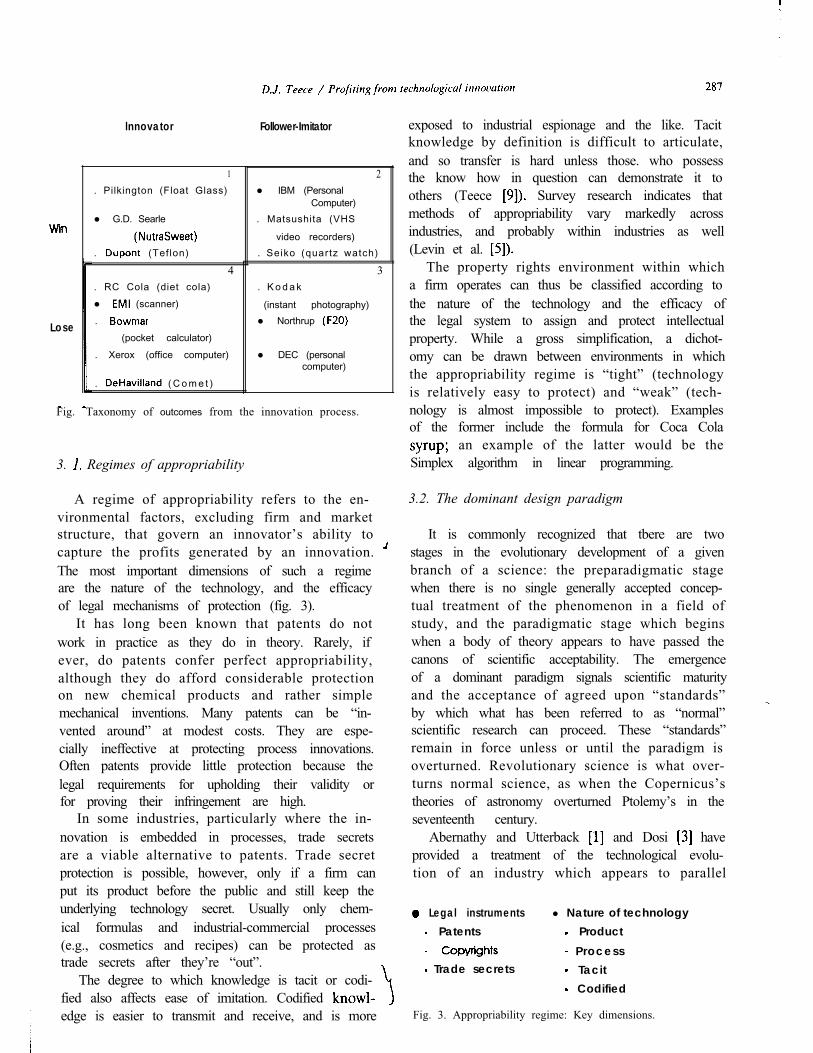

Figure 2 presents a simplified taxonomy of thepossible outcomes from innovation. Quadrant 1represents positive outcomes for the innovator. Afirst-to-market advantage is translated into a sus-tained competitive advantage which either createsa new earnings stream or enhances an existingone. Quadrant 4 and its corollary quadrant 2 arethe ones which are the focus of this paper.

The EM1 CAT scanner is a classic case of thephenomenon to be investigated. By the early

the UK firm Electrical Musical Industries Ltd. was in a variety of product lines

including phonographic records, movies, and ad-vanced electronics. EM1 had developed high reso-lution TVs in the pioneered airborne radarduring World War II, and developed the UK’sfirst all solid-state computers in 1952.

In the late 1960s Godfrey Houndsfield, an EM1senior research engineer engaged in pattern recog-nition research which resulted in his displaying ascan of a pig’s brain. Subsequent clinical workestablished that computerized axial tomography(CAT) was viable for generating cross-sectional“views” of the human body, the greatest advancein radiology since the discovery of X rays in 1895.

While was initially successful with its CAT

The story is summarized in Michael Martin,

Publishing Company, VA, 1984).

scanner, within 6 years of its introduction into theUS in 1973 the company had lost market leader-ship, and by the eighth year had dropped out ofthe CT scanner business, Other companies suc-cessfully dominated the market, though they werelate entrants, and are still profiting in the businesstoday.

Other examples include RC Cola, a small be-verage company that was the first to introducecola in a can, and the first to introduce diet cola.Both Coca Cola and Pepsi followed almost im-mediately and deprived RC of any significantadvantage from its innovation. whichintroduced the pocket calculator, was not able towithstand competition from Texas Instruments,Hewlett Packard and others, and went out ofbusiness. Xerox failed to succeed with its entryinto the office computer business, even thoughApple succeeded with the which con-tained many of Xerox’s key product ideas, such asthe mouse and icons. The de Havilland Cometsaga has some of the same features. The Comet Ijet was introduced into the commercial airlinebusiness 2 years or so before Boeing introducedthe 707, but de Havilland failed to capitalize on itssubstantial early advantage. MITS introduced thefirst personal computer, the Altair, experienced aburst of sales, then slid quietly into oblivion.

If there are innovators who lose there must befollowers/imitators who win. A classic example isIBM with its PC, a great success since the time itwas introduced in 1981. Neither the architecturenor components embedded in the IBM PC wereconsidered advanced when introduced; nor wasthe way the technology was packaged a significantdeparture from then-current practice. Yet the IBMPC was fabulously successful and established DOS as the leading operating system for 16-bitPCs. By the end of 1984, IBM has shipped over500000 PCs, and many considered that it hadirreversibly eclipsed Apple in the PC industry.

3. Profiting from innovation: Basic building blocks

In order to develop a coherent framework withinwhich to explain the distribution of outcomesillustrated in fig. 2, three fundamental buildingblocks must first be put in place: the ity regime, complementary assets, and the domi-nant design paradigm.

Lose

Fig.

lnnovator Follower-Imitator

1

. Pilkington (Float Glass)

!" G.D. Searle

. (Teflon)

4. RC Cola (diet cola)

!" (scanner)

.

(pocket calculator)

. Xerox (office computer)

. ( C o m e t )

2!" IBM (Personal

Computer)

. Matsushita (VHS

video recorders)

. Seiko (quartz watch)

3. K o d a k

(instant photography)

!" Northrup

!" DEC (personalcomputer)

Taxonomy of outcomes from the innovation process.

3. Regimes of appropriability

A regime of appropriability refers to the en-vironmental factors, excluding firm and marketstructure, that govern an innovator’s ability tocapture the profits generated by an innovation. The most important dimensions of such a regimeare the nature of the technology, and the efficacyof legal mechanisms of protection (fig. 3).

It has long been known that patents do notwork in practice as they do in theory. Rarely, ifever, do patents confer perfect appropriability,although they do afford considerable protectionon new chemical products and rather simplemechanical inventions. Many patents can be “in-vented around” at modest costs. They are espe-cially ineffective at protecting process innovations.Often patents provide little protection because thelegal requirements for upholding their validity orfor proving their infringement are high.

In some industries, particularly where the in-novation is embedded in processes, trade secretsare a viable alternative to patents. Trade secretprotection is possible, however, only if a firm canput its product before the public and still keep theunderlying technology secret. Usually only chem-ical formulas and industrial-commercial processes(e.g., cosmetics and recipes) can be protected astrade secrets after they’re “out”.

The degree to which knowledge is tacit or codi-fied also affects ease of imitation. Codified edge is easier to transmit and receive, and is more

exposed to industrial espionage and the like. Tacitknowledge by definition is difficult to articulate,and so transfer is hard unless those. who possessthe know how in question can demonstrate it toothers (Teece Survey research indicates thatmethods of appropriability vary markedly acrossindustries, and probably within industries as well(Levin et al.

The property rights environment within whicha firm operates can thus be classified according tothe nature of the technology and the efficacy ofthe legal system to assign and protect intellectualproperty. While a gross simplification, a dichot-omy can be drawn between environments in whichthe appropriability regime is “tight” (technologyis relatively easy to protect) and “weak” (tech-nology is almost impossible to protect). Examplesof the former include the formula for Coca Cola

an example of the latter would be theSimplex algorithm in linear programming.

