Embed Size (px)

Citation preview

1 PROPERTY INSIGHT - LOGISTICSCBRE|WTW RESEARCH & CONSULTING

PROPERTY INSIGHT

AN INTRODUCTION TO MALAYSIA’S LOGISTICS(OCTOBER 2020)

2 PROPERTY INSIGHT - LOGISTICSCBRE|WTW RESEARCH & CONSULTING

1.0 Overview of Port & Air Traffic Globally (3)• SEA Traffic• Air Traffic

2.0 Regional / Global Trade (5)• The Halal Card

3.0 Malaysia Second Most Active in TEU Handling in Region (6)

4.0 Port Klang Leads as Major Port in Malaysia (7)

5.0 Malaysia Stepping Forward in Air Freight (8)

6.0 Why Invest in Malaysia? (9)• Infrastructure Projects in Malaysia• Selected Mega Infrastructure in Malaysia

7.0 Free Zone (12)• Free Zone in Malaysia

8.0 Leading Manufacturing Countries (14)

9.0 Malaysia as Manufacturing Base (15)

10.0 Compelling Presence of Major 3PL Logistics Players (16)

11.0 Klang Valley Leads The Logistics Sector In Malaysia (17)

12.0 The Future of Malaysia’s Logistics (18)

TABLE OF CONTENTSABBREVIATIONSUNTAD : United Nations Conference on Trade and DevelopmentIATA : International Air Transport AssociationMOT : Ministry of TransportationTEU : Twenty-foot equivalent unitKLIA : Kuala Lumpur International AirportY-O-Y : Year-over-yearGDP : Gross Development ProductFDI : Foreign Direct InvestmentAPAC : Asia Pacific MIL : MillionBIL : Billion

3 PROPERTY INSIGHT - LOGISTICSCBRE|WTW RESEARCH & CONSULTING

Sources: Marine Traffic, UNCTAD, IATA

3.1

4.9

17.4 7.0

20.9

7.4

23.6%21.4%13.5%

AsiaEurope

Legend

Air Freight Routes

Cargo Routes

Notes:

i. Cargo: Figures in TEUs(mil)

ii. Air Frights: Figures in % of freight

tonnes-kilometres

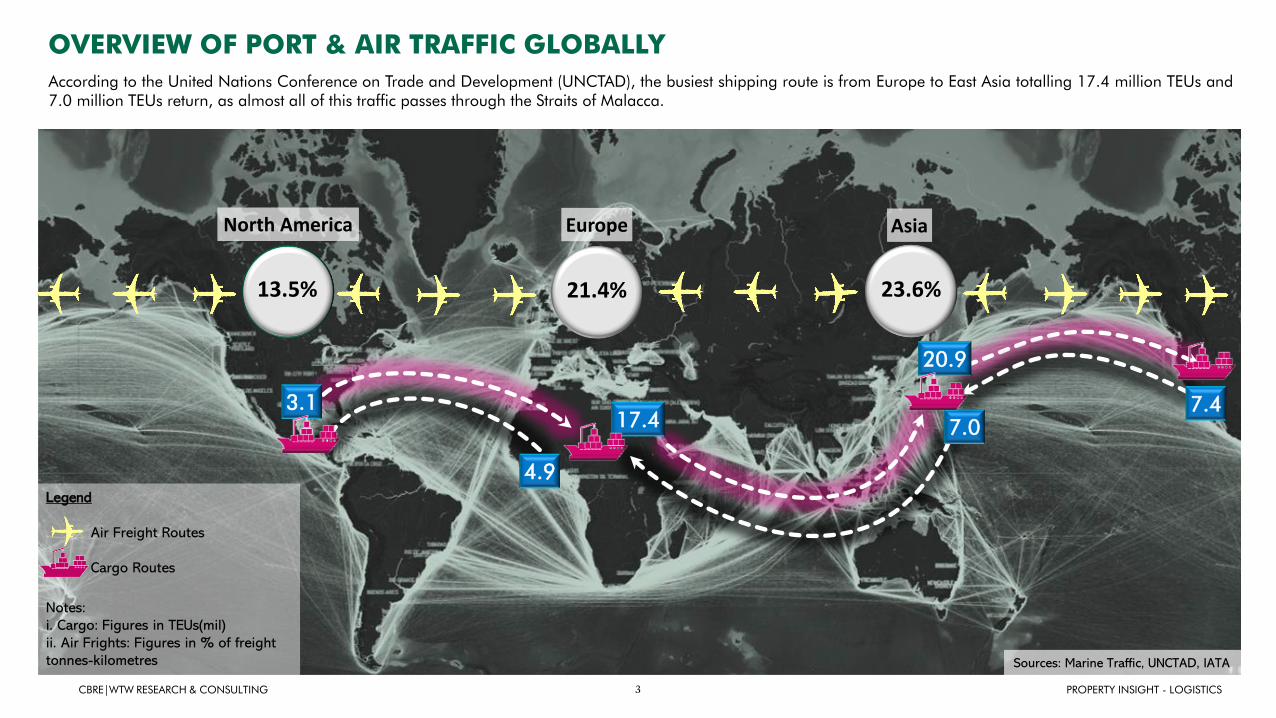

OVERVIEW OF PORT & AIR TRAFFIC GLOBALLYAccording to the United Nations Conference on Trade and Development (UNCTAD), the busiest shipping route is from Europe to East Asia totalling 17.4 million TEUs and7.0 million TEUs return, as almost all of this traffic passes through the Straits of Malacca.

North America

4 PROPERTY INSIGHT - LOGISTICSCBRE|WTW RESEARCH & CONSULTING

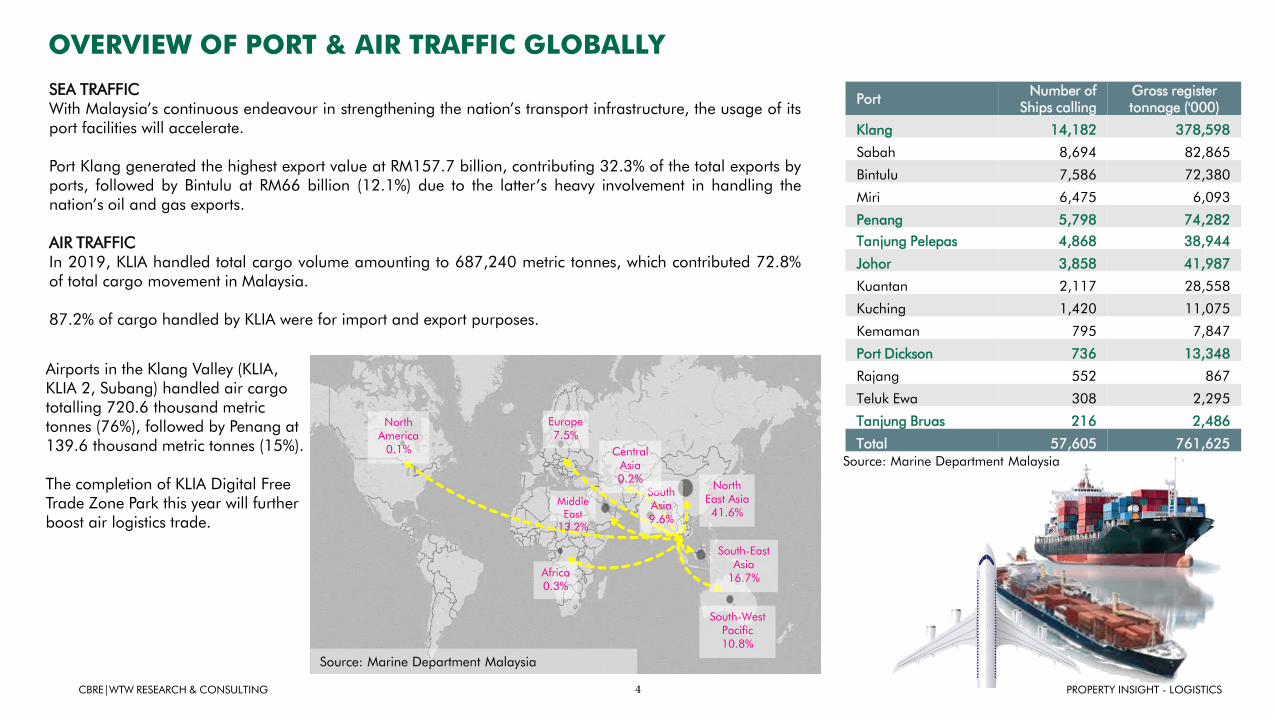

SEA TRAFFICWith Malaysia’s continuous endeavour in strengthening the nation’s transport infrastructure, the usage of itsport facilities will accelerate.

Port Klang generated the highest export value at RM157.7 billion, contributing 32.3% of the total exports byports, followed by Bintulu at RM66 billion (12.1%) due to the latter’s heavy involvement in handling thenation’s oil and gas exports.

AIR TRAFFICIn 2019, KLIA handled total cargo volume amounting to 687,240 metric tonnes, which contributed 72.8%of total cargo movement in Malaysia.