3.2. The dominant design paradigm

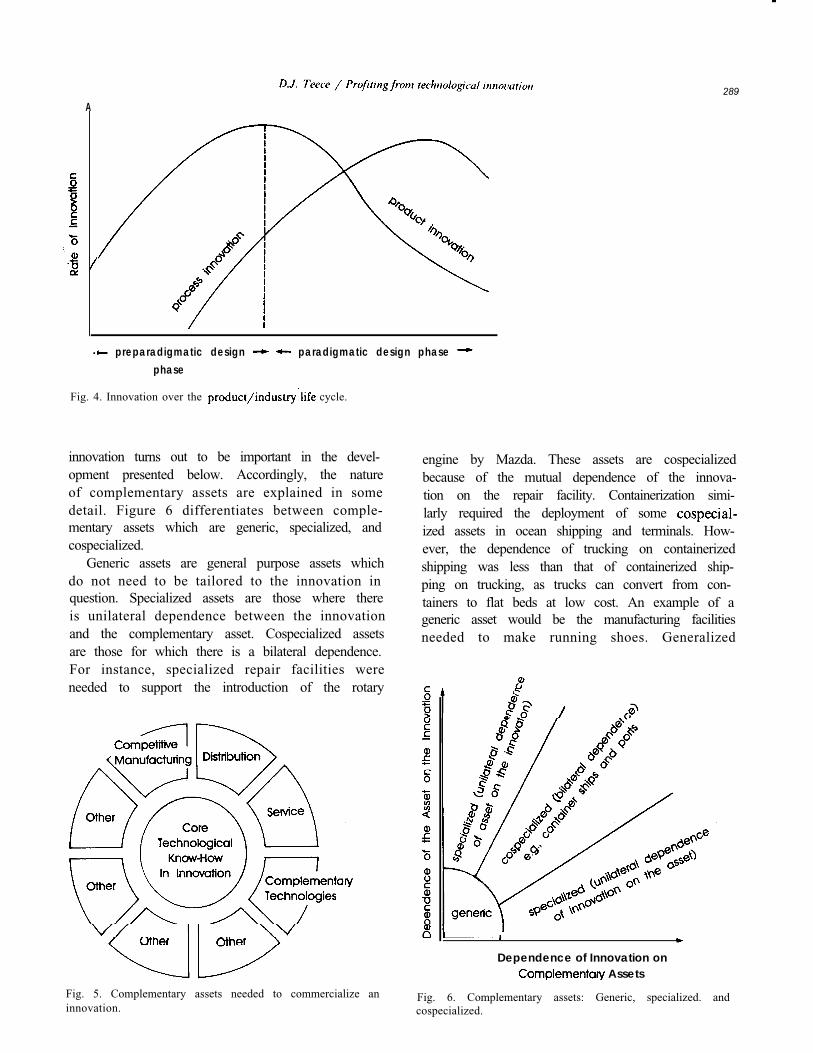

It is commonly recognized that tbere are twostages in the evolutionary development of a givenbranch of a science: the preparadigmatic stagewhen there is no single generally accepted concep-tual treatment of the phenomenon in a field ofstudy, and the paradigmatic stage which beginswhen a body of theory appears to have passed thecanons of scientific acceptability. The emergenceof a dominant paradigm signals scientific maturityand the acceptance of agreed upon “standards”by which what has been referred to as “normal”scientific research can proceed. These “standards”remain in force unless or until the paradigm isoverturned. Revolutionary science is what over-turns normal science, as when the Copernicus’stheories of astronomy overturned Ptolemy’s in theseventeenth century.

Abernathy and Utterback and Dosi haveprovided a treatment of the technological evolu-tion of an industry which appears to parallel

Legal instruments Patents Trade secrets

!"Nature of technology Product

Process Tacit Codified

Fig. 3. Appropriability regime: Key dimensions.

288

notions of scientific evolution. theearly stages of industry development, product de-signs are fluid, manufacturing processes are looselyand adaptively organized, and generalized capitalis used in production. Competition amongst firmsmanifests itself in competition amongst designs,which are markedly different from each other.This might be called the preparadigmatic stage ofan industry.

At some point in time, and after considerabletrial and error in the marketplace, one design or anarrow class of designs begins to emerge as themore promising. Such a design must be able tomeet a whole set of user needs in a relativelycomplete fashion. The Model T Ford, the IBM360, and the Douglas DC-3 are examples of domi-nant designs in the automobile, computer, andaircraft industry respectively.

Once a dominant design emerges, competitionshifts to price and away from design. Competitivesuccess then shifts to a whole new set of variables.

Scale and learning become much more important,and specialized capital gets deployed as in-cumbent’s seek to lower unit costs through ex-ploiting economies of scale and learning. Reduceduncertainty over product design provides an op-portunity toamortize specialized long-lived invest-ments.

Innovation is not necessarily halted once thedominant design emerges; as Clarke points out,it can occur lower down in the design hierarchy.For instance, a cylinder configuration emergedin automobile engine blocks during the 1930s withthe emergence of the Ford V-8 engine. Nicheswere quickly found for it. Moreover, once theproduct design stabilizes, there is likely to be asurge of process innovation as producers attemptto lower production costs for the new product (seefig. 4).

The Abernathy-Utterback framework does notcharacterize all industries. It seems more suited tomass markets where consumer tastes are relativelyhomogeneous. It would appear to be less char-acteristic of small niche markets where the ab-sence of scale and learning economies attachesmuch less of a penalty to multiple designs. Inthese instances, generalized equipment will be em-ployed in production.

See Kuhn

The existence of a dominant design watershedis of great significance to the distribution of its between innovator and follower. The innovatormay have been responsible for the fundamentalscientific breakthroughs as well as the basic designof the new product. However, if imitation is rela-tively easy, imitators may enter the fray, modify-ing the product in important ways, yet relying onthe fundamental designs pioneered by the innova-tor. When the game of musical chairs stops, and adominant design emerges, the innovator mightwell end up positioned disadvantageously relativeto a follower. Hence, when imitation is possibleand occurs coupled with design modification fore the emergence of a dominant design, fol-lowers have a good chance of having their mod-ified product annointed as the industry standard,often to the great disadvantage of the innovator.

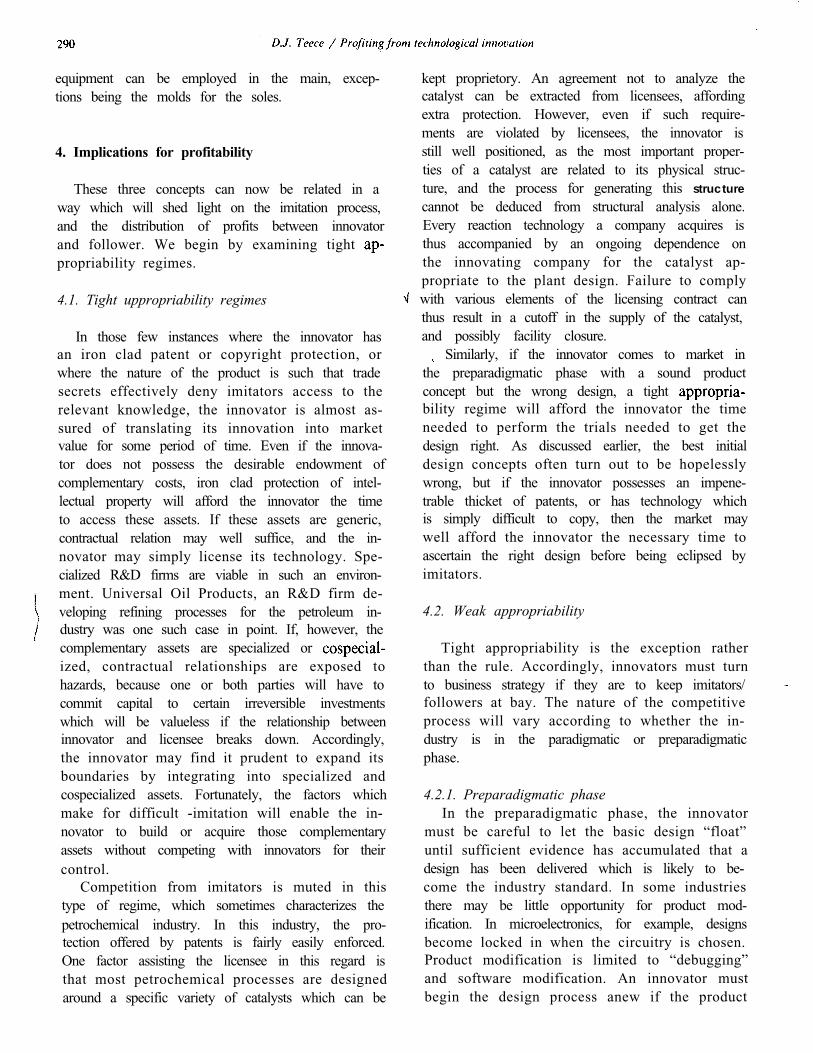

3.3. Complementary assets

Let the unit of analysis be an innovation. Aninnovation consists of certain technical knowledgeabout how to do things better than the existingstate of the art. Assume that the know-how inquestion is partly codified and partly tacit. Inorder for such know-how to, generate profits, itmust be sold or utilized in some fashion in themarket.

In almost all cases, the successful commerciali-zation of an innovation requires that the know-howin question be utilized in conjunction with othercapabilities or assets. Services such as marketing,competitive manufacturing, and after-sales sup-port are almost always needed. These services areoften obtained from complementary assets whichare specialized. For example, the commercializa-tion of a new drug is likely to require the dissemi-nation of information over a specialized tion channel. In some cases, as when the innova-tion is systemic, the complementary assets may be

other parts of a system. For instance; computerhardware typically requires specialized software,both for the operating system, as well as forapplications. Even when an innovation is

J as with plug compatible components, cer-tain complementary capabilities or assets will beneeded for successful commercialization. Figure 5summarizes this schematically.

Whether the assets required for least cost pro-duction and distribution are specialized to the

A

. preparadigmatic design paradigmatic design phase phase

Fig. 4. Innovation over the cycle.

innovation turns out to be important in the devel-opment presented below. Accordingly, the natureof complementary assets are explained in somedetail. Figure 6 differentiates between comple-mentary assets which are generic, specialized, andcospecialized.

Generic assets are general purpose assets whichdo not need to be tailored to the innovation inquestion. Specialized assets are those where thereis unilateral dependence between the innovationand the complementary asset. Cospecialized assetsare those for which there is a bilateral dependence.For instance, specialized repair facilities wereneeded to support the introduction of the rotary

Fig. 5. Complementary assets needed to commercialize aninnovation.

289

engine by Mazda. These assets are cospecializedbecause of the mutual dependence of the innova-tion on the repair facility. Containerization simi-larly required the deployment of some ized assets in ocean shipping and terminals. How-ever, the dependence of trucking on containerizedshipping was less than that of containerized ship-ping on trucking, as trucks can convert from con-tainers to flat beds at low cost. An example of ageneric asset would be the manufacturing facilitiesneeded to make running shoes. Generalized

Dependence of Innovation on Assets

Fig. 6. Complementary assets: Generic, specialized. andcospecialized.

equipment can be employed in the main, excep-tions being the molds for the soles.

4. Implications for profitability

These three concepts can now be related in away which will shed light on the imitation process,and the distribution of profits between innovatorand follower. We begin by examining tight propriability regimes.

4.1. Tight uppropriability regimes

In those few instances where the innovator hasan iron clad patent or copyright protection, orwhere the nature of the product is such that tradesecrets effectively deny imitators access to therelevant knowledge, the innovator is almost as-sured of translating its innovation into marketvalue for some period of time. Even if the innova-tor does not possess the desirable endowment ofcomplementary costs, iron clad protection of intel-lectual property will afford the innovator the timeto access these assets. If these assets are generic,contractual relation may well suffice, and the in-novator may simply license its technology. Spe-cialized R&D firms are viable in such an environ-ment. Universal Oil Products, an R&D firm de-veloping refining processes for the petroleum in-dustry was one such case in point. If, however, thecomplementary assets are specialized or ized, contractual relationships are exposed tohazards, because one or both parties will have tocommit capital to certain irreversible investmentswhich will be valueless if the relationship betweeninnovator and licensee breaks down. Accordingly,the innovator may find it prudent to expand itsboundaries by integrating into specialized andcospecialized assets. Fortunately, the factors whichmake for difficult -imitation will enable the in-novator to build or acquire those complementaryassets without competing with innovators for theircontrol.

Competition from imitators is muted in thistype of regime, which sometimes characterizes thepetrochemical industry. In this industry, the pro-tection offered by patents is fairly easily enforced.One factor assisting the licensee in this regard isthat most petrochemical processes are designedaround a specific variety of catalysts which can be

kept proprietory. An agreement not to analyze thecatalyst can be extracted from licensees, affordingextra protection. However, even if such require-ments are violated by licensees, the innovator isstill well positioned, as the most important proper-ties of a catalyst are related to its physical struc-ture, and the process for generating this structurecannot be deduced from structural analysis alone.Every reaction technology a company acquires isthus accompanied by an ongoing dependence onthe innovating company for the catalyst ap-propriate to the plant design. Failure to comply

with various elements of the licensing contract canthus result in a cutoff in the supply of the catalyst,and possibly facility closure.

Similarly, if the innovator comes to market inthe preparadigmatic phase with a sound productconcept but the wrong design, a tight bility regime will afford the innovator the timeneeded to perform the trials needed to get thedesign right. As discussed earlier, the best initialdesign concepts often turn out to be hopelesslywrong, but if the innovator possesses an impene-trable thicket of patents, or has technology whichis simply difficult to copy, then the market maywell afford the innovator the necessary time toascertain the right design before being eclipsed byimitators.

4.2. Weak appropriability

Tight appropriability is the exception ratherthan the rule. Accordingly, innovators must turnto business strategy if they are to keep imitators/followers at bay. The nature of the competitiveprocess will vary according to whether the in-dustry is in the paradigmatic or preparadigmaticphase.

4.2.1. Preparadigmatic phaseIn the preparadigmatic phase, the innovator

must be careful to let the basic design “float”until sufficient evidence has accumulated that adesign has been delivered which is likely to be-come the industry standard. In some industriesthere may be little opportunity for product mod-ification. In microelectronics, for example, designsbecome locked in when the circuitry is chosen.Product modification is limited to “debugging”and software modification. An innovator mustbegin the design process anew if the product

doesn’t fit the market well. In some respects,however, selecting designs is dictated by the needto meet certain compatibility standards so thatnew hardware can interface with existing appli-cations software. In one sense, therefore, the de-sign issue for the microprocessor industry today isrelatively straightforward: deliver greater powerand speed while meeting the the computer in-dustry standards of the existing software base.However, from time to time windows of opportun-ity emerge for the introduction of entirely newfamilies of microprocessors which will define anew industry and software standard. In these in-stances, basic design parameters are less well de-fined, and can be permitted to “float” until marketacceptance is apparent.

The early history of the automobile industryexemplifies exceedingly well the importance forsubsequent success of selecting the right design inthe preparadigmatic stages. None of the earlyproducers of steam cars survived the early shakeoutwhen the closed body internal engineautomobile emerged as the dominant design. Thesteam car, nevertheless, had numerous earlyvirtues, such as reliability, which the internal com-bustion engine autos could not deliver.

The British fiasco with the Comet I is alsoinstructive. De Havilland had picked an earlydesign with both technical and commercial flaws.By moving into production, significant bilities and loss of reputation hobbled de Havil-land to such a degree that it was unable to convertto the Boeing design which subsequently emergedas dominant. It wasn’t even able to occupy secondplace, which went instead to Douglas.

As a general principle, it appears that tors in weak appropriability regimes need to bei intimately coupled to the market so that user needs can fully impact designs. When multiple

parallel and sequential prototyping is feasible, it has clear advantages. Generally such an approachis simply prohibitively costly. When developmentcosts for a large commercial aircraft exceed onebillion dollars, variations on a theme are all that ispossible.

Hence, the probability that an innovator defined here as a firm that is first to commercial-ize a new product design concept will enter theparadigmatic phase possessing the dominantdesign is problematic. The probabilities will behigher the lower the relative cost of prototyping,

and the more tightly coupled the firm is to themarket. The later is a function of organizationaldesign, and can be influenced by managerialchoices. The former is embedded the technol-ogy, and cannot be influenced, except in minorways, by managerial decisions. Hence, in in-dustries with large developmental and prototyping

, costs and hence significant irreversibilities and where innovation of the product concept is

. easy, then one would expect that the probabilitythat the innovator would emerge as the winner oramongst the winners at the end of the

stage is low.

4.2.2. Paradigmatic stage. In the preparadigmatic phase, complementary

assets do not loom large. Rivalry is focused ontrying to identify the design which will be domi-nant. Production volumes are low, and there islittle to be gained in deploying specialized assets,as scale economies are unavailable, and price isnot a principal competitive factor. However, asthe leading design or designs begin to be revealedby the market, volumes increase and opportunitiesfor economies of scale will induce firms to begingearing up for mass production by acquiring spe-cialized tooling and equipment, and possibly spe-cialized distribution as well. Since these invest-

. ments involve significant irreversibilities, pro-ducers are likely to proceed with caution. Islandsof specialized capital will begin to appear in anindustry, which otherwise features a sea of generalpurpose manufacturing equipment.

JHowever, as the terms of competition begin to

change, and prices become increasingly unim-portant, access to complementary assets becomesabsolutely critical. Since the core technology iseasy to imitate, by assumption, commercial successswings upon the terms and conditions upon whichthe required complementary assets can be accessed.

It is at this point that speeialized and ized assets become critically important. Gener-alized equipment and skills, almost by definition,are always available in an industry, and even ifthey are not, they do not involve significant versibilities. Accordingly, firms have easy accessto this type of capital, and even if there is insuffi-cient capacity available in the relevant assets, itcan easily be put in place as it involves few risks.Specialized assets, on the other hand, involve sig-nificant irreversibilities and cannot be easily

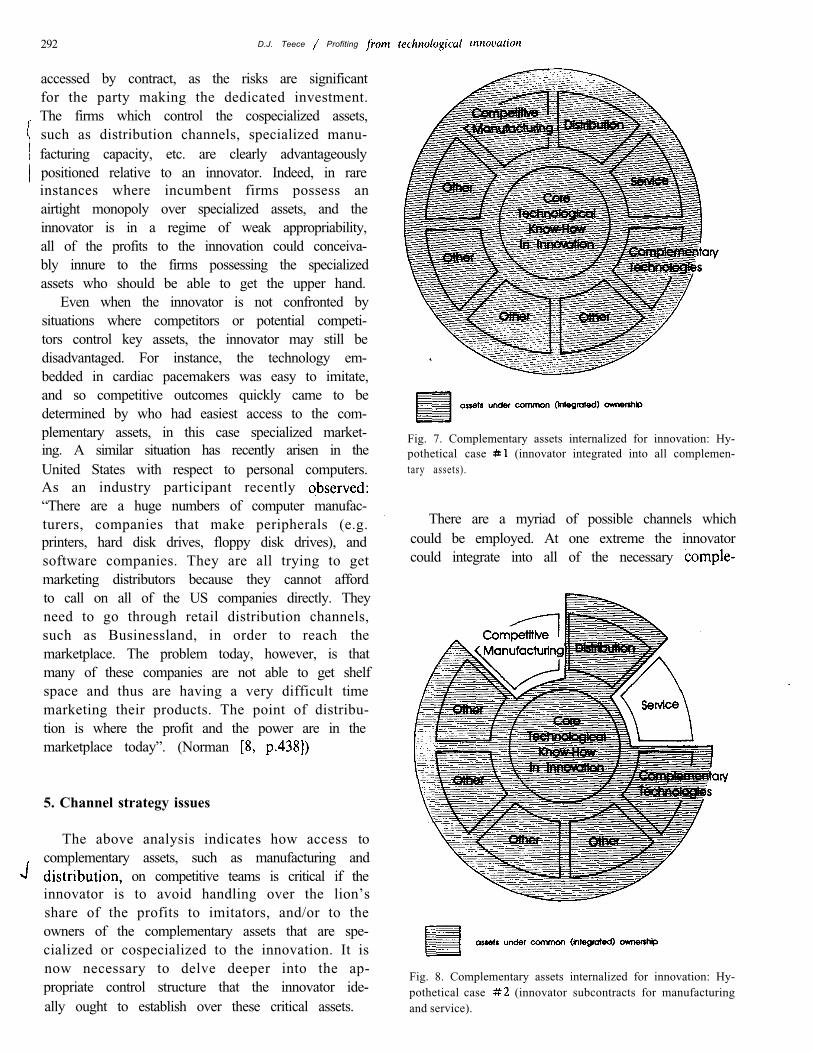

292 D.J. Teece Profiting

accessed by contract, as the risks are significantfor the party making the dedicated investment.The firms which control the cospecialized assets,such as distribution channels, specialized manu-facturing capacity, etc. are clearly advantageously

positioned relative to an innovator. Indeed, in rareinstances where incumbent firms possess anairtight monopoly over specialized assets, and theinnovator is in a regime of weak appropriability,all of the profits to the innovation could conceiva-bly innure to the firms possessing the specializedassets who should be able to get the upper hand.