87.2% of cargo handled by KLIA were for import and export purposes.

Source: Marine Department Malaysia

OVERVIEW OF PORT & AIR TRAFFIC GLOBALLY

PortNumber of

Ships callingGross register tonnage ('000)

Klang 14,182 378,598

Sabah 8,694 82,865

Bintulu 7,586 72,380

Miri 6,475 6,093

Penang 5,798 74,282

Tanjung Pelepas 4,868 38,944

Johor 3,858 41,987

Kuantan 2,117 28,558

Kuching 1,420 11,075

Kemaman 795 7,847

Port Dickson 736 13,348

Rajang 552 867

Teluk Ewa 308 2,295

Tanjung Bruas 216 2,486

Total 57,605 761,625

Airports in the Klang Valley (KLIA, KLIA 2, Subang) handled air cargo totalling 720.6 thousand metric tonnes (76%), followed by Penang at 139.6 thousand metric tonnes (15%).

The completion of KLIA Digital Free Trade Zone Park this year will further boost air logistics trade.

North America

0.1%

Europe7.5%

North East Asia41.6%

South-East Asia

16.7%

South-West Pacific10.8%

Africa0.3%

Middle East

13.2%

South Asia9.6%

Central Asia0.2%

Source: Marine Department Malaysia

5 PROPERTY INSIGHT - LOGISTICSCBRE|WTW RESEARCH & CONSULTING

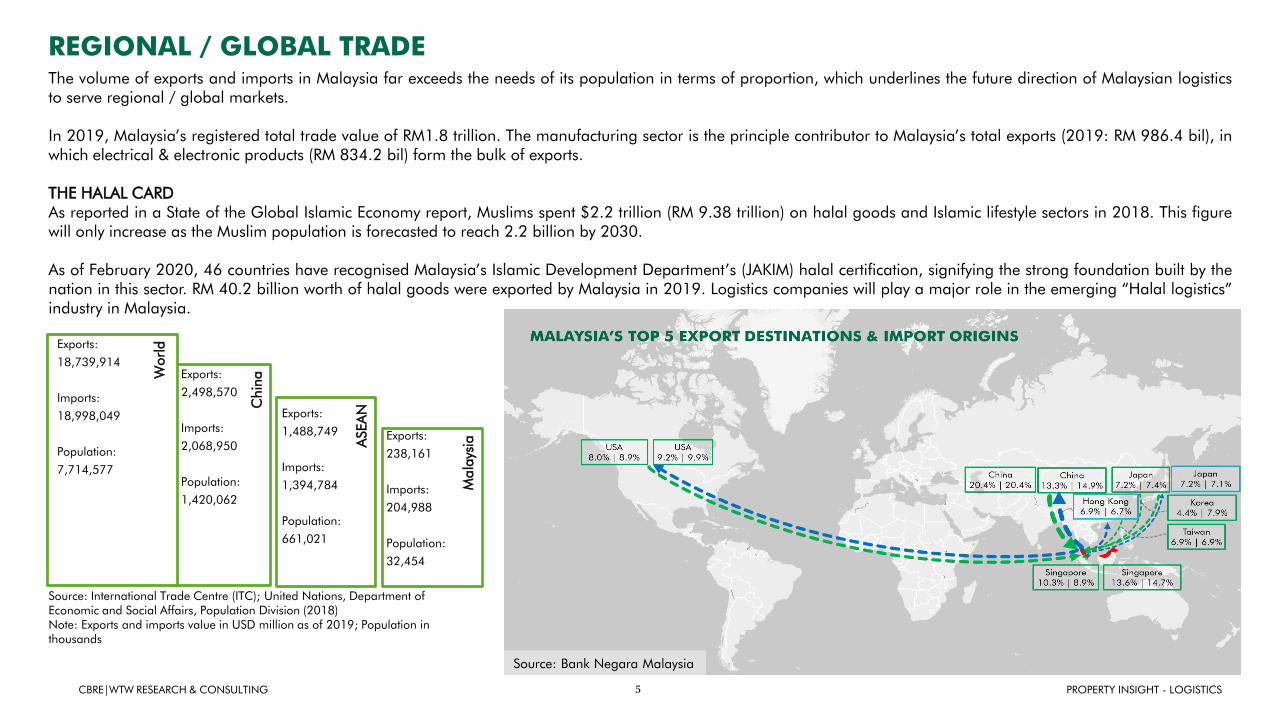

REGIONAL / GLOBAL TRADEThe volume of exports and imports in Malaysia far exceeds the needs of its population in terms of proportion, which underlines the future direction of Malaysian logisticsto serve regional / global markets.

In 2019, Malaysia’s registered total trade value of RM1.8 trillion. The manufacturing sector is the principle contributor to Malaysia’s total exports (2019: RM 986.4 bil), inwhich electrical & electronic products (RM 834.2 bil) form the bulk of exports.

THE HALAL CARDAs reported in a State of the Global Islamic Economy report, Muslims spent $2.2 trillion (RM 9.38 trillion) on halal goods and Islamic lifestyle sectors in 2018. This figurewill only increase as the Muslim population is forecasted to reach 2.2 billion by 2030.

As of February 2020, 46 countries have recognised Malaysia’s Islamic Development Department’s (JAKIM) halal certification, signifying the strong foundation built by thenation in this sector. RM 40.2 billion worth of halal goods were exported by Malaysia in 2019. Logistics companies will play a major role in the emerging “Halal logistics”industry in Malaysia.

ASEA

NChin

a

Mala

ysia

Worl

dExports:

18,739,914

Imports:

18,998,049

Population:

7,714,577

Exports:

2,498,570

Imports:

2,068,950

Population:

1,420,062

Exports:

1,488,749

Imports:

1,394,784

Population:

661,021

Exports:

238,161

Imports:

204,988

Population:

32,454

Source: International Trade Centre (ITC); United Nations, Department of Economic and Social Affairs, Population Division (2018)Note: Exports and imports value in USD million as of 2019; Population in thousands

Source: Bank Negara Malaysia

6 PROPERTY INSIGHT - LOGISTICSCBRE|WTW RESEARCH & CONSULTING

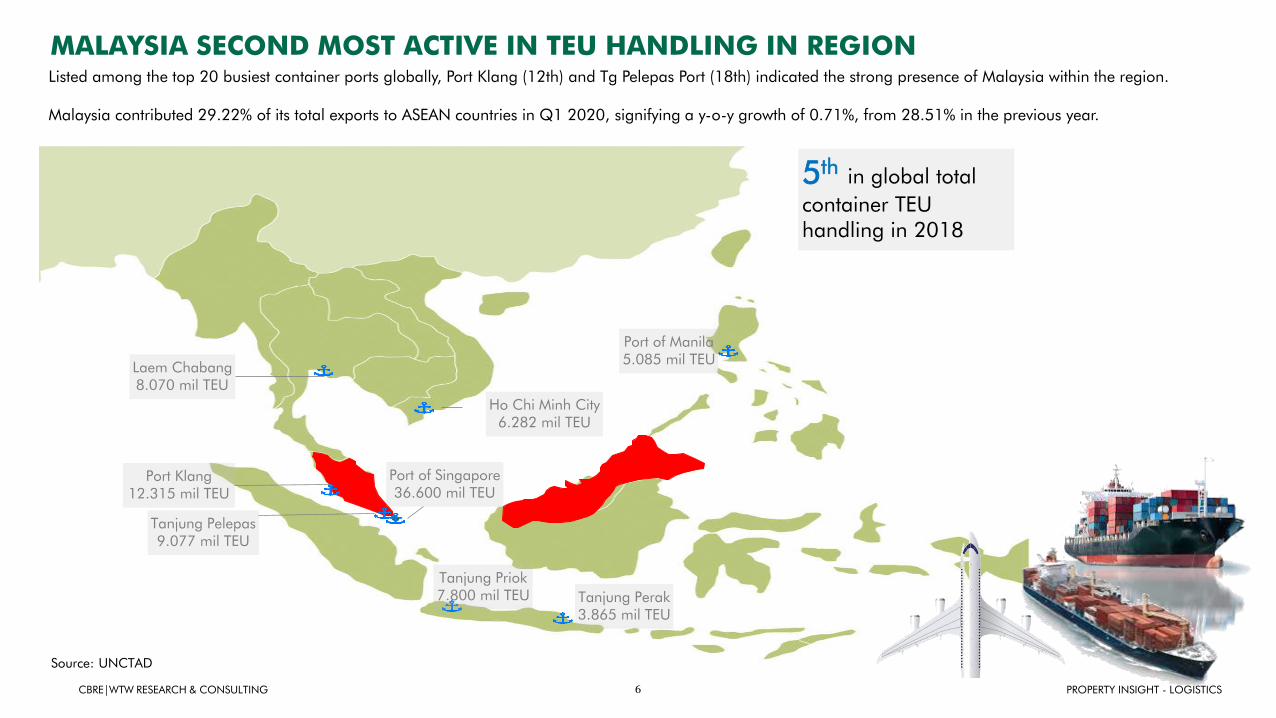

MALAYSIA SECOND MOST ACTIVE IN TEU HANDLING IN REGIONListed among the top 20 busiest container ports globally, Port Klang (12th) and Tg Pelepas Port (18th) indicated the strong presence of Malaysia within the region.