Even when the innovator is not confronted bysituations where competitors or potential competi-tors control key assets, the innovator may still bedisadvantaged. For instance, the technology em-bedded in cardiac pacemakers was easy to imitate,and so competitive outcomes quickly came to bedetermined by who had easiest access to the com-plementary assets, in this case specialized market-ing. A similar situation has recently arisen in theUnited States with respect to personal computers.As an industry participant recently “There are a huge numbers of computer manufac-turers, companies that make peripherals (e.g.printers, hard disk drives, floppy disk drives), andsoftware companies. They are all trying to getmarketing distributors because they cannot affordto call on all of the US companies directly. Theyneed to go through retail distribution channels,such as Businessland, in order to reach themarketplace. The problem today, however, is thatmany of these companies are not able to get shelfspace and thus are having a very difficult timemarketing their products. The point of distribu-tion is where the profit and the power are in themarketplace today”. (Norman

5. Channel strategy issues

The above analysis indicates how access tocomplementary assets, such as manufacturing and

on competitive teams is critical if theinnovator is to avoid handling over the lion’sshare of the profits to imitators, and/or to theowners of the complementary assets that are spe-cialized or cospecialized to the innovation. It isnow necessary to delve deeper into the ap-propriate control structure that the innovator ide-ally ought to establish over these critical assets.

Fig. 7. Complementary assets internalized for innovation: Hy-pothetical case (innovator integrated into all complemen-tary assets).

There are a myriad of possible channels whichcould be employed. At one extreme the innovatorcould integrate into all of the necessary

Fig. 8. Complementary assets internalized for innovation: Hy-pothetical case (innovator subcontracts for manufacturingand service).

D.J. from technological 293

mentary assets, as illustrated in fig. 7, or just a fewof them, as illustrated in fig. 8. Complete integra-tion (fig. 7) is likely to be unnecessary as well asprohibitively expensive. It is well to recognize that the variety of assets and which needto be accessed is likely to be quite large, even foronly modestly complex technologies. To produce apersonal computer, for instance, a company needsaccess to expertise in semiconductor technology,display technology, disk drive technology, net-working technology, keyboard technology, andseveral others. No company can keep pace in allof these areas by itself.

At the other extreme, the innovator could at-tempt to access these assets through straightfor-ward contractual relationships (e.g. componentsupply contracts, fabrication contracts, servicecontracts, etc.). In many instances such contractsmay suffice, although it sometimes exposes theinnovator to various hazards and dependencies J

that it may well wish to avoid. In between thefully integrated and full contractual extremes, thereare a myriad of intermediate forms and channelsavailable. An analysis of the properties of the twoextreme forms is presented below. A brief synop-sis of mixed modes then follows.

5.1. Contractual modes

The advantages of a contractual solution whereby the innovator signs a contract, such as alicense, with independent suppliers, manufacturersor distributors are obvious. The innovator willnot have to make the capital expendituresneeded to build or buy the assets in question. Thisreduces risks as well as cash requirements.

Contracting rather than integrating is likely tobe the optimal strategy when the innovators propriability regime is tight and the complemen- tary assets are available in competitive supply (i.e.there is adequate capacity and a choice of sources).

Both conditions apply in petrochemicals forinstance, so an innovator doesn’t need to be in-tegrated to be a successful. Consider, first, theappropriability regime. As discussed earlier, theprotection offered by patents is fairly easily en-forced, for process technology, in thepetrochemical industry. Given the advantageousfeedstock prices available in hydrocarbon rich pet-rochemical exporters, and the appropriability reg-ime characteristic of this industry, there is no

incentive or advantage in owning the complemen-tary assets (production facilities) as they are nottypically highly specialized to the innovation. Un-ion Carbide appears to realize this; and has re-cently adjusted its strategy accordingly. Essen-tially, Carbide is placing its existing technologyinto a new subsidiary, Engineering and Hydro-carbons Service. The company is engaging inlicensing and offers engineering, construction, andmanagement services to customers who want totake their feedstocks and integrate them forwardinto petrochemicals. But Carbide itself appears tobe backing away from an integration strategy.

Chemical and petrochemical product innova-tions are not quite so easy to protect, which shouldraise new challenges to innovating firms in thedeveloped nations as they attempt to shift out ofcommodity petrochemicals. There are alreadynumerous examples of new products that made itto the marketplace, filled a customer need, butnever generated competitive returns to the innova-tor because of imitation. For example, in the1960s Dow decided to start manufacturing rigidpolyurethene foam. However, it was imitated veryquickly by numerous small firms which had lowercosts. The absence of low cost manufacturingcapability left Dow vulnerable.

Contractual relationships can bring addedcredibility to the innovator, especially if the in-novator is relatively unknown when the contract- ual partner is established and viable. Indeed,arms-length contracting which embodies more thana simple buy-sell agreement is becoming so com-mon, and is so multifaceted, that the term stra-tegic partnering has been devised to describe it.Even large companies such as IBM are now engag-ing in it. For IBM, partnering buys access to newtechnologies enabling the company to “learnthings we couldn’t have learned without manyyears of trial and error.” IBM’s arrangementwith Microsoft to use the latter’s MS-DOS operat-ing system software on the IBM PC facilitated thetimely introduction of IBM’s personal computerinto the market.

Executive V.P. Union Carbide, Robert D. Kennedy, quotedin Chemical Week, Nov. 16, 1983, 48.

Comment attributed to Peter Olson III, IBM’s director ofbusiness development, as reported in The Strategy BehindIBM’s Strategic Alliances, Electronic Business, October 1(1985) 126.

294 D.J.

Smaller less integrated companies are ofteneager to sign on with established companies be-cause of the name recognition and reputation lovers. For instance Cipher Data Products, Inc.contracted with IBM to develop a low-priced ver-sion of IBM’s 3480 0.5 inch streaming cartridgedrive, which is likely to become the industrystandard. As Cipher management points out, “oneof the biggest advantages to dealing with IBM isthat, once you’ve created a product that meets thehigh quality standards necessary to sell into theIBM world, you can sell into any arena.” Simi-larly, IBM’s contract with Microsoft “meant in-stant credibility” to Microsoft 1985, p.94).

It is most important to recognize, however, thatstrategic (contractual) partnering, which is cur-rently very fashionable, is exposed to certain

hazards, particularly for the innovator, when theinnovator is trying to use contracts to access spe-cialized capabilities. First, it may be difficult to

tion of the LaserWriter. The arrangement to have been prudent, yet there were clearlyhazards for both sides. It is difficult to write,execute, and enforce complex development con-tracts, particularly when the design of the newproduct is still “floating.” Apple was exposed tothe risk that its co-innovator Canon would fail todeliver, and Canon was exposed to the risk thatthe Apple design and marketing effort would notsucceed. Still, Apple’s alternatives may have beenrather limited, inasmuch as it didn’t command therequisite technology to “go it alone.”

In short, the current euphoria over “strategicpartnering” may be partially misplaced. The ad-vantages are being stressed (for example, Kenna without a balanced presentation ofcosts and risks. Briefly, there is the risk that thepartner won’t perform according to the innovator’sperception of what the contract requires; there is

induce suppliers to make costly irreversible com-mitments which depend for their success on thesuccess of the innovation. To expect suppliers,manufacturers, and distributors to do so is toinvite them to take risks along with the innovator.The problem which this poses for the innovator issimilar to the problems associated with attractingventure capital. The innovator must persuade itsprospective partner that the risk is a good one.The situation is one open to opportunistic abuseson both sides. The innovator has incentives tooverstate the value of the innovation, while thesupplier has incentives to “run with the tech-nology” should the innovation be a success.

. the added danger that the partner may imitate theinnovator’s technology and attempt to competewith the innovator. This latter possibility is par-ticularly acute if the provider of the complemen-tary asset is uniquely situated with respect to thecomplementary asset in question and has thecapacity to imitate the technology, which the in-novator is unable to protect. The innovator willthen find that it has created a competitor who isbetter positioned than the innovator to take ad-vantage of the market opportunity at hand. Busi-ness Week has expressed concerns along theselines in its discussion of the “Hollow Corpora-tion.”

Instances of both parties making irreversiblecapital commitments nevertheless exist. Apple’sLaser-writer a high resolution laser printer whichallows PC users to produce near typeset qualitytext and art department graphics is a case inpoint. Apple persuaded Canon to participate inthe development of the Laserwriter by providingsubsystems from its copiers but only after Applecontracted to pay for a certain number of copierengines and cases. In short, Apple accepted agood deal of the financial risk in order to induceCanon to assist in the development and

It is important to bear in mind, however, thatcontractual or partnering strategies in certain casesare ideal. If the innovator’s technology is wellprotected, and if what the partner has to provideis a “generic” capacity available from manypotential partners, then the innovator will be ableto maintain the upper hand while avoiding thecosts of duplicating downstream capacity. Even ifthe partner fails to perform, adequate alternativesexist (by assumption, the partners’ capacities arecommonly available) so the innovator’s efforts tosuccessfully commercialize its technology ought toproceed profitably.

Comment attributed to Norman Farquhar, Cipher’s vice See Business Week, March 3 (1986) 57-59. Weekpresident for strategic development, as reported in uses the term to describe a corporation which lacks in-house

October 1 (1985) 128. manufacturing capability.

D.J. Profiting 295

5.2. Integration modes

Integration, which by definition involves own-ership, is distinguished from pure contractualmodes in that it typically facilitates incentivealignment and control. If an innovator owns ratherthan rents the complementary assets needed tocommercialize, then it is in a position to capturespillover benefits stemming from increased de-mand for the complementary assets caused by theinnovation.

Indeed, an innovator might be in the position,at least before its innovation is announced, to buyup capacity in the complementary assets, possiblyto its great subsequent advantage. If futuresmarkets exist, simply taking forward positions inthe complementary assets may suffice to capture ,much of the spillovers.

Even after the innovation is announced, theinnovator might still be able to build or buycomplementary capacities at competitive prices ifthe innovation has iron clad legal protection (i.e. ifthe innovation is in a tight appropriability regime).However, if the innovation is not tightly protected?and once “out” is easy to imitate, then securingcontrol of complementary capacities is likely to bethe key success factor, particularly if thoseties are in fixed supply so called “bottlenecks.”Distribution and specialized manufacturing petences often become bottlenecks.

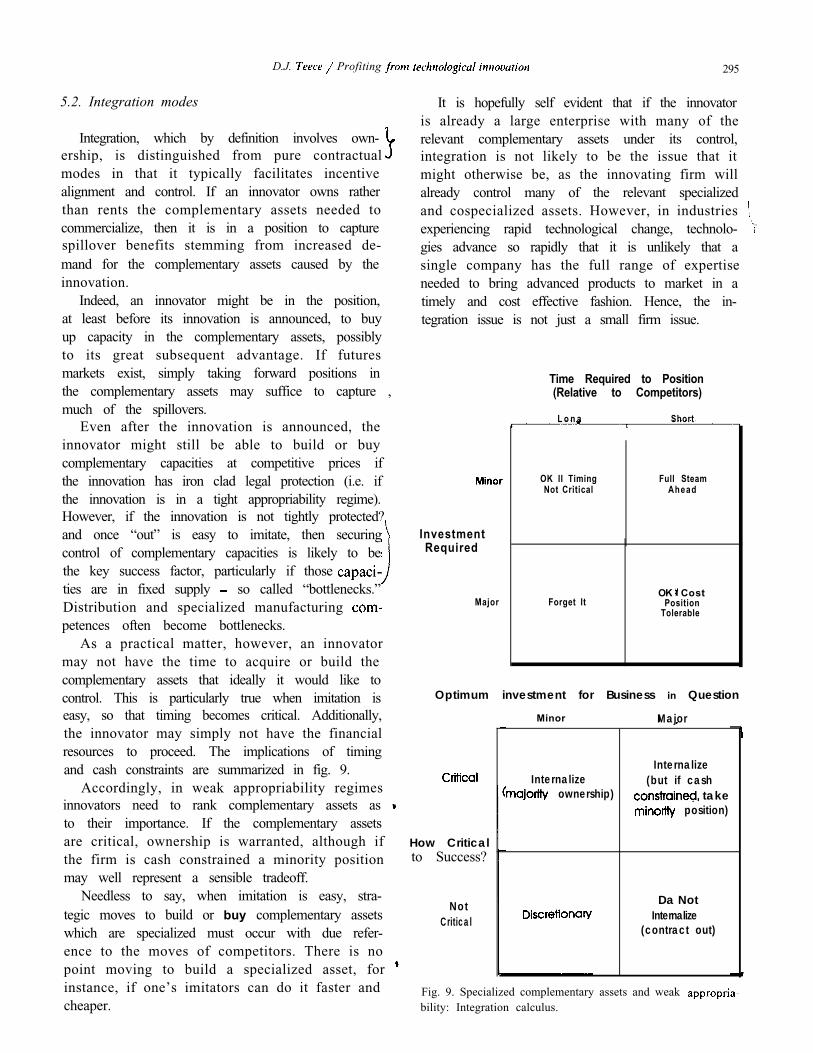

As a practical matter, however, an innovatormay not have the time to acquire or build thecomplementary assets that ideally it would like tocontrol. This is particularly true when imitation iseasy, so that timing becomes critical. Additionally,the innovator may simply not have the financialresources to proceed. The implications of timingand cash constraints are summarized in fig. 9.

Accordingly, in weak appropriability regimesinnovators need to rank complementary assets as to their importance. If the complementary assetsare critical, ownership is warranted, although ifthe firm is cash constrained a minority positionmay well represent a sensible tradeoff.

Needless to say, when imitation is easy, stra-tegic moves to build or buy complementary assetswhich are specialized must occur with due refer-ence to the moves of competitors. There is nopoint moving to build a specialized asset, for instance, if one’s imitators can do it faster andcheaper.

It is hopefully self evident that if the innovatoris already a large enterprise with many of therelevant complementary assets under its control,integration is not likely to be the issue that itmight otherwise be, as the innovating firm willalready control many of the relevant specializedand cospecialized assets. However, in industries experiencing rapid technological change, technolo- gies advance so rapidly that it is unlikely that asingle company has the full range of expertiseneeded to bring advanced products to market in atimely and cost effective fashion. Hence, the in-tegration issue is not just a small firm issue.

Time Required to Position(Relative to Competitors)

L o n a Short

InvestmentRequired

Major

OK II TimingNot Critical

Full SteamAhead

Forget ItOK Cost

PositionTolerable

Optimum investment for Business in Question

Minor Major

How Criticalto Success?

NotCritical

Internalize ownership)

Internalize(but if cash

take position)

Da NotInternalize

(contract out)

Fig. 9. Specialized complementary assets and weak bility: Integration calculus.

2 9 6 D.J. Profiting from technological

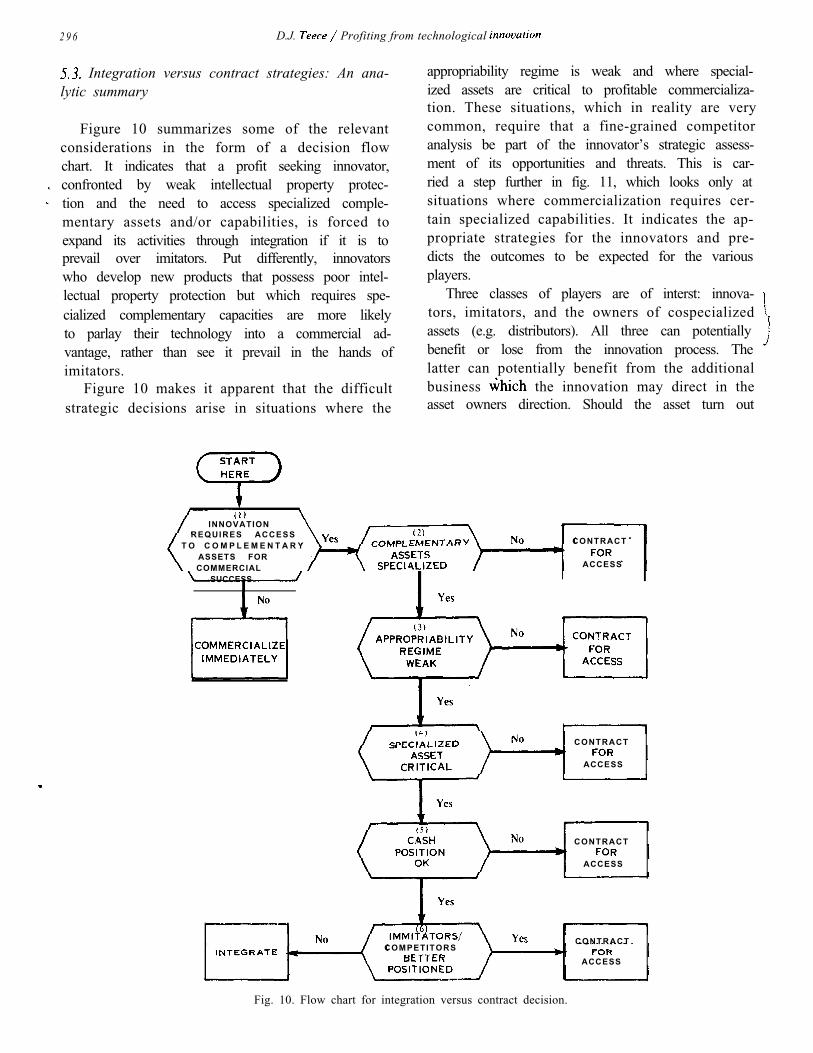

Integration versus contract strategies: An ana-lytic summary

Figure 10 summarizes some of the relevantconsiderations in the form of a decision flowchart. It indicates that a profit seeking innovator,confronted by weak intellectual property protec-tion and the need to access specialized comple-mentary assets and/or capabilities, is forced toexpand its activities through integration if it is toprevail over imitators. Put differently, innovatorswho develop new products that possess poor intel-lectual property protection but which requires spe-cialized complementary capacities are more likelyto parlay their technology into a commercial ad-vantage, rather than see it prevail in the hands ofimitators.

Figure 10 makes it apparent that the difficultstrategic decisions arise in situations where the

appropriability regime is weak and where special-ized assets are critical to profitable commercializa-tion. These situations, which in reality are verycommon, require that a fine-grained competitoranalysis be part of the innovator’s strategic assess-ment of its opportunities and threats. This is car-ried a step further in fig. 11, which looks only atsituations where commercialization requires cer-tain specialized capabilities. It indicates the ap-propriate strategies for the innovators and pre-dicts the outcomes to be expected for the variousplayers.

Three classes of players are of interst: innova-tors, imitators, and the owners of cospecializedassets (e.g. distributors). All three can potentially benefit or lose from the innovation process. Thelatter can potentially benefit from the additionalbusiness the innovation may direct in theasset owners direction. Should the asset turn out

INNOVATIONREQUIRES ACCESS

T O C O M P L E M E N T A R YASSETS FORCOMMERCIAL

SUCCESS

CONTRACT

ACCESS

CONTRACT

ACCESS

CONTRACT

ACCESS

COMPETITORSCONTRACT

ACCESS

Fig. 10. Flow chart for integration versus contract decision.