Malaysia contributed 29.22% of its total exports to ASEAN countries in Q1 2020, signifying a y-o-y growth of 0.71%, from 28.51% in the previous year.

Port Klang12.315 mil TEU

Source: UNCTAD

Port of Singapore36.600 mil TEU

Tanjung Pelepas9.077 mil TEU

Laem Chabang8.070 mil TEU

Tanjung Priok7.800 mil TEU

Ho Chi Minh City6.282 mil TEU

Port of Manila5.085 mil TEU

Tanjung Perak3.865 mil TEU

5th in global total

container TEU handling in 2018

7 PROPERTY INSIGHT - LOGISTICSCBRE|WTW RESEARCH & CONSULTING

Source: Ministry of Transport, Malaysia

Bintulu Port

Johor Port

Tanjung Pelepas

Port Klang

Penang

Kuantan Port

Kuching

Miri

Rajang Port

Sabah Ports

Kemaman Port

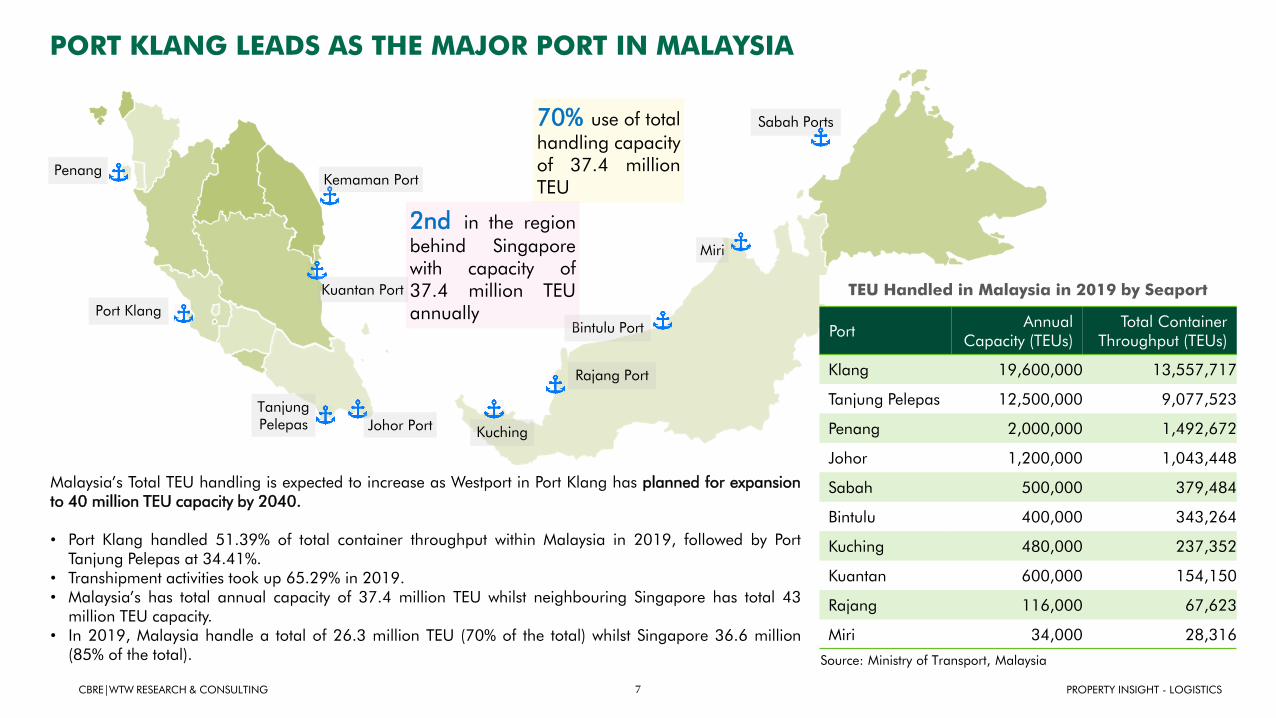

Malaysia’s Total TEU handling is expected to increase as Westport in Port Klang has planned for expansionto 40 million TEU capacity by 2040.

• Port Klang handled 51.39% of total container throughput within Malaysia in 2019, followed by PortTanjung Pelepas at 34.41%.

• Transhipment activities took up 65.29% in 2019.• Malaysia’s has total annual capacity of 37.4 million TEU whilst neighbouring Singapore has total 43

million TEU capacity.• In 2019, Malaysia handle a total of 26.3 million TEU (70% of the total) whilst Singapore 36.6 million

(85% of the total).

PortAnnual

Capacity (TEUs)Total Container

Throughput (TEUs)

Klang 19,600,000 13,557,717

Tanjung Pelepas 12,500,000 9,077,523

Penang 2,000,000 1,492,672

Johor 1,200,000 1,043,448

Sabah 500,000 379,484

Bintulu 400,000 343,264

Kuching 480,000 237,352

Kuantan 600,000 154,150

Rajang 116,000 67,623

Miri 34,000 28,316

PORT KLANG LEADS AS THE MAJOR PORT IN MALAYSIA

70% use of total

handling capacityof 37.4 millionTEU

2nd in the region

behind Singaporewith capacity of37.4 million TEUannually

TEU Handled in Malaysia in 2019 by Seaport

8 PROPERTY INSIGHT - LOGISTICSCBRE|WTW RESEARCH & CONSULTING

Source: Ministry of Transport, Malaysia

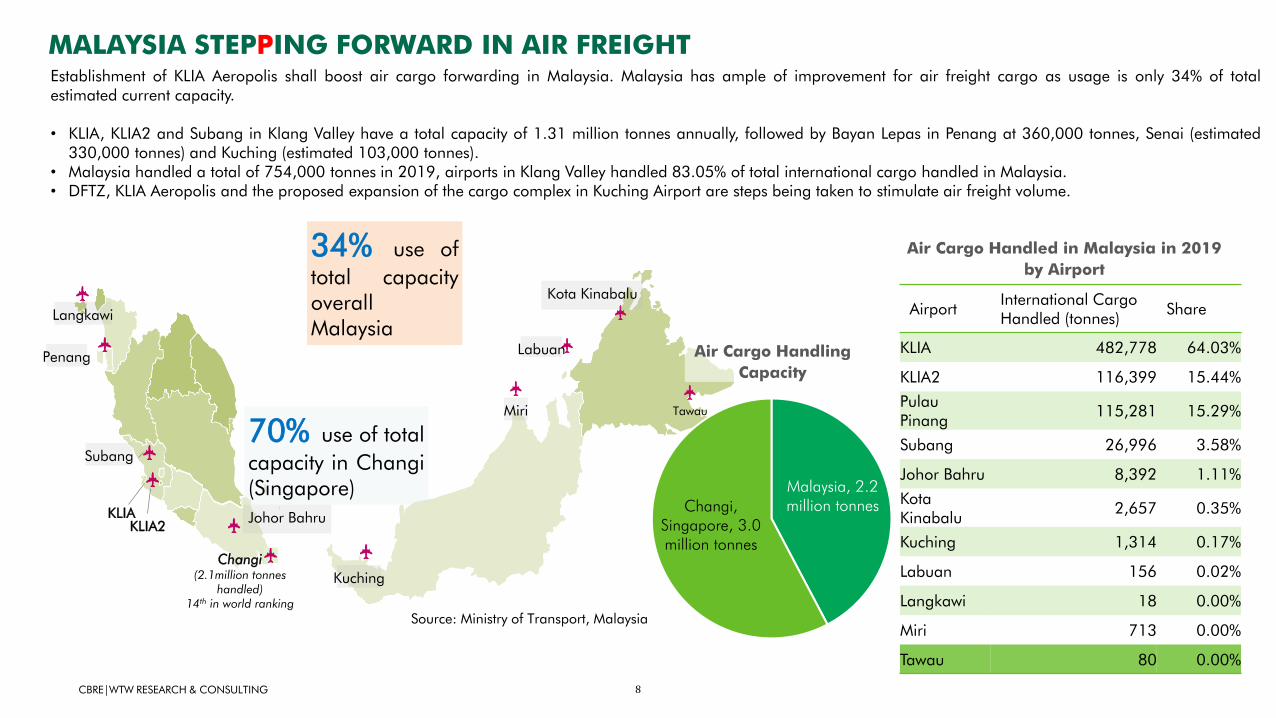

Establishment of KLIA Aeropolis shall boost air cargo forwarding in Malaysia. Malaysia has ample of improvement for air freight cargo as usage is only 34% of totalestimated current capacity.

• KLIA, KLIA2 and Subang in Klang Valley have a total capacity of 1.31 million tonnes annually, followed by Bayan Lepas in Penang at 360,000 tonnes, Senai (estimated330,000 tonnes) and Kuching (estimated 103,000 tonnes).