D.J. Profiting from 297

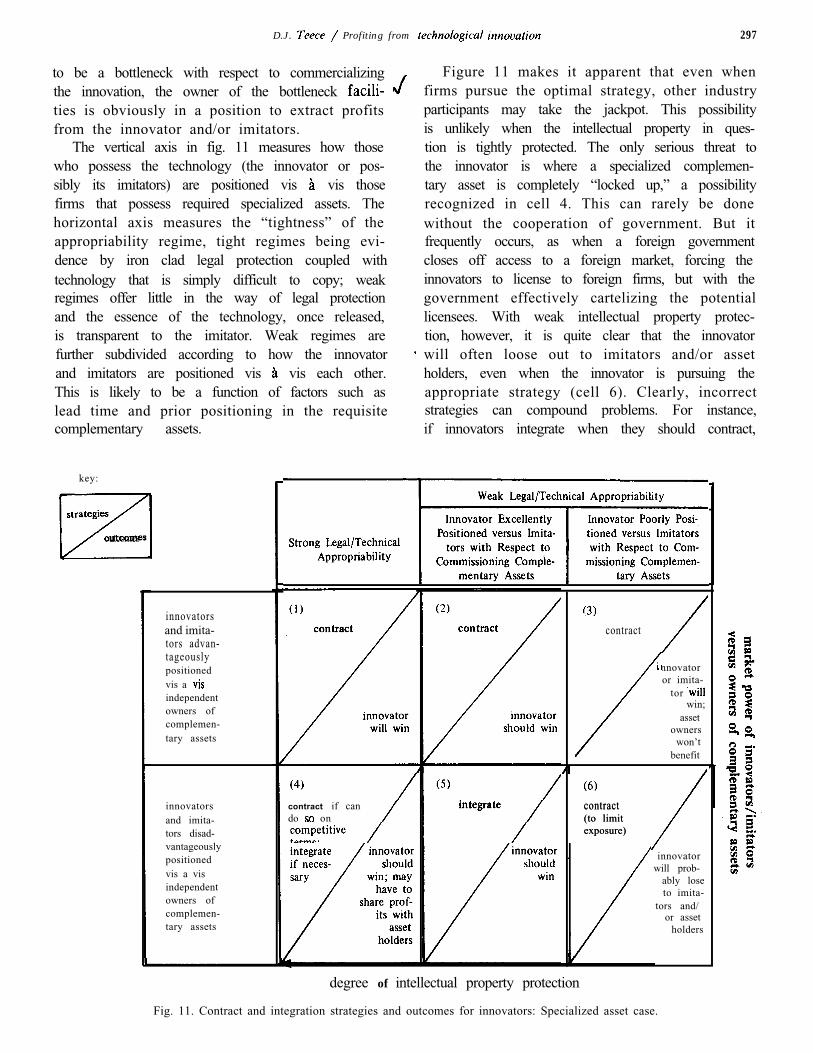

to be a bottleneck with respect to commercializingthe innovation, the owner of the bottleneck ties is obviously in a position to extract profitsfrom the innovator and/or imitators.

The vertical axis in fig. 11 measures how thosewho possess the technology (the innovator or pos-sibly its imitators) are positioned vis vis thosefirms that possess required specialized assets. Thehorizontal axis measures the “tightness” of theappropriability regime, tight regimes being evi-dence by iron clad legal protection coupled withtechnology that is simply difficult to copy; weakregimes offer little in the way of legal protectionand the essence of the technology, once released,is transparent to the imitator. Weak regimes arefurther subdivided according to how the innovatorand imitators are positioned vis vis each other.This is likely to be a function of factors such aslead time and prior positioning in the requisitecomplementary assets.

key:

strategies

outcomes

innovatorsand imita-tors advan-tageouslypositionedvis a independentowners ofcomplemen-tary assets

innovatorsand imita-tors disad-vantageouslypositionedvis a visindependentowners ofcomplemen-tary assets

Figure 11 makes it apparent that even whenfirms pursue the optimal strategy, other industryparticipants may take the jackpot. This possibilityis unlikely when the intellectual property in ques-tion is tightly protected. The only serious threat tothe innovator is where a specialized complemen-tary asset is completely “locked up,” a possibilityrecognized in cell 4. This can rarely be donewithout the cooperation of government. But itfrequently occurs, as when a foreign governmentcloses off access to a foreign market, forcing theinnovators to license to foreign firms, but with thegovernment effectively cartelizing the potentiallicensees. With weak intellectual property protec-tion, however, it is quite clear that the innovatorwill often loose out to imitators and/or assetholders, even when the innovator is pursuing theappropriate strategy (cell 6). Clearly, incorrectstrategies can compound problems. For instance,if innovators integrate when they should contract,

Weak Legal/Technical Appropriability

contract if cando on

contract

innovatoror imita-

tor win;

assetowners

won’tbenefit

contractcontract(to limit(to limitexposure)exposure)

innovatorwill prob-

ably loseto imita-

tors and/or asset

holders

degree of intellectual property protection

Fig. 11. Contract and integration strategies and outcomes for innovators: Specialized asset case.

298 D.J. Profiting from

a heavy commitment of resources will be incurredfor little if any strategic benefit, thereby exposingthe innovator to even greater losses than wouldotherwise be the case. On the other hand, if aninnovator tries to contract for the supply of acritical capability when it should build the capa-bility itself, it may well find it has nutured animitator better able to serve the market than theinnovator itself.

5.4. Mixed modes

The real world rarely provides extreme or purecases. Decisions to integrate license involvetradeoffs, compromises, and mixed approaches. Itis not surprising therefore that the real world ischaracterized by mixed modes of organization,involving judicious blends of integration and con-tracting. Sometimes mixed modes represent transi-tional phases. For instance, because of the conver-gence of computer and telecommunication tech-nology, firms in each industry are discovering thatthey often lack the requisite technical capabilitiesin the other. Since the technological interdepen-dence of the two requires collaboration amongstthose who design different parts of the system,intense cross-boundary coordination and informa-tion flows are required. When separate enterprisesare involved, agreement must be reached on com-plex protocol issues amongst parties who see theirinterests differently. Contractual difficulties canbe anticipated since the selection of common tech-nical protocols amongst the parties will often befollowed by transaction-specific investments inhardware and software. There is little doubt thatthis was the motivation behind IBM’s purchase of15 percent of PBX manufacturer Rolm in 1983, aposition that was expanded to 100 percent in1984. IBM’s stake in Intel, which began with a 12percent purchase in 1982, is most probably not atransitional phase leading to 100 percent purchase,because both companies realized that the two cor-porate cultures are not very compatible, and IBMmay not be as impressed with Intel’s technology asit once was.

5.5. The CAT scanner, the IBM PC, and Sweet: Insights from the framework

failure to reap significant returns fromthe CAT scanner can be explained in large mea-

sure by reference to the concepts developed above.The scanner which EM1 developed was of a tech-nical sophistication much higher than. would nor-mally be found in a hospital, requiring a high levelof training, support, and servicing. had noneof these capabilities, could not easily contract forthem, and was slow to realize their importance. Itmost probably could have formed a partnershipwith a company like Siemens to access the re-quisite capabilities. Its failure to do so was astrategic error compounded by the very limitedintellectual property protection which the law af-forded the scanner. Although subsequent courtdecisions have upheld some of patentclaims, once the product was in the market itcould be reverse engineered and its essential fea-tures copied. Two competitors, GE and nicare, already possessed the complementary ca-pabilities that the scanner required, and they werealso technologically capable. In addition, bothwere experienced marketers of medical equipment,and had reputations for quality, reliability andservice. GE and Technicare were thus able tocommit their R&D resources to developing acompetitive scanner, borrowing ideas from scanner, which they undoubtedly had access tothrough cooperative hospitals, and improving on itwhere they could while they rushed to market. GEbegan taking orders in 1976 and soon after madeinroads on In 1977 concern for rising healthcare costs caused the Carter Administration tointroduce “certificate of need’ regulation, whichrequired HEW’s approval on expenditures on bigticket items like CAT scanners. This severely cutthe size of the available market.

By 1978 EM1 had lost market share leadershipto Technicare, which was in turn quickly over-taken by GE. In October 1979, Godfrey field of EM1 shared the Nobel prize for inventionof the CT scanner. Despite this honor, and thepublic recognition of its role in bringing this medi-cal breathrough to the world, the collapse of itsscanner business forced EM1 in the same year intothe arms of a rescuer, Thorn Electrical Industries,Ltd. GE subsequently acquired what was scanner business from Thorn for what amountedto a pittance. Though royalties continued to flowto the company had failed to capture the

See GE Gobbles a Rival in CT Scanners, Business Week,May 19, 1980, issue no. 2637.

299

lion’s share of the profits generated by the innova-tion it had pioneered and successfully commercial-ized.

If EM1 illustrates how a company with out-standing technology and an excellent product canfail to profit from innovation while the imitatorssucceeded, the story of the IBM PC indicates howa new product representing a very modest techno-logical advance can yield remarkable returns tothe developer.

The IBM PC, introduced in 1981, was a successdespite the fact that the architecture was ordinaryand the components standard. Philip Estridge’sdesign team in Florida, decided touse existing technology to produce a solid, reliablemicro rather than state of the art. With a one-yearmandate to develop a PC, Estridge’s team coulddo little else.

However, the IBM PC did use what at the timewas a new microprocessor (the Intel 8088)and a new disk operating system (DOS) adaptedfor IBM by Microsoft. Other than the micro-processor and the operating system, the IBM PCincorporated existing micro “standards” and usedoff-the-shelf parts from outside vendors. IBM didwrite its own BIOS (Basic Input/Output System)which is embedded in ROM, but this was a rela-tively straightforward programming exercise.

The key to the PC’s success was not the tech-nology. It was the set of complementary assets

which IBM either had or quickly assembled aroundthe PC. In order to expand the market for PCs,there was a clear need for an expandable, flexiblemicrocomputer system with extensive applicationssoftware. IBM could have based its PC system onits own patented hardware and copyrighted soft-ware. Such an approach would cause complemen-tary products to be cospecialized, forcing IBM todevelop peripherals and a comprehensive libraryof software in a very short time. Instead, IBMadopted what might be called an “induced con-tractual” approach. By adopting an open systemarchitecture, as Apple had done, and by makingthe operating system information publicly availa-ble, a spectacular output of third part softwarewas induced. IBM estimated that by mid-1983, atleast 3000 hardware and software products wereavailable for the PC. Put differently, IBM pulled

F. Gens and C. Christiansen, Could IBM PCUsers Be Wrong. November 1983, 88.

together the complementary assets, particularlysoftware, which success required, without evenusing contracts, let alone integration. This wasdespite the fact that the software developers werecreating assets that were in part cospecialized withthe IBM PC, at least in the first instance.