• Malaysia handled a total of 754,000 tonnes in 2019, airports in Klang Valley handled 83.05% of total international cargo handled in Malaysia.• DFTZ, KLIA Aeropolis and the proposed expansion of the cargo complex in Kuching Airport are steps being taken to stimulate air freight volume.

MALAYSIA STEPPING FORWARD IN AIR FREIGHT

Penang

Kuching

Miri

Langkawi

Labuan

Tawau

Subang

KLIAKLIA2

Johor Bahru

Kota Kinabalu

Changi(2.1million tonnes

handled)14th in world ranking

34% use of

total capacityoverallMalaysia

70% use of total

capacity in Changi(Singapore) Malaysia, 2.2

million tonnesChangi, Singapore, 3.0 million tonnes

Air Cargo Handling

Capacity

Air Cargo Handled in Malaysia in 2019

by Airport

AirportInternational Cargo Handled (tonnes)

Share

KLIA 482,778 64.03%

KLIA2 116,399 15.44%

PulauPinang

115,281 15.29%

Subang 26,996 3.58%

Johor Bahru 8,392 1.11%

Kota Kinabalu

2,657 0.35%

Kuching 1,314 0.17%

Labuan 156 0.02%

Langkawi 18 0.00%

Miri 713 0.00%

Tawau 80 0.00%

9 PROPERTY INSIGHT - LOGISTICSCBRE|WTW RESEARCH & CONSULTING

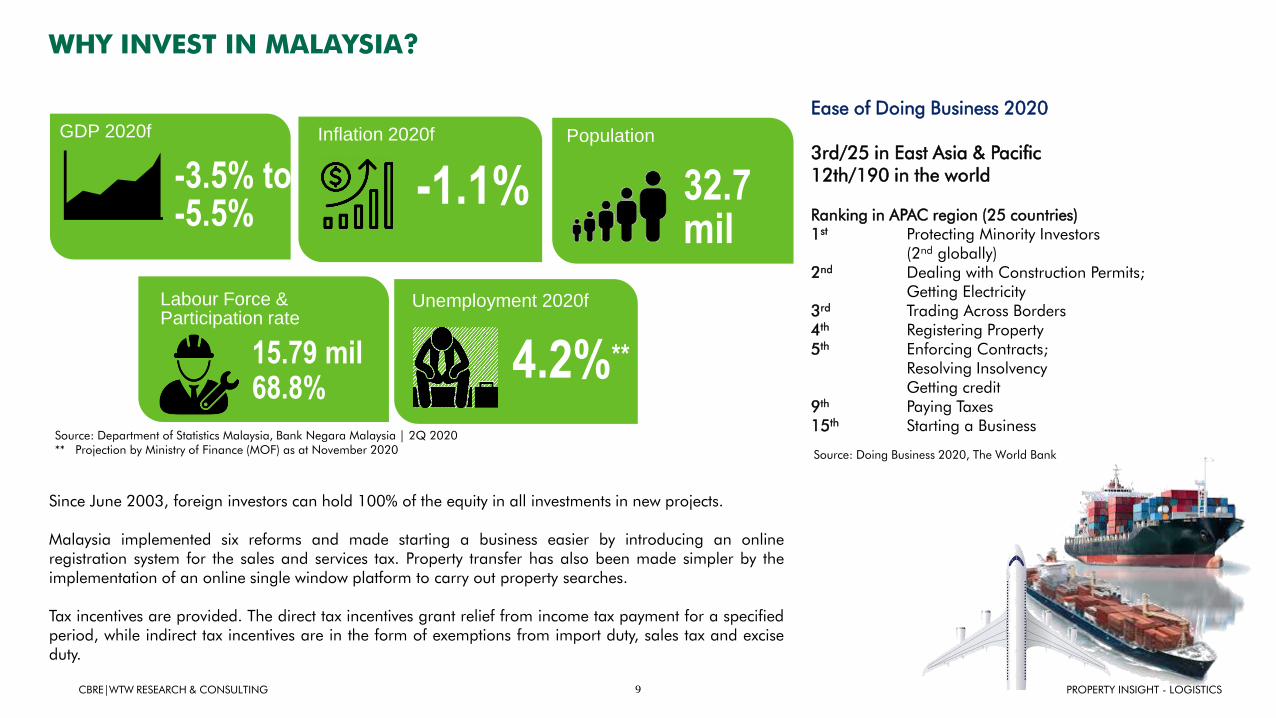

WHY INVEST IN MALAYSIA?

Ease of Doing Business 2020

3rd/25 in East Asia & Pacific12th/190 in the world

Ranking in APAC region (25 countries)1st Protecting Minority Investors

(2nd globally)2nd Dealing with Construction Permits;

Getting Electricity3rd Trading Across Borders4th Registering Property5th Enforcing Contracts;

Resolving InsolvencyGetting credit

9th Paying Taxes15th Starting a Business

GDP 2020f Inflation 2020f Population

32.7 mil

Labour Force & Participation rate

Unemployment 2020f

-3.5% to -5.5%

-1.1%

15.79 mil68.8%

4.2%**

Since June 2003, foreign investors can hold 100% of the equity in all investments in new projects.

Malaysia implemented six reforms and made starting a business easier by introducing an onlineregistration system for the sales and services tax. Property transfer has also been made simpler by theimplementation of an online single window platform to carry out property searches.

Tax incentives are provided. The direct tax incentives grant relief from income tax payment for a specifiedperiod, while indirect tax incentives are in the form of exemptions from import duty, sales tax and exciseduty.

Source: Department of Statistics Malaysia, Bank Negara Malaysia | 2Q 2020** Projection by Ministry of Finance (MOF) as at November 2020 Source: Doing Business 2020, The World Bank

10 PROPERTY INSIGHT - LOGISTICSCBRE|WTW RESEARCH & CONSULTING

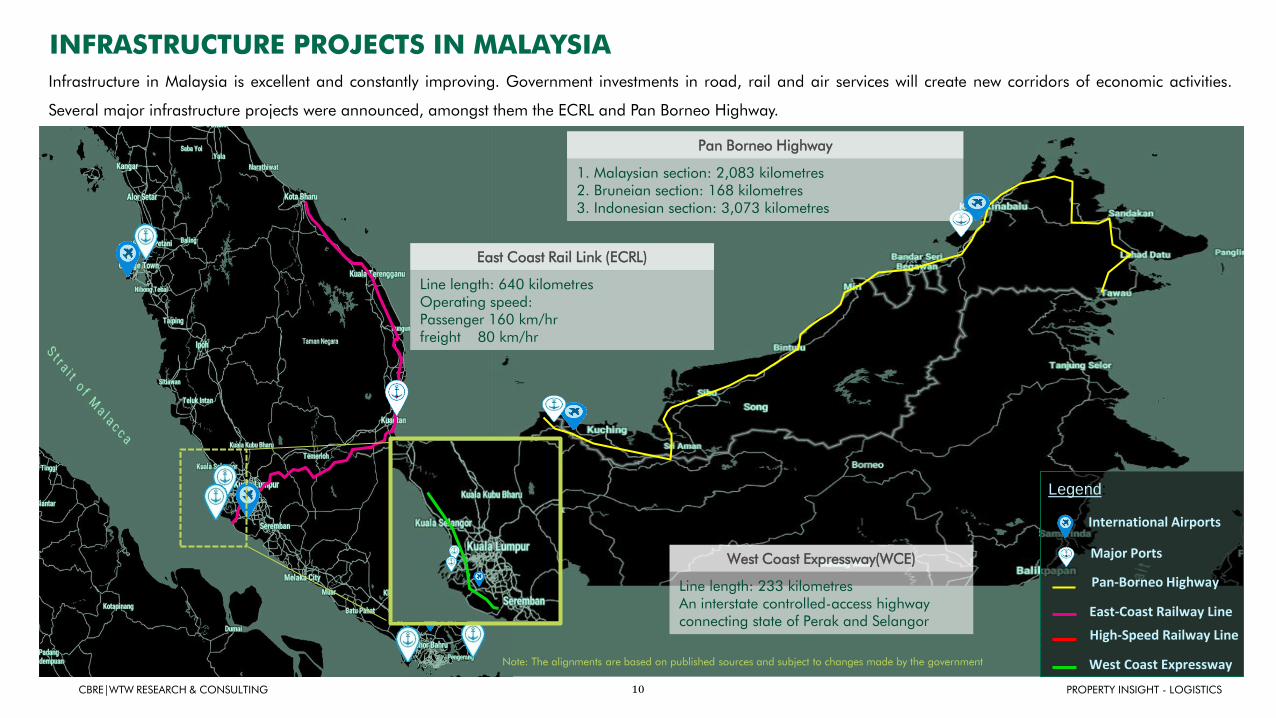

Legend:

International Airports

Major Ports

East-Coast Railway Line

High-Speed Railway Line

Pan-Borneo Highway

Infrastructure in Malaysia is excellent and constantly improving. Government investments in road, rail and air services will create new corridors of economic activities.

Several major infrastructure projects were announced, amongst them the ECRL and Pan Borneo Highway.

Pan Borneo Highway

1. Malaysian section: 2,083 kilometres2. Bruneian section: 168 kilometres3. Indonesian section: 3,073 kilometres

East Coast Rail Link (ECRL)

Line length: 640 kilometresOperating speed: Passenger 160 km/hr freight 80 km/hr

INFRASTRUCTURE PROJECTS IN MALAYSIA

West Coast Expressway(WCE)

Line length: 233 kilometresAn interstate controlled-access highway connecting state of Perak and Selangor

West Coast ExpresswayNote: The alignments are based on published sources and subject to changes made by the government

11 PROPERTY INSIGHT - LOGISTICSCBRE|WTW RESEARCH & CONSULTING

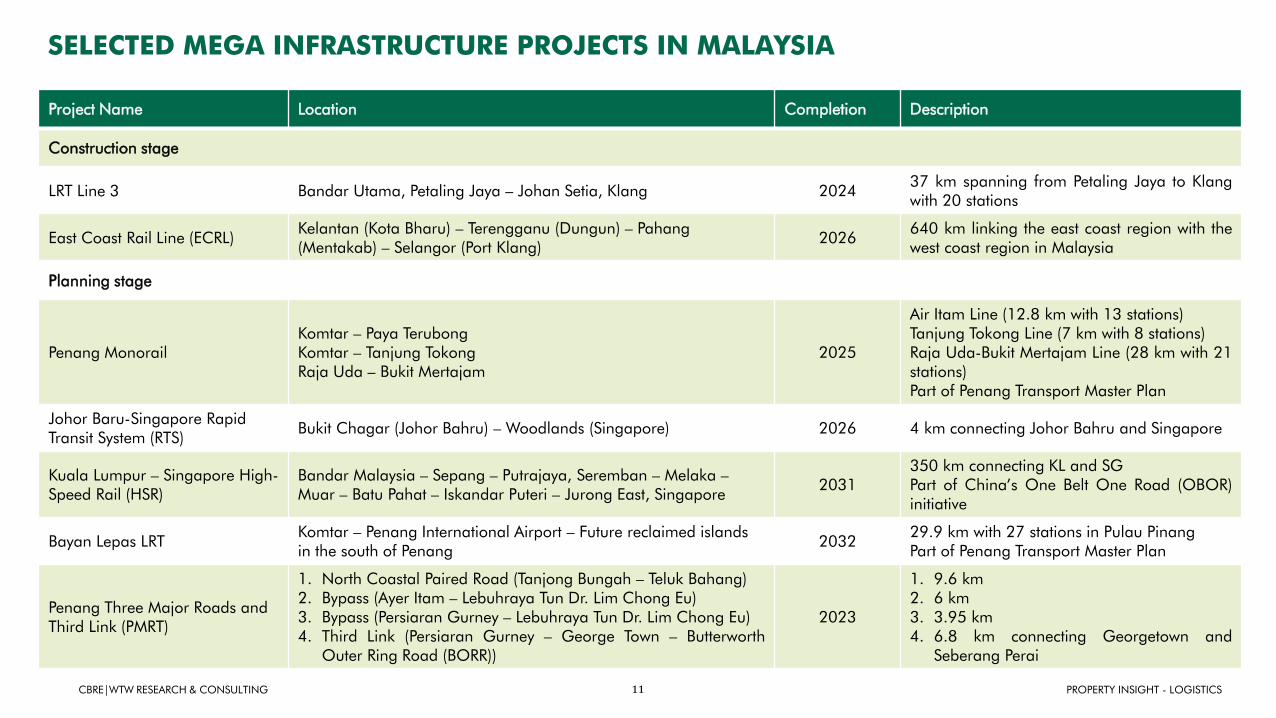

SELECTED MEGA INFRASTRUCTURE PROJECTS IN MALAYSIA

Project Name Location Completion Description

Construction stage

LRT Line 3 Bandar Utama, Petaling Jaya – Johan Setia, Klang 202437 km spanning from Petaling Jaya to Klangwith 20 stations

East Coast Rail Line (ECRL)Kelantan (Kota Bharu) – Terengganu (Dungun) – Pahang (Mentakab) – Selangor (Port Klang)

2026640 km linking the east coast region with thewest coast region in Malaysia

Planning stage

Penang MonorailKomtar – Paya TerubongKomtar – Tanjung TokongRaja Uda – Bukit Mertajam

2025

Air Itam Line (12.8 km with 13 stations)Tanjung Tokong Line (7 km with 8 stations)Raja Uda-Bukit Mertajam Line (28 km with 21stations)Part of Penang Transport Master Plan

Johor Baru-Singapore Rapid Transit System (RTS)

Bukit Chagar (Johor Bahru) – Woodlands (Singapore) 2026 4 km connecting Johor Bahru and Singapore

Kuala Lumpur – Singapore High-Speed Rail (HSR)

Bandar Malaysia – Sepang – Putrajaya, Seremban – Melaka –Muar – Batu Pahat – Iskandar Puteri – Jurong East, Singapore

2031350 km connecting KL and SGPart of China’s One Belt One Road (OBOR)initiative

Bayan Lepas LRTKomtar – Penang International Airport – Future reclaimed islands in the south of Penang

203229.9 km with 27 stations in Pulau PinangPart of Penang Transport Master Plan

Penang Three Major Roads and Third Link (PMRT)

1. North Coastal Paired Road (Tanjong Bungah – Teluk Bahang)2. Bypass (Ayer Itam – Lebuhraya Tun Dr. Lim Chong Eu)3. Bypass (Persiaran Gurney – Lebuhraya Tun Dr. Lim Chong Eu)4. Third Link (Persiaran Gurney – George Town – Butterworth

Outer Ring Road (BORR))

2023

1. 9.6 km2. 6 km3. 3.95 km4. 6.8 km connecting Georgetown and

Seberang Perai

12 PROPERTY INSIGHT - LOGISTICSCBRE|WTW RESEARCH & CONSULTING

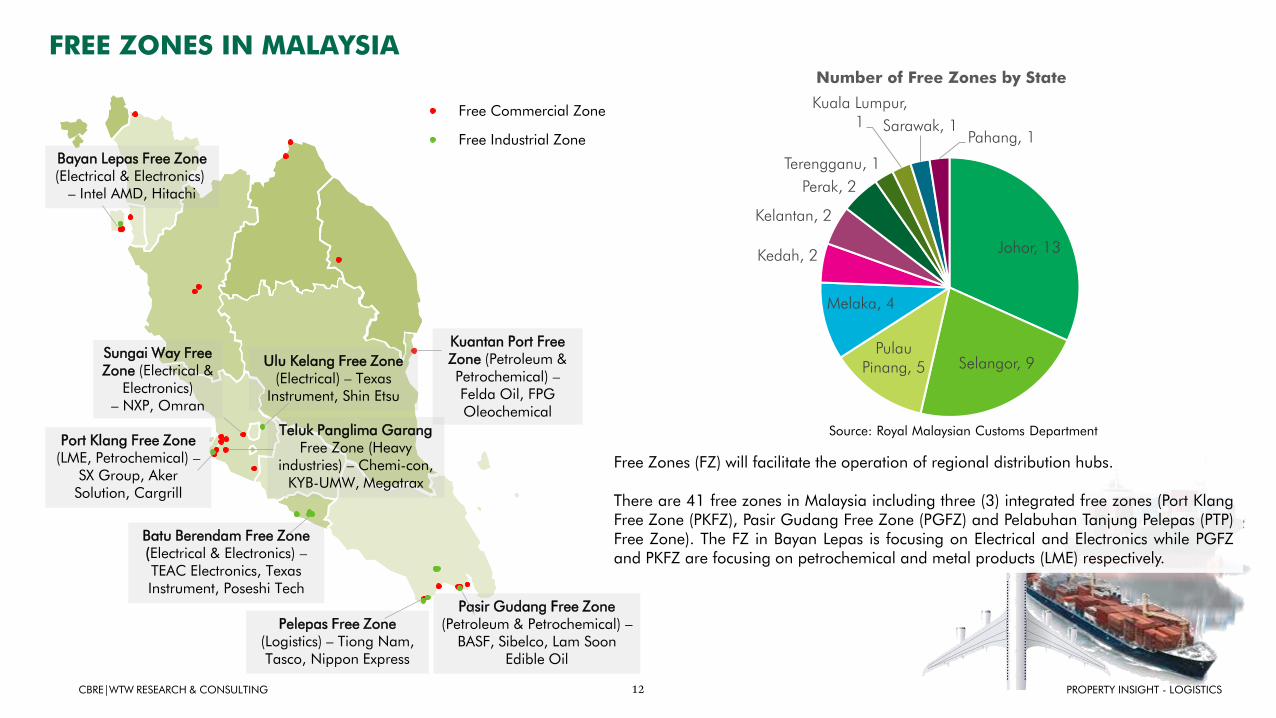

FREE ZONES IN MALAYSIA

Johor, 13

Selangor, 9Pulau

Pinang, 5

Melaka, 4

Kedah, 2

Kelantan, 2

Perak, 2

Terengganu, 1

Kuala Lumpur, 1 Sarawak, 1

Pahang, 1

Number of Free Zones by State

Source: Royal Malaysian Customs Department

Bayan Lepas Free Zone(Electrical & Electronics)

– Intel AMD, Hitachi

Sungai Way Free Zone (Electrical &

Electronics) – NXP, Omran

Port Klang Free Zone (LME, Petrochemical) –

SX Group, Aker Solution, Cargrill

Teluk Panglima GarangFree Zone (Heavy

industries) – Chemi-con, KYB-UMW, Megatrax

Ulu Kelang Free Zone (Electrical) – Texas

Instrument, Shin Etsu

Pelepas Free Zone (Logistics) – Tiong Nam, Tasco, Nippon Express

Pasir Gudang Free Zone (Petroleum & Petrochemical) –

BASF, Sibelco, Lam Soon Edible Oil

Kuantan Port Free Zone (Petroleum & Petrochemical) –Felda Oil, FPG Oleochemical

Batu Berendam Free Zone (Electrical & Electronics) –TEAC Electronics, Texas Instrument, Poseshi Tech

Free Commercial Zone

Free Industrial Zone

Free Zones (FZ) will facilitate the operation of regional distribution hubs.