A number of special factors made this seem areasonable risk to the software writers. A criticalone was IBM’s name and commitment to theproject. The reputation behind the letters I.B.M. is

perhaps the greatest cospecialized asset the com-pany possesses. The name implied that the prod-uct would be marketed and serviced in the IBMtradition. It guaranteed that PC-DOS would be-come an industry standard, so that the softwarebusiness would not be solely dependent on IBM,because emulators were sure to enter. It guaran-teed access to retail distribution outlets on compe-titive terms. The consequences was that IBM wasable to take a product which represented at best amodest technological accomplishment, and turninto a fabulous commercial success. The case dem-onstrates the role that complementary assets playin determining outcomes.

The spectacular success and profitability ofG.D. Searle’s NutraSweet is an uncommon storywhich is also consistent with the above frame-work. In 1982, Searle reported combined sales of$74 million for NutraSweet and its table top ver-sion, Equal. In 1983, this surged to $336 million.In 1985, NutraSweet sales exceeded $700 million and Equal had captured 50 percent of the U.S.sugar substitute market and was number one infive other countries.

NutraSweet, which is Searle’s tradename foraspartame, has achieved rapid acceptance in eachof its FDA approved categories because of itsgood taste and ability to substitute directly forsugar in many applications. However, Searle’searnings from NutraSweet and the absence of astrategic challenge can be traced in part to Searle’sclever strategy.

It appears that Searle has managed to establish!" an exceptionally tight appropriability regime a-

round NutraSweet one that may well continuefor some time after the patent has expired. Nocompetitor appears to have successfully “inventedaround” the Searle patent and commercialized analternative, no doubt in part because the FDA

See 1985.

300 D.J. from

approval process would begin anew for animitator who was not violating Searle’s patents. Acompetitor who tried to replicate the aspartamemolecule with minor modification to circumventthe patent would probably be forced to replicatethe hundreds of tests and experiments whichproved aspartame’s safety. Without patent

t ion, FDA approval would provide no shieldagainst imitators coming to market with an identi-cal chemical and who could establish to the FDA

that it is the same compound that had already been approved. Without FDA approval on the

other hand, the patent protection would be worth-‘! less for the product would not for human consumption.

Searle has aggressively pushed to strengthen itspatent protection. The company was granted U.S.patent protection in 1970. It has also obtainedpatent protection in Japan, Canada, Australia,U.K., France, Germany, and a number of othercountries. However, most of these patents carry a

life. Since the product was only approvedfor human consumption in 1982, the patentlife was effectively reduced to five. Recognizingthe obvious importance of its patent, Searle pressedfor and obtained special legislation in November1984 extending the patent protection on aspar-tame for another 5 years. The U.K. provided asimilar extension. In almost every other nation,however, 1987 will mark the expiration of thepatent.

When the patent expires, however, Searle willstill have several valuable assets to help keepimitators at bay. Searle has gone to great lengthsto create and promulgate the use of its NutraSweetname and a distinctive “Swirl” logo on all goodslicensed to use the ingredient. The company hasalso developed the “Equal” tradename for a tabletop version of the sweetener. Trademark law inthe U.S. provides protection against “unfair”competition in branded products for as long as theowner of the mark continues to use it. Both theNutraSweet and Equal trademarks will become

essential assets when the patents on aspartameexpire. Searle may well have convinced consumersthat the only real form of sweetener is Sweet/Equal. Consumers know most other artifi-cial sweeteners by their generic names saccharinand cyclamates.

Clearly, Searle is trying to build a position incomplementary assets to prepare for the competi-

tion which will surely arise. Searle’s joint venturewith Ajinomoto ensures them access to that com-pany’s many years of experience in the productionof biochemical agents. Much of this knowledge is

associated with techniques for distillation andsynthesis of the delicate hydrocarbon compounds

that are the ingredients of NutraSweet, and is therefore more tacit than codified. Searle has be-\ gun to put these techniques to use in its own $160

million Georgia production facility. It can beexpected that Searle will use trade secrets to themaximum to keep this know-how proprietary.

By the time its patent expires, Searle’s extensiveresearch into production techniques for

and its years of experience in the Geor-gia‘ plant, should give it a significant cost ad-vantage over potential aspartame competitors.Trade secret protection, unlike patents, has nofixed lifetime and may well sustain Searle’s posi-tion for years to come.

Moreover, Searle has wisely avoided renewingcontracts with suppliers when they have expired. Had Searle subcontracted manufacturing forNutraSweet, it would have created a manufacturerwho would then be in a position to enter the

aspartame market itself, or to team up with amarketer of artificial sweeteners. But keepingmanufacturing and by developing a valu-able tradename, Searle has a good chance of pro-tecting its market position from dramatic inroadsonce patents expire. Clearly, Searle seems to beastutely aware of the importance of maintaining a“tight appropriability regime” and using cialized assets strategically.

6. Implications for R&D strategy, industry struc-ture, and trade policy

6.1. Allocating R&D resources

The analysis so far assumes that the firm hasdeveloped an innovation for which a market ex-ists. It indicates the strategies which the firm must

Purification Engineering, which had spent $5 million tobuild a phenylalanine production facility, was told inJanuary 1985 that their contract would not be renewed. InMay, Genex, which claimed to have invested $25 million,was given the same message, A Bad Aftertaste, BusinessWeek, July 15, 1985, issue 2903.

D.J. 301

follow to maximize its share of industry profitsrelative to imitators and other competitors. Thereis no guarantee of success even if optimal strate-gies are followed.

The innovator can improve its total return toR&D, however, by adjusting its R&D investmentportfolio to maximize the probability that techno-logical discoveries will emerge that are either easyto protect with existing intellectual property law,or which require for commercialization ized assets already within the firm’s repertoire ofcapabilities. Put differently, if an innovating firmdoes not target its R&D resources towards newproducts and processes which it can commercial-ize advantageously relative to potential imitatorsand/or followers, then it is unlikely to profit fromits investment in R&D. In this sense, a firm’shistory and the assets it already has in place ought to condition its R&D investment decisions.Clearly, an innovating firm with considerable as-sets already in place is free to strike out in newdirections, so long as in doing so it is cognizant ofthe kinds of capabilities required to successfullycommercialize the innovation. It is therefore ratherclear that the R&D investment decision cannot bedivorced from the strategic analysis of marketsand industries, and the firm’s position within them.

6.2. Small firm versus large firm comparisons

Business commentators often remark that manysmall entrepreneurial firms which generate new,commercially valuable technology fail while largemultinational firms, often with a less meritoriousrecord with respect to innovation, survive andprosper. One set of reasons for this phenomenonis now clear. Large firms are more likely to possessthe relevant specialized and cospecialized assetswithin their boundaries at the time of new productintroduction. They can therefore do a better job ofmilking their technology, however meager, to max-imum advantage. Small domestic firms are lesslikely to have the relevant specialized and cospe-cialized assets within their boundaries and so willeither have to incur the expense of trying to buildthem, or of trying to develop coalitions with com-petitors/owners of the specialized assets.

.

6.3. Regimes of appropriability and industry struc-ture

In industries where legal methods of protectionare effective, or where new products are just hardto copy, the strategic necessity for innovating firmsto integrate into cospecialized assets would appearto be less compelling than in industries wherelegal protection is weak. In cases where legalprotection is weak or nonexistent, the control of cospecialized assets will be needed for long-runsurvival.

In this regard, it is instructive to examine theU.S. drug industry (Temin Beginning in the

the U.S. Patent Office began, for the firsttime, to grant patents on certain natural sub-stances that involved difficult extraction proce-dures. Thus, in 1948 Merck received a patent onstreptomycin, which was a natural substance.However, it was not the extraction process but thedrug itself which received the patent. Hence,patents were important to the drug industry interms of what could be patented (drugs), but theydid not prevent imitation Sometimesjust changing one molecule will enable a companyto come up with a different substance which doesnot violate the patent. Had patents been moreall-inclusive and I am not suggesting they should

licensing would have been an effective mecha-nism for Merck to extract profits from its innova-tion. As it turns out, the emergence of close sub-stitutes, coupled with FDA regulation which hadthe de facto effect of reducing the elasticity ofdemand for drugs, placed high rewards on a prod-uct differentiation strategy. This required exten-sive marketing, including a sales force that coulddirectly contact doctors, who were the purchasersof drugs through their ability to create prescrip-tions. The result was exclusive production (i.e.,the earlier industry practice of licensing wasdropped) and forward integration into marketing(the relevant cospecialized asset).

Generally, if legal protection of the innovator’sprofits is secure, innovating firms can select their

In the period before FDA regulation, all drugs other thannarcotics were available over-the-counter. Since the enduser could purchase drugs directly, sales were price sensi-tive. Once prescriptions were required, this price sensitivitycollapsed; the doctors not only did not have to pay for thedrugs, but in most cases they were unaware of the prices ofthe drugs they were prescribing.

302 D.J. from

boundaries based simply on their ability to iden-tify user needs and respond to those throughresearch and development. The weaker the legalmethods of protection, the greater the incentive tointegrate into the relevant cospecialized assets.Hence, as industries in which legal protection isweak begin to mature, integration into specific cospecialized assets will occur. Often thiswill take the form of backward, forward and lateralintegration. (Conglomerate integration is not partof this phenomenon.) For example, IBM’s pur-chase of Rolm can be seen as a response to theimpact of technological change on the identity ofthe cospecialized assets relevant to IBM’s futuregrowth.

6.4. Industry maturity, new entry, and history

As technologically progressive industries ma-ture, and a greater proportion of the relevantcospecialized assets are brought in under the cor-porate umbrellas of incumbents, new entry be-comes more difficult. Moreover, when it does oc-cur it is more likely to involve coalition formationvery early on. Incumbents will for sure own thecospecialized assets, and new entrants will find itnecessary to forge links with them. Here lies theexplanation for the sudden surge in “strategicpartnering” now occurring internationally, andparticularly in the computer and

, tions industry. Note that it should not be ted in anti-competitive terms. Given existing in-

structure, coalitions ought to be seen not asattempts to stifle competition, but as mechanismsfor lowering entry requirements for innovators.