There are 41 free zones in Malaysia including three (3) integrated free zones (Port KlangFree Zone (PKFZ), Pasir Gudang Free Zone (PGFZ) and Pelabuhan Tanjung Pelepas (PTP)Free Zone). The FZ in Bayan Lepas is focusing on Electrical and Electronics while PGFZand PKFZ are focusing on petrochemical and metal products (LME) respectively.

13 PROPERTY INSIGHT - LOGISTICSCBRE|WTW RESEARCH & CONSULTING

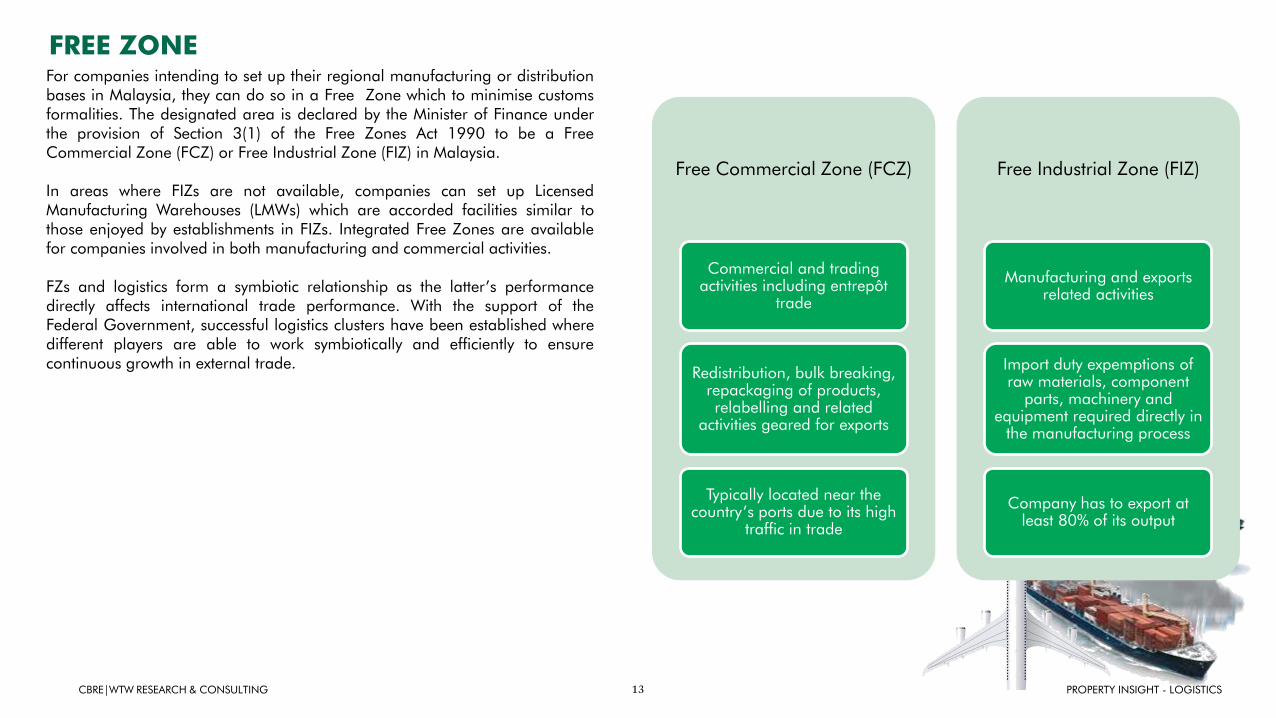

FREE ZONEFor companies intending to set up their regional manufacturing or distributionbases in Malaysia, they can do so in a Free Zone which to minimise customsformalities. The designated area is declared by the Minister of Finance underthe provision of Section 3(1) of the Free Zones Act 1990 to be a FreeCommercial Zone (FCZ) or Free Industrial Zone (FIZ) in Malaysia.

In areas where FIZs are not available, companies can set up LicensedManufacturing Warehouses (LMWs) which are accorded facilities similar tothose enjoyed by establishments in FIZs. Integrated Free Zones are availablefor companies involved in both manufacturing and commercial activities.

FZs and logistics form a symbiotic relationship as the latter’s performancedirectly affects international trade performance. With the support of theFederal Government, successful logistics clusters have been established wheredifferent players are able to work symbiotically and efficiently to ensurecontinuous growth in external trade.

Free Commercial Zone (FCZ)

Commercial and trading activities including entrepôt

trade

Redistribution, bulk breaking, repackaging of products, relabelling and related

activities geared for exports

Typically located near the country’s ports due to its high

traffic in trade

Free Industrial Zone (FIZ)

Manufacturing and exports related activities

Import duty expemptions of raw materials, component

parts, machinery and equipment required directly in

the manufacturing process

Company has to export at least 80% of its output

14 PROPERTY INSIGHT - LOGISTICSCBRE|WTW RESEARCH & CONSULTING

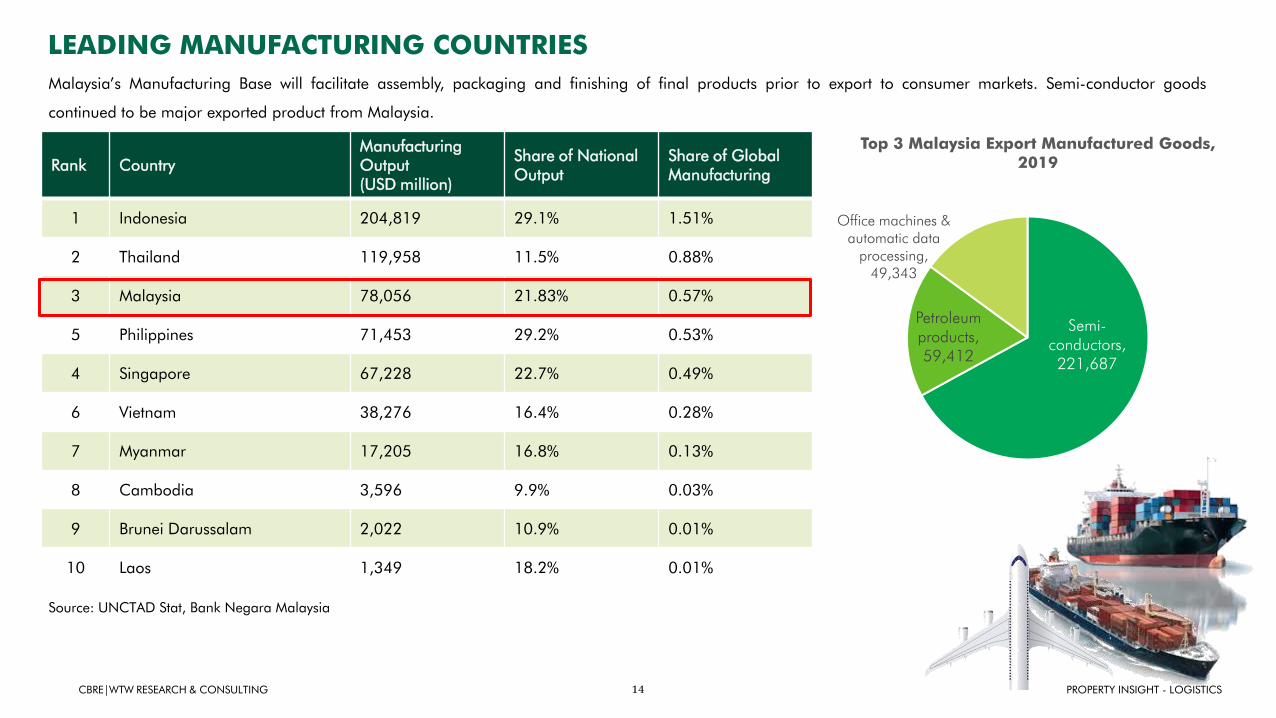

LEADING MANUFACTURING COUNTRIES

Source: UNCTAD Stat, Bank Negara Malaysia

Rank CountryManufacturing Output (USD million)

Share of National Output

Share of Global Manufacturing

1 Indonesia 204,819 29.1% 1.51%

2 Thailand 119,958 11.5% 0.88%

3 Malaysia 78,056 21.83% 0.57%

5 Philippines 71,453 29.2% 0.53%

4 Singapore 67,228 22.7% 0.49%

6 Vietnam 38,276 16.4% 0.28%

7 Myanmar 17,205 16.8% 0.13%

8 Cambodia 3,596 9.9% 0.03%

9 Brunei Darussalam 2,022 10.9% 0.01%

10 Laos 1,349 18.2% 0.01%

Malaysia’s Manufacturing Base will facilitate assembly, packaging and finishing of final products prior to export to consumer markets. Semi-conductor goods

continued to be major exported product from Malaysia.

Semi-conductors, 221,687

Petroleum products, 59,412

Office machines &automatic data

processing, 49,343

Top 3 Malaysia Export Manufactured Goods, 2019

15 PROPERTY INSIGHT - LOGISTICSCBRE|WTW RESEARCH & CONSULTING

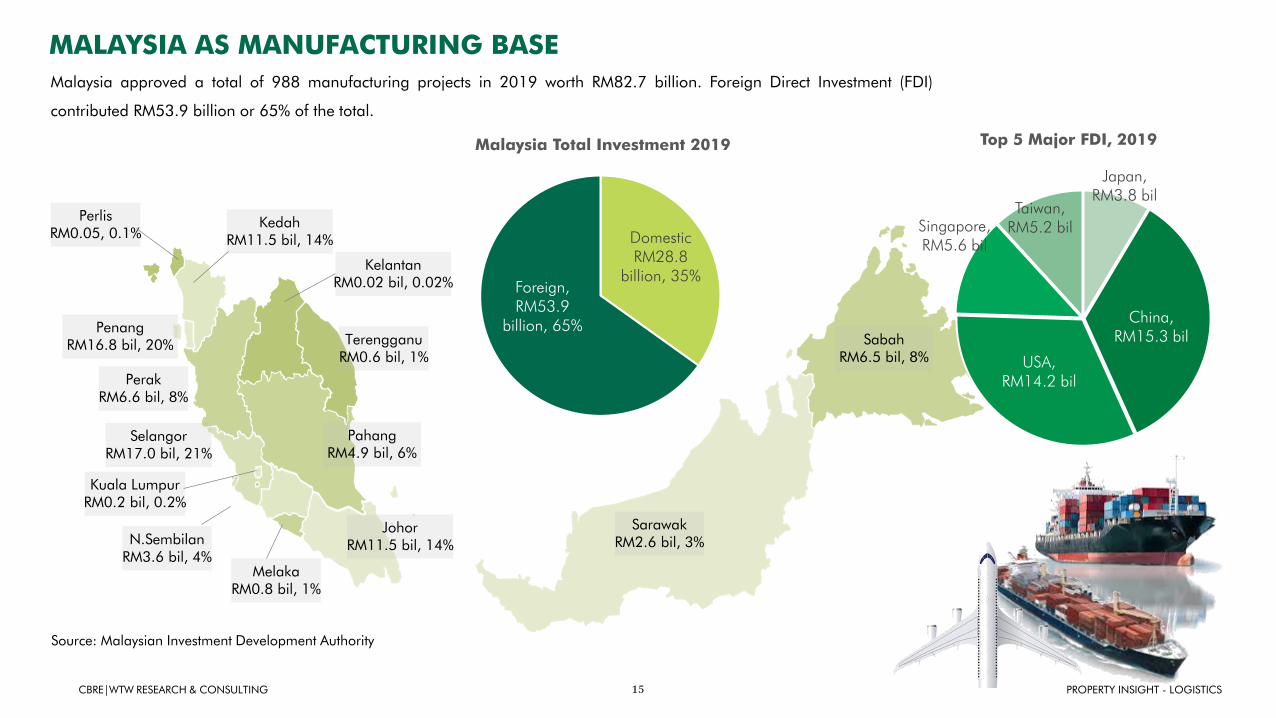

Source: Malaysian Investment Development Authority

JohorRM11.5 bil, 14%

SarawakRM2.6 bil, 3%

SabahRM6.5 bil, 8%

MelakaRM0.8 bil, 1%

N.SembilanRM3.6 bil, 4%

SelangorRM17.0 bil, 21%

PerakRM6.6 bil, 8%

PenangRM16.8 bil, 20%

PerlisRM0.05, 0.1%

KedahRM11.5 bil, 14%

KelantanRM0.02 bil, 0.02%

TerengganuRM0.6 bil, 1%

PahangRM4.9 bil, 6%

Kuala LumpurRM0.2 bil, 0.2%

DomesticRM28.8

billion, 35%Foreign, RM53.9

billion, 65%

Malaysia Total Investment 2019

Malaysia approved a total of 988 manufacturing projects in 2019 worth RM82.7 billion. Foreign Direct Investment (FDI)

contributed RM53.9 billion or 65% of the total.

China, RM15.3 bil

USA, RM14.2 bil

Singapore, RM5.6 bil

Taiwan, RM5.2 bil

Japan, RM3.8 bil

Top 5 Major FDI, 2019

MALAYSIA AS MANUFACTURING BASE

16

Source: CBRE WTW Research

DHL10%

LF Logistics

14%

Tasco / NYK14%

Tiong Nam Logistics Holdings

Bhd16%

CJ Century Logistics

12%

Integrated Logistics Berhad14%

Pos Logistics (formerly known

Konsortium Logistik)

11%

Nippon Express

9%

North Port

Port Klang

Subang

KLIA

BANGI

PUTRAJAYA

PUCHONG

SUBANG JAYA

PETALINGJAYA

SHAH ALAM

KUALA LUMPUR

KLANG

PULAUINDAH

Legend

Warehouses by Major Logistics / 3PL

Top Ten Largest 3PLs by Total Occupied Space

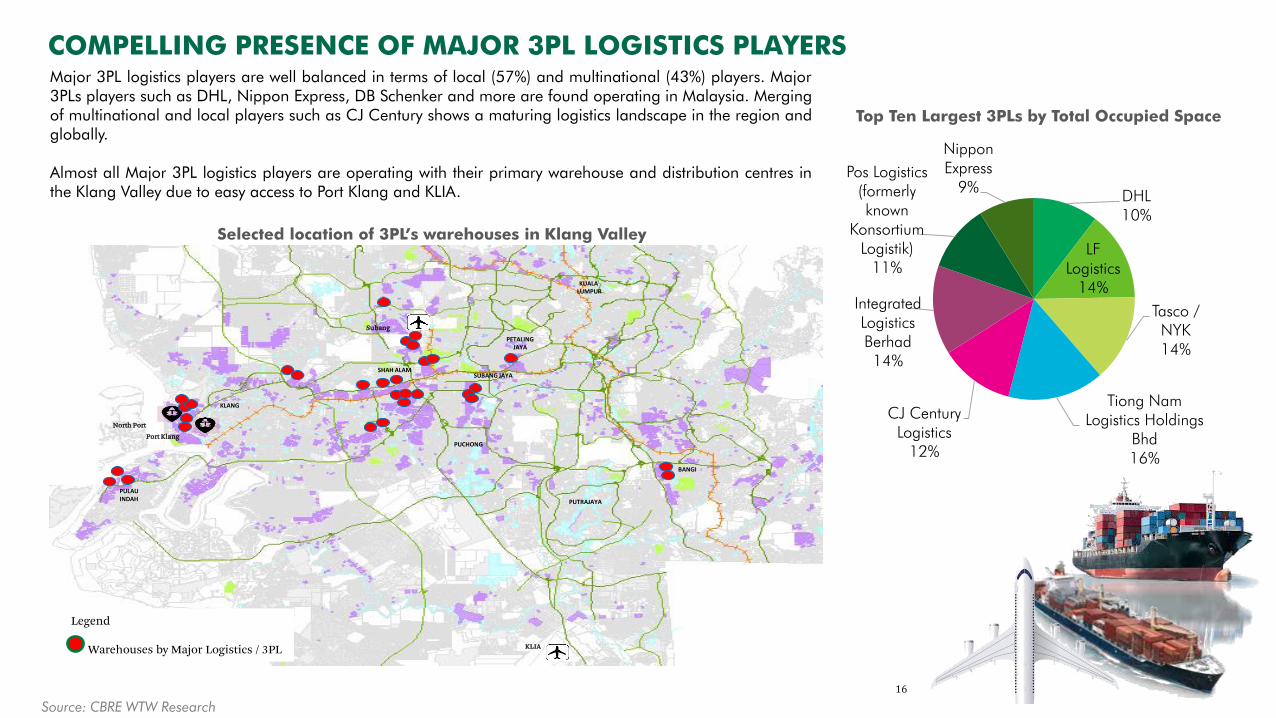

COMPELLING PRESENCE OF MAJOR 3PL LOGISTICS PLAYERS Major 3PL logistics players are well balanced in terms of local (57%) and multinational (43%) players. Major3PLs players such as DHL, Nippon Express, DB Schenker and more are found operating in Malaysia. Mergingof multinational and local players such as CJ Century shows a maturing logistics landscape in the region andglobally.