In industries in which technological change of aparticular kind has occurred, which required de-ployment of specialized and/or cospecialized as-sets at the time, a configuration of firm boundariesmay well have arisen which no longer has compell-ing efficiencies. Considerations which once dic-tated integration may no longer hold, yet theremay not be strong forces leading to divestiture.Hence existing firm boundaries may in some in-dustries especially those where the technologicaltrajectory and attendent specialized asset require-ments has changed be rather fragile. In short,history matters in terms of understanding thestructure of the modern business enterprise. Ex-isting firm boundaries cannot always be assumedto have obvious rationales in terms of today’srequirements.

6.5. The importance of manufacturing interna-tional competitiveness

Practically all forms of technological know-how must be embedded in goods and services to yield value to the consumer. An important policy for

the innovating nation is whether the identity ofthe firms and nations performing this functionmatter.

In a world of tight appropriability and zerotransactions cost the world of tradetheory it is a matter of indifference whether aninnovating firm has an in-house manufacturingcapability, domestic or foreign. It can simply en-gage in arms-length contracting (patent licensing, know-how licensing, co-production, etc.) for thesale of the output of the activity in which it has acomparative advantage (in this case R&D) andwill maximize returns by specializing in what itdoes best.

However, in a regime of weak appropriability,and especially where the requisite manufacturingassets are specialized to the innovation, which isoften the case, participation in manufacturing maybe necessary if an innovator is to appropriate the

rents from its innovation. Hence, if an innovator’smanufacturing costs are higher than those of itsimitators, the innovator may well end up cedingthe lion’s share of profits to the imitator.

In a weak appropriability regime, low cost itator-manufacturers may end up capturing all of

the profits from innovation. In a weak bility regime where specialized manufacturing ca-pabilities are required to produce new products,an innovator with a manufacturing disadvantagemay find that its advantage at early stage researchand development will have no commercial value.This will eventually cripple the innovator, unless itis assisted by governmental processes. For exam-ple, it appears that one of the reasons why U.S.color TV manufacturers did not capture the lion’sshare of the profits from the innovation, for whichRCA was primarily responsible, was that RCAand its American licenses were not competitive atmanufacturing. In this context, concerns that thedecline of manufacturing threatens the entireeconomy appear to be well founded.

A related implication is that as the technologygap closes, the basis of competition in an industrywill shift to the cospecialized assets. This appearsto be what is happening in microprocessors. Intel

is no longer out ahead technologically. As GordonMoore, CEO of Intel points out, “Take the top 10[semiconductor] companies in the world.. . and itis hard to tell at any time who is ahead of whom.. . .It is clear that we have to be pretty damn close tothe Japanese from a manufacturing standpoint tocompete.” It is not just that strength in one areais necessary to compensate for weakness in

another. As technology becomes more public and less proprietary through easier imitation, theni strength in manufacturing and other capabilities is

\

necessary to derive advantage from whatever tech-nological advantages an innovator may possess.

Put differently, the notion that the United Statescan adopt a “designer role” in international com-merce, while letting independent firms in othercountries such as Japan, Korea, Taiwan, or Mexicodo the manufacturing, is unlikely to be viable as along-run strategy. This is because profits willaccrue primarily to the low cost manufacturers (byproviding a larger sales base over which they canexploit their special skills). Where imitation iseasy, and even where it is not, there are obviousproblems in transacting in the market for how, problems which are described in more detailelsewhere In particular, there are difficulties inpricing an intangible asset whose true perfor-mance features are difficult to ascertain ex ante.

The trend in international business towardswhat Miles and Snow call “dynamic networks”

J characterized by vertical disintegration and con-tracting ought thus be viewed with concern.(Business Week, March 3, 1986, has referred tothe same phenomenon as the Hollow Corporation.)

“Dynamic networks” may not so much reflect innovative organizational forms, but the bly of the modern corporation because of

Iterioration in national capacities, manufacturingin particular, which are complementary to techno-logical innovation. Dynamic networks may there-fore signal not so much the rejuvenation ofAmerican enterprise, but its piecemeal demise.

6.6. How trade and investment barriers can impactinnovators’ profits

In regimes of weak appropriability, govern-ments can move to shift the distribution of the

Institutionalizing Revolution, Forbes. June 16, 1986,35.

gains from innovation away from foreign innova-tors and towards domestic firms by denying in-novators ownership of specialized The for-eign firm, which by assumption is an innovator,will be left with the option of selling its intangibleassets in the market for know how if both tradeand investment are foreclosed by governmentpolicy. This option may appear better than thealternative (no renumeration at all from the marketin question). Licensing may then appear profit-,/able, but only because access to the complemen-tary assets is blocked by government.

Thus when an innovating firm generating prof-its needs to access complementary assets abroad,host governments, by limiting access, can some-times milk the innovators for a share of the prof-its, particularly that portion which originates fromsales in the host country. However, the ability ofhost governments to do so depends importantlyon the criticality of the host country’s assets to theinnovator. If the cost and infrastructure character-istics of the host country are such that it is theworld’s lowest cost manufacturing site, and ifdomestic industry is competitive, then by acting asa de facto monopsonist the host country govern-ment ought to be able to adjust the terms of accessto the complementary assets so as to appropriate agreater share of the profits generated by the in-novation.

If, on the other hand, the host country offersno unique complementary assets, except access toits own market, restrictive practices by the govern-ment will only redistribute profits with respect todomestic rather than worldwide sales.

6.7. Implications for the international distribution ofthe benefits from innovation

The above analysis makes transparent that in-novators who do not have access to the relevantspecialized and cospecialized assets may end upceding profits to imitators and other competitors,or simply to the owners of the specialized orcospecialized assets.

Even when the specialized assets are possessedby the innovating firm, they may be located .abroad. Foreign factors of production are thus

If the host country market structure is monopolistic in thefirst instance, private actors might be able to achieve thesame benefit. What government can do is to force collusionof domestic enterprises to their mutual benefit.

304

likely to benefit from research and developmentactivities occurring across borders. There is littledoubt, for instance, that the inability of manyAmerican multinationals to sustain competitivemanufacturing in the U.S. is resulting in decliningreturns to U.S. labor. Stockholders and topmanagement probably do as well if not betterwhen a multinational accesses in the firm’s foreign subsidiaries; however, if thereis unemployment in the factors of productionsupporting the specialized and cospecialized assetsin question, then the foreign factors of production

will benefit from innovation originating beyondnational borders. This speaks to the importance to

, innovating nations of maintaining competence and competitiveness in the assets which complement technological innovation, manufacturing being a

case in point. It also speaks to the importance toinnovating nations of enhancing the protection

afforded worldwide to intellectual property.However, it must be recognized that there are

inherent limits to the legal protection of intellect-: ual property, and that business and national

strategy are therefore likely to the critical factorsin determining how the gains from innovation areshared worldwide. By making the correct strategicdecision, innovating firms can move to protect theinterests of stockholders; however, to ensure thatdomestic rather than foreign cospecialized assetscapture the lion’s share of the externalities spillingover to complementary assets, the supporting in-frastructure for those complementary assets mustnot be allowed to decay. In short, if a nation hasprowess at innovation, then in the absence of ironclad protection for intellectual property, it mustmaintain well-developed complementary assets ifit is to capture the spillover benefits from innova-tion

7. Conclusion

The above analysis has attempted to synthesizefrom recent research in industrial organizationand strategic management a framework withinwhich to analyze the distribution of the profits

from innovation. The framework indicates thatthe boundaries of the firm are an important tegic variable for innovating firms. The ownershipof complementary assets, particularly when theyare specialized and/or cospecialized, help estab-

lish who wins and who loses from innovation.Imitators can often outperform innovators if theyare better positioned with respect to critical com-plementary assets. Hence, public policy aimed atpromoting innovation must focus not only on

R&D, but also on complementary assets, as wellas the underlying infrastructure. If governmentdecides to stimulate innovation, it would seemimportant to clear away barriers which impede thedevelopment of complementary assets which tendto be specialized or cospecialized to innovation.To fail to do so will cause an unnecessary large

portion of the profits from innovation to flow toimitators and other competitors. If these firms liebeyond one’s national borders, there are obviousimplications for the internal distribution of in-come.

When applied to world markets, results similarto those obtained from the “new trade theory” aresuggested by the framework. In particular, tariffsand other restrictions on trade can in some casesinjure innovating firms while simultaneously be-nefiting protected firms when they are imitators.However, the propositions suggested by the frame-work are particularized to appropriability regimes,suggesting that economy-wide conclusions will beillusive. The policy conclusions derivable for com-modity petrochemicals, for instance, are likely tobe different than those that would be arrived atfor semiconductors.

The approach also suggests that the product lifecycle model of international trade will play itselfout very differently in different industries andmarkets, in part according to appropriability regi-mes and the nature of the assets which need to beemployed to convert a technological success into acommercial one. Whatever its limitations, the ap-proach establishes that it is not so much the

structure of markets but the structure of firms,particularly the scope of their boundaries, coupledwith national policies with respect to the develop-ment of complementary assets, which determinesthe distribution of the profits amongst innovatorsand imitator/followers.

References

W.J. Abernathy and J.M. Utterback, Patterns of In-dustrial Innovation, Technology (January/July 1978)

D.J. Teece from technological 305

Kim B. Clarke, The Interaction of Design Hierarchies andMarket Concepts in Technological Evolution,

14 (1985) 235-251. G. Dosi, Technological Paradigms and Technological

Trajectories, Policy 11 (1982) 147-162. Thomas Kuhn, The Structure of 2nd

ed (University of Chicago Press, Chicago, 1970). R. A. Klevorick, N. Nelson, and S. Winter, Survey

Research on R&D Appropriability and Technological Op-portunity, unpublished manuscript, Yale University, 1984.

Regis Market Positioning in High Technology, XXVII (3) (spring 1985).

R.E. Miles and CC. Snow, Network Organizations: NewConcepts for New Forms, (spring 1986) 62-73.

David A. Norman, Impact of Entrepreneurship and In-novations on the Distribution of Personal Computers, in:R. Landau and N. Rosenberg (eds.). The Sum

(National Academy Press, ‘Washington. DC,1986).