Almost all Major 3PL logistics players are operating with their primary warehouse and distribution centres inthe Klang Valley due to easy access to Port Klang and KLIA.

Selected location of 3PL’s warehouses in Klang Valley

17

Source: CBRE WTW Research

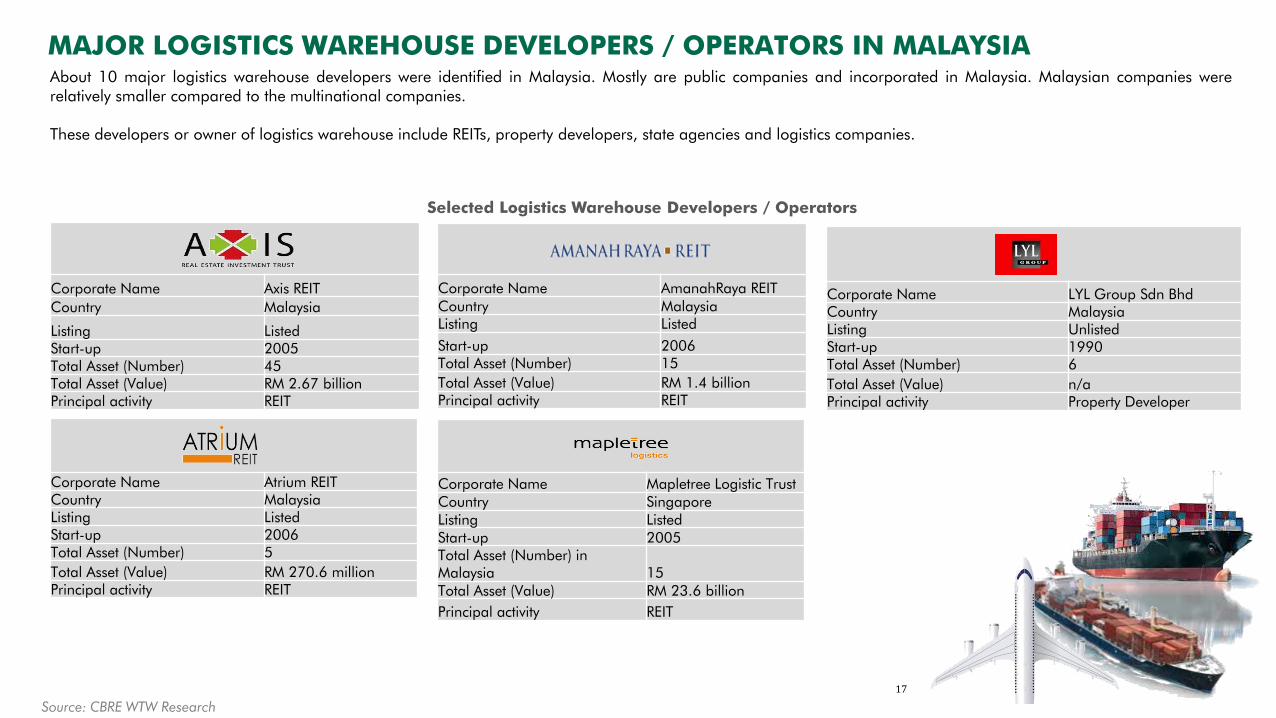

MAJOR LOGISTICS WAREHOUSE DEVELOPERS / OPERATORS IN MALAYSIAAbout 10 major logistics warehouse developers were identified in Malaysia. Mostly are public companies and incorporated in Malaysia. Malaysian companies wererelatively smaller compared to the multinational companies.

These developers or owner of logistics warehouse include REITs, property developers, state agencies and logistics companies.

Corporate Name Axis REIT

Country Malaysia

Listing ListedStart-up 2005Total Asset (Number) 45Total Asset (Value) RM 2.67 billionPrincipal activity REIT

Corporate Name AmanahRaya REITCountry Malaysia Listing Listed

Start-up 2006Total Asset (Number) 15

Total Asset (Value) RM 1.4 billionPrincipal activity REIT

Corporate Name Atrium REITCountry Malaysia Listing ListedStart-up 2006Total Asset (Number) 5

Total Asset (Value) RM 270.6 millionPrincipal activity REIT

Corporate Name Mapletree Logistic TrustCountry SingaporeListing ListedStart-up 2005Total Asset (Number) in Malaysia 15Total Asset (Value) RM 23.6 billion

Principal activity REIT

Selected Logistics Warehouse Developers / Operators

Corporate Name LYL Group Sdn BhdCountry Malaysia Listing UnlistedStart-up 1990Total Asset (Number) 6

Total Asset (Value) n/aPrincipal activity Property Developer

KLANG VALLEY LEADS THE LOGISTICS SECTOR IN MALAYSIAHaving the busiest ports namely Port Klang and North Port coupled with proximity to Kuala Lumpur International Airport (KLIA) placed the Klang Valley as the preferredlocation for logistics. The emergence of e-commerce has boosted logistics activities and surge in warehouse demand.

Recent Observation

Logistics Players

Air Freight

Sea Freight

Most are looking for

expansion especially for

the regional markets

Digital Free Trade Zone

(DFTZ) at KLIA would

boost the long-term

outlook of Malaysia’s

logistics companies

Increase in future demand has led

to some expansion plans by ports

and possibility of developing the

third port terminal at Pulau

Carey, Klang.

19 PROPERTY INSIGHT - LOGISTICSCBRE|WTW RESEARCH & CONSULTING

THE FUTURE OF MALAYSIA’S LOGISTICSLOCATION: Strategically located on the Straits of Malacca and serving as agateway to the South China Sea, Malaysia is ideally positioned to emerge asTHE regional logistics hub.

LOGISTICS ENABLED: Land availability, a skilled labour pool and establishedinfrastructure are among the strengths of Malaysia in becoming a destinationof choice for logistics and multinational companies’ regional distributioncentres (RDC) to better serve the SEA market, and onwards to the Indian,Middle East and African markets.

E-COMMERCE: The rise in e-commerce will spur logistics in areas close toseaports, airports and urban catchments, as retailers and 3PL providers alikeare striving to meet the demand for e-commerce fulfilment. The activeindustrial development market in Malaysia is an underlining testament to theprospects of e-commerce, logistics and warehousing activities.

HALAL TRADE MARKET / AHEAD OF THE CURVE: Providing one of the mostglobally recognised halal certifications, Malaysia is poised to develop as theGlobal Halal Hub to serve the growing halal market in Asia and the MiddleEast.

AIR FREIGHT RISING FROM THE ASHES: One of the worst hit by thepandemic, the air cargo industry will recover due to the surge in e-commercedemand. KLIA Aeropolis will be the primary catalyst in spurring the sector’sgrowth.

GLOBAL SUPPLY CHAIN REALIGNMENT: The changing global manufacturinglandscape may just tip the scale in favour of Malaysia. With readily availablemanufacturing resources and skills, Malaysia can attract manufacturing companieslooking at setting up alternative manufacturing bases. Electrical and electronics (E&E)stands as the country’s strongest manufacturing industry.

FREE ZONE: Free Zones will facilitate import/export activities enabling customsprocess and tariffs to be minimised for re-export manufacturing and regionaldistribution.

GOVERNMENT COMMITMENT: The government continues to invest in portexpansions and road networks to support development of a regional logisticsgateway.

PRIVATE SECTOR CONSENSUS: A round of surveys with the logistics players inMalaysia consolidated our expectations that the future of the logistics industry inMalaysia lies in regional/global growth. 3PL companies are expanding and lookingfor additional warehouse space.

ROOM FOR IMPROVEMENT: Port capacity, technology adoption and efficiency oftrade facilitation mechanisms are key determinants to strengthen Malaysia’scompetitive advantage in the future of Logistics.

20 PROPERTY INSIGHT - LOGISTICSCBRE|WTW RESEARCH & CONSULTING

For more information about this report, please contact:

Prepared by the CBRE|WTW ResearchC H Williams Talhar & Wong Sdn BhdOctober 2020

Limitations / Disclaimer:Our findings contained herein is based on information made available to us at the time of our survey and have been derived from sources which we believe to be reliable. As such, we cannot guarantee its accuracy or completeness. No liability can be accepted for any loss arising from the use of this report. All opinions and estimates expressed herein reflect our judgment as of this date and are subject to change without notice.

Our findings should be regarded as valid for a limited period of time and should be subject to examination at regular intervals.All rights reserved. No part of this report may be reproduced, stored in a retrieval system, or transmitted in many form or by any

means, electronics, mechanical, photocopying, recording or otherwise, without the prior permission of:

C H Williams Talhar & Wong Sdn Bhd

Director

zAziah Mohd [email protected]

Manager

Michael [email protected]

Analysts

Nurzawani [email protected]

Abdul Rahman [email protected]

Sarah [email protected]